key export markets for u.s. defense...

TRANSCRIPT

PRIVATE & CONFIDENTIAL

A quantitative analysis of UAE, Saudi Arabia, and Qatar

Key Export Markets for U.S. Defense Suppliers

Prepared for:

PRIVATE & CONFIDENTIAL | AVASCENT | 2

Executive Summary

The Virginia Economic Development Partnership asked Avascent to evaluate four defense export markets based on current and future procurements of defense materiel

Qatar, Saudi Arabia, and the UAE all exhibit growth in defense spending generally, and defense procurement in particular; further, their historic preference for U.S. equipment makes them attractive export markets

However, the mix of defense investment priorities is shifting in these markets in response to changes in the internal and regional threat environment

Further, an increasing desire to maintain diverse supplier relationships and to develop indigenous industry may present challenges to U.S. firms wishing to serve these markets

PRIVATE & CONFIDENTIAL | AVASCENT | 3

Structure and Definitions

The data used in these reports is sourced from Avascent’s Global Platforms and Systems tool, which takes a bottom-up and top-down approach to identifying and forecasting defense procurement in the U.S. and abroad

In addition to qualitative market analysis, each country report features the following quantitative views:

– Defense Platforms. This view depicts current and future procurements of integrated ground, airborne, and ship platforms as well as integrated air defense systems

– Defense Systems. This view disaggregates platforms into their component electronic systems, spanning C4I, electronic warfare, and sensing equipment

–Prime Contractors. This view displays the market share among major platform integrators

–Sub-Contractors. This view represents a level of granularity below prime contractors and displays the market share among major sub-system manufacturers

–Opportunity Space. This view categorizes emerging stated or projected military requirements by platform type and electronic systems market category

Note: Additional methodology slides are available in the appendix

PRIVATE & CONFIDENTIAL | AVASCENT | 4

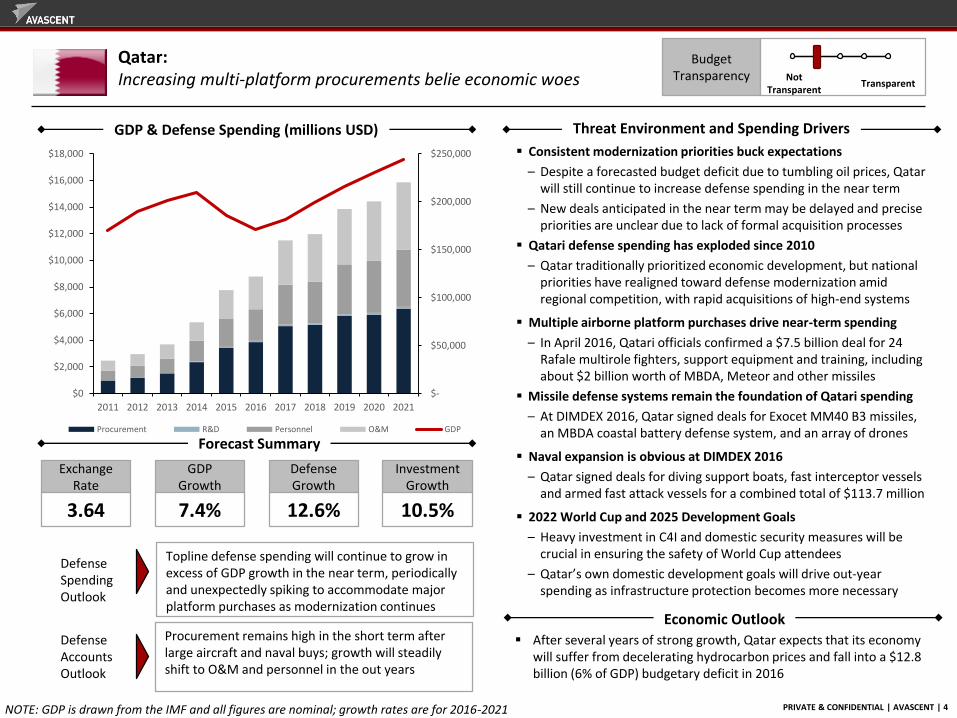

Consistent modernization priorities buck expectations

– Despite a forecasted budget deficit due to tumbling oil prices, Qatar will still continue to increase defense spending in the near term

– New deals anticipated in the near term may be delayed and precise priorities are unclear due to lack of formal acquisition processes

Qatari defense spending has exploded since 2010

– Qatar traditionally prioritized economic development, but national priorities have realigned toward defense modernization amid regional competition, with rapid acquisitions of high-end systems

Multiple airborne platform purchases drive near-term spending

– In April 2016, Qatari officials confirmed a $7.5 billion deal for 24 Rafale multirole fighters, support equipment and training, including about $2 billion worth of MBDA, Meteor and other missiles

Missile defense systems remain the foundation of Qatari spending

– At DIMDEX 2016, Qatar signed deals for Exocet MM40 B3 missiles, an MBDA coastal battery defense system, and an array of drones

Naval expansion is obvious at DIMDEX 2016

– Qatar signed deals for diving support boats, fast interceptor vessels and armed fast attack vessels for a combined total of $113.7 million

2022 World Cup and 2025 Development Goals

– Heavy investment in C4I and domestic security measures will be crucial in ensuring the safety of World Cup attendees

– Qatar’s own domestic development goals will drive out-year spending as infrastructure protection becomes more necessary

Qatar:Increasing multi-platform procurements belie economic woes

Budget Transparency Not

TransparentTransparent

Economic Outlook

Threat Environment and Spending DriversGDP & Defense Spending (millions USD)

Forecast Summary

Exchange Rate

3.64

Topline defense spending will continue to grow in excess of GDP growth in the near term, periodically and unexpectedly spiking to accommodate major platform purchases as modernization continues

Procurement remains high in the short term after large aircraft and naval buys; growth will steadily shift to O&M and personnel in the out years

GDP Growth

7.4%

Defense Growth

12.6%

Investment Growth

10.5%

Defense Spending Outlook

Defense Accounts Outlook

After several years of strong growth, Qatar expects that its economy will suffer from decelerating hydrocarbon prices and fall into a $12.8 billion (6% of GDP) budgetary deficit in 2016

NOTE: GDP is drawn from the IMF and all figures are nominal; growth rates are for 2016-2021

$-

$50,000

$100,000

$150,000

$200,000

$250,000

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Procurement R&D Personnel O&M GDP

PRIVATE & CONFIDENTIAL | AVASCENT | 5

Market Overview: Defense PlatformsAcquisitions are characterized by high-end, big-ticket purchases

• AH-64 Apache

• AH-64E Apache Guardian

• UH-60M Black Hawk

• MH-60R Seahawk

• NH-90 Troop Transport

Rotorcraft

• Rafale

• F-15 Eagle

• E-737B AWACS

• C-17 Globemaster III

Fixed Wing

Aircraft

Market Segment OverviewMarket Size and Forecast (2011-2021)

• Patrol Ship

• Future Amphibious Assault Ship

• Future Corvette

• Future Frigates

Surface Vessels

Key:

$ 544M 24%Fixed Wing Aircraft

2016 CAGR 2016-21

Surface Vessels $199M 24%

• $7.1B

• $1.8B

• $1.1B

• $714M

• $683M

• $1.8B

• $1.7B

• $1.4B

• $690M

• $820M

• $500M

• $300M

• $200M

2011-21 Value

$-

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Mill

ion

s

Rotorcraft Fixed Wing Aircraft

Weapons Surface Vessels

Wheeled & Tracked Combat Vehicles Manportable

Unmanned Aerial Systems Logistics Vehicles

Ground Vehicles

Rotorcraft $ 750M 9%

Weapons $384M 18%

• THAAD Interceptors

• Coastal Battery Defense System

• MICA

• Hammer AASMWeapons

• $2.4B

• $532M

• $520M

• $442M

PRIVATE & CONFIDENTIAL | AVASCENT | 6

Market Overview: Defense SystemsMissile defense systems as well as high-end airborne platforms drive the market for defense electronics

• RF-Based EW Systems

• Optical-Based EW Systems

• EW Expendables

• Other EW/Information Warfare

Electronic Warfare

• Radar Systems

• Optical Systems

• Other Sensors

• Sonar SystemsSensors

Market Segment OverviewMarket Size and Forecast (2011-2021)

• Missiles

• Torpedoes & Weapon Support Equipment

• Ammunition

• Gun Systems

Weapons

Key:

$147M 10%Electronic Warfare (EW)

Sensors $468M 4%

2016 CAGR 2016-21

• Human Machine Interface

• Integrated Systems

• Utilities

• Vehicle Management SystemsAvionics

Weapons $1.1B 11%

Avionics $68M 2%

• $820M

• $411M

• $261M

• $202M

• $2.7B

• $739M

• $652M

• $114M

• $9.0B

• $1.9B

• $358M

• $203M

• $150M

• $140M

• $92M

• $84M

2011-21 Value

$-

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Mill

ion

s

Weapons C4I Sensors EW Avionics

PRIVATE & CONFIDENTIAL | AVASCENT | 7

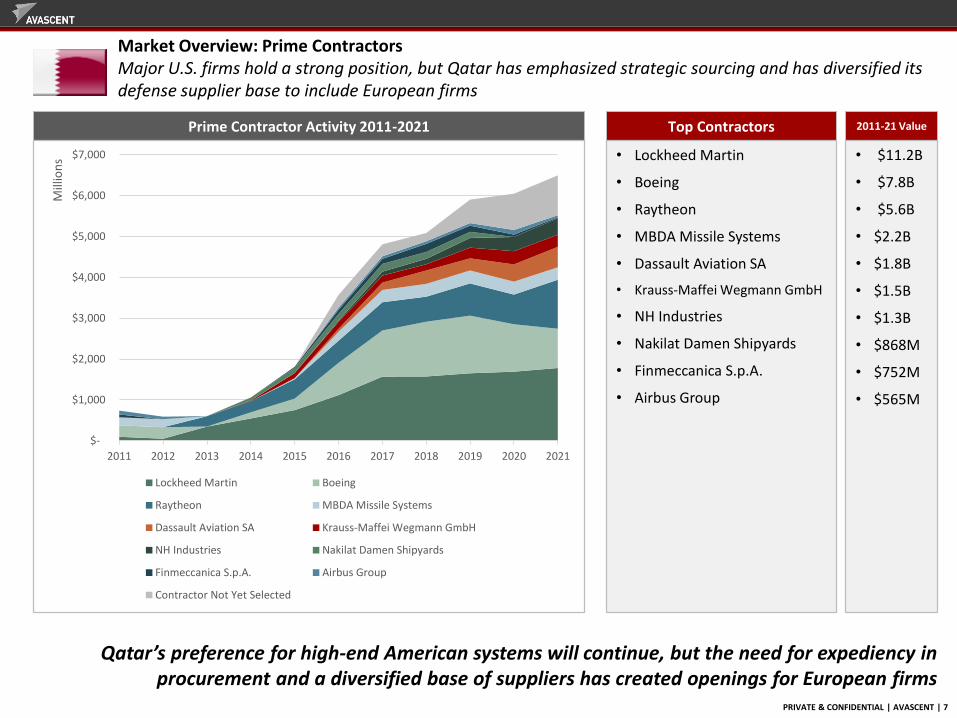

Prime Contractor Activity 2011-2021

Market Overview: Prime ContractorsMajor U.S. firms hold a strong position, but Qatar has emphasized strategic sourcing and has diversified its defense supplier base to include European firms

Top Contractors

• Lockheed Martin

• Boeing

• Raytheon

• MBDA Missile Systems

• Dassault Aviation SA

• Krauss-Maffei Wegmann GmbH

• NH Industries

• Nakilat Damen Shipyards

• Finmeccanica S.p.A.

• Airbus Group

Qatar’s preference for high-end American systems will continue, but the need for expediency in procurement and a diversified base of suppliers has created openings for European firms

2011-21 Value

• $11.2B

• $7.8B

• $5.6B

• $2.2B

• $1.8B

• $1.5B

• $1.3B

• $868M

• $752M

• $565M

$-

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Mill

ion

s

Lockheed Martin Boeing

Raytheon MBDA Missile Systems

Dassault Aviation SA Krauss-Maffei Wegmann GmbH

NH Industries Nakilat Damen Shipyards

Finmeccanica S.p.A. Airbus Group

Contractor Not Yet Selected

PRIVATE & CONFIDENTIAL | AVASCENT | 8

Subcontractor Activity 2011-2021

Market Overview: SubcontractorsThe top components manufacturers largely mirror the top prime contractors, owing to the high value of structural components on airborne platforms

Top Contractors

• Lockheed Martin

• Boeing

• Raytheon

• MBDA Missile Systems

• Airbus Group

• Nakilat Damen Shipyards

• GenCorp, Inc.

• Dassault Aviation SA

• Krauss-Maffei Wegmann GmbH

• Finmeccanica S.p.A.

Similar to Prime Contractors, Qatari procurement will increasingly diversify amongst various international manufacturers rather than rely primarily on the U.S. as it has historically

2011-21 Value

• $6.0B

• $5.8B

• $4.9B

• $1.9B

• $993M

• $839M

• $773M

• $720M

• $692M

• $663M

$-

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

$5,000

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Mill

ion

s

Lockheed Martin Boeing

Raytheon MBDA Missile Systems

Airbus Group Nakilat Damen Shipyards

GenCorp, Inc. Dassault Aviation SA

Krauss-Maffei Wegmann GmbH Finmeccanica S.p.A.

Contractor Not Yet Selected

PRIVATE & CONFIDENTIAL | AVASCENT | 9

Market Overview: Defense Platform OpportunitiesSimilar to Saudi Arabia, Qatar has ambitions to expand into the maritime domain, having largely recapitalized its airborne fleets through a series of recent acquisitions

Surface Vessels

Wheeled & Tracked

Combat Vehicles

Platform Opportunities (2016-2021)

Unmanned Aerial

Systems

Key:

$11M $1.5BSurface Vessels

Wheeled & Tracked Combat Vehicles $12M $250M

2016 Total 2016-21

Logistics Vehicles

Unmanned Aerial Systems $20M $212M

Logistics Vehicles $0M $118M

• Projected Amphibious Lift Ship

• Future Corvette

• Future Frigate

• Future Command Ship

• Wheeled Vehicles

• Ground Vehicle Projected Development

Market Segment Overview

• Future Tactical UAS System

• Logistics Equipment

• $500M

• $300M

• $200M

• $150M

• $139M

• $111M

• $100M

• $82M

2016-21 Value

$-

$100

$200

$300

$400

$500

$600

$700

$800

2016 2017 2018 2019 2020 2021

Mill

ion

s

Surface Vessels Wheeled & Tracked Combat Vehicles

Aircraft Technology Unmanned Aerial Systems

Logistics Vehicles Fixed Wing Aircraft

Submarines Rotorcraft

PRIVATE & CONFIDENTIAL | AVASCENT | 10

Market Overview: Defense Systems OpportunitiesExpansion into the naval domain will require significant investment in a C4I backbone, both in terms of standalone equipment and electronic systems embedded on surface platforms

C4I

Weapons

System Opportunities (2016-2021)

Sensors

Key:

$89M $463MC4I

Weapons $22M $445M

2016 Total 2016-21

Electronic Warfare

Sensors $38M $238M

Electronic Warfare (EW) $11M $223M

• Other C4I

• Network Equipment

• Communications Equipment

• Navigation Systems

• Ammunition

• Torpedoes & Weapon Support Equipment

• Guided Weapons

• Missiles

Market Segment Overview

• Radar Systems

• Other Sensors

• Sonar Systems

• Optical Systems

• RF-Based EW Systems

• EW Expendables

• Other EW/IW

• $138M

• $133M

• $114M

• $34M

• $169M

• $167M

• $50M

• $48M

• $97M

• $75M

• $33M

• $29M

• $30M

• $23M

• $23M

2016-21 Value

$-

$50

$100

$150

$200

$250

$300

$350

$400

2016 2017 2018 2019 2020 2021

Mill

ion

s

C4I Weapons Sensors EW Avionics

PRIVATE & CONFIDENTIAL | AVASCENT | 11

Discussion

Opaque organizational structure and the ubiquity of royal appointments to high-level positions can complicate the task of shaping requirements for foreign firms

Qatar Ministry of DefenseDecision-making remains opaque and largely controlled by the royal family, though a relatively well-established FMS process offsets this to some degree

Ministry of Defense Organizational Chart

Minister of Defense and Commander in Chief

Emir Sheikh Tamim bin Hamid al-Thani

Chief of General Staff & Commander of the Land Forces

Major General Ghanenbin Shaheed al-

Ghanem

Minister of State for Defense

Khalid bin Mohammed al-Attiyah

Commander of the Naval Forces

Commodore Mohamed Nasser al-Mohadani

Commander of the Air Forces

Brigadier General Mubarak Mohammed al-Kumait al-Khayarin

A recent cabinet reorganization ushered a new Minister of Defence into office in late 2015

The reshuffle appears to be a consolidation of several ministries, perhaps reflecting state adjustment to declines in energy prices and a push to trim bureaucracy

The decision-making process remains opaque and dominated largely by the royal family

PRIVATE & CONFIDENTIAL | AVASCENT | 12

Qatar Defense Summary

The country funds major purchases to address immediate requirements largely independent of economic factors, complicating sales that may be subjected to export restrictions

Defense planning is centered on a series of large near-term acquisitions rather than a formalized budgeting process

Qatar has no official offset policy, instead encouraging investment in research, development and education and complicating the bid and pursuit process

Qatar places a high value on its ability to quickly acquire defense materiel; this consideration has prompted an emphasis on maintaining relationships with a diverse range of suppliers

PRIVATE & CONFIDENTIAL | AVASCENT | 13

Regional threats increase O&M

─ The rise of violent extremist groups in Syria, Iraq, and Yemen, competition for oil, and unstable political leadership across the region pose imminent national security threats

─ Kinetic participation in conflicts in Yemen and Syria will continue to drive up spending on O&M, weapons, and personnel and increase spending linked to border protection

Reorganization prioritizes domestic industry, missile defense

─ Beginning in 2017, Saudi Arabia plans to refocus military resources on a nearly non-existent industrial base

─ Perceived threat, historical tensions, and relieved Western sanctions on nuclear Iran will push missile upgrades

US relationship wavers

─ The lifting of sanctions on Iran and increased US pressure on Saudi human rights violations threatens to impact a previously strong defense relationship

─ The Kingdom will continue to entertain non-US suppliers

Airborne Now, Maritime Soon

─ Saudi Arabia has spent billions of dollars on near term airborne platforms, most recently for 30 MH-60R helicopters

─ Spending patterns will shift towards maritime platforms in the out-years, led a multi-billion dollar surface combatant purchase from either Spain or the United States

Saudi Arabia:Modernization and threat environment drive defense spending

Budget Transparency Not

TransparentTransparent

Economic Outlook

Threat Environment and Spending DriversGDP & Defense Spending (millions USD)

Forecast Summary

Exchange Rate

3.75

Military participation in Yemen, major platform additions and upgrades, and perceived Iranian threat keep defense accounts high, although most requirements are being fulfilled

Conclusion of costly airborne acquisition programs and kinetic involvement in region will displace some procurement in favor of O&M; R&D will increase slightly as investment in domestic industry grows

GDP Growth

6.1%

Defense Growth

3.4%

Investment Growth

-0.5%

Defense Spending Outlook

Defense Accounts Outlook

Deputy Crown Prince Mohammed bin Salman announced sweepingplans – “Vision 2030”– to end the KSA’s reliance on oil through aglobal investment fund worth over $2 trillion and dramaticallyincreased domestic industrial investment

The plans will be difficult to implement, and the Kingdom will likelycontinue to be reliant on hydrocarbons into the foreseeable future

NOTE: GDP is drawn from the IMF and all figures are nominal; growth rates are for 2016-2021

$-

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

$90,000

$100,000

$-

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

$90,000

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Procurement R&D Personnel O&M GDP

PRIVATE & CONFIDENTIAL | AVASCENT | 14

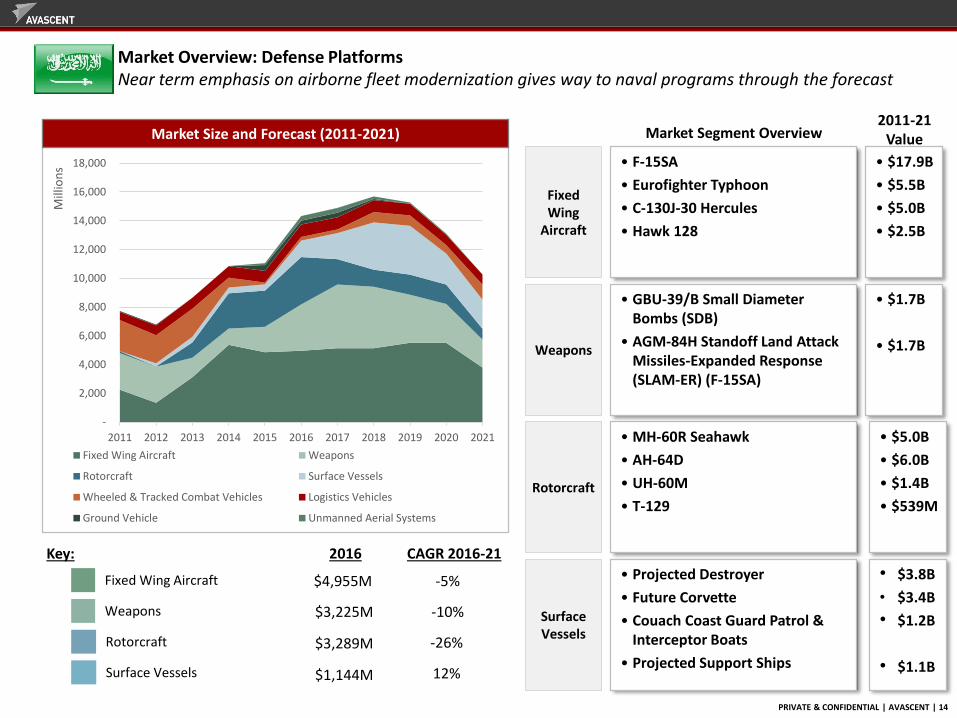

Market Overview: Defense PlatformsNear term emphasis on airborne fleet modernization gives way to naval programs through the forecast

• F-15SA

• Eurofighter Typhoon

• C-130J-30 Hercules

• Hawk 128

Fixed Wing

Aircraft

• GBU-39/B Small Diameter Bombs (SDB)

• AGM-84H Standoff Land Attack Missiles-Expanded Response (SLAM-ER) (F-15SA)

Weapons

Market Segment OverviewMarket Size and Forecast (2011-2021)

• MH-60R Seahawk

• AH-64D

• UH-60M

• T-129Rotorcraft

• Projected Destroyer

• Future Corvette

• Couach Coast Guard Patrol & Interceptor Boats

• Projected Support Ships

Surface Vessels

• $17.9B

• $5.5B

• $5.0B

• $2.5B

• $1.7B

• $1.7B

• $5.0B

• $6.0B

• $1.4B

• $539M

• $3.8B

• $3.4B

• $1.2B

• $1.1B

2011-21 Value

Key:

$4,955M -5%Fixed Wing Aircraft

Weapons $3,225M -10%

2016 CAGR 2016-21

Rotorcraft $3,289M -26%

Surface Vessels $1,144M 12%

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Mill

ion

s

Fixed Wing Aircraft Weapons

Rotorcraft Surface Vessels

Wheeled & Tracked Combat Vehicles Logistics Vehicles

Ground Vehicle Unmanned Aerial Systems

PRIVATE & CONFIDENTIAL | AVASCENT | 15

Market Overview: Defense SystemsHigh OPTEMPO as well as recent platform purchases drive robust demand for weapons systems

• Missiles

• Other Weapons Investment

• Ammunition

• Guided Weapons

• Gun Systems

Weapons

• Other C4I Equipment

• Communications Equipment

• Command & Control Equipment

• Network EquipmentC4I

Market Segment OverviewMarket Size and Forecast (2011-2021)

• Other Sensors

• Radar Systems

• Optical Systems

• Sonar SystemsSensors

Key:

$5,572M -11%Weapons

C4I $1,619M 19%

2016 CAGR 2016-21

• Other EW/Information Warfare

• RF-Based EW Systems

• Optical-Based EW Systems

• EW Expendables

Electronic Warfare

Sensors $1,356M 13%

Electronic Warfare (EW) $745M -1%

• $15.6B

• $13.9B

• $9.3B

• $4.0B

• $1.4B

• $14.5B

• $5.5B

• $2.7B

• $2.5B

• $10.9B

• $5.0B

• $4.2B

• $411M

• $2.9B

• $1.8B

• $1.1M

• $597M

2011-21 Value

$-

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Mill

ion

s

Weapons C4I Sensors EW Avionics

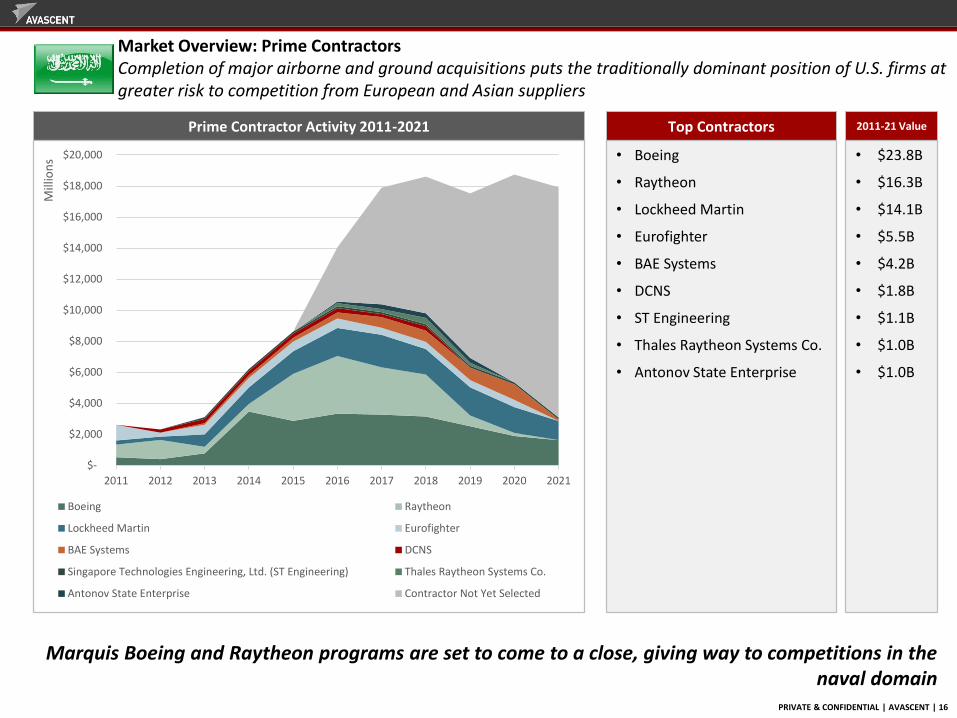

PRIVATE & CONFIDENTIAL | AVASCENT | 16

Prime Contractor Activity 2011-2021

Market Overview: Prime ContractorsCompletion of major airborne and ground acquisitions puts the traditionally dominant position of U.S. firms at greater risk to competition from European and Asian suppliers

Top Contractors

• Boeing

• Raytheon

• Lockheed Martin

• Eurofighter

• BAE Systems

• DCNS

• ST Engineering

• Thales Raytheon Systems Co.

• Antonov State Enterprise

Marquis Boeing and Raytheon programs are set to come to a close, giving way to competitions in the naval domain

2011-21 Value

• $23.8B

• $16.3B

• $14.1B

• $5.5B

• $4.2B

• $1.8B

• $1.1B

• $1.0B

• $1.0B

$-

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

$20,000

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Mill

ion

s

Boeing Raytheon

Lockheed Martin Eurofighter

BAE Systems DCNS

Singapore Technologies Engineering, Ltd. (ST Engineering) Thales Raytheon Systems Co.

Antonov State Enterprise Contractor Not Yet Selected

PRIVATE & CONFIDENTIAL | AVASCENT | 17

Subcontractor Activity 2011-2021

Market Overview: SubcontractorsThe top components manufacturers largely mirror the top prime contractors, owing to high value of structural components on airborne platforms

Top Contractors

• Boeing

• Lockheed Martin

• Raytheon

• BAE Systems

• U.S. Department of Defense

• Eurofighter

• Antonov State Enterprise

• DCNS

• Finmeccanica S.p.A.

• AVIC

Indigenous companies remain largely absent from the list of top components manufacturers as their focus is primarily in sustainment services

2011-21 Value

• $16.7B

• $13.3B

• $11.3B

• $4.6B

• $3.9B

• $2.3B

• $1.0B

• $965M

• $877M

• $800M

$-

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

$20,000

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Mill

ion

s

Boeing Lockheed Martin

Raytheon BAE Systems

U.S. Department of Defense (DoD) Eurofighter

Antonov State Enterprise DCNS

Finmeccanica S.p.A. Aviation Industry Corporation of China (AVIC)

Contractor Not Yet Selected

PRIVATE & CONFIDENTIAL | AVASCENT | 18

Market Overview: Defense Platform OpportunitiesSNEP II offers a bevy of naval modernization opportunities for Western suppliers

Surface Vessels

Weapons

Platform Opportunities (2016-2021)

Logistics Vehicles

Key:

$645M $10,948MSurface Vessels

Weapons $1,316M $10,461M

2016 Total 2016-21

Fixed Wing

AircraftLogistics Vehicles $0 $3,822M

Fixed Wing Aircraft $0 $2,249M

• Future Destroyer

• Future Corvette

• Projected Support Ship

• Replenishment Tanker

• Air Defense System

• Manportable Weapons

• Medium Laser Guided Bomb

• Naval PGM

Market Segment Overview

• Wheeled Vehicles

• Construction/Engineering Equipment

• Logistics Equipment

• Future Maritime Patrol Aircraft

• Eurofighter Typhoon

• Projected Medium Lift

• $3.9B

• $3.4B

• $1.0B

• $990M

• $1.9B

• $1.6B

• $1.2B

• $375M

• $2.3B

• $764M

• $764M

• $1.4B

• $1.2B

• $149M

2016-21 Value

$-

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

2016 2017 2018 2019 2020 2021

Mill

ion

s

Surface Vessels WeaponsLogistics Vehicles Fixed Wing AircraftMultiple Vehicles SubmarinesRotorcraft Wheeled & Tracked Combat VehiclesAirship/Aerostat Unmanned Maritime SystemsGround Systems Unmanned Aerial Systems

PRIVATE & CONFIDENTIAL | AVASCENT | 19

Market Overview: Defense Systems OpportunitiesOngoing operations drive demand for weapons systems as platform fleet recapitalization spurs the need to modernize the C4I backbone

Weapons

C4I

System Opportunities (2016-2021)

Sensors

Key:

$1,411M $14,241MWeapons

C4I $484M $10,852M

2016 Total 2016-21

Electronic Warfare

Sensors $292M $5,827M

Electronic Warfare (EW) $82M $1,381M

• Torpedoes & Weapon Support Equipment

• Ammunition

• Guided Weapons

• Gun Systems

• Other C4I Equipment

• Network Equipment

• Communications Equipment

• Combat Systems

Market Segment Overview

• Other Sensors

• Radar Systems

• Optical Systems

• Sonar Systems

• Other EW/IW

• RF-Based EW Systems

• EW Expendables

• Optical-Based EW Systems

• $7.0B

• $5.0B

• $1.6B

• $396M

• $5.9B

• $1.7B

• $1.7B

• $824M

• $3.7B

• $1.4B

• $405M

• $253M

• $696M

• $390M

• $268M

• $27M

2016-21 Value

$-

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

2016 2017 2018 2019 2020 2021

Mill

ion

s

Weapons C4I Sensors EW Avionics

PRIVATE & CONFIDENTIAL | AVASCENT | 20

Discussion

Saudi Arabia Ministry of DefenseDefense decisions are made via the royal family with direct connections to branches of the military

Government & MoD Organizational Chart (June 2016)

KingSalman bin Abdulaziz al Saud

Crown Prince Muhammad bin

Nayef

MoDMohammad bin Salman Al Saud

RSADFMohammed

Awad Asheim

MOFIbrahim bin

Abdulaziz bin Abdullah Al-Assaf

RSNFAbdullah bin

Sultan al-Sultan

RSLFEid bin Awad

Al-Shalawi

RSAFMohammed bin

Ahmed Alshaa'lan

SANGMutaib bin

Abdullah bin Abdulaziz Al Saud

MoD: Ministry of Defense, MOI: Ministry of Interior, MOF: Ministry of Finance, RSADF: Royal Saudi Air Defense Forces, RSNF: Royal Saudi Naval Forces, RSAF: Royal Saudi Air Force, RSLF: Royal Saudi Land Forces, SANG: Saudi Arabian National Guard, JCS: Joint Chiefs of Staff

JCSAbdul Rahman bin

Saleh Al Banyan

Council of Ministers

MOIMuhammad bin

Nayef

Through its long-standing FMS relationship and the existence of organizations within the DoD such as OPM SANG, U.S. firms are well positioned to navigate the Ministry decision-making process

The SANG is independent of the Saudi MoD, while the MoD and JCS control the traditional four branches of the military

The implications of a 2015 government reorganization that placed a new Defense Minister, with a broad writ outside the Ministry itself, into power remain unclear

Royal Court

PRIVATE & CONFIDENTIAL | AVASCENT | 21

Challenges

Trends

Saudi Arabia Offsets and Defense Policy

Offset Policy

The Saudi Economic Offset program (EOP) is administered through the Ministry of Defense

The EOP requires foreign manufacturers to invest 35% of a contract value in the Saudi economy within ten years of a contract signature

The majority of these agreements are indirect offsets to help diversify the oil-reliant economy

Invested in Saudi economy

35% 65%

Total Foreign OEM Contract Value

Notable Examples – Program and Offset Obligation

BAE- Al Yamamah I,II,III

1985-2006, $7B +

Peace Shield – 1985, $3.8B

Al-Sawary – 1990, $3B

According to Deputy Crown Prince Mohammed bin Salman, KSA wants to source 30-50% of defense procurement from local industry through the ‘Vision 2030 program(Currently, indigenous sourcing is at only 2%)

Although the U.S. prefers direct Foreign Military Sales (FMS), the DoD usually leaves offset negotiations to the private contractors involved with each deal

Foreign manufacturers can only enter the market by creating a joint venture with Saudi firms

Indirect offset agreements further weaken already minimal domestic industrial defense capabilities

Saudi Arabia tends to define requirements in terms of broad capabilities (“naval modernization”), slowing the evaluation and award process

PRIVATE & CONFIDENTIAL | AVASCENT | 22

Saudi Arabia Defense Summary

Regional threats from violent extremism and rising Iranian influence drive a significant defense budget

The US-brokered deal with Iran has hampered a historically strong defense relationship as the Kingdom has entertained non-US suppliers for a variety of recent and future requirements, particularly in the Navy and Air Force

35% offset requirement aids the growth of water, infrastructure, and other sectors but hinders development of indigenous defense industry

Diversification of the economy, increased reliance on local industry are key policy initiatives under the government’s Vision 2030 plan

PRIVATE & CONFIDENTIAL | AVASCENT | 23

Regional rivalry with Iran, involvement in Yemen pushes modernization and increased expenditure on munitions

– January 2016 award to Patria for undisclosed number of AMV’s, likely to meet standing requirement for 8X8 armored vehicles

– $350M contract signed in February at IDEX 2016 for 8 Piaggio P.1HH Hammerhead UAVs

– $617M contract signed at IDEX 2015 for two C-17 transport aircraft

– Failed bid for Mistral-class amphibious assault ships signals a new level of heightened maritime investment and plans for the future

Air defense systems still significant portion of yearly spending...

– Present levels of spending still heavily influenced by older buys of Patriot PAC-3 systems and missiles (est. cost of $2.45B), Pantsir S-1 system (est. cost $800M), and Terminal High Altitude Area Defense system and its interceptors (est. cost of over $6B total)

– The “Diamond Shield” air defense system is still being developed and integrated for an estimated $510M.

… in addition to combat aircraft and associated armament

– 25 F-16 Block 60 aircraft ordered for approximately $4B in 2014

– Remains uncertain whether this will affect the current Fourth Generation Fighter competition, where talks remain stalled

– Fourth Generation Fighter contract award still outstanding, though talks with Dassault have resumed as of April 2015

United Arab Emirates:Regional security pressures drive increases in military expenditure

Budget Transparency Not

TransparentTransparent

Economic Outlook

Threat Environment and Spending DriversGDP & Defense Spending (millions USD)

Forecast Summary

Exchange Rate

3.67

Existing major purchases keep spending high in the near term, but modernization efforts will form the basis of steady out-year spending absent new and unforeseen major procurement efforts

Procurement high to cover past purchases, but O&M and personnel accounts will rise and dwarf nascent R&D account as new acquisitions age;

GDP Growth

8.2%

Defense Growth

5.2%

Investment Growth

1.3%

Defense Spending Outlook

Defense Accounts Outlook

Heavy investment in infrastructure in recent years paying off as the country diversifies and grow its economy outside the scope of hydrocarbons and financial services

The economy is still particularly sensitive to fluctuations in hydrocarbon prices, which directly impact revenue from its dominant energy export sector and, subsequently, the defense budget

NOTE: GDP is drawn from the IMF and all figures are nominal; growth rates are for 2016-2021

$-

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

$450,000

$500,000

$-

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Procurement R&D Personnel O&M GDP

PRIVATE & CONFIDENTIAL | AVASCENT | 24

Market Overview: Defense PlatformsHeavy investment in military modernization boosts aircraft in short term and naval opportunities in future

• F-16

• Future Fighter Aircraft

• Saab AEW&C Aircraft

• Projected Manned ISR Aircraft

Fixed Wing

Aircraft

• Patria AMV

• MaxxPro MRAPs

• Wheeled Vehicles

• Projected Main Battle Tank

Wheeled & Tracked

Combat Vehicles

Market Segment OverviewMarket Size and Forecast (2011-2021)

• Future Medium to Heavy Lift

• CH-47F

• Projected ASW Helicopter

• AW139Rotorcraft

Key:

$1,559M 7%Fixed Wing Aircraft

Wheeled & Tracked Combat Vehicles $1,156M 6%

2016 CAGR 2016-21

• Projected Support Ship

• Falaj-2 (Batch II)

• Amphibious Lift Ship

• Projected Destroyer

Surface Vessels

Rotorcraft $615M -16%

Surface Vessels $314M 16%

• $4.3B

• $1.8B

• $1.4B

• $1.1B

• $2.3B

• $1.5B

• $1.0B

• $938M

• $1.3B

• $640M

• $200M

• $100M

• $300M

• $272M

• $250M

• $250M

2011-21 Value

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Mill

ion

s

Fixed Wing Aircraft Wheeled & Tracked Combat Vehicles

Rotorcraft Surface Vessels

Logistics Vehicles Submarines

Unmanned Aerial Systems Weapons

PRIVATE & CONFIDENTIAL | AVASCENT | 25

Market Overview: Defense SystemsSignificant investment in weapons and AMD boosts drives market for weapons components and C4I electronic systems

• Missiles

• Guided Weapons

• Torpedoes & Weapon Support Equipment

• Ammunition

Weapons

• Communications Equipment

• Other C4I Equipment

• Network Equipment

• Combat SystemsC4I

Market Segment OverviewMarket Size and Forecast (2011-2021)

• Radar Systems

• Other Sensors

• Optical Systems

• Sonar SystemsSensors

Key:

$1,677M -12%Weapons

C4I $970M 0%

2016 CAGR 2016-21

• RF-Based EW Systems

• Optical-Based EW Systems

• Other EW/Information Warfare

• EW Expendables

Electronic Warfare

Sensors $427M 5%

Electronic Warfare (EW) $203M 6%

• $4.3B

• $1.9B

• $1.8B

• $930M

• $1.8B

• $1.3B

• $1.2B

• $942M

• $1.3B

• $1.0B

• $487M

• $62M

• $629M

• $374M

• $237M

• $152M

2011-21 Value

$-

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Mill

ion

s

Weapons C4I Sensors EW Avionics

PRIVATE & CONFIDENTIAL | AVASCENT | 26

Prime Contractor Activity 2011-2021

Market Overview: Prime ContractorsUAE market shows preference toward Western suppliers which is likely to continue into the future due to their desire for advanced, top-of-the-line platforms and systems

Top Contractors

• Lockheed Martin

• Raytheon

• Boeing

• Government Agency*

• Patria Oyj

• Navistar International

• BAE Systems

• Saab AB

• Denel (Pty.) Ltd.

• Tawazun

* “Government Agency” denotes costs borne by the government which are associated with a program – in this case directly related to FMS – which are unaddressable by contractors

Preference for Western systems and platforms evident across existing sales

2011-21 Value

• $14.1B

• $3.9B

• $3.6B

• $2.4B

• $2.3B

• $1.7B

• $1.5B

• $1.4B

• $1.1B

• $776M

$-

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Mill

ion

s

Lockheed Martin Raytheon Boeing

Government Agency Patria Oyj Navistar International

BAE Systems Saab AB Denel (Pty.) Ltd.

Tawazun Contractor Not Yet Selected

PRIVATE & CONFIDENTIAL | AVASCENT | 27

Subcontractor Activity 2011-2021

Market Overview: SubcontractorsUAE market shows preference toward Western suppliers which is likely to continue into the future due to their desire for advanced, top-of-the-line platforms and systems

Top Contractors

• Lockheed Martin

• Raytheon

• BAE Systems

• Boeing

• Navistar International

• Tawazun

• Finmeccanica S.p.A.

• Saab AB

• Patria Oyj

• Government of UAE

Preference for Western systems and platforms evident across existing sales and likely to continue

2011-21 Value

• $10.1B

• $4.0B

• $2.0B

• $1.9B

• $1.7B

• $1.6B

• $1.6B

• $1.4B

• $1.2B

• $682M

$-

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Mill

ion

s

Lockheed Martin Raytheon BAE Systems

Boeing Navistar International Tawazun

Finmeccanica S.p.A. Saab AB Patria Oyj

Government of UAE Contractor Not Yet Selected

PRIVATE & CONFIDENTIAL | AVASCENT | 28

Market Overview: Defense Platform OpportunitiesNear-term opportunities dominated by aircraft, ground vehicles, while naval modernization looms on horizon

Fixed Wing

Aircraft

Wheeled & Tracked

Combat Vehicles

Platform Opportunities (2016-2021)

Weapons

Key:

$120M $4,359MFixed Wing Aircraft

Wheeled & Tracked Combat Vehicles $38M $2,488M

2016 Total 2016-21

RotorcraftWeapons - Airborne $25M $1,993M

Rotorcraft $100M $1,499M

• Future Multirole Fighter Aircraft

• Projected Multi-Mission ISR Aircraft

• Medium Transport Aircraft

• Future Trainer Aircraft

• Other/Multiple Vehicles

• Projected Main Battle Tank

• Future Wheeled Armored Vehicles

• Wheeled and Tracked Combat Vehicles

Market Segment Overview

• Air-to-Ground Missile

• Short Range Air-to-Air Missile

• Beyond Visual Range Air-to-Air Missile

• Fixed Wing Aircraft Weapon

• Future Medium Utility Helicopter

• Projected ASW Helicopter

• $1.8B

• $1.1B

• $500M

• $360M

• $867M

• $650M

• $324M

• $298M

• $700M

• $480M

• $337M

• $300M

• $1.3B

• $200M

2016-21 Value

$-

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

2016 2017 2018 2019 2020 2021

Mill

ion

s

Fixed Wing Aircraft Wheeled & Tracked Combat Vehicles

Weapons Rotorcraft

Surface Vessels Unmanned Aerial Systems

Submarines Logistics Vehicles

Unmanned Maritime Systems Unmanned Ground Systems

PRIVATE & CONFIDENTIAL | AVASCENT | 29

Market Overview: Defense Systems OpportunitiesWeapons buys in support of new aircraft purchases spike otherwise smooth growth across variety of platforms and systems, though C4I otherwise dominates

Weapons

C4I

System Opportunities (2016-2021)

Sensors

Key:

$104M $3,655MWeapons

C4I $201M $3,325M

2016 Total 2016-21

Electronic Warfare

Sensors $166M $1,947M

Electronic Warfare $40M $695M

• Missiles

• Other Weapons Investment

• Ammunition

• Guided Weapons

• Gun Systems

• Other C4I Equipment

• Communication Equipment

• Networking Equipment

• Combat Systems

Market Segment Overview

• Other Sensors

• Radar Systems

• Optical Systems

• Sonar Systems

• RF-Based EW Systems

• Other EW/Information Warfare

• EW Expendables

• Optical-Based EW Systems

• $1.9B

• $1.0B

• $572M

• $146M

• $64M

• $1.3B

• $675M

• $674M

• $274M

• $1.0B

• $673M

• $202M

• $45M

• $266M

• $237M

• $104M

• $87M

2016-21 Value

$-

$500

$1,000

$1,500

$2,000

$2,500

$3,000

2016 2017 2018 2019 2020 2021

Mill

ion

s

Weapons C4I Sensors EW Avionics

PRIVATE & CONFIDENTIAL | AVASCENT | 30

Opaque organizational structure obscures key levers in procurement process

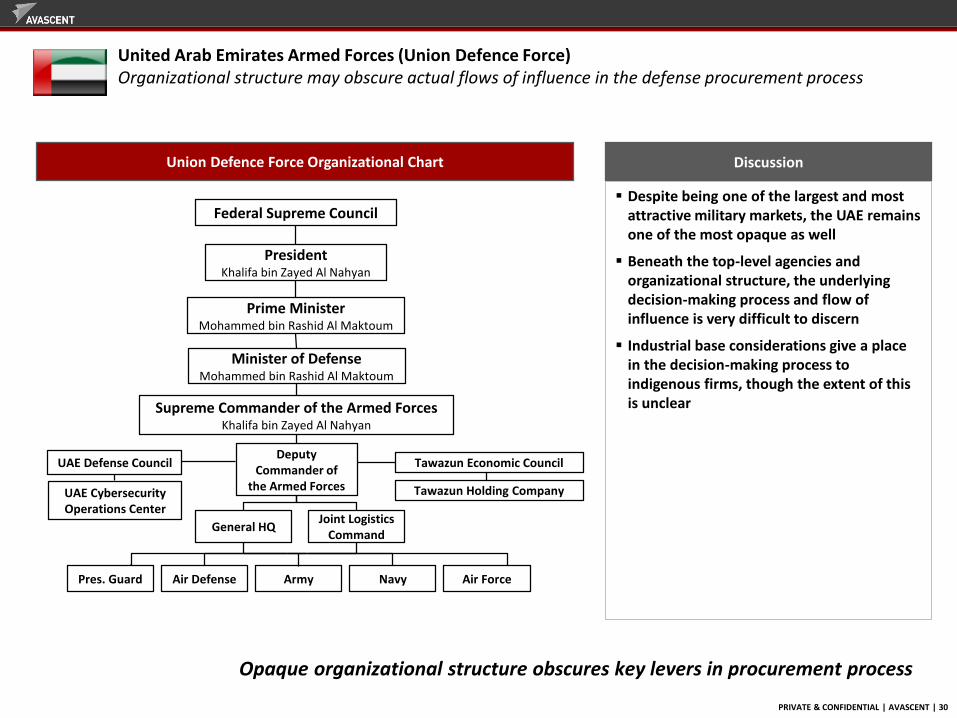

United Arab Emirates Armed Forces (Union Defence Force)Organizational structure may obscure actual flows of influence in the defense procurement process

Army Navy Air ForceAir DefensePres. Guard

General HQJoint Logistics

Command

Deputy Commander of

the Armed Forces

UAE Defense Council

UAE Cybersecurity Operations Center

Tawazun Holding Company

Supreme Commander of the Armed ForcesKhalifa bin Zayed Al Nahyan

Minister of DefenseMohammed bin Rashid Al Maktoum

Prime MinisterMohammed bin Rashid Al Maktoum

PresidentKhalifa bin Zayed Al Nahyan

Federal Supreme Council

DiscussionUnion Defence Force Organizational Chart

Despite being one of the largest and most attractive military markets, the UAE remains one of the most opaque as well

Beneath the top-level agencies and organizational structure, the underlying decision-making process and flow of influence is very difficult to discern

Industrial base considerations give a place in the decision-making process to indigenous firms, though the extent of this is unclear

Tawazun Economic Council

PRIVATE & CONFIDENTIAL | AVASCENT | 31

Discussion

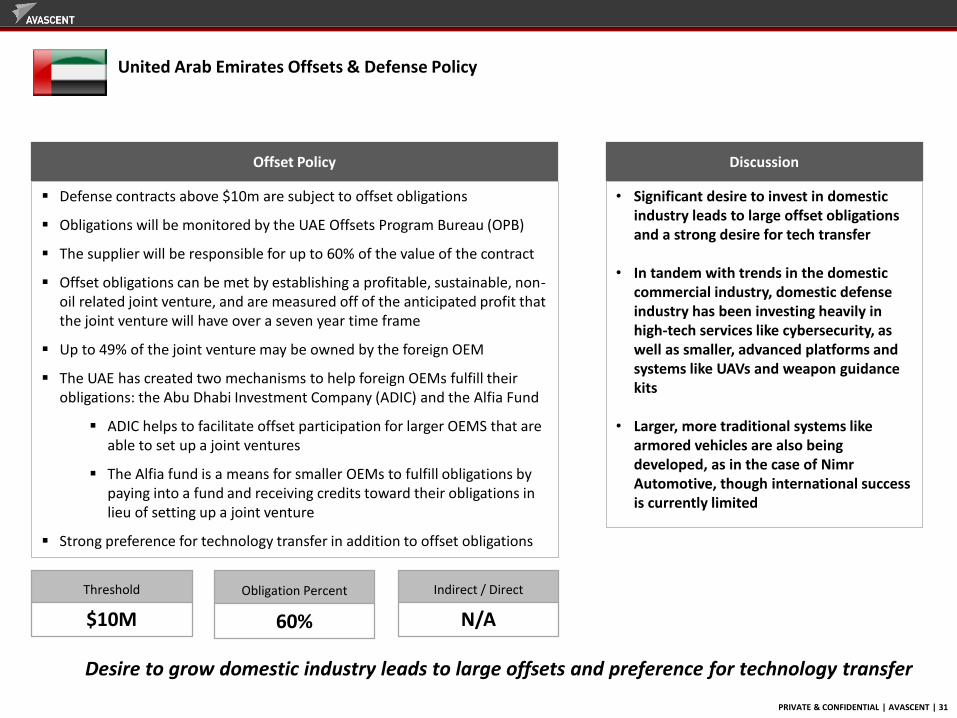

Desire to grow domestic industry leads to large offsets and preference for technology transfer

United Arab Emirates Offsets & Defense Policy

Offset Policy

Defense contracts above $10m are subject to offset obligations

Obligations will be monitored by the UAE Offsets Program Bureau (OPB)

The supplier will be responsible for up to 60% of the value of the contract

Offset obligations can be met by establishing a profitable, sustainable, non-oil related joint venture, and are measured off of the anticipated profit that the joint venture will have over a seven year time frame

Up to 49% of the joint venture may be owned by the foreign OEM

The UAE has created two mechanisms to help foreign OEMs fulfill their obligations: the Abu Dhabi Investment Company (ADIC) and the Alfia Fund

ADIC helps to facilitate offset participation for larger OEMS that are able to set up a joint ventures

The Alfia fund is a means for smaller OEMs to fulfill obligations by paying into a fund and receiving credits toward their obligations in lieu of setting up a joint venture

Strong preference for technology transfer in addition to offset obligations

Threshold

$10M

Obligation Percent

60%

Indirect / Direct

N/A

• Significant desire to invest in domestic industry leads to large offset obligations and a strong desire for tech transfer

• In tandem with trends in the domestic commercial industry, domestic defense industry has been investing heavily in high-tech services like cybersecurity, as well as smaller, advanced platforms and systems like UAVs and weapon guidance kits

• Larger, more traditional systems like armored vehicles are also being developed, as in the case of NimrAutomotive, though international success is currently limited

PRIVATE & CONFIDENTIAL | AVASCENT | 32

United Arab Emirates Defense Summary

Small, very well-equipped military relies on high-end purchases as force multipliers

Heavy investment in recent military modernization made for large, varied purchases across a number of high profile platforms and systems (F-16, THAAD, PATRIOT, Patria AMVs, MaxxPro)

Procurement decision-making process tends to be opaque and relationship-based, complicating market entry for new suppliers

Clear preference for western systems and platforms makes the UAE an attractive customer and provides a modest advantage in dealing with their government

PRIVATE & CONFIDENTIAL | AVASCENT | 33

AppendixThe slides that follow describe the methodology employed in collecting the

underlying market data and offer definitions of the market categories depicted in the “Defense Systems” slides; more granular definitions and representative

examples are available by request

PRIVATE & CONFIDENTIAL | AVASCENT | 34

Top Down and Bottom-up Analysis: Avascent places a detailed bottom-up build of defense procurement in international markets in the context of budget realities

$-

$1

$2

$3

$4

$5

$6

$7

$8

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Bill

ion

s

Awarded Stated Opportunity Projected Opportunity

Projected White Space Investment Topline

1

2

3

4

5

First, Avascent identifies the sum of the R&D and Procurement accounts to use as a bounding function for the bottom-up analysis

Next, the build of Awardedprograms looks at acquisitions that are in progress or that will not be competed

Third, Avascent looks at government documents and statements to identify Stated Opportunities that will be competed

Fourth, Avascent uses gap analysis, life expectancy, and other factors to derive Projected Opportunities that do not reflect a gov’t statement

Finally, the delta between identified spending and the topline is Shapeable Opportunity Space not associated with a requirement

Example: Composition of Defense Investment in Brazil by Opportunity Type Relative to the Procurement and R&D topline

PRIVATE & CONFIDENTIAL | AVASCENT | 35

Platform and System-Level Analysis: Avascent disaggregates spending on acquisition programs to allow for analysis at the level of the major sub-system, integrated platform, or total program

Eurofighter Typhoon

Omani Air Force

$3.8 billion

12 Units to be delivered between 2017 and 2024

Initial Services

$1.2 billion

Total Hardware Cost

$2.6 billion

Training and Support

$257 million

Installation and Fielding

$902 million

Airframe and Structures

$1.1 billion

CAPTOR-E Radar

$227 million

Passive IR Tracking

$136 million

Mission Computers

$90 million

Praetorian Defensive Aid

$113 million

Other Systems

$588 million

Total Program

Integrated Platform

Major Sub-System

PRIVATE & CONFIDENTIAL | AVASCENT | 36

Ground Systems*

Theater Deployable

Tactical/Mobile

Strategic Weapons

Enterprise Fixed

0Manportable

ManportableSystems

Satellites &Launch Vehicles

Space Range Systems

Launch Vehicles

Space Vehicles

Other Systems

Robotics Technology

Multiple Systems

Other

Airborne

Unmanned Aerial Systems

Rotorcraft

Fixed Wing Aircraft

Airship/Aerostat

Aircraft Technology

Multiple Aircraft

• Combat UAS• MALE/HALE• Man-Portable UAS• Other/Various UAS• Tactical UAS• Target Drone• VTOL UAS

• Attack/Armed Reconnaissance

• Maritime• Multiple Rotorcraft• Other Rotorcraft• Utility/Multi-Role

• Fighter/Attack/Bomber• ISR/EW/Special Mission• Mobility Aircraft• Other/Multiple Aircraft• Special Operations• Trainer Aircraft

Ground Vehicle

Logistics Vehicle

Unmanned Ground Systems

Multiple Vehicles

Ground Vehicle Technology

Wheeled & Tracked Combat Vehicles

• Other/Multiple Vehicles• Tracked Vehicles• Wheeled Combat /

Support Vehicles

Maritime

Surface Vessels

Submarines

Multiple Ships

Ship Technology

Unmanned Maritime Systems

• Aircraft Carrier• Amphibious Landing• Logistics/Sealift• Mine Warfare Vessel• Other Vessels• Patrol/Missile Boats• Surface Combatants• Multiple Vessels

Weapons

Maritime

Ground Vehicle

Manportable

Other Systems

Ground Systems*

Airborne

• Multiple Ships• Submarines• Surface Vessels

• Multiple Vehicles• Wheeled & Tracked Combat

Vehicles

• Enterprise Fixed• Strategic Weapons• Tactical/Mobile• Theater Deployable

• Fixed Wing Aircraft• Multiple Aircraft• Rotorcraft

• Multiple Systems

Platform Type Taxonomy

*Unlike Ground Vehicles, Ground Systems are immobile systems or fixed systems

PRIVATE & CONFIDENTIAL | AVASCENT | 37

SECTOR OVERVIEW: C4I

C4I EW/IW Platforms Sensors Weapons

Combat Systems

Airborne CombatSystems

Ship CombatSystems

Ground CombatSystems

Integrated C4ISystems

IntelligenceSystems

Tactical Systems

Strategic Systems

Communications

Line of Sight (LOS)

Beyond Line ofSight (BLOS)

Space Payloads

IntegratedDeployable Comms

C4I Networks

Fixed C4IInfrastructure

Commodity ITResources (C4I)

Security/Encryption

C4I IA

Other C4I

Flight Control &Cockpit Avionics

Other VehicleElectronics

Other C4I Systems

C4I S&T

Perimeter Security

Other ShipElectronics

Unallocated C4I

N/A

Command & Control (C2)

C2 Systems

IFF Systems

Combat ID

Positioning &Navigation Systems

Air TrafficControl Systems

Ground ControlSystems

Weather Systems

Logistics

Training Systems

Fire Control Systems

PRIVATE & CONFIDENTIAL | AVASCENT | 38

C4I

Networks

• Systems that form the network infrastructure of the DoD Enterprise

• Systems in this segment may be closely related to other systems found under Communications, but the emphasis in Network infrastructure is on fixed systems geared towards enterprise-wide uses rather than mission uses

C4I Sector

Communications

• Systems used to transmit, receive and disseminate voice, video and data

• Systems in this segment may be closely related to other systems found under Network Infrastructure, but the emphasis in Communications is on deployable and/or mobile systems geared toward warfighting and combat support activities

Other C4I

• Includes all other programs that do not directly fit into a separate category of analysis

Intelligence Systems

• Systems used to display, organize, manipulate and disseminate intelligence information

• Intelligence Systems may exist at either tactical or strategic levels

• Includes systems geared toward tasking, processing, exploitation, dissemination functions

Command & Control (C2)

• Systems used to display, organize, and manipulate information for purposes of decision support and execution

Combat Systems

• Integrated C4I systems on platforms (e.g. AWACS) or larger weapon systems (e.g. Aegis)

Sector Segment Segment Definition

SEGMENT DEFINITIONS: C4I

PRIVATE & CONFIDENTIAL | AVASCENT | 39

RF-Based EWSystems

ECM Systems

Radar WarningReceivers (RWR)

ESM Systems

EA & JammingSystems

Optical-Based EWSystems

Laser WarningReceiver

EO/IR Jammer

Missile WarningReceivers

Integrated EO/IREW System

Information Warfare

InformationOperations

Other EW/IW

Airborne HFI

EW S&T

IW S&T

Unallocated EW/IW

EW Expendables

Chaff

Flares

CountermeasureDispenser

Decoys & SmartExpendables

C4I EW/IW Platforms Sensors Weapons N/A

SECTOR OVERVIEW: ELECTRONIC WARFARE / INFORMATION WARFARE (EW/IW)

PRIVATE & CONFIDENTIAL | AVASCENT | 40

Other EW/IW

• Includes all other EW/IW funding that does not fit into the other segments

• Includes Airborne Hostile Fire Indicator, and EW/IW S&T

EW/IW

Information Warfare

• Systems used to create information-related effects, including for psychological operations, civil affairs, disinformation, and other purposes

RF-Based EW Systems

• Systems that detect and in some cases counter RF-based systems or threats

• Includes Radar Warning Receivers, ECM, ESM, and Jamming systems

Optical-Based EW Systems

• Systems used to detect and in some cases counter EO/IR based systems

• Includes Laser Warning Receiver, Missile Warning Receiver, EO/IR Jammer

EW Expendables

• Expendables including, chaffs, flares, countermeasure dispenser, decoys and smart expendables

Sector Segment Segment Definition

SEGMENT DEFINITIONS: EW/IW

PRIVATE & CONFIDENTIAL | AVASCENT | 41

Power & Propulsion

Integration ArmorBasic

ConstructionPlatform Services

Other Platform

Turbofan &Turbojet Engines

Turboprop &Turboshaft Engines

Gas/Diesel Engines

Vehicle Transmissions

Platform Integration

Power &Propulsion S&T

Nuclear Power

Rocket Motors

Electric &Hybrid Electric

Auxiliary Power Unit

Tactical MobilePower Generation

ManportablePower

Other Propulsion

Reactive Armor

Passive Armor

Airframe

Active ProtectionSystems

Body Armor

Armor S&T

Administration &Management

Engineering SupportServices

Installation &Fielding

Training

Initial Spares

Training Systems& Simulators

Ejection Seats

CBRNE Equipment

Other SupportEquipment

Other Platform S&T

Other PlatformElectronics

UnallocatedPlatforms

Vehicle Frame

Hull

Satellite Bus

Space LaunchAssembly

Construction &Material S&T

C4I EW/IW Platforms Sensors Weapons N/A

SECTOR OVERVIEW: PLATFORMS*

*The Platform segmentation outlined in this section serves the purpose of breaking out non-electronic platform related value

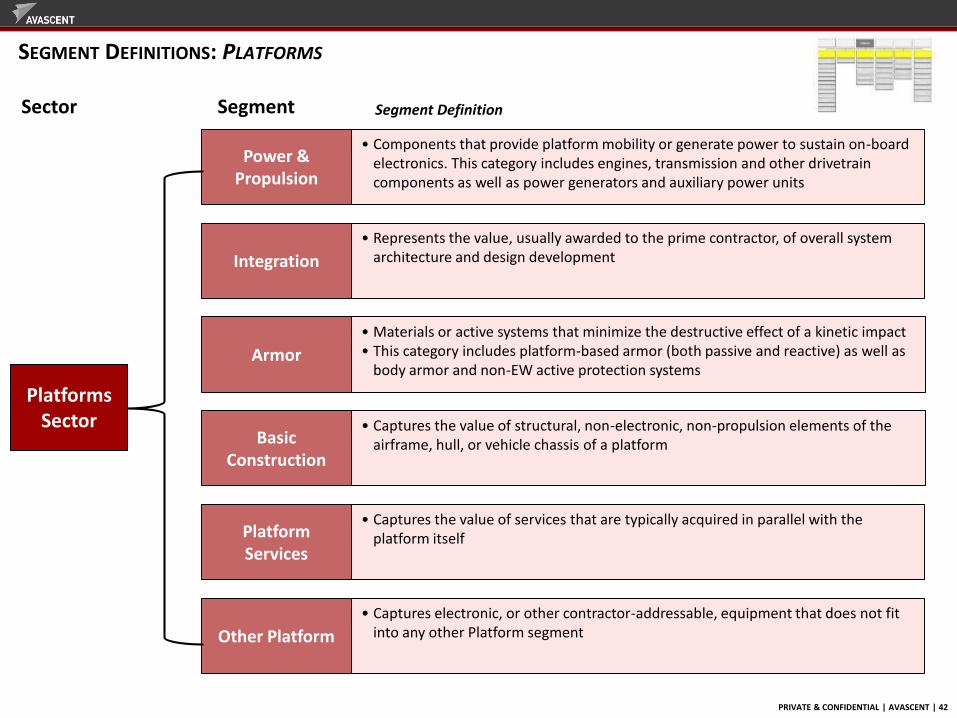

PRIVATE & CONFIDENTIAL | AVASCENT | 42

PlatformsSector

Platform Services

• Captures the value of services that are typically acquired in parallel with the platform itself

Power & Propulsion

• Components that provide platform mobility or generate power to sustain on-board electronics. This category includes engines, transmission and other drivetrain components as well as power generators and auxiliary power units

Integration

• Represents the value, usually awarded to the prime contractor, of overall system architecture and design development

Basic Construction

• Captures the value of structural, non-electronic, non-propulsion elements of the airframe, hull, or vehicle chassis of a platform

Armor

• Materials or active systems that minimize the destructive effect of a kinetic impact• This category includes platform-based armor (both passive and reactive) as well as

body armor and non-EW active protection systems

Other Platform

• Captures electronic, or other contractor-addressable, equipment that does not fit into any other Platform segment

Sector Segment Segment Definition

SEGMENT DEFINITIONS: PLATFORMS

PRIVATE & CONFIDENTIAL | AVASCENT | 43

Optical Systems

Radar Systems Sonar SystemsSIGINT

SystemsPortable Unmanned

SystemsOther Sensors

Night Vision

Laser Surveillance& Targeting

EO/IR Surveillance& Targeting

Optical SatellitePayload

Ground Detection& Targeting

Airborne Fire Control

Counter-Battery

Air & MissileDefense RadarsAirborne Early

Warning

Navigation

Air TrafficControl Radars

Space Surveillance

Meteorology

Mine/IED Detection

Airborne SonarSystems

Ship/Sub SonarSystems

SIGINT Systems

Optical S&T

Sonobuoys

Sonar S&T

UnattendedGround Sensors

Portable UAS

Small UGVs

MaritimeSurveillance

Non-Acoustic ASW

CBRNE Detection

Other Mine/IEDDetection

Multi-SensorSystems

Other AcousticSensors

Other Sensor S&T

Unallocated Sensors

Radar S&T

Integrated EO/Laser/IR Systems

C4I EW/IW Platforms Sensors Weapons N/A

SECTOR OVERVIEW: SENSORS

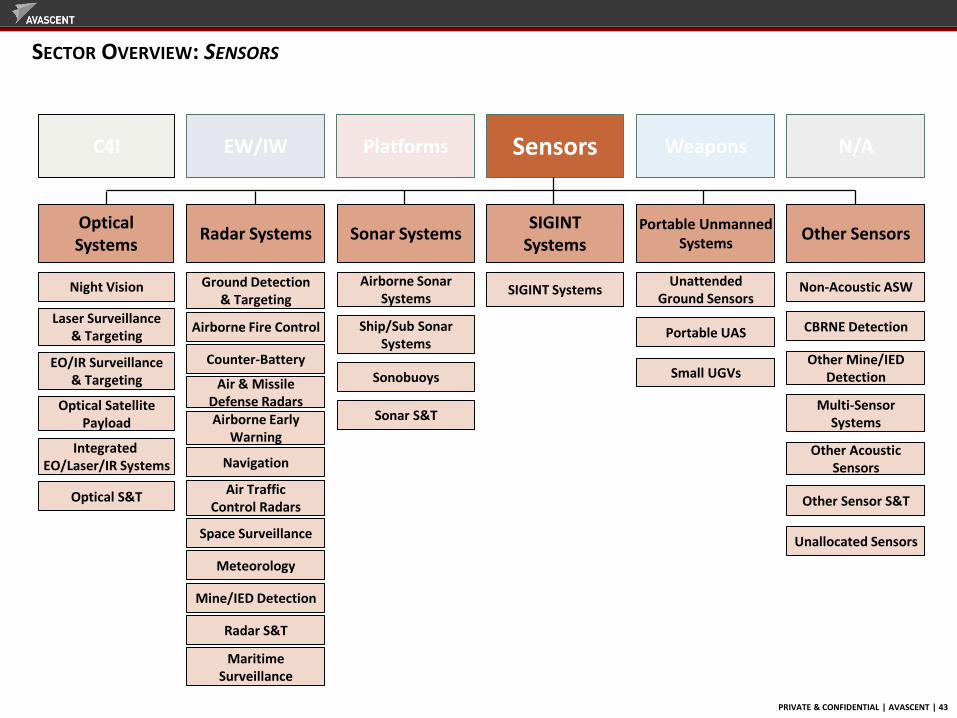

PRIVATE & CONFIDENTIAL | AVASCENT | 44

Other Sensors

• Includes a variety of systems that do not clearly fit within any of the other sub-segments• CBRNE Detection• Multi-Sensor Systems and sensor integration/fusion efforts• S&T on sensor technology that cannot be attributed to specific phenomenologies

SensorsSector

PortableUnmanned

Systems

• Small, man-portable platforms equipped with sensors that have the sole mission of surveillance and reconnaissance

Optical Systems

• Electro-optical cameras used for surveillance and reconnaissance, navigation, night vision enhancement, targeting and fire control, and vehicle self-protection

• Laser systems used for fire control and target acquisition

RadarSystems

• Radar systems of nearly any function or mission

• Radar altimeters may be encompassed within C2-Naviation Systems

SIGINTSystems

• Systems used for the detection, identification, and exploitation of RF signals for intelligence purposes

SonarSystems

• Acoustic systems for navigation, communication, or detection of objects beneath the surface of the water

• Includes both active and passive sonar systems

Sector Segment Segment Definition

SEGMENT DEFINITIONS: SENSORS

PRIVATE & CONFIDENTIAL | AVASCENT | 45

MissilesGuided

WeaponsDirected Energy

Gun Systems AmmunitionOther Weapons

Investment

Air-to-Ground

Air-to-Air

Anti-Ship

Air & MissileDefense Interceptors

Air-to-GroundPrecision Munitions

Precision Artillery& Mortar

Guided WeaponS&T

DE S&T

Anti-Radiation

Strategic Weapons

Land AttackTactical Missiles

Close CombatTactical Missiles

BMD SE&I

Missile S&T

Lethal

Non-Lethal

Airborne GunSystems

Artillery/TankGun Systems

Other VehicleWeapon Systems

Naval GunSystems

Large Caliber

Small Caliber(.50cal and below)

Ammunition S&T

Small Arms

Torpedoes &Equipment

Non-Lethal Weapons(Non-Directed Energy)

Unguided Bombs

EOD & Countermine/ IED Equipment

Targets

Weapon SupportEquipment

Mines

Gun Systems S&T

Unallocated Weapons

Vehicle ActiveProtection Systems

Other Weapon S&T

C4I EW/IW Platforms Sensors Weapons N/A

SECTOR OVERVIEW: WEAPONS

PRIVATE & CONFIDENTIAL | AVASCENT | 46

WeaponsSector

Ammunition• Ammunition for both small (less than 12.5mm / .50cal) and large-caliber

(20mm+) weapons. Includes ammunition for mortars and artillery, but excludes smart ammunition and/or guided munitions (e.g. EXCALIBUR)

Guided Weapons• Includes precision weapons that do not have organic propulsion• Precision guided bombs and precision artillery projectiles

Gun Systems• Large gun systems which are integrally tied to a platform

Directed Energy• Includes both lethal and non-lethal directed energy systems

Other Weapons Investment

• A catch-all category to house specific sub-segments that do not adhere to dynamics relevant to other Weapons market segments

Missiles• Self -propelled guided weapons, fired from multiple platforms, against a variety

of targets

Sector Segment Segment Definition

SEGMENT DEFINITIONS: WEAPONS