peloponnese region investment profile

TRANSCRIPT

Peloponnese Region ‐ Investment Profile

0

Peloponnese Region: Quick overviewPeloponnese Region: Quick overview

• The Peloponnese region is one of the thirteen regions of Greece and covers 11.7% of the total area of the country

• It includes the prefectures of Arkadia, Argolida, Korinthia, Lakonia and Messinia

Corinth• Arkadia and Lakonia are the two prefectures of the

region with the highest percentage of rural population(67.8% and 67.3% respectively), and Argolida prefecturewith the highest percentage in urban population

Argos

Tripoli

• Key cities include namely Tripoli, Argos, Corinth, Sparta and Kalamata

• Tripoli also serves as the Region’s capital

• On the west it is surrounded by the Ionian Sea and bordered by

Sparta

Kalamata

the Region of Western Greece, on the northeast it borders with the region of Attica, while on the east coast it is surrounded by the Sea of Myrtoo

• It has a total area of 15,490 km2 of which 2,154 km² occupied by th f t f A lid 4 419 k ² b th f t f

Main highwaysRailway network

Kalamata the prefecture of Argolida, 4,419 km² by the prefecture of Arkadia, 2,290 km² by the prefecture ofKorinthia, 3,636 km² by the prefecture of Lakonia and 2,991 km² by the prefecture of Messinia

• Tripoli and Kalamata also harbour universities

1

yMain cities

• Tripoli and Kalamata also harbour universities

• Population: 638,942 inhabitants (Census 2001)

• Population density: 41.2 inhabitants / km²

Peloponnese Region: Quick factsPeloponnese Region: Quick facts

• The economic mix of the Region of Peloponnese includes mostly

Investment incentives quickfacts

European Program for Peloponnese, Western Greece and the Ionian Islands: €1.3 bn

New Investment law: Subsidies for up to 50% ofactivities in agriculture and tourism services. Small industrial

activity has been scarce but picking up over the last years

• More specifically, its contribution to the national agricultural

New Investment law: Subsidies for up to 50% of business plans, tax incentives for up to ten years

Jessica Holding Fund for Greece: €250m

Jeremie fund for Greece: €150mproduction is significant. The region’s agricultural sites

correspond to 11% of total sites in Greece. Main agricultural

products are fruits (53% of national production), olive oil (65% of

national production) and potatoes (11% of national production)

Workforce quickfacts

Total workforce: 260,000

Employment rate: 62%

• The Peloponnese is also famous for its wine producing areas

such as Nemea and Mandinea. The region holds the 1st position

in terms of the number of producers, wineries, varieties and

i d i G It t ll t 29 1% f th G k

Employment rate (55‐64 years): 42,5%

Employment rate women: 46,6%

Number of University faculties: 8vineyards in Greece. It actually represents 29.1% of the Greek

vineyard map and produces 1,208 different labels, which ranks

the region 1st in terms of the number of wines produced in

Greece

Cultural and natural quickfacts

Archaeological sites: 60

Museums: 20

2

Museums: 20

Natura 2000 regions: 47

Blue flag awarded beaches: 28

Peloponnese has a breathtaking geography to offerPeloponnese has a breathtaking geography to offer

• Peloponnese has a characteristic and unique morphologywith big mountains occupying a part of the north andwith big mountains occupying a part of the north, andthe entire southeastern part of the western part of thewhole of the Peloponnese

• This geographical position gives the region a character ofan inland southern gateway to the large island of Creteand the island of Cyprus. This position coupled with theimmediate proximity to the metropolitan center of thecountry, Athens, makes a "bridge" that connects thesouthern island part of Europe with the capital ofp p pGreece, Western Europe and the Balkans, taking intoaccount the new road links with European networks

• Today via the creation of major roads and the gradualimprovement of port infrastructure the location of theimprovement of port infrastructure, the location of theregion becomes an advantage for a dynamic growthpath, situated within the geographical area of theEuropean Union

3

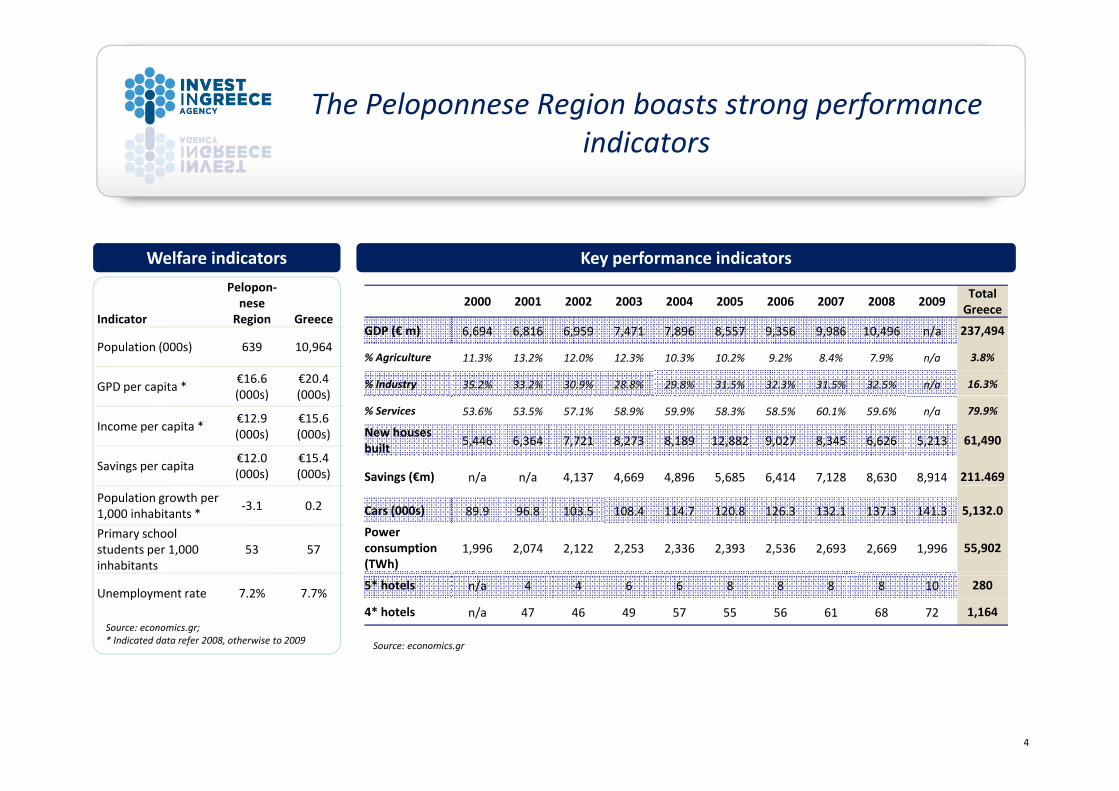

The Peloponnese Region boasts strong performance indicators

Pelopon‐nese

Key performance indicators

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009TotalG

Welfare indicators

IndicatorneseRegion Greece

Population (000s) 639 10,964

GPD per capita *€16.6(000s)

€20.4 (000s)

Greece

GDP (€ m) 6,694 6,816 6,959 7,471 7,896 8,557 9,356 9,986 10,496 n/a 237,494

% Agriculture 11.3% 13.2% 12.0% 12.3% 10.3% 10.2% 9.2% 8.4% 7.9% n/a 3.8%

% Industry 35.2% 33.2% 30.9% 28.8% 29.8% 31.5% 32.3% 31.5% 32.5% n/a 16.3%(000s) (000s)

Income per capita *€12.9 (000s)

€15.6 (000s)

Savings per capita€12.0 (000s)

€15.4 (000s)

% Services 53.6% 53.5% 57.1% 58.9% 59.9% 58.3% 58.5% 60.1% 59.6% n/a 79.9%

New houses built 5,446 6,364 7,721 8,273 8,189 12,882 9,027 8,345 6,626 5,213 61,490

Savings (€m) n/a n/a 4,137 4,669 4,896 5,685 6,414 7,128 8,630 8,914 211.469

Population growth per 1,000 inhabitants *

‐3.1 0.2

Primary school students per 1,000 inhabitants

53 57

Cars (000s) 89.9 96.8 103.5 108.4 114.7 120.8 126.3 132.1 137.3 141.3 5,132.0

Powerconsumption (TWh)

1,996 2,074 2,122 2,253 2,336 2,393 2,536 2,693 2,669 1,996 55,902

Unemployment rate 7.2% 7.7%

Source: economics.gr; * Indicated data refer 2008, otherwise to 2009

5* hotels n/a 4 4 6 6 8 8 8 8 10 280

4* hotels n/a 47 46 49 57 55 56 61 68 72 1,164

Source: economics.gr

4

The strong economy of the Peloponnese Region is reflected in its export activity

Total value of exports: €607m

Key exporting goods

Medical devices

Pharmaceuticals 1,7% Other

9 9%

Total value of exports: €607m

• Approximately half of the exports are destined to EU

Fruit and vegetables 34,3%Vegetable

oils 8,6%

Medical devices 5,1%

9,9%countries

• The most extrovert prefecture is that of Argolida, which

boasts half of the Region’s exports

Petroleum

Tobacco products 14,8%

, g p

• The prefectures of Korinthia and Messinia make up

almost the entire other 50%

products 25,6%

S HEPO

5

Source: HEPO

The Peloponnese Region attracts significant foreign and domestic investment

FDI breakdown per region Foreign vs domestic investments per region

Peloponnese 32%

Western Macedonia

Attica 4%

Other 10%

621

1.178

813

1.057

Mainland Greece

Peloponnese

32%

Eastern Macedonia ‐Thrace 6%

5%

645

370

262

332

Western Greece

Central Macedonia

Foreign

Central

Western Greece 8%

233

500

169

200

Western Macedonia

Eastern Macedonia ‐Thrace

Domestic

Mainland Greece 25%

Macedonia 10%

2.497

944

323

147

Other

Attica

6

Source: Invest in Greece Agency Source: Invest in Greece Agency

Peloponnese offers an ideal environment for investmentPeloponnese offers an ideal environment for investment

Peloponnese’s advantages ..are enhanced by investment incentives

Peloponnese, has very attractive features such as:

1. Proximity and motorway and railway to Athens and the

mainland

• Under the new Investment Incentives Law, Peloponnese

enjoys attractive investment incentives varying from 30% to

50% of the total investment cost, according to the area and

2. Advanced infrastructure networks

3. Natural resources of all kinds

4. Skilled work force, especially in Tourism and Agriculture

g

the size of the company

• The new Law focuses on supporting sustainable

investment projects with efficient tax breaks,

favorable loans and state aids in selected business

activities

7

* Please refer to the full text of the new Law 3851/2010 for detailed and analytical information

Several sectors strive in Peloponnese, presenting concrete investment cases

Corinth

TourismArgos

Tripoli

Renewable Energy Sources

Sparta

Tripoli

Food and beverage

Main highways

p

Kalamata

Waste managementRailway networkMain cities

8

TourismRESFoodWaste

Investment opportunities:Tourism

Significant infrastructure Unique competitive advantages

• Greece held in 2010 the 2nd place among 41 countriesacross Europe, in the European Blue Flag Program with 421beaches and 9 marinas

• 28 beaches and 1 Marina are located in the

• The Peloponnese Region holds unique cultural, historic andarchaeological treasures

• Notably, the first World Heritage site declared fromUNESCO, was the Temple of Apollo and the most

Peloponnese Region• Messinia Prefecture in the Peloponnese, is included in the

20 Best Trips for 2011 by the National Geographic Traveler• The only Integrated Resort in the country, renowned resort

Costa Navarino is to be found in the prefecture of Messinia

, p precent the Mediterranean Diet

• Peloponnese is a region with an amazing variety in sceneryencompassing 47 sites registered and protected by theNatura 2000 program, for its rare species of flora and fauna.

• These sites form a great "natural touring map”Costa Navarino is to be found in the prefecture of Messinia• 601 of the total 9.559 Hotels that exist in Greece, are to be

found in the region of Peloponnese• 10 of them belong in the 5 star category

• These sites form a great natural touring map ,which includes mountains, wetlands, rivers, andpeninsulas of extreme beauty

• Satisfactory tourism infrastructure with opportunities todevelop further high end tourism facilities and services

These translate into concrete

9

These translate into concrete business opportunities

TourismRESFoodWaste

Tourism Facts & Figures:Peloponnese region

Ni ht t t H t l t bli h t &Tourism Arrivals in main airports of Greece‐2009

Nights spent at Hotel establishments & Campsites by Region ‐ 2009

Regions 2009 % of total Athens 3.143.238Heraklion 1.954.611

Crete 15.621.455 23,70%

South Aegean 14.636.435 22,20%

Central Macedonia 7.891.793 12,00%

Heraklion 1.954.611Rhodes 1.325.139

Thessaloniki 1.189.444Corfu 744.225Kos 627.857

Ionian Islands 7.457.180 11,30%

Attica 7.055.609 10,70%

Peloponnese 2.830.581 4,30%

Chania 592.456Zakinthos 430.398Santorini 162.414Aktio 147.574

Thessaly 2.111.634 3,20%

Western Greece 1.861.313 2,80%

Central Greece 1.767.856 2,70%

Kefallonia 143.438Samos 116.203Skiathos 108.829Mykonos 96.745

East Macedonia & Thrace 1.754.483 2,70%

North Aegean 1.635.463 2,50%

Epirus 1.015.199 1,50%

yKavala 83.942Mytilini 71.452Araxos 41.418

Kalamata 30.446

10

West Macedonia 383.269 0,60%

Greece Total 66.022.270 100,00%

Kalamata 30.446Chios 11.967

Limnos 6.563

Source: Civil Aviation Authority Source: Association of Greek Tourism EnterprisesTourismRESFoodWaste

Tourism Facts & Figures:Peloponnese region

N b f 5* H l G k R i 2009Number of 5* Hotels per Greek Region ‐ 2009

7Total Greece:

280

352 % of Hotel beds per category

as of country’s total in the

29

62149 1* 4,6%

2* 7,8%

Peloponnese ‐ 2009

2967

10

3* 8,3%

4* 5,1%

5* 6,4%

67

5 6,4%

11

Source: Hellenic Chamber of Hotels & Association of Greek Tourism Enterprises ‐ 2009 TourismRESFoodWaste

Various tourism segments make up an investment opportunity in the region

Marinas Golf ResortsEco Tourism

Integrated Resorts Development of existing state & private assets

12

TourismRESFoodWaste

Tourism success story: Costa Navarino ResortCosta Navarino Resort,

a prime destination in the Mediterranean

• The first already completed phase of Costa Navarino Resort NavarinoDunes features a 1‐kilometre sandy beach amidst lush olive groves.The site is the setting for The Romanos, a Luxury Collection Resortand The Westin Resort. Starwood Hotels & Resorts operates both 5‐star properties. The two resorts offer extensive facilities andactivities, including The Dunes Golf Course, the first signature 18‐holegolf course in Greece, the House of Events conference centre, and awide range of gourmet experiences, sport and cultural facilities,wide range of gourmet experiences, sport and cultural facilities,outdoors activities, branded stores and well‐designed children andyouth centres

• Anazoe Spa has also opened in Navarino Dunes. The 4,000 m2 spai l d i h li ti th i b d th bi ti f thincludes unique holistic therapies based on the combination of theancient therapeutic expertise and modern cosmetology

• The second phase, the 140 hectare Navarino Bay site will open in the near future and will showcase Banyan Tree all‐pool‐villa resort, the first of its kind in Europe, an 18‐hole signature golf course, as well as another five star hotel

• Two further phases, Navarino Hills and Navarino Blue, will open at a later date

13

later date

TourismRESFoodWaste

Luxury integrated resort in the pipeline: The Porto Heli Collection

• The Porto Heli Collection spreading over an area of 3 470 000 sq m will become home to four five‐star hotels each one offering aThe Porto Heli Collection, spreading over an area of 3,470,000 sq.m., will become home to four five star hotels, each one offering aunique style of vacationing and amenities, catering to a diverse range of travelers. In addition, a number of luxury villas, both brandedfrom the hotels and non branded, will be build throughout the different parts of the resort.

• Special Features: Whatever style of hotel a visitor seeks, from understated elegance, privacy, and opulent luxury, to an activity‐packedbeach holiday with incomparable spa and golf facilities, they will be able to find the perfect holiday destination within The Porto HeliC ll tiCollection.

• Composition:• Europe’s first villa –integrated Aman Hotel, spa, beach club and residences• The Seafront Villas• The Chedi Hotel, spa, club suites and residences

14

• Jack Nicklaus Signature Golf Course• The Nikki at Porto Heli with hotel suites, serviced apartments and beach club• Golf boutique hotel with suites, golf clubhouse and golf residences• Equestrian centre, tennis academy, kid’s club, beach club

TourismRESFoodWaste

Investment opportunities: Renewable Energy Sources – Peloponnese Current Status

Capacity (MW) currently in operation or under construction

Wind Solar Hydro

Wind Energy

Argolida 319,75 45,83 2,00

Arcadia 467,65 75,50 11,16

Lakonia 355,90 69,31 3,99

21%

31%24%

24% Argolida

Arcadia

Lakonia

Messinia 355,90 47,71 0

Total 1499,20 238,35 17,15

31%24% Messinia

Solar Energy Hydro Plants

21%24%

Solar Energy

Argolida

12%23%

0%

Hydro Plants

Argolida

31%24%

Argolida

Arcadia

Lakonia

Messinia65%

Argolida

Arcadia

Lakonia

Messinia

15

TourismRESFoodWaste

Investment opportunities:Renewable Energy Sources – UnexploitedRenewable Energy Sources Unexploited

Capacity

Peloponnese has unexploited capacity in Solar and Wind energy production. As shown in the attached Maps the potential is tremendous.

Solar energy capacity Wind energy capacity

16

TourismRESFoodWaste

Investment opportunities: Renewable Energy Sources – National Targets

Targeted participation of RES & conventional technology in electricity generation for the year 2020 in market shares & numerical targets

• Targets set by the Committee for the National Energy StrategyTargets set by the Committee for the National Energy Strategy

• Targets are binding for the Greek government

• Wind energy is expected to dominate electricity generation from RES

7.500

Participation of RES & Conventional Technology

National Targets for the year 2020

Geothermal 0 24%

PV 1,44% Hydro 6,08% Biomass–Biogas 0 53%

3.237

4.650

2.200

Participation of RES & Conventional Technology in Electricity Generation for the year 2020

0,24% 0.53%

Wind 24,09%

ConcetratedConventional

0 198,3 0

1.297,7

44120 250 350

Hydro Geothermal PV Concetraded Wind Biomass

17

Solar 0.73%66,90%

Source: YPEKA, National Renewable Energy Action Plan

Source: Committee for the National Energy Strategy

Solar

Capacity 2010 Target 2020

TourismRESFoodWaste

Investment opportunities: Food & Beverage Mediterranean DietFood & Beverage ‐Mediterranean Diet,

olive oil sector

Facts on the F&B sector …which form an excellent business case

• Greece holds the 3rd place in world olive oil production

(after Spain and Italy) with more than 140 million trees,

which produce about 400,000 tons of olive oil annually, of

hi h 75 80% i t i i il (hi h t lit )

• Olives are grown mainly in mainland Greece. The

Peloponnese, accounts for approximately 65% of annual

domestic productionwhich 75‐80% is extra virgin oil (highest quality)

• This ranks Greece the 1st country in the world in

production of extra virgin olive oil (Italy is 2nd with

p

• The prefecture of Messinia in the Peloponnese is one of

the few areas where the harvesting of olives is still made by

hand and not with the help of machines40‐45% of its annual production being extra virgin

olive oil and Spain 3rd with 25‐30%)

• In recent years, scientific and medical studies have

hand and not with the help of machines

concluded that the Mediterranean diet is the best recipe

for longevity and is becoming more widely accepted for its

positive effects on health

18

TourismRESFoodWaste

Investment opportunities: F d & B M di DiFood & Beverage ‐Mediterranean Diet,

Wine

• The Peloponnese is also famous for its wine producing

areas such as Nemea andMandinea (Appellation d’ origine

Facts on the F&B sector

areas such as Nemea and Mandinea (Appellation d origine

contrôlée)

• The region holds the 1st position in terms of the number of

d i i i i t i d l d i )producers, wineries, wine variety, vineyard land size)

• The region represents 29.1% of the Greek vineyard

map and produces 1.208 different kinds of wine,

which ranks the region 1st in terms of the number of

wines produced

• A tour of the area's vineyards and local wineries offers the

visitor an opportunity for excellent wine tasting, as well as

an introduction to the history and art of local winemaking,

grape varieties and the region's winemaking ritual with

19

roots deep in antiquity

TourismRESFoodWaste

Investment opportunities:Waste management

According to EU and national directives Greece should: • recover at least 60% by weight all packaging waste by 2011

which includes recycling at least 55%

EU imposed targets …create sound investment opportunities

• Creation of modern, integrated facilities for treating and

disposing municipal solid wastewhich includes recycling at least 55%Current Status: 50%

• decrease biodegradable waste that is sent to landfill by • 1,100,000 tons in 2010

disposing municipal solid waste

• Energy recovery from organic waste

• Rehabilitation of the existing landfills

• 1,900,000 tons in 2013 and • 2,700,000 tons in 2020

Current Status: 461,079 tons (42% target coverage)

• Environmental sound management of industrial, medical

and hazardous waste

• Construction of suitable transfer station networks and

recycling centres

• Selective collection at source and further recycling of

municipal wastemunicipal waste

• Water treatment and sea or brackish water desalination

• Wastewater and sewage treatment

20

TourismRESFoodWaste

There are several investment opportunities available in the Peloponnese Region

Sector Description County Project reference

Tourism Development of 5* resort and vacation residences project at Porto Argolida IP7Tourism Heli Argolida IP7

Tourism Development of vacation residences at Porto Hydra Argolida IP17

Tourism Development of marina with 400 births in Pylos Messinia IP27

Tourism Development of a hotel in Kardamili Messinia IP16

RES Development of Vromosykia & Lamboussa wind farms Argolida RES4

RES Development of Gropes & Kalogerovouni wind farms Lakonia RES4

21

ICT Administration of fiber optic metropolitan area networks Entire region ICT15

The local government is pushing projects to promote the attractiveness of the Region

• Reformation of the Corinth Canal based on its architectureReformation of the Corinth Canal based on its architecture

and design: The Canal is the gateway to the Peloponnese

region and has a width of approximately 6 km

• Restoration of Bourtzi: The restoration of Bourtzi is planned

to materialise through NSRF fundingto materialise through NSRF funding

22

The local government is pushing projects to promote the attractiveness of the Region

• Development of Karathonas: It is planned

to develop Karathonas, which lies next to p

Nafplio, with high end tourism projects

• Improve management of Dyros Caves: It is

estimated that by improving the management of

Dyros Caves the annual visitors could increase by

50% to 150,000

23

24