loretta j. mester federal reserve bank of cleveland … · market discipline working for and...

TRANSCRIPT

MARKETDISCIPLINEWORKINGFORANDAGAINSTFINANCIALSTABILITY:THETWOFACESOFEQUITYCAPITALINU.S.COMMERCIALBANKING

JOSEPHP.HUGHESRUTGERSUNIVERSITY

LORETTAJ.MESTERFEDERALRESERVEBANKOFCLEVELAND

ANDTHEWHARTONSCHOOL,UNIVERSITYOFPENNSYLVANIA

CHOON‐GEOLMOONHANYANGUNIVERSITY

DECEMBER2016

Abstract ThesecondBaselCapitalAccordpointstomarketdisciplineasatooltoreinforcecapitalstandardsandsupervisioninpromotingbanksafetyandsoundness.TheBankforInternationalSettlementscontendsthatmarketdisciplineimposesstrongincentivesonbankstooperateinasafeandefficientmanner–inparticular,tomaintainanadequatecapitalbasetoabsorbpotentiallossesfromtheirriskexposures.

Using2007and2013dataontop‐tier,publiclytradedU.S.bankholdingcompanies,wefindthatmarketdisciplinerewardsrisk‐takingatsomeofthelargestU.S.financialinstitutions.Inparticular,wefindevidenceoftwofacesofequityinvestment–dichotomouscapitalstrategiesformaximizingvalue.Atbankswithhigher‐valuedinvestmentopportunities,amarginalincreaseintheirequitycapitalratioisassociatedwithbetterfinancialperformance,whileatbankswithlower‐valuedinvestmentopportunities,amarginaldecreaseintheirequitycapitalratioisassociatedwithbetterfinancialperformance.BecausethelargestU.S.financialinstitutionstendtohavelower‐valuedinvestmentopportunities,ourresultssuggestthattheymayhaveamarket‐basedincentivetoreducetheircapitalratio.Totheextentthatmarketdisciplinerewardsreducingthecapitalratioamongthelargestbanks,itwouldtendtounderminefinancialstability.Ourresultssupporttheneedforregulatorycapitalrequirements.

*TheviewsexpressedinthispaperdonotnecessarilyreflectthoseoftheFederalReserveBankofClevelandortheFederalReserveSystem.HughesthankstheWhitcombCenterforResearchinFinancialServicesattheRutgersBusinessSchoolforitssupportofdataservicesusedinthisresearch.

CorrespondencetoHughesatDepartmentofEconomics,RutgersUniversity,NewBrunswick,NJ08901‐1248;[email protected],ExecutiveOffice,FederalReserveBankofCleveland,P.O.Box6387,Cleveland,OH44101‐1387;Loretta.Mester@clev.frb.org.ToMoonatDepartmentofEconomicsandFinance,CollegeofEconomicsandFinance,HanyangUniversity,Seoul133‐791,Korea;[email protected]. JEL Codes: C58, G21, G28. Key Words: banking, efficiency, capital structure, charter value

1

MARKETDISCIPLINEWORKINGFORANDAGAINSTFINANCIALSTABILITY:THETWOFACESOFEQUITYCAPITALINU.S.COMMERCIALBANKING

Introduction

ThesecondBaselCapitalAccordrestsonthreecomplementarypillars.TheBankfor

InternationalSettlementsdescribesthethirdpillar:1“Pillar3recognisesthatmarketdisciplinehas

thepotentialtoreinforceminimumcapitalstandards(Pillar1)andthesupervisoryreviewprocess

(Pillar2),andsopromotesafetyandsoundnessinbanksandfinancialsystems.Marketdiscipline

imposesstrongincentivesonbankstoconducttheirbusinessinasafe,soundandefficientmanner,

includinganincentivetomaintainastrongcapitalbaseasacushionagainstpotentialfuturelosses

arisingfromriskexposures.”

Consistentwiththisview,beforethefinancialcrisis,formerFederalReserveBoard

ChairmanAlanGreenspanalsoplacedemphasisonmarketdisciplineasasourceoffinancial

stability:“Exceptwheremarketdisciplineisunderminedbymoralhazard,forexample,becauseof

federalguaranteesofprivatedebt,privateregulationgenerallyhasprovedfarbetterat

constrainingexcessiverisk‐takingthanhasgovernmentregulation.”2Laterheexpressedsurprise

thatmarketdisciplinedidnotrestrainrisk‐takingatthelargestfinancialinstitutions:“...thoseof

uswhohavelookedtotheself‐interestoflendinginstitutionstoprotectshareholders’equity

(myselfespecially)areinastateofshockeddisbelief.”3

Atleastonebankerhassuggestedthatmarketforcesdonotnecessarilyleadtolessrisk‐

taking.CharlesPrince,thenCEOandchairmanofCitigroup,famouslyobserved,“Whenthemusic

1SeeBankforInternationalSettlements(2001),p.1.

2Greenspan(2005).

3Greenspan(2008).

2

stops,intermsofliquidity,thingswillbecomplicated.Butaslongasthemusicisplaying,you'vegot

togetupanddance.We'restilldancing.”4

Inthispaperweinvestigatetheroleofmarketdisciplineinbanks’risk‐taking,inparticular,

therelationshipbetweenequitycapitallevelsandbankfinancialperformance.Weapplythe

measurementsandtechniquesdevelopedbyHughes,Lang,Moon,andPagano(1997)and

describedinHughes,Lang,Mester,Moon,andPagano(2003)andmorerecentlyinHughes,Mester,

andMoon(2016),to2007and2013dataontop‐tier,publiclytradedU.S.bankholdingcompanies.

Wefindevidencesuggestingthatmarketdisciplinerewardsrisk‐takingatsomeofthelargestU.S.

financialinstitutions.Inparticular,wefindevidenceoftwofacesofequityinvestment–

dichotomouscapitalstrategiesformaximizingvalue.Atbankswithhigher‐valuedinvestment

opportunities,onthemarginanincreaseintheirequitycapitalratioisassociatedwithbetter

financialperformance,whileatbankswithlower‐valuedinvestmentopportunities,amarginal

decreaseintheirequitycapitalratioisassociatedwithbetterfinancialperformance.

BecausethelargestU.S.financialinstitutionstendtohavelower‐valuedinvestment

opportunities,ourresultssuggestthattheymayhaveamarket‐basedincentivetoreducetheir

capitalratio.Totheextentthatmarketdisciplinerewardsreducingthecapitalratioamongthe

largestbanks,itwouldtendtounderminefinancialstability.Ourresultssupporttheneedfor

regulatorycapitalrequirements.Theyarealsoconsistentwithotherpapersintheliteraturethat

suggestthatmarketdisciplinemayhaveactuallyencouragedrisk‐takingatlargefinancial

institutionsleadinguptothecrisis.Forexample,LaevenandLevine(2009)examinedthelargest

banksinanumberofcountriesandconcludedthatlarge,diversifiedshareholdersatthesebanks

generallypreferriskierinvestmentstrategiesthanmanagers,andthattheyexercisesufficient

corporatepowertoeffecttheriskierstrategies.

4Prince,asquotedbyNakamotoandWighton(2007).

3

Therestofthepaperisorganizedasfollows.SectionIreviewstheliteratureoncapital

strategies.SectionIIdescribesthetwomeasuresoffinancialperformancethatweuseto

investigatetheroleofequitycapitalinthefinancialperformanceofU.S.commercialbanks.

SectionIIIpresentsameasureofthevalueofbanks’investmentopportunities.SectionIVdiscusses

thedata.SectionVpresentsourresults,andSectionVIconcludes.

I.LiteratureReview

Marcus(1984)investigatesthedifferentrisk‐takingincentivesofbankswithhigh‐valued

investmentopportunitiesversusthosewithlow‐valuedopportunities.Heshowsthatvalue

maximizationforbankswithlow‐valuedinvestmentopportunitiesinvolvestakingmoreriskto

exploittheoptionvalueofexplicitandimplicitdepositinsurance,while,forbankswithhigh‐valued

opportunities,valuemaximizationentailslessriskyinvestmentstrategiestoprotecttheircharters.

Entryintobankingrequiresacharterissuedbyaregulatoryauthority.Restrictionsonbankentry

createmarketpower,whichmakesvaluableinvestmentopportunitiesevenmorevaluable.In

contrast,competitivemarketstendtounderminechartervalue.5Inthecaseofbankswithhigh‐

valuedopportunities,totheextentthatmarketdisciplineencouragesmanagerstoadoptvalue‐

maximizinginvestmentstrategies,thesestrategiesentaillessrisk‐takingandsopromotefinancial

stability,while,inthecaseofbankswithlow‐valuedopportunities,marketdisciplinewould

encouragemorerisk‐takingandwouldtendtoworkagainstfinancialstability.

Acontrastingincentivethatencouragesrisk‐takingresultsfrommispriceddeposit

insurance.Thegenerallackofrisk‐pricingandtheimplicitinsuranceobtainedfromthetoo‐big‐to‐

faildoctrineweakenthelinkbetweenthecostofborrowedfundsandtheriskinessofinvestment

strategies.Thus,thecostoffundsdoesnotrespondfullytomoreriskyinvestmentstrategieswith

higherexpectedreturns.Forbanksoperatinginmorecompetitivemarketsandinmarketswith

5Keeley(1990)findsevidencethatincreasingcompetitioninU.S.bankingmarketsduringthe1980serodedchartervalueandledtoincreasingfinancialleverage.

4

lessvaluableinvestmentopportunities,smallerexpectedbankruptcycostsmakemorerisky

investmentstrategiesthatexploittheoptionvalueofdepositinsuranceandthetoo‐big‐to‐fail

doctrinevaluemaximizing.

Using1994dataonU.S.bankholdingcompanies,Hughes,Lang,Moon,andPagano(1997)

findevidenceofthesedichotomousinvestmentstrategies.Keeley(1990)considerstheperiod

duringwhichinterstatebranchingregulationswereliberalized,whichincreasedcompetition

amongbanksandreducedtheirchartervalues.Helinksthedeclineinchartervalueswith

increasedfinancialleverageinU.S.banking.Grossman(1992)considerstheperiodafterthe

passageofdepositinsuranceforU.S.thriftsin1934andfindsevidencethatinsuredthriftsadopted

moreriskyinvestmentstrategiesthanuninsuredthrifts.

CalomirisandNissim(2007)regresstheratioofthemarketvalueofequitytoitsbookvalue

onvariablescharacterizingbanks’investmentstrategiesandfindthatthemarket‐to‐bookequity

ratioisnegativelyrelatedtocapitalforbankswithlowercapitalratiosandpositivelyrelatedfor

bankswithhighercapitalratios.Thus,bankswithalowercapitalratioappeartobe

overcapitalized,whilethosewithahighercapitalratio,undercapitalized.DeJongheandVander

Vennet(2005)usethenoise‐adjustedmeasureofTobin’sqratiotomeasureperformanceandfind

anonmonotonicrelationshipofmarketvalueandthebook‐valueratioofequitycapitaltoassets–a

relationshipqualitativelythesameastheonefoundbyCalomirisandNissim(2007).

McConnellandServaes(1995)proposeahypothesisfornonfinancialfirmsthatyields

implicationssimilartoMarcus(1984).Firmswithhigh‐valuedinvestmentopportunitiesforwhich

theunderinvestmentproblemisparticularlyacutemaximizevaluebyemployinglessfinancial

leverage.Ontheotherhand,firmswithlow‐valuedinvestmentopportunitiesforwhich

overinvestmentfromfreecashflowreducesvaluemaximizevaluebyusingmorefinancialleverage

5

toputperformancepressureonmanagers.Theauthorsrefertothesedichotomousstrategiesas

the“twofacesofdebt.”

II.MeasuringFinancialPerformance6

Unlikeaccounting‐basedmeasuresofperformancethatgaugecurrentandpast

performance,afirm’smarketvalueprovidesthemarket’sexpectationofthefirm’scurrentand

futurecashflowsdiscountedataratethatreflectsthemarket’sassessmentofthefirm’sexposure

tomarket‐pricedrisk.AsinHughes,Mester,andMoon(2016),wemeasurebanks’performanceby

themarketvalueoftheirassetsandbythedifferencebetweentheirbest‐practicemarketvalueof

assetsandtheirachievedmarketvalue,adjustedtoeliminatestatisticalnoise.Whilemarketvalue

iscorrelatedwithagencyproblems,thedifferencebetweenpotentialandrealizedmarketvalue–

lostmarketvalue–moredirectlygaugestheextentofagencyproblems.

Thebest‐practicemarketvalueofassetsisobtainedfromtheestimationofastochastic

frontier–anupperenvelopeofmarketvalueasafunctionofthebook‐valueinvestmentinassets–

forpubliclytraded,top‐tierU.S.bankholdingcompanies.Thefrontieranswersthequestion:what

isthebest‐practicemarketvalueofassetsobservedforanygivenbook‐valueinvestmentinassets?7

Theeliminationofstatisticalnoisefromthedifferencebetweenthebest‐practiceandobserved

marketvaluesmeansthatthislostmarketvaluerepresentssystematicunderperformance.We

normalizethelostmarketvaluebythebest‐practicevaluesothatitisameasureofthemarket‐

valueinefficiencyratio.Asameasureofsystematicunderperformance,market‐valueinefficiency

6ThissectionfollowstheoriginalexpositionofHughes,Lang,Moon,andPagano(1997),whichisrestatedmorerecentlyinHughes,Mester,andMoon(2016)andHughes,Jagtiani,andMester(2016).

7ThistechniqueofmeasuringperformancewasproposedbyHughes,Lang,Moon,andPagano(1997)andwasusedbyHughes,Lang,Mester,andMoon(1999)tostudybankconsolidation;byHughes,Lang,Mester,Moon,andPagano(2003)tostudybankassetsalesandacquisitions;andbyHughes,Mester,andMoon(2001)andHughesandMester(2013b)toevaluatebankscaleeconomiesmeasuredalonganexpansionofbankoutputthatmaximizesthebank’svalue.Note,thatthispathisnotgenerallyequivalenttothepaththatminimizesthebank’scost.SeeHughesandMester(2013a,2013b)forfurtherdiscussion.

6

capturessuchmanagerialphenomenaassub‐parinvestmentstrategies,perquisiteconsumption,

takingtoolittleortoomuchrisktoenhancecontrol,nepotism,prejudicialdiscrimination,andsub‐

parlocationaldecisions.Whilethemarketvalueofassetsnormalizedbythebookvalue,a

commonlyusedproxyforTobin’sq,measuresachievedperformance,themarket‐valueinefficiency

ratiogaugestheshortfallbetweenbest‐practiceandachievedperformanceand,assuch,measures

theextentofagencycosts.

Ineachofthetwoyears,weusemaximumlikelihoodtechniquestoestimatethehighest

potentialvalueofabank’sinvestmentinitsassetsbyfittinganupperenvelopeofthemarketvalue

ofbanks’assets(MVA)totheirreplacementcost,proxiedbytheirbookvaluenetofgoodwill(BVA):

MVAi=+(BVAi)+(BVAi)2+i, (1)

wherei=i−iisacompositeerrortermusedtodistinguishstatisticalnoise,i~iidN(0,2),

fromthesystematicshortfall,i(0),frombanki’shighestpotential(frontier)marketvalue.We

assumethatiisdistributednormallyforthe2007frontier,i(0)~iidN(0,2),and,forthe

2013frontier,exponentially,i(>0)~θexp(−θu).Thequadraticspecificationallowsthefrontier

tobenonlinear.Thefrontiervalue,FMVAi,isgivenbythedeterministickernelofthestochastic

frontier,

FMVAi=+(BVAi)+(BVAi)2. (2)

Thestochasticfrontier,SFMVAi,consistsofthedeterministickernelandthetwo‐sidederrorterm:

SFMVAi=FMVAi+i.Figure1illustratestherelationshipofthedeterministickerneltoobserved

marketvalueatanygivenbook‐valueinvestmentinassets.

Thedifferencebetweenabank'sstochasticfrontiermarketvalueandtheobservedmarket

valuedefinesthebank’smarket‐valueshortfall,i,whichismeasuredindollarsoflostmarket

value.Formally,abank’sshortfallisdefinedeitherbythedifferencebetweenitspotentialvalueon

7

thestochasticfrontieranditsobservedmarketvalueor,equivalently,bythedifferencebetweenits

valueonthedeterministickernelanditsnoise‐adjustedmarketvalue:

i=SFMVAi−MVAi=FMVAi−(MVAi−i), (3)

whereMVAi−iisthenoise‐adjustedobservedmarketvalueofassets.Sincetheshortfall,i,cannot

bedirectlymeasured,itisestimatedastheexpectationoficonditionaloni:

shortfalli=E(i|i)=FMVAi−(MVAi−E(i|i)). (4)

Formoredetailsonthistechnique,seeBauer(1990)andJondrow,Lovell,Materov,and

Schmidt(1982).Themarket‐valueinefficiencyratioexpressestheshortfallasaproportionof

thehighestpotentialvalue:

market‐valueinefficiencyratioi=shortfalli/FMVAi=E(i|i)/FMVAi. (5)

We can use the noise‐adjustedobservedmarketvalueexpressedin(3)to adjust the

standardproxyforTobin’sqratio,

Tobin’sqratio=MVAi/BVAi, (6)

fornoise:

noise‐adjustedTobin’sqratio=(MVAi−i)/BVAi. (7)

Anumberofstudieshaveusedthemarket‐valueinefficiencyratioaswellasthenoise‐adjustedq

ratiotomeasureperformance.8

Figure1(reproducedfromHughes,Jagtiani,andMester,2016)providesanillustrationof

theconcepts.Inthisexample,bankiinvests100inassetsandachievesamarketvalueadjustedfor

statisticalnoise,i,of108.Itshighestpotentialvalueis120.Theshortfallofitsachievedvalue 8See,forexample,Hughes,Lang,Mester,andMoon(1999);HabibandLjungqvist(2005);DeJongheandVanderVennet(2005);HughesandMoon(2003);Hughes,Mester,andMoon(2001);Hughes,Lang,Mester,Moon,andPagano(2003);Baele,DeJonghe,andVanderVennet(2007);andHughesandMester(2013a,2013b).

8

fromitspotentialis12(=120‐108).Itsmarket‐valueinefficiencyratiois0.10(=12/120),andits

noise‐adjustedTobin’sqratiois1.08(=108/100).

III.MeasuringtheValueofInvestmentOpportunities9

Inadditiontomeasuringfinancialperformance,Tobin’sqratioisalsousedtomeasurethe

valueofinvestmentopportunities.Forexample,Yermack(2006)usestheqratiotomeasureand

controlforthevalueofinvestmentopportunitiesinregressionsintendedtoexplainthepersonal

useofcompanyjetsbytheCEO.InregressionstoexplainCEOcompensation,Core,Holthausen,and

Larcker(1999)usethemarket‐to‐bookratiotocontrolforthevalueofinvestmentopportunities.

TheaccuracyofTobin’sqratioasameasureofthevalueofafirm’sinvestmentopportunitiesis

compromisedwhenagencyproblemsreduceafirm’smarketvalue.Toavoidthisbias,themeasure

shouldbeindependentoftheactionsofafirm’smanagement,anditshouldgaugethehighest

potentialvalueofafirm’sinvestmentopportunities.Thestochasticfrontierestimationcanbeused

toobtainthehighestpotentialvalueofassetsintheparticularmarketsinwhichafirmoperates.This

frontierdiffersfromthefrontierin(1)usedtoestimatethehighestpotentialvalueoverallmarkets

inwhichfirmsinthesampleoperate.Inthecaseoftheefficiencyfrontier(1),abank’shighest

potentialvalueisgaugedfromitspeerswiththesamebook‐valueinvestmentinassets.Inthecase

oftheinvestmentopportunityfrontier,abank’speersarenotjustthoseofthesamesize,butalso

thoseoperatingundersimilarmarketconditionssuchasthemacroeconomicgrowthrateand

marketconcentration.Sincethisfrontierisestimatedovertheentiresampleofbanks,the

estimatedhighestpotentialvalueoftheinvestmentopportunitiesofanyindividualbankis

independentofitsownachievedvalue.

Weobtainthispotentialvaluebyaddingvariablestothefrontierin(1)thatcapturethe

economicopportunitiesofthemarketsinwhichabankoperates–theweightedten‐yearaverage

9ThissectionfollowstheoriginalexpositionofHughes,Lang,Moon,andPagano(1997),whichisrestatedmorerecentlyinHughes,Mester,andMoon(2016)andHughes,Jagtiani,andMester(2016).

9

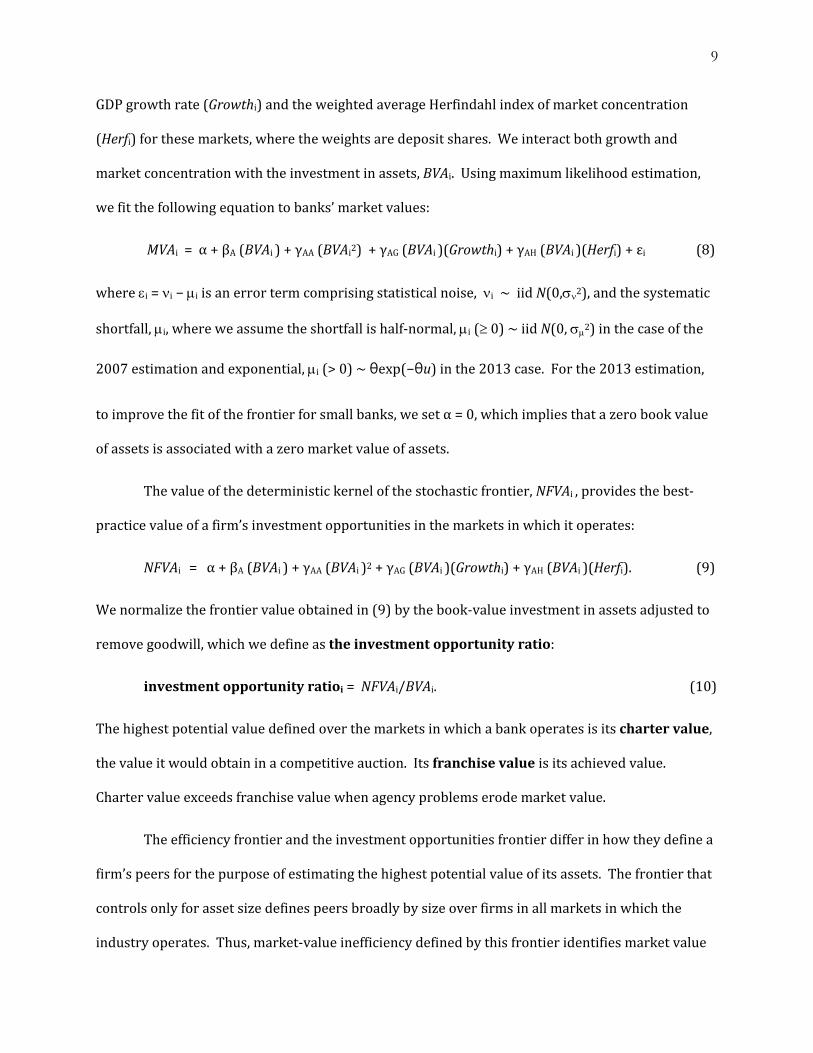

GDPgrowthrate(Growthi)andtheweightedaverageHerfindahlindexofmarketconcentration

(Herfi)forthesemarkets,wheretheweightsaredepositshares.Weinteractbothgrowthand

marketconcentrationwiththeinvestmentinassets,BVAi.Usingmaximumlikelihoodestimation,

wefitthefollowingequationtobanks’marketvalues:

MVAi=α+βA(BVAi)+γAA(BVAi2)+γAG(BVAi)(Growthi)+γAH(BVAi)(Herfi)+εi (8)

wherei=i−iisanerrortermcomprisingstatisticalnoise,i~iidN(0,2),andthesystematic

shortfall,i,whereweassumetheshortfallishalf‐normal,i(0)~iidN(0,2)inthecaseofthe

2007estimationandexponential,i(>0)~θexp(−θu)inthe2013case.Forthe2013estimation,

toimprovethefitofthefrontierforsmallbanks,wesetα=0,whichimpliesthatazerobookvalue

ofassetsisassociatedwithazeromarketvalueofassets.

Thevalueofthedeterministickernelofthestochasticfrontier,NFVAi,providesthebest‐

practicevalueofafirm’sinvestmentopportunitiesinthemarketsinwhichitoperates:

NFVAi=α+βA(BVAi)+γAA(BVAi)2+γAG(BVAi)(Growthi)+γAH(BVAi)(Herfi). (9)

Wenormalizethefrontiervalueobtainedin(9)bythebook‐valueinvestmentinassetsadjustedto

removegoodwill,whichwedefineastheinvestmentopportunityratio:

investmentopportunityratioi=NFVAi/BVAi. (10)

Thehighestpotentialvaluedefinedoverthemarketsinwhichabankoperatesisitschartervalue,

thevalueitwouldobtaininacompetitiveauction.Itsfranchisevalueisitsachievedvalue.

Chartervalueexceedsfranchisevaluewhenagencyproblemserodemarketvalue.

Theefficiencyfrontierandtheinvestmentopportunitiesfrontierdifferinhowtheydefinea

firm’speersforthepurposeofestimatingthehighestpotentialvalueofitsassets.Thefrontierthat

controlsonlyforassetsizedefinespeersbroadlybysizeoverfirmsinallmarketsinwhichthe

industryoperates.Thus,market‐valueinefficiencydefinedbythisfrontieridentifiesmarketvalue

10

fromfirmsoperatinginthemostvaluablemarketsandpenalizesfirmsoperatinginlessvaluable

markets–justascapitalmarketspenalizesuchmarketdisadvantages.Ontheotherhand,the

frontierthatcontrolsforassetsizeaswellasmarketconditionsestimatespotentialvalueforpeers

ofsimilarsizeandmarketopportunities.Thisvalueforanyfirmisgenerallylessthanthatobtained

fromtheformerfrontier.

IV.TheData

Weuse2007dataon219publiclytraded,top‐tierbankholdingcompaniesand2013data

on303companiestoestimatetheefficiencyfrontierandtheinvestmentopportunitiesfrontier.

Dataonownershipandboardstructurelimitthe2007sampleto142holdingcompaniesandthe

2013sampleto167companies.Balance‐sheetandincomestatementdataareobtainedfromthe

Y9‐CCallReportsfiledquarterlywithregulatorsandavailableonthewebsiteoftheFederal

ReserveBankofChicago.CompustatgivesdataonmarketvaluewhiletheCorporateLibrary

providesdataonownershipstructure.AlistofvariablesandtheirdefinitionsisgiveninTable1,

whilesummarystatisticsfor2013and2007aregiveninTables2and3,respectively.

V.FinancialPerformanceandCapitalStructure

Toexploretherelationshipbetweenbanks’financialperformanceandcapitalstructure,we

regressperformancemeasuredbyln(marketvalueofassets)andbythemarket‐valueinefficiency

ratiooncapitalstructureandasetofcontrolvariables,includingassetsize,assetallocation,off‐

balance‐sheetactivities,assetquality,ownershipstructure,andthevalueofinvestment

opportunities.Whilethemarketvalueofassetsmeasuresachievedfinancialperformanceandis

thuscorrelatedwithagencycosts,themarket‐valueinefficiencyratiomoredirectlymeasures

agencycostsasthedifferencebetweenbest‐practiceperformanceandnoise‐adjustedachieved

performance.

11

A.ControllingforCapitalStructure

Theinfluenceofcapitalstructurecandifferbetweenlargerandsmallerbanks.Thebetter

diversificationoflargerbankscouldimplythat,foranygivenexpectedreturn,thelowerassociated

returnriskyieldsalowerriskofinsolvencyforanygivenequitycapitalratio.Tocapturethis

difference,weinteracttheratioofequitycapitalwiththelogofassets.

Theinfluenceofcapitalstructurecanalsodifferbetweenbankswithlower‐andhigher‐

valuedinvestmentopportunities.Asexplainedpreviously,forthosewithlower‐valued

opportunities,higherrisk‐takingmightbecorrelatedwithhighermarketvalue,while,forthose

withlower‐valuedopportunities,lowerrisk‐takingmightbecorrelatedwithhighervalue.Forthe

former,ahigherrisk‐takingstrategycanbeassociatedwithalowercapitalratio,and,forthelatter,

alowerrisk‐takingstrategy,withahighercapitalratio.Tocapturethispossibility,weinteractthe

equitycapitalratiowiththeinvestmentopportunityratio.

Asaresultoftheseinteractionsofthecapitalratiowiththelogofassetsandtheinvestment

opportunityratio,thederivativeofperformancewithrespecttothecapitalratiowilldependnot

justonthecapitalratiobutalsoonthesizeofthebankandthevalueofthebank’sinvestment

opportunities.

Animportantcomponentofdebtthatdistinguishesthebusinessstrategyofbanksistheir

relianceondeposits.Consequently,weincludetheratioofdepositstototalborrowedfunds.

B.ControllingforAssetAllocation,Off‐Balance‐SheetActivities,andAssetQuality

Weaccountfortheconsolidatedassetsofbanksbyincludingtwoterms:thelogofthebook

valueofassetsandthelogsquared.Wecharacterizetheallocationofassetsbytheratiooftotal

loanstoassetsandtheratioofliquidassetstoassets.Liquidassetsaredefinedasthesumofcash,

balancesatotherfinancialinstitutions,federalfundssold,securities,andsecuritiessoldunder

agreementtorepurchase.Off‐balance‐sheetactivitiesarerepresentedbytheratioofnoninterest

12

incometototalincome.Weaccountforthecompositionoftheloanportfoliowiththefollowing

ratios:residentialrealestateloanstoassets,commercialrealestateloanstoassets,consumerloans

toassets,andbusinessloanstoassets.Loanqualityistakenintoaccountbytheratioof

nonperformingloanstoassets,wherenonperformingloansisthesumofpast‐dueandnonaccrual

loans,grosscharge‐offs,andforeclosedrealestateowned.

C.ControllingforOwnershipStructure

JensenandMeckling(1976)pointoutthattheproportionofoutstandingsharesownedby

aninsiderrepresentstheinsider’spriceofadollaroffirmvalueallocatedtotheinsider’sprivate

benefitandarguethathigherinsiderownershipincreasesthepriceofagencygoodsand,thus,

betteralignstheinterestsofinsideownerswiththoseofoutsideowners–aphenomenontheycall

theconvergence‐of‐interestshypothesis.CitingastudybyWeston(1979)thatfindsthatnofirm

whereinsidersown30percentormoreofoutstandingshareshaseverbeenacquiredinahostile

takeover,Morck,Shleifer,andVishny(1988)hypothesizethatincreasedinsiderownership

enhancesinsiders’controlandmakesitmoredifficulttofirethemortoreplacethembyahostile

takeover–aphenomenontheycallentrenchment.Theyaddtothealignment‐of‐interests

hypothesisasecond,contrastingone,theentrenchmenthypothesis.Asinsiderownership

increases,managers’interestsarebetteralignedwiththoseofoutsideownerssomanagerstendto

consumefeweragencygoods;however,managersalsobecomemoreentrenched–moredifficultto

fire–whichimpliestheytendtoconsumemoreagencygoods.UsingU.S.dataonfirms,Morck,

Shleifer,andVishny(1988)estimateapiece‐wiselinearrelationshipbetweenTobin’sqratioand

ownershipbyofficersanddirectors.Forlevelsofinsiderownershipbetween0and5percent,they

findastatisticallysignificant,positiverelationship;between5and25percent,asignificantnegative

relationship;andover25percent,weakerevidenceofapositiverelationship.Theyinterpretthe

positivesignsasevidencethattheconvergence‐of‐interestshypothesisdominatesentrenchment

andthenegativesign,thatentrenchmentdominatesconvergence.DeYoung,Spong,andSullivan

13

(2001)reachsimilarconclusionsfromregressionsthatrelateperformancetoaquadratic

specificationofownershipatbanks.HughesandMester(2013a)useacubicspecificationof

ownershipandfindthethreeregimesofMorck,Shleifer,andVishny(1988),alsoatU.S.banks.

Thesespecificationsassumethattherelationshipbetweenperformanceandagivenlevelof

insiderownershipisindependentofthesizeofthefirm.However,ownershipatlargefinancial

institutionsislimitedbythepersonalwealthofinsiders.Thus,theperformanceincentivesof

owning5percentofoutstandingsharesatalargebankarelikelytodifferfromthoseatasmall

bank.Weallowassetsizetoinfluenceperformanceincentivesbyinteractingtheproportionof

outstandingsharesownedbyinsidersandthesquaredproportionwiththelogarithmic

transformationofassetsize.Asaresultoftheseinteractions,thederivativeofperformancewith

respecttoinsiderownershipdependsnotjustontheproportionofinsiderownership,butalsoon

thelogofassetsizeandtheinteractionofinsiderownershipandthelogofassetsize.

Inaddition,theperformanceincentivescreatedbymanagerialownershipmaydifferbythe

valueofinvestmentopportunitiesthebankexperiences.Higher‐valuedinvestmentopportunities

mayrelieveperformancepressuresonmanagersandallowthemtoconsumemoreagencygoods

whileachievingarelativelyhighmarketvalue.Weinvestigatethisincentivebyinteractingthe

proportionandthesquaredproportionofoutstandingsharesownedbyinsiderswiththe

investmentopportunityratio.Wefollowasimilarstrategywithrespecttotheproportionof

outstandingsharesownedbyblockholders:weinteractthisproportionwiththelogofassetsand

withtheinvestmentopportunityratio.

14

D.ThePerformanceEquations

Weapplythegeneral‐to‐specificmodelingstrategytoidentifythebestspecificationforeach

year’stwoperformanceequations.10Ineachregression,westartwiththesamegeneral

specification,whichincludesalltheexplanatoryvariablesdescribedabove.Therootexplanatory

variablesweconsiderincludetheln(bookvalueofassets)andln(bookvalueofassets)squared;

assetquality,measuredbytheratioofnonperformingloanstototalassets;theproportionof

outstandingcommonsharesownedbyofficersanddirectorsattheendoftheprioryearinteracted

withtheln(bookvalueofassets),andinteractedwiththeinvestmentopportunityratio;the

proportionofoutstandingsharesownedbyblockholders,thatis,holdersof5percentormoreof

outstandingsharesattheendoftheprioryearinteractedwithtwovariables,theln(bookvalueof

assets)andtheinvestmentopportunityratio;11theratiosofloanstoassets,residentialrealestate

loanstoassets,commercialrealestateloanstoassets,consumerloanstoassets,andbusinessloans

toassets;theratioofliquidassetstoassets;off‐balance‐sheetactivitiesmeasuredbytheratioof

noninterestincometototalincome;theratioofdepositstototalborrowedfunds;andtheratioof

equitycapitaltoassetsanditsinteractionwithtwovariables,theln(bookvalueofassets)andthe

investmentopportunityratio.Table1givesthedefinitionsofthesevariables.

Ourinitialspecificationincludesthese20controlvariablesandaninterceptterm.Wefocus,

inpart,ontheeffectsofthecapitalratio’sinteractionwithassetsizeandwiththevalueof

investmentopportunitiesonperformance;consequently,wekeepthesetwovariablesinthe

processofapplyingthegeneral‐to‐specificmodelingstrategy.Hence,exceptforthesetwo

variables,weremovetheexplanatoryvariableassociatedwiththelargestreductionintheAkaike

10Hendry(1983)providesthefirstcompleteapplication.Campos,Ericsson,andHendry(2005)giveandoverviewofthetechnique.Maddala(2001,pp.483‐484)providesatextbook‐levelintroductiontothegeneral‐to‐specificapproach.

11Weusedlaggedownershipstructuretodealwiththeendogeneityofcontemporaneousownership.Inprinciple,onecouldaddresstheendogeneityissueusinginstrumentalvariables,butwecouldnotdeterminegoodinstrumentsthatexplainownershipbutnotfinancialperformance.

15

InformationCriterion(AIC),one–by‐onesequentiallyuntiltheAICstopsdecreasing.Wecarryout

thisstrategyfortheregressionsinvolvingeachofthetwoperformancemeasuresforeachofthe

twoyears.12

Insummary,thegeneralspecificationsoftheperformanceequationsweestimateareas

follows:

Pi=a+Xβ+εi. (11)

wherePi=Performance,asmeasuredbyln(marketvalueofassetsin$1000s)andmarket‐value

inefficiency,andXisthesetofregressors:

nonperformingloans/assets,

insiderownership*ln(bookvalueofassetsin$1000s),

insiderownership*investmentopportunityratio,

insiderownershipsquared*ln(bookvalueofassetsin$1000s),

insiderownershipsquared*investmentopportunityratio,

blockholderownership*ln(bookvalueofassetsin$1000s),

blockholderownership*investmentopportunityratio,

totalloans/totalassets,

residentialrealestateloans/totalassets,

commercialrealestateloans/totalassets,

consumerloans/totalassets,

businessloans/totalassets,

liquidassets/totalassets,

noninterestincome/totalincome,

deposits/totalborrowedfunds,

12Forthe2013ln(marketvalueofassets)regressions,reportedinTable4,theAICdeclinesfrom581.8334forthegeneralspecificationto589.7162forthefinalspecification.Forthe2013market‐valueinefficiencyregressions,theAICdeclinesfrom655.8724forthegeneralspecificationto664.9186forthefinalspecification.Forthe2007ln(marketvalueofassets)regressions,reportedinTable8,theAICdeclinesfrom550.9030forthegeneralspecificationto567.2802forthefinalspecification.Forthe2007market‐valueinefficiencyregressions,theAICdeclinesfrom566.3939forthegeneralspecificationto577.2006forthefinalspecification.

16

equitycapital/totalassets,

equitycapitalratio*ln(bookvalueofassetsin$1000s),

equitycapitalratio*investmentopportunityratio,

ln(bookvalueofassetsin$1000s),

ln(bookvalueofassetsin$1000s)squared.

E.PerformanceIncentivesofCapitalStructure:TheTwoFacesofEquity

Tables4and8reporttheresultsoftheperformanceregressionsfor2013and2007,

respectively.Thegeneralandfinalspecificationsarereportedforeachperformancemeasure.We

focusonthetwofinalspecificationsforeachyearand,withinthosespecifications,theresultsfor

therelationshipofperformancetothecapitalstrategy.

BasedontheestimatedparametersreportedinTable4for2013,thederivativeof

ln(marketvalueofassets($1000))withrespecttothecapitalratiois:

∂ln marketvalueassets)/∂capitalratio=4.83162+(0.23864)(ln(book‐valueassets(1000s))

+(0.65724)(investment‐opportunityratio). (12)

(Coefficientsinboldprintarestatisticallydifferentfrom0ata10percentorbetterlevel.)The

estimatedvalueofthederivativeispositivefor132banksandnegativefor35and97ofthepositive

valuesand15ofthenegativevaluesaresignificantlydifferentfrom0.Onthemargin,areductionin

thecapitalratioatthese15banksexhibitinganegativevalueisassociatedwithahighermarket

value,whichsuggeststhatmarketdisciplinemayworkagainstfinancialstabilityatthesebanks.

Table5liststhese15banksindescendingorderofconsolidatedassets.Notethateachhasmore

than$50billioninassets,whichmakesthemsubjecttoincreasedregulatoryscrutinyunderthe

Dodd‐FrankAct.

Thecomparablederivativewhenperformanceattheendof2013ismeasuredbymarket‐

valueinefficiencyis

17

∂market‐valueinefficiency/∂capitalratio=12.84052+(0.45283)(ln(book‐valueassets(1000s))

+(4.25213)(investment‐opportunityratio). (13)

Inthiscase,133bankshaveanegativevalue,with110beingstatisticallysignificant,and33havea

positivevalue,with20beingstatisticallysignificant.13Thus,atthemargin,areductioninthe

capitalratioatthese20banksiscorrelatedwithreducedmarket‐valueinefficiency,whichsuggests

marketdisciplineatthesebankscouldworkagainstfinancialstability.Table5reportsthesebanks

indescendingorderbyassetsize.Eachholdsconsolidatedassetsgreaterthan$50billion.

Toillustrate,considerthelargestbankonthelistinTable5,JPMorganChase.Thevalueof

thederivativeofln(market‐valueassets)withrespecttotheequitycapitalratioisestimatedtobe

0.99720,indicatingthatadecreaseintheequitycapitalratioof0.01isassociatedwitha+0.997

percentincreaseinmarketvalue.Thenextthreelargestfinancialinstitutionsexhibitasimilar

effect.Thevalueofthederivativeofmarket‐valueinefficiencywithrespecttotheequitycapital

ratioforJPMorganChaseisestimatedtobe1.29674,indicatingthatadecreaseintheequitycapital

ratioof0.01isassociatedwithadecreaseof0.0129674initsmarket‐valueinefficiencyratio.

Twoofthenextthreelargestfinancialinstitutionsexhibitaperformanceeffectofsimilar

magnitude.

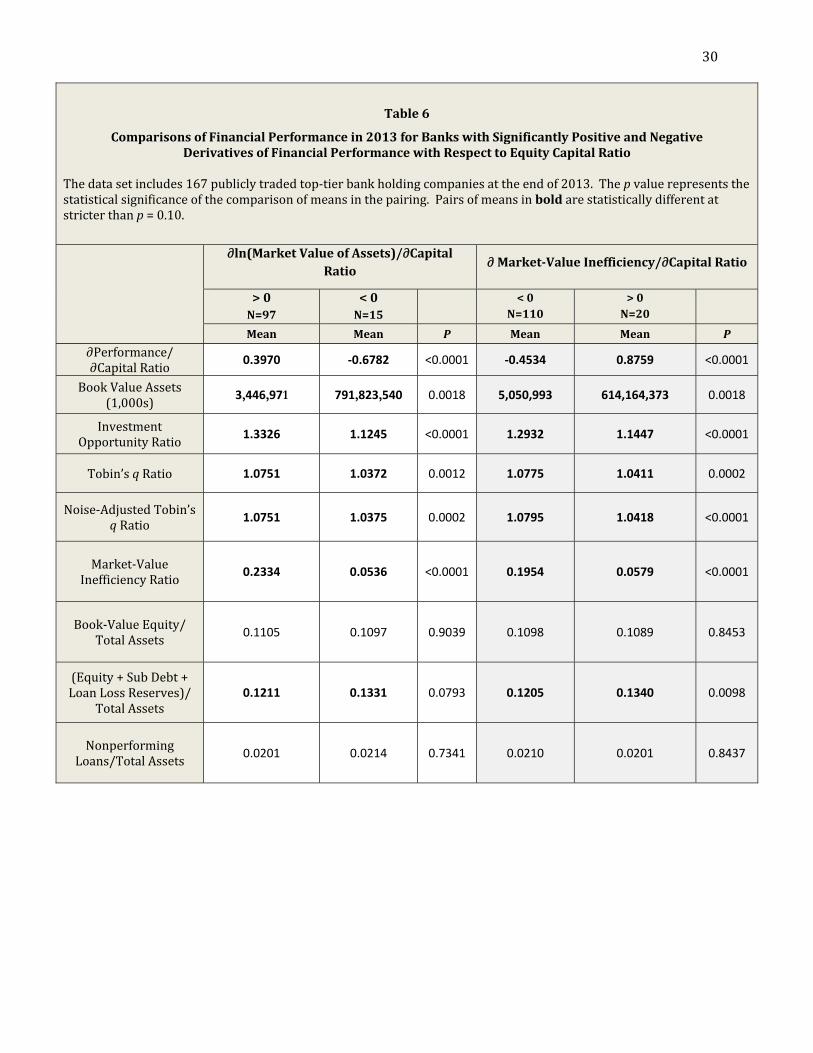

Tables6and7comparethemeansofkeyvariablesforthegroupsofbankswithpositive

andnegativederivativesfor2013.Asshownincolumns2and5ofTable6,forthebankswhose

performanceispositivelyrelatedtotheircapitalratio(whichisthemajority),anincreaseof0.01in

thecapitalratioisassociatedwithanaverageincreaseof0.3970percentinmarketvalueanda

0.4534percentdecreaseinmarket‐valueinefficiency(thatis,withhigherefficiency).Forbanks

whoseperformanceisnegativelyrelatedtotheircapitalratio(whichisasmallnumberofbanks),

anincreaseof0.01intheircapitalratioisassociatedwithanaveragedecreaseof0.6782percentin

13Weobtainedestimatesofmarket‐valueinefficiencyforthe166observationsforwhichwehaddataonthemarketvalueofassets.

18

theirmarketvalueandanaverageincreaseof0.8759intheirmarket‐valueinefficiency.Thus,for

thissmallnumberofbanks,therearemarketincentivestoreducetheircapitalratiosonthemargin.

Butnotethattheaveragesizeofbanksinthiscategoryisconsiderablylargerthanthatofbanksin

theothercategorythatexperiencetheincentivetoincreasetheircapitalratio.The15bankswhose

ln(marketvalueofassets)isnegativelyrelatedtothecapitalratioholdonaverage$791.8billionin

assetsasopposedtothe97withapositivederivativethatholdonaverage$3.4billioninassets.

Similarly,the20bankswhosemarket‐valueinefficiencyispositivelyrelatedtothecapitalratio

holdonaverage$614.2billioninassets,whilethe110bankswithanegativederivativeholdon

average$5.1billioninassets.Thebankswhoseperformanceisnegativelyrelatedtotheircapital

ratioholdmorethan$50billioninassets,whichmakesthemsubjecttoincreasedregulatory

scrutinyundertheDodd‐FrankAct.TheselargebanksonaverageachievealowerTobin’sqratio

butalsoexhibitlower‐valuedinvestmentopportunities.Nevertheless,theyachieveahigher

proportionoftheirpotentialmarketvalue–alowermarket‐valueinefficiencyratio.Hence,it

appearsthattheyexploittheirlower‐valuedinvestmentopportunitiesmoreeffectively.Finally,

theyholdonaverageahigherratioofTier1andTier2capitaltoassets.14Table7comparesmeans

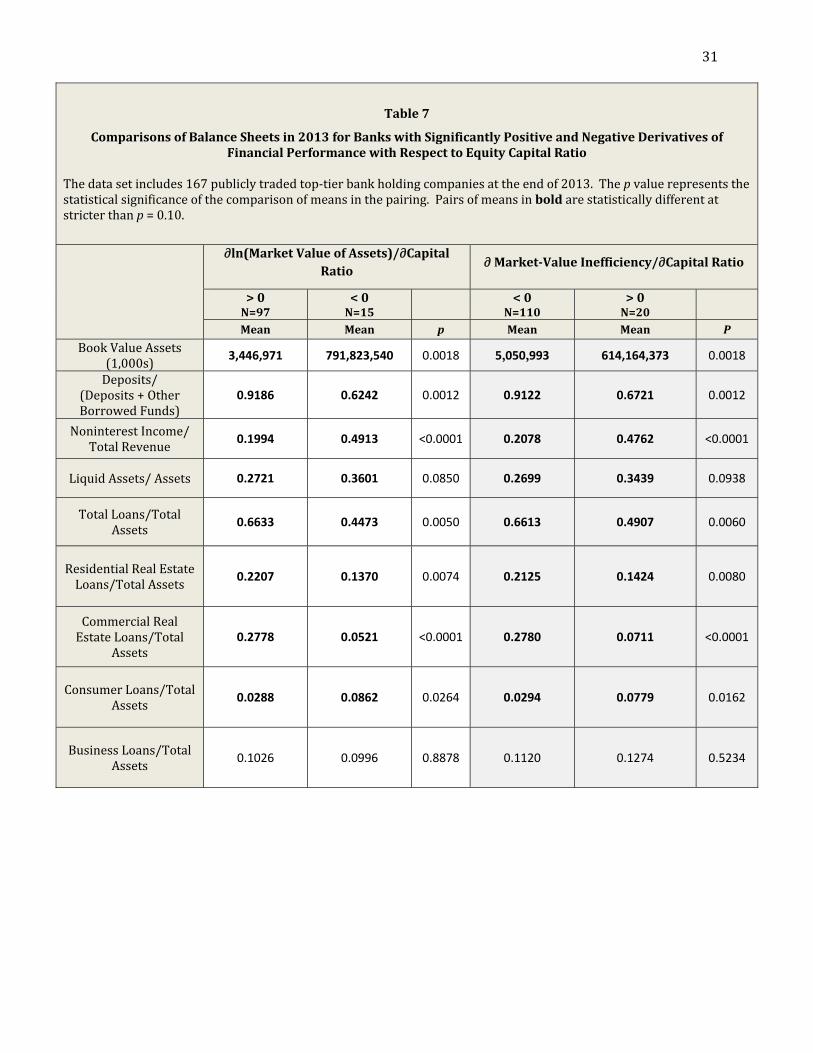

ofvariablesthatcharacterizeassetallocation,off‐balance‐sheetactivities,andrelianceondeposits

forthesetwogroupsofbanks.Asexpected,thesedifferencesreflectthewell‐knowndifferences

betweenlargerandsmallerbanks.

Tables8‐11repeattheanalysisaboveusing2007data.Table8reportstheresultsofthe

performanceregressions.Thederivativeofln(marketvalueofassets($1000))withrespecttothe

capitalratiois:

∂ln marketvalueassets)/∂capitalratio=0.13844+(0.13707)(ln(book‐valueassets(1000s))

+(1.80742)(investment‐opportunityratio). (14)

14TheTier1capitalratioisgivenbythevariableecap_assets,whiletheratiocomprisingthesumofTier1andTier2isgivenbyfcap_assets.

19

Theestimatedvalueofthederivativeispositivefor33banksandnegativefor109,showingthat

rightbeforethecrisishit,fewbanksappearedtohaveamarket‐drivenincentivetoincreasetheir

capitalratio,whilemanyappearedtoexperiencetheoppositeincentive.Noneofthe33positively

valuedderivativesisstatisticallysignificant;only29ofthe109negativelyvaluedderivativesare

statisticallysignificant,butthesebanksareamongthelargestbanksinthesample.PanelAof

Table9liststhederivativesforthe17bankswhoseassetsexceeded$50billionin2007.Notethat

forallofthesebanks,theirderivativesofperformancewithrespecttotheequitycapitalratioare

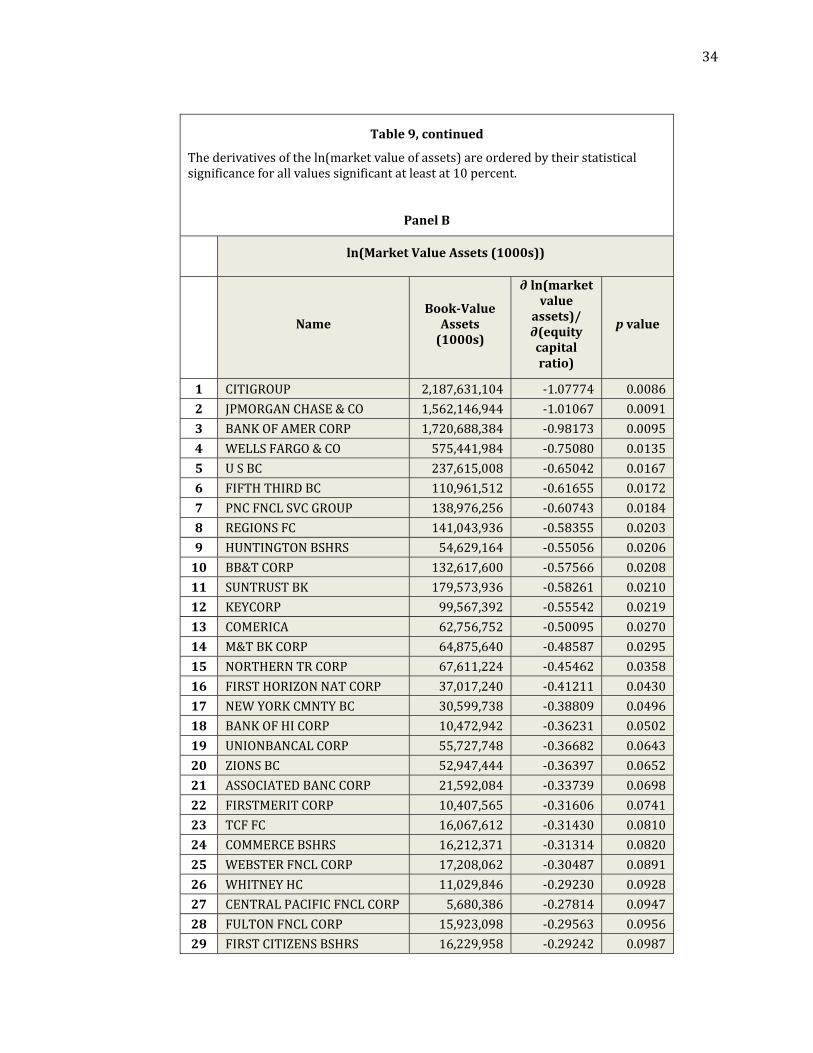

statisticallysignificantlynegative.PanelBofTable9showsall29bankswithstatistically

significantnegativederivatives,orderedbytheirstatisticalsignificance.Thecapital‐market

incentivetoreducethecapitalratioextendsfromthelargestbankstomuchsmallerbanks.Tables

10and11comparethemeansofkeyvariablesforthese29bankswiththoseofthe33bankswith

positivebutstatisticallyinsignificantderivatives.These29banksareonaveragemuchlargerand

exhibitthetypicalcharacteristicsoflargerbanks.

Whenperformanceismeasuredbymarket‐valueinefficiency,thederivativeofperformance

withrespecttotheequitycapitalratiois

∂market‐valueinefficiency/∂capitalratio=3.18169+(0.27177)(ln(book‐valueassets(1000s))

+(1.02550)(investment‐opportunityratio).(15)

Theestimatedderivativeisnegativefor96banks(with61ofthesestatisticallysignificant)and

positivefor46banks(with13ofthesestatisticallysignificant).Thus,increasingthecapitalratiois

associatedwithreducedmarket‐valueinefficiency(thatis,betterperformance)at61banks.But

reducingthecapitalratioatthe13bankswithasignificantpositivederivativeisassociatedwith

reducedmarket‐valueinefficiency.Thissuggeststhatmarketdisciplinemightworkagainst

financialstabilityatthesebankstotheextentthatitgivesanincentivetolowercapitalratios.As

showninTable9,all13bankswithasignificantpositivederivativehadassetsgreaterthan$50

billionin2007.

20

Toillustrate,considerthelargestbankonthelistinTable9,Citigroup.Thevalueofthe

derivativeofln(market‐valueassets)withrespecttotheequitycapitalratioisestimatedtobe

1.07774,indicatingthatadecreaseintheequitycapitalratioof0.01isassociatedwitha

+1.07774percentincreaseinmarketvalue.Thenexttwolargestfinancialinstitutionsexhibita

similareffect.Thevalueofthederivativeofmarket‐valueinefficiencywithrespecttotheequity

capitalratioforCitigroupisestimatedtobe1.60196,indicatingthatadecreaseintheequitycapital

ratioof0.01isassociatedwithadecreaseof0.0160196initsmarket‐valueinefficiencyratio.

Thenexttwolargestfinancialinstitutionsexhibitaperformanceeffectofsimilarmagnitude.These

resultssuggestthatthecapitalmarketappearstorewardriskiercapitalstrategiesin2007.

Ofcourse,ourresultsarebasedonsimpleregressions,andthereareseveralcaveatsthat

oneshouldapplytoavoidover‐interpretingtheseresults.Inparticular,wecannotinfercausation

fromtheseresults.Wetaketheresultsasmerelysuggestiveofastatisticallysignificantassociation

thatcallsforfurtheranalysis.Butwealsotakethemasacautionthatoneshouldbecarefulnotto

assumethatmarketdisciplinewilldriveincentivesleadingtoamorestablefinancialsystem.A

naturalconclusionwouldbethatregulatorycapitalrequirementsarenecessary.

V.Conclusions

Usingmeasuresofperformanceandinvestmentopportunitiesderivedfromstochastic

frontieranalysisand2007and2013dataontop‐tier,publiclytradedU.S.bankholdingcompanies,

wefindevidenceoftwofacesofequityinvestment.Atbankswithhigher‐valuedinvestment

opportunities,onthemarginanincreaseintheirequitycapitalratioisassociatedwithbetter

financialperformance,whileatbankswithlower‐valuedinvestmentopportunities,amarginal

decreaseintheirequitycapitalratioisassociatedwithbetterfinancialperformance.Becausethe

largestU.S.financialinstitutionstendtohavelower‐valuedinvestmentopportunities,ourresults

suggestthattheymayhaveamarket‐basedincentivetoreducetheircapitalratio.Totheextent

21

thatmarketdisciplinerewardsreducingthecapitalratioamongthelargestbanks,itwouldtendto

underminefinancialstability.Ourresultssupporttheneedforregulatorycapitalrequirements.

22

BibliographyBankforInternationalSettlements,BaselCommitteeonBankingSupervision,(September2001).“Pillar3–MarketDiscipline,”WorkingPapersNo7,http://www.bis.org/publ/bcbs_wp7.htm.Baele,L.,DeJonghe,O.,andVanderVennet,R.(2007).Doesthestockmarketvaluebankdiversification?JournalofBankingandFinance31,1999‐2023.Bauer,PaulW.(1990).Recentdevelopmentsintheeconometricestimationoffrontiers,JournalofEconometrics46,39–56.Calomiris,C.W.andNissim,D.(2007).Activity‐basedvaluationofbankholdingcompanies,WorkingPaper12918,NationalBureauofEconomicResearch.Campos,J.,Ericsson,N.R.,andHendry,D.F.(2005).General‐to‐specificmodeling:anoverviewandselectedbibliography,IntroductioninJ.Campos,N.R.Ericsson,andDavidF.Hendry(eds.),General‐to‐SpecificModeling,EdwardElgarPublishing,Cheltenham.Core,J.E.,Holthausen,R.W.,andLarcker,D.F.(1999).Corporategovernance,chiefexecutiveofficercompensation,andfirmperformance,JournalofFinancialEconomics51,371‐406.DeJonghe,O.andVanderVennet,R.(2005).Competitionversusagencycosts:ananalysisofchartervaluesinEuropeanbanking,WorkingPaper,GhentUniversity.DeYoung,R.,Spong,K.andSullivan,R.J.(2001).Who’smindingthestore?Motivatingandmonitoringhiredmanagersatsmall,closelyheldcommercialbanks.JournalofBankingandFinance25,1209‐1243.Greenspan,Alan(2005).Risktransferandfinancialstability,RemarkstotheFederalReserveBankofChicago’sForty‐FirstAnnualConferenceonBankStructure,Chicago,IL,May5,2005.Greenspan,Alan(2008).TestimonyattheHearingonrheFinancialCrisisandtheRoleofFederalRegulators,beforetheCommitteeonOversightandGovernmentReform,U.S.HouseofRepresentatives,October23,2008,https://www.gpo.gov/fdsys/pkg/CHRG‐110hhrg55764/html/CHRG‐110hhrg55764.htm.Grossman,R.S.(1992).Depositinsurance,regulations,andmoralhazardinthethriftindustry:evidencefromthe1930s,AmericanEconomicReview82,800‐821.Habib,M.A.andLjungqvist,A.(2005).Firmvalueandmanagerialincentives:astochasticfrontierapproach,JournalofBusiness78,2053‐2093.Hendry,D.F.(1983).Econometricmodelling:theconsumptionfunctioninretrospect,ScottishJournalofPoliticalEconomy30,193‐220.Hughes,J.P.,Jagtiani,J.,andMester,L.J.(2016).Isbiggernecessarilybetterincommunitybanking?DepartmentofEconomics,RutgersUniversity,WorkingPaper201604.Hughes,J.P.,Lang,W.,Mester,L.J.,andMoonC.‐G.(1999).Thedollarsandsenseofbankconsolidation,JournalofBankingandFinance23,291‐324.

23

Hughes,J.P.,Lang,W.,Mester,L.J.,MoonC.‐G.,andPagano,M.(2003).Dobankerssacrificevaluetobuildempires?Managerialincentives,industryconsolidation,andfinancialperformance,JournalofBankingandFinance27,417‐447.Hughes,J.P.,Lang,W.,MoonC.‐G.andPagano,M.(1997).Measuringtheefficiencyofcapitalallocationincommercialbanking,WorkingPaper98‐2,FederalReserveBankofPhiladelphia(revisedasWorkingPaper2004‐1,RutgersUniversityEconomicsDepartment).Hughes,J.P.andMester,L.J.(2013a).Aprimeronmarketdisciplineandgovernanceoffinancialinstitutionsforthoseinastateofshockeddisbelief,Chapter2inEfficiencyandProductivityGrowth:ModellingintheFinancialServicesIndustry,F.Pasiouras(ed.),JohnWileyandSons:WestSussex,U.K.,19‐47.Hughes,J.P.andMester,L.J.(2013b).Whosaidlargebanksdon’texperiencescaleeconomies?Evidencefromarisk‐return‐drivencostfunction,JournalofFinancialIntermediation22,559‐585.Hughes,J.P.,Mester,L.J.andMoon,C.‐G.(2016).MeasuringagencycostsandthevalueofinvestmentopportunitiesofU.S.bankholdingcompanieswithstochasticfrontierestimation,forthcomingintheResearchHandbookonCompetitioninBankingandFinance,J.A.BikkerandL.Speirdijk(eds.).Hughes,J.P.,Mester,L.J.,andMoon,C.‐G.(2001).Arescaleeconomiesinbankingelusiveorillusive?Evidenceobtainedbyincorporatingcapitalstructureandrisk‐takingintomodelsofbankproduction,JournalofBankingandFinance25,2169‐2208.Hughes,J.P.andMoonC.‐G.(2003).Estimatingmanagers’utility‐maximizingdemandforagencygoods,WorkingPaper2003‐24,DepartmentofEconomics,RutgersUniversity.Jensen,M.C.andMeckling,W.H.(1976).Theoryofthefirm:managerialbehavior,agencycosts,andownershipstructure,JournalofFinancialEconomics5,305‐360.Jondrow,J.,Lovell,C.A.K.,Materov,I.S.,andSchmidt,P.(1982).Ontheestimationoftechnicalefficiencyinthestochasticfrontierproductionfunctionmodel,JournalofEconometrics19,233–238.Keeley,M.C.(1990).Depositinsurance,risk,andmarketpowerinbanking,AmericanEconomicReview80,1183‐1200.Laeven,L.,andLevine,R.(2009).Bankgovernance,regulationandrisktaking,JournalofFinancialEconomics93,259‐275.Maddala,G.S.(2001).IntroductiontoEconometrics,ThirdEdition,MacmillanPublishingCo.,NewYork.Marcus,A.J.(1984).Deregulationandbankfinancialpolicy,JournalofBankingandFinance8,557‐565.McConnell,J.J.andServaes,H.(1995).Equityownershipandthetwofacesofdebt,JournalofFinancialEconomics39,131‐157.

24

Morck,R.,Shleifer,R.M.andVishny,R.W.(1988).Managementownershipandmarketvaluation:anempiricalanalysis,JournalofFinancialEconomics20,293‐316.Nakamoto,M.andWighton,D.(2007),Citigroupchiefstaysbullishonbuy‐outs,FinancialTimes,July9,2007.Weston,J.F.(1979).Thetendertakeover,MergersandAcquisitions,74‐82.Yermack,D.(2006).Flightsoffancy:corporatejets,CEOperquisites,andinferiorshareholderreturns,JournalofFinancialEconomics80,211‐242.

24

Figure115

Market‐ValueFrontierStochasticfrontierestimationyieldsthepotentialmarketvalueofassetsasaquadraticfrontierofthebookvalueofassetsnetofgoodwill.Theerrorterm,i=i−i,iscomposedofstatisticalnoise,i~iidN(0,2),andthesystematicshortfallfrombanki’shighestpotential(frontier)marketvalue.Forthe2007data,weadoptthehalf‐normaldistribution,i(0)~iidN(0,2),forthisshortfall;andforthe2013data,theexponentialdistribution,i(>0)~θexp(−θu).Thequadraticspecificationallowsthefrontiertobenonlinear.Inthisexample,bankiinvests100inassetsandachievesamarketvalueadjustedforstatisticalnoise,i,of108.Itshighestpotentialvalueis120.Theshortfallofitsachievedvaluefromitspotentialis12(=120‐108).Itsmarket‐valueinefficiencyratiois0.10(=12/120),anditsnoise‐adjustedTobin’sqratiois1.08(=108/100).

15ThisfigureisfromHughes,Jagtiani,andMester(2016)andalsoappearsinHughes,Mester,andMoon(2016).

MarketValueofAssets

DeterministicKernelofthePotential‐ValueFrontierFMVAi=+(BVAi)+(BVAi)2

BookValueofAssets(netofgoodwill)

120

108

100

MVShortfall=12

MVInefficiency=12/120

HighestPotentialMarketValueofAssets=+(BVAi)+(BVAi)2

Noise‐AdjustedAchievedMarketValueofAssets=MVAi−i

AchievedMarketValueofAssets=MVAi−i

i

25

Table1

DataDefinitions

Book‐valueofassetsrepresentsbookvalue(thousands)oftotalconsolidatedassetsattheendoftheyear.Adjustedbookvalueisobtainedbysubtractinggoodwillfrombookvaluetoremovecomponentsderivedfrommarketvalue.Themarketvalueofassetsisproxiedbytheratioofthesumofthebookvalueofliabilitiesandthemarketvalueofequitytotheadjustedbookvalueofassets.

Themarket‐valueinefficiencyratioisameasureofrelativeagencycostsgivenbythedifferencebetweenthehighestpotentialvalueofabank’sassetsoverallmarketsfoundinthesampleandthebank’snoise‐adjustedachievedmarketvalue(lostmarketvalue)dividedbythehighestpotentialvalueofassetsoverallmarkets,whichisestimatedbyastochasticfrontiertechnique.ThevalueofaBHC’sinvestmentopportunitiesismeasuredbyfittingastochasticfrontiertothemarketvalueofassetsasafunctionofthebookvalueofassetsand,inthebank’slocalmarkets,themarket‐weighted,10‐yearaveragemacroeconomicgrowthrateandtheBHC’smarket‐weightedHerfindahlindexofconcentration.Theinvestmentopportunityratioisthehighestpotentialvalueofthebank’sassetsinthemarketsinwhichitoperatesdividedbythebookvalueofassetsadjustedtoremovegoodwill.

Tobin’sqratioistheratioofthemarketvalueofassetstotheadjustedbookvalueofassetswherethemarketvalueofassetsisproxiedbythesumofthemarketvalueofequityandthebookvalueofliabilities.Thenoise‐adjustedTobin’sqratioismarketvalueofassetslessstatisticalnoisederivedfromstochasticfrontierestimation.

Thenonperformingassetsratioisthesumofpast‐dueandnonaccrualloans,grosscharge‐offs,andforeclosedrealestateowneddividedbytotalassets.

Liquidassetsaredefinedasthesumofcash,balancesatotherfinancialinstitutions,federalfundssold,securities,andsecuritiessoldunderagreementtorepurchase.

Theratioofequitycapitaltoassetsisgivenbythesumofcommonstock,retainedearnings,andperpetualpreferredstockdividedbytotalassets.Theratiooffinancialcapitaltoassetsisthesumofequitycapital,loan‐lossreserves,andsubordinateddebtdividedbytotalassets.

Insiderownershipistheproportionofoutstandingsharesownedbyofficersanddirectorsintheyearbefore,i.e.,in2006or2012.Blockholderownershipisthepercentofoutstandingsharesheldbyblockholders(holdersof5percentormoreofoutstandingsharesbasedon13Dfilings)atyear‐end2006or2012.

26

Table2

2013Data:SummaryStatistics

Thedatasetincludes167publiclytradedtop‐tierbankholdingcompaniesattheendof2013.

PanelA:AssetsandFinancialPerformance

N Mean Median Std.Dev.

Minimum

Maximum

BookValueAssets(1,000s) 167 81,361,076 6,039,126 322,211,407 711,515 2,415,689,000

InvestmentOpportunityRatio 167 1.271 1.261 0.103 0.988 1.620

Tobin’sqRatio 167 1.072 1.065 0.055 0.926 1.313

Noise‐AdjustedTobin’sqRatio 166 1.073 1.071 0.039 0.943 1.199

Market‐ValueInefficiency 166 0.169 0.144 0.107 0.000 0.479

PanelB:CapitalStructureandAssetQuality

Book‐ValueEquity/TotalAssets 167 0.113 0.112 0.025 0.069 0.229

(Equity+SubDebt+LoanLossReserves)/TotalAssets 167 0.126 0.125 0.026 0.076 0.241

Deposits/(Deposits+OtherBorrowedFunds)

167 0.876 0.909 0.144 0.104 1.000

NonperformingLoans/TotalAssets 167 0.021 0.018 0.017 0.000 0.166

PanelC:OwnershipStructure

OfficerandDirectorOwnership 167 0.094 0.056 0.119 0.000 0.722

BlockholderOwnership 167 0.185 0.166 0.118 0.000 0.867

PanelD:AssetAllocationandOff‐Balance‐SheetActivities

LiquidAssets/Assets 167 0.282 0.248 0.124 0.019 0.785

NoninterestIncome/TotalRevenue 167 0.259 0.237 0.195 ‐1.129 0.928

TotalLoans/TotalAssets 167 0.633 0.658 0.148 0.055 0.962

ResidentialRealEstateLoans/TotalAssets

167 0.199 0.195 0.109 0.000 0.631

CommercialRealEstateLoans/TotalAssets

167 0.229 0.227 0.122 0.000 0.592

ConsumerLoans/TotalAssets 167 0.041 0.016 0.077 0.000 0.823

BusinessLoans/TotalAssets 167 0.121 0.102 0.082 0.000 0.408

27

Table3

2007Data:SummaryStatistics

Thedatasetincludes142publiclytradedtop‐tierbankholdingcompaniesattheendof2007.

PanelA:AssetsandFinancialPerformance

n Mean Median Std.Dev.

Minimum

Maximum

BookValueAssets(1,000s) 142 57,427,092 4,088,173 269,582,515 659,896 2,187,631,104

InvestmentOpportunityRatio 142 1.103 1.094 0.035 1.025 1.185

Tobin’sqRatio 142 1.071 1.066 0.043 0.978 1.230

Noise‐AdjustedTobin’sqRatio 142 1.069 1.066 0.039 0.983 1.200

Market‐ValueInefficiency 142 0.308 0.314 0.162 0.000 0.719

PanelB:CapitalStructureandAssetQuality

Book‐ValueEquity/TotalAssets 142 0.095 0.094 0.020 0.052 0.176

(Equity+SubDebt+LoanLossReserves)/TotalAssets 142 0.110 0.109 0.022 0.063 0.182

Deposits/(Deposits+OtherBorrowedFunds)

142 0.814 0.830 0.127 0.145 0.991

NonperformingLoans/TotalAssets

142 0.017 0.014 0.013 0.001 0.101

PanelC:OwnershipStructure

OfficerandDirectorOwnership 142 0.120 0.077 0.134 0.000 0.694

BlockholderOwnership 142 0.098 0.078 0.102 0.000 0.725

PanelD:AssetAllocationandOff‐Balance‐SheetActivities

LiquidAssets/Assets 142 0.215 0.192 0.091 0.034 0.555

NoninterestIncome/TotalRevenue

142 0.179 0.162 0.081 0.038 0.496

TotalLoans/TotalAssets 142 0.702 0.723 0.102 0.356 0.885

ResidentialRealEstateLoans/TotalAssets 142 0.220 0.219 0.099 0.023 0.526

CommercialRealEstateLoans/TotalAssets 142 0.269 0.264 0.130 0.005 0.663

ConsumerLoans/TotalAssets 142 0.047 0.032 0.042 0.001 0.216

BusinessLoans/TotalAssets 142 0.134 0.120 0.078 0.023 0.463

28

Table42013FinancialPerformanceRegressions

Thedatarepresent167top‐tier,publiclytradedU.S.bankholdingcompaniesatyear‐end2013.ThedataareobtainedfromtheY9‐CCallReports,Compustat,andtheCorporateLibrary.Performanceismeasuredbytheln(marketvalueofassets)andmarket‐valueinefficiency.RegressionsareestimatedwithOLS,andstandarderrorsareheteroscedasticityconsistent.DefinitionsofthevariablesaregiveninTable1.

Variable

DependentVariableln(MarketValueofAssets) Market‐ValueInefficiency

GeneralSpecification FinalSpecification GeneralSpecification FinalSpecification

ParameterEstimate

Pr>|t|ParameterEstimate

Pr>|t|ParameterEstimate

Pr>|t|ParameterEstimate

Pr>|t|

Intercept ‐0.14431 0.7328 ‐0.29960 0.0849 4.41800 <0.0001 4.66226 <0.0001NonperformingLoans/Assets

‐0.52670 0.0023 ‐0.58965 0.0001 0.42848 0.0160 0.41012 0.0112

ManagerialOwnershipln(B.V.Assets)

0.09900 0.0071 0.09287 0.0086 ‐0.07219 0.0169 ‐0.01517 <0.0001

ManagerialOwnershipInv’tOpp’tyRatio

‐1.02906 0.0177 ‐0.94935 0.0204 0.71128 0.0441

ManagerialOwnership2ln(B.V.Assets)

‐0.11904 0.0212 ‐0.11285 0.0239 0.11877 0.0087 0.03014 <0.0001

ManagerialOwnership2Inv’tOpp’tyRatio

1.06986 0.0836 0.99316 0.0923 ‐1.11336 0.0391

BlockholderOwnershipln(B.V.Assets)

0.00203 0.8093 0.00751 0.4137 0.00282 0.0435

BlockholderOwnershipInv’tOpp’tyRatio

‐0.05257 0.5818 ‐0.03351 0.0838 ‐0.05700 0.6017

Loans/Assets 0.38694 <0.0001 0.30128 <0.0001 ‐0.08701 0.3181

ResidentialRealEstateLoans/Assets

‐0.29420 <0.0001 ‐0.25281 <0.0001 0.08081 0.0354

CommercialRealEstateLoans/Assets

‐0.14888 0.0023 ‐0.11629 0.0043 0.05012 0.1493

ConsumerLoans/Assets ‐0.07224 0.2171 0.00900 0.8771

BusinessLoans/Assets ‐0.30346 <0.0001 ‐0.25269 <0.0001 0.14150 0.0074 0.05449 0.1119

LiquidAssets/Assets 0.17951 0.0774 0.13567 0.0986 0.00967 0.9146

NoninterestIncome/TotalIncome

0.01632 0.4145 ‐0.01015 0.5246

Deposits/TotalBorrowedFunds

‐0.00973 0.7186 ‐0.06009 0.0428 ‐0.07357 0.0116

EquityCapital/Assets 4.09352 0.1405 4.83162 0.0535 ‐12.24445 <0.0001 ‐12.84052 <0.0001EquityCapital/Assetsln(B.V.Assets)

‐0.18899 0.0823 ‐0.23864 0.0141 12.84052 <0.0001 0.45283 <0.0001

EquityCapital/AssetsInv’tOpp’tyRatio

‐0.67394 0.4656 ‐0.65724 0.4311 4.03722 <0.0001 4.25213 <0.0001

ln(B.V.Assets) 0.99567 <0.0001 1.01369 <0.0001 ‐0.42580 <0.0001 ‐0.45100 <0.0001(ln(B.V.Assets))2 0.0003460 0.8086 0.01015 <0.0001 0.01080 <0.0001Number+,‐CapitalRatioDerivatives

132+,35‐ 33+,133‐

Number+,‐StatisticallySignificantCapitalRatioDerivatives

97+,15‐ 20+,110‐

Adj.

R2=0.999N=167

Adj.R2=0.999

N=167Adj.

R2=0.914N=166

Adj.R2=0.914

N=166

29

Table5DerivativeofPerformancewithRespecttoEquityCapitalRatio

for2013BanksSubjecttoEnhancedPrudentialSupervisionUndertheDodd‐FrankAct

Thefullsampleconsistsof167publiclytraded,top‐tier,U.S.bankholdingcompaniesatyear‐end2013.ThedataareobtainedfromtheY9‐CCallReports,Compustat,andtheCorporateLibrary.Performanceismeasuredbytheln(marketvalueofassets)andmarket‐valueinefficiency.Thevalueofthederivativesofln(marketvalueassets(1000s))andmarket‐valueinefficiencywithrespecttoequitycapitalisgivenforthe21bankswhoseconsolidatedassetsexceed$50billionin2013,whichsubjectsthemtoenhancedprudentialsupervisionunderthe2010Dodd‐FrankAct. ln(MarketValueAssets(1000s)) Market‐ValueInefficiencyRatio

NameBook‐ValueAssets(1000s)

∂ln(marketvalueassets)/∂(equitycapitalratio)

pvalue

NameBook‐ValueAssets(1000s)

∂(marketvalue

inefficiency/

∂(equitycapitalratio)

pvalue

1JPMORGANCHASE&CO

2,415,689,000 ‐0.99720 0.0186JPMORGANCHASE&CO

2,415,689,000 1.29674 0.0067

2BANKOFAMERICACORP

2,104,995,000 ‐0.98004 0.0196BANKOFAMERICACORP

2,104,995,000 1.33588 0.0046

3 CITIGROUP 1,880,382,000 ‐0.91374 0.0203 CITIGROUP 1,880,382,000 1.03006 0.0223

4WELLS

FARGO&CO1,527,015,000 ‐0.91295 0.0216

WELLSFARGO&CO

1,527,015,000 1.25207 0.0052

5GOLDMANSACHS

911,595,000 ‐0.77960 0.0264GOLDMANSACHS

911,595,000 0.95224 0.0184

6MORGANSTANLEY

832,702,000 ‐0.76961 0.0272MORGANSTANLEY

832,702,000 0.98639 0.0137

7BANKOFNEWYORKMELLON

374,310,000 ‐0.64148 0.0401BANKOFNEW

YORKMELLON

374,310,000 1.02986 0.0038

8 USBC 364,021,000 ‐0.63616 0.0408 USBC 364,021,000 1.02584 0.0037

9PNCFNCLSVC

GROUP320,596,232 ‐0.62675 0.0447

PNCFNCLSVCGROUP

320,596,232 1.10354 0.0016

10 CAPITALONE 297,282,098 ‐0.58763 0.0457 CAPITALONE 297,282,098 0.93282 0.0057

11STATESTREET

243,028,090 ‐0.55566 0.0520STATESTREET

243,028,090 0.94583 0.0038

12 SUNTRUSTBK 175,380,779 ‐0.48244 0.0653 SUNTRUSTBK 175,380,779 0.71779 0.0166

13 BB&TCORP 183,009,992 ‐0.47257 0.0649 BB&TCORP 183,009,992 0.82806 0.0062

14FIFTHTHIRD

BC129,685,180 ‐0.43037 0.0826

FIFTHTHIRDBC

129,685,180 0.82057 0.0040

15 REGIONSFC 117,661,732 ‐0.38704 0.0935 REGIONSFC 117,661,732 0.64639 0.0172

16NORTHERNTRUSTCORP

102,947,333 ‐0.36513 0.1045NORTHERNTRUSTCORP

102,947,333 0.65037 0.0138

17 KEYCORP 92,991,716 ‐0.32508 0.1250 KEYCORP 92,991,716 0.50223 0.0466

18 M&TBKCORP 85,162,391 ‐0.30277 0.1409 M&TBKCORP 85,162,391 0.45389 0.0648

19 COMERICA 65,356,580 ‐0.26408 0.1760 COMERICA 65,356,580 0.49241 0.0341

20 HUNTINGTONBSHRS

59,476,344 ‐0.25163 0.1908 HUNTINGTONBSHRS

59,476,344 0.51472 0.0240

21 ZIONSBC 56,031,127 ‐0.17253 0.3450 ZIONSBC 56,031,127 0.06803 0.7497

30

Table6

ComparisonsofFinancialPerformancein2013forBankswithSignificantlyPositiveandNegativeDerivativesofFinancialPerformancewithRespecttoEquityCapitalRatio

Thedatasetincludes167publiclytradedtop‐tierbankholdingcompaniesattheendof2013.Thepvaluerepresentsthestatisticalsignificanceofthecomparisonofmeansinthepairing.Pairsofmeansinboldarestatisticallydifferentatstricterthanp=0.10.

∂ln(MarketValueofAssets)/∂CapitalRatio

∂Market‐ValueInefficiency/∂CapitalRatio

>0N=97

<0N=15

<0

N=110>0N=20

Mean Mean P Mean Mean P

∂Performance/∂CapitalRatio

0.3970 ‐0.6782 <0.0001 ‐0.4534 0.8759 <0.0001

BookValueAssets(1,000s)

3,446,971 791,823,540 0.0018 5,050,993 614,164,373 0.0018

InvestmentOpportunityRatio

1.3326 1.1245 <0.0001 1.2932 1.1447 <0.0001

Tobin’sqRatio 1.0751 1.0372 0.0012 1.0775 1.0411 0.0002

Noise‐AdjustedTobin’sqRatio

1.0751 1.0375 0.0002 1.0795 1.0418 <0.0001

Market‐ValueInefficiencyRatio

0.2334 0.0536 <0.0001 0.1954 0.0579 <0.0001

Book‐ValueEquity/TotalAssets

0.1105 0.1097 0.9039 0.1098 0.1089 0.8453

(Equity+SubDebt+LoanLossReserves)/

TotalAssets0.1211 0.1331 0.0793 0.1205 0.1340 0.0098

NonperformingLoans/TotalAssets

0.0201 0.0214 0.7341 0.0210 0.0201 0.8437

31

Table7

ComparisonsofBalanceSheetsin2013forBankswithSignificantlyPositiveandNegativeDerivativesofFinancialPerformancewithRespecttoEquityCapitalRatio

Thedatasetincludes167publiclytradedtop‐tierbankholdingcompaniesattheendof2013.Thepvaluerepresentsthestatisticalsignificanceofthecomparisonofmeansinthepairing.Pairsofmeansinboldarestatisticallydifferentatstricterthanp=0.10.

∂ln(MarketValueofAssets)/∂CapitalRatio

∂Market‐ValueInefficiency/∂CapitalRatio

>0N=97

<0N=15

<0N=110

>0N=20

Mean Mean p Mean Mean P

BookValueAssets(1,000s)

3,446,971 791,823,540 0.0018 5,050,993 614,164,373 0.0018

Deposits/(Deposits+OtherBorrowedFunds)

0.9186 0.6242 0.0012 0.9122 0.6721 0.0012

NoninterestIncome/TotalRevenue

0.1994 0.4913 <0.0001 0.2078 0.4762 <0.0001

LiquidAssets/Assets 0.2721 0.3601 0.0850 0.2699 0.3439 0.0938

TotalLoans/TotalAssets

0.6633 0.4473 0.0050 0.6613 0.4907 0.0060

ResidentialRealEstateLoans/TotalAssets

0.2207 0.1370 0.0074 0.2125 0.1424 0.0080

CommercialRealEstateLoans/Total

Assets0.2778 0.0521 <0.0001 0.2780 0.0711 <0.0001

ConsumerLoans/TotalAssets

0.0288 0.0862 0.0264 0.0294 0.0779 0.0162

BusinessLoans/TotalAssets

0.1026 0.0996 0.8878 0.1120 0.1274 0.5234

32

Table82007FinancialPerformanceRegressions

The data represent 142 top‐tier, publicly traded U. S. bank holding companies at year‐end 2007. The data areobtained from the Y9‐C Call Reports, Compustat, and the Corporate Library. Performance is measured by theln(marketvalueofassets)andmarket‐valueinefficiency.RegressionsareestimatedwithOLS,andstandarderrorsareheteroscedasticityconsistent.DefinitionsofthevariablesaregiveninTable1.

Variable

DependentVariable

ln(MarketValueofAssets) Market‐ValueInefficiency

GeneralSpecification FinalSpecification GeneralSpecification FinalSpecification

ParameterEstimate

Pr>|t|ParameterEstimate

Pr>|t|ParameterEstimate

Pr>|t|ParameterEstimate

Pr>|t|

Intercept 0.13844 0.7533 ‐0.05189 0.8545 7.31855 <0.0001 7.34252 <0.0001NonperformingLoans/Assets

‐0.67809 0.0088 ‐0.66483 0.0099 0.75173 <0.0001 0.76133 <0.0001

ManagerialOwnershipln(B.V.Assets)

0.03316 0.6017 ‐0.19395 0.0063 ‐0.18588 0.0086

ManagerialOwnershipInv’tOpp’tyRatio

‐0.45266 0.6027 2.53973 0.0079 2.42871 0.0105

ManagerialOwnership2ln(B.V.Assets)

‐0.04628 0.6356 ‐0.00481 0.0148 0.27328 0.0084 0.25987 0.0133

ManagerialOwnership2Inv’tOpp’tyRatio

0.56530 0.6741 ‐3.53148 0.0130 ‐3.34379 0.0199

BlockholderOwnershipln(B.V.Assets)

‐0.00580 0.7327 0.05921 0.0007 0.05778 <0.0001

BlockholderOwnershipInv’tOpp’tyRatio

0.06358 0.8062 ‐0.84565 0.0008 ‐0.82201 0.0001

Loans/Assets 0.38876 0.0094 0.36718 0.0006 0.12573 0.4033 0.07407 0.0229ResidentialRealEstateLoans/Assets

0.00466 0.9535 ‐0.01902 0.8100

CommercialRealEstateLoans/Assets

‐0.01280 0.8554 ‐0.00864 0.9011

ConsumerLoans/Assets 0.13241 0.2500 0.10526 0.1690 ‐0.13041 0.1297 ‐0.13423 0.0601

BusinessLoans/Assets 0.01654 0.8791 0.00795 0.9314

LiquidAssets/Assets 0.43322 0.0007 0.43352 0.0002 0.04819 0.7105

NoninterestIncome/TotalIncome

0.21069 <0.0001 0.21166 <0.0001 ‐0.01514 0.7332

Deposits/TotalBorrowedFunds

‐0.04135 0.2873 ‐0.01087 0.7687

EquityCapital/Assets ‐1.17943 0.5936 ‐2.87239 0.2571 ‐3.18169 0.2045EquityCapital/Assetsln(B.V.Assets)

‐0.10135 0.2957 ‐0.13707 0.0069 0.27304 0.0302 0.27177 0.0265

EquityCapital/AssetsInv’tOpp’tyRatio

2.42668 0.0310 1.80742 0.0093 ‐1.27077 0.2608 ‐1.02550 0.3608

ln(B.V.Assets) 0.94103 <0.0001 0.95667 <0.0001 ‐0.75182 <0.0001 ‐0.75002 <0.0001(ln(B.V.Assets))2 0.00192 0.1910 0.00164 0.1521 0.01891 <0.0001 0.01884 <0.0001Number+,‐CapitalRatioDerivatives

33+,109

‐ 46+,96‐

Number+,‐StatisticallySignificantCapitalRatioDerivatives

0+,29‐ 13+,61‐

Adj.R2=0.999

N=142 Adj.R2=0.999

N=142 Adj.R2=0.964

N=142 Adj.R2=0.966

N=142

33

Table9

DerivativeofPerformancewithRespecttoEquityCapitalRatio

for2007BanksSubjecttoEnhancedPrudentialSupervisionUndertheDodd‐FrankAct

Thefullsampleconsistsof142publiclytraded,top‐tier,U.S.bankholdingcompaniesatyear‐end2007.ThedataareobtainedfromtheY9‐CCallReports,Compustat,andtheCorporateLibrary.Performanceismeasuredbytheln(marketvalueofassets)andmarket‐valueinefficiency.Thevalueofthederivativesofln(marketvalueassets(1000s))andmarket‐valueinefficiencywithrespecttoequitycapitalisgivenforthe17bankswhoseconsolidatedassetsexceed$50billionin2007,whichsubjectsthemtoenhancedprudentialsupervisionunderthe2010Dodd‐FrankAct.

PanelA

ln(MarketValueAssets(1000s)) Market‐ValueInefficiencyRatio

NameBook‐ValueAssets(1000s)

∂ln(marketvalueassets)/∂(equitycapitalratio)

pvalue

NameBook‐ValueAssets(1000s)

∂(marketvalue

inefficiency/∂(equity

capitalratio)

pvalue

1 CITIGROUP 2,187,631,104 ‐1.07774 0.0086 CITIGROUP 2,187,631,104 1.60196 0.0365

2BANKOF

AMERCORP1,720,688,384 ‐0.98173 0.0095

BANKOFAMERCORP

1,720,688,384 1.50090 0.0441

3JPMORGANCHASE&CO

1,562,146,944 ‐1.01067 0.0091JPMORGANCHASE&CO

1,562,146,944 1.49857 0.0396

4WELLSFARGO

&CO575,441,984 ‐0.75080 0.0135

WELLSFARGO&CO

575,441,984 1.15738 0.0649

5 USBC 237,615,008 ‐0.65042 0.0167 USBC 237,615,008 0.92884 0.0728

6 SUNTRUSTBK 179,573,936 ‐0.58261 0.0210 SUNTRUSTBK 179,573,936 0.83603 0.0879

7 REGIONSFC 141,043,936 ‐0.58355 0.0203 REGIONSFC 141,043,936 0.78971 0.0829

8PNCFNCLSVC

GROUP138,976,256 ‐0.60743 0.0184

PNCFNCLSVCGROUP

138,976,256 0.80040 0.0751

9 BB&TCORP 132,617,600 ‐0.57566 0.0208 BB&TCORP 132,617,600 0.77329 0.0844

10FIFTHTHIRD

BC110,961,512 ‐0.61655 0.0172

FIFTHTHIRDBC

110,961,512 0.76190 0.0686

11 KEYCORP 99,567,392 ‐0.55542 0.0219 KEYCORP 99,567,392 0.70620 0.0862

12NORTHERNTR

CORP67,611,224 ‐0.45462 0.0358

NORTHERNTRCORP

67,611,224 0.57391 0.1255

13 M&TBKCORP 64,875,640 ‐0.48587 0.0295 M&TBKCORP 64,875,640 0.58363 0.1085

14 COMERICA 62,756,752 ‐0.50095 0.0270 COMERICA 62,756,752 0.58575 0.1009

15UNIONBANCAL

CORP55,727,748 ‐0.36682 0.0643

UNIONBANCALCORP

55,727,748 0.48660 0.1833

16HUNTINGTON

BSHRS54,629,164 ‐0.55056 0.0206

HUNTINGTONBSHRS

54,629,164 0.58698 0.0798

17 ZIONSBC 52,947,444 ‐0.36397 0.0652 ZIONSBC 52,947,444 0.47505 0.1856

34

Table9,continued

Thederivativesoftheln(marketvalueofassets)areorderedbytheirstatisticalsignificanceforallvaluessignificantatleastat10percent.

PanelB

ln(MarketValueAssets(1000s))

NameBook‐ValueAssets(1000s)

∂ln(marketvalueassets)/∂(equitycapitalratio)

pvalue

1 CITIGROUP 2,187,631,104 ‐1.07774 0.0086

2 JPMORGANCHASE&CO 1,562,146,944 ‐1.01067 0.0091

3 BANKOFAMERCORP 1,720,688,384 ‐0.98173 0.0095

4 WELLSFARGO&CO 575,441,984 ‐0.75080 0.0135

5 USBC 237,615,008 ‐0.65042 0.0167

6 FIFTHTHIRDBC 110,961,512 ‐0.61655 0.0172

7 PNCFNCLSVCGROUP 138,976,256 ‐0.60743 0.0184

8 REGIONSFC 141,043,936 ‐0.58355 0.0203

9 HUNTINGTONBSHRS 54,629,164 ‐0.55056 0.0206

10 BB&TCORP 132,617,600 ‐0.57566 0.0208

11 SUNTRUSTBK 179,573,936 ‐0.58261 0.0210

12 KEYCORP 99,567,392 ‐0.55542 0.0219

13 COMERICA 62,756,752 ‐0.50095 0.0270

14 M&TBKCORP 64,875,640 ‐0.48587 0.0295

15 NORTHERNTRCORP 67,611,224 ‐0.45462 0.0358

16 FIRSTHORIZONNATCORP 37,017,240 ‐0.41211 0.0430

17 NEWYORKCMNTYBC 30,599,738 ‐0.38809 0.0496

18 BANKOFHICORP 10,472,942 ‐0.36231 0.0502

19 UNIONBANCALCORP 55,727,748 ‐0.36682 0.0643

20 ZIONSBC 52,947,444 ‐0.36397 0.0652

21 ASSOCIATEDBANCCORP 21,592,084 ‐0.33739 0.0698

22 FIRSTMERITCORP 10,407,565 ‐0.31606 0.0741

23 TCFFC 16,067,612 ‐0.31430 0.0810

24 COMMERCEBSHRS 16,212,371 ‐0.31314 0.0820

25 WEBSTERFNCLCORP 17,208,062 ‐0.30487 0.0891

26 WHITNEYHC 11,029,846 ‐0.29230 0.0928

27 CENTRALPACIFICFNCLCORP 5,680,386 ‐0.27814 0.0947

28 FULTONFNCLCORP 15,923,098 ‐0.29563 0.0956

29 FIRSTCITIZENSBSHRS 16,229,958 ‐0.29242 0.0987

35

Table10

ComparisonsofFinancialPerformancein2007forBankswithPositiveandSignificantlyNegativeDerivativesofFinancialPerformancewithRespecttoEquityCapitalRatio

Thedatasetincludes142publiclytradedtop‐tierbankholdingcompaniesattheendof2007.Thereare33bankswithapositivevaluedderivativeoftheln(marketvalueofassets),butnoneofthesevaluesarestatisticallysignificant.Hence,lackinganystatisticallysignificantpositivevalues,these33banksareusedinthecomparisonofmeanswiththe29bankswhosenegativederivativeissignificantlydifferentfrom0.Inthecaseofthederivativeofmarket‐valueinefficiencywithrespecttothecapitalratio,thereare61bankswithastatisticallysignificantnegativederivativeand13bankswithastatisticallysignificantpositivederivative.Thepvaluerepresentsthestatisticalsignificanceofthecomparisonofmeansinthepairing.Pairsofmeansinboldarestatisticallydifferentatstricterthanp=0.10. ∂ln(MarketValueofAssets)/∂Capital

Ratio∂Market‐ValueInefficiency/∂CapitalRatio

>0N=33

<0N=29

<0N=61

>0N=13

Mean Mean P Mean Mean P

∂Performance/∂CapitalRatio 0.0756 ‐0.5042 <0.0001 ‐0.3769 0.9637 <0.0001

BookValueAssets(1,000s)

1,815,671 263,905,273 0.0172 2,154,360 554,126,921 0.0207

InvestmentOpportunityRatio

1.1295 1.0852 <0.0001 1.1128 1.0813 0.0015

Tobin’sqRatio 1.0645 1.0749 0.3599 1.0626 1.0703 0.4943

Noise‐AdjustedTobin’sqRatio

1.0490 1.0779 0.0051 1.0530 1.0715 0.0592

Market‐ValueInefficiencyRatio

0.4968 0.1036 <0.0001 0.4577 0.0631 <0.0001

Book‐ValueEquity/TotalAssets

0.0915 0.0923 0.8665 0.0917 0.0909 0.8866

(Equity+SubDebt+LoanLossReserves)/

Assets0.1010 0.1204 0.0004 0.1008 0.1260 <0.0001

NonperformingLoans/Assets

0.0191 0.0173 0.6544 0.0176 0.0215 0.2162

36

Table11

ComparisonsofBalanceSheetsforBanksin2007withPositiveandSignificantlyNegativeDerivativesofFinancialPerformancewithRespecttoEquityCapitalRatio

Thedatasetincludes142publiclytradedtop‐tierbankholdingcompaniesattheendof2007.Thereare33bankswithapositivevaluedderivativeoftheln(marketvalueofassets),butnoneofthesevaluesarestatisticallysignificant.Hence,lackinganystatisticallysignificantpositivevalues,these33banksareusedinthecomparisonofmeanswiththe29bankswhosenegativederivativeissignificantlydifferentfrom0.Inthecaseofthederivativeofmarket‐valueinefficiencywithrespecttothecapitalratio,thereare61bankswithastatisticallysignificantnegativederivativeand13bankswithastatisticallysignificantpositivederivative.Thepvaluerepresentsthestatisticalsignificanceofthecomparisonofmeansinthepairing.Pairsofmeansinboldarestatisticallydifferentatstricterthanp=0.10. ∂ln(MarketValueofAssets)/∂Capital

Ratio∂Market‐ValueInefficiency/∂CapitalRatio

>0N=33

<0N=29

<0N=61

>0N=13

Mean Mean P Mean Mean P

BookValueAssets(1,000s)

1,815,671 263,905,273 0.0172 2,154,360 554,126,921 0.0207

Deposits/(Deposits+OtherBorrowedFunds)

0.8678 0.6833 <0.0001 0.8649 0.6341 0.0010

NoninterestIncome/TotalRevenue 0.1275 0.2496 <0.0001 0.1468 0.2776 <0.0001

LiquidAssets/Assets 0.2029 0.2065 0.8840 0.2128 0.1794 0.2132

TotalLoans/TotalAssets

0.7410 0.6670 0.0121 0.7244 0.6427 0.0741

ResidentialRealEstateLoans/TotalAssets 0.1951 0.2510 0.0465 0.2170 0.2180 0.9720

CommercialRealEstateLoans/Total

Assets0.3694 0.1617 <0.0001 0.3256 0.1243 <0.0001

ConsumerLoans/TotalAssets 0.0383 0.0618 0.0444 0.0419 0.0816 0.0022

BusinessLoans/TotalAssets

0.1226 0.1432 0.2703 0.1168 0.1531 0.0951