powerpoint presentationeditool.vdm.berlin/archiv_akademie/1498662921_vdm_london...contrary to the...

TRANSCRIPT

June 2017

Economic Outlook

Metals Market Economic Drivers

Frederick R. Demler, Ph.D.

Executive Vice President, LME Metals

INTL FCStone Financial Inc. – FCM Division

+1-917-297-3045; [email protected]

The INTL FCStone Inc. group of companies conducts a global full-service, integrated commodities, futures, investment banking, derivatives trading and risk-management business. Our

research department may provide research, market commentary and general or specific analyses as may be requested from time to time by our clients, which may reflect opinions that are

contrary to the illustrations in this presentation. INTL FC Stone Inc. has adopted policies designed to preserve the independence of our research analysts. These policies prohibit non-

research personnel from influencing research personnel to issue favorable research or offer to change a research rating or price target as consideration for an inducement to obtain

business or other compensation. The INTL FCStone proprietary trading desks and investing businesses may make investment decisions that are inconsistent with the materials in this

document. INTL FCStone Inc. and its affiliates, officers, directors, and employees, will from time to time have long or short positions in, act as principal in, and buy or sell instruments the

derivatives that are identical or economically related to the derivatives referred to in this document.

This presentation is not an offer to sell or a solicitation of an offer to buy any derivative or security and is not a commitment to enter into any derivative or other transaction, and does not

create a binding obligation on INTL FCStone Inc. or any of its affiliates. This presentation does not constitute investment research or a personal recommendation or take into account the

particular investment objectives, financial situations, or needs of individual clients or recipients of this material. You are directed to seek professional and tax advice. Past performance is

not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Fluctuations in exchange rates could have adverse effects on the value or

price of, or income derived from, certain investments. Risks presented by commodities, futures (and options thereon), swaps and other OTC products (“derivatives”) depend upon the

terms of the transaction and your circumstances. Options are not suitable for all investors. Option buyers may lose their entire investment. Option sellers may have an unlimited loss.

Certain derivative contracts contain a variety of selling prices, knock out prices and accumulation periods and require an understanding of the contract’s specific pricing mechanisms

before you enter into such contracts. Derivatives generally involve credit risk, market risk, liquidity risk, funding risk, operational risk, legal and documentation risk, regulatory and tax risk.

You should refrain from entering into derivatives unless you fully understand the risks, including the extent of your potential loss. In evaluating risk, you should consider that an OTC

derivative transaction may be modified or terminated only by mutual consent of the original parties and subject to agreement on individually negotiated terms. Accordingly, it may not be

possible for you to modify, terminate or offset your obligations or your exposure to the risk associated with a transaction prior to its scheduled termination date.

In addition to the general risks associated with derivatives, highly customized derivative transactions may increase liquidity risk and introduce other significant risks. Leveraged

transactions may create exposure to substantial gains or losses in response to relatively small market fluctuations. INTL FCStone Inc. and its affiliates may from time to time take

proprietary positions and make a market in instruments identical or economically related to derivative transactions entered into with you, or may have an investment banking or other

commercial relationship with and access to information from the issuer(s) of securities, financial instruments or other interests underlying derivative transactions entered into with you. INTL

FCStone Inc. and its affiliates may choose to hedge their obligations by trading in derivatives. The costs associated with hedging activity could affect the market value of, or the price at

which we would be willing to enter into a transaction. Further, we may internalize and match order flow or route it externally for execution. If we choose to match orders internally, our

compensation is greater than if we execute the order externally. INTL FCStone Inc. and its affiliates make no representation, warranty or guarantee as to, and shall not be responsible for,

the accuracy or completeness of the information contained in this presentation and have no obligation to update the information.

Any illustrations provided are strictly hypothetical and no representation is being made that any person will, or is likely to achieve profits or losses similar to those examples. You are

advised to undertake an independent review of the potential legal, tax, regulatory and accounting implications of any derivatives transaction to determine whether derivatives or any

particular structure would be suitable for you, and if necessary seek professional advice. Derivatives give rise to substantial risk and are not suitable for all recipients of this presentation.

The INTL FC Stone Inc. group of companies act solely in the capacity of an arm’s length counterparty and not in the capacity of your financial adviser or fiduciary. Prior to undertaking any

transaction, you should discuss with your tax or other adviser how a particular transaction may affect you. Any opinions expressed are subject to change without notice and certain

information is based upon information from third party sources which we have not independently verified.

All references to and discussions of Structured OTC products are made solely on behalf of INTL FCStone Markets, LLC (“IFM”), a subsidiary of INTL FCStone Inc., and a member of the

National Futures Association (“NFA”) and provisionally registered with the U.S. Commodity Futures Trading Commission (“CFTC”) as a swap dealer. IFM’s products are available only to

individuals or firms who qualify under CFTC rules as an ‘Eligible Contract Participant’ (“ECP”).

References to exchange-traded futures and options are made on behalf of FCStone, Financial Inc (IFI) an NFA member and CFTC-registered futures commission merchant, and INTL

FCStone Ltd (“IFL”), a company registered in England and Wales (5616586) which is authorized & regulated by the Financial Conduct Authority [FRN 446717]. IFL is a wholly owned

subsidiary of INTL FCStone Inc., a public company incorporated in the United States, and listed on the NASDAQ stock exchange [Ticker: INTL].

No part of this presentation may be (i) copied, photocopied or duplicated in any form by any means or (ii) redistributed without the prior written consent of INTL FCStone Inc. © Copyright

2017. All rights reserved.

2

Disclaimer

This section of the page should be blank except when footnotes are present.

Economic Briefing

& Metal Outlook

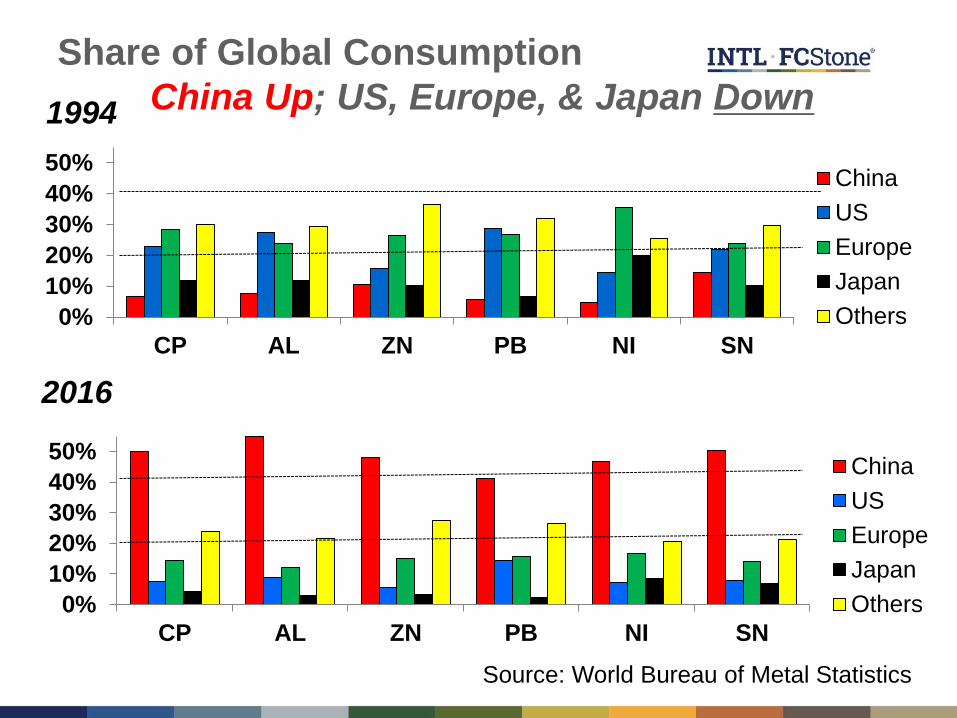

Share of Global Consumption

China Up; US, Europe, & Japan Down

2016

1994

Source: World Bureau of Metal Statistics

0%

10%

20%

30%

40%

50%

CP AL ZN PB NI SN

China

US

Europe

Japan

Others

0%

10%

20%

30%

40%

50%

CP AL ZN PB NI SN

China

US

Europe

Japan

Others

7

8

9

10

11

12

13

14

15

Feb-15 Jun-15 Oct-15 Feb-16 Jun-16 Oct-16 Feb-17

Fixed Asset Investment

Retail Sales

%yoy

China, GDP Growth

Sources: Bloomberg, INTL FCStone estimates

GDP

Fixed Asset Investment

vs Retail Sales

6.4

6.5

6.6

6.7

6.8

6.9

7.0

7.1

7.2

7.3

Q4 1

4

Q1 1

5

Q2 1

5

Q3 1

5

Q4 1

5

Q1 1

6

Q2 1

6

Q3 1

6

Q4 1

6

Q1 1

7

% yoy

-40

-30

-20

-10

0

10

20

30

40

50

Mar-15 Sep-15 Mar-16 Sep-16 Mar-17

Exports Imports

% yoy

GDP Growth is Accelerating

Fixed Investment Firming

Retail Sales Steady

Exports/Imports Slow

from Early ’17 Surge

-10

-5

0

5

10

15

20

25

30

Feb-15 Jun-15 Oct-15 Feb-16 Jun-16 Oct-16 Feb-17

%yoy

-10

-5

0

5

10

15

20

Feb-15 Jun-15 Oct-15 Feb-16 Jun-16 Oct-16 Feb-17

China, Sector Growth

Electricity Consumption Growth

Passenger Car Sales Growth

Sources: Bloomberg, INTL FCStone estimates

Rail Traffic Growth

%yoy

Real Estate Construction Growth

-15

-10

-5

0

5

10

15

20

Feb-15 Jun-15 Oct-15 Feb-16 Jun-16 Oct-16 Feb-17

%yoy

-2

0

2

4

6

8

10

Feb-15 Jun-15 Oct-15 Feb-16 Jun-16 Oct-16 Feb-17

%yoy

• Underlying Strength in Metals-

Using Sectors from Mid 2016,

• BUT Some Recent Softening

– Credit Tightening Slows

Construction

– Autos Hurt by Higher Taxes

China, IP and PMI

Industrial Production

Sources: Bloomberg, INTL FCStone estimates

PMI Index

%yoy

47

48

49

50

51

52

Feb-15 Jun-15 Oct-15 Feb-16 Jun-16 Oct-16 Feb-17

Govt

Caixin

5

5.5

6

6.5

7

7.5

8

Mar-15 Jul-15 Nov-15 Mar-16 Jul-16 Nov-16 Mar-17

• Mixed Signals in PMIs

• Official Caixin

– Domestic Demand Slows

– External Demand Firm

– Construction Slowing

• Govt Efforts to Rein in Credit

Growth (notably in Property)

• IP Steadies at 6.5% after

Early 2017 Surge

– Construction and Real

Estate Slow but Firm

– Investment Growth

Slows But Firm at 8%

– Private Investment Up

China, Some Inflation Concerns

Sources: Bloomberg, INTL FCStone estimates

New Residential Prices…

-8

-6

-4

-2

0

2

4

6

8

10

12

Jan/15 Jun/15 Nov/15 Apr/16 Sep/16 Feb/17

% yoy

0

0.5

1

1.5

2

2.5

3

Feb-15 Jun-15 Oct-15 Feb-16 Jun-16 Oct-16 Feb-17

CPI Core CPI

%yoy

Inflation Accelerates end ‘16

But Some Recent Tapering…

• Underpin by a Weaker

Commodity Prices and

Credit Tightening

China, Credit “Bubble”

0

50

100

150

200

250

300

2011 2012 2013 2014 2015 2016

% of GDP Corporate DebtHousehold DebtGovt Debt

190

195

200

205

210

215

220

Q115

Q215

Q315

Q415

Q116

Q216

Q316

Q416

Q117

% of GDP ,

Social

Financing

Moody’s Downgrades China

but still Investment Grade

• Concern:

– Debt Growth

– Government Stimulus

Officials Focused on

Financial Risks and

Maintaining Demand

• Focus: Slow Credit Growth

• Tighter Monetary Policy

– IR Up but Hold Steady

• Restrictions on Residential

Home Purchases

• Regulatory Crackdown on

Shadow Credit

• Regulators Slowing IPO

Approvals (Good and Bad)

22

23

23

24

24

25

25

26

26

27

27

May-15 Oct-15 Feb-16 Jun-16 Oct-16 Feb-17

Tau

sen

de trillion CNY

Shadow

Banking

Loans

8500

9000

9500

10000

10500

15000

17000

19000

21000

23000

25000

27000

May-15Oct-15 Feb-16 Jun-16 Oct-16 Feb-17

bn CNY bn CNY

Total Household Loans

Med & LongTerm(LHS)

ShortTerm(RHS)

Source: Bloomberg, INTL FCStone estimates

China, Summary

• Key Concern: High Debt (notably Private Debt) and Retain Growth

• Shift from Investment Growth to Consumer Economy & Structural Reforms

– SOE Debt Restructuring, Address Credit Risk/Property Bubble

– Investment to Consumer Econ; Clampdown on Pollution, Excess Cap

– Capital/Property Controls, Tighter Fiscal/Money Policies (Reign in Credit)

– Crackdown on Local Government Borrowing But Retain One Belt/One Road

• Growth Slowdown ‘15/16, Fiscal Stimulus Early ‘16, Firm End ‘16/Start ‘17,

– IR policy eased, credit growth boosts property sales,

– Strength in Construction & Fixed Investment (Power Grid, Railway)

– Business/Consumer Confidence Up, Imports Up, Corp Profits Up

• But Evidence of Recent Slowdown with Credit Tightening

– Auto Production/Sales Soft (with Tax Incentives cut)

– PMI mixed, IP slows, Construction Slows

• Overall: China Economy Growing at Steady Pace, Down from Late ’16/Early ‘17

• Pressure on RMB (But PBOC looks to hold Steady)

• Trump:: Softening/Delayed, Trump now working w China (Korea/own Problems)

-60

-40

-20

0

20

40

(15)

(10)

(5)

0

5

10

Feb/00 Jan/03 Nov/05 Sep/08 Jul/11 May/14 Apr/17

% yoy

(60)

(40)

(20)

0

20

40

60

Feb/00 Jan/03 Nov/05 Sep/08 Jul/11 May/14 Apr/17

% yoy

(25)

(20)

(15)

(10)

(5)

0

5

10

15

Jun/00 Feb/03 Oct/05 Jun/08 Feb/11 Oct/13 Jun/16

% yoy

48

50

52

54

56

58

60

62

Jul/14 Apr/15 Dec/15 Aug/16 Apr/17

Mfg Services

(4)

(3)

(2)

(1)

0

1

2

3

4

5

6

Jun/00 Feb/03 Oct/05 Jun/08 Feb/11 Oct/13 Jun/16

% yoy

United States Growth: Up

Housing

Starts

Vehicle Sales

PMI Index

Industrial Production

GDP

Gross Private

Fixed Investment

Sources: Bloomberg, INTL FCStone estimates

%yoy

Growth Trends Up

Economy is “Resilient”

But Mixed Signals:

• Unemployment Low,

AND Inflation low

Core Growth Good

• Payrolls, PMI, ISM,

Housing, Orders,

Consumers , Invest,

• Apr IP Up (weak Q1),

Weakness: Autos, Orders

Money Policy (IR Up)

(’17: 3x +1; ’18: 3x, ‘19: 3x

• Slow Purchases of

Treasury /Mortgage

Securities (no reinvest)

Trump Factor?

• Less Optimism Chng

• Infrastructure, Regs,

Trade,Tax Cuts, Health

• Political Headwinds

(40)

(30)

(20)

(10)

0

10

20

30

40

Feb/00 Jan/03 Nov/05 Sep/08 Jul/11 May/14 Apr/17

% yoy

-60

-40

-20

0

20

40

60

80

100

Feb/00 Dec/02 Oct/05 Aug/08 Jun/11 Apr/14 Feb/17

(15)

(10)

(5)

0

5

10

15

Jun/00 Feb/03 Oct/05 Jun/08 Feb/11 Oct/13 Jun/16

% yoy

47

48

49

50

51

52

53

54

Jul/14 Apr/15 Dec/15 Sep/16 May/17

Mfg Services

Japan Growth: Up

Although Debt/GDP

Ratio High & Private

Consumption Soft

• GDP Firms

Manufacturing

Sectors Improve

• PMI, Exports,

Autos, Labor,

IP, & Business,

Investment Up,

Inflation Low,

• & Biz/Consumer

Sentiment Up,

IR to Remain Low

• BoJ to Buy

Assets w No

Tightening til ‘18

Housing Starts

Vehicle Sales

PMI Index

Industrial

Production

GDP

Gross Private Fixed Investment

Sources: Bloomberg, INTL FCStone estimates

%yoy

(4)

(2)

0

2

4

6

Jun/00 Jun/03 Jun/06 Jun/09 Jun/12 Jun/15

% yoy

(20)

(15)

(10)

(5)

0

5

10

15

20

Feb/00 Jan/03 Nov/05 Sep/08 Jul/11 May/14 Apr/17

% yoy

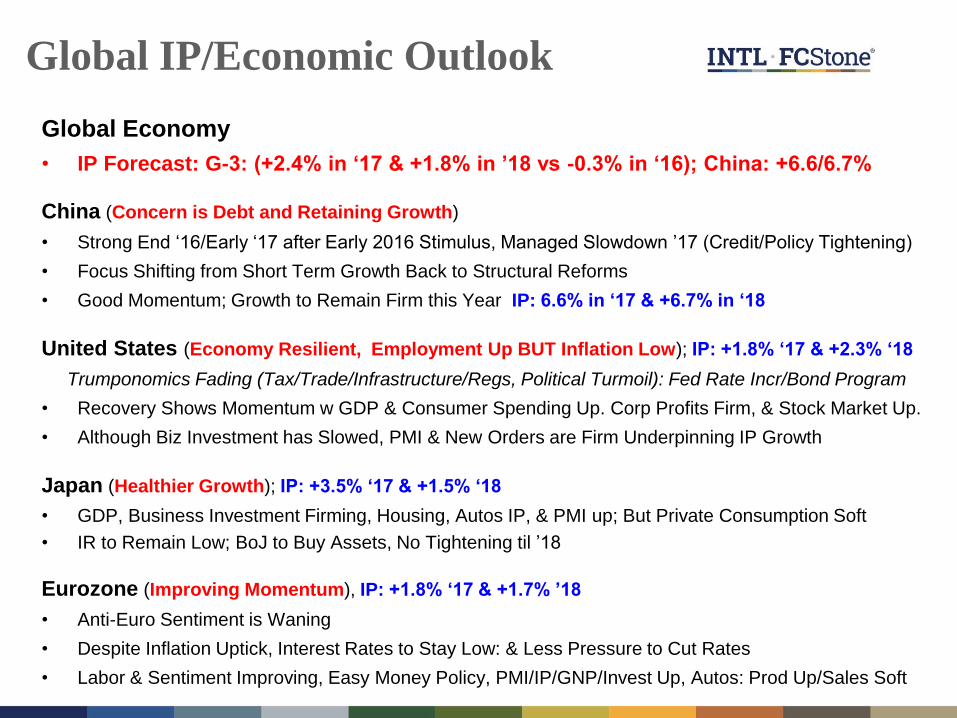

Global IP/Economic Outlook

Global Economy

• IP Forecast: G-3: (+2.4% in ‘17 & +1.8% in ’18 vs -0.3% in ‘16); China: +6.6/6.7%

China (Concern is Debt and Retaining Growth)

• Strong End ‘16/Early ‘17 after Early 2016 Stimulus, Managed Slowdown ’17 (Credit/Policy Tightening)

• Focus Shifting from Short Term Growth Back to Structural Reforms

• Good Momentum; Growth to Remain Firm this Year IP: 6.6% in ‘17 & +6.7% in ‘18

United States (Economy Resilient, Employment Up BUT Inflation Low); IP: +1.8% ‘17 & +2.3% ‘18

Trumponomics Fading (Tax/Trade/Infrastructure/Regs, Political Turmoil): Fed Rate Incr/Bond Program

• Recovery Shows Momentum w GDP & Consumer Spending Up. Corp Profits Firm, & Stock Market Up.

• Although Biz Investment has Slowed, PMI & New Orders are Firm Underpinning IP Growth

Japan (Healthier Growth); IP: +3.5% ‘17 & +1.5% ‘18

• GDP, Business Investment Firming, Housing, Autos IP, & PMI up; But Private Consumption Soft

• IR to Remain Low; BoJ to Buy Assets, No Tightening til ’18

Eurozone (Improving Momentum), IP: +1.8% ‘17 & +1.7% ’18

• Anti-Euro Sentiment is Waning

• Despite Inflation Uptick, Interest Rates to Stay Low: & Less Pressure to Cut Rates

• Labor & Sentiment Improving, Easy Money Policy, PMI/IP/GNP/Invest Up, Autos: Prod Up/Sales Soft

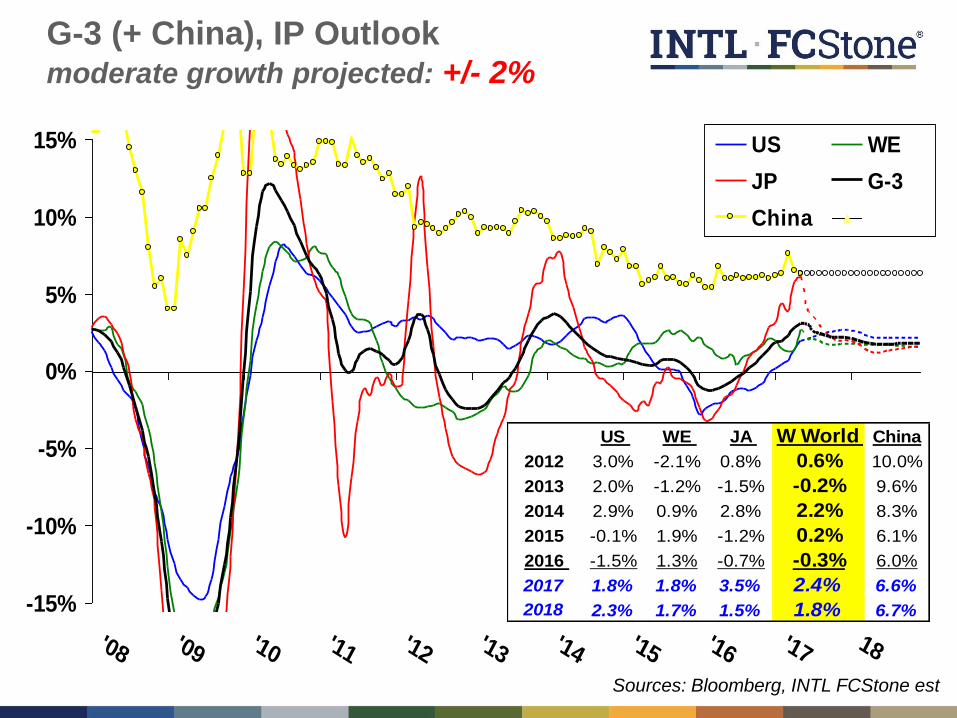

-15%

-10%

-5%

0%

5%

10%

15%

'08 '09 '10 '11 '12 '13 '14 '15 '16 '17 18

US WE

JP G-3

China

G-3 (+ China), IP Outlook moderate growth projected: +/- 2%

Sources: Bloomberg, INTL FCStone est

US WE JA W World China

2012 3.0% -2.1% 0.8% 0.6% 10.0%

2013 2.0% -1.2% -1.5% -0.2% 9.6%

2014 2.9% 0.9% 2.8% 2.2% 8.3%

2015 -0.1% 1.9% -1.2% 0.2% 6.1%

2016 -1.5% 1.3% -0.7% -0.3% 6.0%

2017 1.8% 1.8% 3.5% 2.4% 6.6%

2018 2.3% 1.7% 1.5% 1.8% 6.7%

This section of the page should be blank except when footnotes are present.

Role of Funds

Metals Volumes: Funds vs Trade excludes broker crosses

0

10

20

30

40

50

60

70

80

90

100

'90 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17

Funds

Trade/Other

“funds” account for 60+% of client volumes

Sources: BarclayHedge, Bloomberg, CFTC, LME, INTL FCStone estimates

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

$200

$220

$240

$260

'90 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

Macro

Hedge

1%

7%

11%

8%

8%

6%

2%

11%17%

9%

1%12%

3%

5%

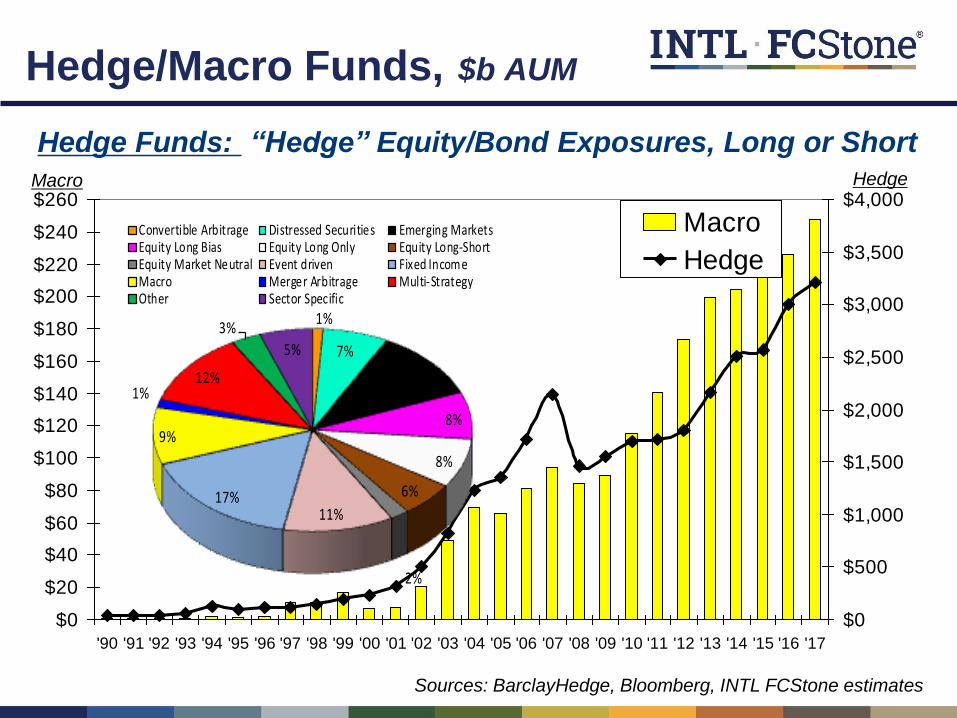

Convertible Arbitrage Distressed Securities Emerging MarketsEquity Long Bias Equity Long Only Equity Long-ShortEquity Market Neutral Event driven Fixed IncomeMacro Merger Arbitrage Multi-StrategyOther Sector Specific

Hedge/Macro Funds, $b AUM

Hedge Funds: “Hedge” Equity/Bond Exposures, Long or Short

Sources: BarclayHedge, Bloomberg, INTL FCStone estimates

Macro Hedge

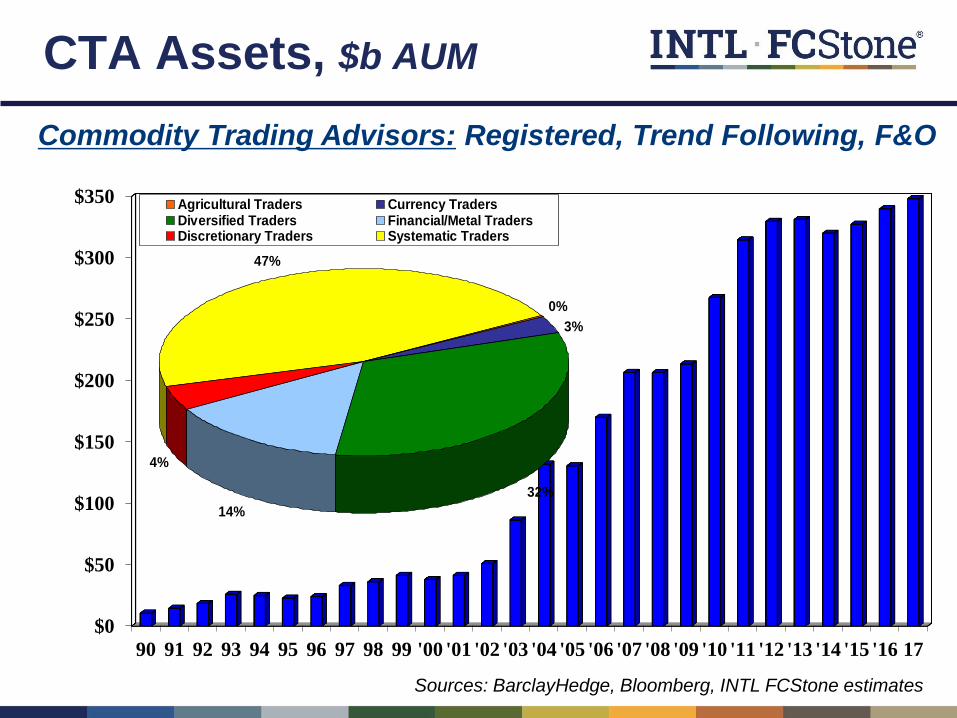

CTA Assets, $b AUM

$0

$50

$100

$150

$200

$250

$300

$350

90 91 92 93 94 95 96 97 98 99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 17

Commodity Trading Advisors: Registered, Trend Following, F&O

0%

32%

14%

4%

47%

3%

Agricultural Traders Currency TradersDiversified Traders Financial/Metal TradersDiscretionary Traders Systematic Traders

Sources: BarclayHedge, Bloomberg, INTL FCStone estimates

$0

$50

$100

$150

$200

$250

90 91 92 93 94 95 96 97 98 99 '00 '01'02'03'04 '05'06'07'08'09 '10'11'12'13'14 '15'16'17

Energy Agric PrecM IndusM

GSCI 70% 20% 4% 7%

DJ-UBS 33% 36% 13% 19%

Rodgers 46% 33% 7% 14%

Merrill Lynch 60% 25% 5% 10%

Average 52% 28% 7% wtd avg 12%

Copper Alum Zinc Nickel Lead

GSCI 48.2% 28.9% 7.2% 9.6% 6.0%

DJ-UBS 42.9% 29.0% 13.2% 14.9% 0.0%

Rodgers 28.6% 28.6% 14.3% 7.1% 14.3%

Merrill Lynch 52.6% 29.6% 8.4% 9.5% 0.0%

Average 43.1% 29.0% 10.8% 10.3% 5.1%

Index Funds, $b AUM

Index of Commodities, Commodity Super Cycle, Diversification

Sources: BarclayHedge, Bloomberg, INTL FCStone estimates

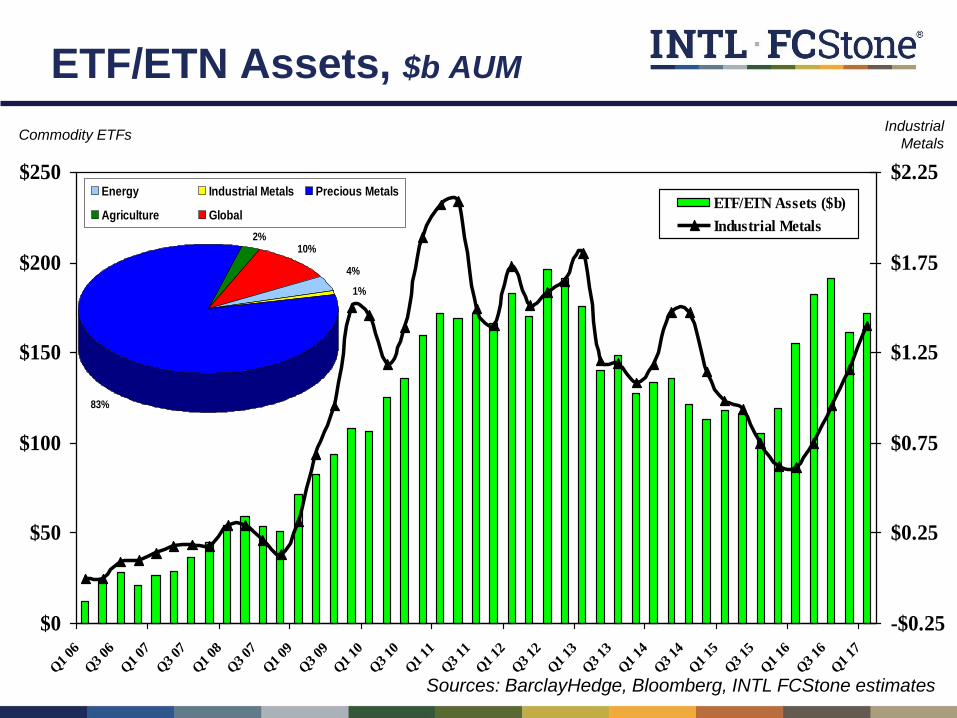

ETF/ETN Assets, $b AUM

$0

$50

$100

$150

$200

$250

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

07

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

Q1

12

Q3

12

Q1

13

Q3

13

Q1

14

Q3

14

Q1

15

Q3

15

Q1

16

Q3

16

Q1

17

-$0.25

$0.25

$0.75

$1.25

$1.75

$2.25

ETF/ETN Assets ($b)

Industrial Metals

4%

83%

2%10%

1%

Energy Industrial Metals Precious Metals

Agriculture Global

Industrial

Metals Commodity ETFs

Sources: BarclayHedge, Bloomberg, INTL FCStone estimates

Industrial Metals, Fund Alloc, $b

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17

Macro CTA

Index ETF/ETN

Sources: BarclayHedge, Bloomberg, CFTC, INTL FCStone estimates

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

'94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17

-18

-15

-12

-9

-6

-3

0

3

6

9

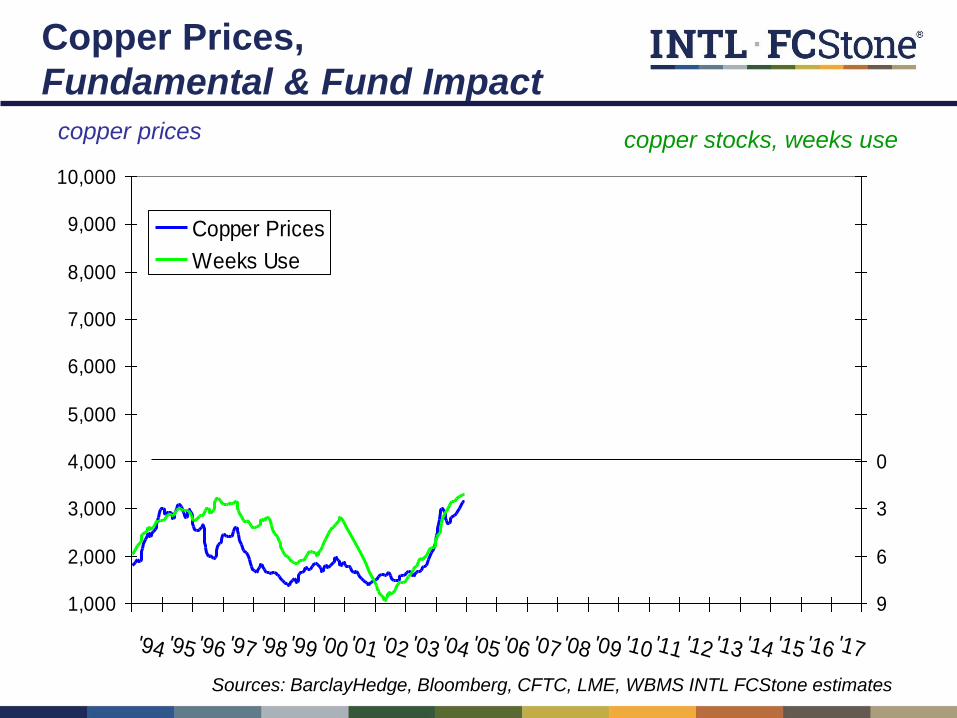

Copper Prices

Weeks Use

copper prices copper stocks, weeks use

Copper Prices,

Fundamental & Fund Impact

Sources: BarclayHedge, Bloomberg, CFTC, LME, WBMS INTL FCStone estimates

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

'94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17

-18

-15

-12

-9

-6

-3

0

3

6

9

Copper Prices

Weeks Use

copper prices copper stocks, weeks use

Copper Prices,

Fundamental & Fund Impact

Sources: BarclayHedge, Bloomberg, CFTC, LME, WBMS INTL FCStone estimates

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

'94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17

-18

-15

-12

-9

-6

-3

0

3

6

9

Copper Prices

Funds $ Index

Weeks Use

copper prices, fund index ($AUM, metals) copper stocks, weeks use

Copper Prices,

Fundamental & Fund Impact

Sources: BarclayHedge, Bloomberg, CFTC, LME, WBMS INTL FCStone estimates

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

'94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17

-18

-15

-12

-9

-6

-3

0

3

6

9

Copper Prices

Funds $ Index

Weeks Use

copper prices, fund index ($AUM, metals) copper stocks, weeks use

Sources: BarclayHedge, Bloomberg, CFTC, LME, WBMS INTL FCStone estimates

Copper Prices,

Fundamental & Fund Impact

Funds, AUM Trends $b

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

Jan-06 Jan-08 Jan-10 Jan-12 Jan-14 Jan-16

Hedge Funds

$100

$150

$200

$250

$300

$350

$400

Jan-06 Jan-08 Jan-10 Jan-12 Jan-14 Jan-16

CTA

$50

$100

$150

$200

$250

$300

Jan-06 Jan-08 Jan-10 Jan-12 Jan-14 Jan-16

Macro

$50

$100

$150

$200

$250

$300

Jan-06 Jan-08 Jan-10 Jan-12 Jan-14 Jan-16

Index Funds

Sources: BarclayHedge, Bloomberg, CFTC, INTL FCStone estimates

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

Aug-14 Oct-14 Jan-15 Mar-15 Jun-15 Sep-15 Nov-15 Feb-16 Apr-16 Jul-16 Oct-16 Dec-16 Mar-17 Jun-17

Ag

gre

ga

te L

ots

Money Managers' Aggregate Positions Net Shorts Longs

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

Jan-17 Feb-17 Mar-17 Mar-17 May-17 Jun-17

Ag

gre

ga

te L

ots

Money Managers' Aggregate Positions Past Year Net Shorts Longs

LME Commitment of Traders Money Managers

Source: LME

60

70

80

90

100

110

120

-600,000

-400,000

-200,000

0

200,000

400,000

August-14 April-15 December-15 August-16 April-17

Ind

ex

Net

Po

sit

ion

s

LME Non-Ferrous CoT

Brokers Money Managers Producer/Merchant/Processor Index

LME Commitment of Traders

Source: LME

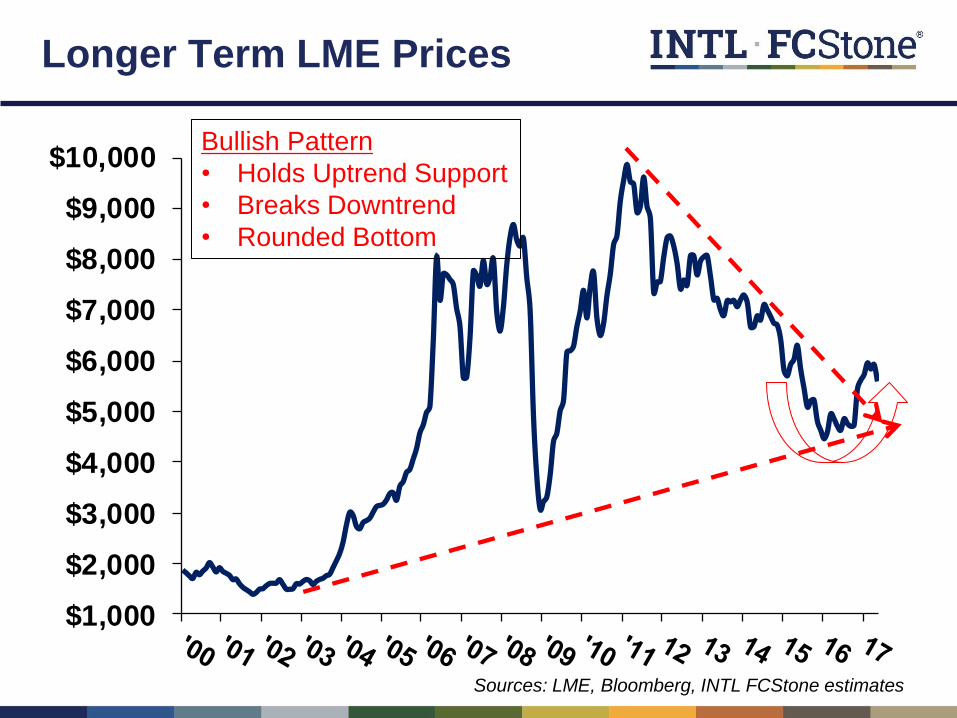

Longer Term LME Prices

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

$10,000

Sources: LME, Bloomberg, INTL FCStone estimates

Bullish Pattern

• Holds Uptrend Support

• Breaks Downtrend

• Rounded Bottom

This section of the page should be blank except when footnotes are present.

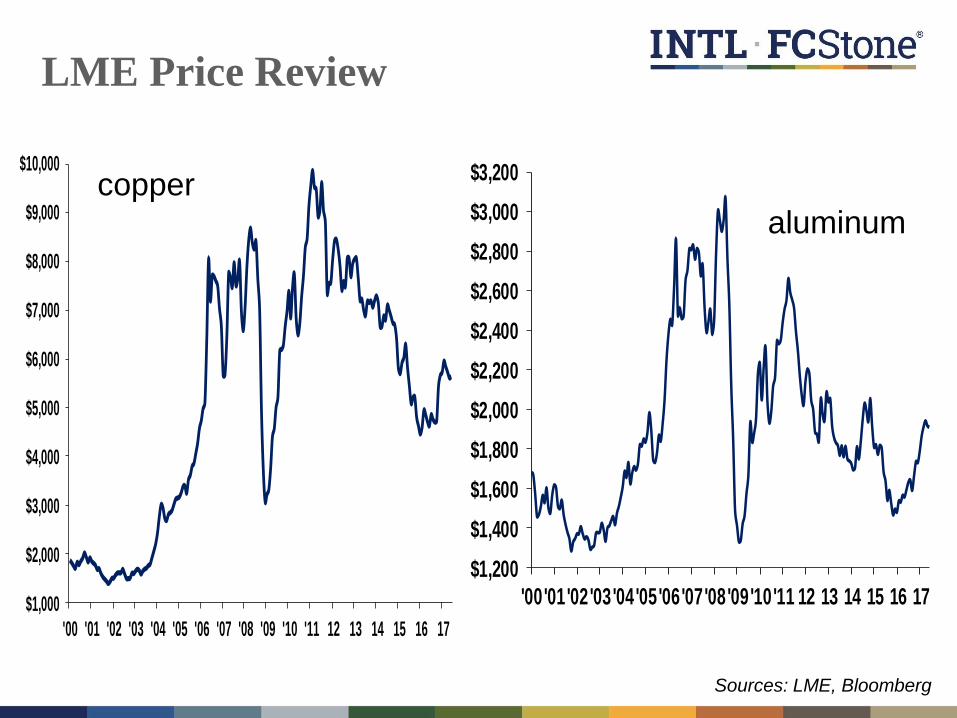

Metals Outlook

LME Price Review

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

$10,000

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 12 13 14 15 16 17

copper

aluminum

Sources: LME, Bloomberg

$1,200

$1,400

$1,600

$1,800

$2,000

$2,200

$2,400

$2,600

$2,800

$3,000

$3,200

'00'01'02'03'04'05'06'07'08'09'10'11 12 13 14 15 16 17

LME Price Review

zinc

tin

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

$45,000

$50,000

$55,000

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17

$3,000

$8,000

$13,000

$18,000

$23,000

$28,000

$33,000

$38,000

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17

nickel

lead

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

'00'01

'02'03

'04'05

'06'07

'08'09

'10'11

'12'13

'14'15

'16'17

Sources: LME, Bloomberg

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

LME Price Review, Copper

Sources: LME, Bloomberg

LME Price Review, Aluminum

Sources: LME, Bloomberg

LME Price Review, Zinc

Sources: LME, Bloomberg

LME Price Review, Lead

Sources: LME, Bloomberg

LME Price Review, Nickel

Sources: LME, Bloomberg

LME Price Review, Tin

Sources: LME, Bloomberg

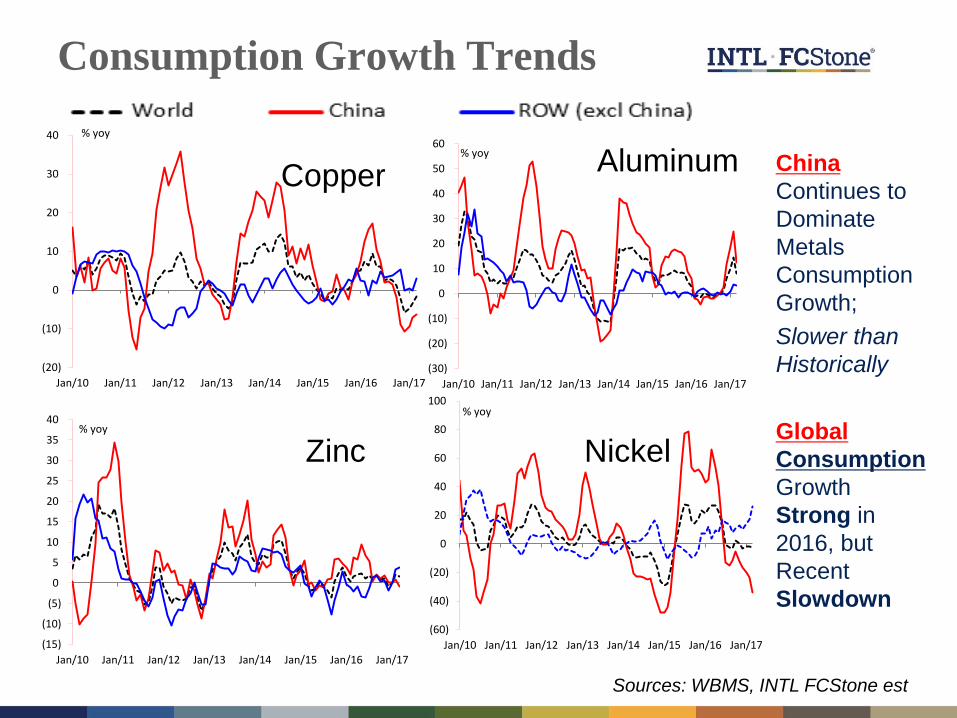

Consumption Growth Trends

Aluminum

Nickel Zinc

Copper China

Continues to

Dominate

Metals

Consumption

Growth;

Slower than

Historically

Global

Consumption

Growth

Strong in

2016, but

Recent

Slowdown

Sources: WBMS, INTL FCStone est

(20)

(10)

0

10

20

30

40

Jan/10 Jan/11 Jan/12 Jan/13 Jan/14 Jan/15 Jan/16 Jan/17

% yoy

(30)

(20)

(10)

0

10

20

30

40

50

60

Jan/10 Jan/11 Jan/12 Jan/13 Jan/14 Jan/15 Jan/16 Jan/17

% yoy

(15)

(10)

(5)

0

5

10

15

20

25

30

35

40

Jan/10 Jan/11 Jan/12 Jan/13 Jan/14 Jan/15 Jan/16 Jan/17

% yoy

(60)

(40)

(20)

0

20

40

60

80

100

Jan/10 Jan/11 Jan/12 Jan/13 Jan/14 Jan/15 Jan/16 Jan/17

% yoy

Mine and Refined Production

Aluminum

Nickel

Zinc

Copper

Copper

Production

Curtailed By

Mine Strikes

/Other but New

& Expanded

Capacity

Aluminum

Grows with

China (but Govt

Mandated Cuts

Soon?)

Zinc: significant

cuts in 2016

(Glencore)?

Nickel:

significant cuts

in 2015/16; Indo

and Phil supply?

Sources: WBMS, INTL FCStone est

China’s Net Metal Trade Reduced: Exports – Imports

-400,000-350,000-300,000-250,000-200,000-150,000-100,000

-50,0000

50,000100,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Tons Aluminum

-120,000-90,000-60,000-30,000

030,00060,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Tons Zinc

-50,000

-25,000

0

25,000

50,000

75,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Tons Lead

-50,000

-40,000

-30,000

-20,000

-10,000

0

20062007200820092010201120122013201420152016

Tons

Nickel

-3,000-2,000-1,000

01,0002,0003,000

20062007200820092010201120122013201420152016

Tin

-400,000

-350,000

-300,000

-250,000

-200,000

-150,000

-100,000

-50,000

0

50,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Copper

Sources: WBMS, INTL FCStone est

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

$10,000

80' 82' 84' 86' 88' 90' 92' 94' 96' 98' 00' 02' 04' 06' 08' 10' 12' 14' 16'

Copper Prices vs 70th %-tile Cost

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

Copper Cost Curves

2016 2015 2014 2013

2012 2011 2010

Sources: LME, WBMS, INTL FCStone est

500

1000

1500

2000

2500

3000

3500

4000

80' 82' 84' 86' 88' 90' 92' 94' 96' 98' 00' 02' 04' 06' 08' 10' 12' 14' 16'

LME Aluminum Prices vs 70th Percentile Costs

Aluminum Monthly Avg Price Al Costs (70th percentile)

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

Aluminum Cost Curve

2016 2015 2014 2013

2012 2011 2010 2009

Sources: LME, WBMS, INTL FCStone est

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

80' 82' 84' 86' 88' 90' 92' 94' 96' 98' 00' 02' 04' 06' 08' 10' 12' 14' 16'

LME Nickel Prices vs 70th Percentile Cost

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

Nickel Cost Curve

2016 2015 2014 20132012 2011 2010 2009

Sources: LME, WBMS, INTL FCStone est

-

500.00

1,000.00

1,500.00

2,000.00

2,500.00

3,000.00

3,500.00

4,000.00

4,500.00

5,000.00

80' 82' 84' 86' 88' 90' 92' 94' 96' 98' 00' 02' 04' 06' 08' 10' 12' 14' 16'

LME Zinc Prices vs 70th Percentile Costs

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

Zinc Cost Curve

2016 2015 2014 2013

2012 2011 2010 2009

Sources: LME, WBMS, INTL FCStone est

0

1,000

2,000

3,000

4,000

5,000

6,000LME

Comex

IPAI

Shang

Inventory Trends

alum

-

200

400

600

800

1,000

1,200

1,400 Producer Consumer

LME Mrchnt

SHFE

zinc

0

50

100

150

200

250

300

350

400

450

500

LME

Prod

Cons

Shang

0

100

200

300

400

500

600

700

05 06 07 08 09 10 11 12 13 14 15 16 17

Producer

Consumer

Comex

LME

SHFE

nickel

copper

Sources: LME, WBMS, INTL FCStone est

0

50

100

150

200

250

300

350

400

15 16 17 18

Comex LME SHFE

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Inventory Trends

alum

-

100

200

300

400

500

600

zinc

0

50

100

150

200

250

300

350

400

450

500

nickel

copper

Sources: LME, WBMS, INTL FCStone est

Copper, Supply-Demand Balance, k tonnes

Supply:

• New Mine Builds in ’15/‘16

to Slow w Little in Pipeline

• Recent Mine Strikes/Losses

More Labor Contracts this Yr

• Shuttered Capacity

• High Prices: High Scrap

Demand

• Hope for China demand

• Questions on Trump Investing

• Europe Steady

• Fund Index Buying

Stocks/Premiums

• Stocks Up (notably China)

• Premiums Low

Forecast: deficit deficit

• Reuters: ‘17: -17k, ‘18: -72k

Sources: LME, WBMS, INTL FCStone est

2013 2014 2015 2016 Jan-Mar'17 2017f 2018f

Total Consumption 21,154 22,702 22,830 23,331 5,614 23,914 24,632

4.3% 7.3% 0.6% 2.2% 2.5% 3.0%

China 9,830 11,303 11,353 11,642 2,671

10.5% 15.0% 0.4% 2.5%

World less China 11,324 11,399 11,477 11,689 2,943

-0.5% 0.7% 0.7% 1.9%

Total Mine Prod 18,188 18,548 19,325 20,719 4,966 21,755 22,843

7.2% 2.0% 4.2% 7.2% 5.0% 5.0%

Total Refined Prod* 20,975 22,426 22,968 23,527 5,762 24,116 24,598

3.0% 6.9% 2.4% 2.4% 2.5% 2.0%

China Refined 6,667 7,649 7,964 8,436 2,133

13.4% 14.7% 4.1% 5.9%

World less China 14,308 14,777 15,004 15,091 3,629

-1.2% 3.3% 1.5% 0.6%

Apparent Balance -180 -276 138 196 148 201 -34

Reported Balance -145 -148 157 59 191 201 -34

Unreported Balance -35 -129 -19 137 -43 0 0

Producers 284 316 299 295 308

Merchants 14 17 16 18 19

Consumers 111 127 128 137 128

Exchange 230 308 483 538 721

Total Stocks** 916 768 926 985 1,176 1,186 1,152

Weeks Use 2.3 1.8 2.1 2.2 2.7 2.6 2.4

Copper Supply/Demand Annual Balances (k tonnes)

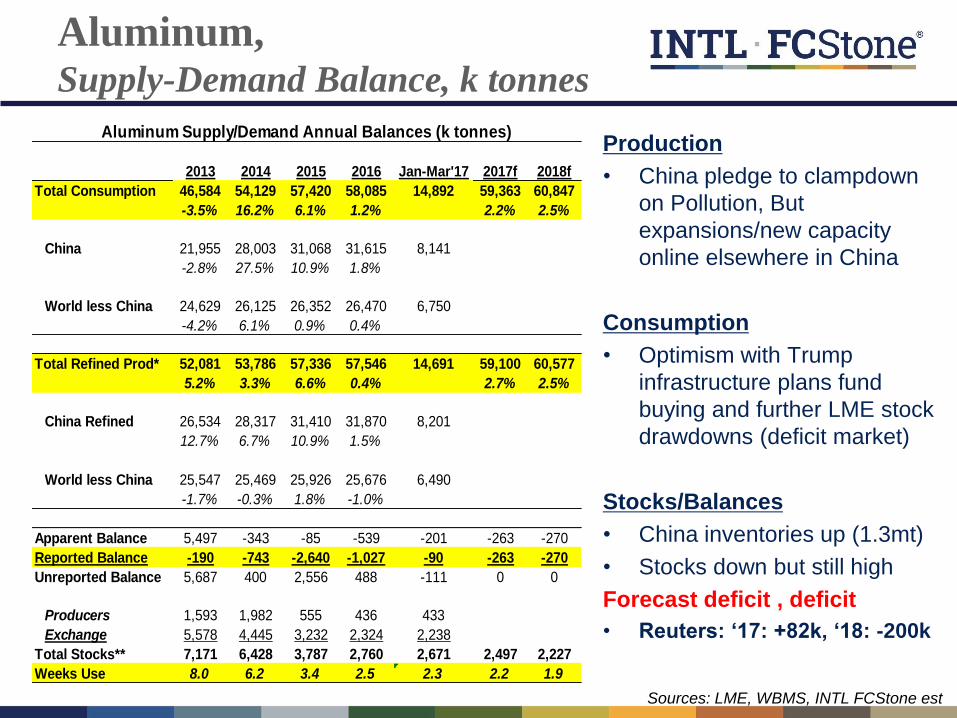

Aluminum, Supply-Demand Balance, k tonnes

Production

• China pledge to clampdown

on Pollution, But

expansions/new capacity

online elsewhere in China

Consumption

• Optimism with Trump

infrastructure plans fund

buying and further LME stock

drawdowns (deficit market)

Stocks/Balances

• China inventories up (1.3mt)

• Stocks down but still high

Forecast deficit , deficit

• Reuters: ‘17: +82k, ‘18: -200k

Sources: LME, WBMS, INTL FCStone est

2013 2014 2015 2016 Jan-Mar'17 2017f 2018f

Total Consumption 46,584 54,129 57,420 58,085 14,892 59,363 60,847

-3.5% 16.2% 6.1% 1.2% 2.2% 2.5%

China 21,955 28,003 31,068 31,615 8,141

-2.8% 27.5% 10.9% 1.8%

World less China 24,629 26,125 26,352 26,470 6,750

-4.2% 6.1% 0.9% 0.4%

Total Refined Prod* 52,081 53,786 57,336 57,546 14,691 59,100 60,577

5.2% 3.3% 6.6% 0.4% 2.7% 2.5%

China Refined 26,534 28,317 31,410 31,870 8,201

12.7% 6.7% 10.9% 1.5%

World less China 25,547 25,469 25,926 25,676 6,490

-1.7% -0.3% 1.8% -1.0%

Apparent Balance 5,497 -343 -85 -539 -201 -263 -270

Reported Balance -190 -743 -2,640 -1,027 -90 -263 -270

Unreported Balance 5,687 400 2,556 488 -111 0 0

Producers 1,593 1,982 555 436 433

Exchange 5,578 4,445 3,232 2,324 2,238

Total Stocks** 7,171 6,428 3,787 2,760 2,671 2,497 2,227

Weeks Use 8.0 6.2 3.4 2.5 2.3 2.2 1.9

Aluminum Supply/Demand Annual Balances (k tonnes)

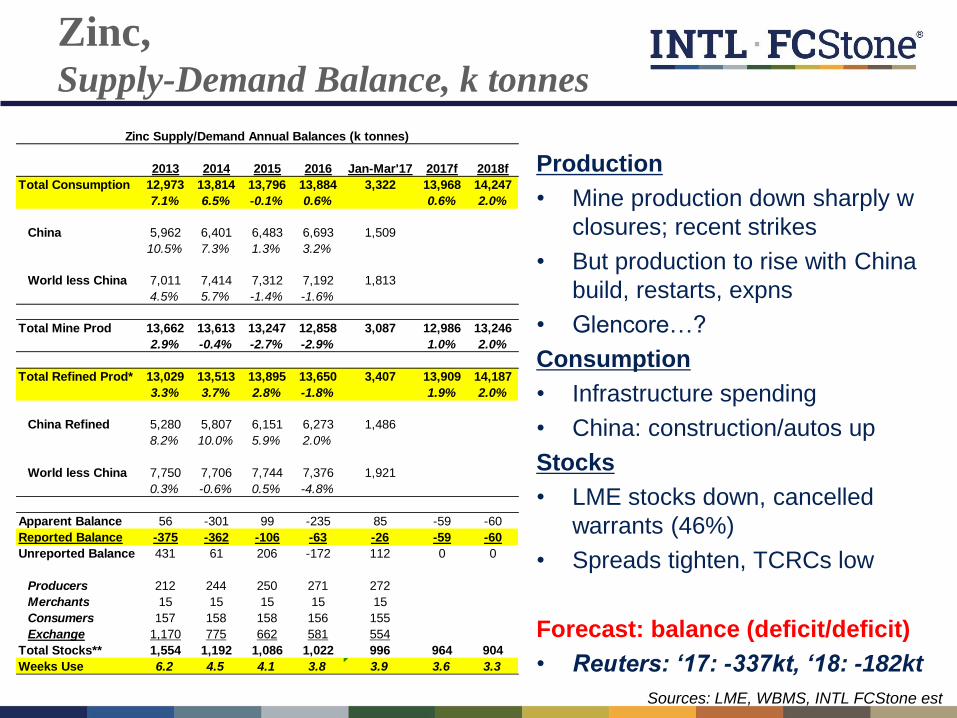

Zinc, Supply-Demand Balance, k tonnes

Production

• Mine production down sharply w

closures; recent strikes

• But production to rise with China

build, restarts, expns

• Glencore…?

Consumption

• Infrastructure spending

• China: construction/autos up

Stocks

• LME stocks down, cancelled

warrants (46%)

• Spreads tighten, TCRCs low

Forecast: balance (deficit/deficit)

• Reuters: ‘17: -337kt, ‘18: -182kt

Sources: LME, WBMS, INTL FCStone est

2013 2014 2015 2016 Jan-Mar'17 2017f 2018f

Total Consumption 12,973 13,814 13,796 13,884 3,322 13,968 14,247

7.1% 6.5% -0.1% 0.6% 0.6% 2.0%

China 5,962 6,401 6,483 6,693 1,509

10.5% 7.3% 1.3% 3.2%

World less China 7,011 7,414 7,312 7,192 1,813

4.5% 5.7% -1.4% -1.6%

Total Mine Prod 13,662 13,613 13,247 12,858 3,087 12,986 13,246

2.9% -0.4% -2.7% -2.9% 1.0% 2.0%

Total Refined Prod* 13,029 13,513 13,895 13,650 3,407 13,909 14,187

3.3% 3.7% 2.8% -1.8% 1.9% 2.0%

China Refined 5,280 5,807 6,151 6,273 1,486

8.2% 10.0% 5.9% 2.0%

World less China 7,750 7,706 7,744 7,376 1,921

0.3% -0.6% 0.5% -4.8%

Apparent Balance 56 -301 99 -235 85 -59 -60

Reported Balance -375 -362 -106 -63 -26 -59 -60

Unreported Balance 431 61 206 -172 112 0 0

Producers 212 244 250 271 272

Merchants 15 15 15 15 15

Consumers 157 158 158 156 155

Exchange 1,170 775 662 581 554

Total Stocks** 1,554 1,192 1,086 1,022 996 964 904

Weeks Use 6.2 4.5 4.1 3.8 3.9 3.6 3.3

Zinc Supply/Demand Annual Balances (k tonnes)

Nickel, Lead Supply-Demand Balance, k tonnes

Nickel Lead

Sources: LME, WBMS, INTL FCStone est

2013 2014 2015 2016 Q1'17 2017f 2018f

Total Consumption 11,304 10,919 10,199 11,291 3,069 11,404 11,632

8.3% -3.4% -6.6% 10.7% 1.0% 2.0%

China 4,927 4,682 3,804 4,655 1,306

6.7% -5.0% -18.8% 22.4%

World less China 6,377 6,237 6,396 6,636 1,763

9.7% -2.2% 2.5% 3.8%

Total Mine Prod 5,294 5,269 4,999 4,710 1,365 4,710 4,757

4.0% -0.5% -5.1% -5.8% 0.0% 1.0%

Total Refined Prod* 11,312 10,932 10,182 11,119 2,965 11,342 11,569

6.5% -3.4% -6.9% 9.2% 2.0% 2.0%

China Refined 4,935 4,704 3,845 4,665 1,281

7.5% -4.7% -18.3% 21.3%

World less China 6,377 6,227 6,337 6,454 1,684

5.8% -2.3% 1.8% 1.8%

Apparent Balance 8 12 -17 -172 -104 -62 -64

Reported Balance -41 -22 -100 15 20 -62 -64

Unreported Balance 49 35 83 -187 -124 0 0

Producers 140 135 118 113 101

Consumers 139 138 137 138 138

Exchange 304 286 205 224 256

Total Stocks** 582 560 460 475 495 413 349

Weeks Use 2.7 2.7 2.4 2.2 2.1 1.9 1.6

Lead Supply/Demand Annual Balances (k tonnes)

2013 2014 2015 2016 Q1'17 2017f 2018f

Total Consumption 1,801 1,587 1,741 1,867 388 1,901 1,939

3.8% -11.9% 9.7% 7.2% 1.8% 2.0%

China 909 654 836 873 137

13.0% -28.1% 27.8% 4.4%

World less China 892 933 905 994 251

-4.1% 4.7% -3.0% 9.8%

Total Mine Prod 2,539 2,063 2,125 1,981 417 2,001 2,041

12.0% -18.7% 3.0% -6.8% 1.0% 2.0%

Total Refined Prod* 1,979 1,831 1,830 1,805 392 1,823 1,869

6.2% -7.4% -0.1% -1.4% 1.0% 2.5%

China Refined 711 537 446 412 61

20.3% -24.4% -16.9% -7.7%

World less China 1,268 1,294 1,384 1,393 331

-0.3% 2.1% 6.9% 0.7%

Apparent Balance 178 244 89 -62 4 -77 -70

Reported Balance 123 161 66 -20 -5 -77 -70

Unreported Balance 54 83 23 -41 9 0 0

Producers

Merchants/Cons 24 31 25 25 26

Exchange 262 415 487 466 460

Total Stocks** 285 446 511 491 486 414 344

Weeks Use 8.3 14.6 15.3 13.7 16.3 11.4 9.3

Nickel Supply/Demand Annual Balances (k tonnes)

Metals Outlook

• Prices recover in late 2016/early 2017 after 5 year bear market

• Global economy (IP) expected to grow slowly (no recession, no boom)

– Labor markets improving, low inflation, monetary/fiscal policy favorable

– China expansion continues but slows from early this year

– US economy growing, Trump infrastructure delayed, some Fed tightening

– Europe holds steady to higher; reduced political uncertainties

• Prices slip below production costs in 2016, forcing cutbacks

– Unplanned production losses offset reduced cap builds, China cuts?

• Inventories starting to decline

– Market shifts into deficit with mine cutbacks and economic recovery

• Fund investment high, albeit down from prior years, but growing

• Prices expected to hold steady to modestly recover over next 2 yrs

– Downside limited with prices below mine cash costs

– Upside capped w still surplus stocks and only modest economic growth

– Supply-demand fundamentals to play important role in base metal prices

Analysts Price Forecasts

Source: Consensus Economics

Current Sep-17 Dec-17 Mar-18 Jun-18 Sep-18 Dec-18 Mar-19

CP $5,640 $5,817 $5,746 $5,794 $5,816 $5,841 $5,857 $5,946

AL $1,865 $1,833 $1,881 $1,861 $1,850 $1,843 $1,853 $1,857

ZN $2,500 $2,804 $2,782 $2,779 $2,762 $2,731 $2,694 $2,609

PB $2,080 $2,203 $2,175 $2,148 $2,116 $2,098 $2,076 $2,099

NI $8,830 $10,475 $10,655 $10,975 $11,088 $11,295 $11,281 $12,067

SN $19,500 $20,219 $20,309 $20,232 $20,419 $20,306 $20,414 $20,520