price, demand and market structure for the … · production or conclusive formation tests to be...

TRANSCRIPT

1

Marcelo S. Pinelli, Petrobras Downstream Planning Manager

PRICE, DEMAND AND MARKET STRUCTURE FOR

THE OIL INDUSTRY: Distillates in the driver’s seat or

Gasoline resurgence ?

Oxford Institute for Energy Studies – February 23 th

2

DISCLAIMER

The presentation may contain forecasts about future events. Such forecasts merely reflect the

expectations of the Company's management. Such terms as "anticipate", "believe", "expect",

"forecast", "intend", "plan", "project", "seek", "should", along with similar or analogous

expressions, are used to identify such forecasts. These predictions evidently involve risks and

uncertainties, whether foreseen or not by the Company. Therefore, the future results of

operations may differ from current expectations, and readers must not base their expectations

exclusively on the information presented herein. The Company is not obliged to update the

presentation/such forecasts in light of new information or future developments.

The United States Securities and Exchange Commission permits oil and gas companies, in their

filings with the SEC, to disclose only proved reserves that a company has demonstrated by actual

production or conclusive formation tests to be economically and legally producible under existing

economic and operating conditions. We use certain terms in this presentation, such as oil and

gas resources, that the SEC’s guidelines strictly prohibit us from including in filings with

the SEC.

CAUTIONARY STATEMENT FOR US INVESTORS

3

OPEC’s oil price mismanagements

Weak Economic

Growth

Crude Oil Spare Capacity in High

Levels

Aggregate Demand

Reduction

Low Oil Prices Financial Speculation feedbacks the process

Geopolitical Factors

Brings Volatility to the

Process, Amplifying

Tendencies

New Refining

Units

FUNDAMENTALS REGARDING OIL MARKET STRUCTURE

Interest Rates

Dollar x Euro

Energetic Efficiency & Biofuel Markets

4

CRUDE OIL FUTURES AND MARKET STRUCTURE

Source: NYMEX

US

$/b

bl

5

25

45

65

85

105

125

jan

/01

jul/

01

jan

/02

jul/

02

jan

/03

jul/

03

jan

/04

jul/

04

jan

/05

jul/

05

jan

/06

jul/

06

jan

/07

jul/

07

jan

/08

jul/

08

jan

/09

jul/

09

jan

/10

jul/

10

jan

/11

jul/

11

jan

/12

jul/

12

jan

/13

US$/bbl nominais

5

Sources: CFTC and NYMEX This chart is based on weekly data

The data above indicates poor correlation and no causality between these variables.

THE ROLE OF FINANCIAL PLAYERS IN OIL MARKET – NYMEX FUTURES POSITIONS

US

$/b

bl

Nu

mb

er

of

Co

ntr

acts

-60000

-40000

-20000

0

20000

40000

60000

80000

100000

120000

140000

ma

r-0

7

ab

r-0

7

ma

i-0

7

jun

-07

jul-

07

se

t-0

7

ou

t-0

7

no

v-0

7

de

z-0

7

jan

-08

fev

-08

ab

r-0

8

ma

i-0

8

jun

-08

jul-

08

ag

o-0

8

se

t-0

8

ou

t-0

8

de

z-0

8

jan

-09

0

20

40

60

80

100

120

140

160Non-Commercial Futures

WTI_Nymex

6

Source: Bloomberg and Platts* Granger’s causality tests were performed between these variables during this period

Among securities, the common stock of natural resource companies (such as gold, timber, and oil) is often considered an

inflation hedge because the value of the companies' assets should rise during a period of inflation.

From August 2007 to July 2008, Brent prices and Brent US$/bbl minus Brent Eur/bbl

spread have caused* the dollar/euro rate and a good correlation between these variables

is noticed from August 2007 to November 2008.

CRUDE OIL WAS USED AS A HEDGE AGAINST INFLATION, AND NOW ?

10

30

50

70

90

110

130

150

jan

/00

may/0

sep

/0

jan

/01

may/0

sep

/0

jan

/02

may/0

sep

/0

jan

/03

may/0

sep

/0

jan

/04

may/0

sep

/0

jan

/05

may/0

sep

/0

jan

/06

may/0

sep

/0

jan

/07

may/0

sep

/0

jan

/08

may/0

sep

/0

jan

/09

US$/bbl and Eur/bbl

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4US$/Eur$Brent US$/bbl

Brent Eur/bbl

USD$/Eur$

7

RESERVE/PRODUCTION RATIO EVOLUTION

Source: BP Statistics 2008

1814

20

46

1822

53

82

24

31

1914

0

10

20

30

40

50

60

70

80

90

19 8 0 2 0 0 7

Total North America Total S. & Cent. America

Total Europe & Eurasia Total Middle East

Total Africa Total Asia Pacific

Years

8

0

10000

20000

30000

40000

50000

60000

70000

80000

900001965

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

Total North America Total S. & Cent. AmericaTotal Europe & Eurasia Total Middle EastTotal Africa Total Asia Pacific

WORLD: OIL PRODUCTION EVOLUTION

Source: BP Statistics 2008

M bpdThousand bpd

9

0

10000

20000

30000

40000

50000

60000

70000

80000

900001965

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

Total North America Total S. & Cent. AmericaTotal Europe & Eurasia Total Middle EastTotal Africa Total Asia Pacific

WORLD: OIL CONSUMPTION EVOLUTION

Source: BP Statistics 2008

M bpdThousand bpd

10

650.000

700.000

750.000

800.000

850.000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Range 2003 - 2007

2007

2008

M bbl

Source: IEA and Platts

U.S., EUROPE, JAPAN PETROLEUM STOCKS AND CRUDE OIL PRICE

30

60

90

120

150

WTI 2007

WTI 2008

US$/bblThousand barrels

11

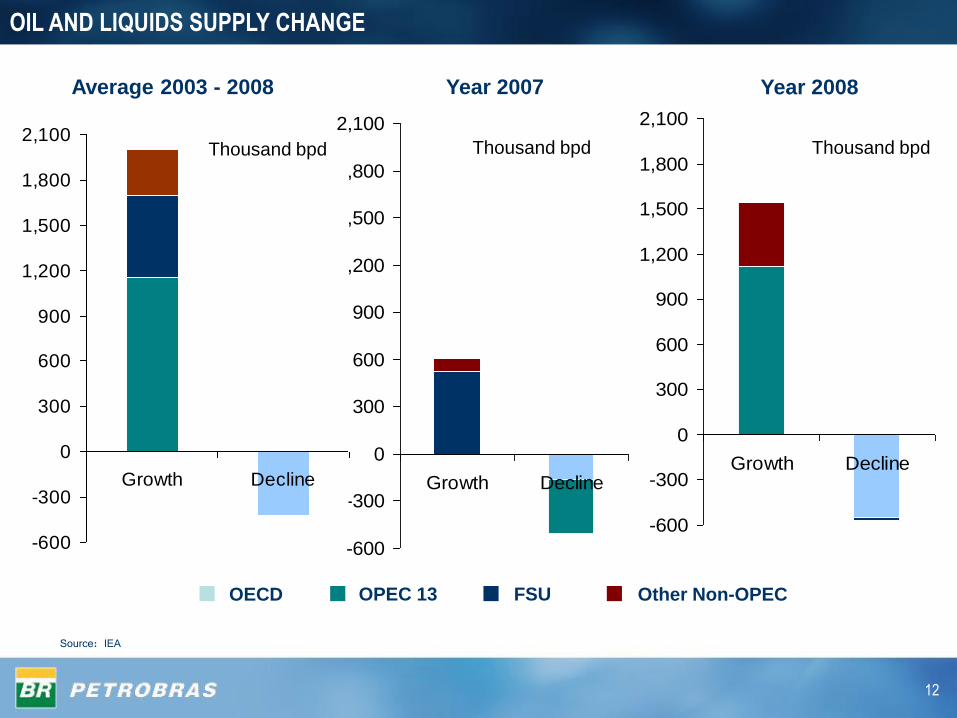

Source: IEA

CONTRIBUTIONS TO OIL AND LIQUIDS DEMAND AND SUPPLY GROWTH

-2,000

-1,000

0

1,000

2,000

3,000

4,000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

NON-OECD Demand

OECD Demand

M bpd

Oil and Liquids Demand

-2.000

-1.000

0

1.000

2.000

3.000

4.000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Non-OPEC 13

OPEC 13

M bpd

Oil and Liquids Supply

Thousand bpd

Thousand bpd

12

-600

-300

0

300

600

900

1,200

1,500

1,800

2,100

Growth Decline

-600

-300

0

300

600

900

1,200

1,500

1,800

2,100

Growth Decline

-600

-300

0

300

600

900

1,200

1,500

1,800

2,100

Growth Decline

Average 2003 - 2008 Year 2007 Year 2008

Source: IEA

M bpd

OIL AND LIQUIDS SUPPLY CHANGE

OECD OPEC 13 FSU Other Non-OPEC

M bpd M bpdThousand bpd Thousand bpd Thousand bpd

13

320

240

127

120

116

94

-1163

-79

-250-1

20

0

-10

00

-80

0

-60

0

-40

0

-20

0

0 20

0

40

0

60

0

China

Saudi Arabia

India

Brazil

Iran

Germany

Italy

Japan

United States

329

141

122

111

98

74

-49

-236

-191

-1

-12

00

-10

00

-80

0

-60

0

-40

0

-20

0

0 20

0

40

0

60

0

China

India

Brazil

Saudi Arabia

Iran

Canada

United States

United Kingdom

Japan

Germany

20082007

Source: IEA

OIL AND LIQUIDS DEMAND CHANGE

OECD

Non-OECD

OECD

Non-OECD

Thousand bpd

Thousand bpd

14

2008 WORLD DEMAND GROWTH: OECD vs NON OECD

Sources: IEA Oil Market Report

IEA forecast revisions for 2008 Oil and Liquids Demand Growth

-2,0

-1,5

-1,0

-0,5

0,0

0,5

1,0

1,5

2,0

2,5

Jan 2008

IEA Estimate

Mar 2008

IEA Estimate

Jun 2008

IEA Estimate

Sep 2008

IEA Estimate

Dec 2008

IEA Estimate

OECD Demand Non-OECD Demand Total Demand

MM bpdMillion bpd

15

WORLD: REGIONAL CONSUMPTION - BY PRODUCT GROUP

Source: BP Statistics 2008

0%

20%

40%

60%

80%

100%1965

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

Light distillates Middle distillates Fuel oil Others

16

WORLD FINAL ENERGY CONSUMPTION BY SECTOR

Total Consumption ( %)

1980

Oil Consumption (%)

1980

2006

2006Source: IEA

Transport

25%

Industry

35%

Residential,

Services

and

Agriculture

40%

Transport

30%

Industry

30%

Residential,

Services

and

Agriculture

40%

Transport

56%

Industry

22%

Residential,

Services

and

Agriculture

40%

Transport

73%

Industry

11%

Residential,

Services and

Agriculture

40%

2007

2007

1980

1980

17

World Product Consumption – Light and Middle Distillates

Source: BP Statistics 2008

0

10.000

20.000

30.000

40.000

50.000

60.000

70.000

19851987

19891991

19931995

19971999

20012003

20052007

middle

light

Thousand bpd

18

Regional Demand - Light and Middle Distillates

Source: BP Statistics 2008

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

9.000

10.000

11.000

12.000

13.000

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

EUROPE Middle distillates

EUROPE Light distillates

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

16.000

18.000

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

US Middle distillates

US Light distillates

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

16.000

18.000

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

Asia Middle distillates

Asia Light distillates

Thousand bpd

19

0

2

4

6

8

10

12

North

America

US Europe FSU Middle

East

Africa Asia

Pacific

China Japan

MMbpd

2000

2001

2002

2003

2004

2005

2006

2007

1.3% 1.1% -2.5% 3.9% 5.4% 2.4% 3.5% 7.1% 0.4%CAGR

LIGHT DISTILLATES CONSUMPTION, 2000-2007

Million bpd

Source: BP Statistics 2008

20

Source: IEA and Platts

CrackSpread Gasoline = Unleaded USG – WTI

U.S., EUROPE, JAPAN GASOLINE STOCKS AND CRACKSPREAD GASOLINE USG MINUS WTI

290,000

310,000

330,000

350,000

370,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Range 2003 - 200720072008

M bbl

-20

0

20

40

60

80

100

Crack-Spread Gasoline 2007

Crack-Spread Gasoline 2008

US$/bbl

Thousand barrels

21

U.S. Finished Motor Gasoline Refinery Yield

Source: EIA DOE

40

41

42

43

44

45

46

47

48

49

jan fev mar abr mai jun jul ago set out nov dez

2005

2006

2007

2008

%

22

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

North

America

US Europe FSU Middle

East

Africa Asia

Pacific

China Japan

MMbpd

2000

2001

2002

2003

2004

2005

2006

2007

MIDDLE DISTILLATES CONSUMPTION, 2000-2007

1.1% 0.9% 2.0% 3.0% 3.9% 3.4% 2.3% 9.0% -2.7%CAGR

Million bpd

Source: BP Statistics 2008

23

Source: IEA and Platts

Crackspread Diesel = N2 Diesel USG - WTI

U.S., EUROPE, JAPAN DIESEL STOCKS AND CRACKSPREAD DIESEL USG MINUS WTI

270,000

300,000

330,000

360,000

390,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Range 2003 - 2007

2007

2008

M bbl

0

10

20

30

40

Crack-Spread Diesel 2007

Crack-Spread Diesel 2008

US$/bblThousand barrels

24

Diesel Prices

0

20

40

60

80

100

120

140

160

Jan-

00

May

-00

Sep

-00

Jan-

01

May

-01

Sep

-01

Jan-

02

May

-02

Sep

-02

Jan-

03

May

-03

Sep

-03

Jan-

04

May

-04

Sep

-04

Jan-

05

May

-05

Sep

-05

Jan-

06

May

-06

Sep

-06

Jan-

07

May

-07

Sep

-07

Jan-

08

May

-08

Sep

-08

Jan-

09

No.2 USG Waterborne Platts Mid

Gasoil 0.2%S NWE FOB Barges Platts Mid

Gasoil 0.5%S Singapore Platts Mid

(US$/BBL)

DIESEL PRICES

25

GASOLINE – DIESEL SPREADS

Gasoline - Diesel Spreads

-30

-20

-10

0

10

20

30

Jan-

00

Apr

-00

Jul-0

0

Oct-0

0

Jan-

01

Apr

-01

Jul-0

1

Oct-0

1

Jan-

02

Apr

-02

Jul-0

2

Oct-0

2

Jan-

03

Apr

-03

Jul-0

3

Oct-0

3

Jan-

04

Apr

-04

Jul-0

4

Oct-0

4

Jan-

05

Apr

-05

Jul-0

5

Oct-0

5

Jan-

06

Apr

-06

Jul-0

6

Oct-0

6

Jan-

07

Apr

-07

Jul-0

7

Oct-0

7

Jan-

08

Apr

-08

Jul-0

8

Oct-0

8

Jan-

09

USG NWE Sing

Hurricane

Gustav

(US$/BBL)

26

US PRODUCTS YIELDS: REFINERY MAXIMIZATION WAR !

20%

25%

30%

35%

40%

45%

jan/

05

mar

/05

mai

/05

jul/0

5

set/0

5

nov/

05

jan/

06

mar

/06

mai

/06

jul/0

6

set/0

6

nov/

06

jan/

07

mar

/07

mai

/07

jul/0

7

set/0

7

nov/

07

jan/

08

mar

/08

mai

/08

jul/0

8

set/0

8

nov/

08

Gasoline Diesel

Source: EIA/DOE

27

Diesel Engine Vehicle Market Shares in Western Europe and the United States, 1999-2007

Source: EIA.

(% of Total New Light-Duty Vehicle Sales)

28

While in Europe, diesel penetration

Source:

0,00%

10,00%

20,00%

30,00%

40,00%

50,00%

60,00%

70,00%

80,00%

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

Petrol

Diesel

Trends in composition of new cars registered in the EU15

29

Average Retail Prices for Premium Gasoline and Diesel Fuel in Western Europe and the US, 1999-2007

Source: EIA.

(Nominal U.S. Dollars per Gallon)

30

0

10

20

30

40

50

60

70

80

90

1999 2000 2001 2002 2003 2004 2005 2006 2007

United States Western Europe Belgium France

Germany Italy Norway Spain

Switzerland United Kingdom

Diesel Engine Vehicle Market Shares in Western Europe and the United States, 1999-2007

Source: EIA.

(% of Total New Light-Duty Vehicle Sales)

31

0

50

100

150

200

250

300

350

400

jan/0

7

abr/

07

jul/07

out/07

jan/0

8

abr/

08

jul/08

out/08

-1000

-800

-600

-400

-200

0

200

400

600Consumption

Retail Prices

Wholesale Price

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

9.000

10.000

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

0

50

100

150

200

250

300

350

Consumption

Retail Gasoline Price

US Gasoline Demand – Downturn in 2008

Source: EIA DOE

Cents/gallon

Thousand bpd

Pump price

Cents/gallon

Thousand bpd

32

2.200

2.250

2.300

2.350

2.400

2.450

2.500

2.550

2.600

2.650

2.700

2.750

2.800

2.850

2.900

2.950

3.000

3.050

19951996

19971998

19992000

20012002

20032004

20052006

20072008

Vehicle-Distance Traveled - Americans are driving less…

Source: US Federal Highway Administration

Inflexion point

Billion Miles

33

US vehicle sales have been trending downward…

Source: US Department of Commerce

Light trucks--trucks up to 14,000 pounds gross vehicle weight, including minivans and sport utility vehicles

Thousands

34

Source: EPA

Fuel Economy in US

*

* Light-duty trucks = sport utility vehicles or SUVs, vans, and pickup

trucks with less than 8500 pounds gross vehicle weight ratings.

35

Fuel Economy by Country/Region

36

0.00

0.50

1.00

1.50

2.00

2.50

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

mm

bp

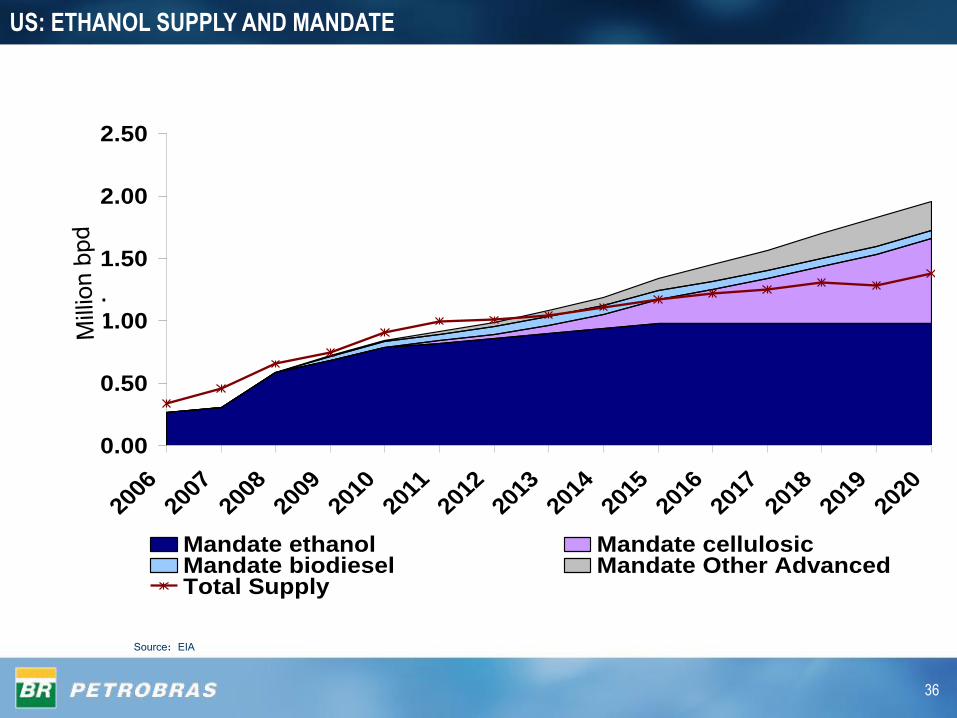

d

Mandate ethanol Mandate cellulosicMandate biodiesel Mandate Other AdvancedTotal Supply

US: ETHANOL SUPPLY AND MANDATE

Source: EIA

37

Total Aircraft deliveries from Airbus – 1992-2008

0

100

200

300

400

500

600

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Source: Airbus (1992-2008 Results).

38

Sources: Platts

Spread Crude Oil Light-Heavy = WTI – Maya

Spread Oil Products Light-Heavy = (Unleaded USG + N2 Diesel USG)/2 – Fuel Oil 3% USG

SPREADS LIGHT – HEAVY: THE COMPLEX REFINER ADVANTAGE

0

5

10

15

20

25

30

35

40

451

98

8

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

WTI - Maya Diesel & Gasoline - Fuel Oil

US$/BBL of 2008

39

0

5

10

15

20

25

30

35

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Margin WTI Cracking

Margin Maya Coking

US$/BBL of 2008

Sources: Platts

US Gasoline Downturn

Gross Refining Margins = Products prices minus crude oil

Margin WTI Cracking = USGC Margin of using WTI with cracking yields

Margin Maya Coking = USGC Margin of using Maya with coking yields

GROSS REFINING MARGINS AT US GULF COAST

40

67.163

0

2

4

6

8

10

12

- 10.000 20.000 30.000 40.000 50.000 60.000 70.000 80.000 90.000 100.000

Mbpd

Refi

nin

g M

arg

in Coking

Cracking

Topping

US$/bbl

71.868

0

2

4

6

8

10

12

- 10.000 20.000 30.000 40.000 50.000 60.000 70.000 80.000 90.000 100.000

Mbpd

Refi

nin

g M

arg

in Coking

Cracking

Topping

US$/bbl

GLOBAL MARGINAL REFINER 2002-2003

Average crude oil quality: 32 api, 1,2 S%, 0,9 TAN

Sources: OGJ, PIRA & Crude Oil Handbook 2002

2003

Topping

2002

Topping

Thousand bpd

Thousand bpd

41

75.677

0

2

4

6

8

10

12

- 10.000 20.000 30.000 40.000 50.000 60.000 70.000 80.000 90.000 100.000

Mbpd

Refi

nin

g M

arg

in Coking

Cracking

Topping

US$/bbl

76.131

0

2

4

6

8

10

12

- 10.000 20.000 30.000 40.000 50.000 60.000 70.000 80.000 90.000 100.000

Mbpd

Refi

nin

g M

arg

in Coking

Cracking

Topping

US$/bbl

GLOBAL MARGINAL REFINER 2005-2006

Sources: OGJ, PIRA & Crude Oil Handbook 2004, 2006

2006

Topping

2005

Average crude oil quality: 32 api, 1,2 S%, 0,9 TAN

Thousand bpd

Thousand bpd

42

77.681

0

2

4

6

8

10

12

- 10.000 20.000 30.000 40.000 50.000 60.000 70.000 80.000 90.000 100.000

Mbpd

Refi

nin

g M

arg

in Coking

Cracking

Topping

US$/bbl

77.387

0

2

4

6

8

10

12

- 10.000 20.000 30.000 40.000 50.000 60.000 70.000 80.000 90.000 100.000

Mbpd

Refi

nin

g M

arg

in Coking

Cracking

Topping

US$/bbl

GLOBAL MARGINAL REFINER 2007-2008

Average crude oil quality: 32 api, 1,2 S%, 0,9 TAN

Sources: OGJ, PIRA & Crude Oil Handbook 2007, 2008

2008

2007

Topping

Topping

Thousand bpd

Thousand bpd

43

REFINERY CAPACITY PROFILE

Coking FCC Hydrocracking

Latin America

-

1,000

2,000

3,000

2004 2005 2006 2007 2008

6% 6% 5% 5% 22%

28% 28% 29% 28% 29%

66%67% 66% 66% 66%Africa

-

100

200

300

400

500

2004 2005 2006 2007 2008

27% 27% 29% 29%33%

11% 11% 17% 17% 14%

53%62% 62% 53% 54%

Middle East

-

500

1,000

1,500

2004 2005 2006 2007 2008

57% 57% 57% 52% 55%

9% 9% 9% 9% 7%

38%34% 34% 34% 40%

Asia

-

2,000

4,000

6,000

8,000

10,000

2004 2005 2006 2007 2008

19% 19% 21% 22%22%

17% 17% 18% 18% 19%

59%64% 64% 62% 60%

FSU

-

500

1,000

1,500

2004 2005 2006 2007 2008

13% 18% 17% 17% 19%

22% 20% 21% 21% 19%

62%65% 63% 62% 62%

North America

-

5,000

10,000

15,000

2004 2005 2006 2007 2008

17% 17% 17% 18% 18%

23% 23% 23% 23% 24%

59%60% 60% 60% 59%

Europe

-

1,000

2,000

3,000

4,000

5,000

2004 2005 2006 2007 2008

30% 30% 31% 32% 32%

9% 9% 9% 9% 10%

58%60% 60% 60% 59%

mbpd

Source: Pira

Thousand bpd

44

• Global demand for middle distillates has been growing faster than for gasoline over the lastdecade and is expected to continue to do so.

• This has gradually been reflected in the price differential between diesel and gasoline. Twofactors have exacerbated this trend: tightening sulfur specifications for diesel and growingethanol and NGL supplies which weigh on gasoline/naphtha prices.

• Developing countries have been a large source of incremental diesel demand over the pastfour years.

• Refiners have been maximizing their diesel yields to take advantage of superior margins forthe product. European refiners have less potential to increase distillate yields further as mostof the measures have already been taken, while US refiners have more potential as they havelong been focused on gasoline production.

• Middle distillate margins are expected to weaken in 2009 from the record levels reached in2007 and 2008, however they are not expected to collapse completely.

• Demand growth in 2009 is likely to be much weaker than in the recent past. The sharpcontraction in the OCDE economies has resulted in a reduction of trade and freightmovements. Thus, demand for diesel for trucking firms, railroads and agricultural sector is alsodown.

• Many of the large refining projects scheduled to come online over the next two years areconfigured to produce a large yield of middle distillates and thus there will be also pressurefrom the supply side.

• As refiners periodically need to rebalance the gasoline market and draw down inventories,many refineries may be forced to cut runs.

• Another argument for continued relatively tight middle distillate markets is that incrementalworld liquids production will be biased toward lighter liquids such as condensates and naturalgas liquids (NGLs). When refined into products, these NGLs yield mostly naphtha andgasoline–boiling range material, and relatively little middle distillates.

DIESEL MARKET - OVERVIEW

45

Crude Oil’s rally in 2007-2008 was caused by fundamentals, but amplified by

financial flows. Will they also amplify a plunge in prices ?

Strong Economic Growth from Non-OCDE countries;

A better classification for Non-commercial players is absolutely needed;

Loose monetary policy has played a role in shaping the Oil Market;

Upstream: tight now and tighter in the future;

Distillates in the Driver's Seat;

Refiners need to look for a stable and secure oil supply sources;

Complex and integrated refiner: good environment.

FINAL REMARKS

46

0

1000

2000

3000

4000

5000

6000

7000

8000

1965

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

Argentina Brazil ColombiaEcuador Peru Trinidad & TobagoVenezuela Other S. & Cent. America

LATIN AMERICA: OIL PRODUCTION EVOLUTION

Source: BP Statistics 2008

M bpdThousand bpd

47

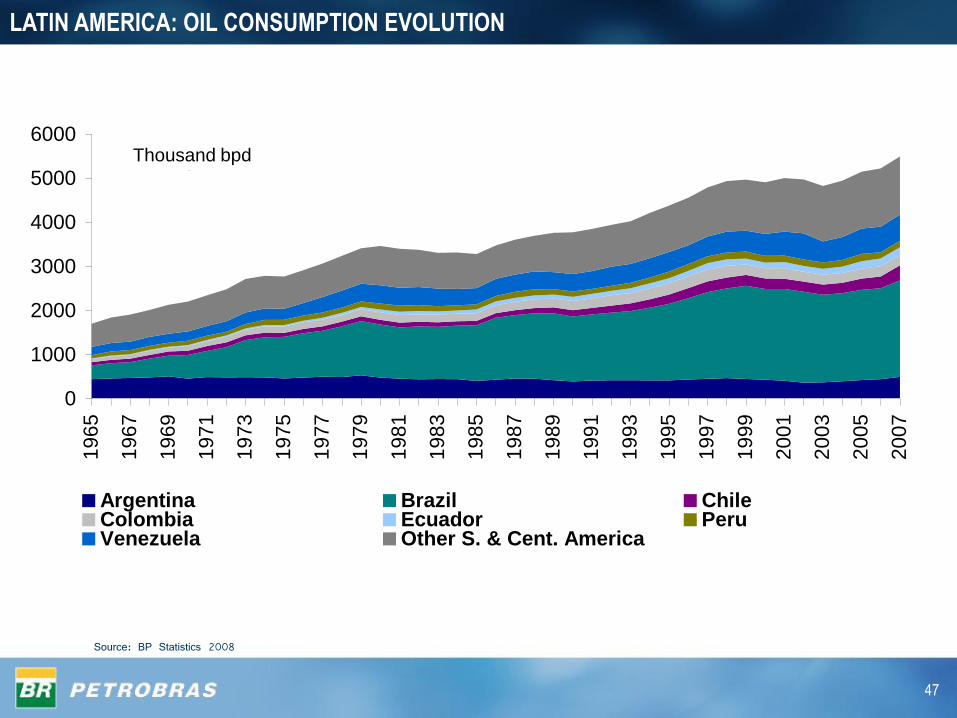

LATIN AMERICA: OIL CONSUMPTION EVOLUTION

Source: BP Statistics 2008

0

1000

2000

3000

4000

5000

6000

1965

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

Argentina Brazil ChileColombia Ecuador PeruVenezuela Other S. & Cent. America

M bpdThousand bpd

48

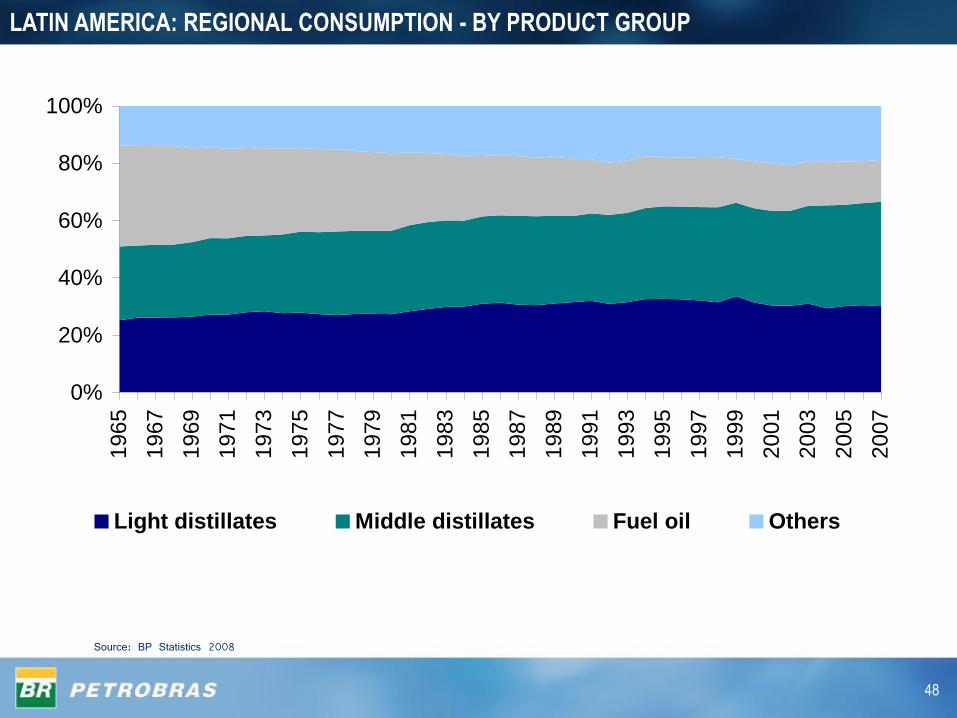

LATIN AMERICA: REGIONAL CONSUMPTION - BY PRODUCT GROUP

Source: BP Statistics 2008

0%

20%

40%

60%

80%

100%1965

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

Light distillates Middle distillates Fuel oil Others

49

25%

Sources: DOE (dez/08) and Brazil's National Petroleum Agency (ANP) (jan/09).

CONSUMER PRICES IN BRAZIL AND USA – GASOLINE AND DIESEL

39%

17%

19%

Crude Oil

Refining

Distribution & Marketing

Taxes

62%

16%

22%

Crude Oil

and Refining

Distribution & Marketingand Biodiesel (3%)

Taxes

DIE

SE

L

BrazilUS

56%

1%

24%

Crude Oil

Refining

Distribution & Marketing

Taxes

33%

17%

41%

Crude Oil

and Refining

Distribution & Marketing

Taxes

GA

SO

LIN

E

BrazilUS

9%Ethanol

25%

19%

50

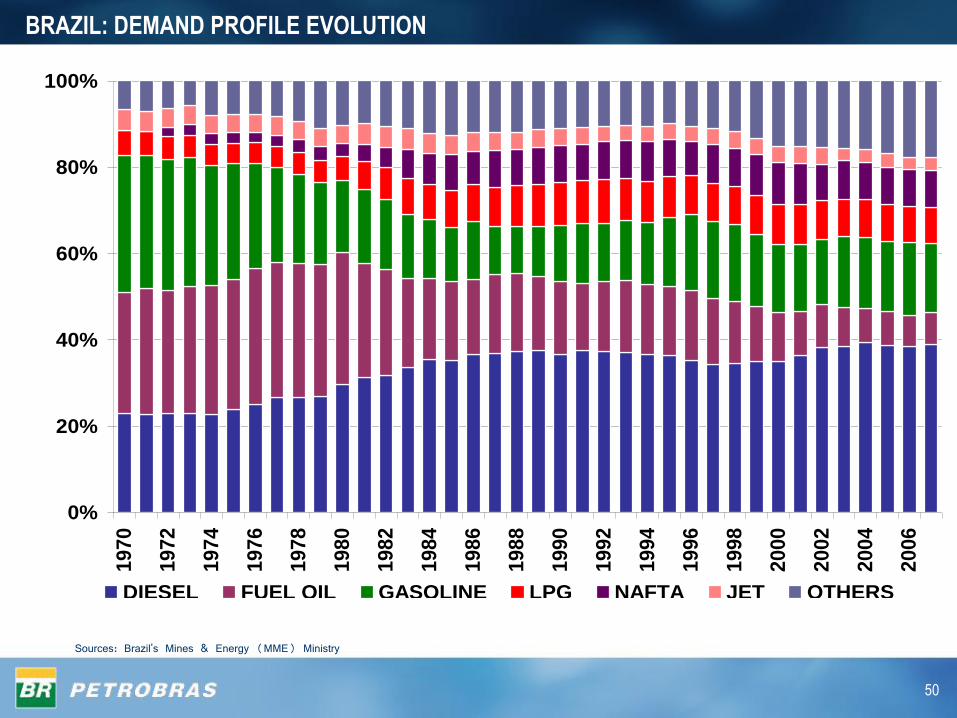

Sources: Brazil's Mines & Energy (MME) Ministry

BRAZIL: DEMAND PROFILE EVOLUTION

0%

20%

40%

60%

80%

100%

19

70

19

72

19

74

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

DIESEL FUEL OIL GASOLINE LPG NAFTA JET OTHERS

51

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

2005 2006 2007 2008

GASOLINE FLEX FUEL ETHANOL DIESEL

BRAZIL: UNIT SALES OF VEHICLES – BY FUEL

Source: ANFAVEA

49% 74%82%

82%

52

GASOLINE

34 51 56 43 34 48 46 6441

2000 2001 2002 2003 2004 2005 2006 2007 2008

DIESEL

99 112 10964 45 36 51 70 89

2000 2001 2002 2003 2004 2005 2006 2007 2008

JET

15 20 17 6 2 6 12 15 25

2000 2001 2002 2003 2004 2005 2006 2007 2008

FUEL OIL

29

10984 102

12698 113

91 73

2000 2001 2002 2003 2004 2005 2006 2007 2008

BRAZIL: SUPPLY AND DEMAND BALANCES

Surplus Deficit

Sources: Brazil's National Petroleum Agency (ANP)

Thousand bpd

53

BRAZIL: ETHANOL EXPORTS

Source: ANP

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

m³

North America S. & Cent. America Europe Others

54

(Thousand bpd)

BRAZILIAN FAST GROWING DOMESTIC DEMAND…

1,906

3.3% p.a.

3.0% p.a.1,945

2,257

2,876

230 257

326 332 367 419

250 218255

24684 89118

179

738 783

901

1224

112

150

182 202

274

400

214208

107119

2007 2008E 2013E 2020E

Others

FO

Diesel

QAV

Naphta

Gasoline

LPG

55

Tighter especifications for Diesel and Jet Fuel;

Better perspectives for Ethanol market than Biodiesel;

Bunker fuel market is going to marine gasoil path ;

Lack new HCCs due to credit crunch;

Excellent perspectives for distillates in emerging economies considering a recovery

of the global economy;

Gasoil demand is less elastic than gasoline. Few substitutes for diesel in relation to

gasoline. These two factors provide a more resilient demand for the diesel slate.

OTHER IMPORTANT ISSUES TO BE CONSIDERED

56