navigating your nonprofit’s financial landscape

TRANSCRIPT

Navigating Your Nonprofit’s Financial Landscape

2019 Nonprofit Leadership Summit September 25, 2019

Charleston Coliseum & Convention Center

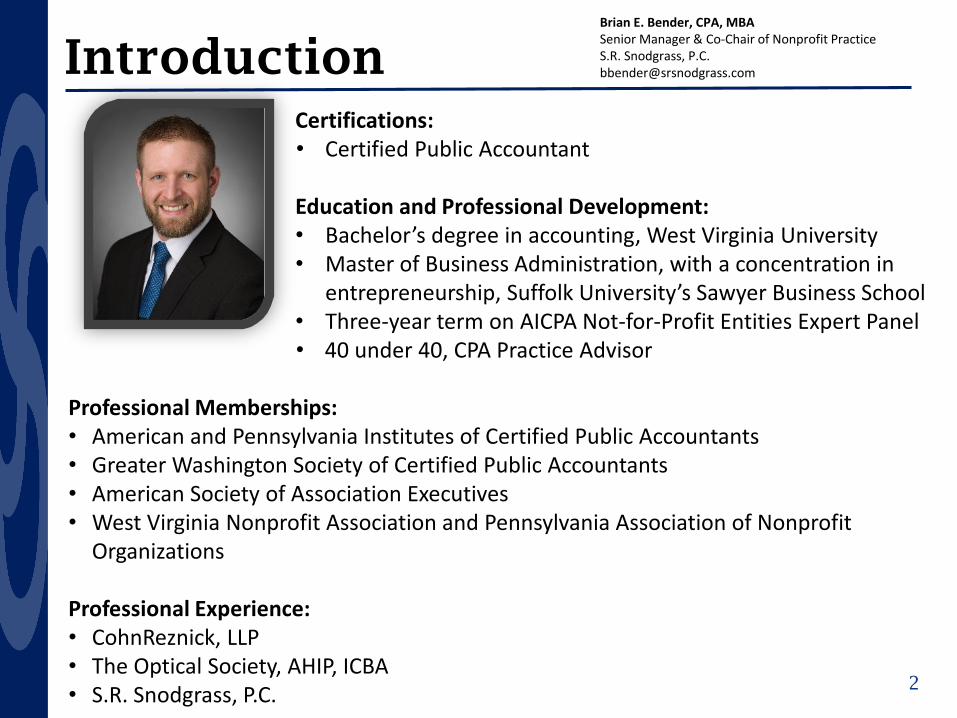

Brian E. Bender, CPA, MBASenior Manager & Co-Chair of Nonprofit Practice

IntroductionCertifications:• Certified Public Accountant

Education and Professional Development:• Bachelor’s degree in accounting, West Virginia University• Master of Business Administration, with a concentration in

entrepreneurship, Suffolk University’s Sawyer Business School• Three-year term on AICPA Not-for-Profit Entities Expert Panel • 40 under 40, CPA Practice Advisor

Professional Memberships:• American and Pennsylvania Institutes of Certified Public Accountants• Greater Washington Society of Certified Public Accountants• American Society of Association Executives• West Virginia Nonprofit Association and Pennsylvania Association of Nonprofit

Organizations

Professional Experience:• CohnReznick, LLP• The Optical Society, AHIP, ICBA• S.R. Snodgrass, P.C.

Brian E. Bender, CPA, MBASenior Manager & Co-Chair of Nonprofit PracticeS.R. Snodgrass, P.C. [email protected]

2

Introduction

3

Objectives

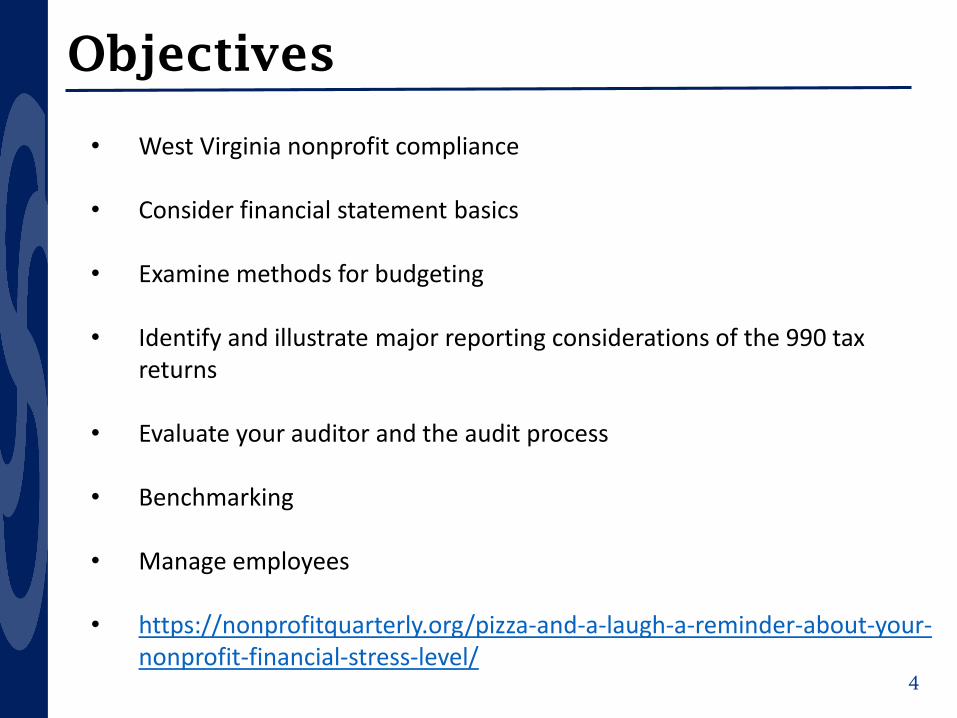

• West Virginia nonprofit compliance

• Consider financial statement basics

• Examine methods for budgeting

• Identify and illustrate major reporting considerations of the 990 tax returns

• Evaluate your auditor and the audit process

• Benchmarking

• Manage employees

• https://nonprofitquarterly.org/pizza-and-a-laugh-a-reminder-about-your-nonprofit-financial-stress-level/

4

Compliance

5

Compliance (continued)

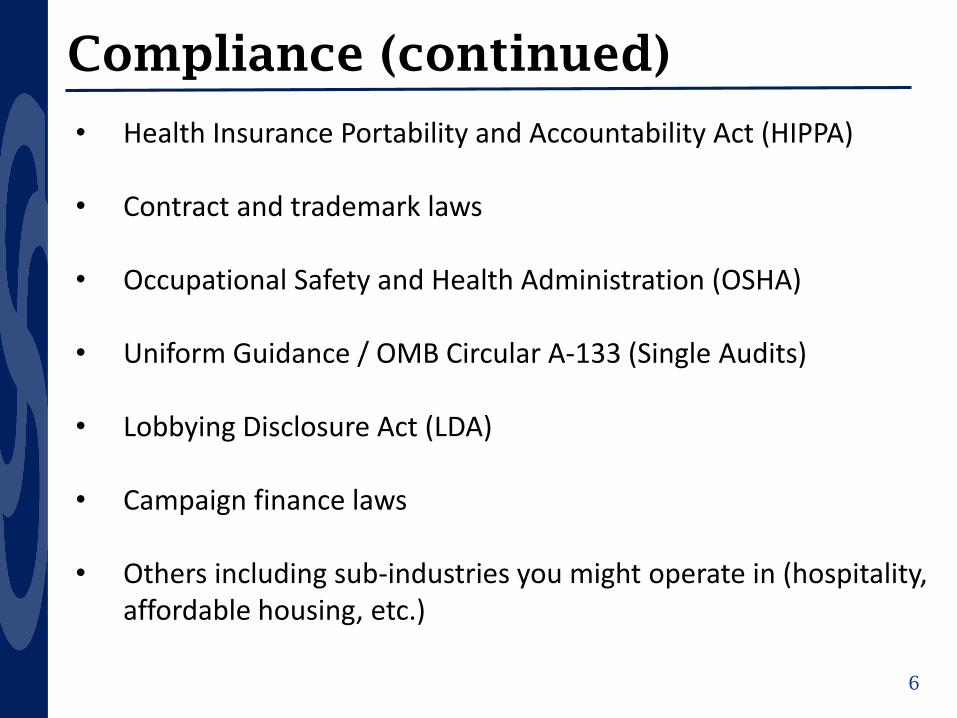

• Health Insurance Portability and Accountability Act (HIPPA)

• Contract and trademark laws

• Occupational Safety and Health Administration (OSHA)

• Uniform Guidance / OMB Circular A-133 (Single Audits)

• Lobbying Disclosure Act (LDA)

• Campaign finance laws

• Others including sub-industries you might operate in (hospitality, affordable housing, etc.)

6

Compliance – WV Charities

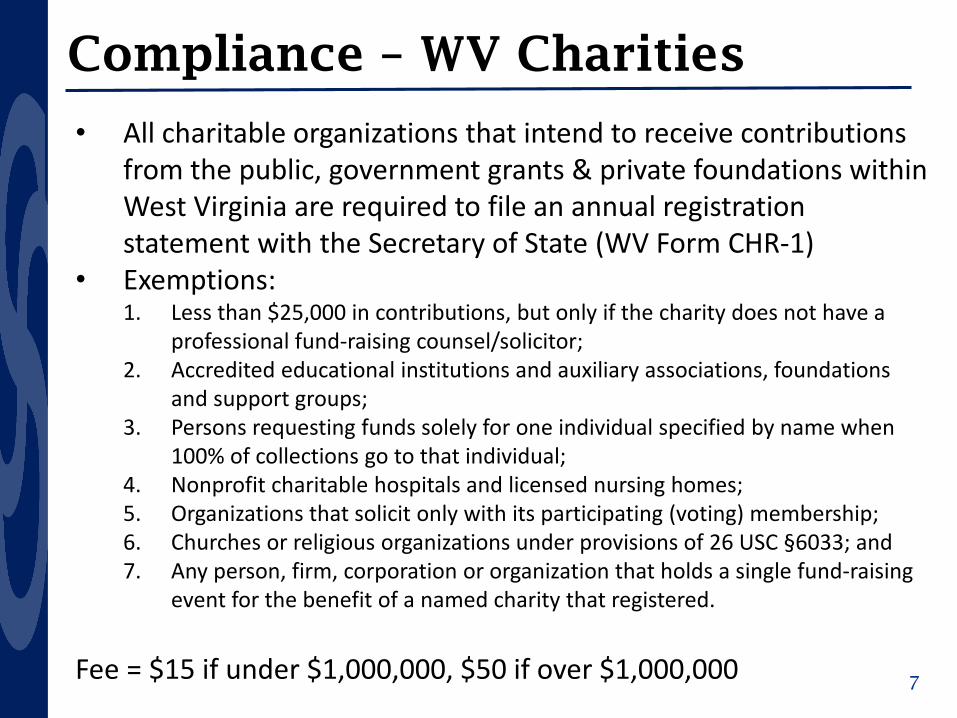

• All charitable organizations that intend to receive contributions from the public, government grants & private foundations within West Virginia are required to file an annual registration statement with the Secretary of State (WV Form CHR-1)

• Exemptions:1. Less than $25,000 in contributions, but only if the charity does not have a

professional fund-raising counsel/solicitor;2. Accredited educational institutions and auxiliary associations, foundations

and support groups;3. Persons requesting funds solely for one individual specified by name when

100% of collections go to that individual;4. Nonprofit charitable hospitals and licensed nursing homes;5. Organizations that solicit only with its participating (voting) membership;6. Churches or religious organizations under provisions of 26 USC §6033; and7. Any person, firm, corporation or organization that holds a single fund-raising

event for the benefit of a named charity that registered.

Fee = $15 if under $1,000,000, $50 if over $1,000,0007

Compliance – WV Charities• Financial statements audited by an independent certified

public accountant, if your organization receives more than $500,000 from all sources except government grants and grants from private foundations.

• If your organization receives more than $200,000 but less than $500,000, a statement of financial review by a certified public accountant will need to be provided.

• Be careful for other states!!! PA, OH, MD, etc.• https://www.councilofnonprofits.org/nonprofit-audit-guide/state-law-audit-requirements

For purposes of this presentation, I will refer to anyone who:• does your books internally as your accountant or bookkeeper,• anyone who performs an audit, compilation, review or prepares

your 990 tax return as your auditor8

Compliance – WV Charities

Level of assurance obtained, according to the AICPA

Compilation:• The Accountant [‘Auditor’] does not obtain or provide any

assurance that there are no material modifications that should be made to the financial statements

Review:• The Accountant [‘Auditor’] obtains limited assurance there

are no material modifications that should be made to the financial statements

Audit:• The Auditor obtains a high, but not absolute, level of

assurance about whether the financial statements are free of material misstatement 9

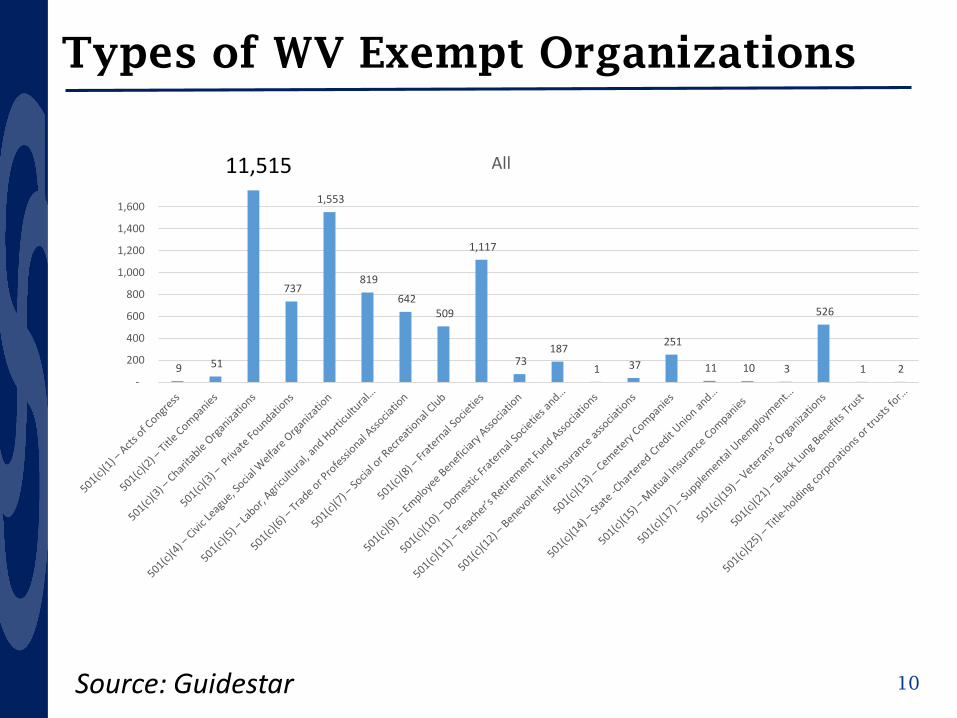

Types of WV Exempt Organizations

10Source: Guidestar

9 51

737

1,553

819

642 509

1,117

73 187

1 37

251

11 10 3

526

1 2 -

200

400

600

800

1,000

1,200

1,400

1,600

All 11,515

Types of WV Exempt Organizations

11Source: Guidestar

1,338

-11

175

135

96

132

35

72

27

12 1

12 10 4 3 -

60

- 2 -

20

40

60

80

100

120

140

160

180

> $50K

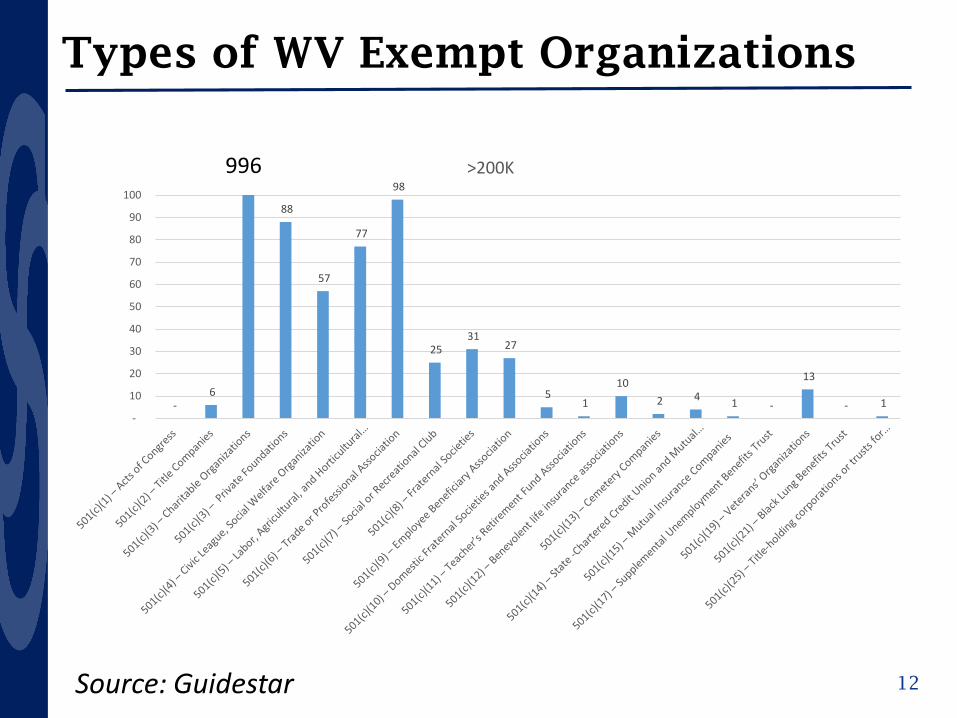

Types of WV Exempt Organizations

12Source: Guidestar

996

-6

88

57

77

98

25 31

27

5 1

10 2 4 1 -

13

- 1 -

10

20

30

40

50

60

70

80

90

100

>200K

Types of WV Exempt Organizations

13Source: Guidestar

679

-2

41

18

43 45

9 8

24

2 -

6

1 2 - -

5

- 1 -

5

10

15

20

25

30

35

40

45

50

>$500K

Types of WV Exempt Organizations

14Source: Guidestar

Financial Statements – Internal / Prepared

15

Not one size fits all

Types of reporters:• Cash basis• Modified cash basis• GAAP basis (accrual)

Basic Financial Statements:• Statement of Financial Position (Balance Sheet)• Statement of Activities (Income Statement)• Statement of Functional Expenses (I’ll explain)• Statement of Cash Flows• Footnote disclosures

• Internal supplemental information (lists of donors, grant information/restricted funds, reserve calculations, capital campaigns or capital spending, budget to actual, etc.)

Balance Sheet – Assets

16

Balance Sheet – Liabilities & Net Assets

17

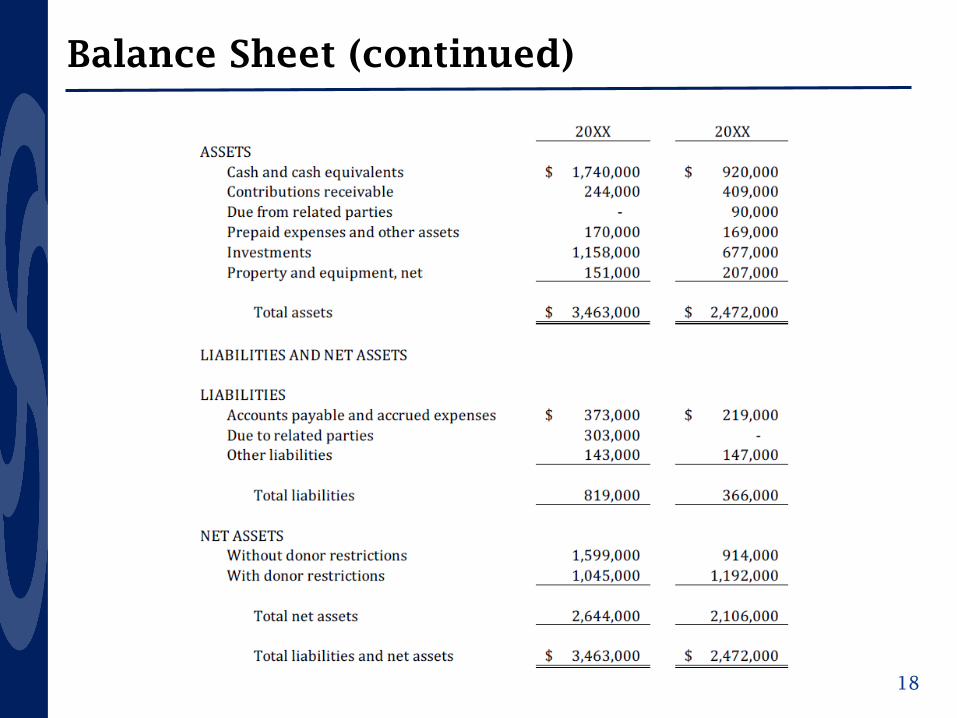

Balance Sheet (continued)

18

Statement of Activities

19

Statement of Functional Expenses

20

Statement of Functional Expenses (continued)

21

Functional Expense – Why do we care?

Stakeholders pay attention!

1) Watchdog Organizations

2) Board Members

3) Related Organizations

4) Membership6) Competitors

5) Federal Agencies 7) Donors 8) Auditors

22

Overview of ASU 2016-14

01

02

03

04

05

Expenses- Report expense by function and

nature- Analysis showing relationship by

function and nature

Cash Flows- Still allow for direct or indirect

method- No longer require indirect

reconciliation for direct method

Investment Return

- Investment return is now required to be presented net of direct internal and external investment expense

- No longer required to disclose netted expenses, although not precluded from including this disclosure

Net Asset Classification- Two, rather than three classes of

net assets- Underwater endowment

accounting changes and additional disclosure requirements

Liquidity and Availability

- Qualitative and quantitate disclosure

- Liquidity and availability of resources tied to PRNA, TRNA, and unrestricted and designated funds

4

1

5

3

2

The nonprofit financial statement presentation and disclosure standard (ASU 2016-14) is effective for year-ends beginning after December 15, 2017 (December 31, 2018 calendar year-ends).

23

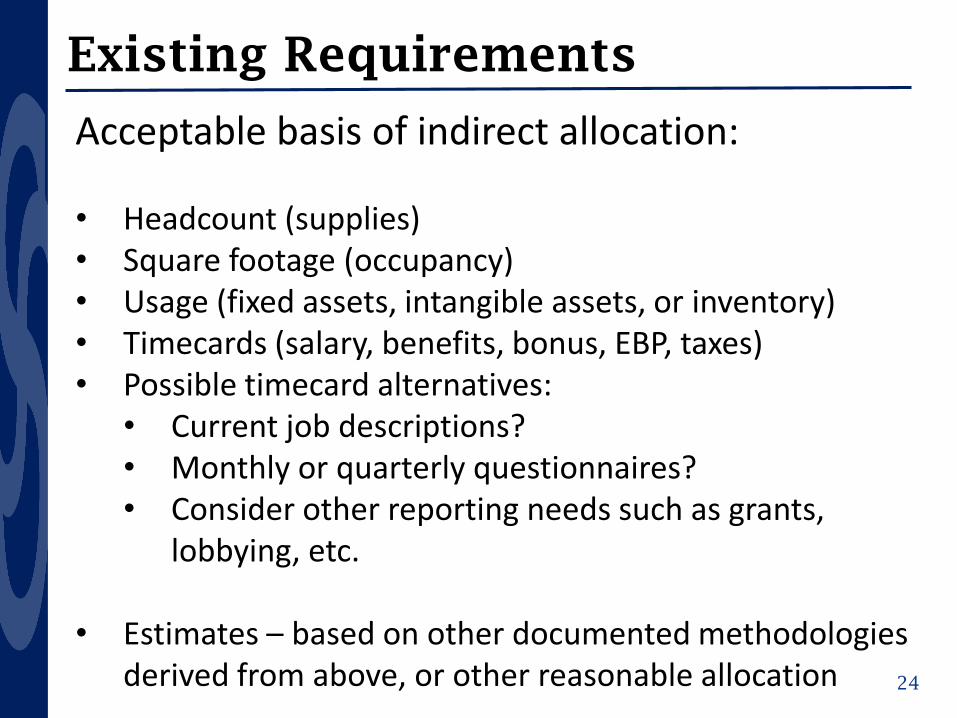

Existing Requirements

Acceptable basis of indirect allocation:

• Headcount (supplies)• Square footage (occupancy)• Usage (fixed assets, intangible assets, or inventory)• Timecards (salary, benefits, bonus, EBP, taxes)• Possible timecard alternatives:

• Current job descriptions?• Monthly or quarterly questionnaires?• Consider other reporting needs such as grants,

lobbying, etc.

• Estimates – based on other documented methodologies derived from above, or other reasonable allocation 24

M&G Per 990* M&G Per FASB/GAAP** M&G Per Fed***BOD meetings and committee meetings

Oversight, business management, and HR

Executive director

Office management General recordkeeping Personnel (oversight)

Staff meetings (unless program or fundraising specific)

Advertising and promoting sales Management information systems

Auditing Budgeting Budget and planning

HR, investment management, and other centralized services

Administering government, foundation, and similar contract’s billing and collection

Finance and business services

Annual report Annual report Safety and risk management

General legal services All other M&G except for direct conduct of programs, fundraising, or member development activities

General counsel

General liability insurance Informing public of NFP’s stewardship of funds

Expense Reporting – Definitions

* Per 990 Instructions ** Per ASU 2016-14 *** Per CFR Chapter II Part 200 Appendix IV (Indirect cost rate – M&G) 25

Financial Statements and Tax Return

26

Total Program M&G Fundraising(member development)

73% 11% 16%

82% 16% 2%

Hero Dogs

Pets for Vets

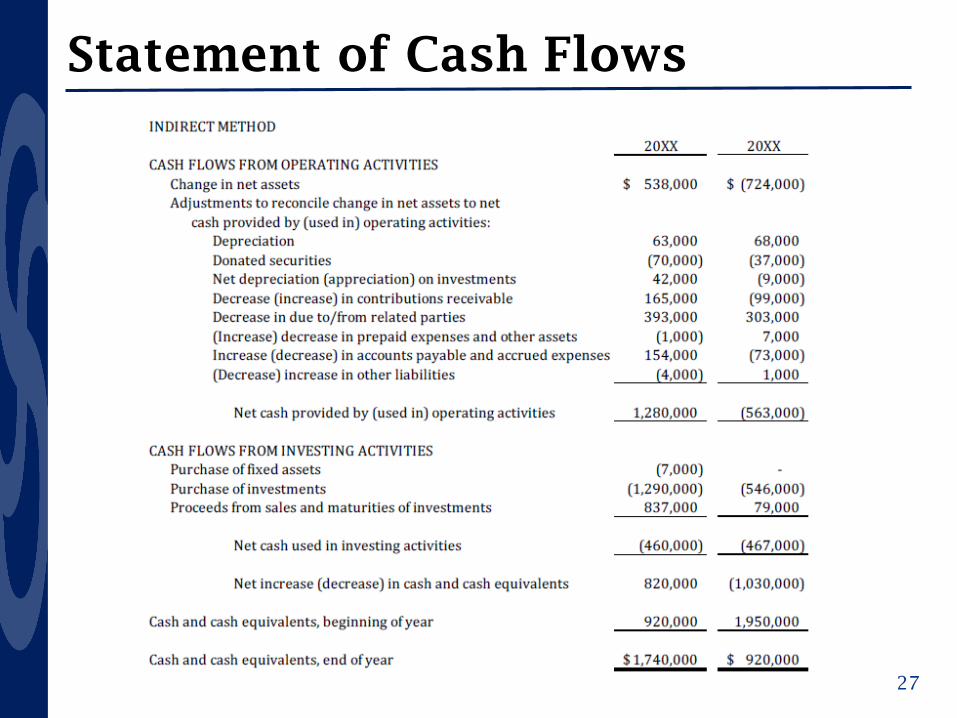

Statement of Cash Flows

27

Budgeting

28

Depends on your organization … but …• should align with both internal financial statements and

internal financial reports (by department)

Very different ways of budgeting

Zero-based BudgetingTraditional Budgeting

Top-Down BudgetingBottom-Up Budgeting

Budgeting

29

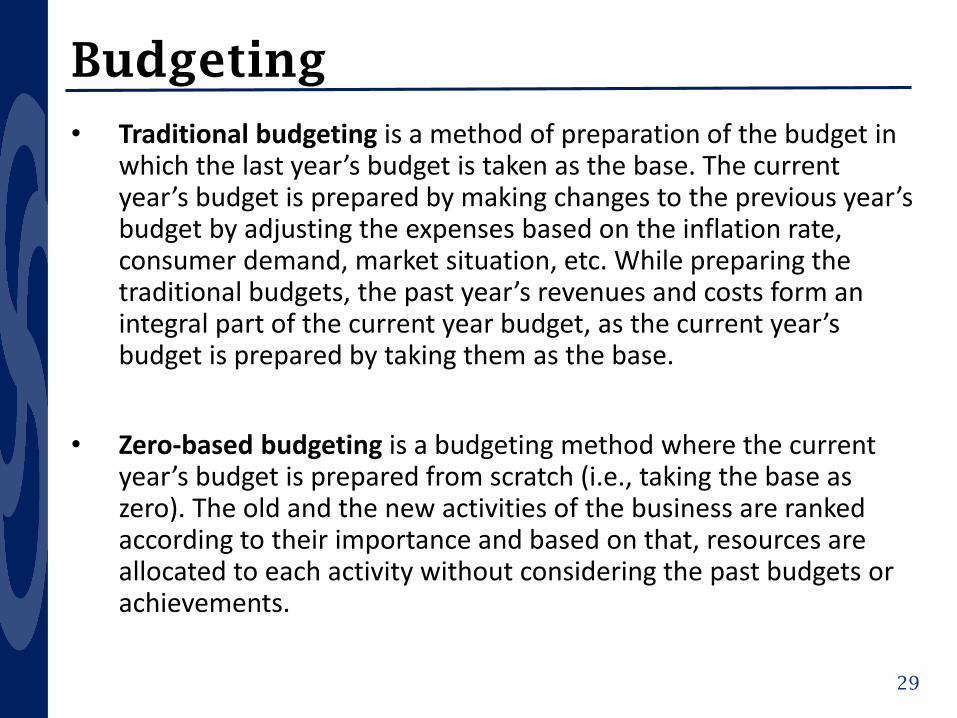

• Traditional budgeting is a method of preparation of the budget in which the last year’s budget is taken as the base. The current year’s budget is prepared by making changes to the previous year’s budget by adjusting the expenses based on the inflation rate, consumer demand, market situation, etc. While preparing the traditional budgets, the past year’s revenues and costs form an integral part of the current year budget, as the current year’s budget is prepared by taking them as the base.

• Zero-based budgeting is a budgeting method where the current year’s budget is prepared from scratch (i.e., taking the base as zero). The old and the new activities of the business are ranked according to their importance and based on that, resources are allocated to each activity without considering the past budgets or achievements.

Budgeting

30

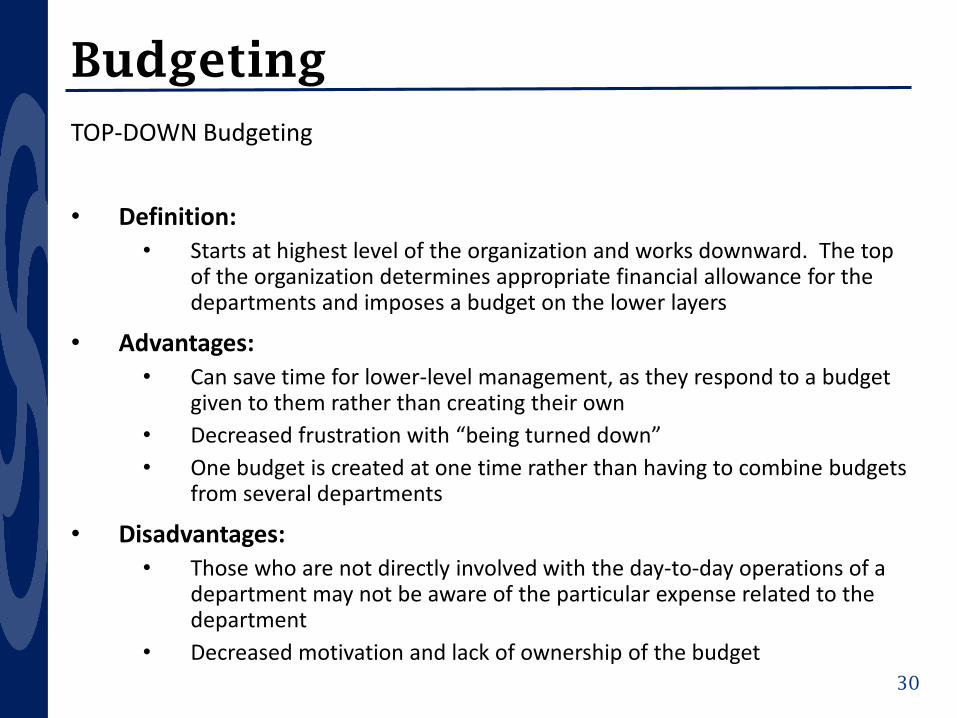

TOP-DOWN Budgeting

• Definition: • Starts at highest level of the organization and works downward. The top

of the organization determines appropriate financial allowance for the departments and imposes a budget on the lower layers

• Advantages:• Can save time for lower-level management, as they respond to a budget

given to them rather than creating their own• Decreased frustration with “being turned down”• One budget is created at one time rather than having to combine budgets

from several departments

• Disadvantages:• Those who are not directly involved with the day-to-day operations of a

department may not be aware of the particular expense related to the department

• Decreased motivation and lack of ownership of the budget

Budgeting

31

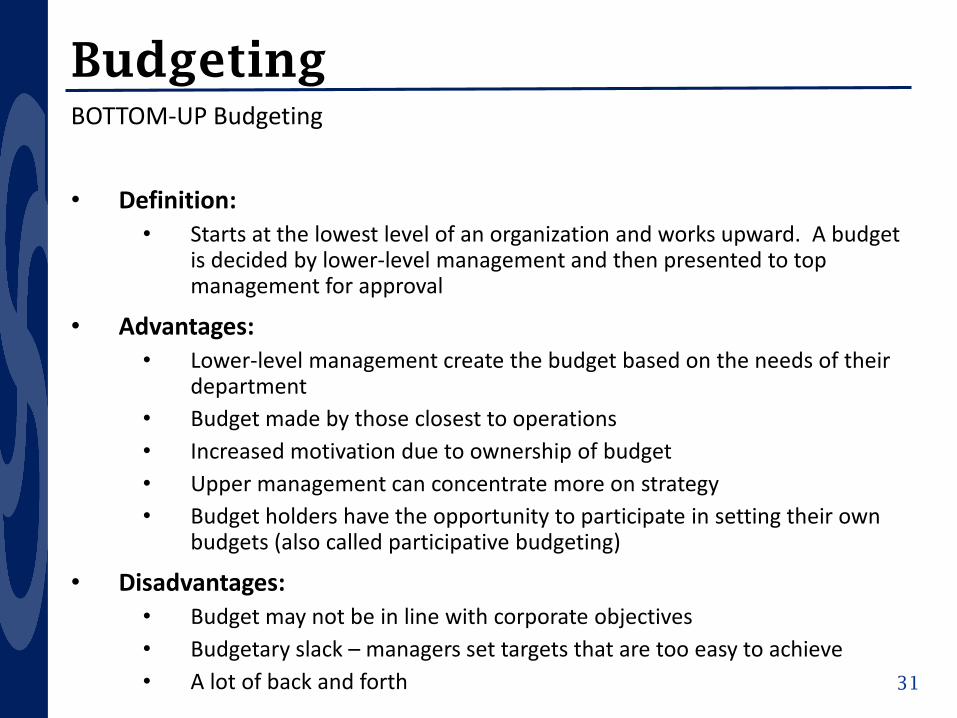

BOTTOM-UP Budgeting

• Definition: • Starts at the lowest level of an organization and works upward. A budget

is decided by lower-level management and then presented to top management for approval

• Advantages:• Lower-level management create the budget based on the needs of their

department• Budget made by those closest to operations• Increased motivation due to ownership of budget• Upper management can concentrate more on strategy• Budget holders have the opportunity to participate in setting their own

budgets (also called participative budgeting)

• Disadvantages:• Budget may not be in line with corporate objectives• Budgetary slack – managers set targets that are too easy to achieve • A lot of back and forth

History of Form 990

32

• Required since 1941 for all exempt organizations except political organizations (required since 2000)

• Evolved from a two-page form to nine pages with two supplemental schedules (A and B) in 2007

• IRS completely redesigned in 2008 with a three-year phase-in• New required thresholds for IRS Form 990, 990-EZ, and 990-N• Core Form with 12 parts (12 pages)• Can include 16 supplemental schedules (A–R)• Focus areas include:

1. Transparency 2. Governance and compliance3. Unrelated business income4. Compensation5. Related-party transactions6. Grants and contributions to individuals and domestic and international

organizations7. Lobbying and political activities

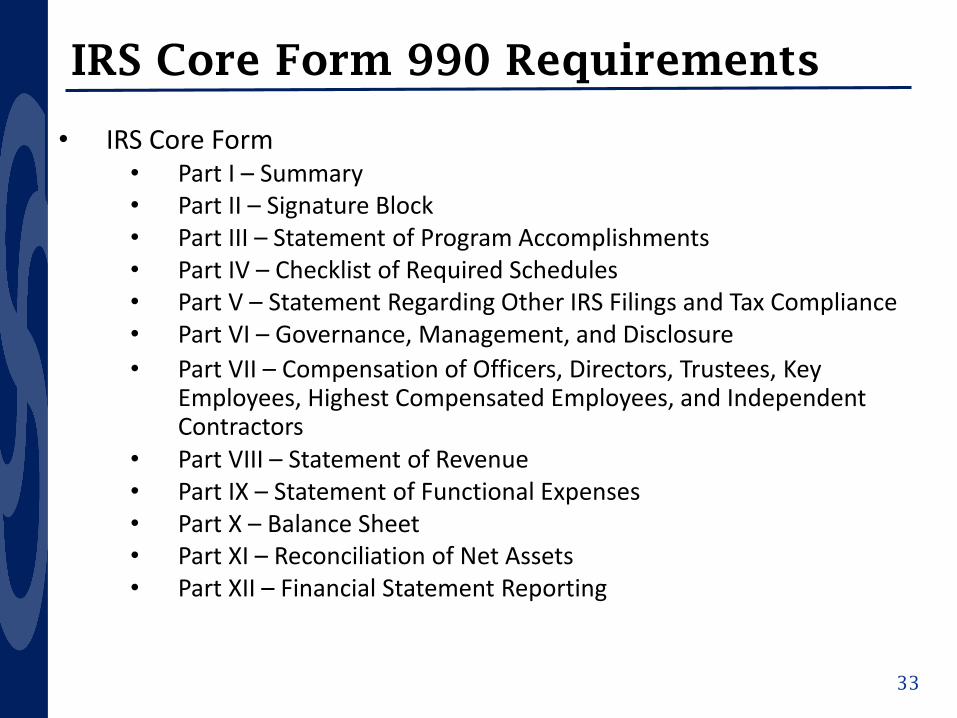

IRS Core Form 990 Requirements

33

• IRS Core Form• Part I – Summary • Part II – Signature Block• Part III – Statement of Program Accomplishments • Part IV – Checklist of Required Schedules• Part V – Statement Regarding Other IRS Filings and Tax Compliance• Part VI – Governance, Management, and Disclosure • Part VII – Compensation of Officers, Directors, Trustees, Key

Employees, Highest Compensated Employees, and Independent Contractors

• Part VIII – Statement of Revenue • Part IX – Statement of Functional Expenses • Part X – Balance Sheet• Part XI – Reconciliation of Net Assets• Part XII – Financial Statement Reporting

Form 990 – Part I: Summary

34

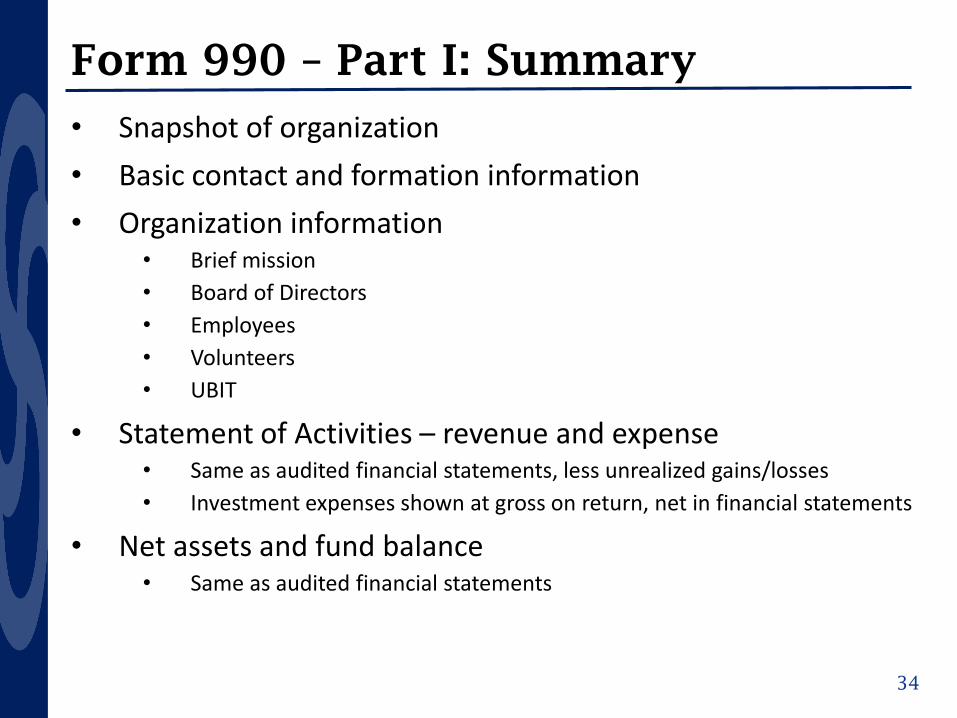

• Snapshot of organization • Basic contact and formation information• Organization information

• Brief mission• Board of Directors• Employees• Volunteers• UBIT

• Statement of Activities – revenue and expense• Same as audited financial statements, less unrealized gains/losses• Investment expenses shown at gross on return, net in financial statements

• Net assets and fund balance• Same as audited financial statements

Form 990 – Part I: Summary

35

Form 990 – Part II: Signature Block

36

• Officer of Organization signs the return

• Paid preparer, if applicable, signs here as well• Personal PTIN • Firm’s EIN• Issuing office address

Form 990 – Part III: Program Accomplishments

37

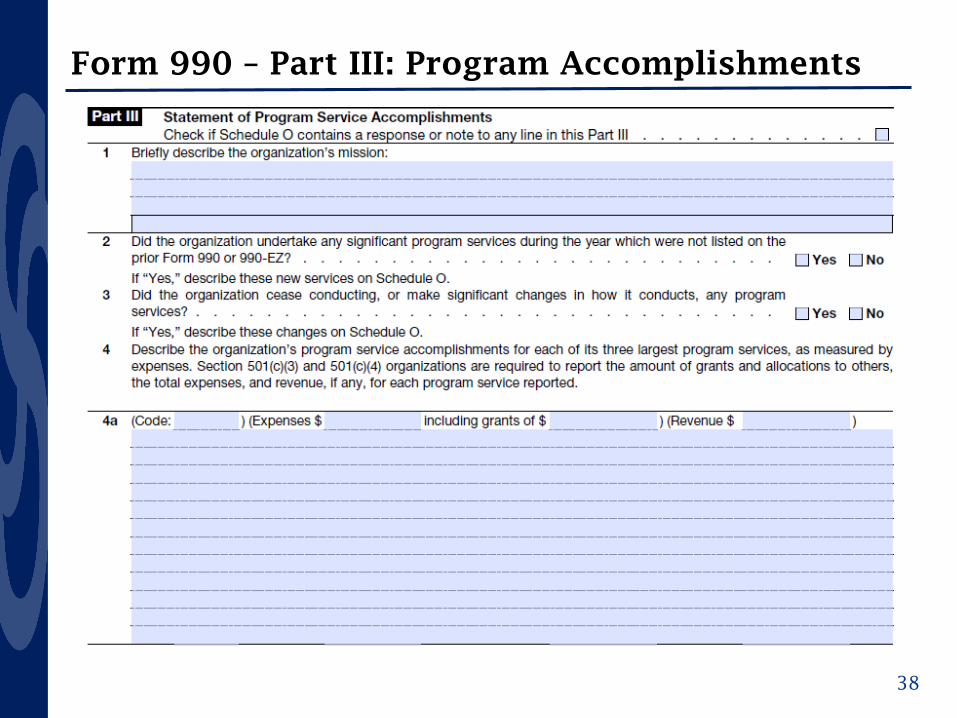

• Extended description of mission• New significant programs or change in existing programs• Describe three largest programs

• Only 501(c)(3) charitable organizations are required to include related to each program:

1. Revenue, 2. Expenses, and 3. Program code section

Form 990 – Part III: Program Accomplishments

38

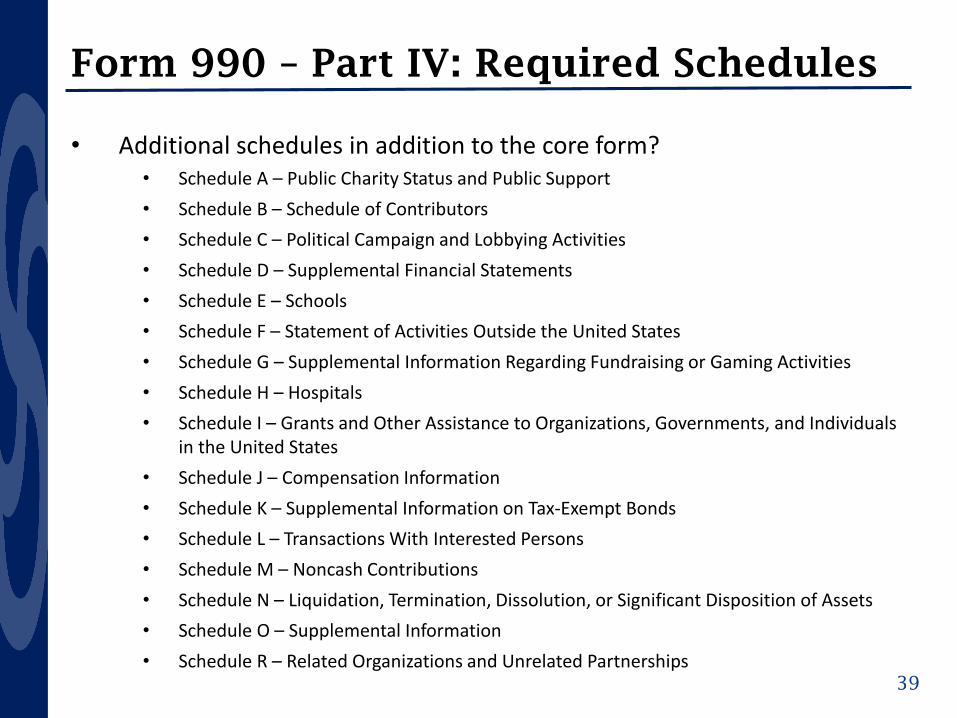

Form 990 – Part IV: Required Schedules

39

• Additional schedules in addition to the core form? • Schedule A – Public Charity Status and Public Support• Schedule B – Schedule of Contributors• Schedule C – Political Campaign and Lobbying Activities• Schedule D – Supplemental Financial Statements• Schedule E – Schools• Schedule F – Statement of Activities Outside the United States • Schedule G – Supplemental Information Regarding Fundraising or Gaming Activities• Schedule H – Hospitals • Schedule I – Grants and Other Assistance to Organizations, Governments, and Individuals

in the United States• Schedule J – Compensation Information• Schedule K – Supplemental Information on Tax-Exempt Bonds • Schedule L – Transactions With Interested Persons • Schedule M – Noncash Contributions • Schedule N – Liquidation, Termination, Dissolution, or Significant Disposition of Assets • Schedule O – Supplemental Information • Schedule R – Related Organizations and Unrelated Partnerships

Form 990 – Part V: Filings and Tax Compliance

40

• Independent contractors • 1099s/1096

• Employees • W2s/W3

• UBIT, foreign bank accounts, tax shelters, etc.• Tanning facilities??? • Other tax situations – many not applicable

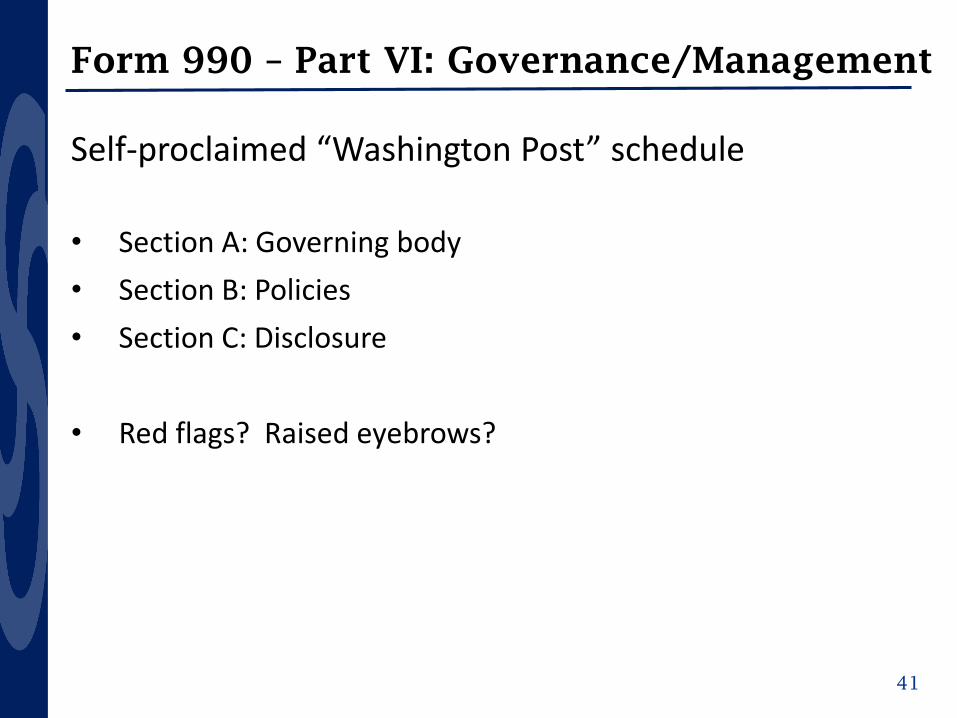

Form 990 – Part VI: Governance/Management

41

Self-proclaimed “Washington Post” schedule

• Section A: Governing body• Section B: Policies• Section C: Disclosure

• Red flags? Raised eyebrows?

Form 990 – Part VI: Governance/Management

42

Form 990 – Part VI: Governance/Management

43

Form 990 – Part VII: Compensation

44

• Includes officers, directors, trustees, key employees, highest compensated employees and independent contractors

• Directors and trustees• Officers (bylaws and top management and finance individual)• Key employees – three-prong test

1. Compensation2. Responsibility3. Top 20

• Highly compensated employee (HCE) – two-prong test 1. Compensation2. Next five after key employees

• Former of any of the above – one-prong test1. Compensation

• Independent contractors – three-prong test1. Compensation paid for services (does not have to be a 1099 vendor)2. Top five3. Not specifically exempted

Form 990 – Part VII: Compensation

45

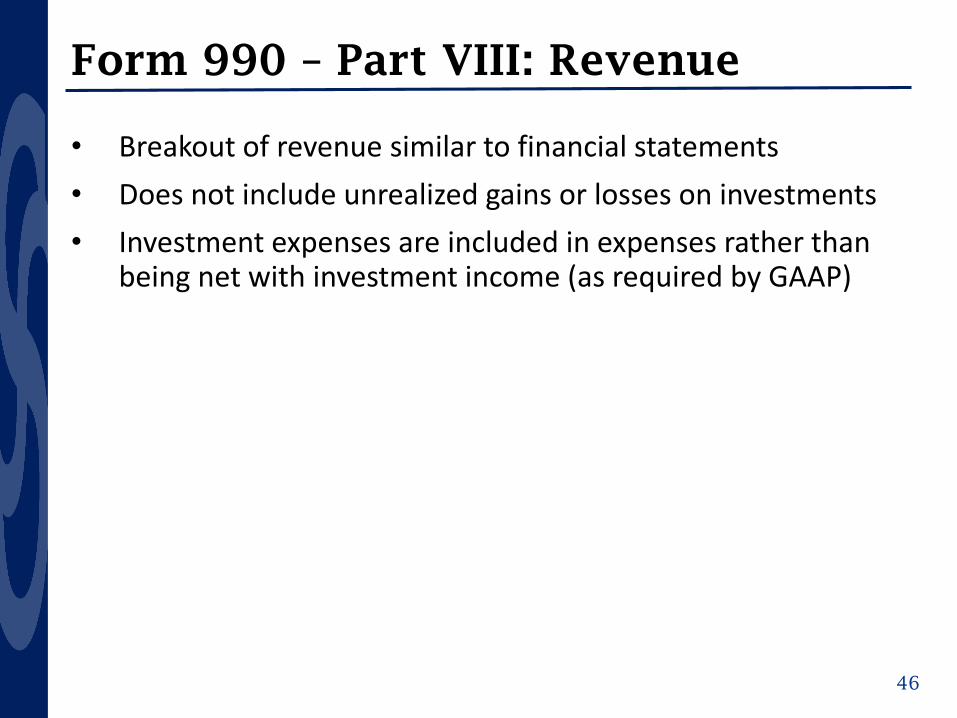

Form 990 – Part VIII: Revenue

46

• Breakout of revenue similar to financial statements• Does not include unrealized gains or losses on investments• Investment expenses are included in expenses rather than

being net with investment income (as required by GAAP)

Form 990 – Part IX: Functional Expenses

47

• Agrees to financial statements with one exception• Investment expenses are gross rather than net with investment income (as required

by GAAP)

• Non-501(c)(3) exempt organizations are not required to report by function—just by natural classification

Form 990 – Part X: Balance Sheet

48

• Mirrors audited financial statements

Form 990 – Part XI: Net Assets

• Reconciles between tax return and audited financial statements

Form 990 – Part XII: Reporting

• Accrual vs. cash method• Separate or consolidated audits• Audit Committee• A-133/Uniform Guidance audit requirement

The Audit (and Tax) Process

49

• Are you happy with your current auditor relationship?• Do your auditors participate in discussions throughout the

year?• Are you billed on a per-hour or flat fee basis?• Are deadlines being met, and if not … is that delay a result of

auditor issues or internal delays?• Do you feel like you go through two audits … one for your

financial statements and one for your tax return?• What other issues might you have faced?

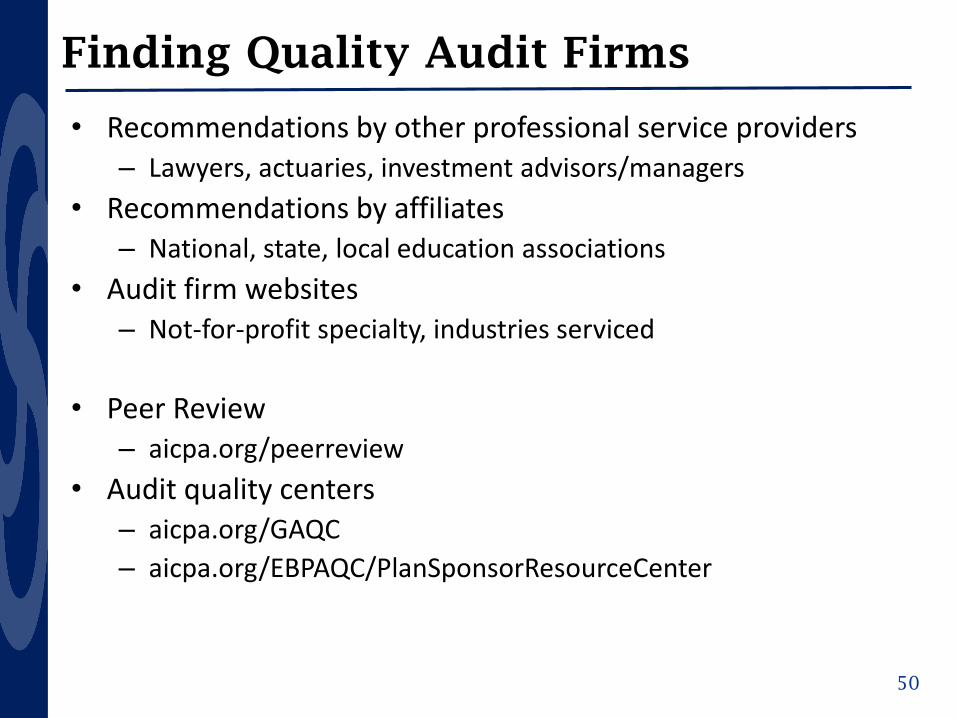

Finding Quality Audit Firms

50

• Recommendations by other professional service providers– Lawyers, actuaries, investment advisors/managers

• Recommendations by affiliates– National, state, local education associations

• Audit firm websites– Not-for-profit specialty, industries serviced

• Peer Review– aicpa.org/peerreview

• Audit quality centers– aicpa.org/GAQC– aicpa.org/EBPAQC/PlanSponsorResourceCenter

Preparing a Request for Proposal (RFP)

51

• Determine your needs – based on type of entity, financial landscape, and regulatory environment– Audit, Review, Compilation, Agreed-Upon Procedures– Tax (Form 990, 990-EZ, 990-N, 990-T)– Compliance (DOL forms; annual state filings; forensic

investigations, Uniform Guidance) – Additional Considerations:

• Issues specific to your nonprofit code• Consolidations

– Other entities under common control (political orgs, other (c)(3) foundations, for-profits, etc.)

• Other industry expertise (EBPs, operations, etc.)

Preparing a Request for Proposal (RFP)

52

• Overview of your organization and reporting structure• Relationship with prior audit firm and reason for issuing RFP• Key contacts for asking and responding to questions • Fees

• Travel and other expenses billed separately?

• Auditor qualifications and background (following slides)– Education and expertise– History and experience – Use of technology

Preparing a Request for Proposal (RFP)

53

• How long has the firm been in business?• How many clients does it service?

– In total– Specific to my industry

• What services does the firm offer other than audit and tax?• How many employees does the firm have?

– Partners/Principals, directors, managers, seniors, staff, admin support– Capabilities to manage the account? Overcommitted? Overworked?– Turnover at various levels?

• In what states is the firm licensed to operate?• Where is the firm located and what are its remote audit capabilities?• What do the firm’s other clients have to say about the firm?

– Check references

Board and/or Audit Committee Involvement

54

• Ultimately, your auditors report to those charged with governance – whether the Board or a committee to act on behalf of the Board

• Every organization is different – not one size fits all– Board of Directors– Audit Committee– Finance Committee– Administrative Committee

• Involvement in initial interviews and assessment• Best and final presentations• Decision

Comparative Analysis

Includes:

1) Organization

2) Comparative Organizations (24)

3) Peer Group (5)

Benchmarking

Footnote

55

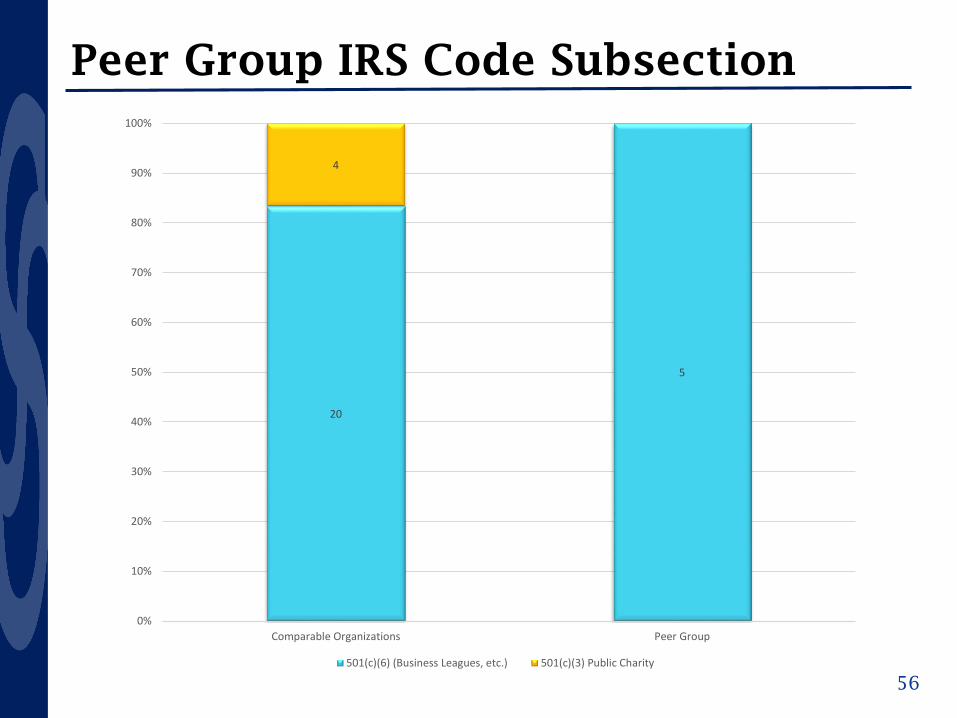

Peer Group IRS Code Subsection

56

20

5

4

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Comparable Organizations Peer Group

501(c)(6) (Business Leagues, etc.) 501(c)(3) Public Charity

General Statistics – Employees

57

0

5

10

15

20

25

30

35

40

45

American Board Of Ophthalmology Comparable Organizations (Average) Peer Group (Average)America’s XYZ Industry Association

Statement of Financial Position

58

$- $5,000,000 $10,000,000 $15,000,000 $20,000,000 $25,000,000 $30,000,000 $35,000,000 $40,000,000

Total Assets

Total Liabilities

Toal Net Assets

Peer Group (Average) Comparable Organizations (Average) American Board Of OphthalmologyAmerica’s XYZ Industry Association

Asset Composition

59

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

American Board Of Ophthalmology Comparable Organizations (Average) Peer Group (Average)

Cash & Cash Equivilents Investments Other Assets

America’s XYZ Industry Association

Net Asset Composition

60

99%

99%

99%

100%

100%

100%

American Board Of Ophthalmology Comparable Organizations (Average) Peer Group (Average)

Unrestricted Net Assets Temporarily Restricted Net Assets Permanently Restricted Net Assets

America’s XYZ Industry Association

Reserve Analysis

61

0.0 5.0 10.0 15.0 20.0 25.0 30.0 35.0 40.0 45.0

Months of cash

Months of cash and investments

Months of estimated liquid unrestricted net assets

Peer Group (Average) Comparable Organizations (Average) American Board Of OphthalmologyAmerica’s XYZ Industry Association

Statement of Activities

62

$(100,000) $1,900,000 $3,900,000 $5,900,000 $7,900,000 $9,900,000 $11,900,000

Total Revenue

Total Expense

Change in Net Assets

Peer Group (Average) Comparable Organizations (Average) American Board Of OphthalmologyAmerica’s XYZ Industry Association

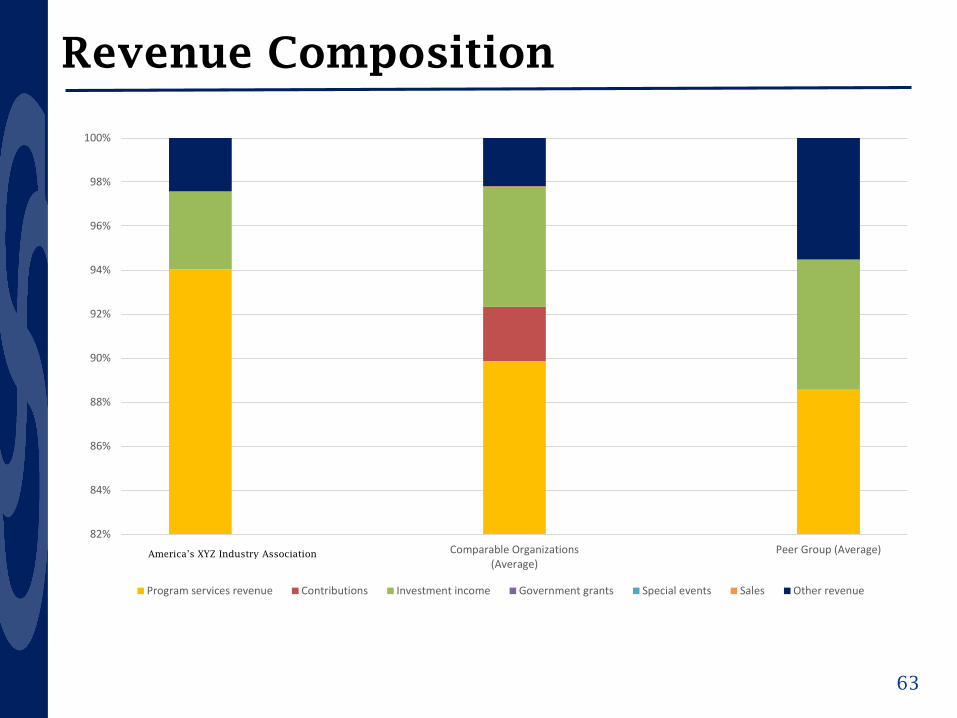

Revenue Composition

63

82%

84%

86%

88%

90%

92%

94%

96%

98%

100%

American Board OfOphthalmology

Comparable Organizations(Average)

Peer Group (Average)

Program services revenue Contributions Investment income Government grants Special events Sales Other revenue

America’s XYZ Industry Association

Unrelated Business Income

64

21%

79%

Comparable Organizations

Organizations withUnrelated BusinessIncome (UBI)

Organizations withoutUnrelated BusinessIncome (UBI)

40%

60%

Peer Group

Expense Composition (As a percentage of total expenses)

65

0.6%

0.6%

1.2%

0.7%

0.9%

46.6%

4.7%

3.2%

41.5%

0.7%

0.3%

5.8%

1.1%

0.4%

2.0%

0.7%

39.8%

2.9%

3.5%

42.8%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Accounting Fees

Advertising Expenses

Information Technology Expenses

Insurance Expenses

Interest Expenses

Investment Management Fees

Legal Fees

Personnel

Pension Plan Contributions / Employee Benefits

Occupancy

Printing and Publications

Professional Fundraising Expenses

All other expense

American Board Of Ophthalmology Peer Group (Average)America’s XYZ Industry Association

Select Ratio Analysis

66

0.00% 0.10% 0.20% 0.30% 0.40% 0.50% 0.60% 0.70% 0.80%

Investment Management Fee as a Percentage of Investment Balance

Peer Group (Average) Comparable Organizations (Average) American Board Of Ophthalmology

0.0% 0.5% 1.0% 1.5% 2.0% 2.5% 3.0% 3.5%

Investment Return/Loss as a Percentage of Investment Balance

Peer Group (Average) Comparable Organizations (Average) American Board Of Ophthalmology

30.0% 32.0% 34.0% 36.0% 38.0% 40.0% 42.0% 44.0% 46.0% 48.0% 50.0%

Personnel and IT Expenses as a Percentage of Total Expenses

Peer Group (Average) American Board Of OphthalmologyAmerica’s XYZ Industry Association

America’s XYZ Industry Association

America’s XYZ Industry Association

67

Questions?