jay blanchard – proactive advisor magazine – volume 3, issue 6

TRANSCRIPT

Data fuels market uncertainty pg. 7

Social Security strategies pg. 3

Sentiment indicators track the herd pg. 4

Ready

climbpg. 8

Jay blanchard

August 7, 2014 | Volume 3 | Issue 6

First magazine focused on active investment management

$50,000 a year. We were able to show them a filing strategy that would result in a $20,000 annual increase in income when both were age 70, all of this within government guidelines.

This is not rocket science once you fully understand the statutes and the many options available. But the key points are how few clients and prospects understand it, how un-der-marketed the knowledge is, and how powerful a draw it can be for en-tering into important conversations with prospects.”

ver the past few years, it has become increasingly

difficult to differentiate advisory ser-vices holding seminars for pre-retirees and retirees. Conducting these semi-nars is important because they can lead to meetings where we give prospects a ‘second opinion’ on their planning and investment strategies and introduce core concepts of our practice such as active investment management.

About a year ago, we shifted our seminar strategy to lead with Social Security filing strategies. This has been very successful in generating attendance and having follow-up conversations.

We feel this area is overlooked by many advisors and people are hungry for information. The complexities of Social Security can have a real impact on retirees’ income streams and sur-vivor benefits, and people find tre-mendous value when a professional can help them navigate it.

Here is one example: A man and his wife came in for a meeting after a seminar and had been planning a pretty standard claiming strategy at age 66, taking full benefits at about

Social Security strategies as prospect “hot button”

Richard D’AmbolaSuccasunna, NJ

Questar Capital CorporationSenior Financial Planner,

Dunn’s Financial Review, Inc.

O“

Securities offered through Questar Capital Corporation (QCC), Member FINRA, SIPC. Advisory Services offered through Questar Asset Management (QAM), a Registered Investment Advisor. Dunn’s Financial Review is independent of QCC and QAM.

Read text only

Last week’s results

VIEWER RESPONSE

Approximately how much of your time is spent on administrative/regulatory compliance tasks?

-Vote to see results

This week’s poll

78% of younger investors say their relationship with their financial advisor is enhanced by:

Answer: About 20%. On average, financial advisors spent one in every five hours of their time on administrative/regulatory compli-ance tasks. Source: NATIXIS/Core Data Research 2013 Global Survey of Financial Advisors

0%40%

30%30%

10%20%30%40% or more

POLLS

VOTE

Technology

Face-to-face meetings

Regular mailings

August 7, 2014 | proactiveadvisormagazine.com 3

TIPS & TOOLS

ne of the more fascinating elements of market analysis is sentiment or the behavior of the crowd and its impact

on the market cycle.According to the Efficient Market Theory, it

is impossible to “beat the market.” The efficien-cy of the market causes existing share prices to incorporate and reflect all relevant information as soon as that information becomes known. There’s no room for pricing inefficiencies that an investor might exploit.

There is a tremendous appeal to the Efficient Market Theory. It’s logical and it doesn’t demand much from us as investors, because it clearly says there is little we can do other than ride the market.

The problem is that according to the theory, market bubbles, i.e., inefficiencies, should not occur. But they do. While there have been market crashes due to external factors, such as the outbreak of war, bubble markets by and large are emotionally driven.

Emotions are messy. They are hard to calculate, hard to predict and inconsistent. And they matter.

The quote above is from the preface of the 1852 edition of Extraordinary Popular Delusions and the Madness of Crowds, originally published in 1841. The author, Charles Mackay, chronicles some of the most extraordinary market bubbles of history, including the Mississippi Scheme, the South Sea Bubble and “Tulip Mania,” along with other manias from fads to

Read text only

Tracking the herd through sentiment indicators

O

By Linda Ferentchak

“Men, it has been well said, think in herds; it will be seen that they

go mad in herds, while they only recover their senses slowly, one by one.”

– Charles Mackay, Extraordinary Popular Delusions and the Madness of Crowds

proactiveadvisormagazine.com | August 7, 20144

national delusions. Look closely and their resemblance to modern times is striking. Something happens when crowd sentiment moves toward the extremes. Markets cease to react logically to information and become part of the stampeding herd.

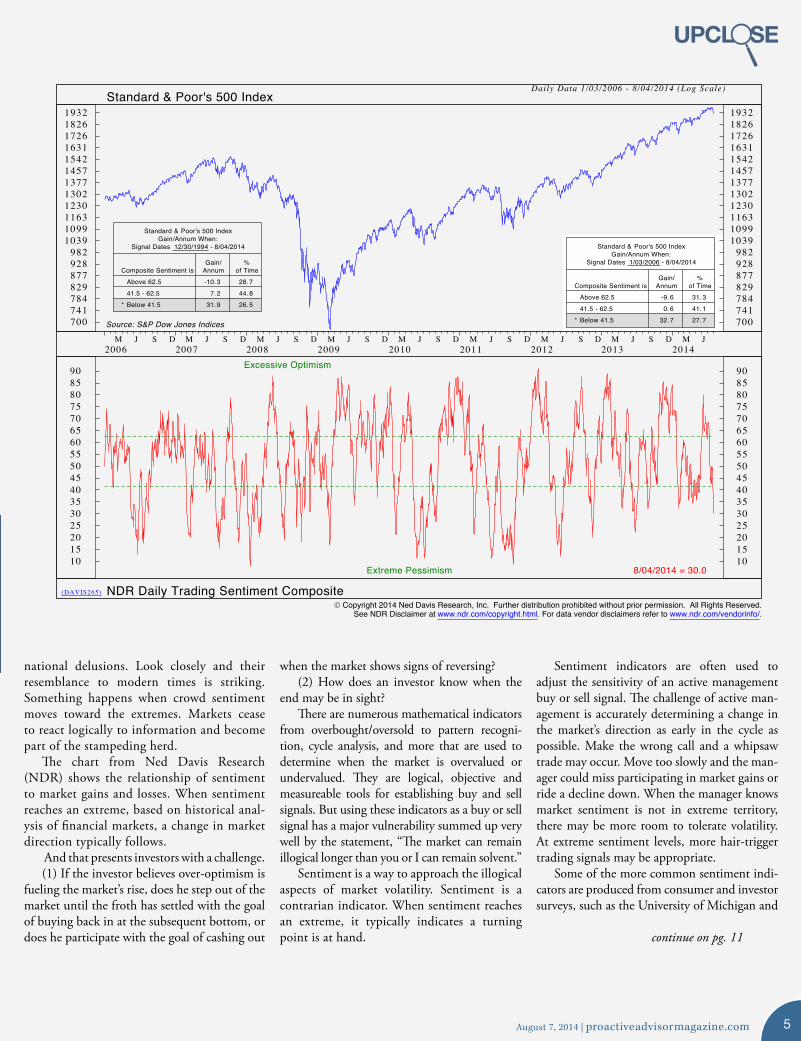

The chart from Ned Davis Research (NDR) shows the relationship of sentiment to market gains and losses. When sentiment reaches an extreme, based on historical anal-ysis of financial markets, a change in market direction typically follows.

And that presents investors with a challenge.(1) If the investor believes over-optimism is

fueling the market’s rise, does he step out of the market until the froth has settled with the goal of buying back in at the subsequent bottom, or does he participate with the goal of cashing out

when the market shows signs of reversing?(2) How does an investor know when the

end may be in sight?There are numerous mathematical indicators

from overbought/oversold to pattern recogni-tion, cycle analysis, and more that are used to determine when the market is overvalued or undervalued. They are logical, objective and measureable tools for establishing buy and sell signals. But using these indicators as a buy or sell signal has a major vulnerability summed up very well by the statement, “The market can remain illogical longer than you or I can remain solvent.”

Sentiment is a way to approach the illogical aspects of market volatility. Sentiment is a contrarian indicator. When sentiment reaches an extreme, it typically indicates a turning point is at hand.

Sentiment indicators are often used to adjust the sensitivity of an active management buy or sell signal. The challenge of active man-agement is accurately determining a change in the market’s direction as early in the cycle as possible. Make the wrong call and a whipsaw trade may occur. Move too slowly and the man-ager could miss participating in market gains or ride a decline down. When the manager knows market sentiment is not in extreme territory, there may be more room to tolerate volatility. At extreme sentiment levels, more hair-trigger trading signals may be appropriate.

Some of the more common sentiment indi-cators are produced from consumer and investor surveys, such as the University of Michigan and

continue on pg. 11

(DAVIS265)

Daily Data 1/03/2006 - 8/04/2014 (Log Scale)

Standard & Poor's 500 IndexGain/Annum When:

Signal Dates 12/30/1994 - 8/04/2014

Gain/ %Composite Sentiment is Annum of Time

Above 62.5 -10. 3 28. 741.5 - 62.5 7. 2 44. 8

* Below 41.5 31. 9 26. 5

Standard & Poor's 500 IndexGain/Annum When:

Signal Dates 1/03/2006 - 8/04/2014

Gain/ %Composite Sentiment is Annum of Time

Above 62.5 -9.6 31. 341.5 - 62.5 0. 6 41. 1

* Below 41.5 32. 7 27. 7Source: S&P Dow Jones Indices700741784829877928982

103910991163123013021377145715421631172618261932

700741784829877928982

103910991163123013021377145715421631172618261932

8/04/2014 = 30.0

Excessive Optimism

Extreme Pessimism1015202530354045505560657075808590

1015202530354045505560657075808590

2006M J S D

2007M J S D

2008M J S D

2009M J S D

2010M J S D

2011M J S D

2012M J S D

2013M J S D

2014M J

Standard & Poor's 500 Index

NDR Daily Trading Sentiment Composite Copyright 2014 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved.

.www.ndr.com/vendorinfo/. For data vendor disclaimers refer to www.ndr.com/copyright.htmlSee NDR Disclaimer at

August 7, 2014 | proactiveadvisormagazine.com 5

An investor should consider the investment objectives, risks, charges, and expenses of The Gold Bullion Strategy Fund before investing. This and other informationcan be found in the Fund’s prospectus, which can be obtained by calling 1-855-650-7453. The prospectus should be read carefully prior to investing.

There is no guarantee that The Gold Bullion Strategy Fund will achieve its investment objectives.

Fund gross estimated annual operating expenses = 1.55%

Flexible Plan Investments, Ltd., serves as investment sub-advisor to The Gold Bullion Strategy Fund, distributed by Ceros Financial Services Inc. (member FINRA).

Ceros Financial Services, Inc. and Flexible Plan Investments, Ltd. are not affi liated entities.

Advisors Preferred, LLC is the Fund’s investment adviser. Advisors Preferred, LLC is a wholly-owned subsidiary of Ceros Financial Services, Inc.

The principal risks of investing in The Gold Bullion Strategy Fund are Risk of the Sub-advisor’s Investment Strategy. Risks of Aggressive Investment Techniques,High Portfolio Turnover, Risk of Investing in Derivatives, Risks of Investing in ETFs, Risks of Investing in Other Investment Companies, Leverage Risk, ConcentrationRisk Gold Risk, Wholly-owned Corporation Risk, Risk of Non-Diversifi cation and Interest Rate Risk. “Gold Risk” includes volatility, price fl uctuations over short periods,risks associated with global monetary, economic, social and political conditions and developments, currency devaluation and revaluation and restrictions, and trading andtransactional restrictions.

For more information on the risks of The Gold Bullion Strategy Fund, including a description of each risk, please refer to the prospectus.

Visit our website to download our free white paper, The Role of Gold in Investment Portfolios

www.goldbullionstrategyfund.com

Pure GoldA durable alternative in a changing world

www.goldbul l ionstra tegyfund.com

Sought after since the beginning of time, gold may offer a valuable hedge should interest rates rise. But, is your allocation to gold tarnished by positions in mining found in many gold mutual or exchange traded funds?

The Gold Bullion Strategy Fund (QGLDX), a mutual fund that tracks the daily movement of gold, is designed to:

• Provide a defensive hedge to infl ation• Diversify a portfolio with a strategic allocation to gold• Offer commodity exposure with no K-1

1.4%

1.2%

1.0%

0.8%

0.6%

0.4%

0.2%

0.0%

04/01 06/02 08/03 10/04 12/05 02/07 04/08 06/09 08/10 10/11 12/12 02/14

0.7%

Conflicting data addsto market uncertainty

ast week was notable for the sheer number of economic reports, as well as some very conflicting data points. Throw in the continuation

of earnings season, ongoing geopolitical concerns, a Fed statement, and the financial issues emanating from Argentina and Portugal, and traders had much to ponder.

The reaction was not pretty, with the S&P 500 having its worse week since June 2012—down -2.7% and moving below its 50-day moving average for the first time since April—and the DJIA slipping into negative territory for the year (as of Friday, 8/1).

Bespoke Investment Group remarked of the week, “All told, the data dump seemed to contribute to volatility as the markets had a very hard time sorting out the implications of conflicting signals coming from business activity, consumer demand, labor market slack, price pressures, and the housing market.”

On the plus side, Q2 GDP registered a preliminary reading of +4.0%, surpassing expectations of 3.0% growth in the quarter. The Conference Board’s measure of Consumer Confidence also surprised to the upside, as did the ISM Manufacturing report. On the other side of the ledger, the Chicago PMI reading was very weak, coming in at 52.6 versus expectations of 63.0, the biggest “miss” since 2005.

L

Lukewarm housing-related and labor market reports added to the mixed picture.

The Fed statement continued to point toward an improving economy, but not enough so to justify an acceleration in the expected timing of interest rate hikes. The Fed also reiterated its intention to reduce bond buying in “further measured steps” and to keep interest rates low for a “considerable time” after ending purchases.

The market sell-off last week was largely attributed to macro global concerns and hints that inflation might be picking up more rapidly than anticipated—forcing the Fed into action at an earlier date. Part of the Fed statement acknowledged this, saying the committee now judges that “the likelihood

of inflation running persistently below two percent has diminished somewhat.”

One component of this argument can be found in the chart above, which notes the increase in the Employment Cost Index. The ECI, from the Bureau of Labor Statistics, measures the total cost of employment. The 0.7% increase quarter-over-quarter (which translates to 2.5% annualized) was a significant increase.

According to Bespoke, this spike in the quarterly reading may indicate good news in the future for Main Street wage earners, but potentially “bad news for Wall Street as corporations would be faced with higher cost of labor and input costs.”

EMPLOYMENT COST INDEX: QUARTERLY CHANGE

Source: Bespoke Investment Group

August 7, 2014 | proactiveadvisormagazine.com 7

TOPPING THE CHARTS

Read text only

Read text only

plans in case of tumultuous times in the econ-omy or the markets.”

Can you expand on that?

Well, you don’t start thinking about what to do when the wings are on fire in a jet … you should know that already. Same thing with investments in terms of having active strategies that are already prepared to react to changes in market conditions.

Over the last thirteen years we have had two 50% crashes in the market. There is no reason to think that cannot happen again, no matter

Proactive Advisor Magazine: Jay, you left the Air Force as a captain and specialist with satellite communications. Does anything from that experience apply to your work as an advisor?

Jay Blanchard: Here is what I tell clients: “I’m an old Air Force officer. I did get to fly, though I wasn’t a pilot. The Air Force teaches the importance of emergency training first. We were taught how to exit the aircraft very quickly in case of emergency or even to eject. Investments are much like that in that we always need to be prepared with contingency

While retirement may be an uphill climb for many,

Jay Blanchard applies active management to prepare his clients for

the inevitable hills and valleys of investing.

Ready

climb

Jay blanchard

By david Wismer

8 proactiveadvisormagazine.com | August 7, 2014

how well the market is behaving today—and especially with many big, troubling issues here at home and abroad.

I am a proactive advisor and not one to sit and wait. We build into our strategies risk mitigation, which is especially important for the retirees and pre-retirees we primarily work with. People have been told over and over again that you cannot time the market. I believe part of that is true, in the sense that over a very long period of time the market will mean revert back to its historical averages and trends. But it is untrue that you cannot employ strategies to avoid risk and those

major hits to your portfolio. Why wouldn’t you use strategies that could do that on behalf of your clients?

How did you first become interested in active management?

This has been a process that has occurred over many years. As you see from my back-ground, I have always been very scientifically- minded and hyper-inquisitive. The investment world has been saying for years that buy-and-hold and traditional allocation models are the best solutions to investment management.

When you see the pain first-hand that has been inflicted on people’s portfolios through these crashes, and the lingering aftereffects, how can a rational person accept that “solution” as the only answer? So I have sought out alterna-tive tactical and risk-managed strategies over the years and have found some excellent third-party managers employing those strategies.

Can you talk about the process of intro-ducing active management to clients?

Certainly, but let me qualify a few things first. We offer a holistic view of financial planning to clients so that discussion does not happen in a vacuum. It is one part of a bigger discussion around planning issues having to do with a client’s future needs, goals, and aspira-tions. And it has to take place within a deep dive into the very practical matters of taxation, college planning, expense management, long-term care, insurance, etc.

It is also colored by their appetite for risk and what makes the most sense in terms of allocations between the big buckets of strategic, tactical and guaranteed investment strategies. I like to keep that discussion as jargon-free as possible, because what client can really relate to a phrase such as “tactical” investment strategies? But I treat clients as an equal partner, recognizing their intelli-gence, and thoroughly discussing the differences between these three distinct approaches.

There is generally a role in most of our cli-ents’ portfolios for all three of these: longer-term core equity and bond strategies, highly adaptive risk-managed active strategies, and strategies that can offer a guaranteed income stream. It is all about managing client expectations and making sure we have the right pieces in place that will help them meet their overall needs

Let’s drill down on the tactical active strategies some more.

Sure. We will usually start by running a Morningstar analysis on their current invest-ment portfolio and how that has performed over the last ten years or so. We will also do something of a risk/return analysis on what they have been doing investment-wise.

This is pretty eye-opening and just about every new client will never have seen anything like this before. I will also take them through some fun-damental concepts of risk/return curves—using graphs—and explain how we utilize tactical active strategies to find the appropriate risk/

continue on pg. 10

Securities & Investment Advisory Services

offered through NEXT Financial Group, Inc.

Member, FINRA/SIPC. The Financial Guys LLC

is not an affiliate of NEXT Financial Group, Inc.

August 7, 2014 | proactiveadvisormagazine.com 9

M U LT I - M A R K E T+

MULTI-STRATEGY+

MULTI-MANAGER

One p rtfolioD Y N A M I C A L LY R I S K - M A N A G E D

L E A R N M O R E

Past performance does not guarantee future results.

The opportunity for profits

carries with it the possibility of losses.

800-347-3539 | flexibleplan.com

A complete list of all of our recommendations over the last 12 months and Brochure Form ADV Part 2A are available upon request.

matters. I have developed an initiative called Wealth to Women that specifically addresses the needs of this audience. This fits in well with my overall philosophy and value proposition of empowering people to feel confident in their financial decision-making.

return profile for a specific strategy or blend of strategies. This takes some time to explain, but it is a highly effective presentation. When they see where a combination of tactical strategies falls in terms of returns, with lower risk than they are now exposed to, that becomes clear as day from a conceptual standpoint.

I will also explain some statistics around the market’s historical performance, showing the percentages of how often markets are in bull, bear, and sideways markets. Again, this is an eye-opener, and once they understand that, I will explain how the tactical strategies are formulated to perform under any market conditions—that we are employing third-party managers who do nothing but analyze and react to current market conditions.

This really starts making sense to clients and I feel confident then that they will be open to exploring a variety of strategy combinations, depending on their specific needs. Setting the appropriate expectations and understanding of strategies becomes especially important when it comes time for client review meetings.

No matter what the overall market may be doing, we will have in place a well-diversified strategy combination, with each element doing what it is supposed to be doing. It is impossible to predict the future, or future returns, but I am firmly convinced that a well-diversified combination of strategies will perform the best, with managed risk, over market cycles.

Excellent, Jay. How do you get the word out to prospective clients?

Our firm, The Financial Guys, LLC, is very active in marketing in the Buffalo, New York area. I help to line up guest speakers and occa-sionally appear myself on our radio show, which is the top-rated business talk show in western New York. This show focuses on personal fi-nance, local economic issues and topical national matters. It has been terrific for name awareness and lead generation, as well as providing a real service to the community. I also do a lot in terms of seminars and speaking engagements, and have a special interest in women’s financial

continued from pg. 9

Pho

togr

aphy

: KC

Kra

tt

10 proactiveadvisormagazine.com | August 7, 2014

There can be no assurance that any investment product will achieve its investment objective(s). There are risks associated with investing, including the entire loss of principal invested. Investing involves market risk. The investment return and principal value of any investment product will fluctuate with changes in market conditions. Guggenheim Investments represents the investment management businesses of Gug-genheim Partners, LLC. Securities offered through Guggenheim Funds Distributors, LLC. Guggenheim Funds Distributors, LLC is affiliated with Guggenheim Partners, LLC. x0515 #12526

Uncover the True Cost of Trading Mutual Funds and ETFs

The reflexive perception that ETFs cost less, simply based on their low expense ratios, and are more cost-effective than mutual funds, is not entirely true. In addition to an expense ratio, there are additional considerations that should be considered when making an informed choice between ETFs and funds— including spreads and commissions. This informative white paper from Rydex Funds provides an in-depth look at the cost of ownership of no-transaction-fee (NTF) mutual funds and ETFs—with a focus on active investing strategies.

Request your free copy.Call 630.505.3749 or visit guggenheiminvestments.com/rydex

Chicago | New York City | Santa Monica

Rydex Funds

A Comparison of ETFs and Mutual Funds—The True Cost of Investing

Conference Board consumer confidence surveys or the American Association of Individual Investors survey. By the simple nature of the survey process, their results tend to lag current sentiment levels and are also vulnerable to the fact that respondents sometimes answer the way they believe the interviewer wants to hear or the way they think others may respond.

To overcome the lag time and potential bias of the survey methodology, analysts look for ways to confirm investor sentiment by the actions of investors. Market breadth is one such tool. Market breadth compares the number of companies advancing in price relative to the number declining. When more companies are rising in value, sentiment is bullish.

Money flows in and out of stocks, put-call ratios, volatility, momentum, and other

technical factors are also considered indicators of investor sentiment. In the prior chart, NDR combines a number of technical indicators to create its Daily Trading Sentiment Composite. These are often complemented by the NDR Crowd Sentiment Poll, which is a more sub-jective tool.

The key to using these indicators is to un-derstand that sentiment has historically only worked as an indicator at the real extremes. The investor needs to know more than just whether or not the market is bullish or bearish, but whether or not sentiment is increasing, at what rate, and how this compares to prior market turning points. And then there’s the matter of the black swans—unexpected events that sud-denly change market dynamics.

There is also the perspective that historical works such as Mackay’s are not a reflection of modern thought processes or available informa-tion. Does the crowd mentality carry the same power today? Certainly many economists and experienced market observers think so.

“Asset price bubbles and crashes are here to stay. They appear to be a consequence of human nature.”

– John C. Williams, President, Federal Reserve Bank of San Francisco, September 9, 2013.

While active management strives to be an objective approach based on mathematical models to generate buy and sell decisions that can be replicated consistently over time, it must also accommodate the illogical aspects of the market as well. Sentiment indicators are one means of fine-tuning the active management model to take into account human nature.

continued from pg. 5

When the manager knows market sentiment is not in extreme territory, there may be more room to tolerate volatility.

11August 7, 2014 | proactiveadvisormagazine.com

The opinions and forecasts expressed herein are those of the author and may not actually come to pass. Any opinions and viewpoints regarding the future of the markets should not be construed as recommendations of any specific security nor specific investment advice. The analysis and information in this edition and on our website is for informational purposes only. No part of the material presented in this edition or on our websites is intended as an investment recommendation or investment advice. Neither the information nor any opinion expressed nor any portfolio constitutes a solicitation to purchase or sell securities or any investment program.

EditorDavid Wismer

Marketing CoordinatorElizabeth Whitley

Contributing WritersLinda Ferentchak

David Wismer

Graphic DesignerTravis Bramble

Contributing PhotographerKC Kratt

August 7, 2014Volume 3 | Issue 6

Proactive Advisor Magazine is dedicated to promoting and educating on active investment management. Distribution reaches a wide audience of financial professionals who advise clients on investments and portfolio management. Each issue features an experienced investment advisor who offers insights on active money management, client service, and investment approaches. Additionally, Proactive Advisor Magazine offers an up-close look at a topic with current relevance to the field of active management.

Advertising proactiveadvisormagazine.com/advertising

Reprintsproactiveadvisormagazine.com/reprints

Contactproactiveadvisormagazine.com/contact

Proactive Advisor MagazineCopyright 2014 © Dynamic Performance Publishing, Inc. All rights reserved. Reproduction of printed form, whole or in part, without permission is prohibited.

Stay connected

Top summer reading for financial advisors Explore ten of the top-rated books for financial advisors, as ranked by Amazon. Enjoy these helpful titles on a getaway—whether it’s on the beach or on a business trip.

Average investors and finance prosthink about risk differently

Here are three ways in which individual investors andfinance professionals differ in their risk thinking

and the major impact that can have on portfolios.

Evaluating advisors’ choices of investment modelsConsulting firm Casey Quirk evaluates four investment models used by financial advisors. The firm says advisors using third-party managers will increase market share over the next three years.

How to solve the referral conundrumFocusing more attention on a formalized process

of obtaining referrals can pay large dividends.

What’s worrying advisors? Think market riskThe most recent Fidelity Advisor Pulse survey, conducted in the second quarter, shows that market volatility is the No. 1 issue on the minds of

the more than 200 advisors polled.

The recession generation: What Millennials want from money managementMillennials, roughly defined as young adults born after 1980, will control $7 trillion in liquid assets by the end of the decade—their investment preferences may be radically different.

12

L NKS WEEK