natenberg _ weithers rmc 2010 notes.pdf

TRANSCRIPT

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 1/50

Material prepared by

Sheldon Natenberg and Tim Weithers

Chicago Trading Co.

141 West Jackson Blvd.

Chicago, IL 60604

tel. 1 312 863 [email protected]

Equity-Related Volatility Skew

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 2/50

Equity-Related Volatility Skew

Option Models and the Real World

Modelling the Skew

Skew Risk and Changing Market Conditions

Skew Sensitive Trading Strategies

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 3/50

Skew: What is it?“Skew” means different things to different people:

To an Option Trader:

the directional bias (with respect to the underlyingasset’s price) reflected in option market prices

How measured (and relative to what baseline)?

Usually discussed in terms of “implied volatility”.

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 4/50

Theoretical Option Valuation

σ

Black-Scholes

European

Call OptionValuation

Model

Theoretical

ValuesC , P

S

X

rt

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 5/50

Implied (Market) Volatility

Black-Scholes

European

Call OptionValuation

Model

Option

Market

Prices

C , P

S

X

rtImplied σ

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 6/50

If Black-Scholes were “true”

(that is, if the real world aligned with the assumptions)

25%

Low X High XATM

Implied

Volatility

For all options with

the same expirationon the same underlying,

the implied volatility

would be a constant.

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 7/50

Implied Volatility

The CBOE has indicated that

“The average level of the implied volatility curvereflects the average volatility expected by the market.”

In this sense, implied volatility (to a certain expiration)can be thought of as the market’s expectation of

future volatility (between now and that expiration date).

But there are lots of options out there . . .

(obviously with options having different expirations,

there can be different implied volatilities, but . . . )

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 8/50

The Volatility “Smile”

Consider an underlying asset (like the S&P 500 or IBM stock). There are many options listed/traded.

The 3 month-expiration options trade on differentimplied volatilities depending on the strike price.

How can the market simultaneously have differentexpectations for how the S&P 500 or IBM stock will fluctuate over the next three months?

The plot of implied volatility versus strike priceis called the “Volatility Smile” or “Vol Skew”.

There is also a term structure of volatility.

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 9/50

Typical Volatility Smile in Indexes

25%

Low X High XATM

Implied

Volatility

28%

22%

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 10/50

Actual Volatility Smile in S&P 500

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 11/50

Actual Volatility Smile in IBM

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 12/50

Option Trader’s View of SkewWhy is there “skew”?

Demand and Supply

The world is “long stock”

so the world wants protection (buys OTM Puts)

and the world attempts to outperform the

competition (sells OTM Calls – yield enhancement,

an income strategy)

and sometimes does both simultaneously (Collars)

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 13/50

As a result of buying OTM Puts

and selling OTM Calls , . . .

25%

Low X High XATM

Implied

Volatility

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 14/50

The Market Is Not StupidThe market remembers:

Stocks tend to fall faster than they rise.

(This is an empirical statement.)

Even if this isn’t true (but people believe it), explains

the interest in purchasing Puts (relative to Calls).

Puts over Calls

(holding something constant: 20% OTM, 10Δ,…)

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 15/50

Why is there an Equity Skew?

(Low-Strike) Puts [Protective Put Strategy] are bid.

(High-Strike) Calls [Covered Calls, Over-Writes,

Buy-Writes Strategy] are offered.

Just the result of people buying and selling options.

What about other product areas?

Is the world long Yen?

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 16/50

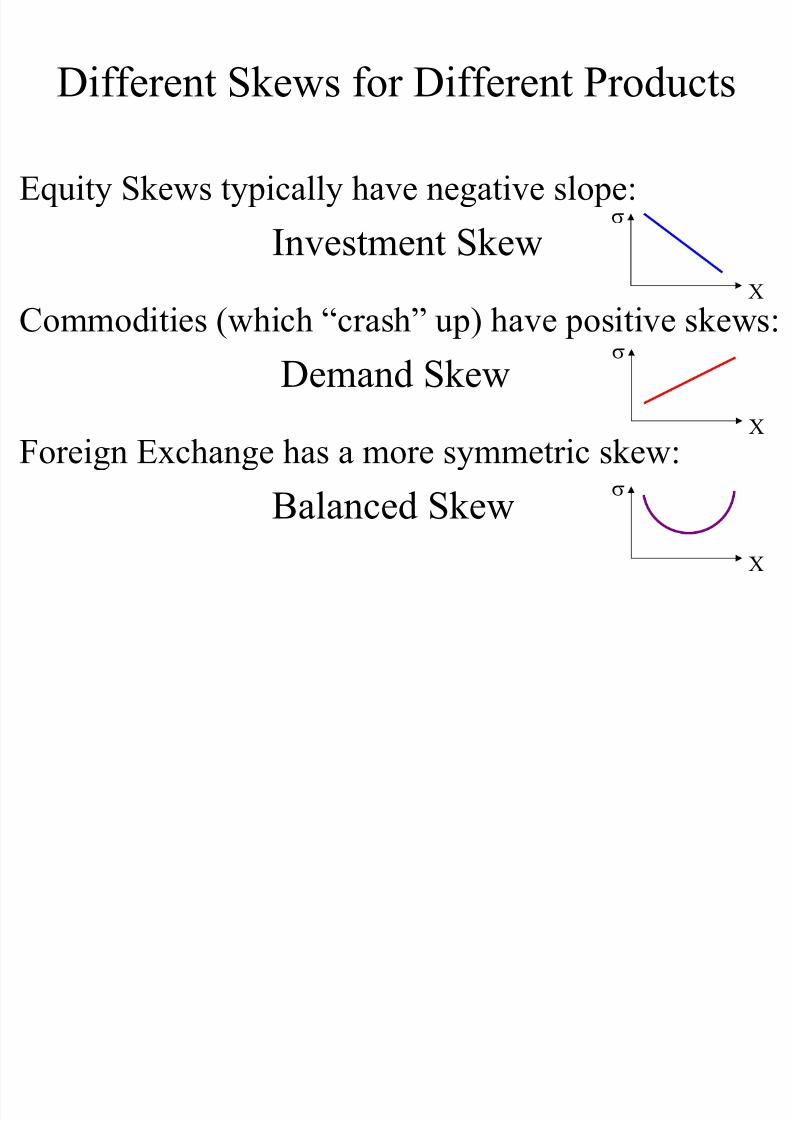

Different Skews for Different Products

Equity Skews typically have negative slope:

Investment Skew

Commodities (which “crash” up) have positive skews:

Demand Skew

Foreign Exchange has a more symmetric skew:

Balanced Skew

σ

X

σ

X

σ

X

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 17/50

Actual Volatility Smiles in Commodities

Soybeans Coffee

Sugar Orange Juice

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 18/50

Actual Volatility Smile in FX (USD|JPY)

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 19/50

Skew: What is it?

“Skew” means different things to different people:

To a Financial Engineer:

the market phenomenon which results from using

a model which, like all models, is not correct.

In other words, the model assumes a probability

distribution (more precisely, a probability densityfunction) for the future price distribution of theunderlying (lognormal) – which is “wrong”!

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 20/50

What’s in the Black(-Scholes) Box?

σ

Black-Scholes

European

Call Option

ValuationModel

Theoretical

Value

S

X

r

t

S

probability distribution

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 21/50

Baseline Distribution

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 22/50

Kurtosis

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 23/50

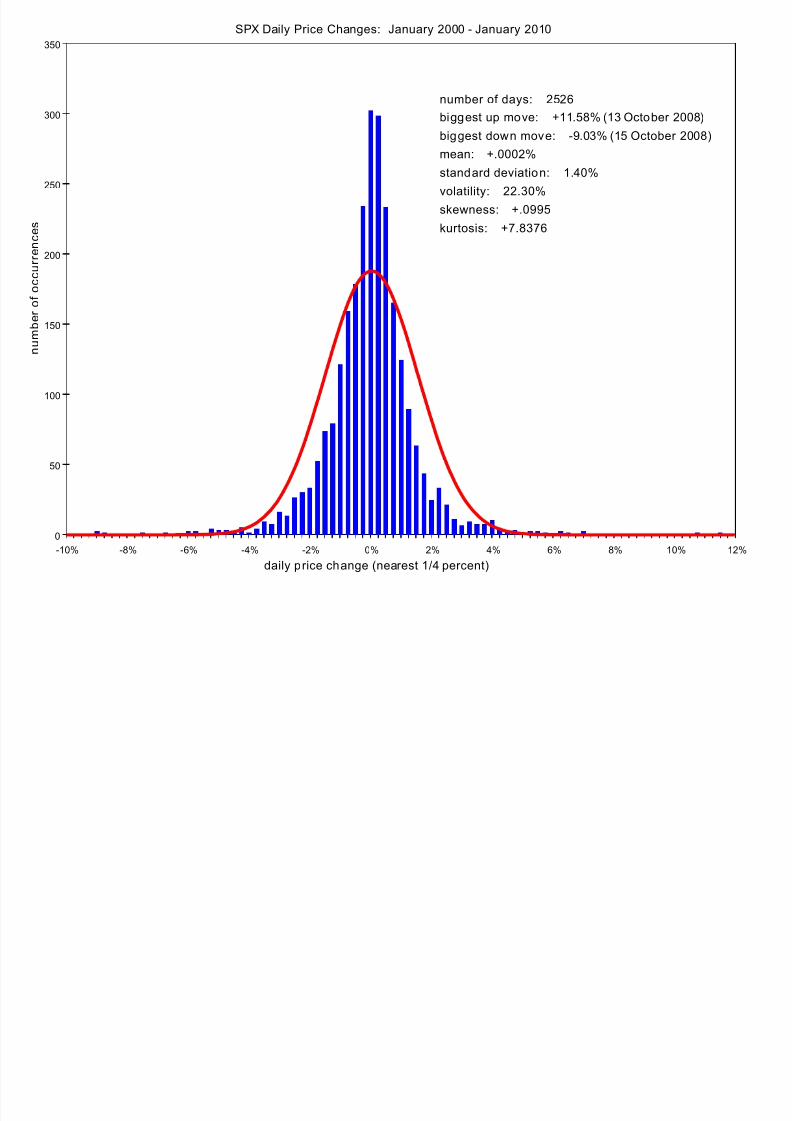

Skew

SPX Daily Price Changes: January 2000 - January 2010

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 24/50

SPX Daily Price Changes: January 2000 January 2010

0

50

100

150

200

250

300

350

-10% -8% -6% -4% -2% 0% 2% 4% 6% 8% 10% 12%

daily price change (nearest 1/4 percent)

n u m b e r

o f o c c u r r e n c e s

number of days: 2526

biggest up move: +11.58% (13 October 2008)

biggest down move: -9.03% (15 October 2008)

mean: +.0002%

standard deviation: 1.40%

volatility: 22.30%

skewness: +.0995kurtosis: +7.8376

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 25/50

Prices are assumed to follow

a Lognormal Distribution

So, really, “skewed” relative to this . . .

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 26/50

Skew: What is it?

“Skew” means different things to different people:

To a Risk Manager:

the relationship between movements in the

underlying asset price and implied volatilitiesWhat will happen to implied volatility as the underlying

price goes down or goes up (and possibly goes down

or up slowly versus goes down or up quickly)?

Market implied volatility is a function of spot price:σ

(S)

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 27/50

Modelling the Skew: What Do You Believe?

Skew is “real” in that it impacts your mark-to-market.

What this means is that in order to “risk manage”a portfolio containing options, you have totake the skew into account . . . and, ultimately,

to be systematic, consistent, robust, . . .you will want to formally “model the skew.”

Volatility by Moneyness (ATM, 10% OTM vol constant)Volatility by Strike (Sticky Strike: vol by strike constant)

Volatility by Delta (Sticky Delta: vol by Delta constant)

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 28/50

And How Do You Manage It?

You can’t just ignore skew; you have to “model” it.

Skew can and will change.

Based on your view on skew,some trades may look attractive

(or more attractive than others).

Shelly: How to model skew?

What is a skew trade?

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 29/50

i m p l i e d v o l a t i l i t

y

exercise price

We need a method of describing

the shape of the skew.

f(x)

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 30/50

In order to model option values and

determine the risk of a position we

need to know how changes in market

conditions will affect…

the location of the skew

the shape of the skew

h ill h i h d l i i

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 31/50

i m p l i e d v o l a t i l i t y

90 exercise price

underlying

price

100 120

What will happen if the underlying price

changes?

105

Will the implied volatility at

at each exercise price remain unchanged?

sticky strike

Wh ill h if h d l i i

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 32/50

i m p l i e d v o l a t i l i t y

90 120

What will happen if the underlying price

changes?

underlying

price

105

Will the implied volatility at

at each exercise price remain unchanged?

sticky strike floating skew

Wh ill h if i li d

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 33/50

100

i m p l i e d v o l a t i l i t y

90

underlying

price

120

What will happen if implied

volatility changes?

floating skew

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 34/50

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 35/50

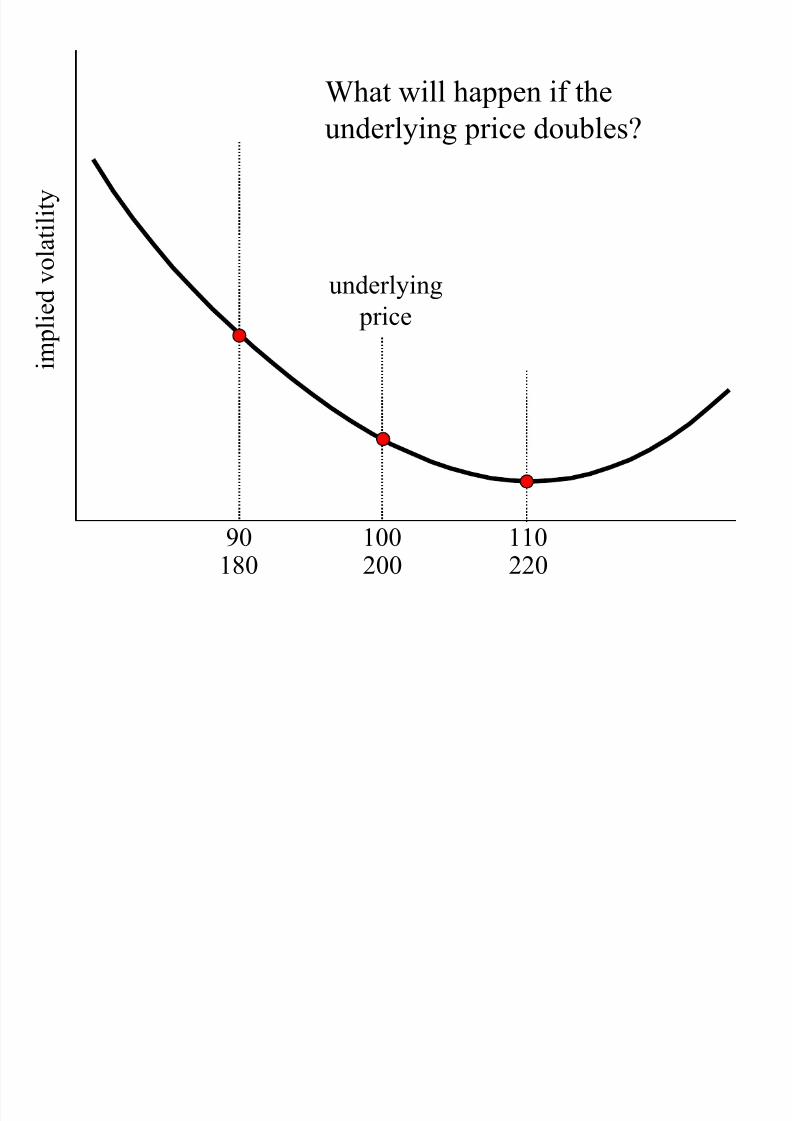

190

i m p l i e d v o l a t i l i t y

underlying

price

200180

What will happen if the

underlying price doubles?

210 220

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 36/50

ln (X / S)

i m p l i e d v o l a t i l i t y

underlying

price

What will happen if the

underlying price doubles?

How will the passage of time

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 37/50

90

i m p l i e d v o l a t i l i t y

3 month

skew

100

underlying

price

What will happen to the implied

volatility of the 90 put if it goes

further out-of-the-money?

How will the passage of time

affect the shape of the skew?

How will the passage of time

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 38/50

90

i m p l i e d v o l a t i l i t y

3 month

skew

100

underlying

price

p g

affect the shape of the skew?

Is the 90 put further out-of-the-money

with three months to expiration or

one month to expiration?

1 monthskew

How will the passage of time

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 39/50

i m p l i e d v o l a t i l i

t y

exercise price

less time

to expiration

more time

to expiration

p g

affect the shape of the skew?

How will the passage of time

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 40/50

ln (X / S) / sqrt (t)

i m p l i e d v o l a t i l i

t y

less time

to expiration

more time

to expiration

p g

affect the shape of the skew?

55%

SPX Implied Volatility Skews – 29 January 2010

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 41/50

10%

15%

20%

25%

30%

35%

40%

45%

50%

55%

500 600 700 800 900 1000 1100 1200 1300 1400 1500

exercise price

i m

p l i e d v o l a t i l i t y

Feb

Mar

Jun

Dec

50%

SPX Implied Volatility Skews – 29 January 2010

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 42/50

10%

15%

20%

25%

30%

35%

40%

45%

-1.3 -1.2 -1.1 -1 -0.9 -0.8 -0.7 -0.6 -0.5 -0.4 -0.3 -0.2 -0.1 0 0.1 0.2 0.3 0.4 0.5

ln(X/S)/sqrt(t)

i m

p l i e d v o l a t i l i t y

Feb

Mar

Jun

Dec

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 43/50

i m

p l i e d v o l a t i l i t y

new implied

volatility

current implied

volatility

exercise price exercise price

How do changes in the

skew affect the “Greeks”?

The underlying price

moves up.

underlying price = 100.00

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 44/50

implied volatility = 26.0%95 put = 2.00

u de y g p ce 00.00

implied delta = -25

underlying price rises to 10195 put ≈ 2.00 - (.25 x 1.00) = 1.75

shifted implied volatility = 27.0%vega of 95 put = .07

95 put≈

1.75 + (1 x .07) = 1.82delta of 95 put = (1.82 - 2.00) / (101 - 100) = -.18

adjusted or skewed delta = -18

underlying price = 100.00

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 45/50

implied volatility = 21%105 call = 2.30

implied delta = 17

underlying price rises to 101105 call ≈ 2.30 + (.17 x 1.00) = 2.47

shifted implied volatility = 20.5%vega of 105 call = .16

105 call≈

2.47 - (.5 x .16) = 2.39delta of 105 call = (2.39 - 2.30) / (101 - 100) = .09

adjusted or skewed delta = 9

y g p

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 46/50

i m

p l i e d v o l a t i l i t y

current implied

volatility

exercise price

How do changes in the

skew affect the “Greeks”?

Time passesnew implied

volatility

underlying price = 100.00

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 47/50

implied volatility = 26.0%95 put = 2.00

y g p

implied theta = -.08

One day passes95 put ≈ 2.00 - .08 = 1.92

shifted implied volatility = 26.3%vega of 95 put = .07

95 put = 1.92 + (.3 x .07)≈

1.94theta of 95 put = (1.94 - 2.00) = -.06

adjusted or skewed theta = -.06

Theoretical Pricing Model

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 48/50

Theoretical Pricing Model

Exercise Price

Time to Expiration

Underlying Price

Interest Rate

Volatility

Skew

theta

delta

rho

gamma / vega

skew sensitivity

f(x) f(a,b,…,x)

Skew Strategies – Buy o-t-m calls (puts)

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 49/50

g

i m p l i

e d v o l a t i l i t y

exercise price

futures

price

y (p )

and sell o-t-m puts (calls). Sell (buy)

futures.Entire position

should be deltaand vega neutral.

Kurtosis Strategies – Buy (sell) o-t-m calls

7/27/2019 Natenberg _ Weithers RMC 2010 notes.pdf

http://slidepdf.com/reader/full/natenberg-weithers-rmc-2010-notespdf 50/50

i m p l i

e d v o l a t i l i t y

exercise price

futures

price

g y ( )

and puts. Sell (buy) a-t-m calls and puts.

Entire position

should be deltaand vega neutral.