issue 14 - inside telecommunications · 6. “airtel africa innovates with mobileum on telco big...

TRANSCRIPT

Inside Telecommunications

Prashant Singhal Global Telecommunications Leader

Greater customer insights, greater network agilityWelcome to the 14th edition of Inside Telecommunications. Our quarterly publication draws on EY’s deep industry expertise to provide unparalleled market intelligence on the critical issues impacting operators around the world.

This issue considers a number of industry themes, from telco big data services and network virtualization initiatives to the latest efforts to combat online piracy and antitrust reviews of in-market mobile mergers. Big data is one of the most important themes in the industry today, with carriers in both developed and emerging markets leveraging a new wave of insights to improve the customer experience, develop new revenue streams and improve organizational agility. Many players are already working more closely with public sector to explore new use cases, and relationships with vendors will play a vital role in supporting operator strategies in the future.

M&A activity in the sector remains pronounced, with in-market deals and moves into adjacent markets featuring prominently in the year-to-date. While many industry executives fear that the regulatory environment will undermine mobile consolidation scenarios, recent merger reviews in Europe point to changing attitudes. In addition, converged capabilities in telecommunications and media are becoming mission-critical as established operators look to boost scale and reduce churn levels. All told, M&A activity is evolving in a number of different directions, marking an exciting phase of the industry’s evolution.

Against this backdrop, we hope you nd this material useful. lease do not hesitate to share your feedback with me or any of my colleagues at EY.

Issue 14

Contents

Service innovation 4

Unlocking new opportunities in big data 4

Operators consider implications of a shifting m O landscape 6

Regulation 14

Industry stakeholders seek new routes to combat online piracy 14

All eyes on European antitrust merger remedies 16

Mergers and Acquisitions 18

Introduction 18

Operators target pay-TV gains 19

Western operators step up adjacent market exposure 20

Footprint growth in focus in Asia and Africa 22

Technology 10

Rewriting the network paradigm with NFV 10

Over 300 LTE networks commercially launched worldwide 12

3Issue 14 |

Meanwhile, many operators are building scale and capabilities in the residential bundle market, with transactions in Europe and the Americas underlining the need for new customer touch points in pay-TV. Yet the battle for the home is extending beyond traditional bundle packages, with smart home solutions now the scene of many converging ambitions. In August, outh

orea’s amsung acquired martThings, following other technology giants into a rapidly evolving segment.

Operators are also moving into adjacent markets in greater numbers, with incubator initiatives opening up new forms of market entry as carriers carve out new roles as supporters of innovative start-ups. Notable recent moves include Deutsche Telekom and Orange’s plans to collaborate over their respective accelerator programs and the hilippines Long Distance Telephone

ompany’s LDT strategic tie-up with Germany’s Rocket Internet with online and mobile payment solutions in mind.

Organizational overhauls are also supporting operator ambitions in the information and communications technology I T landscape. In May, Norway’s Telenor announced a new Group

trategy and Digital Unit in order to boost its responsiveness to customer needs. Earlier this year, Telefonica introduced the role of chief commercial digital of cer in order to spur revenue growth while streamlining its digital unit into a new Global Corporate Center.

Leaner operating models and new leadership roles designed to spearhead digital growth are becoming ever more important for telcos, particularly those with large footprints incorporating markets at different stages of maturity. However, operators’ core businesses face plenty of challenges, particularly on the mobile side.

Foreword

Adrian BaschnongaLead AnalystGlobal Telecommunications [email protected]

number of industry domains. Antitrust remedies to mobile mergers have been in focus, and the European Commission’s green light to consolidation moves in Germany and Ireland could pave the way for in-market mergers elsewhere, with encouragement of mobile virtual network operators (MVNOs) as a measure to support competition levels.

1. “The Communications Market 2014,” Ofcom, August 2014.

Figure 1: Average LTE network speeds by country in 2014

ource “The state of LTE February 2014,” Open ignal.

Download speed Mbps

5

3025201510

0

Aus

tral

iaIta

lyBr

azil

Hon

g Ko

ngDe

nmar

kCa

nada

Swed

enSo

uth

Kore

aU

KFr

ance

Germ

any

Mex

ico

Russ

iaJa

pan

US

Phili

ppin

es

With more than 300 LTE networks now commercially available worldwide, 4G has fast become a mainstay of the mobile industry. While much is made of the high speeds available, performance varies signi cantly. One study released earlier this year showed that those countries with the poorest network speeds could muster only one-fourth of the data throughput rates observable in the highest-performing markets.

As operators look to boost speeds further via LTE-A deployments and the industry at large invests in 5G R&D, it is clear that operators will have to ensure that busier networks do not lead to deteriorating performance. According to OpenSignal, average speeds in the US the rst country to launch LTE have fallen despite infrastructure improvements.

Looking beyond mobile data performance, voice connectivity also remains a challenge one study has showed that one in ve UK mobile users experience dropped calls at least once a week.1 In this light, current voice over LTE VoLTE initiatives will have an important role to play in improving the customer experience. As operators look to tap into new demand scenarios in ICT, they must not lose sight of their core competencies.

4 | Inside Telecommunications

Unlocking new opportunities in big dataBig data is becoming an ever more dominant theme across all industry verticals, as businesses look to improve their organizational agility, generate new forms of customer insight, improve front- and back-end processes, and develop new revenue streams. Global spending on big data technologies and services is expected to grow 30% in 2014, surpassing US 14 billion as demand for big data analytics skills outstrips supply.2

Operators have many advantages compared to other industries when it comes to repurposing data to improve decision-making and create new demand scenarios. A wealth of product, customer and asset data lies at their disposal, while their legacy retail and distribution capabilities also provide a range of customer touch points. This promising position is borne out in average big data spending levels among operators, which outperform those of other sectors.

1.Service innovation

The historic need to extract insights from call data records CDRs means that telcos have long had greater access to big data insights compared to other industries. Even so, and despite relatively high levels of spend among telcos, the travel and nancial services sectors are often perceived to have innovated more quickly when repurposing customer information to develop new offers, for example.

Figure 2: Company spending on big data by industry

Source “Big Data Investment Which industries should be investing more in Big Data ” Tata Consultancy Services, 2012.

Median spending per company by industry in 2012 US m

2. “IDC Predicts 2014 Will Be A Year of Escalation, Consolidation, and Innovation as the Transition to IT’s 3rd Platform’ Accelerates,” IDC, 3 December 2013.

0 10 20 30

Energy and resources

Life sciences

Retail

Manufacturing

Insurance

Utilities

High tech

Banking nancial services

Travel hospitality airlines

Telecommunications

5Issue 14 |

Many operators are already bene ting from a growing focus on big data and analytics, particularly when it comes to the customer experience. US-based AT&T has revealed that it collects 30 billion data points per hour in order to measure network quality that is in turn used to improve the customer experience. Using a tower-outage analyzer, the carrier can build an accurate picture of customers affected by network faults and can prioritize and escalate repairs based on this information.3

A number of factors are setting the stage for greater proliferation of analytics tools. Data storage costs are falling, and the use of open-source tools, such as Hadoop, is compounding a healthier cost pro le for analytics solutions. Meanwhile, the range of use cases is widening big data can be repurposed in several ways, from improving network capacity planning and churn prediction to developing new services for third parties based on aggregated and anonymized customer data.

Meanwhile, Vodafone Netherlands has leveraged SAP In niteInsight, a predictive analytics solution, as part of its anti-churn measures. Instead of manual churn modeling, the operator has used the software to build more than 700 predictive models for churn reduction and cross-selling. This has generated a deeper understanding of customers’ activities for example, ascertaining seasonal roaming behaviors in order to build targeted marketing campaigns.4

Emerging market operators are also keen to improve customer engagement. In February, big data specialist Flytxt announced an agreement to provide its real-time decision-making solution to Africa’s MTN Group.5 In the same month, Bharti Airtel announced that it had begun an analytics project in conjunction with Mobileum to gain a deeper understanding of the travel intentions, travel patterns and service usage habits of Airtel Africa’s customers in order to create tailored offers.6

Carriers are now working more closely with the public sector and industry verticals to explore how mobile data can support new digital services. In May, Telefonica released the ndings of a big data project exploring the effect of foreign tourism on the quality of life for Spanish residents. Using anonymized mobile phone data generated by foreign handsets and electronic payments data handled by BBVA bank’s terminal network, the project analyzed the impact of foreign visitors in Madrid and Barcelona in order to help manage congestion and ensure better interactions with local businesses.7 In the same month, the Spanish incumbent won a smart city platform tender from the Valencia City Council, with the aim of centralizing all municipal information using the European

3. “AT&T Uses Big Data to Improve Customer Experience,” Wall Street Journal, 3 June 2014.

4. “Predictive Analytics Helps Vodafone Ring Up Sales,” Baseline, 3 June 2014. 5. “MTN Group Selects Flytxt Platform for Real-Time Decisioning,” Flytxt, 25 February 2014. 6. “Airtel Africa innovates with Mobileum on Telco Big Data Analytics,” PRNewsire, 24 February 2014. 7. “Big Data and Tourism New Indicators for Tourism Management,” Telefonica and RocaSalvatella, May 2014.

Figure 3: Sample big data use cases for operators

Source EY analysis.

Network Operations Customer Third parties

• Network capacity planning

• Fault detection

• Network protection

• Billing and revenue assurance

• Fraud management

• SLA management

• Churn prediction

• Cross-selling

• Personalized services

• Social media analysis

• Local-based marketing

• Targeted advertising

• Vertical services

Efficiency gains Incremental revenue opportunity

6 | Inside Telecommunications

8. “Telefonica to build the city of the future through the Valencia smart city platform,” 22 May 2014.

. “Parking made easy Smarter parking project in Pisa kicks off,” Deutsche Telekom, 24 June 2014.

10. “5 reasons why mPOS matters now,” Monitise, November 2013. 11. “ABI Research mPOS to make up 46% of all POS terminals in 201 ,” Fierce Wireless, 7 July 2014.

FI-WARE standard and leveraging 350 sensors.8 In June, Deutsche Telekom launched a smart city pilot project in the Italian city of Pisa, using an intelligent parking guidance system to help avoid traf c jams and reduce CO2 emissions.9

As operators turn their attention to a widening array of big data use cases, a number of challenges present themselves. For one, focusing on certain types of data sets and associated use cases will be vital. Call patterns and billing data remain staples of the industry, yet newer data streams, such as social media sentiment analysis and sensor readings from machines, can transform existing customer experience initiatives while opening up a range of new use cases for third parties. Operators can also bene t from understanding the interrelationships between different use cases. Big data solutions that major on fault detection for network planning can certainly be leveraged for customer experience improvements, for example.

Looking ahead, machine learning will help make a growing range of data sources more manageable and compensate for a lack of highly skilled staff inside the organization. Scalability is likely to be a concern for many operators, and those looking to expand their capabilities should make modeling automation a central part of their plans. Data storage strategies will also need to be revisited only by understanding changing business needs can operators determine the most suitable technologies and locations to use in this regard.

At the same time, operators should pay close attention to the impact of big data initiatives on their organizations. While a drive for consistency could see general-purpose analytics tools made available to a small set of users for use across the entire business, the need for speedy implementations could also see use-case-driven solutions gain traction within particular teams.

For larger players, a hybrid approach that balances the demands of centralized expertise and dispersed specialisms may prove bene cial.

The ability to enter new types of relationships with vendors will also be crucial. While many operators will have one eye on making analytics tools more available to non-technical end users, partner selection will be informed by the need for managed and professional services that leverage vendor expertise.

Finally, compliance burdens need to be met head-on. Regulation determining how data can be collected, stored and repurposed is in ux, while trust levels with customers must improve if the reuse of personal data is to become acceptable to consumers. A greater focus on shifting regulatory and customer attitudes to data privacy will be essential for those players with high hopes for the big data market.

Operators consider implications of a shifting mPOS landscape Strong take-up of mobile point-of-sale mPOS terminals has been one of the most notable developments in the payments industry in recent years. While wireless systems have been handling retail POS transactions since the 1990s, the launch of Square’s smartphone-enabled card reader in 2010 has triggered a new phase of innovation in the proximity payments market.

Dongle-based hardware and cradle readers that attach to smartphones and tablets have proved attractive to micro-merchants and small to medium enterprises SMEs given the expense involved in buying or renting traditional card processing equipment. By the end of 2013, some 8 million businesses worldwide were using mPOS devices,10 while the installed base of such devices is set to reach 51 million by 2019, representing 46% of the overall POS terminals market.11

Figure 4: Global mPOS adoption forecast

1

8

1418

11

26

3439

05

10152025303540

2011 2013 2015 2017

Businesses adopting mPOS Addressable market of businesses

Businesses m

Source Monitise.

7Issue 14 |

12. “AT&T Vantiv Announce New Mobile Payments Solutions for Businesses of All Sizes,” AT&T, 14 January 2014. 13. “Telecom Italia, Payleven sign mPOS distribution deal,” Telecompaper, 30 June 2014. 14. “1010 launch new mPOS solution in Hong Kong,” Payments Cards and Mobile, 11 December 2013. 15. “Globe Telecom brings m-commerce to new heights with Globe Charge,” Globe Telecom, 28 April 2014.

16. “SIA Agreement with Orange Business Services for mobile point of sale payment solution in Europe,” Orange Business Services, 27 March 2014.

Alongside the relatively low cost of terminals, a range of drivers have catalyzed take-up of mPOS solutions, including simpli ed pricing structures, straightforward merchant enrollment and the lack of locked-in contracts. While smaller businesses have led the adoption curve to date, larger retailers increasingly see mPOS as a route to enhancing the in-store customer experience and generating ef ciencies. The ability to gather and repurpose product and customer data can pave the way toward new retailer-oriented propositions such as loyalty schemes, till and stock management, location-based services, and m-invoicing.

The number of service providers entering the space has also grown rapidly. Early pioneers such as Square and i ettle have been joined by a raft of players, from online payments providers such as PayPal to mobile payments specialists, banks and traditional POS vendors such as VeriFone. All are eager to tap opportunities represented by mPOS as an extension of smart commerce or digital marketing initiatives.

Mobile operators are also adding mPOS capabilities to their existing portfolios of payment services. In January, AT&T announced a partnership with payments processor Vantiv Inc. to deliver a range of mPOS services. Following the tie-up, the US carrier is offering Vantiv Mobile Checkout, a tablet-based service allowing businesses to process payments, as well as Vantiv Mobile Accept, an app that works with a card reader to allow businesses to take card payments on smartphones and tablets.

AT&T has cited use cases such as plumbers accepting card payments in customer homes as scenarios that could bene t from its new offering.12 Elsewhere, Telecom Italia signed a distribution deal with technology specialist Payleven in June. As a result, the Italian incumbent is offering Payleven’s mobile card reader to business owners faced with new legislation whereby they must allow debit card payments for transactions of over €30.13

Asian operators are also exploring opportunities involving the intersection of card readers and smartphones. Last year, Hong Kong-based operator 1O1O announced the launch of a mobile POS terminal in conjunction with Global Payments Asia-Paci c.14 In April, Globe Telecom launched Globe Charge, a solution that harnesses a mobile card reader and smartphone to accept payments and that is aimed at SMEs in the Philippines.15

Carriers are also sizing up opportunities elsewhere in the value chain, with managed services in mPOS payments seen as an area where they can play a role. In March, Orange Business Services struck an agreement with SIA, leveraging its expertise in machine-to-machine M2M and global roaming to help deliver SIA deliver traf c from mPOS terminals to bank authorization systems worldwide.16

Looking ahead, all players with ambitions in the mPOS market must consider how the ecosystem is likely to evolve. Terminal hardware and basic acceptance software are becoming rapidly commoditized, forcing early front-runners to extend their propositions. Front- and back-of ce capabilities such as loyalty schemes and inventory management have become important differentiators, yet even here the eld of competing solutions is widening at a heady rate. For many mPOS providers and enablers, the route toward scalability will lie in expanding addressable markets to include larger enterprises where they will have to compete with traditional POS vendors. Surveys highlight that many restaurants are factoring mobile solutions into their POS upgrade plans, for example.

8 | Inside Telecommunications

In this light, delineating value-added mPOS propositions for businesses according to size and industry vertical will be mission-critical. Reducing the cost-to-serve for small businesses gave birth to the mPOS business case, but more sophisticated uses focusing on business continuity and greater customer engagement can pave the way for a long-term service roadmap. Security will be an overarching concern as mPOS providers target larger businesses, with solutions that encrypt information relayed from POS to the payment processor coming to the fore.

Meanwhile, the prospect of terminal substitution and convergence gives further food for thought. Medium-sized retailers are already leveraging tablet-based solutions as a complement to traditional equipment, and further inroads can be made into businesses that either lack a legacy of traditional POS infrastructure or where

uctuating customer footfall requires a mix of traditional and mobile infrastructure. All told, there is likely to be increasing convergence between mobile and non-mobile POS infrastructure in years to come.

Operators hold advantages compared to mPOS specialists in view of their existing base of enterprise customers and the partnerships they already have in place with payments providers. However, card issuers and banks are also entering the space in greater numbers in order to combat disintermediation, and mPOS capabilities are likely to become just once facet of a wider revolution in retailers’ omnichannel strategies. As such, carriers will need to monitor a fast-changing ecosystem in order to optimize their partnering scenarios as they take steps to incorporate mPOS within existing proximity marketing and payments initiatives.

upgrades% respondents

Source “2014 POS Software Trends,” Hospitality Technology, 12 December 2013 survey of 100 restaurant operators .

0 10 20 30 40 50 60 70 80

Matching or exceeding competition

Building a robust POS platform

Tighter integration with e-commerce platform

Delivering personalized guest promotions

Enabling new payment options (e-wallet, etc.)

Adding mobile POS

9Issue 14 |

10 | Inside Telecommunications

Rewriting the network paradigm with NFVNetwork function virtualization (NFV) has proved to be one of the sector’s key talking points in 2014. In a world where operator pro tability remains under signi cant pressure, capital intensity levels remain high and service creation scenarios are multiplying, operators are focusing on how they can overhaul existing network architectures in order to become more ef cient organizations.

Against the backdrop of escalating demand for data, higher levels of xed-mobile convergence and the emergence of eet-footed over-the-top (OTT) competitors, scalable and cost-ef cient networks are a must. NFV allows operators transform their network paradigm from xed, closed and vendor-speci c infrastructure to an open, scalable and service-agile environment.

A software-driven network strategy allows operators to decouple network functions, such as caching from proprietary hardware appliances, and run them as virtualized software applications in a

2.Technology

cloud infrastructure, accelerating service provisioning. In tandem with software-de ned networking (SDN) a new approach to managing networks that shifts network control from hardware to software NFV brings a range of advantages to telcos looking to generate savings while improving performance.

Crucially, the need to purchase purpose-built hardware is eliminated and the risk of overprovisioning is reduced, thereby saving on capex, while the automation of application deployment and maintenance, coupled with reduced power consumption, leads to lower opex. All the while, time-to-market for new networking services can be shortened and return on investment improved, with the ultimate bene t of greater exibility overall as services are provided in a way that can adapt to changing business requirements.

0 10 20 30 40 50 60 70 80

Shortening innovation cycles

Reducing opex

Wider ecosystem of companies bringing innovation toyour network

Increased agility to scale services to address changingcustomer and line of business demands

Opening network up to innovation from supplier group

Reducing capex

Competitive pressures from OTT players

Driving new revenue

Figure 6: NFV key business drivers% respondents

Source “Survey of NFV priorities for service provider CIOs and CTOs,” HP, February 2014 (January 2014 global survey of 50 CIOs and 50 CTOs from CSPs).

11Issue 14 |

A number of leading operators have announced signi cant NFV initiatives this year. In February, Telefonica unveiled a group-wide NFV initiative called UNICA, which lays the groundwork for a radical redesign of its xed-line and mobile networks. Seeking to create a global network infrastructure on which multi-vendor platforms, features and services can be developed in standardized form, the Spanish carrier is aiming for 30% of new infrastructure to be aligned with its UNICA approach by 2016.17 As part of its plans, it has formed a R&D program with Ericsson to accelerate technological innovation and is creating a virtual infrastructure management (VIM) platform with the help of Red Hat and Intel in order to help vendors develop virtual functions.18

AT&T has also put NFV at the core of its transformation strategy, having last year announced its Supplier Domain Program 2.0 initiative. Using a combination of NFV and SDN, the US carrier is separating hardware and software functionality in order to simplify and scale its network, and it believes that the program will re ect a “downward bias” in capital spending over the next ve years.19 Since then, six suppliers have been announced, including both established players and specialist start-ups.

In May, NTT DoCoMo announced the completion of proof-of-concept trials with Alcatel-Lucent, Cisco and NEC for NFV. The Japanese operator now plans to virtualize its LTE core network, with commercial services running over it by the end of its 2015 16 nancial year.20 In the same month, parent company NTT Communications Group unveiled cloud-based services for enterprises built using an NFV platform developed by Virtela, which

it acquired in January.21 Elsewhere, China Mobile and Alcatel-Lucent have signed a one-year frame agreement to accelerate the carrier’s move to an all-IP network and pave the way for NFV and cloud services.22

Industry forecasts see the NFV market worldwide growing at a CAGR of 52% in the ve years to 2018,23 while 49% of operators in one global survey see NFV strategies coming of age in 2016 17.24 Con dence across the carrier and supplier landscape is clearly high, yet successful NFV initiatives will have to be carefully planned if open, software-driven networks are to live up to their promise.

Ambitious operators should move beyond a cost-savings mindset and consider new revenue opportunities enabled by NFV and SDN in order to build a strong business case for investment. The timing of investment will also require careful scrutiny. Many players will be focused on extracting value from their existing network elements, while decisions to transform network architecture will also be shaped by deployment plans regarding new technologies such as VoLTE.

Clearly all players will be keen to minimize disruption to their existing business as they virtualize network components. For this to happen, incremental, phased implementations have an important role to play beginning with less critical parts of the network while integration with existing OSS BSS systems will also require a staggered approach. Deciding the order in which network components will be virtualized will also require deliberation operators currently see the LTE core network and content delivery networks as leading candidates to be virtualized rst.

17. “Telefonica forges ahead on end to end virtualisation of its network,” Telefonica, 24 February 2014. 18. “Telefonica to work with Red Hat and Intel to set the ground for next-generation telecommunications virtualized network services,” Telefonica, 28 May 2014. 19. “AT&T Supplier Domain Program 2.0,” AT&T news release, 23 September 2013. 20. “DOCOMO and World-leading Vendors Verify Feasibility of Network Functions Virtualization,” NTT DoCoMo, 27 May 2014.

21. “NTT Launches NFV-Based Cloud Services,” NTT, 29 May 2014. 22. “China Mobile selects Alcatel-Lucent for strategic transformation to all-IP ultra-broadband network,” Alcatel-Lucent, 27 May 2014. 23. “Global Network Functional Virtualization Market 2014-2018,” TechNavio, 7 February 2014. 24. “Survey of NFV priorities for service provider CIOs and CTOs,” HP, February 2014 (January 2014 global survey of 50 CIOs and 50 CTOs from CSPs).

12 | Inside Telecommunications

Operator relationships with their suppliers will also need to evolve in new ways. As demonstrated by existing proof-of-concept trials, closer collaboration is essential and a wide range of vendors from data center technology specialists to systems integrators that can provide a mix of equipment are all in a position to help. At the same time, telcos’ shift away from proprietary hardware platforms will represent a risk to some suppliers, who must refocus their portfolios to cater for telcos’ new network imperatives.

In terms of industry speci cations for NFV, there is also still work to do. A number of operators formed the European Telecommunications Standards Institute (ETSI) Industry Speci cations Group (ISG) in early 2013. Having originally envisaged a two-year time frame to specify NFV, the group has since decided to renew its charter as it explores interoperability for NFV, with an end goal of a common, standardized platform that can bring further economies of scale. In addition, standards will need to evolve so that vendors can develop application programming interfaces (APIs) for OSS solutions that support service orchestration in an NFV environment.

There are also unknowns regarding how NFV, SDN and cloud management technologies will be developed in tandem, an area that again will require higher levels of industry cooperation. Ultimately, the advent of NFV and SDN underline how the worlds of telecommunications and IT are overlapping in new ways. A new lexicon for network technology has emerged as a result, and closer horizontal and vertical collaboration is essential if operators and vendors are to make the most of new network architectures in the long term.

Over 300 LTE networks commercially launched worldwideThe mobile industry’s migration to LTE networks continues at an impressive rate. According to the latest gures released by Global mobile Suppliers Association (GSA), some 318 LTE networks had been launched worldwide by July 2014 in 111 countries. Meanwhile, the number of 4G subscribers worldwide stood at 245.4 million at Q1 2014, and there are now some 769 LTE-capable devices on the market.25

Between April and July, several countries had their rst commercial LTE launches, including Israel, Madagascar and Taiwan. Earlier, in March, Digicel Papua New Guinea became the rst mobile operator to launch a commercial LTE services on the globally harmonized APT 700MHz band, and there are now six networks operating at this frequency. The rst North African LTE network went live in Algeria in May, while a TD-LTE network was launched by YooMee in Ivory Coast one month earlier.

China Mobile has seen strong take-up of LTE services launched at the end of 2013, with the telco adding 3.3 million customers in the month of May alone.26 The operator, a major global backer of the Time-Division Duplex (TDD) variant, had committed US 6.7 billion to rolling out TD-LTE in 2013.27 In June, rival China Telecom received approval to conduct FDD trials from the China’s Ministry of Industry and Information Technology, with a license expected to be allocated in early 2015.28

25. “Over 50 LTE networks launched this year, total is 318 in 111 countries,” GSA, 28 July 2014. 26. “Operation Data,” China Mobile website, 3 July 2014. 27. “China Mobile commits 6.7 B to TD-LTE capex in 2013,” Fierce Wireless, 28 March 2013. 28. “FDD-LTE 4G Licenses Could Get China Telecom Back In The Race,” Forbes website, 25 June 2014.

Figure 7: Commercially launched LTE networks worldwideNumber of LTE networks

Source “Over 50 LTE networks launched this year, total is 318 in 111 countries,” GSA, 28 July 2014.

2 1646

148

267 318

350+

28 July

0

50

100

150

200

250

300

350

400

2009 2010 2011 2012 2013 2014

13Issue 12 |

Globally, the majority of mobile players currently favor the Frequency Division Duplexing (FDD) mode for deployment, with 1800MHz spectrum the most popular band, used in over 45% of commercial LTE networks.29 However, operator interest in reusing other spectrum bands for future LTE deployments continues to grow, with Vodafone unveiling plans to re-farm existing 3G spectrum at 2100MHz for LTE.30 At the same time, the signal propagation characteristics of sub-1GHz spectrum which are ideally suited to rural rollouts are also attracting operator interest, with 55 commercially networks now running on the 800MHz band.

While growth in the number of LTE networks worldwide remains robust, the peak rate of deployments has now passed, and operators are turning their attention to increasing throughput on their 4G infrastructure. LTE Advanced (LTE-A) is an integral part of the industry’s network roadmap, with some 20% of the world’s LTE operators reportedly investing in the technology.31 Carrier aggregation is playing a central role in LTE-A upgrades, allowing mobile carriers to utilize all their spectrum resources to boost data rates. In tandem with other features such as antenna techniques and interference management, operators can now reach network speeds of up to 300Mbps.

While most LTE-A deployments rely on the aggregation of two carrier bands of sub-20MHz, deployments of tri-band carrier aggregation are also in the cards. South Korea’s LG U+ has completed eld trials that aggregate spectrum in the 800MHz,

13Issue 14 |

2100MHz and 2600MHz bands.32 In the UK, EE has also laid out its plans to aggregate a third carrier, thereby increasing peak theoretical speed to 400Mbps.33 Meanwhile, SK Telecom plans to introduce enhanced inter-cell interference, in addition to carrier aggregation, as part of its next phase of LTE-A deployment.34

Beyond advancements in technology, unique LTE service proposition are starting to emerge, with VoLTE deployments proving increasingly popular with telcos. Q2 2014 saw the rst commercial launches in Hong Kong by PCCW HKT and 3HK, followed by launches in Singapore, South Korea and the US. According to the GSA, some 66 operators worldwide are investing in VoLTE studies, trials or deployments, including 10 that have commercially deployed high-de nition (HD) voice. With dropped calls on smartphones still a pain point for consumers and HD voice presenting a new way for operators to differentiate against smartphone calling apps, interest can only grow further.

29. “Over 50 LTE networks launched this year, total is 318 in 111 countries,” GSA, 28 July 2014. 30. “Vodafone 4G Webinar,” Vodafone, 27 March 2014. 31. “World’s 300th LTE network comes online,” Total Telecom Plus, 11 June 2014, via Factiva, © 2014 Terrapinn Holdings Limited.

32. “LG U+ in tri-band carrier aggregation trial,” Total Telecom Plus, 10 June 2014. 33. “EE eyes tri-band carrier aggregation,” Total Telecom Plus, 15 May 2014. 34. “SK Telecom commercially launches 225 Mbps LTE-A service,” Telecompaper, 18 June 2014.

Figure 8: Global LTE deployment status

Commercial LTE availableLTE network deployment planned and underwayLTE trial systems underway

North America – 46.7% of global LTE subscribers

Europe – 11.5% of global LTE subscribers

NAPAC – 38.7% of global LTE subscribers

Rest of the world – 3.1% of global LTE subscribers

Source GSA

14 | Inside Telecommunications

Industry stakeholders seek new routes to combat online piracyOnline piracy remains a signi cant burden on the creative industries worldwide. The music industry was the rst to be affected by large-scale internet piracy, before improvements in internet bandwidth saw the lm industry suffer in turn. Evaluating the economic cost of online piracy is far from straightforward, partly because not every act of illegal le-sharing or streaming displaces a legal purchase, but also because consumers may spend more on other activities if they spend less on music or

lms. However, one study suggested that motion picture piracy in all its forms was already costing the US economy US 20.5 billion annually by 2006, with governments deprived of US 857 million in tax revenue each year.35

3.Regulation

In recent years, governments and regulators worldwide have sought to combat the menace of online piracy, and with some success global infringement relating to BitTorrent portals declined in the wake of the closure of torrent sites Megaupload and Megavideo in 2012, for example. Nevertheless, studies demonstrate that use of infringing content is still growing. During January 2013, 432 million internet users worldwide explicitly sought infringing content, with both the number of users seeking such content and the bandwidth involved seen to rise.36

35. “The True Cost of Motion Picture Piracy to the U.S. Economy,” Institute for Policy Innovation, September 2006. 36. “Sizing the piracy universe,” NetNames envisional, September 2013.

Figure 9: Estimated infringing data as a proportion of video streaming bandwidth% all video streaming bandwidth

Source “Sizing the piracy universe,” NetNames, September 2013.

0

5

10

15

20

25

30

Europe Asia-Paci c North America

15Issue 14 |

Considered from a regional perspective, European internet users are more likely to be visitors to BitTorrent portals than internet users in other geographies, while the continent’s users are also more likely to be users of cyberlocker sites. Faced with this, a variety of stakeholders in the region are looking for new ways to combat online piracy. In July, representatives from the UK’s creative industries and major internet service providers (ISPs) announced Creative Content UK, a partnership designed to boost consumer awareness of legitimate online content services and help reduce online copyright infringement.37

The cross-sector alliance plans to conduct an educational awareness campaign in 2015, led by content creators and part-funded by government. Furthermore, the members are set to introduce a subscriber alerts system that will notify end users when their accounts are believed to have infringed copyright. Founding partners of the scheme include BT, Sky, TalkTalk and Virgin Media alongside the Motion Picture Association (MPA) and the BPI (British Recorded Music Industry).

This new UK alliance represents a signi cant departure from previous anti-piracy approaches. For one, cross-industry cooperation lies at the heart of its activities, in contrast to the ecosystem tension that has accompanied previous attempts to monitor and combat online piracy. Meanwhile, the focus on consumer awareness also signals a more positive tone in content providers’ and ISPs’ interactions with end users regarding piracy.

Even so, the newly announced measures represent a weakening of anti-piracy plans as originally tabled by rights holders. According to news reports, content owners originally wanted access to a database of known illegal downloaders, with letters sent out to infringers warning of the possibility of further legal action.38 Previously, the UK’s Digital Economy Act of 2010 had also sought

stronger measures such as disconnection and the threat of court action before parts of the act addressing copyright infringement were repealed. Depending on how the new scheme performs, there may yet be calls to introduce harsher anti-piracy measures.

Elsewhere, some countries have dispensed with a softer approach. Uncon rmed reports suggest that lawmakers in Australia have drafted proposals to block overseas websites that host pirated content and force ISPs to stop users illegally downloading movies and music. This could in turn entail moves to roll back to the outcome of a court case brought by a group of movie studios against one of the country’s ISPs in 2012.39

Worldwide, there remains a lack of industry consensus on what form penalties for illegal downloaders should take. In 2013, France scrapped a controversial law whereby users suspected of three copyright infringement offenses – following warnings – would be disconnected.40 Monitoring costs proved expensive, and the French Government now favors ning users who fail to respond to warnings, while also sharpening its focus on websites that pro t from pirated material. A growing focus on commercial piracy is evident elsewhere too in July, the UK’s City of London police began placing ads on illegal torrent sites in an effort to curb their advertising revenue.41

In order to combat individuals’ copyright infringement, industry actors are placing more importance on educating end users as an alternative to more draconian approaches – a shift in emphasis that is evident in Creative Content UK’s proposed awareness campaign. This is important in the light of research showing that many consumers are unaware that uploading commercially produced media to le-sharing websites is illegal.

37. “UK Creative Industries and ISPs Partner In Major New Initiative To Promote Legal Online Entertainment,” The British Recorded Music Industry, 19 July 2014. 38. “Deal to combat piracy in UK with ‘alerts’ is imminent,” BBC, 9 May 2014.

39. “Government anti-piracy plan one of the world’s toughest,” Sydney Morning Herald, 27 July 2014. 40. “France drops controversial ‘Hadopi Law’ after spending millions,” The Guardian, 9 July 2013. 41. “Police are Placing Anti-Piracy Warning Ads On Illegal Torrent Sites,” Forbes, 29 July 2014.

16 | Inside Telecommunications

Looking ahead, successful anti-piracy strategies will require a delicate balancing act on the part of all stakeholders. Greater industry focus on educating end users will be essential while more punitive measures against those that pro t from online piracy will also nd more favor. Much will depend on how different industry actors de ne their interdependent roles ISPs are keen not to submit to a burdensome scenario where they have to warn or punish customers accessing infringing online content, while rights owners will continue to point to the economic multiplier effects of healthy creative industries as they look to protect their interests.

Yet the combination of divergent industry attitudes and rising consumer anxiety about data privacy means that deciding on a cross-industry approach, apportioning roles for different industry actors and agreeing on proportionate penalties for illegal downloaders are far from straightforward. Greater formal and informal collaboration between stakeholders will be needed if long-term plans are to mature into holistic and effective strategies.

All eyes on European antitrust merger remediesDeal activity is rising in the telecommunications sector, with 625 deals struck worldwide in 2013 compared to 544 announced in the preceding year. A number of factors are driving this, from macroeconomic recovery to rising con dence in credit availability and advantageous debt nancing terms. Meanwhile, the need for economies of scale, additional spectrum and diversi ed revenue streams are all informing operators’ inorganic growth strategies.

Despite a range of M&A scenarios, in-market consolidation is very much the chief talking point within the industry. Pro tability remains under signi cant pressure, particularly in developed markets where capex burdens and competitive intensity levels are pronounced. Telcos’ appetite for in-market scale is well understood, yet many industry executives fear that regulators will prevent consolidation scenarios from running their course due to antitrust concerns. Such anxieties are particularly pronounced in Europe, where there are 100 operators owned by 40 companies competing over a population of 505 million – and prices continue to fall sharply.42

Recent merger review decisions show that regulators are starting to recognize the need for more rational market structures that can help simulate infrastructure investment. In July, a landmark decision saw the European Commission (EC) approve a merger of Telefonica Deutschland and KPN’s E-Plus business unit, the number three and four players in Germany’s mobile market. Key to the approval are several concessions designed to ensure competition levels are maintained, including the sale of 30% of the combined entity’s spectrum holdings to one or more mobile virtual network operators (MVNOs) and an expansion of the number of virtual players in the market.43

42. “Europe’s telcos press deals,” The Wall Street Journal, 28 February 2013. 43. “Mergers Commission clears acquisition of E-Plus by Telefonica Deutschland, subject to conditions,” European Commission, 2 July 2014.

Figure 10: Consumer awareness of online copyright infringement% internet users

Source “Digital Entertainment Survey,” Wiggins, 23 April 2013 (online survey of 2,500 UK internet users).

0 10 20 30 40 50

Think it is legal or don't know whetherit is legal to copy a lm or TV show

as a le from a friend

Claim it is easy to distinguish betweenlawful and pirate sites

Think it is legal or don't know whether itis legal to upload commercially produced

media to a le-sharing websiteFigure 11: M&A inhibitors in the telecommunications sectorQuestion What is your primary reason for not pursuing an acquisition in the next 12 months

Source , EY, April 2014 (survey of 1,600 senior executives, including 56 from telcos).

0 10 20 30 40

Low board shareholder con dence

Insuf cient acquisition opportunities

Valuation gap

Low con dence in business environment

Data execution and integration capabilities

Funding availability

Regulatory environment

Telecoms All sectors

17Issue 12 |17Issue 14 |

The EC has leveraged antitrust in other European mobile merger reviews. The 2012 acquisition of Orange’s Austrian business by H3G was cleared subject to conditions, including the divestment of spectrum to a new market entrant and an agreement to provide wholesale network access on agreed-upon terms to up to 16 MVNOs over 10 years. Furthermore, the EC approved H3G’s acquisition of O2 Ireland in May this year, also on the promise that the combined entity’s network was opened up to competitors.

Many industry watchers are now wondering whether such remedies proposed by the EC amount to a blueprint for consolidation. Yet each European merger approval to date has hinged on local market factors. In Austria, prices were already very low relative to other EU countries, suggesting a highly competitive market, while Ireland has a high proportion of rural subscribers, making it more challenging for operators to provide high levels of mobile data coverage on a capex-per-head basis. These factors underlined a role for consolidation in producing a market structure better suited to network investment.

Approval of the German deal was seen as crucial test case, not because it would reduce the number of network owners from four to three – as was the case in the other markets – but because the market is large and no new market entrant was expected as a result of 4G spectrum auctions. Furthermore, the fact that German mobile prices have historically been high, despite the presence of virtual operators for some years, meant that many industry watchers were less certain of the read-across from previous EC merger decisions.

The EC’s latest decision suggests that it now looks favorably on four-to-three mobile market consolidation, as long as commitments to divest spectrum or provide wholesale network access to virtual operators are met. Looking ahead, one crucial question would be whether the types of remedies proposed in Austria, Germany and Ireland could be replicated in markets where consolidation involves three-to-two consolidation. A three-to-two mobile merger proposed in Switzerland in 2009 was rejected by the country’s competition agency, and a planned merger between TeliaSonera and Tele2 in Norway is currently being reviewed by the national regulator.

At the same time, national views on consolidation reveal a wide spectrum of opinion. In Ireland, ComReg reacted with dismay to the EC’s merger approval, believing remedies would not safeguard against negative consequences for consumer welfare.44 In Germany, the country’s antitrust regulator, Bundeskartellamt, suggested that prices could rise following a merger, as has proved the case in Austria.45 Meanwhile, a June meeting of various national regulators to review the EC’s approval of the German deal saw just 2 of 12 regulators support the antitrust remedies proposed.46 However, some countries are strongly in favor of consolidation, with the French Government actively seeking a reduction in mobile network owners in order to end a severe price war.

In this light, it is clear a one-size- ts-all approach to consolidation reviews is impossible. However, recent EC decisions do point to the renewed importance of the MVNO model as a catalyst for sustainable competition. Historically, new entrants via spectrum auctions have been seen as catalysts for competition, but that baton appears to be now passing to virtual operators. Europe remains a hotbed for MVNOs, accounting for two-thirds of the global total, yet their combined market share per market remains small outside of Northern European countries.

Certainly, merger remedies that include commitments around spectrum divestment and network capacity offer a rmer basis for MVNOs to compete in the long term, and they signal a departure from previous volume-based agreements. In turn, they also provide a more certain revenue stream for the host operator due to the time commitments involved, paving the way for more sustainable agreements between asset-light players and their network-owning hosts.

Recent decisions regarding in-market mobile mergers suggest the EC’s stance has considerably softened regarding consolidation and may spur more activity in markets where there are four network-owning mobile operators. The EC remains strongly in favor of breaking down national discrepancies in regulation and competition law, and other factors may also shape its perspective going forward. These include the progress of EU-wide sector market reform, the performance of markets where mergers have been approved, related developments in cross-segment consolidation – such as operators acquiring pay-TV businesses – and the way competition from OTTs is perceived.

44. “European Commission completes its investigation into the proposed acquisition by Hutchison 3G UK Holdings Limited of Telefonica Ireland Limited,” ComReg, 28 May 2014. 45. “Austrian Mobile -Service Prices Rise as Much as 11% After Merger in 2013,” Bloomberg, 16 January 2014. 46. “Regulators oppose EC on Telefonica E-Plus deal – report,” Mobile World Live, 23 June 2014.

Figure 12: MVNOs’ market share in selected countries, mid-2013% subscriber market share

Source “MVNO Observatory,” Piran Partners, April 2014.0 10 20 30 40

Netherlands

Germany

UK

France

Spain

Italy

Poland

18 | Inside Telecommunications

Introduction

Deal activity across the telecommunications sector was high in Q2 2014 compared to preceding quarters. The second three months of 2014 saw deals worth a total of US 100.8b announced, an increase of 84% compared to Q1 2014 and one of the highest gures registered in recent years. There were 159 transactions during the second quarter, well up on the 108 deals announced during the rst quarter and back to deal volume levels evident in 2013.

Cross-service consolidation yet again features as a signi cant deal driver, with AT&T’s US 67.1b bid for DirecTV another example of how leading telcos are strengthening their triple-play propositions for residential customers. Transactions involving tower companies scaling up and acquiring operator assets were also strongly represented during the quarter, while footprint growth remains important for emerging market players eager to diversify their revenue streams.

4.Mergers and Acquisitions

Considering transactions by target geography, Europe, Middle East, India and Africa (EMEIA) outpaced other regions in deal volume, accounting for 60% of transactions announced during the quarter. Asia-Paci c saw deal value more than double compared to the rst quarter, with both consolidation and adjacent market moves well represented. Deal volume in the Americas was at compared to the preceding quarter, yet the region accounted for 85% of global deal value in the second quarter, driven principally by AT&T’s bid for DirecTV but with sizable deals also involving Latin American mobile operators alongside wholesalers and tower companies.

US$3,185

US$659

US$50,883

US$3,928

US$1,405

US$14,929

US$84,464

Japan

Asia-Paci c

EMEIA

Americas

2Q 2014 1Q 2014

Figure 13: Telecoms M&A deal value by target area Q2 2014 (US$m)

Sources ThomsonOne, Capital IQ, Mergermarket.

19Issue 14 |

Operators target pay-TV gains Deals driven by ambitions in the residential market are an enduring feature of sector M&A. Combinations of media and telecommunications capabilities are becoming more important as operators look to boost in-market scale and reduce churn levels by tying customers into more products. Triple-play capabilities are more important than ever and AT&T’s acquisition of leading Americas pay-TV provider DirecTV, announced in May, was the quarter’s largest deal. The combination of the two companies creates a content provider with complementary strengths in mobility, video and broadband services, covering 70 million customer locations.47 This multi-platform strength is designed to meet customers’ evolving content consumption needs and changing programming preferences.

Following the closure of the deal, AT&T plans to use merger synergies to build and enhance broadband services to 15 million customer locations, principally in rural areas where high-speed broadband is currently lacking. AT&T has underlined it will provide both bundles as well as stand-alone wireless broadband for customers who wish to consume OTT video services such as Net ix or Hulu. In this light, it has stressed its commitment to net neutrality.48

Aside from adding 20 million DirecTV customers, AT&T is set to bene t from exclusive content rights for the National Football League (NFL) Sunday Ticket and a stronger bidding position for premium content in the future. The acquisition also gives AT&T a foothold in the Latin American pay-TV market, where DirecTV leads

in terms of subscribers. Pay-TV penetration is set for further growth in the region, and the market is expected to double in size between 2013 and 2019, reaching US$30.91 billion.49

47. “DirecTV and AT&T Merger FAQ,” DirecTV, accessed August 2014. 48. “AT&T to Acquire DIRECTV,” AT&T, 18 May 2014.

49. “Latin American pay TV sector to grow 51% by 2019,” ICT Monitor Worldwide, 13 June 2014 via Factiva, © 2014 Telecompaper. 50. “Italy’s Mediaset to Sell Stake in Digital Plus Pay-TV to Spain’s Telefonica,” 4 July 2014. 51. “Vodafone to acquire Grupo Corporativo Ono, S.A.,” Vodafone, 17 March 2014.

Figure 14: Latin America pay-TV penetration

0

10

20

30

40

50

60

2008 2012 2016EPay-TV penetration

% households

Source SNL Kagan.

Carriers in other regions are also aiming to take advantage of pay-TV opportunities. In May, Spain’s Telefonica presented a bid for a majority stake in one of Spain’s largest sports TV broadcasters, Distribuidora de Television Digital S.A., which operates under the Digital Plus brand. The move for a 56% stake held by Spain’s Prisa was then followed by an agreement to acquire a 22% stake held by Italian broadcaster Mediaset.50 Digital Plus owns the broadcasting rights to Spanish soccer games, and Telefonica’s stake increase in the platform follows Vodafone’s acquisition of Spanish cable operator Ono earlier this year.51

20 | Inside Telecommunications

Elsewhere, Telekom Austria announced the acquisition of leading Macedonian cable operator Blizoo, which has 63,000 subscribers and offers TV services, broadband and xed voice. The takeover represents a signi cant step in ful lling the Austrian player’s convergence strategy, with quad-play capability set to bolster the operator’s existing presence through number two mobile player Vip.52 Southeastern Europe saw some more pay-TV-driven M&A activity just after the close of the quarter, with Greek incumbent OTE submitting a non-binding offer for rival Forthnet’s pay-TV platform.53

54. “Swisscom publishes prospectus for the acquisition of PubliGroupe Ltd,” Swisscom, 23 June 2014. 55. “From concept to delivery the M2M market today,” GSMA Intelligence, February 2014. 56. “South Africa’s Telkom takes second shot at IT rm BC , offers $256 million,” Reuters, 22 May 2014. 57. “TeliaSonera acquires Danish IT and system integrator Siminn Danmark,” TeliaSonera, 1 April 2014. 58. “Telecom Acquires Business Cloud Specialist Appserv,” Telecom New ealand, 18 June 2014.

52. “Telekom Austria Group acquires leading cable operators in the Republic of Austria,” Telekom Austria, 23 June 2014. 53. “Greek telco OTE offers to buy rival Forthnet’s pay TV unit,” Reuters, 1 July 2014.

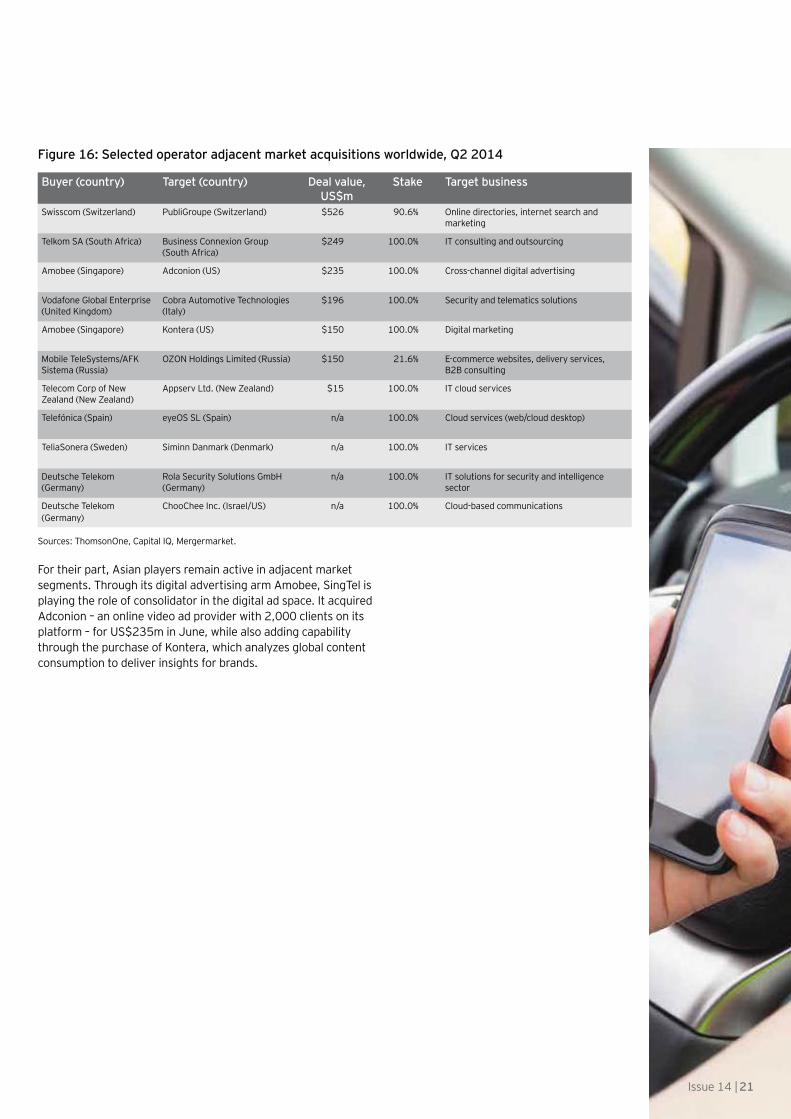

Western operators step up adjacent market exposureM&A is playing a more important role in supporting operator ambitions in the wider technology space. In recent quarters, a number of operators have made acquisitions in adjacent market segments, largely to support their burgeoning enterprise propositions. Much of the early running in this regard has been made by Asia-Paci c operators, yet leading European carriers are now starting to make moves of their own.

Looking to capitalize on growth in digital advertising, Swisscom has taken control of Swiss marketing and advertising rm PubliGroupe, including its online directory and search properties. The state-owned incumbent initially sought to buy out PubliGroupe’s shares in their jointly owned directories business, but, following a bidding war, agreed to form a partnership with rival bidder Tamedia to co-develop the directory business. The deal remains subject to the approval of the Federal Competition Commission.54

In June, UK-based Vodafone announced its intention to acquire Cobra Automotive Technologies in a deal valued at €145 million (US$196 million). Headquartered in Italy, Cobra is a leading provider of security and telematics solutions to the automotive and insurance sectors. Research suggests that adoption rates for machine-to-machine (M2M) solutions are high in the automotive industry relative to other industry verticals,55 and the acquisition signi es a bolder move into connected car solutions for Vodafone, which had previously been a major supplier of subscriber identity modules (SIMs) to the Italian rm.

The need for new capabilities in IT solutions and cloud services has driven a number of other adjacent market moves in the second quarter. In May, South African incumbent Telkom SA bid for complete control of IT infrastructure rm Business Connexion (BC ) seven years after competition concerns scuppered its rst bid.56 Shareholders have approved the deal, and the competition authority is set to make a decision before the end of the year.

Other incumbents are also moving further into the enterprise IT market. In April, Sweden’s TeliaSonera acquired Danish systems integrator Siminn Danmark, which employs 42 people and has 2,800 corporate customers.57 Deutsche Telekom is also actively seeking new technology capabilities and acquired two IT specialists in the three months to June, with Rola Security Solutions set to bolster the German carrier’s new cybersecurity division. Elsewhere, Telecom New ealand struck a conditional agreement to acquire cloud desktop specialist Appserv, viewing the deal as complement to its overall cloud strategy.58

Figure 15: Top 10 telecoms M&A worldwide by deal value, Q2 2014

Sources ThomsonOne, Capital IQ, Mergermarket

US$67,100

US$693

US$882

US$981

US$1,020

US$1,959

US$2,205

US$2,643

US$5,566

US$7,262

Cinven/Gas Natural Fenosa Telecomunicaciones

China Mobile/True Corp.

American Tower/BR Towers

Telefónica/Distribuidora de Television Digital

América Móvil/Telekom Austria

Altice/Numericable

Fonds National de l'Investissement/Orascom Telecom Algeria

Investor Group/AT&T stake in América Móvil

Level 3/tw telecom

AT&T/DirecTV

Buyer/target Deal value (US$m)

21Issue 12 |21Issue 14 |

For their part, Asian players remain active in adjacent market segments. Through its digital advertising arm Amobee, SingTel is playing the role of consolidator in the digital ad space. It acquired Adconion – an online video ad provider with 2,000 clients on its platform – for US$235m in June, while also adding capability through the purchase of Kontera, which analyzes global content consumption to deliver insights for brands.

Buyer (country) Target (country) Deal value, US$m

Stake Target business

Swisscom (Switzerland) PubliGroupe (Switzerland) $526 90.6% Online directories, internet search and marketing

Telkom SA (South Africa) Business Connexion Group (South Africa)

$249 100.0% IT consulting and outsourcing

Amobee (Singapore) Adconion (US) $235 100.0% Cross-channel digital advertising

Vodafone Global Enterprise (United Kingdom)

Cobra Automotive Technologies (Italy)

$196 100.0% Security and telematics solutions

Amobee (Singapore) Kontera (US) $150 100.0% Digital marketing

Mobile TeleSystems/AFK Sistema (Russia)

O ON Holdings Limited (Russia) $150 21.6% E-commerce websites, delivery services, B2B consulting

Telecom Corp of New ealand (New ealand)

Appserv Ltd. (New ealand) $15 100.0% IT cloud services

Telefónica (Spain) eyeOS SL (Spain) n/a 100.0% Cloud services (web/cloud desktop)

TeliaSonera (Sweden) Siminn Danmark (Denmark) n/a 100.0% IT services

Deutsche Telekom (Germany)

Rola Security Solutions GmbH (Germany)

n/a 100.0% IT solutions for security and intelligence sector

Deutsche Telekom (Germany)

ChooChee Inc. (Israel/US) n/a 100.0% Cloud-based communications

Figure 16: Selected operator adjacent market acquisitions worldwide, Q2 2014

Sources ThomsonOne, Capital IQ, Mergermarket.

22 | Inside Telecommunications

Footprint growth in focus in Asia and AfricaWhile adjacent market opportunities are proving important to all players regardless of geography, footprint growth is increasingly the preserve of emerging markets operators. One of the most signi cant deals during the quarter was China Mobile’s acquisition of an 18% stake in Thai telecoms group True Corp for US$881 million. The deal marks China Mobile’s rst signi cant acquisition overseas since the takeover of Pakistan’s Paktel in 2007 and signals a need to diversify beyond an increasingly competitive home market, where network investment needs are high and pricing pressure is rising.

True Corp provides broadband, mobile phone and pay-TV services and is the third-largest mobile operator in Thailand, with 29 million subscribers. As the only Thai operator without a foreign partner, the deal with China Mobile is expected to aid its network expansion. At the same time, the move into Thailand provides China Mobile with an opportunity to diversify its earnings growth in the long term. Thai consumer trends are positive, with promising levels of take-up of smartphones and associated mobile video services compared to other markets in the region.

Telecommunications assets in Africa are also changing hands. In May, UAE mobile market leader Etisalat agreed to sell a substantial portion of its West African operations to Maroc Telecom, the Moroccan incumbent in which it has taken a 53% stake. The deal, valued at US$650 million, sees Etisalat’s units in Benin, Central African Republic, Gabon, Ivory Coast, Niger and Togo transferred to the Moroccan carrier. Meanwhile, regional African mobile operator Africell agreed in May to acquire a majority stake in Orange Uganda, the country’s number three player, with 620,000 customers.59 Having launched in Gambia in 2001, Africell is one of Africa’s largest privately owned telcos and has operations in Sierra Leone and the Democratic Republic of the Congo.

59. “Orange signs an agreement with Africell for the sale of its stake in Orange Uganda,” Orange, 19 May 2014.

% mobile users

Source “The Asian Mobile Consumer Decoded,” Nielsen, 17 September 2013.

0

20

40

60

80

100

Singapore Malaysia Australia China Thailand Indonesia India Philippines

Smartphone penetration Mobile video usage (in last 30 days)

23Issue 14 |

EY | Assurance | Tax | Transactions | Advisory

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

How EY’s Global Telecommunications Center can help your business Telecommunications operators are facing a rapidly transforming business model. Competition from technology companies is creating challenges around customer ownership. Service innovation, pricing pressures and network capacity are intensifying scrutiny on return on investment. Additionally, regulatory pressures and shareholder expectations require agility and cost efficiency. If you are facing these challenges, we can provide a sector-based perspective to addressing your assurance, advisory, transaction and tax needs. Our Global Telecommunications Center is a virtual hub that brings together people, cultures and leading ideas from across the world. Whatever your need, we can help you improve the performance of your business.

© 2014 EYGM Limited. All Rights Reserved.

EYG no. EF0144CSG/GSC2014/1446008ED None

In line with EY’s commitment to minimize its impact on the environment, this document has been printed on paper with a high recycled content.

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

ey.com/telecommunications

Prashant Singhal Global Telecommunications [email protected]

Holger Forst Global Telecommunications Assurance Leader [email protected]

Staffan Ekström Global Telecommunications TAS [email protected]

Amit Sachdeva Global Telecommunications Advisory [email protected]

Bart van Droogenbroek Global Telecommunications Tax Leader [email protected]

Contacts

@EY_Telecoms