journal of technical analysis (jota). issue 52 (1999, summer)

TRANSCRIPT

Summer-Autumn 1999 I Issue 52

A Publication of

MARKET TECHNICIANS ASSOCIATION, INC. One World Trade Center H Suite 4447 n New York, NY 10048 n Telephone: 212/912-0995 m Fax: 212/912-1064 n e-mail: [email protected]

A Not-For-Profit Professional Organization m Incorporated 1973

MTA Journal - Table of Contents Summer a Autumn 1999 = Issue 52

The MTA Journal Staff 3

About the MTA Journal

Market Technicians Association, Inc.

1999-2000 MTA Board of Directors 81 Management Committee

Editorial Commentary: In This Issue

Henry 0. (Hank) Pruden, Ph.D., Editor

7

Guest Editorial: A Technical Analysis Course: Observations and Suggestions

William T. Charlton, Jr., Ph.D., CFA &John H. Earl, Jr., Ph.D., CFA

9

A Composite Indicator Using Momentum and Trend Following Components Provides Early Identification of Turning Points in S&P 500

James E. Young

17

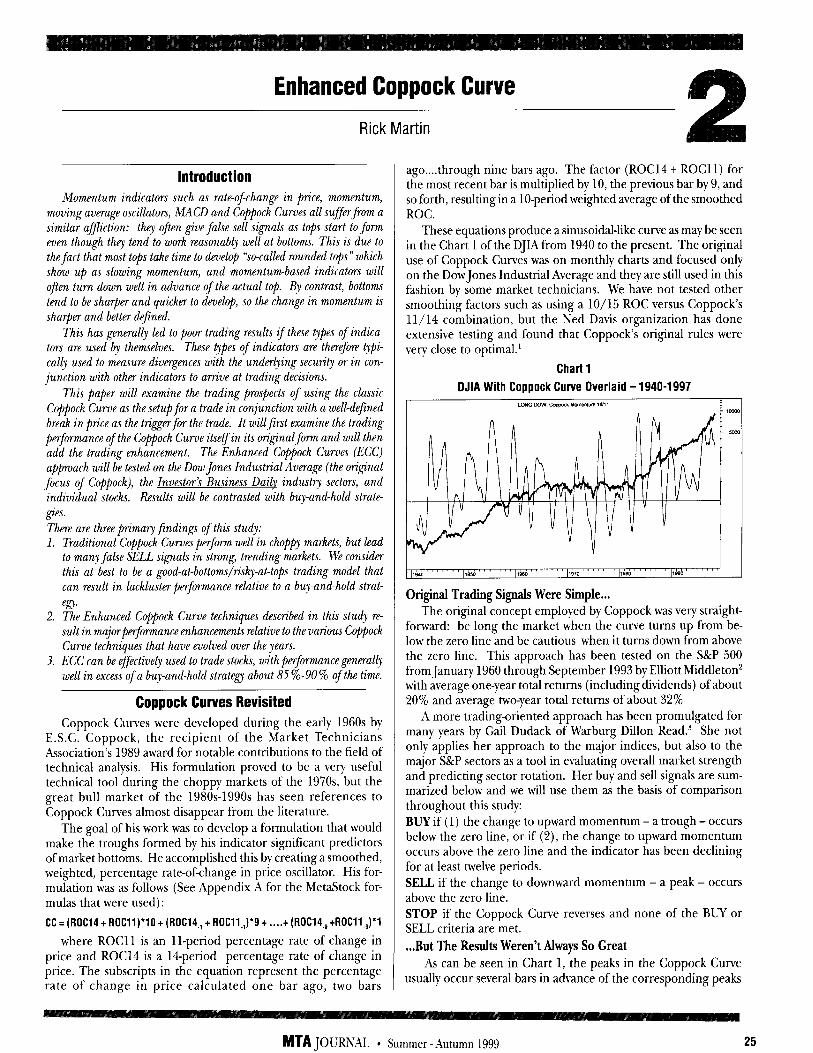

Enhanced Coppock Curve

Rick Martin

25

The Anchor Breakout - A Technical Pattern Derivative

Stephen W. Cox, CMT

Testing the Efficacy of New High/New low Data

Richard T. Williams, CFA, CMT

41

Candlestick Moneyflow

Alan L. Freeman

47

Predicting the Exchange Rate: A Comparison of Econometric Models, Neural Networks and Trading Systems

Giampaolo Gabbi, Ruggero Colombo, Riccardo Bramante, Maria Paola Viola, Paolo de Vito, Albert0 Tumietto

59

MTA JOURNAL * Summer -Autumn 1999

2 MTA JOLXKAL * Summer -Autumn ILKI9

The MTA Journal Staff Summer. Autumn 1999 e Issue 52

Editor Henry 0. Pruden, Ph.D.

Golden Gate University San Francisco, Calijin-nia

Associate Editor David L. Upshaw, CFA, CMT

Lake Quivira, Kansas

Connie Brown, CMT Aerodynamic Investments Inc.

Gainesville, Georgia

John A. Carder, CMT Topline Investment Graphics

Bouldq Colorado

Ann F. Cody, CFA Hilliard Lyons

Louisville, Kentucky

Robert B. Peirce, CFA Cookson, Peirce & Co., Inc.

Pittsburgh, PA

Manuscript Reviewers

Don Dill&one, CFA, CMT Cormorant Bay

Winnefeg Manitoba

Charles D. Kirkpatrick, II, CMT Kirkpatrick and Company, Inc.

Chatham, Massachusetts

John McGinley, CMT Technical Trends

Wilton, Connecticut

Theodore E. Loud, CMT Tel Advisor Inc. of Virginia

Charlottesville, Virginia

Michael J. Moody, CMT Dorsey, Wright & Associates

Pasadena, Calijixnia

Richard C. Orr, Ph.D. ROME Partners

Marblehead, Massachusetts

Kenneth G. Tower, CMT UST Securities

Princeton, New Jmsq

J. Adrian Trezise, M. App. SC. (II) Iris Financial Engineering and Systems

San Francisco, CA

Production Coordinator

Barbara I. Gomperts Financial & Investment Graphic Design

Boston, Massachusetts

Publisher

Market Technicians Association, Inc. One World Trade Centq Suite 4447

New Ymk, New Ywk 10048

MTA JOURhNL l Summer -Autumn 1999 3

Description of the MTA Journal

The Market Technicians Association Journal is pub

lished by the Market Technicians Association, Inc.,

(MTA) One World Trade Center, Suite 4447, New

York, NY 10048. Its purpose is to promote the inves-

tigation and analysis of the price and volume activi-

ties of the world’s financial markets. The MTA Jour-

nalis distributed to individuals (both academic and

practitioner) and libraries in the United States,

Canada, Europe and several other countries. The

MTA Journal is copyrighted by the Market Techni-

cians Association and registered with the Library of

Congress. All rights are reserved.

A Note to Authors About Style

You want your article to be published. The staff of the MTA Journal wants to help you. Our common goal can be achieved efftciently if you will observe the following conventions. You’ll also earn the thanks of our reviewers, editors, and production people.

1. Send your article on a disk. When you send typewritten work, please use 8-l/2” x 11” paper. DOUBLE-SPACE YOUR TEXT. If you use both sides of the paper, take care that it is heavy enough to avoid reverse-side images. Footnotes and references should appear at the end of your article.

2. Submit two copies of your article. 3. All charts should be provided in camera-ready form and be properly labeled for text reference.

Try to avoid using the words “above” or “below,” but rather, Chart A, Table II, etc. when refer- ring to your graphics.

4. Greek characters should be avoided in the text and in all formulae. 5. Include a short (one paragraph) biography. We will place this at the end of your article upon

publication. Your name will appear beneath the title of your article. We will consider any article you send us, regardless of style, but upon acceptance, we will ask

you to make your article conform to the above conventions. For a more detailed style sheet, please contact the MTA Office, One World Trade Center, Suite

4447, New York, NY 10048. Mail your manuscripts to:

Dr. Henry 0. Pruden Golden Gate University

536 Mission Street San Francisco, CA 94105-2968

4 MTA JOURNAL l Summer -Autumn 1999

Market Technicians Association, Inc.

Member and Affiliate Information

Member Member category is available to those “whose professional efforts are spent practicing financial

technical analysis that is either made available to the investing public or becomes a primary input into an active portfolio management process or for whom technical analysis is the basis of their decision-making process.” Applicants for member must be engaged in the above capacity for five years and must be sponsored by three MTA members familiar with the applicant’s work.

Affiliate Affiliate category is available to individuals who are interested in keeping abreast of the field of

technical analysis, but who do not fully meet the requirements for membership or currently do not know three MTA members for sponsorship. Privileges are noted below.

Dues Dues for Members and Affiliates are $200 per year and are payable when joining the MTA and

thereafter upon receipt of annual dues notice mailed on July 1. College students may join at a reduced rate of $50 with the endorsement of a professor.

Application Fees Applicants for member will be charged a onetime, nonrefundable application fee of $25; no fee

for affiliates.

Benefits of the MTA

I Invitation to MTA educational meetings I Receive monthly MTA Newsletter

I Receive MTA Journal

I Use of MTA library n Participate on Various Committees n Colleague of IFTA I Eligible to chair a committee n Eligible to vote

Members w 3 2 w w w w w

Affiliates 3 w w w w w

Annual subscription to the MTAJoumal for nonmembers - $50 (minimum two issues). Single issue of the MTA Journal (including back issues) - $20 each for members and affiliates and $30 for nonmembers.

MTA JOURWK * Summer-Autumn 1999 5

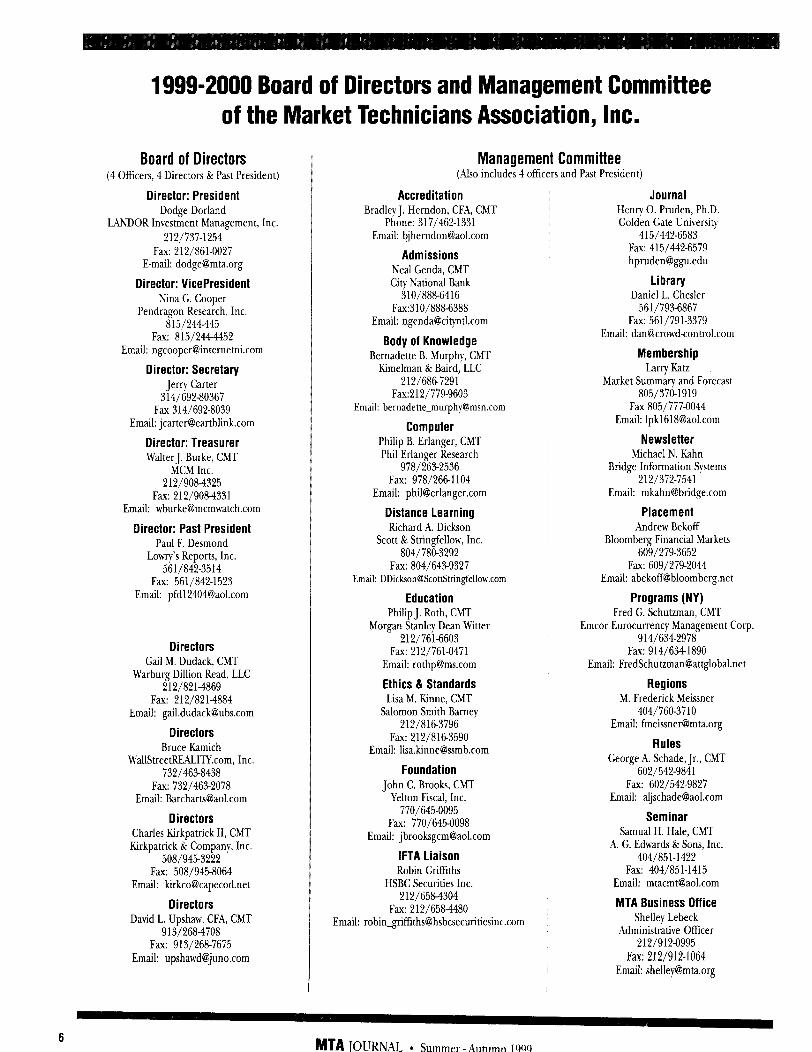

1999-2000 Board of Directors and Management Committee of the Mi lket Technicians Association, Inc.

Board of Directors (4 Offtcers, 4 Directors & Past President)

Director: President Dodge Dorland

LWDOR Investment Management, Inc. 212/137-I254

Fax: 212/861-0027 E-mail: [email protected]

Director: VicePresident Nina G. Cooper

Pendragon Research, Inc. 815/244445

Fax: 815/2444452 Email: [email protected]

Director: Secretary Jerry Carter

314/692-80367 Fax 314/692-8039

Email: [email protected]

Director: Treasurer Walter J. Burke, CMT

MCM Inc. 212/9084325

Fax: 212/9084331 Email: [email protected]

Director: Past President Paul F. Desmond

Lowty’s Reports, Inc. 561/842-3514

Fax: 561/842-1523 Email: pfd12404QaoLcom

Directors Gail M. Dudack, CMT

Warburg Dillion Read, LLC 212/8214869

Fax: 212/8214884 Email: [email protected]

Directors Bruce Kamich

WallStreetREALITY.com, Inc. 732/4638438

Fax: 732/463-2078 Email: [email protected]

Directors Charles Kirkpatrick II, CMT Kirkpatrick & Company, Inc.

508/945-3222 Fax: 508/9458064

Email: [email protected]

Directors David L. Upshaw, CFA, CMT

913/2684708 Fax: 913/268-7675

Email: [email protected]

Management Committee (Also includes 4 officers and Past President)

Accreditation Bradley J. Herndon, CFA, CMT

Phone: 317/462-1331 Email: [email protected]

Admissions Neal Genda, CMT City National Bank

310/888-6416 Fax:310/888-6388

Email: [email protected]

Body of Knowledge Bernadette B. Murphy, CMT

Kimelman & Baird, LLC 212/6867291

Fax:212/779-9603 Email: [email protected]

Computer Philip B. Erlanger, CMT Phil Erlanger Research

978/2632536 Fax: 978/26&1104

Email: [email protected]

Distance Learning Richard A. Dickson

Scott & Stringfellow, Inc. 804/780-3292

Fax: 804/643-9327 Email: [email protected]

Education Philip J. Roth, CMT

Morgan Stanley Dean Witter 212/761-6603

Fax: 212/761-0471 Email: [email protected]

Ethics & Standards Lisa M. Rinne, CMT

Salomon Smith Barney 212/8163796

Fax: 212/81&3590 Email: [email protected]

Foundation John C. Brooks, CMT

Yelton Fiscal, Inc. 770/645-0095

Fax: 770/645-0098 Email: [email protected]

IFTA Liaison Robin Griffiths

HSBC Securities Inc. 212/658-4304

Fax: 212/6584480 Email: [email protected]

Journal Henry 0. Pruden, Ph.D. Golden Gate University

415/442-6583 Fax: 415/442-6579 [email protected]

Library Daniel L. Chesler

561/793-6867 Fax: 561/791-3379

Email: [email protected]

Membership Larrv Rat2

Market Summary and Forecast 805/370-1919

Fax 865/777-0044 Email: Ipkl618@aolcom

Newsletter Michael N. Kahn

Bridge Information Systems 212/372-7541

Email: [email protected]

Placement Andrew Bekoff

Bloomberg Financial Markets 609/279-3652

Fax: 609/279-2044 Email: [email protected]

Programs (NY) Fred G. Schutzman, CMT

Emcor Eurocurrency Management Corp. 914/6342978

Fax: 914/6341890 Email: [email protected]

Regions M. Frederick Meissner

404/760-3710 Email: [email protected]

Rules George A. Schade, Jr., CMT

602/542-9841 Fax: 602/542-9827

Email: [email protected]

Seminar Samuel H. Hale, CMT

A. G. Edwards & Sons, Inc. 404/851-1422

Fax: 404/851-1415 Email: [email protected]

MTA Business Office Shelley Lebeck

Administrative Officer 212/912-0995

Fax: 212/912-1064 Email: [email protected]

6 MTA JOURNAL l Summer-Autumn 1999

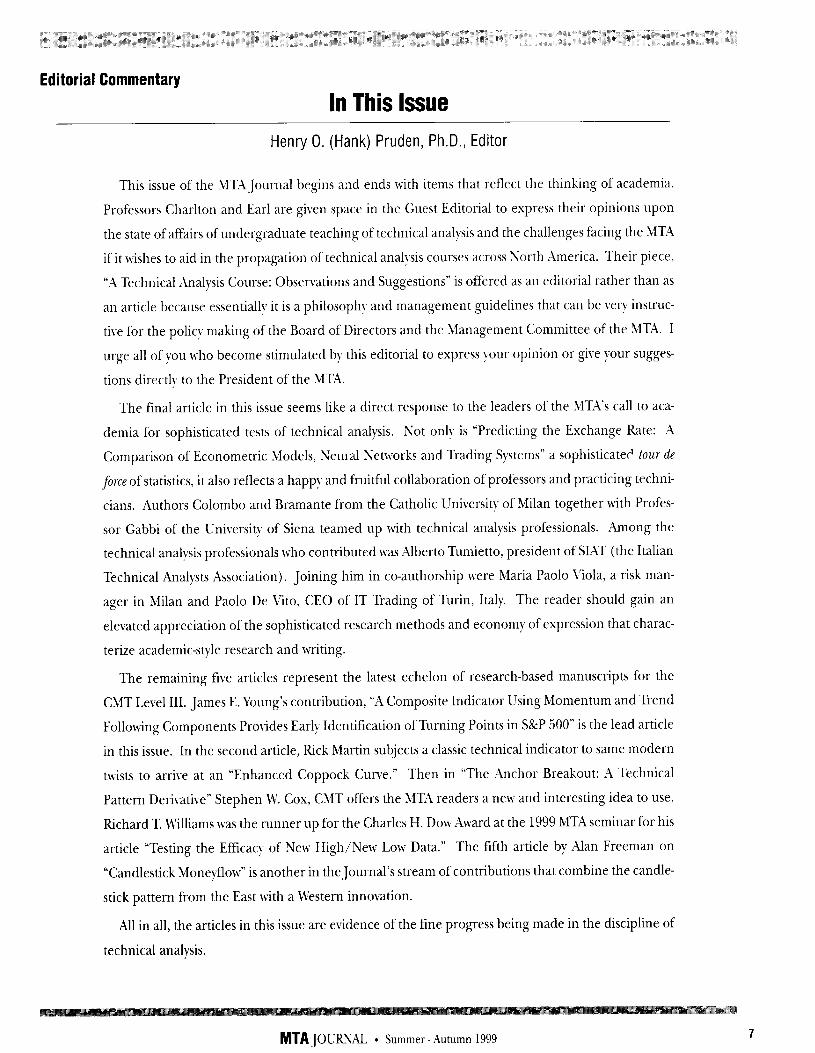

Editorial Commentary

In This Issue

Henry 0. (Hank) Pruden, Ph.D., Editor

This issue of the MTA Journal begins and ends with items that reflect the thinking of academia.

Professors Charlton and Earl are given space in the Guest Editorial to express their opinions upon

the state of affairs of undergraduate teaching of technical analysis and the challenges facing the MT;\

if it wishes to aid in the propagation of technical analysis courses across North America. Their piece,

“A Technical Analysis Course: Observations and Suggestions” is offered as an editorial rather than as

an article because essentially it is a philosophy and management guidelines that can be vely instruc-

tive for the policy making of the Board of Directors and the Management Committee of the MT\. I

urge all of you who become stimulated bp this editorial to express your opinion or give your sugges-

tions directly to the President of the MTA.

The final article in this issue seems like a direct response to the leaders of the MTX’s call to aca-

demia for sophisticated tests of technical analysis. Not only is “Predicting the Exchange Rate: ;1

Comparison of Econometric &Models, Neural Networks and Trading Systems” a sophisticater’ tour de

force of statistics, it also reflects a happy and fruitful collaboration of professors and practicing techni-

cians. Authors Colombo and Bramante from the Catholic University of Milan together with Profes-

sor Gabbi of the University of Siena teamed up with technical analysis professionals. Among the

technical analysis professionals who contributed was Albert0 Tumietto, president of SIAT (the Italian

Technical Analysts Association). Joining him in co-authorship were Maria Paolo Viola, a risk man-

ager in Milan and Paolo De Vito, CEO of IT Trading of Turin, Italy The reader should gain an

elevated appreciation of the sophisticated research methods and economy of expression that charac-

terize academic-style research and writing.

The remaining five articles represent the latest echelon of research-based manuscripts for the

CMT Level III. James E. Young’s contribution, “A Composite Indicator Using Momentum and Trend

Following Components Provides Early Identification of Turning Points in S&P 500” is the lead article

in this issue. In the second article, Rick Martin subjects a classic technical indicator to same modern

twists to arrive at an “Enhanced Coppock Curve.” Then in “The Anchor Breakout: X Technical

Pattern Derivative” Stephen U’. Cox, CMT offers the MTA readers a new and interesting idea to use.

Richard T. M’illiams was the runner up for the Charles H. Dow Award at the 1999 MT;\ seminar for his

article “Testing the Efficacy of New High/New Low Data.” The fifth article by Alan Freeman on

“Candlestick Moneyflow” is another in the Journal’s stream of contributions that combine the candle-

stick pattern from the East with a Western innovation.

All in all, the articles in this issue are evidence of the fine progress being made in the discipline of

technical analysis.

-- -..--

MTA JOURh%L l Summer-Autumn 1999 7

8 MTA JOCRNAL l Summer - LAutumn 1999

Guest Editorial

A Technical Analysis Course: Observations and Suggestions

William T. Charlton, Jr., Ph.D., CFA & John H. Earl, Jr., Ph.D., CFA

Introduction During the past three Tears the Department of Finance at the Univer-

sitJ of Richmond has sponsored a course covering the fundamentals of technical analyis. To our knowledge, this was thefirst technical analysis course offered as part of a degree program at an accredited university’ Subsequently, Rutgers Cniuersit~ has begun offering an MBA course and Baruch College has initiated an undergraduate course. With the growth of interest in technical analysis, our experience with our course may serve as a guideline to other programs. In this paper we discuss the structure of our course, present comparative results from student evaluations, describe the constraints that uniuersitiesface in offfen’nga technical analysis course, and offer suggestions to increase the coverage of technical analysis in col- lege curriculums.

The University of Richmond Technical Analysis Course

Curriculum Tracks Undergraduate finance departments across the country are

increasingly interested in restructuring their course offerings into organized tracks of study (Charlton and Johnson, 1998). Special- ized course tracks combined with nationally recognized designa- tions offer value to students, faculty and universities. A track al- lows students to focus on the areas that hold the most interest to them in terms of their academic and career goals. Finance ma- jors at the University of Richmond can specialize in programs that lead to professional designations in four areas. The invest- ments track (Charlton, 1998) focuses on preparing students to take the Chartered Financial Analyst (CFA’)’ examination given by the Association for Investment Management and Research (AIMR) . The insurance track prepares the student to pursue the Chartered Financial Consultant (ChFC) designation from The American College. The corporate finance track culminates in the Certified Cash Manager (CCM) designation from the Trea- sury Management Association (TMA). The subject of this paper is the fourth designation - the Chartered Market Technician (CMT) issued by the Market Technicians Association, Inc. (MTA).

Designations offer students an advantage in a highly competi- tive job market. For example, preparing for the Level I CFA pro- gram, or having already passed the examination, enables students to differentiate themselves from the thousands of finance majors that graduate each June. Designations also provide an indepen- dent evaluation of the educational value added by the university. Accounting departments have been able to quantify the quality of their programs by comparing the pass rate of their students on the CPA examination to the national average. The increased use of tracks may give finance departments a comparable metric.

One reason for offering a technical analysis course at the Uni- versity of Richmond was the relationship that we developed with MTA. Earning the CMT designation requires a three-step pro- cess consisting of passing two annual examinations and writing

an original research paper. Initially, an agreement with the MTA allowed our students who earned a grade of B or higher in the Technical Analysis course to be credited with having passed the CMT Level I examination. This was a strong incentive to stu- dents to enroll in a nontraditional finance elective. Subsequently, this arrangement was withdrawn by the MTA and our students are now required to sit for the examination.

The Course Structure Our course is taught by Dick Dickson, a technical analyst with

Scott and Stringfellow, Inc., under the guidance of members of the finance department. Table 1 presents the topic coverage for the course offered in the Spring semester of 1999. A number of the lectures are given by visiting technical analysts that specialize in a particular area. We were fortunate to have such prominent technicians as Martin Pring, Phil Roth, Ralph Acampora, and Alan Shaw among others as our guest lectures over the past three years. Enrollment in the course is approximately half undergraduate and half MBA students. Grades are assigned on the basis of stu- dent performance on mid-term and final exams. The course struc- ture was developed to meet student interest in the topic while limiting the impact on already strained faculty resources. A sec- ondary motivation for the course structure was the faculty’s lim- ited exposure to technical analysis concepts. While we have of- fered this course for one semester in each of the past three years, our department has not addressed the broader issue of the ap- propriateness of this course structure within our curriculum. The Technical Analysis course is offered as a Special Topics course during the Spring semester of each year. As a Special Topics course, it is not listed in the college catalog as a regularly offered course which gives the department flexibility on when the course is offered.

Table 1

Technical Analysis Course Outline I. Introduction

A. Course Requirements B. Fundamentals of Technical Analysis C. Dow Theory

II. Chart Construction A. Bar Charts B. Point & Figure Charts C. Candlestick Charts

III. Defining Trends A. Construction of trendlines B. Variations on a theme C. Channels and envelopes D. Moving averages

IV. Determining Support/Resistance A. More on moving averages B. Defining and identifying areas of supply and demand (sup-

port/resistance)

MTA JOURNAL * Summer-Autumn 1999 9

C. Defining & identifying areas of accumulation & distribution. D. Money flow analysis

V. Pattern Recognition A. Philosophy of chart patterns: patterning human nature B. Interpretation of chart patterns

VI. Wyckoff Analysis A. A different perspective on interpreting price/volume action. B. General Principles

VIII. Technical Indicators A. Price oscillators B. Trading and money management C. Mechanical trading systems

IX. Sentiment Indicators X. Relative Strength Analysis A. Principles of relative strength B. Intermarket analysis C. Bottom up forecasting

XI. Cycle Theory A. Stock market cycles B. Elliott Wave analysis C. Gann Analysis

XII. Portfolio Management A. Utilizing technical analysis in portfolio management

Two different textbooks have been used in the three semes- ters that the Technical Analysis course has been offered at the Unirersitv of Richmond. The first semester the course was taught, the book’used was Technical Analvsis ExDlained: The Successful Investor’s Guide to SDottinp Investment Turninn Points authored by Martin Pring and published bp McGraw Hill. The last two se- mesters the text has been Technical Analysis of the Futures ,Mar- ket: h ComDrehensire Guide to Trading Methods and Anplica- tions bp John J. Murphy published by the New York Institute of Finance.

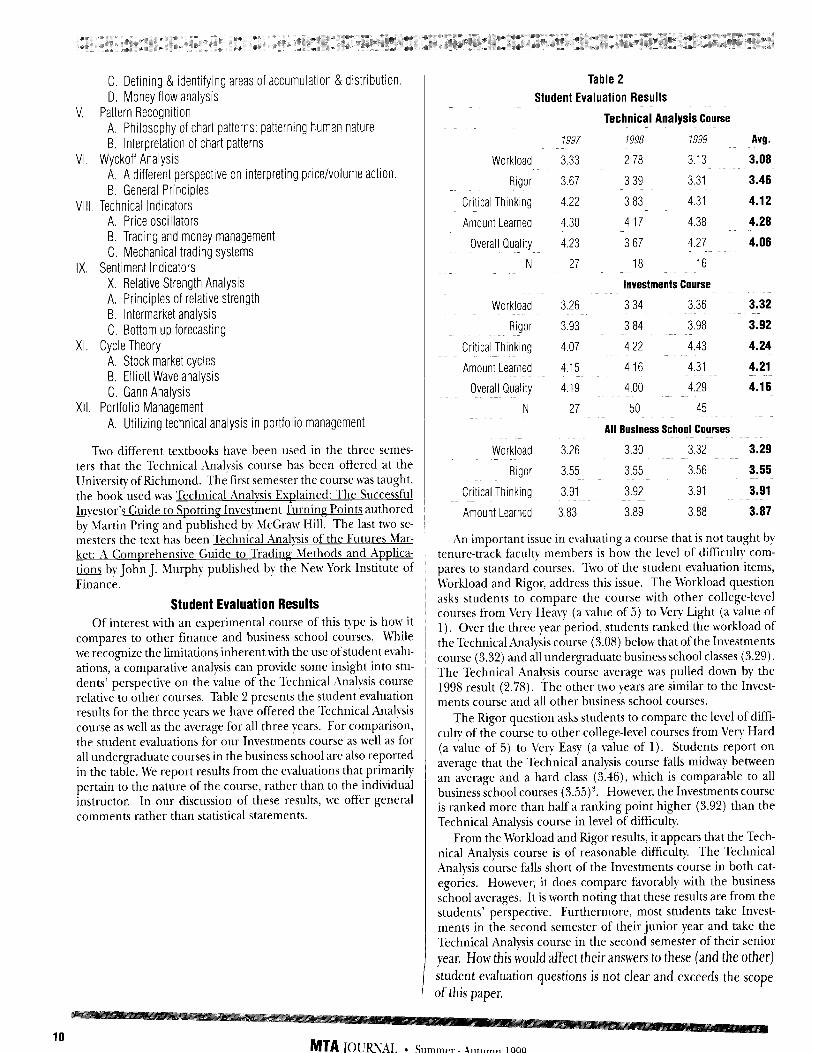

Student Evaluation Results Of interest with an experimental course of this type is how it

compares to other finance and business school courses. MThile we recognize the limitations inherent with the use of student evalu- ations, a comparative analysis can provide some insight into stu- dents’ perspective on the value of the Technical Analysis course relative to other courses. Table 2 presents the student evaluation results for the three years we have offered the Technical Analysis course as well as the average for all three years. For comparison, the student evaluations for our Investments course as well as for all undergraduate courses in the business school are also reported in the table. We report results from the evaluations that primarily pertain to the nature of the course, rather than to the individual instructor. In our discussion of these results, we offer general comments rather than statistical statements.

Table 2

Student Evaluation Results

Technical Analysis Course

Workload

Rigor

Critical Thinking

Amount Learned

Overall Quality

N

1997

3.33

3.67

4.22

4.30

4.23

27

1998 1999

2.78 3.13

3.39 3.31

3.83 4.31

4.17 4.38

3.67 4.27

18 16

Investments Course

Avg.

3.08

3.46

4.12

4.28

4.06

Workload 3.26

Rigor 3.93

Critical Thinking 4.07

Amount Learned 4.15

Overall Quality 4.19

N 27

3.34 3.36

3.84 3.98

4.22 4.43

4.16 4.31

4.00 4.29

50 45

All Business School Courses

3.32

3.92

4.24

4.21

4.16

Workload 3.26 3.30 3.32 3.29

Rigor 3.55 3.55 3.56 3.55

Critical Thinking 3.91 3.92 3.91 3.91

Amount Learned 3.83 3.89 3.88 3.87

An important issue in evaluating a course that is not taught b! tenure-track faculty members is how the level of difficulty com- pares to standard courses. Tivo of the student evaluation items, M’orkload and Rigor, address this issue. The M’orkload question asks students to compare the course with other college-level courses from 1’ery Hea\? (a value of 5) to Very Light (a value of 1). Over the three year period, students ranked the workload of the Technical Analysis course (3.08) below that of the Investments course (3.32) and all undergraduate business school classes (3.29). The Technical Analysis course average was pulled down by the 1998 result (2.78). The other two years are similar to the Invest- ments course and all other business school courses.

The Rigor question asks students to compare the level of diffi- culty of the course to other college-level courses from Very Hard (a value of 5) to \‘ery Easy (a value of 1). Students report on average that the Technical analysis course falls midway between an average and a hard class (3.46), which is comparable to all business school courses (3.55) 3. However, the Investments course is ranked more than half a ranking point higher (3.92) than the Technical Analysis course in level of difficulty.

From the Workload and Rigor results, it appears that the Tech- nical Analysis course is of reasonable difficulty. The Technical Analysis course falls short of the Investments course in both cat- egones. However, it does compare favorably with the business school averages. It is worth noting that these results are from the students’ perspective. Furthermore, most students take Invest- ments in the second semester of their junior year and take the Technical Analysis course in the second semester of their senior year. How this would affect their answers to these (and the other) student evaluation questions is not clear and exceeds the scope of this paper.

MTA JOURNAL l Summer-Autumn 1999

The second hvo student evaluation questions reported in Table 2 reflect more favorably on the Technical Analysis course. Stu- dents were asked to rank the amount the course called upon their ability to think critically and analytically from Very Much (a value of 5) to Very Little (a value of 1). For this question, the Technical Analysis course (4.12) ranks similarly to the Investments courses (4.24) and both are notably higher than all undergraduate busi- ness school courses (3.91). Students ranking of the amount learned in each course also exhibit a similar relationship. The amount learned in the Technical Analysis course (4.28) is almost identical to the Investments course (4.21) and both are substan- tially above the business school average (3.87).

The final student evaluation category we report is the student ranking of the overall quality of the course. Students rank the course from Excellent, which has a numerical value of 5, to Poor, which carries a value of 1. This data item is not available for the All Business School Course sample. As the table shows, the Tech- nical Analysis Course (4.06) and the Investments Course (4.16) are viewed by students to be of similar high overall quality.

While our results with the Technical Analysis course have been good, other programs may have difficulty in duplicating our course due to demands on the limited supply of qualified guest lectur- ers. As discussed below, the long-term viability of our program and any new ones will partially depend how this issue is resolved.

The Fundamental Problem A technical analysis course can be taught by existing full-time

college faculty in the finance department or practicing technical analysts acting in a part time or adjunct teaching capacity. Pres- ently, both groups have limitations that bound the number and quality of technical analysis courses that may be offered. At the vast majority of degree granting universities, the primary focus of investments is fundamental analysis. The study of technical analy- sis is limited to, at most, a single chapter in an investments text- book. Existing finance faculty are either unfamiliar with, and/or skeptical of technical analysis. Thus, their ability and willingness to teach technical analysis topics beyond basic definitions is lim- ited.

Mhile the use of practicing technicians as adjunct faculty ad- dresses the issue of familiarity with technical analysis concepts, professional technicians may not overcome constraints related to accreditation standards. Another problem is that there may not be sufficient availability of practitioners to cover an expanded offering of courses in technical analysis by universities across the country. Furthermore, teaching a semester long course requires a set of organizational and interpersonal skills that are often not inherent to non-faculty professionals.

A key constraint in offering a technical analysis course is find- ing a qualified and knowledgeable instructor. Full-time faculty are qualified to teach at the university level, but may not have sufficient interest or background in technical analysis concepts. Practicing technicians know the material, but may not be quali- fied (according to accreditation bodies) or have the skills neces- sary to teach a college level course. In the sections below, we examine the issues associated with each group in additional de- tail and offer suggestions to address them.

Practitioner Issues

Accreditation The use of practitioners as adjunct faculty is governed by ac-

creditation bodies that oversee universities. Universities are sub ject to accreditation through AACSB (American Association of Colleges and Schools of Business), specifically the standards for accreditation in Business Administration and Accounting. Schools may also be subject to the provisions of a regional accreditation body. The University of Richmond is a member of and subject to the accreditation guidelines of the Southern Association of Col- leges and Schools (SACS).

An overuse of faculty that are not deemed to be “qualified” can endanger a university’s accreditation. In their publication Achieving- Oualitv and Continuous Imnrovement through Self- Evaluation and Peer Review, AACSB states that (page 13) : “ [t] he faculty in aggregate, should have sufficient academic and profes- sional qualifications to accomplish the school’s mission.” Aca- demic qualification is interpreted as a combination of degree completion and post degree activities that maintain the ability to teach in today’s changing environment - research, professional service, and business contacts/relationships. The degree require- ments are [l] a doctoral degree in the area of teaching special- ization, [2] a doctoral degree in a related business area combined with supplemental preparation in the area of teaching, [3] a doc- torate degree outside of business with supplemental preparation in the form of professional development, or [4] substantial coursework in the field of specialization or teaching but no doc- toral degree.

The final provision can apply to specialized instructional re- sources or programs, which might apply to a technical analysis course. In such a case, according to AACSB, the faculty member may have a specialized master’s degree in business, be a current doctoral student, or ABD (all but dissertation completed). These individuals are considered academically qualified but their use should be limited. Under AACSB guidelines, normal academic preparation consists of a minimum of a master’s degree in busi- ness and normal professional experience should be relevant to the faculty member’s teaching assignment. Also, “[t] he greater the disparity between the field of academic preparation and the area of teaching, the greater the need for supplemental prepara- tion in the form of professional development.” (page 14).

The Southern Association of Colleges and Schools has sepa- rate faculty qualifications for undergraduate and graduate pro- grams. SACS addresses this issue in their publication Criteria for Accreditation (page 44) :

Each full-time and part-time faculty member teaching credit courses leading toward the baccalaureate degree, other than physi- cal education activities courses, must have completed at least 18 graduate semester hours in the teaching discipline and hold at least a master’s degree, or hold the minimum of a master’s degree with a major in the teaching discipline. In exceptional cases, outstand- ing professional experience and demonstrated contributions to the teaching discipline maJ be $n-esented in lieu of foal academic p-ybaration. Such cases must be justified by the institution on an individual basis.

Institutions that offer masters or specialized degrees are held to a higher standard. Each faculty member teaching a master’s degree level course &hold a terminal degree in the teaching field or a related discipline. Terminal degree usually means a doctorate but in some cases a specialized master’s degree, In

MTA JOURNAL * Summer -Autumn 1999 11

unusual cases SACS allows exceptions for faculty members that have exceptional scholarly, creative, or professional experience (i.e. Peter Lynch). An exception may be allowed for a new disci- pline when there are no faculty members available with academic credentials. In the event of an unusual case, the university must present evidence to justify employment of the faculty member.

How binding the accreditation constraint is varies by univer- sity and depends on the accreditation agency(ies) they are gov- erned by, how the rest of their faculty stands in terms of qualifica- tions, and the stage of their accreditation process. In the year the university is being reviewed for accreditation they are likely to follow accreditation guidelines closely.

Most academics lack professional development related to the field of technical analysis, but most practitioners lack the academic qualifications to be certified under accreditation guidelines. Uhile the new discipline exemption may apply to technical analysis, its use depends on a university being willing to apply for and pursue an exemption. Thus, accreditation issues may significantly pre- clude many schools from offering a course in technical analysis.

Availability Even if accreditation requirements do not constitute a binding

constraint, the availability of practitioners may limit the ability of the MTA to stalf college offerings. Teaching a course requires a significant commitment of time with regular and relatively inflex- ible meeting times. Practicing technicians who are subject to rap- idly changing demands on their time due to market conditions may find their professional and teaching duties in conflict.

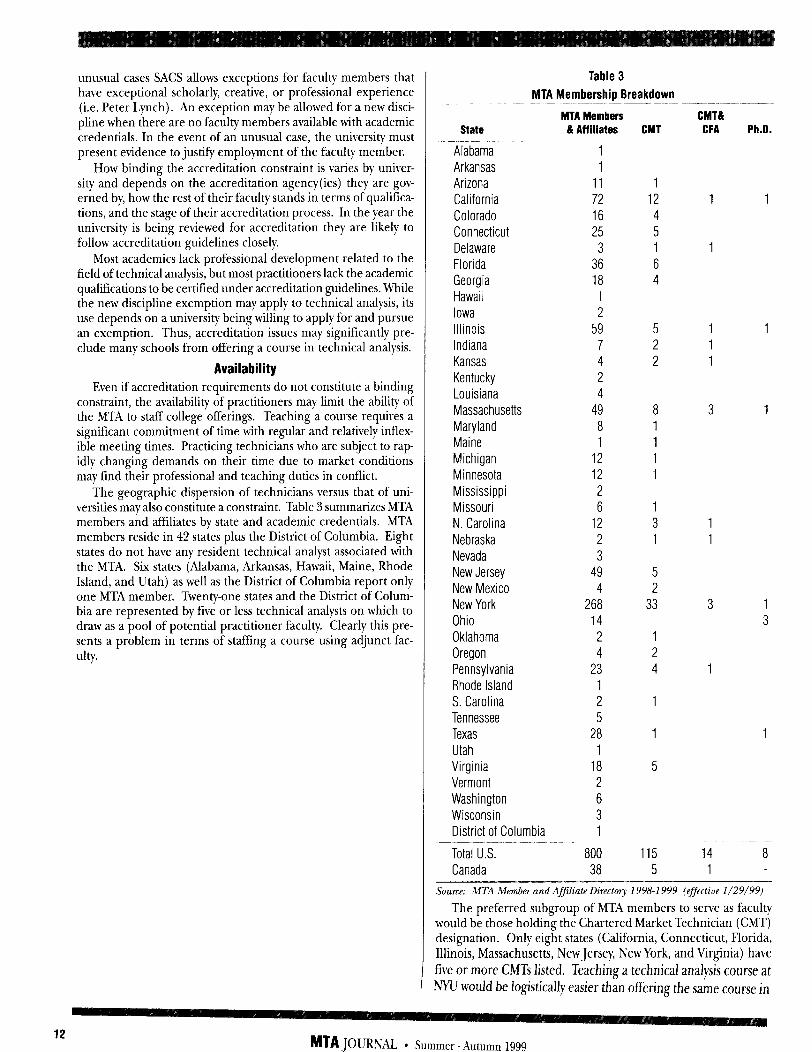

The geographic dispersion of technicians versus that of uni- versities may also constitute a constraint. Table 3 summarizes MTA members and affiliates by state and academic credentials. MTA members reside in 42 states plus the District of Columbia. Eight states do not have any resident technical analyst associated with the MTA. Six states (Alabama, Arkansas, Hawaii, Maine, Rhode Island, and Utah) as well as the District of Columbia report only one MTA member. Twenty-one states and the District of Colum- bia are represented by five or less technical analysts on which to draw as a pool of potential practitioner faculty. Clearly this pre- sents a problem in terms of staffing a course using adjunct fac- ulty.

Table 3

MTA Membership Breakdown

State MTA Members & Aft iliates CMT

CMT& CFA Ph.D.

Alabama 1

Arkansas 1 Arizona 11 California 72 Colorado 16 Connecticut 25 Delaware 3 Florida 36 Georgia 18 Hawaii 1 Iowa 2 Illinois 59 Indiana 7 Kansas 4 Kentucky 2 Louisiana 4 Massachusetts 49 Maryland 8 Maine 1 Michigan 12 Minnesota 12 Mississippi 2 Missouri 6 N. Carolina 12 Nebraska 2 Nevada 3 New Jersey 49 New Mexico 4 New York 268 Ohio 14 Oklahoma 2 Oregon 4 Pennsylvania 23 Rhode Island 1 S. Carolina 2 Tennessee 5 Texas 28 Utah 1 Virginia 18 Vermont 2 Washington 6 Wisconsin 3 District of Columbia 1

1 1

1

1 1 1 1

3 1

1 12 4 5 1 6 4

5 2 2

8 1 1 1 1

1 3 1

5 2

33

1 2 4 1

1

1

5

3 1 3

1

Total U.S. 800 115 14 8 Canada 38 5 1 -

Source: MTA Member and Af,liate Directory 1998-l 999 (effective l/29/99)

The preferred subgroup of MTA members to serve as faculty would be those holding the Chartered Market Technician (CMT) designation. Only eight states (California, Connecticut, Florida, Illinois, Massachusetts, New Jersey, New York, and Virginia) have five or more CMTs listed. Teaching a technical analysis course at NYU would be logistically easier than offering the same course in

MTA JOURNAL l Summer-Autumn 19%

most other states. Fourteen MTA members are listed as holding the combination of a CMT and the fundamental analysis based CFAa designation3, with only Massachusetts (3) and New York (3) reporting more than one. These individuals would be able to teach technical analysis and explain how it relates to and can be used in conjunction with fundamental analysis.

There may be other qualified candidates that are not properly identified in the MTA membership directory. One option to ad- dress this issue is to generate a database of academically qualified technicians and assure that the information is current. Addition- ally, it may be possible to have the CMT designation certified as a specialized designation/degree that qualifies the holder to teach the course in technical analysis. AACSB holds that a JD degree constitutes a terminal degree for individuals teaching business law or legal environment courses. An LLM in taxation or a CPA combined with a master’s degree in accounting is considered a terminal degree for accounting/tax courses. While this course of action would likely be a longer-term solution, it may warrant further investigation.

The ideal combination for teaching technical analysis would be a person who holds both a business doctorate and the CMT designation. Table 3 lists eight MTA members as holding Ph.D.s. However, none hold the combination of a Ph.D. and the CMT designation. Thus, the number of potentially academically quali- fied technical analysts is severely limited and geographically con- centrated. One solution, albeit an unlikely one, is to have exist- ing CMT obtain Ph.D.s from accredited universities. Given the opportunity cost and length of time necessary to obtain a Ph.D., it seems unlikely that this would be a viable solution for the ma- jority of practicing technicians. The alternative solution is for existing Ph.D.s to obtain CMT?. We address this approach in the following sections.

Faculty Issues

Awareness and Promotion of the CMT The CMT is one of a growing number of professional designa-

tions that competes for acceptance with the other established in- dustry credentialing organizations. The CFA has over 25,000 charterholders as compared to the several hundred CMT desig- nees. If one goal of the MTA is to promote the CMT and expand the number of people sitting for the exams, it could begin a cam- paign to increase awareness of the program. The MTA can begin to fill the void of Ph.D.s holding the CMT designation by educat- ing academics as to the value of and requirements for the designa- tion. A good first step for improving the likelihood that existing Ph.D.s would pursue the CMT designation is exposure to techni- cal analysis through seminars, professional exposure (internships) and research opportunities. Something as simple as educator dis- counts for registration for the exams may encourage finance aca- demics to earn their CMT designation. Other designations, such as the CFA, have had similar programs for a number of years and have seen a marked increase in academic participation.

Two organizations can serve as examples for comprehensive programs for increasing awareness. The Treasury Management Association (issuer of the CCM designation) has begun a program that focuses on increasing academic support of the designation. In April, 1999, the TMA sent a two-page academic information request form to university faculty. The letter was addressed Dear Professor and starts off Teaching! Research! Service! These are the criteria on which faculty are evaluated which makes them key

issues for almost university professor. The letter explains how the TMA and the CCM can assist faculty in these critical areas. As part of this program, the TMA will announce a major new pro- gram of financial support for academic research in October. To encourage faculty participation at their annual Treasury Manage- ment Conference, the TMA offers a 75% academic discount. Also, to increase student awareness ofjob opportunities related to Cash Management, the TMA provides free copies of a Treasury Man- agement Careers brochure as well as information on the CCM designation.

While the Chicago Board Options Exchange (CBOE) does not offer a professional designation, it has taken an active role in pro- moting the use and understanding of options. The Options In- stitute was designed to bridge the gap between theory and prac- tice and between academics and practitioners. It offers a com- prehensive curriculum taught by industry professionals that cov- ers the theory, strategy and trading techniques employed in the options markets. Programs are offered in Chicago and around the nation to academics, industry participants, and the public. Also, the CBOE offers a two-day seminars for academics that fo- cuses on teaching applications and research opportunities related to options. Professors are regularly invited to the free seminar.

The MTA can combine aspects of the TMA and CBOE ap- proaches and design an education program to increase aware- ness and acceptance of technical analysis and the CMT designa- tion. A Technical Analysis Institute could provide the forum to teach academics to understand and teach technical analysis at their universities. One of the most important ways for the MTA to increase academic interest in technical analysis issues is through the encouragement and sponsorship of academic research. We discuss this issue in the following section. Following that, we dis- cuss ways to encourage the teaching of technical analysis courses.

Academic Research Of the three components most faculty are evaluated on (re-

search, teaching, and service), research is often the most difficult of the three in which to achieve success. For this and other rea- sons, it is often valued as the most important component. Any way in which the MTA can help academics achieve additional publications would most likely be viewed positively by academics. This could lead to an increase in the amount of technical analysis based academic research. The two main areas where research assistance is most valuable are in helping to get a project off the ground and in increasing the outlets for working projects. We discuss each below.

Most current academics are relatively unfamiliar with technical analysis and, as a result, it may be difficult for them to generate sufficient potential research ideas. The MTA could provide a valu- able service by developing connections between practitioners and academics and encouraging practitioners to use their expertise in assisting academicians. The aforementioned Technical Institute would be a good forum for the development of these relationships. Another important issue for academic research is the availability of good data. Most academics have ready access to U.S. stock mar- ket data. However, many do not have good access to foreign mar- ket data or commodity pricing. Thus, the Institute could also act as a warehouse of datasets commonly used by technical analysts. One usual difference between practitioner (of any type) and aca- demic research is that academics tend to use more historical data whereas practitioners are generally more focused on recent mar- ket conditions. A final suggestion is for the establishment of re- search grants which would encourage academics to start projects.

MTA JOURIUL * Summer-Autumn I999 13

The MTA could also play an important role on the output side of the research pipeline. Competitive monetary research awards are a good way to encourage additional research. There are non- monetary methods of encouragement as well. While not equiva- lent to a publication, most universities view presenting a paper at a conference as evidence of active scholarship. Paper sessions, or tracks, focusing on technical analysis issues at the conferences are a means for professors to receive acknowledgment for their work. These sessions could be held at the national and/or re- gional conferences.

Ultimately what counts are the articles a professor publishes. For most professors, the minimum requirement is that an article be published in a refereed journal. Beyond this exists a relative ranking ofjournals based on their selectivity and the esteem the journal is held in by the profession. The more journals that are available to publish technical analysis articles, and the better these journal are viewed, the more desirable a publication in them will be to a professor.

Textbooks For many professors, teaching is second to research in its im-

portance, for others it is of primary importance. Several impedi- ments currently exist to teaching a technical analysis course be- yond the limitation already discussed above. Perhaps the most significant non-staffing issue is the lack of an adequate technical analysis textbook. Both books used in our course (the Pring and Murphy books) are written for practitioners and do not qualify as academic textbooks. Murphy’s text is narrowly focused on the futures market and is dated (it was published in 1986)j. Both books’ format is consistent with their intended audience - practi- tioners. Their intent is to familiarize readers with technical analysis concepts. Each chapter consists of text ending in a one para- graph conclusion and/or summary.

A book which can serve as a good example of an academic textbook is Investment Analvsis and Portfolio Management by Frank Reilly and Keith Brown. This textbook is commonly used in Investments and Portfolio Management/Security Analysis courses and is required reading for CFA candidates. It combines academic theory and CFA based practical applicatio&. Each chapter begins with a bulleted list of learning objectives that fo- cus the reader on the main points prior to reading the chapter. Also, each chapter ends with a summary followed by a set of short answer questions and a set of problems that allow the student to assess their grasp of the concepts covered in the chapter. A num- ber of the questions and problems are accompanied by a CFA trademark indicating that the question has appeared on a prior CFA examination. A reference section is included in each chap- ter which guides the reader to sources where additional informa- tion can be obtained. While the content of the books vary, most textbooks follow a format similar to the one described above.

Supplemental Materials Academic textbooks are accompanied by a seemingly endless

supply of ancillary materials designed to either help instructors prepare their lectures or students study the material covered in the course. These materials are especially important when a new subject area is being prepped for instruction. A typical set of supplemental materials are those included with Fundamentals of Financial Management by Brigham and Houston. This textbook is widely used and has been adopted by hundreds of universities for their introductory corporate finance course.

We first discuss the materials developed for students, A study

guide is sold to students separately or can be included as a pack- age with the textbook. The study guide provides summaries of the main concepts in each chapter combined with focused ques- tions and problems designed to provide feedback to the students. Problems are usually in a multiple-choice format. The study guide provides structure and pre-examination evaluation to the partici- pants.

Blueprints are an additional learning aid designed to help stu- dents take better notes in class. Students often have to choose between taking notes and listening to the points discussed in class. Blueprints provide students a hard copy and overview of the ma- terial covered by the instructor. Students can augment the gen- eral notes during or after the lecture period. Instructors can modify the blueprints and use them as their lecture notes. The blueprints, a syllabus, and other related materials can be provided to students at the beginning of the semester in a “course pack” available for purchase through the university bookstore.

The authors provide extensive support to professors. Inte- grated cases and presentation software are provided to augment end of chapter problems. These minicases cover the key topics in each chapter in a systematic manner. The cases are designed to focus the students’ attention and allow the instructor to design the lecture material around the case. A set of electronic slides or PowerPoint presentation based on the cases is included. The PowerPoint presentation allows slides to be developed in layers, building a presentation one piece at a time compared to “static” overhead transparencies. The combination of case studies and presentation software is particularly useful for inexperienced teachers or experienced teachers teaching a new course.

Videos covering key financial concepts are also included in the supplemental materials. The authors provide fourteen short videotapes which can be used to introduce various topics. Videos could be a particularly effective tool for teaching technical analy- sis. A library.of in-depth videos could be produced covering the more specialized concepts of techniques included in a technical analysis textbook. For example, candlesticks, sentiment indica- tors, point and figure charts or other subjects could be presented by the leading experts in each area. Fundamental based finance academics may not be comfortable teaching these areas and the assistance of a guest speaker or a video could prove valuable. The previously discussed limitations on guest speakers could make vid- eos an especially attractive alternative. Videos would be most ef- fective if developed specifically for an academic audience rather than edited from a presentation to practitioners. Videocon- ferences could provide an alternative to videos or can be used in conjunction with the video to provide a question and answer ses- sion for students. However, the limited availability of teleconfer- ence facilities on campuses and their relative high cost might con- strain this approach. of this type. The tremendous pace of devel- opment of other distance learning technologies may offer addi- tional capabilities in the near future which could lower the cost hurdle.

Some of the end of the chapter problems in the Brigham and Houston textbook are designed to require the use of a spread- sheet template to solve. A computer problem diskette is provided with the textbook that contains the spreadsheet templates (usu- ally in LOTUS l-2-3 or Microsoft Excel format). The templates are stand alone programs and no knowledge of the underlying spreadsheet programs is required. In theory, hands-on applica- tion reinforces classroom discussion which improves learning. A technical analysis data disk could include time-series market data

14 MTA JOURNAL * Summer -Autumn 1999

and charts which would allow students to apply the techniques they learn in class on historical and/or current sets of financial data. The quantitative nature of technical analysis makes this approach especially appealing.

A test bank is provided to the instructor in book form and as a computer software program. Questions are in multiple choice formats and the software allows for the construction of custom- ized and random examinations. If the instructor prefers essay and non multiple-choice problems, the questions in the test bank can provide a starting point.

The instructor’s manual is the most important of the supple- mental textbook materials. Brigham and Houston include a sample syllabus covering course objectives, class procedures, ex- amination and grading policies, and required materials. Course schedules are provided for a two-day a week (Tuesday and Thurs- day) and three-day a week (Monday, Wednesday, and Friday) teach- ing format that specifies the chapter and the topic for each class period. An examination schedule is also included in the course schedule. These are illustrative but provide valuable guidance to an instructor teaching a new course for the first time. The sample syllabus and course schedule would be invaluable additions to an instructor’s manual accompanying the technical analysis textbook. For each chapter the following is provided: An overview and learn- ing objectives, lecture suggestions, answers to the end of chapter problems, and the solution to the integrated case. Answers to the even numbered questions are often include in the textbook it- self, while the answers to the odd numbered questions are given only in the instructor’s manual.

The MTA could design an academic textbook that follows the format described above while incorporating the major tenets stressed in the CMT examination. Some possible unifying themes for a textbook are given in Table 4 which was derived from MTA members descriptions of themselves. The construction of a text- book could also have other beneficial uses. It could serve as a valuable vehicle for the MTA to articulate the body of knowledge required for the CMT designation.

As discussed, the supplemental materials are often a critical factor in the adoption of a textbook and should be an integral part of the textbook development process. This is especially true given the current acceptance level of technical analysis by profes- sors and their relative inexperience teaching the material. The first step in the textbook process is to agree upon a curriculum. After that, an author and an editor are selected at which point chapters could be assigned to the leading expert in each area. Writing an academic textbook, in conjunction with the necessar) supplemental materials, is a vital step in moving technical analysis toward the mainstream of finance curriculum at the university level.

TABLE 4

MTA Member Profile

Discipline Used Technical Analysis Focus Job Function

Trend/Momentum Equities Technical Analyst Supply/Demand Fixed Income Portfolio Manager Relative Strength Index Futures Research Director

Sentiment .Mutual Funds Trader Intermarket Commodities Broker/Sales

Cycles Foreign Exchange Editor/Publisher/Writer Volume Options Other

Bar Charts Point and Figure Market Profile Candlesticks Elliott Wave

Gann Other

Source: MTA LKmber and Affiliate Directq 1998-l 999

Candidate Issues From our experience, undergraduates considering taking the

examination are concerned about the cost, test sites, experience requirements, scholarships, and the Level III original research paper. The CMT program registration fee is $250 and the Level I exam fee starts at $100. While these fees are lower than those for the CFA, AIMR works with university finance departments to of- fer scholarships to students that plan to sit for the Level I test. Universities are awarded five, ten, or twenty scholarships based on the performance of their students compared to the national pass rate over the prior three years. The scholarships allows stu- dents to sit for the first examination for a total fee of $100. Stu- dents pays the full cost of future examinations. The MTA could develop a similar scholarship program or a special fee structure for students and university faculty.

Experience requirements are often a significant barrier for stu- dents. Currently, passing Level I counts for two years toward a five year experience requirement. For both faculty and students the wider the range ofjob activities that qualify as relevant to meeting the MTA/CMT requirements, the more likely both groups are to participate in the program. For example, does teaching a univer- sity level investments course count as experience? Or, does work- ing as a fundamental research analyst count as experience? Man) students do not accept positions until their final semester, the uncertainty induced by narrow experience requirements make them hesitant to pursue a designation. If academic work does not count as experience for faculty, few would meet the experience requirement. Thus, this is an important issue.

Effective with the 1998-99 registration all CMT candidates are required to be either an MTA member or affiliate and maintain this status throughout the entire CMT process. Academic mem- bership discounts for students and faculty would help to increase enrollment.

The web page for the MTA lists the 2000 exam date as Friday, April 28 and exam sites as Atlanta, Boston, Chicago, Denver, Hous- ton, London, Los Angeles, NewYork, San Francisco, Toronto, and other sites at the discretion of the Accreditation Committee. Ide- ally, the list of exam sites could be expanded to include at a mini- mum any city in which a university course in technical analysis is offered in conjunction with the MTA. If not, it may be impracti- cal for students in cities other than those listed to take the test.

MTA JOURML * Summer -Autumn 1999 15

This would probably limit the availability of technical analysis courses to those universities located near a test site.

Finally, the requirement at Level III to write a research paper approved by the Accreditation Committee creates a logistical bottleneck to expansion of the designation. The number of quali- fied reviewers to read and approve the manuscripts limits the abil- ity to promote the CMT as a mass appeal designation. Proposals to replace the research report with an examination are under consideration by the MTA. If approved a major hurdle will be removed.

Conclusion In general, our experience with the Technical Analysis course

has been positive. Student demand for the course is steady and we expect student interest to remain at its current level for some time to come. The student evaluation results are good with the Technical Analysis course achieving scores comparable to or bet- ter than the average undergraduate business school course. Also, the difficulty of the course meets our expectations for a finance course taught by non-tenure track faculty. At some point, our department may have to address the issue of how this course fits into our curriculum. However, we expect to continue to offer the course in its current form. The ability of other universities to offer similar programs is currently limited by the availability of qualified teachers. While the suggestions offered above do not constitute a comprehensive set of all of the relevant issues, ad- dressing them would lower the hurdles that interested schools currently face. The lower the barriers are, the more likely it is that universities will consider initiating academic coverage of tech- nical analysis.

References Achieving Oualitv and Continuous Imorovement through Self- Evaluation and Peer Review, Standards for Accreditation Busi- ness Administration and Accounting, American Association of Colleges and Schools of Business 19941995 Criteria for Accreditation, Southern Association of Colleges and Schools, Commission on Colleges, 1995, Ninth Edition MTA Member and Affiliate Directorv 1998-1999, Market Tech- nicians Association, Inc. Brigham, Eugene F., and Joel E Houston, Fundamentals of Financial Management, Eighth Edition, 1998, The Dryden Press Charlton, William T. Jr., Course Tracking Along Professional Des- ignations: The CXA Track, August 1998, Financial Practice and Education 8 (No.1, Spring/Summer), 69-82 Charlton, William T. Jr., and Robert Johnson, The CE4 Designa- tion and the Finance Curriculum: A Survq of Faculty, forthcom- ing, Journal of Financial Education. Murphy, John J., Technical Analysis of the Futures Market: A Comnrehensive Guide to Trading Methods and Anolications, New York Institute of Finance, 1986 Murphy, John J., Technical Analysis of the Financial Markets: A Comorehensive Guide to Trading Methods and Anolications, New York Institute of Finance, 1999

q Pring, Martin J., Technical Analvsis Exolained: The Successful Investor’s Guide to Sootting Investment Turning Points, Third Edition, 1991, McGraw-Hill

q Reilly, Frank K. and Keith C. Brown, Investment Analvsis and Portfolio Management, Fifth Edition, 1997, The Dryden Press

Endnotes ’ Prior to the inauguration of our course, Henry Pruden of-

fered a technical analysis course at Golden Gate University. How- ever, the course was offered in the continuing education program rather than as part of the regular curriculum.

* CFA@ is a registered trademark of the Institute of Chartered Financial Analysts, licensed to the Association for Investment Management and Research.

3That the average level of difficulty for all business school is above the average ranking has at least two explanations. First, students may over estimate the difficulty of a course and thereby induce an upward bias. The evaluation form asks respondents to rank the course versus other college-level courses. Therefore, a second reason may be that business school classes are harder than the courses the students take prior to entering the business school. These two possibilities are not mutually exclusive, so both may be present in the sample.

‘The use of distance learning technology may also be a solu- tion to this problem. However, it would most likely only be a partial solution. While it might solve the geographical limitation, accreditation issues remain unresolved. Thus, distance learning technology may be an excellent support tool but not a primary means of offering a course for college credit.

5A newer version of Murphy’s text entitled Technical Analvsis of the Financial Markets has recently been released. Reportedly, it has a greater focus on equity markets. We have not reviewed a copy of the new text, so our comments focus on the previous ver- sion of the book.

6 Ironically, this text, like most fundamental based textbooks, has the obligatory chapter on technical analysis.

William Charlton, Ph.D. &John Earl, Ph.D.

William T. Charlton, Jr., Ph.D., CFA, is an assistant profes- sor of finance at the E.C. Robins School of Business at the University of Richmond. He teaches corporate finance and investments as well as acting as the faculty advisor for the CFA Track and the University of Richmond Student Man- aged Investment Fund (known as the Spider Fund). He holds a bachelors of science in electrical engineering from Texas A&M University, an MBA from St. Mary’s University (San Antonio, Texas), and a Ph.D. in finance from the University of Texas at Austin. Prior to entering the Ph.D. program, he worked for Hewlett Packard for five years as a computer field engineer.

John H. Earl, Jr. Ph.D., is an associate professor of finance at the E.C. Robins School of Business at the University of Richmond. He teaches corporate finance, investments and portfolio management/security analysis at both the under- graduate and graduate levels. John holds bachelors and master’s degrees in finance from the University of Massachu- setts and a Ph.D. in finance from Arizona State University. In addition he holds the CFA, CLU, ChFC, CIC, CFP, and ARM designations.

MTA JOURNAL * Summer-Autumn 1999

A Composite Indicator Using Momentum and Trend Following Components Provides Early Identification of

Turning Points in S&P 500

James E. Young

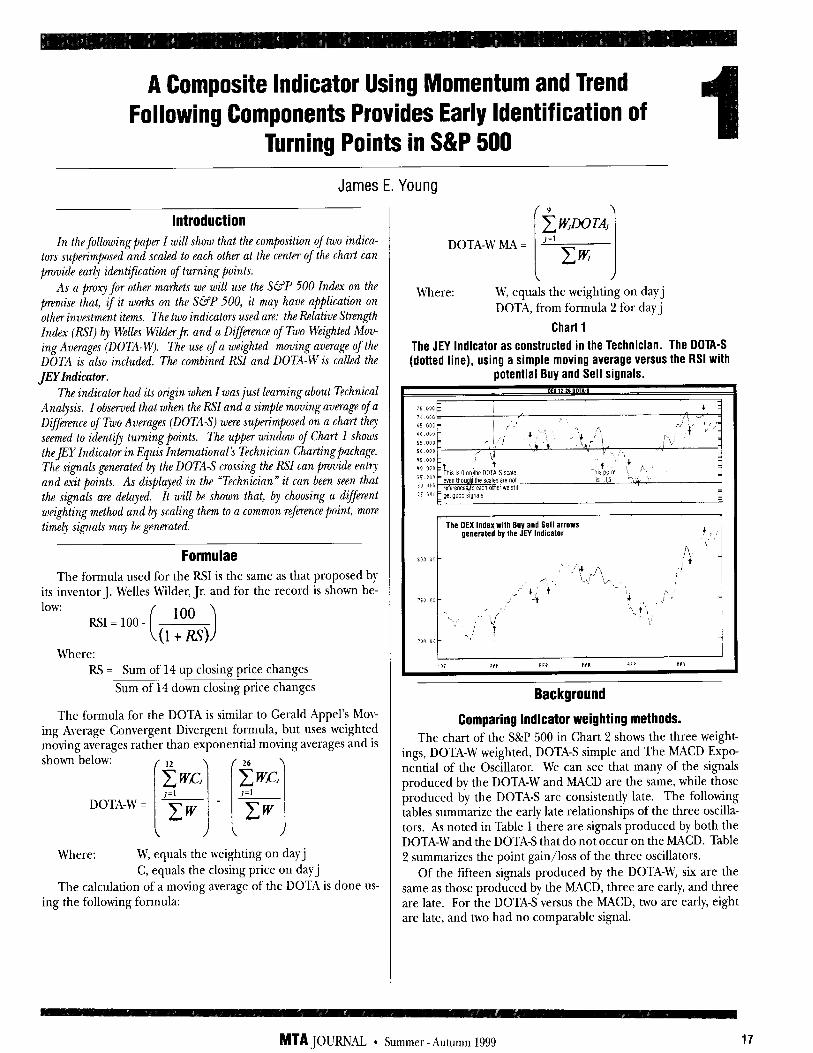

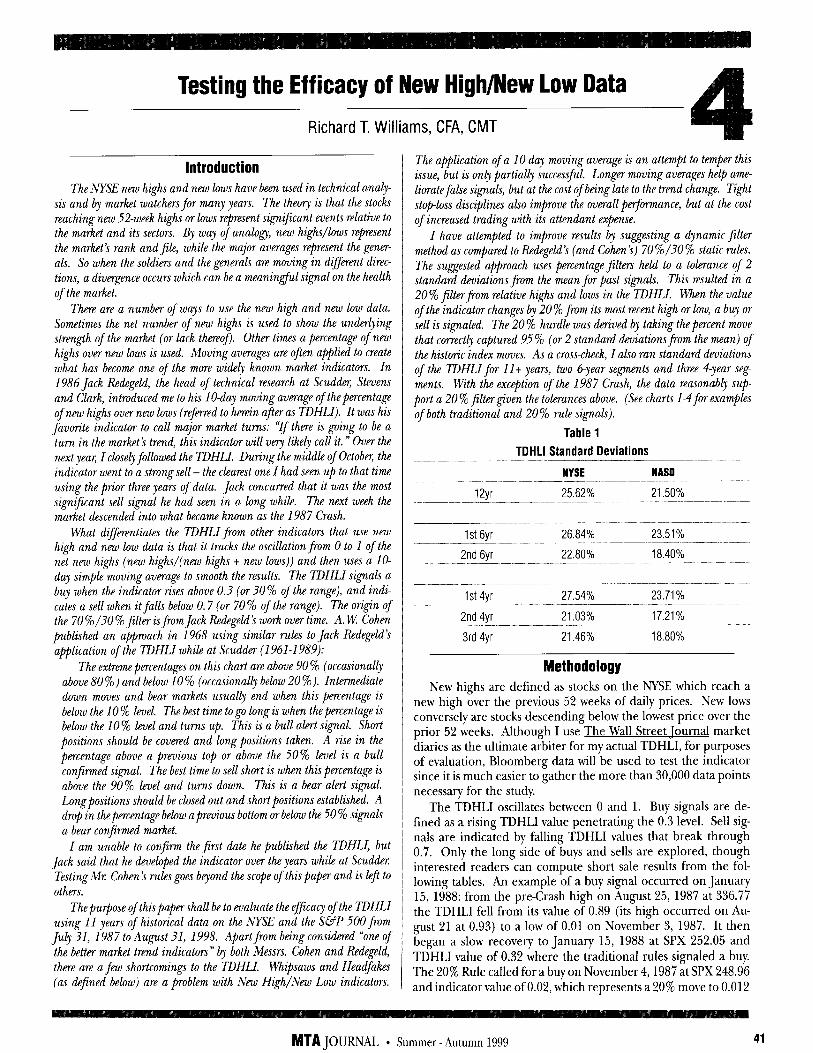

Introduction In the following paper I will show that the composition of two indica-

tors superimposed and scaled to each other at the center of the chart can provide early identification of turning points.

As a proxy for other markets we will use the S&P 500 Index on the premise that, if it works on the S&P 500, it may have application on other investment items. The two indicators used are: the Relative Strength Index (RX) by Welles Wilder Jr. and a DifIfmence of Two Weighted Mov- ing Averages (DOTA-W). The use of a weighted moving average of the DOTA is also included. The combined RSI and DOTA-W is called the JEYIndicator.

The indicator had its origin when I was just learning about Technical Analyis. I observed that when the RSI and a simple moving average of a Difference of Two Averages (DOTA-S) were superimposed on a chart thq

seemed to identify turning points. The upPer window of Chart 1 shows theJEY Indicator in Equis International’s Technician Charting package. The signals generated @ the DOTAS crossing the RSI can @nG’e entv and exit points. As displayed in the “Technician” it can been seen that the signals are delayed. It will be shown that, by choosing a different weighting method and bJ scaling them to a common reference point, more time4 signals may be generated.

Formulae The formula used for the R!3 is the same as that proposed by

its inventor J. Welles Wilder, Jr. and for the record is shown be- low:

RSI = 100 - 100

( ) o+m Where:

RS = Sum of 14 up closing price changes Sum of 14 down closing price changes

The formula for the DOTA is similar to Gerald Appel’s Mov- ing Average Convergent Divergent formula, but uses weighted moving averages rather than exponential moving averages and is shown below: / I2 \ /26 \

cwc, CWCJ ]=l ]=I

DOTA-W = ~ - p cw

! I( ) Where: W, equals the weighting on day j

C, equals the closing price on day j The calculation of a moving average of the DOTA is done us-

ing the following formula:

Where: W, equals the weighting on day j DOTA, from formula 2 for day j

Chart 1

The JEY Indicator as constructed in the Technician. The DDTA-S (dotted line), using a simple moving average versus the RSI with

potential Buy and Sell signals.

The OEX lnde: with Buy and Sell arrows generated by the JEY Indicator

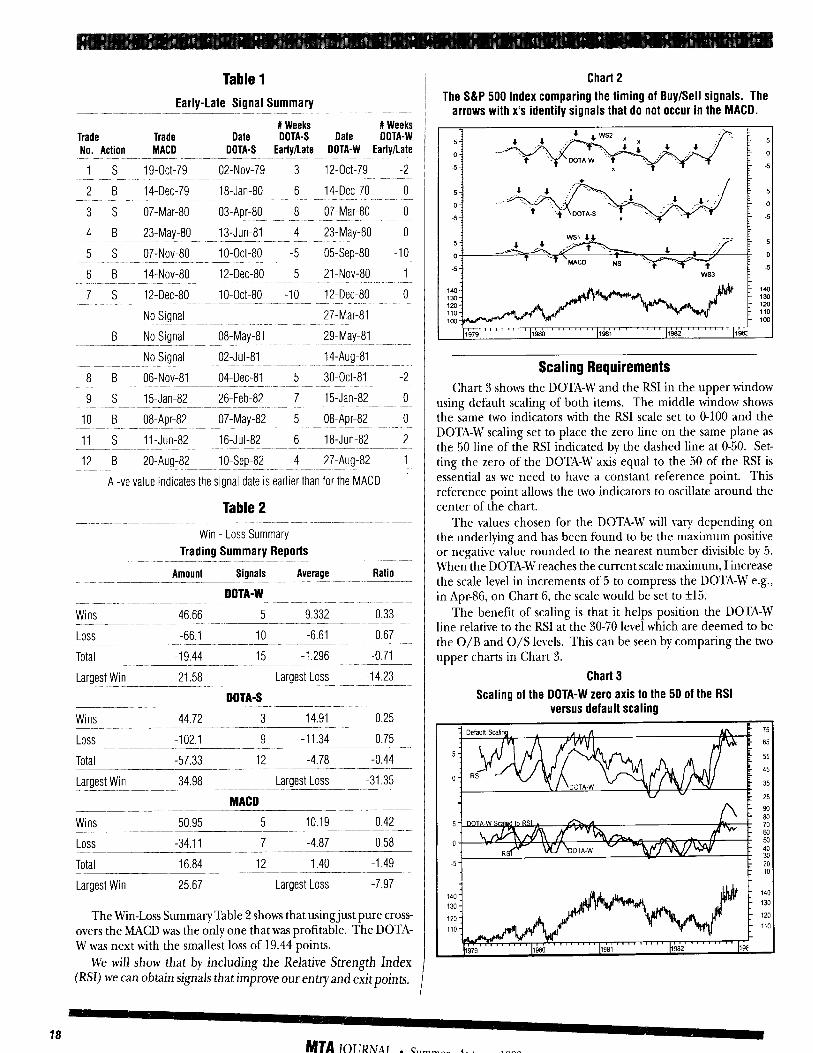

The chart of the S&P 500 in Chart 2 shows the three weight- ings, DOTA-W weighted, DOTA-S simple and The MACD Expo- nential of the Oscillator. We can see that many of the signals produced by the DOTA-W and MACD are the same, while those produced by the DOTA-S are consistently late. The following tables summarize the early late relationships of the three oscilla- tors. As noted in Table 1 there are signals produced by both the DOTA-W and the DOTA-S that do not occur on the MACD. Table 2 summarizes the point gain/loss of the three oscillators.

Of the ftiteen signals produced by the DOTA-W, six are the same as those produced by the MACD, three are early, and three are late. For the DOTA-S versus the MACD, two are early, eight are late, and two had no comparable signal.

Background

Comparing Indicator weighting methods.

MTA JOURhN * Summer-Autumn 1999 17

18

Table 1

Early-Late Signal Summary - -~ ..- -- #Weeks #Weeks

Trade Trade Date DDTA-S Date DDTA-W No. Action MACD DDTA-S Early/Late DDTA-W Early/Late

1 s 19-act-79 02-Nov-79 3 12-act-79 -2

2 B 14-Dee-79 18-Jan-80 6 14-Dec.70 0

3 s 07-Mar-80 03.Apr-80 8 07-Mar-80 0

4 B 23-May-80 13-Jun-81 4 23-May-80 0

5 s 07-Nov-80 1 O-0&80 -5 05-Sep-80 -10

6 B 14-Nov-80 12-Dec.80 5 21-Nov-80 1

7 s 12-Dee-80 1 O-Ott-80 -10 12.Dee-80 0

No Signal 27-Mar-81

B No Signal 08-May-81 29.May-81

No Signal 02-J&81 14-Aug-81 .~. .-----. --- .~ ~~ 8 B 06.Nov-81 04-Dee-81 5 30.Ott-81 -2

9 s 15.Jan-82 26-Feb-82 7 15.Jan-82 0

10 B 08-Apr-82 07-May-82 5 08.Apr-82 0

11 s ll-Jun-82 16-Jul-82 6 18-Jun-82 2

12 B 20.Aug-82 1 O-Sep-82 4 27.Aug-82 1

A -ve value indicates the signal date is earlier than for the MACD

Table 2

Win - Loss Summary Trading Summary Reports

Amount Signals Average Ratio

DOTA-W

Wins 46.66 5 9.332 0.33

Loss -66.1 10 -6.61 0.67

Total -19.44 15 -1.296 -0.71 - Largest Win 21.58 Largest Loss -14.23 _ --~- ~.~ ~-~----

DDTA-S

Wins 44.72 3 14.91 0.25 ~- Loss -102.1 9 -11.34 0.75

Total -57.33 12 -4.78 -0.44

Largest Win 34.98 Largest Loss -31.35

MACD

Wins 50.95 5 10.19 0.42

Loss -34.11 7 -4.87 0.58

Total 16.84 12 1.40 -1.49

Largest Win 25.67 Largest Loss -7.97

The Win-Loss Summary Table 2 shows that usingjust pure cross- overs the h4ACD was the only one that was profitable. The DOTA- W was next with the smallest loss of 19.44 points.

We will show that by including the Relative Strength Index PSI) we can obtain signals that improve our entry and exitpoints.

I

Chart 2

The S&P 500 Index comparing the timing of Buy/Sell signals. The arrows with x’s identify signals that do not occur in the MACD.

Scaling Requirements Chart 3 shows the DOTA-W and the RSI in the upper window

using default scaling of both items. The middle window shows the same two indicators with the RSI scale set to O-100 and the DOTA-W scaling set to place the zero line on the same plane as the 50 line of the RSI indicated by the dashed line at O-50. Set- ting the zero of the DOTA-W axis equal to the 50 of the RSI is essential as we need to have a constant reference point. This reference point allows the two indicators to oscillate around the center of the chart.

The values chosen for the DOTA-W will vary depending on the underlying and has been found to be the maximum positive or negative value rounded to the nearest number divisible by 5. When the DOTA-Wreathes the current scale maximum, I increase the scale level in increments of 5 to compress the DOTA-W e.g., in Apr-86, on Chart 6, the scale would be set to f15.

The benefit of scaling is that it helps position the DOTA-W line relative to the RSI at the 30-70 level which are deemed to be the O/B and O/S levels. This can be seen by comparing the two upper charts in Chart 3.

Chart 3

Scaling of the DOTA-W zero axis to the 50 of the RSI versus default scaling

c I

MTAJOLXNAL * Summer - htllmn IQQO

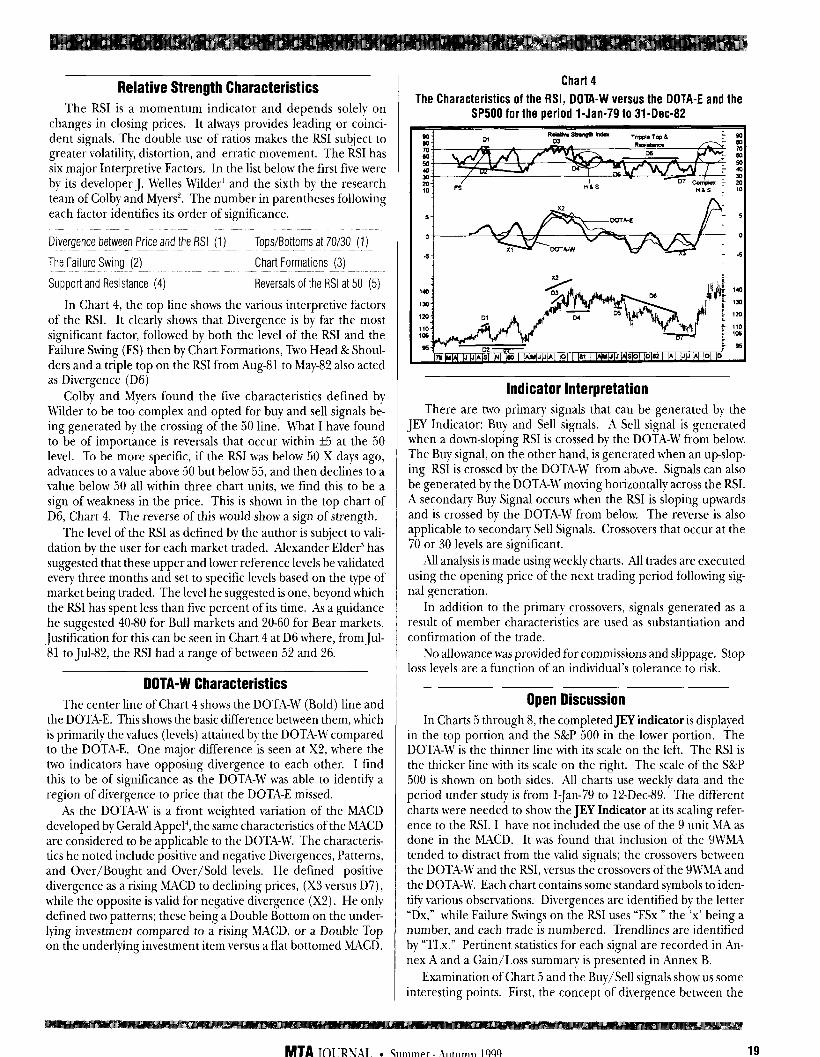

Relative Strength Characteristics The RSI is a momentum indicator and depends solely on

changes in closing prices. It always provides leading or comci- dent signals. The double use of ratios makes the RSI subject to greater volatility, distortion, and erratic movement. The RSI has six major Interpretive Factors. In the list below the first five were by its developer J. Welles Wilder’ and the sixth by the research team of Colby and Myers’. The number in parentheses following each factor identifies its order of significance.

ke&nce between Price and the RSI (1) Tops/Bottoms at 70/30 (1)

The Failure Swing (2) ~- Chart Formations (3)

--- Support and Resistance (4) Reversals of the RSI at 50 (5)

In Chart 4, the top line shows the various interpretive factors of the RSI. It clearly shows that Divergence is by far the most significant factor, followed by both the level of the RSI and the Failure Swing (FS) then by Chart Formations, TNTO Head & Shoul- ders and a triple top on the RSI from Aug-81 to May-82 also acted as Divergence (D6)

Colby and Myers found the fire characteristics defined by Wilder to be too complex and opted for buy and sell signals be- ing generated by the crossing of the 50 line. What I have found to be of importance is reversals that occur within +5 at the 50 level. To be more specific, if the RSI was below 50 X days ago, advances to a value above 50 but below 55, and then declines to a value below 50 all within three chart units, we find this to be a sign of weakness in the price. This is shown in the top chart of D6, Chart 4. The reverse of this would show a sign of strength.

The level of the RSI as defined by the author is subject to vali- dation by the user for each market traded. Alexander Eldeti has suggested that these upper and lower reference levels be validated every three months and set to specific levels based on the type of market being traded. The level he suggested is one, beyond which the RSI has spent less than five percent of its time. As a guidance he suggested 40-80 for Bull markets and 20-60 for Bear markets. Justification for this can be seen in Chart 4 at D6 where, from Jul- 81 to Jul-82, the RSI had a range of between 52 and 26.

DOTA-W Characteristics The center line of Chart 4 shows the DOTA-W (Bold) line and

the DOTA-E. This shows the basic difference between them, which is primarily the values (levels) attained bv the DOTA-W compared to the DOTA-E. One major difference’is seen at X2, where the two indicators have opposing divergence to each other. I find this to be of significance as the DOTA-W was able to identify a region of divergence to price that the DOTA-E missed.

As the DOTA-W is a front weighted variation of the MACD developed by Gerald Appel’, the same characteristics of the MACD are considered to be applicable to the DOTA-U’. The characteris- tics he noted include positive and negative Divergences, Patterns, and Over/Bought and Over/Sold levels. He defined positive divergence as a rising MACD to declining prices, (X3 versus D7), while the opposite is valid for negative divergence (X2). He only defined two patterns; these being a Double Bottom on the under- lying investment compared to a rising ,MACD, or a Double Top on the underlying investment item versus a flat bottomed MACD.

Chart 4

The Characteristics of the RSI, DDlA-W versus the DDTA-E and the SP500 for the period l-Jan-79 to 31-Dee-82

Indicator Interpretation There are two primary signals that can be generated by the

JEY Indicator: Buy and Sell signals. A Sell signal is generated when a down-sloping RSI is crossed by the DOTA-W from below. The Buy signal, on the other hand, is generated when an up-slop- ing RSI is crossed by the DOTA-W from above. Signals can also be generated by the DOTA-W moving horizontally across the RSI. A secondary Buy Signal occurs when the RSI is sloping upwards and is crossed by the DOTA-W from below. The reverse is also applicable to secondary Sell Signals. Crossovers that occur at the 70 or 30 levels are significant.

All analysis is made using weekly charts. All trades are executed using the opening price of the next trading period following sig- nal generation.

In addition to the primary crossovers, signals generated as a result of member characteristics are used as substantiation and confirmation of the trade.

No allowance was provided for commissions and slippage. Stop loss levels are a function of an individual’s tolerance to risk.

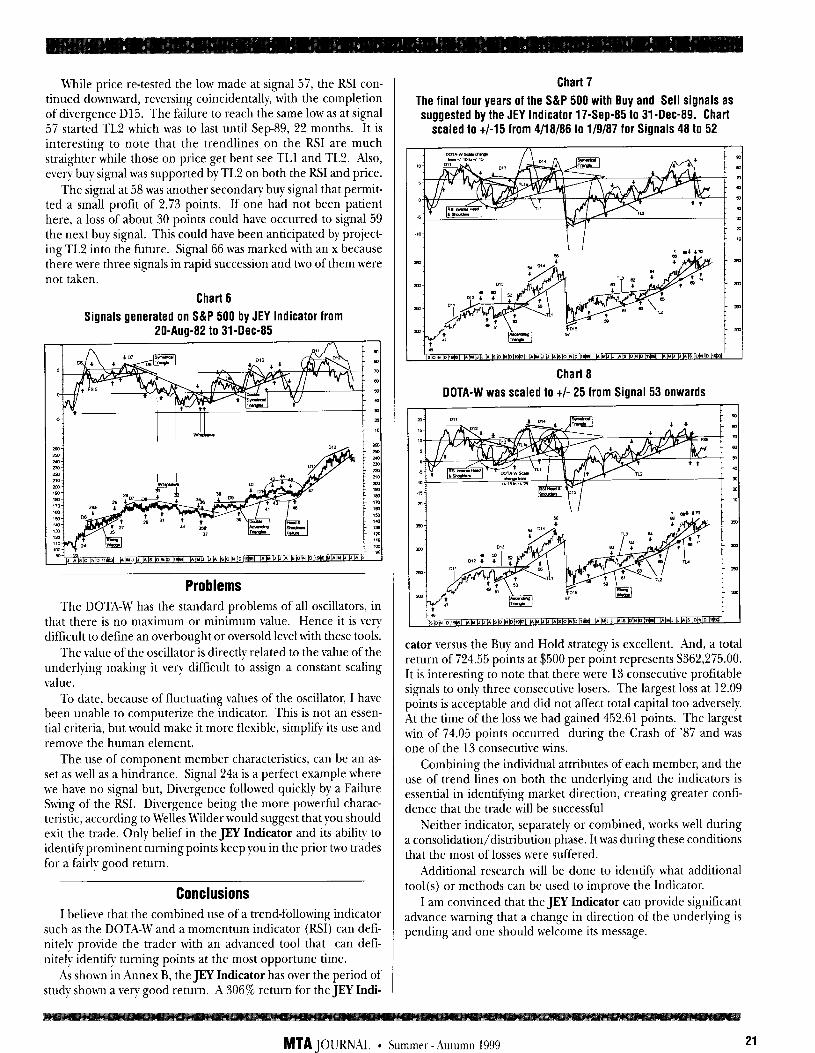

Open Discussion In Charts 5 through 8, the completed JEY indicator is displayed

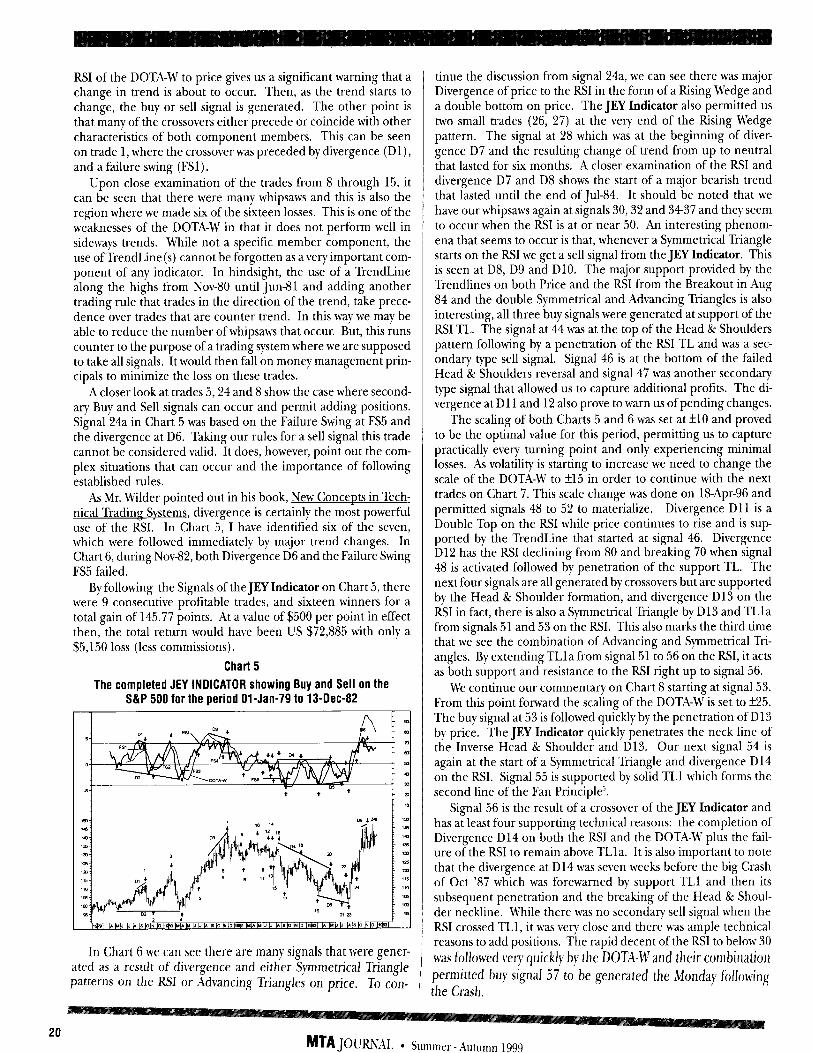

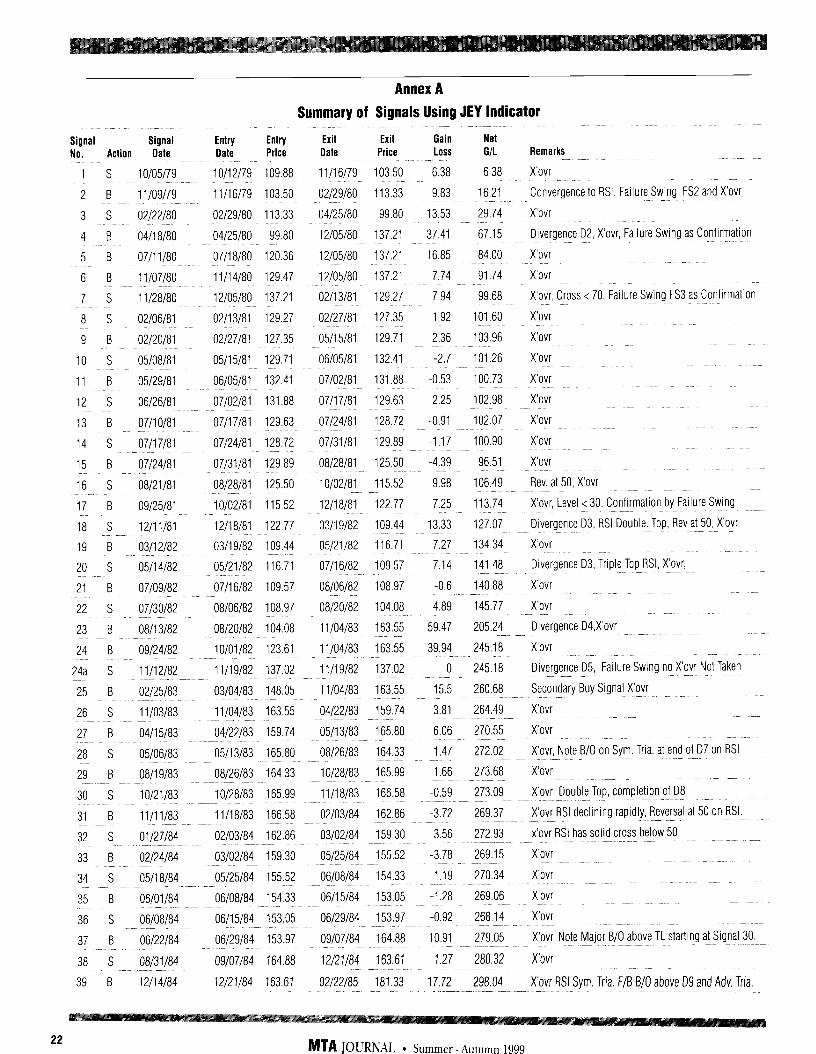

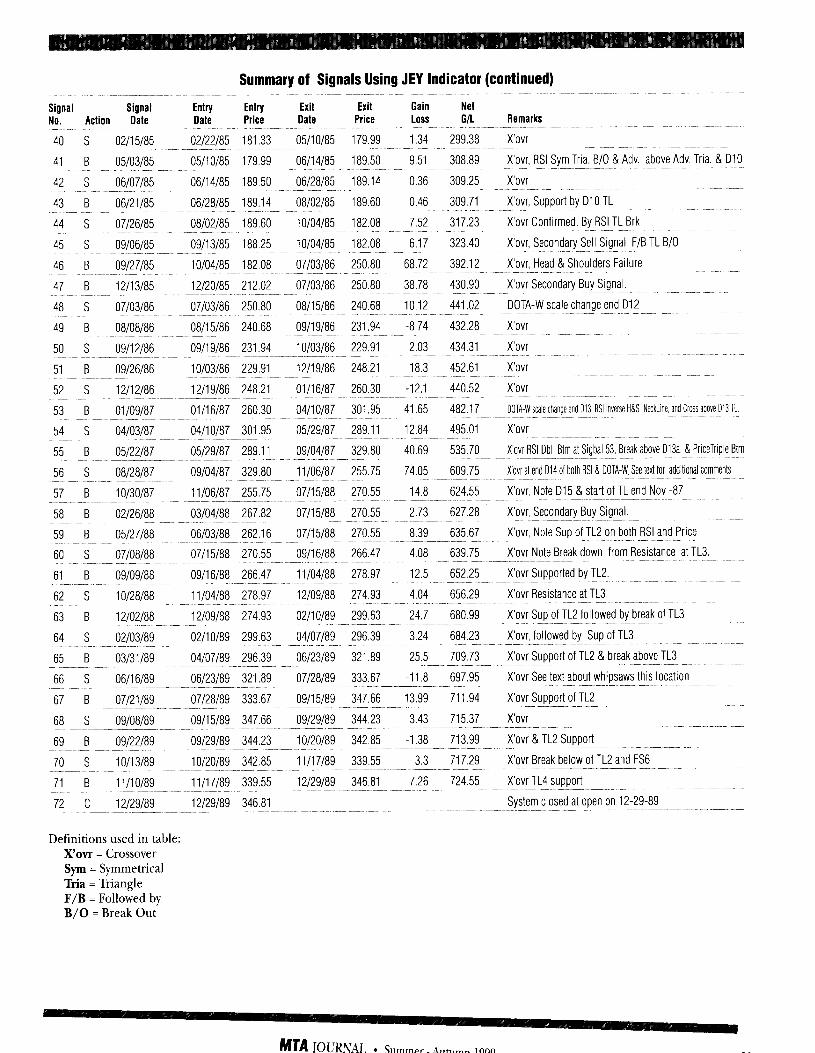

in the top portion and the S&P 500 in the lower portion. The DOTA-W is the thinner line with its scale on the left. The RSI is the thicker line with its scale on the right. The scale of the S&P 500 is shown on both sides. All charts use weekly data and the period under study is from l-Jan-79 to 12-Dee-89. The different charts were needed to show the JEY Indicator at its scaling refer- ence to the RSI. I have not included the use of the 9 unit MA as done in the MACD. It was found that inclusion of the 9NWA tended to distract from the valid signals; the crossovers between the DOTA-M’ and the RSI, v-ersus the crossovers of the 9MMA and the DOTA-W. Each chart contains some standard symbols to iden- tify various observations. Divergences are identified bv the letter “Dx,” while Failure Swings on the RSI uses “FSx n the “x’ being a number, and each trade is numbered. Trendlines are identified by “TLx.” Pertinent statistics for each signal are recorded in An- nex A and a Gain/Loss summary is presented in Annex B.

Examination of Chart 5 and the Buy/Sell signals show us some interesting points. First, the concept of divergence between the

MTA JOURML l Summer - Autumn 1999 19

RSI of the DOTA-W to price gives us a significant warning that a change in trend is about to occur. Then, as the trend starts to change, the buy or sell signal is generated. The other point is that many of the crossovers either precede or coincide with other characteristics of both component members. This can be seen on trade 1, where the crossover was preceded by divergence (D 1)) and a failure swing (FSl).

Upon close examination of the trades from 8 through 15, it can be seen that there were many whipsaws and this is also the region where we made six of the sixteen losses. This is one of the weaknesses of the DOTA-W in that it does not perform well in sideways trends. While not a specific member component, the use of TrendLine cannot be forgotten as a very important com- ponent of any indicator. In hindsight, the use of a TrendLine along the highs from Nov-80 until Jun-81 and adding another trading rule that trades in the direction of the trend, take prece- dence over trades that are counter trend. In this way we may be able to reduce the number of whipsaws that occur. But, this runs counter to the purpose of a trading system where we are supposed to take all signals. It would then fall on money management prin- cipals to minimize the loss on these trades.

A closer look at trades 5,24 and 8 show the case where second- ary Buy and Sell signals can occur and permit adding positions. Signal 24a in Chart 5 was based on the Failure Swing at FS5 and the divergence at D6. Taking our rules for a sell signal this trade cannot be considered valid. It does, however, point out the com- plex situations that can occur and the importance of following established rules.

As Mr. Wilder pointed out in his book, New Concents in Tech- nical Trading Svstems, divergence is certainly the most powerful use of the RSI. In Chart 5, I have identified six of the seven, which were followed immediately by major trend changes. In Chart 6, during No\r-82, both Divergence D6 and the Failure Swing FS5 failed.

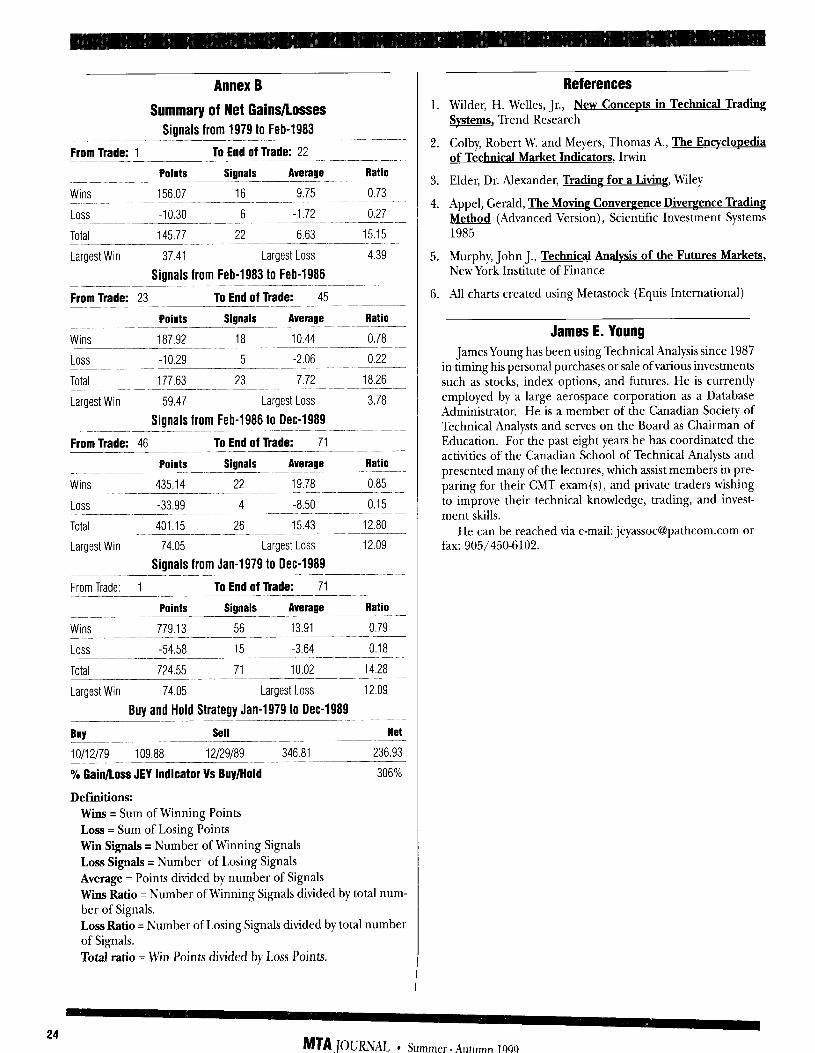

By following the Signals of the JEY Indicator on Chart 5, there were 9 consecutive profitable trades, and sixteen winners for a total gain of 145.77 points. At a value of $500 per point in effect then, the total return would have been US $72,885 with only a $5,150 loss (less commissions).

Chart 5

The completed JEY INDICATOR showing Buy and Sell on the S&P 500 for the period Ol-Jan-79 to 13-Dee-82

In Chart 6 we can see there are many signals that were gener- ated as a result of divergence and either Symmetrical Triangle patterns on the RSI or Advancing Triangles on price. To con-

tinue the discussion from signal 24a, we can see there was major Divergence of price to the RSI in the form of a Rising Wedge and a double bottom on price. The JEY Indicator also permitted us hvo small trades (26, 27) at the very end of the Rising Wedge pattern. The signal at 28 which was at the beginning of diver- gence D7 and the resulting change of trend from up to neutral that lasted for six months. A closer examination of the RSI and divergence D7 and D8 shows the start of a major bearish trend that lasted until the end of Jul-84. It should be noted that we have our whipsaws again at signals 30,32 and 3437 and they seem to occur when the RSI is at or near 50. An interesting phenom- ena that seems to occur is that, whenever a Symmetrical Triangle starts on the RSI we get a sell signal from the JEY Indicator. This is seen at D8, D9 and DlO. The major support provided by the Trendlines on both Price and the RSI from the Breakout in Aug 84 and the double Symmetrical and Advancing Triangles is also interesting, all three buy signals were generated at support of the RSI TL. The signal at 44 was at the top of the Head & Shoulders pattern following by a penetration of the RSI TL and was a sec- ondary type sell signal. Signal 46 is at the bottom of the failed Head & Shoulders reversal and signal 47 was another secondary type signal that 11 a owed us to capture additional profits. The di- vergence at Dll and 12 also prove to warn us of pending changes.