lighthouse macro report - 2013 - april

TRANSCRIPT

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 1/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 1

Macro Report Economic Indicators - USA - April 2013

Contents

Summary ....................................................................................................................................................... 2

Lighthouse Recession Probability Index........................................................................................................ 3

Introduction .................................................................................................................................................. 4

Fed Funds Rate .............................................................................................................................................. 8

Crude Oil ....................................................................................................................................................... 9

Construction: Building permits ................................................................................................................... 10

Employment: Non-Farm Payrolls ................................................................................................................ 11

Employment: Jobs Gained / Lost ................................................................................................................ 12

Employment: Jobs Gained/Lost (zoomed-in) .............................................................................................. 13

Employment: Hire and Fire ......................................................................................................................... 14Employment: Initial and Revised Non-Farm Payrolls .................................................................................. 15

Employment: Full Time ............................................................................................................................... 16

Employment: Part Time .............................................................................................................................. 17

Employment: Full-Time to Part-Time Ratio ................................................................................................ 18

Consumer Sentiment: University of Michigan Survey ................................................................................ 19

Consumer Confidence: Conference Board Survey ...................................................................................... 20

Total Credit Outstanding ............................................................................................................................. 21

Electricity Usage .......................................................................................................................................... 22

Retail Sales: Nominal .................................................................................................................................. 23

Retail Sales: Real ......................................................................................................................................... 24

Retail Sales: Real per-capita ........................................................................................................................ 25

Manufacturing: Hours Worked ................................................................................................................... 26

Manufacturing: Orders ............................................................................................................................... 27

Transportation: Miles Traveled ................................................................................................................... 28

Orders: Capital Goods ................................................................................................................................. 29

Output: Electricity and Gas ......................................................................................................................... 30

Manufacturing: Supplier Deliveries ............................................................................................................ 31

Transportation: Gasoline Consumption ...................................................................................................... 32

Inflation: Implicit Price Deflator .................................................................................................................. 33

Inflation: Consumer Price Index .................................................................................................................. 34

Inflation Expectations ................................................................................................................................. 35

Inflation Expectations and Stock Market .................................................................................................... 36

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 2/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 2

Summary

Improvements in this report:

• More granularity on employment trends (hiring and separations, full-time and part-time)

• Retail sales (now including real and real per-capita sales)

• Inflation (PCE-derived inflation, inflation and stock market correlation)

March 2013 highlights:

• The likelihood of recession declined slightly to 5% from remained a revised 10% in the previous

month

• Output by electric and gas utilities, industrial electricity consumption and miles traveled are the

only variables showing recessionary tendencies

• Retail sales growth continues to slow

• Average monthly employment increased slightly from 169k to 173k per month.

April 2013 trends:

• Slightly lower UoM Consumer Sentiment contrasted higher CB Consumer Confidence

• Slight decrease in average weekly hours

• ISM manufacturing new orders and deliveries hover slightly above 50

• PCE-derived inflation fell to 1.2% in Q1 2013, the lowest since Q3 2009, and below the Fed's

target range of 2% +/- 0.5%

CONCLUSION:

• Based on our set of 13 weighted indicators the probability for US recession remains low.

• However, economic growth remains very weak

• The Federal Reserve will not be able to reduce 'quantitative easing' under these circumstances

• Should disinflationary trends continue, the Fed will have no other choice than to increase the

pace of printing money

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 3/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 3

Lighthouse Recession Probability Index

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 4/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 4

Introduction

Recessions are bad for company profits and hence stock prices. Knowing when an economic slow-down

looms can give important clues about asset class selection.

In the US, the beginning and the end points of recessions are declared by the NBER (National Bureau of

Economic Research). The NBER defines recessions as a "significant decline in economic activity spread

across the economy" (not, as often believed, as two consecutive quarters of negative GDP growth).

The NBER takes it's time to date the beginning and the end of a down-turn; it announced the beginning

of the last recession (December 2007) only on December 1, 2008 - one year later. By that time, the S&P

500 Index had fallen from 1,575 points to 741. Similarly, the end of the recession in June 2009 was

announced on September 20, 2010 - more than one year later. By that time, the S&P 500 had already

soared from 940 points to 1,142.

Waiting for the NBER to declare beginning and end of recessions would have led to inferior investment

results (the NBER is correct in taking it's time, since many economic indicators are being revised multiple

times as preliminary data gets updated).

Traditional leading indicators include values such as the stock market and the slope of the yield curve.

However, the stock market does not seem very good at anticipating recessions, as the S&P 500 index

marked an all-time high in mid-October 2007, a mere six weeks before the most severe recession of the

last 8 decades began.

The yield curve has historically been a very good warning sign of recessions, as the Federal Reserve Bankwas forced to increase short-term rates in order to cool an overheating economy (thereby triggering a

recession). However, with short-term interest rates near zero for the foreseeable future, the yield curve

could only invert if long-term yields dipped into negative territory. While not entirely impossible

(negative yields for up to 2 year maturities have been observed in German, Swiss, Danish and other

government bond markets) it is very unlikely to happen in US Treasuries. Therefore, the slope of the US

yield curve is unlikely to give any hints about a recession occurring under ZIRP (zero-interest-rate-

policy).

Indicators published by other institutions, such as ECRI (Economic Cycle Research Institute), are

proprietary and not transparent, giving investors only the choice to "believe-it-or-leave-it".

The Conference Board Leading Indicator includes questionable values such as the S&P 500 Index, the

slope of the US yield curve and M2 money supply (which we have found to have little correlation with

economic cycles).

As most recessions last rarely longer than a year, the economy usually had already exited a recession by

the time the NBER declared it to be in one.

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 5/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 5

Revisions to GDP growth render it useless for investment purposes; On August 28, 2008 (already 8

months into the "great recession"), Q2 2008 GDP growth was revised upwards from an initial +1.9% to

+3.3%, triggering a 2% stock market rally. Later, growth was revised down to 1.3%, with the following

quarters delivering -3.7%, -9.2% and -5.4% (quarter-on-quarter, annualized). The S&P 500 Index didn't

regain the level attained that day for another 2 1/2 years.

Finding a reliable indicator for identifying recessions "real-time" would already be a great improvement

over waiting for the NBER.

Over the past 50 years, every recession was easily explained by two factors: oil and the Fed.

Unfortunately, this does not have to be the case going forward. Due to impotence of monetary policy at

the lower zero bound and rapidly increasing government debt the Fed might not be able to raise rates in

the foreseeable future. A recession might hence happen without prior tightening by the Fed.

We looked at many indicators from every angle; most had to be smoothed to cancel out short-term

"noise" in order to prevent false signals (we use 3-months moving averages).

Some indicators do not reveal useful signals unless you look at decline from recent peaks. Other data

needs to be trend adjusted (number of miles driven, for example, benefits from rising number of cars

and population).

The table on the following page shows indicators we have tested. Our criteria:

• false positives (calling for a recession when there was none)• false negatives (missed a recession)

• confidence it will work in the future and

• lead / lag time

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 6/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 6

No two recessions are the same. Trigger levels can be too strict (missing some recessions) or too lose

(giving too many false positives). We therefore created a range. The lower ("strict") boundary is the level

necessary to avoid false positives; the upper ("lenient") boundary is the level necessary to catch all

recessions. A high-quality indicator will have a narrow range, and recessions will be called with high

confidence. An indicator at the upper boundary will be awarded a 50% probability, increasing towards

100% at the lower boundary.

The overall "LighthouseRecession Probability

Indicator" (LRPI) is a

weighted mean of individual

indicators. High confidence

and timeliness of signal

have been awarded higher

weights (maximum: 3) then

those with low confidence

or tardiness (minimum: 1).

On the following page yousee the LRPI since 1971,

predicting every recession

(assumed once 40%-50%

probability is exceeded).

The Federal Reserve Bank of

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 7/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 7

St. Louis publishes a recession probability indicator by Chauvet / Piger (black line). It is based on four

inputs (non-farm payrolls, industrial production, real personal income and real manufacturing and trade

sales). However, the most recent data point for Chauvet/Piger is usually three months old, while LRPI is

constantly updated (1 months old data).

You can see that LRPI shows first warnings signs much earlier than Chauvet/Piger.

In a recent response to a blog post, Chauvet clarified their indicator calls for a recession only "after

exceeding 80% for a couple of months". Additionally, their indicator is "smoothed" as the raw data can

reach 70% (2003/4) without being followed by a recession. Their indicator initially showed a recession

probability of 20% for August 2012, only to be revised down to 1.7% six months later.

Verification of LRPI:

We set 40% as threshold for the LRPI to indicate a buy (recession probability <40%) or sell (>40%) signal.

Transactions have been done at the monthly closing price of the S&P 500 following the month for which

the signal occurred (in order to accommodate time lag):

An investor using the LRPI as a trading tool would have suffered only one loss of 7% (August 1980) while

avoiding the dot-com crash (2001) and the 'great recession' (2008-2009). The system creates no

unnecessary churn. While the control group ('buy-and-hold') would have created a higher return (with

higher volatility) this might be due to the test period coinciding with one of the longest bull markets inhistory (1982-2000).

Annex: LRPI Components

Please find charts for all contributors to the LRPI on the following pages.

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 8/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 8

Fed Funds Rate

The US central bank ("Fed") increased interest rates ahead of each of the last 9 recessions. The black line

shows the absolute level of the Fed Funds rate; the blue line the increase from the prior post-recession

low. An increase between 2 and 4.5 percentage points from the previous low preceded every recession

since 1954.

Recessions are shaded in gray. Yellow dots indicate the beginning of a recession; green dots the end.

The absolute level (black line) is usually on the right-hand scale, while percentage changes (blue line) are

on the left-hand scale. Negative absolute numbers should be ignored as they are merely needed for

better formatting.

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 9/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 9

Crude Oil

• An increase in the price of crude oil of 75% to 100% preceded five out of the last six recessions.

• Close call in March 2011 and February 2012.

• Currently not a red flag.

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 10/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 10

Construction: Building permits

Want to build a house? Need a permit! Any decline in permits of 25%+ from prior peak and you can bet

on a recession. Missed the one in 2001 though. 2011 was a close call. Absolute level still below 1990/91

recession lows (despite US population growth from 250m then to 315m in 2012).

Due to housing overhang unlikely to give a boost to the economy. Due to low level unlikely to do much

damage to GDP either (should permits decline again).

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 11/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 11

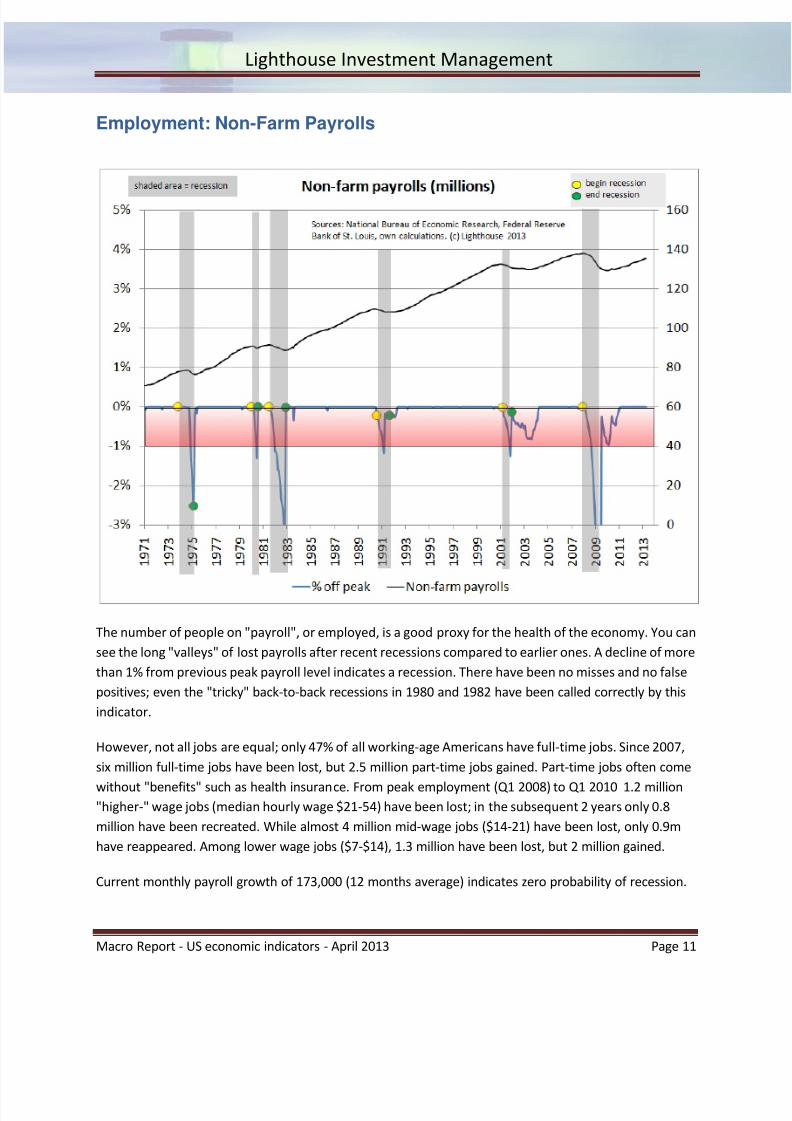

Employment: Non-Farm Payrolls

The number of people on "payroll", or employed, is a good proxy for the health of the economy. You can

see the long "valleys" of lost payrolls after recent recessions compared to earlier ones. A decline of more

than 1% from previous peak payroll level indicates a recession. There have been no misses and no false

positives; even the "tricky" back-to-back recessions in 1980 and 1982 have been called correctly by this

indicator.

However, not all jobs are equal; only 47% of all working-age Americans have full-time jobs. Since 2007,

six million full-time jobs have been lost, but 2.5 million part-time jobs gained. Part-time jobs often come

without "benefits" such as health insurance. From peak employment (Q1 2008) to Q1 2010 1.2 million"higher-" wage jobs (median hourly wage $21-54) have been lost; in the subsequent 2 years only 0.8

million have been recreated. While almost 4 million mid-wage jobs ($14-21) have been lost, only 0.9m

have reappeared. Among lower wage jobs ($7-$14), 1.3 million have been lost, but 2 million gained.

Current monthly payroll growth of 173,000 (12 months average) indicates zero probability of recession.

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 12/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 12

Employment: Jobs Gained / Lost

Current monthly payroll growth of 173,000 (12 months average) indicates zero probability of recession.

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 13/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 13

Employment: Jobs Gained/Lost (zoomed-in)

• April payroll data was better (+165,000) than expected (+153,000)

• However, it should be noted that the margin of error is around 100,000, and revisions can be up

to 300,000

• More important than the April number were revisions for earlier months; February from an

initial 236,000 to 332,000, and March from 88,000 to 138,000.

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 14/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 14

Employment: Hire and Fire

• Each month, more than 4 million people are newly employed and more than 4 million people

quit their job or are fired.

• These are big numbers compared to the balance between those two (the monthly change in

non-farm payrolls).

• The difference between those two lines are the net changes in employment (lower chart).

• You will notice less separations (fewer employees resign) during the 'great recession';

unemployment rose simply because new hires fell even faster.

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 15/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 15

Employment: Initial and Revised Non-Farm Payrolls

• This chart shows monthly changes in employment as initially reported (black dotted line), the

revised number (thick black line) and the difference between the two (green/red chart, right hand

scale).

• During the last recession (we didn’t know we were in one yet), monthly employment numbers were

revised downwards by up to 273,000.

• In Q3 2008, revisions were -159k, -190k and -273k (that’s before Lehman happened).

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 16/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 16

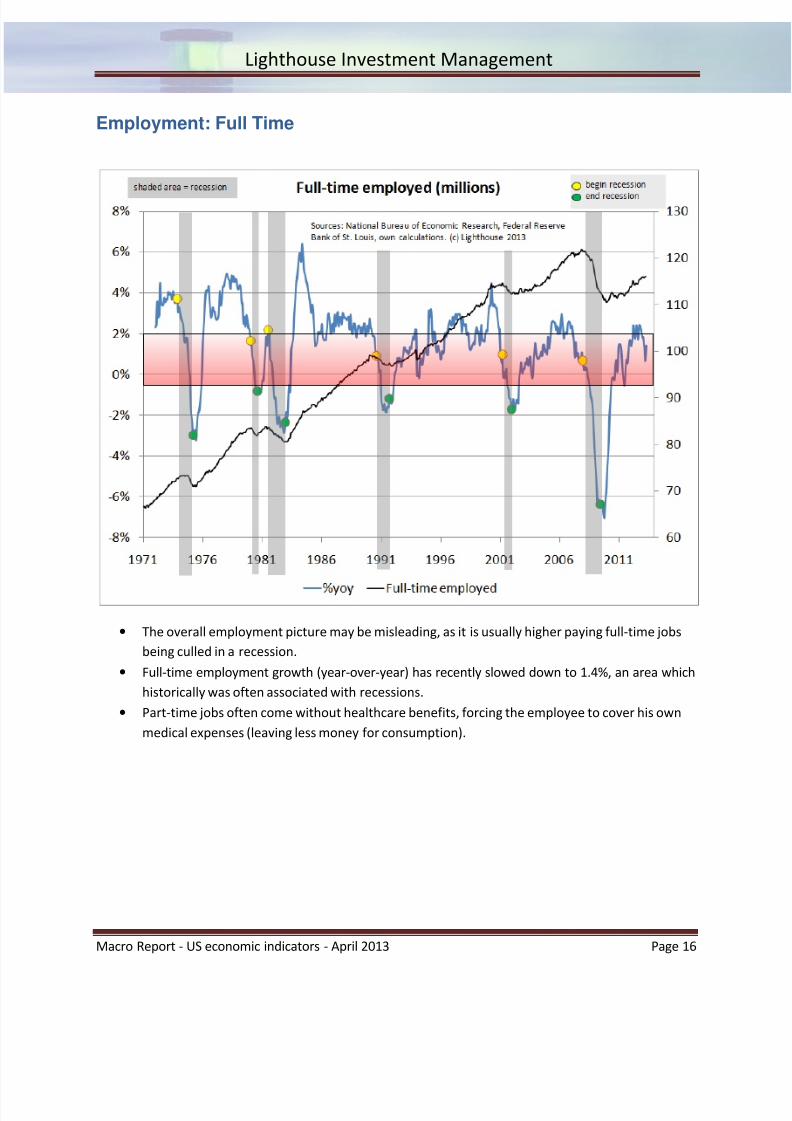

Employment: Full Time

• The overall employment picture may be misleading, as it is usually higher paying full-time jobs

being culled in a recession.

• Full-time employment growth (year-over-year) has recently slowed down to 1.4%, an area which

historically was often associated with recessions.

• Part-time jobs often come without healthcare benefits, forcing the employee to cover his own

medical expenses (leaving less money for consumption).

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 17/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 17

Employment: Part Time

• During each recession, the number of part-time employees spikes up

• Companies, uncertain regarding the economic outlook, prefer not to enter longer-term

commitments

• A part-time job may be better than no job, but usually does not sustain the costs of living of a

family.

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 18/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 18

Employment: Full-Time to Part-Time Ratio

• The number of full-time employees used to be more than five times the number of part-time

employees

• In each recession, full-time employees are replaced by part-timers

• The ratio has not recovered in a meaningful way since the 'great recession'

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 19/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 19

Consumer Sentiment: University of Michigan Survey

• The University of Michigan, together with Thompson-Reuters, conducts more than 500

telephone interviews twice a month to gauge consumer sentiment, with a reference point from

1964 set to 100. A preliminary mid-month survey is followed up by a final one towards the end

of the month.

• The indicator had one false positive (2005) and one miss (1981; the 1980-1981 recessions were

back-to-back, so let's not be too harsh about that).

• A decline of 25%+ from previous peak indicates a recession.

• 2011 was a close call.

• The final reading for the month (76.4) came in higher than the preliminary number (72.3).

• This indicator currently does not deliver a warning sign.

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 20/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 20

Consumer Confidence: Conference Board Survey

• The Conference Board, an independent business membership and research association,

conducts a survey of consumer confidence by mailing out surveys to more than 3,000 randomly

selected households. The cut-off date for a preliminary number is the 18th of the months. The

final number includes all surveys returned after that date.

• The indicator had two false positives (1992, 2003), but it did catch all recessions including the

ones in 1981/2 and 2001 (difficult for a lot of other indicators).

• 2011 was a "close call".

• This indicator's initial reading for the month (68.1) showed an improvement from the prior

month (61.9).

• No red flag currently.

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 21/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 21

Total Credit Outstanding

Most recessions have been accompanied by a reduction in the growth of debt. But, for the first time in

60 years, debt has actually shrunk in 2009. A meager 2% reduction caused a massive recession. The

classic question of chicken and egg comes to mind: did the recession cause debt to shrink or did

shrinking debt induce a recession?

I have included the 1987 stock market crash (red triangle). A dramatic revelation dawns: economic

growth is dependent on credit (debt) growth; without additional debt, growth is impossible.

Unfortunately, data becomes available only once every quarter, with the latest data often many monthsold. To ensure timeliness for our LRPI we had to exclude this measure, however present it here for

informational purposes.

In Q4 2012, TCMDO was growing at a $2.9 trillion rate over the last 8 quarters (versus revised 2.7 trillion

in Q3)). TCMDO-to-GDP has increased to 355% (Q3: 352%, Q2: 354%, previous peak was 385% in Q1'09).

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 22/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 22

Electricity Usage

• If you run a business you need electricity

• Weather can have an impact as electricity use in the US peaks in summer due to air conditioning

• If electricity usage drops by 1% or more, it's a recession

• Limited historic data, but no misses and no false positives.

• Currently indicating a 50% likelihood of recession.

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 23/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 23

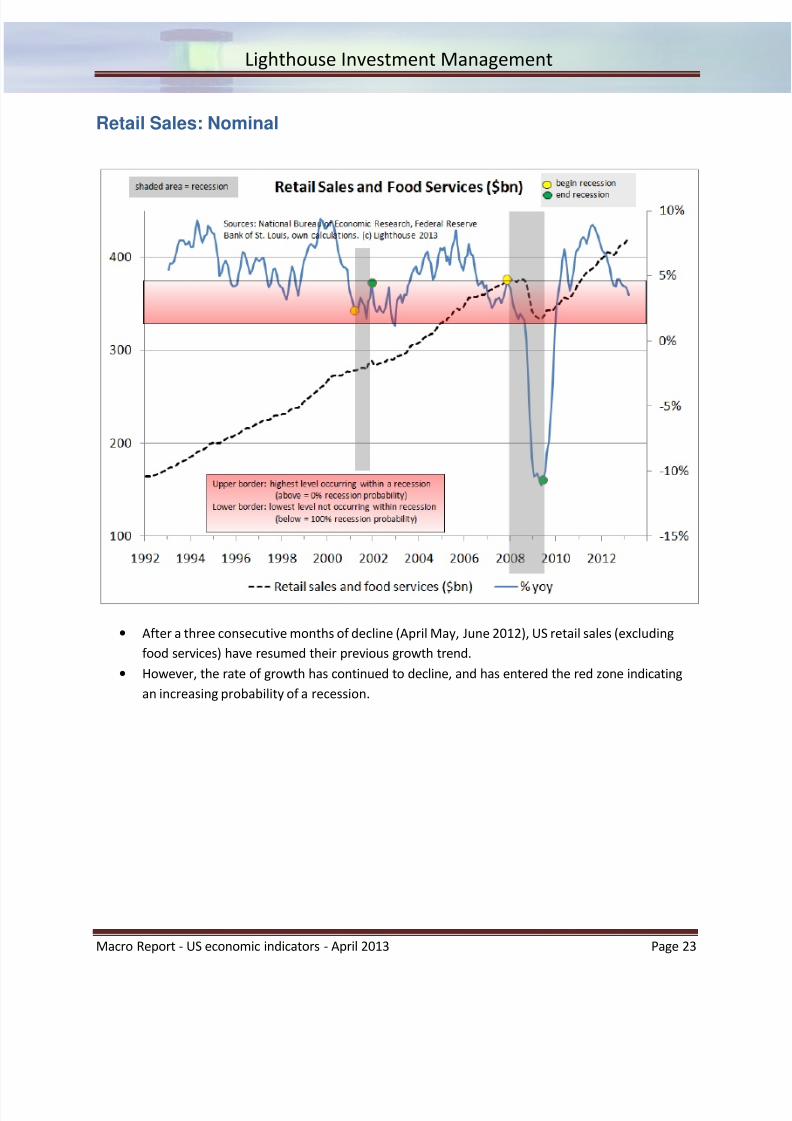

Retail Sales: Nominal

• After a three consecutive months of decline (April May, June 2012), US retail sales (excluding

food services) have resumed their previous growth trend.

• However, the rate of growth has continued to decline, and has entered the red zone indicating

an increasing probability of a recession.

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 24/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 24

Retail Sales: Real

• Real retail sales (volumes) have only recently reached their pre-recession level

• The rate of growth continues to slow down

• No recession signal currently

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 25/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 25

Retail Sales: Real per-capita

• Real per-capita retails sales are still 5% below their pre-recession peak

• The rate of growth continues to slow down (1.3%)

• No recession signal (yet)

• The rate of change in nominal retail sales excluding autos has reached 100% recession

probability. Auto sales continue to benefit from very low interest rates, abundant credit and

deep-subprime used-car loans.

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 26/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 26

Manufacturing: Hours Worked

• Companies prefer to reduce employee's working hours rather than firing them straight away

• A drop in average weekly working hours in the manufacturing sector of 2% or more indicates a

recession (except for 1996)

• According to this indicator, the US economy is still sailing smoothly

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 27/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 27

Manufacturing: Orders

• The Institute for Supply Management (ISM) regularly asks company executives about orders,

sales, inventories etc.

• A level of 50 indicates "unchanged" (economy stagnates).

• This indicator delivered one false positive (1989).

• The ISM new orders index improved slightly in March (52.3 versus 51.4) after briefly dipping into

dangerous territory (December 2012).

• Currently no warning sign.

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 28/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 28

Transportation: Miles Traveled

The US population increases approximately 1% per annum, so traffic increases constantly. If total miles

driven grow less than 0.1% versus its own trend, you are likely to be in a recession (the unemployed

drive less).

The 2001 recession was missed. This indicator says we had a recession in 2011 (which is theoretically

possible - we might not know it yet). The prolonged decline in miles traveled since 2007 is puzzling; the

decline being deeper than the back-to-back recession 1980/81. Online shopping, car pooling and work-

from-home jobs might have contributed to this trend.

Unfortunately, the data is made available only with a time lag of three months. This, combined with

lower confidence, made us exclude this indicator from the LRPI. In March, historic data has been revised

going back for years, denting confidence in this indicator further.

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 29/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 29

Orders: Capital Goods

Defense and aircraft orders are lumpy and distort trends, so we exclude them here. We have "medium"

confidence in this indicator due to limited historic data. The "red zone" has been set at -8% to 0%.

February non-defense durable goods ex-aircraft orders were revised downwards by $1.4bn. March came

in at $64.5bn, up slightly from a revised $64.3bn in February - the highest since 53 months (for which I

have no good explanation).

However, defense and aircraft orders are more than twice as much as the rest. Any cuts in defense

spending and problems with Boeing's 787 model affect total orders, with repercussions for manysuppliers. So I wouldn't get too excited about the non-defense ex-aircraft data.

• This indicator currently gives a 50% probability of recession

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 30/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 30

Output: Electricity and Gas

• Electricity production should be linked to economic growth.

• This indicator, unfortunately, had many false positives (1983, 1992, 1997, 2006), so confidence

is "medium".

• Setting the trigger lower than -0.5% would eliminate false positives, but make you also miss

some recessions.

• Recent data has seen quite some revisions of up to 2.5% magnitude.

• Electricity production suggests we are in a recession with around 70% likelihood.

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 31/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 31

Manufacturing: Supplier Deliveries

• Multiple false positives (1985, 1989, 1995, 1998, 2005) muddy the water.

• Therefore, this indicator has been slapped with "low" confidence and a corresponding

weighting.

• Recent surveys hovered around the 50-point mark.

• The current reading suggests a slight growth in manufacturing supplier deliveries.

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 32/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 32

Transportation: Gasoline Consumption

• Cars need gas, and gas needs to be delivered to gas stations.

• Inventory effects are unlikely because of high turnover.

• "Low" confidence because of false positive (1996) and limited historic data.

• The harsh decline in 2012 is puzzling, but recovered since March 2012.

• This indicator is currently giving a 55% likelihood of recession.

This indicator is related to "miles driven", confirming trends on one hand, but being redundant on the

other. It has therefore been excluded from LRPI.

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 33/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 33

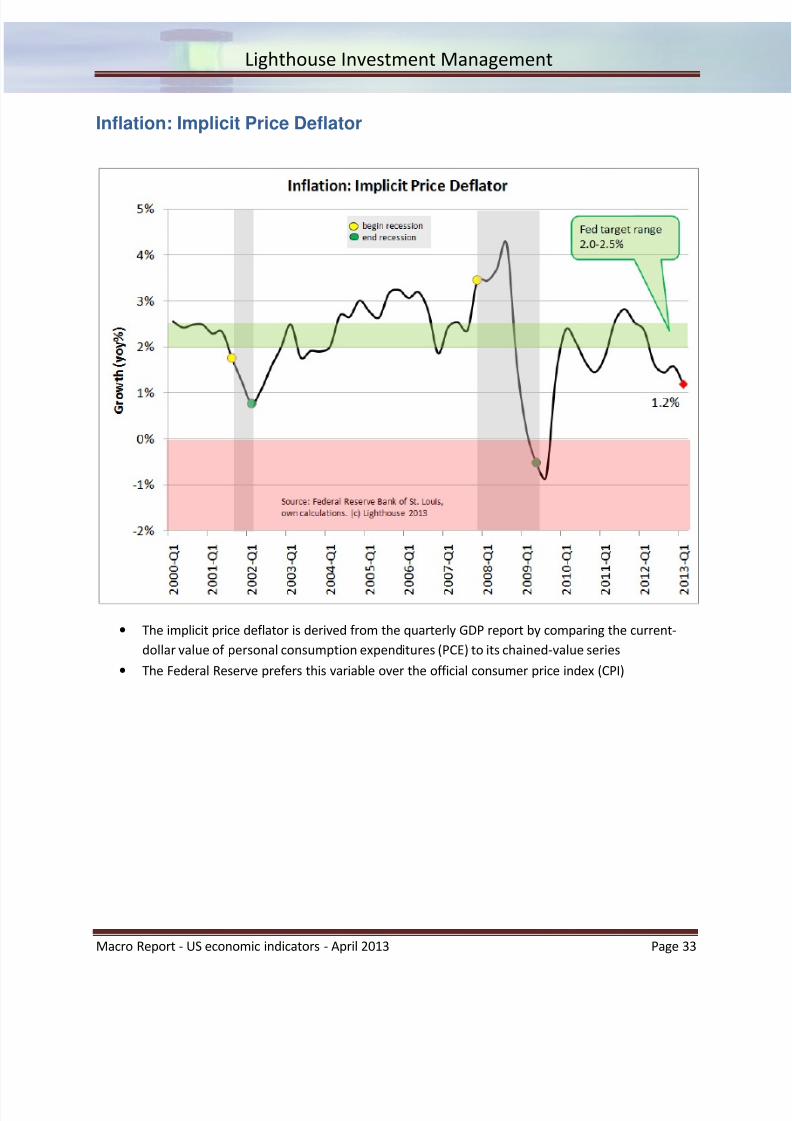

Inflation: Implicit Price Deflator

• The implicit price deflator is derived from the quarterly GDP report by comparing the current-

dollar value of personal consumption expenditures (PCE) to its chained-value series

• The Federal Reserve prefers this variable over the official consumer price index (CPI)

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 34/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 34

Inflation: Consumer Price Index

• Headline CPI-U ("consumer price index for urban consumers") is currently rising at a seasonally

adjusted rate of 1.5% (previously: 2.0%).

• Core CPI-U (excluding effects from food and energy prices) is currently rising at a seasonally

adjusted rate of 1.9% (previously 2.0%) .

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 35/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 35

Inflation Expectations

• Real yield = nominal yield minus inflation

• You can resolve the formula for [inflation = nominal yield minus real yield]

• We use Treasury bonds for nominal yields, and TIPS (Treasury Inflation Protected Securities) for

real yield.

• The break-even rate of inflation is the rate at which it does not matter if you bought Treasury

bonds or TIPS (return would be the same).

• The resulting implied inflation rates for over the next 5 (red), 10 (blue) and 30 (black) years are

printed in above chart.

• If you know the average rate over 10 years, and for the first 5 years of those 10 years, you can

derive the expected rate of inflation for years 6 to 10 (green).• The "expected" rate of inflation is not a forecast; it may or may not come true. Market

expectations change.

• Changes in the expected rate of inflation are of interest due to a high correlation (over 75% until

mid-February 2012) to changes in the S&P 500 Index (see next page).

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 36/37

Lighthouse Investment Management

Macro Report - US economic indicators - April 2013 Page 36

Inflation Expectations and Stock Market

• The current data point (red) is the farthest away from the regression line since the beginning of

2012

• Assuming historic correlations remain valid, either the stock market is over-extended or inflation

expectations would have to catch up substantially.

• The expected value for the S&P 500 given current inflation expectations is around 1,400

(currently 1633).

Any questions or feedback highly welcome.

7/30/2019 Lighthouse Macro Report - 2013 - April

http://slidepdf.com/reader/full/lighthouse-macro-report-2013-april 37/37

Lighthouse Investment Management

Disclaimer: It should be self-evident this is for informational and educational purposes only and shall not be

taken as investment advice. Nothing posted here shall constitute a solicitation, recommendation or

endorsement to buy or sell any security or other financial instrument. You shouldn't be surprised that

accounts managed by Lighthouse Investment Management or the author may have financial interests in any

instruments mentioned in these posts. We may buy or sell at any time, might not disclose those actions andwe might not necessarily disclose updated information should we discover a fault with our analysis. The

author has no obligation to update any information posted here. We reserve the right to make investment

decisions inconsistent with the views expressed here. We can't make any representations or warranties as to

the accuracy, completeness or timeliness of the information posted. All liability for errors, omissions,

misinterpretation or misuse of any information posted is excluded.

+ + + + + + + + + + + + + + + + + + + + + + + + + + + + + + + + + + + + + + +

All clients have their own individual accounts held at an independent, well-known brokerage company (US)

or bank (Europe). This institution executes trades, sends confirms and statements. Lighthouse Investment

Management does not take custody of any client assets.