presentation on fatca and nris by ca n s srinivasan … · presentation on fatca and nris by ca n s...

TRANSCRIPT

PRESENTATION ON FATCA AND NRIs

By

Ca n s srinivasan

ON

WEDNESDAY THE 16 TH MARCH 2016

FATCA & NRI s

FATCA impacts only NRIS who are either citizens of US or residents of US.

Hence called hereinafter as USNRIS

SNAPSHOT OF PRESENTATION

Brief overview of FBAR / FATCA regulations

Brief overview of Amnesty schemes in US

Brief overview of Indian Statutory framework for FATCA

Impact of FATCA for US NRIs

Mitigatory measures to be taken by delinquent US NRIs

RESIDENTS OF US

Staying in US on employment / business visas for more than threshold period.

Even students with F1 visas could be residents in certain circumstances

Green card holders

COMPLIANCE OBLIGATIONS OF US NRIs

To report their global income to US IRS and pay tax

To report complete details of foreign bank accounts (FBAR)

To disclose full details of foreign financial assets (FATCA)

FBAR DISCLOSURE OBLIGATIONS

FBAR reporting in Treasury - Form TD F 90 - 22.1-separate form

To be filed before 30th June of next year with US Department of Treasury.

This is independent of filing US tax return

FBAR applies not only to ownership interest (whether present / future / contingent) but also to signing authority, whether sole or joint.

Even interest as nominee is covered.

Signing authority on behalf of companies / entities not covered.

Reporting required only if aggregate of balances in foreign bank and financial accounts exceeds US 10K.

If all incomes already reported and tax paid, but FBAR not complied, it can be quietly regularized (subject to penalties for past omissions)

If all incomes reported and existence of foreign bank accounts disclosed in the tax returns, then regularization of FBAR disclosure may not be an issue.

Minimum penalty for non compliance is US $ 10K- further penalty leviable for continuing offence with the maximum penalty capped at US $ 50K

FATCA DISCLOSURE OBLIGATIONS

FORM 8938

(EFFECTIVE FROM 01.01.2011)

To be filed with US IRS

To report ownership of foreign financial assets if their value exceeds threshold.

This is in addition to TD F 90-22.1

To be filed along with annual tax return

Need not be filed if no tax return is required to be filed

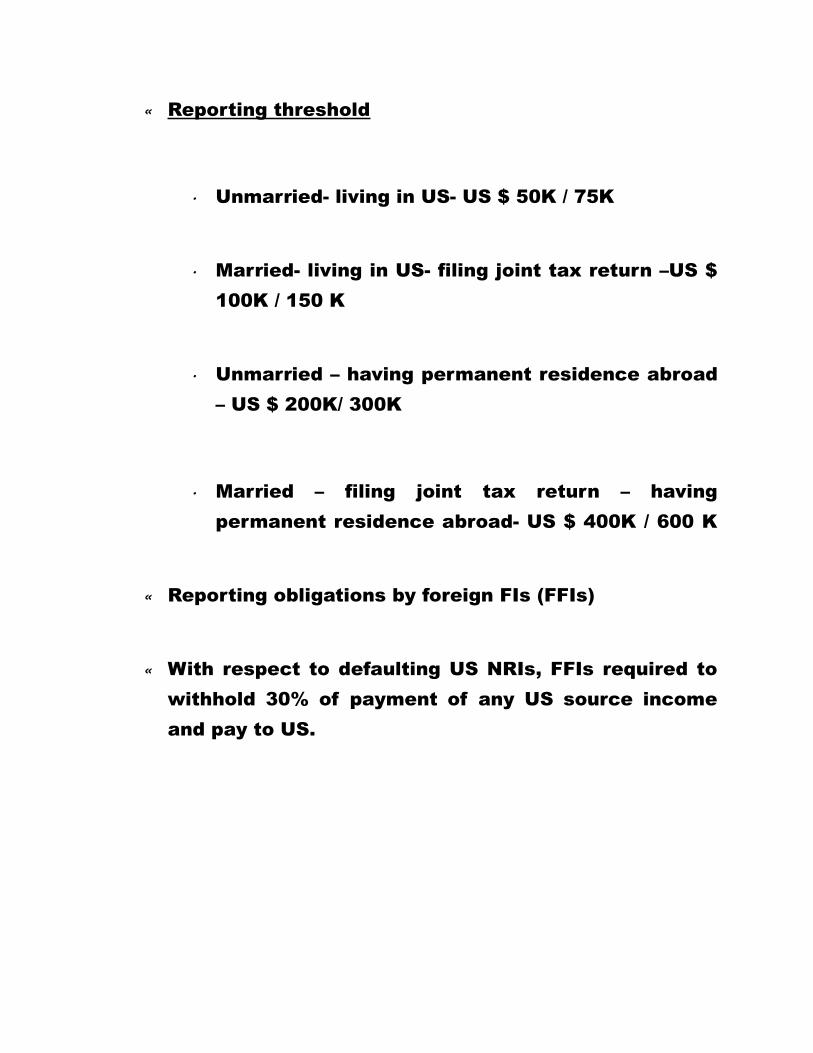

Reporting threshold

Unmarried- living in US- US $ 50K / 75K

Married- living in US- filing joint tax return –US $ 100K / 150 K

Unmarried – having permanent residence abroad – US $ 200K/ 300K

Married – filing joint tax return – having permanent residence abroad- US $ 400K / 600 K

Reporting obligations by foreign FIs (FFIs)

With respect to defaulting US NRIs, FFIs required to withhold 30% of payment of any US source income and pay to US.

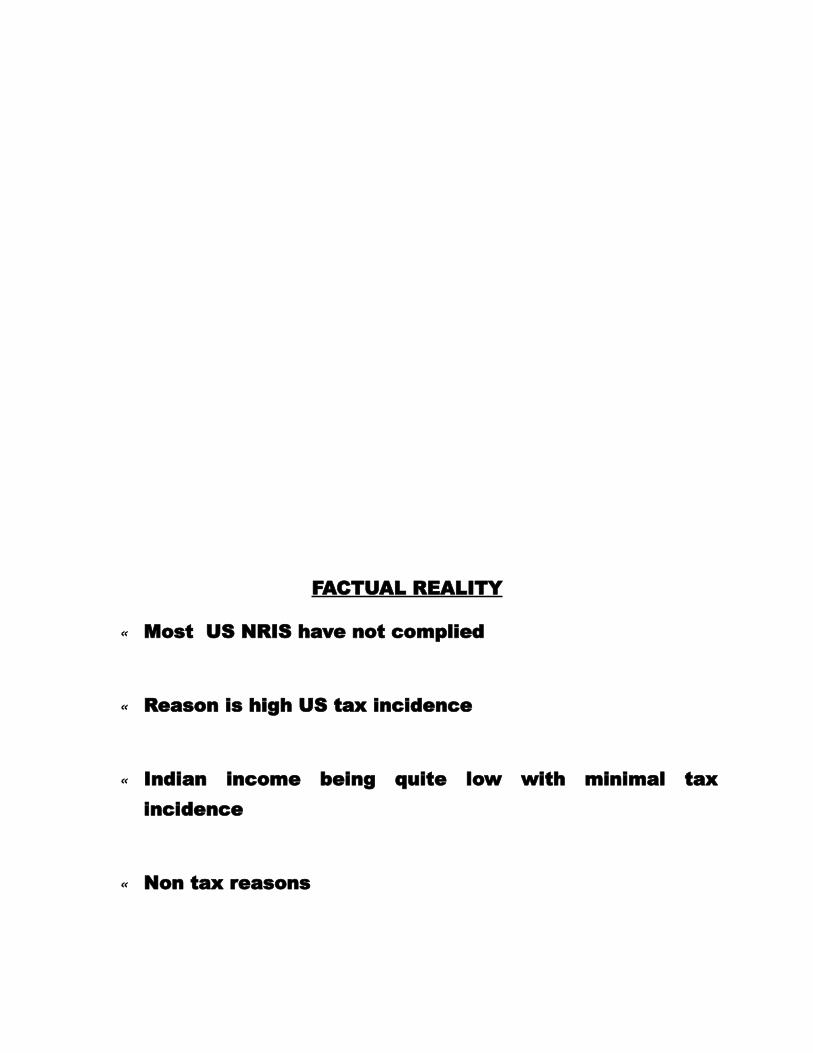

FACTUAL REALITY

Most US NRIS have not complied

Reason is high US tax incidence

Indian income being quite low with minimal tax incidence

Non tax reasons

Even if they want to regularise FBAR / FATCA, they don’t since put off by high tax and penalty for past periods

OVDPs

Simplified Amnesty schemes for regularisation

FATCA STATUTORY FRAMEWORK IN INDIA

Inter - Governmental Agreement (IGA) between India and US dated 9.7.2015 to implement FATCA regulations in India.

Section 285BA of I.T. Act 1961 read with Section 295 for issue of notifications

Rules 114F to 114H and Form 61-B of I.T. Rules 1962 introduced through CBDT Notification No. 62/2015]

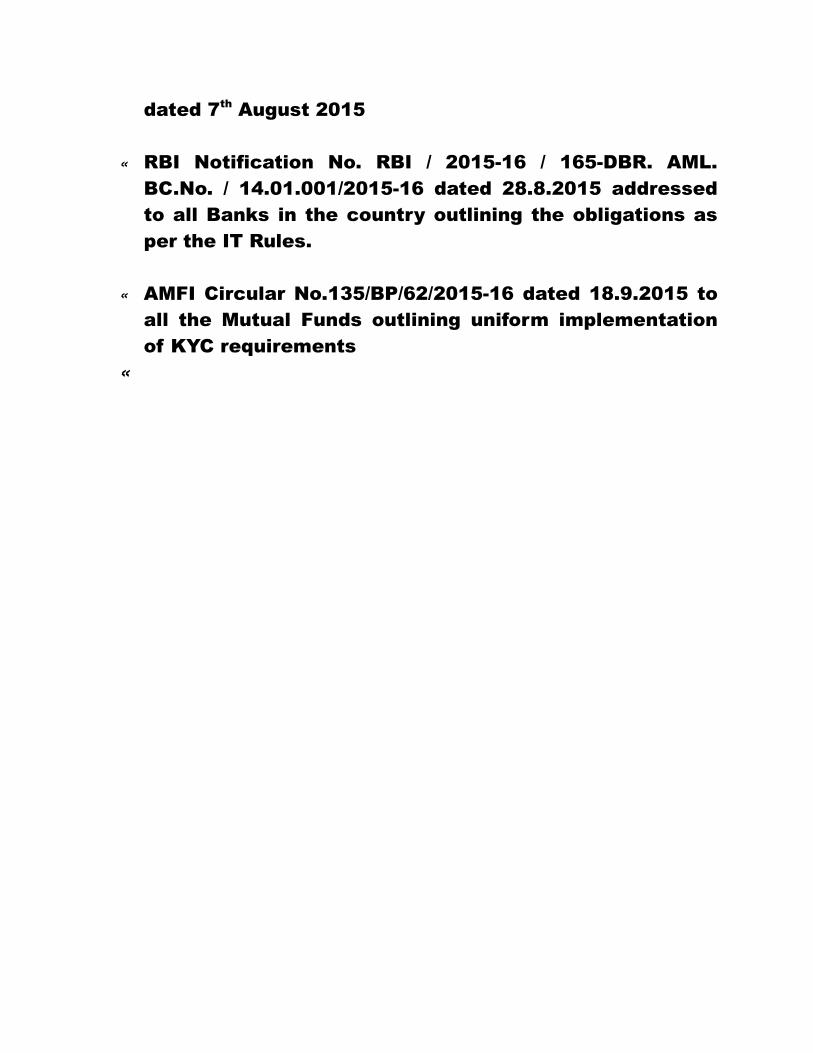

dated 7th August 2015

RBI Notification No. RBI / 2015-16 / 165-DBR. AML. BC.No. / 14.01.001/2015-16 dated 28.8.2015 addressed to all Banks in the country outlining the obligations as per the IT Rules.

AMFI Circular No.135/BP/62/2015-16 dated 18.9.2015 to all the Mutual Funds outlining uniform implementation of KYC requirements

SALIENT FEATURES OF RULES 114F TO 114H

Rule 114F – Definitions

Rule 114G – Lays down the obligations to maintain information and reporting

Rule 114H – Lays down the obligations to conduct due diligence review

Rule 114F – Important Definitions

Financial Account

o This is an exhaustive definition o Means accounts maintained by a financial

institution other than excluded accounts. o Such accounts include all deposits, DP accounts,

Equity or debt interest, insurance policies etc.,

Excluded Accounts

Retirement/pension accounts with annual contributions not exceeding US$ 50K

Senior Citizen Saving Scheme Account

Estate Accounts

Accounts maintained as per court orders/decrees

EMD/Advances accounts regarding transactions for purchase/sale/lease of properties

Financial Asset

Shares, stocks, bonds, debentures, futures and options, swaps, insurance policies, annuities, interest in partnership

Financial institutions

Banks, mutual funds, DPs, insurance companies, other financial entities and intermediaries

Non Reporting financial institutions

Government entities

International reporting organizations

Qualified credit card issuers

Financial institutions with local client base (not having place of business outside India and 98% of the accounts held by the residents)

Local banks (includes RRBs, UCBs, SCBs, DCCBs, LABs)

Financial institutions with low value accounts

PF/Gratuity funds

Passive income

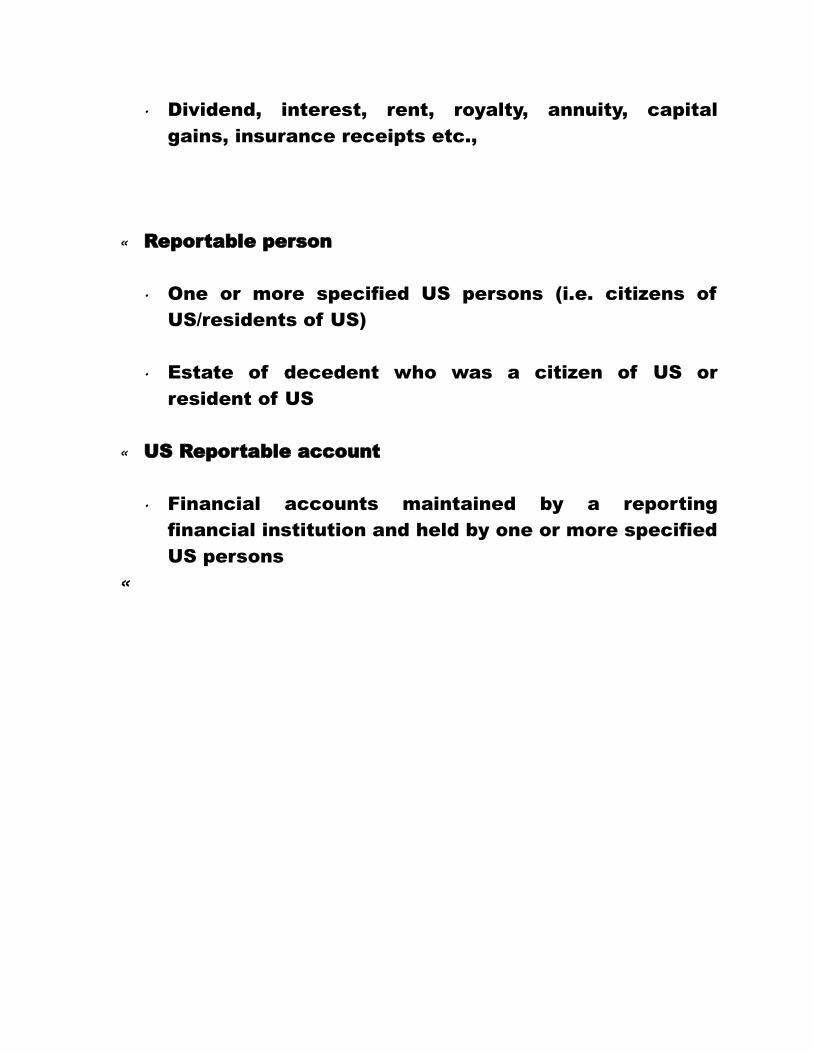

Dividend, interest, rent, royalty, annuity, capital gains, insurance receipts etc.,

Reportable person

One or more specified US persons (i.e. citizens of US/residents of US)

Estate of decedent who was a citizen of US or resident of US

US Reportable account

Financial accounts maintained by a reporting financial institution and held by one or more specified US persons

Rule 114G – Information maintenance and reporting

This applies to all the reporting financial institutions

They have to maintain and report information on financial accounts of specified US persons

The information includes name, address, TIN, date and place of birth, account number, balance/value of investment at the end of the year (if the account is closed during the year, information as on the immediately preceding date)

Where an entity has one or more controlling persons who are reportable persons, to furnish aforesaid information with respect to each of them.

DPs/Custodial account keepers to furnish information re: gross interest/dividend/sale/redemption proceeds

If an account holder is resident of more than one country, TIN to be furnished for each country of residence.

If there are no information to be reported, NIL statement to be furnished

Every RFI shall communicate the name, designation and contact details of the designated Director and Principal Officer to the concerned reporting authority and obtain a registration number

The statement to be furnished in IT Form 61-B for every calendar year and it should be furnished for every calendar year on or before 31st May of next year. This has to be furnished online with the digital signature of the designated Director/Principal Officer.

The statement to be furnished to Director of Income Tax (Intelligence and Criminal Investigation Unit)

For calendar years 2014 and 2015, information required to be reported only with regard to US reportable accounts.

For calendar years 2016 onwards, information required to be reported for all reportable accounts

Rule 114-H – DDR Obligation

Obligations are spelt out separately for pre-existing accounts and new accounts

The accounts are also classified as individual accounts, entity accounts and NPFIs.

A reportable account is a financial account identified through DDR and held by a reportable person or a foreign entity controlled by specified US person or a passive non-financial entity with one or more controlling specified US persons

US reportable account is a financial account held by a US person or entity not based in US, but controlled by specified US person

Minimum threshold prescribed beyond which only, this obligation apples

For instance, in the case of pre-existing accounts, no review/reporting required if the balance as on 30.6.2014 does not exceed US$ 50K or cash value of insurance policies does not exceed US$ 250K

HOW FATCA WILL AFFECT US NRIs

For US NRIs already disclosing all their global incomes and assets to US Government , there is no impact.

Only those who have not disclosed any of their global assets / incomes or made only partial disclosure, there could be problems

HOW FATCA WILL IMPACT

By virtue of IT Rule 114 G, Indian Tax authorities collect information

Such information will be exchanged with US IRS

When US IRS find mismatch between disclosure already made and information obtained from India, it could lead to disastrous consequences by way of steep penalties, tax liabilities and interest liabilities on past incomes and prosecution also

The penalty will be for non filing of tax returns as well as late payment of taxes, non filing of FBAR / FATCA

HOW FATCA TRAP IS AVOIDED

To review global undisclosed assets and income

If the value of those assets less than reporting thresholds for FBAR / FATCA , then examine the likely US tax liability on incomes from those assets for past six years.

If the US tax liability with penalty under OVDP or regularization scheme is not much, to opt for the same.

Otherwise , to transfer out the assets to other family members (other than spouse and children) subject to other considerations.

Even interest in assets (interest in estate, trust, HUF) to be relinquished.

Later, those assets may be transferred to US through other schemes under FEMA.

Settlement by family members to US NRIs through trusts with benefits distribution deferred to future period.

Maintaining bank accounts with smaller banks

OTHER PRECAUTIONS RE : US NRIs

All tax free Indian incomes to be reported to US (Eg: Interest on FCNR / NRE deposits and tax free bonds, dividends, LTCG on shares)

Certain standard deductions under Indian tax laws not available in US (Eg: 30% deduction for property income). Instead, only the actual expenditure is deductible

Provisions re: Capital gains computation are different under US tax laws.

Especially, exemptions not available for re-investment made in India.

Even though tax credit available in US for Indian tax paid, to consider State tax payable in US to arrive at overall tax liability

To consider incidence of inheritance tax and its mitigatory measures.

While transferring out assets to other family members, to consider impact of gift tax as well as inheritance tax.

To be careful before obtaining citizenship for parents / parents in law

Surrendering US citizenship

NO. OF US CITIZENS GIVING UP CITIZENSHIP

2013 – 2999

2014 – 3415

Others are still retaining citizenship for different reasons which are :

For receiving pensions (whether employment oriented or social security) already vested

For getting medical treatment at a nominal cost whenever they want to visit US

For avoiding hassles of getting US VISA for visiting their near and dear living in US

For getting either free or concessional educational facilities for their children who are born in US and hence are naturalized US citizens

Due to prohibitive cost in the form of exit tax levied by US IRS on assets left behind in US

SIMPLIFIED AMNESTY SCHEME

For US NRIs living in US – 6 years income disclosure with 5% penalty on the maximum value of undisclosed assets at any time during the last six years

For US NRIs living outside US – 3 years income disclosure with no penalty

This is far better than OVDP of 2012 wherein the penalty could go upto 27.5% of the maximum value of undisclosed assets at any time during the last eight years