post-issuance matters georgia fiscal managers council september 2015 conference 1

TRANSCRIPT

POST-ISSUANCE MATTERS

Georgia Fiscal Managers CouncilSeptember 2015 Conference

1

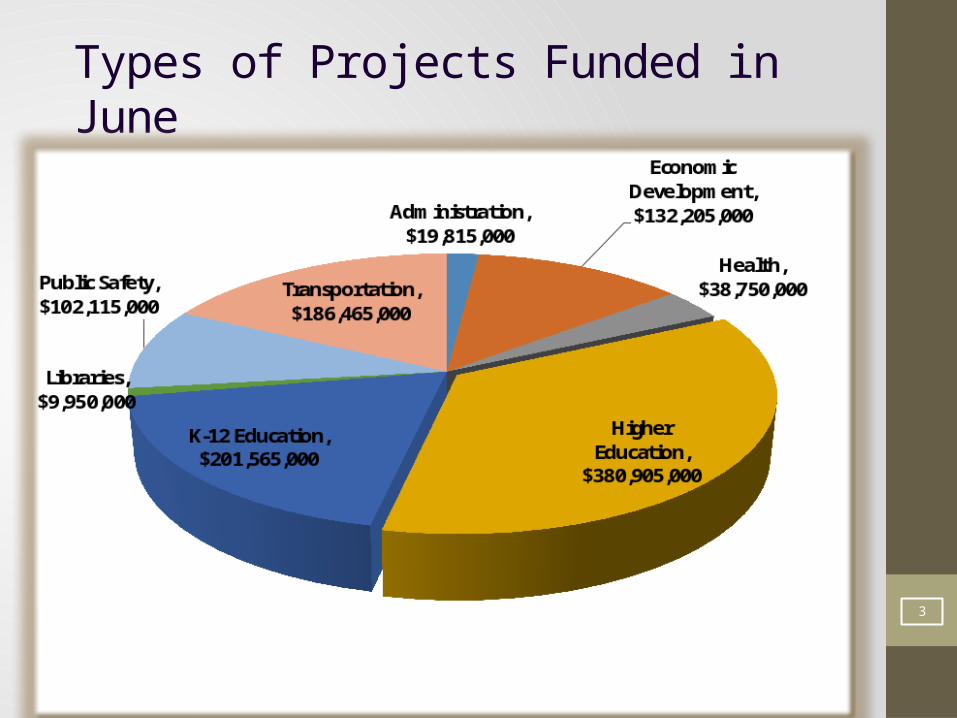

June 2015 Bond Sale

$ 1,284,340,000State of Georgia

(Largest Sale for the State)

$560,525,000 General Obligation Bonds 2015A$447,830,000 General Obligation Bonds 2015B (Federally Taxable)

$275,985,000 General Obligation Refunding Bonds 2015C

2

Types of Projects Funded in June

3

Post- Issuance: Why do we care?

4

5

Not an option…

6

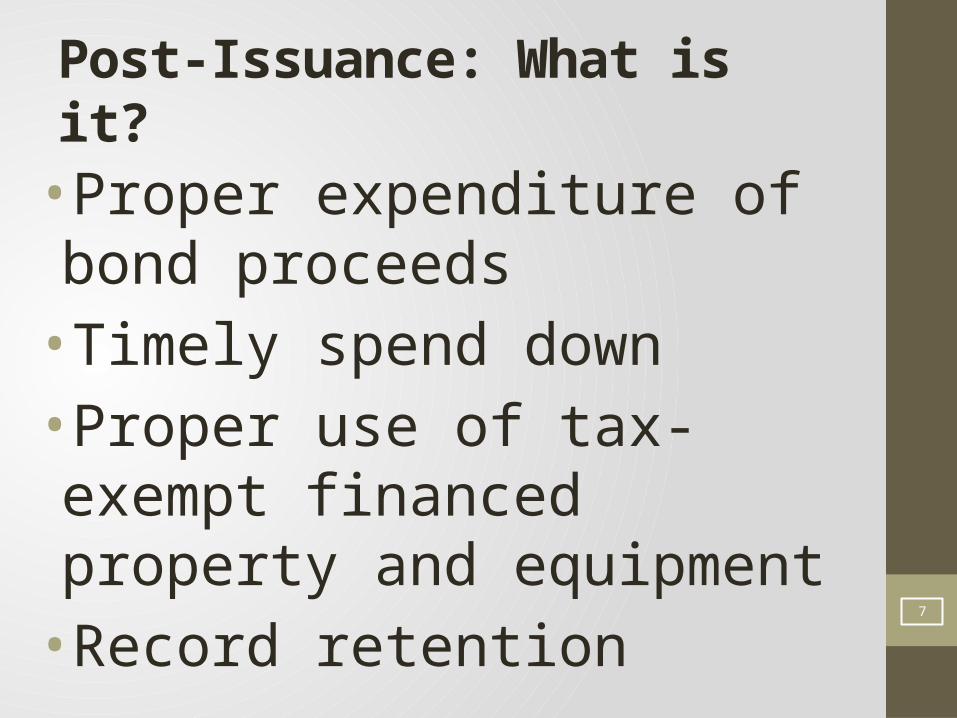

Post-Issuance: What is it?

•Proper expenditure of bond proceeds

•Timely spend down•Proper use of tax-exempt financed property and equipment

•Record retention7

Pop Quiz Time

8

QUESTION 1

WHAT 4 THINGS MAKE A PROJECT ELIGIBLE FOR

TAX-EXEMPT BOND PROCEEDS?

9

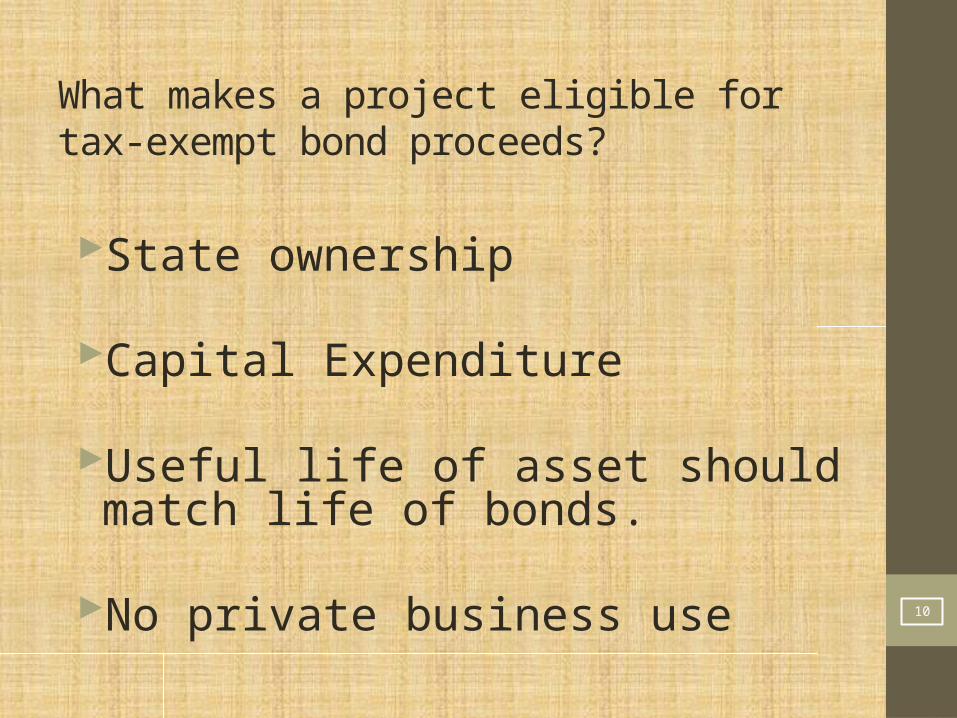

What makes a project eligible for tax-exempt bond proceeds?

State ownership

Capital Expenditure

Useful life of asset should match life of bonds.

No private business use10

Expenditures Ineligible for Reimbursement

• Personal services• Lease payments• Maintenance agreements for copiers or

computers• Depletable/disposable items• Moving Costs• Decorative items• Office supplies• Fuel oil• Termite inspections• Drug tests for employees• Annual fire inspections

11

QUESTION 2

WHAT 3 ITEMS NEED TO BE DOCUMENTED FOR EACH

PROJECT FUNDED BY BOND PROCEEDS?

(HINT: WE CALL THIS ASSET TRACKING)

12

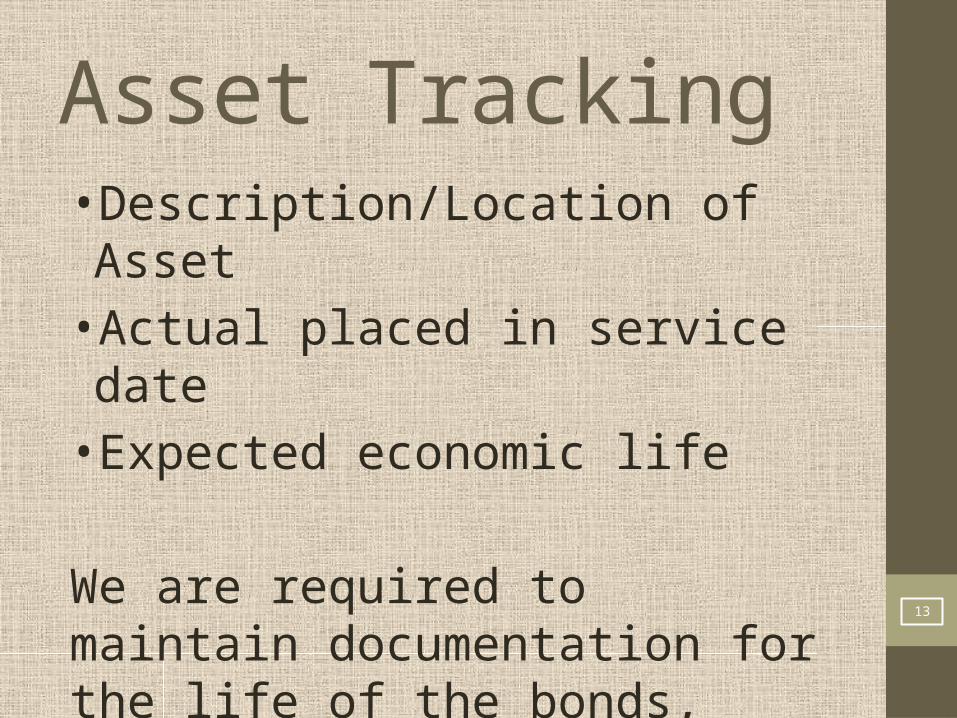

Asset Tracking• Description/Location of Asset• Actual placed in service date• Expected economic life

We are required to maintain documentation for the life of the bonds, plus five years.

13

QUESTION 3 – SPEND-DOWN

WHAT IS THE FIRST SPEND-DOWN DEADLINE?

6 Months14

QUESTION 4 – SPEND-DOWN

HOW MUCH NEEDS TO BE SPENT OR CONTRACTUALLY OBLIGATED AT THAT TIME?

5% Spent or Contractually Obligated 15

QUESTION 5 – SPEND DOWN

WHAT IS THE SECOND SPEND DOWN DEADLINE?

3 Years16

QUESTION 6 – SPEND-DOWN

HOW MUCH NEEDS TO BE SPENT AT THAT TIME?

85% Spent

***(Unlike 6 month spend down this spend down has to be amounts SPENT not Contractually Obligated)

17

QUESTION 7 – SPEND-DOWN

WHAT IS THE FINAL SPEND DOWN DEADLINE?

5 Years18

QUESTION 8 – SPEND-DOWN

WHAT HAPPENS IF FUNDS ARE NOT SPENT BY THAT TIME?

Proceeds are forfeited!

19

6 Months5% Spent

or Contractually

Obligated

3 Years85% Spent

5 Years100% Spent

ALL proceeds must be spent or forfeited PRIOR to reaching the 5 Year date.

IRS Spend-Down Rules Recap

20

QUESTION 9

WHAT IS PRIVATE BUSINESS USE?

21

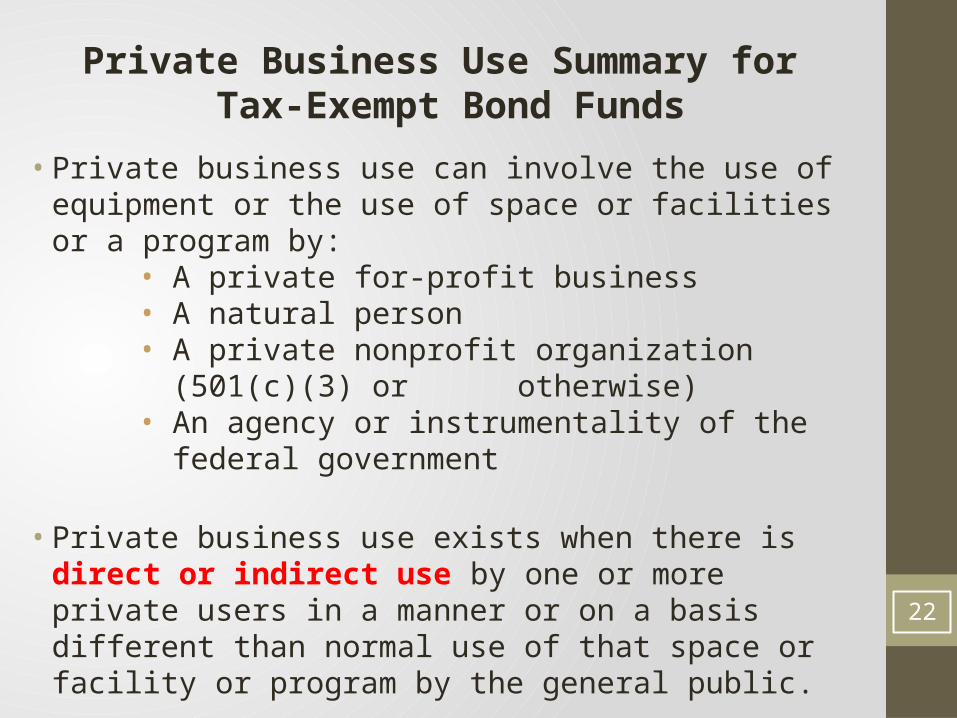

• Private business use can involve the use of equipment or the use of space or facilities or a program by:

• A private for-profit business• A natural person• A private nonprofit organization (501(c)(3) or

otherwise)• An agency or instrumentality of the federal

government

• Private business use exists when there is direct or indirect use by one or more private users in a manner or on a basis different than normal use of that space or facility or program by the general public.

22

Private Business Use Summary for Tax-Exempt Bond Funds

Private Business Use May Include management or service contracts leases research contracts (including any with federal

government) parking contracts use of space within a public use facility by a private

citizen or company for the operation of a business enterprise, even if that enterprise serves the visiting public, agency clients or customers, or state employees

naming rights for buildings and athletic facilities use by the federal government Some examples: food services operated by a private

vendor, prison facility operated by a private vendor, land leased to a private entity. (janitorial services ok)

If in doubt – Ask.23

Qualified Management Agreements• Reasonable

• Not give the service provider the equivalent of an ownership interest in the financed facility

• Compensation not based in whole or in part on a share of the net profits of the operations of the facility 24

PBU Annual Survey Example

25

QUESTION 10

HOW CAN YOU KEEP OUR TAX-EXEMPT BONDS

TAX-EXEMPT?

26

27