mgmt-165 chapter 06 slides - kids in prison program – # ... · 6-5 6.1 incremental cash flows...

TRANSCRIPT

6-0McGraw-Hill/Irwin Copyright © 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

Making Capital Investment

Decisions

Chapter 6

6-1

What is capital budgeting?

• Chapters 5 (which we covered already), 6 and 7 focus on capital budgeting, i.e., the decision making process for accepting or rejecting long-term investment projects.

• Long-term decisions that involve large expenditures.

• Very important to a firm’s future.

Should we build this

plant?

6-2

Steps to Capital Budgeting

1. Estimate CFs (inflows & outflows).

2. Assess riskiness of CFs.

3. Determine the appropriate cost of capital.

4. Find NPV or IRR (or whatever method you are using).

5. Accept if NPV > 0 or IRR > Required Return.

6-3

Key Concepts and Skills

• Understand how to determine the relevant cash flows for various types of capital investments

• Be able to compute depreciation expense for tax purposes

• Incorporate inflation into capital budgeting• Understand the various methods for

computing operating cash flow• Evaluate special cases of discounted cash flow

analysis

6-4

Chapter Outline

6.1 Incremental Cash Flows

6.2 The Baldwin Company: An Example

6.3 Inflation and Capital Budgeting

6.4 Alternative Definitions of Operating Cash Flow

6.5 Some Special Cases of Discounted Cash Flow Analysis

6-5

6.1 Incremental Cash Flows• Cash flows matter—not accounting earnings (this is a major

difference between Corporate Finance and Financial Accounting).

• When making a capital budgeting decision, always use cash flows. Earnings do not represent real money! You cannot spend out of earnings.

• Incremental cash flows matter: in calculating the NPV of a project only cash flows that are incremental to the project should be used. We are interested in the difference between the cash flows with the project and the cash flows without the project (not easy to do).

• Sunk costs do not matter. A sunk cost is a cost that has already occurred and cannot be recovered or changed by the decision to accept or reject the project.

6-6

Incremental Cash Flows (continued)

• Opportunity costs matter (e.g. Service Merchandise, ToysRUs or Kmart).

• Side effects like cannibalization (e.g. iPhones cannibalizing the sales of iPods), erosion (taking money out of profitable areas and using it to fund projects that may or may not be profitable in the future) and synergy (when a new project increases the cash flows of existing projects) matter. HP and Compaq claimed synergies, and so did Mercedes-Benz and Chrysler.

• Taxes matter: we want incremental after-tax cash flows.

• Inflation matters (it affects revenue and costs).

6-7

Cash Flows—Not Accounting Income

• Consider depreciation expense.

– You never write a check made out to “depreciation.”

• Much of the work in evaluating a project lies in taking accounting numbers and generating cash flows.

6-8

Project Cash Flows• Relevant cash flows – cash flows that occur (or don’t occur) because a project is undertaken. Cash flows that will occur regardless of whether or not we accept a project aren’t relevant.

• Incremental cash flows – any and all changes in the firm’s future cash flows that are a direct consequence of taking the project

• The Stand-Alone Principle: Viewing projects as “mini-firms” with their own assets, revenues, and costs allows us to evaluate the investments separately from the other activities of the firm.

6-9

Asking the Right Question

• You should always ask yourself “Will this cash flow change ONLY if we accept the project?”

– If the answer is “yes,” it should be included in the analysis because it is incremental

– If the answer is “no,” it should not be included in the analysis because it is not affected by the project

– If the answer is “part of it,” then we should include the part that occurs because of the project

6-10

Incremental Cash Flows

• Sunk costs are not relevant– Just because “we have come this far” does not

mean that we should continue to throw good money after bad.

• Opportunity costs do matter. Just because a project has a positive NPV, that does not mean that it should also have automatic acceptance. Specifically, if another project with a higher NPV would have to be passed up, then we should not proceed.

6-11

Incremental Cash Flows

• Side effects matter.

–Cannibalization is a “bad” thing. If our new product causes existing customers to demand less of our current products, we need to recognize that.

– If, however, synergies result that create increased demand of existing products or cost cutting, we also need to recognize that.

6-12

Interest Expense

• Later chapters will deal with the impact that the amount of debt that a firm has in its capital structure has on firm value.

• For now, it is enough to assume that the firm’s level of debt (and, hence, interest expense) is independent of the project at hand. The Separation Theorem dictates that the financing and investment decisions are separate activities.

6-13

Estimating Cash Flows• Capital budgeting relies heavily on pro forma accounting

statements, particularly income statements.

• Net Capital Spending

– Do not forget salvage value (after tax, of course).

• Changes in Net Working Capital (increases in NWC in the early years of the project (funded by cash generated elsewhere in the firm→ cash outflows) and decreases in NWC at the end of the project (cash inflows))

• Project cash flow = Project operating cash flow

- Project capital spending

- Change in project net working capital

6-14

Estimating Cash Flows (continued)

• Cash Flow from Operations

– Recall that:

OCF = EBIT + Depreciation – Current Taxes

Or OCF = NI + depreciation (because we do not consider the interest expense). This is called the bottom-up approach.

OCF = Sales – Costs – Taxes (do not subtract non-cash deductions). This is called the top-down approach.

CF(A) = OCF – NCS - ΔNWC, where CF(A) is cash flow from assets

6-15

More on NWC

• Changes in NWC reflect net increased investment in receivables, inventory and cash necessary to support additional sales.

• They also account for portion of this increased investment that is funded by increases in accounts payable (new firm short term liabilities).

6-16

Tax Shield Approach

• You can also find operating cash flows using the tax shield approach

• OCF = (Sales – costs)*(1 – T) + Depreciation*T• OCF has two components: • First component: Project’s cash flow if there were no

depreciation expense. • Second component: Depreciation deduction multiplied by

the tax rate. It is called depreciation tax shield. • This form may be particularly useful when the major

incremental cash flows are the purchase of equipment and the associated depreciation tax shield – such as when you are choosing between two different machines

6-17

Depreciation and the Tax Shield Approach

• Depreciation itself is a non-cash expense; consequently, it is only relevant because it affects taxes

• The depreciation expense used for capital budgeting should be the depreciation schedule required by the IRS for tax purposes

• Depreciation tax shield = (Depreciation expense)x(Marginal Tax Rate)

• Particularly useful when using accelerated depreciation.

6-18

Computing Depreciation

• Straight-line depreciation:– (Initial Cost – Salvage Value) / Number of Years– Salvage value=what we think the asset will be worth when we

dispose it. – Very few assets are depreciated straight-line for tax purposes

• MACRS (Modified Accelerated Cost Recovery System)– Need to know which asset class is appropriate for tax purposes– Multiply percentage given in table by the initial cost– Depreciate to zero– Half year convention(e.g., for a 3-year-class property, the

recovery period begins in the middle of the year the asset is placed in service and ends three years later. The effect of the half-year convention is to extend the recovery period out one more year, so 3-year-class property is depreciated over 4 years. )

6-19

MACRS Property Classes

6-20

After Tax Salvage

• If the salvage value is different from the book value of the asset, then there is a tax effect

• Book value = initial cost – accumulated depreciation

• After tax salvage = salvage – T(salvage – book value)

6-21

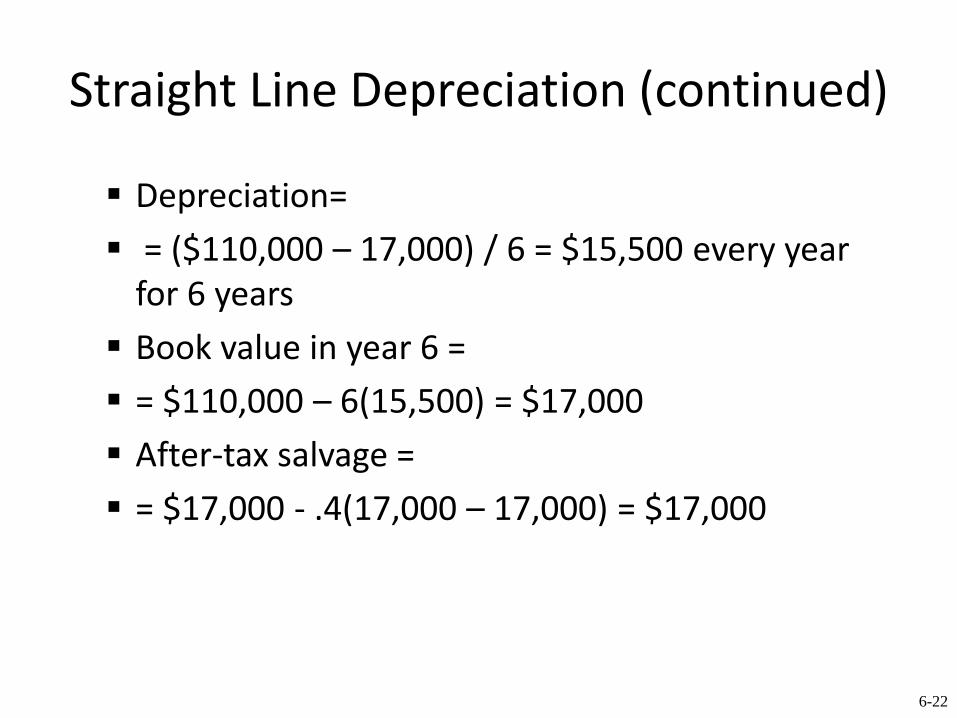

Example: Straight Line Depreciation

You purchase equipment for $100,000 and it costs $10,000 to have it delivered and installed. Based on past information, you believe that you can sell the equipment for $17,000 when you are done with it in 6 years. The company’s marginal tax rate is 40%. What is the depreciation expense each year, and the after tax salvage in year 6, assuming that the appropriate depreciation schedule is straight-line?

6-22

Straight Line Depreciation (continued)

Depreciation=

= ($110,000 – 17,000) / 6 = $15,500 every year for 6 years

Book value in year 6 =

= $110,000 – 6(15,500) = $17,000

After-tax salvage =

= $17,000 - .4(17,000 – 17,000) = $17,000

6-23

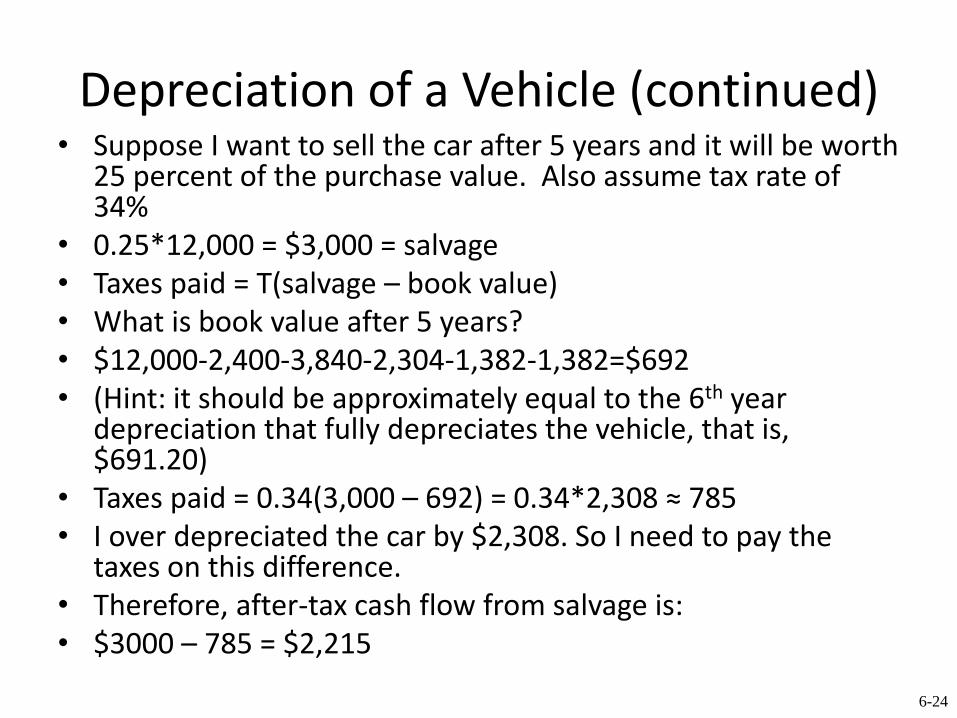

Example: Depreciation of a Vehicle

• Consider an automobile costing $12,000. How

is it depreciated? MACRS, 5 year.

6-24

Depreciation of a Vehicle (continued)• Suppose I want to sell the car after 5 years and it will be worth

25 percent of the purchase value. Also assume tax rate of 34%

• 0.25*12,000 = $3,000 = salvage• Taxes paid = T(salvage – book value)• What is book value after 5 years?• $12,000-2,400-3,840-2,304-1,382-1,382=$692• (Hint: it should be approximately equal to the 6th year

depreciation that fully depreciates the vehicle, that is, $691.20)

• Taxes paid = 0.34(3,000 – 692) = 0.34*2,308 ≈ 785• I over depreciated the car by $2,308. So I need to pay the

taxes on this difference. • Therefore, after-tax cash flow from salvage is:• $3000 – 785 = $2,215

6-25

6.2 The Baldwin Company

• Capital budgeting example.• Sports equipment manufacturer (mostly golf

balls)• Project: Colored bowling balls• Questionnaires in test markets (Phil., LA, New

Haven): 10-15% of market share• Need new machine, use existing (vacant)

building that otherwise could be sold. • 5 year horizon (life of machine, after which

salvage value of $30,000)

6-26

The Baldwin Company

Costs of test marketing (already spent): $250,000Current market value of proposed factory site (which

we own): $150,000Cost of bowling ball machine: $100,000 (depreciated

according to MACRS 5-year) Increase in net working capital (purchase raw material

before production→investment in inventory, cash buffer against unforseen expenditures, cash from sales will be received later→accounts receivable): $10,000

All working capital is assumed to be recovered at the end (typical assumption in capital budgeting): all inventory is sold; cash buffer is liquidated; all accounts receivable are collected.

Production (in units) by year during 5-year life of the machine: 5,000, 8,000, 12,000, 10,000, 6,000

6-27

The Baldwin Company

Price during first year is $20; price increases 2% per year thereafter.

Production costs during first year are $10 per unit and increase 10% per year thereafter.

Working Capital: initial $10,000 changes with sales (analyst gives you figures)

Costs, revenues are in nominal $, and required nominal return is 10%

6-28

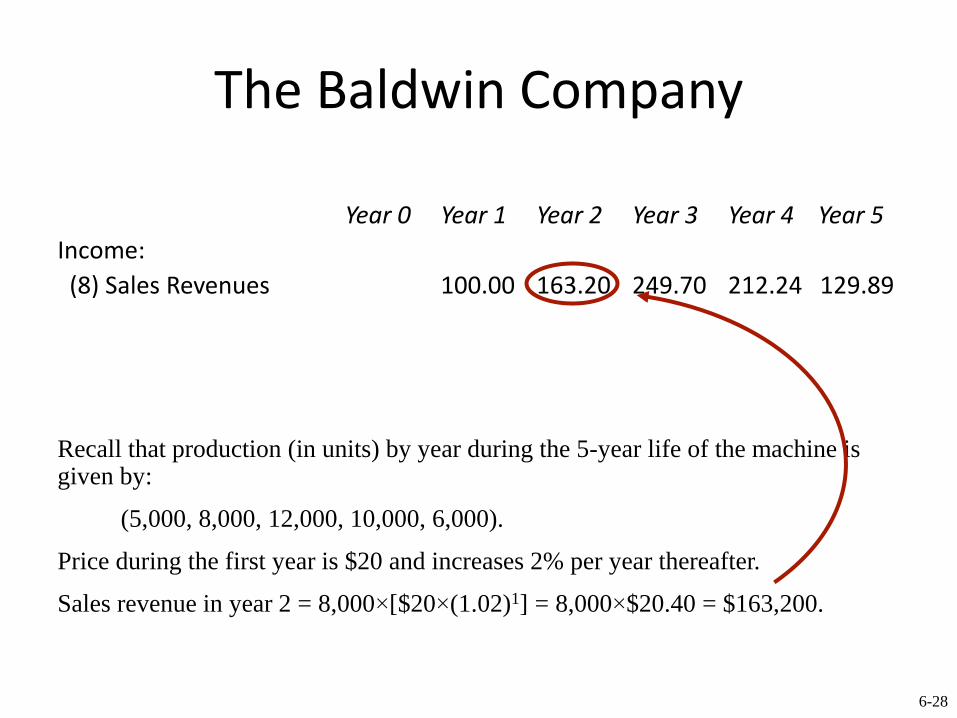

The Baldwin Company

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5

Income:

(8) Sales Revenues 100.00 163.20 249.70 212.24 129.89

Recall that production (in units) by year during the 5-year life of the machine is given by:

(5,000, 8,000, 12,000, 10,000, 6,000).

Price during the first year is $20 and increases 2% per year thereafter.

Sales revenue in year 2 = 8,000×[$20×(1.02)1] = 8,000×$20.40 = $163,200.

6-29

The Baldwin Company

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5Income:(8) Sales Revenues 100.00 163.20 249.70 212.24 129.89(9) Operating costs 50.00 88.00 145.20 133.10 87.85

Again, production (in units) by year during 5-year life of the machine is given by:

(5,000, 8,000, 12,000, 10,000, 6,000).

Production costs during the first year (per unit) are $10, and they increase 10% per year thereafter.

Production costs in year 2 = 8,000×[$10×(1.10)1] = $88,000

6-30

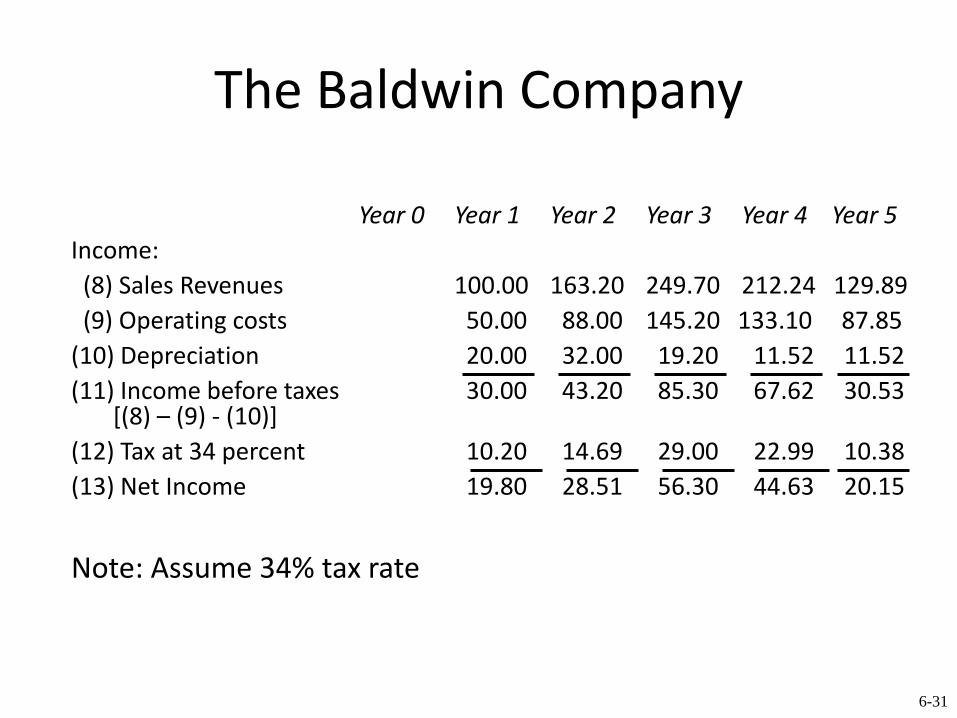

The Baldwin Company

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5

Income:

(8) Sales Revenues 100.00 163.20 249.70 212.24 129.89

(9) Operating costs 50.00 88.00 145.20 133.10 87.85

(10) Depreciation 20.00 32.00 19.20 11.52 11.52

Depreciation is calculated using the Modified Accelerated Cost Recovery System (shown at right).

Our cost basis is $100,000.

Depreciation charge in year 4

= $100,000×(.1152) = $11,520.

Year ACRS %

1 20.00%

2 32.00%

3 19.20%

4 11.52%

5 11.52%

6 5.76%

Total 100.00%

6-31

The Baldwin Company

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5

Income:

(8) Sales Revenues 100.00 163.20 249.70 212.24 129.89

(9) Operating costs 50.00 88.00 145.20 133.10 87.85

(10) Depreciation 20.00 32.00 19.20 11.52 11.52

(11) Income before taxes 30.00 43.20 85.30 67.62 30.53[(8) – (9) - (10)]

(12) Tax at 34 percent 10.20 14.69 29.00 22.99 10.38

(13) Net Income 19.80 28.51 56.30 44.63 20.15

Note: Assume 34% tax rate

6-32

The Baldwin Company: Incremental After Tax Cash Flows: OCF

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5

(1) Sales

Revenues

$100.00 $163.20 $249.70 $212.24 $129.89

(2) Operating

costs

-50.00 -88.00 -145.20 133.10 -87.85

(3) Taxes -10.20 -14.69 -29.00 -22.99 -10.38

(4) OCF

(1) – (2) – (3)

39.80 60.51 75.50 56.15 31.67

OCF = Sales – Costs – Taxes (top-down approach)

6-33

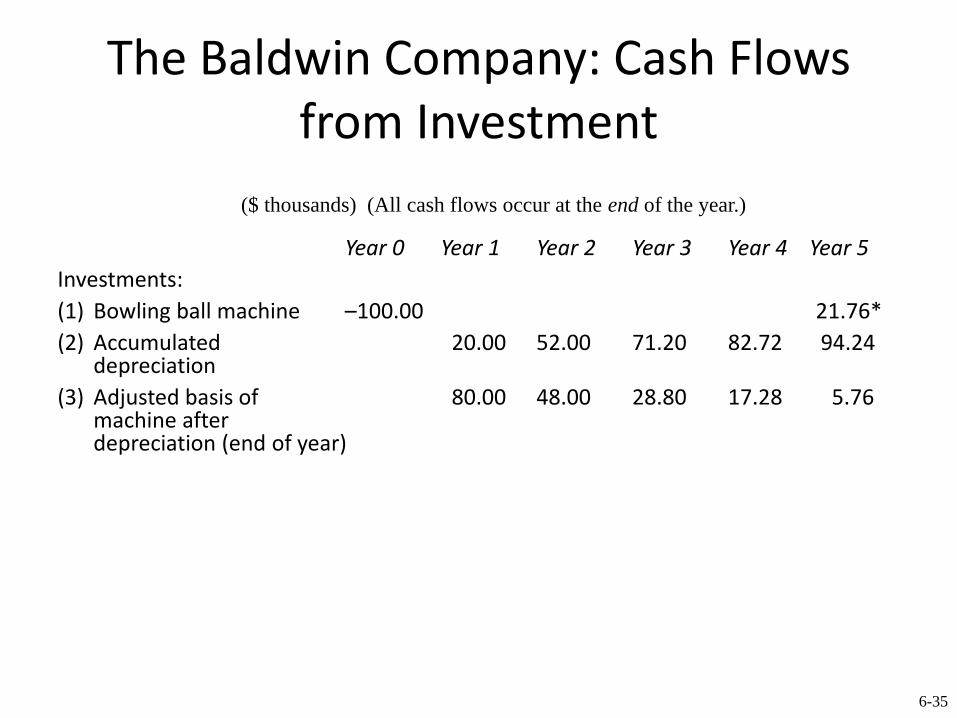

The Baldwin Company: Cash Flows from Investment

• Three kinds:

• 1) the bowling ball machine

• 2) the warehouse

• 3) changes in net working capital

6-34

The Baldwin Company: Cash Flows from Investment

• 1) the bowling ball machine

• Recall:

– $100,000 investment

– MACRS depreciation

– $30,000 salvage

• Imply depreciated value, end of year 5 = $5760 (see next slide…)

6-35

The Baldwin Company: Cash Flows from Investment

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5

Investments:

(1) Bowling ball machine –100.00 21.76*

(2) Accumulated 20.00 52.00 71.20 82.72 94.24 depreciation

(3) Adjusted basis of 80.00 48.00 28.80 17.28 5.76 machine after depreciation (end of year)

($ thousands) (All cash flows occur at the end of the year.)

6-36

The Baldwin Company: Cash Flows from Investment

• 1) the bowling ball machine

• Recall:– $100,000 investment

– MACRS depreciation

– $30,000 salvage

• Imply depreciated value, end of year 5 = $5760

• Therefore, year 5 taxes = .34 x (30,000-5760) = $8242

• Therefore, year 5 cash flow = $30,000 - $8242 = $21,758

6-37

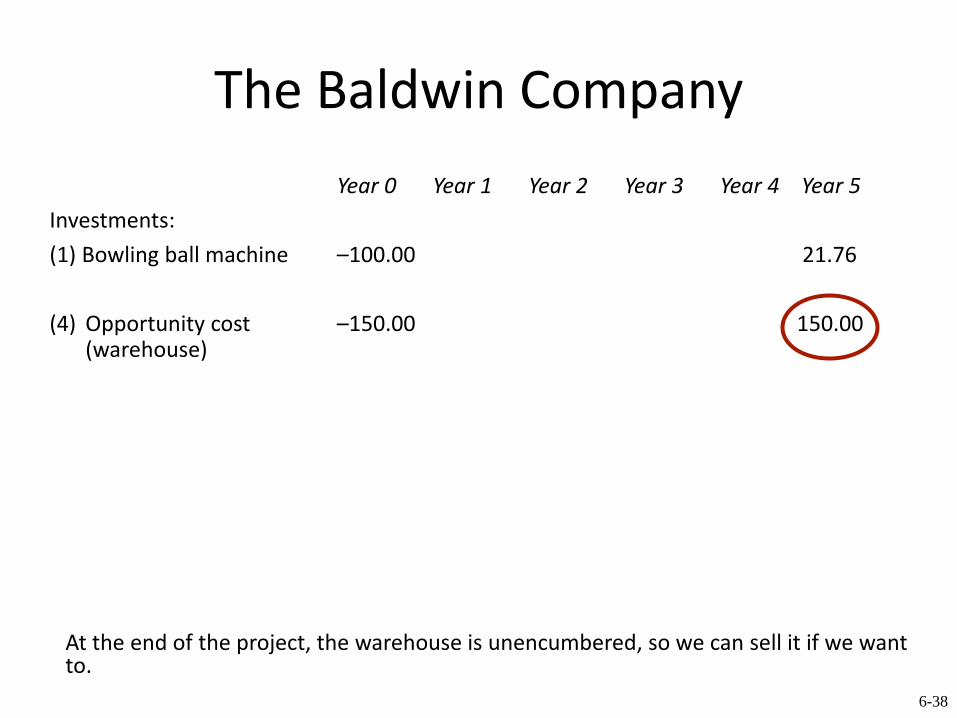

The Baldwin Company: Cash Flows from Investment

• Next:

• 2) the warehouse

• Recall

• $150,000 opportunity cost

• Assume same sale value in 5 years (no inflation!)

6-38

The Baldwin Company

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5

Investments:

(1) Bowling ball machine –100.00 21.76

(4) Opportunity cost –150.00 150.00(warehouse)

At the end of the project, the warehouse is unencumbered, so we can sell it if we want to.

6-39

The Baldwin Company: Cash Flows from Investment

• Finally:

• 3) changes in net working capital (given to you by analyst)

6-40

The Baldwin Company

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5

Investments:

(1) Bowling ball machine –100.00 21.76*

(2) Accumulated 20.00 52.00 71.20 82.72 94.24 depreciation

(3) Adjusted basis of 80.00 48.00 28.80 17.28 5.76 machine after depreciation (end of year)

(4) Opportunity cost –150.00 150.00(warehouse)

(5) Net working capital 10.00 10.00 16.32 24.97 21.22 0 (end of year)

(6) Change in net –10.00 –6.32 –8.65 3.75 21.22 working capital

(7) Total cash flow of –260.00 –6.32 –8.65 3.75 192.98 investment[(1) + (4) + (6)]

($ thousands) (All cash flows occur at the end of the year.)

6-41

The Baldwin Company

• Adding it all together… and discounting at, say, 10% cost of capital…

6-42

Incremental After Tax Cash Flows (IATFC)

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5

(1) Sales

Revenues

$100.00 $163.20 $249.70 $212.24 $129.89

(2) Operating

costs

-50.00 -88.00 -145.20 -133.10 -87.85

(3) Taxes -10.20 -14.69 -29.00 -22.99 -10.38

(4) OCF

(1) – (2) – (3)

39.80 60.51 75.50 56.15 31.67

(5) Total CF of

Investment

–260. –6.32 –8.65 3.75 192.98

(6) IATCF

[(4) + (5)]

–260. 39.80 54.19 66.85 59.90 224.65

59.51$

)10.1(

66.224$

)10.1(

90.59$

)10.1(

85.66$

)10.1(

19.54$

)10.1(

80.39$260$

5432

NPV

NPV

6-43

NPV of Baldwin Company

1

39.80

51.59

–260

CF1

F1

CF0

I

NPV

10

1

54.19CF2

F2

1

66.85CF3

F3

1

59.90CF4

F4

1

224.65CF5

F5

6-44

Baldwin Company: What have we done?

• Incremental cash flows, sunk costs do not matter ($250,000 on test marketing), opportunity costs (of warehouse) do matter

• Separation of financing from project evaluation (interest is not considered here)

• How to estimate cash flows – as distinct from accounting values (such as depreciation)

6-45

6.3 Inflation and Capital Budgeting

• Inflation is an important fact of economic life and must be considered in capital budgeting.

• Consider the relationship between interest rates and inflation, often referred to as the Fisher equation:

(1 + Nominal Rate) = (1 + Real Rate) × (1 + Inflation Rate)

Hence,

Real Interest Rate =1+Nominal Interest Rate

1+Inflation Rate− 1

6-46

Inflation and Capital Budgeting

• For low rates of inflation, this is often approximated: Real Rate Nominal Rate – Inflation Rate

• While the nominal rate in the U.S. has fluctuated with inflation, the real rate has generally exhibited far less variance than the nominal rate.

• In capital budgeting, one must compare real cash flows discounted at real rates or nominal cash flows discounted at nominal rates.

6-47

Inflation and Capital Budgeting• The approximation

Real Rate Nominal Rate – Inflation Rate• Is pretty good when inflation is low. • Example 1: Country X has nominal interest rates of 10% and

inflation of 3%. What is real rate of interest?• Truth: Real rate = [(1+nominal)/(1+infl.)]-1• = (1.1/1.03)-1 = 6.8%• Approximation: Real rate = Nominal – infl. = 7%• However, example 2: Country Y has nominal interest rates

of 400% and inflation of 350%. What is real rate of interest?

• Truth: Real rate = [(1+nominal)/(1+infl.)]-1• = (5/4.5)-1 = 11.11%• Approximation: Real rate = Nominal – infl. = 50%

6-48

6.5 Some Special Cases of Discounted Cash Flow Analysis

• Cost-Cutting Proposals

• Investments of Unequal Lives

6-49

Cost-Cutting Proposals• Cost savings will increase (pretax) income

– But, we have to pay taxes on this amount

• Depreciation will reduce our tax liability

• Does the present value of the cash flow associated with the cost savings exceed the cost?

– If yes, then proceed.

6-50

Investments of Unequal Lives

• There are times when application of the NPV rule can lead to the wrong decision. Consider a factory that must have an air cleaner that is mandated by law. There are two choices:– The “Cadillac cleaner” costs $4,000 today, has

annual operating costs of $100, and lasts 10 years.– The “Cheapskate cleaner” costs $1,000 today, has

annual operating costs of $500, and lasts 5 years.

• Assuming a 10% discount rate, which one should we choose?

6-51

Investments of Unequal Lives

The Cheapskate cleaner has a higher NPV.

10

–100

–4,614.46

– 4,000

CF1

F1

CF0

I

NPV

10

5

–500

–2,895.39

–1,000

CF1

F1

CF0

I

NPV

10

Cadillac Air Cleaner Cheapskate Air Cleaner

6-52

Investments of Unequal Lives

• This overlooks the fact that the Cadillac cleaner lasts twice as long.

• When we incorporate the difference in lives, the Cadillac cleaner is actually cheaper (i.e., has a higher NPV).

6-53

Equivalent Annual Cost (EAC)

• This approach puts costs on a per year basis.

• The EAC is the value of the level payment annuity that has the same PV as our original set of cash flows.

• Find NPV, then compute payment PMT, where NPV is the PV, N=number of years and I/Y=rate– For example, the EAC for the Cadillac air cleaner is

$750.98.

– The EAC for the Cheapskate air cleaner is $763.80, thus we should reject it (because it has higher costs).

6-54

Cadillac EAC with a Calculator

10

–100

–4,614.46

–4,000

CF1

F1

CF0

I

NPV

10 750.98

10

–4,614.46

10

PMT

I/Y

FV

PV

N

PV

6-55

Cheapskate EAC with a Calculator

5

–500

–2,895.39

–1,000

CF1

F1

CF0

I

NPV

10 763.80

10

-2,895.39

5

PMT

I/Y

FV

PV

N

PV

6-56

Replacement Chain Method

• Repeat projects until they have the same life.

• Given that Cadillac cleaner lasts twice as long, assume that Cheapskate cleaner is purchased again in 5 years. What is the NPV of the Cheapskate cleaner then?

• However, if one machine, say, 7 years and the other machine lasted, say, 8 years,…

• …to get equal horizons the first machine should be replicated 8 times and the second machine 7 times to get 56 years for both (complicated).

• The EAC method is applicable to a more robust set of circumstances.