morgan stanley light s.a.: overview & brazil utilities ...ri.light.com.br/ptb/7413/light s.a....

TRANSCRIPT

1

Morgan Stanley

Brazil Utilities Corporate Access DayLight S.A.: Overview & Strategy

September, 2018

2

Important Notice

This presentation may include declarations that represent forward-looking statements according to

Brazilian regulations and international movable values. These declarations are based on certain

assumptions and analyses made by the Company in accordance with its experience, the economic

environment, market conditions and future events expected, many of which are out of the Company’s

control. Important factors that can lead to significant differences between the real results and the future

declarations of expectations on events or business-oriented results include the Company’s strategy, the

Brazilian and international economic conditions, technology, financial strategy, developments of the public

service industry, hydrological conditions, conditions of the financial market, uncertainty regarding the

results of its future operations, plain, goals, expectations and intentions, among others, Because of these

factors, the Company’s actual results may significantly differ from those indicated or implicit in the

declarations of expectations on events or future results.

The information and opinions herein do not have to be understood as recommendation to potential

investors, and no investment decision must be based on the veracity, the updated or completeness of this

information or opinions. None of the Company’s assessors or parts related to them or its representatives

will have any responsibility for any losses that can elapse from the use or the contents of this presentation.

This material includes declarations on future events submitted to risks and uncertainties, which are based

on current expectations and projections on future events and trends that can affect the Company’s

businesses. These declarations include projections of economic growth and demand and supply of energy,

in addition to information on competitive position, regulatory environment, potential growth opportunities

and other subjects. Various factors can adversely affect the estimates and assumptions on which these

declarations are based on.

3

SP

76 5

8

RJ

Rio Paraíba

do Sul

4

1 Amazônia Energia

2 Renova

3 Guanhães Energia

4 HPP Ilha dos Pombos

5 SHPP Paracambi

6 Complexo de Lajes

7 HPP Santa Branca

8 HPP Itaocara I

Generation

Light LightComLight SESA A B

25,846 GWh (2017)

Total Billed Market

4.5 mm

Clients

R$ 8.5 bn

Net RAB

31

Municipalities Served

1,028 MW1

Installed Capacity

74

# of HPPs

R$ 207 / MWh3

Average Sales Price

7,243 GWh in 2017

Commercialized Energy

Notes:

1 855 MW of total installed capacity are in full control of the company

2 Proportional to Light’s stake

3 Considers the average price for the 2016-2022 period, net of taxes

4 Considers only HPPs in which Light has full control

11 mm

People Served

11,000 sq. km

Area Coverage

Distribution Generation + Commercialization

686 MWavg2

Assured Energy

1

3

2

Well positioned in distribution & generation segments

4

Light SESA: distribution segment

The distribution segment accounted for 86.8% of Light’s Consolidated Net Revenues and 75% of Adj. EBITDA(4) in

2017

Distribution Concession: Rio de Janeiro

GDP

Population

Accounts billed

Concession until 2026

2rd largest in the Country

2nd biggest, over 16 million of people(3)

4.5 million accounts billed and over 11 million people served

Market Share Analysis (per Volume and RAB)(2,5)

Source: ANEEL

(1) As of 2017

(2) As of June, 2018

(3) 16.7 million of people according to 2017 IBGE and the second largest GDP according to 2015 IBGE data(4) Adjusted EBITDA as EBITDA plus equity in the earnings of subsidiaries, other operating revenue (expenses), provisions and financial assets and liabilities of the sector. EBITDA as net income (loss) for the period plus net financial

result, income tax and social contribution expenses, and depreciation and amortization costs and expenses.

(5) RAB means regulatory asset base. RAB consists of the amount of investments made by energy distribution companies that will be included in the tariffs charged to consumers.

Total Volume (“000 GWh”) (1) Net RAB (R$ bn) (2,5)

32.8

25.1

20.4

19.7

19.7

16.3

14.1

11.0

Eletropaulo

Cemig

CPFL

Light

Copel

Coelba

Celesc

Celg

4th

8.9

8.5

7.4

6.0

6.0

5.2

4.9

3.5

Cemig

Light

Eletropaulo

Enel

Coelba

Copel

CPFL

Celpa

2nd

5

Light Energia: generation segment

Light Energia accounted for 8.2% of Light’s Consolidated Revenues and 16% of Adj. EBITDA(2) in 2017

Generation Plants: Fully Owned

RJ

3

2

1

100% ACL: Free Trading

Energy sold to LightCom

Fixed Price Contracts

Generation: Installed Capacity (GW)-Private Sector Companies (1)

8.3

7.0

3.3

2.7

2.3

2.2

1.6

1.3

1.1

1.1

1.0

CTG

Engie

CPFL

AES Tiete

EDP

Eneva

Neoenergia

Enel

Brookfield

CPFL Renovaveis

Light 11th

Source: (1) ANEEL and Abradee(2) Adjusted EBITDA as EBITDA plus equity in the earnings of subsidiaries, other operating revenue (expenses), provisions and financial assets and liabilities of the sector. EBITDA as net income (loss) for the

period plus net financial result, income tax and social contribution expenses, and depreciation and amortization costs and expenses.

3

Concession until 2026

1 HPP Ilha dos Pombos 187 MW Capacity

2 Complexo de Lajes 612 MW Capacity

HPP Santa Branca 56 MW Capacity

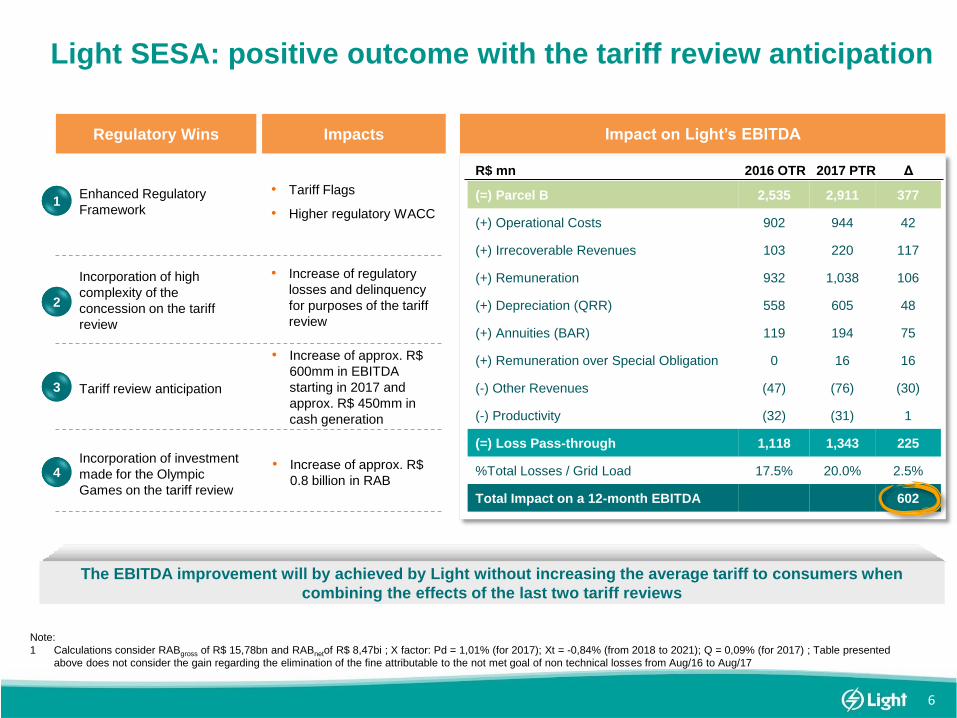

6

Regulatory Wins Impacts

Enhanced Regulatory

Framework

• Tariff Flags

• Higher regulatory WACC

Incorporation of high

complexity of the

concession on the tariff

review

• Increase of regulatory

losses and delinquency

for purposes of the tariff

review

Tariff review anticipation

• Increase of approx. R$

600mm in EBITDA

starting in 2017 and

approx. R$ 450mm in

cash generation

Incorporation of investment

made for the Olympic

Games on the tariff review

• Increase of approx. R$

0.8 billion in RAB

Impact on Light’s EBITDA

1

2

3

4

(=) Parcel B 2,535 2,911 377

(+) Operational Costs 902 944 42

(+) Irrecoverable Revenues 103 220 117

(+) Remuneration 932 1,038 106

(+) Depreciation (QRR) 558 605 48

(+) Annuities (BAR) 119 194 75

(+) Remuneration over Special Obligation 0 16 16

(-) Other Revenues (47) (76) (30)

(-) Productivity (32) (31) 1

(=) Loss Pass-through 1,118 1,343 225

%Total Losses / Grid Load 17.5% 20.0% 2.5%

Total Impact on a 12-month EBITDA 602

2017 PTR2016 OTR ΔR$ mn

The EBITDA improvement will by achieved by Light without increasing the average tariff to consumers when

combining the effects of the last two tariff reviews

Note:

1 Calculations consider RABgross of R$ 15,78bn and RABnetof R$ 8,47bi ; X factor: Pd = 1,01% (for 2017); Xt = -0,84% (from 2018 to 2021); Q = 0,09% (for 2017) ; Table presented

above does not consider the gain regarding the elimination of the fine attributable to the not met goal of non technical losses from Aug/16 to Aug/17

Light SESA: positive outcome with the tariff review anticipation

7

Covenants agreed with

ANEELCorporate Governance

• Covenants agreed with ANEEL

are more flexible than the

current covenants of debt

Light SESA is a subsidiary of Light S.A.,

company listed at the highest level of

corporate governance in

BM&FBOVESPA

Net Debt

(EBITDA – QRR)

1

(0.8 x SELIC)≤

For 2018:

Net Debt

(EBITDA – QRR)

1

(1.11 x SELIC)≤

For 2019 onwards:

QRR = regulatory depreciation

• Requirement of a High level of

corporate governance

DEC / FEC

(Quality Indicators)

18,15 18,70

12,35 12,61 11,709,14 7,81

11,99 11,399,80

8,23 8,14 8,02 7,84

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Actual DEC

ANEEL Results Plan (2016 and 2017) and New Goals 5th amendment (2018onwards)

8,39 8,406,60 6,44 6,48

5,26 4,71

6,36 5,99 6,01 5,72 5,43 5,15 4,86

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Actual FEC

ANEEL Results Plan (2016 and 2017) and New Goals 5th amendment (2018onwards)

FEC (times) 12 Months

DEC (hours) 12 Months

Actual Jun//2018

Actual Jun/2018

Light SESA: financial and operational targets agreed with ANEEL

8

Light SESA: diversified concession area with captive costumer base in

Rio de Janeiro metropolitan region

Retail-Focused Distribution Concession in Brazil’s 2nd Largest Metropolitan Area

Consumer ConcentrationConsumed Energy by Client Segment (GWh)

Residential36%

Comercial31%

Industrial19%

Others14%

Residential40%

Comercial18%

Industrial23%

Others19%

Light S.A

All Sector

Top 20 15%

Others 85%

Average Temperature

21

23

25

27

29

31

Jan Feb Mar Apr May Jun Jul Ago Sep Oct Nov Dec

RJ

9

23.92%21.75%

22.98%

16.48%

19.89% 20.62%

2Q16 2Q17 2Q18

Gap Between Real Losses and Regulatory

Target (%)

7.44 p.p. 1.86 p.p. 2.36 p.p.

Difference between actual loss and regulatory target

Changes in total losses 12 months

Light SESA: strategic remodeling of Losses’ Program (1 of 3)

Focus: Loss Reduction in Non-Risk Areas

New Approach to Management of Losses

Regulatory Target

Actual Losses

10

Increase of the Collection Rate

100.2% 97.3%98.2%

Total

99.3%

Retail

101.2% 101.5%

Large Clients

97.7% 100.0%

Public Sector

1S17 1S18

Collection Rate (Considering Overdue Installments)

105.0%

4Q16

98.6%

3Q162Q16 1Q17

97.6% 93.1%104.0%

2Q17

98.3%

3Q17

92.0%

4Q17

97.6%

1Q18

102.8%

2Q18

Total Collection Rate (Considering Overdue Installments)

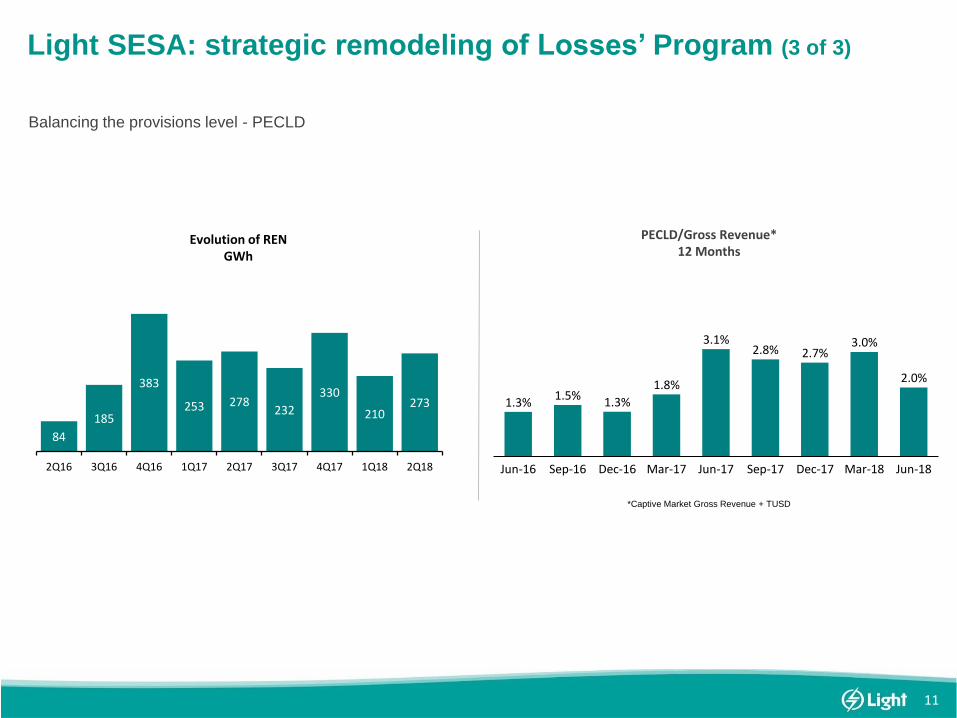

Light SESA: strategic remodeling of Losses’ Program (2 of 3)

11

Balancing the provisions level - PECLD

Evolution of RENGWh

84

185

383

253 278232

330

210273

2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 1Q18 2Q18

PECLD/Gross Revenue*12 Months

*Captive Market Gross Revenue + TUSD

Jun-16 Dec-16 Mar-17Sep-16 Jun-18Jun-17 Sep-17 Dec-17 Mar-18

1.3%1.5%

1.3%

1.8%

3.1%2.8% 2.7%

3.0%

2.0%

Light SESA: strategic remodeling of Losses’ Program (3 of 3)

12

R$ Millions 1S17 1S18

CVM EBITDA 661 849

(+/-) Equity Income (33) 39

(+/-) Other Operating Revenues (expenses) 74 30

Adjusted EBITDA 702 918

(-) Income Tax and Social Contribution (158) (90)

(-) Interest (362) (240)

(-/+) Accounts Receivable (37) (125)

(-/+) Financial assets and Liabilities of the sector 85 (254)

(-/+) Suppliers 32 (358)

(-/+) Others (254) (3)

Cash From Operations (CFO) 8 (152)

(-) Capex (236) (292)

(-) Minority Investments (119) (60)

Free Cash Flow to Firm (FCFF) (347) (504)

(-) Amortization (59) 806

Free Cash Flow to Equity (FCFE) (406) 302

(-) Dividends - (30)

Reflection of Operational Improvement

Lower Cost of Debt

Reflection of Operational Improvement

Pass through on next Tariff Reviews

1S17 1S18

(77) 102

(432) (250)

Excluding the Financial assets and Liabilities of the sector

Evolution of Free Cash Flow

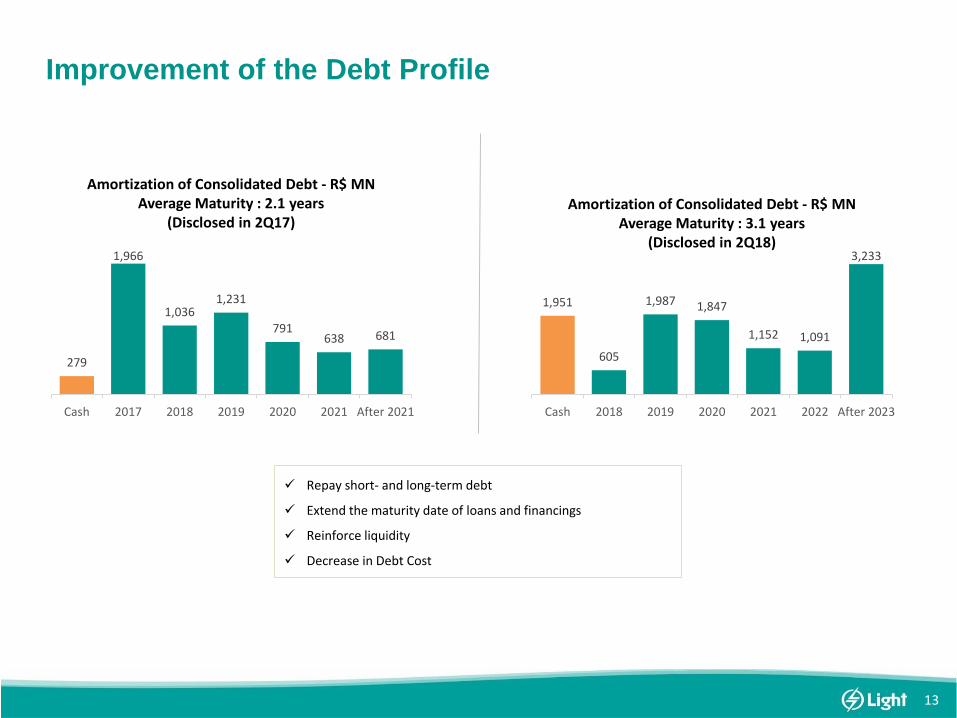

13

279

1,966

1,0361,231

791638 681

Cash 2017 2018 2019 2020 2021 After 2021

Amortization of Consolidated Debt - R$ MNAverage Maturity : 2.1 years

(Disclosed in 2Q17)

1,951

605

1,987 1,847

1,152 1,091

3,233

Cash 2018 2019 2020 2021 2022 After 2023

Amortization of Consolidated Debt - R$ MNAverage Maturity : 3.1 years

(Disclosed in 2Q18)

Repay short- and long-term debt

Extend the maturity date of loans and financings

Reinforce liquidity

Decrease in Debt Cost

Improvement of the Debt Profile

14

Luis Fernando Paroli Santos

CEO, Director of Business Development and Investor Relations

Fernanda Crespo

Head Of Participations and Investor Relations and Energy Business & Power Purchase

+ 55 21 2211 2508

Marcio Loures Penna

Investor Relations Specialist

+ 55 21 2211 2828

ri.light.com.br

Contacts

15

3

2Q18 Operational Highlights

Billed Market- GWh Billed Market- GWh

DEC - Hours (12 months) FEC - Times (12 months)

7,1906,824

7,160

2Q16 2Q17 2Q18

-0.4% 14,806 14,892 14,618

1S16 1S17 1S18

-1.3%

11.46 10.97

7.81

2Q16 2Q17 2Q18

-31.8%

6.30 6.09 4.73

2Q16 2Q17 2Q18

-24.9%

-29.1%

-23.0%

5th ANEEL Addendum = 9.80 hours 5th ANEEL Addendum = 6.01 times

4.9%

-1.8%

16

4

2Q18 Financial Highlights

Net Revenue - R$ MN EBITDA - R$ MN

PMSO - R$ MN Net Debt (R$ MN) andNet Debt/EBITDA - covenants (x)

2,0372,288

2,778

2Q16 2Q17 2Q18

36.4%

200 212

446

2Q16 2Q17 2Q18

123.0%

241

258 248

2Q16 2Q17 2Q18

2.9%

6,059 6,669

7,935

2Q16 2Q17 2Q18

3.98

3.23 3.32

21.5%

110.8%

-3.9%

17

Non Core Assets’

Note:

1 Sale of Alto Sertão III (433 MW) project to Brookfield ongoing. Binding Offer from CEMIG to purchase Chipley (148 MW)

2 PPA in Regulated Contracting Environment

ProjectInstalled Capacity

(MW)Description Shareholders

Light ESCO n/A ► Energy efficiency subsidiary

► Sale agreement signed in March ‘18 with Ecogen

(Mitsui Group)

► Closing subject to conditions precedent

► Light: 100%

Renova

672

► Renewable energy company

► Focus on assets and projects sale 1

► Light: 17.2%

► CEMIG: 36.2%

► Others: 46.6%

Belo Monte

11,223

► Operations started in 2016

► 100% of assured energy (4,571 MWavg) achieved in

Jan '18

► Light: 2.5%

► CEMIG: 7,3%

► Eletrobras Group: 49.9%

► Others: 40.3%

Guanhães

44

► 4 SHPPs located in Minas Gerais

► Winner of ANEEL’s A-5 auction in 20142

► Construction restarted in Nov’17 (conclusion

expected for 2Q19)

► Light: 51%

► CEMIG: 49%

Itaocara

150

► Project will not be implemented

► 70% of PPAs with DisCos cancelled

► Interactions with ANEEL to cancel the concession

► Light: 51%

► CEMIG: 49%

Light S.A.: improved liquidity, FCF and leverage (3 of 3)

Reduction of Exposure to Non Core Assets - Strategic direction to focus on core business