personal finance: what i’ve learned after graduation

TRANSCRIPT

Personal Finance: Personal Finance: What I’ve Learned After What I’ve Learned After

GraduationGraduation

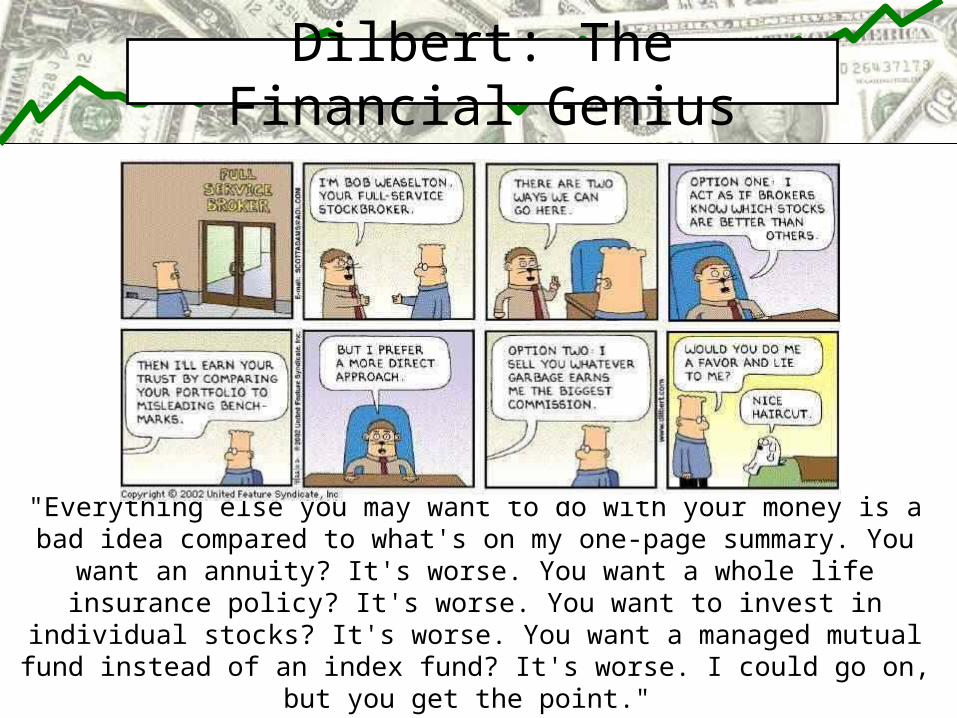

"Everything else you may want to do with your money is a bad idea compared to what's on my one-page summary. You want an annuity? It's worse. You

want a whole life insurance policy? It's worse. You want to invest in individual stocks? It's worse. You want a managed mutual fund instead of an index fund?

It's worse. I could go on, but you get the point." -Scott Adams

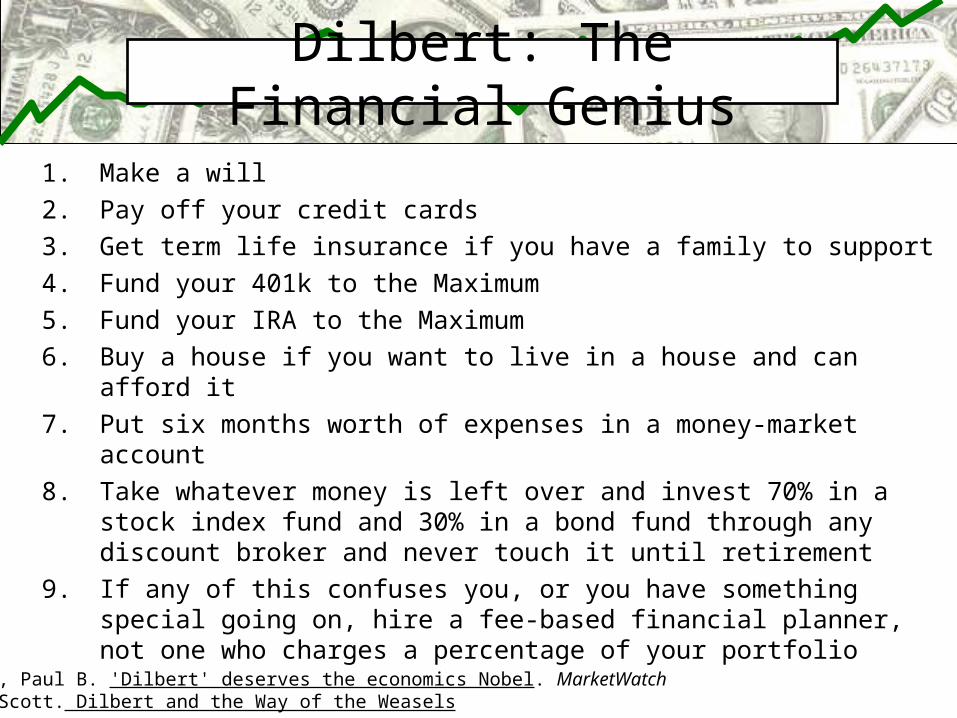

Dilbert: The Financial Genius

1. Make a will

2. Pay off your credit cards

3. Get term life insurance if you have a family to support

4. Fund your 401k to the Maximum

5. Fund your IRA to the Maximum

6. Buy a house if you want to live in a house and can afford it

7. Put six months worth of expenses in a money-market account

8. Take whatever money is left over and invest 70% in a stock index fund and 30% in a bond fund through any discount broker and never touch it until retirement

9. If any of this confuses you, or you have something special going on, hire a fee-based financial planner, not one who charges a percentage of your portfolio

Dilbert: The Financial Genius

Farrell, Paul B. 'Dilbert' deserves the economics Nobel. MarketWatchAdams, Scott. Dilbert and the Way of the Weasels

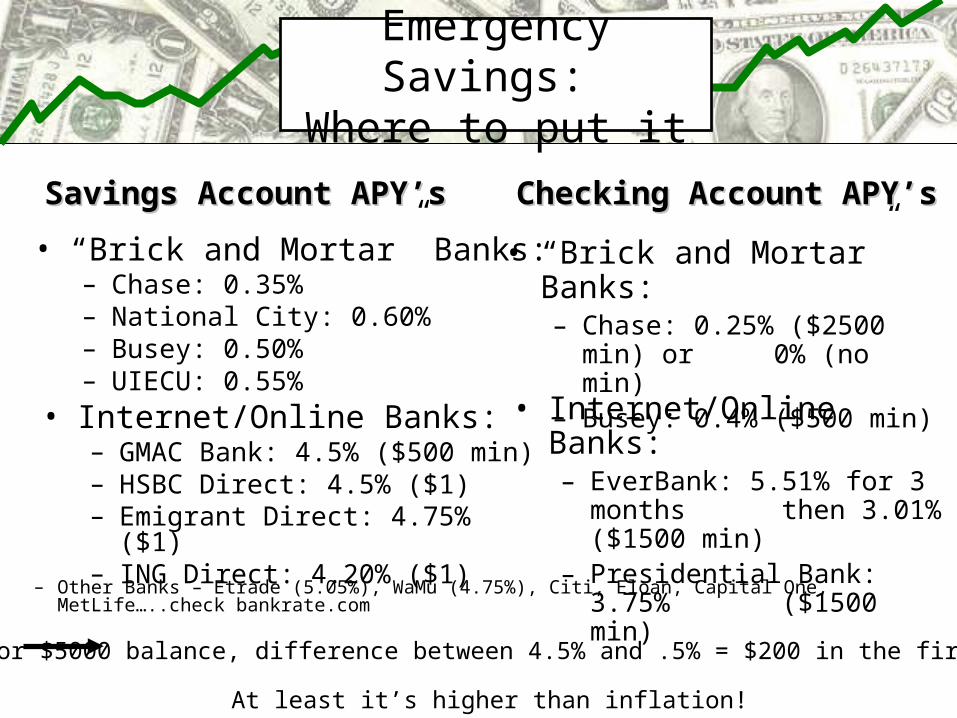

• “Brick and Mortar” Banks: – Chase: 0.35%– National City: 0.60%– Busey: 0.50%– UIECU: 0.55%

Emergency Savings: Where to put it

Savings Account APY’sSavings Account APY’s

• “Brick and Mortar” Banks: – Chase: 0.25% ($2500 min) or

0% (no min)– Busey: 0.4% ($500 min)

Checking Account APY’sChecking Account APY’s

• Internet/Online Banks:– GMAC Bank: 4.5% ($500 min)– HSBC Direct: 4.5% ($1)– Emigrant Direct: 4.75% ($1)– ING Direct: 4.20% ($1)

For $5000 balance, difference between 4.5% and .5% = $200 in the first year

At least it’s higher than inflation!

• Internet/Online Banks:– EverBank: 5.51% for 3 months

then 3.01% ($1500 min)

– Presidential Bank: 3.75% ($1500 min)

– Other Banks – Etrade (5.05%), WaMu (4.75%), Citi, Eloan, Capital One, MetLife…..check bankrate.com

• Stocks– U.S. Companies

• Large Cap: Found in the S&P 500, Dow Jones, Nasdaq

– ExxonMobil, McDonalds, GE, P&G, etc• Mid Cap• Small Cap

– International• Europe, Asia, Emerging Markets

• Bonds– Corporate Bonds

• Long term, short term– Government Bonds

• 30 year, EE/E Savings Bonds, I-Bonds, etc.

• Treasury Bills– 28 day, 91 day, 182 day

What to do with the rest: Investments

• Dow Jones-Wilshire 5000– All U.S. companies that offer stock– ~ $16 trillion total market cap

• S&P 500 – 500 largest U.S. companies– Makes up ~30% of the total value of

the DJW 5000• Dow Jones

– 30 of the biggest U.S. companies– Makes up ~20% of the total value of

the DJW 5000• Nasdaq - 100

– 100 biggest “tech” companies• Russell 2000

– 2000 smallest U.S. companies

U.S. Stock Market: Famous Indexes

3M

AT&TBoeing

Caterpillar

Coca-Cola

Microsoft

Honeywell

Merck

Citigroup

P&G

Home Depot

JPMorgan Chase

DuPont

GM

Pfizer

HP

GE

IBM

ExxonMobil

McDonalds

Walt Disney

Johnson & JohnsonVerizon

United TechnologiesWal-Mart

Intel

American ExpressAGI

Alcoa

Altria Group

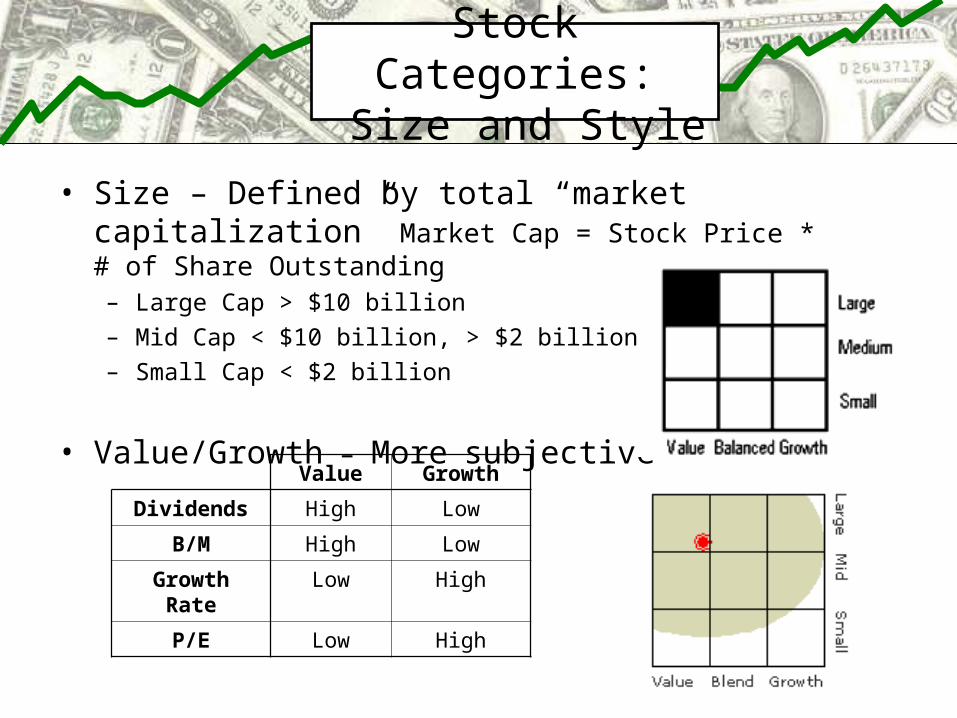

• Size – Defined by total “market capitalization” Market Cap = Stock Price * # of Share Outstanding– Large Cap > $10 billion

– Mid Cap < $10 billion, > $2 billion

– Small Cap < $2 billion

• Value/Growth – More subjective

Stock Categories: Size and Style

Value Growth

Dividends High Low

B/M High Low

Growth Rate Low High

P/E Low High

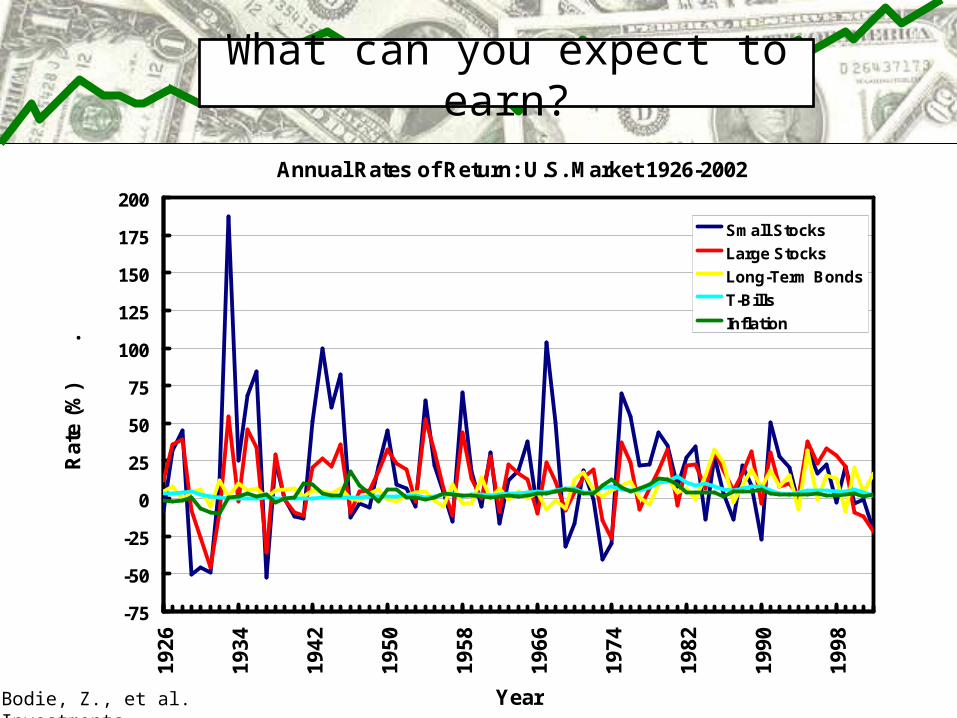

What can you expect to earn?

Annual Rates of Return: U.S. Market 1926-2002

-75

-50

-25

0

25

50

75

100

125

150

175

200

1926

1934

1942

1950

1958

1966

1974

1982

1990

1998

Year

Rat

e (%

)

.

Small Stocks

Large Stocks

Long-Term Bonds

T-Bills

Inflation

Bodie, Z., et al. Investments

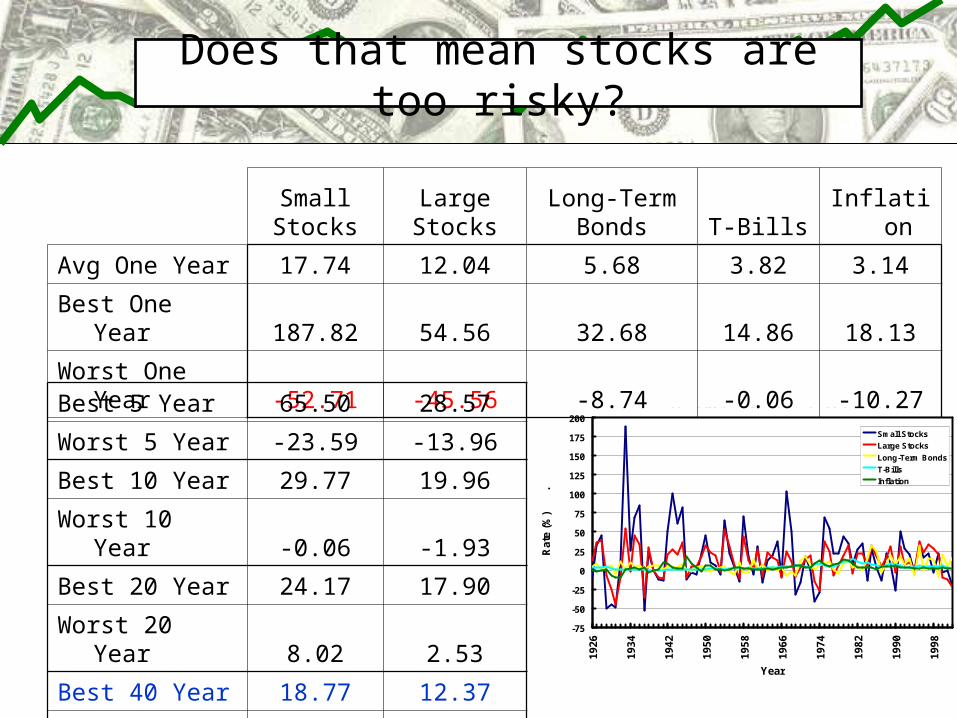

SmallStocks

LargeStocks

Long-TermBonds T-Bills Inflation

Avg One Year 17.74 12.04 5.68 3.82 3.14

Best One Year 187.82 54.56 32.68 14.86 18.13

Worst One Year -52.71 -45.56 -8.74 -0.06 -10.27

Does that mean stocks are too risky?

Best 5 Year 65.50 28.57

Worst 5 Year -23.59 -13.96

Best 10 Year 29.77 19.96

Worst 10 Year -0.06 -1.93

Best 20 Year 24.17 17.90

Worst 20 Year 8.02 2.53

Best 40 Year 18.77 12.37

Worst 40 Year 11.28 8.53

Annual Rates of Return: U.S. Market 1926-2002

-75

-50

-25

0

25

50

75

100

125

150

175

200

192

6

193

4

194

2

195

0

195

8

196

6

197

4

198

2

199

0

199

8

Year

Rat

e (%

)

.

Small Stocks

Large Stocks

Long-Term Bonds

T-Bills

Inflation

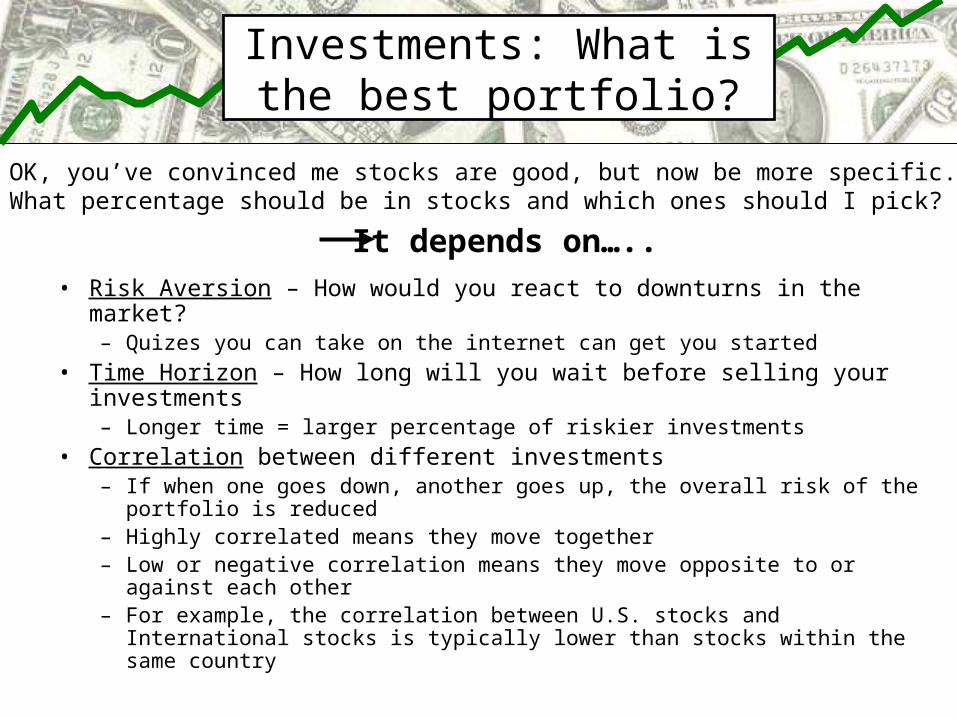

Investments: What is the best portfolio?

OK, you’ve convinced me stocks are good, but now be more specific. What percentage should be in stocks and which ones should I pick?

• Risk Aversion – How would you react to downturns in the market?– Quizes you can take on the internet can get you started

• Time Horizon – How long will you wait before selling your investments– Longer time = larger percentage of riskier investments

• Correlation between different investments – If when one goes down, another goes up, the overall risk of the portfolio is

reduced– Highly correlated means they move together– Low or negative correlation means they move opposite to or against each

other– For example, the correlation between U.S. stocks and International stocks

is typically lower than stocks within the same country

It depends on…..

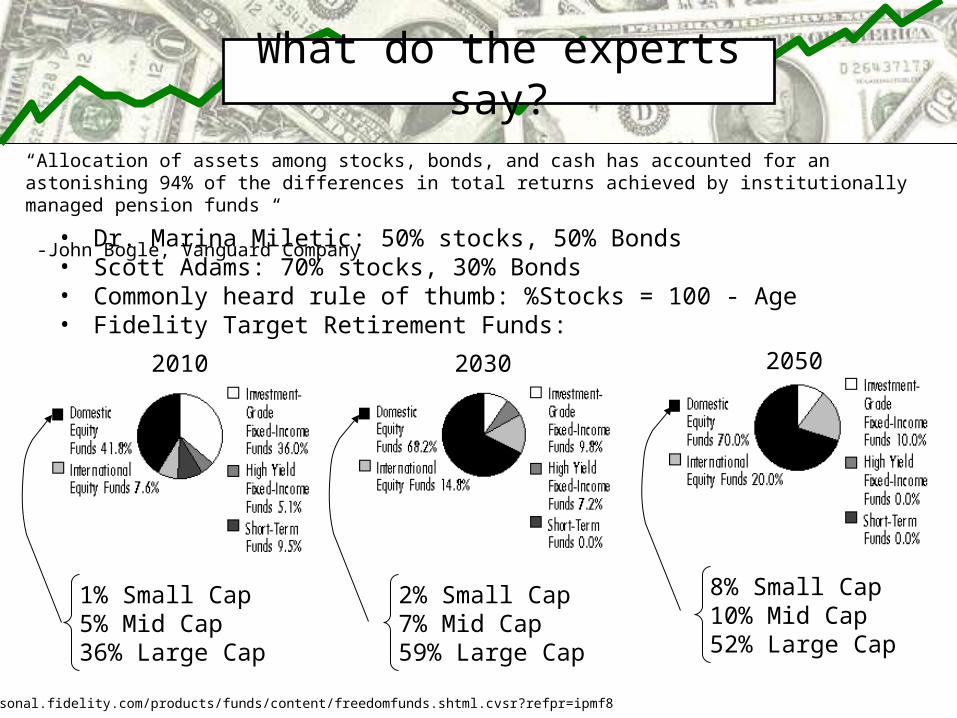

• Dr. Marina Miletic: 50% stocks, 50% Bonds• Scott Adams: 70% stocks, 30% Bonds• Commonly heard rule of thumb: %Stocks = 100 - Age• Fidelity Target Retirement Funds:

What do the experts say?

2010 2030 2050

1% Small Cap5% Mid Cap36% Large Cap

2% Small Cap7% Mid Cap59% Large Cap

8% Small Cap10% Mid Cap52% Large Cap

http://personal.fidelity.com/products/funds/content/freedomfunds.shtml.cvsr?refpr=ipmf8

“Allocation of assets among stocks, bonds, and cash has accounted for an astonishing 94% of the differences in total returns achieved by institutionally managed pension funds “

-John Bogle, Vanguard Company

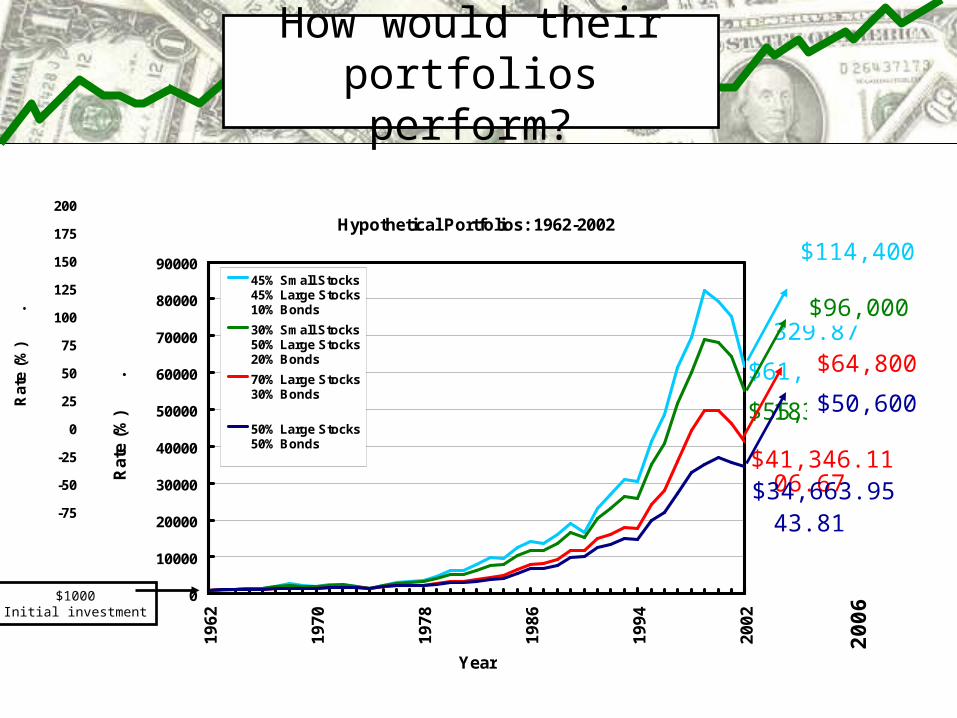

How would their portfolios perform?

$3329.87

$2183.56

$806.67

$443.81

Hypothetical Portfolios: 1926-2002

-75

-50

-25

0

25

50

75

100

125

150

175

200

1926

1934

1942

1950

1958

1966

1974

1982

1990

1998

Year

Rat

e (%

)

.

45% Small Stocks45% Large Stocks10% Bonds30% Small Stocks50% Large Stocks20% Bonds 70% Large Stocks30% Bonds

50% Large Stocks50% Bonds

Hypothetical Portfolios: 1926-2002

0

1000

2000

3000

4000

5000

1926

1934

1942

1950

1958

1966

1974

1982

1990

1998

Year

Rat

e (%

)

.

45% Small Stocks45% Large Stocks10% Bonds

30% Small Stocks50% Large Stocks20% Bonds

70% Large Stocks30% Bonds

50% Large Stocks50% Bonds

Hypothetical Portfolios: 1962-2002

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

1962

1970

1978

1986

1994

2002

Year

Rat

e (%

)

.

45% Small Stocks45% Large Stocks10% Bonds

30% Small Stocks50% Large Stocks20% Bonds

70% Large Stocks30% Bonds

50% Large Stocks50% Bonds

$1000Initial investment

$61,595.18

$55,238.68

$41,346.11$34,663.95

2006

$114,400

$96,000

$64,800

$50,600

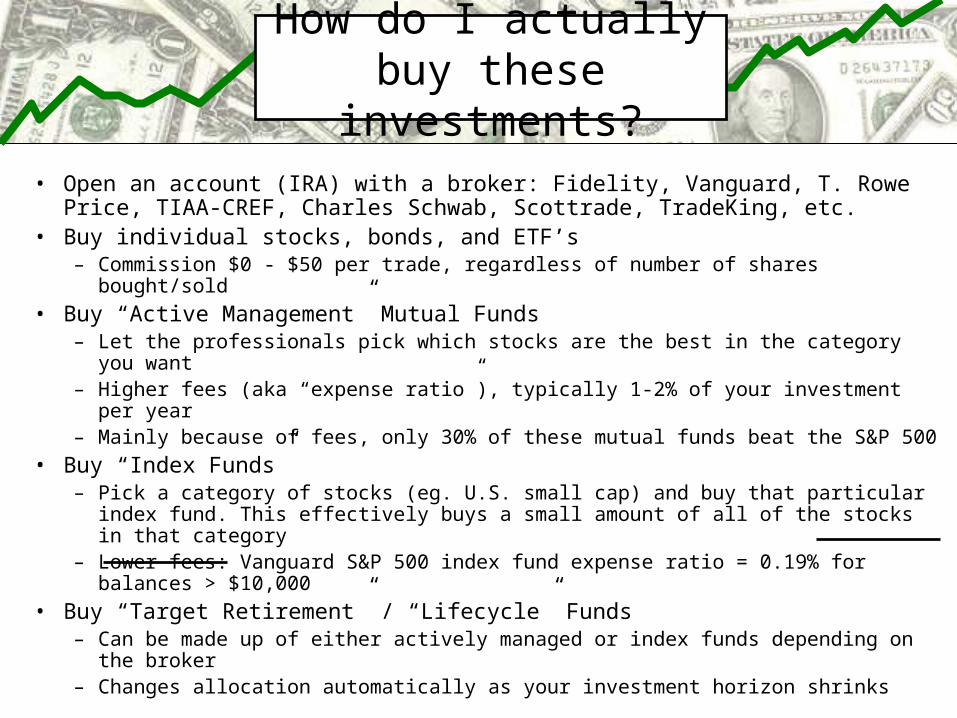

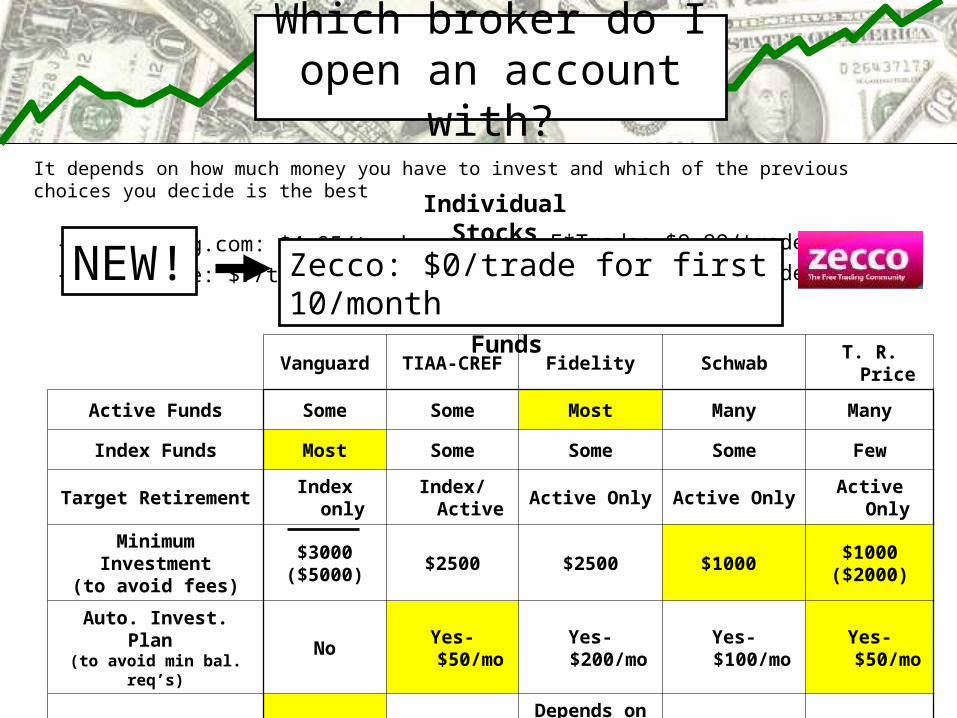

• Open an account (IRA) with a broker: Fidelity, Vanguard, T. Rowe Price, TIAA-CREF, Charles Schwab, Scottrade, TradeKing, etc.

• Buy individual stocks, bonds, and ETF’s– Commission $0 - $50 per trade, regardless of number of shares bought/sold

• Buy “Active Management” Mutual Funds– Let the professionals pick which stocks are the best in the category you want– Higher fees (aka “expense ratio”), typically 1-2% of your investment per year– Mainly because of fees, only 30% of these mutual funds beat the S&P 500

• Buy “Index Funds”– Pick a category of stocks (eg. U.S. small cap) and buy that particular index

fund. This effectively buys a small amount of all of the stocks in that category– Lower fees: Vanguard S&P 500 index fund expense ratio = 0.19% for balances

> $10,000

• Buy “Target Retirement” / “Lifecycle” Funds– Can be made up of either actively managed or index funds depending on the

broker– Changes allocation automatically as your investment horizon shrinks

How do I actually buy these investments?

– TradeKing.com: $4.95/trade– Scottrade: $7/trade

Which broker do I open an account with?

It depends on how much money you have to invest and which of the previous choices you decide is the best

– E*Trade: $9.99/trade– Schwab: $12.95/trade

Mutual Funds

Vanguard TIAA-CREF Fidelity Schwab T. R. Price

Active Funds Some Some Most Many Many

Index Funds Most Some Some Some Few

Target Retirement Index only Index/Active Active Only Active Only Active Only

Minimum Investment(to avoid fees)

$3000 ($5000)

$2500 $2500 $1000 $1000

($2000)

Auto. Invest. Plan (to avoid min bal. req’s)

No Yes- $50/mo Yes- $200/mo Yes- $100/moYes- $50/mo

Average Expenses Lowest LowDepends on

Active / IndexHigh High

Individual Stocks

Zecco: $0/trade for first 10/monthNEW!

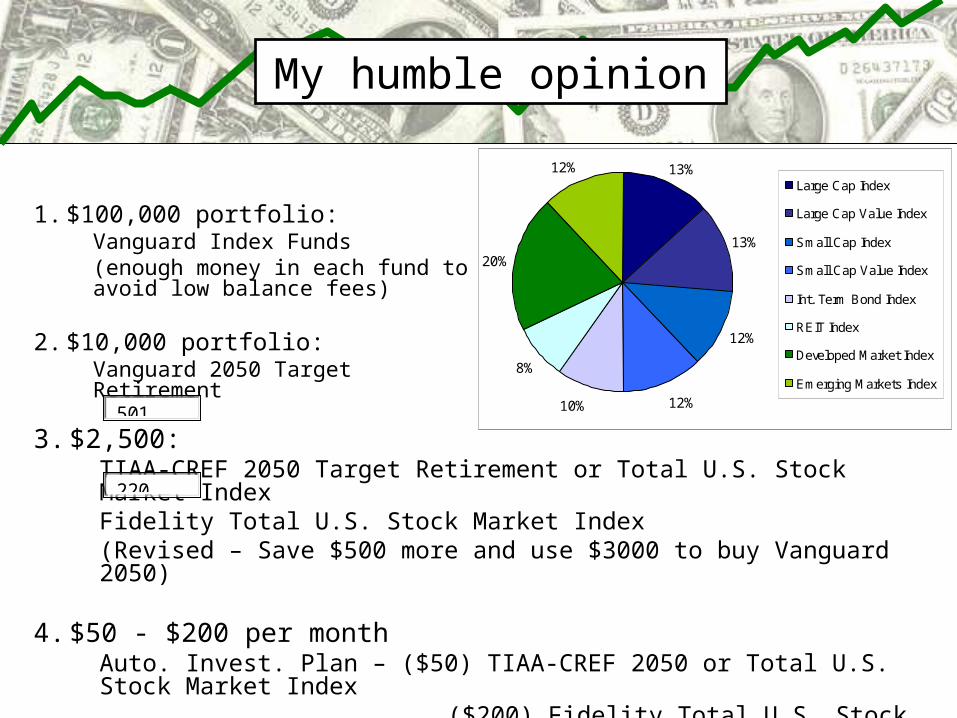

My humble opinion

1. $100,000 portfolio: Vanguard Index Funds(enough money in each fund to avoid low balance fees)

2. $10,000 portfolio:Vanguard 2050 Target Retirement

3. $2,500:TIAA-CREF 2050 Target Retirement or Total U.S. Stock Market IndexFidelity Total U.S. Stock Market Index(Revised – Save $500 more and use $3000 to buy Vanguard 2050)

4. $50 - $200 per monthAuto. Invest. Plan – ($50) TIAA-CREF 2050 or Total U.S. Stock Market Index

($200) Fidelity Total U.S. Stock Market Index

13%

13%

12%

12%10%

8%

20%

12%Large Cap Index

Large Cap Value Index

Small Cap Index

Small Cap Value Index

Int. Term Bond Index

REIT Index

Developed Market Index

Emerging Markets Index

501

220