investor presentation · market structure and trends – zooplus operates in a large niche market...

TRANSCRIPT

Investor Presentation Deutsches Eigenkapitalforum, Frankfurt

Dr. Cornelius Patt, CEO

Andreas Grandinger, CFO

November 11-13th, 2013

Deutsches Eigenkapitalforum | page 2

This document includes supplemental financial measures that are or may be non-GAAP financial measures. These supplemental

financial measures should not be viewed in isolation as alternatives to measures of zooplus’ financial condition, results of

operations or cash flows as presented in accordance with IFRS in its Consolidated Financial Statements. Other companies that

report or describe similarly titled financial measures may calculate them differently.

This document contains statements related to our future business and financial performance and future events or developments

involving zooplus that may constitute forward-looking statements. We may also make forward-looking statements in other reports,

in presentations, in material delivered to stockholders and in press releases. In addition, our representatives may from time to time

make oral forward-looking statements. Such statements are based on the current expectations and certain assumptions of zooplus’

management, and are, therefore, subject to certain risks and uncertainties. A variety of factors, many of which are beyond zooplus’

control, affect zooplus’ operations, performance, business strategy and results and could cause the actual results, performance or

achievements of zooplus to be materially different from any future results, performance or achievements that may be expressed or

implied by such forward-looking statements or anticipated on the basis of historical trends. Further information about risks and

uncertainties affecting zooplus is included throughout our most recent annual and interim reports, which are available on the

zooplus website, www.zooplus.de. Should one or more of these risks or uncertainties materialize, or should underlying assumptions

prove incorrect, actual results, performance or achievements of zooplus may vary materially from those described in the relevant

forward-looking statement as being expected, anticipated, intended, planned, believed, sought, estimated or projected. zooplus

neither intends, nor assumes any obligation, to update or revise these forward-looking statements in light of developments which

differ from those anticipated.

Due to rounding, numbers presented throughout this and other documents may not add up precisely to the totals provided and

percentages may not precisely reflect the absolute figures.

Safe Harbor Statement

Deutsches Eigenkapitalforum | page 3

zooplus is the leading European e-commerce company for

pet food and pet supplies

» 1st company to start e-commerce for pet supplies

» 1st company to go international with e-commerce for pet supplies

» Among 1st companies to close the gap in size to the leading offline competitors

1999 – 2004 0 to 20 € m Early start and break-even early on

2005 - 2009 28 to 129 € m zooplus goes international

2010 - 2013 193 to 415 € m Intensifying competition and major changes in logistics

2014 - 2019 500 to 1,000 € m Close the gap in size in setup in relevance

zooplus: prepared to stay ahead of the competition

Deutsches Eigenkapitalforum | page 4

Market structure and trends – zooplus operates in a

large niche market with further growth potential

Germany

3.9

UK

4,6

France

3.4

Italy

2,5

Benelux

1,7

Poland

0,6

Rest of

Europe

4,0

Spain 1,3

Market volume by country

€ bn

» 22 € bn total market

» Specialty retail 1/3 of total market

» Steadily growing market with 2-3 % p.a.

» Main categories cats & dogs food

Grocery

and other

63%

Specialty

retail

33%

Online 4%

Sales channels

Source: Euromonitor

2012, zooplus

estimation

» Fragmented market

» No pan-European player in stationary

business

» zooplus only pan-European e-commerce

retailer

Source: Euromonitor

2012, zooplus

estimation

Deutsches Eigenkapitalforum | page 5

The company has consistently put the user experience first

» Driven by e-commerce aptitude (markets, customers,

infrastructure)

» A niche market (only 1/3 of

households own pets)

» Product typically very bulky

(size and weight)

» Retention is the key business

driver

» Market difficult to enter

Operational

excellence

Reliable Marketing / Advertising

Functionality

Price / Performance

Relevance

Customer loyalty and high

retention

The great user experience

Deutsches Eigenkapitalforum | page 6

Local sales office

Fulfilment center

zooplus headquarter

» Similar patterns in customer behavior

» Integrated international

platform

HU

• Significant overlap in assortment, inter-

nationally sourced

• Outsourced pan-

European logistics

structure (D, NL, PL)

• Second label bitiba

in DE, FR, UK and ES

Having operated as a German outfit for the first

five years we now take a pan-European approach

Deutsches Eigenkapitalforum | page 7

Since 2009 the competitive landscape is populating –

offliners, smaller pure-plays and amazon joining the category

DE, FR, UK, IT

Deutsches Eigenkapitalforum | page 8

As a deliberate act to defend our leading position we

adjusted our pricing – impacting our gross margins

41%

42%

38%

39%

37%

36% 35%

34%

67%

64%

64%

61%

63%

65%

70%

74%

H1/2010 (a) H2/2010 (a) H1/2011 H2/2011 H1/2012 H2/2012 H1/2013 H2/2013e

18 months : H2/2010 – H1/2012

Repositioning in price, unchanged

product mix

-5%p

18 months : H1/2012 – H2/2013

Remaining change in margin driven by

change in product mix – less accessories

-1%p / -2%p Margin

dog/cat food

sales

(of total sales)

(a) (a)

(a) : one-off effects of logistics migration adjusted – impacting

other income and logistics / administration costs

Deutsches Eigenkapitalforum | page 9

H1/2010 (a) H2/2010 (a) H1/2011 H2/2011 H1/2012 H2/2012 H1/2013 H2/2013 (e)

At the same time we achieved substantial efficiency gains

– giving us a critical edge over the competition

2013 (e):

€ 415 m

2010 (a):

€ 187 m

81.6

105.8

118.7

138.4

152.3

183.2

198.8

216.0

92.0 86.6 82.7 74.3 70.2

63.0 60.0 50.2

Other countries D.A.CH

Total cost

(without COGS)

on total sales

Total sales

44,1%

32,1%

(a) (a)

(a) : one-off effects of logistics migration adjusted – impacting

other income and logistics / administration costs

Result: a continuous ramp-up of sales, driven by domestic and international markets

Deutsches Eigenkapitalforum | page 10

IT/Admin (incl.

depreciation &

interest)

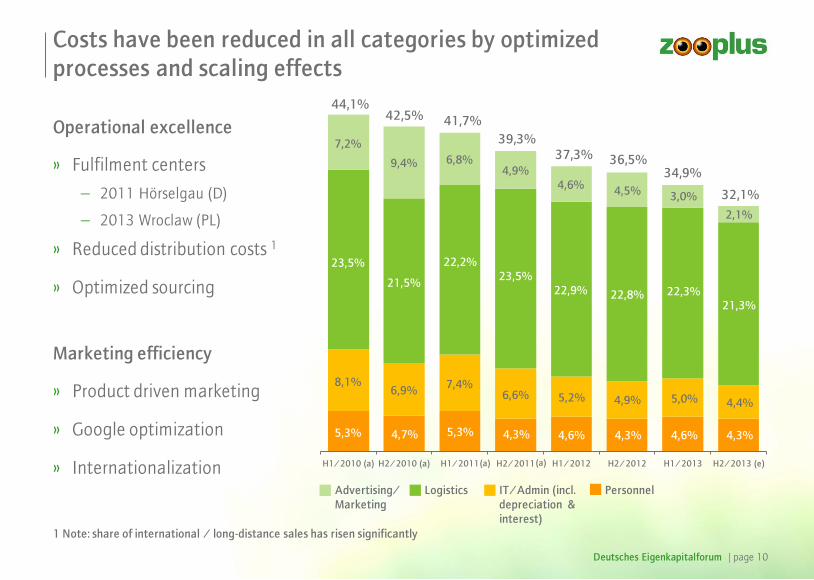

Costs have been reduced in all categories by optimized

processes and scaling effects

Operational excellence

» Product driven marketing

» Google optimization

» Internationalization

» Fulfilment centers

2011 Hörselgau (D)

2013 Wroclaw (PL)

» Reduced distribution costs 1

» Optimized sourcing

Marketing efficiency

H1/2010 (a) H2/2010 (a) H1/2011 H2/2011 H1/2012 H2/2012 H1/2013 H2/2013 (e)

5,3% 4,7% 5,3% 4,3% 4,6% 4,3% 4,6% 4,3%

8,1% 6,9%

7,4% 6,6% 5,2% 4,9% 5,0% 4,4%

23,5%

21,5%

22,2%

23,5%

22,9% 22,8% 22,3% 21,3%

7,2%

9,4% 6,8% 4,9%

4,6% 4,5% 3,0%

2,1%

Advertising/

Marketing

Logistics Personnel

44,1% 42,5% 41,7%

39,3% 37,3% 36,5%

34,9%

32,1%

1 Note: share of international / long-distance sales has risen significantly

(a) (a)

Deutsches Eigenkapitalforum | page 11

Customer loyalty – the winning factor of the business

model – has improved significantly

2009 2010 2011 2012 2013 (e)

143 114

105 99 98

94

64 53 51

114

72 64

145

102

154

92% 80% 94% 99%

84%

63% 90%

70%

<=2009

2010 a

<=2009 <=2009

2010 a+1

2011 a

2012 a

2011 a+1

2010 a+2

<=2009

2013 a

2012 a+1

2011 a+2

2010 a+3

<=2009

Total sales per

annual customer

group (€ m)

143

208

283

369

469

68%

Kohort Analysis – Sales incl. VAT

Deutsches Eigenkapitalforum | page 12

Drivers for the profitability: (a) share of repeat business

and (b) development stage of the supply chain

direct / optimized

supply chain

indirect / intermediate stage

supply chain

new customers

(sales in the year

of acquisition)

repeat customers (consecutive years’ sales)

–

– –

+ +

+

Deutsches Eigenkapitalforum | page 13

While the repeat business has gained a larger share we are

still mid-way in setting up a pan-European supply chain

2010

new customers

2013

repeat customers new customers repeat customers

direct

supply

chain(1)

indirect

supply

chain

(1) D, A, CH, NL, BE

» Sales to repeat customers (sales in the years after the year of acquisition) have risen from 55% to 68%

» The share of sales using indirect supply chains is now 45%, up from 32%

» As zooplus grows towards the € 1 bn most key markets will be served using

direct supply chains / optimized supply chains

indirect

supply

chain

15% 69

40% 168

17%

83

28% 131

43% 88

12% 25

25% 53

20%

42

Sales (€ m) incl. VAT

direct

supply

chain(1)

Deutsches Eigenkapitalforum | page 14

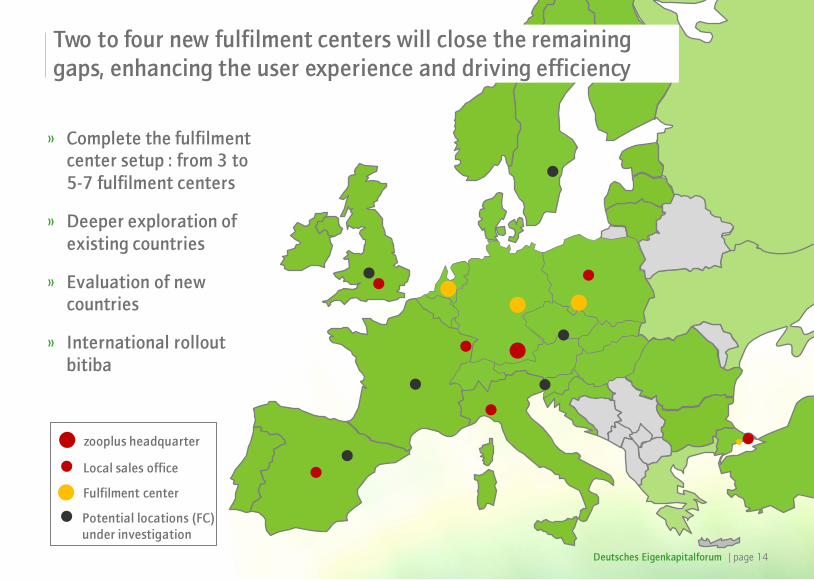

Local sales office

Fulfilment center

zooplus headquarter

» Complete the fulfilment center setup : from 3 to

5-7 fulfilment centers

» Deeper exploration of

existing countries

» Evaluation of new

countries

» International rollout

bitiba

HU

Potential locations (FC)

under investigation

Two to four new fulfilment centers will close the remaining

gaps, enhancing the user experience and driving efficiency

Deutsches Eigenkapitalforum | page 15

Current guidance and mid-term outlook

Total Sales EBT ROS

2014 : € 500 mm + > € 5 mm > 1,0%

Total Sales EBT ROS

2015 : € 600 mm > € 10 mm ~ 2,0%

2016 : € 700 mm ~ € 25 mm ~ 3,5%

Current guidance – for next year

Outlook from today’s perspective – mid-term

EBT: Earnings before taxes ROS: Return on sales = EBT on Total Sales

Deutsches Eigenkapitalforum | page 16

P&L

in mm EUR

9M 2013 9M 2012 D abs D %

Total Sales 306,7 237,8

abs. 68,9 52,7

D in % 29% 28%

COGS 201,4 65,7%

151,4 63,7%

50,0 2,0%

Logistics 67,3

22,0%

54,7 23,0%

12,6 -1,1%

Payment 4,4

1,4%

3,3 1,4%

1,1 0,0%

Customer Acquisition 8,3

2,7%

11,7 4,9%

-3,4 -2,2%

Personnel 13,8 4,5%

10,8 4,5%

3,0 0,0%

G&A 9,5

3,1%

8,0 3,4%

1,4 -0,3%

EBITDA 2,0

0,7%

-2,1 -0,9%

4,1 1,6%

EBT 1,2

0,4%

-2,7 -1,1%

3,9 1,5%

EPS in EUR 0,05 -0,33 0,4 -

Cash Flow

CF from Operations -2,9 -3,7 0,8 -

P&L structure 9M / 2013

» Total sales increase by 29% vs. PY

» COGS increased due to better prices for

customers and change in product mix

» Significant cost reductions in logistics,

customer acquisition and G&A as % of

total sales

» Positive EBT and strong improvement compared to PY

Deutsches Eigenkapitalforum | page 17

P&L

in mm EUR

Q3 2013 Q3 2012 D abs D %

Total Sales 107,8 85,4

abs. 22,4 19,0

D in % 26% 33%

COGS 71,5

66,3%

55,2 64,6%

16,3 1,7%

Logistics 23,0

21,3%

19,8 23,2%

3,2 -1,9%

Payment 1,6

1,4%

1,2 1,4%

0,4 0,1%

Customer Acquisition 2,3

2,1%

4,6 5,4%

-2,3 -3,3%

Personnel 4,6

4,3%

3,7 4,3%

0,9 0,0%

G&A 2,9

2,7%

2,6 3,1%

0,3 -0,4%

EBITDA 2,0

1,8%

-1,6 -1,9%

3,6 3,7%

EBT 1,7

1,6%

-1,8 -2,1%

3,5 3,7%

EPS in EUR 0,15 -0,22 0,4 -

P&L structure Q3 / 2013

» Total sales increase by 26% vs. PY

» COGS increased due to better prices for

customers and change in product mix

» Significant cost reductions in logistics,

customer acquisition and G&A as % of

total sales

» Positive EBT ratio of 1,6%

Deutsches Eigenkapitalforum | page 18

Balance Sheet Sept. 30th, 2013

in mm EUR Sep. 30th, 2013 Dec. 31th, 2012 D abs

A. Non-Current Assets

I. PP&E 0,6 0,7 -0,1

II. Intangible Assets 4,1 2,1 2,0

III. Financial Assets 0,0 0,1 -0,1

IV. Deferred Tax Assets 7,6 8,2 -0,6

Total Non-Current Assets 12,3 11,1

B. Current Assets

I. Inventories 40,2 32,9 7,3

II. Trade Receivables 11,2 9,3 1,9

III. Other Current Assets 5,6 9,1 -3,5

IV. Cash and Cash Equivalents 7,6 3,0 4,6

Total Current Assets 64,6 54,3

76,9 65,4 11,5

Assets Equity and Liabilities

in mm EUR Sep. 30th, 2013 Dec. 31th, 2012 D abs

A. Equity

I. Capital Subscribed 6,1 6,1 0,0

II. Capital Reserves 50,0 49,4 0,6

III. Other Reserves 0,0 -0,1 0,1

IV. Profit and Loss carried forward -21,2 -21,5 0,3

Total Equity 34,9 33,9

B. Current Liabilities

I. Trade payables 12,0 16,8 -4,8

II. Financial Liabilities 13,0 2,0 11,0

III. Derivative Financial Instruments

0,1 0,3 -0,2

IV. Other Current Liabilities 12,8 9,1 3,7

V. Tax Liabilites 0,3 0,1 0,2

VI. Provisions 2,8 2,2 0,6

VII. Deferred Income 1,0 0,9 0,1

Total Current Liabilities 42,0 31,5

76,9 65,4 11,5

Equity (Ratio in %) 45,4% 51,9%

» Attractive balance sheet structure - equity ratio > 40%

» Investments in growth already covered in result

» No impairment risks

» Highly efficient capital utilization

» No further equity raisings envisaged

» Attractive and long-term financing lines in place

Deutsches Eigenkapitalforum | page 19

Shareholder structure and market capitalization

1 Burda Digital Ventures GmbH

2 Others

3 BDV Beteiligungen GmbH & Co. KG

4 Burda GmbH

5 Capital Research

6 The Nomad Investment Partnership LP

7 Ruane, Cunniff & Goldfarb Inc.

8 Wasatch Advisors

9 Burda (others)

22.70 %

5.39 %

7.99 %

2.81 %

7.98 %

8.60 %

24.35 % 5.90 %

14.28 %

1

2

5

9 8 7

6

4

3

Shareholder structure

+82%

Share price development

Jan. 1st, 2013: € 31.95 Nov. 8th, 2013: € 58.21 Market capitalization ~ € 350 m

Free float (according to Deutsche Börse definition): 49,96%