is the uk life assurance market competitive? evidence from

TRANSCRIPT

ab cdIs the UK life assurance

market competitive?Evidence from companies’

charges

2003 Life Convention, 9-11 NovemberHilton Birmingham Metropole Hotel

Chris O’BrienCentre for Risk and Insurance Studies,Nottingham University Business School

Plan

Regulation and competitionThe nature of life assurance: customers

and competitionTheories: what might we expect?Results: PIA data 1995-99FSA comparative tables 2003

Regulation and competitionFSA’s role

• “The key purpose of the FSA’s regulatory regime is to correct market failure”

• Forthcoming FSA paper, “Harnessing Market Forces”

• Does the market work satisfactorily?

Regulation and competitionResponses to Sandler consultation

• The government has a high threshold for persuasion for moving from 1% cap

• Charge caps are wrong in principle, the market is competitive

• May be market failures but other responses appropriate, e.g. benchmarking

Customers and competitionSandler report: consumer weakness

• Products complex, hard to assess, including price & quality (& trade-off)

• Long-term nature, infrequent purchase • Opaque, inconsistent terminology• Product proliferation, differentiation

doesn’t reflect true differences• Low financial literacy

Other barriers to competition?

• With profits: advantage of existing firms with estate, 10% ppn non-competitive?

• Distribution channels• Regulation a deterrent to new entrants

– Solvency requirements– Conduct of business rules– Regulatory environment

Theories: over time

New entrants have low chargesExiters have high chargesMergers: low charge product chosen

economies of scale or elimination of inefficient activities

We shall also look at effect of distribution channel

Theories: cross-section data

Low charges associated with:Direct distributionLarge sizeMutualityBancassurerLow credit rating

PIA data 1995-99

RIY data for products (estimates, inconsistencies, eg post-merger)but a reasonable cost measure?

With profit endowments (10 yrs)Low cost mortgage endowments (25 yrs)Unit-linked personal pensions (25 yrs)Market coverage nearly complete?

Average chargesfor 3 products (unweighted)

1

1.5

2

2.5

3

3.5

4

1995 1996 1997 1998 1999

RIY

(%) EAP 10

LCEAP25ULPP25

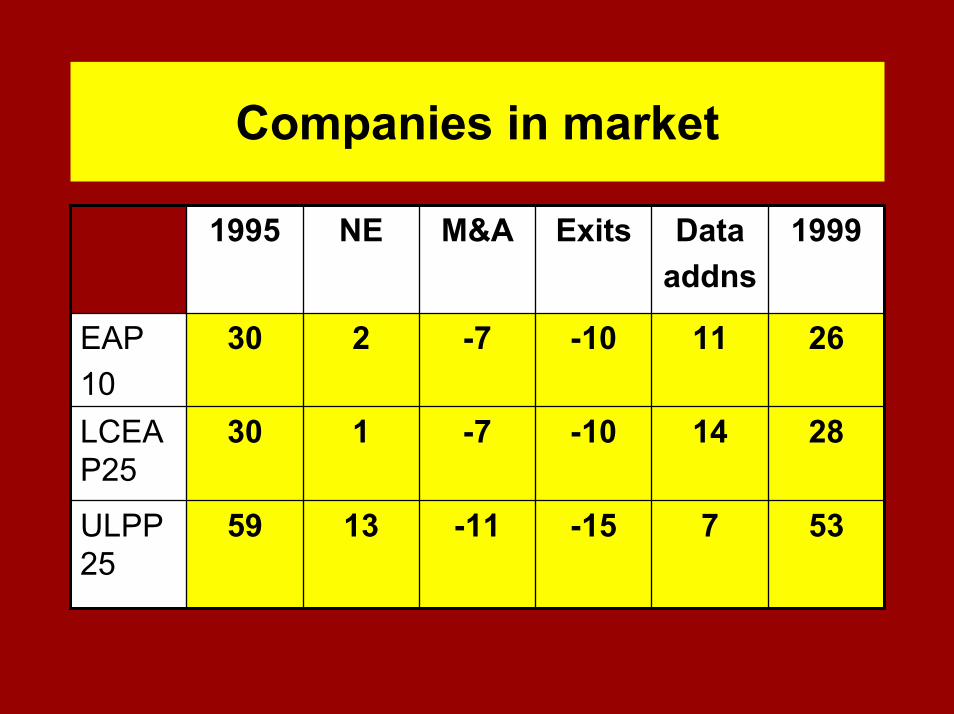

Companies in market

537-15-111359ULPP25

2814-10-7130LCEAP25

2611-10-7230EAP10

1999Dataaddns

ExitsM&ANE1995

Charges relative to average:EAP10: new entrants 95%, exiters 110%

0%20%40%60%80%

100%120%140%160%180%

New entrantsExiters

Charges relative to average:LCEAP25: new entrant 123%, exiters 116%

0%20%40%60%80%

100%120%140%160%180%200%

New entrantsExiters

Charges relative to average:ULPP25: new entrants 77%, exiters 112%

0%

20%

40%

60%

80%

100%

120%

140%

160%

New entrantsExiters

Charges pre- & post-merger:6 above line, 18 below diagonal

0

1

2

3

4

5

0 1 2 3 4 5Avge pre-merger RIY

Post

-mer

ger R

IY

EAP10LCAP25ULPP25Diagonal

Contributors to change in RIYEAP10

-0.2

-0.15

-0.1

-0.05

0

0.05

0.1

1996 1997 1998 1999

Chan

ge in

redu

ctio

n in

yie

ld (%

)

ExitsContinuersM&AsM&A consolNew entrantsData additions

Contributors to change in RIYLCEAP25

-0.2

-0.15

-0.1

-0.05

0

0.05

0.1

1996 1997 1998 1999

Chan

ge in

redu

ctio

n in

yie

ld (%

)

ExitsContinuersM&AsM&A consolNew entrantsData additions

Contributors to change in RIYULPP25

-0.2

-0.15

-0.1

-0.05

0

0.05

1996 1997 1998 1999

Chan

ge in

redu

ctio

n in

yie

ld (%

)

ExitsContinuersM&AsM&A consolNew entrantsData additions

Contributors to change in RIYTotal 1995-99

-0.4-0.35-0.3

-0.25-0.2

-0.15-0.1

-0.050

0.050.1

EAP10 LCEAP25 ULPP25

Chan

ge in

redu

ctio

n in

yie

ld (%

)

ExitsContinuersM&AsM&A consolNew entrantsData additions

Distribution channels

• What might differences in distribution channels be?

• IFA highest charges – CR/AR – Direct –No advice lowest (quality of service)

• Or the reverse (competitiveness)• Dispersion of charges: lowest for IFA

(most competitive)?

Average charges10-year with profit endowment

1

1.5

2

2.5

3

3.5

4

1995 1996 1997 1998 1999

RIY

(%) IFA

CRARDirect

Average charges25-year low cost with profit endowment

1

1.2

1.4

1.6

1.8

2

2.2

1995 1996 1997 1998 1999

RIY

(%) IFA

CRARDirect

Average charges25-year unit-linked personal pension

1

1.2

1.4

1.6

1.8

2

2.2

1995 1996 1997 1998 1999

RIY

(%) IFA

CRARDirect

Dispersion: standard deviation10-year with profit endowment

00.10.20.30.40.50.60.70.80.9

1

1995 1996 1997 1998 1999

RIY

(%) IFA

CRARDirect

Dispersion: standard deviation25-year low cost with profit endowment

00.10.20.30.40.50.60.70.80.9

1

1995 1996 1997 1998 1999

RIY

(%) IFA

CRARDirect

Dispersion: standard deviation25-year unit-linked personal pension

00.10.20.30.40.50.60.70.80.9

1

1995 1996 1997 1998 1999

RIY

(%)

IFACRARDirect

Cross-section analysis

Product data from FSA Comparative tables: charges vary with what?

Investment bonds £10000 SP57 UL, 44 WP bonds

Personal pensions £50 per month75 UL, 20 WP policies

US evidence onlong-term care pricing (JRI 1999)

Proprietary companies: lower pricesLarge companies; higher pricesNew entrants: higher pricesDistribution system: not significantLow solvency: higher prices (would

stronger insurers can charge premium for more security: how test this in UK?)

Investment bondsMultiple regression

Independent variable = charges over 10 years, as at end of period: £10000 SP

Variables = firm and product characteristics

R2 = .227 (13 variables, adjusted R2 = .111)

Significance of model = .034

Investment bonds: results

.124-Ln assets

. 091+Friendly society

.045+Proprietary

.089+Tied

.110-Direct

.057-With profits

SignificanceEffect on charges

Investment bondsInsignificant items

Min withdrawal (+), min balance (-), additional payments (-), no. of funds (-), no. of free switches (-)

Assumption of large investment amount by firms targeting more sophisticated customers

Bancassurer + (.402)

Personal pensions

Monthly premium £50R2 = .250 (11 variables, adjusted R2 =

.151)Significance of model = .009Direct significant (.026): negativeNo. of free switches (0.002): negative

i.e. high premium target market effect

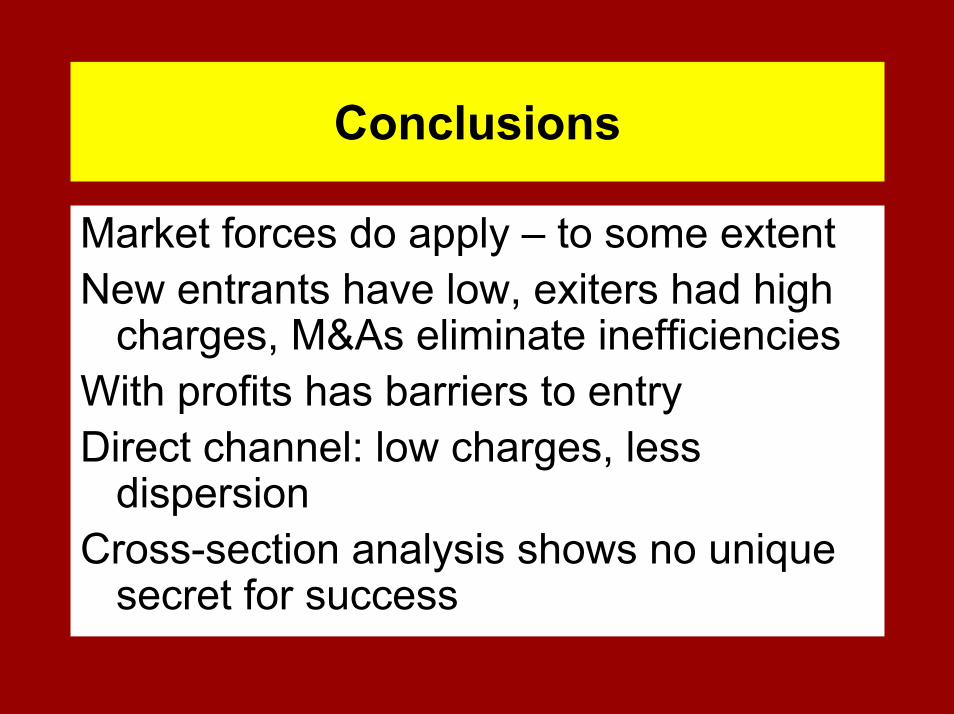

Conclusions

Market forces do apply – to some extentNew entrants have low, exiters had high

charges, M&As eliminate inefficienciesWith profits has barriers to entryDirect channel: low charges, less

dispersionCross-section analysis shows no unique

secret for success