ireland’s response to the looming world energy crisis by colin campbell aspo

Post on 19-Dec-2015

222 views

TRANSCRIPT

Ireland’s Response to the

Looming World Energy Crisis

by

Colin Campbell

ASPO

Background

1951-7 Studied geology at Oxford– PhD on Connemara geology

That started a long love affair with Ireland

1958 - Joined the oil industry– Exploration geologist in Latin America– 1972- 90 Executive, Europe, Norway

• Pioneered Irish exploration venture 1972-76

1990 Retired - if that is the word

On a mule in Colombia in 1960

Outline

• Geological background– “You have to find it first”

• Depletion is easy to grasp– Why and how self-evident reality has been

concealed and confused

• A Devastating Realisation

• Ireland’s Response

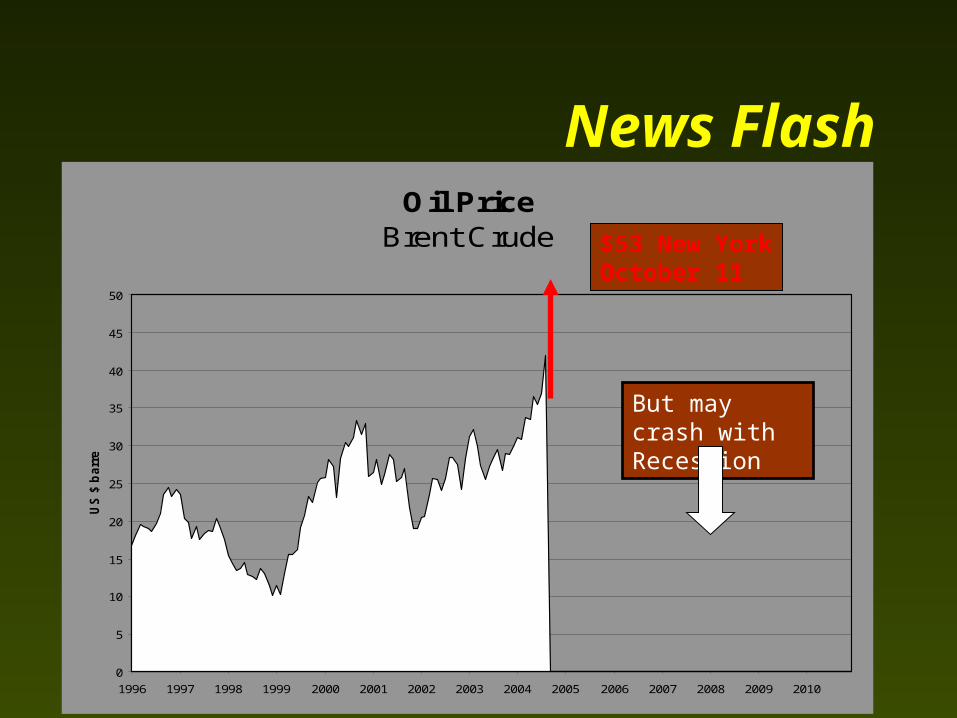

News FlashOil Price

Brent Crude

0

5

10

15

20

25

30

35

40

45

50

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

US

$ b

arr

el

$53 New York October 11

But may crash with Recession

PETROLEUM GEOLOGY

in3 Minutes

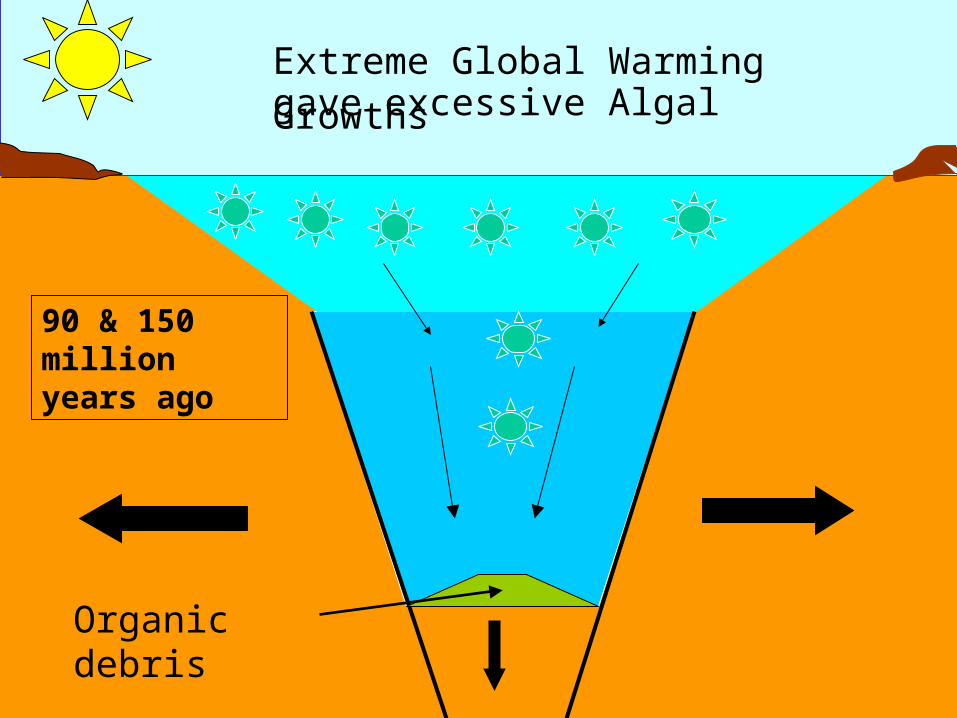

Extreme Global Warminggave excessive Algal Growths

Organic debris

90 & 150 million years ago

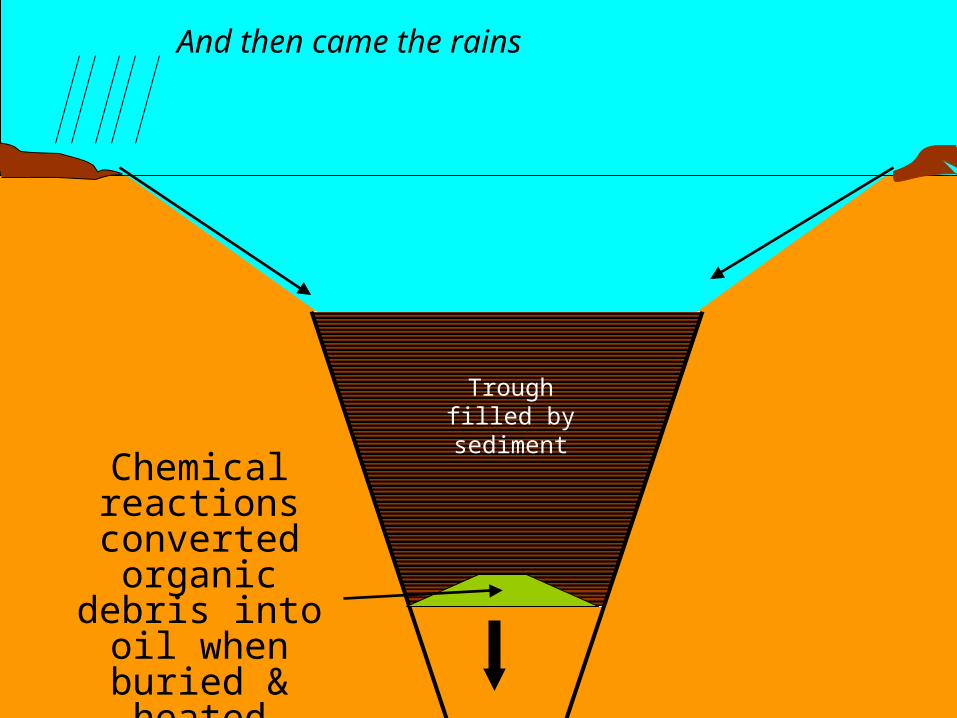

Chemical reactions converted

organic debris into oil when

buried & heated

Trough filled by sediment

And then came the rains

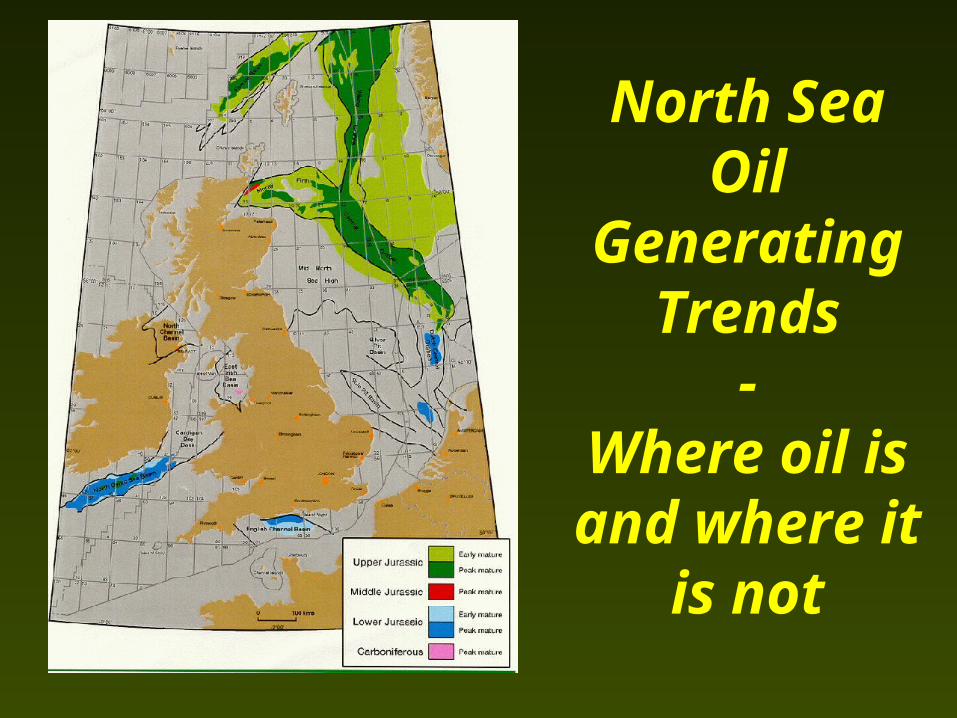

North SeaOil Generating

Trends-

Where oil is and where it is not

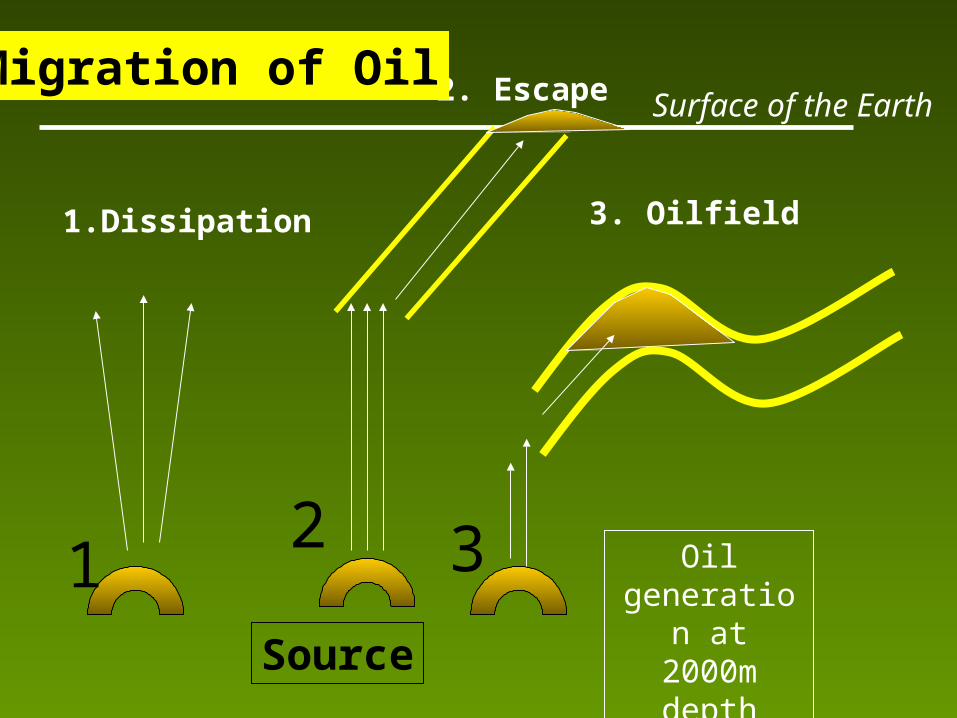

1.Dissipation

2. Escape

3. Oilfield

Source

Migration of OilSurface of the Earth

Oil generation at 2000m

depth

12 3

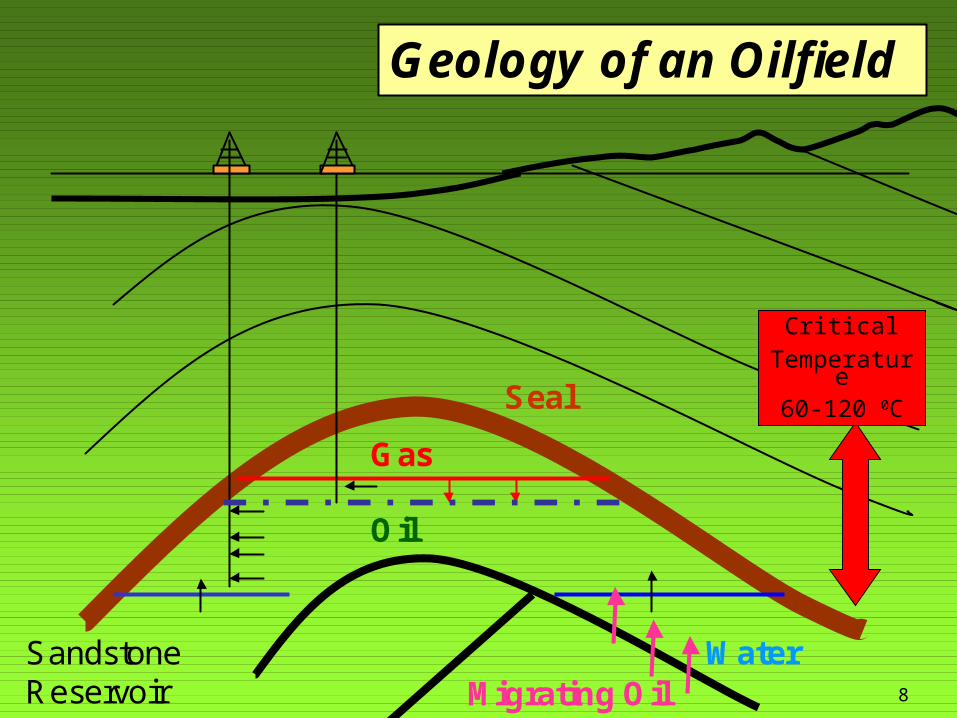

8

Oil

Gas

Water

Geology of an Oilfield

SandstoneReservoir Migrating Oil

Seal

CriticalTemperature

60-120 0C

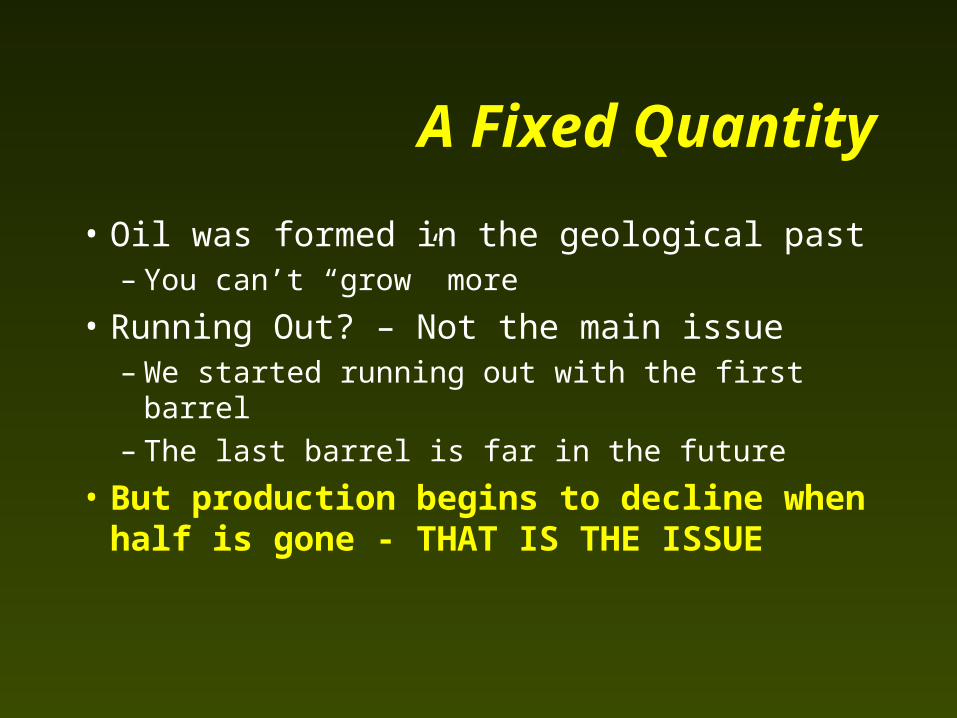

A Fixed Quantity

• Oil was formed in the geological past– You can’t “grow” more

• Running Out? – Not the main issue– We started running out with the first barrel– The last barrel is far in the future

• But production begins to decline when half is gone - THAT IS THE ISSUE

Why we need to know

Oil & Gas now dominate our lives– 40% of traded energy is oil– >90% transport fuel is oil

• Trade depends on transport

– Much electricity from gas

• Critical for agriculture– fuelling the tractor– synthetic nutrients and pesticides– pumping irrigation

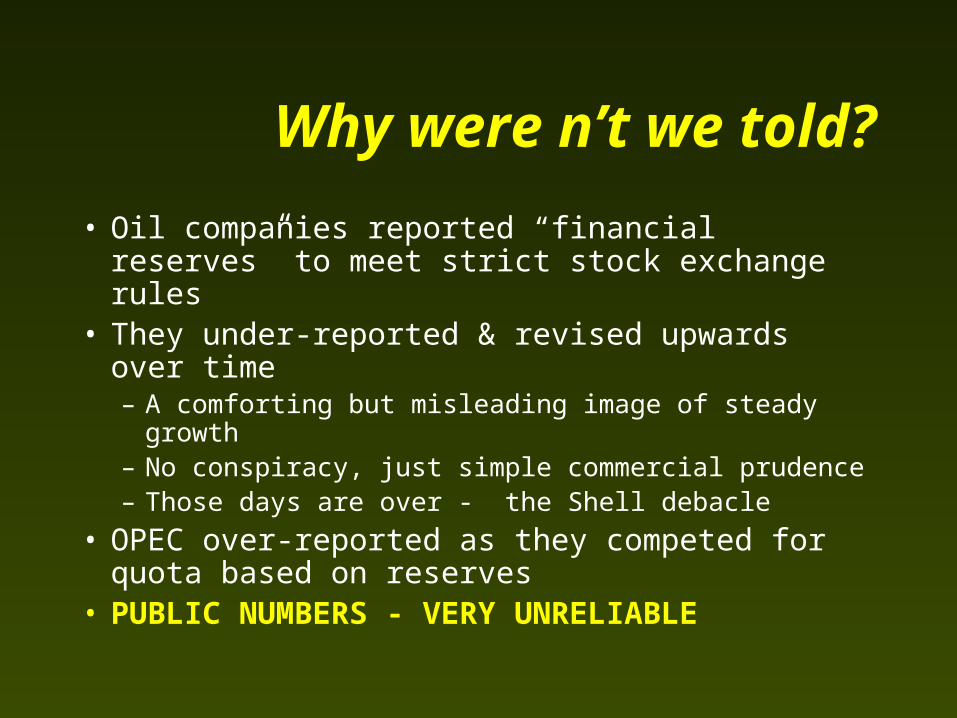

Why were n’t we told?

• Oil companies reported “financial reserves” to meet strict stock exchange rules

• They under-reported & revised upwards over time– A comforting but misleading image of steady growth– No conspiracy, just simple commercial prudence– Those days are over - the Shell debacle

• OPEC over-reported as they competed for quota based on reserves

• PUBLIC NUMBERS - VERY UNRELIABLE

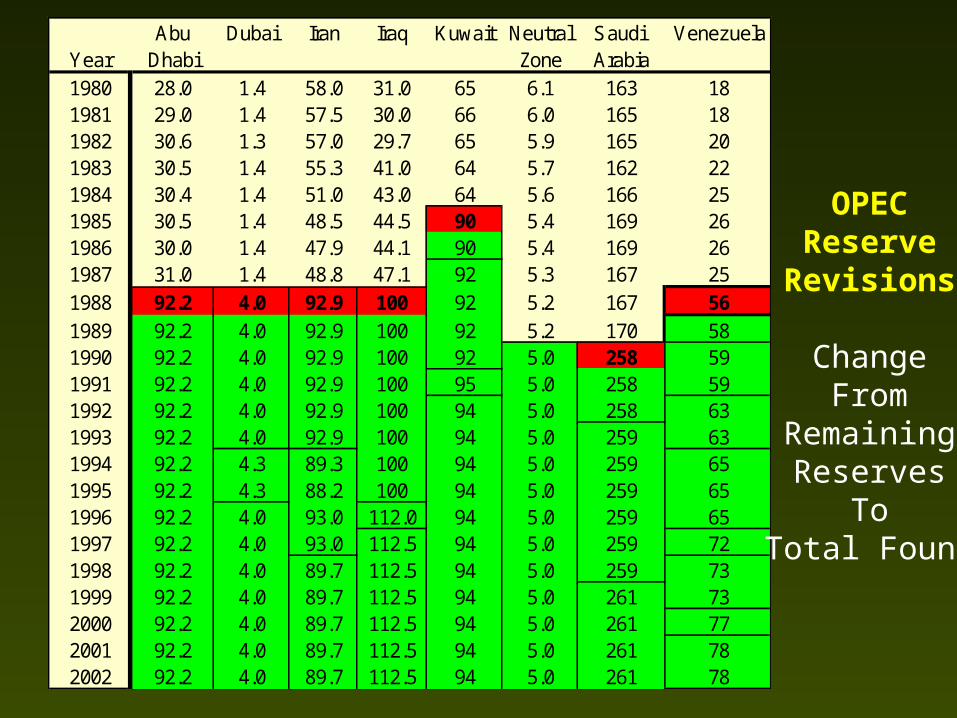

Abu Dubai Iran Iraq Kuwait Neutral Saudi VenezuelaYear Dhabi Zone Arabia1980 28.0 1.4 58.0 31.0 65 6.1 163 181981 29.0 1.4 57.5 30.0 66 6.0 165 181982 30.6 1.3 57.0 29.7 65 5.9 165 201983 30.5 1.4 55.3 41.0 64 5.7 162 221984 30.4 1.4 51.0 43.0 64 5.6 166 251985 30.5 1.4 48.5 44.5 90 5.4 169 261986 30.0 1.4 47.9 44.1 90 5.4 169 261987 31.0 1.4 48.8 47.1 92 5.3 167 251988 92.2 4.0 92.9 100 92 5.2 167 561989 92.2 4.0 92.9 100 92 5.2 170 581990 92.2 4.0 92.9 100 92 5.0 258 591991 92.2 4.0 92.9 100 95 5.0 258 591992 92.2 4.0 92.9 100 94 5.0 258 631993 92.2 4.0 92.9 100 94 5.0 259 631994 92.2 4.3 89.3 100 94 5.0 259 651995 92.2 4.3 88.2 100 94 5.0 259 651996 92.2 4.0 93.0 112.0 94 5.0 259 651997 92.2 4.0 93.0 112.5 94 5.0 259 721998 92.2 4.0 89.7 112.5 94 5.0 259 731999 92.2 4.0 89.7 112.5 94 5.0 261 732000 92.2 4.0 89.7 112.5 94 5.0 261 772001 92.2 4.0 89.7 112.5 94 5.0 261 782002 92.2 4.0 89.7 112.5 94 5.0 261 78

OPECReserve

Revisions

ChangeFrom

RemainingReserves

ToTotal Found

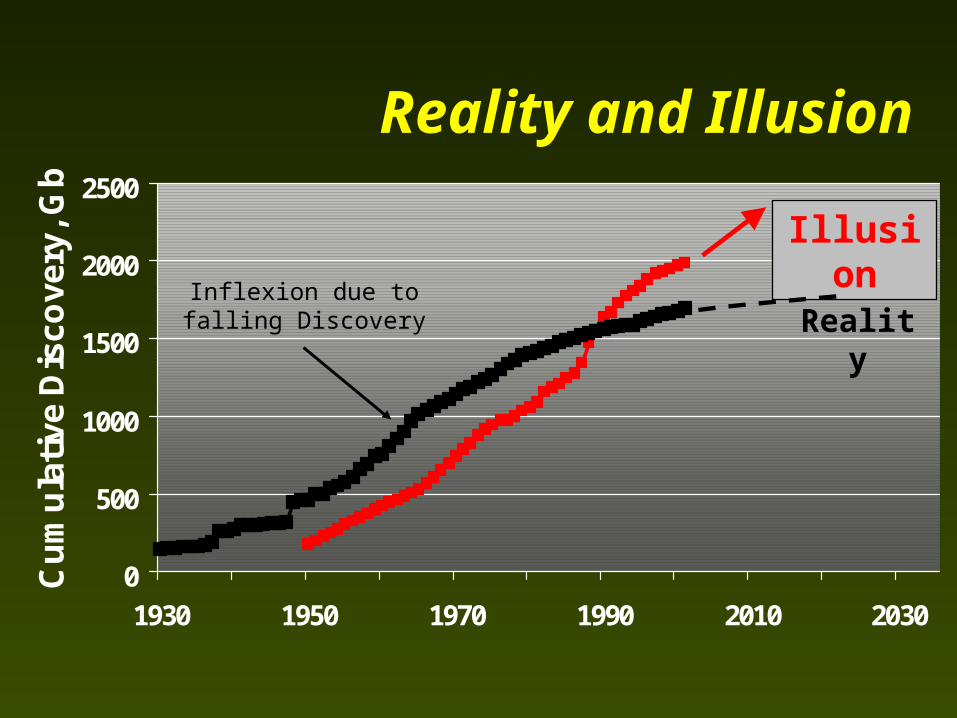

Reality and Illusion

0

500

1000

1500

2000

2500

1930 1950 1970 1990 2010 2030

Cu

mu

lati

ve D

isco

very

, Gb

Inflexion due tofalling Discovery Reality

Illusion

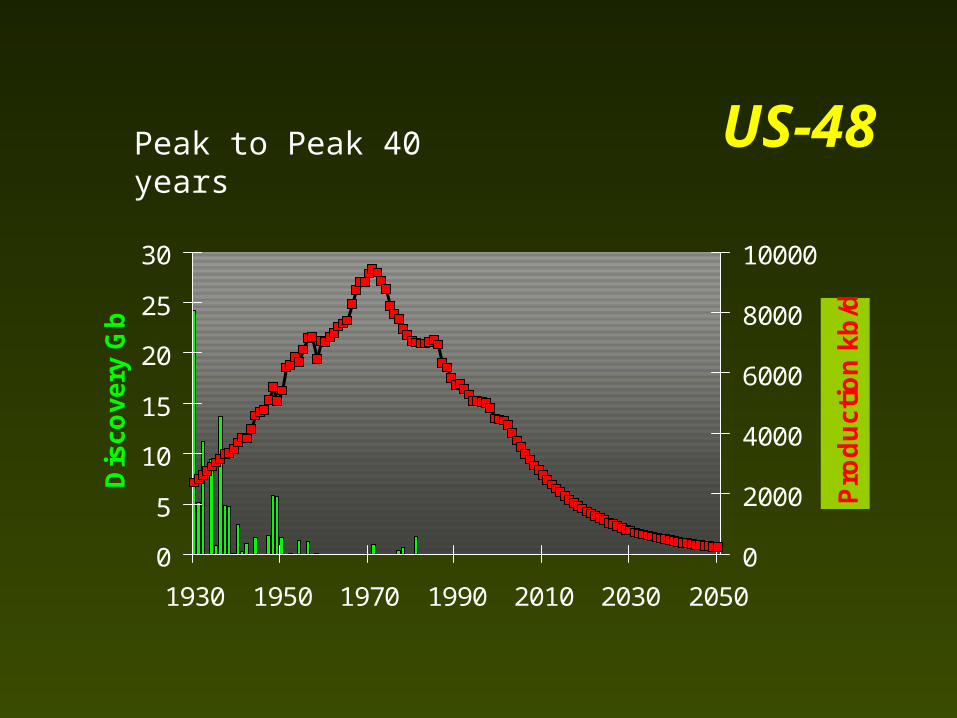

US-48

0

5

10

15

20

25

30

1930 1950 1970 1990 2010 2030 2050

Dis

co

ve

ry G

b

0

2000

4000

6000

8000

10000

Pro

du

cti

on

kb

/d

Peak to Peak 40 years

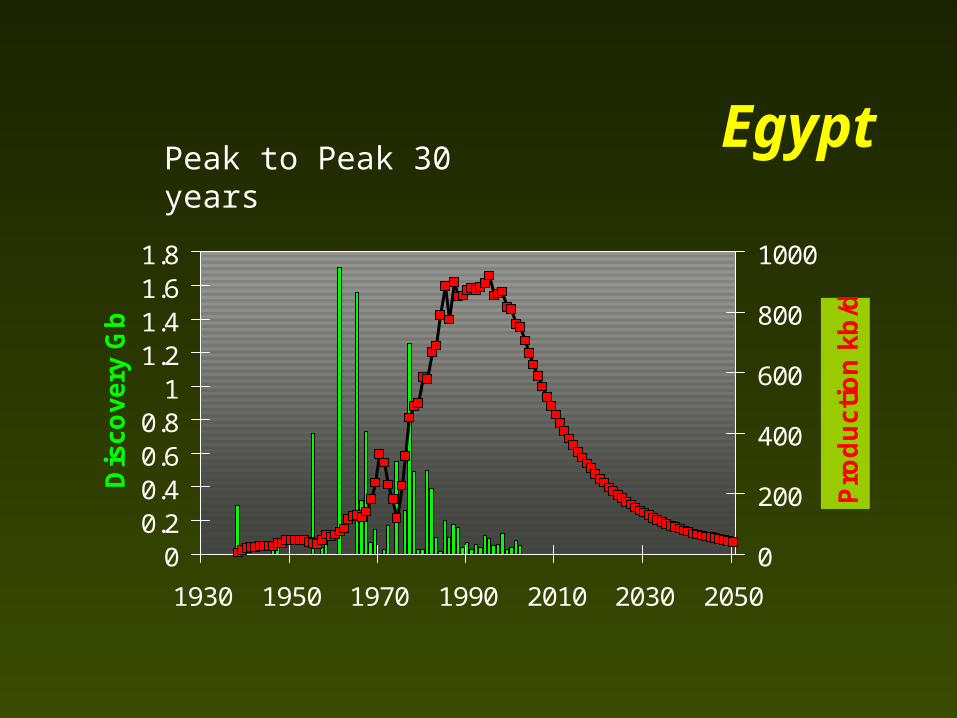

Egypt

00.20.40.60.8

11.21.41.61.8

1930 1950 1970 1990 2010 2030 2050

Dis

co

ve

ry G

b

0

200

400

600

800

1000

Pro

du

cti

on

kb

/d

Peak to Peak 30 years

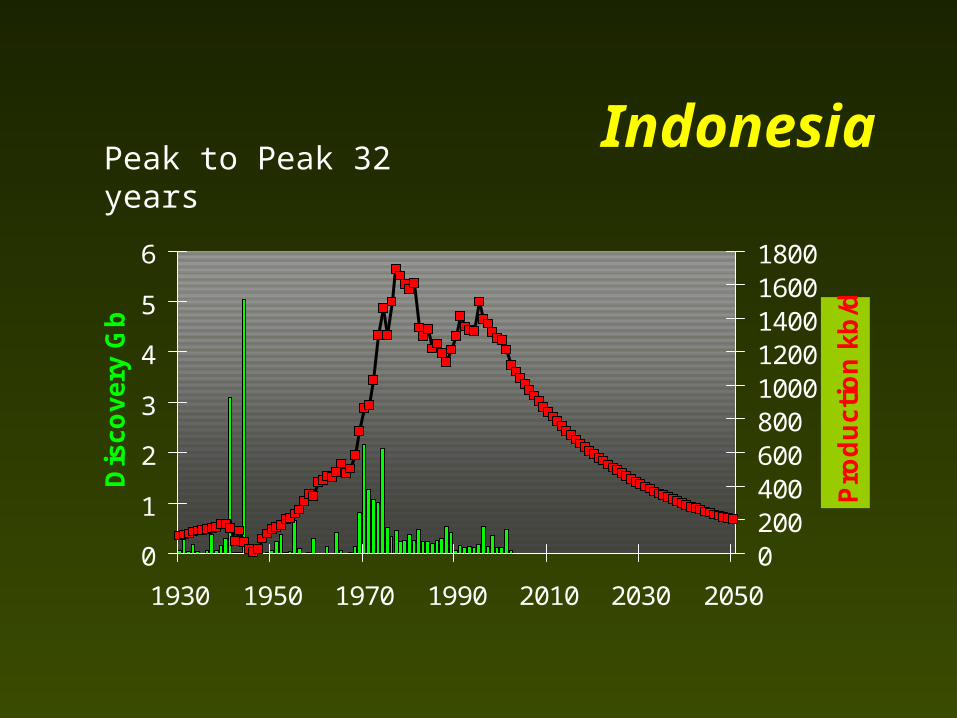

Indonesia

0

1

2

3

4

5

6

1930 1950 1970 1990 2010 2030 2050

Dis

co

ve

ry G

b

020040060080010001200140016001800

Pro

du

cti

on

kb

/d

Peak to Peak 32 years

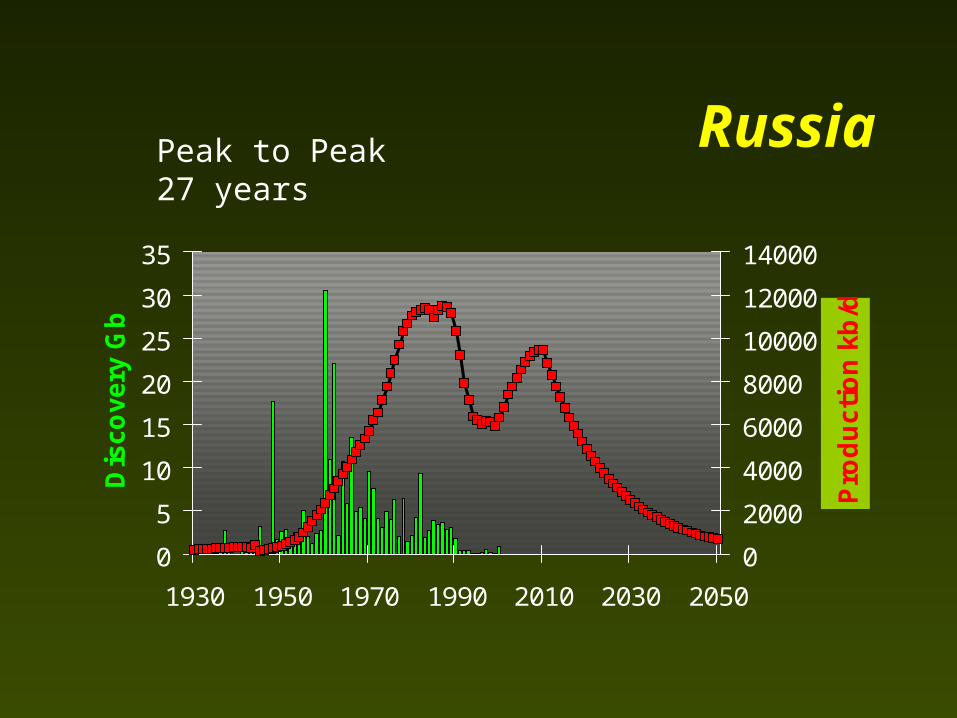

Russia

0

5

10

15

20

25

30

35

1930 1950 1970 1990 2010 2030 2050

Dis

co

ve

ry G

b

0

2000

4000

6000

8000

10000

12000

14000

Pro

du

cti

on

kb

/d

Peak to Peak 27 years

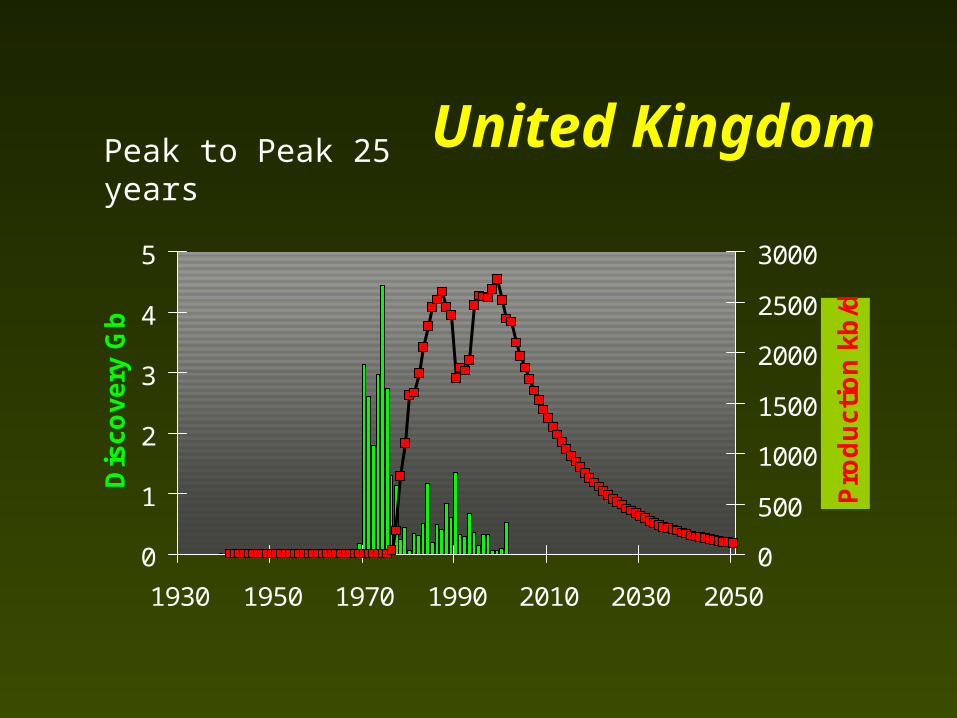

United Kingdom

0

1

2

3

4

5

1930 1950 1970 1990 2010 2030 2050

Dis

co

ve

ry G

b

0

500

1000

1500

2000

2500

3000

Pro

du

cti

on

kb

/d

Peak to Peak 25 years

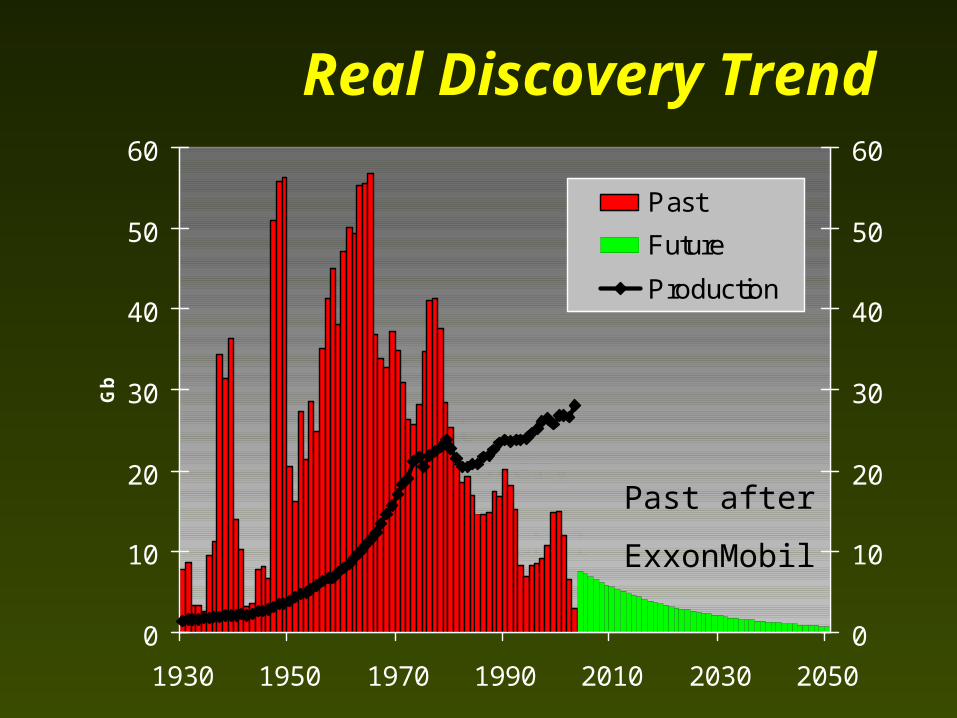

Real Discovery Trend

Past discovery by ExxonMobil

0

10

20

30

40

50

60

1930 1950 1970 1990 2010 2030 2050

Gb

0

10

20

30

40

50

60

Past

Future

Production

Past after

ExxonMobil

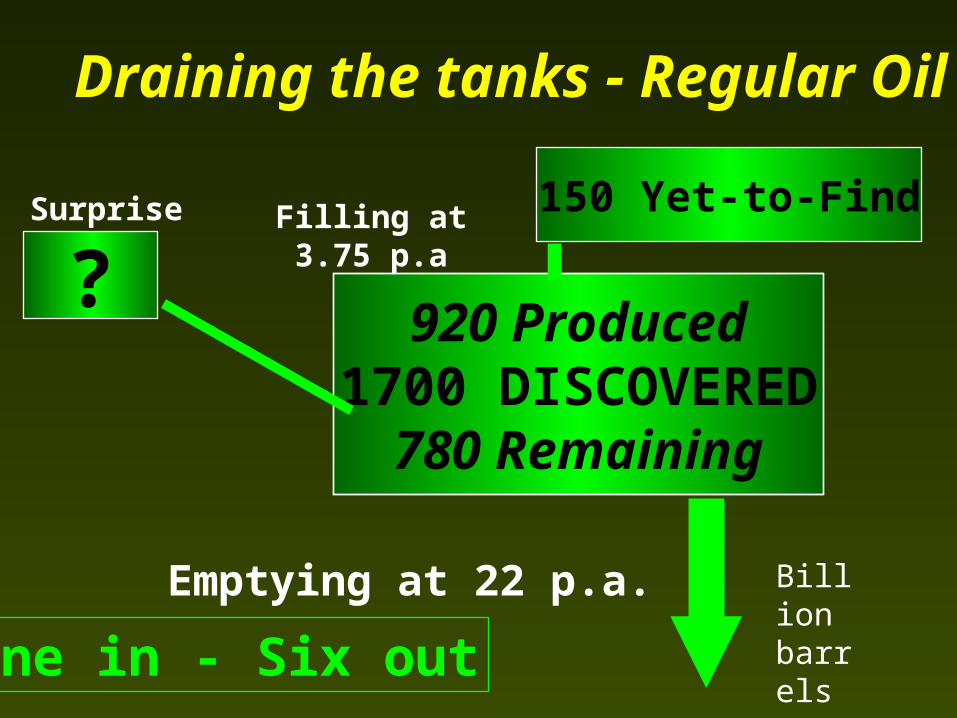

Draining the tanks - Regular Oil

150 Yet-to-Find

920 Produced1700 DISCOVERED

780 Remaining

?Filling at 3.75 p.a

Emptying at 22 p.a.

One in - Six out

Surprise

Billion barrels

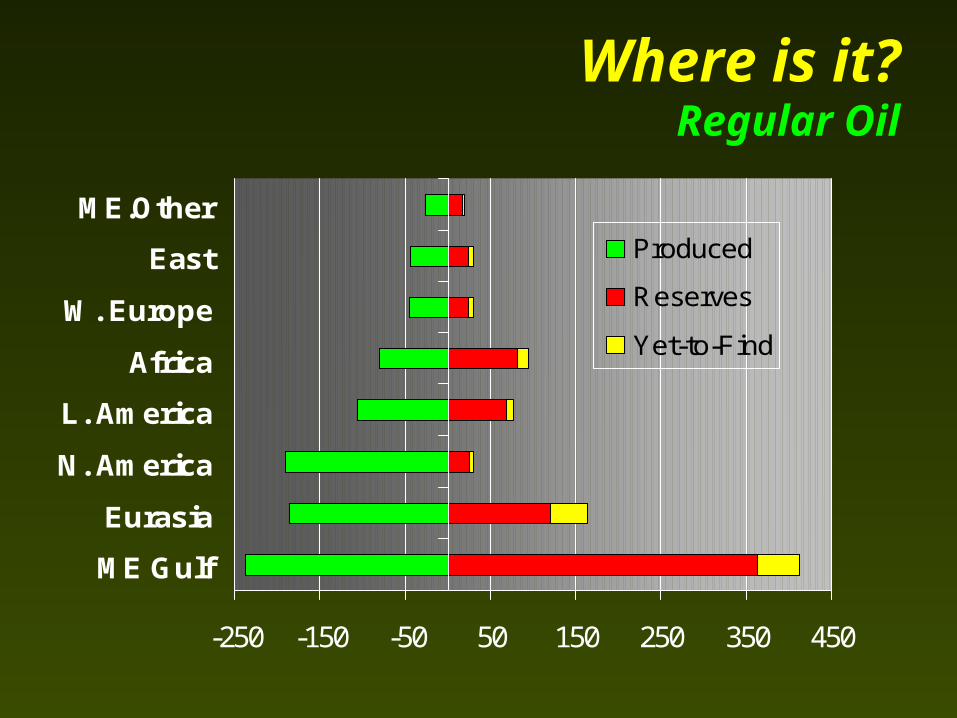

Where is it?Regular Oil

-250 -150 -50 50 150 250 350 450

ME Gulf

Eurasia

N. America

L. America

Africa

W. Europe

East

ME.Other

Produced

Reserves

Yet-to-Find

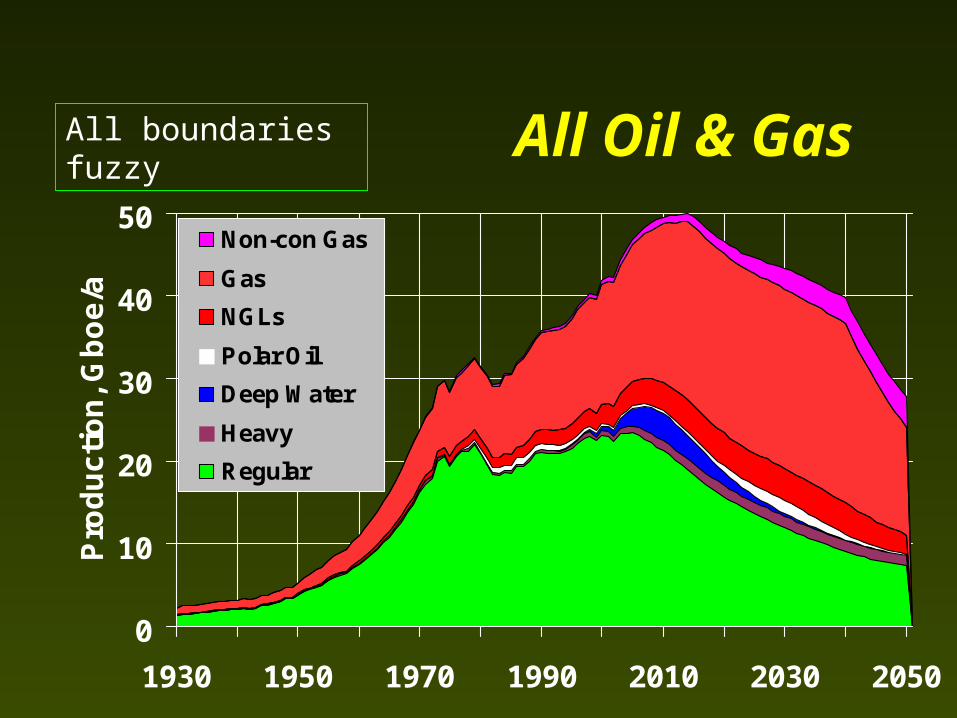

All Oil & Gas

0

10

20

30

40

50

1930 1950 1970 1990 2010 2030 2050

Pro

du

cti

on

, G

bo

e/a

Non-con Gas

Gas

NGLs

Polar Oil

Deep Water

Heavy

Regular

All boundaries fuzzy

The Devastating Realisation

So, oil will soon be in terminal decline

• Gas follows a few years later

• Colossal Impact – Economy - stockmarket crash inevitable– Society– Politics– Environment

• We are totally unprepared

End of the First Half of Oil Age

• First half lasted 150 years, stimulating– Industry– Transport & trade– Agriculture & people– Growth of financial capital

• Second Half dawns, meaning decline of oil– And all that depends on it– Including Financial Capital

• Spelling Recession - Depression

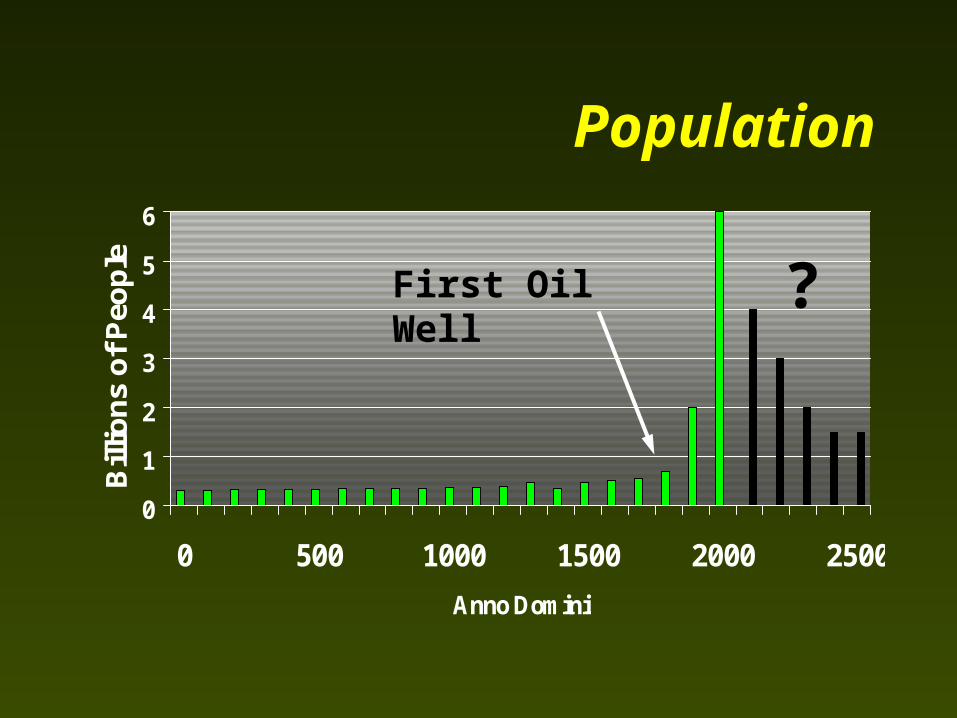

Population

0

1

2

3

4

5

6

0 500 1000 1500 2000 2500

Anno Domini

Bill

ion

s o

f P

eop

le

First Oil Well ?

But World begins to wake up

• This has been evident for years but denied– We faced malign influence of Economists with

outdated principles and practices – Now at last, high prices force admission by

• World Energy Council• International Energy Agency - obliquely• Even BP (long bent on denial) now confesses

• US prefers military conquest of oil to cutting excessive demand

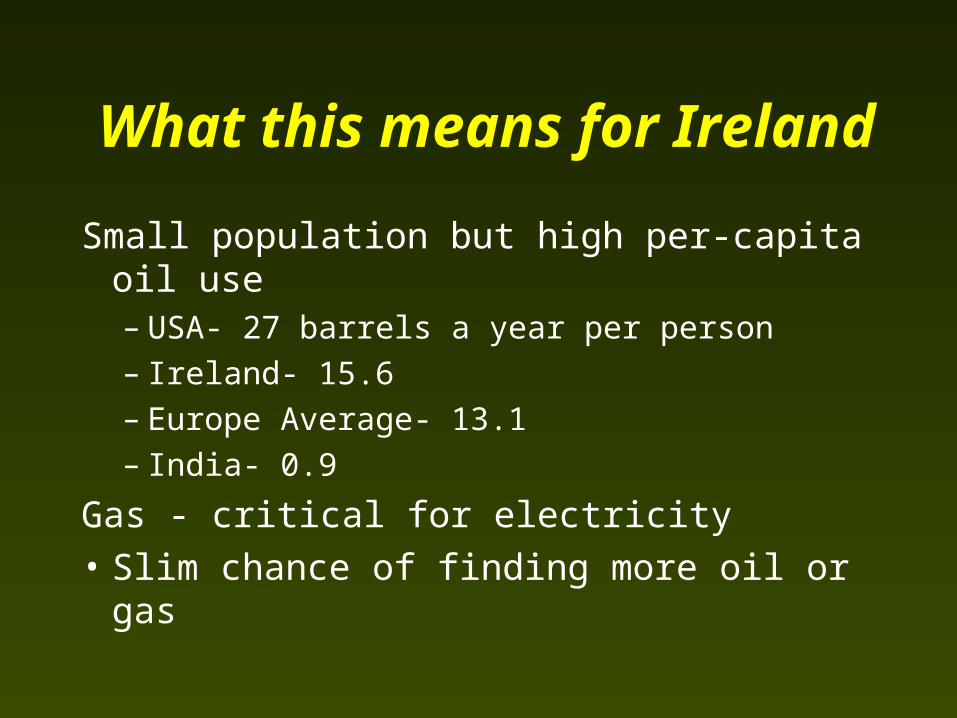

What this means for Ireland

Small population but high per-capita oil use– USA- 27 barrels a year per person– Ireland- 15.6 – Europe Average- 13.1– India- 0.9

Gas - critical for electricity

• Slim chance of finding more oil or gas

Ireland’s Electricity

• Priority in the early days of the Republic– Shannon Hydro-electric scheme– Rural electrification by ESB

• Electricity came to Ballydehob in 1951

• It was a National Priority

• But then the CELTIC TIGER stalked in by dead of night & sold out to the Market

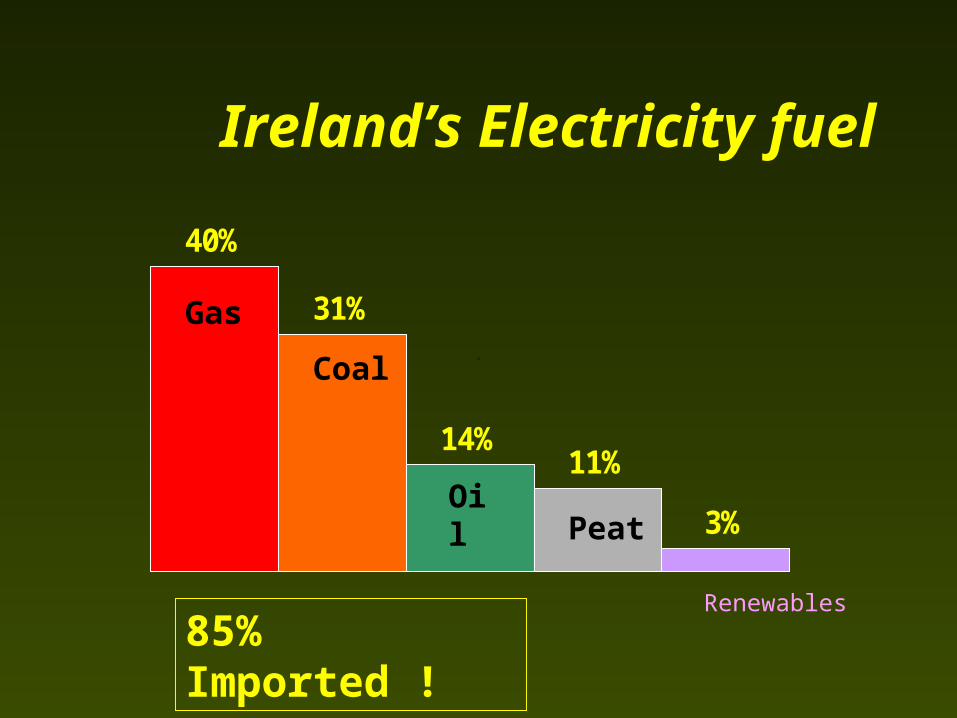

Ireland’s Electricity fuel

40%

31%

14%11%

3%

Gas0.4

0.310.140.110.03

Coal

OilPeat

Renewables

85% Imported !

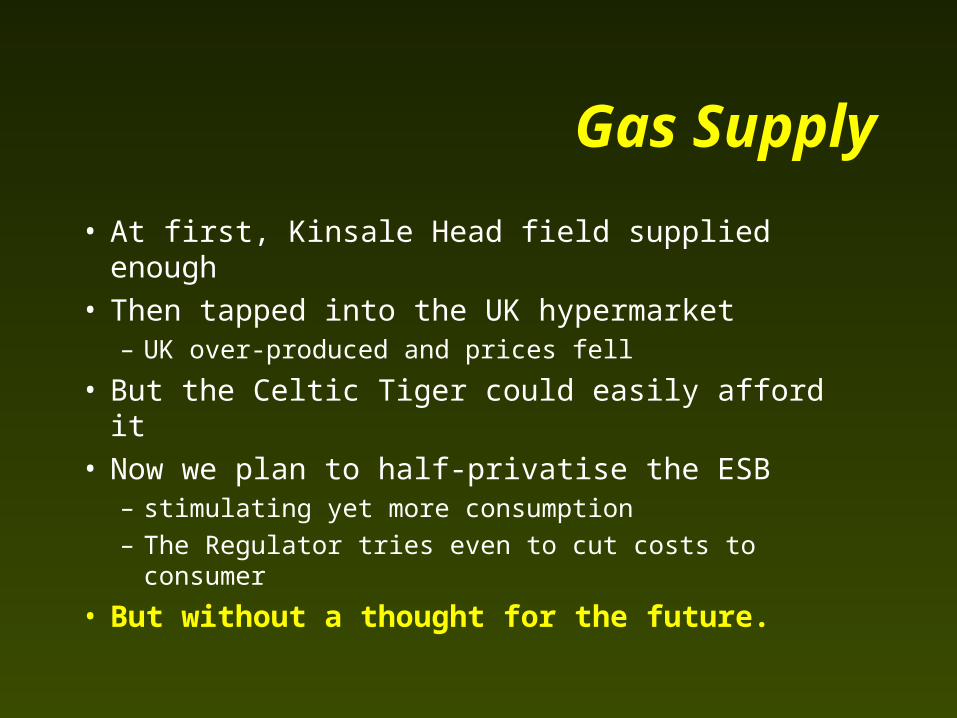

Gas Supply

• At first, Kinsale Head field supplied enough• Then tapped into the UK hypermarket

– UK over-produced and prices fell

• But the Celtic Tiger could easily afford it• Now we plan to half-privatise the ESB

– stimulating yet more consumption

– The Regulator tries even to cut costs to consumer

• But without a thought for the future.

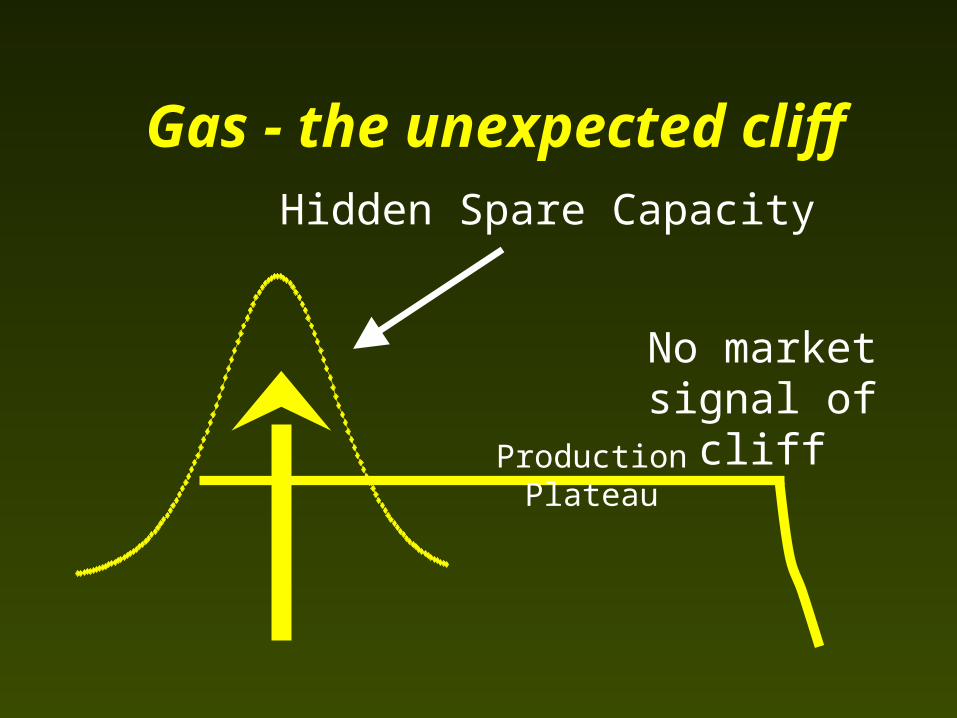

Gas - the unexpected cliff Hidden Spare Capacity

No market signal of cliff

Production Plateau

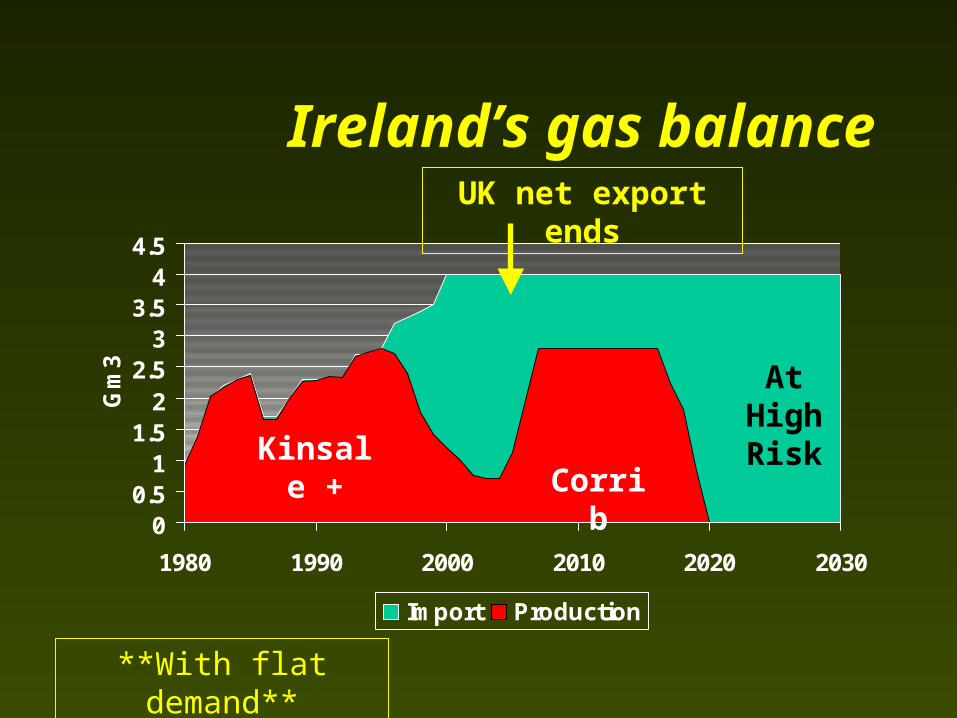

Ireland’s gas balance

00.5

11.5

22.5

33.5

44.5

1980 1990 2000 2010 2020 2030

Gm

3

Import Production

Kinsale + Corrib

UK net export ends

**With flat demand**

At HighRisk

Where will gas come from ?

• Britain becomes a net importer - from• Norway• Siberia• Central Asia, Middle East, N. Africa…….

• Many hungry transit countries in between– Ireland at the end of the line

• Will Britain re-export to Ireland ?– When she needs all she can get – and at what price?

A Grave Crisis in the Making

• This is a major crisis in the making– the lights will go out unless something is done– An economic recession affecting everyone

• The Government seems blissfully ignorant– Misplaced faith that the market must deliver– Relies on bad advice form IEA, EU

• It needs to use the short time left to prepare• Everyone needs to know and contribute

Plan of Action

• Fund a small office to study properly

• Launch a programme of public education

• Don’t wait for Brussels– It is an investment giving Ireland a strong

competitive edge

• Take a lead in a World Depletion Protocol• Back the 2005 Lisbon Initiative

Solution-1 : Stop wasteDomestic and industrial energy audits

– Charges to penalise waste & reward savings.• A modest cheap ration but high price for excess

– Better insulation & industrial heat recovery – Disallow energy costs as a charge against tax

• Stop tax-free aviation fuel

– More public transport

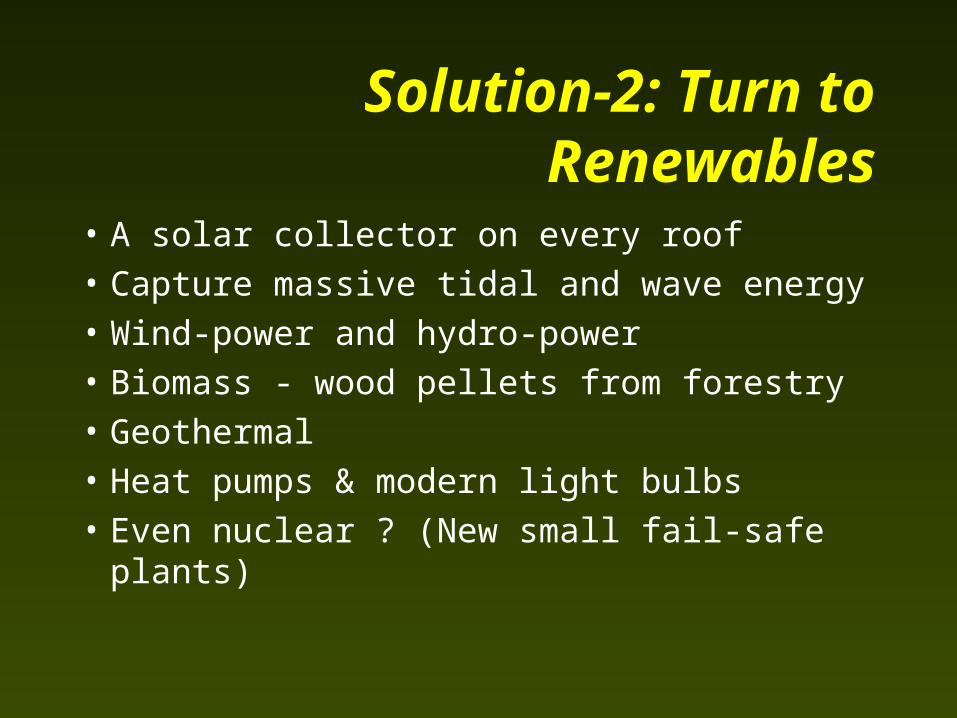

Solution-2: Turn to Renewables

• A solar collector on every roof

• Capture massive tidal and wave energy

• Wind-power and hydro-power

• Biomass - wood pellets from forestry

• Geothermal

• Heat pumps & modern light bulbs

• Even nuclear ? (New small fail-safe plants)

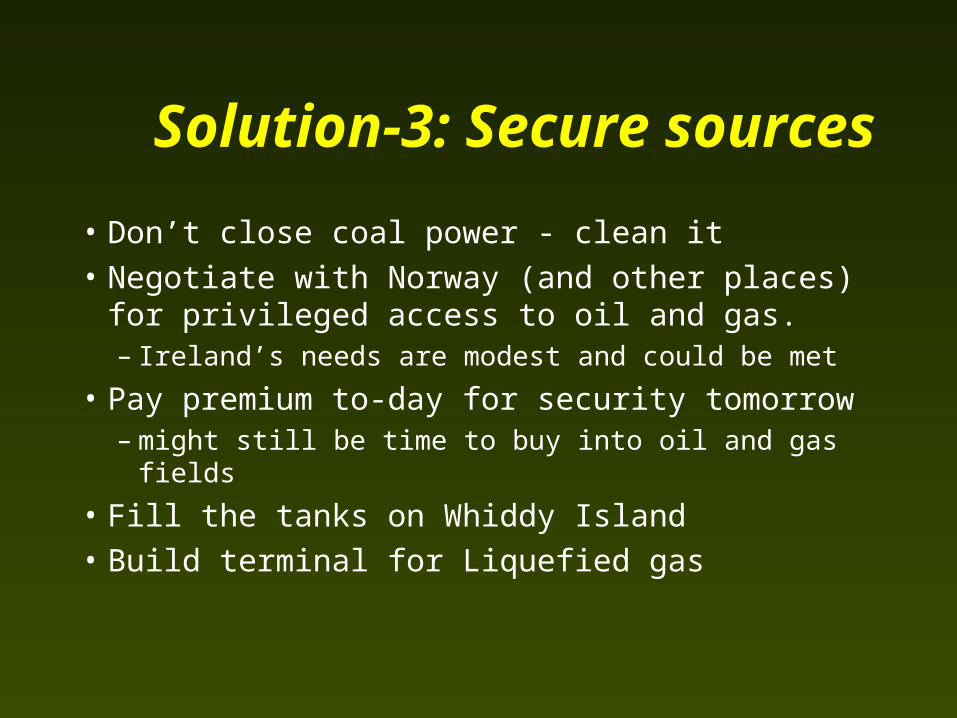

Solution-3: Secure sources

• Don’t close coal power - clean it

• Negotiate with Norway (and other places) for privileged access to oil and gas. – Ireland’s needs are modest and could be met

• Pay premium to-day for security tomorrow– might still be time to buy into oil and gas fields

• Fill the tanks on Whiddy Island

• Build terminal for Liquefied gas

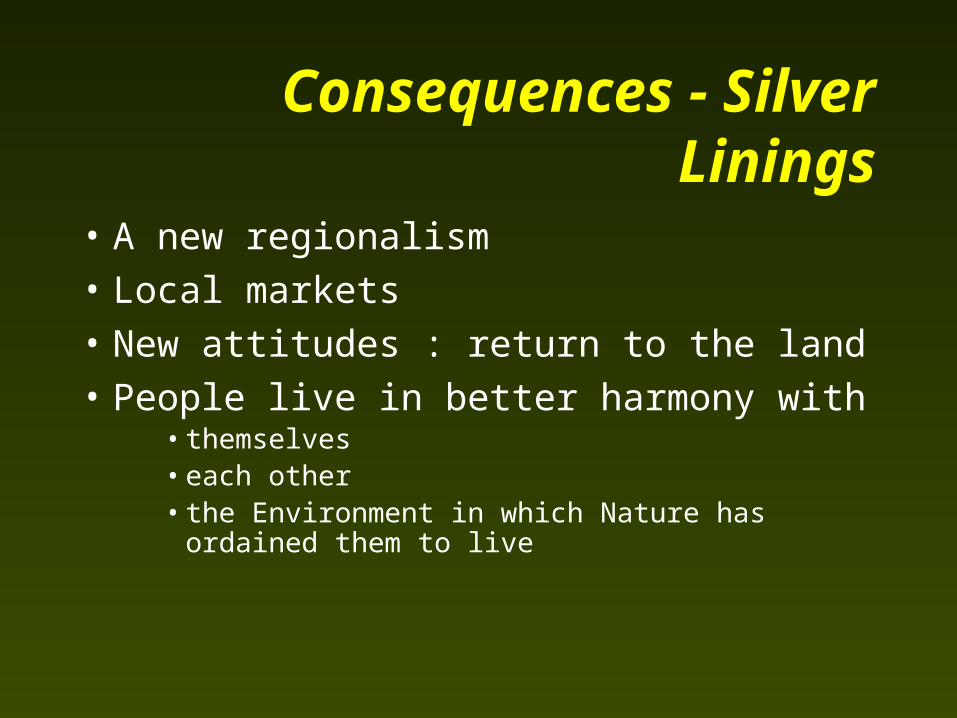

Consequences - Silver Linings

• A new regionalism

• Local markets

• New attitudes : return to the land

• People live in better harmony with• themselves• each other• the Environment in which Nature has ordained them

to live

The Celtic Fox thrives in Ireland: The Tiger belongs to the Zoo