ppp trends and initiatives in south asian countries

TRANSCRIPT

PPP trends and initiatives in South Asian Countries

Policy Dialogue on PPP for Infrastructure

Development in South Asia

Organized by UN ESCAP

21-22 September 2015

Page 2

Agenda

Infrastructure Assessment of South Asian Countries 1

Emergence of PPPs in South Asia

India’s experience so far 3

Challenges and Way Ahead for PPPs in South Asian Countries 4

2

Page 3

South Asia region lags behind in infrastructure development…

Key points:

►No South Asian country in Top-50

►Huge infrastructure gap in all South Asian countries

Source: The Global Competitiveness Report 2014–2015

Note: Information not available for Afghanistan and Maldives

Infrastructure Ranking

127

92 87

132 119

75

Bangladesh Bhutan India Nepal Pakistan Sri Lanka

Page 4

…hence, the region requires $ 4-5 trillion of investment by 2030…

Key points:

►Investment to a tune of USD 4-5 trillion required between 2010 and 2030 to bridge

the gap

Americas

$16–17 trillion

Europe

$8–10 trillion Asia/Oceania

$15-20 trillion

Africa/Middle-East

$2–3 trillion

US / Canada

~$6-6.5 trillion

China ~$6.5-7 trillion

India ~$3-3.5 trillion WORLD TOTAL

$40 – 50 trillion

Source: BCG report – The Global Infrastructure Challenge 2010, Secondary research, EY Analysis

Infrastructure Investment Requirement

Page 5

Public sector spending alone wouldn’t suffice $ 4-5 trillion investment requirement…1/2

Source: www.cia.gov, EY Analysis (As per 2004 estimates)

Key points:

►Budget deficit has put substantial constraints on scarce public resources in most

south Asian countries

-12 -10 -8 -6 -4 -2 0 2

Bangladesh

Bhutan

India

Nepal

Pakistan

Sri Lanka

Budget Surplus/Deficit (as % of GDP)

Page 6

Public sector spending alone wouldn’t suffice $ 4-5 trillion investment requirement…2/2

Source: www.cia.gov, EY Analysis (As per 2014 estimates)

Key points:

►Huge public debt puts further constraints on scarce public resources

►Major share of USD 4-5 trillion of investment to come from the private sector

0 20 40 60 80 100

Bangladesh

Bhutan

India

Nepal

Pakistan

Sri Lanka

Public Debt (as % of GDP)

Page 7

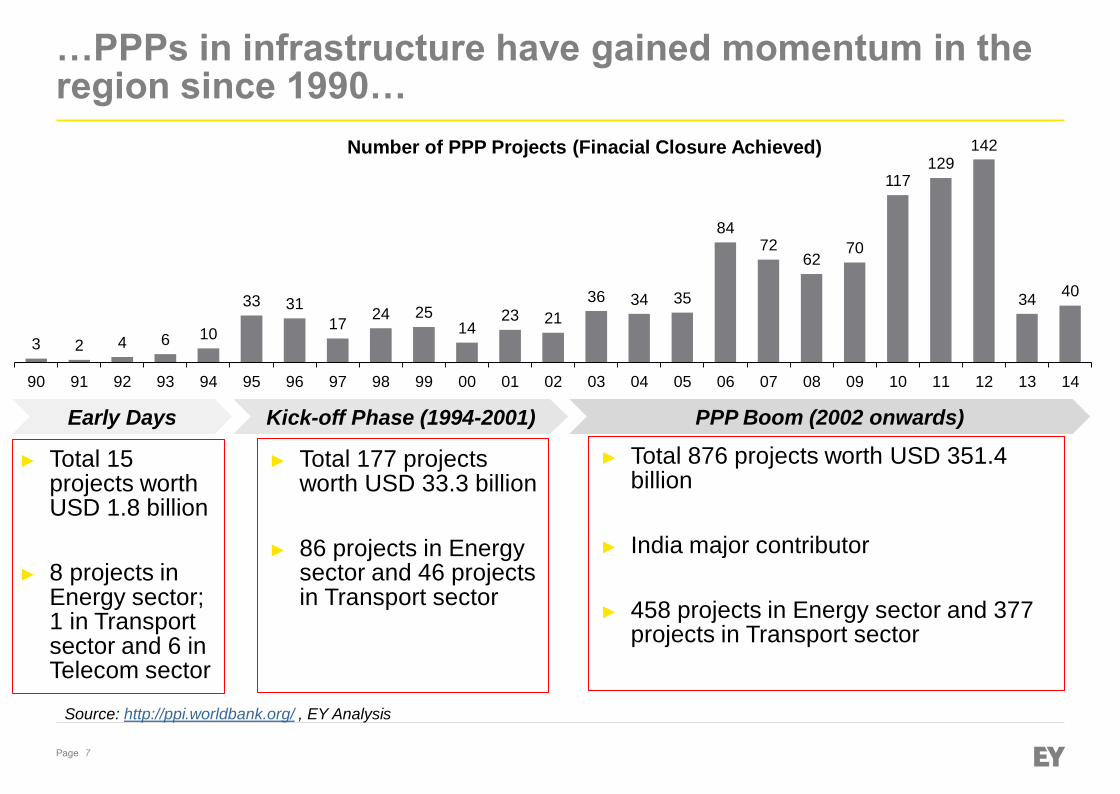

3 2 4 6 10

33 31

17 24 25

14 23 21

36 34 35

84 72

62 70

117 129

142

34 40

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

Number of PPP Projects (Finacial Closure Achieved)

…PPPs in infrastructure have gained momentum in the region since 1990…

Source: http://ppi.worldbank.org/ , EY Analysis

Early Days Kick-off Phase (1994-2001) PPP Boom (2002 onwards)

► Total 15 projects worth USD 1.8 billion

► 8 projects in Energy sector; 1 in Transport sector and 6 in Telecom sector

► Total 177 projects worth USD 33.3 billion

► 86 projects in Energy sector and 46 projects in Transport sector

► Total 876 projects worth USD 351.4 billion

► India major contributor

► 458 projects in Energy sector and 377 projects in Transport sector

Page 8

India

0

50

100

150

200

250

300

350

400

0 100 200 300 400 500 600 700 800 900

Inve

stm

ent

in U

SD

bill

ion

Total Number of PPP Projects

India is leading the way for PPP projects in the region…

Country wise PPP projects and investments till 2014 ► India front runner in PPP projects -

Financial closure for 847 projects

(76% of total projects) amounting to

USD 338 billion

► Energy and Transport sectors have

been the focus of private sector

participations in the region

Key points:

►India is front runner in terms of numbers of PPP projects and investments

►Afghanistan, Bhutan and Maldives have not seen much PPP investments

Source: http://ppi.worldbank.org/ , http://www8.cao.go.jp/pfi, EY Analysis

Page 9

India’s PPP story so far 50% of infrastructure investment to come from private

22%

37%

48%

Tenth FYP Eleventh FYP Twelfth FYP (P)

Infrastructure investment

Private

Public

Source: Twelfth Five Year Plan and Eleventh Five Year

Plan, Planning Commission

0123456789

20

02

-03

20

03

-04

20

04

-05

20

05

-06

20

06

-07

20

07

-08

20

08

-09

20

09

-10

20

10

-11

20

11

-12*

Investment (as %age of GDP)

Private Public Total

Tenth FYP Eleventh FYP

* Estimated, Source: Gajendra Haldea, “Building Infrastructure: Challenges and

Opportunities,” 7 July 2010; Twelfth Five Year Plan 2012-2017, Planning

Commission

Key points:

►Private sector participation has continuously increased with 12th FYP envisaging

around 50% of infrastructure investment to come from private sector

Page 10

India’s PPP story so far Score on Critical Success Factors (CSFs) encouraging PPP

Weak

Moderate

Strong

*Scoring is based on our perception

PPP Projects in India

Robust Risk

Allocation

Framework

Economic &

Financial

Viability

Adequate

Government

Support

Strong &

Matured

Private Sector

Stakeholders

Participation &

Interactions

Stable Political

Situation & Will

Transparent &

Fair

Procurement

Process

Well

developed

Financial

Market

Strong Legal/

Regulatory

Framework

Page 11

1

India’s PPP story so far But still lot to be achieved

Policy / Regulatory Reforms ► Preparation and implementation of dedicated PPP policy and rule

► Creation of an Independent PPP Regulator and Dispute resolution courts

► Making Value-for-money (VFM) mandatory for each project in the PPP policy/ rule

2 Institutional Reforms

► Development of institutional capacity at state and local body level

► Improvement of PPP database management at national and state level

3 Financing Reforms

► Development of long term lending financial markets in the country

► Development of new financial products such as take-out financing and refinancing

Page 12

PPP projects in the South Asia region face multi-facet challenges…

Weak Legal/ Regulatory Framework

Poorly Prepared/ Structured Projects

Lack of Capacities

Weak Financial Environment

►Absence of

legislation

►Absence of sector

specific regulators

in many countries

except India

►Absences of Model

Concession

Agreements

(MCAs) with robust

risk allocation

framework in many

countries

►Dispute resolution

mechanism is a

major area of

concern

►Value for money

analysis not given

much priority

►Except for India,

most countries in

the region

significantly lack in

capacities, both in

public and private

sector

►Lack of dedicated

financial

institutions in most

countries

►Limited

involvement of

insurance/ pension

funds

►Lack or

underdeveloped

financial products

such as long term

loans, take-out

finance, etc.

Page 13

To foster infrastructure investment and thus growth, the Region needs to overcome existing challenges by…

►Regional co-operation on knowledge sharing, improvement of financial

climate, and capacity building of both private and public sector

►Strengthening the regulatory and legal framework

►Putting more emphasis on project preparation including value for money

analysis

►Development of robust risk allocation framework and dispute resolution

mechanism

►Development of local infrastructure bond markets, long term lending

institutions, and innovative products such as take-out financing and

refinancing

Page 14

Thank You Abhaya Agarwal Partner - Infrastructure and PPP

Ernst & Young LLP 6th Floor, Hindustan Times House, 18-20, Kasturba Gandhi Marg, New Delhi, Delhi 110 001, India

Phone: +91 11 4363 3000 Email: [email protected]