ppt cash book navneet mishra

TRANSCRIPT

Cash book is the special journal which

is used for recording all cash

transactions. It may be defined as the

book in which transactions are

recorded in detailed particulars of all

money received and paid.

Cash book is divided into two parts ;

A) Cash receipt

B) Cash payment

FEATURES OF CASH BOOK

• To keep record of only cash transactions

• All receipts are recorded in debit side

• All payments are recorded in credit side

• Chronological (date wise) transaction recording of all

transactions.

• Performs function of both journal and ledger.

Date Particular Lf Cash Date Particular Lf Cash

` `

Cr

.

To ascertain the balance of cash in hand and at bank at any time

without actually counting cash and examining Bank passbook

To verify the correctness of cash in hand and bank.

IMPORTANCE OF CASH BOOK

It is both a subsidiary book and a principal book.

It helps the trader to understand the cash in hand and cash at bank.

It gives information about

daily closing cash and bank balance at the end of

each day.

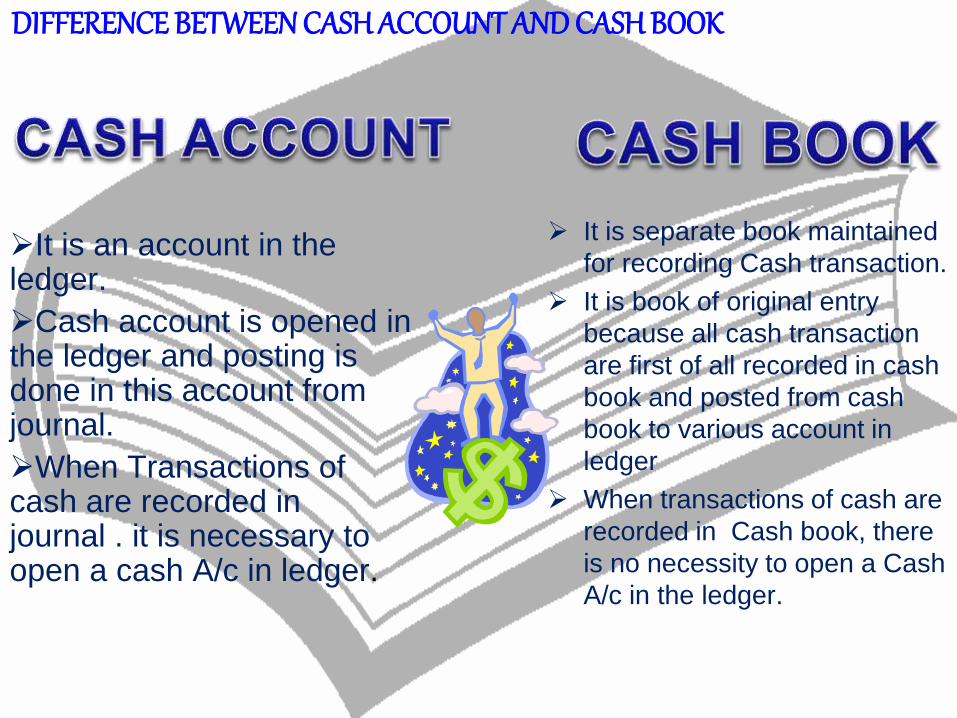

It is an account in the ledger.

Cash account is opened in the ledger and posting is done in this account from journal.

When Transactions of cash are recorded in journal . it is necessary to open a cash A/c in ledger.

It is separate book maintained

for recording Cash transaction.

It is book of original entry

because all cash transaction

are first of all recorded in cash

book and posted from cash

book to various account in

ledger

When transactions of cash are

recorded in Cash book, there

is no necessity to open a Cash

A/c in the ledger.

DIFFERENCE BETWEEN CASH ACCOUNT AND CASH BOOK

Discount allowed is given to customers by the business when they pay their accounts quickly.

The discount allowed is put on the debit side of the cashbook.

DISCOUNT RECEIVED

The business also receive a discount from its

suppliers if it pays its accounts quickly and this

is called discount received.

The discount received is put on the credit side

of the cashbook.

The discount column in the CASH BOOK are merely

totalled and not balanced.

Discount account are opened again in ledger and

totals of discount columns in the CASH BOOK are

posted there.

Discount column is only memorandum column and

not based on double entry system.

• Bank Overdraft is the excess amount withdrawn from the bank account than the amount deposited in it.

• Bank over draft is recorded in the credit side of the cash book in bank column.

Two (Double) Column Cash Book

When discount is allowed on the receipt of

cash and discount is received when payment

is made to suppliers, it becomes desirable to

add discount column along with cash on both

sides of the cash book.

Format of Double Columns Cash Book

Date Particulars L.

F

Discount Cash Date Particula

rs

L.

F

Discount Cash

` ` ` `

Dr

.Cr.

Format of Double Columns Cash Book

Date Particulars L.F Bank Cash Date Particular

s

R.No. L.

F

Bank Cash

` ` ` `

Dr

.Cr.

Some transactions are recorded in a Cash

book and bank book ,i.e., balance of one

decreases and that of the other increases

due to such transactions. Such transactions

are entered on both sides of the cash book.

Such entries are known as Contra Entries. It

is denoted by

Jan 4 `2000from office and deposited in bank

Jan 8 ` 3500 are withdrawn for office use

Date Particul

ar

L .f Cash

(`)

Bank (`) Date Particul

ar

L .f Cash

(`)

Bank

(`)

Jan. 4 To cash C - 2000 Jan.4 By bank C 2000 -

Jan . 8 To

bank

C 3500 - Jan . 8 By cash C - 3500

Three column cash book is a cash book

which has three columns on each side; one

column to record discount allowed, another

to record discount received, another to

record cash transactions and yet another to

record bank transactions. In other words,

we can say that triple or three-column Cash

Book represent two account i.e., Cash

account and bank account .

DATE PARTICULAR L

.

F

DISCO

UNT

CAS

H

BANK DATE PARTICULAR L

.

F

DISC

OUN

T

CASH BANK

Dr. C

r.

Date Particulars L.F.Discount Cash

Bank Date Particulars L.F. Discount Cash

Bank

2013

Jan.1 To Balance

b/d

1,550 13,575 Jan 1 By Office

Equip.

750

Jan 1 To Sales a/c 1,315 Jan 3 By Bank c 500

Jan 3 To Cash a/c c 500 Jan 6 By

Purchases

a/c

1,005

Jan 4 To A Hussan 2,550 Jan 8 By Bank c 2,550

Jan 8 To Cash c 2,550 Jan 16 By Salman 5 915

Jan 10 To Hayat

Khan15 775 Jan 27 By Gulzar 650

Jan 12 To Sales a/c 1,500 Jan 30 By Salaries

a/c

1,750

Jan 31 To Cash c 775 Jan 31 By Bank c 775

Jan 31 To Bank c 250 Jan 31 By Cash c 250

By

Balanced

c/d

1,865 14,330

2013

feb 1

To balance

b/d

1,865 14,330

Jan.1Purchased office typewriter for cash `750;

cash sales `315Jan 31 Deposited into bank the cheque of Hayat Khan.Jan 30 Paid salaries by cheque `1,750Jan 27 Paid to Gulzar Ahmad by cheque `650Jan 16 Paid Salman `915 by cheque, discount received `5

Jan 12 Sold merchandise to Divan Bros. for `1,500 who paid by cheque which was deposited in the bank.

Jan 10 Received from Hayat Khan a cheque for `775 in full settlement of his

account and allowed him discount `15.Jan 8 Deposited into bank the cheque received from A. Hussan.Jan 6 Paid by cheque for merchandise purchased worth `1,005

Jan 4 Received from A. Hussan a cheque for

`2,550 in part payment of his accountJan 3 Deposited cash `500Jan 31 Drew from bank for office use `250.

• Endorsement of a cheque :-Sometimes, a

cheque received from a customer is not

deposited into bank, but it may be given to some

other persons i.e., endorsed. On receipt, it will

be entered in the cash column on the debit side.

On endorsement, it will be entered in the cash

column on the credit side

• Bank charges :- Bank usually charges some

amount for the services rendered to its

customers. Such charges will be recorded on the

credit side as ‘By Bank Charges` and the

amount will be recorded in the bank column.

.

Some important Transaction

• Bank charges on dishonored

cheques:- Expenses charges by the

bank on dishonored cheques will be

added into the amount of dishonored

cheques itself.

• Amount directly deposited by a

customer into our Bank A/c:- When

the information of such a deposit is

receive by the trader, it will be

recorded on the debit side of the cash

book and amount will be entered in

the bank column.

•Internet allowed by the bank:- Internet allowed (credited) by the bank increases the balance at bank. The entry for such interest is, therefore, recorded on the debit side in the bank

column.

• Internet charges by bank:-

when interest is charged (debited) by the bank on the amount of bank over draft, the entry is recorded on the credit side in

bank column.

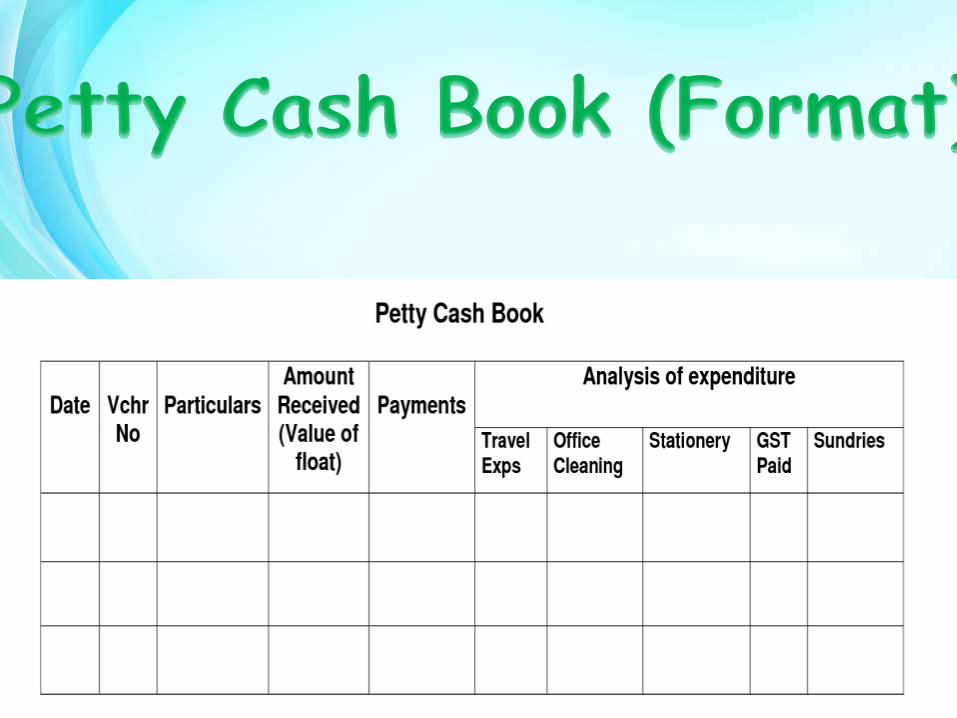

• The petty cashier is given a definite sum, says `2,500, at the time beginning of a certain period. this amount is called 'imprest amount'.

• The petty cashier goes on paying all petty, say after a month, the chief cashier reimburses the amount actually spent by the petty expenses out of this impress amount and records them in the petty cash book maintained by him.

Cash column of the cash book, will always have a debit balance, because cash payment cannot be mare than the cash in hand.

Bank column of the cash book can either debit balance, because in bank column in the cash book represents bank account.

Bank account will have a credit balance if it is overdrawn and will otherwise have a debit balance.