pat assigned 1

TRANSCRIPT

8/18/2019 Pat Assigned 1

http://slidepdf.com/reader/full/pat-assigned-1 1/54

THIRD DIVISION

[G.R. No. 112675. January 25, 1999.]

AFISCO INSURANCE CORPORATION; CCC INSURANCE CORPORATION; CHARTER INSURANCE

CO., INC.; CIBELES INSURANCE CORPORATION; COMMONWEALTH INSURANCE COMPANY;

CONSOLIDATED INSURANCE CO., INC.; DEVELOPMENT INSURANCE & SURETY CORPORATION;

DOMESTIC INSURANCE COMPANY OF THE PHILIPPINES; EASTERN ASSURANCE COMPANY &

SURETY CORP.; EMPIRE INSURANCE COMPANY; EQUITABLE INSURANCE CORPORATION;

FEDERAL INSURANCE CORPORATION INC.; FGU INSURANCE CORPORATION; FIDELITY & SURETY

COMPANY OF THE PHILS., INC.; FILIPINO MERCHANTS' INSURANCE CO., INC.; GOVERNMENT

SERVICE INSURANCE SYSTEM; MALAYAN INSURANCE CO., INC.; MALAYAN ZURICH INSURANCE

CO., INC.; MERCANTILE INSURANCE CO., INC.; METROPOLITAN INSURANCE COMPANY; METRO-

TAISHO INSURANCE CORPORATION; NEW ZEALAND INSURANCE CO., LTD.; PAN-MALAYAN

INSURANCE CORPORATION; PARAMOUNT INSURANCE CORPORATION; PEOPLE'S TRANS-EAST

ASIA INSURANCE CORPORATION; PERLA COMPANIA DE SEGUROS, INC.; PHILIPPINE BRITISH

ASSURANCE CO., INC.; PHILIPPINE FIRST INSURANCE CO., INC.; PIONEER INSURANCE & SURETY

CORP.; PIONEER INTERCONTINENTAL INSURANCE CORPORATION; PROVIDENT INSURANCE

COMPANY OF THE PHILIPPINES; PYRAMID INSURANCE CO., INC.; RELIANCE SURETY &

INSURANCE COMPANY; RIZAL SURETY & INSURANCE COMPANY; SANPIRO INSURANCE

CORPORATION; SEABOARD-EASTERN INSURANCE CO., INC.; SOLID GUARANTY, INC.; SOUTH SEA

SURETY & INSURANCE CO., INC.; STATE BONDING & INSURANCE CO., INC.; SUMMA INSURANCE

CORPORATION; TABACALERA INSURANCE CO., INC. — all assessed as "POOL OF MACHINERY

INSURERS," petitioners,vs. COURT OF APPEALS, COURT OF TAX APPEALS and COMMISSIONER OF

INTERNAL REVENUE, respondents.

Angara Abello Concepcion Regala for petitioners.

SYNOPSIS

8/18/2019 Pat Assigned 1

http://slidepdf.com/reader/full/pat-assigned-1 2/54

This is a Petition For Review onCertiorari assailing the Decision of the Court of Appeals dismissing petitioners' appeal of the

Decision of the Court of Tax Appeals which had sustained petitioners' liability for deficiency income tax, interest and withholding tax.

Petitioners contended that the Court of Appeals erred in finding that the pool or clearing house was an informal partnership, which

was taxable as a corporation under the NIRC. Petitioners further claimed that the remittances of the pool to the ceding companies

and Munich are not dividends subject to tax. They insisted that taxing such remittances contravene Sections 24 (b) (I) and 263 of the

1977 NIRC and would be tantamount to an illegal double taxation. Moreover, petitioners argued that since Munich was not a

signatory to the Pool Agreement, the remittances it received from the pool cannot be deemed dividends. However, even if such

remittances were treated as dividends, they would have been exempt under the previously mentioned sections of the 1977 NIRC, as

well as Article 7 of paragraph 1 and Article 5 of the RP-West German Tax Treaty. Petitioners likewise contended that the Internal

Revenue Commissioner was already barred by prescription from making an assessment.

In the present case, the ceding companies entered into a Pool Agreement or association that would handle all the insurance

businesses covered under their quota-share reinsurance treaty and surplus reinsurance treaty with Munich.AScHCD

Petitioner's allegation of double taxation is untenable. The pool is a taxable entity distinct from the individual corporate entities of the

ceding companies. The tax on its income is different from the tax on the dividends received by the said companies. The tax

exemptions claimed by petitioners cannot be granted. The sections of the 1977 NIRC which petitioners cited are inapplicable,

because these were not yet in effect when the income was earned and when the subject information return for the year ending 1975

was filed. Petitioners' claim that Munich is tax-exempt based on the RP-West German Tax Treaty is likewise unpersuasive, because

the Internal Revenue Commissioner assessed the pool for corporate taxes on the basis of the information return it had submitted for

the year ending 1975, a taxable year when said treaty was not yet in effect. Petitioners likewise failed to comply with the requirement

of Section 333 of the NIRC for the suspension of the prescriptive period. The Resolutions of the Court of Appeals are affirmed.

SYLLABUS

1. REMEDIAL LAW; EVIDENCE; RULING OF THE COMMISSION OF INTERNAL REVENUE IS ACCORDED WEIGHT AND EVEN

FINALITY IN THE ABSENCE OF SHOWING THAT IT IS PATENTLY WRONG. — The opinion or ruling of the Commission of

Internal Revenue, the agency tasked with the enforcement of tax laws, is accorded much weight and even finality, when there is no

showing that it is patently wrong, particularly in this case where the findings and conclusions of the internal revenue commissioner

were subsequently affirmed by the CTA, a specialized body created for the exclusive purpose of reviewing tax cases, and the Court

of Appeals. Indeed, "[I]t has been the long standing policy and practice of this Court to respect the conclusions of quasi-judicial

agencies, such as the Court of Tax Appeals which, by the nature of its functions, is dedicated exclusively to the study and

8/18/2019 Pat Assigned 1

http://slidepdf.com/reader/full/pat-assigned-1 3/54

consideration of tax problems and has necessarily developed an expertise on the subject, unless there has been an abuse or

improvident exercise of its authority."TIAEac

2. CIVIL LAW; PARTNERSHIP; REQUISITES. — Article 1767 of the Civil Code recognizes the creation of a contract of partnership

when "two or more persons bind themselves to contribute money, property, or industry to a common fund, with the intention of

dividing the profits among themselves." Its requisites are: "(1) mutual contribution to a common stock, and (2) a joint interest in the

profits." In other words, a partnership is formed when persons contract "to devote to a common purpose either money, property, or

labor with the intention of dividing the profits between themselves." Meanwhile, an association implies associates who enter into a

"joint enterprise . . . for the transaction of business."

3. ID.; ID.; INSURANCE POOL IN CASE AT BAR DEEMED PARTNERSHIP OR ASSOCIATION TAXABLE AS A CORPORATION

UNDER SECTION 24 OF THE NIRC. — In the case before us, the ceding companies entered into a Pool Agreement or an

association that would handle all the insurance businesses covered under their quota-share reinsurance treaty and surplus

reinsurance treaty with Munich. The following unmistakably indicates a partnership or an association covered by Section 24 of

the NIRC: (1) The pool has a common fund, consisting of money and other valuables that are deposited in the name and credit of

the pool. This common fund pays for the administration and operation expenses of the pool. (2) The pool functions through an

executive board, which resembles the board of directors of a corporation, composed of one representative for each of the ceding

companies. (3) True, the pool itself is not a reinsurer and does not issue any insurance policy; however, its work is indispensable,

beneficial and economically useful to the business of the ceding companies and Munich, because without it they would not have

received their premiums. The ceding companies share "in the business ceded to the pool" and in the "expenses" according to a

"Rules of Distribution" annexed to the Pool Agreement. Profit motive or business is, therefore, the primordial reason for the pool's

formation.

4. TAXATION; NIRC; SECTION 24 THEREOF, UNREGISTERED PARTNERSHIPS AND ASSOCIATIONS ARE CONSIDERED AS

CORPORATIONS FOR TAX PURPOSES. — This Court rules that the Court of Appeals, in affirming the CTA which had previously

sustained the internal revenue commissioner, committed no reversible error. Section 24 of the NIRC, as worded in the year ending

1975, provides: "SEC. 24. Rate of tax on corporations. — (a) Tax on domestic corporations. — A tax is hereby imposed upon the

taxable net income received during each taxable year from all sources by every corporation organized in, or existing under the laws

of the Philippines, no matter how created or organized, but not including duly registered general co-partnership (compañias

colectivas), general professional partnerships, private educational institutions, and building and loan associations . . . ." Ineludibly,

the Philippine legislature included in the concept of corporations those entities that resembled them such as unregistered

partnerships and associations. Parenthetically, the NLRC's inclusion of such entities in the tax on corporations was made even

clearer by the Tax Reform Act of 1997, which amended the Tax Code. The Court of Appeals did not err in applying Evangelista,

which involved a partnership that engaged in a series of transactions spanning more than ten years, as in the case before us.

8/18/2019 Pat Assigned 1

http://slidepdf.com/reader/full/pat-assigned-1 4/54

5. ID.; DOUBLE TAXATION; DEFINED; NO DOUBLE TAXATION IN CASE AT BAR. — Double taxation means taxing the same

property twice when it should be taxed only once. That is, ". . . taxing the same person twice by the same jurisdiction for the same

thing." In the instant case, the pool is a taxable entity distinct from the individual corporate entities of the ceding companies. The tax

on its income is obviously different from the tax on the dividends received by the said companies. Clearly, there is no double taxation

here.

6. ID.; TAX EXEMPTION; GRANT THEREOF NOT JUSTIFIED IN CASE AT BAR; REASONS. — The tax exemptions claimed by

petitioners cannot be granted, since their entitlement thereto remains unproven and unsubstantiated. It is axiomatic in the law of

taxation that taxes are the lifeblood of the nation. Hence, "exemptions therefrom are highly disfavored in law and he who claims tax

exemption must be able to justify his claim or right." Petitioners have failed to discharge this burden of proof. The sections of the

1977 NIRC which they cite are inapplicable, because these were not yet in effect when the income was earned and when the subject

information return for the year ending 1975 was filed. Referring to the 1975 version of the counterpart sections of the NIRC, the

Court still cannot justify the exemptions claimed. Section 255 provides that no tax shall ". . . be paid upon reinsurance by any

company that has already paid the tax . . . ." This cannot be applied to the present case because, as previously discussed, the pool

is a taxable entity distinct from the ceding companies; therefore, the latter cannot individually claim the income tax paid by the former

as their own.EDSAac

7. ID.; ID.; CANNOT BE CLAIMED BY NON-RESIDENT FOREIGN INSURANCE CORPORATION IN CASE AT BAR; REASONS;

TAX EXEMPTION CONSTRUEDSTRICTISSIMI JURIS. — Section 24 (b) (1) pertains to tax on foreign corporations; hence, it

cannot be claimed by the ceding companies which are domestic corporations. Nor can Munich, a foreign corporation, be granted

exemption based solely on this provision of the Tax Code because the same subsection specifically taxes dividends, the type of

remittances forwarded to it by the pool. Although not a signatory to the Pool Agreement, Munich is patently an associate of the

ceding companies in the entity formed, pursuant to their reinsurance treaties which required the creation of said pool. Under its pool

arrangement with the ceding companies, Munich shared in their income and loss. This is manifest from a reading of Articles 3 and

10 of the Quota-Share Reinsurance Treaty and Articles 3 and 10 of the Surplus Reinsurance Treaty. The foregoing interpretation of

Section 24 (b) (1) is in line with the doctrine that a tax exemption must be construedstrictissimi juris, and the statutory exemption

claimed must be expressed in a language too plain to be mistaken.

8. ID.; ID.; BASED ON TAX TREATY NOT APPLICABLE IN CASE AT BAR; REASON. — The petitioners' claim that Munich is tax-

exempt based on the RP-West German Tax Treaty is likewise unpersuasive, because the internal revenue commissioner assessed

the pool for corporate taxes on the basis of the information return it had submitted for the year ending 1975, a taxable year when

8/18/2019 Pat Assigned 1

http://slidepdf.com/reader/full/pat-assigned-1 5/54

said treaty was not yet in effect. Although petitioners omitted in their pleadings the date of effectivity of the treaty, the Court takes

judicial notice that it took effect only later, on December 14, 1984.

9. ID.; ASSESSMENT AND COLLECTION OF TAX; PRESCRIPTION; CHANGE IN THE ADDRESS OF THE TAXPAYER WILL NOT

TOLL THE RUNNING OF THE PRESCRIPTIVE PERIOD UNLESS THE COMMISSIONER OF INTERNAL REVENUE HAS BEEN

INFORMED OF SAID CHANGE. — The CA and the CTA categorically found that the prescriptive period was tolled under then

Section 333 of the NIRC, because "the taxpayer cannot be located at the address given in the information return filed and for which

reason there was delay in sending the assessment." Indeed, whether the government's right to collect and assess the tax has

prescribed involves facts which have been ruled upon by the lower courts. It is axiomatic that in the absence of a clear showing of

palpable error or grave abuse of discretion, as in this case, this Court must not overturn the factual findings of the CA and the CTA.

Furthermore, petitioners admitted in their Motion for Reconsideration before the Court of Appeals that the pool changed its address,

for they stated that the pool's information return filed in 1980 indicated therein its "present address." The Court finds that this falls

short of the requirement of Section 333 of the NIRC for the suspension of the prescriptive period. The law clearly states that the said

period will be suspended only "if the taxpayer informs the Commissioner of Internal Revenue of any change in the address."

D E C I S I O N

PANGANIBAN, Jp:

Pursuant to "reinsurance treaties," a number of local insurance firms formed themselves into a "pool" in order to facilitate the

handling of business contracted with a nonresident foreign reinsurance company. May the "clearing house" or "insurance pool" so

formed be deemed a partnership or an association that is taxable as a corporation under the National Internal Revenue

Code (NIRC)? Should the pool's remittances to the member companies and to the said foreign firm be taxable as dividends? Under

the facts of this case, has the government's right to assess and collect said tax prescribed? cdasia

The Case

These are the main questions raised in the Petition for Review onCertiorari before us, assailing the October 11, 1993 Decision 1 of

the Court of Appeals 2 in CA-GR SP 29502, which dismissed petitioners' appeal of the October 19, 1992 Decision 3 of the Court of

Tax Appeals 4 (CTA) which had previously sustained petitioners' liability for deficiency income tax, interest and withholding tax. The

Court of Appeals ruled:

"WHEREFORE, the petition is DISMISSED, with costs against petitioners." 5

8/18/2019 Pat Assigned 1

http://slidepdf.com/reader/full/pat-assigned-1 6/54

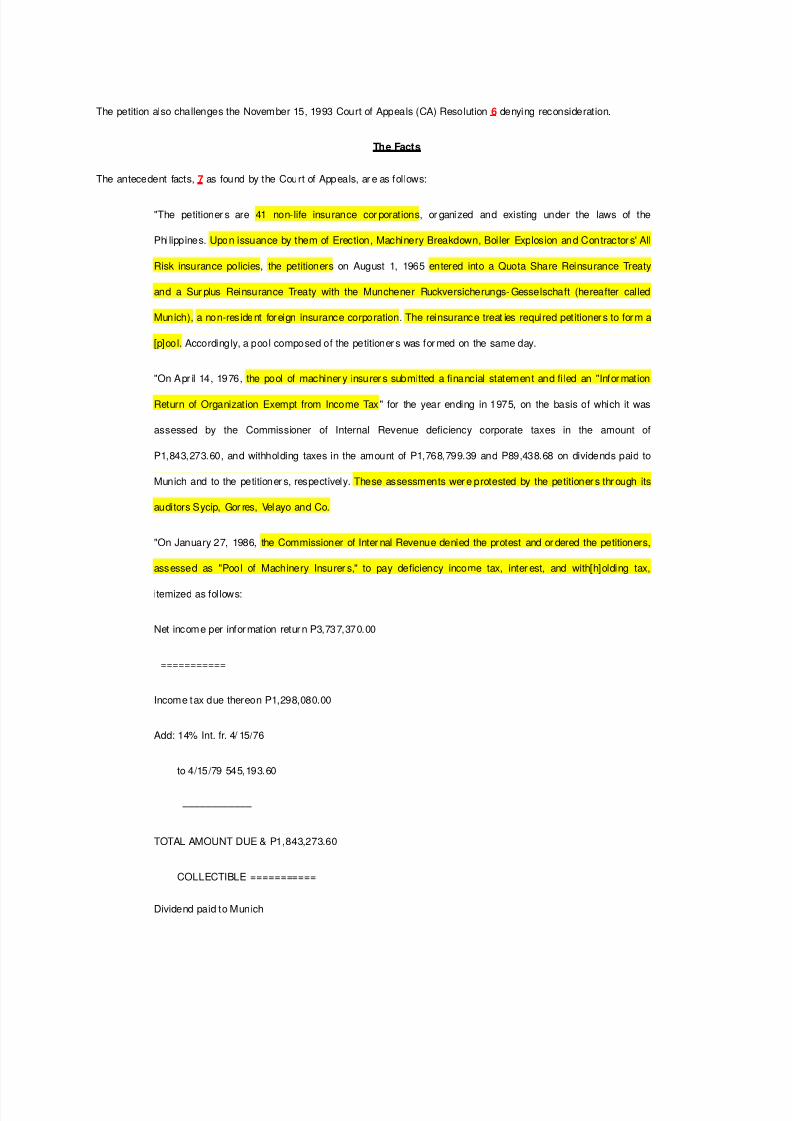

The petition also challenges the November 15, 1993 Court of Appeals (CA) Resolution 6 denying reconsideration.

The Facts

The antecedent facts, 7 as found by the Court of Appeals, are as follows:

"The petitioners are 41 non-life insurance corporations, organized and existing under the laws of the

Philippines. Upon issuance by them of Erection, Machinery Breakdown, Boiler Explosion and Contractors' All

Risk insurance policies, the petitioners on August 1, 1965 entered into a Quota Share Reinsurance Treaty

and a Surplus Reinsurance Treaty with the Munchener Ruckversicherungs-Gesselschaft (hereafter called

Munich), a non-resident foreign insurance corporation. The reinsurance treaties required petitioners to form a

[p]ool. Accordingly, a pool composed of the petitioners was formed on the same day.

"On April 14, 1976, the pool of machinery insurers submitted a financial statement and filed an "Information

Return of Organization Exempt from Income Tax" for the year ending in 1975, on the basis of which it was

assessed by the Commissioner of Internal Revenue deficiency corporate taxes in the amount of

P1,843,273.60, and withholding taxes in the amount of P1,768,799.39 and P89,438.68 on dividends paid to

Munich and to the petitioners, respectively. These assessments were protested by the petitioners through its

auditors Sycip, Gorres, Velayo and Co.

"On January 27, 1986, the Commissioner of Internal Revenue denied the protest and ordered the petitioners,

assessed as "Pool of Machinery Insurers," to pay deficiency income tax, interest, and with[h]olding tax,

itemized as follows:

Net income per information return P3,737,370.00

===========

Income tax due thereon P1,298,080.00

Add: 14% Int. fr. 4/15/76

to 4/15/79 545,193.60

––––––––––––

TOTAL AMOUNT DUE & P1,843,273.60

COLLECTIBLE ===========

Dividend paid to Munich

8/18/2019 Pat Assigned 1

http://slidepdf.com/reader/full/pat-assigned-1 7/54

Reinsurance Company P3,728,412.00

===========

35% withholding tax at source due thereon P1,304,944.20

Add: 25% surcharge 326,236.05

14% interest from

1/25/76 to 1/25/79 137,019.14

Compromise

penalty-non-filing of return 300.00

late payment 300.00

––––––––––––

TOTAL AMOUNT DUE & P1,768,799.39

COLLECTIBLE ===========

Dividend paid to Pool Members P655,636.00

===========

10% withholding tax at

source due thereon P65,563.60

Add: 25% surcharge 16,390.90

14% interest from

1/25/76 to 1/25/79 6,884.18

Compromise

penalty-non-filing of return 300.00

late payment 300.00

––––––––––––

TOTAL AMOUNT DUE & P89,438.68

8/18/2019 Pat Assigned 1

http://slidepdf.com/reader/full/pat-assigned-1 8/54

COLLECTIBLE ==========" 8

The CA ruled in the main that the pool of machinery insurers was a partnership taxable as a corporation, and that the latter's

collection of premiums on behalf of its members, the ceding companies, was taxable income. It added that prescription did not bar

the Bureau of Internal Revenue (BIR) from collecting the taxes due, because "the taxpayer cannot be located at the address given in

the information return filed." Hence, this Petition for Review before us. 9

The Issues

Before this Court, petitioners raise the following issues:

"1. Whether or not the Clearing House, acting as a mere agent and performing strictly administrative

functions, and which did not insure or assume any risk in its own name, was a partnership or association

subject to tax as a corporation;

"2. Whether or not the remittances to petitioners and MUNICHRE of their respective shares of reinsurance

premiums, pertaining to their individual and separate contracts of reinsurance, were "dividends" subject to

tax; and

"3. Whether or not the respondent Commissioner's right to assess the Clearing House had already

prescribed." 10

The Court's Ruling

The petition is devoid of merit. We sustain the ruling of the Court of Appeals that the pool is taxable as a corporation, and that the

government's right to assess and collect the taxes had not prescribed.

First Issue:

Pool Taxable as a Corporation

Petitioners contend that the Court of Appeals erred in finding that the pool or clearing house was an informal partnership, which was

taxable as a corporation under the NIRC. They point out that the reinsurance policies were written by them "individually and

separately," and that their liability was limited to the extent of their allocated share in the original risks thus reinsured.11 Hence, the

pool did not act or earn income as a reinsurer. 12 Its role was limited to its principal function of "allocating and distributing the risk(s)

arising from the original insurance among the signatories to the treaty or the members of the pool based on their ability to absorb the

risk(s) ceded[;] as well as the performance of incidental functions, such as records, maintenance, collection and custody of funds,

etc."13

8/18/2019 Pat Assigned 1

http://slidepdf.com/reader/full/pat-assigned-1 9/54

Petitioners belie the existence of a partnership in this case, because (1) they, the reinsurers, did not share the same risk or solidary

liability; 14 (2) there was no common fund; 15 (3) the executive board of the pool did not exercise control and management of its

funds, unlike the board of directors of a corporation; 16 and (4) the pool or clearing house "was not and could not possibly have

engaged in the business of reinsurance from which it could have derived income for itself."17

The Court is not persuaded. The opinion or ruling of the Commission of Internal Revenue, the agency tasked with the enforcement

of tax laws, is accorded much weight and even finality, when there is no showing that it is patently wrong, 18 particularly in this case

where the findings and conclusions of the internal revenue commissioner were subsequently affirmed by the CTA, a specialized

body created for the exclusive purpose of reviewing tax cases, and the Court of Appeals.19 Indeed,

"[I]t has been the long standing policy and practice of this Court to respect the conclusions of quasi-judicial

agencies, such as the Court of Tax Appeals which, by the nature of its functions, is dedicated exclusively to

the study and consideration of tax problems and has necessarily developed an expertise on the subject,

unless there has been an abuse or improvident exercise of its authority."20

This Court rules that the Court of Appeals, in affirming the CTA which had previously sustained the internal revenue commissioner,

committed no reversible error.Section 24 of the NIRC, as worded in the year ending 1975, provides:

"SEC. 24.Rate of tax on corporations. — (a)Tax on domestic corporations. — A tax is hereby imposed upon

the taxable net income received during each taxable year from all sources by every corporation organized in,

or existing under the laws of the Philippines, no matter how created or organized, but not including duly

registered general co-partnership (compañias colectivas), general professional partnerships, private

educational institutions, and building and loan associations . . . ."

Ineludibly, the Philippine legislature included in the concept of corporations those entities that resembled them such as unregistered

partnerships and associations. Parenthetically, the NLRC's inclusion of such entities in the tax on corporations was made even

clearer by the Tax Reform Act of 1997, 21 which amended the Tax Code.Pertinent provisions of the new law read as follows:

"SEC. 27.Rates of Income Tax on Domestic Corporations. —

(A)In General. — Except as otherwise provided in this Code, an income tax of thirty-five percent (35%) is

hereby imposed upon the taxable income derived during each taxable year from all sources within and

without the Philippines by every corporation, as defined in Section 22 (B) of this Code, and taxable under this

Title as a corporation . . . ."

"SEC. 22.Definition. — When used in this Title:

8/18/2019 Pat Assigned 1

http://slidepdf.com/reader/full/pat-assigned-1 10/54

xxx xxx xxx

(B) The term 'corporation' shall include partnerships, no matter how created or organized, joint-stock

companies, joint accounts (cuentas en participacion), associations, or insurance companies, but does not

include general professional partnerships [or] a joint venture or consortium formed for the purpose of

undertaking construction projects or engaging in petroleum, coal, geothermal and other energy operations

pursuant to an operating or consortium agreement under a service contract without the Government.

'General professional partnerships' are partnerships formed by persons for the sole purpose of exercising

their common profession, no part of the income of which is derived from engaging in any trade or

business.LLphil

xxx xxx xxx."

Thus, the Court inEvangelista v. Collector of Internal Revenue 22 held that Section 24 covered these unregistered partnerships and

even associations or joint accounts, which had no legal personalities apart from their individual members.23 The Court of Appeals

astutely appliedEvangelista: 24

". . . Accordingly, a pool of individual real property owners dealing in real estate business was considered a

corporation for purposes of the tax in Sec. 24 of the Tax Code inEvangelista v. Collector of Internal

Revenue,supra. The Supreme Court said:

'The term 'partnership' includes a syndicate, group, pool, joint venture or other unincorporated

organization, through or by means of which any business, financial operation, or venture is carried

on . . . (8 Merten's Law of Federal Income Taxation, p. 562 Note 63)'"

Article 1767 of the Civil Code recognizes the creation of a contract of partnership when "two or more persons bind themselves to

contribute money, property, or industry to a common fund, with the intention of dividing the profits among themselves." 25 Its

requisites are: "(1) mutual contribution to a common stock, and (2) a joint interest in the profits."26 In other words, a partnership is

formed when persons contract "to devote to a common purpose either money, property, or labor with the intention of dividing the

profits between themselves." 27 Meanwhile, an association implies associates who enter into a "joint enterprise . . . for the

transaction of business." 28

In the case before us, the ceding companies entered into a Pool Agreement 29 or an association 30 that would handle all the

insurance businesses covered under their quota-share reinsurance treaty 31 and surplus reinsurance treaty32 with Munich. The

following unmistakably indicates a partnership or an association covered by Section 24 of the NIRC:

8/18/2019 Pat Assigned 1

http://slidepdf.com/reader/full/pat-assigned-1 11/54

(1) The pool has a common fund, consisting of money and other valuables that are deposited in the name and credit of the

pool. 33 This common fund pays for the administration and operation expenses of the pool. 34

(2) The pool functions through an executive board, which resembles the board of directors of a corporation, composed of one

representative for each of the ceding companies.35

(3) True, the pool itself is not a reinsurer and does not issue any insurance policy; however, its work is indispensable, beneficial and

economically useful to the business of the ceding companies and Munich, because without it they would not have received their

premiums. The ceding companies share "in the business ceded to the pool" and in the "expenses" according to a "Rules of

Distribution" annexed to the Pool Agreement.36 Profit motive or business is, therefore, the primordial reason for the pool's

formation. As aptly found by the CTA:

". . . The fact that the pool does not retain any profit or income does not obliterate an antecedent fact, that of

the pool being used in the transaction of business for profit. It is apparent, and petitioners admit, that their

association or coaction was indispensable [to] the transaction of the business. . . If together they have

conducted business, profit must have been the object as, indeed, profit was earned. Though the profit was

apportioned among the members, this is only a matter of consequence, as it implies that profit actually

resulted."37

The petitioners' reliance onPascual v. Commissioner 38 is misplaced, because the facts obtaining therein are not on all fours with

the present case. InPascual, there was no unregistered partnership, but merely a co-ownership which took up only two isolated

transactions. 39 The Court of Appeals did not err in applyingEvangelista, which involved a partnership that engaged in a series of

transactions spanning more than ten years, as in the case before us.

Second Issues:

Pool's Remittances Are Taxable

Petitioners further contend that the remittances of the pool to the ceding companies and Munich are not dividends subject to tax.

They insist that taxing such remittances contravene Sections 24 (b) (I) and 263 of the 1977 NIRC and "would be tantamount to an

illegal double taxation, as it would result in taxing the same premium income twice in the hands of the same taxpayer."40 Moreover,

petitioners argue that since Munich was not a signatory to the Pool Agreement, the remittances it received from the pool cannot be

deemed dividends. 41 They add that even if such remittances were treated as dividends, they would have been exempt under the

previously mentioned sections of the 1977 NIRC, 42 as well as Article 7 of paragraph 143 and Article 5 of paragraph 544 of the

RP-West German Tax Treaty. 45

8/18/2019 Pat Assigned 1

http://slidepdf.com/reader/full/pat-assigned-1 12/54

Petitioners are clutching at straws. Double taxation means taxing the same property twice when it should be taxed only once. That

is, ". . . taxing the same person twice by the same jurisdiction for the same thing." 46 In the instant case, the pool is a taxable entity

distinct from the individual corporate entities of the ceding companies. The tax on itsincome is obviously different from the tax on

thedividends received by the said companies. Clearly, there is no double taxation here.

The tax exemptions claimed by petitioners cannot be granted, since their entitlement thereto remains unproven and unsubstantiated.

It is axiomatic in the law of taxation that taxes are the lifeblood of the nation. Hence, "exemptions therefrom are highly disfavored in

law and he who claims tax exemption must be able to justify his claim or right." 47 Petitioners have failed to discharge this burden of

proof. The sections of the 1977 NIRC which they cite are inapplicable, because these were not yet in effect when the income was

earned and when the subject information return for the year ending 1975 was filed.

Referring to the 1975 version of the counterpart sections of the NIRC, the Court still cannot justify the exemptions claimed. Section

255 provides that no tax shall ". . . be paid upon reinsurance by any company that has already paid the tax . . . ." This cannot be

applied to the present case because, as previously discussed, the pool is a taxable entity distinct from the ceding companies;

therefore, the latter cannot individually claim the income tax paid by the former as their own.

On the other hand, Section 24 (b) (1) 48 pertains to tax on foreign corporations; hence, it cannot be claimed by the ceding

companies which are domestic corporations. Nor can Munich, a foreign corporation, be granted exemption based solely on this

provision of the Tax Code, because the same subsection specifically taxesdividends, the type of remittances forwarded to it by the

pool. Although not a signatory to the Pool Agreement, Munich is patently an associate of the ceding companies in the entity formed,

pursuant to their reinsurance treaties which required the creation of said pool.

Under its pool arrangement with the ceding companies, Munich shared in their income and loss. This is manifest from a reading

of Articles 3 49 and 1050 of the Quota-Share Reinsurance Treaty and Articles 3 51 and 10 52 of the Surplus Reinsurance Treaty.

The foregoing interpretation of Section 24 (b) (1) is in line with the doctrine that a tax exemption must be construedstrictissimi juris,

and the statutory exemption claimed must be expressed in a language too plain to be mistaken.53

Finally, the petitioners' claim that Munich is tax-exempt based on the RP-West German Tax Treaty is likewise unpersuasive, because

the internal revenue commissioner assessed the pool for corporate taxes on the basis of the information return it had submitted for

the year ending 1975, a taxable year when said treaty was not yet in effect. 54 Although petitioners omitted in their pleadings the

date of effectivity of the treaty, the Court takes judicial notice that it took effect only later, on December 14, 1984. 55

Third Issue:

Prescription

8/18/2019 Pat Assigned 1

http://slidepdf.com/reader/full/pat-assigned-1 13/54

Petitioners also argue that the government's right to assess and collect the subject tax had prescribed. They claim that the subject

information return was filed by the pool on April 14, 1976. On the basis of this return, the BIR telephoned petitioners on November

11, 1981, to give them notice of its letter of assessment dated March 27, 1981. Thus, the petitioners contend that the five-year

statute of limitations then provided in the NIRC had already lapsed, and that the internal revenue commissioner was already barred

by prescription from making an assessment. 56

We cannot sustain the petitioners. The CA and the CTA categorically found that the prescriptive period was tolled under then Section

333 of the NIRC,57 because " the taxpayer cannot be located at the address given in the information return filed and for which

reason there was delay in sending the assessment." 58 Indeed, whether the government's right to collect and assess the tax has

prescribed involves facts which have been ruled upon by the lower courts. It is axiomatic that in the absence of a clear showing of

palpable error or grave abuse of discretion, as in this case, this Court must not overturn the factual findings of the CA and the CTA.

Furthermore, petitioners admitted in their Motion for Reconsideration before the Court of Appeals that the pool changed its address,

for they stated that the pool's information return filed in 1980 indicated therein its "present address." The Court finds that this falls

short of the requirement of Section 333 of the NIRC for the suspension of the prescriptive period. The law clearly states that the said

period will be suspended only "if the taxpayer informs the Commissioner of Internal Revenue of any change in the address."

WHEREFORE, the petition is DENIED. The Resolutions of the Court of Appeals dated October 11, 1993 and November 15, 1993

are hereby AFFIRMED. Costs against petitioners.cdasia

SO ORDERED.

||| (Afisco Insurance Corp. v. Court of Appeals, G.R. No. 112675, [January 25, 1999], 361 PHIL 671-691)

8/18/2019 Pat Assigned 1

http://slidepdf.com/reader/full/pat-assigned-1 14/54

[G.R. No. 45425. April 29, 1939.]

JOSE GATCHALIAN, ET AL., plaintiffs-appellants,vs. THE COLLECTOR OF INTERNAL

REVENUE, defendant-appellee.

Guillermo B. Reyesfor appellants.

Solicitor-General Tuasonfor appellee.

SYLLABUS

1. PARTNERSHIP OF A CIVIL NATURE; COMMUNITY OF PROPERTY; SWEEPSTAKES; INCOME TAX. —

According to the stipulated facts the plaintiffs organized a partnership of a civil nature because each of them put up money to

buy a sweepstakes ticket for the sole purpose of dividing equally the prize which they may win, as they did in fact in the amount

of P60,000 (article 166C, Civil Code). The partnership was not only formed, but upon the organization thereon and the winning

of the prize, J. G. personally appeared in the office of the Philippine Charity Sweepstakes, in his capacity as co-partner, as

such collected the prize, the office issued the check for P60,000 in favor of J. G. and company, and the said partner, in the

same capacity, collected the check. All these circumstances repel the idea that the plaintiffs organized and formed a community

of property only.

2. ID.; ID.; ID.; ID. — Having organized and constituted a partnership of a civil nature, the said entity is the one

bound to pay the income tax which the defendant collected under the aforesaid section 10 (a) of Act No. 2833, as amended by

section 2 of Act No. 3761. There is no merit in plaintiffs' contention that the tax should be prorated among them and paid

individually, resulting in their exemption from the tax.

D E C I S I O N

IMPERIAL, Jp:

The plaintiff brought this action to recover from the defendant Collector of Internal Revenue the sum of P1,863.44,

with legal interest thereon, which they paid under protest by way of income tax. They appealed from the decision rendered in

8/18/2019 Pat Assigned 1

http://slidepdf.com/reader/full/pat-assigned-1 15/54

the case on October 23, 1936 by the Court of First Instance of the City of Manila, which dismissed the action with the costs

against them.

The case was submitted for decision upon the following stipulation of facts:

"Come now the parties to the above-mentioned case, through their respective undersigned

attorneys, and hereby agree to respectfully submit to this Honorable Court the case upon the following

statement of facts:

"1. That plaintiffs are all residents of the municipality of Pulilan, Bulacan, and that defendant is the

Collector of Internal Revenue of the Philippines;

"2. That prior to December 15, 1934 plaintiffs, in order to enable them to purchase one

sweepstakes ticket valued at two pesos (P2), subscribed and paid therefor the amounts as follows:

1. Jose Gatchalian P0.18

2. Gregoria Cristobal .18

3. Saturnina Silva .08

4. Guillermo Tapia .13

5. Jesus Legaspi .15

6. Jose Silva .07

7. Tomasa Mercado .08

8. Julio Gatchalian .18

9. Emiliana Santiago .18

10. Maria C. Legaspi .16

11. Francisco Cabral .13

12. Gonzalo Javier .14

13. Maria Santiago .17

14. Buenaventura Guzman .13

15. Mariano Santos .14

——

Total 2.00

8/18/2019 Pat Assigned 1

http://slidepdf.com/reader/full/pat-assigned-1 16/54

"3. That immediately thereafter but prior to December 16, 1934, plaintiffs purchased, in the ordinary

course of business, from one of the duly authorized agents of the National Charity Sweepstakes Office one

ticket bearing No. 178637 for the sum of two pesos (P2) and that the said ticket was registered in the name of

Jose Gatchalian and Company;

"4. That as a result of the drawing of the sweepstakes on December 15, 1934, the above-

mentioned ticket bearing No. 178637 won one of the third prizes in the amount of P50,000 and that the

corresponding check covering the above-mentioned prize of P50,000 was drawn by the National Charity

Sweepstakes Office in favor of Jose Gatchalian & Company against the Philippine National Bank, which

check was cashed during the latter part of December, 1934 by Jose Gatchalian & Company;

"5 That on December 29, 1934, Jose Gatchalian was required by income tax examiner Alfredo

David to file the corresponding income tax return covering the prize won by Jose Gatchalian & Company and

that on December 29, 1934, the said return was signed by Jose Gatchalian, a copy of which return is

enclosed as Exhibit A and made a part hereof;

"6. That on January 8, 1935, the defendant made an assessment against Jose Gatchalian &

Company requesting the payment of the sum of P1,499.94 to the deputy provincial treasurer of Pulilan,

Bulacan, giving to said Jose Gatchalian & Company until January 20, 1935 within which to pay the said

amount of P1,499.94, a copy of which letter marked Exhibit B is inclosed and made a part hereof;

"7. That on January 20, 1935, the plaintiffs, through their attorney, sent to defendant a reply, a copy

of which marked Exhibit C is attached and made a part hereof, requesting exemption from the payment of the

income tax to which reply there were enclosed fifteen (15) separate individual income tax returns filed

separately by each one of the plaintiffs, copies of which returns are attached and marked Exhibits D-1 to D-

15, respectively, in order of their names listed in the caption of this case and made parts hereof; a statement

of sale signed by Jose Gatchalian showing the amounts put up by each of the plaintiffs to cover up the cost

price of P2 of said ticket, copy of which statement is attached and marked as Exhibit E and made a part

hereof; and a copy of the affidavit signed by Jose Gatchalian dated December 29, 1934 is attached and

marked Exhibit F and made part hereof;

"8. That the defendant in his letter dated January 28, 1935, a copy of which marked Exhibit G is

enclosed, denied plaintiffs' request of January 20, 1935, for exemption from the payment of tax and reiterated

his demand for the payment of the sum of P1,499.94 as income tax and gave plaintiffs until February 10,

1935 within which to pay the said tax;

8/18/2019 Pat Assigned 1

http://slidepdf.com/reader/full/pat-assigned-1 17/54

"9. That in view of the failure of the plaintiffs to pay the amount of tax demanded by the defendant,

notwithstanding subsequent demand made by defendant upon the plaintiffs through their attorney on March

23, 1935, a copy of which marked Exhibit H is enclosed, defendant on May 13, 1935 issued a warrant of

distraint and levy against the property of the plaintiffs, a copy of which warrant marked Exhibit I is enclosed

and made a part hereof;

"10. That to avoid embarrassment arising from the embargo of the property of the plaintiffs, the said

plaintiffs on June 15, 1935, through Gregoria Cristobal, Maria C. Legaspi and Jesus Legaspi, paid under

protest the sum of P601.51 as part of the tax and penalties to the municipal treasurer of Pulilan, Bulacan, as

evidenced by official receipt No. 7454879 which is attached and marked Exhibit J and made a part hereof,

and requested defendant that plaintiffs be allowed to pay under protest the balance of the tax and penalties

by monthly installments;

"11. That plaintiffs' request to pay the balance of the tax and penalties was granted by defendant

subject to the condition that plaintiffs file the usual bond secured by two solvent persons to guarantee prompt

payment of each installments as it becomes due;

"12. That on July 16, 1935, plaintiff filed a bond, a copy of which marked Exhibit K is inclosed and

made a part hereof, to guarantee the payment of the balance of the alleged tax liability by monthly

installments at the rate of P118.70 a month, the first payment under protest to be effected on or before July

31, 1935;

"13. That on July 16, 1935 the said plaintiffs formally protested against the payment of the sum of

P602.51, a copy of which protest is attached and marked Exhibit L but that defendant in his letter dated

August 1, 1936 overruled the protest and denied the request for refund of the plaintiffs;

"14. That, in view of the failure of the plaintiffs to pay the monthly installments in accordance with

the terms and conditions of the bond filed by them, the defendant in his letter dated July 23, 1935, copy of

which is attached and marked Exhibit M, ordered the municipal treasurer of Pulilan, Bulacan to execute within

five days the warrant of distraint and levy issued against the plaintiffs on March 13, 1935;

"15. That in order to avoid annoyance and embarrassment arising from the levy of their property,

the plaintiffs on August 28, 1936, through Jose Gatchalian, Guillermo Tapia, Maria Santiago and Emiliano

Santiago, paid under protest to the municipal treasurer of Pulilan, Bulacan. the sum of P1,260.93

representing the unpaid balance of the income tax and penalties demanded by defendant as evidenced by

income tax receipt No. 35811 which is attached and marked Exhibit N and made a part hereof; and that on

8/18/2019 Pat Assigned 1

http://slidepdf.com/reader/full/pat-assigned-1 18/54

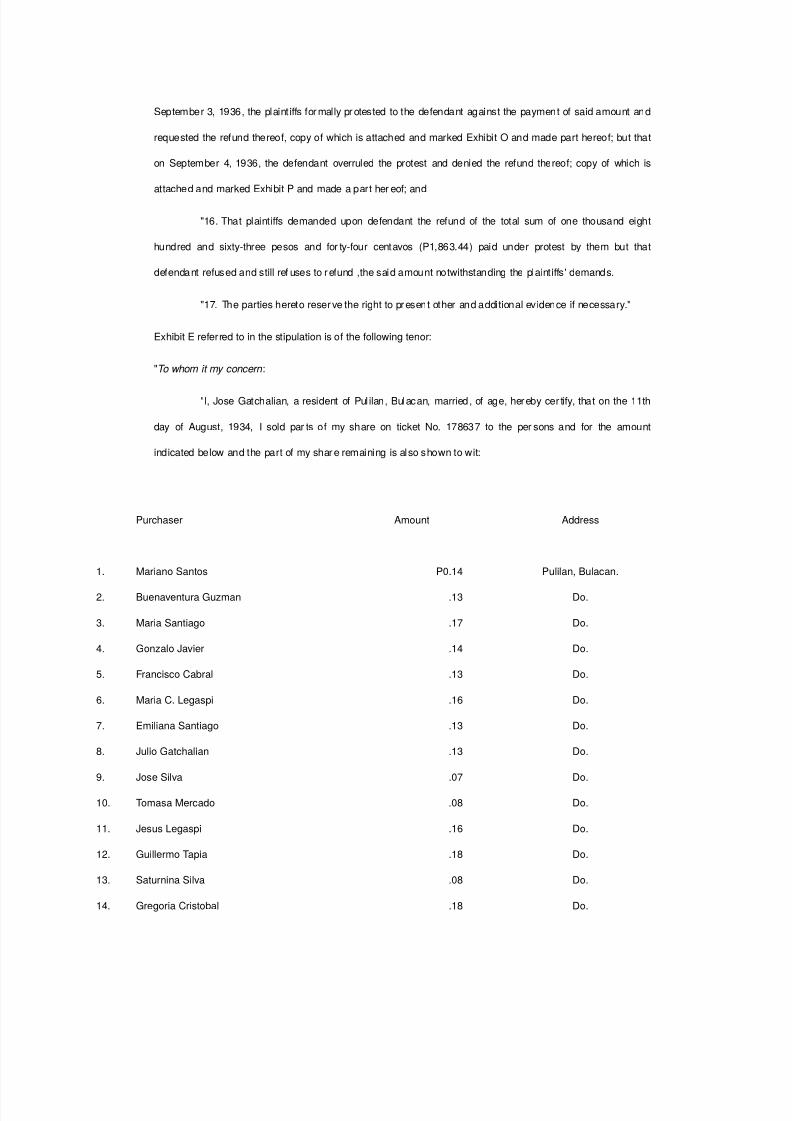

September 3, 1936, the plaintiffs formally protested to the defendant against the payment of said amount and

requested the refund thereof, copy of which is attached and marked Exhibit O and made part hereof; but that

on September 4, 1936, the defendant overruled the protest and denied the refund thereof; copy of which is

attached and marked Exhibit P and made a part hereof; and

"16. That plaintiffs demanded upon defendant the refund of the total sum of one thousand eight

hundred and sixty-three pesos and forty-four centavos (P1,863.44) paid under protest by them but that

defendant refused and still refuses to refund ,the said amount notwithstanding the plaintiffs' demands.

"17. The parties hereto reserve the right to present other and additional evidence if necessary."

Exhibit E referred to in the stipulation is of the following tenor:

"To whom it my concern:

"I, Jose Gatchalian, a resident of Pulilan, Bulacan, married, of age, hereby certify, that on the 11th

day of August, 1934, I sold parts of my share on ticket No. 178637 to the persons and for the amount

indicated below and the part of my share remaining is also shown to wit:

Purchaser Amount Address

1. Mariano Santos P0.14 Pulilan, Bulacan.

2. Buenaventura Guzman .13 Do.

3. Maria Santiago .17 Do.

4. Gonzalo Javier .14 Do.

5. Francisco Cabral .13 Do.

6. Maria C. Legaspi .16 Do.

7. Emiliana Santiago .13 Do.

8. Julio Gatchalian .13 Do.

9. Jose Silva .07 Do.

10. Tomasa Mercado .08 Do.

11. Jesus Legaspi .16 Do.

12. Guillermo Tapia .18 Do.

13. Saturnina Silva .08 Do.

14. Gregoria Cristobal .18 Do.

8/18/2019 Pat Assigned 1

http://slidepdf.com/reader/full/pat-assigned-1 19/54

15. Jose Gatchalian .18 Do.

——

2.00

Total cost of said ticket; and that, therefore, the persons named above are entitled to the parts of whatever

prize that might be won by said ticket.

"Pulilan, Bulacan, P. I.

(Sgd.) "JOSE GATCHALIAN"

And a summary of Exhibits D-1 to D-15 inserted in the bill of exceptions as follows:

"RECAPITULATIONS OF 15 INDIVIDUAL INCOME TAX RETURNS FOR 1934 ALL DATED JANUARY 19,

1935 SUBMITTED TO THE COLLECTOR OF INTERNAL REVENUE.

Exhibit Purchase Price Net

Name No. Price won Expenses prize

1. Jose Gatchalian D-1 P0.18 P4,425 P480 3,945

2. Gregoria Cristobal D-2 .18 4,575 2,000 2,575

3. Saturnina Silva D-3 .08 1,875 360 1,515

4. Guillermo Tapia D-4 .13 3,325 360 2,965

5. Jesus Legaspi by Maria

Cristobal D-5 .15 3,825 720 3,105

6. Jose Silva D-6 .08 1,875 360 1,615

7. Tomasa Mercado D-7 .07 1,875 360 1,515

8. Julio Gatchalian by Bea

triz Guzman D-8 .13 3,150 240 2,910

9. Emiliana Santiago D-9 .13 3,325 360 2,966

10. Maria C. Legaspi D-10 .16 4,100 960 3,140

11. Francisco Cabral D-11 .13 3,325 360 2965

12. Gonzalo Javier D-12 .14 3,325 360 2,965

13. Maria Santiago D-13 .17 4,350 360 3,990

14. Buenaventura Guzman D-14 .13 3,325 360 2,965

8/18/2019 Pat Assigned 1

http://slidepdf.com/reader/full/pat-assigned-1 20/54

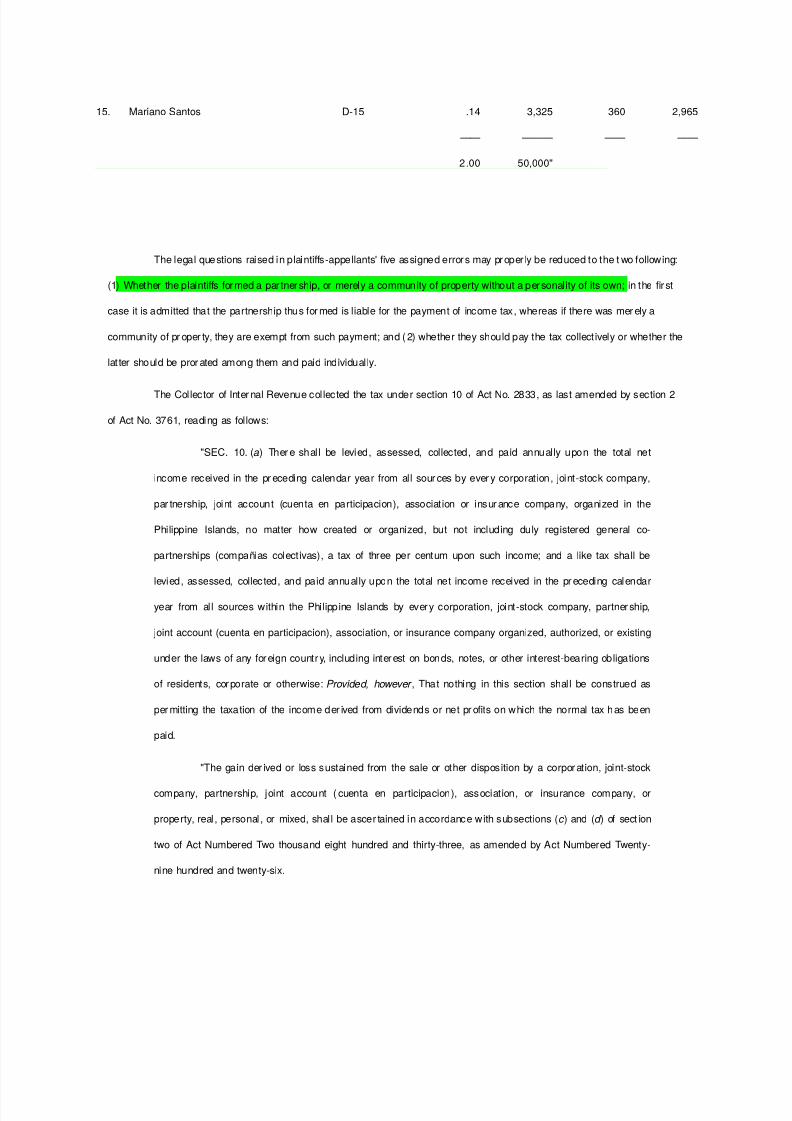

15. Mariano Santos D-15 .14 3,325 360 2,965

—— ——— —— ——

2.00 50,000"

The legal questions raised in plaintiffs-appellants' five assigned errors may properly be reduced to the two following:

(1) Whether the plaintiffs formed a partnership, or merely a community of property without a personality of its own; in the first

case it is admitted that the partnership thus formed is liable for the payment of income tax, whereas if there was merely a

community of property, they are exempt from such payment; and (2) whether they should pay the tax collectively or whether the

latter should be prorated among them and paid individually.

The Collector of Internal Revenue collected the tax under section 10 of Act No. 2833, as last amended by section 2

of Act No. 3761, reading as follows:

"SEC. 10. (a) There shall be levied, assessed, collected, and paid annually upon the total net

income received in the preceding calendar year from all sources by every corporation, joint-stock company,

partnership, joint account (cuenta en participacion), association or insurance company, organized in the

Philippine Islands, no matter how created or organized, but not including duly registered general co-

partnerships (compañias colectivas), a tax of three per centum upon such income; and a like tax shall be

levied, assessed, collected, and paid annually upon the total net income received in the preceding calendar

year from all sources within the Philippine Islands by every corporation, joint-stock company, partnership,

joint account (cuenta en participacion), association, or insurance company organized, authorized, or existing

under the laws of any foreign country, including interest on bonds, notes, or other interest-bearing obligations

of residents, corporate or otherwise:Provided, however, That nothing in this section shall be construed as

permitting the taxation of the income derived from dividends or net profits on which the normal tax has been

paid.

"The gain derived or loss sustained from the sale or other disposition by a corporation, joint-stock

company, partnership, joint account (cuenta en participacion), association, or insurance company, or

property, real, personal, or mixed, shall be ascertained in accordance with subsections (c) and (d) of section

two of Act Numbered Two thousand eight hundred and thirty-three, as amended by Act Numbered Twenty-

nine hundred and twenty-six.

8/18/2019 Pat Assigned 1

http://slidepdf.com/reader/full/pat-assigned-1 21/54

"The foregoing tax rate shall apply to the net income received by every taxable corporation, joint-

stock company, partnership, joint account (cuenta en participacion), associations or insurance company in

the calendar year nineteen hundred and twenty and in each year thereafter."

There is no doubt that if the plaintiffs merely formed a community of property the latter is exempt from the payment of

income tax under the law. But according to the stipulated facts the plaintiffs organized a partnership of a civil nature because

each of them put up money to buy a sweepstakes ticket for the sole purpose of dividing equally the prize which they may win,

as they did in fact in the amount of P50,000 (article 1665, Civil Code). The partnership was not only formed, but upon the

organization thereof and the winning of the prize, Jose Gatchalian personally appeared in the office of the Philippine Charity

Sweepstakes, in his capacity as co-partner, as such collected the prize, the office issued the check for P50,000 in favor of Jose

Gatchalian and company, and the said partner. in the same capacity, collected the said check. All these circumstances repel

the idea that the plaintiffs organized and formed a community of property only.

Having organized and constituted a partnership of a civil nature, the said entity is the one bound to pay the income

tax which the defendant collected under the aforesaid section 10 (a) of Act No. 2833, as amended by section 2 of Act No. 3761.

There is no merit in plaintiffs' contention that the tax should be prorated among them and paid individually, resulting in their

exemption from the tax.

In view of the foregoing, the appealed decision is affirmed, with the costs of this instance to the plaintiff. appellants.

So ordered.

Avanceña, C.J., Villa-Real, Diaz, Laurel, ConcepcionandMoran, JJ., concur.

||| (Gatchalian v. Collector of Internal Revenue, G.R. No. 45425, [April 29, 1939], 67 PHIL 666-674)

8/18/2019 Pat Assigned 1

http://slidepdf.com/reader/full/pat-assigned-1 22/54

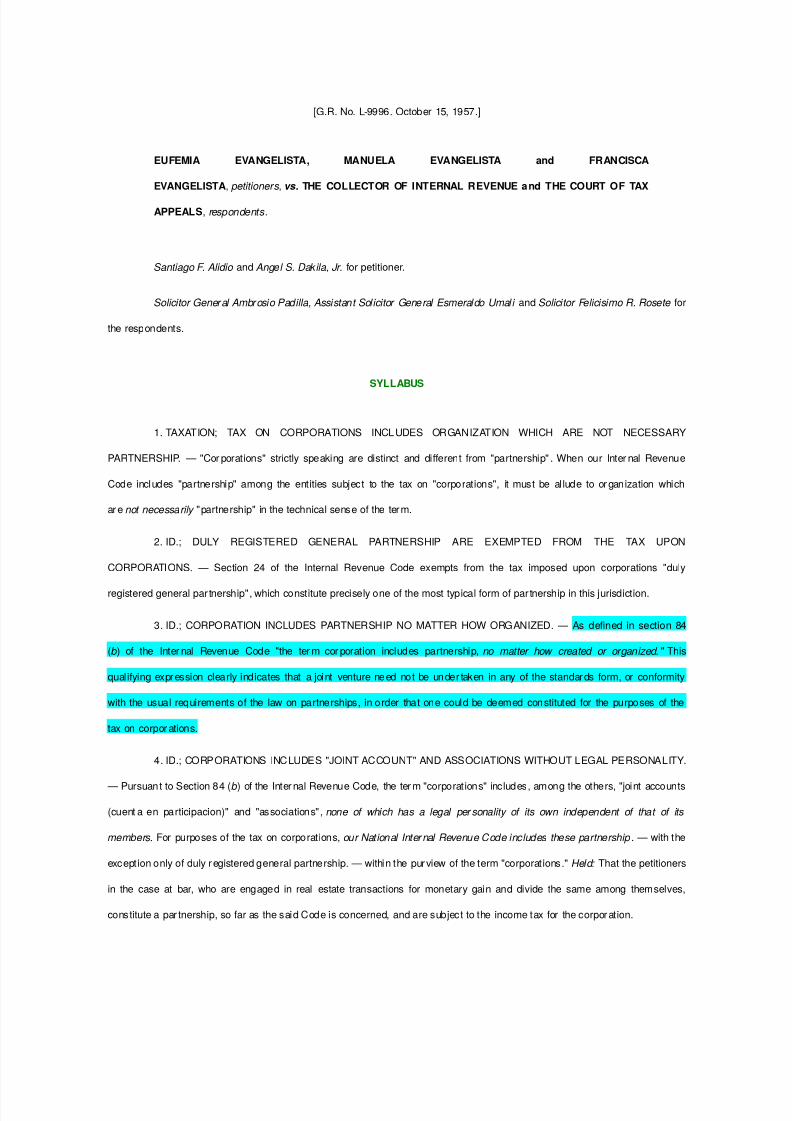

[G.R. No. L-9996. October 15, 1957.]

EUFEMIA EVANGELISTA, MANUELA EVANGELISTA and FRANCISCA

EVANGELISTA, petitioners,vs. THE COLLECTOR OF INTERNAL REVENUE and THE COURT OF TAX

APPEALS, respondents.

Santiago F. Alidioand Angel S. Dakila, Jr. for petitioner.

Solicitor General Ambrosio Padilla, Assistant Solicitor General Esmeraldo Umaliand Solicitor Felicisimo R. Rosete for

the respondents.

SYLLABUS

1. TAXATION; TAX ON CORPORATIONS INCLUDES ORGANIZATION WHICH ARE NOT NECESSARY

PARTNERSHIP. — "Corporations" strictly speaking are distinct and different from "partnership". When our Internal Revenue

Code includes "partnership" among the entities subject to the tax on "corporations", it must be allude to organization which

arenot necessarily "partnership" in the technical sense of the term.

2. ID.; DULY REGISTERED GENERAL PARTNERSHIP ARE EXEMPTED FROM THE TAX UPON

CORPORATIONS. — Section 24 of the Internal Revenue Code exempts from the tax imposed upon corporations "duly

registered general partnership", which constitute precisely one of the most typical form of partnership in this jurisdiction.

3. ID.; CORPORATION INCLUDES PARTNERSHIP NO MATTER HOW ORGANIZED. — As defined in section 84

(b) of the Internal Revenue Code "the term corporation includes partnership,no matter how created or organized." This

qualifying expression clearly indicates that a joint venture need not be undertaken in any of the standards form, or conformity

with the usual requirements of the law on partnerships, in order that one could be deemed constituted for the purposes of the

tax on corporations.

4. ID.; CORPORATIONS INCLUDES "JOINT ACCOUNT" AND ASSOCIATIONS WITHOUT LEGAL PERSONALITY.

— Pursuant to Section 84 (b) of the Internal Revenue Code, the term "corporations" includes, among the others, "joint accounts

(cuenta en participacion)" and "associations", none of which has a legal personality of its own independent of that of its

members. For purposes of the tax on corporations,our National Internal Revenue Code includes these partnership. — with the

exception only of duly registered general partnership. — within the purview of the term "corporations."Held:That the petitioners

in the case at bar, who are engaged in real estate transactions for monetary gain and divide the same among themselves,

constitute a partnership, so far as the said Code is concerned, and are subject to the income tax for the corporation.

8/18/2019 Pat Assigned 1

http://slidepdf.com/reader/full/pat-assigned-1 23/54

5. ID.; CORPORATION; PARTNERSHIP WITHOUT LEGAL PERSONALITY SUBJECT TO RESIDENCE TAX ON

CORPORATION. — The pertinent part of the provision of Section 2 of Commonwealth Act No. 465 which says: "The term

corporation as used in this Act includes joint-stock company, partnership, joint account (cuentas en participacion), association

or insurance company, no matter how created or organized." is analogous to that of Section 24 and 84 (b) of our Internal

Revenue Code which was approved the day immediately after the approval of said Commonwealth Act No. 565. Apparently, the

terms "corporation" and "Partnership" are used both statutes with substantially the same meaning,Held:That the petitioners

are subject to the residence tax corporations.

D E C I S I O N

CONCEPCION, Jp:

This is a petition, filed by Eufemia Evangelista, Manuela Evangelista and Francisca Evangelista, for review of a

decision of the Court of Tax Appeals, the dispositive part of which reads:

"FOR ALL THE FOREGOING, we hold that the petitioners are liable for the income tax, real estate dealer's

tax and the residence tax for the years 1945 to 1949, inclusive, in accordance with the respondent's assessment for

the same in the total amount of P6,878.34, which is hereby affirmed and the petition for review filed by petitioners is

hereby dismissed with costs against petitioners."

It appears from the stipulation submitted by the parties:

"1. That the petitioners borrowed from their father the sum of P59,140.00 which amount together

with their personal monies was used by them for the purpose of buying real properties;

"2. That on February 2, 1943 they bought from Mrs. Josefina Florentino a lot with an area of

3,713.40 sq. m. including improvements thereon for the sum of P100,000.00; this property has an assessed

value of P57,517.00 as of 1948;

"3. That on April 3, 1944 they purchased from Mrs. Josefa Oppus 21 parcels of land with an

aggregate area of 3,718.40 sq. m. including improvements thereon for P18,000.00; this property has an

assessed value of P8,255.00 as of 1948;

"4. That on April 23, 1944 they purchased from the Insular Investments, Inc., a lot of 4,358 sq. m.

including improvements thereon for P108,825.00. This property has an assessed value of P4,983.00 as of

1943;

8/18/2019 Pat Assigned 1

http://slidepdf.com/reader/full/pat-assigned-1 24/54

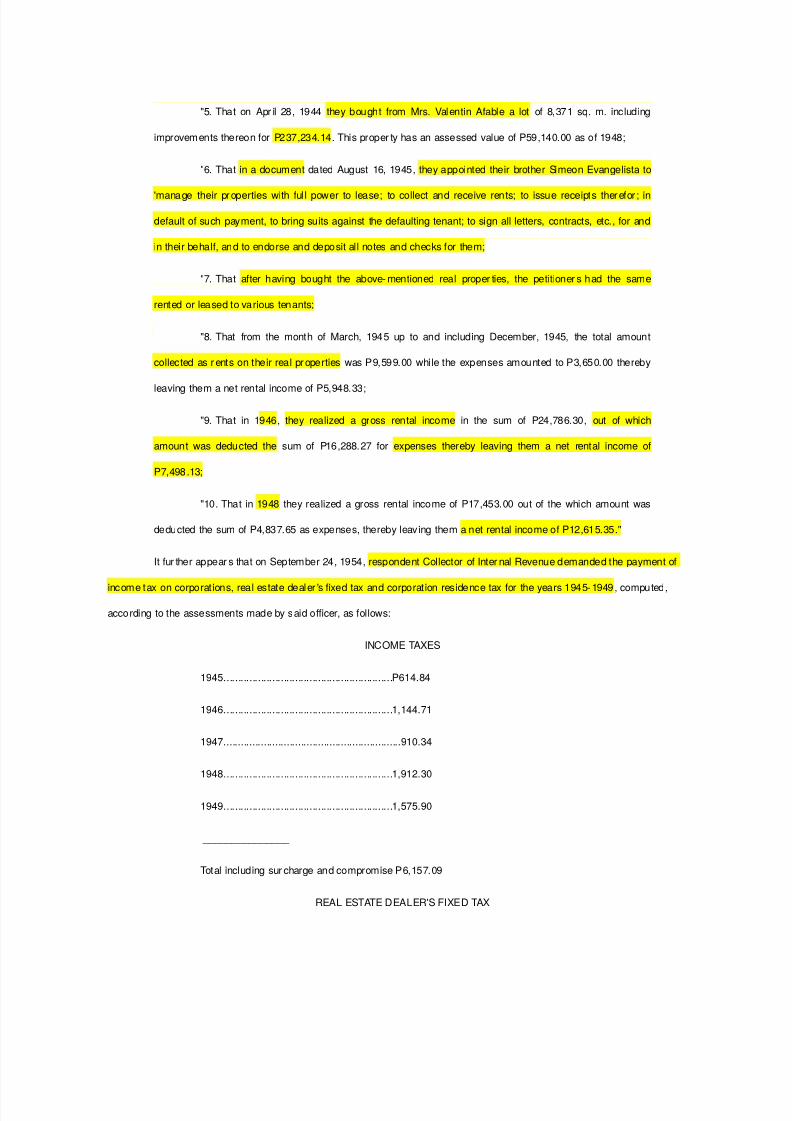

"5. That on April 28, 1944 they bought from Mrs. Valentin Afable a lot of 8,371 sq. m. including

improvements thereon for P237,234.14. This property has an assessed value of P59,140.00 as of 1948;

"6. That in a document dated August 16, 1945, they appointed their brother Simeon Evangelista to

'manage their properties with full power to lease; to collect and receive rents; to issue receipts therefor; in

default of such payment, to bring suits against the defaulting tenant; to sign all letters, contracts, etc., for and

in their behalf, and to endorse and deposit all notes and checks for them;

"7. That after having bought the above-mentioned real properties, the petitioners had the same

rented or leased to various tenants;

"8. That from the month of March, 1945 up to and including December, 1945, the total amount

collected as rents on their real properties was P9,599.00 while the expenses amounted to P3,650.00 thereby

leaving them a net rental income of P5,948.33;

"9. That in 1946, they realized a gross rental income in the sum of P24,786.30, out of which

amount was deducted the sum of P16,288.27 for expenses thereby leaving them a net rental income of

P7,498.13;

"10. That in 1948 they realized a gross rental income of P17,453.00 out of the which amount was

deducted the sum of P4,837.65 as expenses, thereby leaving them a net rental income of P12,615.35."

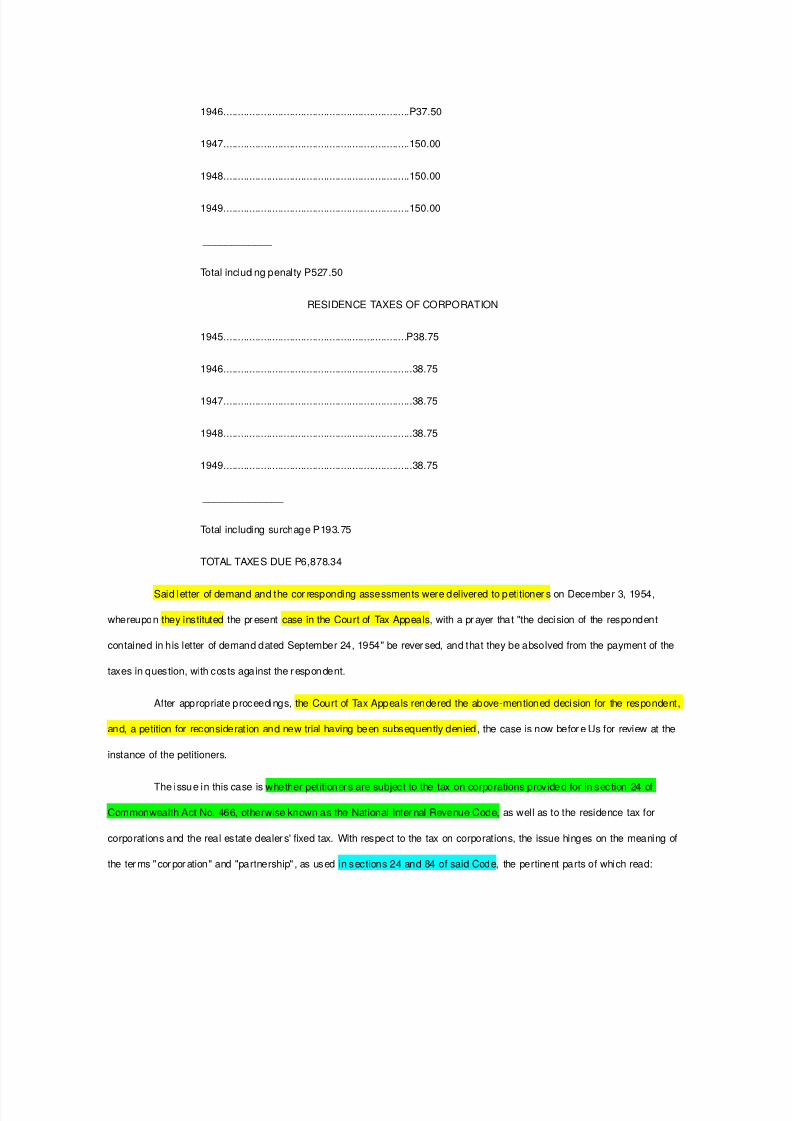

It further appears that on September 24, 1954, respondent Collector of Internal Revenue demanded the payment of

income tax on corporations, real estate dealer's fixed tax and corporation residence tax for the years 1945-1949, computed,

according to the assessments made by said officer, as follows:

INCOME TAXES

1945...........................................................P614.84

1946...........................................................1,144.71

1947..............................................................910.34

1948...........................................................1,912.30

1949...........................................................1,575.90

_______________

Total including surcharge and compromise P6,157.09

REAL ESTATE DEALER'S FIXED TAX

8/18/2019 Pat Assigned 1

http://slidepdf.com/reader/full/pat-assigned-1 25/54

1946.................................................................P37.50

1947.................................................................150.00

1948.................................................................150.00

1949.................................................................150.00

____________

Total including penalty P527.50

RESIDENCE TAXES OF CORPORATION

1945................................................................P38.75

1946..................................................................38.75

1947..................................................................38.75

1948..................................................................38.75

1949..................................................................38.75

______________

Total including surchage P193.75

TOTAL TAXES DUE P6,878.34

Said letter of demand and the corresponding assessments were delivered to petitioners on December 3, 1954,

whereupon they instituted the present case in the Court of Tax Appeals, with a prayer that "the decision of the respondent

contained in his letter of demand dated September 24, 1954" be reversed, and that they be absolved from the payment of the

taxes in question, with costs against the respondent.

After appropriate proceedings, the Court of Tax Appeals rendered the above-mentioned decision for the respondent,

and, a petition for reconsideration and new trial having been subsequently denied, the case is now before Us for review at the

instance of the petitioners.

The issue in this case is whether petitioners are subject to the tax on corporations provided for in section 24 of

Commonwealth Act No. 466, otherwise known as the National Internal Revenue Code, as well as to the residence tax for

corporations and the real estate dealers' fixed tax. With respect to the tax on corporations, the issue hinges on the meaning of

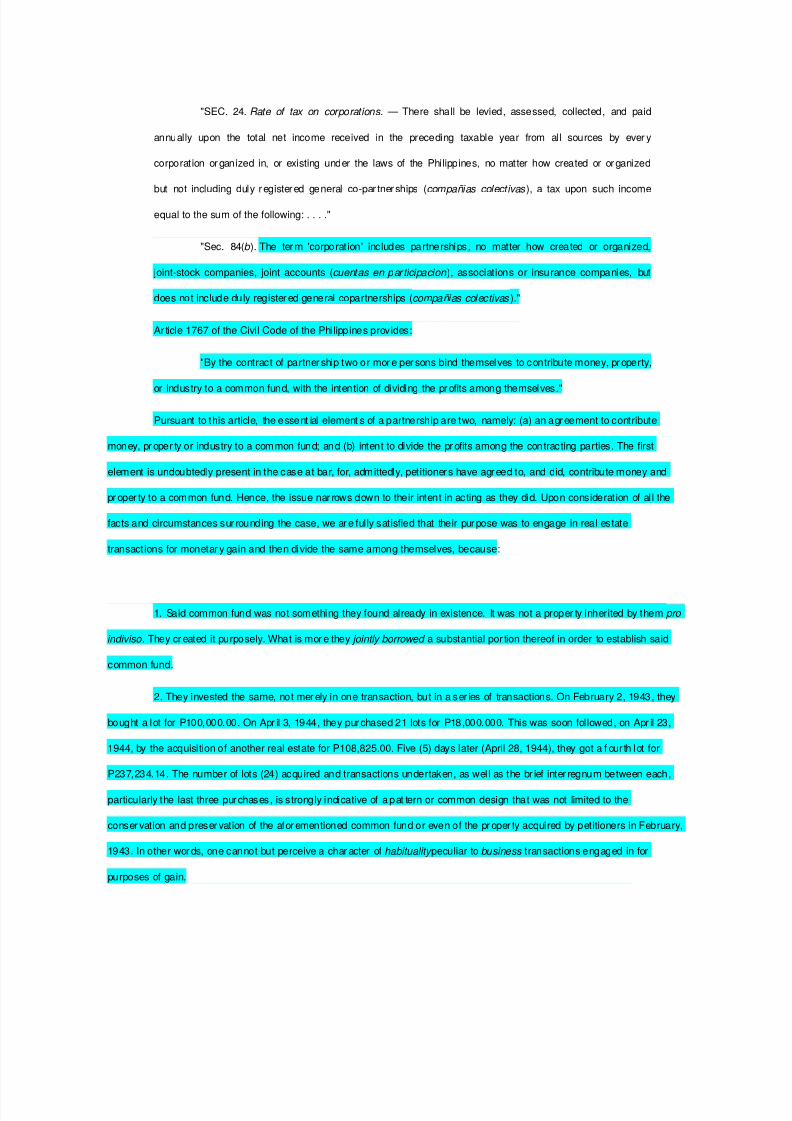

the terms "corporation" and "partnership", as used in sections 24 and 84 of said Code, the pertinent parts of which read:

8/18/2019 Pat Assigned 1

http://slidepdf.com/reader/full/pat-assigned-1 26/54

"SEC. 24.Rate of tax on corporations. — There shall be levied, assessed, collected, and paid

annually upon the total net income received in the preceding taxable year from all sources by every

corporation organized in, or existing under the laws of the Philippines, no matter how created or organized

but not including duly registered general co-partnerships (compañias colectivas), a tax upon such income

equal to the sum of the following: . . . ."

"Sec. 84(b). The term 'corporation' includes partnerships, no matter how created or organized,

joint-stock companies, joint accounts (cuentas en participacion), associations or insurance companies, but

does not include duly registered general copartnerships (compañias colectivas)."

Article 1767 of the Civil Code of the Philippines provides:

"By the contract of partnership two or more persons bind themselves to contribute money, property,

or industry to a common fund, with the intention of dividing the profits among themselves."

Pursuant to this article, the essential elements of a partnership are two, namely: (a) an agreement to contribute

money, property or industry to a common fund; and (b) intent to divide the profits among the contracting parties. The first

element is undoubtedly present in the case at bar, for, admittedly, petitioners have agreed to, and did, contribute money and

property to a common fund. Hence, the issue narrows down to their intent in acting as they did. Upon consideration of all the

facts and circumstances surrounding the case, we are fully satisfied that their purpose was to engage in real estate

transactions for monetary gain and then divide the same among themselves, because:

1. Said common fund was not something they found already in existence. It was not a property inherited by them pro

indiviso. They created it purposely. What is more they jointly borrowed a substantial portion thereof in order to establish said

common fund.

2. They invested the same, not merely in one transaction, but in a series of transactions. On February 2, 1943, they

bought a lot for P100,000.00. On April 3, 1944, they purchased 21 lots for P18,000.000. This was soon followed, on April 23,

1944, by the acquisition of another real estate for P108,825.00. Five (5) days later (April 28, 1944), they got a fourth lot for

P237,234.14. The number of lots (24) acquired and transactions undertaken, as well as the brief interregnum between each,

particularly the last three purchases, is strongly indicative of a pattern or common design that was not limited to the

conservation and preservation of the aforementioned common fund or even of the property acquired by petitioners in February,

1943. In other words, one cannot but perceive a character ofhabitualitypeculiar tobusiness transactions engaged in for

purposes of gain.

8/18/2019 Pat Assigned 1

http://slidepdf.com/reader/full/pat-assigned-1 27/54

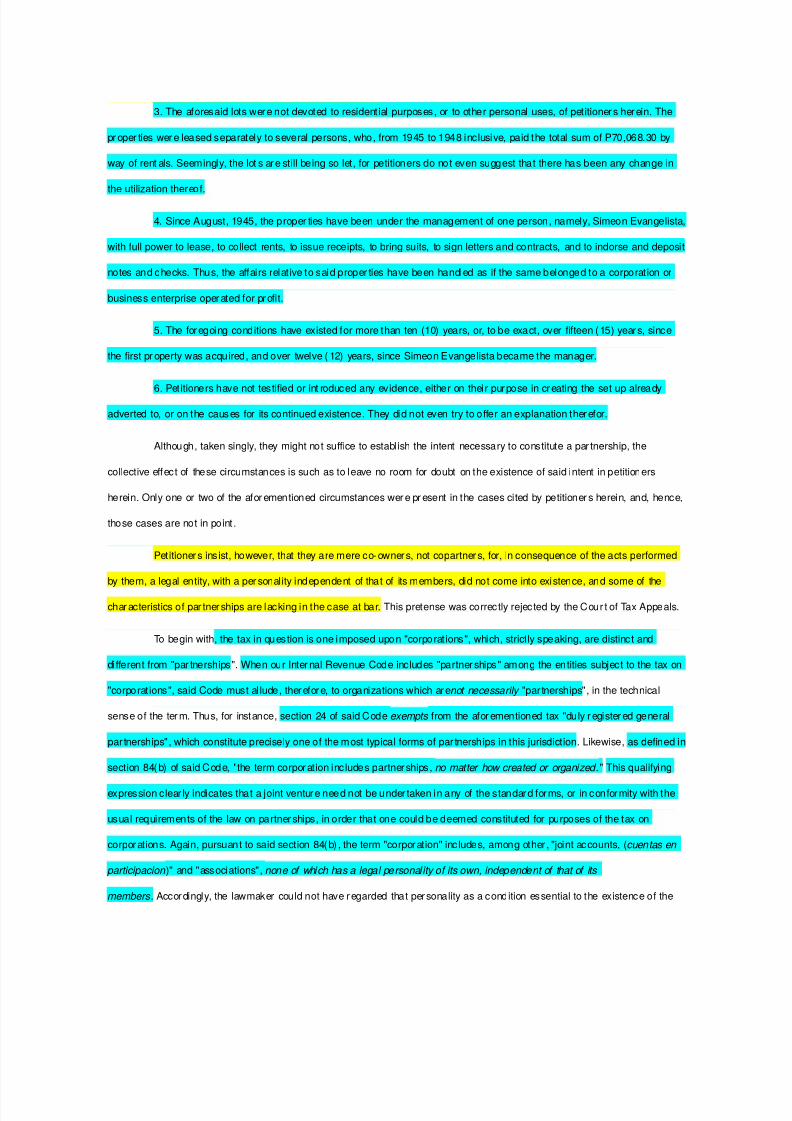

3. The aforesaid lots were not devoted to residential purposes, or to other personal uses, of petitioners herein. The

properties were leased separately to several persons, who, from 1945 to 1948 inclusive, paid the total sum of P70,068.30 by

way of rentals. Seemingly, the lots are still being so let, for petitioners do not even suggest that there has been any change in

the utilization thereof.

4. Since August, 1945, the properties have been under the management of one person, namely, Simeon Evangelista,

with full power to lease, to collect rents, to issue receipts, to bring suits, to sign letters and contracts, and to indorse and deposit

notes and checks. Thus, the affairs relative to said properties have been handled as if the same belonged to a corporation or

business enterprise operated for profit.

5. The foregoing conditions have existed for more than ten (10) years, or, to be exact, over fifteen (15) years, since

the first property was acquired, and over twelve (12) years, since Simeon Evangelista became the manager.

6. Petitioners have not testified or introduced any evidence, either on their purpose in creating the set up already

adverted to, or on the causes for its continued existence. They did not even try to offer an explanation therefor.

Although, taken singly, they might not suffice to establish the intent necessary to constitute a partnership, the

collective effect of these circumstances is such as to leave no room for doubt on the existence of said intent in petitioners

herein. Only one or two of the aforementioned circumstances were present in the cases cited by petitioners herein, and, hence,

those cases are not in point.

Petitioners insist, however, that they are mere co-owners, not copartners, for, in consequence of the acts performed

by them, a legal entity, with a personality independent of that of its members, did not come into existence, and some of the

characteristics of partnerships are lacking in the case at bar. This pretense was correctly rejected by the Court of Tax Appeals.

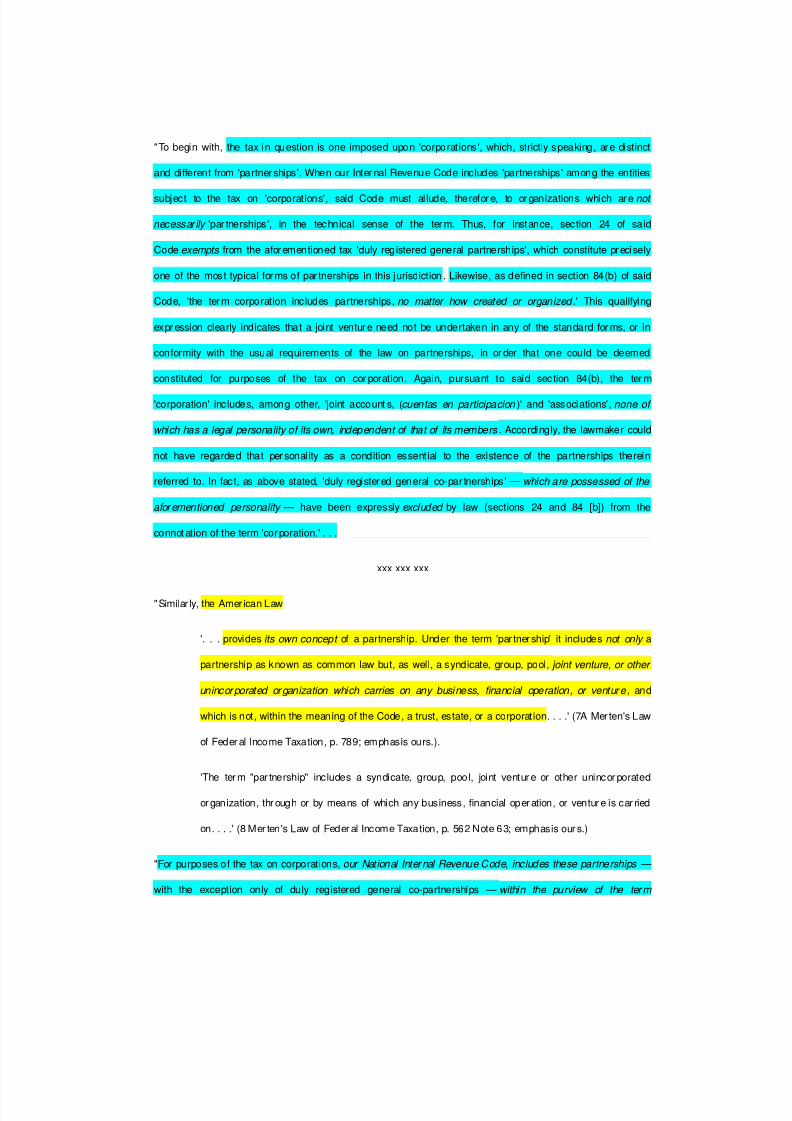

To begin with, the tax in question is one imposed upon "corporations", which, strictly speaking, are distinct and

different from "partnerships". When our Internal Revenue Code includes "partnerships" among the entities subject to the tax on

"corporations", said Code must allude, therefore, to organizations which arenot necessarily"partnerships", in the technical

sense of the term. Thus, for instance, section 24 of said Codeexempts from the aforementioned tax "duly registered general

partnerships", which constitute precisely one of the most typical forms of partnerships in this jurisdiction. Likewise, as defined in

section 84(b) of said Code, "the term corporation includes partnerships,no matter how created or organized." This qualifying

expression clearly indicates that a joint venture need not be undertaken in any of the standard forms, or in conformity with the

usual requirements of the law on partnerships, in order that one could be deemed constituted for purposes of the tax on

corporations. Again, pursuant to said section 84(b), the term "corporation" includes, among other, "joint accounts, (cuentas en

participacion)" and "associations",none of which has a legal personality of its own, independent of that of its

members.Accordingly, the lawmaker could not have regarded that personality as a condition essential to the existence of the

8/18/2019 Pat Assigned 1

http://slidepdf.com/reader/full/pat-assigned-1 28/54

partnerships therein referred to. In fact, as above stated, "duly registered general copartner ships" —which are possessed of

the aforementioned personality— have been expresslyexcluded by law (sections 24 and 84 [b]) from the connotation of the

term "corporation." It may not be amiss to add that petitioners' allegation to the effect that their liability in connection with the

leasing of the lots above referred to, under the management of one person — even if true, on which we express no opinion

tends to increase the similarity between the nature of their venture and that of corporations, and is, therefore, an additional

argument in favor of the imposition of said tax on corporations.

Under the Internal Revenue Laws of the United States, "corporations" are taxed differently from "partnerships". By

specific provision of said laws, such "corporations" include "associations, joint-stock companies and insurance companies."

However, the term "association" is not used in the aforementioned laws

". . . in any narrow or technical sense. It includes any organization, created for the transaction of

designated affairs, or the attainment of some object, which, like a corporation, continues notwithstanding that

its members or participants change, and the affairs of which, like corporate affairs, areconducted by a single

individual,a committee, a board, or some other group, acting in a representative capacity. It is immaterial

whether such organization is created by an agreement, a declaration of trust, a statute, or otherwise. It

includes a voluntary association, a joint-stock corporation or company, a 'business' trusts a 'Massachusetts'

trust, a 'common law' trust, and 'investment' trust (whether of the fixed or the management type), an

interinsurance exchange operating through an attorney in fact, a partnership association, and any other type

of organization (by whatever name known) which is not, within the meaning of the Code, a trust or an estate,

or a partnership." (7A Merten's Law of Federal Income Taxation, p. 788; italics ours.)

Similarly, the American Law.

". . . providesits own concept of a partnership. Under the term 'partnership' it includes not only a

partnership as known at common law but, as well, a syndicate, group, pool, joint venture, or other

unincorporated organization which carries on any business, financial operation, or venture, and which is not,

within the meaning of the Code, a trust, estate, or a corporation. . . .." (7A Merten's Law of Federal Income

Taxation, p. 789; italics ours.)

"The term 'partnership' includes a syndicate, group, pool, joint venture or other unincorporated

organization, through or by means of which any business, financial operation, or venture is carried on,. . .." (8

Merten's Law of Federal Income Taxation, p. 562 Note 63; italics ours.)

For purposes of the tax on corporations,our National Internal Revenue Code, includes these partnerships — with the

exception only of duly registered general copartnerships — within the purview of the term "corporation." It is, therefore, clear to

8/18/2019 Pat Assigned 1

http://slidepdf.com/reader/full/pat-assigned-1 29/54

our mind that petitioners herein constitute a partnership, insofar as said Code is concerned, and are subject to the income tax

for corporations.

As regards the residence tax for corporations, section 2 of Commonwealth Act No. 465 provides in part:

"Entities liable to residence tax. — Every corporation,no matter how created or organized, whether

domestic or resident foreign, engaged in or doing business in the Philippines shall pay an annual residence

tax of five pesos and an annual additional tax which, in no case, shall exceed one thousand pesos, in

accordance with the following schedule: . . .

"The term 'corporation' as used in this Act includes joint-stock company, partnership, joint account

(cuentas en participacion), association or insurance company,no matter how created or organized."(italics

ours.)

Considering that the pertinent part of this provision is analogous to that of sections 24 and 84(b) of our National

Internal Revenue Code (Commonwealth Act No. 466), and that the latter was approved on June 15, 1939, the day immediately

after the approval of said Commonwealth Act No. 465 (June 14, 1939), it is apparent that the terms "corporation" and

"partnership" are used in both statutes with substantially the same meaning. Consequently, petitioners are subject, also, to the

residence tax for corporations.

Lastly, the records show that petitioners have habitually engaged in leasing the properties above mentioned for a

period of over twelve years, and that the yearly gross rentals of said properties from 1945 to 1948 ranged from P9,599 to

P17,453. Thus, they are subject to the tax provided in section 193 (q) of our National Internal Revenue Code, for "real estate

dealers," inasmuch as, pursuant to section 194(s) thereof:

"'Real estate dealer' includes any person engaged in the business of buying, selling,

exchanging, leasing, or renting property or his own account as principaland holding himself out as a full or

part- time dealer in real estate or as an owner of rental property or properties rented or offered to rent for an

aggregate amount of three thousand pesos or more a year. . . .." (Italics ours.)

Wherefore, the appealed decision of the Court of Tax Appeals is hereby affirmed with costs against the petitioners

herein. It is so ordered.

||| (Evangelista v. Collector of Internal Revenue, G.R. No. L-9996, [October 15, 1957], 102 PHIL 140-152)

8/18/2019 Pat Assigned 1

http://slidepdf.com/reader/full/pat-assigned-1 30/54

[G.R. No. L-68118. October 29, 1985.]

JOSE P. OBILLOS, JR., SARAH P. OBILLOS, ROMEO P. OBILLOS and REMEDIOS P. OBILLOS,

brothers and sisters, petitioners, vs. COMMISSIONER OF INTERNAL REVENUE and COURT OF TAX

APPEALS, respondents.

Demosthenes B. Gadioma for petitioners.

D E C I S I O N

AQUINO, Jp:

This case is about the income tax liability of four brothers and sisters who sold two parcels of land which they had acquired from

their father.

On March 2, 1973 Jose Obillos, Sr. completed payment to Ortigas & Co., Ltd. on two lots with areas of 1,124 and 963 square meters

located at Greenhills, San Juan, Rizal. The next day he transferred his rights to his four children, the petitioners, to enable them to

build their residences. The company sold the two lots to petitioners for P178,708.12 on March 13 (Exh. A and B, p. 44, Rollo).

Presumably, the Torrens titles issued to them would show that they were co-owners of the two lots.LexLib

In 1974, or after having held the two lots for more than a year, the petitioners resold them to the Walled City Securities Corporation

and Olga Cruz Canda for the total sum of P313,050 (Exh. C and D). They derived from the sale a total profit of P134,341.88 or

P33,584 for each of them. They treated the profit as a capital gain and paid an income tax on one-half thereof or on P16,792.

In April, 1980, or one day before the expiration of the five year prescriptive period, the Commissioner of Internal Revenue required

the four petitioners to paycorporate income tax on the total profit of P134,336 in addition to individual income tax on their shares

thereof. He assessed P37,018 as corporate income tax, P18,509 as 50% fraud surcharge and P15,547.56 as 42% accumulated

interest, or a total ofP71,074 56. LexLib

Not only that. He considered the share of the profits of each petitioner in the sum of P33,584 as a"distributive dividend" taxable in

full (not a mere capital gain of which 1/2 is taxable) and required them to pay deficiency income taxes

aggregatingP56,707.20 including the 50% fraud surcharge and the accumulated interest.

8/18/2019 Pat Assigned 1

http://slidepdf.com/reader/full/pat-assigned-1 31/54

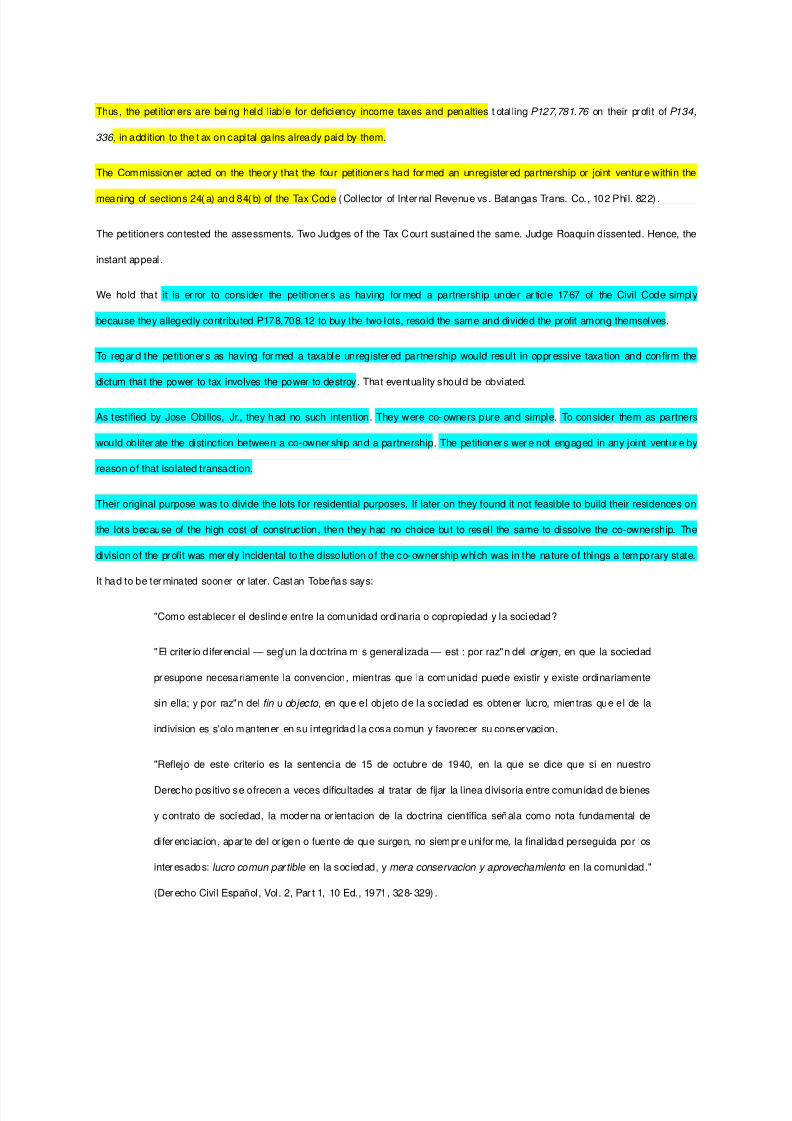

Thus, the petitioners are being held liable for deficiency income taxes and penalties totallingP127,781.76 on their profit ofP134,

336, in addition to the tax on capital gains already paid by them.

The Commissioner acted on the theory that the four petitioners had formed an unregistered partnership or joint venture within the

meaning of sections 24(a) and 84(b) of the Tax Code (Collector of Internal Revenue vs. Batangas Trans. Co., 102 Phil. 822).

The petitioners contested the assessments. Two Judges of the Tax Court sustained the same. Judge Roaquin dissented. Hence, the

instant appeal.

We hold that it is error to consider the petitioners as having formed a partnership under article 1767 of the Civil Code simply

because they allegedly contributed P178,708.12 to buy the two lots, resold the same and divided the profit among themselves.

To regard the petitioners as having formed a taxable unregistered partnership would result in oppressive taxation and confirm the

dictum that the power to tax involves the power to destroy. That eventuality should be obviated.

As testified by Jose Obillos, Jr., they had no such intention. They were co-owners pure and simple. To consider them as partners