investor presentation -...

TRANSCRIPT

Confidential

September 2017

Investor Presentation

Grupo Traxion, S.A.B. de C.V.

2

Content

(Top Alignment)

2.30

Subtitles

(bottom alignment) 2.62

Page Titles

3.09

Page Content

Left Alignment

4.60

Page Content

Right Alignment

4.60

Content

(Bottom Alignment)

3.00

Footnotes

(Top Alignment)

3.15

#0

#74

#130

#207

#223

#0

#119

#147

#60

#194

#199

#205

#75

#172

#198

#247

#150

#70

#101

#100

#106

Disclaimer

The material that follows presents general background information about Grupo Traxion, S.A.B. de C.V. (the “Company”) as of the date of the presentation. This information

consists of information concerning the Company. It is information in summary form and does not purport to be complete. It is not intended to be relied upon as advice to

potential investors and does not form the basis for an informed investment decision. This presentation is strictly confidential and may not be disclosed to any other person.

The information in this presentation is preliminary in nature and subject to change. No representation or warranty, express or implied, is made concerning, and no reliance

should be placed on, the accuracy, fairness or completeness of the information presented herein. All information in this presentation is subject to verification, correction,

completion and change without notice. In giving this presentation, none of the Company, any of its affiliates, directors, officers, agents or employees, nor any placement

agents, managers or initial purchasers undertake any obligation to provide the recipient with access to any additional information or to update this presentation or any

information or to correct any inaccuracies in any such information.

This presentation may contain statements that are forward-looking. Such forward-looking statements are only predictions and are not guarantees of future performance.

Investors are cautioned that any such forward-looking statements are and will be, as the case may be, subject to many risks, uncertainties and factors relating to the

operations and business environments of the Company and its subsidiaries that may cause the actual results of the Company to be materially different from any future results

expressed or implied in such forward-looking statements. None of the Company, any of its affiliates, directors, officers, agents or employees, nor any placement agents,

managers or initial purchasers, shall be liable to any third party (including investors) for any investment or business decision made or action taken in reliance on the information

and statements contained in this presentation or for any consequential, special or similar damages.

Securities may not be offered or sold in the United States unless they are registered or exempt from registration under the U.S. Securities Act of 1933, as amended (the

“Securities Act”). This presentation is being made only to investors that, by means of their attendance at this presentation, represent that they are “qualified institutional

buyers” as that term is defined in Rule 144A under the Securities Act. Any offering of securities to be made outside of Mexico will be made by means of an offering

memorandum that will be sent to you at the address that you provided today. Such offering memorandum will contain, or incorporate by reference, detailed

information about the Company and its business and financial results, as well as its financial statements. Investment decisions should be solely made on the

basis of the offering memorandum and not on the basis of this presentation.

This presentation does not constitute an offer, or an invitation or solicitation for an offer, to subscribe for or purchase any securities, nor shall any part of it nor the fact of its

dissemination form part of or be relied on in connection with any contract or investment decision relating thereto. Neither this presentation nor anything contained herein shall

form the basis of any contract or commitment. If the Company should at any time commence an offering of securities, any decision to invest in such offer to subscribe for or

acquire securities of the Company must be based wholly on the information contained in the offering memorandum to be issued by the Company in connection with any such

offer and not on the contents hereof.

By attending this presentation, you agree to be bound by terms and conditions set out above.

3

Content

(Top Alignment)

2.30

Subtitles

(bottom alignment) 2.62

Page Titles

3.09

Page Content

Left Alignment

4.60

Page Content

Right Alignment

4.60

Content

(Bottom Alignment)

3.00

Footnotes

(Top Alignment)

3.15

#0

#74

#130

#207

#223

#0

#119

#147

#60

#194

#199

#205

#75

#172

#198

#247

#150

#70

#101

#100

#106

16x Fleet growth

over the last 6 years

Traxion – The Mexican Ground Transportation Platform

Notes:

1. According to T21 Magazine (December 2016) and public filings of companies in the ground transportation industry

2. Average pro-forma units for 2016 (includes Egoba, MyM, Grupo SID, LIPU and AFN); 4,621 owned and 342 leased power units

3. Pro-forma figures as of 2016 include revenues or Adjusted EBITDA, respectively, of Grupo SID and LIPU for the full year and exclude 2016 Revenues or Adjusted EBITDA, respectively, of AFN prior to its acquisition; converted using 2016 average exchange rate of Ps$18.66 per US$ according to Banxico

4. Calculated as per audited financials

We believe we are the first and only

ground transportation and logistics

consolidator in Mexico

We operate through two

complementary business segments

Broad portfolio of services providing

a one-stop solution

Unique success story evolving into the largest company

in the Mexican ground transportation and logistics

industry(1) with an owned fleet of 4,963(2) power units

− Cargo Transportation and Logistics

(“Cargo & Logistics”)

− Contracted Personnel and Student

Transportation (“Contracted

Passenger Services”)

+345 MM kms driven per year

(214 million miles)

Nationwide Presence

+9,500 Employees

~US$329MM(3)

in Revenues

131.8% Revenue growth(4) over

the last 2 years

4 companies acquired

over the last 6 years

+900 Customers

Adjusted EBITDA of

~US$64MM(3)

4

Content

(Top Alignment)

2.30

Subtitles

(bottom alignment) 2.62

Page Titles

3.09

Page Content

Left Alignment

4.60

Page Content

Right Alignment

4.60

Content

(Bottom Alignment)

3.00

Footnotes

(Top Alignment)

3.15

#0

#74

#130

#207

#223

#0

#119

#147

#60

#194

#199

#205

#75

#172

#198

#247

#150

#70

#101

#100

#106

Snapshot of Segment Overview

Cargo & Logistics Contracted Passenger Services

One of the largest Cargo & Logistics service providers in Mexico

with the broadest array of service offerings

Cargo transportation services are offered on a spot or dedicated

basis

Notes:

1. Year average (2016)

2. Pro-forma, includes Egoba, MyM, Grupo SID and AFN; owned fleet

3. 3,057 power units are owned and 342 are leased

Largest contracted personnel and student

transportation platform in the country with

unmatched scale and regional reach

Dedicated service

Power units(1)(2)

5.4 Avg. fleet age

vs. 16.6 in the

industry

290k sqm of

warehousing

facilities

Power units(1)(3)

6.0 Avg. fleet age

Dry vans

Distribution and moving

International cargo

Logistics and distribution

International cargo and intermodal

Contracted Personnel and Student Transportation

1,564 3,046 3,399

Source: Company information, SCT

5

Content

(Top Alignment)

2.30

Subtitles

(bottom alignment) 2.62

Page Titles

3.09

Page Content

Left Alignment

4.60

Page Content

Right Alignment

4.60

Content

(Bottom Alignment)

3.00

Footnotes

(Top Alignment)

3.15

#0

#74

#130

#207

#223

#0

#119

#147

#60

#194

#199

#205

#75

#172

#198

#247

#150

#70

#101

#100

#106

History of Growth and Excellence for +65 Years

1952

Proven strategy to deliver profitable growth through organic expansion and M&A

Average fleet size (# of power units)

Lijtszain Family

(Founders)

Founded Muebles y

Mudanzas ("MyM") in 1952

2011 2012 2013 2015 2016 2014

776

4,963

760

752

316 300

Capital raise and

partnership to create

Acquisition of Egoba,

adding 300 units

Acquisition of Lipu,

adding 3,399 units

Acquisition of Grupo Mudancero

(MyM), adding 428 units

Acquisition of Grupo

SID, adding 580 units

Acquisition of AFN,

adding 222 units

'11-'16 Fleet CAGR: 75.3%

Capital Raise

Capital Raise

PROCEEDS

IPO

6

Content

(Top Alignment)

2.30

Subtitles

(bottom alignment) 2.62

Page Titles

3.09

Page Content

Left Alignment

4.60

Page Content

Right Alignment

4.60

Content

(Bottom Alignment)

3.00

Footnotes

(Top Alignment)

3.15

#0

#74

#130

#207

#223

#0

#119

#147

#60

#194

#199

#205

#75

#172

#198

#247

#150

#70

#101

#100

#106

Traxion: An Attractive Investment Opportunity

1

2

3

4

5

6

7

Largest ground transportation services and logistics company

in Mexico with strong industry fundamentals

Nationwide presence with focus on the fastest growing regions in

the country

Diversified and resilient business model

Best-in-class platform designed for growth

Track-record of disciplined acquisitions and successful

integration

Proven history of profitable growth

Experienced management team with strong corporate governance

and sophisticated shareholder base

SMART SPEED

7

Content

(Top Alignment)

2.30

Subtitles

(bottom alignment) 2.62

Page Titles

3.09

Page Content

Left Alignment

4.60

Page Content

Right Alignment

4.60

Content

(Bottom Alignment)

3.00

Footnotes

(Top Alignment)

3.15

#0

#74

#130

#207

#223

#0

#119

#147

#60

#194

#199

#205

#75

#172

#198

#247

#150

#70

#101

#100

#106

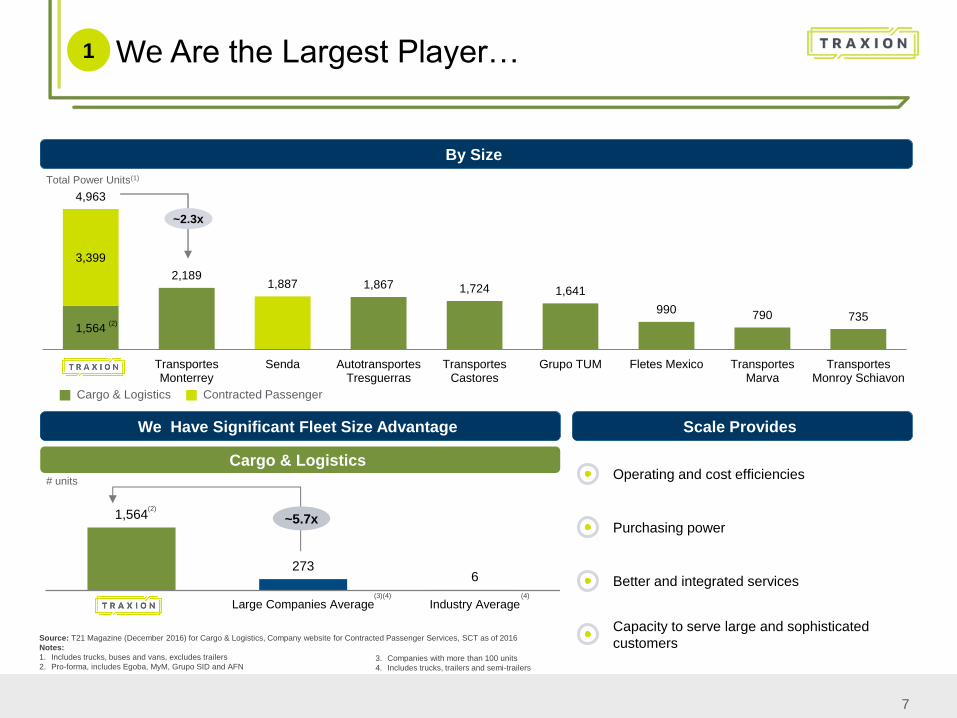

Total Power Units(1)

Source: T21 Magazine (December 2016) for Cargo & Logistics, Company website for Contracted Passenger Services, SCT as of 2016

Notes:

1. Includes trucks, buses and vans, excludes trailers

2. Pro-forma, includes Egoba, MyM, Grupo SID and AFN

By Size

We Are the Largest Player… 1

Cargo & Logistics

We Have Significant Fleet Size Advantage

# units

3. Companies with more than 100 units

4. Includes trucks, trailers and semi-trailers

Scale Provides

Operating and cost efficiencies

Purchasing power

Better and integrated services

Capacity to serve large and sophisticated

customers

1,564

273 6

Large Companies Average Industry Average

~5.7x

(3)(4) (4)

(2)

1,564

3,399

4,963

2,189 1,887 1,867 1,724 1,641

990 790 735

TransportesMonterrey

Senda AutotransportesTresguerras

TransportesCastores

Grupo TUM Fletes Mexico TransportesMarva

TransportesMonroy Schiavon

Cargo & Logistics Contracted Passenger

~2.3x

(2)

8

Content

(Top Alignment)

2.30

Subtitles

(bottom alignment) 2.62

Page Titles

3.09

Page Content

Left Alignment

4.60

Page Content

Right Alignment

4.60

Content

(Bottom Alignment)

3.00

Footnotes

(Top Alignment)

3.15

#0

#74

#130

#207

#223

#0

#119

#147

#60

#194

#199

#205

#75

#172

#198

#247

#150

#70

#101

#100

#106

…With the Broadest Portfolio of Service Offerings…

1

Truckload Intermodal Logistics

Cargo & Logistics

Personnel

Contracted Passenger

Student Tourism

Company

Number of

Units(1)

Domestic

Freight

Int’l Freight

& Transfers Moving LTL Intermodal Logistics Personnel Student Tourism

4,963(2)

Transportes

Monterrey 2,189

Senda 1,887

Autotransportes

Tresguerras 1,867

Transportes

Castores 1,724

Grupo TUM 1,641

Fletes Mexico 990

Transportes

Marva 790

T. Monroy

Schiavon 735

Material level of service offering No service offering

A True One-Stop Solution

Source: T21 Magazine (December 2016), Management estimates, companies websites

Note:

1 Including trucks, buses and vans, excludes trailers

2 Pro-forma, includes Egoba, MyM, Grupo SID, LIPU and AFN

9

Content

(Top Alignment)

2.30

Subtitles

(bottom alignment) 2.62

Page Titles

3.09

Page Content

Left Alignment

4.60

Page Content

Right Alignment

4.60

Content

(Bottom Alignment)

3.00

Footnotes

(Top Alignment)

3.15

#0

#74

#130

#207

#223

#0

#119

#147

#60

#194

#199

#205

#75

#172

#198

#247

#150

#70

#101

#100

#106

…in an Industry that has a Paramount Role in the Mexican Economy…

Source: INEGI, SCT, EMIS Insights

Notes:

1. Includes air, maritime, rail. cargo and passenger road transportation, as of 2015

2. Using 2015 average exchange rate of Ps$15.85 per US dollar according to Banxico

3. Includes transportation, postal and storage services according to INEGI, as of 2016

Road Transportation

86%

14%

Other Transportation Modes

5.9%(3) Contribution to GDP

Ps$1,432 billion (US$90Bn)(2)

Road Transportation

Ps$64 billion (US$4Bn)(2)

Rail Transportation

Road represents

56.2%(4) of Cargo Transportation

Road represents

96.0%(5) of Passenger Transportation

Share of Total Revenues(1)

Total Revenues(1): Ps$1,668 billion (US$105Bn)(2)

Road is the Backbone of the Mexican Transportation Industry

1

Ps$153 billion (US$10Bn)(2)

Air Transportation

Ps$19 billion (US$1Bn)(2)

Maritime Transportation

Ps$300Bn Government investment

between 2012-2016 in

road infrastructure(6)

4. Autotransporte de Carga, Estadistica Basica del Autotransporte Federal SCT, as of 2016

5. Autotransporte Federal de Pasajeros, Estadistica Basica del Autotransporte Federal SCT, as of 2016

6. Presidencia de la Republica, 4o informe de gobierno

10

Content

(Top Alignment)

2.30

Subtitles

(bottom alignment) 2.62

Page Titles

3.09

Page Content

Left Alignment

4.60

Page Content

Right Alignment

4.60

Content

(Bottom Alignment)

3.00

Footnotes

(Top Alignment)

3.15

#0

#74

#130

#207

#223

#0

#119

#147

#60

#194

#199

#205

#75

#172

#198

#247

#150

#70

#101

#100

#106

…that is Highly Fragmented with Room for Consolidation

1

Largest Player in a Highly Fragmented Industry

Cargo & Logistics

Road Cargo Transportation Industry Structure (Participation in the Market Category Per Unit)

Small Companies

(6-30 units)

Medium Companies

(31-100 units)

Large Companies

(+100 units)

Owner Operators

(1-5 units)

Notes:

1. Includes trucks, trailers and semi-trailers

81%

25%

16%

30%

2%

17%

1%

29%

% Companies % Units

140.8k companies

864.8k units(1)

More than 900 sizable

potential targets

with +245K units present

enormous opportunity to

consolidate the industry

Source: SCT, as of 2016

11

Content

(Top Alignment)

2.30

Subtitles

(bottom alignment) 2.62

Page Titles

3.09

Page Content

Left Alignment

4.60

Page Content

Right Alignment

4.60

Content

(Bottom Alignment)

3.00

Footnotes

(Top Alignment)

3.15

#0

#74

#130

#207

#223

#0

#119

#147

#60

#194

#199

#205

#75

#172

#198

#247

#150

#70

#101

#100

#106

We Grow Faster than the Industry

Traxion Footprint: Focus on the Fastest Growing

Regions in the Country

Quintana Roo Baja

California

Aguascalientes

Guanajuato

Queretaro

Jalisco

2010 – 2015 Real GDP CAGR

2.8% National GDP Growth Average

All Subsidiaries Present

No Presence

Main Operations / Economic Regions

2

Source: INEGI, Company information

Sonora

Nuevo

Leon

San Luis

Potosi

Large Companies are Growing Faster Than the Rest

of the Cargo Industry

Cargo Transportation Industry | Number of Units (000’s)(1)

Source: SCT

191 203 194 199 206 215

207 221 226 235 245 260

112 122 123 127 133

143 148

170 186 202

222 246

659 716 729

763 806

865

2011 2012 2013 2014 2015 2016

2011 - 2016

CAGR

10.7%

4.9%

4.7%

2.4%

2011 - 2016PF CAGR(2): 39.1%

Small Companies

(6-30 units)

Medium Companies

(31-100 units)

Large Companies

(+100 units)

Owner Operators

(1-5 units)

Notes:

1. Includes trucks, trailers and semi-trailers

2. CAGR of power units in the Cargo & Logistics segment

6.3%

5.4%

5.4%

5.0% 3.3%

3.9%

3.9%

4.0%

3.8%

12

Content

(Top Alignment)

2.30

Subtitles

(bottom alignment) 2.62

Page Titles

3.09

Page Content

Left Alignment

4.60

Page Content

Right Alignment

4.60

Content

(Bottom Alignment)

3.00

Footnotes

(Top Alignment)

3.15

#0

#74

#130

#207

#223

#0

#119

#147

#60

#194

#199

#205

#75

#172

#198

#247

#150

#70

#101

#100

#106

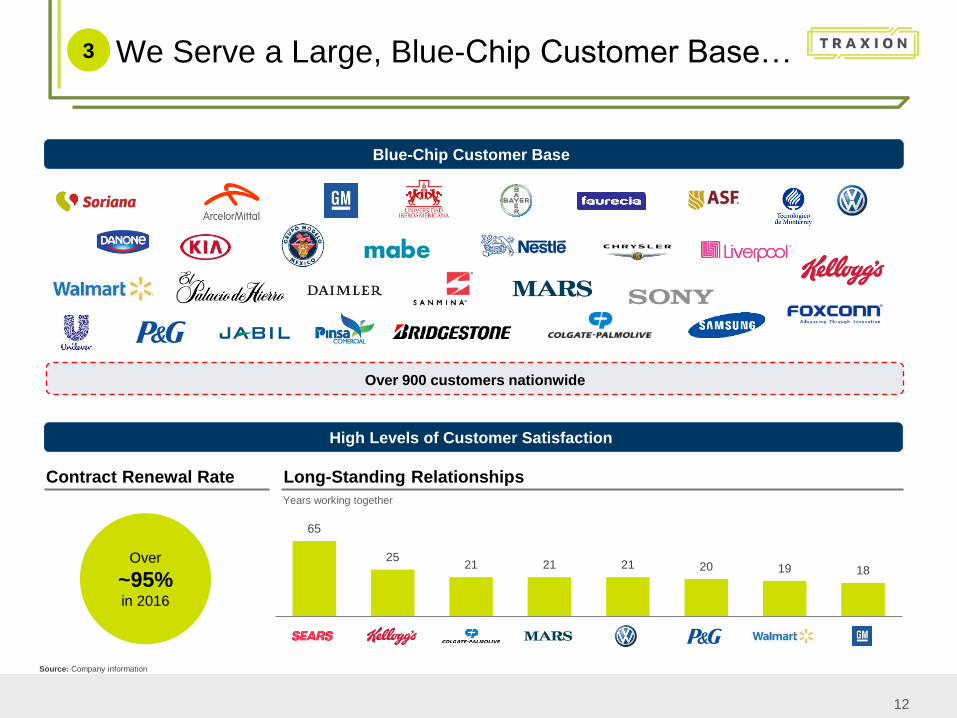

We Serve a Large, Blue-Chip Customer Base…

Blue-Chip Customer Base

Over 900 customers nationwide

High Levels of Customer Satisfaction

Contract Renewal Rate Long-Standing Relationships

65

25 21 21 21 20 19 18

Over

~95% in 2016

Years working together

3

Source: Company information

13

Content

(Top Alignment)

2.30

Subtitles

(bottom alignment) 2.62

Page Titles

3.09

Page Content

Left Alignment

4.60

Page Content

Right Alignment

4.60

Content

(Bottom Alignment)

3.00

Footnotes

(Top Alignment)

3.15

#0

#74

#130

#207

#223

#0

#119

#147

#60

#194

#199

#205

#75

#172

#198

#247

#150

#70

#101

#100

#106

Top 10

Top 20

Top 40

Top 30

Top 50

Other

…Which Supports our Diversified and Resilient Business Model

Revenue Breakdown(1)

Notes:

1. Based on 2016 Pro-forma figures

2. Company estimates according to 2016 Pro-forma financials

By Segment

3

Source: Company financials, Company information

Commercial Agreements

Contracted

Passenger

Services

38% Cargo &

Logistics

62%

Other

1%

Cargo

52%

Logistics

11%

Passenger

36%

Cargo

51%

Logistics

11%

Passenger

38%

No customer represents

more than 5% of the

company’s revenue

Partner of choice for international peers that need a local operating

partner

− 33 commercial agreements with leading international cargo &

logistics companies

Automotive

23%

Industrial

19%

School

6%

Tech

3%

Other

11% Government

3%

Retail

36%

By Industry(2) By Customer Concentration(2)

26%

46%

57%

38%

52%

14

Content

(Top Alignment)

2.30

Subtitles

(bottom alignment) 2.62

Page Titles

3.09

Page Content

Left Alignment

4.60

Page Content

Right Alignment

4.60

Content

(Bottom Alignment)

3.00

Footnotes

(Top Alignment)

3.15

#0

#74

#130

#207

#223

#0

#119

#147

#60

#194

#199

#205

#75

#172

#198

#247

#150

#70

#101

#100

#106

Well-Defined Strategy to Deliver Further Profitable Growth

Operations Financial M&A Commercial

• Continuous monitoring

and improvement to

drive margin

expansion

• Seamless nationwide

reach and international

connection

• One-stop solution

• Reliability and quality

in our services

• Brand differentiation

• Strong customer

relationships

• Increased share of

customers’ wallet

• Cross-selling

• Disciplined use of

leverage

• Cost control and

efficiency

• Allocation of growth

capital to maximize

returns

• Smart capital

allocation & selective

acquisitions

• Opportunistic

acquisitions

• Synergy analysis and

implementation

Proven ability to grow organically and inorganically thanks to a well defined strategy

An integrated approach to support further growth

4

15

Content

(Top Alignment)

2.30

Subtitles

(bottom alignment) 2.62

Page Titles

3.09

Page Content

Left Alignment

4.60

Page Content

Right Alignment

4.60

Content

(Bottom Alignment)

3.00

Footnotes

(Top Alignment)

3.15

#0

#74

#130

#207

#223

#0

#119

#147

#60

#194

#199

#205

#75

#172

#198

#247

#150

#70

#101

#100

#106

Best-In-Class Efficiently Run Operations 4

Robust Technological Platform With Focus on

GPS

Electronic Toll-Collection

System

Safe Driving Training

In-house Maintenance

Speed Control

Renewal of Fleet

Route Evaluation

24/7/365

Tracking &

Tracing

Interface with

any ERP

System

Company to provide

information

Industry Certifications

Best TMS(1) on Warehouse Management Systems

Reliability

Quality Safety

Operating

and cost

efficiencies

5.8 Average

Fleet Age

as of 2016(2)

94.9%

Fleet

Utilization

in 2016(2)

96.1%

sqm utilization

in 2016(2) Source: Company information Notes:

1. Transportation Management System

2. Average fleet age for all power units, fleet utilization for cargo segment and

sqm utilization for logistics operations

16

Content

(Top Alignment)

2.30

Subtitles

(bottom alignment) 2.62

Page Titles

3.09

Page Content

Left Alignment

4.60

Page Content

Right Alignment

4.60

Content

(Bottom Alignment)

3.00

Footnotes

(Top Alignment)

3.15

#0

#74

#130

#207

#223

#0

#119

#147

#60

#194

#199

#205

#75

#172

#198

#247

#150

#70

#101

#100

#106

Differentiated Commercial Strategy Driving Superior Organic Growth

4

Commercial Strategy Description

New Customers

Customer

Relationships

Cross-Selling

Strong specialized team

Corporate strategy

Dedicated and highly specialized customer service team

Focus on maintaining our client base

Capitalize further growth of our clients

Corporate team specialized on identifying opportunities

Broad service offering

One-Stop Solution for Client Needs

Cargo

Logistics

Personnel

Within Existing Customer Base

+900

Customers Product Personnel

17

Content

(Top Alignment)

2.30

Subtitles

(bottom alignment) 2.62

Page Titles

3.09

Page Content

Left Alignment

4.60

Page Content

Right Alignment

4.60

Content

(Bottom Alignment)

3.00

Footnotes

(Top Alignment)

3.15

#0

#74

#130

#207

#223

#0

#119

#147

#60

#194

#199

#205

#75

#172

#198

#247

#150

#70

#101

#100

#106

A Platform Providing Unique Competitive Advantages

4

Increase Synergies Potential

HR Commercial

• Cultural alignment

• Build management and

leadership development

programs

Shared Services Best Practices

Corporate

support

Sharing best practices

Sharing business knowledge

EBITDA

Growth

IT Systems Commercial

Strategy

Human

Resources Financial

Procurement

Management groups

Continuous improvement

Procurement IT

• Assigned IT budget

• Corporate IT Initiatives plan

• Most robust IT systems in

the Industry

• Best processes and policies

in industry

• Savings through scale:

diesel, tires, lubricants and

other

• Cross Selling

• Commercial strategy

Efficient

Management

Cost

Reduction

Quality

Servicing

Incorporation

of New Companies

Constant

Growth

18

Content

(Top Alignment)

2.30

Subtitles

(bottom alignment) 2.62

Page Titles

3.09

Page Content

Left Alignment

4.60

Page Content

Right Alignment

4.60

Content

(Bottom Alignment)

3.00

Footnotes

(Top Alignment)

3.15

#0

#74

#130

#207

#223

#0

#119

#147

#60

#194

#199

#205

#75

#172

#198

#247

#150

#70

#101

#100

#106

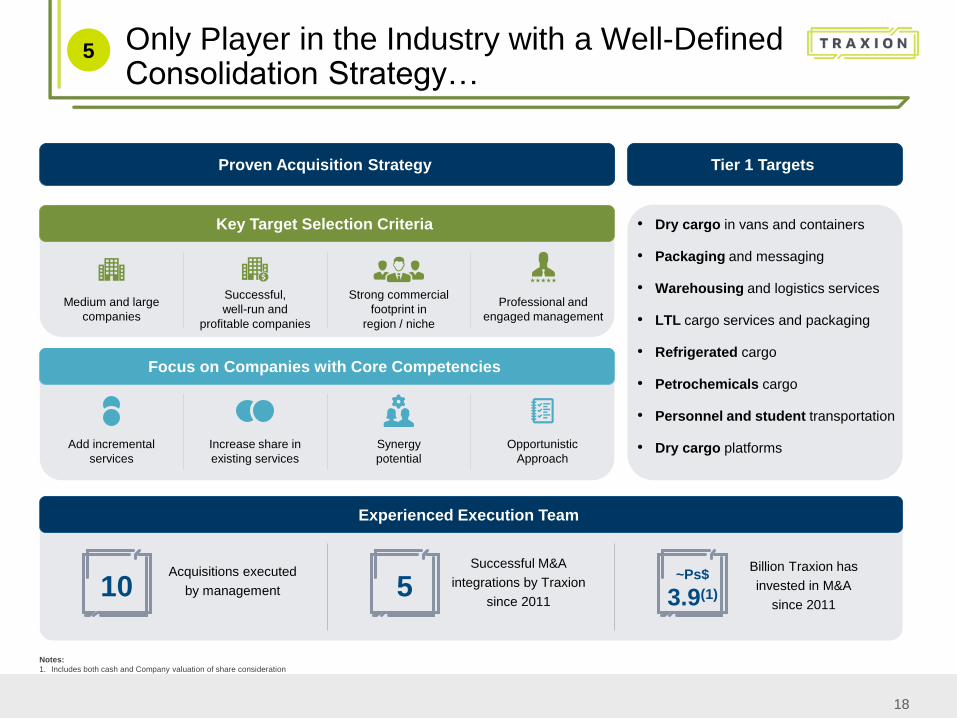

Only Player in the Industry with a Well-Defined Consolidation Strategy…

Acquisitions executed

by management

Successful M&A

integrations by Traxion

since 2011

Billion Traxion has

invested in M&A

since 2011

Experienced Execution Team

Notes:

1. Includes both cash and Company valuation of share consideration

Medium and large

companies

Successful,

well-run and

profitable companies

Strong commercial

footprint in

region / niche

Professional and

engaged management

Key Target Selection Criteria

Focus on Companies with Core Competencies

Add incremental

services

Increase share in

existing services

Synergy

potential

Opportunistic

Approach

Proven Acquisition Strategy

5

5 10 ~Ps$

3.9(1)

Tier 1 Targets

• Dry cargo in vans and containers

• Packaging and messaging

• Warehousing and logistics services

• LTL cargo services and packaging

• Refrigerated cargo

• Petrochemicals cargo

• Personnel and student transportation

• Dry cargo platforms

19

Content

(Top Alignment)

2.30

Subtitles

(bottom alignment) 2.62

Page Titles

3.09

Page Content

Left Alignment

4.60

Page Content

Right Alignment

4.60

Content

(Bottom Alignment)

3.00

Footnotes

(Top Alignment)

3.15

#0

#74

#130

#207

#223

#0

#119

#147

#60

#194

#199

#205

#75

#172

#198

#247

#150

#70

#101

#100

#106

…a Concrete M&A Pipeline Already Identified…

5

Refrigerated Cargo

Services Offered

Near-term opportunities of over 4,000 power units

Dry Cargo

Petrochemicals Cargo

Personnel Transportation

Messaging and Packaging

Identified Targets(1)

• 3 targets

• 4 targets

• 5 targets

• 2 targets

• 1 target

Rationale

New Service Regional

Expansion Strategic Fit Synergies

Notes:

1. No assurance can be given that the acquisitions of these potential targets will be completed. Some targets may not have been approached by the Company and there may not be ongoing discussions with respect to potential transactions. If acquisitions are consummated, there is no assurance that they will be accretive to the Company or that any synergies or additional economies of scale will be achieved

Dry Cargo / LTL • 1 target

20

Content

(Top Alignment)

2.30

Subtitles

(bottom alignment) 2.62

Page Titles

3.09

Page Content

Left Alignment

4.60

Page Content

Right Alignment

4.60

Content

(Bottom Alignment)

3.00

Footnotes

(Top Alignment)

3.15

#0

#74

#130

#207

#223

#0

#119

#147

#60

#194

#199

#205

#75

#172

#198

#247

#150

#70

#101

#100

#106

… and Strong Track-Record of Disciplined Acquisitions and Successful Integrations

We Have Maintained Financial Discipline in Each of our Acquisitions

Acquired: Dec 2011

Fleet: 300

Acquired: May 2016

Fleet: 580

Acquired: June 2016

Fleet: 222

Acquired: October 2016

Fleet: 3,399

Acquired: June 2013

Fleet: 428

• Transfer of best practices • Procurement efficiencies • Commercial intelligence

Proven Acquisition Model

5

• Cargo: fleet utilization

• Logistics: optimize

customer base

• Accelerate fleet growth

• Growth opportunities

with additional equity

• Expand number of

clients

• Extract economies of

scale

• Growth opportunities

with additional equity

Egoba MyM Grupo

SID AFN LIPU

• Commercial strategy

• Management

professionalization

(business plan and

KPIs)

• Increase profitability of

business structure

• Professionalization

(business plan and

KPIs)

21

Content

(Top Alignment)

2.30

Subtitles

(bottom alignment) 2.62

Page Titles

3.09

Page Content

Left Alignment

4.60

Page Content

Right Alignment

4.60

Content

(Bottom Alignment)

3.00

Footnotes

(Top Alignment)

3.15

#0

#74

#130

#207

#223

#0

#119

#147

#60

#194

#199

#205

#75

#172

#198

#247

#150

#70

#101

#100

#106

Traxion continues to deliver a strong track record of growth into 1H17

Revenue

1,592 1,746

3,249 3,789

1,733 2,018

425

2,311

1,058

1,431

1,597 1,748

3,702

6,134

2,801

3,465

2014A 2015A 2016A 2016 PF 1H16 PF 1H17

Ps$MM Average power units

1,564 1,552

3,399 3,690

760 776

4,963

5,242

2014A 2015A 2016 PF 1H17

Cargo & Logistics Contracted Passenger Sevices

Source: Company financials

Notes:

1. Pro-Forma figures include revenues of Grupo SID and LIPU for the full relevant period and include AFN figures from audited financials

2. Pro-Forma figures include average power units of Egoba, MyM, Grupo Sid, LIPU and AFN

Proven History of Growth…

(1) (1)

6

Cargo & Logistics Contracted Passenger Services Other

(2)

Fleet Growth

22

Content

(Top Alignment)

2.30

Subtitles

(bottom alignment) 2.62

Page Titles

3.09

Page Content

Left Alignment

4.60

Page Content

Right Alignment

4.60

Content

(Bottom Alignment)

3.00

Footnotes

(Top Alignment)

3.15

#0

#74

#130

#207

#223

#0

#119

#147

#60

#194

#199

#205

#75

#172

#198

#247

#150

#70

#101

#100

#106

Adjusted EBITDA Adjusted EBITDA Margin

Maintenance of Units(2)

Ps$MM

220 286

768

1,191

470

630

2014A 2015A 2016A 2016 PF 1H16 PF 1H17

%

13.8

16.3

20.7 19.4

16.8 18.2

2014A 2015A 2016A 2016 PF 1H16 PF 1H17

Source: Company financials

Notes:

1. Pro-Forma figures include Grupo SID and LIPU for the full relevant period and include AFN figures from audited financials

2. Maintenance of units included in COGS; already accounted for in Adjusted EBITDA

…Profitability…

(1)

Ps$MM

119 74

612

469 7.4% 4.2%

16.5%

13.5%

2014A 2015A 2016A 1H17

Acquisition of Transportation Equipment and Machinery as % of Revenue

(1) (1)

6

(1)

Acquisition of Transportation Equipment and Machinery

Ps$MM

76 88

183 168

4.8%

5.0%

4.9% 4.8%

2014A 2015A 2016A 1H17

Maintenance of Units as % of Revenue

23

Content

(Top Alignment)

2.30

Subtitles

(bottom alignment) 2.62

Page Titles

3.09

Page Content

Left Alignment

4.60

Page Content

Right Alignment

4.60

Content

(Bottom Alignment)

3.00

Footnotes

(Top Alignment)

3.15

#0

#74

#130

#207

#223

#0

#119

#147

#60

#194

#199

#205

#75

#172

#198

#247

#150

#70

#101

#100

#106

…and Disciplined Financial Strategy

Leverage • Commitment to maintain a strong, bullet-proof balance sheet

• Long-term target Net Debt / EBITDA level of 1.5-2.5x

Liquidity • Maintain adequate liquidity to fund working capital

• Maintain a goal of 60 days of receivables

Capex • Capex allocation based on higher return projects and approved by executive committee

• Target companies must meet financial returns thresholds

Margins • Maintain solid margins

• Improve target’s margins as appropriate through efficiencies

6

24

Content

(Top Alignment)

2.30

Subtitles

(bottom alignment) 2.62

Page Titles

3.09

Page Content

Left Alignment

4.60

Page Content

Right Alignment

4.60

Content

(Bottom Alignment)

3.00

Footnotes

(Top Alignment)

3.15

#0

#74

#130

#207

#223

#0

#119

#147

#60

#194

#199

#205

#75

#172

#198

#247

#150

#70

#101

#100

#106

Experienced Management Team…

Years of relevant experience

Bernardo Lijtszain

Hector Gonzalez

Rodolfo Mercado Victor Bravo Adolfo Salame

Jose Suarez

Rotter

Jose Luis

Estrada

Patricio

Pasquel

Elias Dana

Roffe

Alejandro

Marroquin

45+

30+

20+ 30+ 10+

40+ 40+ 20+ 12+ 15+

Aby Lijtszain

20+

Chairman of the Board

Vice Chairman / CEO

Internal Auditor

COO CFO M&A

Corporate Structure

7

Top Management Background

Bernardo

Lijtszain

Chairman

Aby Lijtszain

Vice Chairman &

Corporate CEO

Rodolfo

Mercado

Corporate COO

Victor Bravo

Corporate CFO

Adolfo Salame

M&A Director

• Co-founder and current Chairman of Traxion with over 45

years of relevant experience

• Board member of Union Nacional de Credito de

Autotransporte, former President of CANACAR(1) and former

President of Confederacion del Autotransporte, among other

relevant positions in the industry

• Co-founder, Vice Chairman and CEO of Traxion, responsible

for strategic planning with over 20 years of experience in the

transportation industry

• Member of the Board of Directors and COO of Traxion with

over 20 years of relevant experience

• He previously served as COO of Lipu and CEO of Settepi

prior to its acquisition by Lipu

• CFO of Traxion with ample experience in positions in

Corporate Finance, Project Finance, Infrastructure

Operations and General Management

• Previously served as OMA’s(2) Airports CFO and later CEO,

as well as ICA’s CFO

• Led OMA’s(2) Airports IPO in 2006

• M&A Director of Traxion with over 10 years of relevant

experience

• Previously served 7 years at Von Wobeser y Sierra advising

leading multinational companies in corporate and regulatory

administrative issues Notes:

1 Camara Nacional del Autotransporte de Carga

2 OMA is a public airports operator with a market cap of ~US$2.5Bn

Over 20+ years of relevant experience on average

25

Content

(Top Alignment)

2.30

Subtitles

(bottom alignment) 2.62

Page Titles

3.09

Page Content

Left Alignment

4.60

Page Content

Right Alignment

4.60

Content

(Bottom Alignment)

3.00

Footnotes

(Top Alignment)

3.15

#0

#74

#130

#207

#223

#0

#119

#147

#60

#194

#199

#205

#75

#172

#198

#247

#150

#70

#101

#100

#106

Independent(1)

67%

Non-independent

33%

Strong Corporate Governance

Current Ownership Structure

Board of Directors Composition Solid Shareholder Base

Our process of institutionalization started 10 years ago

Audit committee

Corporate governance committee

Code of ethics

7 …with Strong Corporate Governance and Sophisticated Investor Base…

Total = 15 Members

Instrumental Pillars of our Success

Well-known, highly reputable investor base with entrenched

relationships in the industry

Develop joint vision of business objectives and execution

strategy:

Larger scale

Execute attractive acquisitions

Improve profitability Notes:

1 According to Ley del Mercado de Valores

Management team with ~23% ownership

Individuals 21.3%

Other 16.3%

17.7%

44.7%

26

Content

(Top Alignment)

2.30

Subtitles

(bottom alignment) 2.62

Page Titles

3.09

Page Content

Left Alignment

4.60

Page Content

Right Alignment

4.60

Content

(Bottom Alignment)

3.00

Footnotes

(Top Alignment)

3.15

#0

#74

#130

#207

#223

#0

#119

#147

#60

#194

#199

#205

#75

#172

#198

#247

#150

#70

#101

#100

#106

A Superior Platform Built for Long-Term Growth

Mexico’s largest ground

transportation and logistics

services platform(1) with

nationwide presence and focus

on the fastest growing regions

in the country

Proven history of high growth

and profitability

We believe we are the first and

only transportation and

logistics consolidator in

Mexico with a solid track-

record of disciplined acquisitions

and successful integration

Note:

1. According to T21 Magazine (December 2016) and public filings of companies in the ground transportation industry

Supplemental Information

Appendix

28

Content

(Top Alignment)

2.30

Subtitles

(bottom alignment) 2.62

Page Titles

3.09

Page Content

Left Alignment

4.60

Page Content

Right Alignment

4.60

Content

(Bottom Alignment)

3.00

Footnotes

(Top Alignment)

3.15

#0

#74

#130

#207

#223

#0

#119

#147

#60

#194

#199

#205

#75

#172

#198

#247

#150

#70

#101

#100

#106

Leverage and Capital Structure

1H17 Debt Profile Debt Amortization Schedule

Capitalization Table

Notes:

1. Includes current installments of long-term debt and long-term debt

12%

88%

Short-term debt

Long-term debt

Debt(1)= Ps$3,183MM

262 271 310 486

656

995

2017 2018 2019 2020 2021 2022 2023

1H17 | Ps$MM 1H17

Current installments of long-term debt 378

Current installments of obligations under capital leases 59

Long-term debt, excluding current installments 2,805

Obligations under capital leases, excluding current installments 185

Total debt 3,427

Total shareholders’ equity 5,039

Total capitalization 8,465

Total debt / equity (%) 68.0%

Ps$MM

29

Content

(Top Alignment)

2.30

Subtitles

(bottom alignment) 2.62

Page Titles

3.09

Page Content

Left Alignment

4.60

Page Content

Right Alignment

4.60

Content

(Bottom Alignment)

3.00

Footnotes

(Top Alignment)

3.15

#0

#74

#130

#207

#223

#0

#119

#147

#60

#194

#199

#205

#75

#172

#198

#247

#150

#70

#101

#100

#106

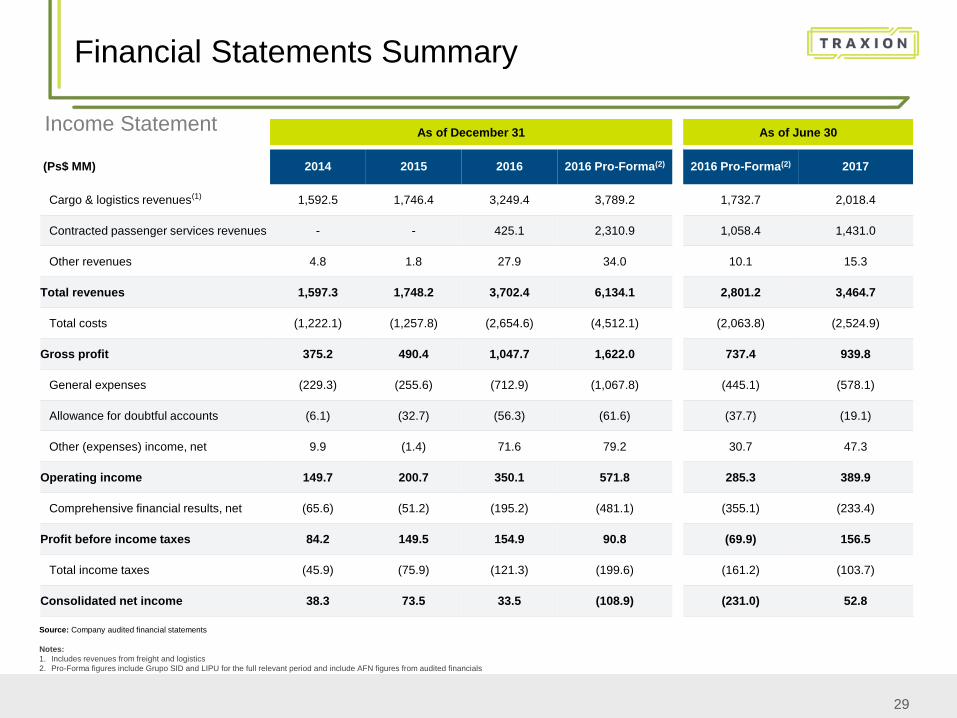

Financial Statements Summary

Income Statement

(Ps$ MM) 2014 2015 2016 2016 Pro-Forma(2)

Cargo & logistics revenues(1) 1,592.5 1,746.4 3,249.4 3,789.2

Contracted passenger services revenues - - 425.1 2,310.9

Other revenues 4.8 1.8 27.9 34.0

Total revenues 1,597.3 1,748.2 3,702.4 6,134.1

Total costs (1,222.1) (1,257.8) (2,654.6) (4,512.1)

Gross profit 375.2 490.4 1,047.7 1,622.0

General expenses (229.3) (255.6) (712.9) (1,067.8)

Allowance for doubtful accounts (6.1) (32.7) (56.3) (61.6)

Other (expenses) income, net 9.9 (1.4) 71.6 79.2

Operating income 149.7 200.7 350.1 571.8

Comprehensive financial results, net (65.6) (51.2) (195.2) (481.1)

Profit before income taxes 84.2 149.5 154.9 90.8

Total income taxes (45.9) (75.9) (121.3) (199.6)

Consolidated net income 38.3 73.5 33.5 (108.9)

Source: Company audited financial statements

As of December 31 As of June 30

2016 Pro-Forma(2) 2017

1,732.7 2,018.4

1,058.4 1,431.0

10.1 15.3

2,801.2 3,464.7

(2,063.8) (2,524.9)

737.4 939.8

(445.1) (578.1)

(37.7) (19.1)

30.7 47.3

285.3 389.9

(355.1) (233.4)

(69.9) 156.5

(161.2) (103.7)

(231.0) 52.8

Notes:

1. Includes revenues from freight and logistics

2. Pro-Forma figures include Grupo SID and LIPU for the full relevant period and include AFN figures from audited financials

30

Content

(Top Alignment)

2.30

Subtitles

(bottom alignment) 2.62

Page Titles

3.09

Page Content

Left Alignment

4.60

Page Content

Right Alignment

4.60

Content

(Bottom Alignment)

3.00

Footnotes

(Top Alignment)

3.15

#0

#74

#130

#207

#223

#0

#119

#147

#60

#194

#199

#205

#75

#172

#198

#247

#150

#70

#101

#100

#106

Financial Statements Summary (Cont’d)

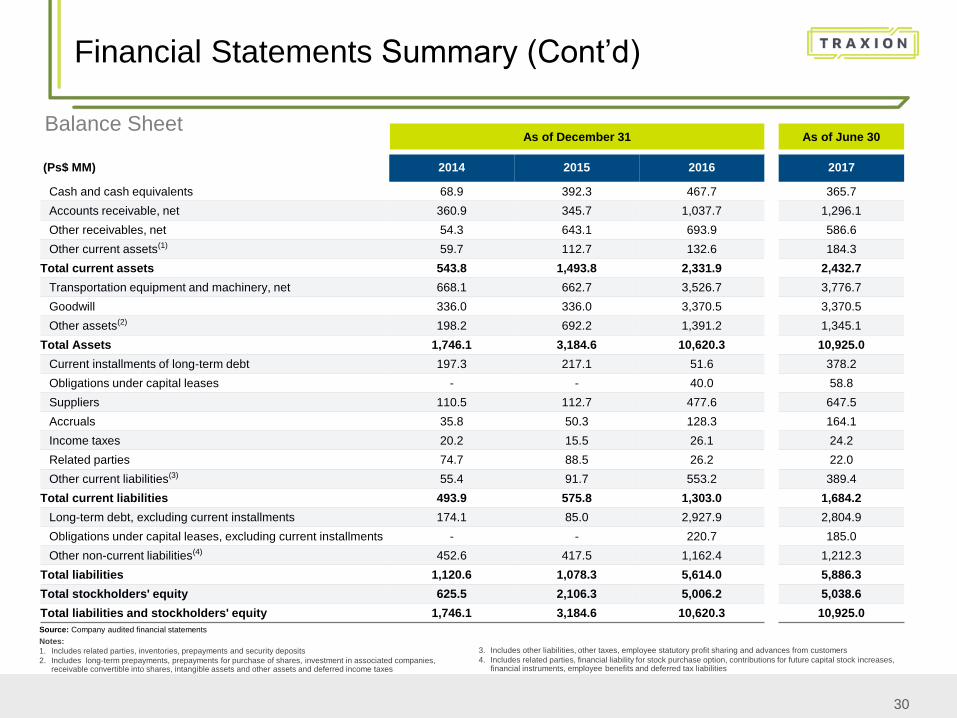

Balance Sheet

(Ps$ MM) 2014 2015 2016

Cash and cash equivalents 68.9 392.3 467.7

Accounts receivable, net 360.9 345.7 1,037.7

Other receivables, net 54.3 643.1 693.9

Other current assets(1) 59.7 112.7 132.6

Total current assets 543.8 1,493.8 2,331.9

Transportation equipment and machinery, net 668.1 662.7 3,526.7

Goodwill 336.0 336.0 3,370.5

Other assets(2) 198.2 692.2 1,391.2

Total Assets 1,746.1 3,184.6 10,620.3

Current installments of long-term debt 197.3 217.1 51.6

Obligations under capital leases - - 40.0

Suppliers 110.5 112.7 477.6

Accruals 35.8 50.3 128.3

Income taxes 20.2 15.5 26.1

Related parties 74.7 88.5 26.2

Other current liabilities(3) 55.4 91.7 553.2

Total current liabilities 493.9 575.8 1,303.0

Long-term debt, excluding current installments 174.1 85.0 2,927.9

Obligations under capital leases, excluding current installments - - 220.7

Other non-current liabilities(4) 452.6 417.5 1,162.4

Total liabilities 1,120.6 1,078.3 5,614.0

Total stockholders' equity 625.5 2,106.3 5,006.2

Total liabilities and stockholders' equity 1,746.1 3,184.6 10,620.3

As of December 31

Source: Company audited financial statements

Notes:

1. Includes related parties, inventories, prepayments and security deposits

2. Includes long-term prepayments, prepayments for purchase of shares, investment in associated companies, receivable convertible into shares, intangible assets and other assets and deferred income taxes

3. Includes other liabilities, other taxes, employee statutory profit sharing and advances from customers

4. Includes related parties, financial liability for stock purchase option, contributions for future capital stock increases, financial instruments, employee benefits and deferred tax liabilities

2017

365.7

1,296.1

586.6

184.3

2,432.7

3,776.7

3,370.5

1,345.1

10,925.0

378.2

58.8

647.5

164.1

24.2

22.0

389.4

1,684.2

2,804.9

185.0

1,212.3

5,886.3

5,038.6

10,925.0

As of June 30

31

Content

(Top Alignment)

2.30

Subtitles

(bottom alignment) 2.62

Page Titles

3.09

Page Content

Left Alignment

4.60

Page Content

Right Alignment

4.60

Content

(Bottom Alignment)

3.00

Footnotes

(Top Alignment)

3.15

#0

#74

#130

#207

#223

#0

#119

#147

#60

#194

#199

#205

#75

#172

#198

#247

#150

#70

#101

#100

#106

Financial Statements Summary (Cont’d)

Reconciliation from Net Income to Adjusted EBITDA

Source: Company audited financial statements

As of December 31 As of June 30

Notes:

1. Pro-Forma figures include Grupo SID and LIPU for the full relevant period and include AFN figures from audited financials

2. Includes certain receivables from former related parties written-off, legal and tax advisory professional fees

3. Inventory adjustment due to change in accounting policies

4. Includes professional services fees and commissions

(Ps$ MM) 2014 2015 2016 2016 Pro-Forma(1)

Consolidated net income (loss) 38.3 73.5 33.5 (108.9)

Plus: Total income taxes 45.9 75.9 121.3 199.6

Plus: Comprehensive financial results,

net 65.6 51.2 195.2 481.1

Plus: Depreciation 63.6 72.0 238.5 368.3

Plus: Amortization 7.2 12.6 24.6 47.3

Plus: Restructuring expenses(2) - 0.5 102.4 123.4

Plus: Inventory valuation adjustment(3) - - 19.6 19.6

Plus: Refinancing expenses(4) - - 32.5 60.7

Adjusted EBITDA 220.5 285.8 767.8 1,191.3

2016 Pro-Forma(1) 2017

(231.0) 52.8

161.2 103.7

355.1 233.4

161.8 216.4

22.6 23.5

- -

- -

- -

469.7 629.9