perspective analyst(s): david furlonger - amazon s3€¦ · g00297526 2016 cio agenda: a financial...

TRANSCRIPT

G00297526

2016 CIO Agenda: A Financial ServicesPerspectivePublished: 19 February 2016

Analyst(s): David Furlonger

FI CIOs are responding to digital challenges and new businessopportunities. Their institutions must realign their organizations andmindsets in terms of a networked ecosystem of multifaceted businessmodels, delivery mechanisms, talent, leadership and "coopetition" to surviveand thrive.

Key Findings■ We are now knee-deep in the era of digital business, but most FIs are struggling to reimagine

industry business and operating models based on digital capabilities and emergent newecosystems.

■ Ecosystem strategies provide a solid foundation for transitioning the business away from alinear value chain into a broad-based network of physically and digitally connected entities.

■ The ecosystem challenge and imperative will be further accentuated by the entry of large digitalplayers as strong competitors in the FS domain. They "own" a captive ecosystem andtransactional context that FIs will struggle to replicate.

■ "Fintech" is merely a precursor to a more radical shift in the sourcing, management and use ofFS — regardless of historic standard industry classification codes.

Recommendations■ Impress upon your CEOs and boards the need for more coherence and clarity concerning

digital strategy and the role of the FI in digital ecosystems that are co-creating value forparticipants.

■ Identify and rationalize processes and silos that would otherwise create frictional barriers tobusiness partners and the digital ecosystem. Trends fostering openness promote more-porousinstitutional boundaries that allow for the capture of new economic opportunities.

■ Ensure the digital strategy stays on track by closely monitoring business returns. Leading CIOsspend up to 70% of their time "in the business" and "with the business." This is a goal to whichall CIOs should aspire.

■ Seek to delegate more day-to-day operational IT activities, and spend more time withcustomers and business leaders, to influence and increase enterprise digital savvy, as well asbuild stakeholder power.

Table of Contents

Survey Objective.................................................................................................................................... 3

Data Insights.......................................................................................................................................... 3

The State of Industry Digitalization.................................................................................................... 5

The Technology Opportunity: Capitalize on the Customer Context via Big Data and Digital Business

.......................................................................................................................................................11

Business Threats Are Substantial: Resources, Security, Fintech Disruption, Cultural Behavior.........15

Digital Execution and Performance Relies on Organizational Change.............................................. 18

Digitalization Fundamentally Alters the Way Business Is Done, Behaviorally and Culturally; Sufficient

Talent Is One Thing, Having the Right Talent Is Something Else.......................................................20

Regardless of the Presence of a Chief Digital Officer, Advanced Technology Leadership Is an

Essential Component of Digital Excellence......................................................................................23

Methodology.................................................................................................................................. 27

Gartner Recommended Reading.......................................................................................................... 28

List of Figures

Figure 1. Digital Business Development Path.......................................................................................... 6

Figure 2. Digitalization Creates Greater Access to, and Greater Numbers of, Reward Opportunities....... 7

Figure 3. Across the World, the Picture Is the Same — an Expectation of Significant Digital Revenue

Growth................................................................................................................................................... 8

Figure 4. Digitalization Is Still Quite Operational, the Potential Is Much Greater......................................10

Figure 5. The Technology Opportunity: Capitalize on the Customer Context via Big Data and Digital

Business.............................................................................................................................................. 12

Figure 6. The Technology Opportunity: There Is Global Variance: Balance Shared Services With

Localized Execution..............................................................................................................................13

Figure 7. Top Banking Solution/System Priorities, 2016........................................................................ 14

Figure 8. Where Is the Money, and Is It in the IT Budget?......................................................................15

Page 2 of 29 Gartner, Inc. | G00297526

Figure 9. The Threat Matrix Is Evolving, Commercial Pressures and Execution Capability Outweigh

Security Risks.......................................................................................................................................17

Figure 10. Bimodal Is Becoming Increasingly Real, at Least From an IT Perspective............................. 18

Figure 11. The Most Impactful Bimodal Tactics Are Not the Most Used................................................ 20

Figure 12. Talent Issues Are the Biggest Barrier to CIO Success...........................................................21

Figure 13. Biggest Talent Gaps.............................................................................................................22

Figure 14. Some FS CIOs Are Leading Digital Transformation and Innovation....................................... 24

Figure 15. CIOs Are Enjoying Opportunities to Lead Change................................................................ 25

Figure 16. What CIOs Hate About Their Jobs....................................................................................... 26

Figure 17. Time Invested by CIOs in Their Personal Development.........................................................27

Survey ObjectiveThis document was revised on 29 February 2016. The document you are viewing is the correctedversion. For more information, see the Corrections page on gartner.com.

Gartner's annual CIO Survey is the largest annual survey of its kind, collecting data from 2,944 CIOsfrom 84 different countries, representing approximately $11 trillion in revenue, and $250 billion in ITspending. This report focuses on the major priorities and business/technology trends impactingfinancial services (FS) CIOs, as revealed by the 290 FS participants in the survey. The analysisuncovers core focus areas in the industry as CIOs set their agendas for the coming year, and offersa comparison picture of how the industry is shaping up — regionally, by financial institution (FI) size,and (where appropriate) by industry segment. The report uncovers the maturity of digital business,technology goals, challenges, and organizational and leadership trends in the FS industry. The goalsof the report are to:

■ Understand the maturity and evolution of digital business in Gartner's FS CIO client base.

■ Discern how FI CIOs are planning for the future.

■ Explore some of the business and technical drivers and inhibitors FI CIOs are experiencing.

Data InsightsWhen considering these survey results, it's important to remember three things:

■ We are now knee-deep in the era of digital business, but most FIs are struggling to reimagineindustry business and operating models based on digital capabilities that improve futureperformance.

Gartner, Inc. | G00297526 Page 3 of 29

■ The 2016 Gartner CIO Survey reveals that leading FIs must shift to an ecosystem approach interms of their business models, delivery mechanisms, talent, and leadership to survive andthrive.

■ Ecosystem strategies provide a solid foundation for transitioning the business away from alinear value chain into a broad-based network of physically and digitally connected entities.

As the implications of digitalization play out in an industry challenged with performance andregulatory issues, it is becoming clearer that 20th century business and operating models areinadequate. An added challenge is that regulators (for the most part) are a few years behind the newcapabilities enabled by technology. This leaves FIs with an unclear and risky option of investing inareas where regulators do not yet have a stated, consensus position.

Increasingly the FS industry is evolving into a broad ecosystem, where multiple networks ofstakeholders bring value to each other by exploiting network effects (positive feedback and numberof connections that increase value through more customers having and using a product or service).As digital business matures, the unbundling of the financial services industry value chains is set tocontinue. In many cases financial technology (fintech) startups (such as Nutmeg, OnDeck, Estimize,ZestFinance) are showing the way for traditional incumbents to follow as they "cherry pick"customer segments and attack pieces of the more-"vanilla" end of the FI franchise, deliberatelybreaking apart previously locked-in value chain components. FIs will need a strategy to compete,partner (that is, be coopetitive with — both competing and cooperating) or even acquire thesestartups.

Leading FI CIOs are already reconsidering their roles and responsibilities as mainstream/traditionalfirms go through a digital transformation. They are asking some critical questions of their leadershippeers:

■ How do we create value through connections and interactions rather than ownership ofindividual resources, products, services and delivery mechanisms?

■ How do we manage and grow flexible, dynamic connections, rather than fixed hierarchies?

■ How do we manage semiporous and fluid operational boundaries (such as, technology, humanresources, intellectual property, information, and so on) rather than enforce hard delineation ofinternal and external value? For example, how do we expose components (e.g., trading models)that are not yet products to the outside, or allow apps to be accessed from the outside, andeven permitting external entities access to the institution's core to co-create products andservices, perform data analysis, etc.?

■ How do we support continuous learning and change, rather than focusing on "running thefinancial institution" with expensive and risky big-bang approaches?

■ How do we enhance business agility to leverage unanticipated opportunities or defend againstunanticipated threats?

CIOs have long understood the notion of platforms in terms of internal architectures (buses, APIs,object orientation, modularity, reusability, etc.), and technology products and services. Thechallenge is that sometimes these platforms have been designed from the FI's own perspective,

Page 4 of 29 Gartner, Inc. | G00297526

with limited focus on customer needs and wants (in their context). The designs have concentratedon how to individually compete against known actors, protecting the entire franchise.

More often than not, technical platforms that support FS activity are a view from the (internal)bottom of the institution. Economic (and digital) ecosystems are a view from the (external) top of themarket — a contrast between "inside-out" versus "outside-in"(starting with the end customer)business and technology strategies. One way of ensuring that the enterprise is structured aroundand focused on the outside-in" approach is to migrate from a "product value chain" strategy to a"customer value chain" strategy (see "Leverage a Customer Value Chain for Better CustomerExperience").

The change happening now, propelled by digital business and the insight gained from this year'sCIO survey, is that ecosystems are coming to dominate the future of the FS industry. Fintech ismerely a precursor to a more radical shift in how FS are sourced, managed and used — regardlessof historic standard industry classification codes.

The State of Industry Digitalization

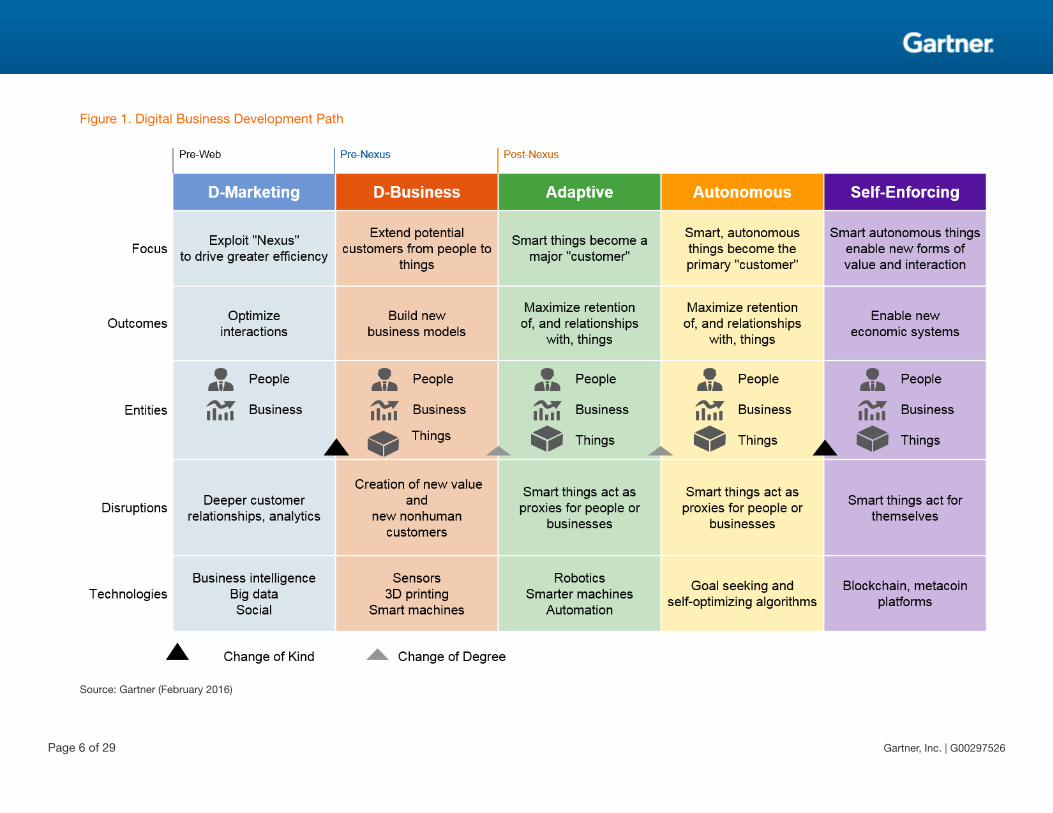

While the meaning of digital revenue and processes is open to interpretation, digital business is areality now, and it is expected to be a very significant aspect of achieving competitive advantageand differentiation using information and technology. Gartner has described this journey as the"digital business development path" (see Figure 1).

Gartner, Inc. | G00297526 Page 5 of 29

Figure 1. Digital Business Development Path

Source: Gartner (February 2016)

Page 6 of 29 Gartner, Inc. | G00297526

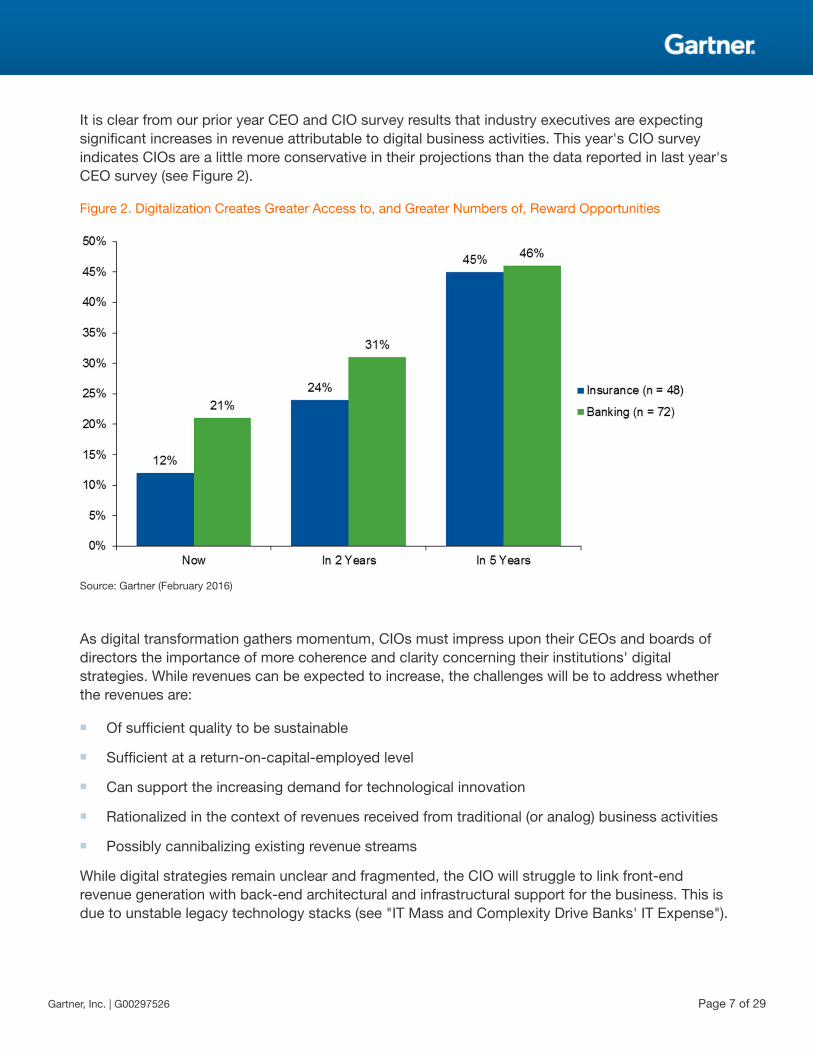

It is clear from our prior year CEO and CIO survey results that industry executives are expectingsignificant increases in revenue attributable to digital business activities. This year's CIO surveyindicates CIOs are a little more conservative in their projections than the data reported in last year'sCEO survey (see Figure 2).

Figure 2. Digitalization Creates Greater Access to, and Greater Numbers of, Reward Opportunities

Source: Gartner (February 2016)

As digital transformation gathers momentum, CIOs must impress upon their CEOs and boards ofdirectors the importance of more coherence and clarity concerning their institutions' digitalstrategies. While revenues can be expected to increase, the challenges will be to address whetherthe revenues are:

■ Of sufficient quality to be sustainable

■ Sufficient at a return-on-capital-employed level

■ Can support the increasing demand for technological innovation

■ Rationalized in the context of revenues received from traditional (or analog) business activities

■ Possibly cannibalizing existing revenue streams

While digital strategies remain unclear and fragmented, the CIO will struggle to link front-endrevenue generation with back-end architectural and infrastructural support for the business. This isdue to unstable legacy technology stacks (see "IT Mass and Complexity Drive Banks' IT Expense").

Gartner, Inc. | G00297526 Page 7 of 29

Eventually, digital revenue otherwise accruing from those strategies will not turn into sustainableprofits as customers go over to fintechs and startup FS competitors.

Globally, the picture is similar in terms of revenue growth projections (see Figure 3). Although, it isinteresting to note how limited the opportunity appears to be from the perspective of NorthAmerican CIOs.

Figure 3. Across the World, the Picture Is the Same — an Expectation of Significant Digital Revenue Growth

North America (n = 22), Latin America (n = 14), EMEA (n = 50), APAC (n = 34).Where sample size less than 30, results are directional.

Source: Gartner (February 2016)

A number of reasons could influence this view:

■ Existing perceptions of high levels of digital capabilities/maturity — client inquiries indicate thisperception is not borne out in terms of reality

■ The more-insular nature of the market

■ A more-fragmented market structure

The impact of these results will be felt in added pressure, especially on noninsurance line-of-business CIOs, to convert their enabling processes and technology environments to moreadequately support a fast-moving business landscape (see "Make Business Operations More AgileWith Intelligent Business Processes That Reshape Themselves as They Run"). Interacting withcustomers digitally is important, but not necessarily supported by internal process capabilities, nornecessarily aligned with nondigital interactions.

Page 8 of 29 Gartner, Inc. | G00297526

The challenge here is that while FI CIOs are responding to business pressure to provide economiesof access via digital capabilities, those digital interactions still require significant work-arounds interms of manual intervention and/or integration initiatives involving risk management, informationmanagement and analysis, pricing, delivery and ongoing customer support. Supporting real-timetransaction execution is comparatively easy, but real-time customer identification/authentication,credit analysis, collateral management, risk assessments, etc. are not as seamless and morechallenging.

Silos persist throughout institutions (due to compensation, product and organizational legacy).These silos, in turn, are hard-wired in terms of their application and data architecture. Asinstitutional boundaries become more porous, and the ecosystem of economic opportunitydevelops, it becomes more important for CIOs to identify and rationalize processes and silos thatwould otherwise create frictional barriers to the business.

CIOs continue to believe there is a limit to the business processes that digital business will touch.This may indicate that CIOs have a more realistic view of their business in terms of, for example, theongoing need for human interaction. It also may indicate the realization that some businessprocesses are unclear or too firmly entrenched to be rationalized in a digital context. This alsoimplies there may be a floor at which efficiency ratios will be reached — which, admittedly, are along way from the persistent industry average of more than 60% (see "The Financial ServicesRevolution Is Postponed").This should be of concern to business executives looking to compete inan economic ecosystem replete with fintechs (and the likes of Google, Alibaba et al) who lack suchlegacy environments. In fact, client inquiry has revealed that fintechs and challenger banks oftenhave an IT cost per user of less than $15 (similar to large digital firms), far less than the $150 peruser of traditional banks.

Execution speed, as well as effectiveness of product and service delivery and support, will becritical. Any delays or missteps will have an amplified effect on an FI's ability to maintaincompetitive footing. CIOs must ensure they have a clear line of sight to business returns, directlyconnected to the overall institutional digital strategy, to adequately prioritize initiatives and maintainIT department organizational relevance.

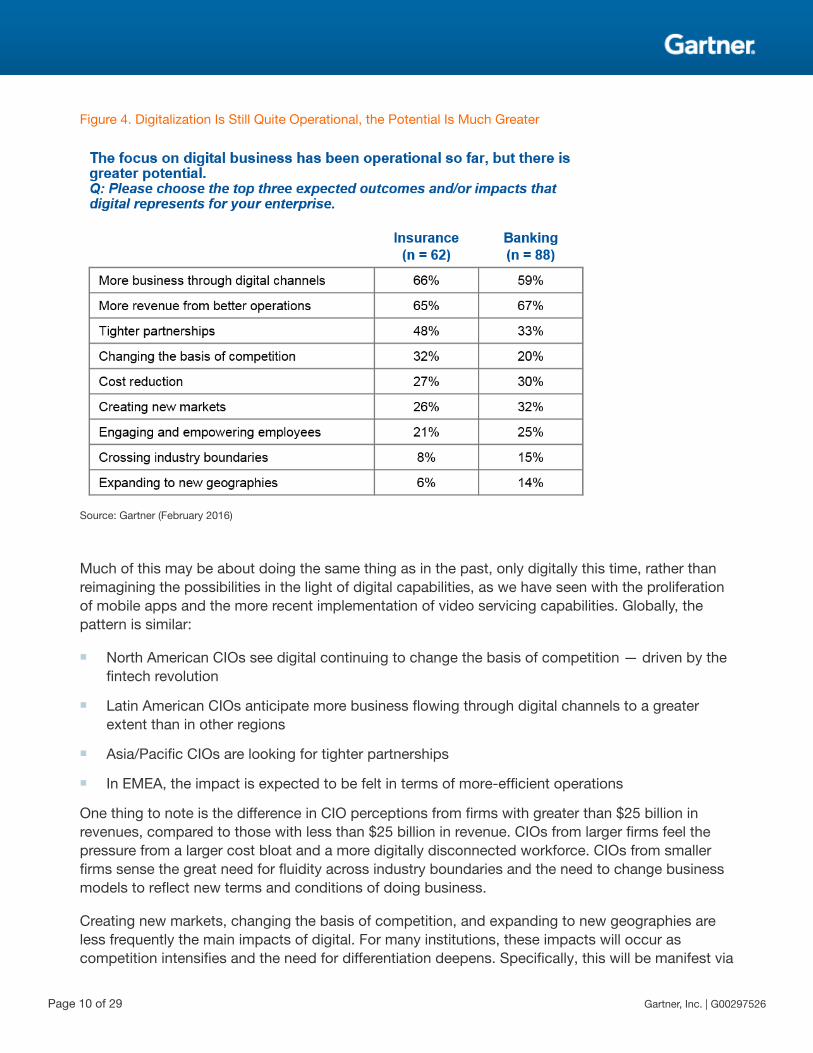

Figure 4 reveals that the top impacts of digital are still relatively operational for most institutions:

■ Driving revenue through better operations

■ Using digital channels more

Gartner, Inc. | G00297526 Page 9 of 29

Figure 4. Digitalization Is Still Quite Operational, the Potential Is Much Greater

Source: Gartner (February 2016)

Much of this may be about doing the same thing as in the past, only digitally this time, rather thanreimagining the possibilities in the light of digital capabilities, as we have seen with the proliferationof mobile apps and the more recent implementation of video servicing capabilities. Globally, thepattern is similar:

■ North American CIOs see digital continuing to change the basis of competition — driven by thefintech revolution

■ Latin American CIOs anticipate more business flowing through digital channels to a greaterextent than in other regions

■ Asia/Pacific CIOs are looking for tighter partnerships

■ In EMEA, the impact is expected to be felt in terms of more-efficient operations

One thing to note is the difference in CIO perceptions from firms with greater than $25 billion inrevenues, compared to those with less than $25 billion in revenue. CIOs from larger firms feel thepressure from a larger cost bloat and a more digitally disconnected workforce. CIOs from smallerfirms sense the great need for fluidity across industry boundaries and the need to change businessmodels to reflect new terms and conditions of doing business.

Creating new markets, changing the basis of competition, and expanding to new geographies areless frequently the main impacts of digital. For many institutions, these impacts will occur ascompetition intensifies and the need for differentiation deepens. Specifically, this will be manifest via

Page 10 of 29 Gartner, Inc. | G00297526

the adoption of new business models (see "Maverick* Research: Multiply Value Creation WithProgrammable Business Models").

One area of concern is the lack of digital impact CIOs perceive in terms of engaging andempowering employees. Gartner consumer research continues to indicate that FI customers,regardless of demographic, do not see digital capabilities as a total replacement for humaninteraction. For institutions to successfully integrate digital business into the customer journey,employees must gain a firm grasp of the technological and process changes that digital affords.Responding to a customer via a video interaction changes the nature of the relationship — whetherit was one just over the phone, or originally in-person. CIOs increasingly must be aware of theimpact of digital reach, and the effect it has on a globalized and mobile customer base andworkforce. This includes cultural, compliance, social and other considerations. While enterprisescan't (and shouldn't try to) do everything digital all at once, they should consider 360 degrees ofdigital possibilities and operational risks before choosing their focus areas, (see "Digital WorkplaceKey Initiative Overview").

The Technology Opportunity: Capitalize on the Customer Context via Big Data andDigital Business

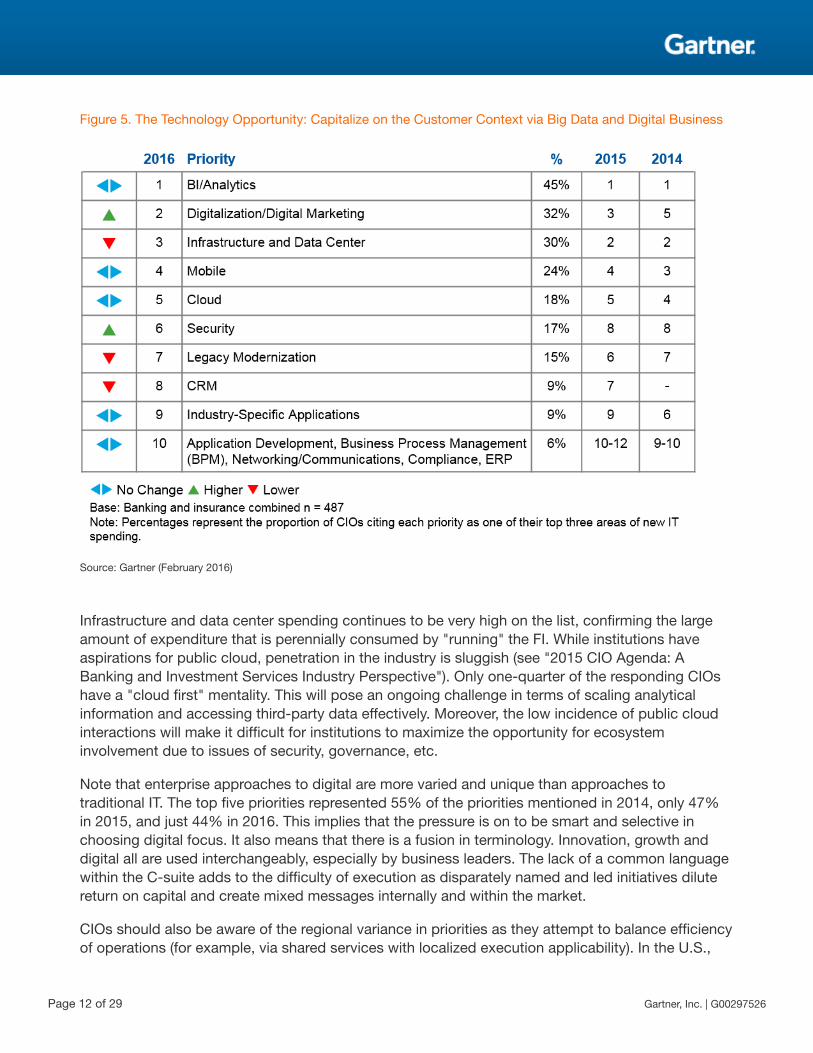

CIOs continue to believe there is a significant opportunity to maximize the value from big data andanalytics. The opportunity is to monetize big data, amplifying marketing initiatives (for example, bylinking lending rates to retail purchases, underpinned by customer mobility and the cloud via theuse of location-based services linked to broad risk assessment algorithms that enable instantlending offers). The top areas of new technology spending (see Figure 5) make it clear thatsignificant spending and opportunity continue in various aspects of big data and analytics, and thatmobile continues to have significant momentum. As has always been the case with businessintelligence (BI), the key to big data is to point it at opportunities to harvest real business value fromilluminating the customer context, hence the re-emergence of CRM as an administrative priority. It isalso to allow customers an opportunity to have access to some of the tools and the data to do theirown research.

Gartner, Inc. | G00297526 Page 11 of 29

Figure 5. The Technology Opportunity: Capitalize on the Customer Context via Big Data and Digital Business

Source: Gartner (February 2016)

Infrastructure and data center spending continues to be very high on the list, confirming the largeamount of expenditure that is perennially consumed by "running" the FI. While institutions haveaspirations for public cloud, penetration in the industry is sluggish (see "2015 CIO Agenda: ABanking and Investment Services Industry Perspective"). Only one-quarter of the responding CIOshave a "cloud first" mentality. This will pose an ongoing challenge in terms of scaling analyticalinformation and accessing third-party data effectively. Moreover, the low incidence of public cloudinteractions will make it difficult for institutions to maximize the opportunity for ecosysteminvolvement due to issues of security, governance, etc.

Note that enterprise approaches to digital are more varied and unique than approaches totraditional IT. The top five priorities represented 55% of the priorities mentioned in 2014, only 47%in 2015, and just 44% in 2016. This implies that the pressure is on to be smart and selective inchoosing digital focus. It also means that there is a fusion in terminology. Innovation, growth anddigital all are used interchangeably, especially by business leaders. The lack of a common languagewithin the C-suite adds to the difficulty of execution as disparately named and led initiatives dilutereturn on capital and create mixed messages internally and within the market.

CIOs should also be aware of the regional variance in priorities as they attempt to balance efficiencyof operations (for example, via shared services with localized execution applicability). In the U.S.,

Page 12 of 29 Gartner, Inc. | G00297526

the current security focus due to high visibility of fraud occurrences, may mean a shift to EMVimplementation in 2016 (see Figure 6).

Figure 6. The Technology Opportunity: There Is Global Variance: Balance Shared Services With LocalizedExecution

Same number of "votes" denoted by =

Source: Gartner (February 2016)

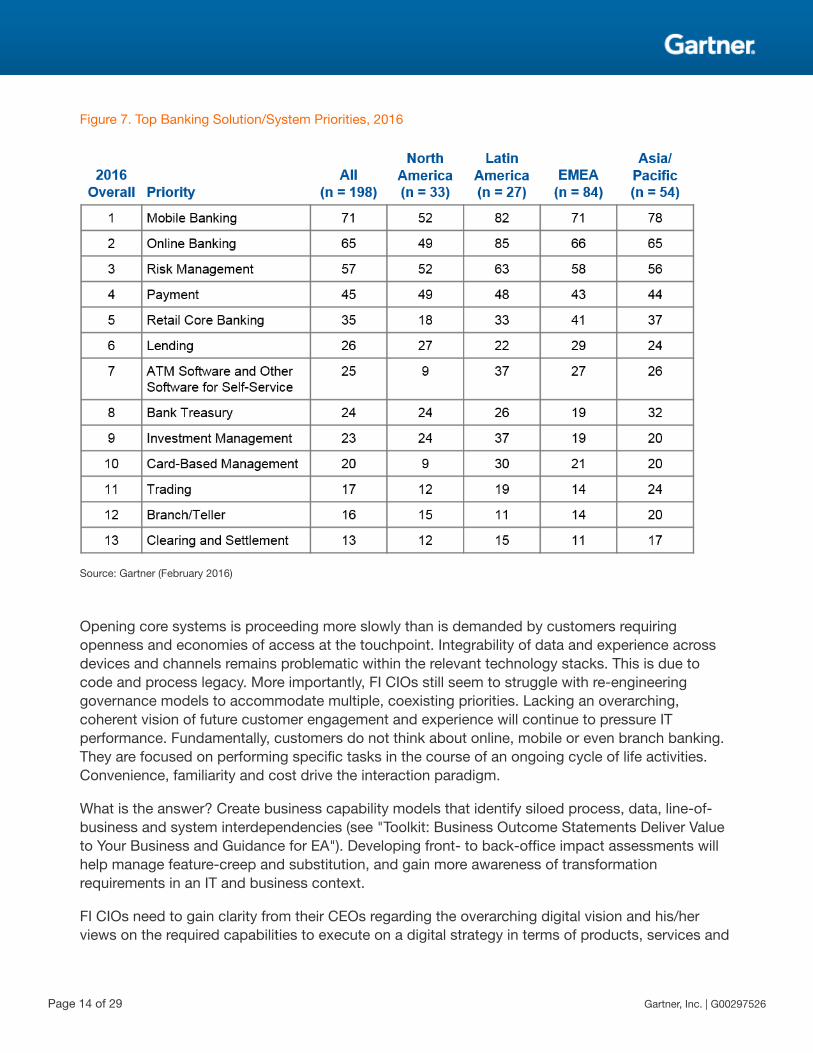

At a more specific level, we asked CIOs to share their top banking solution/system priorities for2016 (see Figure 7). As we saw in earlier research (see "Top Global Banks' IT Investments, 2014"),mobile continues to dominate the FI CIO technology solutions agenda. For all the hype about digitalbusiness, a significant minority of CIOs are still focusing on branch and teller systems. Whilephysical presence will remain a critical component of delivery strategy, the branch transformationswe have seen with "concepts" kiosks, ATMs, etc., continue to reinforce an older, cost-orienteddelivery model. Branches need to be more digitally capable; however, this capability needs to beunderstood from a client servicing/satisfaction/adoption perspective — not merely as a cost-savingploy by institutions. This raises an important consideration that continues to infuse Gartner'scustomer inquiries. Namely, the relationship between different customer engagement initiatives andhow they are integrated from an institutional and customer standpoint.

Gartner, Inc. | G00297526 Page 13 of 29

Figure 7. Top Banking Solution/System Priorities, 2016

Source: Gartner (February 2016)

Opening core systems is proceeding more slowly than is demanded by customers requiringopenness and economies of access at the touchpoint. Integrability of data and experience acrossdevices and channels remains problematic within the relevant technology stacks. This is due tocode and process legacy. More importantly, FI CIOs still seem to struggle with re-engineeringgovernance models to accommodate multiple, coexisting priorities. Lacking an overarching,coherent vision of future customer engagement and experience will continue to pressure ITperformance. Fundamentally, customers do not think about online, mobile or even branch banking.They are focused on performing specific tasks in the course of an ongoing cycle of life activities.Convenience, familiarity and cost drive the interaction paradigm.

What is the answer? Create business capability models that identify siloed process, data, line-of-business and system interdependencies (see "Toolkit: Business Outcome Statements Deliver Valueto Your Business and Guidance for EA"). Developing front- to back-office impact assessments willhelp manage feature-creep and substitution, and gain more awareness of transformationrequirements in an IT and business context.

FI CIOs need to gain clarity from their CEOs regarding the overarching digital vision and his/herviews on the required capabilities to execute on a digital strategy in terms of products, services and

Page 14 of 29 Gartner, Inc. | G00297526

resources. Press the CEO on the impact digital transformation will have on legacy infrastructure andarchitecture — from a business performance standpoint.

Business Threats Are Substantial: Resources, Security, Fintech Disruption, CulturalBehavior

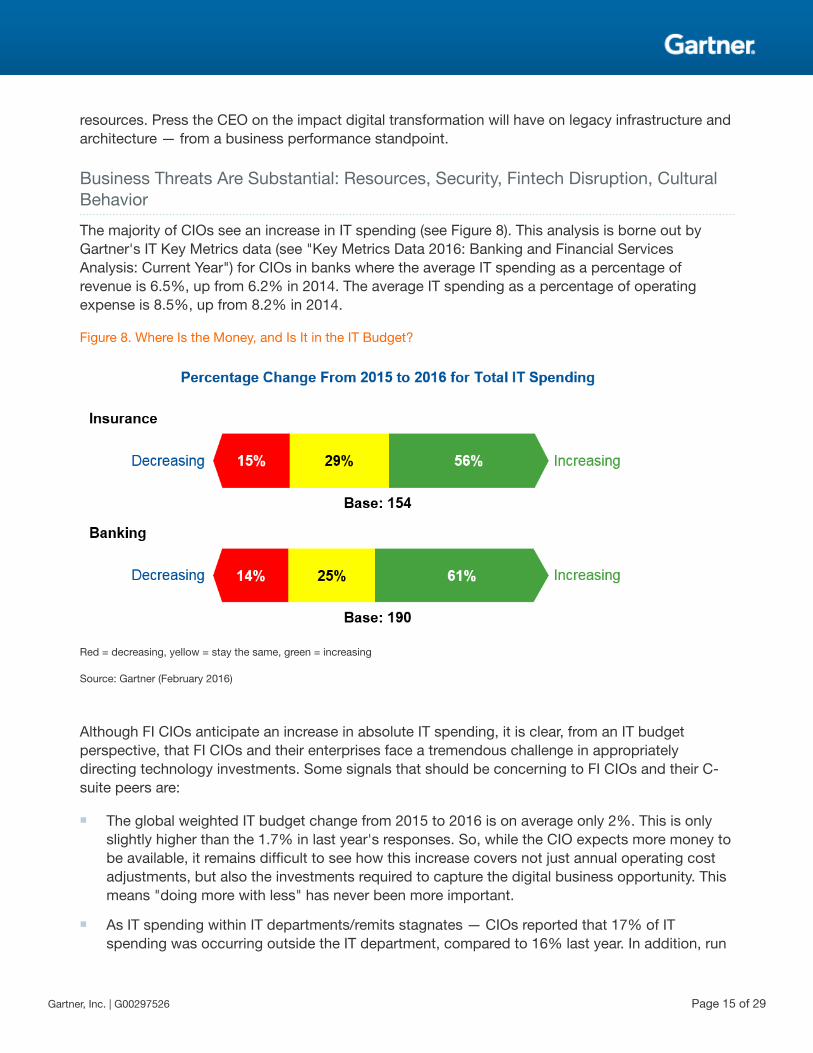

The majority of CIOs see an increase in IT spending (see Figure 8). This analysis is borne out byGartner's IT Key Metrics data (see "Key Metrics Data 2016: Banking and Financial ServicesAnalysis: Current Year") for CIOs in banks where the average IT spending as a percentage ofrevenue is 6.5%, up from 6.2% in 2014. The average IT spending as a percentage of operatingexpense is 8.5%, up from 8.2% in 2014.

Figure 8. Where Is the Money, and Is It in the IT Budget?

Red = decreasing, yellow = stay the same, green = increasing

Source: Gartner (February 2016)

Although FI CIOs anticipate an increase in absolute IT spending, it is clear, from an IT budgetperspective, that FI CIOs and their enterprises face a tremendous challenge in appropriatelydirecting technology investments. Some signals that should be concerning to FI CIOs and their C-suite peers are:

■ The global weighted IT budget change from 2015 to 2016 is on average only 2%. This is onlyslightly higher than the 1.7% in last year's responses. So, while the CIO expects more money tobe available, it remains difficult to see how this increase covers not just annual operating costadjustments, but also the investments required to capture the digital business opportunity. Thismeans "doing more with less" has never been more important.

■ As IT spending within IT departments/remits stagnates — CIOs reported that 17% of ITspending was occurring outside the IT department, compared to 16% last year. In addition, run

Gartner, Inc. | G00297526 Page 15 of 29

the business spending has increased to 64% from 61% (see "Key Metrics Data 2016: Bankingand Financial Services Analysis: Current Year"). This should generate C-suite conversationsabout funding allocations and IT spending quality.

■ Revenue per employee (productivity) ratios can help determine employee productivity in termsof revenue-generation intensity. This measure is typically influenced by company businessmodel and staffing strategy. However, these ratios for banking show a declining revenue pictureconsistently for the past five years, from $486,000 per employee to $460,000. Full-timeequivalent (FTE) reductions, and all the focus on digital business, does not seem to be positivelyimpacting institutional performance. This is also a function of how effectively digitaltechnologies drive operational efficiencies, and hence supplant pure people costs. Similarly ITspending per employee helps to highlight the link between IT investment and automation (andhence digitalization) levels within the context of the workforce that supports revenue. ITspending per employee is rising — since 2011, as much as 10% in banking (5% in insurance),suggesting productivity improvements. However, this is somewhat less than in the media (13%),retailing (22%) and telecommunications industries (12%). This implies near-competitors (at leastto the retail financial services segment of the industry), are potentially extracting greaterproductivity improvements from their digital investments (see "Key Metrics Data 2016: Bankingand Financial Services Analysis: Current Year," "IT Key Metrics Data 2016: Key IndustryMeasures: Banking and Financial Services Analysis: Multiyear," "IT Key Metrics Data 2016: KeyIndustry Measures: Insurance Analysis: Current Year" and "IT Key Metrics Data 2016: KeyIndustry Measures: Insurance Analysis: Multiyear"). For example, CIOs and business leadersshould investigate whether digital technologies deployed in a branch equate to a correspondingdecrease in the people needed to man that branch — all other criteria being equal. Many FIsstruggle with the absence of that correlation (often reinforced by arcane labor laws, notably inGermany and France).

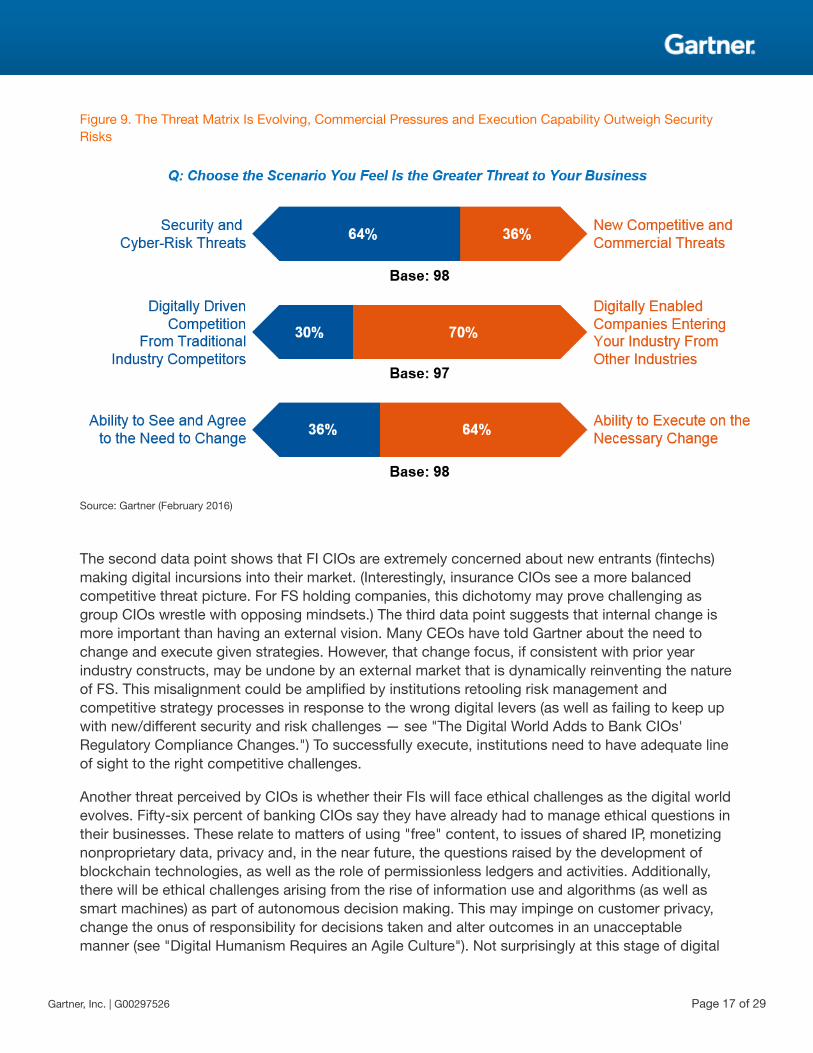

Along with the imperatives around capturing innovation opportunities, digital business also has adark side — the need to adapt threat perception, including the balance of threats and how tomitigate them. Figure 9 highlights that the balance is shifting significantly. The first data point showsthat a very significant majority of CIOs (64%) see cyber-risk and security threats as greater than newcommercial and competitive threats. While CIOs need to exhibit diligence with respect to risk andcompliance requirements, they should ensure they have an adequate risk framework in place thatmeets the need for openness and access to the digital ecosystem. CIOs and business leaders willneed to improve their understanding of intellectual property (IP) rights, data privacy, riskinterdependency and the various risk-reward trade-offs such that the maintenance of strongfirewalls doesn't simultaneously prevent business activity in the ecosystem.

Page 16 of 29 Gartner, Inc. | G00297526

Figure 9. The Threat Matrix Is Evolving, Commercial Pressures and Execution Capability Outweigh SecurityRisks

Source: Gartner (February 2016)

The second data point shows that FI CIOs are extremely concerned about new entrants (fintechs)making digital incursions into their market. (Interestingly, insurance CIOs see a more balancedcompetitive threat picture. For FS holding companies, this dichotomy may prove challenging asgroup CIOs wrestle with opposing mindsets.) The third data point suggests that internal change ismore important than having an external vision. Many CEOs have told Gartner about the need tochange and execute given strategies. However, that change focus, if consistent with prior yearindustry constructs, may be undone by an external market that is dynamically reinventing the natureof FS. This misalignment could be amplified by institutions retooling risk management andcompetitive strategy processes in response to the wrong digital levers (as well as failing to keep upwith new/different security and risk challenges — see "The Digital World Adds to Bank CIOs'Regulatory Compliance Changes.") To successfully execute, institutions need to have adequate lineof sight to the right competitive challenges.

Another threat perceived by CIOs is whether their FIs will face ethical challenges as the digital worldevolves. Fifty-six percent of banking CIOs say they have already had to manage ethical questions intheir businesses. These relate to matters of using "free" content, to issues of shared IP, monetizingnonproprietary data, privacy and, in the near future, the questions raised by the development ofblockchain technologies, as well as the role of permissionless ledgers and activities. Additionally,there will be ethical challenges arising from the rise of information use and algorithms (as well assmart machines) as part of autonomous decision making. This may impinge on customer privacy,change the onus of responsibility for decisions taken and alter outcomes in an unacceptablemanner (see "Digital Humanism Requires an Agile Culture"). Not surprisingly at this stage of digital

Gartner, Inc. | G00297526 Page 17 of 29

business evolution, CIOs from large global institutions say ethical questions come up four timesmore often than those from small, national institutions. They are also twice as prevalent in EMEAand Asia/Pacific as in North America and Latin America.

The challenge for CIOs will be in preparing to handle ethical concerns. Interestingly, surveyresponses indicate that the CIOs who have already experienced an issue are only a little moreprepared. In other words, they have not yet institutionalized the capability to respond to ethicalissues. Gartner clients are advised to review "Kick-Start the Conversation on Digital Ethics" toprepare the C-suite for this new operational risk paradigm.

Digital Execution and Performance Relies on Organizational Change

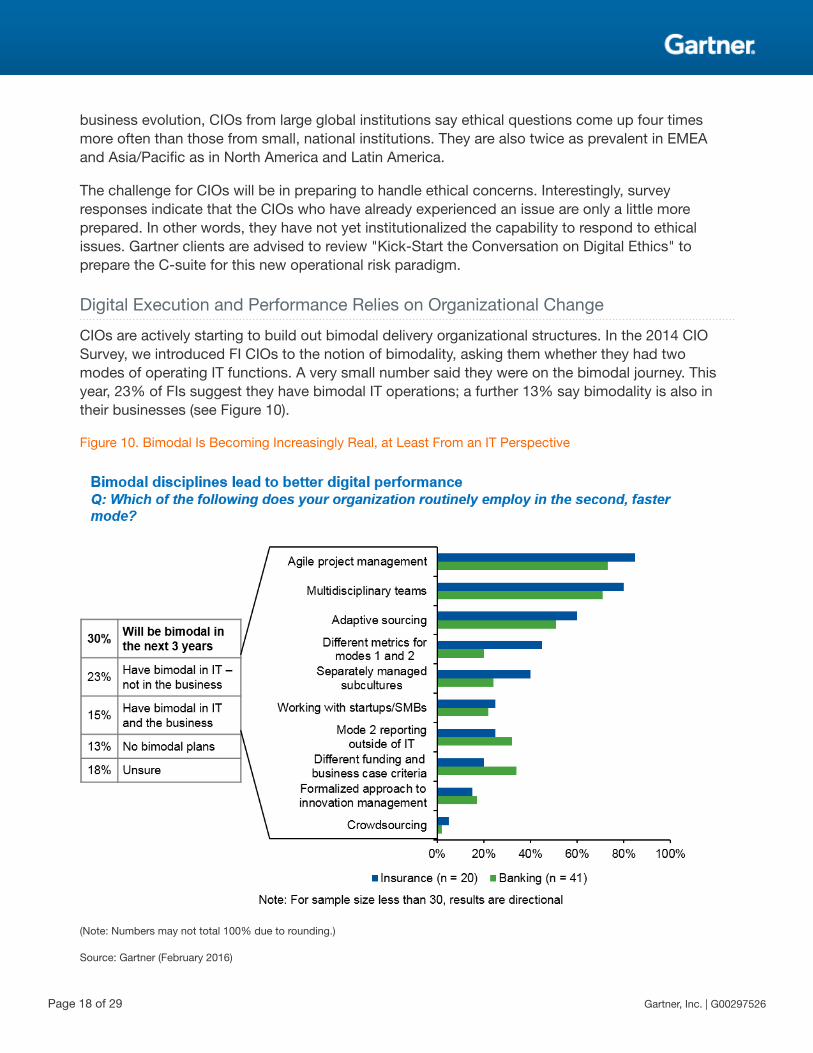

CIOs are actively starting to build out bimodal delivery organizational structures. In the 2014 CIOSurvey, we introduced FI CIOs to the notion of bimodality, asking them whether they had twomodes of operating IT functions. A very small number said they were on the bimodal journey. Thisyear, 23% of FIs suggest they have bimodal IT operations; a further 13% say bimodality is also intheir businesses (see Figure 10).

Figure 10. Bimodal Is Becoming Increasingly Real, at Least From an IT Perspective

(Note: Numbers may not total 100% due to rounding.)

Source: Gartner (February 2016)

Page 18 of 29 Gartner, Inc. | G00297526

It seems that CIOs are slowly gaining a deeper understanding of what it takes to be truly bimodal.However, bimodal can still be misinterpreted by many as simply the introduction of agile tools andmethodologies, like Scrum. When we map the impact of individual bimodal aspects with theiradoption, it becomes clear that many are focused on what is easy, rather than what is mosteffective. Some of the most effective techniques — crowdsourcing, using different outcome metricsand formal innovation management processes — are also some of the least adopted by CIOs. It isnot unreasonable to start with things that are easier, to gain buy-in and experience, but the keymessage is not to get stuck there. If CIOs want to get the biggest bang for the buck from bimodal,they need to take on some of these tougher changes.

Indeed, the defining characteristic of bimodal is having two differentiated approaches to operatingIT (and ultimately the business) — one suitable for more predictable, run the FI work (includingoperations and development), the other for exploratory or innovative work. Each operational moderequires different subcultures, tools, approaches and metrics. The far end of the bimodal journey isseparation between Mode 1 IT and other business function "factories," and Mode 2 multidisciplinaryteams that target deepening the digitalization of a particular aspect of the business (customersegment, product/service line or business process). Workflows between the two modes of bimodalare based on the need to exploit versus explore, time to market versus stability and risk-rewardratios.

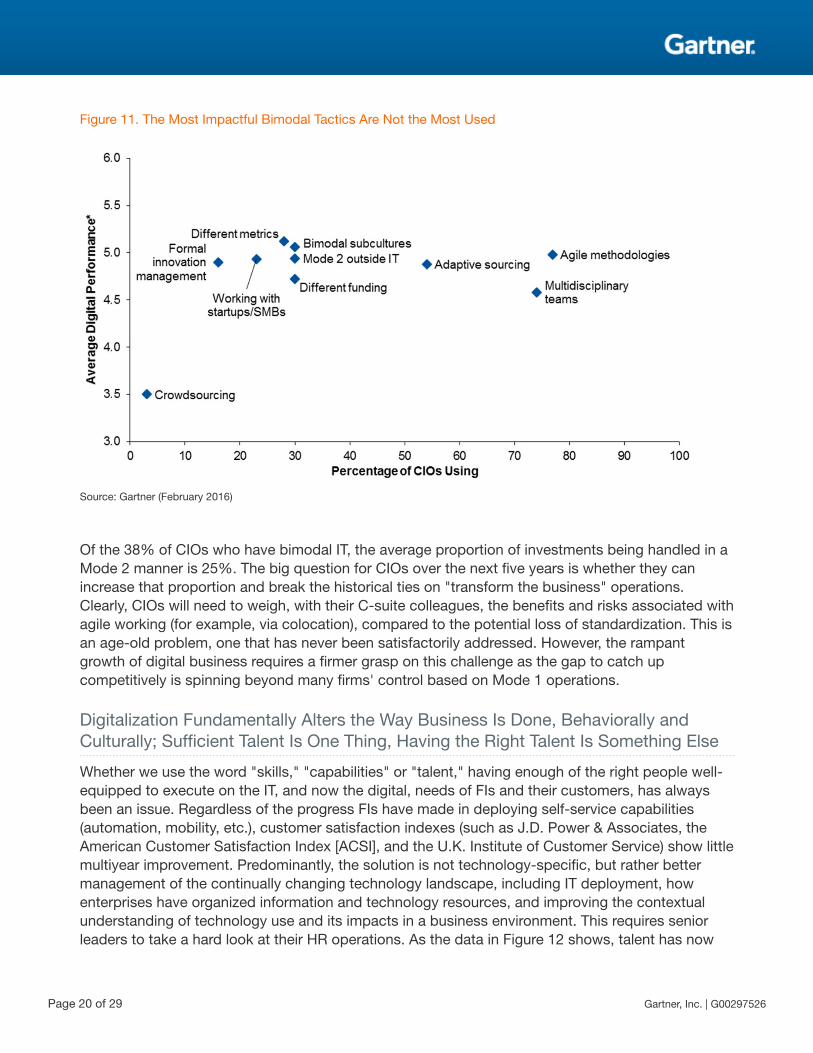

Ultimately, Gartner believes there is a correlation between bimodality and digital performance.Interestingly CIOs believe that all techniques for bimodal afford the same level of digitalperformance (see Figure 11). This implies that CIOs do not have the granularity of metrics to assessoperational performance in this context, or the extent of institutionalization of the operating modelsis very embryonic.

Note that every bimodal-related capability need not be used on every Mode 2 project. Dependingon the institution's business context, it may be appropriate to develop a "palette" of Mode 2 tools,from which the delivery team chooses for each project. The palette includes Scrum, Kanban,extreme programming and pair programming, and each project has a Sprint Zero, a Scrum phasewhere the team selects the most suitable tools.

Gartner, Inc. | G00297526 Page 19 of 29

Figure 11. The Most Impactful Bimodal Tactics Are Not the Most Used

Source: Gartner (February 2016)

Of the 38% of CIOs who have bimodal IT, the average proportion of investments being handled in aMode 2 manner is 25%. The big question for CIOs over the next five years is whether they canincrease that proportion and break the historical ties on "transform the business" operations.Clearly, CIOs will need to weigh, with their C-suite colleagues, the benefits and risks associated withagile working (for example, via colocation), compared to the potential loss of standardization. This isan age-old problem, one that has never been satisfactorily addressed. However, the rampantgrowth of digital business requires a firmer grasp on this challenge as the gap to catch upcompetitively is spinning beyond many firms' control based on Mode 1 operations.

Digitalization Fundamentally Alters the Way Business Is Done, Behaviorally andCulturally; Sufficient Talent Is One Thing, Having the Right Talent Is Something Else

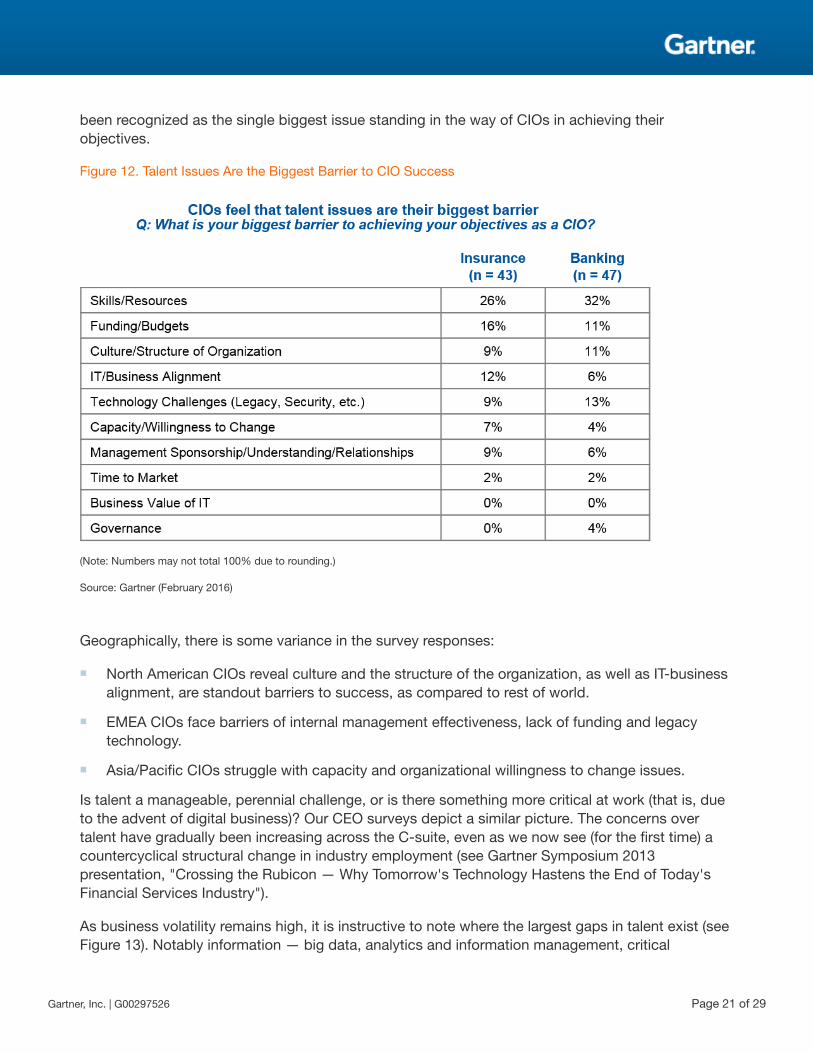

Whether we use the word "skills," "capabilities" or "talent," having enough of the right people well-equipped to execute on the IT, and now the digital, needs of FIs and their customers, has alwaysbeen an issue. Regardless of the progress FIs have made in deploying self-service capabilities(automation, mobility, etc.), customer satisfaction indexes (such as J.D. Power & Associates, theAmerican Customer Satisfaction Index [ACSI], and the U.K. Institute of Customer Service) show littlemultiyear improvement. Predominantly, the solution is not technology-specific, but rather bettermanagement of the continually changing technology landscape, including IT deployment, howenterprises have organized information and technology resources, and improving the contextualunderstanding of technology use and its impacts in a business environment. This requires seniorleaders to take a hard look at their HR operations. As the data in Figure 12 shows, talent has now

Page 20 of 29 Gartner, Inc. | G00297526

been recognized as the single biggest issue standing in the way of CIOs in achieving theirobjectives.

Figure 12. Talent Issues Are the Biggest Barrier to CIO Success

(Note: Numbers may not total 100% due to rounding.)

Source: Gartner (February 2016)

Geographically, there is some variance in the survey responses:

■ North American CIOs reveal culture and the structure of the organization, as well as IT-businessalignment, are standout barriers to success, as compared to rest of world.

■ EMEA CIOs face barriers of internal management effectiveness, lack of funding and legacytechnology.

■ Asia/Pacific CIOs struggle with capacity and organizational willingness to change issues.

Is talent a manageable, perennial challenge, or is there something more critical at work (that is, dueto the advent of digital business)? Our CEO surveys depict a similar picture. The concerns overtalent have gradually been increasing across the C-suite, even as we now see (for the first time) acountercyclical structural change in industry employment (see Gartner Symposium 2013presentation, "Crossing the Rubicon — Why Tomorrow's Technology Hastens the End of Today'sFinancial Services Industry").

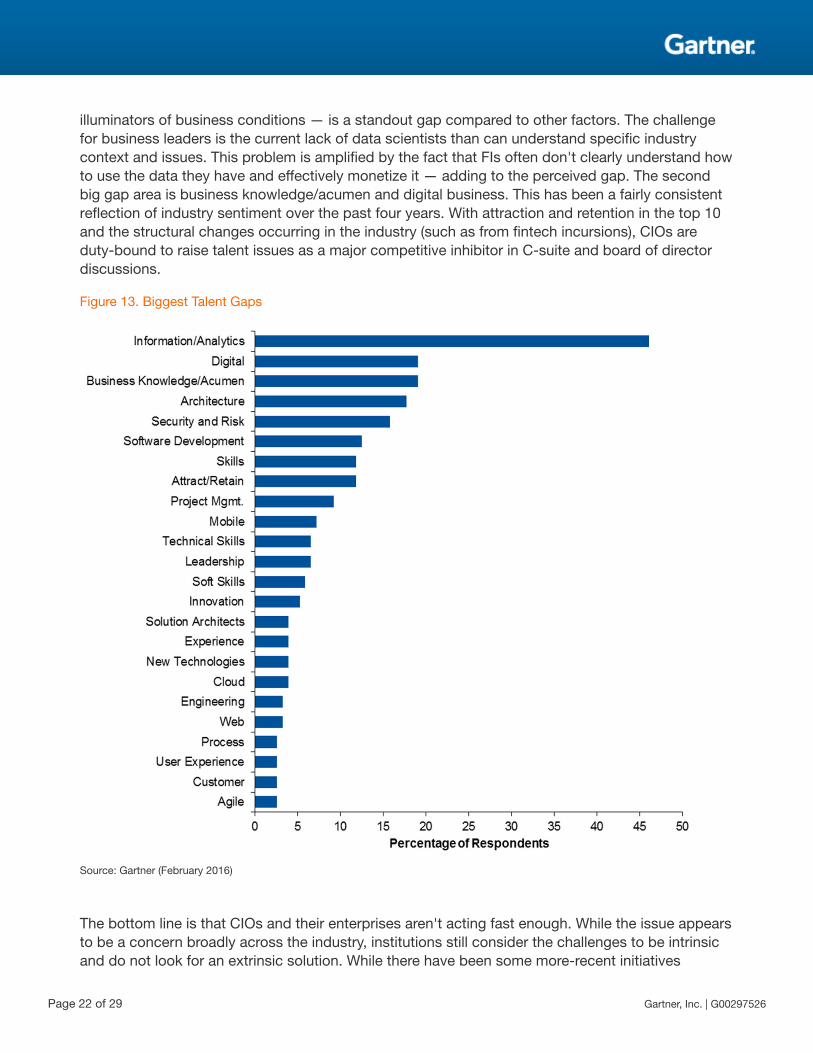

As business volatility remains high, it is instructive to note where the largest gaps in talent exist (seeFigure 13). Notably information — big data, analytics and information management, critical

Gartner, Inc. | G00297526 Page 21 of 29

illuminators of business conditions — is a standout gap compared to other factors. The challengefor business leaders is the current lack of data scientists than can understand specific industrycontext and issues. This problem is amplified by the fact that FIs often don't clearly understand howto use the data they have and effectively monetize it — adding to the perceived gap. The secondbig gap area is business knowledge/acumen and digital business. This has been a fairly consistentreflection of industry sentiment over the past four years. With attraction and retention in the top 10and the structural changes occurring in the industry (such as from fintech incursions), CIOs areduty-bound to raise talent issues as a major competitive inhibitor in C-suite and board of directordiscussions.

Figure 13. Biggest Talent Gaps

Source: Gartner (February 2016)

The bottom line is that CIOs and their enterprises aren't acting fast enough. While the issue appearsto be a concern broadly across the industry, institutions still consider the challenges to be intrinsicand do not look for an extrinsic solution. While there have been some more-recent initiatives

Page 22 of 29 Gartner, Inc. | G00297526

involving accelerator and incubator programs, the outcome is more focused on technology/productacquisition, as opposed to talent co-option. Industry leaders still view the marketplace innonecosystem terms.

Building a platform of "sustainable" internships, university partnerships, crowdsourcing,hackathons, citizen development, job rotations, etc. will be critical to overcoming these challenges.Non-FI companies sometimes allow individuals to choose their projects and managers (according toa 2014 Harvard Business Review report, "Let Employees Choose When, Where, and How to Work").This ensures that talented people work on projects they are passionate about. It also changes therole of management from "owner of talent" to "advocate of the talent's projects and work styles."Managers will need to internally advertise their work and style to attract team members. Specifically,CIOs need to think about talent as an institutional growth lever that engages institutional reachacross semiporous industry boundaries (see "Industries Will Become Fluid in the Era of DigitalBusiness").

Clearly, the talent pool and talent management practices are not keeping up with the pressingneeds of the digital world. Indeed, it would be madness to think that continuing the same old humanresources management practices will magically solve the problem.

Regardless of the Presence of a Chief Digital Officer, Advanced TechnologyLeadership Is an Essential Component of Digital Excellence

As the implications of digitalization play out across the industry, it is becoming clearer thathardcoded and one-dimensional business and operating models will not suffice (see "Maverick*Research: Multiply Value Creation With Programmable Business Models"). Leading economistshave noted the increasing prevalence of platform business models, where multiple ecosystems ofstakeholders bring value to each other by exploiting network effects (positive feedback thatincreases value through more customers having and using a product or service). Technologists havelong recognized the power of platform approaches to information and technology architecture. Whatis new is that platform dynamics are being applied to create value in all aspects of the business.

One thing that has not, and will not, change is that leadership is critical of all business success.Digital businesses are no different in that respect. Gartner has been following the rise of the chiefdigital officer (CDO) during the past few years, predicting that the CDO role will be influential for afew years to come, and then die away as digital business considerations are embedded in the DNAof an organization. However, globally, the evolution of a CDO role seems to be stalling; only 15% ofFI CIOs report the existence of that role (base = 487).

In 2014, 9% of FI CIO survey respondents said they had a CDO or someone with "digital" in theirtitle at the C-level. So, with all the hype around digital business and fintech, it remains surprisingthat leadership in this critical area seems to be a gap. Based on Gartner's conversations with CEOs,(such as in Asia/Pacific), it is likely that the absence of appropriate talent to take on this senior roleis a significant barrier. Indeed, many FS CEOs have said they looked — unsuccessfully — for asuitable candidate for many months before giving up the effort!)

Gartner, Inc. | G00297526 Page 23 of 29

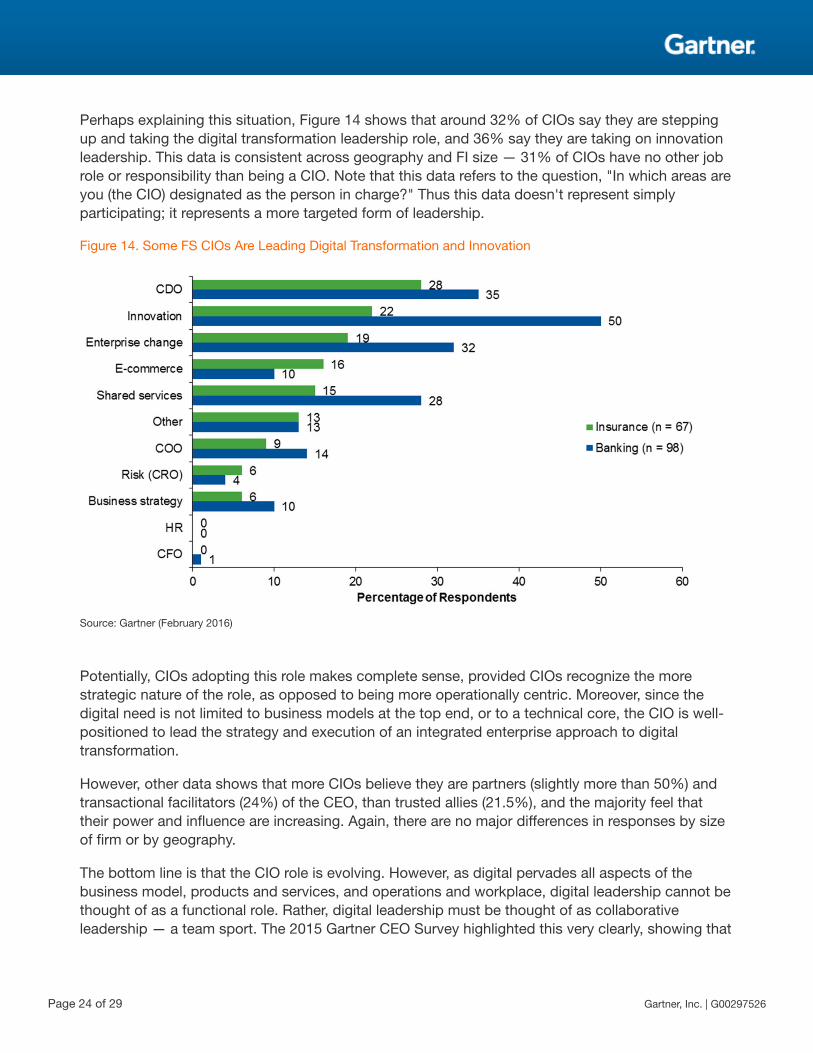

Perhaps explaining this situation, Figure 14 shows that around 32% of CIOs say they are steppingup and taking the digital transformation leadership role, and 36% say they are taking on innovationleadership. This data is consistent across geography and FI size — 31% of CIOs have no other jobrole or responsibility than being a CIO. Note that this data refers to the question, "In which areas areyou (the CIO) designated as the person in charge?" Thus this data doesn't represent simplyparticipating; it represents a more targeted form of leadership.

Figure 14. Some FS CIOs Are Leading Digital Transformation and Innovation

Source: Gartner (February 2016)

Potentially, CIOs adopting this role makes complete sense, provided CIOs recognize the morestrategic nature of the role, as opposed to being more operationally centric. Moreover, since thedigital need is not limited to business models at the top end, or to a technical core, the CIO is well-positioned to lead the strategy and execution of an integrated enterprise approach to digitaltransformation.

However, other data shows that more CIOs believe they are partners (slightly more than 50%) andtransactional facilitators (24%) of the CEO, than trusted allies (21.5%), and the majority feel thattheir power and influence are increasing. Again, there are no major differences in responses by sizeof firm or by geography.

The bottom line is that the CIO role is evolving. However, as digital pervades all aspects of thebusiness model, products and services, and operations and workplace, digital leadership cannot bethought of as a functional role. Rather, digital leadership must be thought of as collaborativeleadership — a team sport. The 2015 Gartner CEO Survey highlighted this very clearly, showing that

Page 24 of 29 Gartner, Inc. | G00297526

most CEOs see their CIOs as having the most digital leadership responsibility, but sharing thisresponsibility more broadly across the C-level.

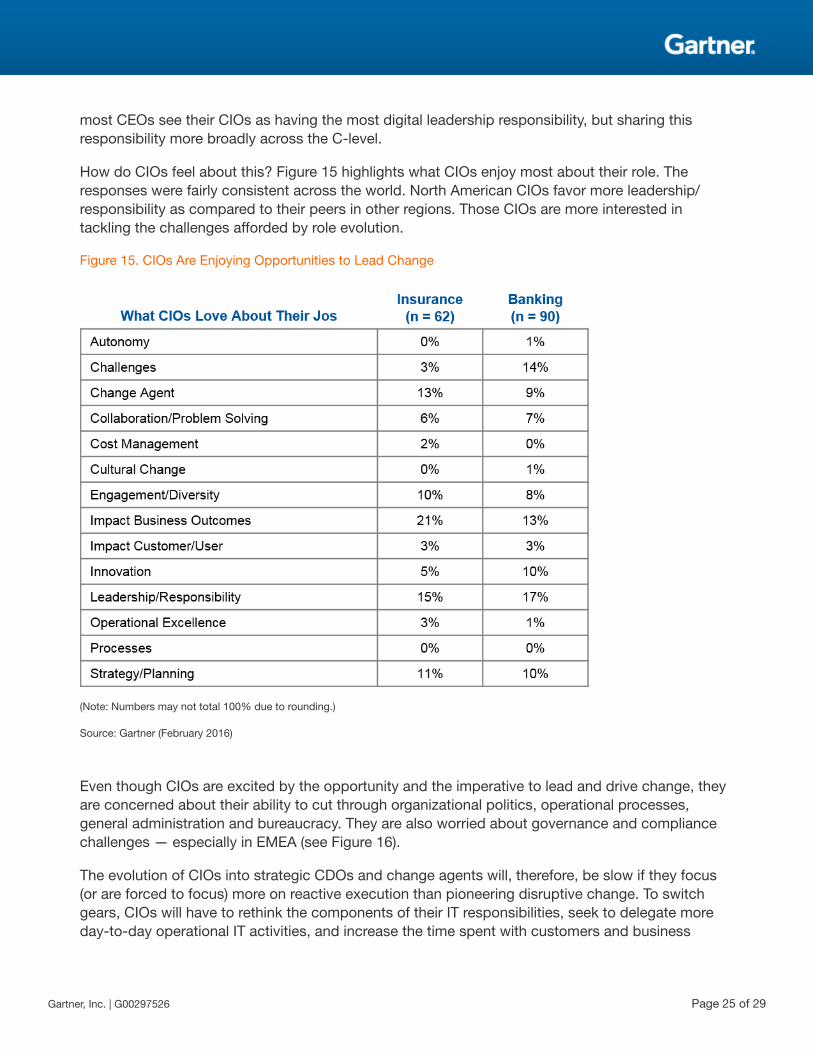

How do CIOs feel about this? Figure 15 highlights what CIOs enjoy most about their role. Theresponses were fairly consistent across the world. North American CIOs favor more leadership/responsibility as compared to their peers in other regions. Those CIOs are more interested intackling the challenges afforded by role evolution.

Figure 15. CIOs Are Enjoying Opportunities to Lead Change

(Note: Numbers may not total 100% due to rounding.)

Source: Gartner (February 2016)

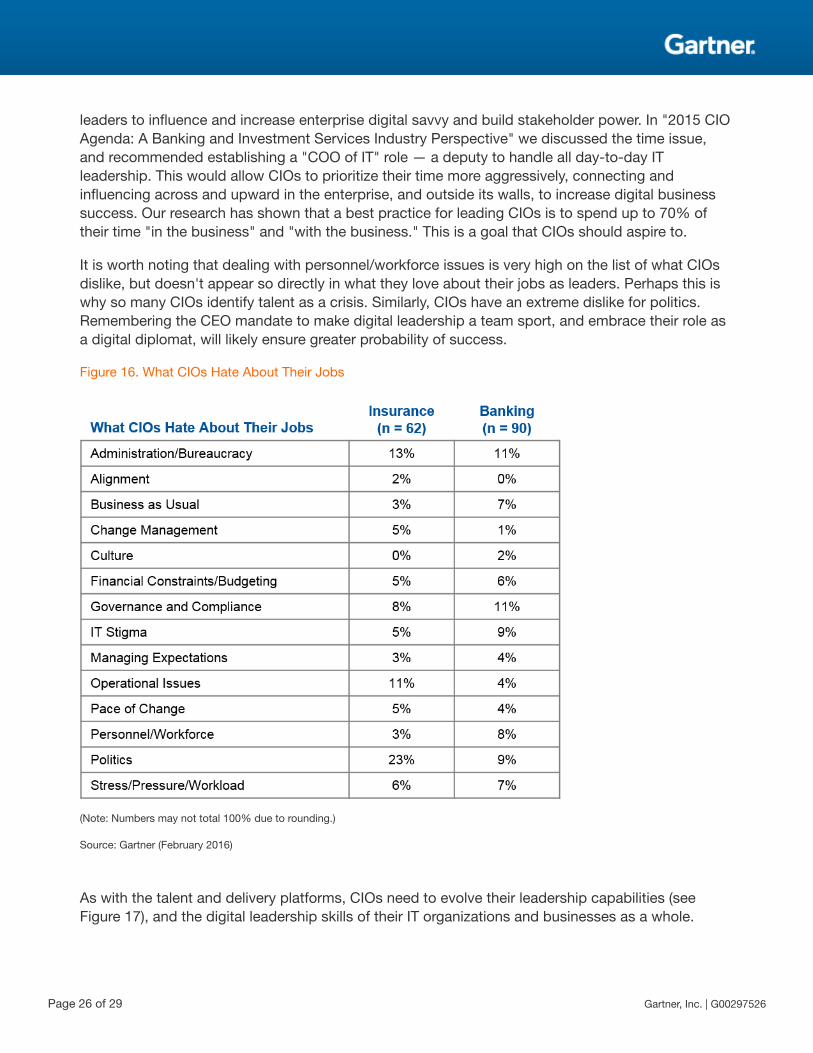

Even though CIOs are excited by the opportunity and the imperative to lead and drive change, theyare concerned about their ability to cut through organizational politics, operational processes,general administration and bureaucracy. They are also worried about governance and compliancechallenges — especially in EMEA (see Figure 16).

The evolution of CIOs into strategic CDOs and change agents will, therefore, be slow if they focus(or are forced to focus) more on reactive execution than pioneering disruptive change. To switchgears, CIOs will have to rethink the components of their IT responsibilities, seek to delegate moreday-to-day operational IT activities, and increase the time spent with customers and business

Gartner, Inc. | G00297526 Page 25 of 29

leaders to influence and increase enterprise digital savvy and build stakeholder power. In "2015 CIOAgenda: A Banking and Investment Services Industry Perspective" we discussed the time issue,and recommended establishing a "COO of IT" role — a deputy to handle all day-to-day ITleadership. This would allow CIOs to prioritize their time more aggressively, connecting andinfluencing across and upward in the enterprise, and outside its walls, to increase digital businesssuccess. Our research has shown that a best practice for leading CIOs is to spend up to 70% oftheir time "in the business" and "with the business." This is a goal that CIOs should aspire to.

It is worth noting that dealing with personnel/workforce issues is very high on the list of what CIOsdislike, but doesn't appear so directly in what they love about their jobs as leaders. Perhaps this iswhy so many CIOs identify talent as a crisis. Similarly, CIOs have an extreme dislike for politics.Remembering the CEO mandate to make digital leadership a team sport, and embrace their role asa digital diplomat, will likely ensure greater probability of success.

Figure 16. What CIOs Hate About Their Jobs

(Note: Numbers may not total 100% due to rounding.)

Source: Gartner (February 2016)

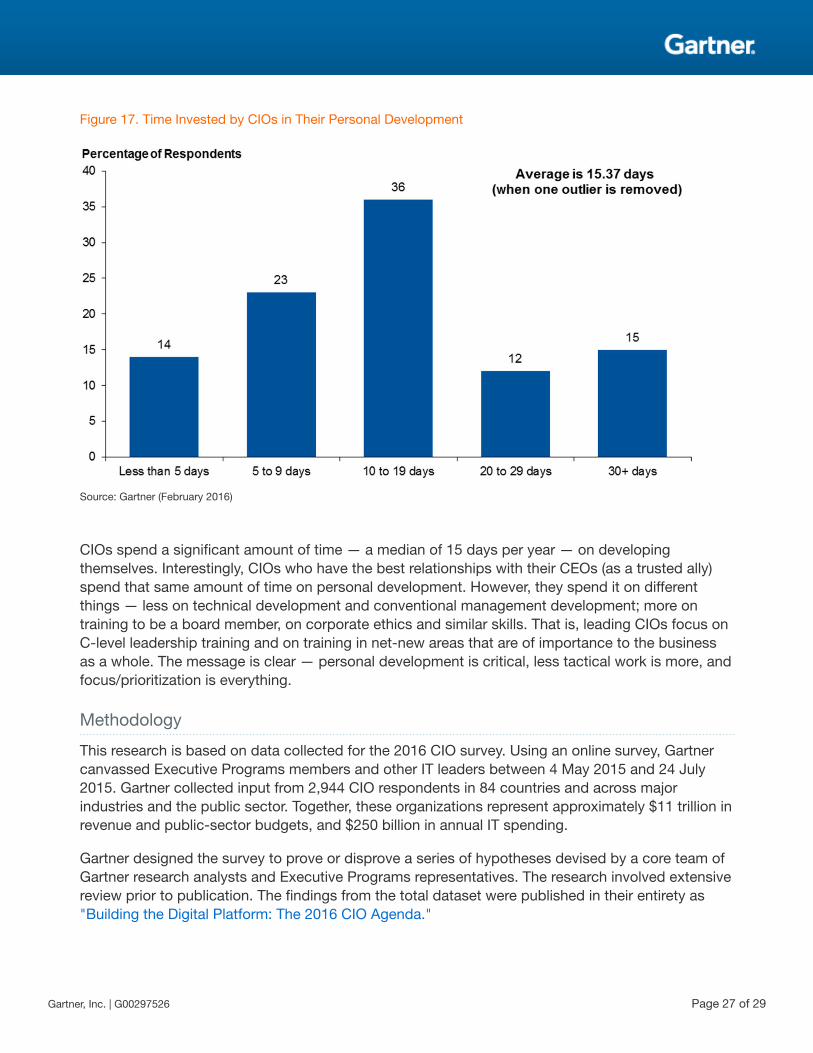

As with the talent and delivery platforms, CIOs need to evolve their leadership capabilities (seeFigure 17), and the digital leadership skills of their IT organizations and businesses as a whole.

Page 26 of 29 Gartner, Inc. | G00297526

Figure 17. Time Invested by CIOs in Their Personal Development

Source: Gartner (February 2016)

CIOs spend a significant amount of time — a median of 15 days per year — on developingthemselves. Interestingly, CIOs who have the best relationships with their CEOs (as a trusted ally)spend that same amount of time on personal development. However, they spend it on differentthings — less on technical development and conventional management development; more ontraining to be a board member, on corporate ethics and similar skills. That is, leading CIOs focus onC-level leadership training and on training in net-new areas that are of importance to the businessas a whole. The message is clear — personal development is critical, less tactical work is more, andfocus/prioritization is everything.

Methodology

This research is based on data collected for the 2016 CIO survey. Using an online survey, Gartnercanvassed Executive Programs members and other IT leaders between 4 May 2015 and 24 July2015. Gartner collected input from 2,944 CIO respondents in 84 countries and across majorindustries and the public sector. Together, these organizations represent approximately $11 trillion inrevenue and public-sector budgets, and $250 billion in annual IT spending.

Gartner designed the survey to prove or disprove a series of hypotheses devised by a core team ofGartner research analysts and Executive Programs representatives. The research involved extensivereview prior to publication. The findings from the total dataset were published in their entirety as"Building the Digital Platform: The 2016 CIO Agenda."

Gartner, Inc. | G00297526 Page 27 of 29

Gartner Recommended ReadingSome documents may not be available as part of your current Gartner subscription.

"Hints and Tips on Using Gartner Numbers When Reviewing IT Spending Plans"

"2015 CIO Agenda: A Banking and Investment Services Perspective"

"New Year's Resolutions for Financial Services CIOs in 2106"

"Predicts 2016: Digital Banking Initiatives Will Fail Without Strategic Investments in EmergingTechnologies"

Evidence

This research is based on data findings from the 2016 Gartner CIO Survey. The original survey datawas collected online from 2,944 members of Gartner Executive Programs and other IT leadersbetween 4 May 2015 and 24 July 2015.

This is part of an in-depth collection of research. See the collection:

■ 2016 CIO Agenda: Global Perspectives on Building the Digital Platform

Page 28 of 29 Gartner, Inc. | G00297526

GARTNER HEADQUARTERS

Corporate Headquarters56 Top Gallant RoadStamford, CT 06902-7700USA+1 203 964 0096

Regional HeadquartersAUSTRALIABRAZILJAPANUNITED KINGDOM

For a complete list of worldwide locations,visit http://www.gartner.com/technology/about.jsp

© 2016 Gartner, Inc. and/or its affiliates. All rights reserved. Gartner is a registered trademark of Gartner, Inc. or its affiliates. Thispublication may not be reproduced or distributed in any form without Gartner’s prior written permission. If you are authorized to accessthis publication, your use of it is subject to the Usage Guidelines for Gartner Services posted on gartner.com. The information containedin this publication has been obtained from sources believed to be reliable. Gartner disclaims all warranties as to the accuracy,completeness or adequacy of such information and shall have no liability for errors, omissions or inadequacies in such information. Thispublication consists of the opinions of Gartner’s research organization and should not be construed as statements of fact. The opinionsexpressed herein are subject to change without notice. Although Gartner research may include a discussion of related legal issues,Gartner does not provide legal advice or services and its research should not be construed or used as such. Gartner is a public company,and its shareholders may include firms and funds that have financial interests in entities covered in Gartner research. Gartner’s Board ofDirectors may include senior managers of these firms or funds. Gartner research is produced independently by its research organizationwithout input or influence from these firms, funds or their managers. For further information on the independence and integrity of Gartnerresearch, see “Guiding Principles on Independence and Objectivity.”

Gartner, Inc. | G00297526 Page 29 of 29