july 2017 council deck

TRANSCRIPT

PROPANE EDUCATION & RESEARCH COUNCILDENVER, COLORADO

July 11-12, 2017

CHAIRMAN’S REPORT

Drew Combs

INDUSTRY OUTREACH COMMITTEE REPORT

Bob Barry

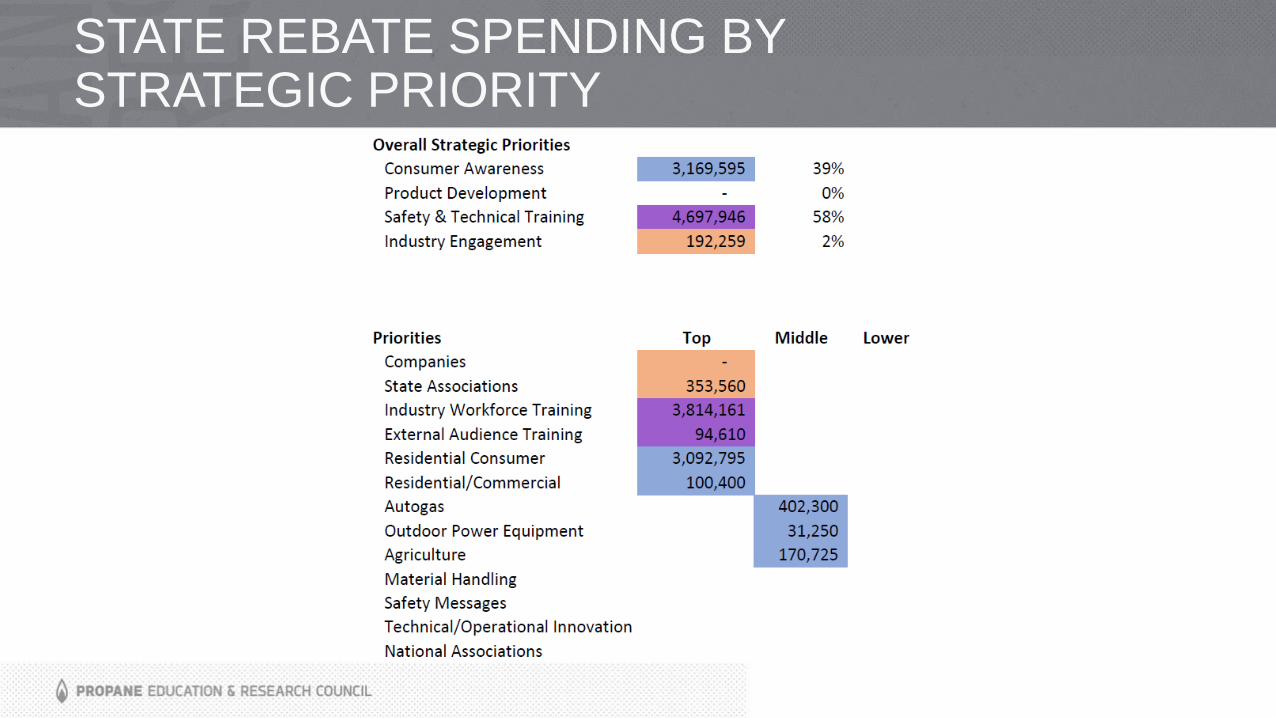

STATE REBATE SPENDING BY STRATEGIC MATRIX

STATE REBATE SPENDING BY STRATEGIC PRIORITY

AUDIT COMMITTEE REPORT

Gene Bissell

ADVISORY COMMITTEE REPORT

Bruce MontroyChairman, Safety & Training Working Group

NPGA REPORT

Chris Earhart

GPA MIDSTREAM REPORT

Mark Sutton

CHAIRMAN’S COMMENTS

TREASURER’S REPORT

Randy Doyle

REPORT AGENDA

• April Financial Summary and Variance Analysis

• 2017 Forecast and Variance Analysis• At current assessment rate

• At proposed .5 cent assessment rate (October 1, 2017)

• 2017 Cash Flow Projected Balances • At current and proposed assessment rate

• Investment Performance

2017 BUDGET VS ACTUALS AS OF APRIL 30, 2017

Category 2017 Budget 2017 Actuals Variance

Revenue $16,076,169 $14,489,604 ($1,586,565)

Carry-Forward $2,630,737 $1,297,939 ($1,332,798)

Spending ($26,508,516) ($26,133,680) ($374,836)

NET BUDGET ($10,429,347) ($11,644,076) ($1,961,421)

Deobligations $500,000 $1,646,075 $1,146,075

SURPLUS ($7,243,610) ($8,688,307) ($1,444,698)

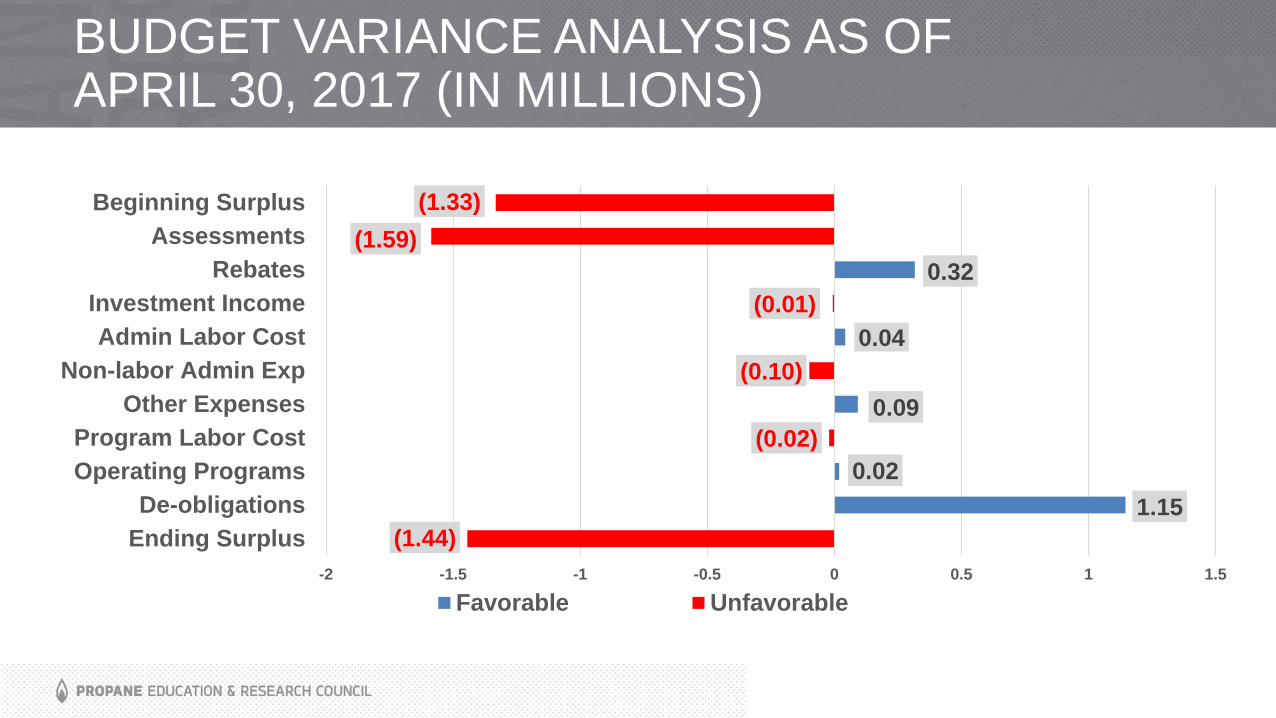

BUDGET VARIANCE ANALYSIS AS OF APRIL 30, 2017 (IN MILLIONS)

1.15

0.02

0.09

0.04

0.32

(1.44)

(0.02)

(0.10)

(0.01)

(1.59)

(1.33)

-2 -1.5 -1 -0.5 0 0.5 1 1.5

Ending Surplus

De-obligations

Operating Programs

Program Labor Cost

Other Expenses

Non-labor Admin Exp

Admin Labor Cost

Investment Income

Rebates

Assessments

Beginning Surplus

Favorable Unfavorable

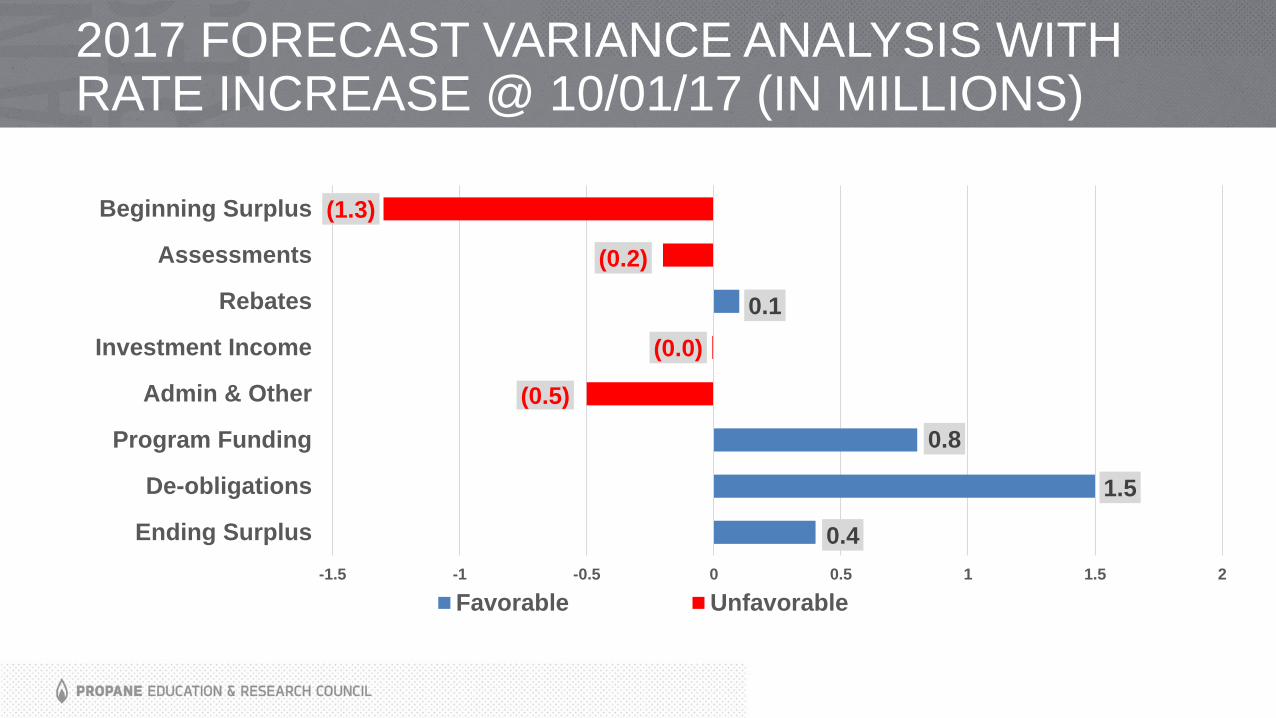

2017 FORECAST VARIANCE ANALYSIS WITH RATE INCREASE @ 10/01/17 (IN MILLIONS)

Category BudgetForecast @

.0045

Variance @

.0045

Forecast @

.005

Variance @

.005

Beginning Surplus $2.6 $1.3 ($1.3) $1.3 ($1.3)

Assessments $38.9 $37.4 ($1.5) $38.7 ($0.2)

Investment Income $0.2 $0.2 - $0.2 -

Rebates ($7.8) ($7.5) $0.3 ($7.7) $0.1

Administrative

& Other($3.2) ($3.7) ($0.5) ($3.7) ($0.5)

Program Funding ($31.0) $(30.2) $0.8 ($30.2) $0.8

Deobligations $0.5 $2.0 $1.5 $2.0 $1.5

Ending Surplus $0.2 ($0.5) ($0.7) $0.6 $0.4

2017 FORECAST VARIANCE ANALYSISWITHOUT RATE INCREASE (IN MILLIONS)

1.5

0.8

0.3

(0.7)

(0.5)

(0.0)

(1.5)

(1.3)

-2 -1.5 -1 -0.5 0 0.5 1 1.5 2

Ending Surplus

De-obligations

Program Funding

Admin & Other

Investment Income

Rebates

Assessments

Beginning Surplus

Favorable Unfavorable

2017 FORECAST VARIANCE ANALYSIS WITH RATE INCREASE @ 10/01/17 (IN MILLIONS)

0.4

1.5

0.8

0.1

(0.5)

(0.0)

(0.2)

(1.3)

-1.5 -1 -0.5 0 0.5 1 1.5 2

Ending Surplus

De-obligations

Program Funding

Admin & Other

Investment Income

Rebates

Assessments

Beginning Surplus

Favorable Unfavorable

$17.7

$11.3$12.0

$5

$7

$9

$11

$13

$15

$17

$19

May June July August September October November December

@ .45 cents @ .5 cents

2017 PROJECTED CASH FLOW BALANCES@ .45 CENTS & .5 CENTS PER GALLON (IN MILLIONS)

PERC INVESTMENT ALLOCATION AS OF APRIL 30, 2017 (IN MILLIONS)

Cash & Money Market (Deposits),

$8.3, 45%

Cert.of Deposits (CD), $9.26, 50%

Municipal Bond (MB), $0.80 , 5%

TOTAL: $18.36 M

PERC TWELVE MONTH CUMULATIVE INVESTMENT RETURNS AT APRIL 30, 2016 & 2017

0.00%

1.00%

2.00%

3.00%

2016 2017

0.81%0.62%

1.13%

2.20%

Return %

Investment

Actual Returns CPI

CONSENT CALENDAR

CHIEF EXECUTIVE OFFICER’S REPORT

Tucker Perkins

ENGINE FUEL ($5,940,500)

DOCKET BUDGETED2017 FUNDING

REQUESTEDTOTAL REMAINING

High Efficiency, High

Performance, Ultra-Low

NOx Medium Duty

Propane Engine

$6,083,162 $1,500,000 $1,243,704

* Additional $2,108,694 included in the 2018 Budget

DOCKET 20905 – CHANGE ORDER ($3,608,694)

High Efficiency, High Performance, Medium Duty Propane Engine, $3,608,694

• Development and demonstration

• Engine suitable for class 5-7 trucks, including bobtails

• PERC and engine partner very pleased with results

• Total contribution: PERC $6,083,162, partner $6,083,162 + infrastructure

• Budget cash flow:

- 2016 $1,000,000 (funded) - 2019 $1,172,774

- 2017 $1,500,000 - 2020 $301,694

- 2018 $2,108,694

2016 2017 2018 2019 2020

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Analysis and Controls Integration

Design

Engine Testing

Vehicle Demonstration

Component MRD

Prototype

Procurement

Vehicle Test

Vehicle Integration

Mule MCE TestingVVA, charge flow, CDA, 1D test data

MS1 MS3 MS2

MS4

MS5MS6

MS7

MS8

ENGINE FUEL ($5,940,500)

DOCKET BUDGETED2017 FUNDING

REQUESTEDTOTAL REMAINING

High Efficiency, High

Performance, Ultra-Low

NOx Medium Duty

Propane Engine

$6,083,162 $1,500,000 $1,243,704

* Additional $2,108,694 included in the 2018 Budget

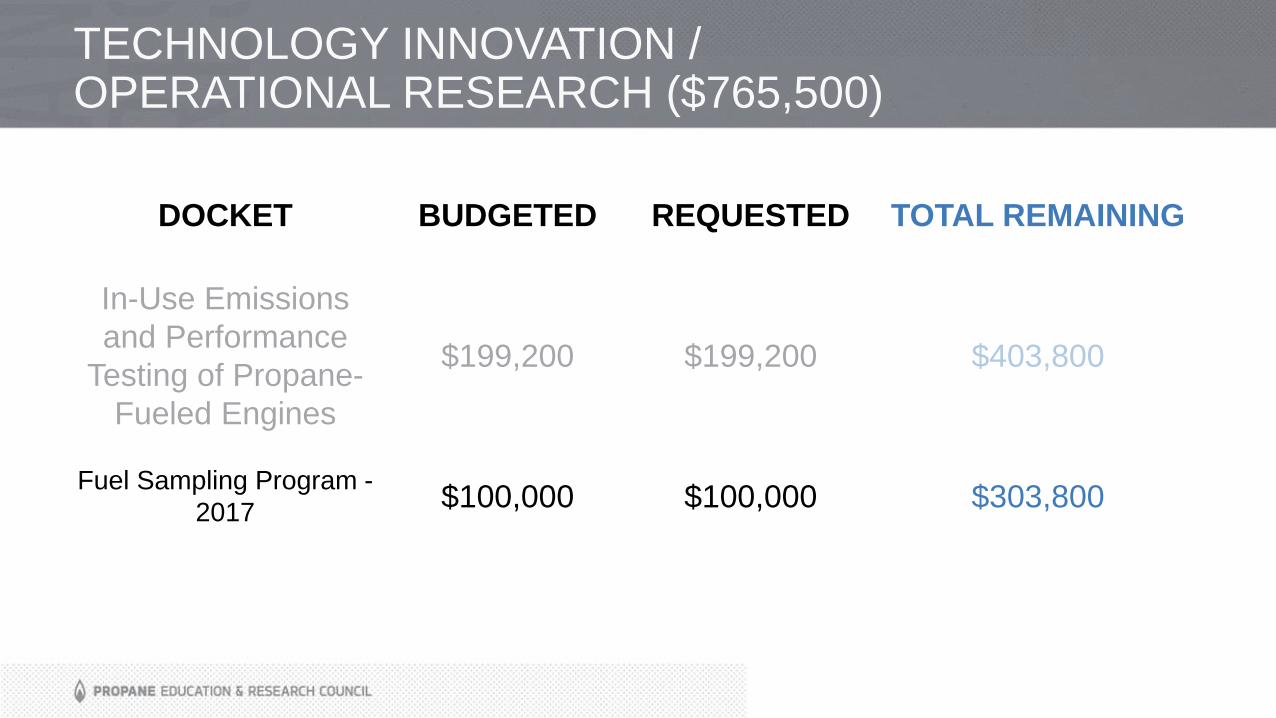

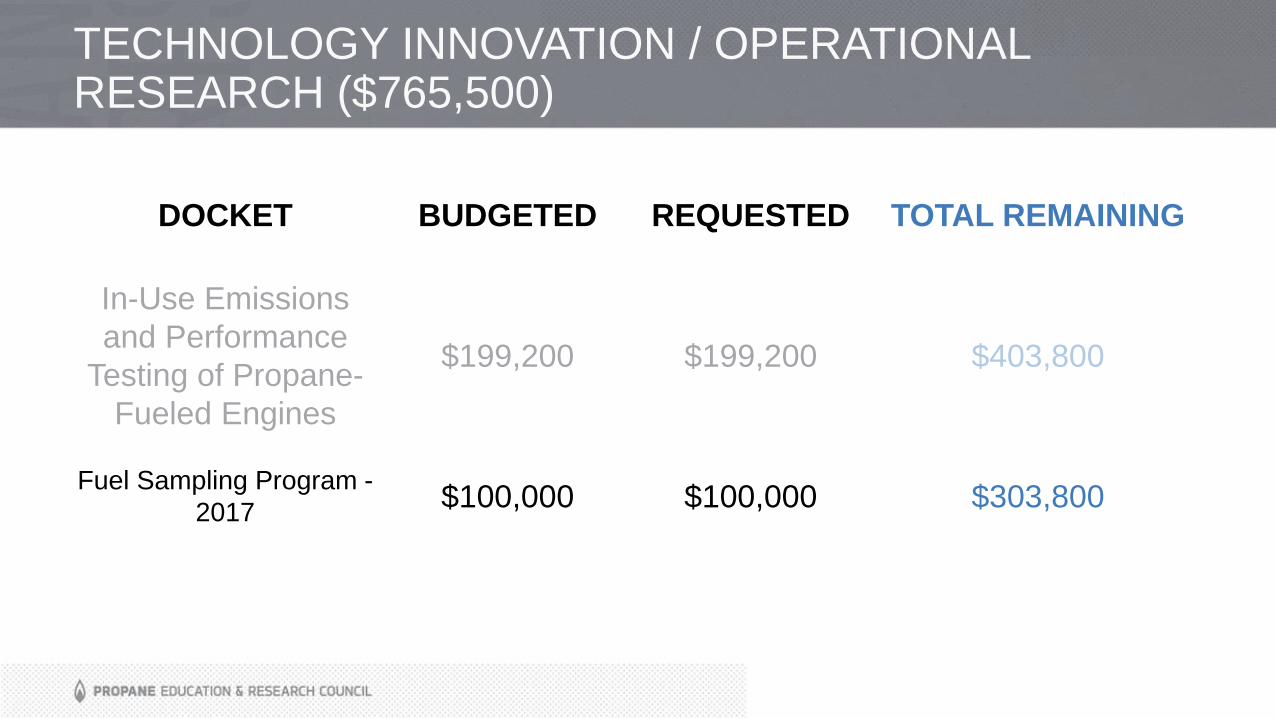

TECHNOLOGY INNOVATION / OPERATIONAL RESEARCH ($765,500)

DOCKET BUDGETED REQUESTED TOTAL REMAINING

In-Use Emissions

and Performance

Testing of Propane-

Fueled Engines

$199,200 $199,200 $403,800

Fuel Sampling Program -

2017$100,000 $100,000 $303,800

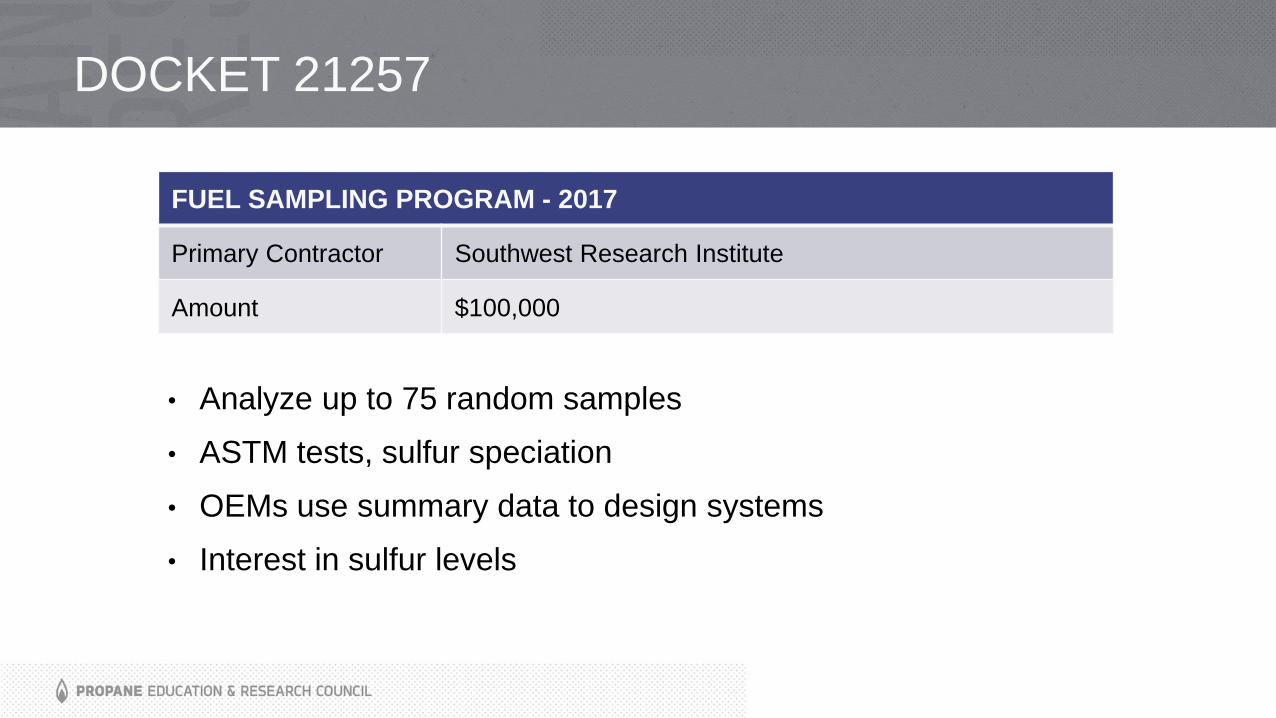

DOCKET 21257

• Analyze up to 75 random samples

• ASTM tests, sulfur speciation

• OEMs use summary data to design systems

• Interest in sulfur levels

FUEL SAMPLING PROGRAM - 2017

Primary Contractor Southwest Research Institute

Amount $100,000

TECHNOLOGY INNOVATION / OPERATIONAL RESEARCH ($765,500)

DOCKET BUDGETED REQUESTED TOTAL REMAINING

In-Use Emissions

and Performance

Testing of Propane-

Fueled Engines

$199,200 $199,200 $403,800

Fuel Sampling Program -

2017$100,000 $100,000 $303,800

CHIEF INFORMATION OFFICER’S REPORT

Kay Howell

– ND Marketer

“I now see the value of my assessment dollars.”

INDUSTRY ENGAGEMENT TACTICS

• Newsletters, Social media, email campaigns

• Videos, webinars, podcasts

• Presentations/exhibits at state/regional meetings

• Catalog and website

• State-level promotion

• Face-to-face meetings with states & companies

• MTST Classroom & Digital

• Advisory Committee

INDUSTRY OUTREACH –TRADESHOWS/CONVENTIONS

• Southeast Expo

• 3,982 attendees • Conducted 5 educational sessions• PERC Update attendance: 600• Distributed 2,200+ items and 34 unique products • Added 392 new contacts to our database• Expanded use of Social Media to engage with marketers:

• Total number of Expo-related posts: 14• Total impressions: 60,635 compared to 32,000 in 2016 and 8,600 in 2015• Total engagements: 1,840 compared to 1,154 in 2016 and 228 in 2015

• Western

• 2,000 total attendees • 500+ collateral pieces distributed• PERC Update: 30 attendees

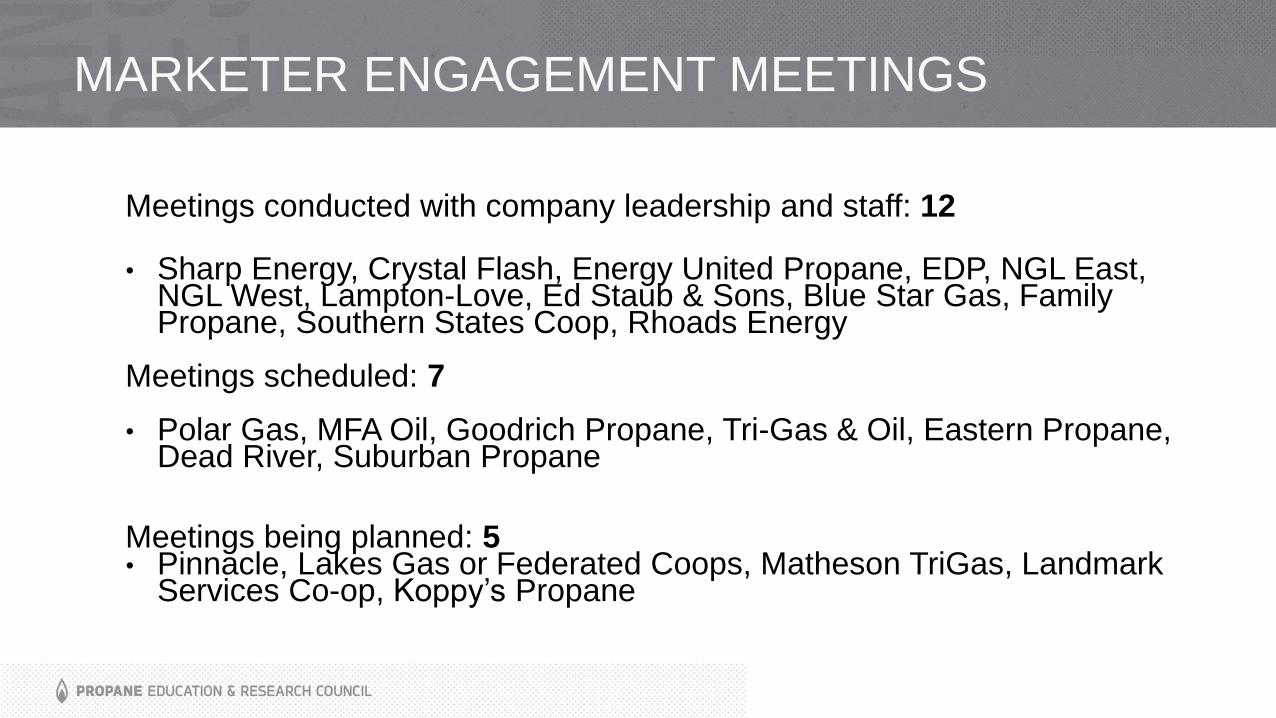

MARKETER ENGAGEMENT MEETINGS

Meetings conducted with company leadership and staff: 12

• Sharp Energy, Crystal Flash, Energy United Propane, EDP, NGL East, NGL West, Lampton-Love, Ed Staub & Sons, Blue Star Gas, Family Propane, Southern States Coop, Rhoads Energy

Meetings scheduled: 7

• Polar Gas, MFA Oil, Goodrich Propane, Tri-Gas & Oil, Eastern Propane, Dead River, Suburban Propane

Meetings being planned: 5• Pinnacle, Lakes Gas or Federated Coops, Matheson TriGas, Landmark

Services Co-op, Koppy’s Propane

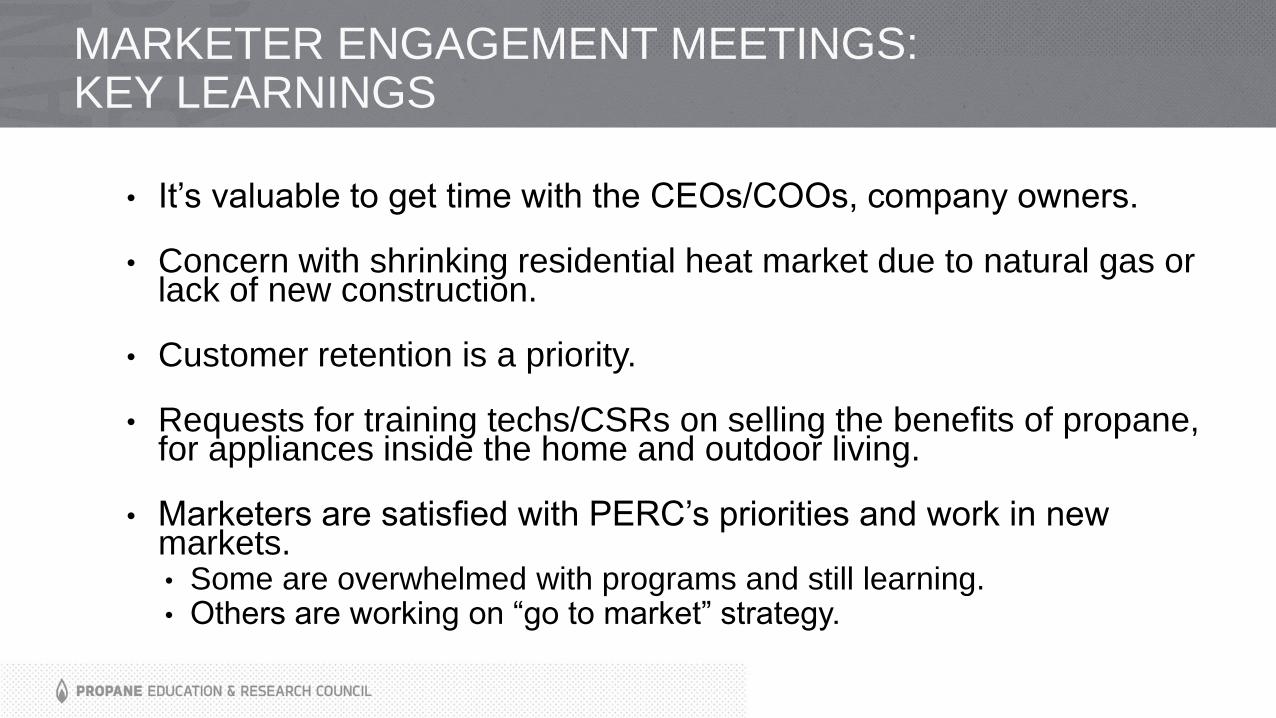

MARKETER ENGAGEMENT MEETINGS: KEY LEARNINGS

• It’s valuable to get time with the CEOs/COOs, company owners.

• Concern with shrinking residential heat market due to natural gas or lack of new construction.

• Customer retention is a priority.

• Requests for training techs/CSRs on selling the benefits of propane, for appliances inside the home and outdoor living.

• Marketers are satisfied with PERC’s priorities and work in new markets. • Some are overwhelmed with programs and still learning. • Others are working on “go to market” strategy.

MARKETER ENGAGEMENT MEETINGS

Recommendations:

• Develop quarterly or bi-annual personal message from PERC CEO to industry CEOs/Owners; utilize email or print. Highlight PERC achievements, invite feedback.

• Work with MOT Res/Comm project team to develop training and collateral; repackage existing materials for upselling appliances.

• Promote continuing education. Conduct Marketing Symposium to educate marketers on market opportunities and marketing techniques; plan regional MTST sessions.

STATE LEADERSHIP ENGAGEMENT

• Personal meetings with new state executives have been well received

• PGANE, Pacific completed

• CO/AZ/NM, NJ, WI scheduled

• Rocky Mountain, VA, AR planned

• 2017 Leadership Summit

• Date and venue confirmed (Nov. 16 and 17 in DC)

• Planning committee:

• 5 state execs + PERC & 2 NPGA staff

• Agenda being developed - specific request made to hear vision of new CEO and update of IOC

INDUSTRY OUTREACH –STATE MEETINGS SUPPORT

• Attended 26 industry meetings (through June)

• Key takeaways:

• Proudly Propane campaign updates and how marketers/PGA can leverage its benefits are popular topics

• Interest in specific local market insights and opportunities

• School bus market growth

• Volkswagen settlement opportunity

• New PERC resources for safety and training

INDUSTRY MEETINGS ATTENDED (AS OF JULY 1)

• Minnesota Propane Association Annual Meeting and Convention

• Arizona PGA Board Meeting

• Rocky Mountain Propane Association Membership Meeting

• North Carolina PGA Spring Board Meeting

• New York PGA Spring Meeting

• Wisconsin PGA Spring Convention

• Pennsylvania PGA Spring Board and Membership Meeting

• Virginia PGA Spring Meeting

• PGA of New England Spring Meeting

• Colorado PGA Board Meeting

• NPGA Southeastern Convention & International Propane Expo

• Kentucky PGA Spring Board Meeting

• Western Propane Trade Show and Convention

• Nevada Propane Dealers Association Membership Meeting

• Pacific PGA Membership Meeting

• Western PGA Board of Directors Meeting

• Rocky Mountain Propane Association Membership Meeting

• Arizona PGA Membership Meeting

• Mississippi PGA Summer Convention

• Alabama / Louisiana PGAs Convention

• Ray Murray Open House

• Mid-States Propane Expo (IA, KS, MO)

• New York / New Jersey PGAs Joint Meeting

• North Dakota PGA Annual Meeting

• Arkansas & Oklahoma PGAs Annual Convention

• New Mexico PGA & Colorado PGA Annual Convention

MARKETER TECHNOLOGY & SALES TRAINING

• Held 16 of 28 scheduled classroom sessions thru June 30 (budgeted for 60):

- CSR: 9 - Commercial: 1

- Residential: 1 - Residential Plus: 3

- Mowers: 1 - Autogas: 1

• Marketer Momentum Newsletter: 3,200 subscribers

- Open rate for last two issues: 38.49% and 44.46%

• Webinars

• Launched Digital MTST in April

- 174 registrants

- Adding new educational elements monthly – scheduled out over next 12 months

- Soliciting feedback from early registrants via personal calls

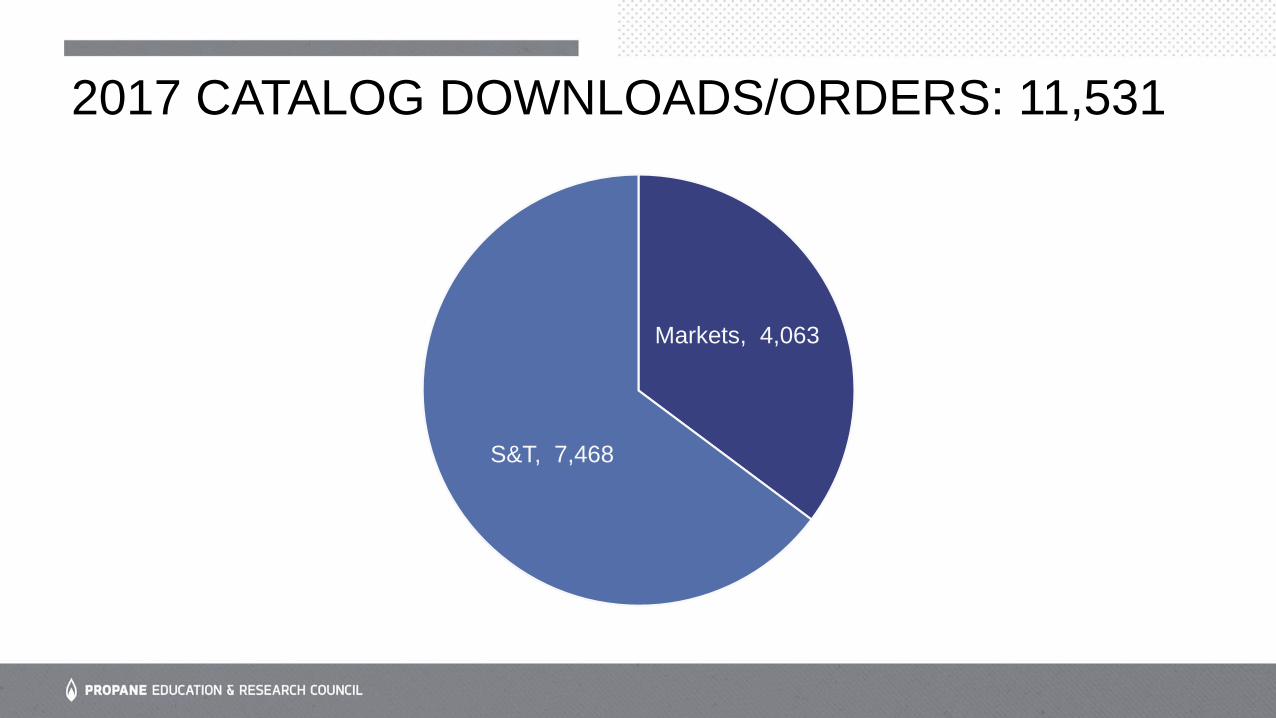

2017 CATALOG DOWNLOADS/ORDERS: 11,531

Markets, 4,063

S&T, 7,468

NEWLY ADDED SAFETY & TRAINING RESOURCES/PROGRAMS

• Blended Learning

• Refresher Training Program • PowerPoint & On-line E-Learning formats

• Propane Autogas Technician Training

• Safety Talk Presentations

• Consumer Safety Videos

SAFETY MEETING PRESENTATIONS

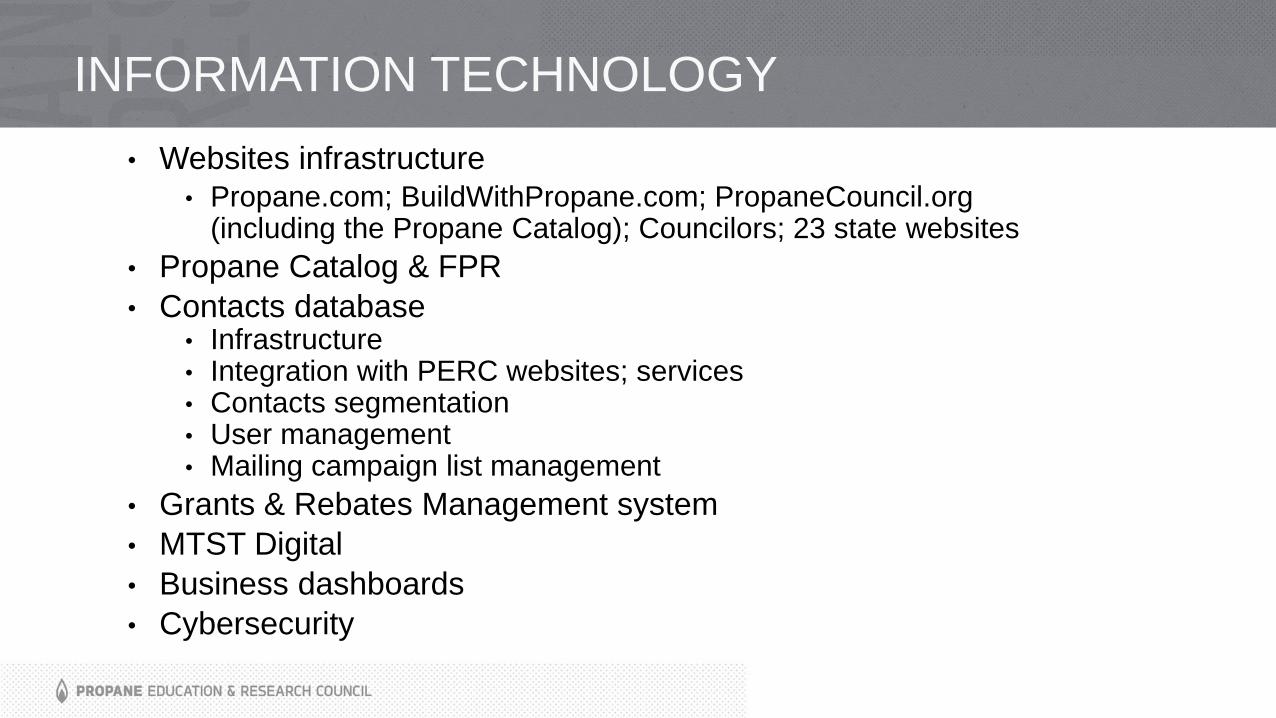

INFORMATION TECHNOLOGY

• Websites infrastructure

• Propane.com; BuildWithPropane.com; PropaneCouncil.org (including the Propane Catalog); Councilors; 23 state websites

• Propane Catalog & FPR

• Contacts database• Infrastructure• Integration with PERC websites; services• Contacts segmentation• User management• Mailing campaign list management

• Grants & Rebates Management system

• MTST Digital

• Business dashboards

• Cybersecurity

PROPANE SUPPLY CHAIN & INFRASTRUCTURE: MARKET ANALYSIS – PART 1

Rusty Braziel, RBN Energy

© Copyright 2017 RBN Energy

Propane Supply Chain and Infrastructure: Market Analysis – Phase I

July 11, 2017

RBN Propane TeamDavid BrazielRusty Braziel

Noel CopelandRon GistJohn Hall

Scott PotterKelly Van Hull

52© Copyright 2017 RBN Energy

Propane Supply Chain and Infrastructure: Project Design

» Current Market Developments and Projected Supply/Demand Dynamics▪ Supply/Demand Forecast▪ Assessment of Market Behavior▪ Evaluation of Findings

Phase I

» Implications of Phase I Findings on the Propane Supply Chain▪ Delineate Supply Chain Risks Faced by

Propane Retailers▪ Develop Model to Simulate How

Triggering Events Can Result In Market Disruptions

▪ Recommend Risk Mitigation Measures

Phase II

53© Copyright 2017 RBN Energy

Propane Supply Chain and Infrastructure: Phase I

» Phase I - Project Objectives, Recent Market Developments, Methodology

» U.S. Propane Supply/Demand Analysis▪ Supply▪ Demand, Flows, Balances▪ Market Implications

» U.S. Propane Regional/ Infrastructure Analysis▪ Regional Profiles – Strengths and Weaknesses▪ Concept: Propane Supply Reliability Index

» Conclusions

» Phase II – Methodology and Update

54© Copyright 2017 RBN Energy

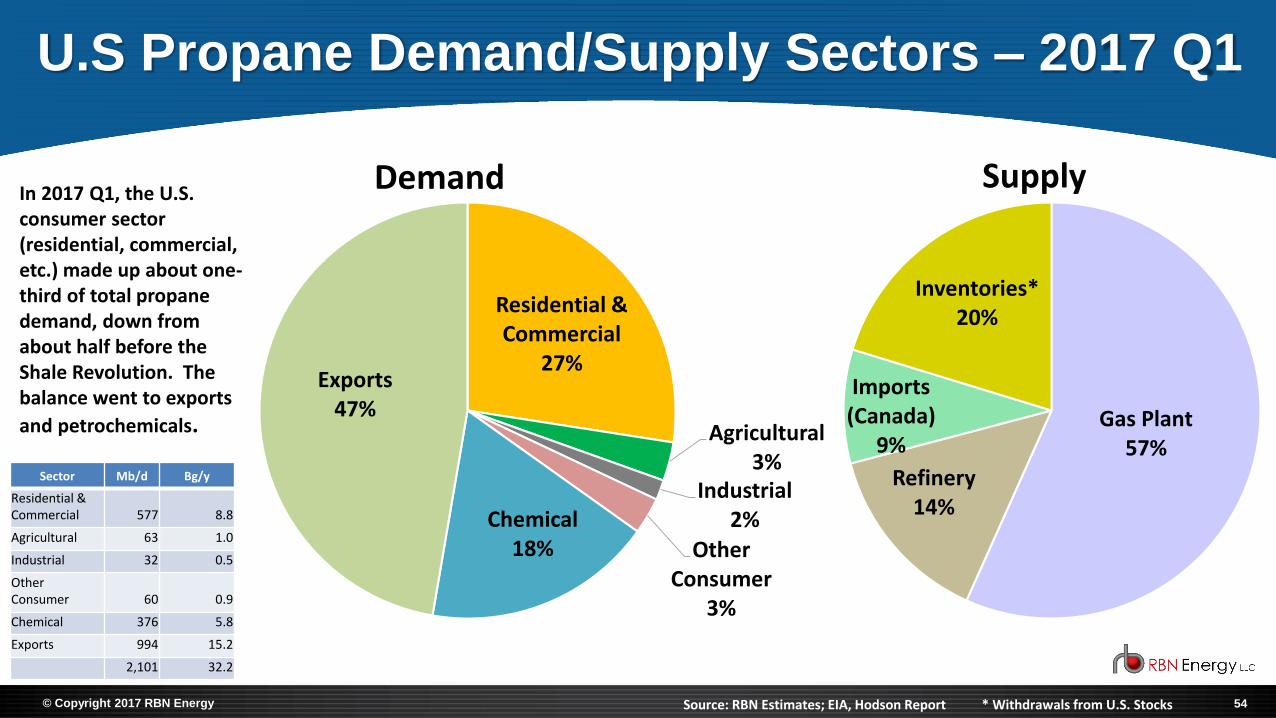

U.S Propane Demand/Supply Sectors – 2017 Q1

Residential & Commercial

27%

Agricultural3%

Industrial2%

Other Consumer

3%

Chemical18%

Exports47%

Source: RBN Estimates; EIA, Hodson Report

Sector Mb/d Bg/y

Residential & Commercial 577 8.8

Agricultural 63 1.0

Industrial 32 0.5

Other Consumer 60 0.9

Chemical 376 5.8

Exports 994 15.2

2,101 32.2

Gas Plant57%

Refinery14%

Imports (Canada)

9%

Inventories*20%

Demand Supply

* Withdrawals from U.S. Stocks

In 2017 Q1, the U.S. consumer sector (residential, commercial, etc.) made up about one-third of total propane demand, down from about half before the Shale Revolution. The balance went to exports

and petrochemicals.

55© Copyright 2017 RBN Energy

-

2

4

6

8

10

12

14

16

18

20

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

Bg/

y

Mb

/d

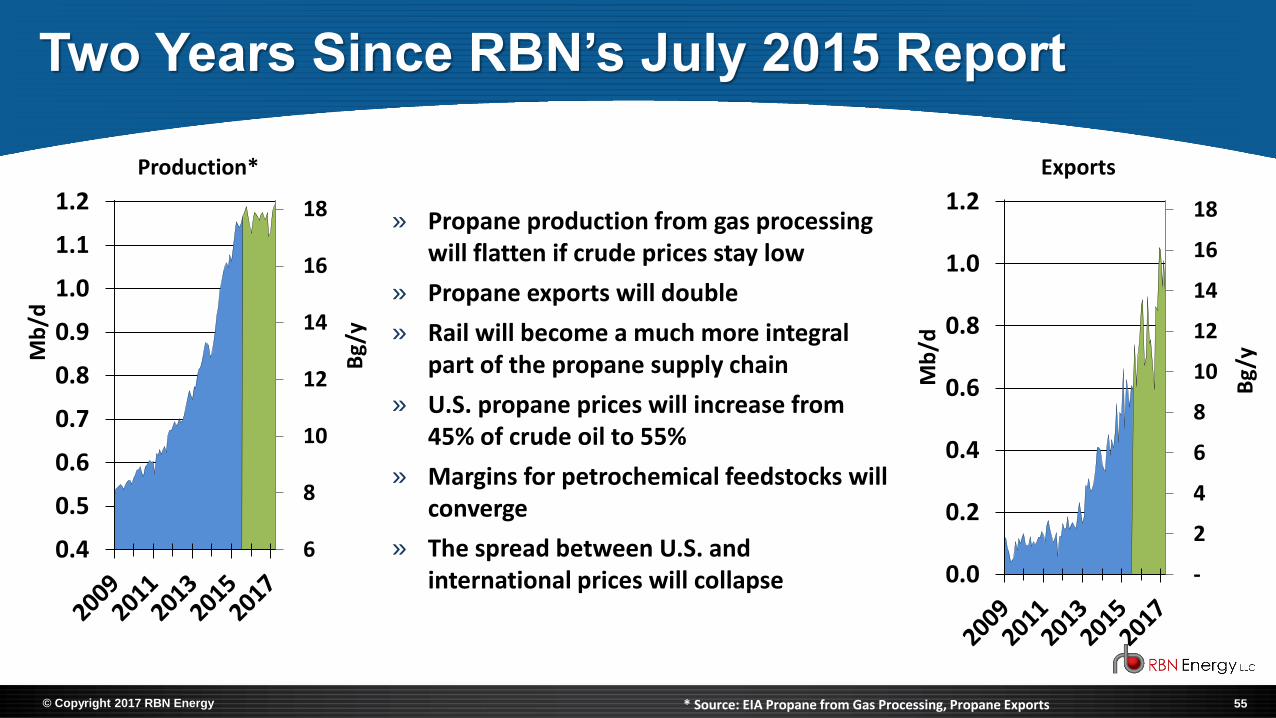

» Propane production from gas processing will flatten if crude prices stay low

» Propane exports will double

» Rail will become a much more integral part of the propane supply chain

» U.S. propane prices will increase from 45% of crude oil to 55%

» Margins for petrochemical feedstocks will converge

» The spread between U.S. and international prices will collapse

6

8

10

12

14

16

18

20

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

1.4

Bg/

y

Mb

/dTwo Years Since RBN’s July 2015 Report

Production* Exports

* Source: EIA Propane from Gas Processing, Propane Exports

56© Copyright 2017 RBN Energy

Risks In Today’s Propane Market

More Exports

More Rail

Two Warm

Winters

57© Copyright 2017 RBN Energy

» Propane is now a true global commodity. International developments exert a much greater influence over U.S. propane balances and prices. U.S. prices and differentials to international markets increasingly impact the level of exports.

» During periods of severe weather, it is likely that the consumer/retail market will acquire incremental supplies from barrels otherwise destined for exports and petrochemical supplies.

▪ If European and Asian markets experience severe weather at the same time as the U.S., these supplies will be very expensive, possibly unavailable.

» Supplies sourced from cancelled cargos will face significant supply chain challenges to meet demand peaks in market regions located long distances from export hubs.

▪ Consequently, peak demand during periods of severe weather must be met with supplies much closer to demand, deliverable via reliable, resilient supply chain infrastructure.

» Unfortunately several midstream companies have indicated that they plan to reduce inventories held for consumer markets due to losses experienced over the past two warm winters, making it more important than ever for individual propane companies to insure

their access to secure sources of local supply.

Risks In Today’s Propane Market

58© Copyright 2017 RBN Energy

MB Propane Price and Relationship to Crude Oil

25

35

45

55

65

75

85

95

c/ga

l

Propane Price

Source: OPIS/CME NYMEX

35%

40%

45%

50%

55%

60%

65%

70%

75%Propane % of Crude Oil (WTI)

35%

40%

45%

50%

55%

60%

65%

70%

75%Propane % of Crude Oil (WTI)

59© Copyright 2017 RBN Energy

U.S. Propane Exports (2016-17)

-

2

4

6

8

10

12

14

16

-

200

400

600

800

1,000

Bg

/y

Mb

/d

Gulf Coast

Enterprise ETP/Sunoco Freeport/P66 Ingleside

Riverside Targa Trafigura

-

0.20

0.40

0.60

0.80

1.00

-

10

20

30

40

50

60

70

Bg

/y

Mb

/d

East Coast (Marcus Hook)

60© Copyright 2017 RBN Energy

U.S. Propane Inventories (Stocks)

0

20

40

60

80

100

120

MM

bl

Weeks

Y-1 Previous 5 Year Range 2016 2017

61© Copyright 2017 RBN Energy

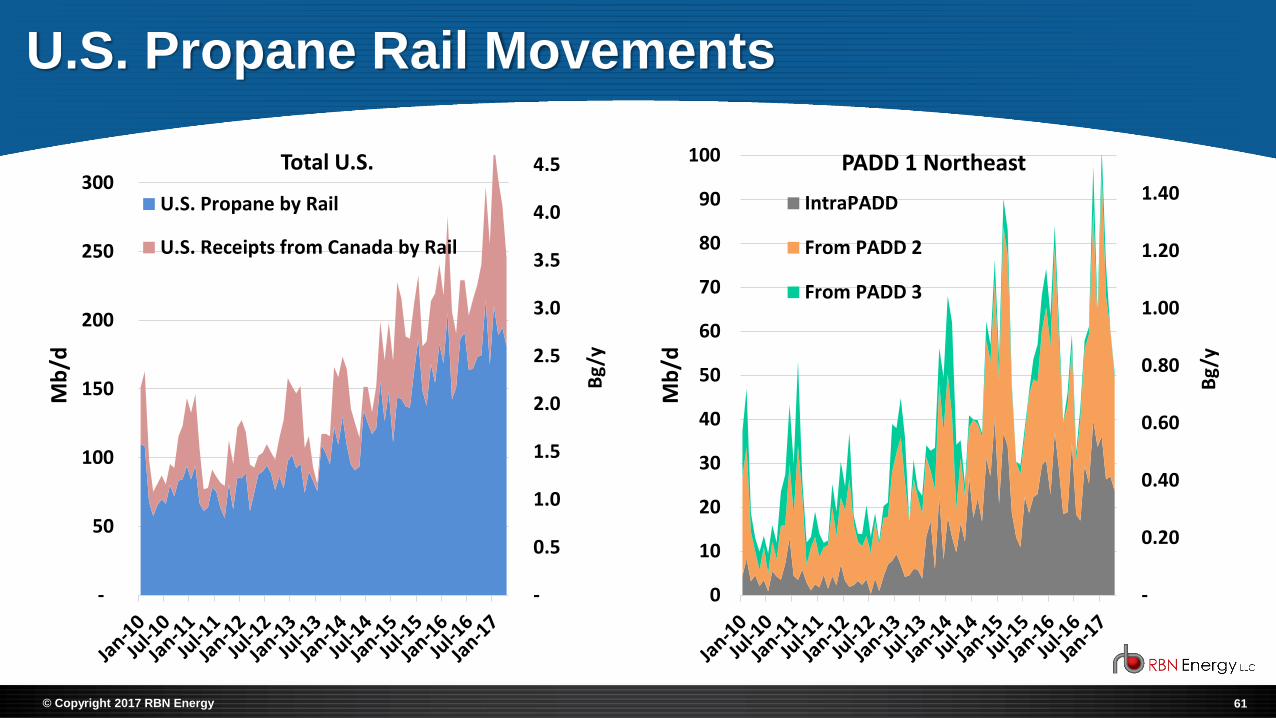

U.S. Propane Rail Movements

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

-

50

100

150

200

250

300

Bg

/y

Mb

/d

Total U.S.

U.S. Propane by Rail

U.S. Receipts from Canada by Rail

-

0.20

0.40

0.60

0.80

1.00

1.20

1.40

0

10

20

30

40

50

60

70

80

90

100

Bg

/y

Mb

/d

PADD 1 Northeast

IntraPADD

From PADD 2

From PADD 3

62© Copyright 2017 RBN Energy

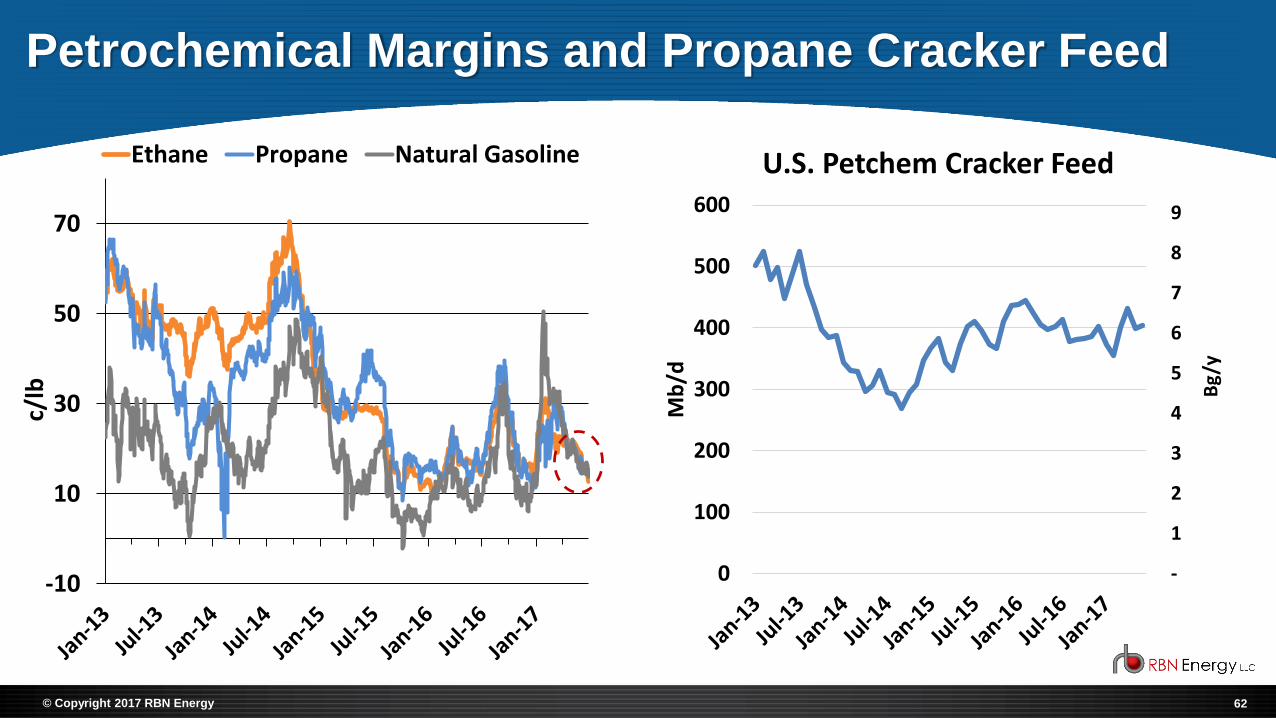

Petrochemical Margins and Propane Cracker Feed

-10

10

30

50

70

c/lb

Ethane Propane Natural Gasoline

-

1

2

3

4

5

6

7

8

9

0

100

200

300

400

500

600

Bg

/y

Mb

/d

U.S. Petchem Cracker Feed

63© Copyright 2017 RBN Energy

Northwest

Southwest

WMW

SouthSoutheast

EMW

NE-

New England

PERC Regions and EIA PADDs

NE-

Mid Atlantic

PADD 1PADD 2

PADD 4

PADD 5

PADD 3

PADD 1

PADD 2

PADD 4

PADD 5

Northwest

Southwest

WMW

South

Southeast

EMW

NE-

New England

NE-

Mid Atlantic

PADD 3

64© Copyright 2017 RBN Energy

4 Models: Production Scenarios and Demand Cases

Demand Cases

Co

ntr

acti

on

Gro

wth

Sup

ply

Sce

nar

ios

Normal Weather Severe Weather*

High crude prices, normal

weather

High crude prices, “Severe

Weather” winter weather

Low crude prices, normal

weather

Low crude prices, “Severe

Weather” winter

weather

* a.k.a., Polar Vortex

65© Copyright 2017 RBN Energy

4 Models: Production Scenarios and Demand Cases

$40

$45

$50

$55

$60

$65

$70

$75

$80

$/B

bl

Crude Oil: WTI Cushing

Growth Contraction

$2.70

$3.00

$3.30

$3.60

$3.90

$/M

Mb

tu

Natural Gas: Henry Hub

Growth Contraction

15

16

17

18

19

20

1,000

1,050

1,100

1,150

1,200

1,250

1,300

1,350

Bg/

y

Mb

/d

Severe Weather Case: Average Nov-Feb Demand*

* Red Columns indicate winters with severe weather conditions

66© Copyright 2017 RBN Energy

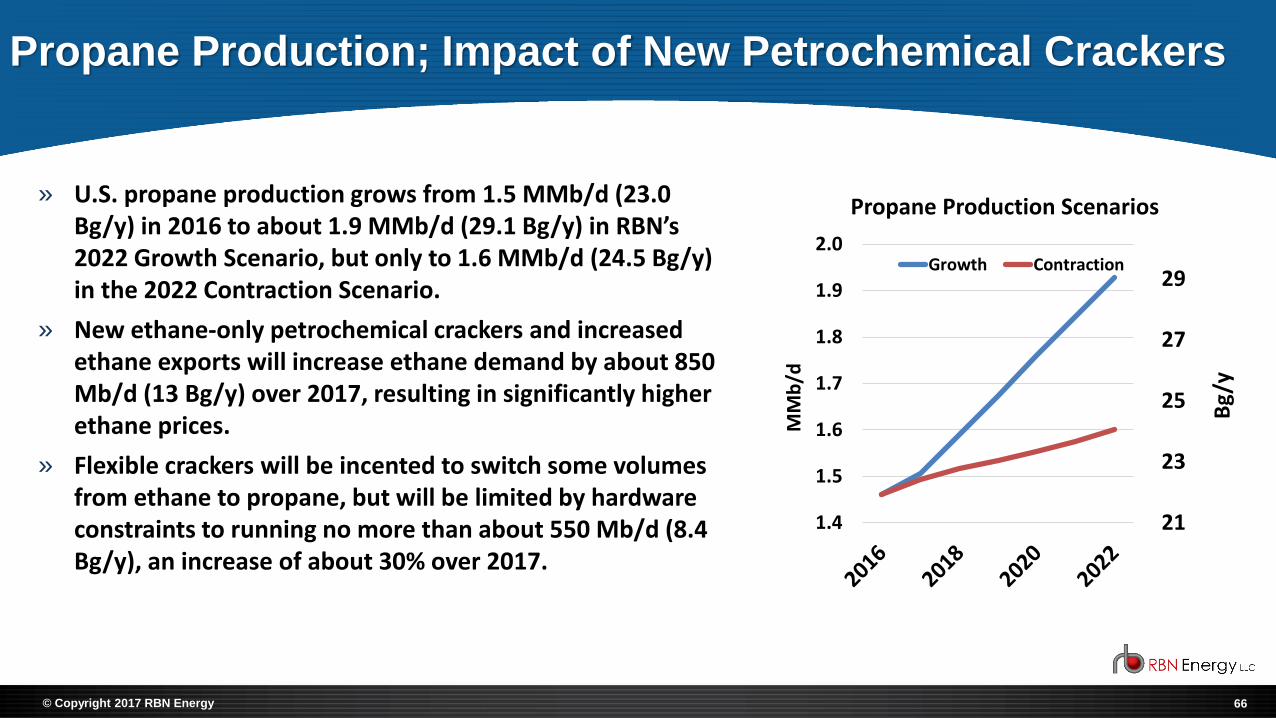

Propane Production; Impact of New Petrochemical Crackers

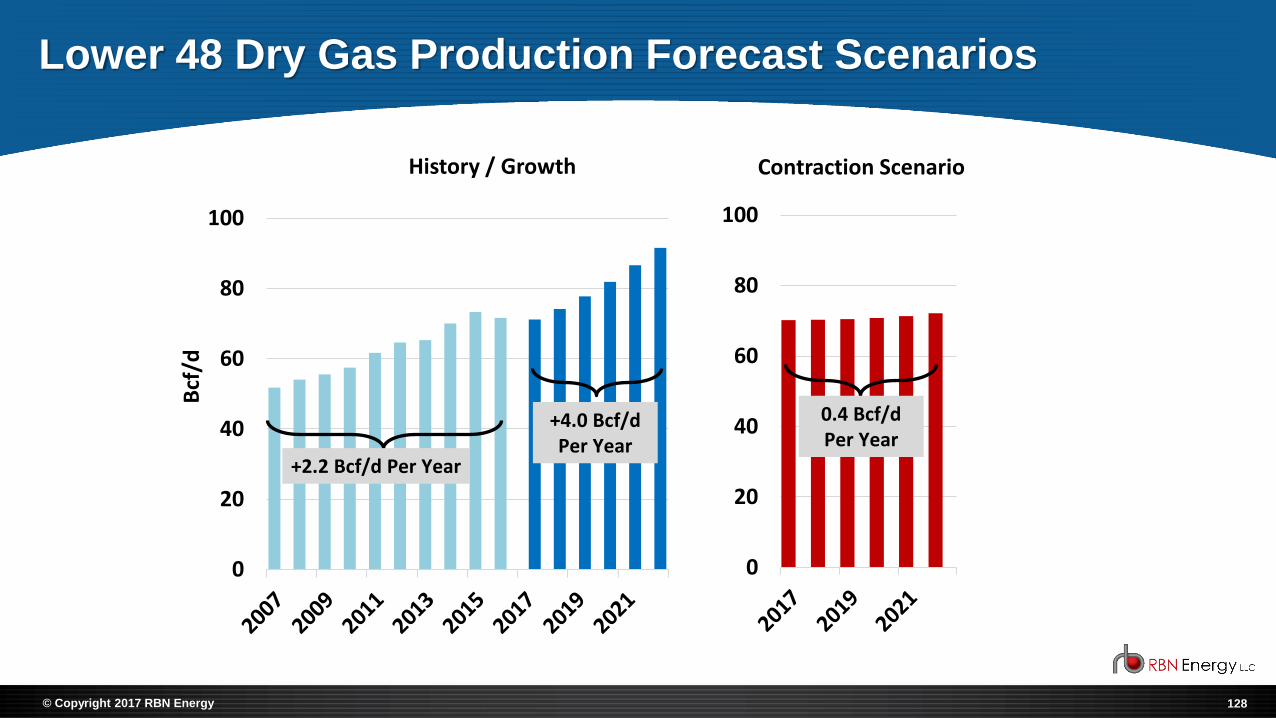

» U.S. propane production grows from 1.5 MMb/d (23.0 Bg/y) in 2016 to about 1.9 MMb/d (29.1 Bg/y) in RBN’s 2022 Growth Scenario, but only to 1.6 MMb/d (24.5 Bg/y) in the 2022 Contraction Scenario.

» New ethane-only petrochemical crackers and increased ethane exports will increase ethane demand by about 850 Mb/d (13 Bg/y) over 2017, resulting in significantly higher ethane prices.

» Flexible crackers will be incented to switch some volumes from ethane to propane, but will be limited by hardware constraints to running no more than about 550 Mb/d (8.4 Bg/y), an increase of about 30% over 2017.

21

23

25

27

29

1.4

1.5

1.6

1.7

1.8

1.9

2.0

Bg/

y

MM

b/d

Propane Production Scenarios

Growth Contraction

67© Copyright 2017 RBN Energy

Total Incremental Ethane Demand

-

2

4

6

8

10

12

14

16

0

100

200

300

400

500

600

700

800

900

1,000

1,100

Bg/

y

Mb

/d

Exports

Petchem

» Tighter ethane markets and higher ethane prices will result in narrow spreads between alternative steam cracker petrochemical feedstocks.

» Higher prices for any one feedstock will encourage crackers to reduce runs of that feedstock and switch to others.

» Consequently, higher propane prices resulting from severe weather will encourage steam crackers to reduce propane usage, making more barrels available to consumer markets.

68© Copyright 2017 RBN Energy

Propane Exports – Growth and Contraction Scenarios

» At the U.S. level, consumer demand in the two Scenarios is relatively similar, therefore any additional volume over petrochemical demand between the two Scenarios is expected to move to export markets.

» In the Contraction scenario with modest production growth, exports decline as new cracker and PDH demand pulls supply from the export market.

» In the Growth Scenario, exports increase to average 1.1 MMb/d (16.9 Bg/y) by 2022.

» The location of propane exports shifts significantly, with Marcus Hook LPG exports increasing to 232 Mb/d (3.5 Bg/y) in 2022 from 70 Mb/d (1.1 Bg/y) in 2017 (Growth Scenario, mostly propane).

9

11

13

15

17

0.6

0.7

0.8

0.9

1.0

1.1

1.2

Bg/

y

MM

b/d

Propane Export Scenarios

Growth Contraction

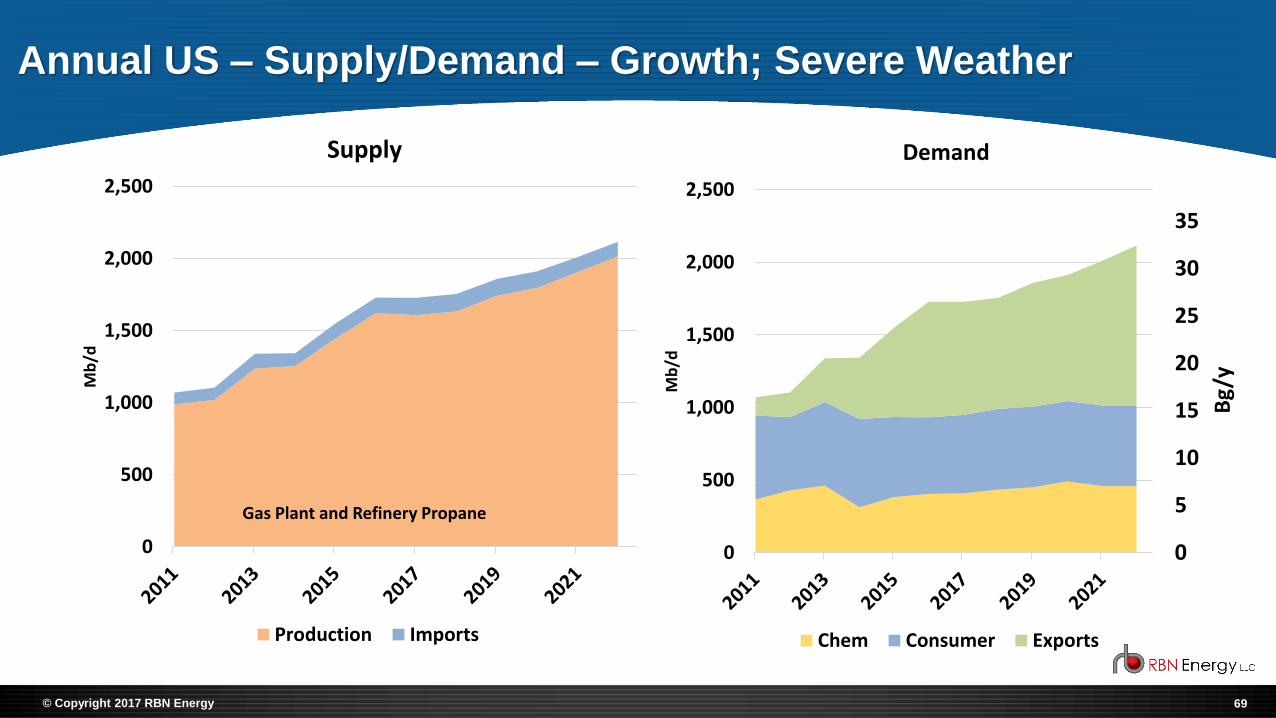

69© Copyright 2017 RBN Energy

Annual US – Supply/Demand – Growth; Severe Weather

0

500

1,000

1,500

2,000

2,500

Mb

/d

Supply

Production Imports

0

5

10

15

20

25

30

35

0

500

1,000

1,500

2,000

2,500

Bg/

y

Mb

/d

Demand

Chem Consumer Exports

Gas Plant and Refinery Propane

70© Copyright 2017 RBN Energy

Annual US – Supply/Demand – Contraction; Severe Weather

0

500

1,000

1,500

2,000

2,500

Mb

/d

Supply

Production Imports

Gas Plant and Refinery Propane

0

5

10

15

20

25

30

35

0

500

1,000

1,500

2,000

2,500

Bg

/yMb

/d

Demand

Chem Consumer Exports

71© Copyright 2017 RBN Energy

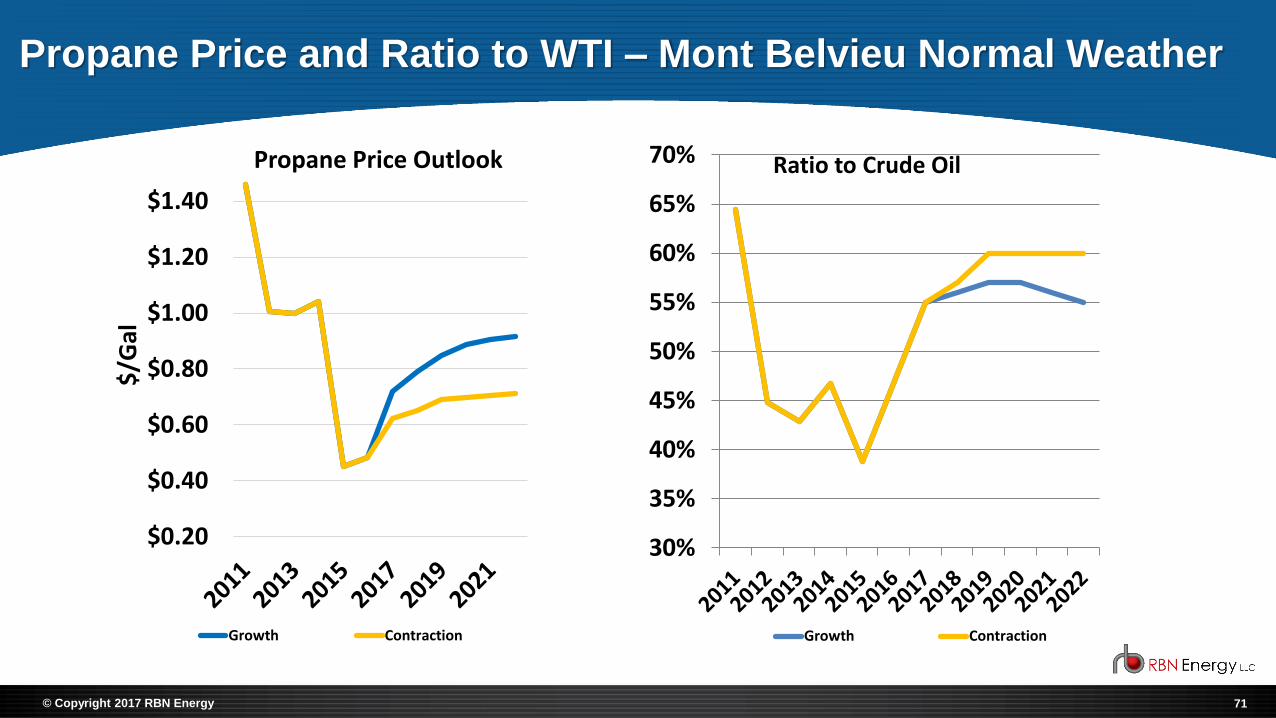

Propane Price and Ratio to WTI – Mont Belvieu Normal Weather

30%

35%

40%

45%

50%

55%

60%

65%

70% Ratio to Crude Oil

Growth Contraction

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

$/G

alPropane Price Outlook

Growth Contraction

72© Copyright 2017 RBN Energy

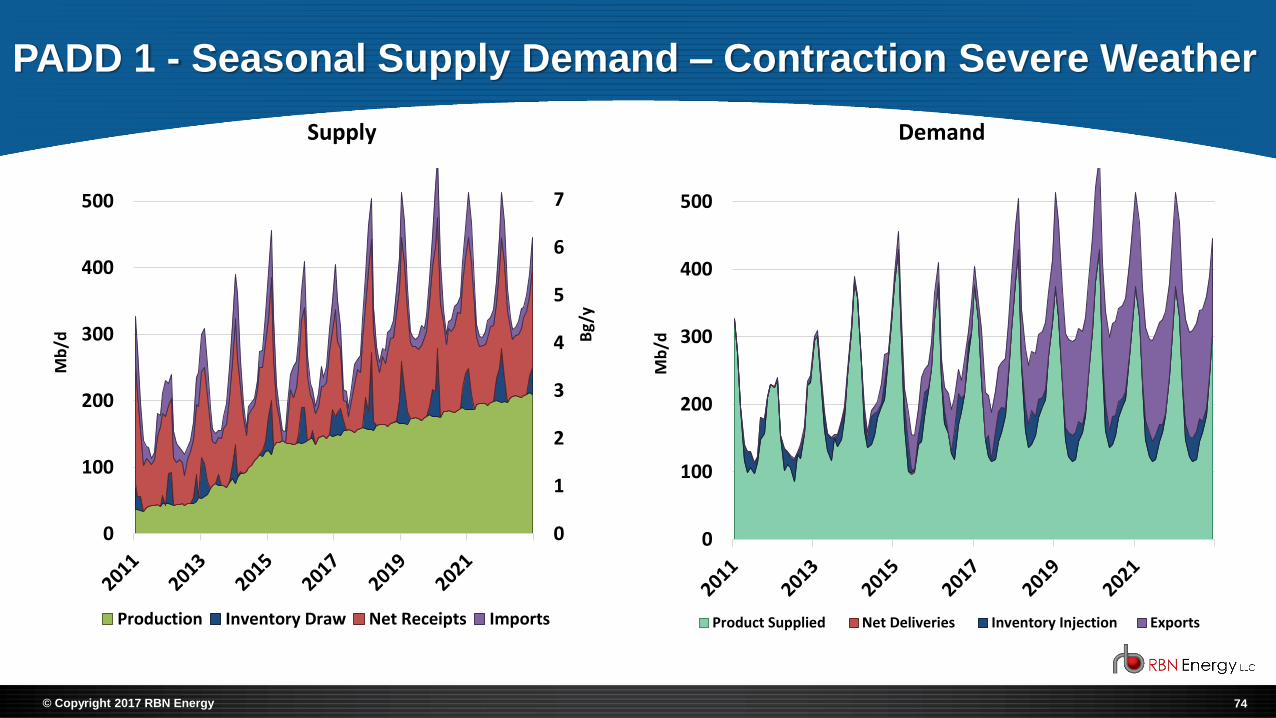

Seasonal Supply Demand – PADD Level Presentation Format

1. Product Supplied (Consumer + Petchem Demand)2. Inventory Injections (Builds)3. Net Deliveries (to other PADDs)4. Exports

Demand

1. U.S. Production2. Inventory Withdrawals (Draws)3. Net Receipts (from other PADDs)4. Imports

Supply

73© Copyright 2017 RBN Energy

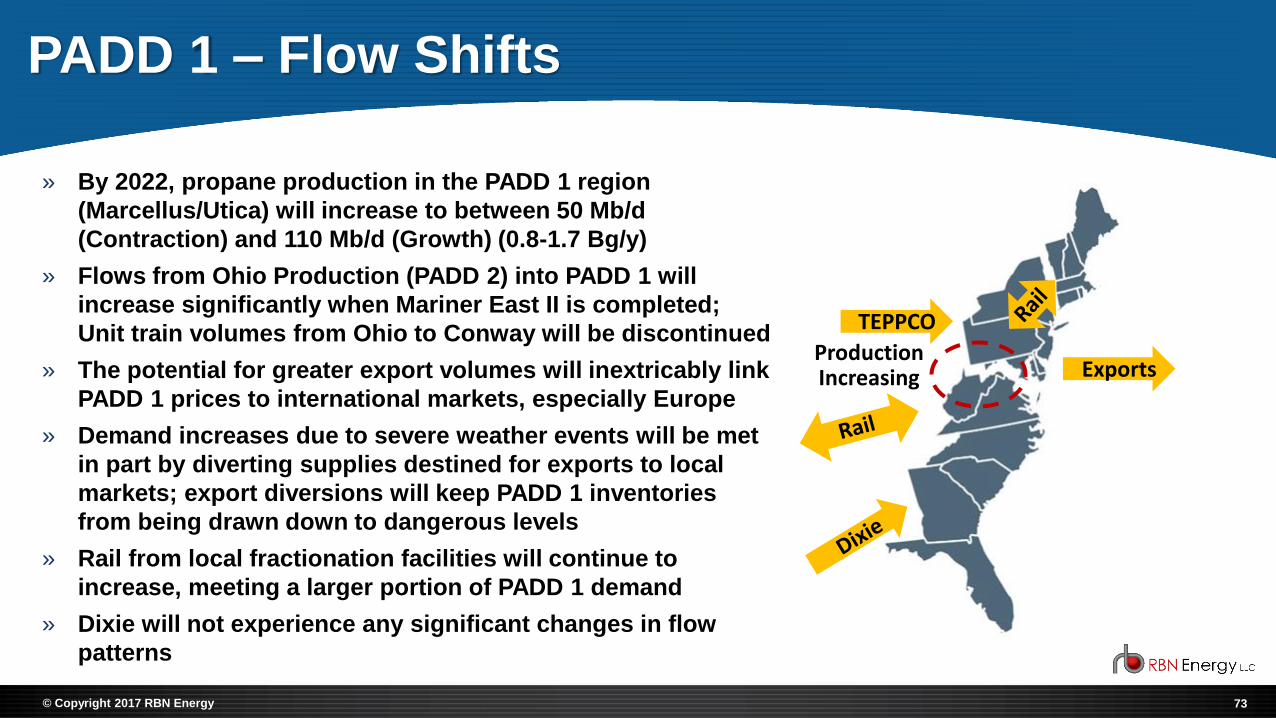

PADD 1 – Flow Shifts

» By 2022, propane production in the PADD 1 region

(Marcellus/Utica) will increase to between 50 Mb/d

(Contraction) and 110 Mb/d (Growth) (0.8-1.7 Bg/y)

» Flows from Ohio Production (PADD 2) into PADD 1 will

increase significantly when Mariner East II is completed;

Unit train volumes from Ohio to Conway will be discontinued

» The potential for greater export volumes will inextricably link

PADD 1 prices to international markets, especially Europe

» Demand increases due to severe weather events will be met

in part by diverting supplies destined for exports to local

markets; export diversions will keep PADD 1 inventories

from being drawn down to dangerous levels

» Rail from local fractionation facilities will continue to

increase, meeting a larger portion of PADD 1 demand

» Dixie will not experience any significant changes in flow

patterns

TEPPCO

Production Increasing Exports

74© Copyright 2017 RBN Energy

PADD 1 - Seasonal Supply Demand – Contraction Severe Weather

0

1

2

3

4

5

6

7

0

100

200

300

400

500

Bg

/y

Mb

/d

Supply

Production Inventory Draw Net Receipts Imports

0

100

200

300

400

500

Mb

/d

Demand

Product Supplied Net Deliveries Inventory Injection Exports

75© Copyright 2017 RBN Energy

PADD 1 – Weather Sensitivities – Contraction

0

1

2

3

4

5

050

100150200250300350

Bg/

y

Mb

/d

Receipts

Pipeline from PADD3 (Propane - Dixie)

Rail from PADD3 (Propane )

Pipeline from PADD 2 (Propane-TEPPCO and ME 2)

Rail from PADD 2 (Propane)

Imports (Propane)

0

1

2

3

4

5

6

7

8

9

MM

bb

l

Inventories

Last 5 year Range PV 19-20

76© Copyright 2017 RBN Energy

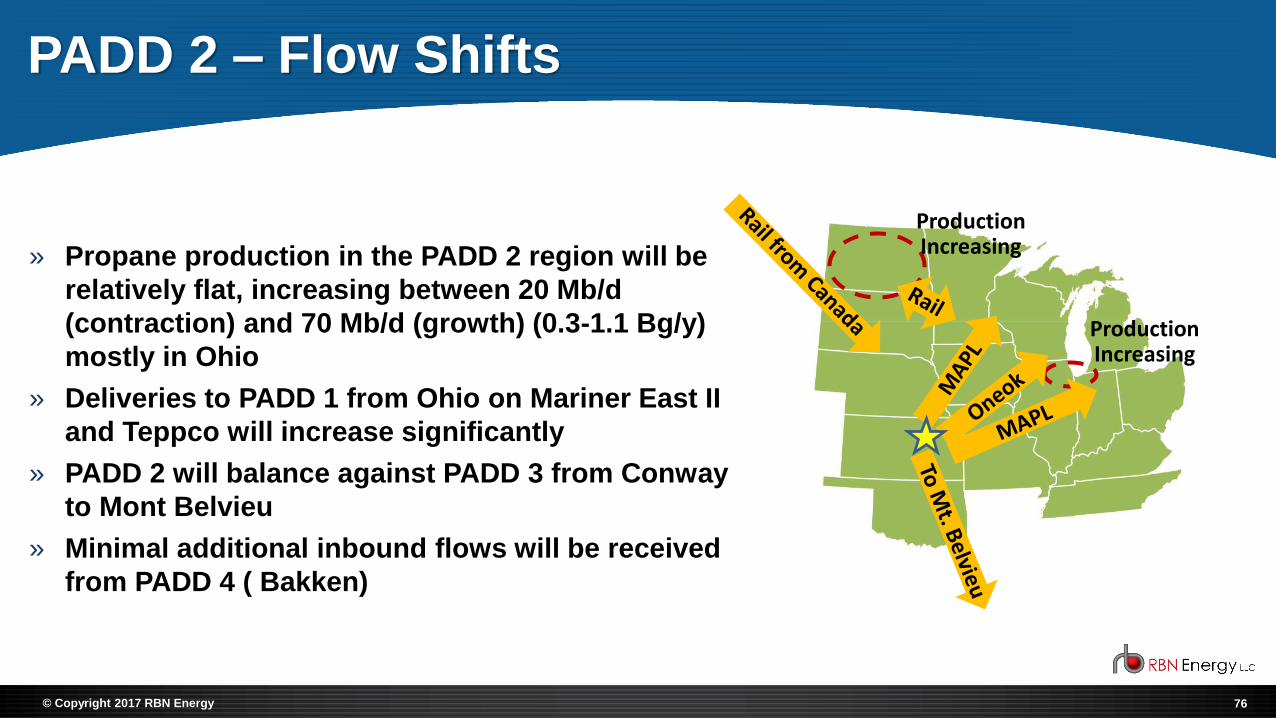

PADD 2 – Flow Shifts

» Propane production in the PADD 2 region will be

relatively flat, increasing between 20 Mb/d

(contraction) and 70 Mb/d (growth) (0.3-1.1 Bg/y)

mostly in Ohio

» Deliveries to PADD 1 from Ohio on Mariner East II

and Teppco will increase significantly

» PADD 2 will balance against PADD 3 from Conway

to Mont Belvieu

» Minimal additional inbound flows will be received

from PADD 4 ( Bakken)

Production Increasing

Production Increasing

77© Copyright 2017 RBN Energy

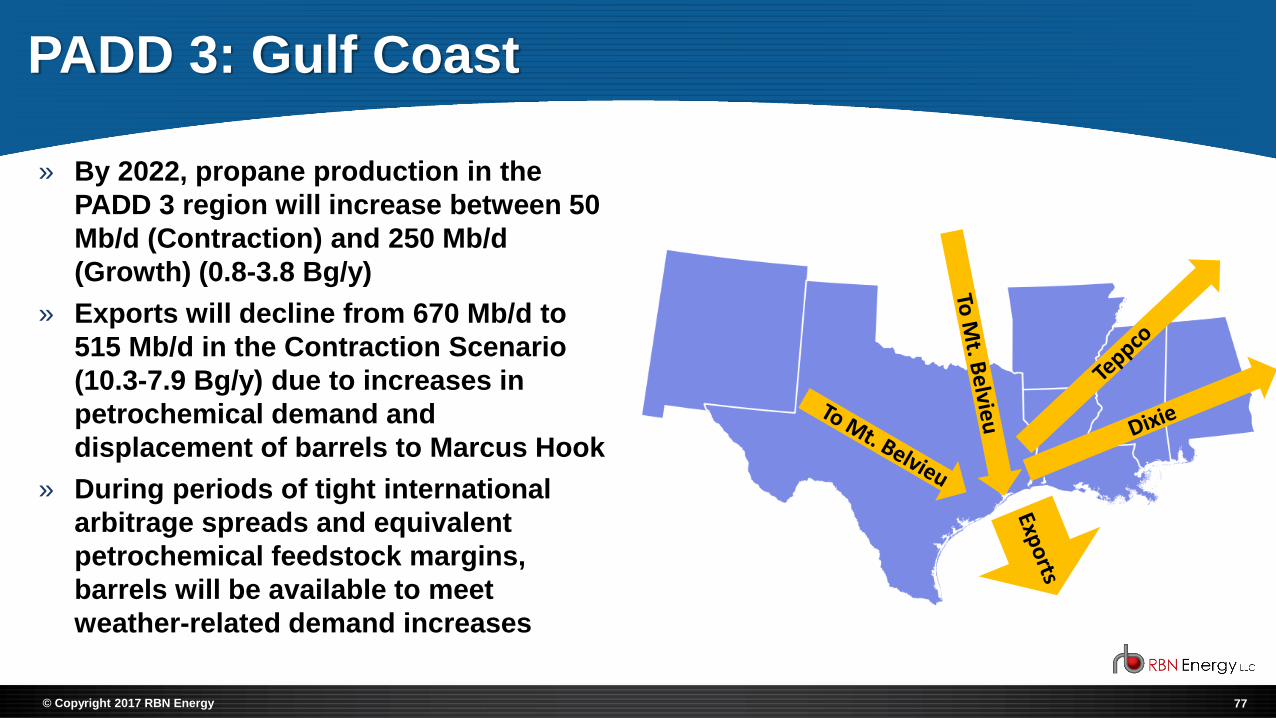

PADD 3: Gulf Coast

» By 2022, propane production in the

PADD 3 region will increase between 50

Mb/d (Contraction) and 250 Mb/d

(Growth) (0.8-3.8 Bg/y)

» Exports will decline from 670 Mb/d to

515 Mb/d in the Contraction Scenario

(10.3-7.9 Bg/y) due to increases in

petrochemical demand and

displacement of barrels to Marcus Hook

» During periods of tight international

arbitrage spreads and equivalent

petrochemical feedstock margins,

barrels will be available to meet

weather-related demand increases

78© Copyright 2017 RBN Energy

PADDs 4 and 5

» By 2022, propane production in the PADD 4 region will

increase to between 130 Mb/d (contraction) and 145 Mb/d

(growth) (2-2.2 Bg/y)

» 64 Mb/d (contraction) to 72 Mb/d (growth) of Bakken

propane (in y-grade) in 2020 will move from PADD 2 to

PADD 4, then move back to Conway, KS (PADD 2) on

Overland Pass (1-1.1 Bg/y)

» PADD 5 production is essentially unchanged at 45 Mb/d

(0.7 Bg/y)

» PADD 5 will compete for Canadian barrels against exports

to Asia from Ferndale and new British Columbia terminals

79© Copyright 2017 RBN Energy

Phase I Conclusions: Current Market Environment

» In the 3.5 years since the Polar Vortex of 2013-14, propane production has flattened, propane exports have doubled, rail has become a much more integral part of the propane supply chain, the spread between U.S. and international prices has collapsed, and margins for petrochemical feedstocks have converged.

» With more propane supply moving to exports than to U.S. consumer markets, international developments now exert a much greater influence over U.S. propane balances and prices. Likewise, U.S. prices and differentials to international markets impact the level of U.S. exports.

» During periods of severe weather, it is likely that the market will acquire incremental supplies from barrels otherwise destined for exports and petrochemical supplies. Propane prices will increase to a level that will result in export cargo cancellations and petchem feedstock switching. Consequently, it is less likely that U.S. inventories at major hubs will be drawn down to dangerous levels during severe weather events.

» However, this market behavior is primarily contingent on cargo cancellations. In the event that severe weather events overseas result in high demand levels for international supplies, significant U.S. price increases may be required to trigger cargo cancellations.

» Supplies sourced from cancelled cargos must be moved from export supply points (fractionators and storage feeding export demand), which during periods of severe weather will be subject to supply chain delays and disruptions.

80© Copyright 2017 RBN Energy

Phase I Conclusions: Market Outlook

» U.S. propane production is expected to increase from 1.5 MMb/d (23.0 Bg/y) in 2016 to about 1.9 MMb/d (29.1 Bg/y) in RBN’s 2022 Growth Scenario, but only to 1.6 MMb/d (24.5 Bg/y) in the 2022 Contraction Scenario. Appalachia (Marcellus/Utica) and Texas (Permian) will be the highest growth regions.

» In the Growth Scenario, supplies are abundant and exports continue to increase. There is enough supply to meet rising Marcus Hook exports, based on Mariner East II capacity (…but not ME2X or Mariner East II expansion, which would require incremental rail/pipeline receipts).

» Propane prices in the Growth Scenario increase in sympathy with crude oil price increases ($70/bbl in 2022), but as a percentage of crude maintain at 55%.

» In the Contraction scenario, modest production growth and increasing demand tightens the supply/demand balance. New ethane-only crackers and increasing ethane exports bid up the price of ethane, which encourages some petrochemical crackers to run more propane. Propane exports decline slightly due to declining surpluses, and some volumes shift from the Gulf Coast to the Northeast due to minimum commitments from Marcus Hook.

» Propane prices in the Contraction Scenario are constrained by lower prices of crude oil, but due to tighter supplies increase in relation to crude, up to 60% in the normal weather case.

81© Copyright 2017 RBN Energy

Phase I Conclusions: Market Outlook (Continued)

» Propane transportation by rail continues to increase, becoming still more important component of the propane supply chain.

» With increasing Appalachian production near Northeast and Midwest demand regions, better rail connectivity, and export volumes that can be bid away from global markets, the U.S. propane industry is in a better position to handle a “Polar Vortex” event than it was in the Winter of 2013-14.

» However, prices have the potential to be quite volatile in any weather-related event, since it is only higher prices that will bid supplies away from international and petrochemical markets.

» Extreme price volatility and supply chain disruptions are more likely in the Contraction Scenario than the Growth Scenario due to a lower absolute level of supply availability.

© Copyright 2017 RBN Energy

U.S. Propane Regional/ Infrastructure Analysis

83© Copyright 2017 RBN Energy

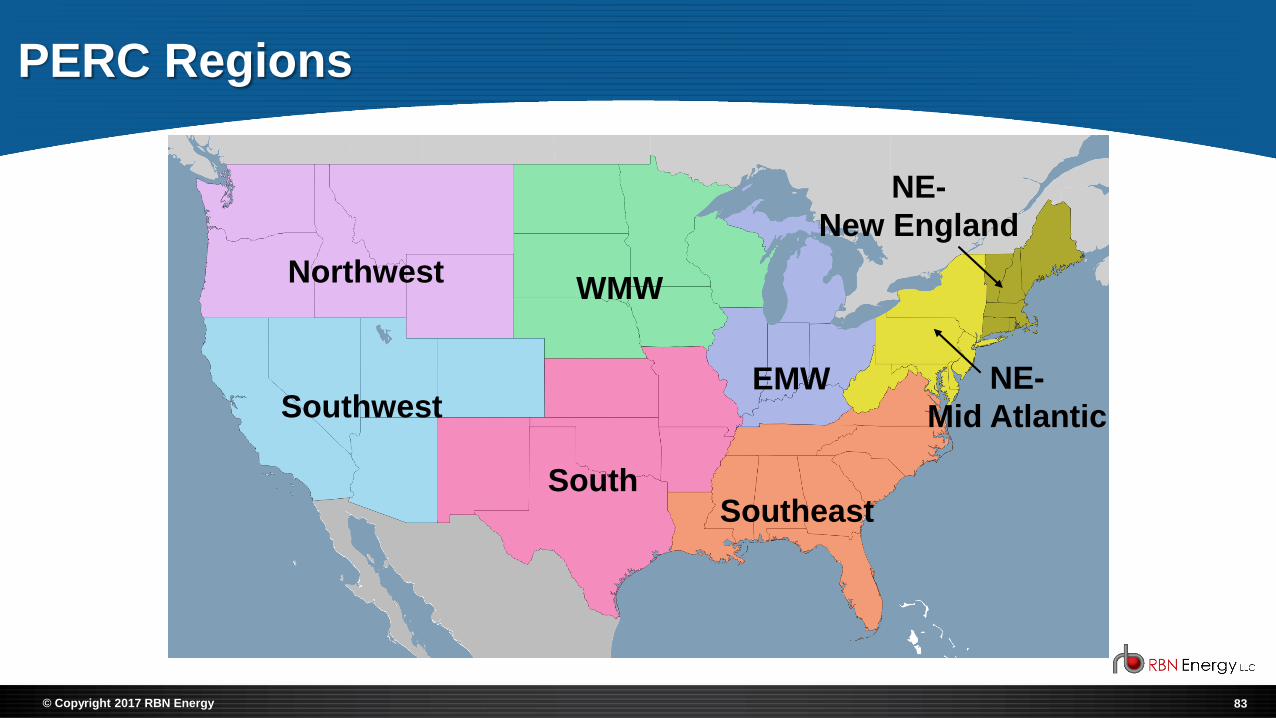

PERC Regions

Northwest

Southwest

WMW

SouthSoutheast

EMW

NE-

New England

NE-

Mid Atlantic

84© Copyright 2017 RBN Energy

U.S Propane Demand

Agricultural5%

Chemical55%

Commercial9%

Industrial2%

Other5%

Residential24%

Sectors

Source: API 2015; Includes Propylene

New England4% MidAtlantic

7%

Southeast23%

Southwest5%

EMW8%WMW

8%Northwest2%

South43%

Regions

85© Copyright 2017 RBN Energy

Supply Chain Reliability

» A retailer’s supply chain is one of its most

important investments

» The level of investment must be commensurate

with the supply chain risks faced by that retailer

» Different regional markets have widely

divergent supply chain risk factors, depending

on seasonal weather patterns, infrastructure,

and proximity to sources of supply

» Propane supply chain reliability can be

assessed (i.e., measured)▪ Regional Factor

▪ Retailer (individual company) Factor

▪ Composite Factor (combine regional and retailer)

86© Copyright 2017 RBN Energy

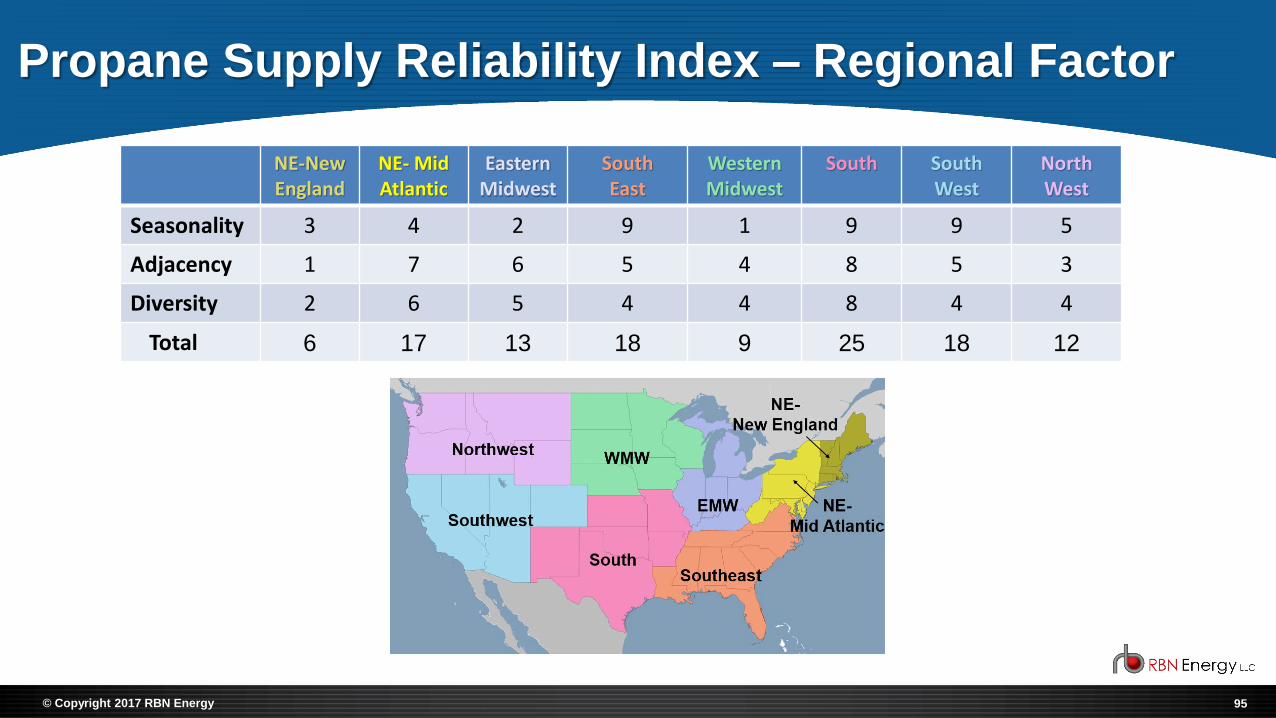

Propane Supply Reliability Index – Regional Factor

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 20 10 21 22 23 24 25 26 27 28 29 30

87© Copyright 2017 RBN Energy

Propane Supply Reliability Index - Concept

» PSRI score is a measure of propane supply risk associated with an individual propane retailer within that retailer’s geographic area

» The composite PSRI (regional factor + retailer factor) provides an indication of the supply risk associated with a specific firm’s supply profile in a given region

Regional Factor

RetailerFactor

PSRI Score

88© Copyright 2017 RBN Energy

Propane Supply Reliability Index – Regional Components

» Proximity of a market region to that region’s sources of supply. Metric is indicative of the most significant supply sources for the region.

Adjacency

Diversity

Seasonality

» The number of different supply sources for that region. Incorporates both diversity in individual supply points and number of transportation/storage alternatives available.

» Relationship of high/peak season demand to low season demand. Metric is based on average level and range of heating degree days in a region.

89© Copyright 2017 RBN Energy

Propane Supply Reliability Index - Concept

» Adjacency (10 = close to

supply, 1 = far from supply)

» Diversity (10 = several

sources of supply, 1 = few sources of supply)

» Seasonality (10 = small

seasonal swing, 1 = big seasonal swing)

Ad

jace

ncy

Diversity

Best

Worst

Regional Factor» Adjacency (access to and

reliability of local storage and supply sources)

» Diversity (supply

alternatives, including both physical and contractual terms)

» Seasonality (relationship

of peak season demand to low season demand; demand spike factor)

Retailer Factor

90© Copyright 2017 RBN Energy

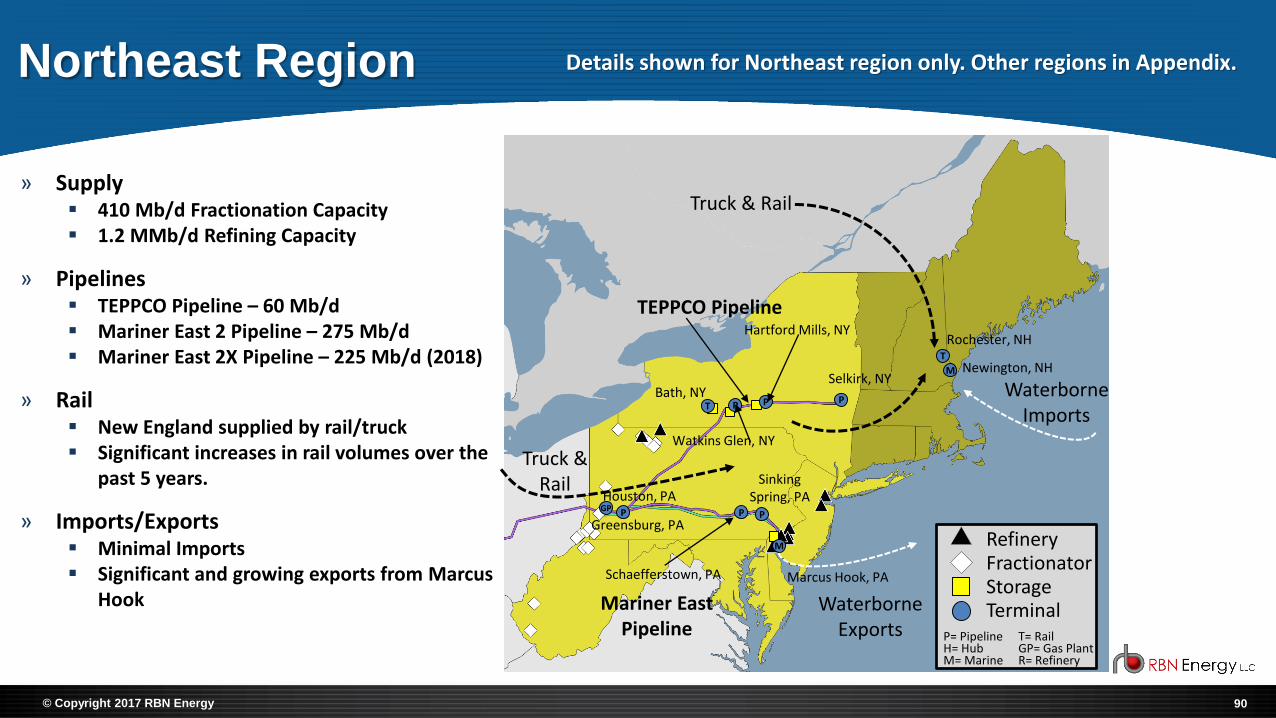

» Supply▪ 410 Mb/d Fractionation Capacity▪ 1.2 MMb/d Refining Capacity

» Pipelines▪ TEPPCO Pipeline – 60 Mb/d▪ Mariner East 2 Pipeline – 275 Mb/d▪ Mariner East 2X Pipeline – 225 Mb/d (2018)

» Rail▪ New England supplied by rail/truck▪ Significant increases in rail volumes over the

past 5 years.

» Imports/Exports▪ Minimal Imports▪ Significant and growing exports from Marcus

Hook

Northeast Region

TEPPCO Pipeline

Truck & Rail

WaterborneImports

Truck & Rail

Mariner East Pipeline

T

M

M

PT P

PPPGP

RefineryFractionatorStorageTerminal

P= PipelineH= Hub

T= RailGP= Gas Plant

M= Marine R= Refinery

Selkirk, NYBath, NY

P

Hartford Mills, NYRochester, NH

Newington, NH

Marcus Hook, PA

Sinking Spring, PA

Schaefferstown, PA

Houston, PA

Greensburg, PA

Watkins Glen, NY

WaterborneExports

Details shown for Northeast region only. Other regions in Appendix.

91© Copyright 2017 RBN Energy

Refinery

Northeast- New England Region

Fractionator

Truck & Rail

WaterborneImports

Truck & Rail

0 -

17

1 1

27

1

745 Million Gallons (49 Mb/d)

Agricultural (5) Chemical

Commercial (264) Industrial (17)

Internal Combustion (18) Residential (421)

Sales to Retailers (19)

0

200

400

600

800

1000

1200

1400

1600

# o

f H

DD

s

New England Average

WaterborneImports

Source: Map-RBN, Demand-API (includes RGP), HDDs-Bloomberg (million gallons in parenthesis, Mb/d in graphic)

M

Rochester, NH

Newington, NHT

P

Selkirk, NY

92© Copyright 2017 RBN Energy

Northeast- New England Region

Truck & Rail

Truck & Rail

WaterborneImports

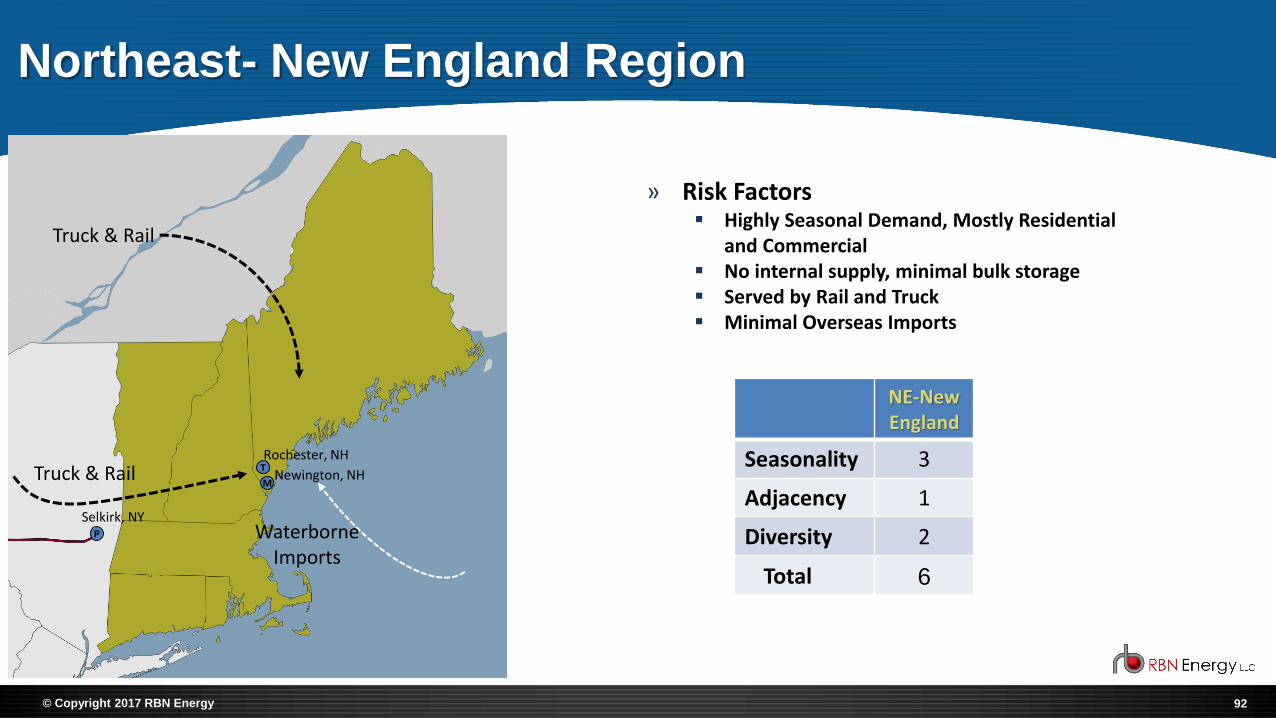

» Risk Factors▪ Highly Seasonal Demand, Mostly Residential

and Commercial▪ No internal supply, minimal bulk storage▪ Served by Rail and Truck▪ Minimal Overseas Imports

NE-New England

Seasonality 3

Adjacency 1

Diversity 2

Total 6

M

T

P

Selkirk, NY

Rochester, NH

Newington, NH

93© Copyright 2017 RBN Energy

Northeast Mid-Atlantic Region

TEPPCO Pipeline

Truck & Rail

WaterborneImports

Truck & Rail

Mariner East Pipeline

RefineryFractionatorStorageTerminal

P= PipelineH= Hub

T= RailGP= Gas Plant

M= Marine R= Refinery

3

13

15

3 4

39

3

1.2 Billion Gallons (80 Mb/d)

Agricultural (51) Chemical (206)

Commercial (277) Industrial (41)

Internal Combustion (57) Residential (600)

Sales to Retailers (45)

0

200

400

600

800

1000

1200

1400

1600

# o

f H

DD

s

Sum of Mid-Atlantic Average

Source: Map-RBN, Demand-API (includes RGP), HDDs-Bloomberg (million gallons in parenthesis, Mb/d in graphic)

M

PPPGP

Bath, NY

Hartford Mills, NY

Marcus Hook, PASchaefferstown, PA

Greensburg, PA

Watkins Glen, NY

Sinking Spring, PAHouston, PA

PPT

94© Copyright 2017 RBN Energy

TEPPCO Pipeline

Truck & Rail

WaterborneImports

Truck & Rail

RefineryFractionatorStorageTerminal

P= PipelineH= Hub

T= RailGP= Gas Plant

M= Marine R= Refinery

Mariner East Pipeline

M

P

PPGP

P

Hartford Mills, NY

Marcus Hook, PASchaefferstown, PA

Greensburg, PA

Watkins Glen, NY

Sinking Spring, PAHouston, PA

T

Northeast Mid-Atlantic Region

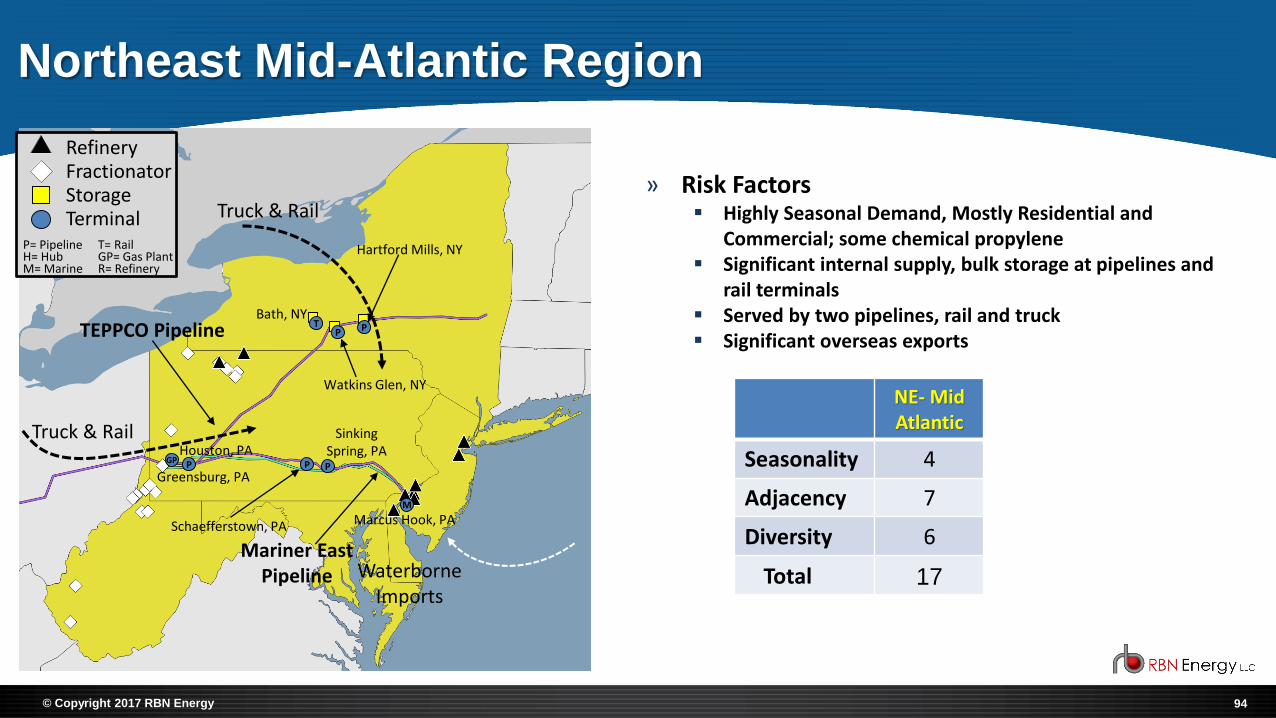

» Risk Factors▪ Highly Seasonal Demand, Mostly Residential and

Commercial; some chemical propylene▪ Significant internal supply, bulk storage at pipelines and

rail terminals▪ Served by two pipelines, rail and truck▪ Significant overseas exports

NE- Mid Atlantic

Seasonality 4

Adjacency 7

Diversity 6

Total 17

Bath, NY

P

95© Copyright 2017 RBN Energy

Propane Supply Reliability Index – Regional Factor

NE-New England

NE- Mid Atlantic

Eastern Midwest

SouthEast

Western Midwest

South South West

North West

Seasonality 3 4 2 9 1 9 9 5

Adjacency 1 7 6 5 4 8 5 3

Diversity 2 6 5 4 4 8 4 4

Total 6 17 13 18 9 25 18 12

96© Copyright 2017 RBN Energy

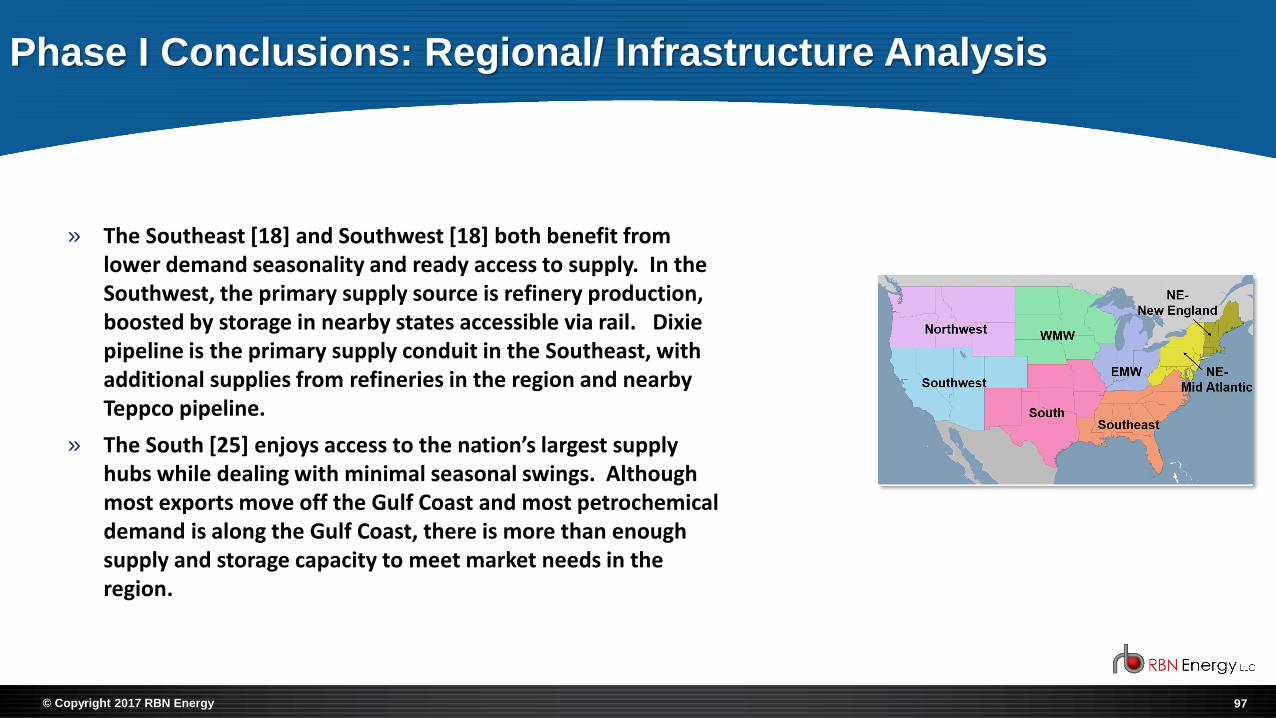

Phase I Conclusions: Regional/ Infrastructure Analysis

» Northeast-New England [6] and Western Midwest [9] must deal with huge seasonal swings in demand, which complicates supply chain planning. New England has no pipeline supply and little storage, thus is particularly vulnerable to disruption. Supply in Western Midwest has some pipeline access which improves reliability, but supply planning is complicated by the possibility of large agricultural demand spikes prior to onset of the heating demand season.

» Eastern Midwest [13] and Northeast-Mid Atlantic [17] also have significant seasonal demand swings but the regions have access to more adjacent supply sources in the form of fractionators, refineries and storage. In recent years, Northeast-Mid Atlantic has enjoyed significant increases in supplies, with much of the volume moving to market destinations via rail, which is typically more susceptible to disruption than pipeline.

» The Northwest [12] suffers from limited access to local supplies, with only a few refineries providing volumes within the area and all other barrels moved into the region via rail (both domestic and Canadian imports). While severe seasonal spikes are infrequent, when they happen the region is susceptible to supply chain disruption, such as the events of 2016-17.

97© Copyright 2017 RBN Energy

Phase I Conclusions: Regional/ Infrastructure Analysis

» The Southeast [18] and Southwest [18] both benefit from lower demand seasonality and ready access to supply. In the Southwest, the primary supply source is refinery production, boosted by storage in nearby states accessible via rail. Dixie pipeline is the primary supply conduit in the Southeast, with additional supplies from refineries in the region and nearby Teppco pipeline.

» The South [25] enjoys access to the nation’s largest supply hubs while dealing with minimal seasonal swings. Although most exports move off the Gulf Coast and most petrochemical demand is along the Gulf Coast, there is more than enough supply and storage capacity to meet market needs in the region.

98© Copyright 2017 RBN Energy

Phase I Conclusions: Strategic Propane Reserve

» In the aftermath of the Polar Vortex winter of 2013-14 there were calls to establish a “Strategic Propane Reserve” to provide additional supply reliability for the U.S. propane industry.

» If such a reserve was in a central location, there were significant doubts as to whether a Reserve would have helped during that winter. That is because most of the supply chain disruptions were due to local market and logistical glitches, not shortages at central hub locations. Thus to address supply chain disruption problems, there would need to be many such Reserves setup all across the various regions which are most susceptible to supply chain difficulties.

» Due to the wide disparity between the logistical networks in each region, any dispersed Reserve program would need to be customized for the specific area being served. By doing so, the Reserve facility would be likely to compete with commercial facilities offering similar services, creating a variety of commercial difficulties.

» Furthermore, due to the widely diverse needs of individual retail propane retailers, a program designed to incentivize investment by each retailer based on that firm’s needs is likely to be much more successful than a mandated, regional or national level Reserve.

99© Copyright 2017 RBN Energy

Propane Supply Chain and Infrastructure: Project Design

Phase II

» Overview: Phase II focused on the propane supply and distribution network, constraints that develop within that network, and strategies to mitigate those constraints.

» Progress to Date: RBN has conducted phone interviews so far with the following firms to help define and understand the Phase II project scope.

• AmeriGas • Ferrell Gas

• CHS • Targa Resources

• Crestwood Energy • Thompson Gas

100© Copyright 2017 RBN Energy

Propane Supply Chain and Infrastructure: Phase II

T

M

Rochester, NH

Newington, NH

P

Selkirk, NY

T

Walpole, NH

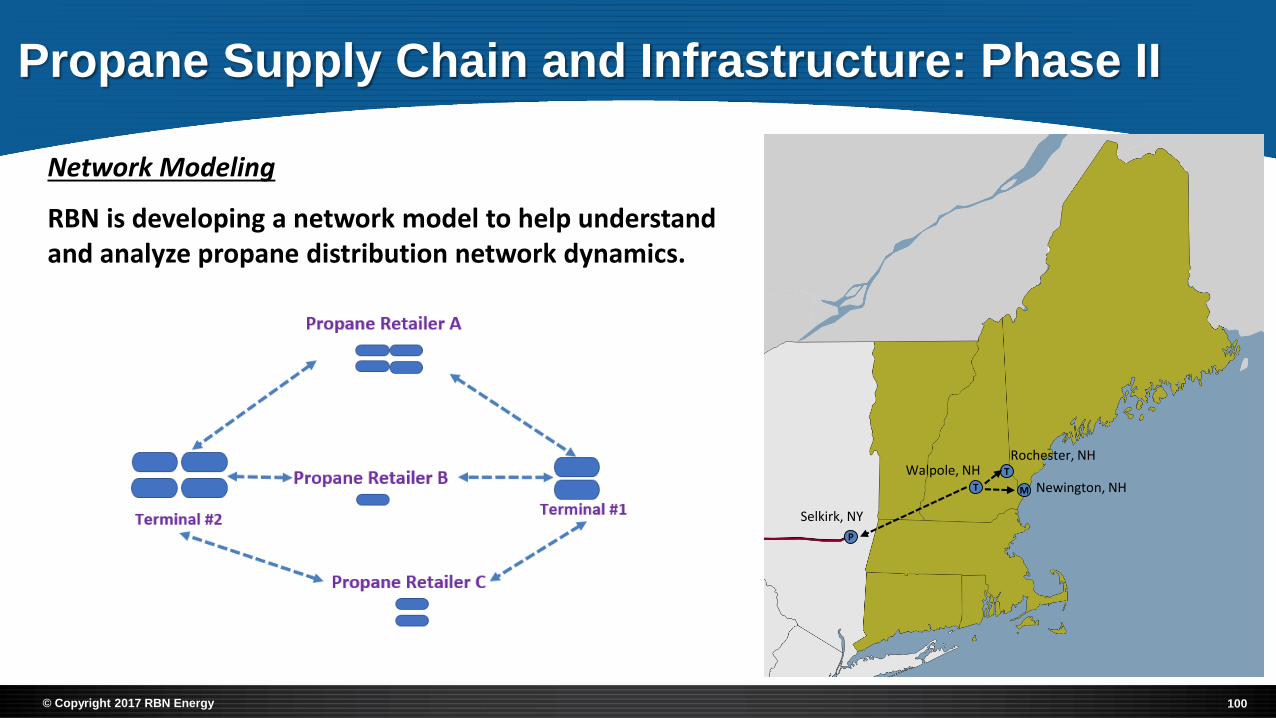

Network Modeling

RBN is developing a network model to help understand and analyze propane distribution network dynamics.

101© Copyright 2017 RBN Energy

Propane Supply Chain and Infrastructure: Phase II

Retailer Factor (Supply Chain Score)

Adjacency • “X” days of supply on hand in owned or directly controlled storage during peak season.• Distance (in hours) from primary and secondary supply points; fulfillment capacity of those supply points• Supply chain risk factors – transportation assets, transportation manpower, logistical vulnerabilities

Diversity • Number of physical supply source alternatives (physical supply source locations)• Diverse transport modes into supply sources (pipeline, rail, truck, barge, etc.)• Alternative supply pricing/contractual mechanisms (fixed/index/spot, owned/take-or-pay/spot)

Seasonality • Winter/summer ratio (relationship between average Oct-Mar demand vs. Apr-Sep)• Lowest to highest month ratio (e.g., Jan vs. Jul)• Demand spike factor (multiplier for peak period demand based on severe weather)

102© Copyright 2017 RBN Energy

Next Steps – Phase II

» Objectives for Phase II

▪ Delineate the supply chain risks faced by propane retailers related to potential severe weather events

▪ Develop a model of the propane supply network that simulates how triggering weather events can result in disruptions that cascade across the market into a specific retail propane business’s supply chain

▪ Recommend risk mitigation measures designed to minimize the impact on each propane retailer in a given region, thereby managing risk for the entire retail distribution network

» Phase II - Project Definition

▪ Scope

▪ Deliverables

▪ Timeline

103© Copyright 2017 RBN Energy

104© Copyright 2017 RBN Energy

The Domino Effect

“This book is about understanding

energy markets: prices, flows, infrastructure, value, and economics.”

Book about energy markets

From Rusty Braziel

www.thedominoeffect.com

© Copyright 2017 RBN Energy

Appendix I: Regional Infrastructure Analysis

106© Copyright 2017 RBN Energy

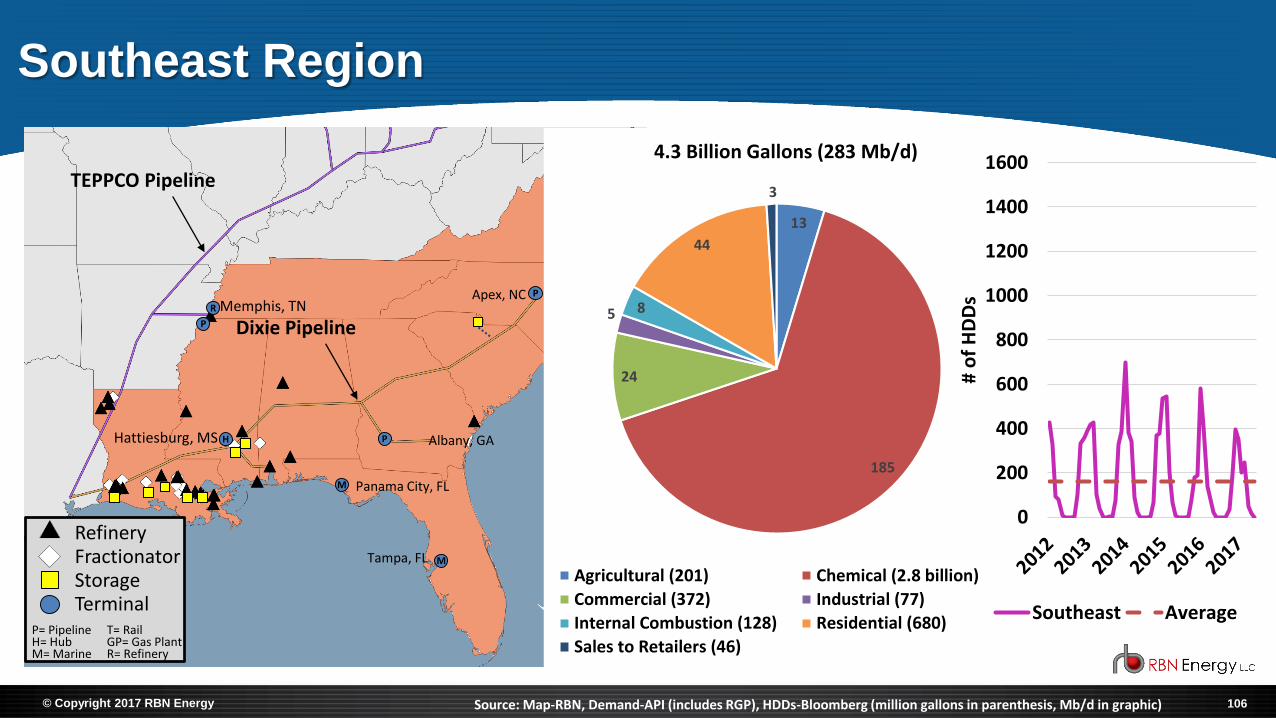

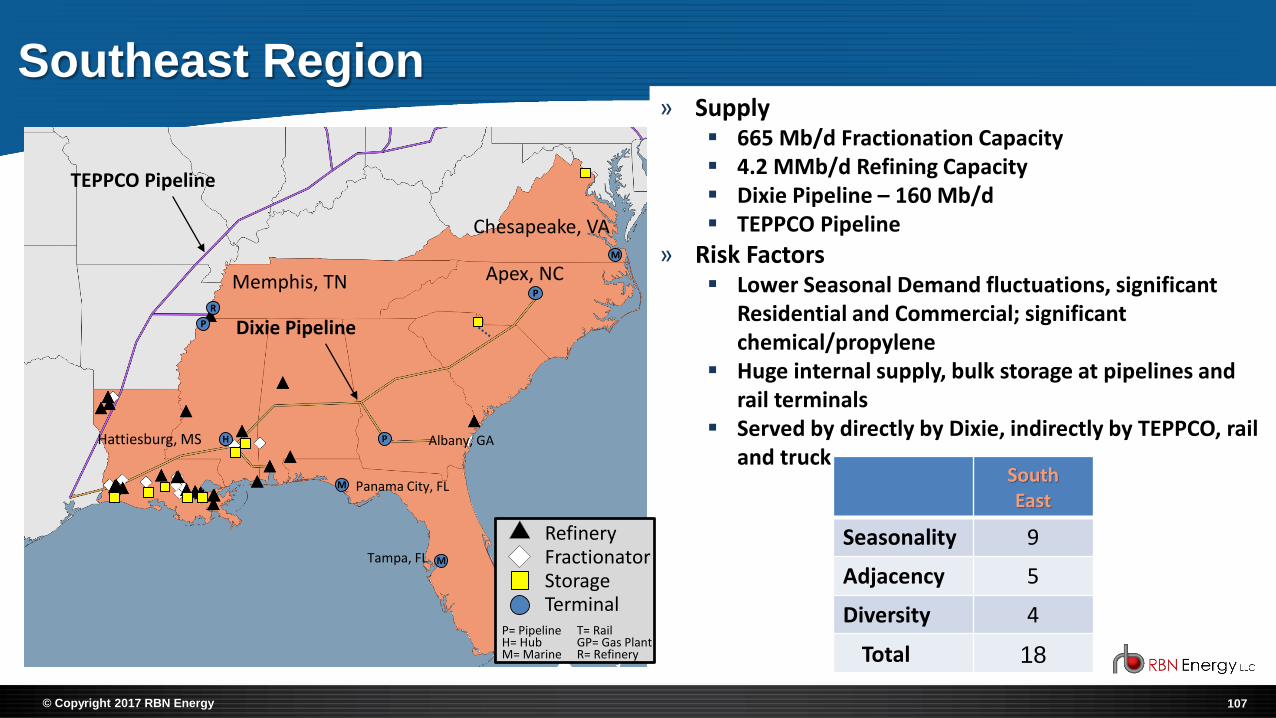

Southeast Region

Dixie Pipeline

RefineryFractionatorStorageTerminal

P= PipelineH= Hub

T= RailGP= Gas Plant

M= Marine R= Refinery

M

R

M

P

P

M

PH

Apex, NC

TEPPCO Pipeline

Memphis, TN

Hattiesburg, MS Albany, GA

Panama City, FL

Tampa, FL

13

185

24

5 8

44

3

4.3 Billion Gallons (283 Mb/d)

Agricultural (201) Chemical (2.8 billion)

Commercial (372) Industrial (77)

Internal Combustion (128) Residential (680)

Sales to Retailers (46)

0

200

400

600

800

1000

1200

1400

1600

# o

f H

DD

s

Southeast Average

Source: Map-RBN, Demand-API (includes RGP), HDDs-Bloomberg (million gallons in parenthesis, Mb/d in graphic)

107© Copyright 2017 RBN Energy

Southeast Region

Dixie Pipeline

RefineryFractionatorStorageTerminal

P= PipelineH= Hub

T= RailGP= Gas Plant

M= Marine R= Refinery

M

R

M

P

P

M

PH

Apex, NC

Chesapeake, VA

TEPPCO Pipeline

Memphis, TN

Hattiesburg, MS Albany, GA

Panama City, FL

Tampa, FL

» Supply▪ 665 Mb/d Fractionation Capacity▪ 4.2 MMb/d Refining Capacity▪ Dixie Pipeline – 160 Mb/d▪ TEPPCO Pipeline

» Risk Factors▪ Lower Seasonal Demand fluctuations, significant

Residential and Commercial; significant chemical/propylene

▪ Huge internal supply, bulk storage at pipelines and rail terminals

▪ Served by directly by Dixie, indirectly by TEPPCO, rail and truck

SouthEast

Seasonality 9

Adjacency 5

Diversity 4

Total 18

108© Copyright 2017 RBN Energy

Western Midwest Region

EnterpriseMAPL Pipeline

ONEOK North Pipeline

NuStarEast Sys. Pipeline

Alliance Pipeline

RefineryFractionatorStorageTerminal

P= PipelineH= Hub

T= RailGP= Gas Plant

M= Marine R= Refinery

P

T

P

Iowa City, IA

Pine Bend, MN

Superior, WI

20

5

9

5

4

52

1

1.5 Billion Gallons (96 Mb/d)

Agricultural (303) Chemical (71)

Commercial (138) Industrial (76)

Internal Combustion (66) Residential (801)

Sales to Retailers (19)

0

200

400

600

800

1000

1200

1400

1600

# o

f H

DD

s

WMW Average

Source: Map-RBN, Demand-API (includes RGP), HDDs-Bloomberg (million gallons in parenthesis, Mb/d in graphic)

109© Copyright 2017 RBN Energy

Western Midwest Region

EnterpriseMAPL Pipeline

ONEOK North Pipeline

NuStarEast Sys. Pipeline

Alliance Pipeline

RefineryFractionatorStorageTerminal

P= PipelineH= Hub

T= RailGP= Gas Plant

M= Marine R= Refinery

P

T

P

Iowa City, IA

Pine Bend, MN

Superior, WI

» Supply▪ 26 Mb/d Fractionation Capacity▪ 480 Mb/d Refining Capacity▪ MAPL Pipeline ▪ ONEOK North Pipeline -- 125 Mb/d

» Risk Factors▪ Highly Seasonal Demand, Largest agricultural

demand sector▪ Served by pipelines, rail and truck▪ Significant rail imports from Canada

Western Midwest

Seasonality 1

Adjacency 4

Diversity 4

Total 9

110© Copyright 2017 RBN Energy

Eastern Midwest Region

RefineryFractionatorStorageTerminal

P= PipelineH= Hub

R= RailGP= Gas Plant

M= Marine R= Refinery

T T

P

GP

East St Louis, IL

Marysville, MI

St. Clair, MI

Hopedale, OH

9 2

9

5

7

61

2

1.5 Billion Gallons (95 Mb/d)

Agricultural (145) Chemical (29)

Commercial (134) Industrial (76)

Internal Combustion (111) Residential (933)

Sales to Retailers (34)

0

200

400

600

800

1000

1200

1400

1600

# o

f H

DD

s

EMW Average

Source: Map-RBN, Demand-API (includes RGP), HDDs-Bloomberg (million gallons in parenthesis, Mb/d in graphic)

111© Copyright 2017 RBN Energy

Eastern Midwest Region

RefineryFractionatorStorageTerminal

P= PipelineH= Hub

R= RailGP= Gas Plant

M= Marine R= Refinery

T T

P

GP

East St Louis, IL

Marysville, MI

St. Clair, MI

» Supply▪ 466 Mb/d Fractionation Capacity▪ 2.3 MMb/d Refining Capacity▪ MAPL Pipeline – 275 Mb/d▪ TEPPCO Pipeline – 60 Mb/d▪ Marysville Storage

» Risk Factors▪ Highly Seasonal Demand, largest residential sector in the U.S.▪ Significant new Utica production in Ohio▪ Served by pipelines, rail and truck▪ Canadian barrels delivered into Aux Sable via Alliance

Eastern Midwest

Seasonality 2

Adjacency 6

Diversity 5

Total 13

Hopedale, OH

112© Copyright 2017 RBN Energy

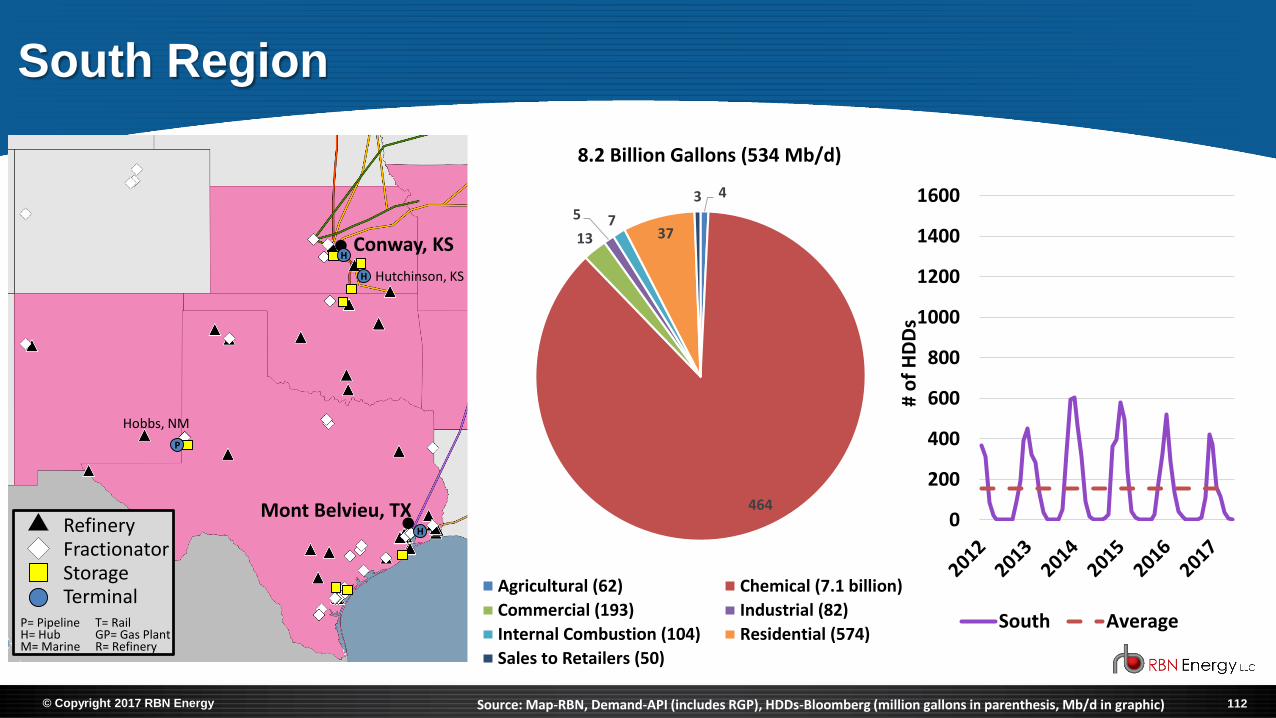

South Region

Conway, KS

Mont Belvieu, TXRefineryFractionatorStorageTerminal

P= PipelineH= Hub

T= RailGP= Gas Plant

M= Marine R= Refinery

H

P

H

H

Hobbs, NM

Hutchinson, KS

4

464

13

5 7 37

3

8.2 Billion Gallons (534 Mb/d)

Agricultural (62) Chemical (7.1 billion)

Commercial (193) Industrial (82)

Internal Combustion (104) Residential (574)

Sales to Retailers (50)

0

200

400

600

800

1000

1200

1400

1600

# o

f H

DD

s

South Average

Source: Map-RBN, Demand-API (includes RGP), HDDs-Bloomberg (million gallons in parenthesis, Mb/d in graphic)

113© Copyright 2017 RBN Energy

South Region

Conway, KS

Mont Belvieu, TXRefineryFractionatorStorageTerminal

P= PipelineH= Hub

T= RailGP= Gas Plant

M= Marine R= Refinery

H

P

H

H

Hobbs, NM

Hutchinson, KS

» Supply▪ 3 MMb/d Fractionation Capacity▪ 6.8 MMb/d Refining Capacity▪ Mont Belvieu and Conway Storage▪ Pipelines out of the region

» Risk Factors▪ Low seasonal demand fluctuations, by far the largest

petrochemical sector▪ Growing supply, mostly from Permian▪ Huge Gulf Coast exports▪ Served by pipelines, rail and truck

South

Seasonality 9

Adjacency 8

Diversity 8

Total 25

114© Copyright 2017 RBN Energy

2 -

6

3

2

13

1

421 Million Gallons (27 Mb/d)

Agricultural (31) Chemical

Commercial (91) Industrial (42)

Internal Combustion (38) Residential (200)

Sales to Retailers (19)

Northwest Region

Opal, WY

Ferndale, WA

Casper, WYRefineryFractionatorStorageTerminal

P= PipelineH= Hub

T= RailGP= Gas Plant

M= Marine R= Refinery 0

200

400

600

800

1000

1200

1400

1600

# o

f H

DD

s

Northwest Average

Source: Map-RBN, Demand-API (includes RGP), HDDs-Bloomberg (million gallons in parenthesis, Mb/d in graphic)

M

PGP

GP

115© Copyright 2017 RBN Energy

Northwest Region

RefineryFractionatorStorageTerminal

P= PipelineH= Hub

T= RailGP= Gas Plant

M= Marine R= Refinery

» Supply▪ 55 Mb/d Fractionation Capacity▪ 985 Mb/d Refining Capacity▪ Export capacity from Ferndale, WA▪ Significant rail imports from Canada

» Risk Factors▪ Moderate seasonal demand fluctuations, relatively

small market▪ Coastal demand distant from Rockies supply▪ Served by rail and truck▪ Increasing competition from Canadian exports to Asia

North West

Seasonality 5

Adjacency 3

Diversity 4

Total 12

M Ferndale, WA

PGP

GPCasper, WY

Opal, WY

116© Copyright 2017 RBN Energy

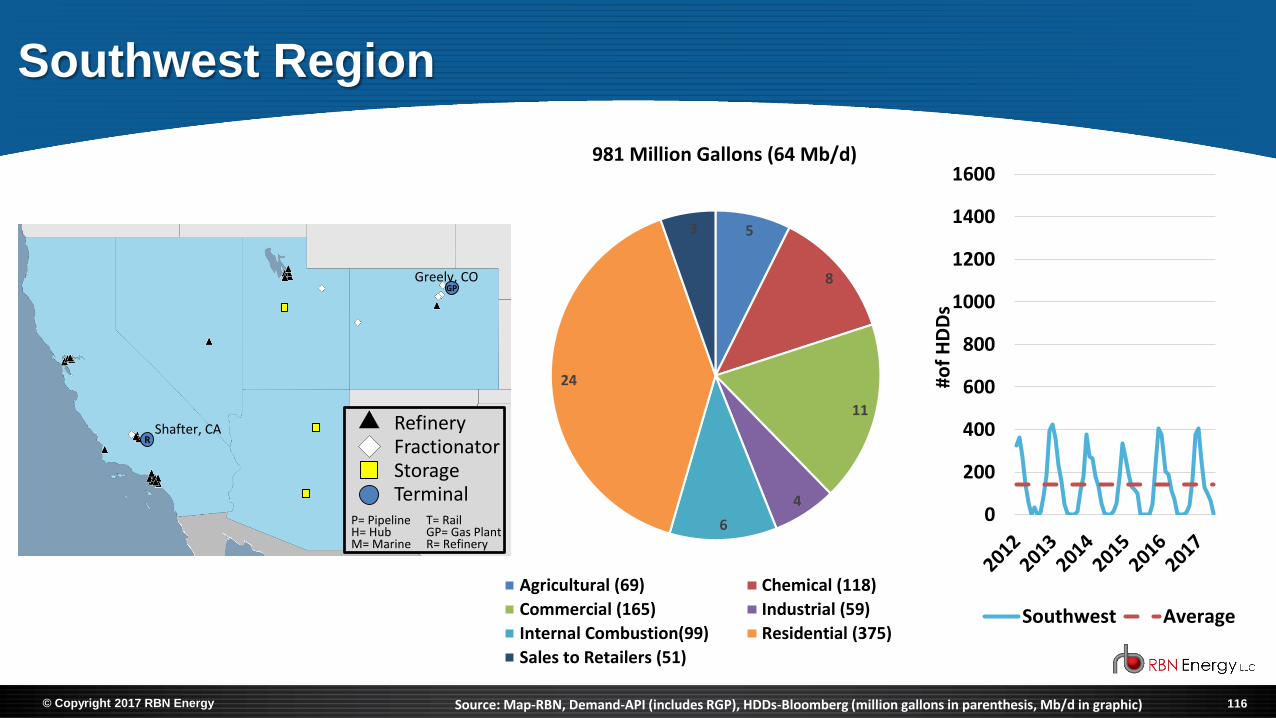

5

8

11

4

6

24

3

981 Million Gallons (64 Mb/d)

Agricultural (69) Chemical (118)

Commercial (165) Industrial (59)

Internal Combustion(99) Residential (375)

Sales to Retailers (51)

Southwest Region

Greely, CO

Shafter, CA RefineryFractionatorStorageTerminal

P= PipelineH= Hub

T= RailGP= Gas Plant

M= Marine R= Refinery

0

200

400

600

800

1000

1200

1400

1600

#of

HD

Ds

Southwest Average

Source: Map-RBN, Demand-API (includes RGP), HDDs-Bloomberg (million gallons in parenthesis, Mb/d in graphic)

R

GP

117© Copyright 2017 RBN Energy

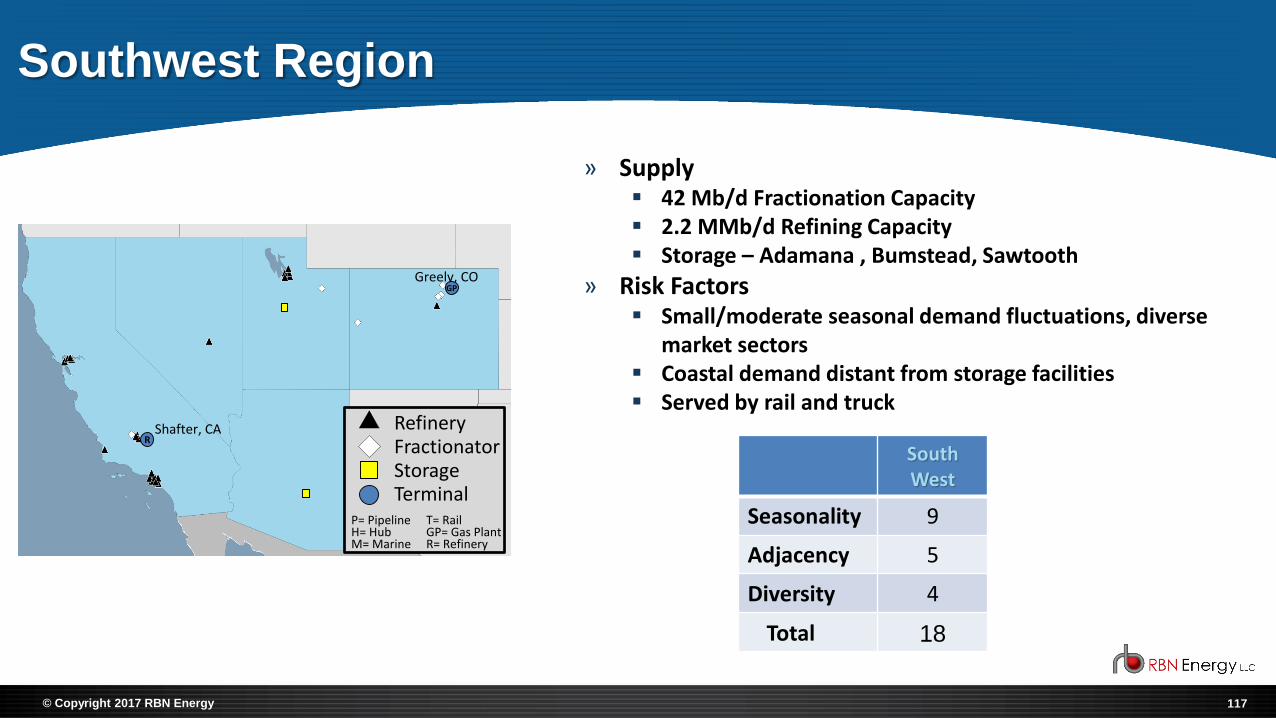

Southwest Region

Greely, CO

Shafter, CA RefineryFractionatorStorageTerminal

P= PipelineH= Hub

T= RailGP= Gas Plant

M= Marine R= Refinery

» Supply▪ 42 Mb/d Fractionation Capacity▪ 2.2 MMb/d Refining Capacity▪ Storage – Adamana , Bumstead, Sawtooth

» Risk Factors▪ Small/moderate seasonal demand fluctuations, diverse

market sectors▪ Coastal demand distant from storage facilities▪ Served by rail and truck

South West

Seasonality 9

Adjacency 5

Diversity 4

Total 18

GP

R

© Copyright 2017 RBN Energy

Appendix II: Supply/Demand Analysis

119© Copyright 2017 RBN Energy

8.5

8.6

8.7

8.8

8.9

9.0

9.1

9.2

9.3

9.4

MM

B/d

U.S. Crude Oil Production

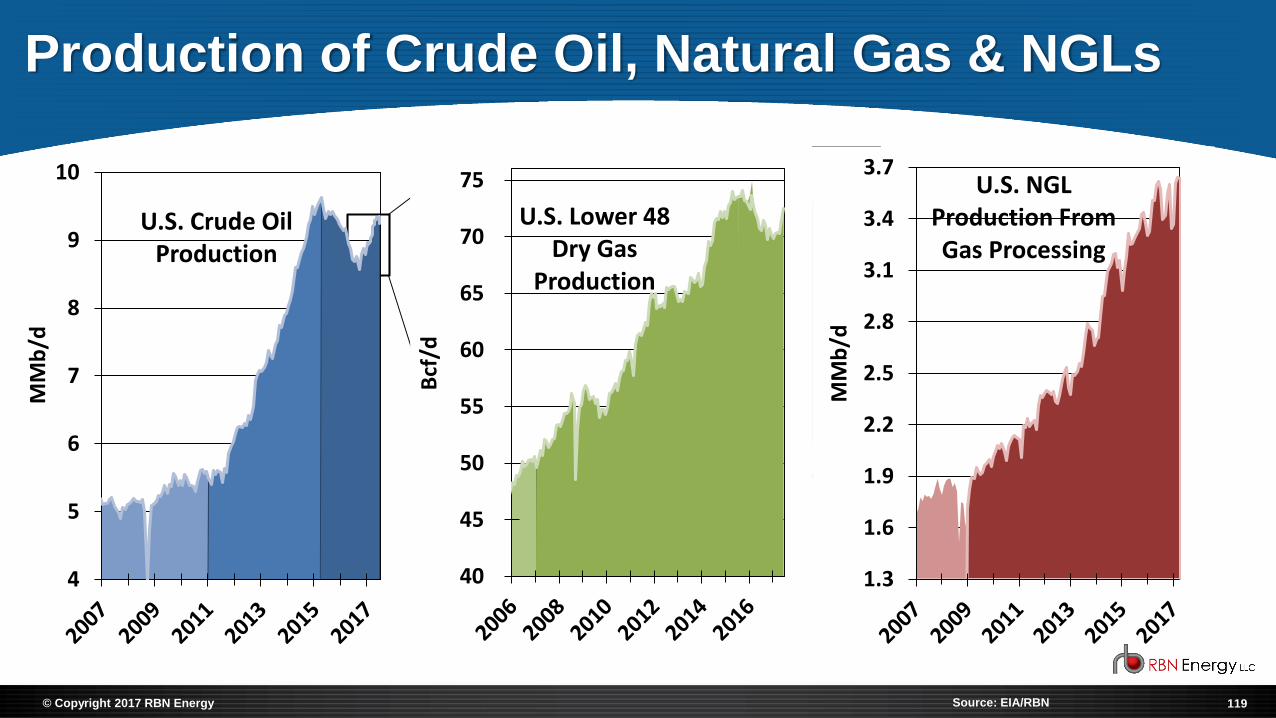

Production of Crude Oil, Natural Gas & NGLs

Source: EIA/RBN

4

5

6

7

8

9

10

MM

b/d

U.S. Crude Oil Production

40

45

50

55

60

65

70

75

Bcf

/d

U.S. Lower 48 Dry Gas

Production

1.3

1.6

1.9

2.2

2.5

2.8

3.1

3.4

3.7

MM

b/d

U.S. NGLProduction From Gas Processing

120© Copyright 2017 RBN Energy

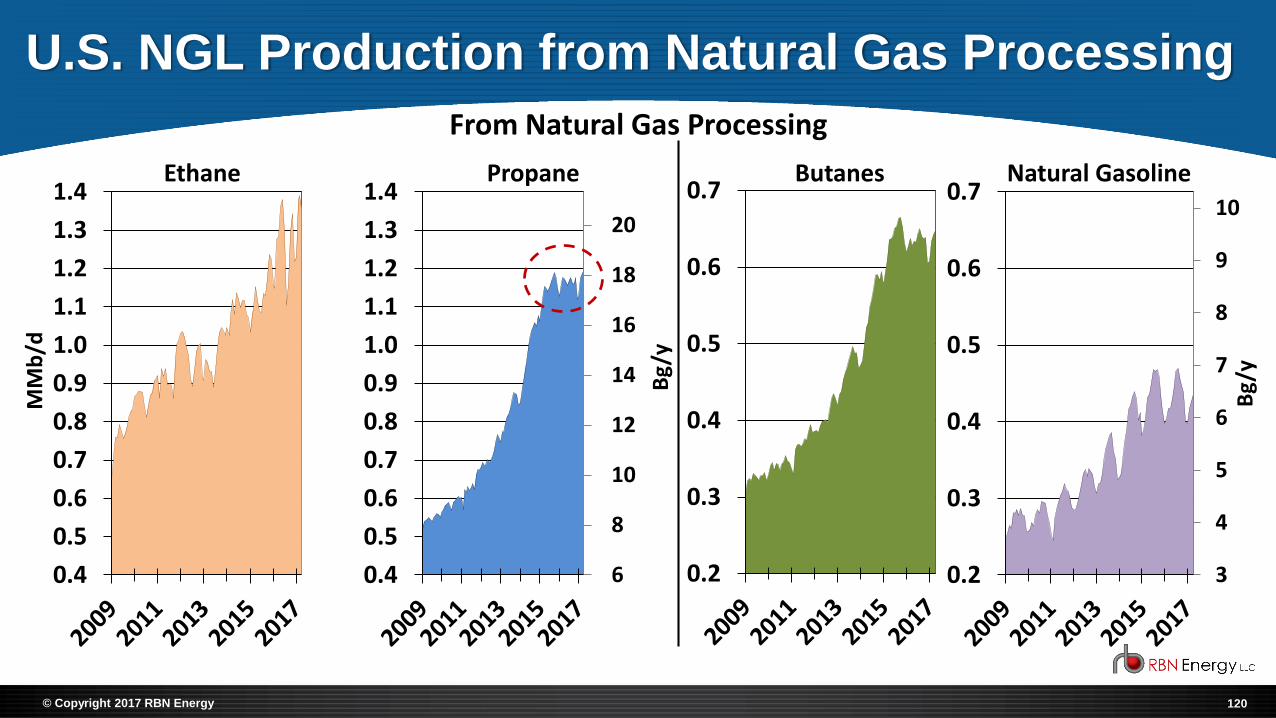

U.S. NGL Production from Natural Gas Processing

0.2

0.3

0.4

0.5

0.6

0.7Butanes

From Natural Gas Processing

3

4

5

6

7

8

9

10

0.2

0.3

0.4

0.5

0.6

0.7

Bg/

y

Natural Gasoline

6

8

10

12

14

16

18

20

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

1.4

Bg/

y

Propane

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

1.4

MM

b/d

Ethane

121© Copyright 2017 RBN Energy

U.S. LPG Exports (Propane & Butane)

-

2

4

6

8

10

12

14

16

-

200

400

600

800

1,000

Bg/

y

U.S. Total Overseas LPG Exports

West Coast

East Coast

Gulf Coast

Mb

/d

-

200

400

600

800

1,000

U.S. Total LPG Imports

Mb

/d

Source: RBN NGL Voyager Report

122© Copyright 2017 RBN Energy

Europe - Mt. Belvieu Propane Arb (Price Differential)

-20

0

20

40

60

80

c/ga

l

123© Copyright 2017 RBN Energy

Methodology: U.S. Propane Supply/Demand Balance

Propane Supply

Propane Demand

124© Copyright 2017 RBN Energy

U.S. Propane Supply Scenarios

Crude Oil Price

Natural Gas Price

Crude Oil Production

Natural Gas

Production

Gas Plant NGL

Production

Refinery Runs

Propane Production

Propane Imports

Propane Supply

125© Copyright 2017 RBN Energy

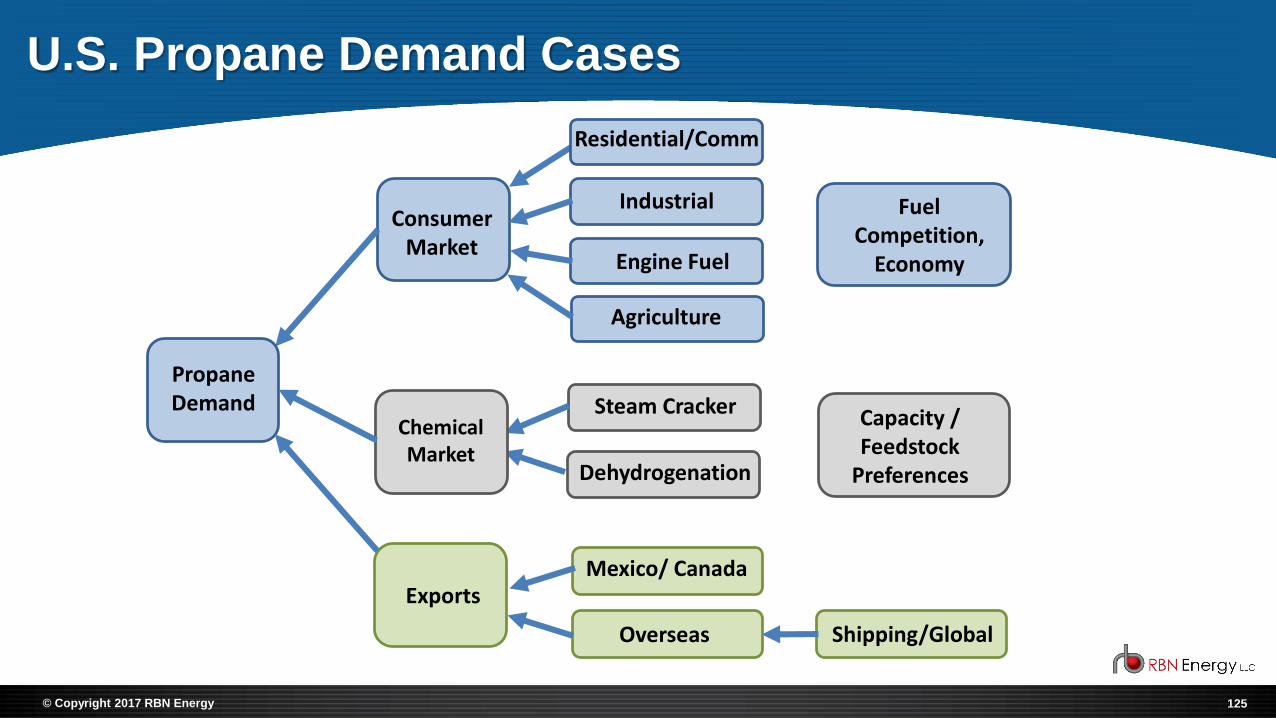

U.S. Propane Demand Cases

Consumer Market

Propane Demand

Exports

Fuel Competition,

Economy

Industrial

Engine Fuel

Agriculture

Residential/Comm

Capacity / Feedstock

Preferences

Steam Cracker

Dehydrogenation

Mexico/ Canada

Overseas Shipping/Global

Chemical Market

126© Copyright 2017 RBN Energy

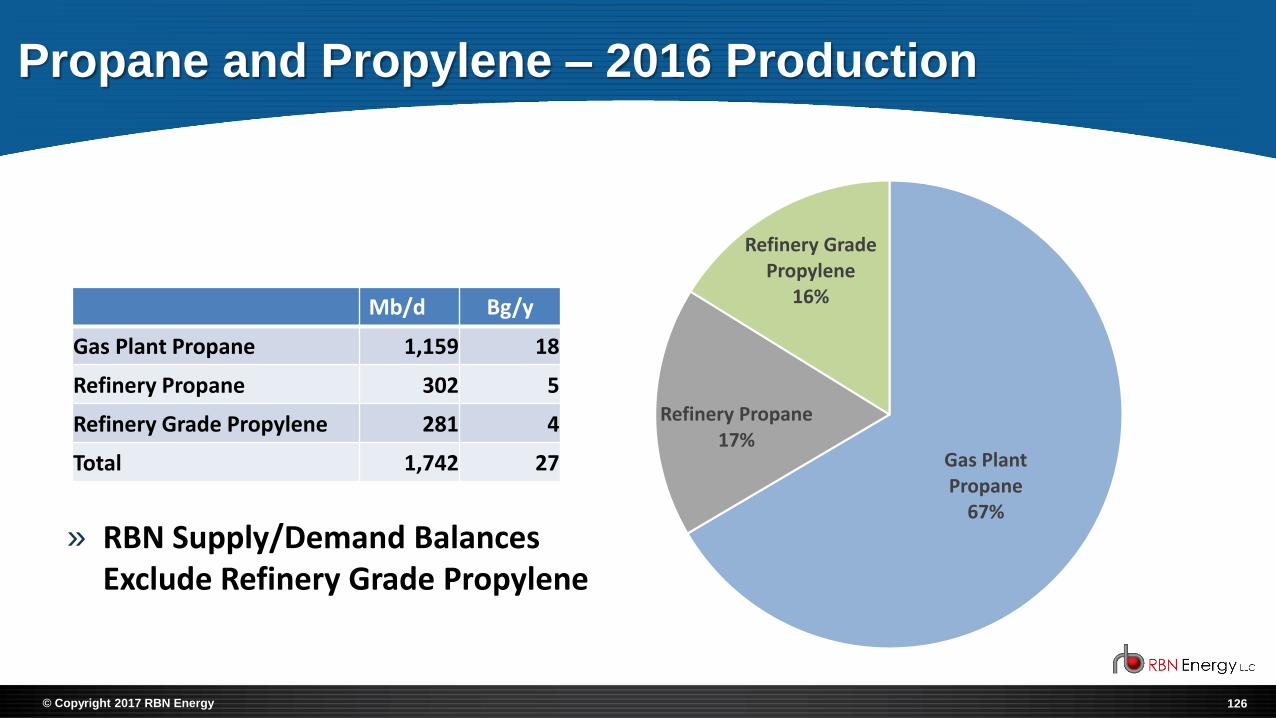

Propane and Propylene – 2016 Production

Gas Plant Propane

67%

Refinery Propane17%

Refinery Grade Propylene

16%Mb/d Bg/y

Gas Plant Propane 1,159 18

Refinery Propane 302 5

Refinery Grade Propylene 281 4

Total 1,742 27

» RBN Supply/Demand Balances Exclude Refinery Grade Propylene

127© Copyright 2017 RBN Energy

U.S. Crude Oil Production Forecast Scenarios

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

MM

b/d

2008-2015 2016-2022 Growth 2016-2022 Contraction

12.7

10.0

128© Copyright 2017 RBN Energy

Lower 48 Dry Gas Production Forecast Scenarios

0

20

40

60

80

100B

cf/d

History / Growth

+4.0 Bcf/d Per Year

+2.2 Bcf/d Per Year

0

20

40

60

80

100

Contraction Scenario

0.4 Bcf/d Per Year

129© Copyright 2017 RBN Energy

U.S. NGL Gas Plant Potential Production

» Growing volumes of ‘wet’,

high-BTU gas are driving

increases in NGL production

» Pipeline constraints out of the

Northeast and Williston Basin

keep rejection happening

through 2022

0

20

40

60

80

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500

6,000

Bg

/y

Mb

/d

NGL Production Ethane Rejection

Contraction Scenario

Growth Scenario

130© Copyright 2017 RBN Energy

Annual US – Consumer Supply

326

360

394

428

462

496

530

564

598

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

Mb

/d

Bg/

y

Growth Normal Contraction PV

131© Copyright 2017 RBN Energy

0

2

4

6

8

10

12

0

100

200

300

400

500

600

700

800

Bg/

y

Mb

/d

Existing Mariner East

Mariner East II

ME2X

Mariner East II Expansion

Contraction - Polar Vortex

Growth - Normal

* Contracted and forecasted ethane volumes removed from capacity and volumes

Marcus Hook Propane Export Capacity vs. Volumes

» Demand cases assume that the Mariner East II Expansion increases capacity to 275 Mb/d, but actual flows (Contraction) average only 81 Mb/d in 2018, even with severe weather.

» Even in the Contraction Scenario, exports are assumed to fall no lower than 50% of total capacity, due to contractual commitments and overseas demand.

132© Copyright 2017 RBN Energy

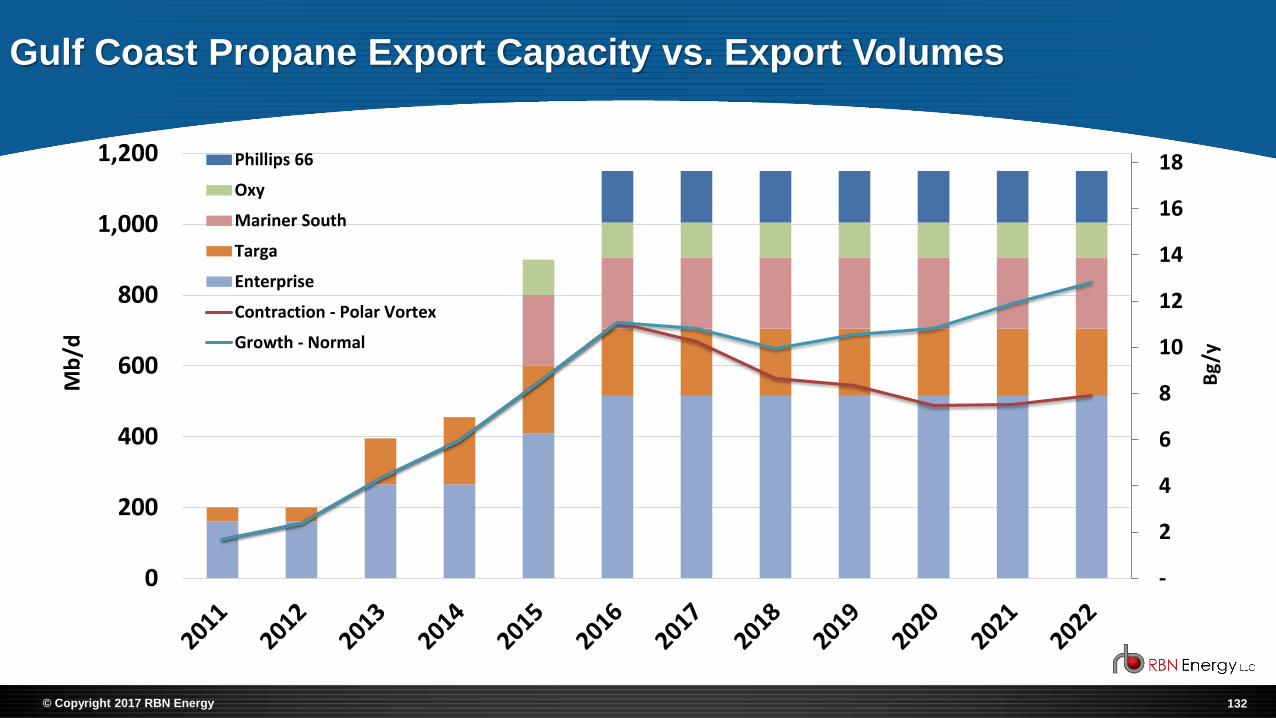

Gulf Coast Propane Export Capacity vs. Export Volumes

-

2

4

6

8

10

12

14

16

18

0

200

400

600

800

1,000

1,200

Bg

/y

Mb

/d

Phillips 66

Oxy

Mariner South

Targa

Enterprise

Contraction - Polar Vortex

Growth - Normal

133© Copyright 2017 RBN Energy

Only Under Construction Propane Dehydrogenation Units

Will be Completed by 2021 in All Cases

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

0

20

40

60

80

100

120

Bg/

y

Pro

pan

e D

em

and

Mb

/d

Petrologistics Enterprise Dow Formosa

PDH Units Under Evaluation • Marcus Hook • C3 Petrochemicals (Ascend)

» Enterprise PDH starts up in July 2017, and Formosa in 2020 adding 54 Mb/d of demand

134© Copyright 2017 RBN Energy

PADD 2 - Seasonal Supply Demand – Contraction Severe Weather

0

2

4

6

8

10

0

100

200

300

400

500

600

700

Bg

/y

Mb

/d

Supply

Production Inventory Draw Net Receipts Imports

0

100

200

300

400

500

600

700

Mb

/d

Demand

Product Supplied Net Deliveries Inventory Injection Exports

135© Copyright 2017 RBN Energy

PADD 2 – Weather Sensitivities – Contraction Severe Weather

0

1

2

3

4

5

40

90

140

190

240

290

340

Bg/

y

Mb

/d

Net Deliveries

Net Deliveries - Normal Weather

Net Deliveries - Polar Vortex

0

5

10

15

20

25

30

35

MM

bb

l

Inventories

Last 5 year Range PV 19-20

136© Copyright 2017 RBN Energy

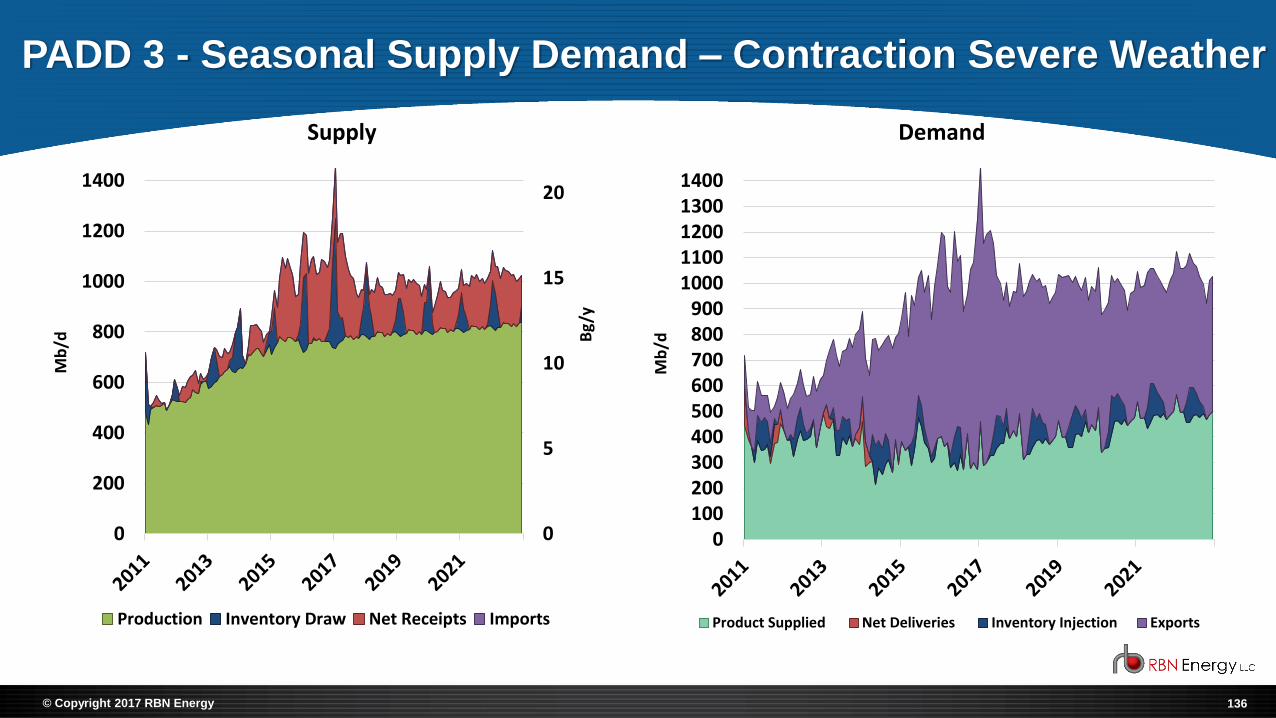

PADD 3 - Seasonal Supply Demand – Contraction Severe Weather

0

5

10

15

20

0

200

400

600

800

1000

1200

1400

Bg

/y

Mb

/d

Supply

Production Inventory Draw Net Receipts Imports

0100200300400500600700800900

10001100120013001400

Mb

/d

Demand

Product Supplied Net Deliveries Inventory Injection Exports

137© Copyright 2017 RBN Energy

PADD 3 – Weather Sensitivities – Contraction Severe Weather

6

7

8

9

10

11

12

13

14

15

400

500

600

700

800

900

1000

Bg/

y

Mb

/d

Exports

Exports - Normal Weather

Exports - Polar Vortex

0

10

20

30

40

50

60

70

MM

bb

l

Inventories

Last 5 year Range PV 19-20

138© Copyright 2017 RBN Energy

PADD 5 - Seasonal Supply Demand – Contraction Severe Weather

0

0.5

1

1.5

0

20

40

60

80

100

120

Bg

/y

Mb

/d

Supply

Production Inventory Draw Net Receipts Imports

0

20

40

60

80

100

120

Mb

/d

Demand

Product Supplied Net Deliveries Inventory Injection Exports

INDUSTRY & PUBLIC COMMENTS

PROPANE EDUCATION & RESEARCH COUNCILDENVER, COLORADO

July 11-12, 2017

PROPOSED 2018 BUDGET

Rob Chalmers

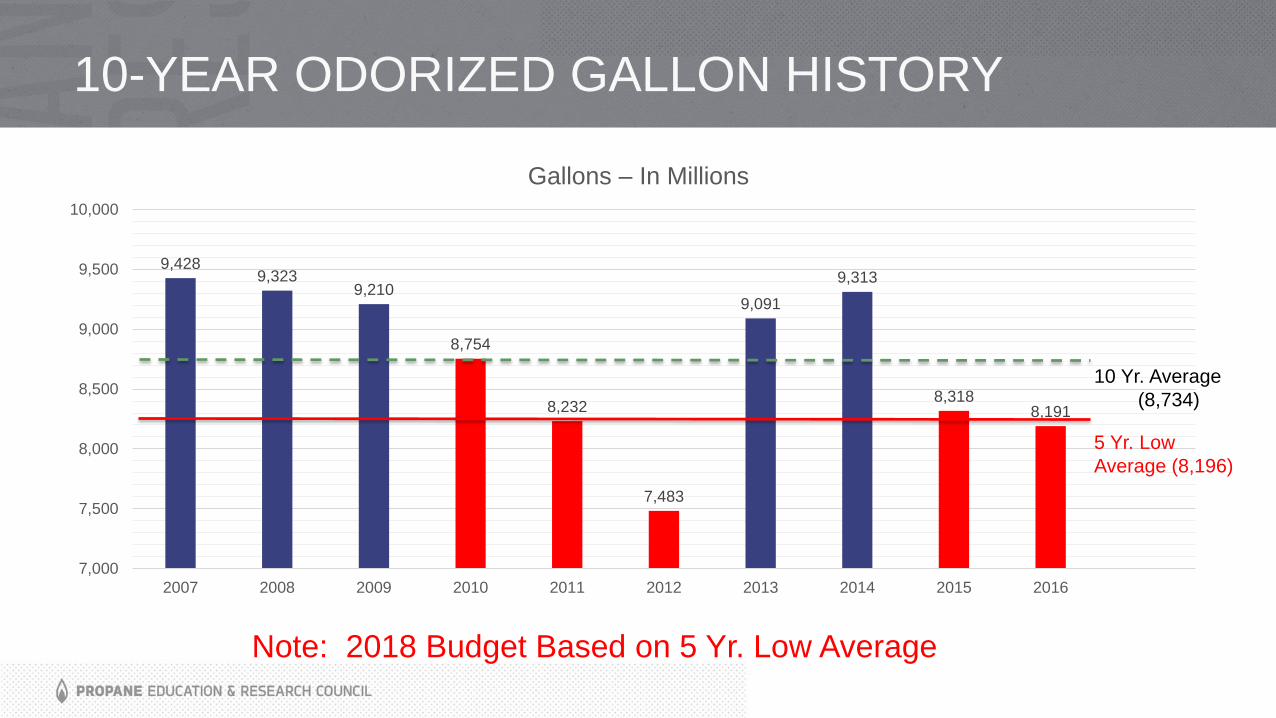

10-YEAR ODORIZED GALLON HISTORY

9,4289,323

9,210

8,754

8,232

7,483

9,091

9,313

8,3188,191

7,000

7,500

8,000

8,500

9,000

9,500

10,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Gallons – In Millions

10 Yr. Average

(8,734)

5 Yr. Low

Average (8,196)

Note: 2018 Budget Based on 5 Yr. Low Average

PROPANE EDUCATION & RESEARCH COUNCIL

2018 BUDGET FOR APPROVAL

2017 Budget

2018 Budget

Proposal

Variance

Favorable

(Unfavorable)

2018 Budget

Proposal

Variance

Favorable

(Unfavorable)

REVENUES:

Assessment Collections 38,948,400$ 36,880,120$ (2,068,280)$ 40,977,911$ 2,029,511$

Less State Rebates (7,789,680)$ (7,376,024)$ 413,656$ (8,195,582)$ (405,902)$

Net Assessment Revenue 31,158,720$ 29,504,096$ (1,654,624)$ 32,782,329$ 1,623,609$

Investment Income 164,000$ 140,000$ (24,000)$ 140,000$ (24,000)$

Fulfillment -$ -$ -$ -$ -$

Total Revenues 31,322,720$ 29,644,096$ (1,678,624)$ 32,922,329$ 1,599,609$

EXPENDITURES:

Expenses

Administrative Expenses 2,653,500$ 2,751,867$ 98,367$ 2,751,867$ 98,367$

Other Expenses:

Assessment & Collections 82,000$ 83,500$ 1,500$ 83,500$ 1,500$

Depreciation Expenses 457,000$ 485,000$ 28,000$ 485,000$ 28,000$

Total Other Expenses 539,000$ 568,500$ 29,500$ 568,500$ 29,500$

Total expenses 3,192,500$ 3,320,367$ 127,867$ 3,320,367$ 127,867$

Program Funding

Operating programs 26,338,200$ 21,643,758$ 4,694,442$ 24,921,991$ 1,416,209$

Program Labor 3,685,000$ 4,112,604$ (427,604)$ 4,112,604$ (427,604)$

Program Benefits 538,000$ 567,366$ (29,366)$ 567,366$ (29,366)$

IT Support 447,000$ 600,000$ (153,000)$ 600,000$ (153,000)$

Total Program Funding 31,008,200$ 26,923,728$ 4,084,472$ 30,201,961$ 806,239$

TOTAL EXPENDITURES 34,200,700$ 30,244,095$ 3,956,605$ 33,522,328$ 678,372$

Increase/(Decrease) in Net Assets (2,877,980)$ (600,000)$ 2,277,980$ (600,000)$ 2,277,980$

Beginning Surplus 2,630,737$ 600,000$ (2,030,737)$ 600,000$ (2,030,737)$

Add De-obligations 500,000$ 500,000$ -$ 500,000$ -$

Ending Surplus 252,757$ 500,000$ 247,243$ 500,000$ 247,243$

Capital Budget: 183,000$ 645,000$ (462,000)$ 645,000$ (462,000)$

With Rate IncreaseNo Rate Increase

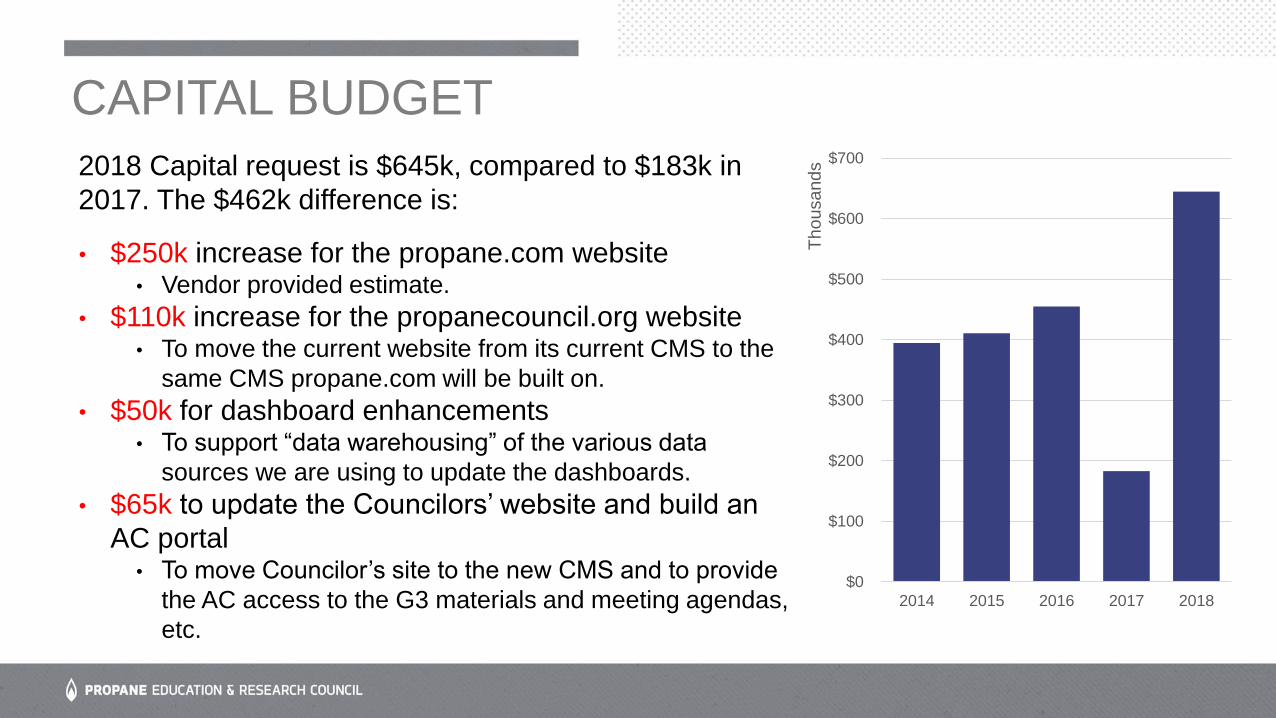

2018 Capital request is $645k, compared to $183k in

2017. The $462k difference is:

• $250k increase for the propane.com website• Vendor provided estimate.

• $110k increase for the propanecouncil.org website• To move the current website from its current CMS to the

same CMS propane.com will be built on.

• $50k for dashboard enhancements • To support “data warehousing” of the various data

sources we are using to update the dashboards.

• $65k to update the Councilors’ website and build an

AC portal • To move Councilor’s site to the new CMS and to provide

the AC access to the G3 materials and meeting agendas,

etc.

$0

$100

$200

$300

$400

$500

$600

$700

2014 2015 2016 2017 2018

Tho

usands

CAPITAL BUDGET

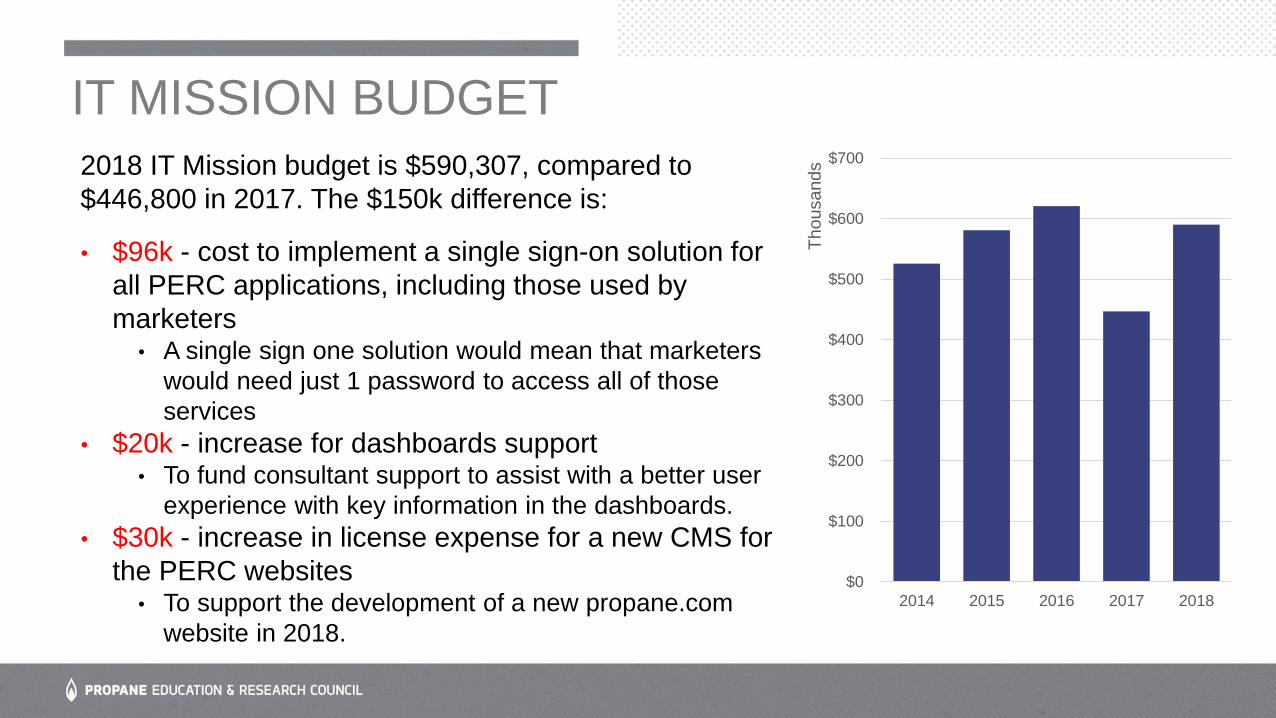

2018 IT Mission budget is $590,307, compared to

$446,800 in 2017. The $150k difference is:

• $96k - cost to implement a single sign-on solution for

all PERC applications, including those used by

marketers• A single sign one solution would mean that marketers

would need just 1 password to access all of those

services

• $20k - increase for dashboards support• To fund consultant support to assist with a better user

experience with key information in the dashboards.

• $30k - increase in license expense for a new CMS for

the PERC websites• To support the development of a new propane.com

website in 2018.

$0

$100

$200

$300

$400

$500

$600

$700

2014 2015 2016 2017 2018

Tho

usands

IT MISSION BUDGET

• Cash balances correspond to 2018 Monthly Cash Flows

• Balances

• Beginning of Year (January)

• $13M / $13.3M

• Highest Balance (April)

• $16.8M / $17.2M

• End of Year (December)

• $10.3M / $10.6M$5

$7

$9

$11

$13

$15

$17

$19

@ .45 cents

@ .5 cents

2018 PROJECTED CASH BALANCES @ .45 CENTS AND .5 CENTS PER GALLON (IN MILLIONS)

PROPOSED 2018 PROGRAM BUDGET

Strat Ranking

2018 STRATEGIC PRIORITIZATION

MOT Average

STT Average

RTD Average

Staff Average

Council (18:21)

2018 STRATEGIC RANKING

Industry Engagement - Propane Marketer Companies 25.24

Industry Engagement - State Associations 25.24

Product Development - Propane Autogas 24.76

Consumer Awareness - Construction Professionals 23.33

Safety & Technical Training - Workforce Training 22.86

Consumer Awareness - Propane Autogas 22.86

Consumer Awareness - Homeowners 22.38

Safety & Technical Training - Safety Messaging 21.43

Safety & Technical Training - Technical Training 20.95

Product Development - Residential & Commercial 20.95

Product Development - Material Handling 18.57

Product Development - Technical Innovation & Improvement 18.10

Consumer Awareness - Material Handling 17.62

Industry Engagement - National Associations 17.14

Product Development - Agriculture 16.19

Product Development - Outdoor Power Equipment 14.76

Consumer Awareness - Agriculture 14.76

Consumer Awareness - Outdoor Power Equipment 12.86

0

1

2

3

4

5

Consu

me

r A

wa

rene

ss H

om

eo

wner

Consu

me

r A

wa

rene

ss C

on

str

uction

Pro

s

Consu

me

r A

wa

rene

ss A

gricu

ltu

re

Pro

du

ct D

eve

lopm

en

t A

uto

ga

s

Ind

ustr

y E

ng

ag

em

en

t S

tate

Assns

Consu

me

r A

wa

rene

ss O

PE

Adm

inis

trative

Ind

ustr

y E

ng

ag

em

en

t N

atio

nal

Associa

tio

ns

Ind

ustr

y E

ng

ag

em

en

t M

ark

ete

rC

om

pan

ies

Consu

me

r A

wa

rene

ss A

uto

ga

s

Pro

du

ct D

eve

lopm

en

t A

gricu

ltu

re

Pro

du

ct D

eve

lopm

en

t T

ech

Inn

ovatio

n

Consu

me

r A

wa

rene

ss

Safe

ty &

Te

ch T

rain

ing E

xte

rna

l A

ud

.T

rain

ing

Safe

ty &

Te

ch T

rain

ing W

ork

forc

eT

rain

ing

Consu

me

r A

wa

rene

ss M

ate

ria

lH

and

ling

Pro

du

ct D

eve

lopm

en

t M

ate

ria

lH

and

ling

Pro

du

ct D

eve

lopm

en

t R

es/C

om

Safe

ty &

Te

ch T

rain

ing S

afe

tyM

essa

gin

g

Pro

du

ct D

eve

lopm

en

t O

PE

Mill

ion

s

PROPOSED 2018 PROGRAM BUDGET

Budget @ .45¢: $21,653,758 Budget @ 0.5¢: $24,931,991

Consumer Awareness

56%

Product Development

20%

Industry Engagement

12%

Administrative6%

Safety & Technical Training

6%

2018 PROPOSED PROGRAM BUDGET BY STRATEGIC IMPERATIVE

Consumer Awareness

60%

Product Development

18%

Industry Engagement

11%

Safety & Technical Training6%

Administrative5%

PROPOSED 2018 PROGRAM BUDGET –ACTIVITY TYPE

$0

$2

$4

$6

$8

$10

$12

$14

Mill

ions

2017 2018 - 0.45¢ 2018 - 0.5¢

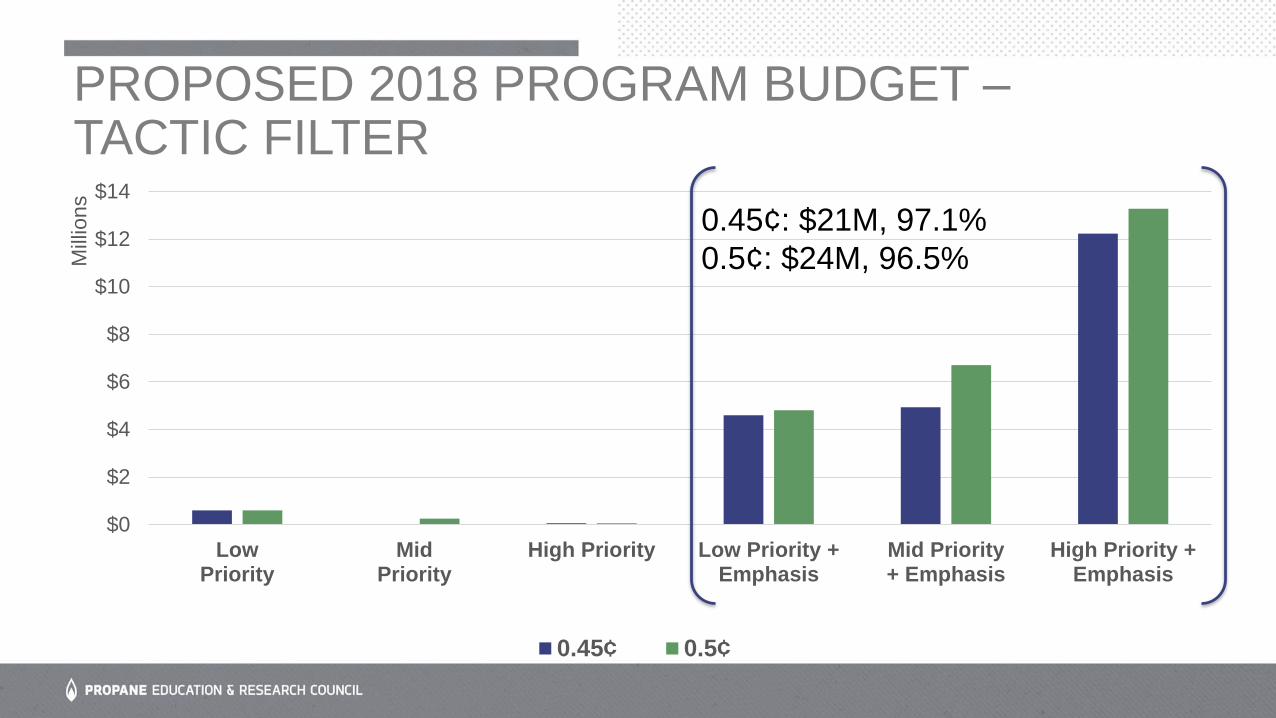

PROPOSED 2018 PROGRAM BUDGET –TACTIC FILTER

$0

$2

$4

$6

$8

$10

$12

$14

LowPriority

MidPriority

High Priority Low Priority +Emphasis

Mid Priority+ Emphasis

High Priority +Emphasis

Mill

ions

0.45¢ 0.5¢

0.45¢: $21M, 97.1%

0.5¢: $24M, 96.5%

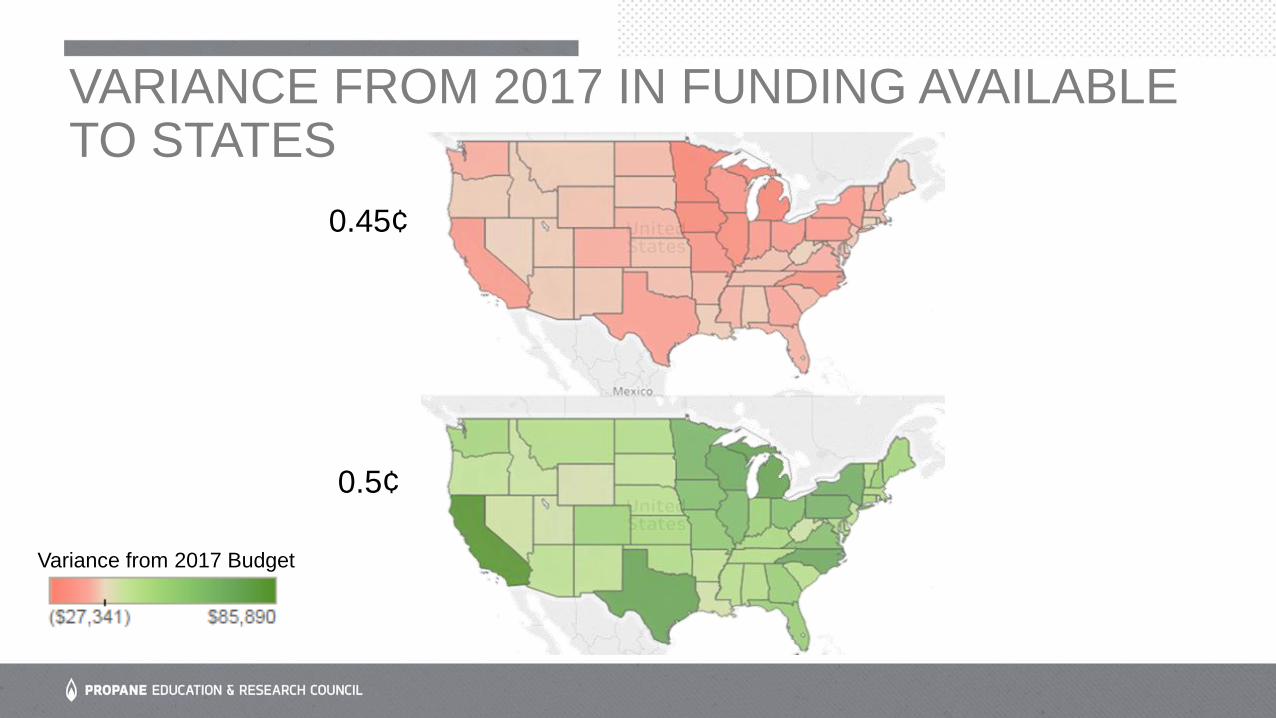

VARIANCE FROM 2017 IN FUNDING AVAILABLE TO STATES

Variance from 2017 Budget

0.45¢

0.5¢

CHIEF MARKETING OFFICER’S REPORT

Dennis Vegas

NATIONAL CONSUMERBRAND CAMPAIGN

Integrated Brand

“Propane Clean American Energy”

OPE

Off-Road

Material Handling

Autogas

Ag

Res-Com

Homeowner

GALLON GROWTH

(logo)

BRAND STRATEGY

• Drive consumers from awareness to advocacy.

• Improve familiarity, favorability and willingness to consider propane.

• Promote the value, features, and benefits of propane and its applications.

• Inspire states to use campaign materials to promote propane.

• Increase consumer receptiveness to marketer messages.

PERC promotes the fuel, and marketers promote their companies.

AWARENESS CONSIDERATION ADOPTION EXPANDED USEFAVORABILITY LOYALTY ADVOCACY

BRAND STRATEGY

• Drive consumers from awareness to advocacy.

• Improve familiarity, favorability and willingness to consider propane.

• Promote the value, features, and benefits of propane and its applications.

• Inspire states to use campaign materials to promote propane.

• Increase consumer receptiveness to marketer messages.

PERC promotes the fuel, and marketers promote their companies.

AWARENESS CONSIDERATION ADOPTION EXPANDED USEFAVORABILITY LOYALTY ADVOCACY

BRAND STRATEGY

• Drive consumers from awareness to advocacy.

• Improve familiarity, favorability and willingness to consider propane.

• Promote the value, features, and benefits of propane and its applications.

• Inspire states to use campaign materials to promote propane.

• Increase consumer receptiveness to marketer messages.

PERC promotes the fuel, and marketers promote their companies.

AWARENESS CONSIDERATION ADOPTION EXPANDED USEFAVORABILITY LOYALTY ADVOCACY

BRAND STRATEGY

• Drive consumers from awareness to advocacy.

• Improve familiarity, favorability and willingness to consider propane.

• Promote the value, features, and benefits of propane and its applications.

• Inspire states to use campaign materials to promote propane.

• Increase consumer receptiveness to marketer messages.

PERC promotes the fuel, and marketers promote their companies.

AWARENESS CONSIDERATION ADOPTION EXPANDED USEFAVORABILITY LOYALTY ADVOCACY

BRAND STRATEGY

• Drive consumers from awareness to advocacy.

• Improve familiarity, favorability and willingness to consider propane.

• Promote the value, features, and benefits of propane and its applications.