math 373 test 4 fall 2013jbeckley/q/wd/ma373/f13/ma373 f13 test 4-1... · the annual risk free...

TRANSCRIPT

Math 373 Test 4

Fall 2013 December 10, 2013

1. (3 points) List the three conditions that must be present for there to be arbitrage.

No risk

No net investment

Guarantee of a positive cash flow or profit

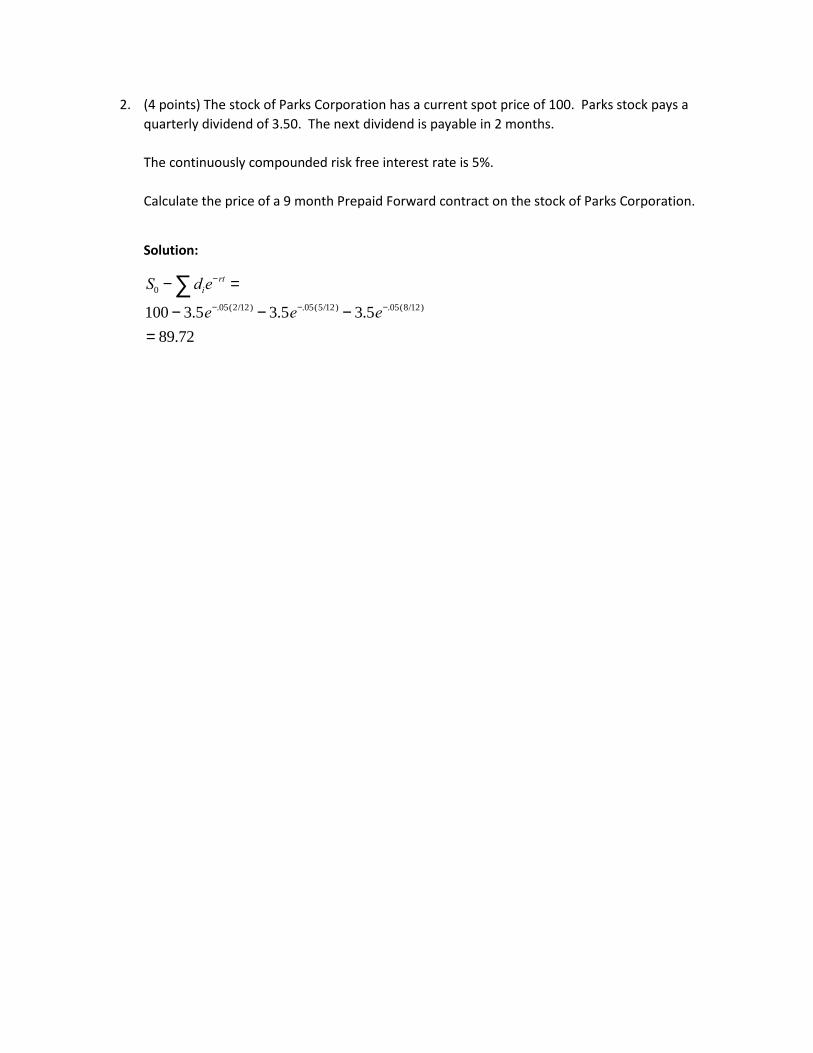

2. (4 points) The stock of Parks Corporation has a current spot price of 100. Parks stock pays a

quarterly dividend of 3.50. The next dividend is payable in 2 months.

The continuously compounded risk free interest rate is 5%.

Calculate the price of a 9 month Prepaid Forward contract on the stock of Parks Corporation.

Solution:

S0 - die-rt =å

100 - 3.5e-.05(2/12) - 3.5e-.05(5/12) - 3.5e-.05(8/12)

= 89.72

3. (6 points) Tianyi buys 5 futures contracts on the S&P 500 Index. The current futures price on the

S&P 500 is 1500.

For the futures contracts that Tianyi purchases, the margin requirement is 15% and the

maintenance margin is 75%. The margin account will earn an interest rate of 7.8% compounded

continuously.

The futures contracts are marked to market at the end of each week. After one week, the

futures price is 1478.

Determine the amount in the margin account at the end of one week.

Solution:

5(250)(1500) = 1875000(.15) = 281,250 = Margin

281,250e^(.078/52) = 281,672.19

1500 – 1478 = 22

22(5)(250) = 27500 loss

281,672.19 – 27500 = 254,172.19 left in account

Determine the amount of the Margin Call at the end of one week.

Solution:

281,250(.75) = 210,937.50 required

210,937.50 – 254,172.19 = -43,234.69

Therefore, the margin call is zero.

4. (4 points) There are four uses of derivatives. The four situations described below are examples

of those four uses. For each situation, identify which use is being illustrated. Each use should

be used once.

i. Matt thinks that the stock of Fletcher Inc will increase in price so he buys a call

which will allow him to purchase the stock in the future at the strike price. This

will allow him to make a profit on the stock.

This is an example of ____speculation .

ii. Sui owns Fang stock but is worried that the stock could decrease in price.

Therefore, Sui buys a put.

This is an example of _____risk management_____________ .

iii. The transaction cost to buy a stock is 35 while the transaction cost to enter into

a long forward contract on the same stock is 20 and to buy a zero coupon bond

is 10. The stock does not pay dividends. Jake decides to enter into the long

forward and also buys a zero coupon bond.

This is an example of ______reduce transaction costs___ .

iv. Stocks may be reported in a company’s financial statements differently than

derivatives.

This is an example of _____regulatory arbitrage______ .

5. (4 points) The current spot price of Yang Corporation stock is 72. The six month forward price of

Yang Corporation stock is 75.12. The annual risk free interest rate is 8% compounded

continuously.

State explicitly what actions Yuxi should take to arbitrage this situation.

Solution:

The theoretical forward price is (0.08)(0.5)72 74.94e which is less that the real forward price of

75.12. We want to Buy Low and Sell High so we will buy the synthetic forward and short the real

forward.

To buy the synthetic forward

synthetic forward = stock - zero coupon bond

Therefore,

Short the real forward

Buy the stock using borrowed money.

6. (6 points) For the stock of Bontrager Corporation, a one year European-style call and a one year

European-style put have the following premiums:

Strike Price Call Premium Put Premium

40 6.21 2.37

44 4.21 4.21

Bontrager Stock does not pay dividends.

Calculate the current spot price for Bontrager stock.

Solution:

If C = P, then F = K = 44

0

0

0

or 1 1

44 406.21 2.37

1

43.84 1 1.041667

1

406.21 2.37

1.041667

42.24

F K KC P C P S

i i

i

ii

S

S

7. (1 point) Draw the profit graph of a collar.

8. (6 points) The stock price of Conway Corporation is 32 today. You can purchase one year

European-style call options on Conway Corporation with the following strike prices and call

premiums.

Strike Price Call Premium

28 6.70

32 4.24

36 2.51

Remember that you can get put premiums if needed by using the put call parity formula.

The annual effective risk free interest rate is 7%.

Heather buys a strangle on Conway Corporation which expires in one year.

Calculate the profit on Heather’s strangle if the stock price at expiry is 40.

Solution:

Buy call with K > S0 S0=32, K=36

Buy put with K < S0 S0=32, K=28

C - P = S0 -K

1+ i

6.70 - P = 32 -28

1.07

P = .868224

Call

Put

Spot Payoff FV Cost Profit Payoff FV Cost Profit Total Profit

40 40-36=4 2.52(1.07)=2.6857 1.3143 0 .8682(1.07)=.928974 -0.928974 0.39

9. (1/2 point) The payoff on a forward is equal to the profit on a forward.

True or False

10. (1/2 point) The profit on a forward contract is equal to the profit on the purchase of the

underlying stock when the underlying stock does not pay a dividend.

True or False

11. (1 point) Kexin owns a 120 strike put option on Nie stock which will expire in 3 months. The cost

of the put option was 10.00. The current price of Nie stock is 125. This option is “In the

Money.”

True or False

12. (3 points) The current spot price of the stock of Wu Manufacturing is 83. This stock does not

pay a dividend. The annual effective risk free interest rate is 4%.

Ethan buys the stock today and sells it at the end of 9 months. Complete the following payoff

and profit table for Ethan’s transaction. SHOW YOUR WORK IF YOU WANT CREDIT!

Spot Price at End of 9 Months

Payoff Future Value of Cost Profit

60

=Spot

=60 83(1.04)^.75=85.48

Payoff – Profit = -25.48

70

70 85.48 -15.48

80

80 85.48 -5.48

90

90 85.48 4.52

100

100 85.48 14.52

13. (5 points) Yishen wants to buy 100 ounces of gold at the end of one year. She also wants to buy

250 ounces of gold at the end of two years. Finally, she wants to buy 400 ounces of gold at the

end of three years.

You are given the following spot interest rates and forward gold prices:

Time t Spot rate tr Forward Gold Price

0.5 4.0% 1225

1.0 4.3% 1250

1.5 4.7% 1275

2.0 5.2% 1300

2.5 5.8% 1330

3.0 6.5% 1360

Yishen enters into a three year Swap contract to fix the price of gold.

Calculate the Swap Rate on Yishen’s Swap.

Solution:

2 3

2 3

1 1 1100 (1250) 250 (1300) 400 (1360)

1.043 1.052 1.0651323.09

1 1 1100 250 400

1.043 1.052 1.065

R

14. (5 points) Smith LTD borrows 1,000,000 for the next three years. The interest rate on the loan is

variable and will be the one year interest rate each year. Smith purchases a three year interest

rate Swap to fix the interest rate.

You are given the following spot interest rates:

Time t Spot rate tr

0.5 4.0%

1.0 4.3%

1.5 4.7%

2.0 5.2%

2.5 5.8%

3.0 6.5%

Determine the fixed interest rate the Smith will pay under the Swap.

Solution:

3

2 3

11

1 (0,3) 1.0650.06399

(0,1) (0,2) (0,3) 1 1 1

1.043 1.052 1.065

P

P P P

15. (5 points) Cunningham Airlines entered into a Swap contract for jet fuel one year ago. As of

today, under the Swap contract, Cunningham will purchase 100,000 gallons of jet fuel at the end

of six months and 200,000 gallons of jet fuel at the end of two years. The Swap Rate will be 3.00

per gallon of jet fuel.

You are given the following spot interest rates and forward prices on jet fuel as of today:

Time t Spot rate tr Forward Prices on Jet Fuel

0.5 4.0% 2.90

1.0 4.3% 3.05

1.5 4.7% 3.15

2.0 5.2% 3.25

2.5 5.8% 3.30

3.0 6.5% 3.32

Calculate the market value of the Swap today.

Solution:

100,000(2.90 - 3)1

1.04

æ

èçö

ø÷

1/2

+ 200,000(3.25 - 3)1

1.052

æ

èçö

ø÷

2

= 35,373.39

16. (1/2 point) You can create a Bull spread by buying a put and selling a put with a higher strike

price.

True or False

17. (1/2 point) If you make a loan, the profit on the loan is equal to the interest that you earn on the

loan.

True or False

18. (2 points) If you expect the price of a stock to remain unchanged, circle any of the following

positions that you would enter into? (You may circle as few as zero and as many as four.)

a. A written straddle

b. A purchased strangle

c. Sell an At-The- Money Put

d. Purchase an At-The- Money Call

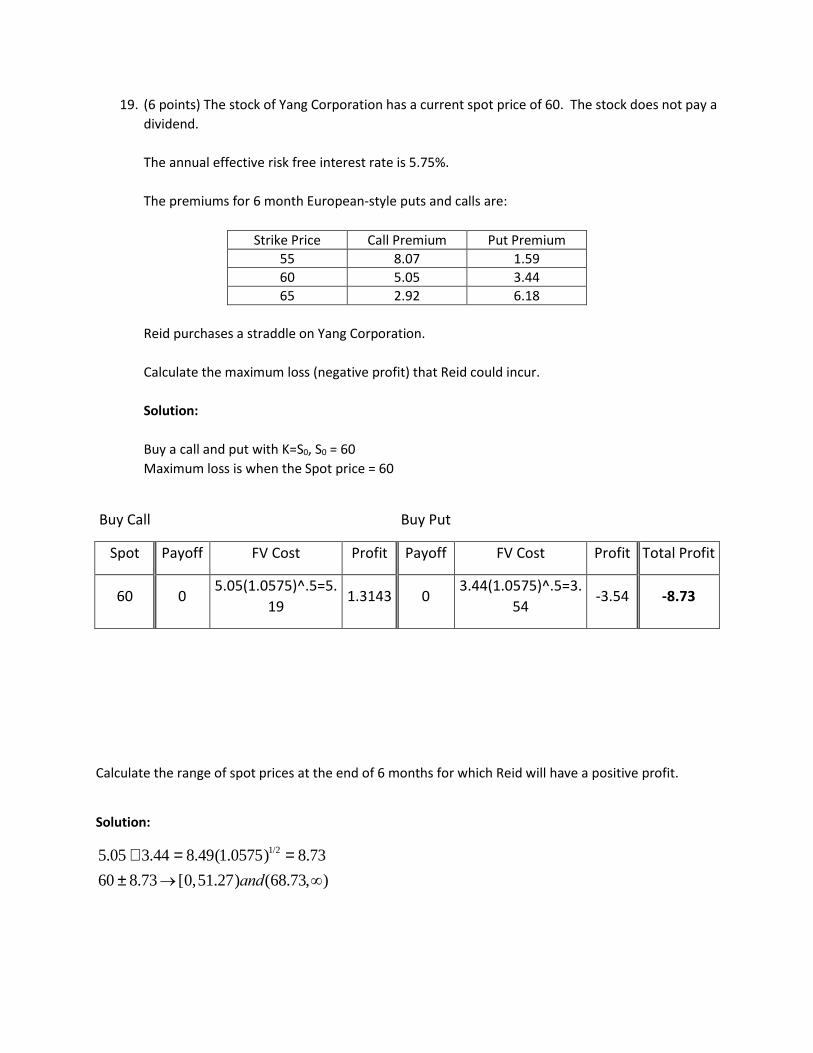

19. (6 points) The stock of Yang Corporation has a current spot price of 60. The stock does not pay a

dividend.

The annual effective risk free interest rate is 5.75%.

The premiums for 6 month European-style puts and calls are:

Strike Price Call Premium Put Premium

55 8.07 1.59

60 5.05 3.44

65 2.92 6.18

Reid purchases a straddle on Yang Corporation.

Calculate the maximum loss (negative profit) that Reid could incur.

Solution:

Buy a call and put with K=S0, S0 = 60

Maximum loss is when the Spot price = 60

Buy Call

Buy Put

Spot Payoff FV Cost Profit Payoff FV Cost Profit Total Profit

60 0 5.05(1.0575)^.5=5.

19 1.3143 0

3.44(1.0575)^.5=3.

54 -3.54 -8.73

Calculate the range of spot prices at the end of 6 months for which Reid will have a positive profit.

Solution:

5.05 + 3.44 = 8.49(1.0575)1/2 = 8.73

60 ± 8.73® [0,51.27)and(68.73,¥)

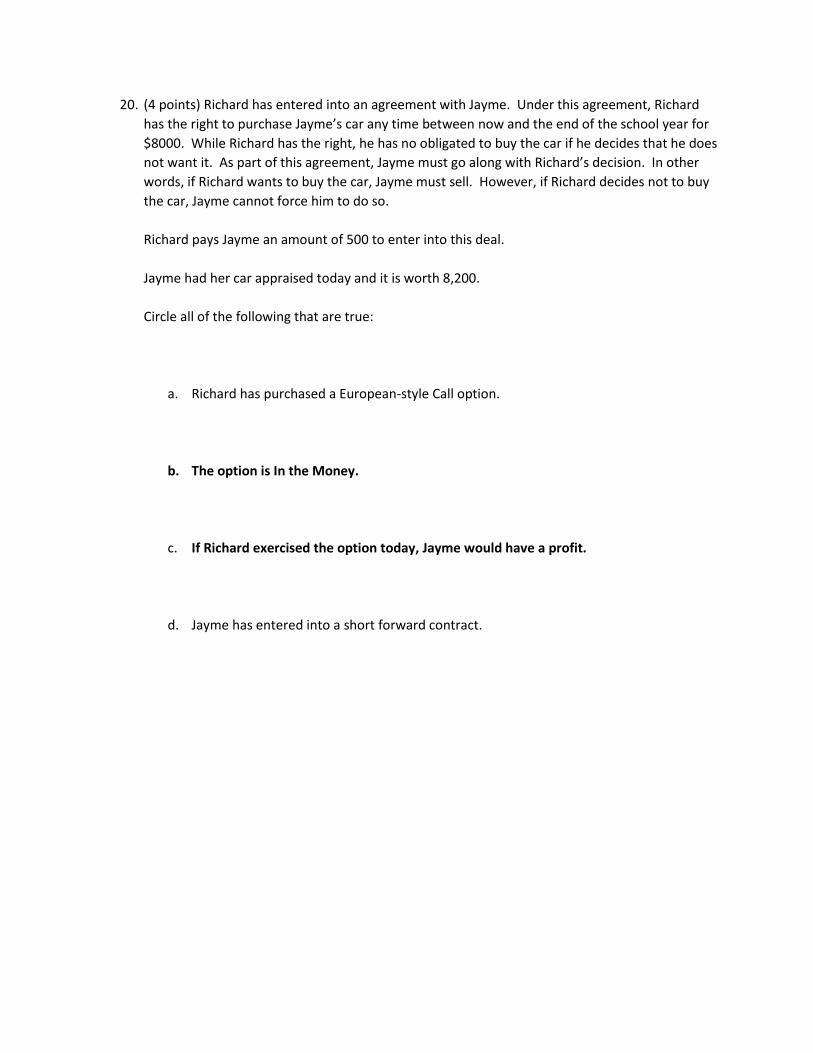

20. (4 points) Richard has entered into an agreement with Jayme. Under this agreement, Richard

has the right to purchase Jayme’s car any time between now and the end of the school year for

$8000. While Richard has the right, he has no obligated to buy the car if he decides that he does

not want it. As part of this agreement, Jayme must go along with Richard’s decision. In other

words, if Richard wants to buy the car, Jayme must sell. However, if Richard decides not to buy

the car, Jayme cannot force him to do so.

Richard pays Jayme an amount of 500 to enter into this deal.

Jayme had her car appraised today and it is worth 8,200.

Circle all of the following that are true:

a. Richard has purchased a European-style Call option.

b. The option is In the Money.

c. If Richard exercised the option today, Jayme would have a profit.

d. Jayme has entered into a short forward contract.

21. (4 points) The price of a 3 month prepaid forward on Stoakes Corporation is 40.

The forward price for a 3 month forward on Stoakes Corporation is 41.

Stoakes Corporation pays quarterly dividends of 4. The next dividend is due in 2 months.

Calculate the current spot price of the stock of Stoakes Corporation.

Solution:

0, 0,

3

0.2512

(2/12)

0

.09877(2/12)

0 0

( )

41 40 ln1.025 ln 4ln1.025 0.09877

40 4

40 4 43.93

P rT

T T

rr

r

F F e

e e r

S e

S e S

22. (6 points) You can purchase one year European-style call options on Cui Corporation with the

following strike prices and call premiums.

Strike Price Call Premium

14 1.86

18 0.52

Remember that you can get put premiums if needed by using the put call parity formula.

The annual effective risk free interest rate is 7% and the current spot price of Cui Corporation

stock is 14. Cui Corporation does not pay dividends.

Determine the cost to buy a collar on Cui Corporation.

Solution:

Buy a put, sell a call with higher strike

Buy 14 strike put, sell 18 strike call

01

141.86 14 0.944

1.07

0.94 0.52 0.42

KC P S

i

P P

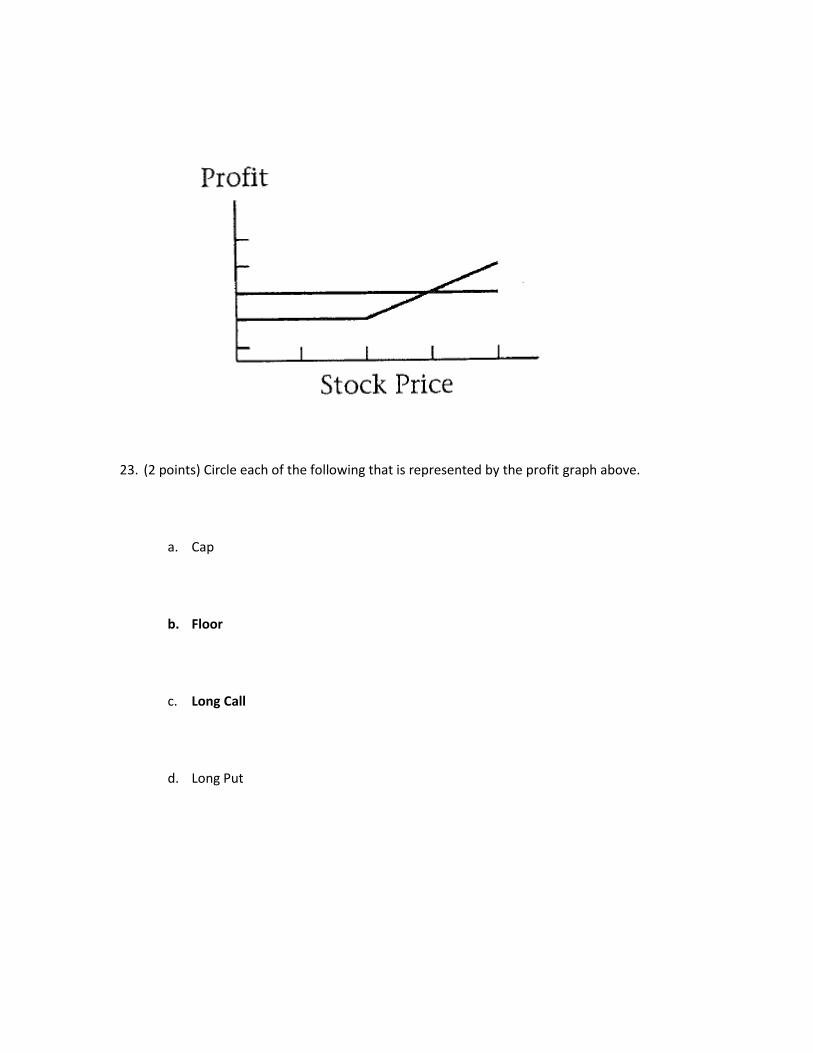

23. (2 points) Circle each of the following that is represented by the profit graph above.

a. Cap

b. Floor

c. Long Call

d. Long Put

24. (5 points) The bid price for Temiz Corporation stock is 50.00 per share. The bid-ask spread

is 0.50.

Pinar wants to buy X shares of Temiz stock. Pinar can buy the stock from Batta Brokers or

from Deepa Discount Dealers. Batta Brokers charges a commission of 0.25% of the purchase

price. Deepa charges a flat commission of 35 without regard to the number of shares.

Determine the minimum value of X where Pinar should use Deepa Discount Dealers to

purchase the stock.

Solution:

Ask=50.50

50.50X + .0025(50.50X) = 50.62625X

50.50X +35 = 50.62625

X = 277.2

278 shares

25. (2 points) Define credit risk.

Solution:

The risk that a borrower will default on an obligation by failing to make required payments

26. (3 points) Circle each of the following that are true with regard to futures contracts and forward

contracts:

A forward contract is an exchange traded futures contract.

Forward contracts have credit risk, but futures contracts eliminate all credit risk through the use

of margin accounts and price limits.

A futures contract is liquid.

27. (4 points) The current spot price on the stock of Liu LTD is 100. Liu LTD does not pay a dividend.

The one year forward price on the stock of Liu LTD is 104.60.

Yong sell a 6 month European-style put contract on the stock of Liu LTD. The strike price of the

put is 102 and the premium for the put is 6.95.

Calculate the payoff and profit that Yong will realize at the end of 6 months if the spot price of

Liu stock is 98.

Solution:

100(1 ) 104.60 4.6%i i

Spot Payoff FV Cost Profit

98 -MAX(0, 102-98)= -4 -6.95(1.046)0.5

= -7.108052 -4+7.11=3.11

28. (4 points) The S&P 500 Index has a current spot price of 1600. The Index pays dividends at a

rate of 2.3% compounded continuously.

The continuously compounded risk free interest rate is 6%.

Calculate the forward price for a forward contract on the S&P 500 that expires in 8 months.

Solution:

8

(0.06 0.023)( ) 12

0, 0 1600 1639.96T r

TF S e e

29. (3 points) List the three styles of options and define each style.

Solution:

American – can exercise at any time prior to expiry

Bermuda – can exercise at specified times prior to expiry

Europe – can only exercise at expiry