leading the way in asia, africa and the middle east here

TRANSCRIPT

Standard Chartered Bank Zambia Plc Annual Report 2012

Leading the way in Asia, Africa and the Middle East Here for good

2 Standard Chartered Bank Zambia Plc Annual Report 2012

Standard Chartered Bank Zambia Plc has again delivered a strong performance.

The Bank is integral to the development of the country and our performance clearly demontrates our powerful brand promise, Here for good.

Financial highlights

Revenue

ZMK620,417m2011: ZMK479,317m / 2010: ZMK451,138m

Total assets

ZMK5,163,618m2011: ZMK4,585,674m / 2010: ZMK4,572,218m

Normalised return on equity

37%2011: 41% / 2009: 30%

Non-financial highlights

Profit before taxation

ZMK339,618m2011: ZMK226,087 / 2010: ZMK229,744m

Normalised earnings per share

ZMK132.572011: ZMK79.46 / 2010: ZMK5.42

Dividend per share

ZMK0.002011: ZMK0.00 / 2010: ZMK20.00

Employees

696 2011: 650

Outlets

24 2011: 20

Standard Chartered Bank Zambia Plc Annual Report 2012

1

What’s inside this report

Supplementary information79- 86Additional information for shareholders

Financial statements and notes19 - 78Detailed financial information forthe year ended 31 December 2012

Corporate governance10 - 18An explanation of our approachto corporate governance with keydevelopments during the year, togetherwith profiles of our Board Directors

Operating and financial review7 - 9A review of our businesses, theirfinancial performance and outlookfor 2013

Overview2 - 6Performance highlights andan introduction to our business structures and strategy

Financial highlights2 Chairman’s statement4 Chief Executive Officer’s statement

7 Consumer banking8 Wholesale banking

10 Board of directors13 Directors’ report14 Statement on corporate governance17 Senior Management Committee18 Making a difference in our community

79 Five year summary 80 Principal addresses and senior management81 Branch management83 Dividend84 Notice of annual general meeting and agenda85 Form of proxy

20 Directors’ responsibilities in respect of the preparations of financial statements

21 Independent auditor’s report23 Statement of comprehensive income25 Statement of financial position 26 Statement of changes in equity28 Statement of cash flows29 Notes to the financial statements

Su

pp

lem

en

tary in

form

atio

nO

verview

Op

era

ting

an

d fi

na

nc

ial review

Co

rpo

rate g

ove

rna

nc

eF

ina

nc

ial sta

tem

en

ts an

d n

ote

s

2 Standard Chartered Bank Zambia Plc Annual Report 2012

Chairman’s statement

It gives me great pleasure to present Standard Chartered Bank Zambia Plc’s annual report and financial statements for the year ended 31st December 2012. The Bank continued its custom of achieving a good performance and putting in place strategies focusing on its client service delivery objectives. Our performance in 2012 once again demonstrates our ability to deliver substantial, sustained value for our shareholders. Despite our sterling performance, the 2012 financial year has been another challenging one for financial institutions in general, and for the Group in particular. The macroeconomic environment has again been dominated by uncertainty and volatility in global financial markets. The economic and regulatory pressures were unrelenting. Competition was intense. The New York State Department of Financial Services ‘event’ was particularly challenging to the Group. But we have proved our resilience. Once again we have outperformed our competitors on so many levels, notwithstanding the challenges and difficulties we encountered.

Locally in Zambia, the Government in 2012 introduced a number of new regulations that affected the Bank directly. Being the right partner to the Central Bank, the Bank ensured 100 per cent compliance to all new regulations and through them all still achieved a superb financial performance.

Financial HighlightsRevenue increased by 29 per cent to ZMK620bn and Profit before taxation increased by 50 per cent to ZMK340bn. Basic and diluted earnings per share were 67 per cent higher at ZMK132.57 per share.

The Board is recommending that all profits after tax be retained. Bank of Zambia had in early 2012 revised the minimum primary capital requirement for Banks in Zambia, with a requirement to maintain a minimum Tier 1 capital of ZMK520bn for international banks and ZMK104bn for local banks. A further stipulation was that of the Tier 1 capital, at least 80% should be kept in nominal paid-up common shares and the balance may be held only in any one or more categories including share premium, revenue reserves, general reserves and other statutory reserves. All Banks were required to comply with this new directive by 31 December 2012.

The board is pleased to announce that the retention of profits for the year 2012 and the resultant capitalization of the Bank meant that the Bank was able to meet the Bank of Zambia requirements as at 31st December 2012. Standard Chartered Bank Zambia Plc is therefore fully compliant with the recapitalization requirements.

The Domestic EconomyFollowing the achievement of its maiden USD 750mn Eurobond issuance (the USD 11.9bn order book reflected strong appetite) in 2012, Zambia has entered a new chapter. We saw rising copper output, agriculture gains, government

3O

verview

spending (especially on transport infrastructure), and power generation capacity all contributing to the growth of GDP.

Despite concerns about capacity for higher spending, infrastructure shortcomings was less of a constraint on economic activity. Zambia’s ability to keep inflation at 6-7% will be closely watched as the Zambian Kwacha (ZMK) was rebased to remove three zeros on 1 January 2013.

The rebasing aims to cement macroeconomic stability by committing to low and stable inflation in the future, and to boost economic activity by aiding pricing transparency. This follows earlier measures to reverse dollarisation in the economy. However, with the old and new kwacha notes existing side-by-side for six months, higher money supply to facilitate the rebasing, potential pressure on the FX rate, and sequencing with other reforms (including bank capitalization), inflation will need to be carefully monitored.

Following a doubling of mining-sector royalties in 2012, efforts to boost mining revenue will continue, with the 2013 budget streamlining the sector’s tax concessions. Zambia has been criticized for its generous fiscal legislation, that allows mining companies to carry forward losses for 10 years. However, under new legislation, capex deductions can be made only when equipment is put to use, and capital allowances are reduced to 25% from 100%. Furthermore, new mine operators may have to start paying taxes before recovering all their investment. However the new fiscal regime is unlikely to discourage existing operators.

Outlook Standard Chartered Bank Zambia Plc remains a core part of the Bank’s Africa strategic footprint and has consistently been among the top five revenue contributors for the Africa region. With 24 outlets,45 ATMs and close to 700 staff,

the Bank’s economic contribution to Zambia has been the culmination of 107 years of sustained and increased investment in the country.

Ten years ago we launched our strategic intent: to be the world’s best international bank, leading the way in Asia, Africa and the Middle East. The time is right for us to re-engage and recommit to our strategic intent. We have re-examined the strategy and resolved to remain strong and committed to continuity and commitment.

Our business and strategy is long term and enduring. We want to be the best. We will remain focused and continue to be the quintessential ‘international’ bank. ‘Leading the way in Asia, Africa and the Middle East’ captures what we want to achieve: Leadership across multiple dimensions in the markets we know best.

Summary I am proud of what we achieved in the year 2012. I am particularly proud of how we have turned our thinking and ambition to be a force for good into tangible business opportunities. I would like to thank the Board, the management team and the Banks’ employees for their dedication and hard work. The Bank has had an extremely strong 2012, and I believe the positive momentum will continue in 2013.

Michael M. Mundashi, SCChairman 21 February 2013

4 Standard Chartered Bank Zambia Plc Annual Report 2012

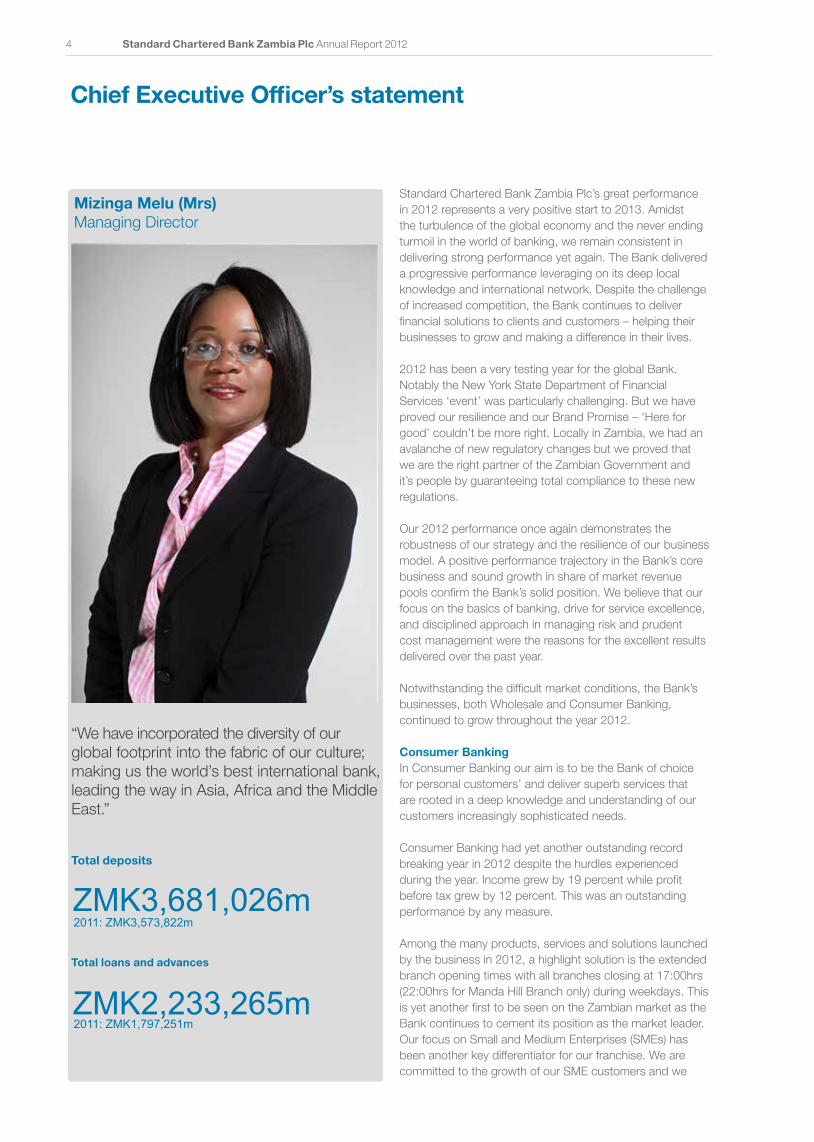

Chief Executive Officer’s statement

Standard Chartered Bank Zambia Plc’s great performance in 2012 represents a very positive start to 2013. Amidst the turbulence of the global economy and the never ending turmoil in the world of banking, we remain consistent in delivering strong performance yet again. The Bank delivered a progressive performance leveraging on its deep local knowledge and international network. Despite the challenge of increased competition, the Bank continues to deliver financial solutions to clients and customers – helping their businesses to grow and making a difference in their lives.

2012 has been a very testing year for the global Bank. Notably the New York State Department of Financial Services ‘event’ was particularly challenging. But we have proved our resilience and our Brand Promise – ‘Here for good’ couldn’t be more right. Locally in Zambia, we had an avalanche of new regulatory changes but we proved that we are the right partner of the Zambian Government and it’s people by guaranteeing total compliance to these new regulations.

Our 2012 performance once again demonstrates the robustness of our strategy and the resilience of our business model. A positive performance trajectory in the Bank’s core business and sound growth in share of market revenue pools confirm the Bank’s solid position. We believe that our focus on the basics of banking, drive for service excellence, and disciplined approach in managing risk and prudent cost management were the reasons for the excellent results delivered over the past year.

Notwithstanding the difficult market conditions, the Bank’s businesses, both Wholesale and Consumer Banking, continued to grow throughout the year 2012.

Consumer Banking In Consumer Banking our aim is to be the Bank of choice for personal customers’ and deliver superb services that are rooted in a deep knowledge and understanding of our customers increasingly sophisticated needs.

Consumer Banking had yet another outstanding record breaking year in 2012 despite the hurdles experienced during the year. Income grew by 19 percent while profit before tax grew by 12 percent. This was an outstanding performance by any measure.

Among the many products, services and solutions launched by the business in 2012, a highlight solution is the extended branch opening times with all branches closing at 17:00hrs (22:00hrs for Manda Hill Branch only) during weekdays. This is yet another first to be seen on the Zambian market as the Bank continues to cement its position as the market leader. Our focus on Small and Medium Enterprises (SMEs) has been another key differentiator for our franchise. We are committed to the growth of our SME customers and we

5O

verview

have remained the market leader in promoting business and trade between Africa and Asia in general, and China and Zambia in particular. These are markets in which we have operated for over 150 years. In 2013, we will continue to focus on providing our customers with ground-breaking solutions for their businesses.

We will continue to strengthen our ability to compete effectively in the retail market by expanding our alternate distribution channels to drive deposit growth.

Wholesale Banking Our WB business is made up of two units namely Origination and Client Coverage (OCC) and Global Markets (GM), which focus on delivering a broad range of solutions to our corporate and institutional clients in support of their operating activities.

In our Wholesale Banking business, we aim to be the leader in corporate banking through our world class solutions in treasury products, cash management and trade finance. We will deepen our client relationships by adding value to their businesses.

Wholesale Banking year on year revenue grew by 29% to ZMK322 billion, largely due to good performance on trade products in the Global Corporates and Agriculture & Commodity traders customer segments. Rates trading also contributed positively.

Wholesale Banking continues to focus on mainstay products of cash, trade, lending, terms loans, structured arrangements and foreign exchange, where our historical know-how enables us to compete and have unique capabilities around customers, products and delivery. We will continue to bring to our local market the dimension of “international” which means for us, the highest global standards of customer segmentation, marketing, staff quality, risk management and, mordern and innovative products.

Risk Management The management of risk lies at the heart of Standard Chartered Bank’s business model. We are aware that successful risk management is essential to being able to produce profits consistently and sustainably and is, as a result, vital to the financial and operational management of the Bank.

Although we are continually investing to enhance our risk management infrastructure and capabilities, our fundamental approach to risk has stayed consistent over many years. Through our risk management framework we manage business wide risk with the objective of maximizing risk adjusted returns while remaining within our risk appetite.

It is with great pleasure that we announce that we had no failed audits in the year 2012. As part of our continuous improvement strategy, we will continue to manage our risks to build a sustainable franchise in the interests of all stakeholders.

Our People We are convinced that the secret to our accomplishment is our people. More than any other challenge, we are focused on attracting and retaining the right people to continue our success. We have recruited and are developing the best talent from across the globe to accomplish this. This dedication to skills extends to creating a performance culture within the Bank. We have gone to great lengths to develop a performance management system for all staff to ensure that their goals are aligned with those of the Bank. We are also committed to making the Bank the best place to work by creating an environment where all staff are able to excel and achieve their full potential.

Outlook for 2013 Much of what drives the Standard Chartered Bank story remains constant. Our strategy remains unchanged, and our aspiration remains the same – we want to be the world’s best international Bank, leading the way in Asia, Africa and the Middle East. We are putting even greater focus on our clients and customers, on building deep and long–standing relationships, on improving the quality of our service and solutions. We continue to be obsessed with the basics of banking – balancing the pursuit of growth with disciplined management of costs and risks, keeping a firm grip on liquidity and capital. We are continuing to focus on culture and values, on the way we work together across multiple geographies, products and segments, combining deep local knowledge with global capability. These fundamentals underscore everything the Bank does, and everything we as a Bank stand for.

We should have no illusions about the scale of the challenges ahead in 2013. Firstly, a turbulent global economy; the markets have greeted 2013 with enthusiasm, but we should not get carried away. We should expect bumps. Secondly, sustained political and public hostility towards banks; this is not going to go away any time soon. Thirdly, the continuing avalanche of regulatory change. Fourthly, rapid technology change; the digitisation of banking has only just begun, and it will erode margins and put intense pressure on our cost structures. Finally, intense competition; we face profound challenges to our business model. The economics of some of our businesses are changing fundamentally. Inspite of all these challenges our markets continue to grow strongly. Rapid evolution has been our recipe for success, but now we may have to be even more rapid and perhaps more revolutionary than evolutionary. This is an overview of the Bank’s 2013 priorities:

• Build stronger relationships with our clients and customers. When every bank claims to be focused on client relationships, we need to be just that much better.

• Prove we are Here for good. We can not shy away from Here for good. We must redouble our commitment to it.

• Innovate and digitise. Technology based innovation is the key to improving productivity, the key to customer differentiation.

6 Standard Chartered Bank Zambia Plc Annual Report 2012

• Intensify collaboration across the network. Our ability to collaborate across geographies, businesses and functions sets us apart. We need to play to these strengths and make them even stronger.

• Get fitter and more flexible in the way we work. More efficient. More disciplined in our deployment of scarce resources. More adaptable and agile.

• Accelerate the next generation of leaders. Leadership capacity remains one of our biggest constraints. We continue to attract great talent and will continue developing people.

• Deliver superior financial performance. A non-negotiable outcome and a prerequisite for everything else we do.

Summary 2012 has been a very good year as we have delivered a great financial performance and this is largely because we have the right staff working for the Bank. I would like to thank them for their unwavering professionalism and commitment. I would also like to thank my Chairman, Mr. Michael Mundashi SC, fellow directors, the shareholders and all the other stakeholders for their support during 2012.

Mizinga Melu (Mrs)

Managing Director 21 February 2013

7O

pe

ratin

g a

nd

fin

an

cia

l review

2012 review 2012 was a breakthrough year for the Consumer Banking business despite the headwinds experienced during the year. Income grew by 19 percent while operating profit grew by 12 percent. This was a remarkable growth by any standard.

Despite the drop in interest rates and the shrinkage of margins on foreign currency income, the business remained resilient and delivered on its commitments.

In line with our transformation strategy and our participation model, we expanded our integrated distribution network by opening four new branches in Lusaka and relocating one on the Copperbelt. As a leading Bank in innovation, our new Branches include Express Banking Centres which are the only ones of their kind in the country.

Branch opening times were extended and this was another ‘first’ we recorded in the market. We currently have the longest banking hours in the country and this is yielding positive results. Our balance sheet grew by 24 percent with loans and advances to personal customers growing by 105 percent.

Outlook Building on the momentum established in 2012, we are entering 2013 with a lot of confidence and boldness. We will remain committed to our strategy as we continue to focus on balance sheet momentum and expanding our digital capabilities.

From our experience in 2012, we have learnt to timely adapt to sudden change and to deliver superior financial performance despite the turbulence. We do not expect 2013 to be any different. However, despite any future changes, we are confident that we will deliver expectation and seize every opportunity.

Our customers will always be the centre of focus and we will continue to deepen relationships as we offer needs based solutions.

Our staff are clear that it’s not what we sell, but it’s the experience and how we meet the customer needs that will make a difference.

Consumer Banking

“We have continued to demonstrate superior financial performance amidst increasing economic and regulatory changes, a clear indication of an engaged, focused and resilient team.”

Our Objectives To be the best Consumer Bank in the market and the most desired Bank for our high value client coverage. We will continue to offer exceptional solutions and service to our customers and to recognise our staff for their dedication to ensuring our Brand stands tall in the market.

Our Strategy In 2012, we remained committed to our strategy and this is not about to change. We believe we are playing to our strength and we participating in the right segments in our chosen local markets. We will therefore continue to focus and fine tune the key drivers on the three pillars of strategy by: • Accelerating our shift to a “customer-centric”

organisation “

• Reinforcing basics and standardisation”, focused on simplification and enhancing efficiencies and the Customer experience

• Implementing country “participation models” to gain market share in our chosen segments or markets

Sonny ZuluHead of Consumer Banking

8 Standard Chartered Bank Zambia Plc Annual Report 2012

Wholesale BankingFocused execution and consistent client-led strategy delivering growth

Arjuna BalasinghamHead of Origination & Client CoverageCo-Head, Wholesale Banking

Stanley TamaleHead of Global MarketsCo-Head, Wholesale Banking

“Our success criteria has been anchored on risk management across the Board. The continued focus is a key enabler of our growth and it differentiates our value proposition in the market”

Wholesale Banking will keep focusing on our core products of cash, trade, lending, terms loans, structured arrangements and foreign exchange, where our historical experience enables us to compete and have distinctive capabilities around customers, products and delivery. We will continue to bring to our local market the dimension of “international” which means for us, high standards of customer segmentation, marketing, staff quality, risk management, modern and innovative products.”

Our Objectives• To become the strategic financial partner of choice to

our clients, deepening and building relationships and delivering seamless solutions to our clients

• To be Zambia’s best bank, connecting Zambia to the world through our international network and cross border product capabilities

Our Strategy• Strategically leverage on our balance sheet strength

and create capacity to support our clients through disciplined portfolio management

• Strengthen our support to grow trade and investment corridors between Zambia, Asia, the Middle East, and the rest of Africa

• Nurturing the Bank’s corporate culture, values and “Here for good” brand promise as the Bank continues to grow

Our Priorities • Build stronger relationships with our clients and

customers

• Prove we are here for good by supporting and benefiting the communities in which we operate

• Innovate and digitise in order to match customer needs, enhance quality and speed of delivery of e-solutions to our customers

• Intensify collaboration across the network in order to leverage on the international network and expertise of the Bank and ensure consistency of service quality

• Get more fitter and flexible in the way we work, in order to efficiently and effectively serve our customers

• Maintaining the right balance in pursuing growth opportunities in tandem with appropriate governance, systems, controls, processes and information flows

Our 2013 business endeavour • Meeting clients business needs – We shall endeavour

to understand and anticipate clients’ requirements and provide the right products to meet those specific business needs

• Cross selling/Product Partners – We shall endeavour to provide a ‘one stop shop’ offering and complete suite of products to meet client needs

• Leverage Our Client Base – We bank many blue chip companies in emerging markets and we shall continue to leverage our position while increasing

9

our share of customers ‘wallets and forging lasting business relationships

• Client Working Capital management – We shall continue to support client operations through our ability to manage cash, execute foreign exchange, support network payments and finance trade

Financial Markets The year saw many changes in financial market regulation which resulted in the further development of the derivatives market with clients increasingly hedging their interest and exchange rate exposures. Continued discipline and balance sheet management over the years has helped us maintain our strong liquidity and capital positions.

Increased use of instruments such as interest rate swaps, cross currency swaps, yield enhancing deposits, commodity derivatives, swaps and fx forwards characterised 2012 Wholesale Banking year on year revenue grew 37%, mainly on account of good performance on trade products, in the Global Corporates and Agriculture & Commodity traders customer segments. Rates trading also contributed positively.

Below is a summary of assets and customer deposits –

Wholesale Banking Graphs

LOANS AND ADVANCES (ZMK billion) CUSTOMER DEPOSITS (ZMK billion)

Op

era

ting

an

d fi

na

nc

ial review

1,500

1,000

500

-

10 Standard Chartered Bank Zambia Plc Annual Report 2012

Board of directors

1 2

5

7

4 6

3

1. MICHAEL M. MUNDASHI, SC Independent Non Executive Director

/ Chairman Appointed to the board on 1 March

2005 and Chairman in March 2009.He is an eminent lawyer, enjoying the rank and dignity of State Counsel and Principal Partner of Messrs Mulenga Mundashi & Company.

Mr. Mundashi was the first non Executive Chairman of the Revenue Appeals Tribunal and has worked on a number of Zambia Government teams on negotiation of double taxation agreements with other countries. He also sits on a few other boards and pension funds, notably African Life Assurance Limited of which he is the Chairman. He is also a member of the Konkola Copper Mines Plc Advisory Council.

2. EDSON HAMAKOWA Independent Non Executive Director Appointed to the board on 27 July

2009. Mr. Hamakowa is an eminent Accountant with an illustrious career in the BP Plc Group both within and outside Zambia.

Mr. Hamakowa has served on the Boards of Zambia National Commercial Bank, Zambia Centre for Accountancy Studies, Saturnia Regna Pension Fund, Zesco Ltd, Zambia Airways and Dunrobin Gold Mine, among others. He is also currently a member of CEC Board. He chairs the Board Risk Committee and Board Audit Committee.

3. ROBIN MILLER Independent Non Executive Director Appointed to the board on 7

August 2012. He was appointed the Managing Director of Farmers House Plc in 1996, renamed to Real Estate Investments Zambia PLC in 2012.

Robin has been a member of the Board of the Zambian Wildlife Authority, a past Chairman of Zambia’s leading independent newspaper “The Post”, a member of the Government of the Republic of Zambia/European Union Trade Enterprise Support Facility and was the founding Chairman of The Tourism Council of Zambia. Robin is a member of several boards including Madison General Insurance Company Ltd and City Investments Ltd. He chairs the Board Credit Committee.

11C

orp

ora

te go

vern

an

ce

4. EBENEZER ESSOKA Non Executive Director Appointed to the Board on 27

March 2012 . He joined SCB in 1986 and is currently Chief Executive Officer, South Africa and Area General Manager Southern Africa. Prior to this appointment, he was Chief Executive Officer of Standard Chartered Bank, Central and West Africa.

He has served on twelve SCB subsidiary Boards, currently as chairman of SCB Cameroon, Chairman of SCB Securities, South Africa and previously Chairman of SCB Côte d’Ivoire and Non Executive Director of ten others including Nigeria and Pakistan. In South Africa (SA), he currently serves as Director on the Main Board of the Banking Association, is Vice Chairman of the International Bankers’ Association and Council Member of Business Leadership SA. In addition he serves on the Global Advisory Council of the London Business School and a founding member and trustee of the Global Reach Network Foundation – an organisation focused on bridging opportunity gaps for individuals and communities worldwide.

5. MIZINGA MELU (MRS.) Managing Director Appointed to the Board as

Managing Director on 1 January, 2008. Mrs. Melu joined Standard Chartered Bank Zambia in 1993 and has worked in many markets of the Group. Prior to her appointment as Managing Director, she was Group Head for Development Organizations based in London. She has held various senior positions including Treasurer and Head of Financial Institutions, and has worked in over five countries.

Mrs. Melu, a Zambian national, is a qualified Banker and an MBA holder from Henley Management in the UK.

6. KELVIN MUSANA Executive Director Finance &

Administration Appointed to the Board on 30

January, 2007. He joined Standard Chartered Bank Zambia Plc in1998, as Financial Controller and was appointed Chief Financial Officer in February, 2005. He has undertaken assignments within the Group in Uganda, UK and Nigeria.He is a Fellow of the ACCA and ZICA, a holder of a Bachelors Degree in Accountancy from the Copperbelt University and an MBA in Finance from Manchester Business School. He is a member of the Institute of Directors.

7. CELINE MEENA NAIR Company Secretary Appointed to the Board as

Company Secretary on 17 July, 2006. She joined Standard Chartered Bank Zambia Plc on 17 July 2006. Previously she worked for the Lusaka Stock Exchange as Legal Counsel and Company Secretary. Ms. Nair is a vastly experienced practitioner with over 14 years at the Zambian Bar and holds a Bachelors Degree in Law (UNZA) and a Masters Degree in

Banking and Commercial Law (UNISA). She is a member of the Institute of Directors and Director Training Committee. She is also a trained trainer in Corporate Governance under the International Finance Corporation (IFC/World Bank).

12 Standard Chartered Bank Zambia Plc Annual Report 2012

13

Activities The company engages principally in the business of commercial banking in its widest aspects and in the provision of related services. The company also runs a successful securities services business.

Share Capital During the year 2012, the paid up primary capital of the company was increased from ZMK12,285,500,000 to ZMK 416,745,000.000. The authorized share capital of the company increased from ZMK 30,000,000,000 to ZMK 900,000,000,000 This increase was as a result of two successful bonus issues in June 2012 and October 2012 awarded to all eligible shareholders. In November 2012, there was a consolidation of the authorised and issued share capital of the Company on the basis of 1 new SCBZ Consolidated Share of par value ZMK250 for every 500 SCBZ ordinary shares of ZMK 0.50 par value each held as at the record date. This resulted in 1,800,000,000 authorised shares and 1,666,980,000 issued and fully paid shares valued at ZMK 250 per share.

Results The results for the year are set out in the statement of comprehensive income on Page 23.

Dividends At the Board Meeting held on 21 February 2013 the Directors recommended that there would be no payment of a dividend for the year ended 31 December 2012 (2011: Nil).

Directors Details of the Board of Directors are on page 10.

Secretariat There was no change to the Secretariat during 2012.

Directors’ Interests in ordinary shares The only director’s interest recorded are those in a company called Namulundu Investments, in which the Board Chairman and his wife, Mildred Mundashi have 50,933 shares in Standard Chartered Bank Zambia Plc.

Gifts and DonationsDuring the year, the bank made donations of ZMK430m (2011: ZMK483m) to charitable organisations and events.

Number of Employees and remunerationThe total remuneration of employees during the year amounted to ZMK125,500m (2011: ZMK107,930m ) and the average number of employees was as follows:

Month Number Month Number

January 639 July 660

February 655 August 656

March 651 September 658

April 656 October 661

May 654 November 671

June 654 December 696

Directors’ Report

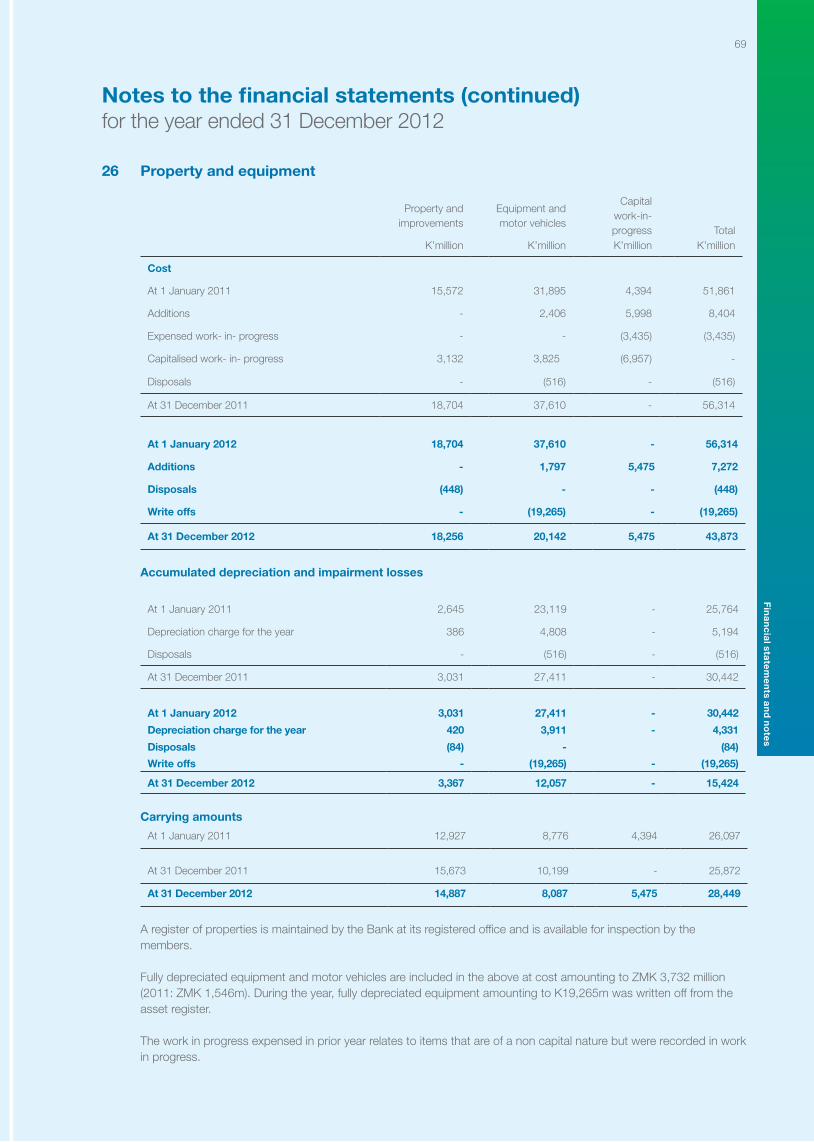

Property, Plant and EquipmentThe Bank purchased property and equipment amounting to ZMK7,272m (2011: ZMK8,404m) during the year. In the opinion of the Directors, the carrying value of property, plant and equipment is not less than their recoverable value.

Research and DevelopmentDuring the year, the Bank did not incur any research and development cost (2011: Nil).

Related Party TransactionsRelated party transactions are disclosed in Note 36 to the financial statements.

Directors’ Emoluments and InterestsDirectors’ Emoluments and Interests are disclosed in Note 36 to the financial statements.

Prohibited Borrowing or LendingThere was no prohibited borrowings or lending as defined under Sections 72 and 73 of the Banking and Financial Services Act, 1994 (as amended).

Heath and SafetyThe Bank has policies and procedures to safeguard the occupational health, safety and welfare of its employees. In addition the Bank has a dedicated Health, Safety and Environment Manager.

AuditorsThe Bank’s Auditors, Messers KPMG, have indicated their willingness to continue in office. A resolution proposing their reappointment and authorising the directors to fix their remuneration will be put to the Annual General Meeting.

By Order of the Board

Celine M. Nair Company Secretary

Co

rpo

rate g

ove

rna

nc

e

14 Standard Chartered Bank Zambia Plc Annual Report 2012

Standard Chartered Bank Zambia Plc acknowledges that as we continue our journey to becoming the world’s best international bank, it is important that we continue to conduct our business to the highest standards to deliver on our promise to build a sustainable business over the long term, to be trusted worldwide for upholding the highest standards of corporate governance and to demonstrate that we are Here for good.

“Governance” is the framework of systems, processes and controls used to ensure the effective management of the Group. The Group has an integrated approach to governance. This ensures that the Group is effectively managed and controlled, in line with our strategy; in keeping with our values and culture, and with regard to the requirements of our key stakeholders. In addition to customers and clients, these key stakeholders include governments, regulators, shareholders, employees and the communities in which we operate. Our robust approach combines formal structures applied consistently across the Group’s multiple businesses, functions and legal entities (subject only to variations in local laws and regulations), delivered within a culture of transparency, accountability and collaboration.

As a locally listed bank we believe that exemplary standards of governance are crucial to our success and ultimately depend as much on behaviour as on structure and process. It is the responsibility of all employees to be responsive and vigilant to ensure compliance with our governance framework. We take care to ensure that all employees have and demonstrate the necessary skills, values and experience commensurate with their responsibilities. We place as much emphasis on the way employees behave as on what they deliver.

Statement on corporate governance

Further, the Group’s approach to governance is underpinned by the legal and regulatory framework in each of the countries in which we operate

Standard Chartered Bank Zambia Plc recognizes that strong corporate governance is essential for delivering sustainable shareholder value and as a leading international bank, we are at the forefront of corporate governance. We believe that simply complying with written corporate governance standards is not enough. It is vital for companies to have an underlying culture with behaviours and values that support effective corporate governance. At Standard Chartered Bank Zambia Plc, each and every one of us is expected to live our brand promise and to build on a culture which is open, challenging yet cohesive and collaborative.

Regulatory Compliance: The bank has continued to perform very well in all aspects while ensuring regulatory compliance and exemplary governance at all times. To this end we have yet again achieved great success in demonstrating compliance to the banking laws and regulations. The Managing Director and the senior management team have set the right tone and messaging that non compliance is not an option, but an integral part of doing business in a sustainable way.

2012 has been a busy year in as far as new regulations are concerned. A number of regulatory pronouncements were made, among which were the regulation on recapitalization of banks, Cheque truncation , Basel II, Statutory Instrument no. 33 (Currency regulations), Rebasing of the Kwacha. As a bank we have a robust process of interpreting and communicating these new regulations throughout the bank to ensure a seamless implementation and adoption with no disruptions to the business operations.

Our relationship with the regulators has continued to be very cordial; however we have continued to focus on further enhancing the regulatory engagement especially in light of the new regulatory changes.

Standard Chartered Bank remains committed to the Zambian market. It is our brand promise to be here for good and we are confident that with our focus on regulatory compliance and strong corporate governance standards, we will continue to be seen as a leading bank that operates with great integrity and trust.

Risk Management The Bank adds value to customers and generates returns for shareholders by taking and managing risk in line with strategy and within risk appetite. Risk management is the set of end-to-end activities through which we make risk-taking decisions and we control and optimize the risk-return profile of the bank. The management of risk lies at the heart of business, as a central role of a Bank is to ‘warehouse’ risk by extending credit to selected clients and to provide products which enable clients to off-lay their price and liquidity risks to the Bank. Effective risk management is a central part of the financial and operational management of the bank and fundamental to our ability to generate profits consistently and maximize the interests of our shareholders

15

and other stakeholders. Our risk agenda addresses the following issues:

• Embedding a risk management framework, whose core components are risk classification, risk principles and standards, definitions of roles and responsibilities, governance structure.

• Improving knowledge and data management and discipline through our lessons learned, business risk review and portfolio review processes.

• Streamlining facilitation of day to day activities by locating experienced risk practitioners within the businesses, capable of drawing on the centres of excellence established within Risk.

• Ensuring the bank has appropriate systems, controls

and standards in place to accommodate the bank’s expanding product capabilities.

• Investing in our people, building bench strength and identifying succession plans.

• Risk limit setting aims to support the strategic growth of the business, but within risk appetite.

• Enhanced vigilance of the risks and identify potential adverse changes in the operating environment for early mitigation.

We are committed to grow a sustainable business and focus very strongly on exemplary risk management and the concept of zero tolerance towards regulatory breaches. We are continuously improving the way we work, balancing the pursuit of growth with control of cost and risk. The bank has a very robust risk governance structure. It is through this process that we strive to always achieve exemplary governance and ethical behavior where ever we are and to meet the regulatory standards. In this regard risk management at all levels continues to be a primary goal of the bank.”

Technology and Operations ProjectsCurrency Rebasing: The Government of the Republic of Zambia, on January 23, 2012, approved the recommendation of the Bank of Zambia to rebase the Zambian Currency. The rebased currency became legal tender on January 1, 2013. SCB Zambia set aside about ZMK 5bn for the smooth preparation and implementation. Months of strategizing and planning culminated in a successful cut-over on 1 January 2013.

The Cheque Truncation System (CTS) is an efficient method of clearing cheques using images between banks as opposed to sending physical cheques presented for payment in a bank by individuals or corporate bodies. Implementation of the cheque truncation will benefit banks and the public in a number of ways including;

- It will shorten and standardize the clearing period across the country to one clearing day (T+1),meaning value

to the cheque will be given a day after the cheque is deposited and thus facilitate early access to funds by customers.

- It will eliminate the cumbersome physical presentation of cheques by banks to the Clearing house saving time and costs associated with physical handling of cheques.

- It will reduce risks associated with manual handling and physical movement of cheques.

- It will reduce frauds and encourage wider usage and acceptance of cheques as a payment instrument.

The Bankers Association of Zambia (BAZ) has introduced new cheques with enhanced security features which are consistent with the operational requirements of the CTS. The new cheque will have the following distinct features; Watermark, a translucent image in the cheque that is seen when the cheque is held against a light source. Check digital value (CDV),representing the last two digits on the MICR code line after the space. This is a security feature generated by special algorithm and appended to the MICR code line.

Effective February 1, 2013 customers are not allowed to issue non CTS cheques as they will not be accepted for deposit. However, non-CTS cheque issued prior to cut over date of 1 February, 2013 will be accepted for clearing up to 31 July 2013 after which non CTS cheque will be completely phased out of the system. Prior to cross-over which was achieved on the 1 February 2013, SCB set aside ZMK 3.8bn for the smooth implementation of this regulatory project.

eTax this project is aimed at automating Tax payments to The Zambia Revenue Authority (ZRA) by use of online banking platforms. Currently a handful of banks which include Citi & Zanaco have already linked their systems to ZRA. This project is spearheaded by Transaction Banking and supported by GTO. We are currently engaged in talks with ZRA and reviewing proposals from vendors. Roll-out date will be advised as soon as talks are exhausted. National switch This project involves the creation of a local settlement switch for all ATM and POS systems. This is a Government initiated project aimed at eliminating the dependency on VISA. The project was first conceptualized in 2007 but was pushed back. We now expect to implement this in quarter three (Q3) of 2013.

Board Evaluation Annually, the bank conducts an independent annual online Board evaluation the results of which are shared with the Institute of Directors Zambia and the Lusaka Stock Exchange. Areas of strength and improvement are discussed in the Board meeting and an action plan is put in place to ensure the issues are tracked until closure.

Environment The bank has continued with its Environmental sustainability agenda and in the year under review undertook a number of projects such as the tree planting exercise at the Levy Mwanawasa General Hospital, participated in the 2012 Earth-hour, in which power was switched off for a full hour

Co

rpo

rate g

ove

rna

nc

e

16 Standard Chartered Bank Zambia Plc Annual Report 2012

at Standard Chartered House and North-end buildings, thereby joining several other Countries in this massive energy saving initiative and statement. In the same year, Standard Chartered Bank Zambia Plc under took a clearing of mosquito-infested areas in Garden compound and distributed 2000 treated mosquito nets to the local community.This last effort led to Zambia being awarded the Outstanding Employee Volunteering Achievement, a global recognition for a noteworthy intervention in a local community. What made this even more outstanding was the fact that it was arranged in such a way that it coincided with the World Malaria Day activities and thus enabled the bank to join the rest of the Country in supporting the fight against Malaria.

Human Resources: Staff Composition The Bank ended the year with 696 staff broken down as follows: Consumer Banking : 488 Wholesale Banking : 50 Support Functions : 158

In 2012, we remained committed and focused to support the developmental needs of our staff and have strived to be the employer of choice in the Zambian Market. Owing to the Banks reputation and stability, Standard Chartered has had and still has the ability to retain our close to 700 staff.

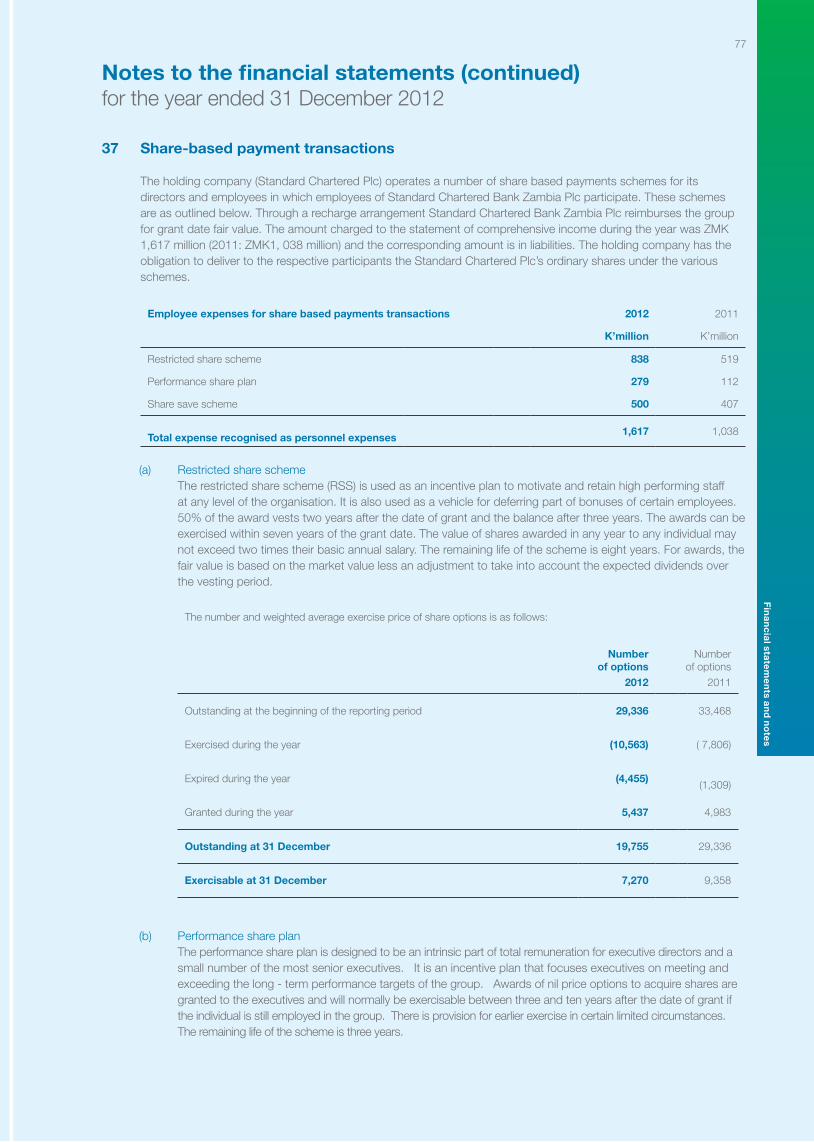

Share based payments The Banks’ employees participate in a number of share based payment schemes operated by Standard Chartered Plc, the ultimate holding company of Standard Chartered Bank Zambia Plc. Participating employees are awarded ordinary shares in Standard Chartered Plc in accordance with the terms and conditions of the relevant scheme. In addition, employees have the choice of opening a three-year savings contract. Within a period of six months after the third anniversary, as appropriate, employees may purchase ordinary shares of Standard Chartered Bank Plc. The price at which they may purchase shares is at a discount of up to twenty per cent on the share price at the date of invitation. There are no performance conditions attached to options granted under all employee share save schemes. Equity settled options or share awards are calculated at the time of grant based on the fair value of the equity instruments

granted and that grant date fair value is not subject to change the fair value of equity instruments.

HIV/AIDS Programmes The Bank’s response to HIV/AIDS stems from a desire to protect basic human rights, preserve the integrity of its labour force, reduce costs associated with HIV/AIDS, and respond to what the company recognises as a global challenge.

In a continued effort to work with partners, awareness sessions were held to educate our community on the pandemic and a total of 600 people were reached through the sessions.

Standard Chartered Bank Zambia limited donated dell desktop computers to the Network of Zambian People Living with HIV and Aids (NZP+) in Lusaka on 4th December 2012.

The desktop computers will be used in the NZP+ Resource Centres and information hubs in Lusaka, Livingstone, Mongu and Mufulira. Some of the computers will be allocated to NZP+ district Chapters, where they will be used for information processing and generation of programme and financial reports. The donation will have a multiplier effect because the computers will be used to reach other infected members of the public in those districts.

In terms of social responsibility various departments in the bank have participated in several initiatives to sensitize local communities on HIV/AIDS through employee volunteering activities. The Bank provides its staff members 3 days of volunteering leave in addition to their annual leave, in which they can work on such initiatives in the communities we operate in.

By Order of the Board

Celine M. Nair Company Secretary 21 February 2013

17

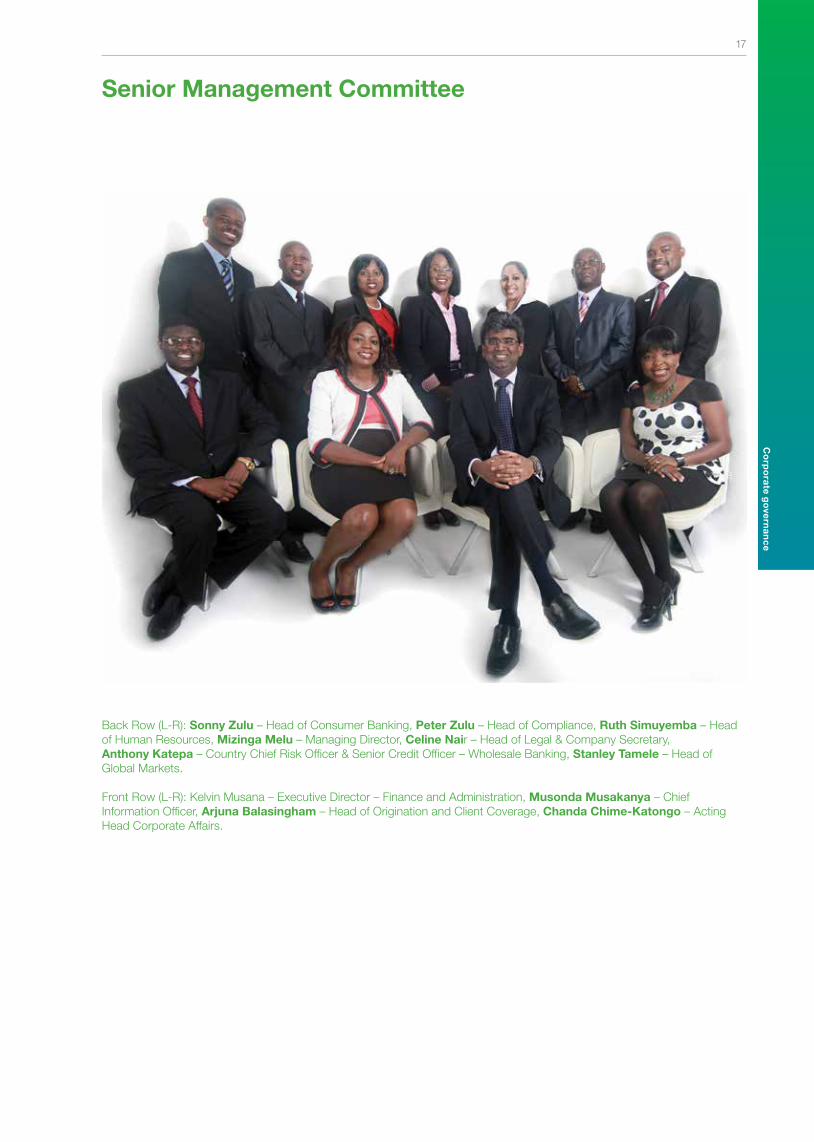

Senior Management Committee

Back Row (L-R): Sonny Zulu – Head of Consumer Banking, Peter Zulu – Head of Compliance, Ruth Simuyemba – Head of Human Resources, Mizinga Melu – Managing Director, Celine Nair – Head of Legal & Company Secretary, Anthony Katepa – Country Chief Risk Officer & Senior Credit Officer – Wholesale Banking, Stanley Tamele – Head of Global Markets.

Front Row (L-R): Kelvin Musana – Executive Director – Finance and Administration, Musonda Musakanya – Chief Information Officer, Arjuna Balasingham – Head of Origination and Client Coverage, Chanda Chime-Katongo – Acting Head Corporate Affairs.

Co

rpo

rate g

ove

rna

nc

e

18 Standard Chartered Bank Zambia Plc Annual Report 2012

Making a difference in our communities

Staff planting trees

We consider the environmental challenges across the countries where we operate and proactively manage the direct impact of our operations. In 2012, we improved the energy efficiency of our offices and branches and decreased our paper consumption per full time employee (FTE). Standard Chartered Bank Zambia Plc has continued with its Environmental sustainability agenda and in the year under review undertook a number of projects such as the tree planting exercises at the Levy Mwanawasa General Hospital and the SOS children’s village in Lusaka, The Bank was awarded the Outstanding Employee Volunteering Achievement, a global recognition for a noteworthy intervention in a local community.

Seeing is believing

Eye screening at the market place Seeing is Believing is a global collaboration between Standard Chartered Bank and leading international eye care NGOs, to tackle preventable blindness. Standard Chartered Bank has raised USD20m, as at 2012, to provide 20 million people in impoverished urban areas with access to comprehensive eye-care services worldwide. In Zambia, the SiB project has changed lives of more than 1 million people. In 2012 we invested a further USD1m into this project as we partnered with ORBIS Africa, an NGO with a history of 30 years of sight saving. The Bank has also partnered with Sight Savers International since 2009 and in 2012 this particular partnership saw close to 65,000 adults and children screened, 2,000 cataracts and trichiasis operations performed, 7,000 spectacles dispensed, and, 400,000 trachoma drugs disbursed.

Volunteering at UTH

A few years ago, the Bank carried out a complete refurbishment of three paediatrics wards because we believe in making a sustainable difference in the community.

It is for this reason that in July 2012 we painted the three paediatrics wards and donated blankets for the children. Our contribution did not end in monetary form as our members of staff, volunteered by way of participating in the painting.

19

Annual financial statements

for the year ended 31 December 2012

Fin

an

cia

l state

me

nts a

nd

no

tes

20 Standard Chartered Bank Zambia Plc Annual Report 2012

KPMG Chartered Accountants Telephone + 260 211 372 900 First Floor, Elunda Two Website www.kpmg.com Addis Ababa Roundabout Rhodes Park P O Box 31282

Lusaka, Zambia

KPMG Chartered Accountants, a Zambian partnership, is a member firm of the partners: A list of the Partners is available KPMG network of independent member firms affiliated with KPMG International at the above mentioned address Cooperative ("KPMG International"), a Swiss entity. All rights reserved

17

Directors’ responsibilities in respect of the preparation of financial statements

The Bank’s directors are responsible for the preparation and fair presentation of the financial statements of Standard Chartered Bank Zambia Plc, comprising the statements of financial position as at 31 December 2012, and the statements of comprehensive income, changes in equity and cash flows for the year then ended, and the notes to the financial statements which include a summary of significant accounting policies and other explanatory notes in accordance with International Financial Reporting Standards, the Banking and Financial Services Act and in the manner required by the Companies Act of Zambia. In addition, the directors are responsible for preparing the director’s report.

The directors are also responsible for such internal control as the Directors determine is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error and for maintaining adequate accounting records and an effective system of risk management as well as the preparation of the supplementary schedules included in these financial statements.

The Directors have made an assessment of the Bank’s ability to continue as a going concern and have no reason to believe the business will not be a going concern in the year ahead.

The auditor is responsible for reporting on whether the annual financial statements are fairly presented in accordance with International Financial Reporting Standards.

Approval of the financial statements The financial statements, of the Bank as indicated above and set out on pages 23 to 78 were approved by the Directors on 21 February 2013 and were signed on their behalf by:

M. Mundashi M. MeluChairman Managing Director

K. MusanaExecutive Director - Finance and Administration

21

KPMG Chartered Accountants Telephone + 260 211 372 900 First Floor, Elunda Two Website www.kpmg.com Addis Ababa Roundabout Rhodes Park P O Box 31282

Lusaka, Zambia

KPMG Chartered Accountants, a Zambian partnership, is a member firm of the partners: A list of the Partners is available KPMG network of independent member firms affiliated with KPMG International at the above mentioned address Cooperative ("KPMG International"), a Swiss entity. All rights reserved

17

Independent Auditor’s Report to the Members of Standard Chartered Bank Zambia Plc

Report on the Financial Statements We have audited the annual financial statements of Standard Chartered Bank Zambia Plc which comprises the statement of financial position as at 31 December 2012, and the statements of comprehensive income, changes in equity and cash flows for the year then ended, and the notes to the financial statements which include a summary of significant accounting principles and other explanatory notes, as set out on pages 23 to 78.

Directors’ responsibility for the financial statements The Bank’s Directors are responsible for the preparation and fair presentation of these financial statements in accordance with International Financial Reporting Standards, the Banking and Financial Services Act of Zambia and in the manner required by the Companies Act of Zambia, and for such internal control as the Directors determine is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with International Standards on Auditing. Those Standards require that we comply with relevant ethical requirements and plan and perform the audit to obtain reasonable assurance whether the financial statements are free of material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on our judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, we consider internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting principles used and the reasonableness of the accounting estimates made by the Directors, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion In our opinion, the financial statements present fairly, in all material respects, the financial position of Standard Chartered Bank Zambia Plc as at 31 December 2012 and of its financial performance and cash flows for the year then ended in accordance with International Financial Reporting Standards and the requirements of the Banking and Financial Services Act and the, Companies Act of Zambia.

KPMG

Other matter Supplementary information set out on page 79 does not form part of the annual financial statements and is presented as additional information. We have not audited this schedule and accordingly we do not express an opinion on it.

Report on Other Legal and Regulatory Requirements In accordance with Section 173 (3) of the Companies Act of Zambia, we report that, in our opinion the required accounting records, other records and registers have been properly kept in accordance with the Act.

In accordance with Section 64 (2) of the Banking and Financial Services Act we report that in our opinion:

• the Bank made available all necessary information to enable us to comply with the requirements of this Act;

• the Bank has complied in all material respects with the provisions of this Act and the regulations, guidelines and prescriptions under this Act.

• there were no non-performing or restructured loans owing to the Bank whose principal amount exceeds 5% of the regulatory capital.

KPMG Chartered Accountants

Dumi Tshuma 04 March 2013

Partner Lusaka, Zambia

KPMG

23

Statement of comprehensive incomefor the year ended 31 December 2012

Notes 2012 2011

K’million K’million

Interest income 9 405,617 314,540

Interest expense 10 (83,921) (57,127)

Net interest income 321,696 257,413

Fee and commission income 11 173,815 139,613

Fee and commission expense 11 (18,183) (14,033)

Net fee and commission income 155,632 125,580

Net trading income 12 114,055 86,212

Net income from financial instruments at fair value through profit or loss 13 22,452 9,318

Other income 14 6,582 794

143,089 96,324

Revenue 620,417 479,317

Personnel expenses 15 (169,155) (143,389)

Depreciation, amortisation, premises and equipment expenses 15 (38,202) (33,709)

Other expenses 15 (70,164) (68,813)

Impairment on loans and advances 25 (3,278) (7,319)

Profit before income tax 339,618 226,087

Income tax expense 17 (118,625) (93,634)

Profit for the year 220,993 132,453

Other comprehensive income, net of income tax

Net changes in fair value reserve on available for sale securities 2,071 (379)

Net amount transferred to profit and loss on available for sale securities (1,850) (2,737)

Other comprehensive income for the year, net of income tax 221 (3,116)

Total comprehensive income for the year 221,214 129,337

The notes on pages 29 to 78 are an integral part of these financial statements.

23F

ina

nc

ial sta

tem

en

ts an

d n

ote

s

24 Standard Chartered Bank Zambia Plc Annual Report 2012

Statement of comprehensive income (continued)for the year ended 31 December 2012

Notes

2012 2011

K’million K’million

Profits attributable to:

Equity holders of the banks 220,993 132,453

Profit for the year 220,993 132,453

Total comprehensive income attributable:

Equity holders of the banks 221,214 129,337

Total comprehensive income for the year 221,214 129,337

Earnings per share

Basic and diluted earnings per share (Kwacha) 18 132.57 79.46

The notes on pages 29 to 78 are an integral part of these financial statements.

24 Standard Chartered Bank Zambia Plc Annual Report 2012

25

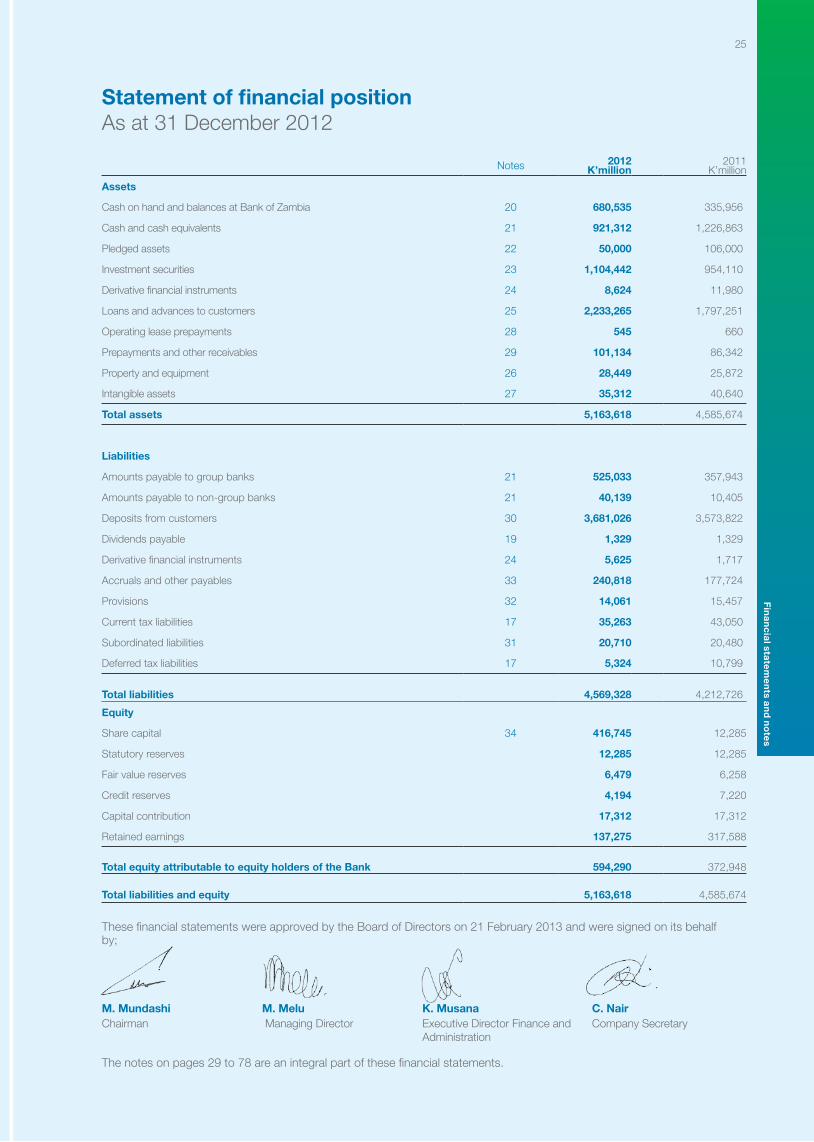

Statement of financial positionAs at 31 December 2012

Notes 2012 K’million

2011 K’million

Assets

Cash on hand and balances at Bank of Zambia 20 680,535 335,956

Cash and cash equivalents 21 921,312 1,226,863

Pledged assets 22 50,000 106,000

Investment securities 23 1,104,442 954,110

Derivative financial instruments 24 8,624 11,980

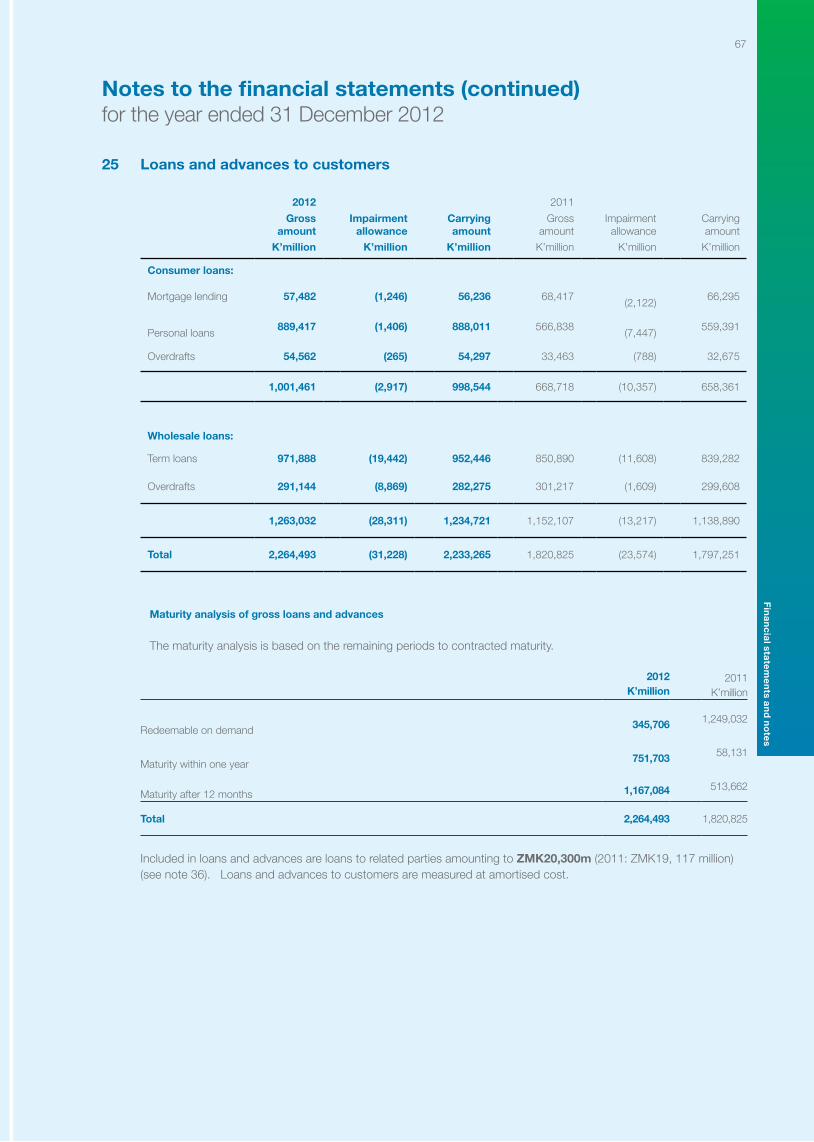

Loans and advances to customers 25 2,233,265 1,797,251

Operating lease prepayments 28 545 660

Prepayments and other receivables 29 101,134 86,342

Property and equipment 26 28,449 25,872

Intangible assets 27 35,312 40,640

Total assets 5,163,618 4,585,674

Liabilities

Amounts payable to group banks 21 525,033 357,943

Amounts payable to non-group banks 21 40,139 10,405

Deposits from customers 30 3,681,026 3,573,822

Dividends payable 19 1,329 1,329

Derivative financial instruments 24 5,625 1,717

Accruals and other payables 33 240,818 177,724

Provisions 32 14,061 15,457

Current tax liabilities 17 35,263 43,050

Subordinated liabilities 31 20,710 20,480

Deferred tax liabilities 17 5,324 10,799

Total liabilities 4,569,328 4,212,726

Equity

Share capital 34 416,745 12,285

Statutory reserves 12,285 12,285

Fair value reserves 6,479 6,258

Credit reserves 4,194 7,220

Capital contribution 17,312 17,312

Retained earnings 137,275 317,588

Total equity attributable to equity holders of the Bank 594,290 372,948

Total liabilities and equity 5,163,618 4,585,674

These financial statements were approved by the Board of Directors on 21 February 2013 and were signed on its behalf by;

M. Mundashi M. Melu K. Musana C. NairChairman Managing Director Executive Director Finance and

AdministrationCompany Secretary

The notes on pages 29 to 78 are an integral part of these financial statements.

25F

ina

nc

ial sta

tem

en

ts an

d n

ote

s

26 Standard Chartered Bank Zambia Plc Annual Report 2012

Statement of changes in equityAs at 31 December 2012

2011 Share capital

Statutory reserves

Fair value reserves

Credit reserves

Share-based

payment reserves

Capital Contribution

Retained earnings

Total

K’million K’million K’million K’million K’million K’million K’million K’million

Balance at 1 January 2011 2,048 2,048 9,374 1,634 - 17,312 293,095 325,511

Total comprehensive income for the year

Profit for the year - - - - - - 132,453 132,453 Other comprehensive income net of income taxFair value reserve on available-for-sale investment securities

- Net change in fair value - - (379) - - - - (379)- Net amount transferred to profit and

loss- - (2,737) - - - - (2,737)

Total comprehensive income for the year

-- (3,116) - - 132,453 129,337

Transfer from retained earnings 5,586 (5,586) -

Transactions with owners, recognised directly in equity

Dividend to equity holders - - - - - - (81,900) (81,900)

Bonus issue

10,237 10,237 - - - - (20,474) -Share based payment transactions - - - - 1,038 - (1,038) -

Distribution - - - - (1,038) - 1,038 -

Total contributions by and distributions to owners

10,237 10,237 - - - - (102,374) (81,900)

Balance at 31 December 2011 12,285 12,285 6,258 7,220 - 17,312 317,588 372,948

2012 Share capital Statutory reserves

Fair value reserves

Credit reserves

Share-based

payment reserves

Capital Contribution

Retained earnings Total

K’million K’million K’million K’million K’million K’million K’million K’million

Balance at 1 January 2012 12,285 12,285 6,258 7,220 - 17,312 317,588 372,948

Total comprehensive income for the year

Profit for the year - - - - - - 220,993 220,993

Other comprehensive income net of income tax - - - - - - - -

Fair value reserve on available-for-sale investment securities - - - - - - - -

- Net change in fair value - - 2,071 - - - - 2,071

- Net amount transferred to profit and loss - - (1,850) - - - - (1,850)

Total comprehensive income for the year - - 221 - - - 220,993 221,214

Transfer from retained earningsUnclaimed dividends written back

--

--

--

(3,026)-

--

--

3,026 128

- 128

Transactions with owners, recognised directly in equity

Bonus issue 404,460 - - - - - (404,460) -

Share based payment transactions - - - - 1,617 - (1,617) -

Distribution - - - - (1,617) - 1,617 -

Total contributions by and distributions toowners

404,460 - - - - - (404,460) -

Balance at 31 December 2012 416,745 12,285 6,479 4,194 - 17,312 137,275 594,290

26 Standard Chartered Bank Zambia Plc Annual Report 2012

27

Statement of changes in equity (continued)As at 31 December 2012

Fair value reserve

The fair value reserve comprises the fair value movement of financial assets classified as available-for-sale. Gains and losses

are deferred to this reserve until such time as the underlying asset is sold or matures.

Credit reserve

The credit reserve is a loan loss reserve that relates to the excess of impairment provision as required by the Banking and

Financial Services Act of Zambia over the impairment provision computed in terms of International Financial Reporting Stan-

dards.

Share based payment reserves

This relates to the equity settled share based payment transactions the Bank employees have with the Standard Chartered

Holdings (Africa) BV.

Capital contribution

The capital contribution reserve relates to the franchise value arising from the acquisition of the Security Services business.

The franchise value is the amount paid on behalf of the Bank by Standard Chartered Plc (there after referred to as the group)

for the acquisition of the Security Services business.

Retained earnings

Retained earnings are the carried forward recognised income net of expenses of the Bank plus current period profit

attributable to shareholders less distribution to shareholders.

Statutory reserves

Statutory reserves comprise transfers out of net profits prior to dividends, of amounts prescribed under statutory instrument

No. 21 of 1995: The Banking and Financial Services (Reserve Account) Regulations 1995.

27F

ina

nc

ial sta

tem

en

ts an

d n

ote

s

28 Standard Chartered Bank Zambia Plc Annual Report 2012

Statement of cash flowsfor the year ended 31 December 2012

Note 2012

K’million2011

K’million

Cash flow from operating activities

Profit before tax 339,618 226,087

Adjustment for items not involving cash or shown separately

Depreciation of property and equipment 26 4,331 5,194

Amortisation of intangible assets 27 5,328 5,809

Expensed work in progress 26 - 3,435

Equity-settled share-based payments transaction 15 1,617 1,038

Expensed portion of leasehold land prepayment 15 13 17

Impairment losses 25 3,278 7,319

Gain on disposal of property and equipment 14 (6,235) (201)

Net interest income (322,519) (269,943)

Effect of exchanges rate fluctuations on subordinated loan capital 230 1,360

25,661 (19,885)

Change in operating assets and liabilities

Pledged assets 56,000 (106,000)

Loans and advances to banks - 83,101

Loans and advances to customers (436,014) (645,866)

Derivative financial instruments 7,264 (10,175)

Prepayments and other receivables (14,792) (58,485)

Deposits from customers 107,204 409,235

Provisions (1,396) (287)

Accruals and other payables 63,095 64,717

(218,639) (263,760)

Interest received 406,440 314,540

Interest paid (83,921) (57,127)

322,519 257,413

Net cash generated from operating activities before taxation Income tax paid 17

129,541

(132,006)

(26,232)

(89,327)

Net cash used in operating activities (2,465) (115,559)

Cash flows from investing activities

Aquisition of property and equipment to maintain operations 26 (7,272) (8,404)

Investment in government securities (150,332) 25,074

Proceeds from disposal of property and equipment 6,316 201

Net cash used in investing activities (151,288) 16,871

Cash flows from financing activities

Dividends paid 19 - (81,926)

Net cash used in financing activities - (81,826)

Net decrease in cash and cash equivalents (153,753) (180,614)

Cash and cash equivalents at beginning of year 1,194,471 1,376,908

Effect of exchange rate fluctuation on cash held (4,043) (1,823)

Cash and cash equivalents at end of year21

1,036,675 1,194,471

The notes on pages 29 to 78 are an integral part of these financial statements.

28 Standard Chartered Bank Zambia Plc Annual Report 2012

29

Notes to the financial statements for the year ended 31 December 2012

1 Reporting entity

Standard Chartered Bank Zambia Plc (“the Bank”) is a company domiciled in Zambia. The address of the Bank’s registered office is Standard Chartered House, Cairo Road, Lusaka. The Bank is primarily involved in wholesale and consumer banking.

2 Basis of preparation

2.1 Statement of compliance The Bank’s financial statements have been prepared in accordance with International Financial Reporting Standards

(IFRSs) as issued by the International Accounting Standards Board (IASB), the requirements of the Banking and Financial Services Act and the Companies Act of Zambia.

2.2 Basis of measurement The financial statements have been prepared on the historical cost basis except for the following:

• derivative financial instruments are measured at fair value; • available-for-sale financial assets are measured at fair value; and • financial instruments at fair value through profit or loss are measured at fair value.

2.3 Functional and presentation currency These financial statements are presented in Zambian Kwacha (“Kwacha”), which is the Bank’s functional currency. All

financial information presented in Kwacha has been rounded to the nearest million, except when otherwise indicated.

2.4 Use of estimates and judgments The preparation of financial statements requires management to make judgements, estimates and assumptions that

affect the application of accounting policies and the reported amounts of assets, liabilities, income and expenses. Actual results may differ from these estimates.

Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognised in the period in which the estimate is revised and in any future periods affected.

Information about significant areas of estimation uncertainty and critical judgements in applying accounting policies that have the most significant effect on the amounts recognised in the financial statements are described in note 6.

3 Significant accounting policies

The principal accounting policies applied in the preparation of these financial statements are set out below. These policies have been consistently applied to all the years presented, unless otherwise stated.

3.1 Interest income and expense Interest income and expense are recognised in statement of comprehensive income using the effective interest

method. The effective interest method is a method of calculating the amortised cost of a financial asset or a financial liability and of allocating the interest income or interest expense over the relevant period. The effective interest rate is the rate that exactly discounts estimated future cash payments or receipts through the expected life of the financial instrument or, when appropriate ,a shorter period to the carrying amount of the financial asset or financial liability. When calculating the effective interest rate, the Bank estimates future cash flows considering all contractual terms of the financial instrument (for example, repayment options) but does not consider future credit losses. The calculation includes all fees and points paid or received between parties to the contract that are an integral part of the effective interest rate, transaction costs and all other premiums or discounts. Transaction costs are incremental costs that are directly attributable to the acquisition, issue or disposal of a financial asset or liability. The effective interest rate is established on initial recognition of the financial asset and liability and is not revised subsequently.

29F

ina

nc

ial sta

tem

en

ts an

d n

ote

s

30 Standard Chartered Bank Zambia Plc Annual Report 2012

Notes to the financial statements (continued)for the year ended 31 December 2012

3 Significant accounting policies (continued)

3.1 Interest income and expense (continued)Interest income and expense presented in the statement of comprehensive income includes:

• interest on financial assets and financial liabilities at amortised cost on an effective interest basis; • interest on available-for-sale investment securities on an effective interest basis; and • Interest on financial assets at fair value through profit or loss on an effective interest basis.

Interest income and expense on all trading assets and liabilities are considered to be incidental to the Bank’s trading operations and are presented together with all other changes in the fair value of trading assets and liabilities in net trading income.

Once a financial asset or a group of similar financial assets has been written down as a result of an impairment loss, interest continues to be recognised on the impaired asset using the original effective interest rate.

3.2 Fees and commissions Fees and commissions income is recognised on an accrual basis when the service has been provided. Loan

syndication fees are recognised as revenue when the syndication has been completed and the Bank retained no part of the loan package for itself or retained a part at the same effective interest rate as the other participants. Portfolio and other management advisory and service fees are recognised based on the applicable service contracts as the service is provided, which is usually on a time basis.

Fees and commission income and expenses that are integral to the effective interest rate on a financial asset or financial liability are included in the measurement of the effective interest rate.

Other fees and commission income, including account servicing fees, investment management fees, sales commission, and placement fees, are recognised as the related services are performed. When a loan commitment is not expected to result in a draw-down of a loan, loan commitment fees are recognised on a straight-line basis over the commitment period.

Other fees and commission expense relate mainly to transaction and service fees, which are expensed as the services are received.

3.3 Net trading income Net trading income comprises gains less losses related to trading assets and liabilities, and includes all realised and

unrealised fair value changes, interest and foreign exchange differences.

3.4 Net income from financial instruments at fair value through profit or loss Net income from other financial instruments at fair value through profit or loss relates to gains and loss arising

from changes in the fair value of the financial assets at fair value through profit or loss, financial assets mandatorily measured at fair value through profit or loss other than those held for trading, and financial assets and liabilities designated at fair value through profit or loss.

3.5 Lease payments Payments made under operating leases are recognised in profit or loss on a straight-line basis over the term of the

lease. Lease incentives received are recognised as an integral part of the total lease expense, over the term of the lease.

3.6 Income tax Income tax expense Income tax expense comprises current and deferred tax. Income tax expense is recognised in profit or loss except to

the extent that it relates to items recognised directly in equity or in other comprehensive income.

The current tax charge is determined in accordance with the provisions of the Income Tax Act 1966 (as amended) (Chapter 323 of the laws of Zambia), and is based on the adjusted profit for the year using tax rates enacted or substantively enacted at the reporting date and any adjustment to tax payable in respect of previous years. The current tax charge is recognised as an expense in the period in which profits arise.

30 Standard Chartered Bank Zambia Plc Annual Report 2012

31

Notes to the financial statements (continued)for the year ended 31 December 2012

3 Significant accounting policies (continued)

3.6 Income tax (continued)

Deferred tax Deferred tax is recognised in respect of temporary differences between the carrying amounts of assets and liabilities

for financial reporting purposes and the amounts used for taxation purposes.

Deferred tax is not recognised for the following temporary differences: the initial recognition of assets or liabilities in a transaction that is not a business combination and that affects neither accounting nor taxable profit or loss, and differences relating to investments in subsidiaries and jointly controlled entities to the extent that it is probable that they will not reverse in the foreseeable future. In addition, deferred tax is not recognised for taxable temporary differences arising on the initial recognition of goodwill.

Deferred tax is measured at the tax rates that are expected to be applied to temporary differences when they reverse, based on the laws that have been enacted or substantively enacted by the reporting date.

Deferred tax assets and liabilities are offset if there is a legally enforceable right to offset current tax liabilities and assets, and they relate to income taxes levied by the same tax authority on the same taxable entity, or on different tax entities, but they intend to settle current tax liabilities and assets on a net basis or their tax assets and liabilities will be realised simultaneously.