investor & analyst presentation · investor & analyst presentation - annual report 2018 |...

TRANSCRIPT

Investor & Analyst PresentationCapital Markets Day

London, March 20th, 2019

Dr. Cornelius Patt, CEO

Andreas Grandinger, CFO

Investor & Analyst Presentation - Annual Report 2018 | page 2

This document includes supplemental financial measures that are or may be non-GAAP financial measures. These supplemental

financial measures should not be viewed in isolation as alternatives to measures of zooplus’ financial condition, results of

operations or cash flows as presented in accordance with IFRS in its Consolidated Financial Statements. Other companies that

report or describe similarly titled financial measures may calculate them differently.

This document contains statements related to our future business and financial performance and future events or developments

involving zooplus that may constitute forward-looking statements. We may also make forward-looking statements in other

reports, in presentations, in material delivered to stockholders and in press releases. In addition, our representatives may from

time to time make oral forward-looking statements. Such statements are based on the current expectations and certain

assumptions of zooplus’ management, and are, therefore, subject to certain risks and uncertainties. A variety of factors, many of

which are beyond zooplus’ control, affect zooplus’ operations, performance, business strategy and results and could cause the

actual results, performance or achievements of zooplus to be materially different from any future results, performance or

achievements that may be expressed or implied by such forward-looking statements or anticipated on the basis of historical

trends. Further information about risks and uncertainties affecting zooplus is included throughout our most recent annual and

interim reports, which are available on the zooplus website, www.zooplus.de. Should one or more of these risks or uncertainties

materialize, or should underlying assumptions prove incorrect, actual results, performance or achievements of zooplus may vary

materially from those described in the relevant forward-looking statement as being expected, anticipated, intended, planned,

believed, sought, estimated or projected. zooplus neither intends, nor assumes any obligation, to update or revise these forward-

looking statements in light of developments which differ from those anticipated.

Due to rounding, numbers presented throughout this and other documents may not add up precisely to the totals provided and

percentages may not precisely reflect the absolute figures.

Safe Harbor Statement

Investor & Analyst Presentation - Annual Report 2018 | page 3

Your presenters today

Management owns around 5% of the shares of the company

Dr. Cornelius Patt

CEO, Founder

Andreas Grandinger

CFO

» Corporate Management

» Business Development &

Systems Development

» IT

» Human Resources

» Finance

» Controlling

» Legal

» Internal Audit

» Investor Relations

Investor & Analyst Presentation - Annual Report 2018 | page 4

Annual results 2018Capital Markets Day

London, March 20th, 2019

Dr. Cornelius Patt, CEO

Andreas Grandinger, CFO

Investor & Analyst Presentation - Annual Report 2018 | page 5

zooplus continued to improve its market leadership position in 2018

» Sales increased by 21% to EUR 1,342 m

− European market leader position in online retailing sustained

− Double-digit growth rates in all 30 European markets

» Customer loyalty with 95% sales retention

− High loyalty of existing customers shows strength of business model

− Acceleration of new customer growth in H2 2018

» Logistics infrastructure significantly expanded

− New fulfillment centers in UK, Poland and Spain

» Result before tax (EBT) of EUR -2.3 m

− Significantly improved EBT in H2 2018 (EUR 6.9 m)

» Free cash flow of EUR 14.3 m

− Further improvement in working capital from 5.1% to 2.7% of sales

Investor & Analyst Presentation - Annual Report 2018 | page 6

The growth path continued and sales have increased by EUR 231 m in 2018

Sales 2012-2018 (EUR m)

1) in local currencies201720162013 2014

1,342

2012 2015 2018

319

543

711

407

1,111

909

+88

+136

+168

+198

+202

+231

85%91%

94%

92%

94%1

93%

93%1

22%28%31%33%28%30%Sales growth

vs. PY

Repeat

customer sales

New customer

sales (1st year)

21%

94%

95%1

Investor & Analyst Presentation - Annual Report 2018 | page 7

Sales of over EUR 1.3 bn in 2018

1,111

1,342

2017 2018

23%

11%

Food Non-Food

+ 21%

FX adjusted + 21%

Sales (EUR m) Sales growth by category

Investor & Analyst Presentation - Annual Report 2018 | page 8

Quarter on quarter sales development

in EUR m

+ 66

257

208

165 168178

200

2015 2016 2017 2015 2016 2015 2016 2015 20162017 201720172018

221 227

253

Quarter 1 Quarter 2 Quarter 3 Quarter 4

323

260278

316

+ 49+ 39

+ 51

+ 52320

+ 60

2018

331

+ 53

2018

368

+ 63

2018

Investor & Analyst Presentation - Annual Report 2018 | page 9

Private label sales continued to grow significantly faster than branded products in 2018

Private label growth

» Private label food and cat litter

» Strong focus on increasing

share of private label

» Margin advantage of private

label reinvested in growing

private label business

36% 35%

2017 2018

Investor & Analyst Presentation - Annual Report 2018 | page 10

Sales 2018

HU

Source: zooplus sales, unaudited data, growth rates compared to 2017;

market shares based on Euromonitor 2016 market data and zooplus estimation

112m

Total market 2018

23bnSales zooplus

in 2018

DK, SE,

FI, NO

D,A,CHCZ, SK, HU, RO,

SI, HR, BG, TR,

GR, LV. LT, EE

ES, PT

zooplus is the online market leader across Europe

NL, BE, LU

+24%

+17%

+22%

+20%

+20%

+35%

+16%

+20%

86m

149m

387m

84m

224m

82m

108m

1,342m

zooplus market

share in 2018

7.0%

2.7%

6.0%

4.7%

4.4%

5.7%

8.2%

5.4%

5.8%

» EUR 1,342 m,

sales growth rate +21%

» Double-digit sales growth

rates in all countries

UK, IE

IT

FR, MC

Sales growth in

2018

110m16.0%

+37%

PL

Investor & Analyst Presentation - Annual Report 2018 | page 11

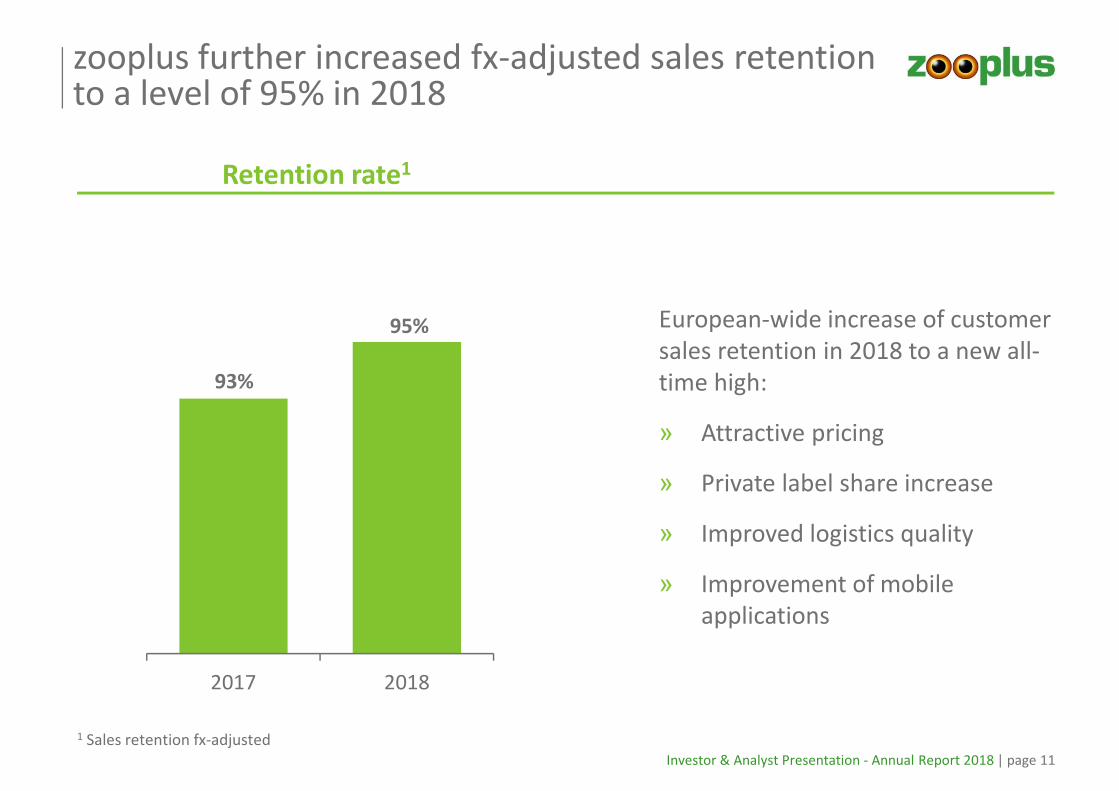

zooplus further increased fx-adjusted sales retention to a level of 95% in 2018

93%

95%

2017 2018

Retention rate1

European-wide increase of customer

sales retention in 2018 to a new all-

time high:

» Attractive pricing

» Private label share increase

» Improved logistics quality

» Improvement of mobile

applications

1 Sales retention fx-adjusted

Investor & Analyst Presentation - Annual Report 2018 | page 12

New customer trend positive since Q3 2018

755

651

694

818

Q1 2018 Q2 2018 Q3 2018 Q4 2018

New customers (in k)

» New customer trend positive

since Q3 2018

» More focused approach of new

customer acquisition

- Stronger focus on registering

- Google bidding adaptations

» Growth of new customer intake

supported by higher marketing

acquisition costst/o registered 644 545 594 722

t/o unregistered 111

106

100

96

Investor & Analyst Presentation - Annual Report 2018 | page 13

Basket value with positive development since Q2 2018

53.6

54.5 54.754.9

Q1 2018 Q2 2018 Q3 2018 Q4 2018

Basket value (EUR)

» Reduction of non-profitable

orders

» Adaptation of free shipping

thresholds

» Reduction of parcel split ratio

» Additional logistics fee charged

for selected orders that need

more than one parcel

Investor & Analyst Presentation - Annual Report 2018 | page 14

Long-term gross margin decline halted

2012 2013 2014 2015 2016 2017 2018

Gross margin1

1 Sales - COGS; years prior to 2018 adjusted from published

external figures to new IFRS 15

in % of sales

37.4%35.8%

32.3%

30.6%

28.7% 28.5% 28.7%

» Less customer and

transactional

discounts

» Reduction of non-

profitable orders

» Higher charges for

shipping

» Margin increase

due to better

sourcing

Investor & Analyst Presentation - Annual Report 2018 | page 15

2017 2018

Gross margin improvement in spite of higher food share

2017 2018

» Supplier contribution

for marketing etc.

since 2018 within

gross margin (IFRS 15)

» Other income:

dunning fees,

exchange rate gains,

others

+ 0.2%p

28.5% 28.7%

in % of sales

1 Share of food and cat litter

on sales

+ 1.4%p

83.5%84.9%

2017 2018

in % of sales

+ 0.1%p

29.2% 29.3%

3 Gross margin + other income on sales2 Sales - CoGS

Total margin3Gross margin2Product mix1

Investor & Analyst Presentation - Annual Report 2018 | page 16

3.2% 3.3%

3.0% 3.3%

19.8% 19.7%

1.7% 2.2%

2017 2018

29.5%

Cost leadership position in 2018 sustained but reflects stronger investment focus

Total margin1

» Marketing up for new

customer acquisition

» IT/Admin impacted by

higher depreciation

» Personnel reflects

stronger IT development

resources

» Increase in depreciationIT/Admin/ (incl. depreciation

& interest)

Advertising/

Marketing

Logistics2

Personnel4

1.0% 1.1% Payment3

28.8%

29.3%29.2%

+ 0.7%p

Total margin & cost structure (in % of sales)

1 gross margin + other income on sales2 logistics costs reclassified to depreciation according to IAS 173 impairment expenses on financial assets reclassified to payment4 including LTI & SOP; own work capitalized reclassified to personnel

Investor & Analyst Presentation - Annual Report 2018 | page 17

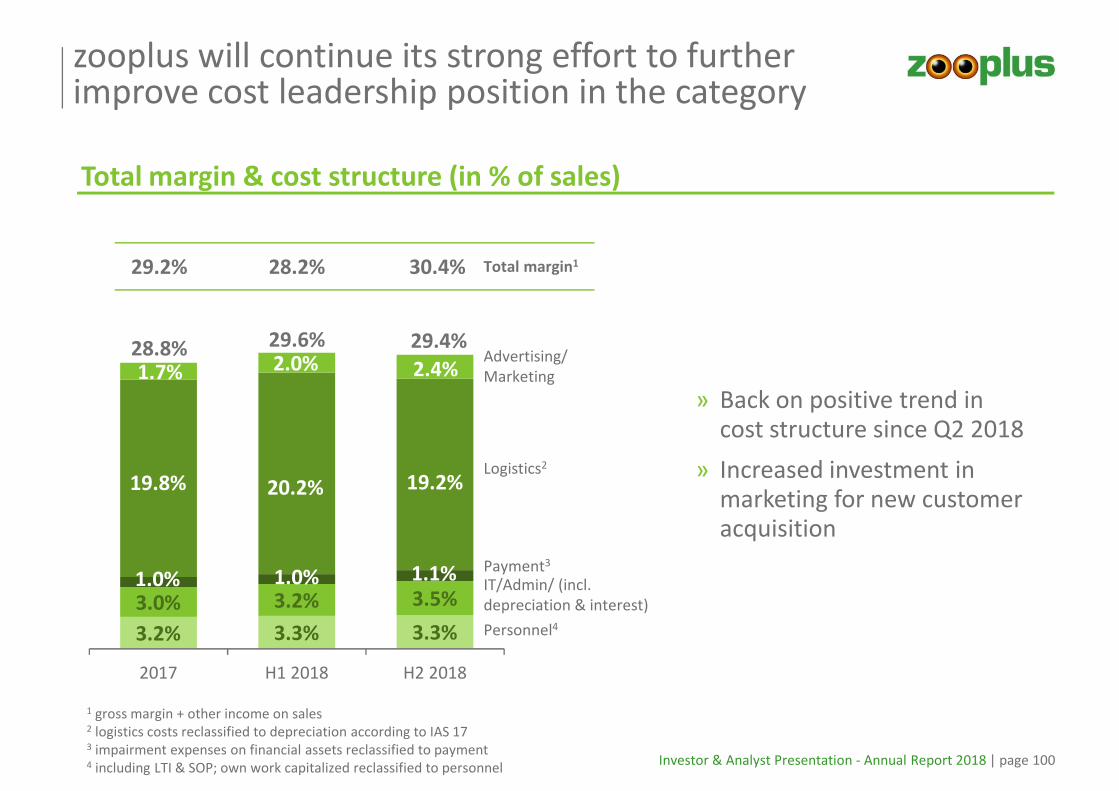

Significantly improved cost position in H2 2018

Total margin & Cost structure (in % of sales)

3.3% 3.3%

3.2% 3.5%

20.2% 19.2%

2.0% 2.4%

H1 2018 H2 2018

Total margin1

1.0% 1.0%

29.4%

1.1%IT/Admin/ (incl.

depreciation & interest)

Advertising/

Marketing

Logistics2

Personnel4

Payment3

30.4%

29.6%

28.2%

» Back on positive trend in cost structure since H2 2018

» Significant reduction in logistics costs (efficiency + increased value per parcel)

» IT/Admin solely impacted by higher depreciation

» Increased investment in marketing for new customer acquisition

1 gross margin + other income on sales2 logistics costs reclassified to depreciation according to IAS 173 impairment expenses on financial assets reclassified to payment4 including LTI & SOP; own work capitalized reclassified to personnel

Investor & Analyst Presentation - Annual Report 2018 | page 18

zooplus earnings before tax (EBT) in 2018 reflects investment in marketing, IT and logistics infrastructure

8.88.6

2017 2018

4.1

-2.3

2017 2018

- 0.2 -6.4

in % of sales 0.8 % 0.6 %

in % of sales 0.4 %

-0.2 %

EBITDA (EUR m) EBT (EUR m)

Logistics costs reclassified to depreciation according to IAS 17

Investor & Analyst Presentation - Annual Report 2018 | page 19

Profitability of repeat customers business invested to grow the business with long-term perspective

Repeat customer and new customer contribution (EUR m)

271 24% - 17 - 6.3%840 76% 21 + 2.5%

New customers(sales in the year of acquisition)

Repeat customers(consecutive year’s sales)

2017

Net

Sales

% of

total z+

EBT EBT-

margin

Net

Sales

% of

total z+

EBT EBT-

margin

293 22% - 23 - 7.8%1049 78% 21 + 2.0%2018

+ 0.4% + 3.6%

H1 H2

2018

Investor & Analyst Presentation - Annual Report 2018 | page 20

Cash flow from

operating

activities

Cash flow from

investing activities

Free cash flow

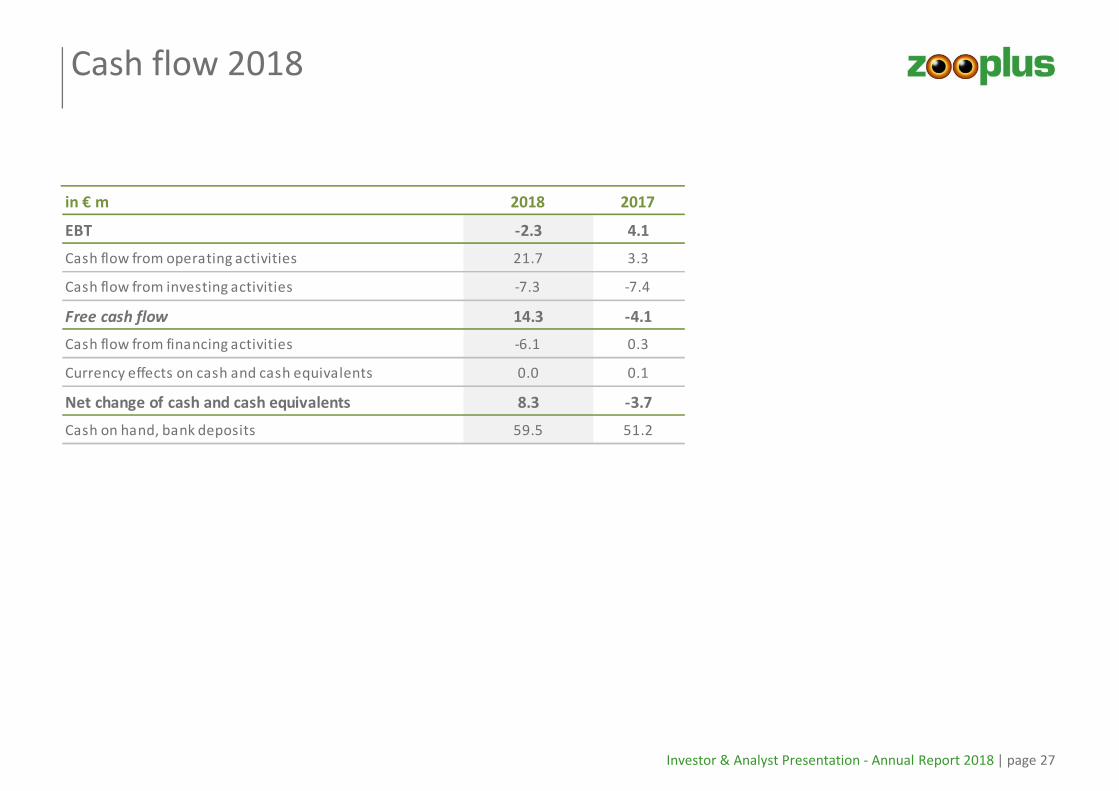

Free cash flow positive with EUR 14 m in 2018

2018

21.7

-7.3

14.3

Operating and free cash flow (EUR m)

» Financing sales growth of EUR 231 m and EBT of EUR - 2.3 m internally

» Main driver: significantly improved working capital

Investor & Analyst Presentation - Annual Report 2018 | page 21

Working Capital has been further improved in 2018

Working capital in % sales

9.5%

8.1%

6.3%

5.1%

2.7%

2014 2015 2016 2017 2018

» Continued focus on

working capital

» Main driver:

Improvement in

supplier payment days

Working Capital = inventory + prepayments + receivables - liabilities

Average of quarters Q1 – Q4

Investor & Analyst Presentation - Annual Report 2018 | page 22

zooplus shows a strong balance sheet at end of 2018

» Positive cash balance of EUR 60 m at 12/31/2018

» Equity ratio of 37%

» No financial debt

» Credit lines of EUR 50 m – until end 2020 without guarantees

Solid foundation for further growth

Investor & Analyst Presentation - Annual Report 2018 | page 23

2018 results

Q & A

Investor & Analyst Presentation - Annual Report 2018 | page 24

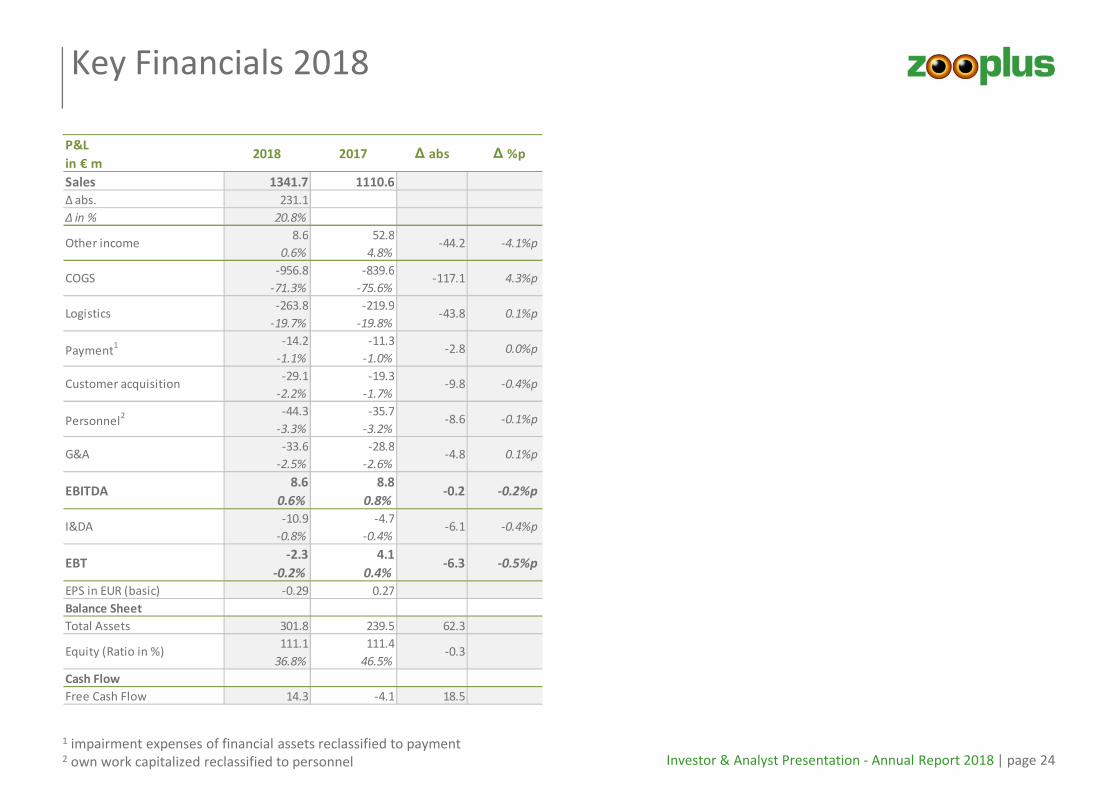

P&L

in € m

Sales 1341.7 1110.6

Δ abs. 231.1

Δ in % 20.8%

8.6 52.8

0.6% 4.8%

-956.8 -839.6

-71.3% -75.6%

-263.8 -219.9

-19.7% -19.8%

-14.2 -11.3

-1.1% -1.0%

-29.1 -19.3

-2.2% -1.7%

-44.3 -35.7

-3.3% -3.2%

-33.6 -28.8

-2.5% -2.6%

8.6 8.8

0.6% 0.8%

-10.9 -4.7

-0.8% -0.4%

-2.3 4.1

-0.2% 0.4%

EPS in EUR (basic) -0.29 0.27

Balance Sheet

Total Assets 301.8 239.5 62.3

111.1 111.4

36.8% 46.5%

Cash Flow

Free Cash Flow 14.3 -4.1 18.5

Other income -44.2 -4.1%p

COGS -117.1 4.3%p

Logistics -43.8 0.1%p

Payment1 -2.8 0.0%p

EBITDA -0.2 -0.2%p

Customer acquisition -9.8 -0.4%p

Personnel2 -8.6 -0.1%p

2018 2017 ∆ abs ∆ %p

Equity (Ratio in %) -0.3

I&DA -6.1 -0.4%p

EBT -6.3 -0.5%p

G&A -4.8 0.1%p

Key Financials 2018

1 impairment expenses of financial assets reclassified to payment2 own work capitalized reclassified to personnel

Investor & Analyst Presentation - Annual Report 2018 | page 25

Profit & Loss 2018

abs % abs %

Sales1341.7 100.0% 1110.6 100.0%

Other income 8.6 0.6% 52.8 4.8%

Own work capitalized 2.8 0.2% 3.5 0.3%

Cost of materials -956.8 -71.3% -839.6 -75.6%

Personnel costs -47.1 -3.5% -39.1 -3.5%

Depreciation -10.1 -0.8% -4.3 -0.4%

Impairment expenses on financial

assets -2.7 -0.2% 0.0 0.0%

Other expenses -337.9 -25.2% -279.3 -25.1%

thereof logistics / fulfillment -263.8 -19.7% -219.9 -19.8%

thereof marketing -29.1 -2.2% -19.3 -1.7%

thereof payment -11.4 -0.9% -11.3 -1.0%

thereof other costs -33.6 -2.5% -28.8 -2.6%

Earnings before interest and taxes

(EBIT) -1.5 -0.1% 4.4 0.4%

Financial income 0.0 0.0% 0.0 0.0%

Financial expenses -0.8 -0.1% -0.4 0.0%

Earnings before taxes (EBT) -2.3 -0.2% 4.1 0.4%

Taxes on income 0.2 0.0% -2.1 -0.2%

Consolidated net result -2.1 -0.2% 1.9 0.2%

Differences from currency translation -0.7 -0.1% -0.5 0.0%

Hedge reserve 0.3 0.0% -2.0 -0.2%

Items that may be relclassified

subsequently to profit or loss -0.4 0.0% -2.5 -0.2%

Comprehensive income -2.5 -0.2% -0.6 -0.1%

Earnings per share in €

basic -0.29 - 0.27 -

diluted -0.29 - 0.27 -

in € m2018 2017

Investor & Analyst Presentation - Annual Report 2018 | page 26

Balance Sheet as of December 31st, 2018

Assets Equity and Liabilities

in € mDec. 31st.

2018

Dec. 31st.

2017∆ abs

A. Non-current assets

I. PP&E 55.9 15.0 40.9

II. Intangible assets 14.2 13.1 1.1

III. Other financial assets 0.0 0.0 0.0

IV. Deferred tax assets 0.0 0.0 0.0

Total non-current assets 70.0 28.1 42.0

B. Current assets

I. Inventories 107.6 104.5 3.0

II. Advance payments 0.4 0.6 -0.2

III. Accounts receivable 28.1 26.4 1.8

IV. Other current assets 16.1 27.5 -11.3

V. Contract assets 19.0 0.0 19.0

VI. Tax receivables 0.9 1.2 -0.3

VII.Derivative financial

instruments0.0 0.0 0.0

VIII. Cash and cash equivalents 59.5 51.2 8.3

Total current assets 231.7 211.4 20.3

301.8 239.5 62.3

in € mDec. 31st.

2018

Dec. 31st.

2017∆ abs

A. Equity

I. Capital subscribed 7.1 7.1 0.0

II. Capital reserves 100.8 98.8 2.0

III. Other reserves -1.8 -1.4 -0.4

IV. Pro fit and Loss carried forward 4.9 6.8 -1.9

Total equity 111.1 111.4 -0.3

B. Non-current liabilities 41.4 11.1 30.3

C. Current liabilities

I. Accounts payable 99.7 78.1 21.6

II Derivative financial instruments 0.1 0.5 -0.5

III. Other current liabilities 19.9 24.6 -4.6

IV. Contract liabilities 17.1 0.0 17.1

V. Tax liabilites 0.1 1.3 -1.2

VI. Finance lease 9.8 2.1 7.7

VII. Provisions 2.6 7.4 -4.9

VIII. Deferred income 0.0 2.9 -2.9

Total current liabilities 149.3 117.0 32.3

301.8 239.5 62.3

Investor & Analyst Presentation - Annual Report 2018 | page 27

Cash flow 2018

in € m 2018 2017

EBT -2.3 4.1

Cash flow from operating activities 21.7 3.3

Cash flow from investing activities -7.3 -7.4

Free cash flow 14.3 -4.1

Cash flow from financing activities -6.1 0.3

Currency effects on cash and cash equivalents 0.0 0.1

Net change of cash and cash equivalents 8.3 -3.7

Cash on hand, bank deposits 59.5 51.2

Investor & Analyst Presentation - Annual Report 2018 | page 28

Strategy & OutlookCapital Markets Day

London, March 20th, 2019

Dr. Cornelius Patt, CEO

Andreas Grandinger, CFO

Investor & Analyst Presentation - Annual Report 2018 | page 29

Main takeaways from today’s presentation about zooplus’ strategic perspective

» Pet supplies continues to be a very attractive and growing market.

» zooplus is by far market leader online and already No. 2 in the total market. zooplus has a very loyal

and continuously growing customer base of around 7 m customers.

» Competition comes from amazon, brick-and-mortar and small regional onliners. Overall zooplus’

competitive position is today stronger than 12 months ago.

» Amazon is the major competitor but zooplus differentiates today significantly from amazon and

tomorrow even more. There is enough room for growth for a specialist next to the generalist amazon.

» zooplus has the most relevant platform for specialist pet supplies manufacturers and is the only

specialist platform in the category that can efficiently ship a parcel to any place in Europe.

» Sustainable new customer growth but not at any price continues to be priority for zooplus. Sales

growth might be slightly lower going forward but future outlook continues to be very positive.

» zooplus has a clear long-term perspective for future structural profitability of 5-7% EBITDA margin

with a stabilized / improved gross margin and further optimization of cost structure.

» Opportunities arise from brand development and social media marketing, pricing optimization,

private label share increase, more detailed data analyses especially for CRM and suppliers as well as

pet services platform integration to develop the most customer centric pet ecosystem in Europe.

Investor & Analyst Presentation - Annual Report 2018 | page 30

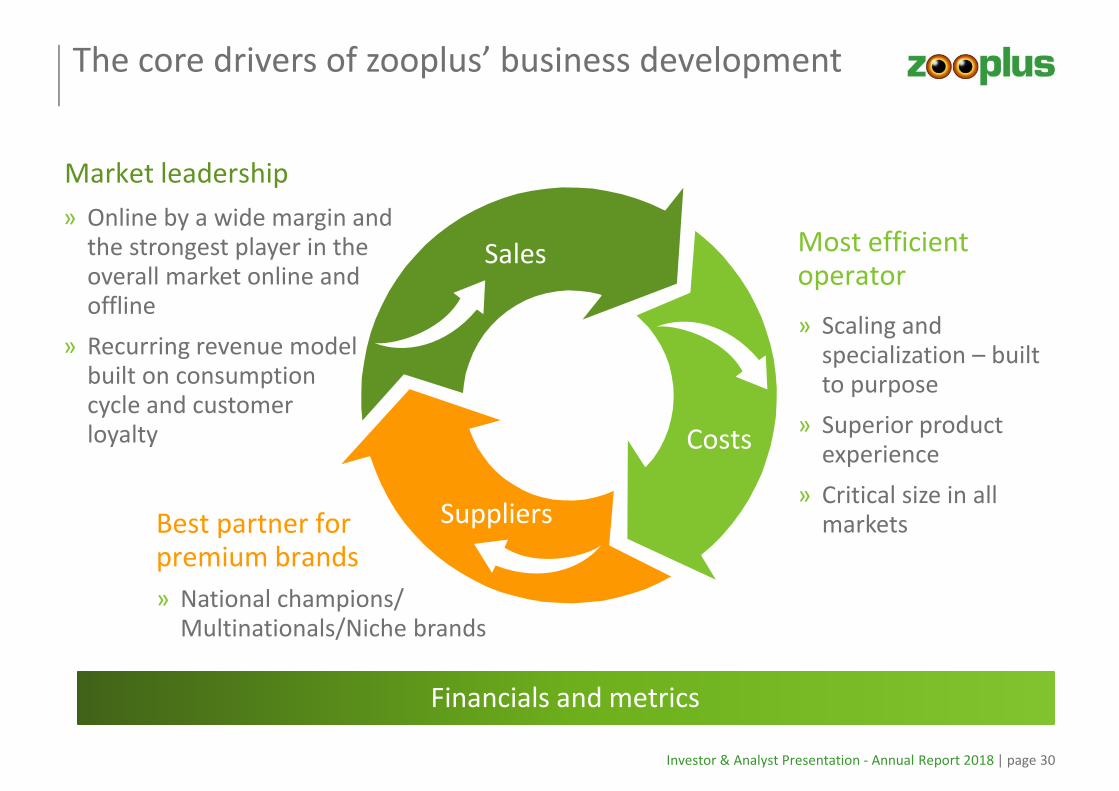

The core drivers of zooplus’ business development

» Online by a wide margin and the strongest player in the overall market online and offline

» Recurring revenue model built on consumption cycle and customer loyalty

» Scaling and specialization – built to purpose

» Superior product experience

» Critical size in all markets

Financials and metrics

Sales

Costs

Suppliers

Market leadership

Most efficient operator

» National champions/ Multinationals/Niche brands

Best partner for premium brands

Investor & Analyst Presentation - Annual Report 2018 | page 31

Different to amazon

Margin focus / private label growth

Market place / intermediary for services

Efficiency and scale

zooplus’ key priorities for 2019 and beyond

Sales growth (retention + new customers)

1

2

3

4

5

Building Europe’s most relevant and customer centric pet platform for consumers and suppliers

Market & Competition

Investor & Analyst Presentation - Annual Report 2018 | page 33

European pet supplies market is a very attractive and growing market

Pet supplies market in Europe 2009-2025e (gross sales EUR bn)

» Ownership of pets is on the rise in Europe

» Humanization of pets drives spending

» Trend towards more premium products

» Market is resilient to economic cycles

» Consumables recurring revenue – subscription like

» No technology and fashion obsolescence risk

» Low product return rates

20 21 2223 23

2425 26 26

27

33

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 … 2025e

Source: Euromonitor 2016 and zooplus estimation

CAGR +3% p.a.

Investor & Analyst Presentation - Annual Report 2018 | page 34

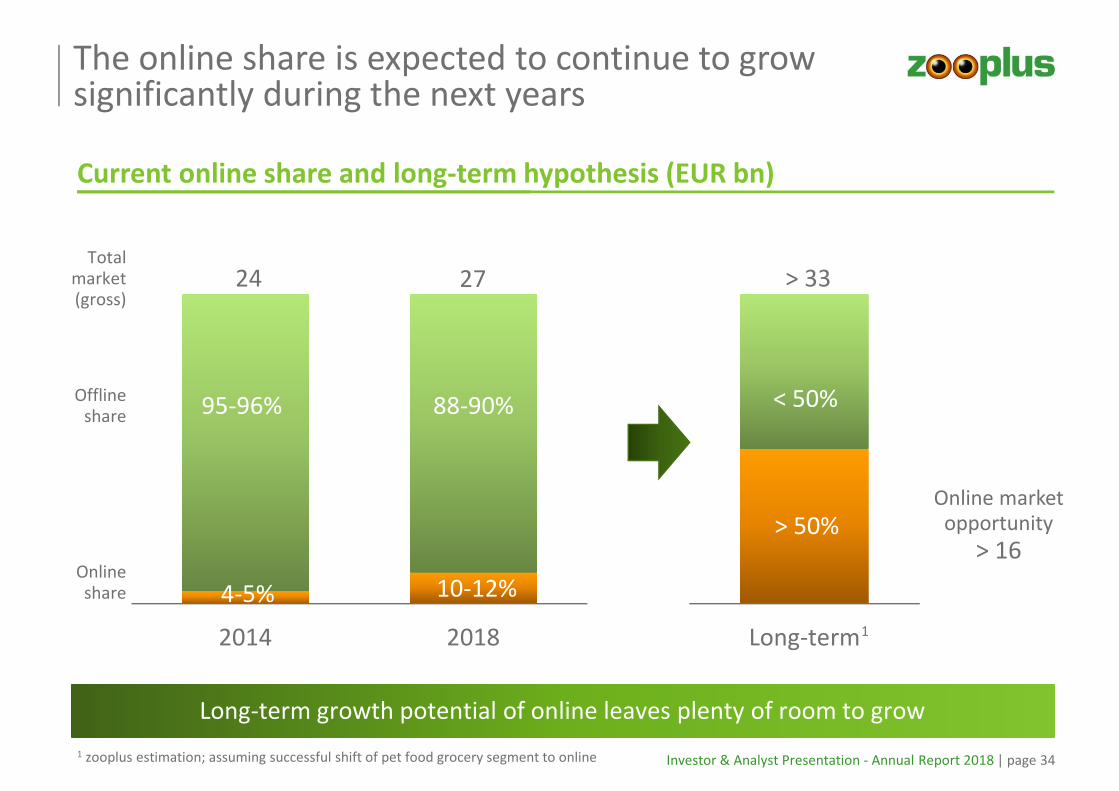

The online share is expected to continue to grow significantly during the next years

Current online share and long-term hypothesis (EUR bn)

2014 2018

24 27

10-12%

88-90%

8-10%

Offline share

Online share

Total market (gross)

< 50%

Long-term

> 50%

> 33

Online market opportunity

> 16

Long-term growth potential of online leaves plenty of room to grow

4-5%

95-96%

1 zooplus estimation; assuming successful shift of pet food grocery segment to online

1

92-90%

Investor & Analyst Presentation - Annual Report 2018 | page 35

zooplus strengthened No. 2 position in Europe in 2018 and is well on its way towards market leadership

Net sales and growth 2018 – European market (EUR bn)

Benefitting from all the advantages of size and market leadership

Source: Company data for 2018 figures; zooplus assumptions

n/a

1.1

1.3

1.9+ 6%

+21%

+7%

Online ~0.08

Online ~0.08

1

2

32)

1) Net sales estimated from gross sales 2) Includes services 3) amazon global online store sales

4 3)+13%

(+ EUR 110 m)

(+ EUR 231 m)

(+ EUR 70 m)

1)

Investor & Analyst Presentation - Annual Report 2018 | page 36

online market position

zooplus is by far the European market leader in online pet supplies

zooplus sales 2018 (EUR m) and market share of total market

growth rate

% of total net sales

84

82

86

108

110

112

149

224

387

Other EE

ES, PT

DK, SE, FI, NO

IT

PL

UK, IE

NL, BE, LU

FR

D, A, CH 29%

17%

11%

8%

8%

8%

6%

6%

6%

16%

20%

20%

17%

37%

20%

22%

24%

35%

7.0%

6.0%

8.2%

2.7%

16.0%

4.4%

5.4%

4.7%

5.7%

Source: market shares zooplus estimation

absolute growth

52 m

37 m

25 m

16 m

30 m

18 m

16 m

16 m

22 m

1

1

1

2

1

1

1

1

1

Investor & Analyst Presentation - Annual Report 2018 | page 37

Competitors fall into three categories

» Generalist, focus on mass & accessories

» Limited premium offer on amazon direct

» Will stay and continue to grow

Brick & mortar

Regional onliners

amazon

» Small independents getting fewer in number

» Chain store online expertise still limited, focus on stores, sales prices offline still much higher

» Challenging times still to come – declining like-for-like unless resized number of outlets

» Mid-term non competitive margin & cost structure

» First signs of consolidation

» Only few very specialized stores will survive

Long-term zooplus and amazon as the two leading concepts in the category

Investor & Analyst Presentation - Annual Report 2018 | page 38

Category

Premium brands

Additional pet content

Pricing

Pet specialist

All relevant premium brands

Pet specific content & services

More competitive or same price

Private label 14% of food sales

There is a good way of living next to amazon as a differentiated category specialist

Supply chain > 99% Direct (control of supply chain)

zooplus with the vision of most relevant platform both for products and services will clearly differentiate versus amazon’s transactional approach

Assortment Food + curated accessories

Generalist

Limited assortment

None

Competitive

< 1% of sales

Direct (20-50%) + Marketplace

Focus on mass & accessories

Investor & Analyst Presentation - Annual Report 2018 | page 39

zooplus has a complete offer and keeps a relevant price advantage versus amazon and the competition

Top 500 articles Top 1000 articles

UK

amazon direct 20% 21%

amazon MP 80% 79%

Pets at Home online 55% 52%

Fetch 54% 50%

amazon direct share reduced over last months, market place significantly more expensive, continued price advantage for zooplus towards the competition

Germany

amazon direct 17% 19%

amazon MP 83% 81%

Fressnapf online 37% 41%

Zooroyal 43% 38%

Source: zooplus research via pricegrabbing March 2019

Assortment overlap Assortment overlap

Investor & Analyst Presentation - Annual Report 2018 | page 40

amazon will not build a monopoly in the pet supplies category

zooplus will continue to develop its business model next to amazon as the leading pet specialist retailer

� There are bigger markets to conquer first

� Pets category one of the most emotional categories in retailing

� Comparatively low margin products with little cash generation today

� Challenges with logistics (bulky & heavy, parcel split)

� Suppliers see challenges for premium brand development on amazon

� Not all consumers are amazon addicts

� Competition authorities will watch the amazon development

� Chewy in the US impressively shows that it is possible to build a customer centric pet retailer next to amazon

Investor & Analyst Presentation - Annual Report 2018 | page 41

Market overall continues to be attractive and growing

Summary market & competition

Brick and mortar will continue to struggle with online

amazon is the only relevant long-term online competitor next to zooplus

Majority of smaller (online) specialists will consolidate or disappear mid-term

Online will take considerably more share in the next years

The market is big enough for both amazon and zooplus in the long run

zooplus strongly differentiates from amazon as the pet specialist

1

2

4

5

6

7

3

Investor & Analyst Presentation - Annual Report 2018 | page 42

Q & A

Brand & Shop portfolio

Investor & Analyst Presentation - Annual Report 2018 | page 44

Key drivers for the attractiveness of the zooplus business model from a shopper perspective

USP and differentiation towards competition

1Price

attractiveness

2Completeness

of offer

3Performance

quality

4Content

“At zooplus or bitibaI always find the best price.”

“Whenever I need to order, the products are available.”

“I can choose the last mile provider and the delivery is very reliable.”

“On zooplus I find very detailed product descriptions and additional information. I can even ask questions to a veterinarian.”

Investor & Analyst Presentation - Annual Report 2018 | page 45

Differentiated brand portfolio to cover all relevant market segments

Discount oriented pet retailer

with focused product portfolio for price sensitive customers

Pet specialist

with broad profile of covered product segments & brands

Vet specialist

with focus on health products and high quality nutrition

Brand opportunity:zooplus and adjacent brands to be developed much stronger in future

Investor & Analyst Presentation - Annual Report 2018 | page 46

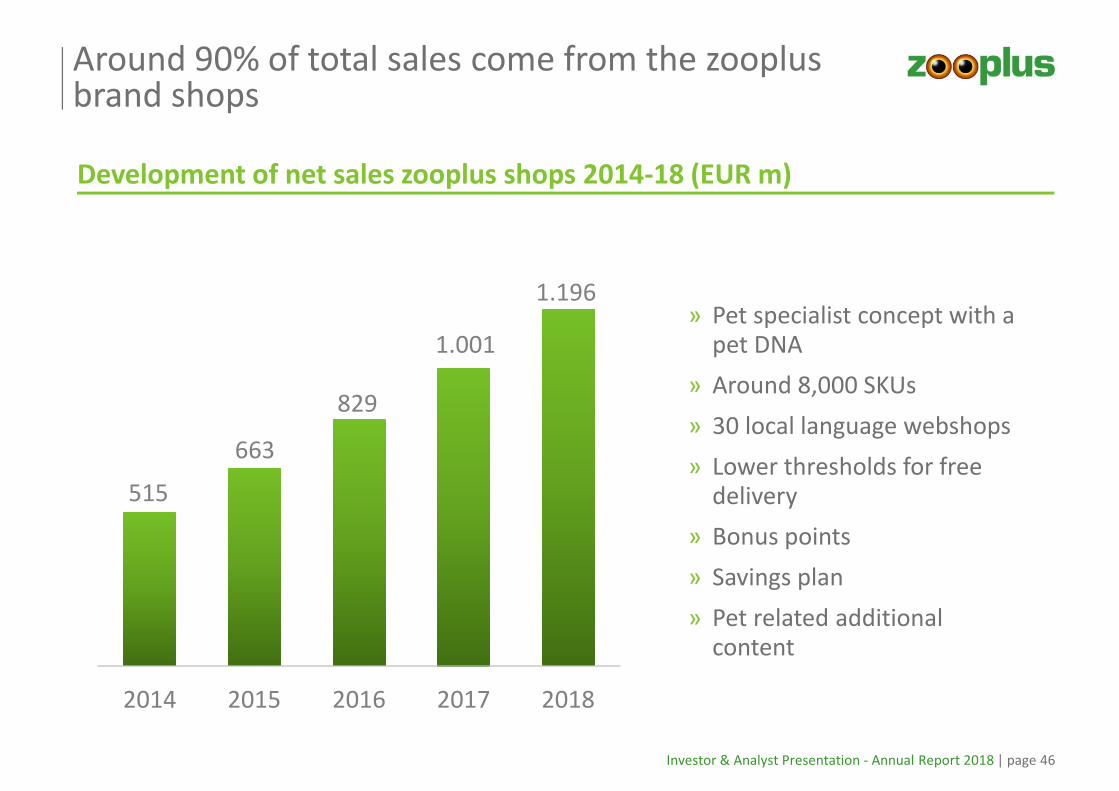

Around 90% of total sales come from the zooplusbrand shops

515

663

829

1.001

1.196

2014 2015 2016 2017 2018

Development of net sales zooplus shops 2014-18 (EUR m)

» Pet specialist concept with a pet DNA

» Around 8,000 SKUs

» 30 local language webshops

» Lower thresholds for free delivery

» Bonus points

» Savings plan

» Pet related additional content

Investor & Analyst Presentation - Annual Report 2018 | page 47

Around 10% of total sales come from the bitibabrand shops

28

48

79

110

146

2014 2015 2016 2017 2018

Development of net sales bitiba shops 2014-18 (EUR m)

» Focused concept for price sensitive customers

» Reduced number of SKUs

» 14 local language webshops

» Higher thresholds for free delivery

» No bonus points and savings plan

» Uses same infrastructure as zooplus

» Slightly lower levels of customer and sales retention

» Contribution margin on similar level as for zooplus customers

Investor & Analyst Presentation - Annual Report 2018 | page 48

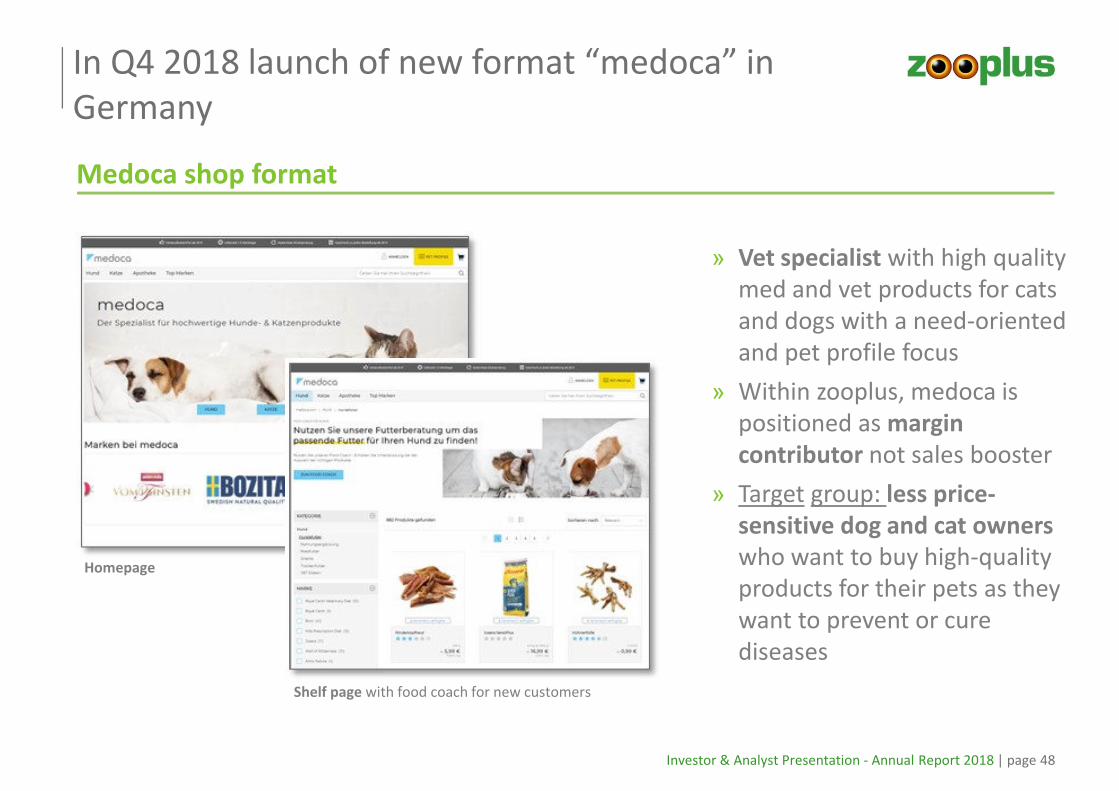

In Q4 2018 launch of new format “medoca” in

Germany

» Vet specialist with high quality

med and vet products for cats

and dogs with a need-oriented

and pet profile focus

» Within zooplus, medoca is

positioned as margin

contributor not sales booster

» Target group: less price-

sensitive dog and cat owners

who want to buy high-quality

products for their pets as they

want to prevent or cure

diseases

Shelf page with food coach for new customers

Homepage

Medoca shop format

Customer loyalty / Retention

Investor & Analyst Presentation - Annual Report 2018 | page 50

Loyal customers are the core base of zooplusgrowth path

Sales retention 2018

95%

» Record high sales retention rate in 2018

» Industry-wide and across industries leading retention rate

» Clear sign that zooplus customers are extremely loyal

Stands for excellent consumer acceptance of product offer and strength of

business model

Fx-adjusted

Investor & Analyst Presentation - Annual Report 2018 | page 51

zooplus business model with high retention is like a subscription business

Retention rates – Cohort analysis – Sales (EUR m)

Reading example: 2012 a = sales of 2012’s new customers in 2012 1) in local currencies

133 131 131 135 138 139 137

62 56 55 56 56 56 56125 87 79 78 77 77 76

105 95 91 88 87

127 119 115

202167 144 136

253217 189

271254

293

2012 2013 2014 2015 2016 2017 2018

135

174 145

101%

90% 99%

70% 91%

78%

<=2010

2011 a+1

2012 a

2013 a

Ø 85%

Ø 91%

Ø 94%

2014 a

2015 a

90%

2016 a

83%

99%

102%

104%

83%

Ø 92%

Ø 94%1)

88%

96%

99%

100%

101%

319

407

543

711

909

2017 a

99%

86%

86%

94%

97%

99%

100%

101%

1,111

94%

87%

94%

96%

98%

99%

100%

99%

2018 a

Ø 94%

Ø 95%1)

Ø 93%

Ø 93%1)

1,342

Investor & Analyst Presentation - Annual Report 2018 | page 52

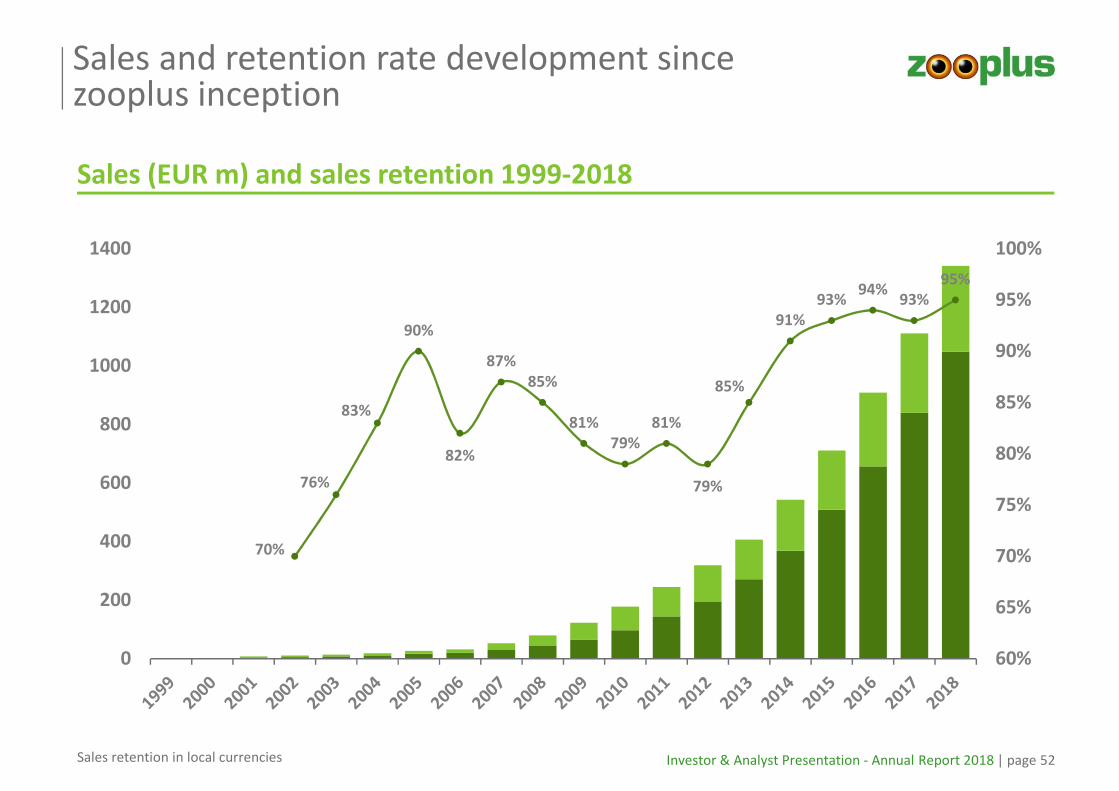

Sales and retention rate development since zooplus inception

Sales (EUR m) and sales retention 1999-2018

70%

76%

83%

90%

82%

87%

85%

81%

79%

81%

79%

85%

91%

93%94%

93%

95%

60%

65%

70%

75%

80%

85%

90%

95%

100%

0

200

400

600

800

1000

1200

1400

Sales retention in local currencies

Investor & Analyst Presentation - Annual Report 2018 | page 53

Account value and customer account retention increase with length of customer life

198

237266

288 299 305 303 310326

343 358

a a+1 a+2 a+3 a+4 a+5 a+6 a+7 a+8 a+9 a+10

Projected sales per active account out of 2018 (in €)

Cumulated

sales per

account created

over a+10

years: € 1,692

100%1 79% 63% 56% 51% 48% 38%

Account survival

rate2

a: year of

acquisition = 2018

1 customers with at least one consecutive purchase after first transaction2 Projected rate based on account retention rate of respective cohort3 Average projected share of remaining accounts based on account survival rate

Share of remaining

accounts345% 43% 41% 40%

100%1 79% 80% 89% 92% 93% 95% 95% 96% 96% 96%

198 187 167 161 153 146 137138 134 135 136 Sales per account

created (€ 1,692)

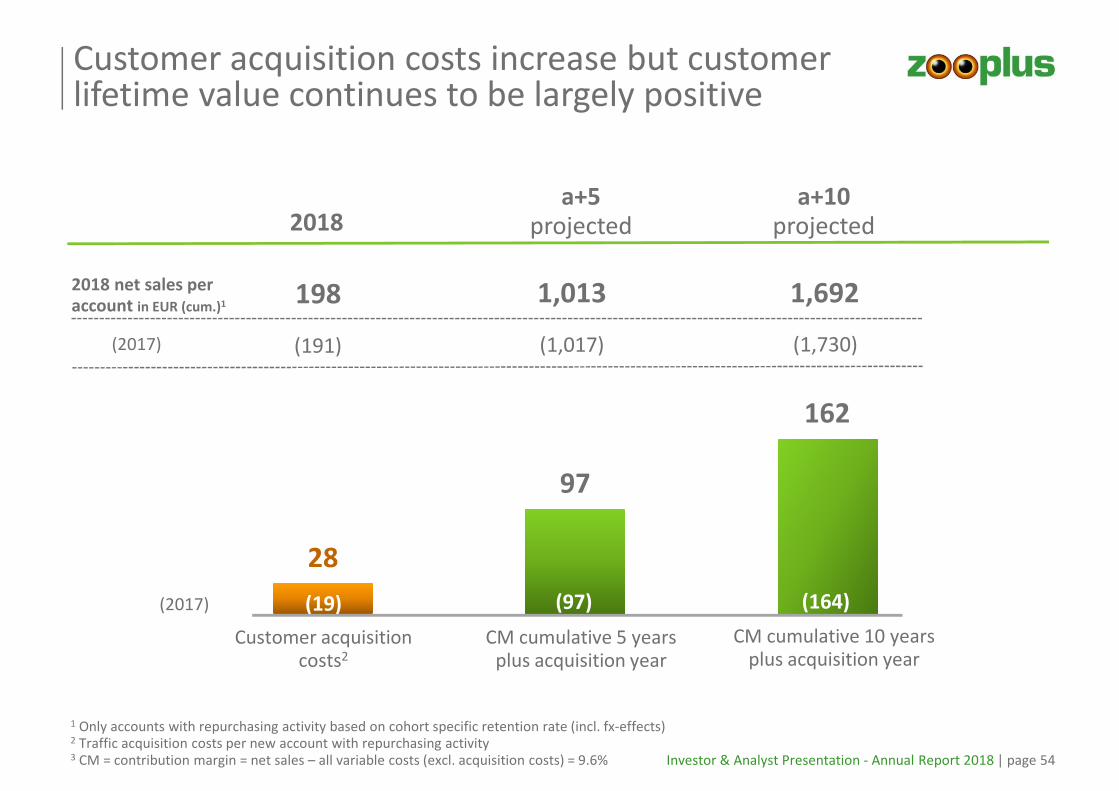

Investor & Analyst Presentation - Annual Report 2018 | page 54

28

97

162

Customer acquisition costs increase but customer lifetime value continues to be largely positive

Customer acquisitioncosts2

CM cumulative 5 yearsplus acquisition year

CM cumulative 10 yearsplus acquisition year

1 Only accounts with repurchasing activity based on cohort specific retention rate (incl. fx-effects)2 Traffic acquisition costs per new account with repurchasing activity3 CM = contribution margin = net sales – all variable costs (excl. acquisition costs) = 9.6%

2018a+5

projecteda+10

projected

1,013 1,6921982018 net sales per account in EUR (cum.)1

(2017) (191) (1,017) (1,730)

(97) (164)(19)(2017)

Investor & Analyst Presentation - Annual Report 2018 | page 55

Strong profitability of repeat customers business invested to grow the business with long-term perspective

Repeat customers and new customers contribution (EUR m)

271 24% - 17 - 6.3%840 76% 21 + 2.5%

New customers(sales in the year of acquisition)

Repeat customers(consecutive year’s sales)

2017

Net

Sales

% of

total z+

EBT EBT-

margin

Net

Sales

% of

total z+

EBT EBT-

margin

293 22% - 23 - 7.8%1,049 78% 21 + 2.0%2018

+ 0.4% + 3.6%

H1 H2

2018

Investor & Analyst Presentation - Annual Report 2018 | page 56

� Competitive pricing

� Brand development

� Personalization & emotionalization

� Data / CRM opportunities:

− Stronger focus on customer-individual analyses in relation to sales frequency

− Intensified analyses of current share of wallet of customers and further potential

− Create additional sales from existing customers

� Logistics - last mile flexibility

Further initiatives planned to support retention

Key priorities

Customer acquisition

Investor & Analyst Presentation - Annual Report 2018 | page 58

135

174

202

253271

293

2013 2014 2015 2016 2017 2018

New customers sales (EUR m) and acquisition costs per new customer1 (EUR)

Growth of new customer business –acquisition costs rising

CAC1

Customer acquisition expected to continue to increase

24 18 18 15 19 28

» Price inflation in Google keywords (SEA)

» Limited growth of Google traffic

» Lower conversion in mobile

» Increasing new customer numbers

1 Per new account with

repurchasing activity

Investor & Analyst Presentation - Annual Report 2018 | page 59

Share of product searches Why shoppers start on amazon

Sources: Jumpshot Inc.; Profitero

amazon gets more important for product searches

54%

46%

54%

46%

2015 2018

1. Variety of products 79%

2. Free shipping 64%

3. Better deals 60%

4. Customer reviews 55%

5. Search capabilities 54%

6. Mobile experience 29%

More premium brands

> 90% free shipping, no prime fee

Same price or more competitive

More specific reviews

Focused pet related search

Best in category

US market figures

Investor & Analyst Presentation - Annual Report 2018 | page 60

Development of Google shopping 2014-2019

Google shopping is today the dominant source for paid online traffic

Source: Merkle Inc.

0%

20%

40%

60%

80%

100%

2014 2014 2015 2015 2016 2016 2017 2017 2018 2018

Non-Brand Overall

Investor & Analyst Presentation - Annual Report 2018 | page 61

Google shopping ad spend UK

zooplus has already achieved the shift towards mobile

9.9% 8.1% 6.8% 5.0%

47.2%

16.1%

52.3%

14.9%

34.8%

50.5%

35.6%

67.6%

8.1%

25.3%

5.3%12.6%

Ad spend zooplus Clicks zooplus

Desktop

SEA

Desktop

shopping

Mobile

shopping

Mobile

SEA

Source: Adthena Search Advertising Report Q1 2018

Investor & Analyst Presentation - Annual Report 2018 | page 62

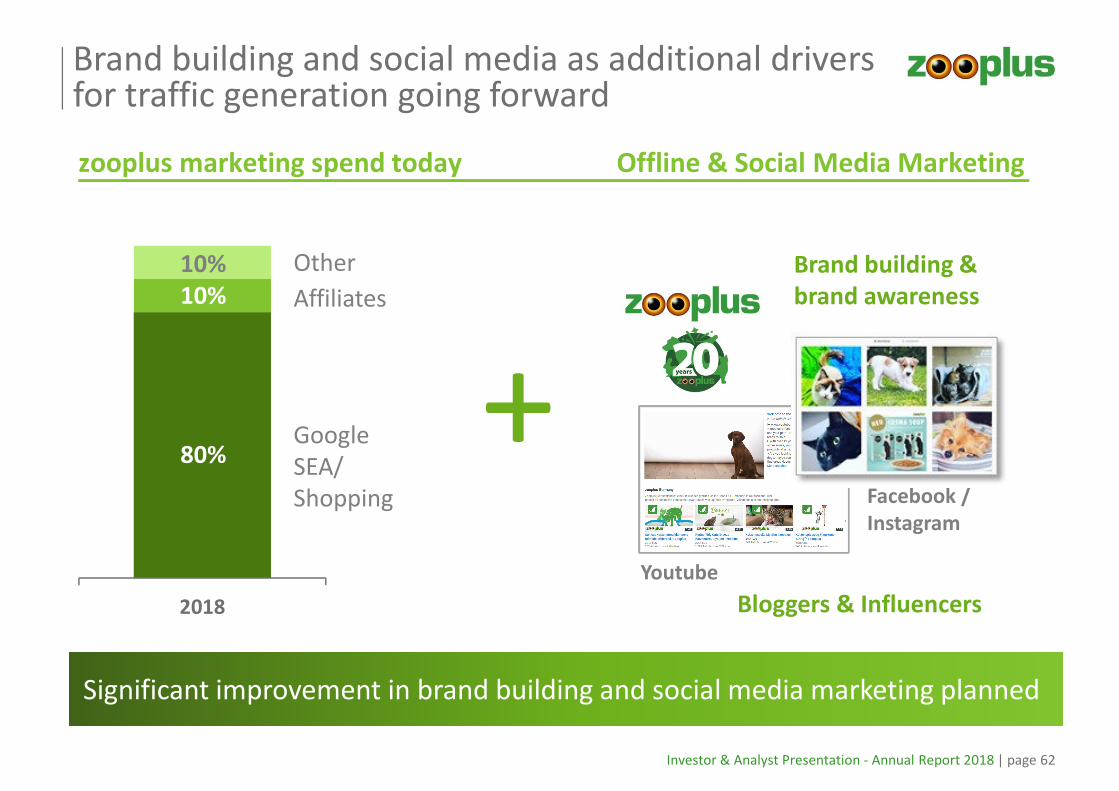

zooplus marketing spend today Offline & Social Media Marketing

Brand building and social media as additional drivers for traffic generation going forward

Bloggers & Influencers2018

SEA/

Shopping

Affiliates

Other

+

Brand building &

brand awareness

Youtube

Facebook /

Significant improvement in brand building and social media marketing planned

10%

10%

80%

Investor & Analyst Presentation - Annual Report 2018 | page 63

Key priorities

� Optimization of traffic conversion trough website improvements

� Ongoing improvement of mobile usage

� Additional ways of customer acquisition:

− Brand building

− Social Media

− Additional content

− Pet related services

New customer acquisition remains major focus for 2019 and beyond

Focus on mobile

Investor & Analyst Presentation - Annual Report 2018 | page 65

zooplus is a digital multi-channel retailer

» Mobile share of orders around 30% and growing

» Mobile will be the dominant channel in the future

» Own zooplus smartphone Apps (iOS and Android)

» Significant investment in mobile channel

» More technical features and optimized UX to come in future

» Online activities adapted to mobile usage

Investor & Analyst Presentation - Annual Report 2018 | page 66

Mobile channel has considerably increased its share and is continuing to grow

Visits

83 m

+28%

Visits

83 m

+28%

Order

share

App

+4%p

Order

share

App

+4%p

Orders

7.0 m

+61%

Orders

7.0 m

+61%

Note: TY 2018 figures, growth: 2018 vs. 2017

Mobile: traffic by mobile phones (incl. app)

Mobile business zooplus 2018 vs. 2017

Clear focus on mobile in all activities

Investor & Analyst Presentation - Annual Report 2018 | page 67

Desktop Tablet Mobile -

Web

Mobile -

App

KPIs – Mobile vs. desktop

Major KPIs (2018)

Desktop Tablet Mobile -

Web

Mobile -

App

38%43%

Desktop Tablet Mobile -

Web

Mobile -

App

22%

58%

21%

7%

Conversion rate

Visits Orders

Desktop Tablet Mobile -

Web

Mobile -

App

Basket value (in EUR)

56

51

8% 10%

16% 54

10% 11%

15%

57

Further business driver mid-term: Pet Services

Investor & Analyst Presentation - Annual Report 2018 | page 69

Pet services marketplace to create additional customer loyalty, differentiation and traffic

zooplus as the most relevant pet platform for products and pet related services

» Pet specialist – fulfilling all pet customer needs

» Differentiating versus amazon and smaller competitors

» Additional traffic generation

» Supported by manufacturer brands

Grooming

zooplus is the only European platform that can activate users on large scale

Breeders / shelters Day-walking

Veterinarians

Insurances

Other

Investor & Analyst Presentation - Annual Report 2018 | page 70

Vet search and vet ratings will be running in six major markets in Q2 2019

» Running in DE and PL, in FR, NL, IT, ES starting Q2 2019

» More than 30,000 vets connected to the platform

» Self-care tool for veterinarians to update and add content to their profiles

» User acceptance in DE for both user groups (pet owners and vets) above expectations

Vet search

Investor & Analyst Presentation - Annual Report 2018 | page 71

Vet search confirms interest for pet service marketplace – further steps planned for 2019

» Flexible multi-offer platform under development

» Better visibility and integration in zoopluswebsite

» Breeders / shelters as next development step

Mock-up: breeders

Example breeders

Gross margin

Investor & Analyst Presentation - Annual Report 2018 | page 73

Long-term gross margin decline halted

in % of sales

1 Sales – CoGS; years prior to 2018 adjusted from published

external figures to new IFRS 15

Gross margin1

2012 2013 2014 2015 2016 2017 2018

37.4%

30.6%32.3%

35.8%

28.7% 28.5% 28.7%

» Selective increase of product prices

» Limitation of discount / coupon usage

» Adjustment of shipping conditions and fees

» Promotion of private label brands

» Optimization of savings plan

Investor & Analyst Presentation - Annual Report 2018 | page 74

Drivers for further stabilization and improvement of gross margin

1Total

margin

Pricing

Puchasing power

Private label share

increase

Consolidation

Improved and more data driven management of consumer sales prices

Using weight of biggest purchasing volume in the category for improved terms & conditions from suppliers

Significant increase in private label share and making full use of private label margin advantage

Consolidation of regional onliners expected – amazon as price follower, brick-and-mortar incumbents should have interest in higher sales prices to secure their store networks

AssortmentOptimization of assortment by reducing loss making products and orders

Investor & Analyst Presentation - Annual Report 2018 | page 75

Margin stabilization – reducing non-profitable articles and orders

On order /article/ supplier level:

Non profitable orders significantly reduced in 2018

» Delisting of articles with negative contribution if no specific support from suppliers

» Adding surcharges like logistics fee for products with high logistics costs but low sales value

» Cutting off sales of orders that will never make a positive contribution margin

Branded suppliers

Investor & Analyst Presentation - Annual Report 2018 | page 77

zooplus is the most relevant online platform for pet specialist suppliers

zooplus USP

Suppliers need zooplus to distribute their brands across Europe online

» European market leader by far

» Pet specialist platform with more than 7 m customers

» The only retailer with real European-wide reach and

access to 30 country markets

» Pet specific environment, significantly more to come

» Biggest base of pet data

» Long-term the only real counterpart to amazon in the

online pet category

Investor & Analyst Presentation - Annual Report 2018 | page 78

zooplus has the biggest consumer pet database on a pan-European level

Data opportunity still to be explored

» Pet profiles

» Sales data

» Product mix analysis

» Behavioral data

» Brand shift data

» Health data

» Product reviews

Highly relevant for branded suppliers

Accessible only via zooplus

Full and representative coverage – unlike

offline loyalty cards

Potential for much deeper co-operation

with suppliers in future

Movie: 1st zooplus partner conference 2019

Private label

Investor & Analyst Presentation - Annual Report 2018 | page 81

Private label – leading private label operator in the pet specialist online category

Strategic view on private label business

» Strong focus on growing share of private label

» Positioned as products “exclusive to zooplus” – not simple me-too products

» Further portfolio expansion planned

» Margins superior to average of branded products

» Building private label next to expansion of supplier branded products

Sales growth

Improved terms and conditions with manufacturers

Making full use of margin advantage in P&L – today still in investment mode

Further expansion of private label margin:

1

2

3

14%Private label sales share of food and cat litter

Investor & Analyst Presentation - Annual Report 2018 | page 82

13% 14%Share of

total food & cat litter

1.5 1.6Growth index

private label / food

5% 6%Share of

first order sales

Online private label business gains traction and will continue to grow above average

Further significant increase in private label share planned for coming years

Figures for 2017 and 2018

Investor & Analyst Presentation - Annual Report 2018 | page 83

The single private label brands are designed for dedicatedtarget groups and reflect latest nutritional trends

Segment description:Dry food, wet food and snacks

Positioning: Wild and Free! Wolf of Wilderness has beenformulated to mimic the wild wolf´s diet

USP: High fresh meat content, grain-free, species

Target customer: Premium focused dog owners who look fornatural products with holistic concepts (grainless, berries etc.) and strong emotional messages

Price Positioning: Premium

Number of SKUs: 65

Investor & Analyst Presentation - Annual Report 2018 | page 84

New brands will continue to drive private label sales

Segment description:Wet and dry food for dogs and cats

Positioning: Dietetic complete pet food for adult cats and dogs

USP: Appropriate and need-based nutrition for themost frequent diagnosed medical conditions

Target customer: Dog and cat owners whose pets have specialdiseases and need according dietetic completefood

Price Positioning: Premium

Number of SKUs: 28 (wet & dry food)

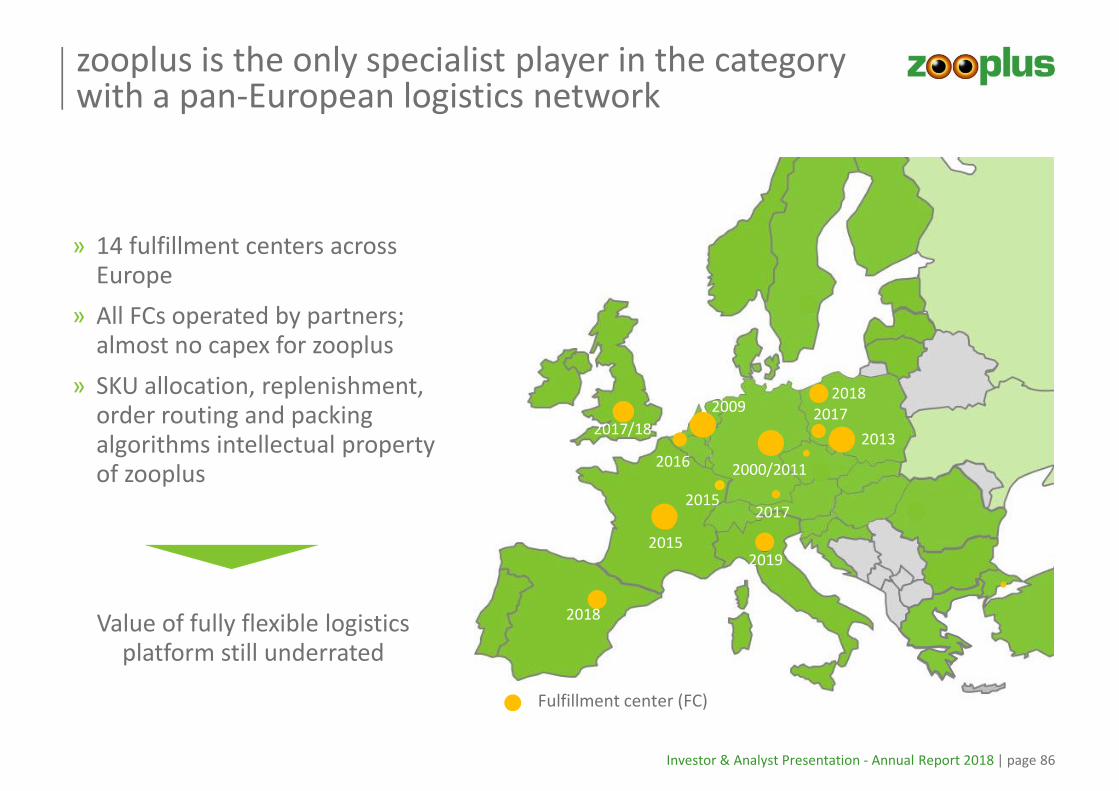

Pan-European logistics infrastructure

Investor & Analyst Presentation - Annual Report 2018 | page 86

» 14 fulfillment centers across Europe

» All FCs operated by partners; almost no capex for zooplus

» SKU allocation, replenishment, order routing and packing algorithms intellectual property of zooplus

zooplus is the only specialist player in the category with a pan-European logistics network

2013

2015

Fulfillment center (FC)

2009

2015

2016

2017/18

2000/2011

2017

2017

2018

2019

2018Value of fully flexible logistics platform still underrated

Investor & Analyst Presentation - Annual Report 2018 | page 87

zooplus logistics – significant expansion of pan-European network in 2018

» Size of FC UK tripled in Q2 incurring

one-off costs and reduced efficiency

for transition period

» New FC Poland started end of

September 2018 – 40,000 sqm

» New FC Spain started in September

2018 – closing of white spot in

network and strong improvement of

delivery speed to customers

» New FC Spain operated by

4th FC partner – XPO Logistics

Coventry (UK)

Krosno (PL)

Madrid (ES)

Investor & Analyst Presentation - Annual Report 2018 | page 88

zooplus operates fulfillment centers with four logistics experts

Capex per center: € 20 – 35 m1) provided by partners

1) Including facility / building for big zooplus fulfillment centers

» Dirks (PL, UK)

» Rhenus (DE, NL, FR, PL)

» Katoen Natie (BE)

» XPO (ES)

» Experts in their field, exclusive for zooplus in pet category

» Synergies as logistics providers

» More flexibility and grip on costs for zooplus

Investor & Analyst Presentation - Annual Report 2018 | page 89

zooplus’ logistics structure is tailor-made for heavy and bulky products in inbound and outbound logistics

zooplus

logistics

Antwerp, Belgium Antwerp, Belgium

Tilburg, Netherlands Tilburg, Netherlands

Antwerp:

16,000 sqm

Logistics partner:

Katoen Natie

Source: zooplus

Investor & Analyst Presentation - Annual Report 2018 | page 90

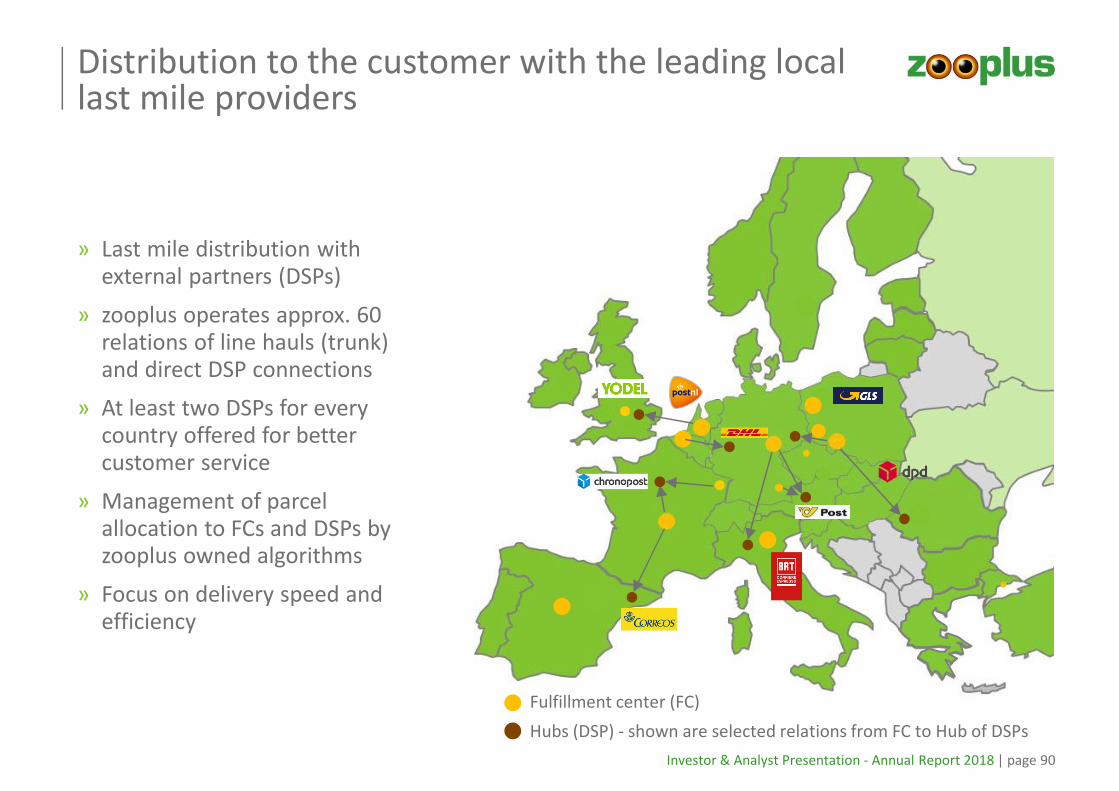

Distribution to the customer with the leading local last mile providers

» Last mile distribution with external partners (DSPs)

» zooplus operates approx. 60 relations of line hauls (trunk) and direct DSP connections

» At least two DSPs for every country offered for better customer service

» Management of parcel allocation to FCs and DSPs by zooplus owned algorithms

» Focus on delivery speed and efficiency

Fulfillment center (FC)

Hubs (DSP) - shown are selected relations from FC to Hub of DSPs

Investor & Analyst Presentation - Annual Report 2018 | page 91

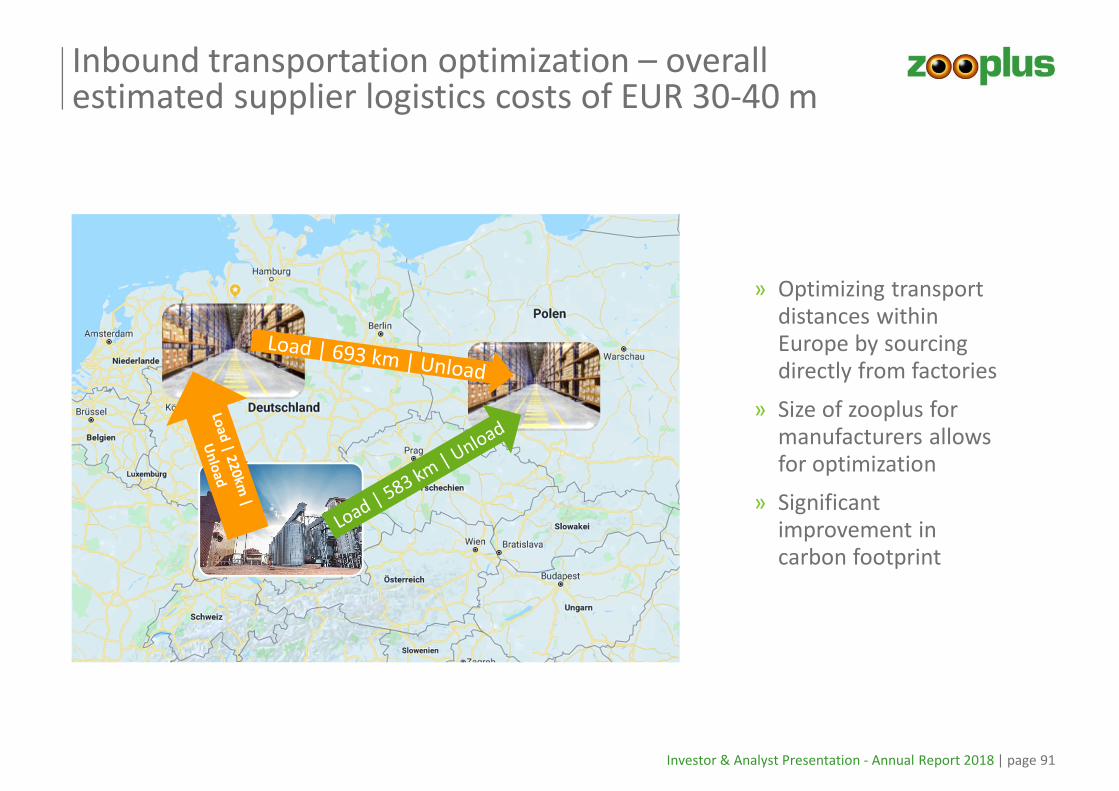

Inbound transportation optimization – overall estimated supplier logistics costs of EUR 30-40 m

» Optimizing transport distances within Europe by sourcing directly from factories

» Size of zooplus for manufacturers allows for optimization

» Significant improvement in carbon footprint

Investor & Analyst Presentation - Annual Report 2018 | page 92

Further development of logistics costs

Overall logistics cost expected to further decrease as percentage of sales

Unit cost for last mile expected to increase in 2019 in major markets due to capacity constraints of parcel service providers and increasing labor cost in this sector

Drivers for improvement in logistics costs:

Scale, efficiency and costs Value per parcel

» Significant additional FC capacity in Poland

» Efficiencies within network

» Optimization of line hauls

» Inbound optimization together with suppliers

» Reduction of parcel split ratio

» Increase of basket size

» Optimize thresholds for free delivery

» Charge additional fees to consumers

Investor & Analyst Presentation - Annual Report 2018 | page 93

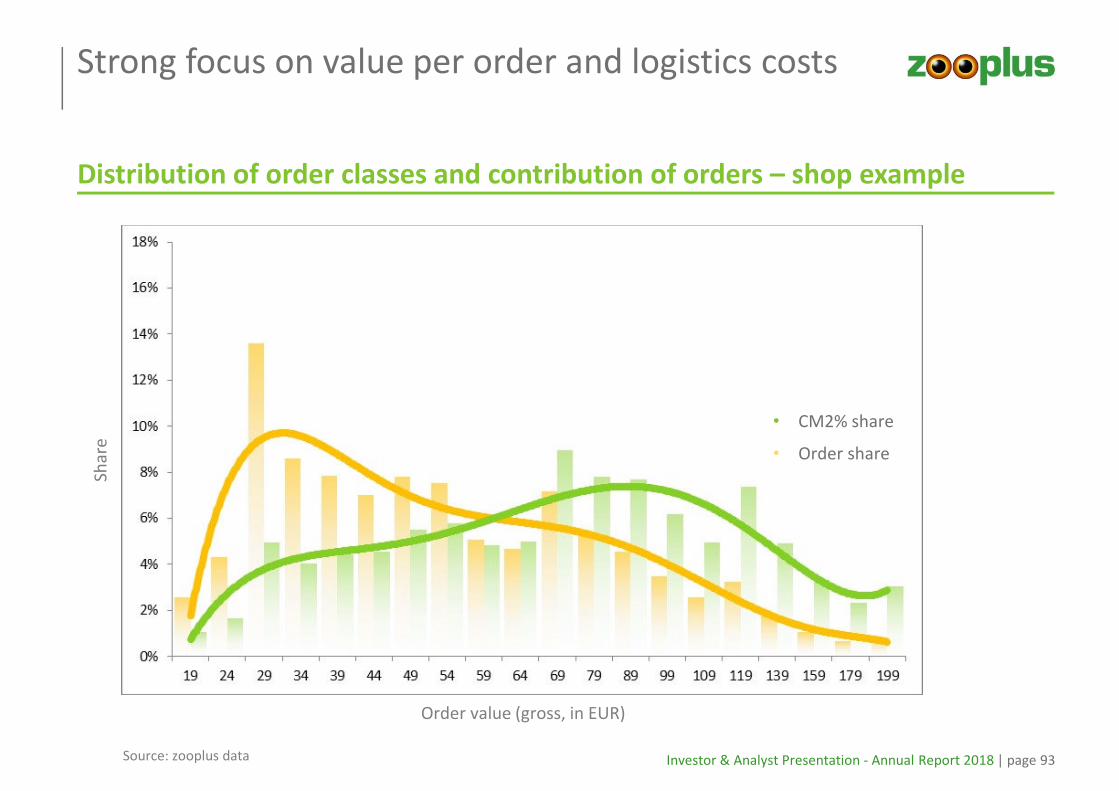

Strong focus on value per order and logistics costs

Distribution of order classes and contribution of orders – shop example

Source: zooplus data

Orders

Contribution

Order value (gross, in EUR)

Sha

re

• CM2% share

• Order share

Investor & Analyst Presentation - Annual Report 2018 | page 94

All order classes with positive contribution, however low order values with very high logistics costs

Development of logistics costs by order value – shop example

Source: zooplus data

Logistics costs in %

Logistics costs

Contribution

Order value (gross)

Log

isti

cs c

ost

s in

%

Logistics costs

Contribution

Logistics costs in %

IT infrastructure and resources

Investor & Analyst Presentation - Annual Report 2018 | page 96

Technology environment specifically designed for zooplus business model

» One central platform

» Mix of inhouse developed systems and standard systems

» SAP Finance for Accounting since 01/2017

» Central data warehouse on SAP Hana

» Inhouse developed algorithms for:

• Google bidding and listing management

• Replenishment and demand forecast

• Pricing

• Order routing

• Parcel building

• Systems monitoring

zooplus specific and scalable - differentiation factor

Investor & Analyst Presentation - Annual Report 2018 | page 97

Strong internal IT development teams as driving force for future developments and differentiation

Strong differentiating factor versus the competition1

Munich, DE Krakow, PL

Bucarest, RO

(External partner)Madrid, ES

» Four internal IT hubs plus one external hub

» More than 200 IT developers

» Additionally external experts as freelancers

» Focus on internal systems, processes & algorithms and product features

Vienna, AT

1 excluding amazon

Cost efficiency / Most efficient operator

Investor & Analyst Presentation - Annual Report 2018 | page 99

Continued focus on retention and sales growth as main drivers for future profitability

Retention

Sales growth

Margin & cost structure

Profitability

Sales growth means

» Keeping the competition including amazon at a distance

» Faster reach of dominant market position

» Better purchasing terms in all areas (COGS & other services)

» More efficiency gains

» More scale in overhead

Investor & Analyst Presentation - Annual Report 2018 | page 100

1 gross margin + other income on sales2 logistics costs reclassified to depreciation according to IAS 173 impairment expenses on financial assets reclassified to payment4 including LTI & SOP; own work capitalized reclassified to personnel

zooplus will continue its strong effort to further improve cost leadership position in the category

Total margin & cost structure (in % of sales)

3.2% 3.3% 3.3%

3.0% 3.2% 3.5%

19.8% 20.2% 19.2%

1.7% 2.0% 2.4%

2017 H1 2018 H2 2018

Total margin1

1.0% 1.0% 1.0%

28.8% 29.4%

1.1%IT/Admin/ (incl.

depreciation & interest)

Advertising/

Marketing

Logistics2

Personnel4

Payment3

29.2% 30.4%

29.6%

28.2%

» Back on positive trend in cost structure since Q2 2018

» Increased investment in marketing for new customer acquisition

Investor & Analyst Presentation - Annual Report 2018 | page 101

29%

45% 43%48%

54%

43% 42%

zooplus is clear cost leader in the category – both online and offline

Cost ratio - selected competitors

Source: annual reports 2017 – Fressnapf 2016: all costs except for costs of goods sold, including depreciation and interest; arcaplanet w/o interest

Cost advantage for zooplus of more than 10%-points

Investor & Analyst Presentation - Annual Report 2018 | page 102

Q & A

Guidance 2019

Investor & Analyst Presentation - Annual Report 2018 | page 104

Sales and profit guidance for full year 2019

zooplus well positioned to continue the sales growth pathin 2019

Guidance

1,342 (+21%) 8.6

EBITDA (EUR m)Sales (EUR m)

2019e

2018

+14% to +18%(+188 to +242)

10 - 30

Investor & Analyst Presentation - Annual Report 2018 | page 105

zooplus changes profit guidance 2019 to EBITDA as key indicator

» EBITDA shows more realistic picture of operating performance of the company

» New IFRS 16 standard treats lease / rent of logistics infrastructure similar to owning the infrastructure, therefore IFRS now allows for a better comparison of EBITDA performance between companies who own logistics infrastructure and those like zooplus that work with external service providers

» Up to now logistics costs of zooplus have always been overstated compared to most competitors in ecommerce who own logistics infrastructure

» Therefore with the change of IFRS 16, which requires a deeper analysis of structural changes in P&L and balance sheet, it is now a good moment to change to EBITDA profit guidance

» Impact of full application of IFRS 16 in 2019 for EBITDA is EUR +14 m vs. 2018 (all other things equal)

» EBITDA guidance of 10 to 30 m EUR translates into former EBT figure of EUR -15 to +5 m

Investor & Analyst Presentation - Annual Report 2018 | page 106

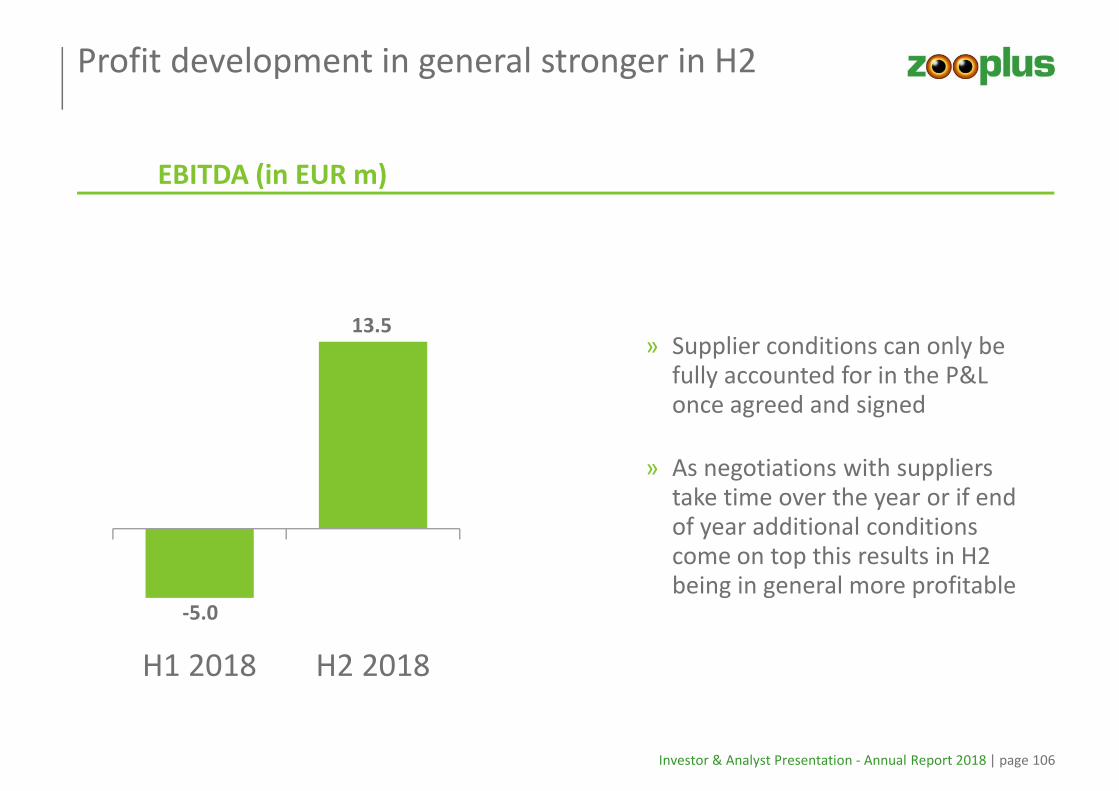

Profit development in general stronger in H2

» Supplier conditions can only be fully accounted for in the P&L once agreed and signed

» As negotiations with suppliers take time over the year or if end of year additional conditions come on top this results in H2 being in general more profitable

H1 2018 H2 2018

EBITDA (in EUR m)

13.5

-5.0

The way forward – 2019 and beyond

Investor & Analyst Presentation - Annual Report 2018 | page 108

The online share is expected to continue to grow significantly during the next years

Current online share and long-term hypothesis (EUR bn)

2014 2018

25 27

10-12%

88-90%

8-10%

Offline share

Online share

Total market (gross)

< 50%

Long-term

> 50%

> 33

Online market opportunity

> 16

Long-term growth potential of online leave enough growth potential for zooplus

4-5%

95-96%

1 zooplus estimation; assuming successful shift of pet food grocery segment to online

1

92-90%

Investor & Analyst Presentation - Annual Report 2018 | page 109

Focus will continue to be on sales growth – but not at any price

» 2 bn target for 2020 set in 2016 too ambitious from today’s perspective but will come only a bit later and growth will continue after 2 bn sales

» Overall competitive position, long-term growth perspective and outlook matter

» Clear market leadership

» Differentiation from amazon

» Customer loyalty

» Cost leadership

» Fully integrated pan-European logistics network

» Strategic relevance for suppliers178 245

319407

543

711

909

1,111

1,342

1,530-

1,584

Investor & Analyst Presentation - Annual Report 2018 | page 110

The moat around zooplus will only get stronger

Growing existing loyal customer base 1

More differentiation through pet related services platform

Cost advantage towards competition in the category both online and offline– further economies of scale

Getting even more relevant for the branded manufacturers (volume and data)

More differentiation versus amazon (assortment, private label, personalization,

emotionalization)

Unique flexible and pan-European logistics platform

2

3

4

5

6

Investor & Analyst Presentation - Annual Report 2018 | page 111

Strong drivers for gross margin stabilization and improvement over the next years

Pricing / Assortment Purchasing power

Private label share

increase Consolidation

1 2

3 4

Investor & Analyst Presentation - Annual Report 2018 | page 112

Over the next years zooplus will continue to drive down costs

» Additional efficiency gains in network

» Inbound logistics optimization

» Value per parcel focus

» Further scale expected

» Further scale expected

» Focus on IT, marketing & brand development and data analytics

Logistics

IT / Admin

Personnel

1

2

3

Investor & Analyst Presentation - Annual Report 2018 | page 113

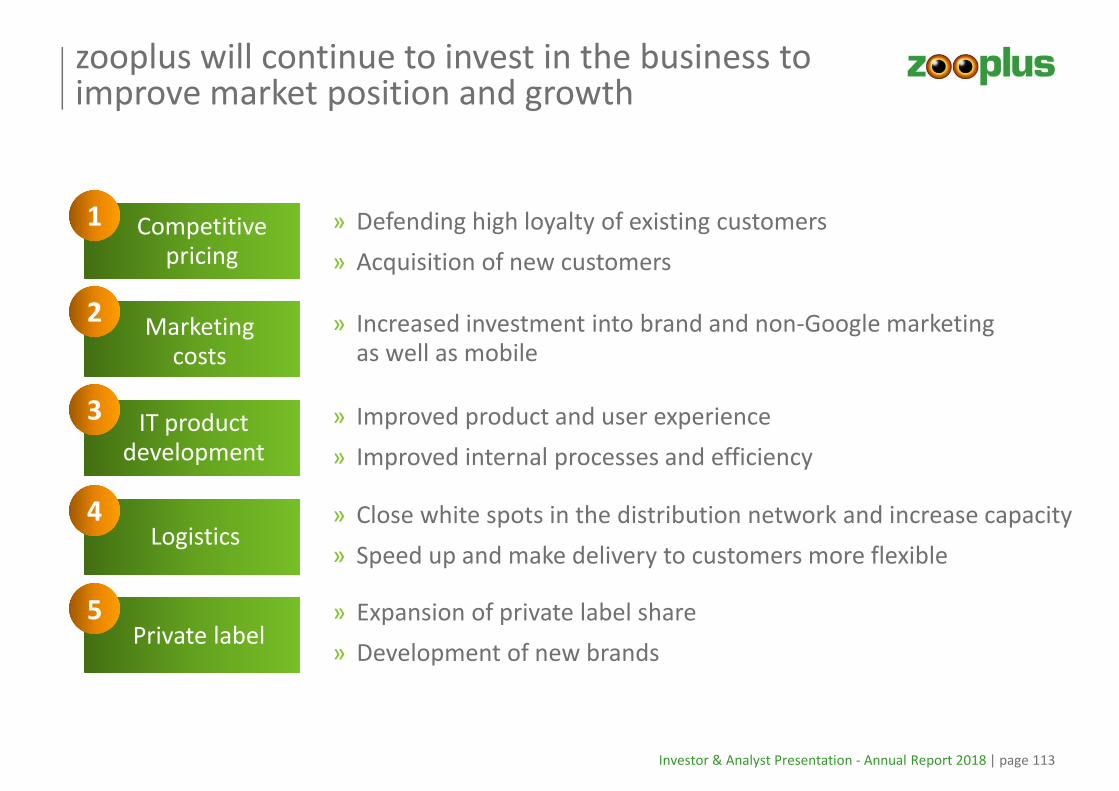

zooplus will continue to invest in the business to improve market position and growth

» Defending high loyalty of existing customers

» Acquisition of new customers

» Increased investment into brand and non-Google marketing as well as mobile

» Improved product and user experience

» Improved internal processes and efficiency

» Close white spots in the distribution network and increase capacity

» Speed up and make delivery to customers more flexible

Competitive pricing

Marketing costs

IT product development

Private label

1

2

4

5

Logistics

3

» Expansion of private label share

» Development of new brands

Investor & Analyst Presentation - Annual Report 2018 | page 114

There are still big opportunities to explore in detail

Brand & Social Media

Pricing Data / CRM Private label

Opportunities

Pet services platform

Investor & Analyst Presentation - Annual Report 2018 | page 115

Structural profitability in the long run with 5-7% EBITDA margin

2018 EBITDA margin: 0.6% long-term target EBITDA impact

Gross margin: 28.7% 30% +1.3%p

Logistics: 19.7% 17% +2.7%p 1)

Overhead: 5.8% 4.0% +1.8%p

Marketing steady state: 2% +0.0%p

Total target potential: ~ 5- 6%p

Structural EBITDA margin 5 – 7%

1) thereof approx. +1%p from IFRS 16 change

Investor & Analyst Presentation - Annual Report 2018 | page 116

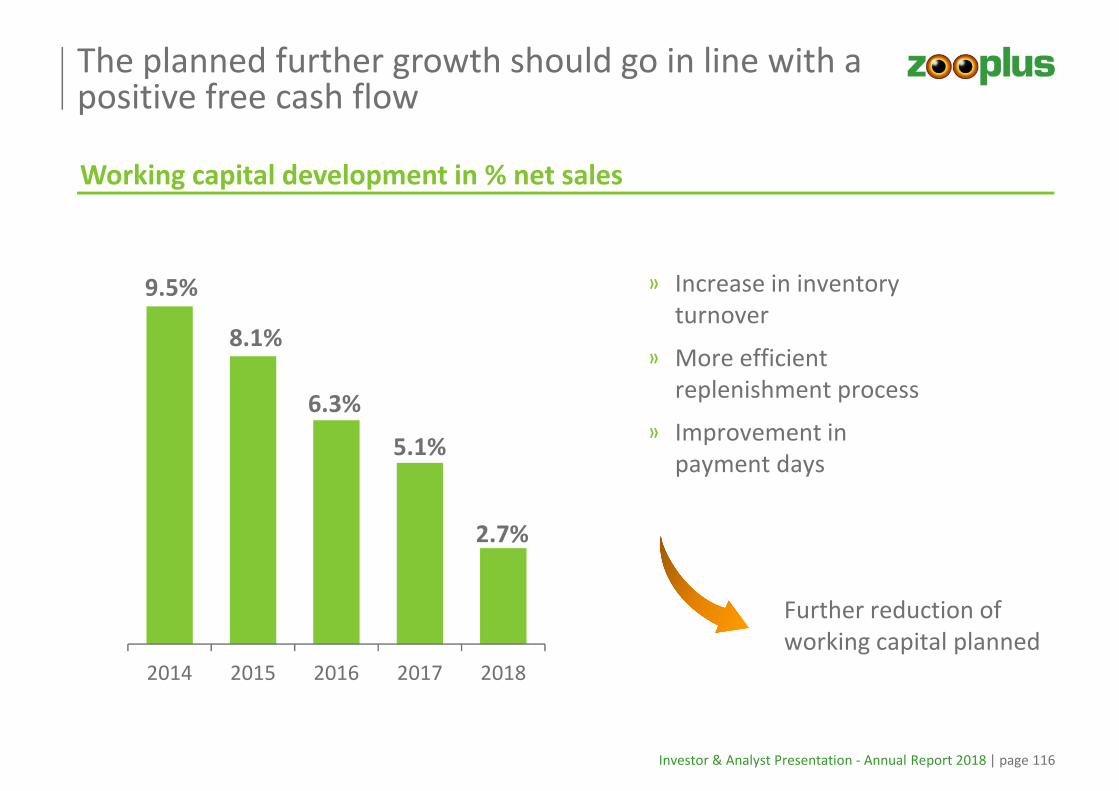

The planned further growth should go in line with a positive free cash flow

Working capital development in % net sales

9.5%

8.1%

6.3%

5.1%

2.7%

2014 2015 2016 2017 2018

» Increase in inventory

turnover

» More efficient

replenishment process

» Improvement in

payment days

Further reduction of

working capital planned

Investor & Analyst Presentation - Annual Report 2018 | page 117

Main takeaways from today’s presentation about zooplus’ strategic perspective

» Pet supplies continues to be a very attractive and growing market.

» zooplus is by far market leader online and already No. 2 in the total market. zooplus has a very loyal

and continuously growing customer base of around 7 m customers.

» Competition comes from amazon, brick-and-mortar and small regional onliners. Overall zooplus

competitive position today stronger than 12 months ago.

» Amazon is the major competitor but zooplus differentiates today significantly from amazon and

tomorrow even more. There is enough room for growth for a specialist next to the generalist amazon.

» zooplus has the most relevant platform for specialist pet supplies manufacturers and is the only

specialist platform in the category that can efficiently ship a parcel to any place in Europe.

» Sustainable new customer growth but not at any price continues to be priority for zooplus. Sales

growth might be slightly lower going forward but future outlook continues to be very positive.

» zooplus has a clear long-term perspective for future structural profitability of 5-7% EBITDA margin

with a stabilized / improved gross margin and further optimization of cost structure.

» Opportunities arise from brand development and social media marketing, pricing optimization,

private label share increase, more detailed data analysis especially for CRM and suppliers as well as

pet services platform integration to develop the most customer centric pet ecosystem in Europe.

Investor & Analyst Presentation - Annual Report 2018 | page 118

Q & A