itulip.com - itulip, inc © 2007 itulip, inc. the contrary market view of the markets predicting...

TRANSCRIPT

iTulip.com - iTulip, Inc © 2007iTulip.com - iTulip, Inc © 2007

iTulip, Inc.iTulip, Inc.

The Contrary Market View of the Markets

Predicting your economic future since 1998

The Contrary Market View of the Markets

Predicting your economic future since 1998

Eric JanszenFounder and PresidentiTulip, Inc.

iTulip.com

iTulip.com - iTulip, Inc © 2007iTulip.com - iTulip, Inc © 2007

iTulip, Inc.iTulip, Inc. All information provided "as is" for

informational purposes only, not intended for trading purposes or advice. Nothing appearing in this presentation should be considered a recommendation to buy or to sell any security or related financial instrument. iTulip, Inc. is not liable for any informational errors, incompleteness, or delays, or for any actions taken in reliance on information contained herein. See full disclaimer here: http://www.itulip.com/GeneralDisclaimer.htm

All information provided "as is" for informational purposes only, not intended for trading purposes or advice. Nothing appearing in this presentation should be considered a recommendation to buy or to sell any security or related financial instrument. iTulip, Inc. is not liable for any informational errors, incompleteness, or delays, or for any actions taken in reliance on information contained herein. See full disclaimer here: http://www.itulip.com/GeneralDisclaimer.htm

iTulip.com

iTulip.com - iTulip, Inc © 2007iTulip.com - iTulip, Inc © 2007

HistoryHistory

Founded: 1998Visitors: 7,000,000

Members: 2,200

Economic and Financial MarketsMacro Trends

Founded: 1998Visitors: 7,000,000

Members: 2,200

Economic and Financial MarketsMacro Trends

Bill Griffeth, CNBC

iTulip.com - iTulip, Inc © 2007iTulip.com - iTulip, Inc © 2007

What is iTulip?What is iTulip?

March 2006: “ iTulip.com, which was restarted this week after a three-year hiatus, does not hesitate to claim credit for accurately predicting that the bubble would pop. It even got the timing right."

March 2006: “ iTulip.com, which was restarted this week after a three-year hiatus, does not hesitate to claim credit for accurately predicting that the bubble would pop. It even got the timing right."

iTulip.com - iTulip, Inc © 2007iTulip.com - iTulip, Inc © 2007

What is iTulip?What is iTulip?

May 2007 "A typical down cycle [for residential real estate] is five to seven years," says Eric Janszen, co-author of America's Bubble Economy: Profit When It Pops (Wiley, 2006), one of a recent crop of bubble books and far from the gloomiest and doomiest.”

May 2007 "A typical down cycle [for residential real estate] is five to seven years," says Eric Janszen, co-author of America's Bubble Economy: Profit When It Pops (Wiley, 2006), one of a recent crop of bubble books and far from the gloomiest and doomiest.”

iTulip.com - iTulip, Inc © 2007iTulip.com - iTulip, Inc © 2007

Other iTulip FirstsOther iTulip Firsts

Housing BubbleAugust 2002: “Yes. It’s a Housing bubble.”January 2004: “Will end by seizing up.”January 2005: “Will Last 10+ Years.”June 2005: “It’s a top.”All-Assets-Up Global Credit Bubble June 2006: “All assets positively correlated, driven by excess global liquidity.”

Housing BubbleAugust 2002: “Yes. It’s a Housing bubble.”January 2004: “Will end by seizing up.”January 2005: “Will Last 10+ Years.”June 2005: “It’s a top.”All-Assets-Up Global Credit Bubble June 2006: “All assets positively correlated, driven by excess global liquidity.”

Money Matters

Finance

Award

iTulip.com - iTulip, Inc © 2007iTulip.com - iTulip, Inc © 2007

The ModelThe Model

Ka-Poom Theory of Bubble CyclesDeveloped for Osborn Capital, LLC in 1999 to time stock sales, re-investment of proceedsApplicationSpring 2000: Exit tech stocks and purchase US Treasury Bonds

Sell Cisco @ $68, buy 10 year Treasuries 6.51%

Summer 2001: Purchase Precious Metals

Buy gold @ $270, silver $4.25, platinum $452

Ka-Poom Theory of Bubble CyclesDeveloped for Osborn Capital, LLC in 1999 to time stock sales, re-investment of proceedsApplicationSpring 2000: Exit tech stocks and purchase US Treasury Bonds

Sell Cisco @ $68, buy 10 year Treasuries 6.51%

Summer 2001: Purchase Precious Metals

Buy gold @ $270, silver $4.25, platinum $452

iTulip.com - iTulip, Inc © 2007iTulip.com - iTulip, Inc © 2007

Ka-Poom Theory V1.0 (1999)

Ka-Poom Theory V1.0 (1999)

US Foreign and domestic debt repudation1. Bubble formation2. Bubble collapse and disinflation3. Domestic reflation to protect the

economy (rate cuts, tax cuts, dollar depreciation)

4. Repatriation of dollar denominated assets

5. Global central bank cooperation to support the US dollar fails

6. Declining dollar, high inflation, rising interest rates, slowing economy

7. Go to Step 3

US Foreign and domestic debt repudation1. Bubble formation2. Bubble collapse and disinflation3. Domestic reflation to protect the

economy (rate cuts, tax cuts, dollar depreciation)

4. Repatriation of dollar denominated assets

5. Global central bank cooperation to support the US dollar fails

6. Declining dollar, high inflation, rising interest rates, slowing economy

7. Go to Step 3

Monetize Debt

Inflation

Expectations of Future Inflation

Consume Now

Buy on Credit

Insufficient Domestic Savings

Classic vicious circle inflation driven by currency depreciation

iTulip.com - iTulip, Inc © 2007iTulip.com - iTulip, Inc © 2007

Ka-Poom Theory V1.0 (1999)

Ka-Poom Theory V1.0 (1999)

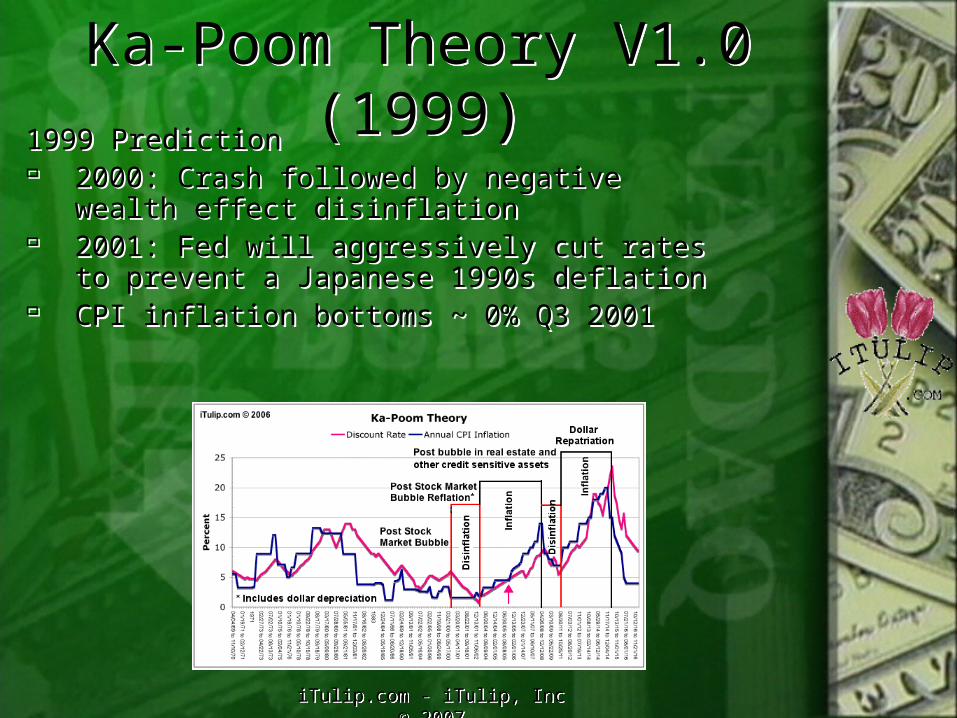

1999 Prediction 2000: Crash followed by negative

wealth effect disinflation 2001: Fed will aggressively cut rates

to prevent a Japanese 1990s deflation CPI inflation bottoms ~ 0% Q3 2001

1999 Prediction 2000: Crash followed by negative

wealth effect disinflation 2001: Fed will aggressively cut rates

to prevent a Japanese 1990s deflation CPI inflation bottoms ~ 0% Q3 2001

iTulip.com - iTulip, Inc © 2007iTulip.com - iTulip, Inc © 2007

Ka-Poom Theory V1.0 (1999)

Ka-Poom Theory V1.0 (1999)

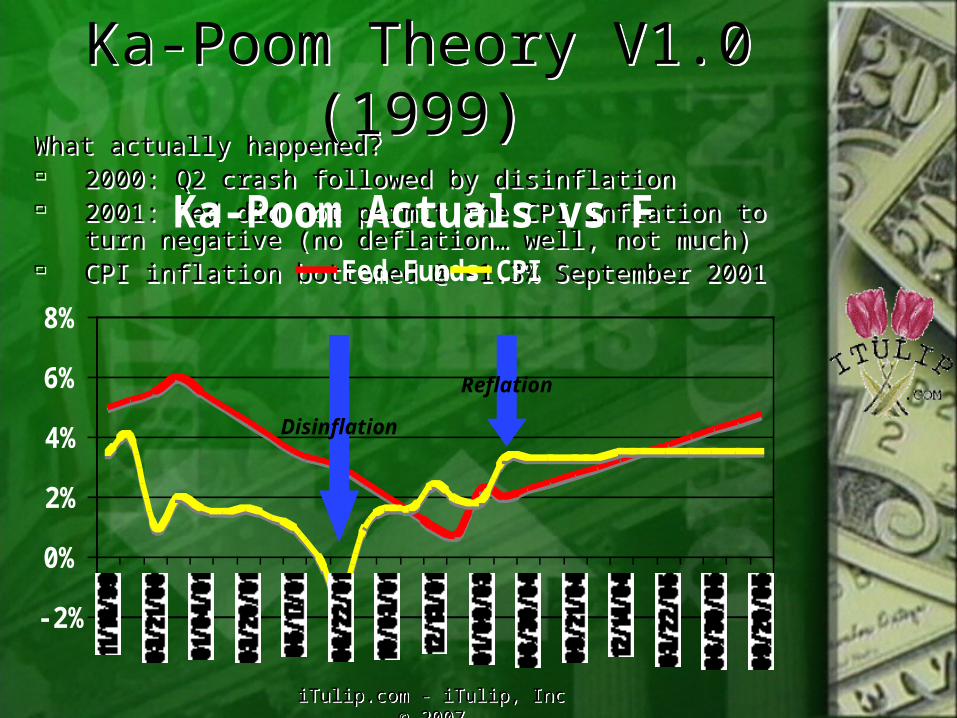

What actually happened? 2000: Q2 crash followed by disinflation 2001: Fed did not permit the CPI inflation to

turn negative (no deflation… well, not much) CPI inflation bottomed @ -1.3% September 2001

What actually happened? 2000: Q2 crash followed by disinflation 2001: Fed did not permit the CPI inflation to

turn negative (no deflation… well, not much) CPI inflation bottomed @ -1.3% September 2001

Ka-Poom Actuals vs Forecast

-2%

0%

2%

4%

6%

8%

11/18/9903/21/0001/04/0103/20/0105/17/0108/22/0110/03/0112/13/0101/09/0306/30/0409/21/0412/14/0403/22/0506/30/0509/20/05

Fed Funds CPI

Disinflation

Reflation

iTulip.com - iTulip, Inc © 2007iTulip.com - iTulip, Inc © 2007

Ka-Poom TheoryKa-Poom Theory

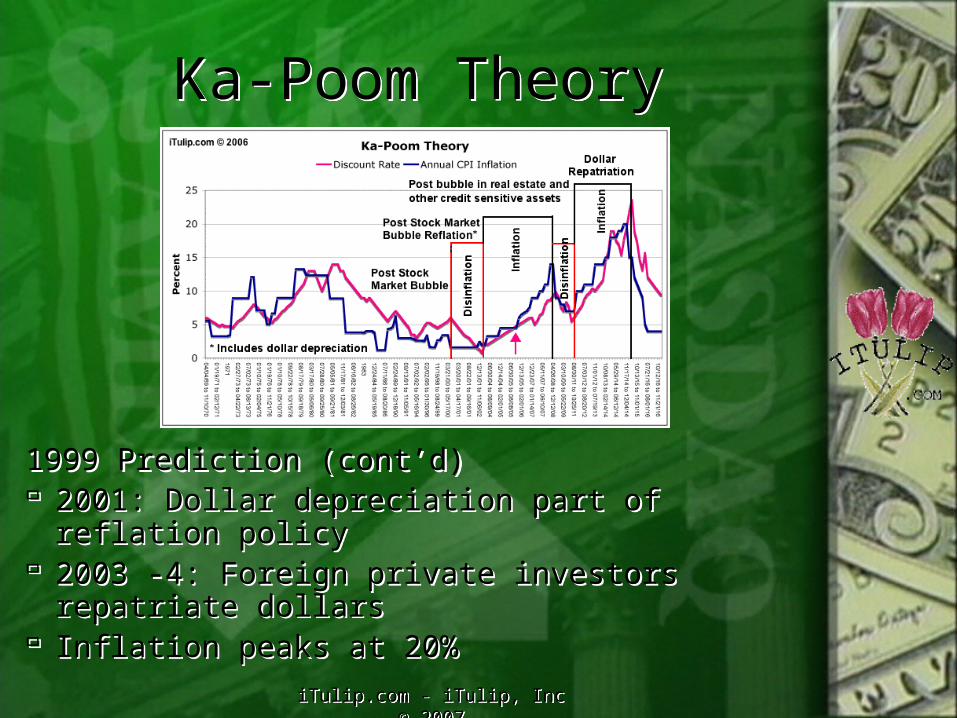

1999 Prediction (cont’d) 2001: Dollar depreciation part of reflation

policy 2003 -4: Foreign private investors repatriate

dollars Inflation peaks at 20%

1999 Prediction (cont’d) 2001: Dollar depreciation part of reflation

policy 2003 -4: Foreign private investors repatriate

dollars Inflation peaks at 20%

iTulip.com - iTulip, Inc © 2007iTulip.com - iTulip, Inc © 2007

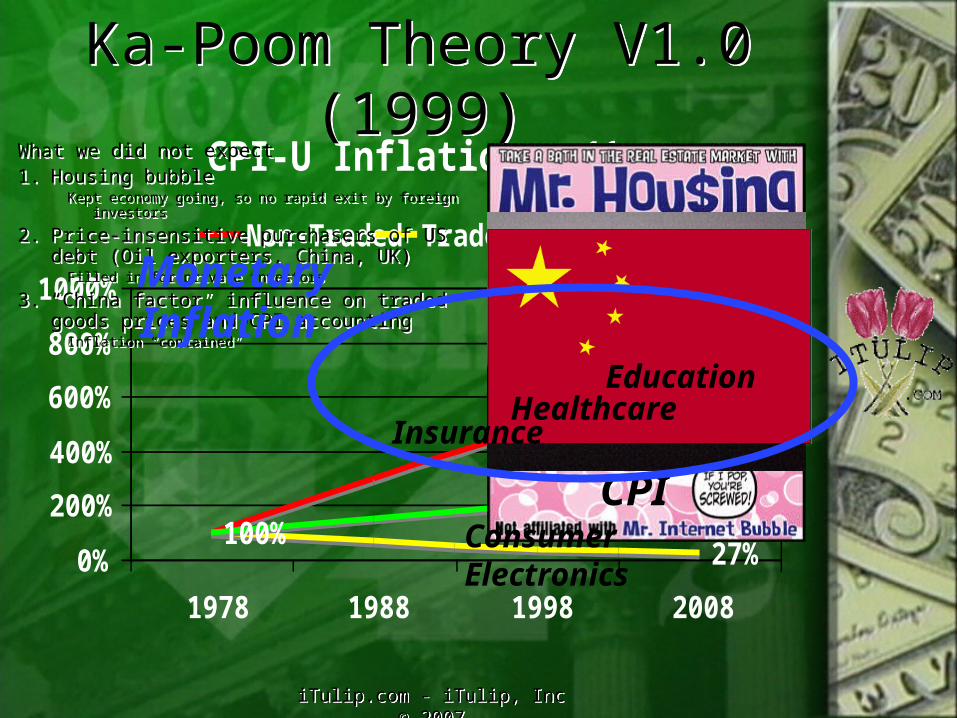

CPI-U Inflation - 1978 to 2008

800%

27%100%

300%

0%

200%

400%

600%

800%

1000%

1978 1988 1998 2008

Non-Traded Traded Total

Ka-Poom Theory V1.0 (1999)

Ka-Poom Theory V1.0 (1999)

What we did not expect1. Housing bubble

Kept economy going, so no rapid exit by foreign investors

2. Price-insensitive purchasers of US debt (Oil exporters, China, UK)

Filled in for private investors

3. “China factor” influence on traded goods prices and CPI accounting

Inflation “contained”

What we did not expect1. Housing bubble

Kept economy going, so no rapid exit by foreign investors

2. Price-insensitive purchasers of US debt (Oil exporters, China, UK)

Filled in for private investors

3. “China factor” influence on traded goods prices and CPI accounting

Inflation “contained” EducationHealthcare

Insurance

Consumer Electronics

CPI

Monetary

Inflation

iTulip.com - iTulip, Inc © 2007iTulip.com - iTulip, Inc © 2007

Ka-Poom Theory V2.0 (2004)

Ka-Poom Theory V2.0 (2004)

Ka-Poom disinflation-reflation cycle

1. Bubble formation2. Bubble collapse and disinflation3. Domestic reflation policies for

economic recovery4. Cooperative currency

depreciation props up US dollar5. Go to Step 1

Ka-Poom disinflation-reflation cycle

1. Bubble formation2. Bubble collapse and disinflation3. Domestic reflation policies for

economic recovery4. Cooperative currency

depreciation props up US dollar5. Go to Step 1

iTulip.com - iTulip, Inc © 2007iTulip.com - iTulip, Inc © 2007

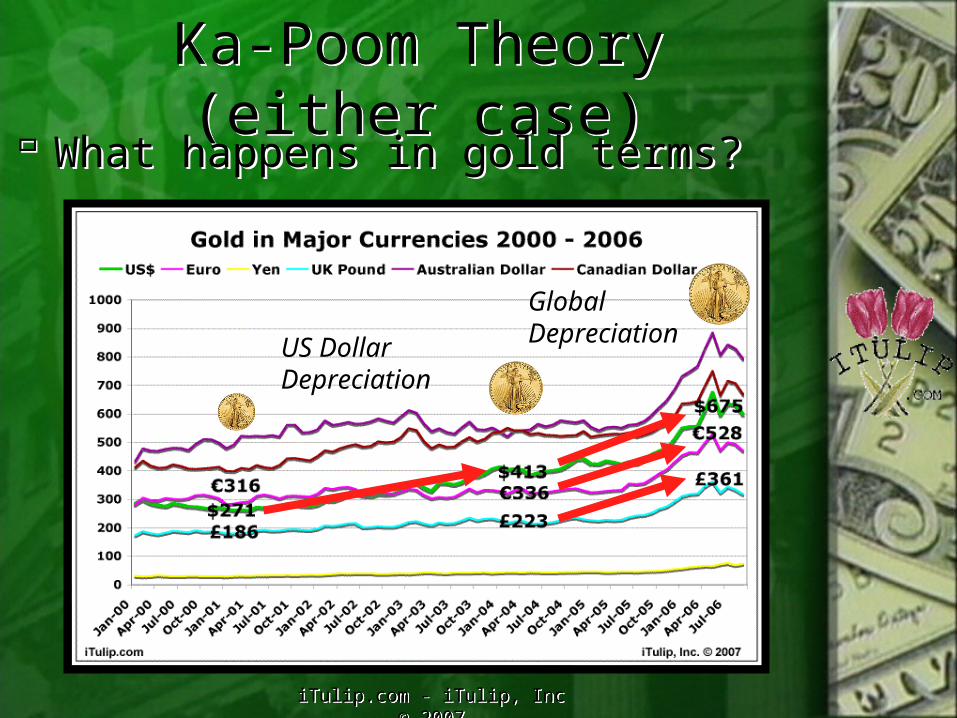

Ka-Poom Theory (either case)

Ka-Poom Theory (either case)

What happens in gold terms? What happens in gold terms?

US Dollar Depreciation

Global Depreciation

iTulip.com - iTulip, Inc © 2007iTulip.com - iTulip, Inc © 2007

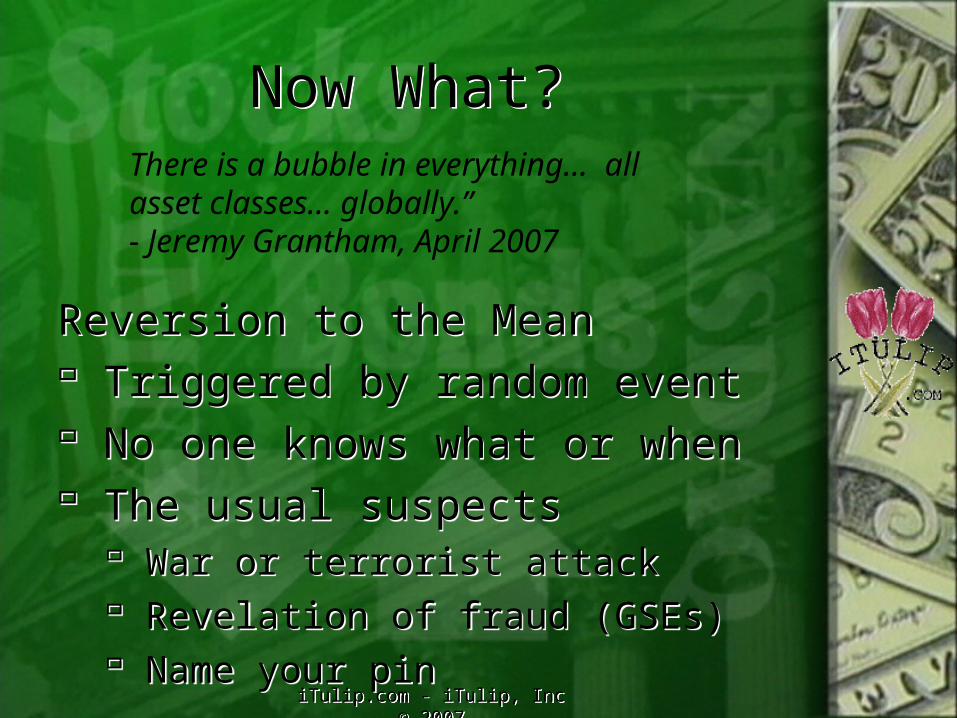

Now What?Now What?

Reversion to the Mean Triggered by random event No one knows what or when The usual suspects

War or terrorist attack Revelation of fraud (GSEs) Name your pin

Reversion to the Mean Triggered by random event No one knows what or when The usual suspects

War or terrorist attack Revelation of fraud (GSEs) Name your pin

There is a bubble in everything… all asset classes… globally.” - Jeremy Grantham, April 2007

iTulip.com - iTulip, Inc © 2007iTulip.com - iTulip, Inc © 2007

Then What?Then What?Disinflation Phase - Risk Adjustments Within asset classes

From most risky to least Among asset classes

Purchasing power vs yield Liquidity vs value

Among geographies Local vs remote Lowest economic and political risk

Disinflation Phase - Risk Adjustments Within asset classes

From most risky to least Among asset classes

Purchasing power vs yield Liquidity vs value

Among geographies Local vs remote Lowest economic and political risk

0

2,0004,000

6,000

8,000

10,00012,000

14,000

1st 2ndQtr

3rdQtr

4thQtr

5thQtr

6thQtr

7thQtr

8thQtr

9thQtr

10thQtr

Stocks Bonds Gold

Crisis

CrisisCrisis

Crisis

iTulip.com - iTulip, Inc © 2007iTulip.com - iTulip, Inc © 2007

What happens to gold?What happens to gold?

Previous asset price reversion periods Capital flight to political safety

Dollar rises, gold falls US Government policy fights disinflation

Rate cuts, gov’t spending, $ depreciation

Coordinated global central bank policy But unlike the 2001 version…

Previous asset price reversion periods Capital flight to political safety

Dollar rises, gold falls US Government policy fights disinflation

Rate cuts, gov’t spending, $ depreciation

Coordinated global central bank policy But unlike the 2001 version…

Reflation

5.25%

4.25%

3.25%

2.25%

5%

3%

6%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

1st Qtr 2nd Qtr 3rd Qtr 4th Qtr

Fed Funds RateDeficit % GDP

iTulip.com - iTulip, Inc © 2007iTulip.com - iTulip, Inc © 2007

After Disinflation?After Disinflation?

What’s different this time? Not in 2001 “Kansas” anymore Oil is at $60 not $20 Global inflation is high not low US is at war not “peace” US running huge fiscal deficit vs surplus Dollar is weak not strong Euro has never been stress-tested

What’s different this time? Not in 2001 “Kansas” anymore Oil is at $60 not $20 Global inflation is high not low US is at war not “peace” US running huge fiscal deficit vs surplus Dollar is weak not strong Euro has never been stress-tested

iTulip.com - iTulip, Inc © 2007iTulip.com - iTulip, Inc © 2007

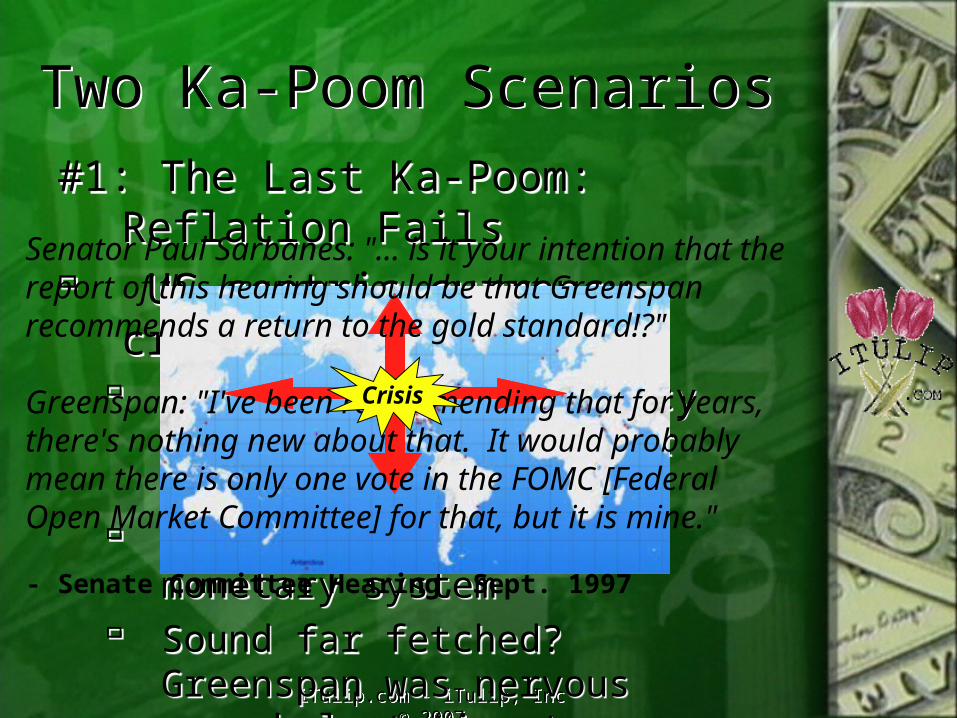

Two Ka-Poom ScenariosTwo Ka-Poom Scenarios

#1: The Last Ka-Poom: Reflation Fails

US-centric currency crisis 1997/1998 style currency crisis,

except in major currencies Dissolution of global monetary

system Sound far fetched? Greenspan

was nervous enough last time to propose…

#1: The Last Ka-Poom: Reflation Fails

US-centric currency crisis 1997/1998 style currency crisis,

except in major currencies Dissolution of global monetary

system Sound far fetched? Greenspan

was nervous enough last time to propose…

Senator Paul Sarbanes: "... is it your intention that the report of this hearing should be that Greenspan recommends a return to the gold standard!?"

Greenspan: "I've been recommending that for years, there's nothing new about that. It would probably mean there is only one vote in the FOMC [Federal Open Market Committee] for that, but it is mine."

- Senate Committee Hearing, Sept. 1997

Crisis

iTulip.com - iTulip, Inc © 2007iTulip.com - iTulip, Inc © 2007

Two Ka-Poom ScenariosTwo Ka-Poom Scenarios

#2: New Ka-Poom Cycle: Relfation Succeeds

The Next Bubble Developed by markets Encouraged by government tax

and monetary policy Alternative Energy and

Infrastructure

#2: New Ka-Poom Cycle: Relfation Succeeds

The Next Bubble Developed by markets Encouraged by government tax

and monetary policy Alternative Energy and

Infrastructure

“We are too dependent on imported oil from troubled parts of the world, so the question was, how would we craft something that would give us energy security as soon as possible? … we had presentations from terrific scientists on progress that's been made in technology and a number of alternative sources of energy — everything from solar to wind to energy to batteries and clean coal.

-Treasury Secretary Henry Paulson Feb. 2007

iTulip.com - iTulip, Inc © 2007iTulip.com - iTulip, Inc © 2007

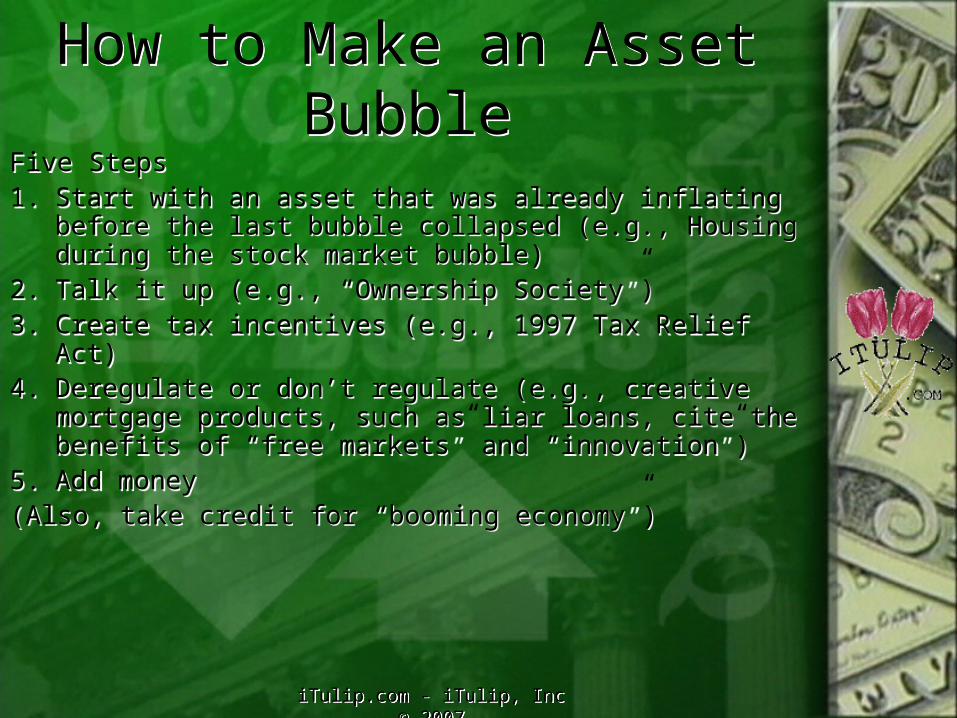

How to Make an Asset Bubble

How to Make an Asset Bubble

Five Steps1. Start with an asset that was already inflating

before the last bubble collapsed (e.g., Housing during the stock market bubble)

2. Talk it up (e.g., “Ownership Society”)3. Create tax incentives (e.g., 1997 Tax Relief Act)4. Deregulate or don’t regulate (e.g., creative

mortgage products, such as liar loans, cite the benefits of “free markets” and “innovation”)

5. Add money(Also, take credit for “booming economy”)

Five Steps1. Start with an asset that was already inflating

before the last bubble collapsed (e.g., Housing during the stock market bubble)

2. Talk it up (e.g., “Ownership Society”)3. Create tax incentives (e.g., 1997 Tax Relief Act)4. Deregulate or don’t regulate (e.g., creative

mortgage products, such as liar loans, cite the benefits of “free markets” and “innovation”)

5. Add money(Also, take credit for “booming economy”)

iTulip.com - iTulip, Inc © 2007iTulip.com - iTulip, Inc © 2007

The Tea LeavesThe Tea LeavesHard Assets: The Fourth Currency1. Disinflation period when gold

declines 25%+ during rush to liquidity (ala Feb. 2007 and Spring 2006)

2. If continues, asymmetric economic impact causes unexpected change in pricing relationships (outside “model”)

3. Hits currency and credit derivatives

4. Capital seeks safety from chaos while global central banks cope

Hard Assets: The Fourth Currency1. Disinflation period when gold

declines 25%+ during rush to liquidity (ala Feb. 2007 and Spring 2006)

2. If continues, asymmetric economic impact causes unexpected change in pricing relationships (outside “model”)

3. Hits currency and credit derivatives

4. Capital seeks safety from chaos while global central banks cope

iTulip.com - iTulip, Inc © 2007iTulip.com - iTulip, Inc © 2007

iTulip SelectiTulip Select

Specialist Interviews:Jim RogersMartin MayerDr. Jamie GalbraithJames Scurlock

Specialist Interviews:Jim RogersMartin MayerDr. Jamie GalbraithJames Scurlock

iTulip.com

CommentariesBook ReviewsPortfolio

ModelingShadowFed

CommentariesBook ReviewsPortfolio

ModelingShadowFed

http://www.itulip.com

The Investment Thesis for the Next Cycle