corporate presentation - oro negro presentation website.pdf · of televisa at a us$.3bn valuation,...

TRANSCRIPT

Corporate Presentation

State-of-the-art-fleet

Financial Highlights

Our Company

Overview

Oro Negro at a glance

Oro Negro is funded in February 2012.

Secures $245mm from Ares, Temasek and Axis

In August 2012 Oro Negro Acquires Todco

Primus is delivered

Contracted Fortius and Decus

Company launched in February 2012 with the aim of becoming a leadingoil field services firm

Strategy: (i) acquire strategic assets, (ii) partner with leading O&G servicesfirms, and (iii) acquire controlling interests in operating companies

The shareholders have committed US$645mm to Oro Negro of whichUS$590mm have already been contributed

Oro Negro’s Team has proven experience working together at leadinginternational Oil & Gas companies

With 8 premium jackups + 1 modular rig (4 premium jackups currentlyunder contract with Pemex), Oro Negro is positioned as one of the leadingjackup operators in Mexico with the largest fleet of premium assets

~$1.9 billion of committed hard asset investments in premium drilling assets and ~US$700mm of current contract

backlog

Axis contributes $200mm

Secures additional $200mm in equity commitments

Decusdelivered

Impetus to be delivered

Vastus, Supremus & Animus expected to be delivered

8

Growth trajectory

2012

2013

Laurus and Fortiusdelivered

Contracted Impetus, Vastus, Supremusand Animus

2014

2015

Sponsor overview

9

Axis participated as principal in the purchase of the minority shareholdersof Televisa at a US$.3bn valuation, served as the executor arm of an M&Astrategy, carried out an institutionalization process and managed thegroup´s corporate finances and capital markets strategy

In just 4.5 years, Televisa became a global Spanish-speaking media companyand was listed in the NYSE at a market cap. of US$8.9Bn

I50purchase of PanAmsat, 1st private satellite network with internationalorbits US$200MM. Axis identified the arbitrage opportunity in developinga Pan Regional pay TV service at substantially lower subscriberadministration cost than any other competing atlternative

The company was listed in the Nasdaq Stock Exchange and was later sold toHughes Electronics generating a net profit of US$1,710mm

1990, Axis purchased VideoVisa with other private investors, a video rentaland movie distribution company in Mexico

1991 sold 27% for US$40mm, listed the company in the Mexican Stock Exchangeand in 1993 sold the control to a private group for US$150M. The totalcompound annual return of the investment was more than 70% over 2.5 yearperiod

1991 Axis acquired Coronado, a 60 year old private family run company inthe consumer segment

Axis institutionalized and expanded the FDA approval required in USA and wassold it to Grupo Bimbo for US$29m, generating Axis a 18% IRR after a 100%Mexican peso devaluation.

In 2005, Axis created Navitas Investments, a NY Law-Note PurchaseProgram with the purpose of financing projects in the Mexican oil fieldservices sector (OFS)

In 2007, Axis Sofom was created to streamline the tax impact of Navitas lendingactivities. Since inception, Navitas and Axis Sofom have made loans for morethan US$900 million and have not had a single default in its loan portfolio

In 2007 Axis launched Navix, a non-bank financial intermediary, in order tocreate a solid, well capitalized, institutional platform to consolidate itsstructured financing activities associated with the oil services industry inMexico

In 2009 Navix entered into a US$330mm Partnership Product Program withCitibankIn 2010, Navix completed an offering of US$300mm CKD focused in the energysectorCombined with Navitas + Axis, the group has underwritten over Mx$35bn ofloans in the OFS sector

Axis Capital Management is a private investment firm founded in 1990 that has specialized in privateequity investments, advisory services and structured lending. Since inception, the firm has executed, asprincipal, and agent over US$13billion in transactions

Axis has distinguished itself by identifying arbitrage opportunities across a diverse range of industriesand markets:

Navitas

Experienced team with proven industry leadership

10

The Group´s management and Board of Directors have extensive international and domestic experience within the oil and gas industry, as well as a long-standing relationships with PEMEX

The Group´s operational team has an average relevant drilling experience of over 30 years working in more than 50 different countries

We have developed, implemented and practiced ZERO HARM policy, whereby we endeavor to prevent any harm against the People, Environment, ´People or our Equipment

The Quality Management System defines the Company´s goals concerning operational excellence and provides clear execution parameters of quality objectives

30 years + 50 different countries

International + domestic

experience

Zero Harm + QMS policy

Falcon Drilling Co.

Frontier Drilling

Oro Negro was founded in February 2012 and since then we have developed a robust operational set up with a perfect safety record, with no major incidents registered

State-of-the-art-fleet

Financial Highlights

Our Company

2014 F 2015 F 2016ERig 3

Type: PlatformBuilt: 1993

Revenues USD 19m USD 18m USD 17m Total Asset Value: USD 38mEBITDA USD 9m USD 9m USD 8m

Primus

Type: Jackup Mod V-BBuilt: 2012Max Water Depth (ft.):400

Revenues USD 59m USD 60m USD 59mTotal Asset Value:

USD 235mEBITDA USD 30m USD 34m USD 35m

Laurus

Type: Jackup Mod V-BBuilt: 2013Max Water Depth (ft.):400

Revenues USD 60m USD 59m USD 59mTotal Asset Value:

USD 246mEBITDA USD 30m USD 34m USD 35m

Fortius

Type: Jackup Pacific ClassBuilt: 2013Max Water Depth (ft.):400

Revenues USD 51m (1) USD 60m USD 60mTotal Asset Value:

USD 244mEBITDA USD 28m (1) USD 35m USD 36m

Decus

Type: Jackup Pacific ClassBuilt: 2014Max Water Depth (ft.):400

Revenues USD 34m (2) USD 60m USD 60mTotal Asset Value:

USD 242mEBITDA USD 19m (2) USD 35m USD 37m

Total Revenues USD 223m USD 258m USD 255m Total

Total EBITDA USD 117m USD 148m USD 151m USD 1,004m

Rig 3Operation start date: Aug-12Charter duration: 4 years

50.0 23.4 20,100PEMEX, September 2015

PrimusOperation start date: Jun-13Charter duration: 2.8 years

159.0 59.8 97,800PEMEX, April 2016

LaurusOperation start date: Nov-13Charter duration: 3.4 years

159.0 59.9 156,000PEMEX, April 2017

FortiusOperation start date: Feb-14Charter duration: 4 years

161.1 57.9 204,500PEMEX, January 2018

DecusOperation start date: Jun-14Charter duration: 3.7 years

161.1 57.4 208,000PEMEX, February 2018

Current Contract Backlog

Daily rate Total Daily Direct Operating costs

US$ 000’

Current Fleet

Contract backlog*

1.Fortius started operations February 8th 2014. Fortius cost US$2mm more than Decus.2.Decus started operations June 10th, 2014* Data as of July 31st 2014

State-Of-The-Art Fleet generating stable future cash flows

Under contract with Pemex

12

Total Current Backlog:

US$686,400

Impetus

Type: Jackup Pacific ClassBuilt: 2014Max Water Depth (ft.):400

Revenues USD 40m USD 60mEstimated Total Asset Value:

USD 234mEBITDA USD 24m USD 37m

Vastus

Type: Jackup Pacific ClassBuilt: 2015Max Water Depth (ft.):400

Revenues USD 25m USD 60mEstimated Total Asset Value:

USD 234mEBITDA USD 15m USD 37m

Supremus

Type: Jackup Pacific ClassBuilt: 2015Max Water Depth (ft.):400

Revenues USD 5m USD 60mEstimated Total Asset Value:

USD 234mEBITDA USD 3m USD 37m

Animus

Type: Jackup Pacific ClassBuilt: 2015Max Water Depth (ft.):400

Revenues - USD 55mEstimated Total Asset Value:

USD 234mEBITDA - USD 34m

Total Revenues USD 70m USD 235m Total

Total EBITDA USD 42m USD 145m USD 936m

2015 F 2016F

Jackups under construction

Assumptions: all platforms at a minimum dayrate of US$161M.

13

Estimated Contract Backlog

Daily rate Total Daily Direct Operating costs

Contract backlog

Projects under construction focused on premium assets

Impetus*Operation start date: Apr-15Charter duration: 3.6 years

161.1 56.9 Delivery: Dec-14 November 2018 209,430

Vastus*Operation start date: Jul-15Charter duration: 3.6 years

161.1 56.9 Delivery: Mar-15 February 2019 209,430

Supremus*Operation start date: Nov-15Charter duration: 3.6 years

161.1 56.9 Delivery: Jul-15 June 2019 209,430

Animus*Operation start date: Jan-16Charter duration: 3.6 years

161.1 56.9 Delivery: Sep-2015 August 2019 209,430

US$ 000’

Total Estimated Backlog:

US$837,720

1

2

2

3

1

4

3

4

5

1

1

1

2

2

3

4

1

1

10

Ezion

Goimar

KCA Deutag

Operadora Cicsa

Aban Offshore

AMS/Ezion

CP Latina

COSL

Diamond Offshore

GSP

Ensco

Oro Negro

Perforadora Central

Perforadora Mexico

Seadrill

Noble

Premium Conventional

1

2

2

2

3

1

4

5

5

6

8

1

1

1

2

2

3

4

1

1

10

Ezion

Goimar

KCA Deutag

Operadora Cicsa

Aban Offshore

AMS/Ezion

CP Latina

Pemex

COSL

Diamond Offshore

GSP

Ensco

Perforadora Mexico

Seadrill

Perforadora Central

Grupo R

Oro Negro

Noble

Premium Conventional4

4

4

4

5

5

6

7

7

8

8

9

12

19

Ensco

Greatship

Rowan

Vantage Drilling

Jindal Drilling

Perforadora Central

Grupo R

Transocean

UMW Standard Drilling

Bestford Capital

Oro Negro

Aban Offshore

COSL

Seadrill 15%

12%

9%

9%

8%

8%

6%

5%

5%

5%

3%

3%

3%

3%

2%

2%

2%2%

1. Source:

2. (1) Petrodata. Premium jackups: 350-400 ft depth, IC, as of YE 2016

3. (2) (3) ODS Petrodata, Pemex: Market share is calculated by % of the total number of jackups. Market share data does not take into account scrapings. Due to the old age of some conventional jackups, some contract renewals are unlikely.

Mexico Market share(2)

Pro-forma market share including jackups in the pipeline(2)(3)

Leading position in Mexico´s premium jackup market

Mkt share

Significant barriers to entry for non-established drillers

In less than 24 months Oro Negropositioned itself as the 4thlargest owner of premiumjackups in the world

Pro-forma worldwide position in the premium jack up market(1)

Limited supplyPremium jack-ups are in limited supply worldwide and require a

long lead time to construct

Capital requirements

Premium jack-up rigs require substantial capital expenditures

(~$230mm) and contractor must have exclusive rights to the rig

before submitting contract request to Pemex

Economies of scale Synergies are required to sustain high onshore costs

Pemex relationshipsLong-term relationship and deep understanding of Pemex's

internal procedures is highly beneficial

Pre-qualification

requirements

Pemex contractors require at least 2 years of operating

experience to operate rigs without third-parties in some cases

(Todco is a pre-qualified operator already)

Mexican premium jack-up market has significant barriers to entry for non-established

drillers

Mkt share

20%

10%

10%

8%

8%

8%

6%

6%

6%

4%

4%

4%

2%

2%

2%2%

14

(4)*

(2)*

(6)*

* Under construction

State-of-the-art-fleet

Financial Highlights

Our Company

10

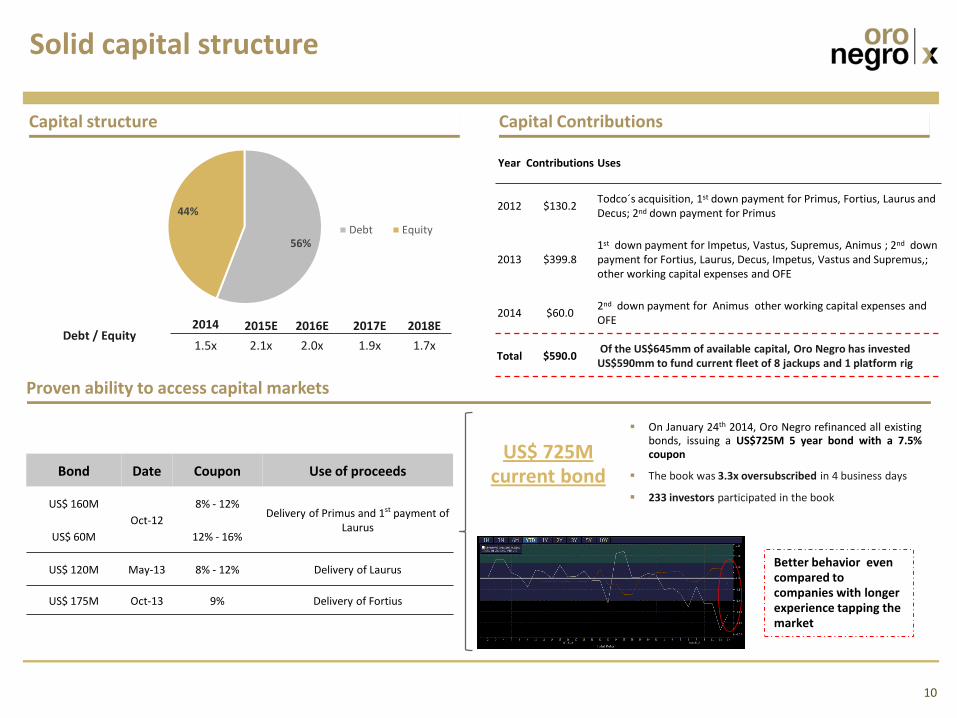

Proven ability to access capital markets

Solid capital structure

Bond Date Coupon Use of proceeds

US$ 160M

Oct-12

8% - 12%Delivery of Primus and 1st payment of

LaurusUS$ 60M 12% - 16%

US$ 120M May-13 8% - 12% Delivery of Laurus

US$ 175M Oct-13 9% Delivery of Fortius

US$ 725M current bond

On January 24th 2014, Oro Negro refinanced all existingbonds, issuing a US$725M 5 year bond with a 7.5%coupon

The book was 3.3x oversubscribed in 4 business days

233 investors participated in the book

Capital Contributions

Better behavior even compared to companies with longer experience tapping the market

Capital structure

56%

44%

Debt Equity

Debt / Equity2014 2015E 2016E 2017E 2018E

1.5x 2.1x 2.0x 1.9x 1.7x

Year Contributions Uses

2012 $130.2 Todco´s acquisition, 1st down payment for Primus, Fortius, Laurus and Decus; 2nd down payment for Primus

2013 $399.8 1st down payment for Impetus, Vastus, Supremus, Animus ; 2nd down payment for Fortius, Laurus, Decus, Impetus, Vastus and Supremus,;other working capital expenses and OFE

2014 $60.0 2nd down payment for Animus other working capital expenses and OFE

Total $590.0 Of the US$645mm of available capital, Oro Negro has invested

US$590mm to fund current fleet of 8 jackups and 1 platform rig

53%

57%

60%60%

58%

48%

50%

52%

54%

56%

58%

60%

62%

2014 2015E 2016E 2017E 2018E

0

50

100

150

200

250

300

350

EBITDA EBITDA margin

11

Return on total assets

Revenues (1) EBITDA vs EBITDA Margin

Financial outlook

Company leverage (2)

US$m US$m

223

328

492 492473

2014 2015E 2016E 2017E 2018E

Note: The financial estimates for 2015-2018 are assuming that four additional premium jackups will be under contract at a daily rate of US$161,000(1). Revenues start declining in 2018 because mobilization revenue is not considered(2).Assuming US$175M new debt issuance per jackup delivery

5.3%

6.6%

11.6% 11.6% 10.7%

2014 2015 2016 2017 2018

EBIT/Assets

7.5x7.3x

4.3x3.9x

3.6x

0.0 x

1.0 x

2.0 x

3.0 x

4.0 x

5.0 x

6.0 x

7.0 x

8.0 x

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

2014 2015 2016 2017 2018

LTV Net Debt/EBITDA