ogx petróleo e gás s.a. - under court- supervised

TRANSCRIPT

KPDS 159597

OGX Petróleo e Gás S.A. - Under court-supervised reorganization Interim Financial

Information (ITR) on June

30, 2016 and Independent

Auditors’ Report on review

of the Interim Financial

Information (ITR)

OGX Petróleo e Gás S.A. - Under court-supervised reorganization

Interim Financial Information (ITR) on June 30, 2016

and Independent Auditors’ Report on review of the

Interim Financial Information (ITR)

2

Contents Management report 3

Independent auditor’s report on review of quarterly information 11

Statements of financial position 14

Statements of income 16

Statements of comprehensive income 18

Statements of changes in equity (unsecured liabilities) 19

Statements of cash flows 20

Statements of value added 21

Notes to the financial information 22

3

Management’s Report

Dear shareholders,

The Management of OGX Petróleo e Gás S.A. (“OGX P&G” or “Company”) (in court-

supervised reorganization), in fulfillment of legal and statutory requirements, is submitting

Management`s Report with financial statements and corresponding independent auditors' report

for the quarter ended June 30, and for subsequent events relevant for the market.

Key metrics 2016 2015

Net revenue (R$ million) 54 263

Operating EBITDA (R$ million) (100) (84)

Profit / (loss) (R$ million) 62 (320)

CAPEX (R$ million) 31 11

Cash position (US$ million) 6 6

1. MESSAGE FROM MANAGEMENT

In the second quarter, OGX P&G and OGpar made substantial progress in the negotiation with

OSX-3 Leasing B.V. creditors, and signed an agreement (“Partial Agreement”) on July 15th,

2016, suspending the litigation between the parties for a period of 30 business days as of the

date of approval by the competent Court. The Partial Agreement guarantees the continuity of

the Company’s activities and creates an opportunity for the execution of a definitive agreement

in order to reduce operating costs and end all existing disputes between the parties.

In the same period, the Company ratified a capital increase approved by the Board of

Directors’ Meeting of June 3rd, 2016, with contribution of capital totaling R$ 117,273,261.79

through the capitalization of credit and the private issuance of 12,513,821 shares, under the

negotiation with the creditors of OSX-1 Leasing B.V. in order to decommission the OSX-1

platform.

Given the recovery in oil prices in international markets on the last few months, production

was resumed in the Tubarão Martelo Field on July, averaging 9.8 thousand barrels of oil per

day, allowing the return of cash generation for the Company and new growth prospects.

Also during the second quarter of 2016, OGX received the payment related to PIS and

COFINS tax credits, in the amount of R$ 193.2 million, which contributed to reduce the

pressure on its cash position and comply with short-term obligations until the resume and

stabilization of production at the Tubarão Martelo Field.

4

2. Assets under Development

Development of the Atlanta and Oliva fields (“BS-4”)

Atlanta is a post-salt field located in BS-4 Block, in the Santos Basin. OGX has a 40% interest in

the consortium, in partnership with Barra Energia do Brasil Petróleo e Gás Ltda., with a 30%

interest, and Queiroz Galvão Exploração e Produção S.A. (“QGEP”), the block’s operator, also

with a 30% interest.

On August 10th, 2016, the field’s operator disclosed to the market that, due to challenges found in

the process of customizing the FPSO Petrojarl I, the vessel expectancy to arrive was postponed

to the first quarter of 2017. In this sense, the first oil of the Early Production System (“SPA”) in

the Atlanta Field which was scheduled for the last quarter of 2016, should only occur on the first

semester of 2017. In this first phase, potential production is estimated at 20,000 bbl/d, with two

producing wells that were already drilled and equipped with submersible pumps and wet

Christmas trees. The projection has a margin variation of +/-10%. Production in the SPA may

reach around 30,000 bbl/d with three producing wells, however, the operator will disclose the

production curve in Atlanta Field once the third well drilling schedule is defined.

FPSO Petrojarl I will be chartered for five years, with a termination clause valid after the third

year, and the consortium has also contracted the necessary equipment and underwater solutions.

OGX Austria GmbH, a wholly owned subsidiary of OGX P&G, signed an agreement for the sale

of oil (COSA - Crude Oil Sales Agreement) corresponding to OGX’s share of production for the

Atlanta Field SPA. The agreement has a term of three years and may be extended for another

year. The sale of oil to Shell Western Supplyand Trading Ltd. (“Shell”) will be Free on Board

(“FOB”) in the FPSO with a netback pricing mechanism.

The estimated CAPEX of the consortium is US$ 100 million for 2016 and US$ 150 million for

2017, and OGX P&G is responsible for 40% of the estimated CAPEX. The total estimated

operating cost for the charter and maintenance serves for the SPA is US$ 480 thousand per day,

including leasing, services, logistics, insurance and abandonment fund costs, among others.

3. Mature Assets

3.1 Campos Basin

3.1.1 Tubarão Azul Field

In January 2016, OGX concluded the decommissioning of FPSO OSX-1 platform, fulfilling all

of the commitments entered into with OSX 1 Leasing B.V., its respective creditors and OSX

Serviços Operacionais Ltda. – under Court-Supervised Reorganization. The success of the

decommissioning results from OGX’s capacity to negotiate with its creditors and regulatory

agents.

As part of the agreement, OSX-1 Leasing B.V. deposited US$32 million in an escrow account

with the sole purpose of guaranteeing the fulfillment of the obligations associated with the

abandonment of the Tubarão Azul field wells.

5

The amount deposited by OSX-1 Leasing B.V. was paid to the Company through a capital increase,

approved at the Board of Directors’ Meeting of June 3, 2016, via a private share issue.

3.1.2 Tubarão Martelo Field

A – Production

On March 5th, 2016, the Company temporarily suspended production in the Tubarão Martelo

Field, due to the persistent fall in oil prices in the international market, which made the operation

on the field economically unfeasible at the time.

However, due to the recovery in oil prices in the international market, the Company reviewed its

decision and, on April 26th, 2016, filed with ANP a request to resume production in the four wells

connected on the Tubarão Martelo Field, aiming to generate cash in a more favorable market

scenario. After receiving approval by ANP, on July 1st, 2016, production was resumed on the

field. The activities in the four wells are stable and operating normally.

The chart below shows the evolution in Brent oil prices in the first six months of 2016.

Brent Oil Prices (US$)

6

4. Assets in the Exploration phase

4.1 Exploration Portfolio of Margem Equatorial

ExxonMobil Exploração Brasil Ltda. requested the return of the POT-M-762 block, which is

under review by the ANP.

As for the PAMA-M-591 and PAMA-M-624 blocks, on June 15, 2016, the Company was notified

by the ANP of the waiver from Minimum Exploratory Program compliance, due to the absence

of the environmental permit.

The Company is also awaiting review and final approval by the ANP regarding the sale of its

stake in CE-M-603 and POT-M-475 blocks, operated by ExxonMobil Exploração Brasil Ltda.,

signed in a farm out agreement in September 2015. OGX will keep its shareholders and the market

informed about the developments of this matter.

5. Assets Available for Sale

5.1 Parnaíba Gás Natural Shares

On March 24, 2016, the Company entered into an agreement with Eneva S.A. (“Eneva”), pledging

to subscribe part of the new common shares to be issued under Eneva’s private capital increase,

by means of the contribution of all of its interest held in PGN at the time of subscription.

Cambuhy also signed an agreement with Eneva, whereby it would contribute all of its interest in

PGN and PGN’s third- and fourth-issue convertible debentures.

As a result of the implementation of the aforementioned capital increase, Eneva may hold 100%

of PGN’s capital stock and OGX will hold interest in Eneva.

Additionally, as part of the agreement, OGX signed an agreement with Cambuhy, to sell the 5%

interest it holds in PGN’s capital stock for R$10 million, which is also subject to suspensive

conditions, including the authorization of the court-supervised reorganization.

5.2 Royalties Rights Abroad

In April 2016, the Company sold its rights to royalties of 3% of the revenue generated from the

sale of hydrocarbons in the VIM-5 and VIM-19 blocks for approximately R$10.4 million,

allowing the generation of cash in the short term and concluding the sale of all assets located in

Colombia, pursuant to the Company’s Judicial Reorganization Plan.

7

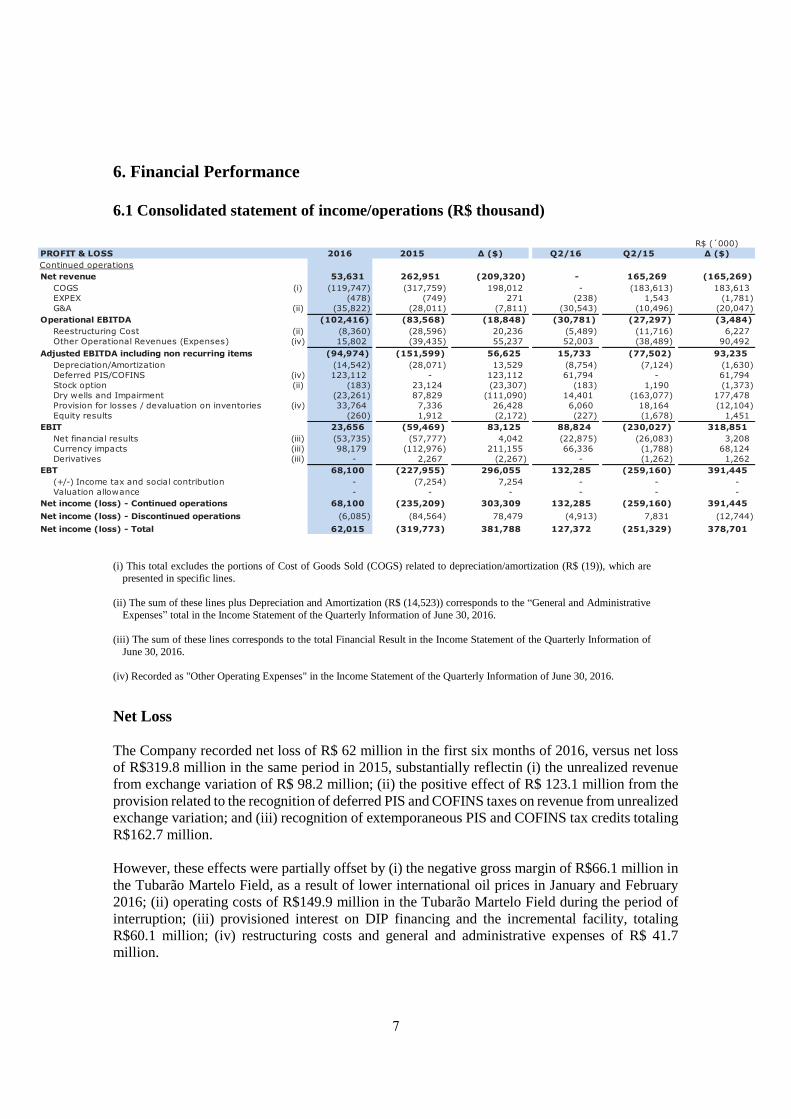

6. Financial Performance

6.1 Consolidated statement of income/operations (R$ thousand)

(i) This total excludes the portions of Cost of Goods Sold (COGS) related to depreciation/amortization (R$ (19)), which are

presented in specific lines.

(ii) The sum of these lines plus Depreciation and Amortization (R$ (14,523)) corresponds to the “General and Administrative

Expenses” total in the Income Statement of the Quarterly Information of June 30, 2016.

(iii) The sum of these lines corresponds to the total Financial Result in the Income Statement of the Quarterly Information of

June 30, 2016.

(iv) Recorded as "Other Operating Expenses" in the Income Statement of the Quarterly Information of June 30, 2016.

Net Loss

The Company recorded net loss of R$ 62 million in the first six months of 2016, versus net loss

of R$319.8 million in the same period in 2015, substantially reflectin (i) the unrealized revenue

from exchange variation of R$ 98.2 million; (ii) the positive effect of R$ 123.1 million from the

provision related to the recognition of deferred PIS and COFINS taxes on revenue from unrealized

exchange variation; and (iii) recognition of extemporaneous PIS and COFINS tax credits totaling

R$162.7 million.

However, these effects were partially offset by (i) the negative gross margin of R$66.1 million in

the Tubarão Martelo Field, as a result of lower international oil prices in January and February

2016; (ii) operating costs of R$149.9 million in the Tubarão Martelo Field during the period of

interruption; (iii) provisioned interest on DIP financing and the incremental facility, totaling

R$60.1 million; (iv) restructuring costs and general and administrative expenses of R$ 41.7

million.

R$ (´000)

PROFIT & LOSS 2016 2015 ∆ ($) Q2/16 Q2/15 ∆ ($)

Continued operations

Net revenue 53,631 262,951 (209,320) - 165,269 (165,269)

COGS (i) (119,747) (317,759) 198,012 - (183,613) 183,613

EXPEX (478) (749) 271 (238) 1,543 (1,781)

G&A (ii) (35,822) (28,011) (7,811) (30,543) (10,496) (20,047)

Operational EBITDA (102,416) (83,568) (18,848) (30,781) (27,297) (3,484)

Reestructuring Cost (ii) (8,360) (28,596) 20,236 (5,489) (11,716) 6,227

Other Operational Revenues (Expenses) (iv) 15,802 (39,435) 55,237 52,003 (38,489) 90,492

Adjusted EBITDA including non recurring items (94,974) (151,599) 56,625 15,733 (77,502) 93,235

Depreciation/Amortization (14,542) (28,071) 13,529 (8,754) (7,124) (1,630)

Deferred PIS/COFINS (iv) 123,112 - 123,112 61,794 - 61,794

Stock option (ii) (183) 23,124 (23,307) (183) 1,190 (1,373)

Dry wells and Impairment (23,261) 87,829 (111,090) 14,401 (163,077) 177,478

Provision for losses / devaluation on inventories (iv) 33,764 7,336 26,428 6,060 18,164 (12,104)

Equity results (260) 1,912 (2,172) (227) (1,678) 1,451

EBIT 23,656 (59,469) 83,125 88,824 (230,027) 318,851

Net financial results (iii) (53,735) (57,777) 4,042 (22,875) (26,083) 3,208

Currency impacts (iii) 98,179 (112,976) 211,155 66,336 (1,788) 68,124

Derivatives (iii) - 2,267 (2,267) - (1,262) 1,262

EBT 68,100 (227,955) 296,055 132,285 (259,160) 391,445

(+/-) Income tax and social contribution - (7,254) 7,254 - - -

Valuation allowance - - - - - -

Net income (loss) - Continued operations 68,100 (235,209) 303,309 132,285 (259,160) 391,445

Net income (loss) - Discontinued operations (6,085) (84,564) 78,479 (4,913) 7,831 (12,744)

Net income (loss) - Total 62,015 (319,773) 381,788 127,372 (251,329) 378,701

8

Given the recent rise in oil prices in the international market and the more favorable market

scenario, the Company reassessed its decision of interrupting the production in the Tubarão

Martelo Field and, on April 26th, 2016, it filed a request with the ANP, for resumption of

production in the four wells connected at Tubarão Martelo Field to generate cash in a more

favorable scenario. Consequently, after ANP’s approval, on July 1st, 2016, production was

resumed in said field.

6.2 Statement of Financial Position (R$ thousand)

Cash and Cash Equivalents

(*) This total does not include Leasing costs.

R$ (´000)

06/30/2016 12/31/2015 Var. 06/30/2016 12/31/2015 Var.

Assets Liabilities

Current assets Current

Cash and cash equivalents 20,089 23,546 (3,457) Trade payables 47,184 139,057 (91,873)

Escrow deposits - - - Taxes, contributions and government takes 19,368 19,725 (357)

Accounts receivable - - - Salaries and payroll taxes 14,648 20,403 (5,755)

Derivative financial instruments - - - Loans and financings 1,301,337 1,526,411 (225,074)

Taxes and contributions recoverable - 15,000 (15,000) Loans with related parties - - -

Oil inventory - 17,168 (17,168) Accounts payable to related to parties 512,902 457,397 55,505

Other credits and prepaid expenses 7,956 12,538 (4,582) Sundry provisions 177,132 214,479 (37,347)

28,045 68,252 (40,207) Other accounts payable 25,908 10,744 15,164

2,098,479 2,388,216 (289,737)

Non current asset held for sale 234,875 232,433 2,442

Non current Non current

Long-term assets 777,958 733,410 44,548 Sundry provisions 424,301 490,260 (65,959)

Escrow deposits 152,799 59,800 92,999 Deferred PIS/COFINS 18,926 142,038 (123,112)

Materials and supplies 11,731 21,374 (9,643) Loans with related parties 46,154 56,148 (9,994)

Loans with related parties 71,079 85,854 (14,775) 489,381 688,446 (199,065)

Taxes and contributions recoverable 128,045 153,738 (25,693)

Deferred income taxes 358,223 358,223 - Shareholders' equity

Credits with related parties 56,081 54,421 1,660 Paid-in capital 8,607,471 8,607,346 125

Capital Reserve 117,273 - 117,273

Investments 153,112 151,779 1,333 Currency translation adjustments (212,333) (542,428) 330,095

Retained earnings (deficit) (8,681,841) (8,743,856) 62,015

Fixed assets 653,925 639,917 14,008 (169,430) (678,938) 509,508

Intangible 570,515 571,933 (1,418)

Total Asset 2,418,430 2,397,724 20,706 Total Liability + Shareholders' equity 2,418,430 2,397,724 20,706

CASH AND CASH EQUIVALENTS R$ ('000)

Balance as of December 31, 2015 23,546

(+) Cash effects of gross margim (*) 12,030

(-) Idleness of Tubarão Martelo field (*) (42,954)

(+) Receipt of Tax Credits 193,167

(-) Payment of Royalties (15,801)

(-) Payment of Cash Calls (33,962)

(-) Amortisation of debts (7,765)

(-) AFBV Funding (13,809)

(-) G&A - included restructuring costs (44,182)

(-) Exploration expenses (478)

(+) Sale of rights on the royalties Colombia 10,412

(-) Payment of suppliers (64,501)

(+) Others 4,386

Balance as of June 30, 2016 20,089

10

Non-current assets available for sale

This refers to the 36.33% non-controlling interest in Parnaíba Gás Natural S.A. (“PGN”),

which is available for sale and was measured at fair value.

Fixed Assets (CAPEX)

(*) Included amount of discontinued operations.

Borrowings and Financings with Third Parties and Related Parties

Accounts Payable to Related Parties

These basically refer to amounts payable to companies from the OSX Group for the charter of

the FPSOs OSX1 and OSX3. The increase of approximately R$154 million over December

31, 2015 is associated with the leasing of FPSO OSX3 in the first six months of 2016, mainly

offset by the effect of the positive exchange variation on outstanding liabilities due to the

period appreciation of the Real against the dollar.

FIXED ASSETS R$ (´000)

Balance as of December 31, 2015 639,917

(+) CAPEX

Campos Basin (15,618)

Santos Basin 46,131

Parnaíba Basin -

Ceará and Potiguar Basin 148

Pará Maranhão Basin -

Corporate -

30,661

(-) Asset retirement obligation (1,285)

(-) CTA International (27,061)

(-) Depreciation (13,114)

(-) Impairment (i) (24,502)

(+) Write off Dry/Subcommercial wells -

(+) PIS/COFINS Credit 49,309

Balance as of June 30, 2016 653,925

LOANS AND FINANCINGS R$ ('000)

Balance as of December 31, 2015 (1,582,559)

(-) Accrued interests (DIP, Incremental Facility and Intercompanys) (60,081)

(+) Amortization of principal and interests 7,765

(+) Currency exchange 287,384

Balance as of June 30, 2016 (1,347,491)

10

7. Personnel Management

The Company closed the second quarter of 2016 with 211 employees on its payroll and 168

outsourced workers, a reduction of approximately 16% in the number of employees and

outsourced workers on the quarterly comparison and a decline of 38% over December 31, 2015.

The reduction in the number of outsourced workers continued in the second quarter of 2016, due

to the decommissioning of the FPSO OSX-1 platform and the temporary suspension of production

in the Tubarão Martelo field.

8. Audit Committee

On August 10, 2016, the Statutory Audit Committee (“CAE”) of OGX Petróleo e Gás S.A.

reviewed the Management Report, the Quarterly Information and related Notes, and the

Independent Auditor’s Report for the period ended June 30, 2016. Based on said review and

considering the information and clarifications provided by the Company’s Management and

KPMG Auditores Independentes, the Committee decided to recommend that the Board of

Directors approve said Quarterly Information, without any qualification.

9. Declaration of the Board of Executive Officers

Pursuant to Article 25 of CVM Instruction 480/2009, the Board of Executive Officers hereby

declares that it has discussed, reviewed and agreed with the conclusion in the independent

auditors’ report, issued on August 12, 2016, and with the quarterly information for the period

ended June 30, 2016.

10. Adherence to the arbitration chamber

The Company, its shareholders, management and members of the Board of Directors are hereby

obliged to resolve, through arbitration, any and all disputes or controversies that may arise

between them, related to or arising from, especially, the application, validity, effectiveness,

interpretation, violations and effects of violations of the provisions included in the Novo Mercado

Listing Agreement, Novo Mercado Listing Regulations, Bylaws, shareholders’ agreements filed

at the Company’s headquarters, Brazilian Corporation Law, standards issued by the National

Monetary Council, the Brazilian Central Bank or the CVM, the Bovespa’s regulations, other

standards applicable to the operation of the capital market in general, Arbitration Clauses and

Arbitration Rules of the Market Arbitration Chamber, conducted pursuant to the Arbitration Rules

of the Market Arbitration Chamber.

KPMG Auditores Independentes, uma sociedade simples brasileira e firma-membro da rede KPMG de firmas-membro independentes e afiliadas à KPMG International Cooperative (“KPMG International”), uma entidade suíça.

KPMG Auditores Independentes, a Brazilian entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

11

KPMG Auditores Independentes

Av. Almirante Barroso, 52 - 4º andar

20031-000 - Rio de Janeiro/RJ - Brasil

Caixa Postal 2888 - CEP 20001-970 - Rio de Janeiro/RJ - Brasil

Telefone +55 (21) 3515-9400, Fax +55 (21) 3515-9000

www.kpmg.com.br

Independent Auditor’s Review Report on Interim

Financial Information - ITR

(A free translation of the original report in Portuguese, as filed with the Brazilian Securities

and Exchange Commission (CVM), prepared in accordance with the accounting practices

adopted in Brazil, rules of the CVM and the International Financial Reporting Standards -

IFRS)

To

The Board of Directors

OGX Petróleo e Gás S.A. - Judicial Recovery

Rio de Janeiro - RJ

Introduction

We have reviewed the individual and consolidated interim financial information of OGX

Petróleo e Gás S.A. - Judicial Recovery (“Company”), contained in the quarterly information

form - ITR for the quarter ended June 30, 2016, which comprises the balance sheet as of

June 30, 2016 and the respective statements of income and comprehensive income for

the three and six month period ended on that date, and changes in shareholders’ equity

and cash flows for the six month period ended on that date, including the explanatory

notes.

Management is responsible for the preparation of the individual and consolidated interim

financial information in accordance with CPC 21(R1) and the international accounting rule

IAS 34 - Interim Financial Reporting, issued by the International Accounting Standards

Board - IASB, as well as the presentation of this information in accordance with the

standards issued by the Brazilian Securities and Exchange Commission (CVM), applicable

to the preparation of quarterly information - ITR. Our responsibility is to express our

conclusion on this interim accounting information based on our review.

Scope of the review

We conducted our review in accordance with Brazilian and International Interim Information

Review Standards (NBC TR 2410 - Revisão de Informações Intermediárias Executada pelo

Auditor da Entidade and ISRE 2410 - Review of Interim Financial Information Performed by

the Independent Auditor of the Entity, respectively). A review of interim information

consists of making inquiries primarily of the management responsible for financial and

accounting matters and applying analytical procedures and other review procedures. The

scope of a review is significantly less than an audit conducted in accordance with auditing

standards and, accordingly, it did not enable us to obtain assurance that we were aware of

all the significant matters that could have been identified in an audit. Therefore, we do not

express an audit opinion.

KPMG Auditores Independentes, uma sociedade simples brasileira e firma-membro da rede KPMG de firmas-membro independentes e afiliadas à KPMG International Cooperative (“KPMG International”), uma entidade suíça.

KPMG Auditores Independentes, a Brazilian entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

12

Conclusion on the interim financial information

Based on our review, we are not aware of any fact that might lead us to believe that the

individual and consolidated interim financial information included in the aforementioned

quarterly information were not prepared, in all material respects, in accordance with CPC

21(R1) and IAS34, issued by the IASB, applicable to the preparation of the quarterly review

ITR, and presented in accordance with the standards issued by the Brazilian Securities and

Exchange Commission.

Emphasis

Judicial Recovery Plan

As mentioned in explanatory note 1, on October 30, 2013 Óleo e Gás Participações S.A. -

Judicial Recovery, Company´s parent company at that time, filed, in the Judicial District of

the capital of the State of Rio de Janeiro, a request for a court-supervised reorganization

(judicial recovery) of the Company and its subsidiaries, that was granted on November 21,

2013. At the June 3, 2014 general meeting, the plans were approved by the creditors,

being approved afterwards, on June 13, 2014 by the 4th Business Court of the Judicial

District in the capital of the State of Rio de Janeiro. In April 2015, the Company signed its

first standstill agreement ("Private Instrument of Non-execution Commitment") with the

holders of convertible debentures (DIP) and credits of "incremental facility" provided in the

original plan, where they abstained from voting or from taking any action related to claim

collection of the amounts or to execute guarantees from DIP or incremental facility for the

term of the contract, which was extended until October 30, 2015. General meetings of

debenture holders subsequent to that date, being the last held on August 12, 2016, have

postponed the resolution of this matter. Actions for the preservation of such guarantees,

and other conditions to the conversion of these debts into shares, are described in the

same note. Our conclusion does not contain any modification with respect to this matter.

Going Concern

As mentioned in explanatory note 1, we draw attention to the fact that the interim financial

information for the six month period ended June 30, 2016 indicate that the Company and

its subsidiaries incurred in losses of R$62,015 thousand (individual and consolidated) and,

on that date, the current liabilities exceeded its current assets by R$1,888,031 thousand

and R$1,835,559 thousand, on the parent company and consolidated balances,

respectively. Additionally, the interim financial information present a deficit in shareholder

equity at the period then ended of R$169,430 thousand (individual and consolidated). The

Company's financial restructuring depends on the success of the court-supervised

reorganization plan, as well as on Management's action to manage the short-term

operating cash flows. Such conditions indicate the existence of significant uncertainty that

could raise relevant doubt as to the Company's ability to continue as a going concern. Our

conclusion does not contain any modification with respect to this matter.

KPMG Auditores Independentes, uma sociedade simples brasileira e firma-membro da rede KPMG de firmas-membro independentes e afiliadas à KPMG International Cooperative (“KPMG International”), uma entidade suíça.

KPMG Auditores Independentes, a Brazilian entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

13

Other matters

Interim information of added value

We also reviewed the individual and consolidated interim statement of added value for the

six month period ended June 30, 2016, prepared under Management responsibility, for

which presentation is required in the interim information in accordance with the standards

issued by the Brazilian Securities and Exchange Commission (CVM) applicable to the

preparation of quarterly information - ITR, and considered as supplementary information by

IFRS, which does not require the presentation of the statements of added value. These

statements were submitted to the same review procedures described previously and,

based on our review, we are not aware of any fact that might lead us to believe that they

were not prepared, in all material respects, in accordance with the individual and

consolidated interim accounting information, taken as a whole.

Rio de Janeiro, August 12, 2016

KPMG Auditores Independentes

CRC SP-014428/O-6 F-RJ

Anderson C. V. Dutra

Accountant CRC RJ-093231/O-6

OGX Petróleo e Gás S.A. - Under court-supervised

reorganization

(Publicly-held Company)

Statements of financial position at June 30, 2016 and December 31,

2015

(Amounts in thousands of Reais)

14

Company Consolidated

Note 06/30/2016 12/31/2015 6/30/2016 12/31/2015

Assets

Current Assets

Cash and cash equivalents 5 326 21,979 20,089 23,546

Income tax, social contribution and other

recoverable taxes 13 - 15,000 - 15,000

Oil inventories 8 - 17,168 - 17,168

Other credits and prepaid expenses 9 8,278 12,603 7,956 12,538

8,604 66,750 28,045 68,252

Non-current asset held for sale 10 234,875 232,433 234,875 232,433

Total Current Assets 243,479 299,183 262,920 300,685

Non-Current Assets

Long-term assets

Escrow deposits 6 152,799 59,800 152,799 59,800

Material supplies 8 5,676 15,319 11,731 21,374

Loans with related parties 14 12,238,291 14,860,630 71,079 85,854

Income tax, social contribution and other

recoverable taxes 13 126,940 152,780 128,045 153,738

Deferred income tax and social

contribution 13 358,223 358,223 358,223 358,223

Credits with related parties 14 44,530 44,530 56,081 54,421

12,926,459 15,491,282 777,958 733,410

Investments 10 4,533 6,979 153,112 151,779

Fixed assets 11 535,539 491,818 653,925 639,917

Intangible assets 12 570,515 571,933 570,515 571,933

Total Non-Current Assets 14,037,046 16,562,012 2,155,510 2,097,039

Total Assets 14,280,525 16,861,195 2,418,430 2,397,724

The accompanying notes are an integral part of the quarterly information.

OGX Petróleo e Gás S.A. - Under court-supervised

reorganization

(Publicly-held Company)

Statements of financial position at June 30, 2016 and December 31,

2015

(Amounts in thousands of Reais)

15

Company Consolidated

Note 06/30/2016 12/31/2015 6/30/2016 12/31/2015

Liabilities

Current liabilities

Trade accounts payable 15 46,587 134,729 47,184 139,057

Income and social contribution taxes,

government takes and other taxes to be

paid 13 19,352 19,725 19,368 19,725

Salaries and payroll charges 14,635 20,403 14,648 20,403

Accounts payable to related parties 14 550,509 487,114 512,902 457,397

Borrowings and financing 16 1,301,337 1,526,411 1,301,337 1,526,411

Sundry provisions 17 177,132 214,479 177,132 214,479

Other accounts payable 21,958 5,938 25,908 10,744

Total Current Liabilities 2,131,510 2,408,799 2,098,479 2,388,216

Non-Current Liabilities

Loans with related parties 14 and

16 10,648,023 12,488,322 46,154 56,148

Sundry provisions 17 424,301 490,260 424,301 490,260

Deferred PIS and COFINS 13 and

26 18,926 142,038 18,926 142,038

Provision for losses on investments in

subsidiaries 10 1,227,195 2,010,714 - -

Total Non-Current Liabilities 12,318,445 15,131,334 489,381 688,446

Equity (unsecured liabilities)

Capital stock 19 8,607,471 8,607,346 8,607,471 8,607,346

Capital reserves 19 117,273 - 117,273 -

Currency translation adjustments (212,333) (542,428) (212,333) (542,428)

Accumulated losses (8,681,841) (8,743,856) (8,681,841) (8,743,856)

Total Equity (unsecured liabilities) (169,430) (678,938) (169,430) (678,938)

Total Liabilities and Equity (unsecured

liabilities) 14,280,525 16,861,195 2,418,430 2,397,724

The accompanying notes are an integral part of the quarterly information.

OGX Petróleo e Gás S.A. - Under court-supervised

reorganization

(Publicly-held Company)

Statements of income

Three- and six-month periods ended June 30, 2016 and 2015

(In thousands of Reais, except for basic and diluted earnings (loss) per share

16

Company

04/01/2016

to 01/01/2016 to

04/01/2015 to 01/01/2015 to

Note 06/30/2016 06/30/2016 06/30/2015 06/30/2015

Net sales revenue 21 - 53,631 165,269 262,951

Cost of goods sold 22 - (124,318) (195,674) (349,212)

Gross profit (loss) - (70,687) (30,405) (86,261)

Operating expenses

Exploration expenses 24 (238) (478) 1,543 (679)

General and administrative expenses 23 (35,469) (45,190) (17,417) (30,846)

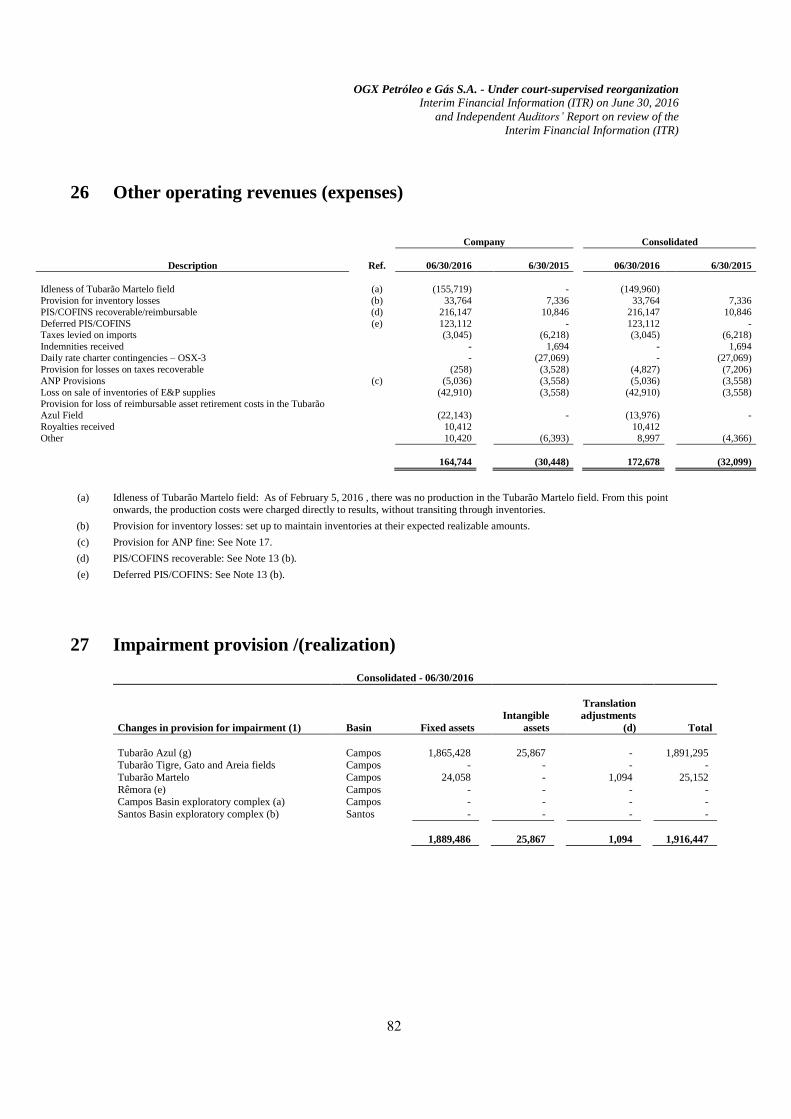

Other operating revenues / expenses 26 114,769 164,744 (20,112) (30,448)

79,062 119,076 (35,986) (61,973)

Provision for/realization of impairment 27 10,564 (31,373) (178,047) 69,291

Equity in the earnings of subsidiaries 10 228,307 432,235 80,465 (328,346)

Results before financial result and taxes on

income

317,933 449,251 (163,973) (407,289)

Financial Results

Financial revenue 25 15,122 17,476 4,226 11,813

Financial expenses 25 (42,309) (77,921) (28,054) (64,753)

Net exchange variation 25 (158,461) (320,706) (71,359) 232,274

(185,648) (381,151) (95,187) 179,334

Results before taxes on income 132,285 68,100 (259,160) (227,955)

Income tax and social contribution 13 - - - (7,254)

Net results of continuing operations 132,285 68,100 (259,160) (235,209)

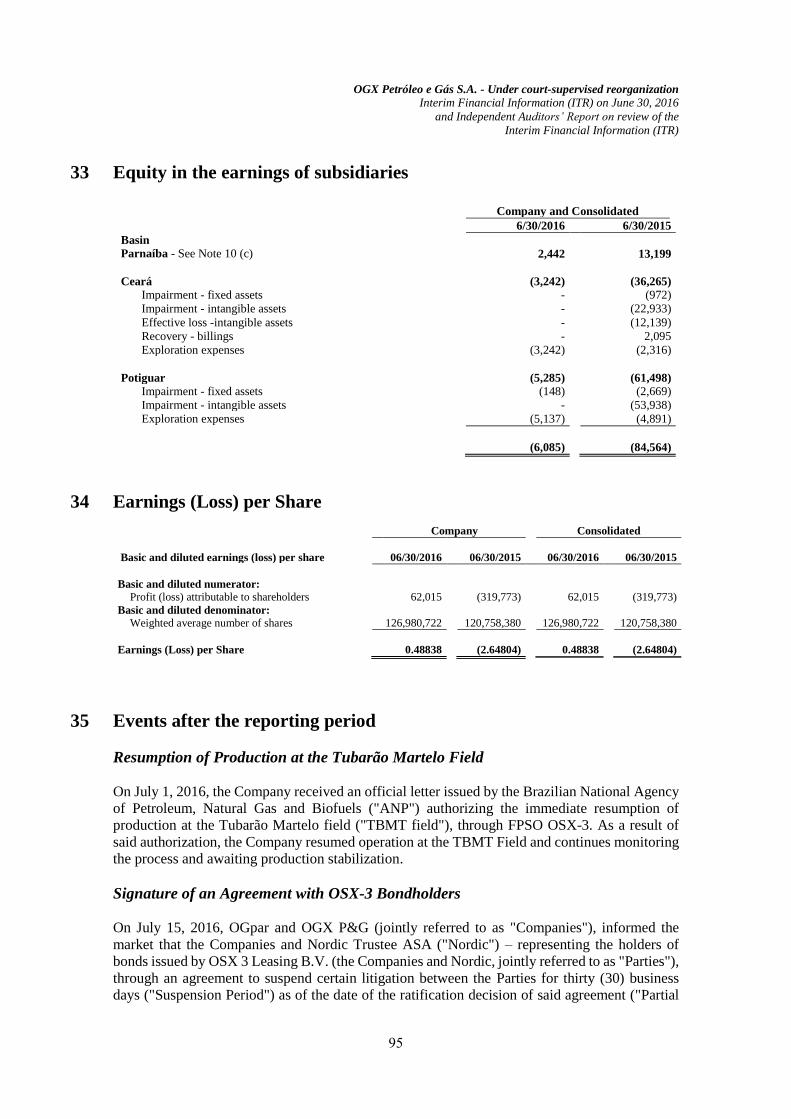

Discontinued operations 33 (4,913) (6,085) 7,831 (84,564)

Profit (loss) for the period 127,372 62,015 (251,329) (319,773)

Basic and diluted earnings (loss) per share

(R$)

34

0.48838 (2.64804)

The accompanying notes are an integral part of the quarterly information.

17

Consolidated

04/01/2016 to 01/01/2016 to 04/01/2015 to 01/01/2015 to

Note 06/30/2016 06/30/2016 06/30/2015 06/30/2015

Net sales revenue 21 - 53,631 165,269 262,951

Cost of goods sold 22 - (119,766) (186,843) (336,108)

Gross profit (loss) - (66,135) (21,574) (73,157)

Operating expenses

Exploration expenses 24 (238) (478) 1,543 (679)

General and administrative expenses 23 (44,969) (58,888) (24,916) (43,205)

Other operating revenues / expenses 26 119,857 172,678 (20,325) (32,099)

74,650 113,312 (43,698) (75,983)

Provision for/realization of impairment 27 14,401 (23,261) (163,077) 87,759

Equity in the earnings of subsidiaries 10 (227) (260) (1,678) 1,912

Results before financial result and taxes on

income

88,824 23,656 (230,027) (59,469)

Financial Results

Financial revenue 25 20,464 23,237 3,613 13,173

Financial expenses 25 (43,089) (76,722) (30,958) (68,683)

Net exchange variation 25 66,086 97,929 (1,788) (112,976)

43,461 44,444 (29,133) (168,486)

Results before taxes on income 132,285 68,100 (259,160) (227,955)

Income tax and social contribution 13 - - - (7,254)

Net results of continuing operations 132,285 68,100 (259,160) (235,209)

Discontinued operations 33 (4,913) (6,085) 7,831 (84,564)

Profit (loss) for the period 127,372 62,015 (251,329) (319,773)

Basic and diluted earnings (loss) per share

(R$)

34

0.48838 (2.64804)

OGX Petróleo e Gás S.A. - Under court-supervised

reorganization

(Publicly-held Company)

Statements of comprehensive income

Three- and six-month periods ended June 30, 2016 and 2015

(Amounts in thousands of Reais)

18

Company and Consolidated

04/01/2016 to 01/01/2016 to 04/01/2015 to 01/01/2015 to

06/30/2016 06/30/2016 06/30/2015 06/30/2015

Profit (loss) for the period 127,372 62,015 (251,329) (319,773)

Currency translation adjustments (CTA) 129,227 330,095 41,476 (159,457)

Total comprehensive income 256,599 392,110 (209,853) (479,230)

The accompanying notes are an integral part of the quarterly information.

OGX Petróleo e Gás S.A. - Under court-supervised reorganization

(Publicly-held Company)

Statements of changes in equity

Periods ended June 30, 2016 and 2015

(Amounts in thousands of Reais)

19

The accompanying notes are an integral part of the quarterly information.

Note

Capital

stock/

Advances for

future capital

increase

(AFAC)

Capital

reserve

Other

comprehensi

ve income

Retained

earnings /

accumulated

losses Total

Balances as of January 1, 2015 8,607,346 461,941 (21,592) (8,429,384) 618,311

Pro rata recognition and cancellation / forfeiture of stock options 19 - (22,127) - - (22,127)

Currency translation adjustments (CTA) 20 - - (159,457) - (159,457)

Profit (loss) for the period 10 - - - (319,773) (319,773)

Balances as of June 30, 2015 8,607,346 439,814 (181,049) (8,749,157) 116,954

Currency translation adjustments (CTA) 35 - - (361,379) - (361,379)

Profit (loss) for the period 19 - - - (434,513) (434,513)

Offsetting accumulated losses - (439,814) - 439,814 -

Balances as of December 31, 2015 8,607,346 - (542,428) (8,743,856) (678,938)

Capital increase / AFAC 20 125 - - - 125

Goodwill in the issuance of shares 20 - 117,273 - - 117,273

Currency translation adjustments (CTA) 10 - - 330,095 - 330,095

Profit for the period - - - 62,015 62,015

Balances as of June 30, 2016 8,607,471 117,273 (212,333) (8,681,841) (169,430)

OGX Petróleo e Gás S.A. - Under court-supervised

reorganization

(Publicly-held Company)

Statements of cash flows

Periods ended June 30, 2016 and 2015

(Amounts in thousands of Reais)

20

The accompanying notes are an integral part of the quarterly information.

Company Consolidated

Note 06/30/2016

06/30/2015

06/30/2016

06/30/2015

Cash flows from operating activities

Profit (loss) for the period from continuing operations 68,100 (235,209) 68,100 (235,209)

Profit (loss) for the period from discontinued operations (6,085) (84,564) (6,085) (84,564)

Adjustments to reconcile results to cash flows from operating activities:

Depreciation of fixed assets and amortization of intangible assets 8, 11 and 12 13,606 22,220 14,542 32,034

Equity in the earnings of subsidiaries 10 (432,235) 328,346 260 (1,912)

Restatement - non-current assets available for sale 10 (2,442) (13,199) (2,442) (13,199)

Stock options (pro rata, cancellation, forfeiture and guarantees) 17 and 20 183 (23,125) 183 (23,125)

Write-offs of dry wells and sub-commercial areas 11 and 12 - (70) - (70)

Impairment losses on decommissioned assets 89,158 92,651 89,158 92,651

Impairment losses 11, 12, 27 and 33 (68,689) (79,686) (64,656) (87,984)

Provision for inventory losses 8 (43,688) (25,033) (43,688) (25,033)

Sundry provisions 17 6,315 3,558 6,315 3,558

Unrealized exchange variation on loans and financing 521,665 (352,839) 111,849 (20,342)

Interest/charges on financing 16 56,704 41,429 58,491 43,656

Amortization of funding costs 16 - 10,954 - 10,954

Deferred income tax and social contribution 13 - 7,254 - 7,254

Deferred PIS and COFINS 13 and 26 (123,112) - (123,112) -

Interest and exchange variation on provision for ARO 17 (108,519) 93,126 (108,519) 93,126

MTM valuation of derivatives - 2,561 - 2,561

Other (10,328) - (10,328) -

Cash provided by (used in) operations (39,367) (211,626) (9,932) (205,644)

Changes in assets and liabilities:

Other credits and related parties 9 and 14 90,019 194,285 102,109 174,253

Income tax, social contribution and other recoverable taxes 13 (8,469) 16,851 (8,616) 16,676

Trade accounts receivable 7 - 22,285 - 25,590

Inventories 8 70,489 (51,904) 70,489 (51,264)

Escrow deposits 6 (130,902) - (130,902) -

Trade accounts payable 15 (75,585) 16,068 (79,316) 8,272

Salaries and payroll charges (5,768) (3,797) (5,755) (3,797)

Income and social contribution taxes, government takes and other taxes to be paid 13 (373) (1,011) (357) (1,011)

Sundry provisions - guaranteed minimum payment 17 - (13,967) - (13,967)

Other accounts payable 16,020 (2,394) 15,164 1,164

(44,569) 176,416 (37,184) 155,916

Net cash provided by (used in) operating activities (83,936) (35,210) (47,116) (49,728)

Cash flows from financing activities

Escrow deposits 6 227 (15,645) 227 (15,645)

Capital increase in equity interest 10 (18,743) (51,307) (35,051) (30,250)

Acquisition of fixed assets 11 (28,344) (36,480) (30,660) (42,990)

Sale of fixed assets 11 - 2,708 - 2,708

Acquisition of intangible assets 12 - (22) - (22)

Net cash provided by (used in) financing activities (46,860) (100,746) (65,484) (86,199)

Cash flows from financing activities

Capital increase 19 125 - 125 -

Amortization of principal 16 (7,650) - (7,650) -

Payment of interest 16 (605) - (605) -

Cash received on conversion of stocks of liabilities associated with TBAZ Field

abandonment guarantee 20 117,273 - 117,273 -

Net cash provided by (used in) financing activities 109,143 - 109,143 -

Cash and cash equivalents (21,653) (135,956) (3,457) (135,927)

Variation in cash and cash equivalents

Opening balance of cash and cash equivalents 21,979 172,537 23,546 177,607

Closing balance of cash and cash equivalents 326 36,581 20,089 41,680

Variation in cash and cash equivalents (21,653) (135,956) (3,457) (135,927)

OGX Petróleo e Gás S.A. - Under court-supervised

reorganization

(Publicly-held Company)

Statements of value added

Periods ended June 30, 2016 and 2015

(Amounts in thousands of Reais)

21

Company Consolidated

Note 06/30/2016 06/30/2015 06/30/2016 06/30/2015

Net sales revenue

Sale of products 21 53,631 262,951 53,631 262,951

Inputs acquired from third parties

Costs of products, merchandise and services, less

royalties

22 (118,401) (302,560) (113,849) (289,456)

Materials, energy, outsourced services and others 51,263 (24,271) 45,431 (26,002)

(Provision for)/realization of impairment 27 (31,373) 69,291 (23,261) 87,759

Effect of stock options 20 (183) 23,124 (183) 23,124

(98,694) (234,416) (91,862) (204,575)

Gross added value (45,063) 28,535 (38,231) 58,376

Retentions

Depreciation of fixed assets and amortization of

intangible assets

11 and

12 (13,606) (22,220) (14,542) (32,034)

Amortization of funding costs 16 - (10,954) - (10,954)

(13,606) (33,174) (14,542) (42,988)

Net value added produced by the Company (58,669) (4,639) (52,773) 15,388

Value added received in transfer

Equity in the earnings of subsidiaries 10 432,235 (328,346) (260) 1,912

Equity in the earnings of subsidiaries 33 (6,085) (84,564) (6,085) (84,564)

Financial revenue 25 17,476 244,087 23,237 13,173

443,626 (168,823) 16,892 (69,479)

Total value added to distribute 384,957 (173,462) (35,881) (54,091)

Distribution of value added

Employees

Direct remuneration 25,030 23,604 25,204 23,854

Benefits 3,411 5,090 3,422 5,090

Accrued severance pay (FGTS) 3,126 4,261 3,126 4,261

31,567 32,955 31,752 33,205

Taxes

Taxes, fees and contributions (113,150) 20,300 (114,339) 22,515

Royalties 22 5,898 28,303 5,898 28,303

Financial expenses 25 398,627 64,753 (21,207) 181,659

Value distributed to shareholders

Profit (loss) for the period attributable to shareholders 62,015 (319,773) 62,015 (319,773)

Total value added distributed 384,957 (173,462) (35,881) (54,091)

The accompanying notes are an integral part of the quarterly information.

OGX Petróleo e Gás S.A. - Under court-supervised reorganization

Interim Financial Information (ITR) on June 30, 2016

and Independent Auditors’ Report on review of the

Interim Financial Information (ITR)

22

Notes to the quarterly information

(Amounts expressed in thousands of Brazilian Reais, except when indicated

otherwise)

1 Operations

1.1 Corporate Structure

As of June 30, 2016, the corporate structure of OGX P&G is as follows:

OGX Petróleo e Gás S.A. - Under court-supervised reorganization (“OGX P&G” or

“Company”): Originally founded as a limited liability company (Ltda.) on June 27, 2007 and

headquartered in the city of Rio de Janeiro, the Company’s purpose is to engage in activities

authorized or granted by the Brazilian federal government involving research, extraction, refining,

processing, sale and transportation of oil, natural gas and other hydrocarbons, as well as any other

correlated activities. By acting either directly or through subsidiaries, OGX P&G may further

carry out the activities that make up its purpose in Brazil or outside of the nation’s territory and

hold interests in other companies. On July 2, 2012, it became a joint stock corporation (S.A.) and,

on account of this change, its reference name was changed from “OGX Ltda.” to “OGX P&G”.

On September 30, 2014, in order to optimize the operating costs of the OGPar Group, the interests

that OGPar held in OGX International and OGX R-11 were transferred to OGX P&G. Further on

the latter date, all the conditions precedent required for extinction of the pre-petition and post-

petition debts of OGX P&G through the issue of equity instruments had already been fulfilled.

As a result, the conversion was already mandatory as prescribed by the court-supervised

reorganization Plan approved by the creditors and ratified by the Reorganization Court. The

conversion and resulting dilution of the interest of OGPar to

OGX Petróleo e Gás S.A. - Under court-supervised reorganization

Interim Financial Information (ITR) on June 30, 2016

and Independent Auditors’ Report on review of the

Interim Financial Information (ITR)

23

28.57% was formalized on October 16, 2014. And finally, on March 30, 2016, the Board of

Directors of OGX P&G resolved on the increase of capital stock by capitalizing the credit

associated with the abandonment guarantee related to the Tubarão Martelo field (See Note 19 (a)),

within the limit of authorized capital, pursuant to Article 6 of the Bylaws of OGX P&G. The

capital increase was carried out upon private issue of 12,531,821 registered book-entry common

shares with no par value, at the issue price of R$ 9.38 per share, being R$ 0.01 per share allocated

to the capital stock account given the Company’s negative shareholders’ equity, and the remaining

R$9.37 per share allocated to the capital reserve. Although the issue of shares is still in progress,

the Company understood that the conversion of equity instruments in the first quarter of 2016 was

appropriate. As a result of the issue of shares referred to above, OGpar’s interest in OGX P&G

was once again diluted from 28.57% to 25.89%.

Sucursal Colômbia (“OGX Colômbia”): The Colombian branch of OGX P&G was founded on

October 26, 2010 to manage operations involving the exploration blocks acquired in that country.

Parnaíba Gás Natural S.A. (“PGN”): Founded on September 25, 2009 under the legal name

OGX Maranhão Petróleo e Gas Ltda, and headquartered in the city of Rio de Janeiro, this

subsidiary has the same corporate purpose as OGX P&G. On December 29, 2011, it was

transformed from a limited liability company into a joint stock corporation and on September 10,

2013 OGPar transferred the shares it held in PGN to OGX P&G through a capital increase. On

October 30, 2013, its name was changed from OGX Maranhão Petróleo e Gás S.A. to the current

name. On February 19, 2014, DD Brazil Holdings S.À.R.L. (“E.ON”) and an investment fund

managed by Cambuhy Investimentos Ltda. (“Cambuhy”) concluded their investment in Parnaíba

Gás Natural S.A. (“PGN”) by means of a capital increase, as prescribed in the Subscription

Agreement entered into on October 30, 2013 by the Company, E.ON, Cambuhy, Eneva S.A.,

PGN and others. After the completion of the capital increase, OGX Petróleo e Gás S.A., had an

interest equivalent to 36.36% of PGN’s capital stock, while Eneva, E.ON and Cambuhy had

interests of 18.18%, 9.09% and 36.37%, respectively. On March 24, 2016, an agreement was

entered between OGX P&G and Eneva S.A. (“OGX Subscription Agreement”) and an agreement

was entered between Eneva and Cambuhy I Fundo de Investimento em Participações

("Cambuhy") ("Cambuhy Subscription Agreement"), and jointly with OGX Subscription

Agreement, "Subscription Agreements"). Pursuant to the agreement, OGX P&G undertook to

subscribe part of the new common shares to be issued within the scope of Eneva’s private capital

increase, upon contribution of its total equity interest held in Parnaíba Gás Natural S.A. ("PGN")

at the time of subscription ("OGX Interest"). In turn, under the Cambuhy Subscription Agreement,

Cambuhy undertook, subject to certain conditions precedent, to subscribe part of the new common

shares to be issued within the scope of Eneva’s private capital increase, upon contribution (i) of

its total equity interest held in PGN ("Cambuhy Interest"); and (ii) of PGN’s total convertible

debentures of the 3rd and 4th issues ("Debentures" and, jointly with Cambuhy Interest, " Cambuhy

Assets" and, jointly with OGX Interest, "PGN Assets"). Eneva, in turn, subject to certain

conditions precedent, will hold a capital increase for private subscription ("Private Capital

Increase "), enabling the contribution of the PGN Assets by Cambuhy and by OGX at an estimated

amount of approximately R$1.15 billion, subject to approval of the respective valuation reports

by the general shareholders’ meeting of Eneva, pursuant to Article 8 of Brazilian Corporation

Law. The agreed price of the shares issue is R$0.15 per share, determined pursuant to Article 170,

paragraph 1, item III, of Brazilian Corporation Law. As a result of the Private Capital Increase

upon contribution of the Cambuhy Assets or of the total PGN Assets into Eneva’s capital (as the

case may be, the “Transaction”), Eneva may thereafter hold up to 100% of the capital stock of

PGN, thus becoming its sole

shareholder. On the other hand, Cambuhy and OGX P&G may thereafter become shareholders of

OGX Petróleo e Gás S.A. - Under court-supervised reorganization

Interim Financial Information (ITR) on June 30, 2016

and Independent Auditors’ Report on review of the

Interim Financial Information (ITR)

27

Eneva. On July 15, 2016, the Company informed the market that Nordic had agreed to the

immediate sale, by OGX P&G, of shares corresponding to five percent (5%) of its interest in

PGN. For further information, see Note 35.

OGX R-11 Petróleo e Gás S.A. (“OGX R-11”): This subsidiary was founded on October 4,

2013, headquartered in the city of Rio de Janeiro, and it has the same corporate purpose as OGX

P&G.

OGX International GmbH - Under court-supervised reorganization (“OGX

International”): Founded on November 11, 2009, headquartered in the city of Vienna, Austria,

this subsidiary’s purpose is to hold interests in other companies and engage in any type of

business.

OGX Austria GmbH - Under court-supervised reorganization (“OGX Austria”): Likewise

founded on November 11, 2009 and headquartered in Vienna, Austria, this subsidiary’s purpose

is to engage in all activities related to the sale of oil, natural gas and all other hydrocarbons,

including import, export, processing, transportation and storage. It may further acquire, maintain

and dispose of interests in other companies and sign lease agreements.

OGX Netherlands Holding B.V. (“OGX Netherlands Holding”): Founded on July 23, 2012,

headquartered in The Hague, in the Netherlands, this subsidiary’s purpose is to engage in the

exploration, production and sale of oil and its by-products, natural gas and other hydrocarbons. It

may further hold interests in other companies and provide technical services for the O&G

industry, and also engage in other activities associated with this industry. At present, its main

operating activities consist of holding interests in other Dutch companies.

OGX Netherlands Holding B.V. (“OGX Netherlands”): This subsidiary was founded on

March 19, 2010, also headquartered in The Hague, in the Netherlands. Its corporate purpose is

the exploration and production, as well as sale of oil and its by-products, natural gas and other

hydrocarbons. It may further provide technical services for the O&G industry, as well as engage

in other activities associated with this industry. At present, its main operating activities consist of

acquiring and leasing equipment to OGX P&G for use in the O&G industry.

Parnaíba B.V. (“Parnaíba B.V.”): Founded on November 15, 2012, this subsidiary is also

headquartered in The Hague, in the Netherlands, and has the same purpose as OGX Netherlands.

Currently, its main operations consist of acquiring and leasing to PGN equipment to be used in

the O&G industry.

Atlanta Field B.V. (“Atlanta Field”): This subsidiary was founded on November 2, 2012, and

is headquartered in Rotterdam, in the Netherlands. At present, its main operations consist of

acquiring and leasing equipment to be used in O&G exploration and production by the consortium

comprised of OGX P&G, Queiroz Galvão E&P and Barra Energia for operations in the Atlanta

and Oliva fields.

OGX Petróleo e Gás S.A. - Under court-supervised reorganization

Interim Financial Information (ITR) on June 30, 2016

and Independent Auditors’ Report on review of the

Interim Financial Information (ITR)

25

1.2 Portfolio

Fields being developed and producing As of June 30, 2016, the Company holds interests in the following fields:

No. Country Basin Blocks Field Operator

% held

by OGX

P&G

Contractual production

phase

1 Brazil Campos BMC 41 Tubarão Azul OGX P&G 100% 05/09/2012 to 05/09/2039 (iv)

2 Brazil Campos BMC 39 / 40 Tubarão Martelo OGX P&G 100% 04/19/2012 to 04/19/2039 (v) 3 Brazil Santos BS-4 Atlanta Queiroz Galvão E&P 40% 12/27/2006 to 12/27/2033

4 Brazil Santos BS-4 Oliva Queiroz Galvão E&P 40% 12/27/2006 to 12/27/2033

Exploratory concessions

As of June 30, 2016, the Company participates in the following exploratory concessions:

No.

Country

Basin

Blocks

Operator

% held by OGX

P&G

Contractual exploration

phase

1 Brazil Espírito-Santo BM-ES-40 Perenco 50% (i)

2 Brazil Espírito-Santo BM-ES-41 Perenco 50% (i) 3 Brazil Potiguar POT-M-475 ExxonMobil 65% 09/15/2020 (ii)

4 Brazil Ceará CE-M-603 ExxonMobil 50% 08/28/2020 (ii)

5 Colombia Cesar Rancheria CR-2 OGX P&G 30% (iii) 6 Colombia Cesar Rancheria CR-3 OGX P&G 30% (iii)

7 Colombia Cesar Rancheria CR-4 OGX P&G 30% (iii)

(i ) The operator filed a revised proposal for the Discovery Appraisal Plan for BM-ES-40 and BM-ES-41. On April 19,

2016, the Company submitted to the ANP a request for authorization of the assignment of rights. After approval by

the ANP, the 50% interest held by the Company will be assigned as follows: (i) 40% to the current operator Perenco

and (ii) 10% to Sinochem.

(ii) Date of the end of the second exploratory period. On September 11, 2015, the Company signed an agreement to

assign these areas to Azibras Exploração de Petróleo e Gás Ltda, including but not limited to approval by the ANP.

(iii) In December 2014, Colombia’s National Hydrocarbon Agency (“ANH”) approved the sale of 100% of the blocks

located in the Lower Magdalena Valley basins (“VIM-5” and “VIM-19”) and 100% of the economic rights to the

blocks located in the Cesar Rancheria basins (“CR-2”, “CR-3” and “CR-4”). The sale of blocks CR-2, CR-3 and

CR-4 calls for an initial transfer of 70% of the interest held by OGX in the blocks to the buyer, with OGX remaining,

on a provisional basis, as operator and holder of 30% of such assets until the exploratory period ends.

(iv) In the process of definitive ARO. As per material fact of January 22, 2016, we concluded the decommissioning of

production ship FPSO OSX-1, which operated in the field.

(v) On January 19, 2016, the Company filed a request for the temporary suspension of production in the Tubarão Martelo

Field (”TBMT Field”) with the Brazilian National Agency of Petroleum, Natural Gas and Biofuels ("ANP"). The

temporary suspension of production in the TBMT Field was requested mainly based on (a) the current challenges

faced by the O&G industry, including the downward trend of Brent prices in the international market; (b) the initial

high estimate of productivity of the wells, which later proved to be incompatible with the field’s effective potential;

and (c) high operating lease costs of FPSO OSX-3. On April 26, 2016, the Company filed a request with the ANP

to resume production at the TBMT field. On July 1, 2016, the Company received a letter from the ANP authorizing

the immediate resumption of production at the TBMT field, through FPSO OSX-3. The TBMT field is currently

operational.

OGX Petróleo e Gás S.A. - Under court-supervised reorganization

Interim Financial Information (ITR) on June 30, 2016

and Independent Auditors’ Report on review of the

Interim Financial Information (ITR)

28

1.3 Return of areas On February 3, 2015, the Company sent an official letter to the ANP informing it of the return of

the Rêmora field in block BMC 40 of the Campos basin. The return of this field, whose CAPEX

was already provisioned for the loss, does not affect the Company’s Business Plan, as approved

by the Board of Directors at the beginning of 2015, which already did not consider any revenues,

expenses and other expenditures relating to Rêmora. On October 19, 2015, the ANP’s Board of

Directors approved the return of the Rêmora Field.

On April 1, 2015, the Company informed the ANP of the return of five exploratory blocks it was

operating in the Pará-Maranhão Basin, as further exploratory activity in such blocks was rendered

unfeasible owing to lack of definition regarding the environmental licensing process for such

areas. On May 27, 2015, the ANP approved the return of Pará Maranhão blocks PAMA–M-407,

PAMA –M-408, PAMA –M-443 PAMA –M-591, PAMA –M-624.

1.4 Court-supervised reorganization

I. Court-supervised reorganization of the OGX Group On October 30, 2013, Óleo e Gás Participações S.A. - Under court-supervised reorganization

(“OGPar”), in view of the unfavorable financial situation facing it and the series of losses, as well

as the then recently and shortly due maturity of most of its indebtedness, filed for court-

supervised reorganization, under No. 0377620-56.2013.8.19.0001, in the Fourth Judicial

Corporate District of the Capital of the State of Rio de Janeiro. This petition was filed by OGPar

together with similar petitions for its subsidiaries OGX Petróleo e Gás S.A. - Under court-

supervised reorganization (OGX P&G), OGX International GmbH - Under court-supervised

reorganization and OGX Austria GmbH - Under court-supervised reorganization, as provided by

Article 51 and subsequent articles of Law 11101/05 (“LFR”), as an urgent measure, as decided

by its Board of Directors on October 30, 2013 (“Court-supervised reorganization”).

The Management of OGPar and its subsidiaries controlled until that time believed that, given the

challenges arising from the Group’s economic-financial situation, a court-supervised

reorganization was the most appropriate measure to preserve the continuity of its business as a

going concern and to protect the interests of OGPar and its stakeholders.

On November 21, 2013, the Reorganization Judge rendered a decision (i) granting the processing

of the court-supervised reorganization of OGPar and OGX P&G, as well as (ii) not granting the

processing of the court-supervised reorganization of OGX International and OGX Austria, since

the judge believed that his court had no jurisdiction over the latter two companies. An

interlocutory appeal (No. 0064658-77.2013.8.19.0000) was filed against the latter decision,

which was unanimously granted on February 19, 2014. On July 23, 2014, the appeal for

clarification of the cited decision filed by the prosecution office was denied. The special appeal

filed by the prosecution office against the decision in the appeal was not admitted by the Court

of Justice of Rio de Janeiro by decision published on July 2, 2015, and is not yet unappealable.

On February 14, 2014, each company filed an individual Court-supervised Reorganization Plan

(“Plan”), detailing the reorganization means to be employed, demonstrating their economic

feasibility , and appraisal reports of their assets. The companies further submitted the list of

creditors that are being paid under the terms and conditions indicated in each Plan. The notice

containing the list of creditors was published on March 6, 2014 and the interested parties

submitted to the court-appointed administrator (“Deloitte”) their qualifications or disagreements

as regards the credits listed. The Plan was approved by the respective creditors in each of the

OGX Petróleo e Gás S.A. - Under court-supervised reorganization

Interim Financial Information (ITR) on June 30, 2016

and Independent Auditors’ Report on review of the

Interim Financial Information (ITR)

28

general meetings held on June 3, 2014 and ratified by the Reorganization Court, according to the

decision published in the Diário Oficial de Justiça of June 26, 2014 (“Confirmatory Decision”).

II. COGX Group Reorganization Plan In brief, the OGX Group Plan calls for the following means of reorganization: (i) obtaining new

financings; (ii) selling off assets; (iii) resizing operations; (iv) paying off part of the debts in cash;

(v) converting part of the debts into OGX P&G’s capital stock; and (vi) carrying out the corporate

reorganization of the OGX Group.

The OGX Group has obtained funding through the following financings, in the manner prescribed

by Articles 66 and 67 of the above-cited Law (LFR), in chronological order:

i. Bridge Loans Very short-term loans contracted by OGPar in the amounts of US$15 million and US$50 million,

used to recover OGX’s working capital and settle obligations with the consortium known as

Consórcio BS-4;

ii. Debtor-in-Possession (DIP) Financing This type of financing has been granted by creditors and some new financing entities, by means

of subscription to debentures, in the total amount of US$215 million, which will be converted

into capital in the event certain conditions precedent are fulfilled, such that these creditors and

new financing entities become shareholders of OGX (“DIP Financing”); and

iii. Additional Loan The main portion of the additional loan, in the amount of approximately US$73 million, was

allocated to the settlement of cash calls outstanding with respect to Consórcio BS-4, in view of

the importance of this asset for OGX.

a. Details on the DIP financing

Form: OGX P&G issued convertible debentures in the total amount of US$215 million

(“Debentures”). The Debentures have been issued in 3 series, as follows:

i. 1st Series Debentures: issued, subscribed and paid up in the total amount of US$125 million;

ii. 2nd Series Debentures: issued, subscribed and paid up in the total amount of US$82.5 million;

iii. 3rd Series Debentures: issued, subscribed and paid up in the total amount of US$7.5 million.

Destination: the funds obtained by means of the DIP Financing have been used to pay off post-

petition obligations, finance certain capital investments and operating expenses in order to

maintain the activities of OGX P&G, as well as paying expenses related to the court-supervised

reorganization.

Guarantees:

Chattel mortgage of the oil and gas owned by OGX P&G in any of the following production

fields, respecting OGX P&G’s interests in each one of these fields: (a) Block BS-4; (b) Tubarão

Martelo; and (c) Blocks POT-M-762, CE-M-661, POT-M-475 and CE-M-603;

Fiduciary assignment of: (a) all the credit rights arising from the sale of oil and gas owned by

OGX, (b) the credit rights held by OGX P&G with respect to PGN arising from the Shared Costs

OGX Petróleo e Gás S.A. - Under court-supervised reorganization

Interim Financial Information (ITR) on June 30, 2016

and Independent Auditors’ Report on review of the

Interim Financial Information (ITR)

28

Agreement Termination and Release entered into by OGX P&G, PGN and Eneva S.A. on

October 30, 2013, as well as the promissory notes issued by PGN in favor of OGX P&G related

to the Shared Costs Agreement Termination and Release; and (c) the restricted account into which

the funds derived from such credit rights will be deposited;

Fiduciary assignment of: (a) the credit rights held by OGX P&G against the Brazilian Federal

Government based on its right to reimbursement for overpayment of Corporate Income Tax, and

(b) the restricted account into which the funds derived from such credit rights will be deposited;

Pledge of the rights emerging from the interest held by OGX P&G in the contracts related to the

BS-4 concession;

Fiduciary assignment of the following, among other rights: (a) the credit rights held by OGX

with respect to Cambuhy derived from the Purchase and Sale Agreement, (b) OGPar’s credit

rights from any subrogation with respect to the rights of the respective creditors of the Private

Indenture for the First Public Issue of Non-Convertible Unsecured Debentures, with Personal

Guarantee, in a Single Series, of Parnaíba; Credit Agreement entered into by PGN, OGPar, MPX

Energia S.A. and Morgan Stanley Bank, N.A.; and the Private Instrument for Chattel Mortgage

of Shares and Other Settlements entered into by OGPar, MPX Energia S.A., Planner Trustee

Distribuidora de Títulos e Valores Mobiliários Ltda. and PGN, (c) the restricted accounts into

which the funds derived from such credit rights will be deposited;

Fiduciary assignment of the credit rights held by OGX P&G and OGPar arising from: (a)

insurance contracts; (b) judicial and extrajudicial litigation (including in the case of

commencement of litigation against Brasil E&P Ltda.); (c) agreements and other instruments; (d)

any other credit rights that are not the object of another specific guarantee, and (e) fiduciary

assignment of the restricted accounts into which the funds derived from such credit rights will be

deposited;

Chattel mortgage of the assets owned by Parnaíba B.V.;

Fiduciary assignment of: (a) any and all credit rights held by OGX P&G arising from the paying

in of the 1st Series of Debentures under the Credit Instrument, which will be deposited into an

restricted account maintained by OGX and (b) the restricted account in question;

Pledge of all the shares issued by Parnaíba B.V.;

Pledge of the credit rights held by OGX Netherlands against MPX Energia GmbH derived from

the sale of the shares issued by Parnaíba B.V.;

Pledge of the credit rights held by OGX Netherlands against Parnaíba B.V.;

Pledge of receivables, right of sale and other rights related to the exportation agreement of OGX

P&G and the Guarantors;

Chattel mortgage of OGX P&G and OGPar shares, to be constituted by the parties after approval

of the Reorganization Plan;

Pledge of the rights emerging from the interests held by OGX P&G in the concession agreements

relating to Tubarão Martelo’s BM-C-39 and BM-C-40, and the concession agreements for the

11th Round to be constituted by the parties after approval of the Reorganization Plan; and

OGX Petróleo e Gás S.A. - Under court-supervised reorganization

Interim Financial Information (ITR) on June 30, 2016

and Independent Auditors’ Report on review of the

Interim Financial Information (ITR)

28

Pledge of shares issued by OGX International, OGX Austria, OGX Netherlands B.V. and OGX

Netherlands Holding B.V., to be constituted after approval of the Reorganization Plan.

Conversion into capital: The Debentures will be automatically converted into shares after

fulfillment or express waiver of the conditions precedent indicated in the respective debenture

indenture and subscription agreement (“Capital Increase Through Conversion of Debentures”).

b. Restructuring of the pre-petition and post-petition debts held by debtors expressly

adhering to the Plan

Form The JR Plans call for restructuring of concourse and extra-concourse credits held by held by

creditors signing on to the Plan through conversion of such credits into capital of OGX P&G

(“Capital Increase Through Capitalization of Credits”).

OGPar’s unsecured creditors are to be paid in 48 equal and consecutive monthly installments,

with the first payment occurring on January 30, 2015, and the remaining payments on the 30th

day of each month through December 30, 2018. Creditors that are suppliers of OGX P&G may

choose to receive a cash amount corresponding to as much as R$30,000, limited to the amount

of the respective credit. This amount was paid in three equal and consecutive monthly

installments on January 30, February 28 and March 30, 2015. Any remaining credit balance was

converted into OGX P&G’s capital stock.

Finally, the financial credits of OGPar and OGX P&G, including, but not limited to, the pre-

petition debts retained by the Bondholders relating to the 2018 Bonds and the 2022 Bonds, as

well as the credits held by the OSX Group, will be paid in full through the conversion of the

credits into OGX P&G’s capital, provided that certain conditions precedent, which are listed in

the Plans, are fulfilled.

Such conversion of the pre-petition and post-petition debts occurred on October 16, 2014. See

item G - Status of implementing the means for reorganization.

So far, the OGX Group does not have any labor credit subject to the court-supervised

reorganization. In the event any labor credits are recognized by court decision or agreement

between the parties, such labor credits will be paid in twelve (12) equal and consecutive monthly

installments.

Moreover, so far the OGX Group does not have any credit with tangible guarantee posted. In the

event any credits with personal guarantee are recognized owing to a court decision, arbitration

proceeding or agreement between the parties, said creditors will be treated in the same manner as

the unsecured creditors.

The credits held by related parties that are direct or indirect subsidiaries of OGPar are novated

by the Plan and will be paid in a lump sum of the principal due in twenty (20) years counting

from the Plan approval date or on July 30, 2034, whichever occurs last. In addition, OGX Austria

has acknowledged that it is a debtor of OGX P&G by force of the subrogation in favor of OGX

P&G as a result of the delivery of shares for payment of the Bondholders’ pre-petition debts, as

per implementation of the Capital Increase Through Capitalization of Credits.

OGX Petróleo e Gás S.A. - Under court-supervised reorganization

Interim Financial Information (ITR) on June 30, 2016

and Independent Auditors’ Report on review of the

Interim Financial Information (ITR)

32

Amount of the capital increase, unit price of shares and first refusal rights

The amount of the capital increase corresponds to the total amount of the pre-petition debts in

the list of creditors, plus the total amount of the post-petition debts adhering to the Plan. In the

event of an increase in the amount of credits arising from a unappealable court decision, OGX

P&G is to issue as many common shares as are required to allow the capitalization of the new

credits. The unit price of the shares was calculated in such a manner as to grant the pre-petition

and post-petition debtors adhering to the Plan a joint interest equivalent to 71.43% of the shares.

After the conversion of the 1st, 2nd and 3rd series of Debentures into OGX’s capital and merger

of OGPar by OGX P&G (see the following section entitled “Merger and Restructured OGX”),

the final joint interest of the creditors will be 25% of the shares issued by Restructured OGX.

The Capital Increase Through Capitalization of Credits occurred in a private manner, therefore

granting first refusal rights to the shareholders of OGX. The shareholders of OGX P&G waived

this right, thus allowing the entire amount of the credits to be capitalized in shares.

c. Corporate Restructuring (Merger and Restructured OGX) After carrying out and implementing (i) the Capital Increase Through Capitalization of Credits;

and (ii) the Capital Increase Through Conversion of Debentures, the Management of OGPar and

OGX P&G undertake to take such steps as required for the merger of OGPar by OGX (“Merger”),

including proposing such operation to the respective shareholders. The Merger will result in a

new publicly-held company with shares traded on the listing segment known as the

BM&FBOVESPA’s Novo Mercado (“Restructured OGX”).

The exchange ratio to be proposed to the shareholders of OGPar and OGX P&G for the Merger

will be that which results in the following final corporate structure of Restructured OGX

immediately after the Merger:

Shareholders Stake in

Restructured OGX

Eike Batista 1 share

EBX 5.02%

Other OGPar shareholders (as of the date of the calling of the Extraordinary Shareholders’

Meeting related to the Merger) 4.98%

New financing entities of the 1st Series of Debentures 41.98%

New financing entities of the 2nd and 3rd Series of Debentures 23.02%

Pre-petition and post-petition debtors (that adhered to the Plan) 25.00%

The purpose of the Merger, after the capitalization operations prescribed in the Plan are carried

out, is to level all the stakeholders in one company and to grant all the then shareholders access

to the capital markets, with the possibility of trading their shares and monetizing them as they

deem fit, as well as to participate in any appreciation in the value of the assets, if such is the case.

Warrants As an additional advantage to the subscription of the new shares of OGX P&G to be issued as a

result of the Merger, the shareholders of OGPar will receive a warrant of Restructured OGX

under the following terms and conditions: (i) exercise term of five years; (ii) a number of

common shares to be subscribed to that represents 15% of the total capital stock of Restructured

OGX, considering an issue price based on the appraisal value of the Restructured Company in

the amount of US$1.5 billion.

OGX Petróleo e Gás S.A. - Under court-supervised reorganization

Interim Financial Information (ITR) on June 30, 2016

and Independent Auditors’ Report on review of the

Interim Financial Information (ITR)

32

d. Resolutory terms and conditions of the Plan The following are resolutory terms and conditions that may result in the cancellation of the

approval already granted to the Plan and the immediate calling of a new meeting of creditors to

decide on an alternative to the Plan or the bankruptcy of OGPar: (i) the verification, up to the

time the Capital Increase Through Capitalization of Credits occurs, of any false or incorrect

statement in any representation or guarantee provided by OGPar in the Plan; (ii) non-compliance

by any of the direct and indirect shareholders of OGPar with any obligation assumed under the

Plan or the carrying out of any act or measure that is incompatible with the Plan’s provisions;

(iii) failure to meet the conditions precedent for the Capital Increase Through Capitalization of

Credits within 120 days of the ratification of the Plan or by September 30, 2014, whichever occurs

first (a condition which was waived at the general creditors’ meeting held on September 29,

2014); (iv) failure to hold an Extraordinary Shareholders’ Meeting and perform other acts

required to implement the Capital Increase Through Capitalization of Credits within 140 days of

the ratification of the Plan or by October 20, 2014, whichever occurs first; (v) the non-adherence

to the Plan by post-petition debtors that are related parties, especially the companies of the OSX

Group; and/or (vi) non-approval of the Plan by the General Creditors’ Meeting, in the manner

provided by the Brazilian Bankruptcy Law.

e. Appeals pending judgment Although a special appeal to the Superior Court of Justice (STJ) was lodged against the decision