investor presentation/media/files/b/bpost... · may - june 2016 . investor presentation . first...

TRANSCRIPT

May - June 2016

Investor presentation

First quarter 2016

2

Investor presentation first quarter 2016

Disclaimer

This presentation is based on information published by bpost in its First Quarter 2016 Interim Financial Report, made available on May, 2nd 2016 at 5.45pm CET on corporate.bpost.be/investors. This information forms regulated information as defined in the Royal Decree of 14 November 2007. The information in this document may include forward-looking statements1, which are based on current expectations and projections of management about future events. By their nature, forward-looking statements are not guarantees of future performance and involve known and unknown risks, uncertainties, assumptions and other factors because they relate to events and depend on circumstances that will occur in the future whether or not outside the control of the Company. Such factors may cause actual results, performance or developments to differ materially from those expressed or implied by such forward-looking statements. Accordingly, no assurance is given that such forward-looking statements will prove to have been correct. They speak only as at the date of the Presentation and the Company undertakes no obligation to update these forward-looking statements contained herein to reflect actual results, changes in assumptions or changes in factors affecting these statements. This material is not intended as and does not constitute an offer to sell any securities or a solicitation of any offer to purchase any securities.

More on corporate.bpost.be/investors

11.05.2016 Ordinary General Meeting of Shareholders

19.05.2016 Payment date of the dividend

08.08.2016 (17:45 CET) Quarterly results 2Q16

09.11.2016 (17:45 CET) Quarterly results 3Q16

Financial Calendar

1 as defined among others under the U.S. Private Securities Litigation Reform Act of 1995

bpost at a glance Highlights 1Q16 – 4 Outlook 2016 – 5 Overview – 6 Products – 7 Strategy – 8 Domestic Mail – 9 Parcels – 10 Domestic Parcels acquisition – 11 International parcels acquisitions – 12 Additional sources of revenues – 13 Transformation – 14 Productivity – 15 Vision 2020 – 16 Alpha – 17 CSR – 18 Dividend policy – 19 Summary of key financials FY15 – 20 Balance sheet – 21 Relationship with State – 22 Management – 23

More detail on 1Q16 EBITDA bridge – 25 Key financials – 26 Revenues – 27 Domestic Mail – 28 Parcels – 29 Additional sources of revenues – 30 Costs – 31 Cash flow – 32

Contents

Additional Info European mail market – 34 Key contacts – 35

bpost at a glance

4

Highlights of 1Q16

bpost at a glance

Improved underlying Domestic Mail evolution • Driven by advertising mail

Cost savings on track and delivered on all cost items • Underlying average FTE reduction of 7341 for the quarter

Outstanding domestic parcels performance, slow-down of international due to strong USD • Domestic: double-digit volume growth driven by e-commerce and C2C;

price/mix effect of -4.6% fully mix related • International: US flows hampered by strong USD, continued growth to &

from China

-4.0%

+14.6%

+ € 0.5m

- € 15.2m

Revenues down 2.0% • Resilient Domestic Mail performance and Parcels growth offset by

anticipated lower SGEI compensation

€ 604.5m

1 i.e. excluding 379 additional FTEs and interims for higher parcels & solutions volumes, Deltamedia integration, new subsidiaries and absorption of holidays leading to a reported average reduction of FTEs and interims of 355

EBITDA up € 3.2m, reduced SGEI compensation fully absorbed

BGAAP net profit of bpost SA/NV up € 2.6m

Outlook maintained

€ 175.9m

€ 90.0m

5

Outlook for 20161

bpost at a glance

Top line

• Underlying Domestic Mail volume decline between 5 and 6%2

• Compensation for SGEI: € 26.8m lower than in 2015 excluding inflation and volume impact

• Domestic Parcels: double digit volume growth

• International Parcels: continued growth in flows from the US but at a slower pace mainly due to strong US dollar

Costs

• Productivity improvements: low end of 800 to 1,200 FTE/year range excluding impact of Deltamedia integration.

• Strong focus on all cost items and factor cost levers (e.g. abolishment of Saturday compensation, tax shift).

Recurring EBITDA and dividend payment at the same level as 2015

FCF

• Gross capex: c. € 80.0m

• Cash generation from operating activities will be negatively impacted by lower compensation and changed payment terms for SGEI (€ -36.8m), the Alpha pay-outs and a settlement on terminal dues with another postal operator.

1 Outlook 2016 excludes the impact of the acquisition of the Belgian activities of Lagardère Travel Retail 2 2Q16 will count 2 working days more, 3Q16 will count 1 day less (except for stamps which will count the same number of days) and 4Q16 will count 1 day less vs.

same quarter of 2015.

6

Belgium’s leading postal operator

bpost at a glance

2015 figures (normalized)

Leading market position in the resilient Belgian mail market with a balanced regulatory framework Focused mail and parcels business with a proven strategy for profitable growth Scope for continued cost improvements Strong financial performance supporting a high level of cash flow generation and dividends Proven performance track record

Built on strong foundations and with ambitious targets

€ 2.4bn revenues

€ 583.6m 24.2% EBITDA

€ 494.4m 20.5% EBIT

€ 328.1m net profit

9.1m letters handled every day

126,000 parcels handled every day

664 678 post franchised offices post points

5 sorting centres

24,703 average # FTE & interims

7

A modern and diversified mail operator

bpost at a glance

Domestic Mail € 1,464m 61%

Transactional mail

1 Including a.o. SGEI compensation for the retail network, philately, retailer products, “unallocated” operating income

€ 918m 38%

Parcels € 341m 14%

Additional sources of revenues € 589m 25%

€ 2,408m normalized revenues 2015

Advertising mail € 251m 11%

Press € 296m 12%

Domestic € 161m 7%

International € 170m 7%

Special Logistics € 10m 0%

International mail € 176m 7%

Value added services € 96m 4%

Banking and finance € 205m 9%

Other1 € 112m 5%

One integrated domestic distribution network for mail and parcels

International player hubs in London LHR and Brussels

strategically located facilities in US, Canada, China, HK, Singapore, the Netherlands and Australia

Revenues % of total

8

Focused strategy to create value and reward shareholders

bpost at a glance

Continue to focus on core

mail business

Generate continued

productivity gains

Value creation &

rewarding of shareholders

+

Keep stakeholders on board

+

Innovate/ grow

within core competencies

9

Continue to focus on core mail business

bpost at a glance

While being impacted by e-substitution mail remains important…

79% satisfaction level for the paper channel (vs. 54% on average for digital channels)1

Volume 2 specific programs to support mail resilience

Pricing

Price-cap formula for single piece mail & USO2 parcels falling within “small user basket” (inflation + quality bonus + unused credit3)

Volume and operational discounts allowed for other USO products (bulk)

Price increases done in practice on a yearly basis (1 January): +1.5% on average in 2016

Offers solutions to address customers’ preference for paper

Proves effectiveness & relevance in marketing mix of Direct Mail

1 Source: bpost commissioned market research, 2016 (1.015 face to face interviews) 2 Universal Service Obligation 3 Quality bonus = [Average quality – 90%]^2 / 1,000; unused credit = cumulated price increases allowed under cap but not applied for last 3 years. Price

increases need to be approved by the regulator

Telco Cie

Telco Cie à votre service:(voir au dos de votre facture)

Telco CieTelco Cie

Telco Cie à votre service:(voir au dos de votre facture)

Transactional Mail

Advertising

10

Innovate/grow within core competencies (1/4) bpost has an established position in parcels…

bpost at a glance

B2B1: ~€ 750-800m

Double market share by 2017

Unique selling proposition

Offer best last mile and broadest delivery options:

• Home delivery 7 d/week & evening delivery

• 1,250 pick-up and drop-off points

• ~146 parcel lockers

• Click & Collect

B2C/C2X1: ~€ 170-230m

Keep market share and capture e-commerce growth

Rationale

How we do it

Solutions for international e-tailers to ship parcels cross border. Main market is US with several lanes (to Canada, Europe, Australia & Asia).

• Direct access to international commercial and postal networks • Asset-light business model • Dedicated international sorting centre & integrated service range (incl.

customs clearance, fulfillment, payment options, track & trace, etc.) • Strategic presence in North America, Europe & Asia

Domestic parcels

International parcels

1 Source market shares: bpost data, Datamonitor, “European Express Benchmarking 2011”

Others

~50% ~5%

Others

11 bpost at a glance

Retail (220 shops)

Con

ven

ien

ce &

P

roxi

mit

y R

etai

l

• Pre-paid services (Alvadis) • Impulse products (Buronville)

Convenience distribution

Pre

ss

Log

isti

cs

Newspaper Magazines International press

Press distribution to 5,345 POS

Non

-P

ress

Lo

gis

tics

Parcels & Logistic Services (735 pick-up drop-off points)

Lagardère Travel retail in Belgium

Sales 2014: € 440.0m • Retail: 41% (€ 180.0m) • Convenience distribution: 18% (€ 80.0m) • Press distribution: 41% (€ 180.0m)

EBITDA 2014: € 15.6m (3.5% margin)

Rationale for bpost

Diversify into the growing proximity & convenience distribution • Grow at least in line with convenience & proximity

retail market (4-6% annually 2015-20) • Footprint expansion (30 to 45 new stores in the

next 3 to 5 years) and remodeling • Accelerate product diversification in order to

enhance profitability

Further enable domestic parcels growth strategy • Improve delivery options and increase coverage

(network of > 1,900 points across Belgium)

• Fully cash financed (consideration not disclosed) • Fully accretive as of 2017 • Preliminary synergy estimate of €4-5m annually

after full integration • Closing and full consolidation after anti-competition

clearance • Total capex planned < € 10m/year

Transaction details

Innovate/grow within core competencies (2/4) Acquisition agreement for the Belgian activities of Lagardère Travel Retail

12 bpost at a glance

Success Partners Europe (Poland)

Rationale for bpost

Support our international e-commerce cross-border parcels strategy • Offer complete service range to international e-commerce customers (including fulfillment)

• Further build out the US market through a complete service offering

Economize on last mile distribution • In-house last mile distribution vs. use of incumbent postal operators or alternative distributors

Freight Distribution Management (Australia)

Innovate/grow within core competencies (3/4) Bolt-on acquisitions in international parcels

• Logistics, distribution and fulfillment across Europe for US e-tailers

• 100% acquisition in Nov. 2015, full consolidation as of Dec. 2015

• Earn-out on 2015 EBITDA (€ 0.2m financial liability)

Initial consideration Sales 2014

Key figures

€ 3.5m

$ 3.4m

• Third Party Logistics (3PL), warehousing, transport & distribution for US e-tailers

• 100% acquisition in March 2016, full consolidation as of April 2016

Initial consideration Sales 2015

EBITDA 2015

Key figures

€ 14.4m

c. € 24.0m

c. € 2.4m

13

Innovate/grow within core competencies (4/4) bpost has other sources of revenues besides mail and parcels

bpost at a glance

Mail originating from foreign countries and delivered to other countries

International mail What?

Asset-light business model and fully variable costs Dedicated sorting centre and hub in Brussels Active in the US, Europe and Asia

Business model

Customer specific solutions which leverage our key assets: last mile, retail network and financial backbone

Value added services Collect and handling services for mail Services at the front door (gaz, water, electricity) Solutions tailored to specific needs

Associate 50/50 with BNP Paribas Fortis (bpost is sole retail agent) Agent of bpost bank ~50% of revenue (commissions)

Payment services, cash at the counter, public finance solutions Direct offering ~50% of revenue

Banking & finance

14

Continuous improvement is in our DNA. We have a 10-year proven transformation track record…

bpost at a glance

2004 • Building of new

sorting centres • Transformation of

the network

2003 Start of continuous optimization of delivery rounds

2009 Implemen-tation of new distribution structure with reduced number of buildings

2011-2017 New strategic ‘Vision 2020’ program in mail service operations to further increase efficiency

2003 New management

& start of the transformation

period

2006 CVC and Danish Post enter into the capital

for 50%-1 share (split 50/50), government holds 50%+1 share

2008 Danish Post

sells its stake to CVC

2013 IPO in June at €14.5/share CVC sells 30% in IPO and

remaining 20% in December

Tran

sfor

mat

ion

jou

rney

K

ey e

ven

ts

Normalized1 EBIT

1 Normalized figures are neither audited nor have been subject to a limited review

2007 Automated round sorting and mail sequencing

15

… and we have plans for further productivity gains

bpost at a glance

Historic FTE evolution Average FTEs, ‘000

-4.0% p.a.

bpost has a systematic, well-rounded approach to identify and capture cost improvements across the entire organization

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

24

39

bpost has plans for further productivity gains supported by natural attrition and Vision 2020

2014 to 15: -711

38% of bpost’s employees are above 50

years old

Age pyramid Headcount per age, 31.12.2015

40-49

7,920

0-39

8,024 9,604

50+

Statutories

Non pay-scale contractuals Pay-scale contractuals

2014 2015

16

Vision 2020 will drive substantial productivity improvements by 2017 in the field

bpost at a glance

Improved operational platform

4 industrial mail sorting facilities

Automated sorting of all formats on MSMs (13 installed end 2015)

Central mailbag preparation

Further FTE reduction by eliminating manual mailbag preparation and transport time to/from start of postmen’s round

1 new sorting facility for mail and parcels (Brussels) with increased capacity merging the two existing facilities (Antwerp and Charleroi)

Further reduction of mail centres from current c. 250 to 60

Enabling

Declining mail

volumes

Increasing parcels volumes

Increasingly complex

product mix

1

17

Alpha targets a decrease in support functions at the headquarters

bpost at a glance

End of August 2014, bpost embarked upon the “Alpha program”, a headcount reduction program targeting the support functions at the corporate headquarters.

2

2610 FTE

Scope of Alpha

analysis

-24%

Productivity improvements

identified

177

625

282

118

Still to do Realized 1Q16

Realized FY15

Realized 4Q14

48

Identified reduction

• At 31 March 2016, 448 FTE were saved in the Alpha scope since the start of the analysis. • Savings

• Estimated average unit cost/FTE: € 68k • FY impact as of 2018: € 42.5m annual savings

• Full restructuring provision booked in 3Q15: € 54.5m; total Alpha pay-outs since start of the program: € 26.3m

18

75

88

85

912

We want to keep stakeholders on board…

bpost at a glance

Distribution quality Percentage letters1 in D+1

+6

2003 2015

Customer satisfaction3

Percent

+13

2003 2015

Environment

1st on the IPC

Environmental Ranking in 2015,

2014 & 2013 Carbon disclosure project: 99B

Committed employer

Commitment & well-being

2015 2014

-12%

Recognize experience

# work accidents

205 people graduated

1 D+1 delivery of domestic single piece items up to 2 kg, stamped at “Prior tariff” 2 Quality scores for 2015 subject to approval by the IBPT/BIPT 3 “Satisfied customers” (score of 5 or above on a scale from 1 to 7 on the question: “Overall, how satisfied are you about bpost?”) based on bpost commissioned

survey by Ipsos-Synovate

Note: more information regarding bpost’s Corporate Social Responsibility is available on the website: http://corporate.bpost.be/sustainability

CO2 reduction objective: -45% by 2020 (vs. 2007)

19

Reward shareholders

bpost at a glance

Dividend Policy

Annual dividend of minimum 85% of BGAAP net profit (unconsolidated)

Interim in December of financial year based on 10-month results

Final in May of year following financial year

Constrained by the net results of a given year + distributable reserves

Distributable reserves built gradually as from 2013, primarily to safeguard the dividend level in case of exceptional costs (€ 97m end 2015)

0.93 1.04 1.05

0.200.22

+2% +12%

2015

1.29 0.24*

2014

1.26

2013

1.13

Interim gross DPS (€) Final gross DPS (€)

* Proposed final gross dividend per share to be approved by General Meeting of May 11, 2016

20

Summary of key financials FY15

bpost at a glance

Note: an Excel download of detailed financials per quarter is available on the website: http://corporate.bpost.be/investors/results-reports-and-presentations/quarterly-results/2016

€ million

1 Normalized figures are neither audited nor have been subject to a limited review

FY14 FY15 FY14 FY15 % ΔTotal operating income (revenues) 2,464.7 2,433.7 2,464.7 2,407.6 -2.3%Operating expenses 1,892.6 1,878.5 1,892.6 1,824.0 -3.6%EBITDA 572.0 555.2 572.0 583.6 2.0%Margin (%) 23.2% 22.8% 23.2% 24.2%EBIT 480.2 466.1 480.2 494.4 3.0%Margin (%) 19.5% 19.2% 19.5% 20.5%Profit before tax 454.1 470.6 454.1 499.0 9.9%Income tax expense 158.6 161.4 158.6 170.9 Net profit 295.5 309.3 295.5 328.1 11.0%FCF 373.3 315.9 373.5 315.9 -15.4%bpost S.A./N.V. net profit (BGAAP) 296.9 287.7 296.9 303.6 2.3%Net Debt/ (Net cash), at 31 Dec. (486.2) (549.5) (486.2) (549.5) 13.0%

Reported Normalized1

Alpha social plan provision of

€ 54.5m

Gain from sale of sizeable building

€ 26.1m

21

Supported by a strong balance sheet

bpost at a glance

Assets

1 bpost has no pension deficit: as is customary in Belgium all pensions are paid as part of national social security

Equity and liabilities

PPE & intangible assets

Inventories

Trade & other receivables

Investments in associates

Other assets

Cash & cash equivalents

Mar 31, 2016

2,285.0

643.7

10.6

328.3

390.0

54.2

858.3

Dec 31, 2015

2,112.0

638.1

11.1

413.5

375.0

58.5

615.7

Total equity

Employee benefits

Trade & other payables

Provisions

Interest-bearing loans & borrowings

Mar 31, 2016

2,285.0

806.9

343.7

1,005.2

63.5 65.8

Dec 31, 2015

2,112.0

694.8

346.2

940.9

64.2 65.8

€ million

297.1 49.1

148.1

108.9

77.7

11.6

Long term benefits • Pension savings days • Quota days • Part-time work

Other long term benefits (disability annuities)

Deferred tax asset

• Mostly unfunded (no investment risk)

• Volatility mainly through the discount rate

• No pension liabilities1

Employee benefit liabilities

Termination (early retirement)

Post retirement

(family allowance, transport, bank, …)

22

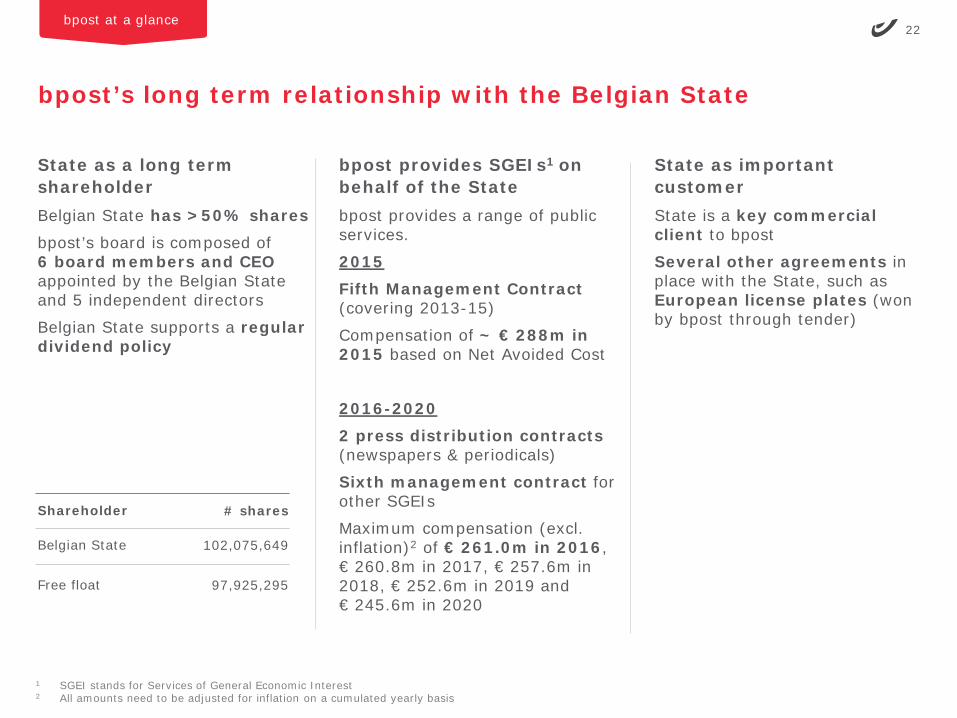

bpost’s long term relationship with the Belgian State

bpost at a glance

State as a long term shareholder Belgian State has >50% shares bpost’s board is composed of 6 board members and CEO appointed by the Belgian State and 5 independent directors

Belgian State supports a regular dividend policy

bpost provides SGEIs1 on behalf of the State bpost provides a range of public services. 2015 Fifth Management Contract (covering 2013-15)

Compensation of ~ € 288m in 2015 based on Net Avoided Cost

2016-2020 2 press distribution contracts (newspapers & periodicals)

Sixth management contract for other SGEIs

Maximum compensation (excl. inflation)2 of € 261.0m in 2016, € 260.8m in 2017, € 257.6m in 2018, € 252.6m in 2019 and € 245.6m in 2020

State as important customer State is a key commercial client to bpost

Several other agreements in place with the State, such as European license plates (won by bpost through tender)

1 SGEI stands for Services of General Economic Interest 2 All amounts need to be adjusted for inflation on a cumulated yearly basis

Shareholder

Belgian State Free float

# shares

102,075,649

97,925,295

23

bpost’s management team and organization

bpost at a glance

Kurt Pierloot Director International & Parcels

Mark Michiels CHRO

Koen Van Gerven CEO

Marc Huybrechts

Director Mail & Retail Solutions

Philippe Dubois Director Mail Services Operations

Koen Beeckmans CFO

Current Trading 1Q16

25

+15.2

+5.9+3.6

EBITDA 1Q16

+175.9

Costs Corporate Additional sources of revenues

-6.3

Parcels Domestic Mail

-8.1

SGEI Compensation

-7.2

EBITDA 1Q15

+172.7

Resilient domestic mail trend and parcels growth combined with further cost reductions led to EBITDA uplift of €+3.2m, thereby fully absorbing the lower SGEI compensation on our bottom-line.

1Q16

Total operating income (revenues)

1 Normalized figures are not audited

€ +10.4m / +6.0%

Normalized1, € million

Sales of building (€ +5.0m) Lower contractual cap

26

Summary of key financials 1Q16

1Q16

€ million

1Q15 1Q16 % ΔTotal operating income (revenues) 616.6 604.5 -2.0%Operating expenses 443.9 428.7 -3.4%EBITDA 172.7 175.9 1.8%Margin (%) 28.0% 29.1%EBIT 151.6 153.9 1.5%Margin (%) 24.6% 25.5%Profit before tax 149.0 149.3 0.2%Income tax expense 52.4 53.4 Net profit 96.6 95.9 -0.7%FCF 298.1 245.9 -17.5%bpost S.A./N.V. net profit (BGAAP) 87.3 90.0 3.0%Net Debt/ (Net cash), at 31 March (785.1) (792.2) 0.9%

Reported

27

Total operating income (revenues)

1Q16

€ million

1 Defined as domestic and Belgian in- and outbound

1Q15 SGEI Organic 1Q16 % Org

Transactional mail 232.6 - -8.8 223.7 -3.8%Advertising mail 64.7 - 0.4 65.1 0.6%Press 74.0 -1.4 0.3 72.9 0.4%

Domestic parcels1 39.5 - 3.6 43.1 9.1%International parcels 41.2 - 0.5 41.7 1.2%Special logistics 2.6 - -0.5 2.1 -19.0%

International mail 45.3 - -5.9 39.3 -13.1%Value added services 24.3 - 1.5 25.8 6.2%Banking and financial 51.7 -3.0 -0.2 48.5 -0.4%Other 29.4 -2.8 -1.7 24.9 -5.7%

Corporate 11.4 - 5.9 17.4 51.9%

616.6 -7.2 -4.9 604.5 -0.8%

Domestic mail

Parcels

Additional sources of revenues

TOTAL

28

Improved domestic mail underlying volume trend of -4.0% driven by advertising mail

1Q16

Total operating income (revenues), € million

1 1Q16 had the same number of business working days as 1Q15 except for stamps which had 1 working day less in 1Q16 vs. 1Q15 2 FY15 corrected for requalification of advertising mail to administrative mail.

• Transactional Mail: continued e-substitution without notable acceleration, shift towards cheaper products (less registered letters).

• Advertising Mail: good direct mail performance in focus sectors, and strong quarter in unaddressed.

• Press: slightly better volume trend versus FY15, mainly driven by periodicals.

FY15 1Q16 FY15 1Q16Transactional mail -5.1% -5.6% -5.3% -5.3%Advertising mail -6.9% 0.1% -4.9% 0.1%Press -2.8% -2.6% -2.8% -2.6%Domestic Mail -5.3% -4.2% -5.0% -4.0%

Reported Underlying 1,2

5.5Price/Mix

Volume

1Q16

-8.1

361.7

-0.6 Working Day impact stamps

-13.1

1Q15 before organic evolution 369.9

SGEI -1.4

1Q15 371.3

29

Excellent growth in domestic parcels but slow-down of international

1Q16

Total operating income (revenues), € million

86.8

+3.6

1Q16

Special Logistics -0.5

International Parcels 0.5

3.6

1Q15 83.2

• Highest volume growth ever of 14.6% driven by excellent e-commerce and continued growth in C2C (online offering).

• Negative price/mix of -4.6% fully mix related (product & client mix).

• From US (€ -1.5m) hampered by strong USD decreasing price competiveness & attractiveness of US goods.

• From China (€ +0.2m) combined with good milk powder volumes to China (€ +1.2m).

1 Defined as domestic and Belgian in- and outbound

Domestic Parcels1

• Mainly due to lower revenues from Sprint activities

30

Additional sources of revenues mainly affected by international mail in part compensated by continued growth in solutions

1Q16

Total operating income (revenues), € million

138.6

-1.7

Banking & Financial -0.2

VAS 1.5

International Mail -5.9

1Q15 before organic evolution 144.9

SGEI -5.8

1Q15 150.6

1Q16

-6.3

Others

• Impact of consequent execution of price strategy (no price discounts granted) to safeguard reasonable profit margins

• Positive contribution of solutions mainly driven by telco contract for decoder swap (€ +0.8m) and City Depot (€ +0.2m).

• Mainly decreasing volumes in philately (€ -0.6m) and lower sales of retailer products (€ -0.9m; mainly utility company front office)

• Mainly impacted by lower volumes of financial transactions managed on behalf of the Belgian State.

31

All cost items contributed to € 15.2m of cost savings

1Q16

428.7

-15.2

1Q16

Other costs -3.2

Other SG&A -3.1

Payroll & Interim -6.7

Transport -2.2

1Q15 443.9

Operating expenses excl. depreciation and amortization, € million

• Average reported FTE reduction of 355 FTE leading to € -5.2m cost savings, underlying FTE reduction is 734 for the quarter.

• Favourable FTE mix of € -4.9m thanks to the recruitment of auxiliary postmen (€ -2.2m) and the reduction of management level FTE (€ -2.6m)

• Negative price effect of € +3.1m explained by phasing elements (a.o. holiday pay related Alpha departures) and merit increase

• Decrease in transport costs linked to the evolution of international activities.

• Higher increase of recoverable VAT for costs and capex incurred in previous years (€ -3.0m).

• Mainly lower 3rd party costs (€ -1.3m), maintenance costs (€ -1.2m) and energy costs (€ -1.3m), partly offset by higher other operating costs

• Higher increase of recoverable VAT (from 14% in 2015 to ~19% in 2016) for 1Q16 expenses (€ -0.8m)

32

Decrease in operating FCF mainly driven by SGEI, Alpha pay-outs and acquisitions.

1Q16

• Proceeds sale of buildings: € +7.3m • Capex: € -1.0m • Final payment for acquisition SPE in Poland: € -0.2m • Acquisition FDM in Australia: € -12.1m • Purchase 24.5% additional shares in LGI: € -20.7m

• Lower compensation and changed payment terms for SGEI: € -36.8m • Lower income tax paid in 1Q16 vs. 1Q15 relating to previous years: € +21.3m • Alpha pay-outs: € -12.0m • Excluding the above:

• Results of operating activities: € +5.7m • Working capital evolution: € -3.8m, mainly due to Social Security payment terms

1 Operating free cash flow = cash flow from operating activities + cash flow from investing activities

€ million 1Q15 1Q16 Delta

Cash flow from operating activities +306.6 +281.1 -25.5Cash flow from investing activities -8.5 -35.1 -26.6Operating free cash flow1 +298.1 +245.9 -52.1Financing activities -0.2 -2.1 -1.9Net cash movement +297.9 +243.9 -54.0

Capex -11.4 -12.4 -1.0

• Payment of a dividend to minority interests: € -2.0m

Additional info

34

A relatively resilient mail market vs. other European operators

European mail market

2008-15 CAGR for addressed mail volumes as reported by major incumbent European postal operators, percent

46

82

142

146

182

193

215

216

223

259

DK

IT

NL

SW

BE

FR

UK

AU

DE

CH

Addressed mail volume per capita 2015 operator level*

1

11

3

8

6

7

10

5

2

4

SOURCE: Company information; Annual reports; Investor presentations; IPC; Eurostat

Note: definition of addressed mail may differ by operator 1 Includes addressed mail 2 Includes addressed mail 3 Includes addressed mail 4 Includes addressed mail 5 Includes mail communication and dialogue marketing 6 Includes addressed mail

7 Includes addressed mail (publishers services excl.) 8 Includes addressed mail excluding press 9 Includes all domestic mail 10 Includes inland addressed mail 11 Includes letter mail and addressed direct mail / media post * Excludes domestic competitors

-2.0

-3.0

-3.0

-3.9

-4.7

-5.0

-9.1

-9.2

-3.4

IT

DK

NL

FR

UK

SW

BE

CH

AU

DE

-11.5

3

9

4

5

6

7

11

10

1

2

(*)

(*)

(*) 2014 data

(*)

(*)

(*) 2008-2014

35

Key contacts

Baudouin de Hepcée

Director External Communication, Investor Relations & Public Affairs

• Email: [email protected] • Direct: +32 (0) 2 276 22 28 • Mobile: +32 (0) 476 49 69 58 • Address: bpost, Centre Monnaie, 1000 Brussels, Belgium

Saskia Dheedene

Manager Investor Relations

• Email: [email protected] • Direct: +32 (0) 2 276 76 43 • Mobile: +32 (0) 477 92 23 43 • Address: bpost, Centre Monnaie, 1000 Brussels, Belgium