international journal of zambrut · - waktu dan biaya aktual - bcws, bcwp, dan acwp pengurutan data...

TRANSCRIPT

International Journal of Engineering & Industry ISSN: 2191-3315, Volume 3, Issue 1, page 19 - 31

Zambrut

Zambrut.com. Publication date: June 5, 2019.

Komarudin, T., Bahrowi, N., Mayangsari, Y. & Setyowati, A. 2019. Evaluation of Project Control Method

of Variance Analysis and Concept Development ................

19

Evaluation of Project Control

Method of Variance Analysis

and Concept Development in

the Value of the Fish Auction (Studied in Cianjur, West Java, Indonesia)

Totok Komarudin1, Nasrul Bahrowi

2, Yuni Mayangsari

3 & Anita Setyowati

4

1Dr. Totok Komarudin,

2Dr. Nasrul Bahrowi,

3Yuni Mayangsari, M.Si. &

4Anita Setyowati, M.Si.

1Widya Kartika University, Surabaya

2Panca Marga University, Probolinggo

3Technology University, Surabaya 4Kanjuruhan University, Malang

Indonesia

1. Introduction Projects are dynamic, which must respond to changing circumstances if it is to succeed and be

successful. This is done in a continuous environmental conditions change, so always needs to establish

a policy planning in anticipation of the above circumstances, so that the project can go ahead without

delay, Lock [1].

In a planning project to prevent delays in implementation time and waste in the use of cost, the

necessary improvement of the schedule of activities and budgeting to a minimum, so the turnaround

time and costs used to provide the maximum benefit for the executor, Reksohadiprodjo [2]

In fact, often an organization faces difficulties in terms of resources, including materials and

labor. Therefore, the planning of the resources should be conducted with respect to the lack of resources

Abstract: Control project is afoot to organize and regulate corporate resources to achieve

project goals, namely schedule, budget, and quality. There are two methods used, the

method of Analysis of Variance and Methods Concepts Value Results. Results of the

evaluation on the construction project is a fish auction place schedules and costs that are

not in accordance with planning. Variance costs by Rp. 2,929,000, - caused by the

accelerated activity giving rise to additional labor costs. Variance project time by 1 (one)

day, which is caused by the delay in the project.

Keywords: Variance Analysis, Concept of Value Results, Schedule, Budget, Quality.

International Journal of Engineering & Industry ISSN: 2191-3315, Volume 3, Issue 1, page 19 - 31

Zambrut

Zambrut.com. Publication date: June 5, 2019.

Komarudin, T., Bahrowi, N., Mayangsari, Y. & Setyowati, A. 2019. Evaluation of Project Control Method

of Variance Analysis and Concept Development ................

20

to obtain the optimum schedule. Delays in completion of the project will cause penalty fees that can

reduce the benefits to be gained, Suharto [3].

In addition the project is composed of several activities undertaken one or not continuous, but the

search time can be determined based on past experience. Completion of a project can also be used as

the basis for other similar project in the future. Based on the experiences that have then found to

frequent delays in the completion of a project, this is caused by many factors. It required a better

planning system in the implementation of the project, Ali [4].

Cianjur district with the topography of different types, has marine, reservoirs, rivers, and ponds

nature. In the ecosystem there fishing activities. In coastal areas overlooking the Indian Ocean, many

fishermen who conduct fishing activities in the sea. Currently in District Cidaun already built Jayanti

Fish Landing Base area of 2 ha, with the main facilities and facilities support activities, among others:

the pier, where anchoring, navigation tools, office, mini ice plant capacity of 2.5 tonnes, packing sheds,

shanties marketing fish, workshop machinery, means of communication, and others. In 2008, the

Department of Animal Husbandry and Fisheries Cianjur, has completed building the fish auction place

(TPI) Apra in District Sindangbarang. However, on the implementation of the project there is a delay of

a predetermined schedule and cost overruns that occurred. Department of Animal Husbandry and

Fisheries Cianjur requires an evaluation of the project in 2009 because of a similar project which will

be built in the district Cikakap TPI Agrabinta, Department of Animal Husbandry and Fisheries Cianjur

[5]

Based on the background mentioned above, the problem in this research is how to evaluate the

implementation of development projects TPI. Apra using value analysis method results and methods of

analysis of variance. While the purpose of this study is proposed in the form of project control project

performance measures (cost and schedule) to approach the concept of the value of the results and the

method of analysis of variance, so as to reduce the risk of deviation costs and schedule deviations for

similar projects to be built.

2. METHODOLOGY This study uses PDM (Precedence Diagram Method), with consideration: this method can

describe the operational plan integrally, shows the interrelation of each activity and can show the

critical path. Besides its network is relatively simple, because the activities are done over and over can

be described as a job and are not required dummy.

Data collection was conducted as input for project control processes, such as: working calendar,

list of activities, execution time of each activity, activity dependency logic, planning cost of each

activity, and the actual cost of each activity.

While the Data Processing is done with the following steps:

a. Ordering Data Activity / Activities Project

Sorting kergiatan activities undertaken on the project to construct or create a Network Diagram.

b. Creating network diagrams (Network Diagram)

To create a network can be seen from the description of the activity of a project, ie which activities

can be done simultaneously and which activities must wait previous activities to be completed first.

In the preparation of this network, there are two things that made reference in its manufacture,

which is a natural dependency factor and factor Bar Chart of the company. Natural factors derived

from the logic of the connection an activity with other activities.

Methods of identifying a network of activities that are critical to the project, especially in the

aspects of the schedule and planning. Generally, the critical activity of not more than 20% of the

total project activities, and he knew this part then the manager can give attention.

c. Making the Bar Chart

Making the Bar Chart using data including the time / duration of each activity / activities, the cost

for each activity per day required by each activity. The procedure of making Bar Chart:

1) Arrange the project activities mentioned initial activity and activity end.

2) Calculate the earliest start (ES) and earliest finish (EF) based on the duration and number of

events similarity (activity)

International Journal of Engineering & Industry ISSN: 2191-3315, Volume 3, Issue 1, page 19 - 31

Zambrut

Zambrut.com. Publication date: June 5, 2019.

Komarudin, T., Bahrowi, N., Mayangsari, Y. & Setyowati, A. 2019. Evaluation of Project Control Method

of Variance Analysis and Concept Development ................

21

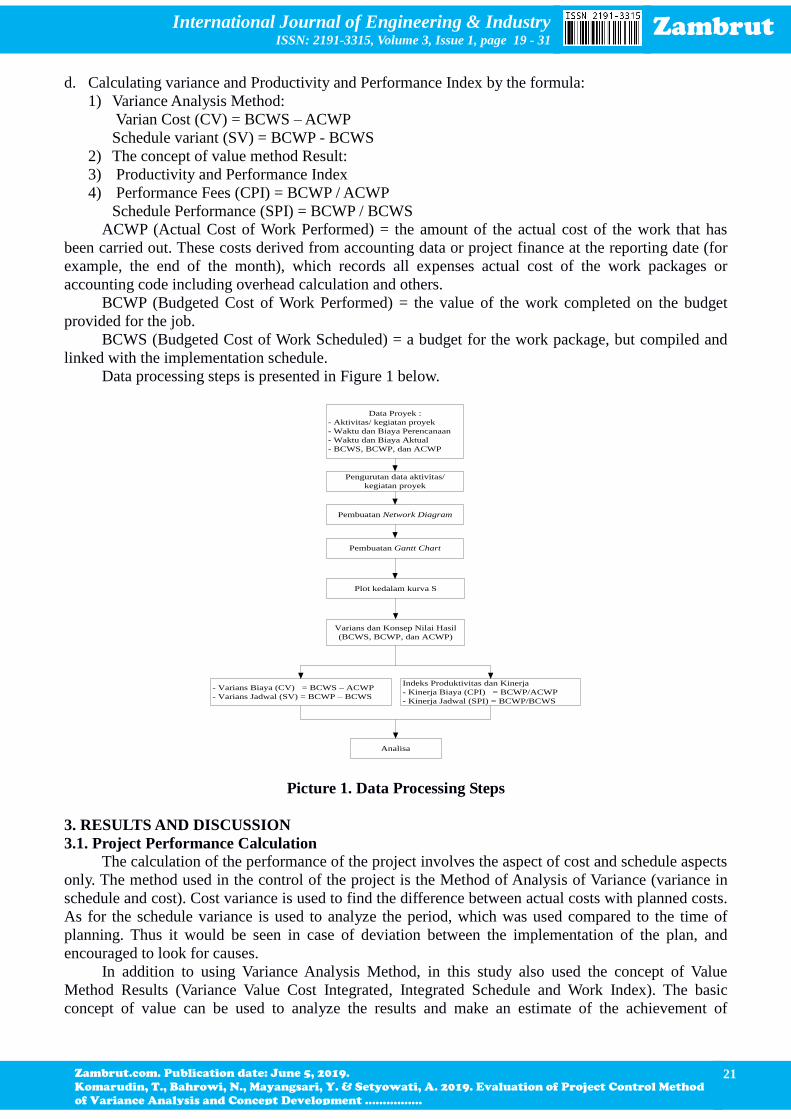

d. Calculating variance and Productivity and Performance Index by the formula:

1) Variance Analysis Method:

Varian Cost (CV) = BCWS – ACWP

Schedule variant (SV) = BCWP - BCWS

2) The concept of value method Result:

3) Productivity and Performance Index

4) Performance Fees (CPI) = BCWP / ACWP

Schedule Performance (SPI) = BCWP / BCWS

ACWP (Actual Cost of Work Performed) = the amount of the actual cost of the work that has

been carried out. These costs derived from accounting data or project finance at the reporting date (for

example, the end of the month), which records all expenses actual cost of the work packages or

accounting code including overhead calculation and others.

BCWP (Budgeted Cost of Work Performed) = the value of the work completed on the budget

provided for the job.

BCWS (Budgeted Cost of Work Scheduled) = a budget for the work package, but compiled and

linked with the implementation schedule.

Data processing steps is presented in Figure 1 below.

Data Proyek :

- Aktivitas/ kegiatan proyek

- Waktu dan Biaya Perencanaan

- Waktu dan Biaya Aktual

- BCWS, BCWP, dan ACWP

Pengurutan data aktivitas/

kegiatan proyek

Pembuatan Network Diagram

Pembuatan Gantt Chart

Plot kedalam kurva S

Varians dan Konsep Nilai Hasil

(BCWS, BCWP, dan ACWP)

- Varians Biaya (CV) = BCWS – ACWP

- Varians Jadwal (SV) = BCWP – BCWS

Indeks Produktivitas dan Kinerja

- Kinerja Biaya (CPI) = BCWP/ACWP

- Kinerja Jadwal (SPI) = BCWP/BCWS

Analisa

Picture 1. Data Processing Steps

3. RESULTS AND DISCUSSION

3.1. Project Performance Calculation The calculation of the performance of the project involves the aspect of cost and schedule aspects

only. The method used in the control of the project is the Method of Analysis of Variance (variance in

schedule and cost). Cost variance is used to find the difference between actual costs with planned costs.

As for the schedule variance is used to analyze the period, which was used compared to the time of

planning. Thus it would be seen in case of deviation between the implementation of the plan, and

encouraged to look for causes.

In addition to using Variance Analysis Method, in this study also used the concept of Value

Method Results (Variance Value Cost Integrated, Integrated Schedule and Work Index). The basic

concept of value can be used to analyze the results and make an estimate of the achievement of

International Journal of Engineering & Industry ISSN: 2191-3315, Volume 3, Issue 1, page 19 - 31

Zambrut

Zambrut.com. Publication date: June 5, 2019.

Komarudin, T., Bahrowi, N., Mayangsari, Y. & Setyowati, A. 2019. Evaluation of Project Control Method

of Variance Analysis and Concept Development ................

22

performance targets. So we use three indicators, namely; ACWP ((Actual Cost of Work Performed),

BCWP (Budgeted Cost of Work Performed) and BCWS (Budgeted Cost of Work Scheduled).

3.1.1. ACWP (Actual Cost of Work Performed)

ACWP is the actual amount of spending or the funds used to carry out the work at a certain time.

Table 1. ACWP (Actual Cost of Work Performed)

No. Week- ACWP Cumulative ACWP

1 1 USD 8,850,366.25 USD 8,850,366.25

2 2 USD 2,254,271.25 USD 11,104,637.50

3 3 USD 12,669,180.21 USD 23,773,817.71

4 4 USD 53,647,641.26 USD 77,421,458.97

5 5 USD 53,019,947.65 USD 130,441,406.62

6 6 USD 31,022,830.15 USD 161,464,236.77

7 7 USD 59,575,971.81 USD 221,040,208.58

8 8 USD 23,266,067.41 USD 244,306,275.99

9 9 USD 27,091,832.47 USD 271,398,108.46

10 10 USD 43,959,819.04 USD 315,357,927.50

11 11 USD 17,984,197.50 USD 333,342,125.00

12 12 USD 28,660,337.50 USD 362,002,462.50

13 13 USD 31,343,987.50 USD 393,346,450.00

14 14 USD 9,982,800.00 USD 403,329,250.00

15 15 USD 9,982,800.00 USD 413,312,050.00

16 16 USD 2,264,614.29 USD 415,576,664.29

17 17 USD 1,193,464.29 USD 416,770,128.58

18 18 Rp 862,958.92 USD 417,633,087.50

19 19 Rp 338,316.07 USD 417,971,403.57

20 20 USD 19,315,177.68 USD 437,286,581.25

21 21 USD 25,480,075.00 USD 462,766,656.25

22 22 USD 8,576,343.75 USD 471,343,000.00

3.1.2. BCWP (Budgeted Cost of Work Performed)

This indicator shows the value of the work completed on the budget provided for the job. When

compared with the BCWP ACWP numbers, it would look a comparison between the cost incurred for

work already carried out on the costs that should be spent for this purpose. Calculation formula to

determine the value Hasi ladalah as follows:

Table 2. BCWP (Budgeted Cost of Work Performed)

No. Sunday

to-

Weight

Cumulative budgets BCWP

1 1 1.89% USD 8,850,366.25 Rp 167,221.69

2 2 2:31% USD 10,824,637.50 Rp 250,147.90

3 3 5:08% USD 23,780,683.33 USD 1,207,309.99

4 4 17:02% USD 79,735,088.97 USD 13,572,789.06

5 5 27.41% USD 128,381,406.62 USD 35,186,364.13

6 6 34.03% USD 159,404,236.77 USD 54,246,266.55

7 7 46.66% USD 218,580,208.58 USD 101,998,035.03

8 8 51.63% USD 241,846,275.99 USD 124,867,363.51

9 9 57.58% USD 269,708,875.96 USD 155,296,122.17

International Journal of Engineering & Industry ISSN: 2191-3315, Volume 3, Issue 1, page 19 - 31

Zambrut

Zambrut.com. Publication date: June 5, 2019.

Komarudin, T., Bahrowi, N., Mayangsari, Y. & Setyowati, A. 2019. Evaluation of Project Control Method

of Variance Analysis and Concept Development ................

23

10 10 66.76% USD 312,696,927.50 USD 208,745,614.92

11 11 70.60% USD 330,681,125.00 USD 233,447,348.78

12 12 76.71% USD 359,341,462.50 USD 275,667,009.68

13 13 83.41% USD 390,685,450.00 USD 325,855,164.11

14 14 85.54% USD 400,668,250.00 USD 342,720,427.99

15 15 87.67% USD 410,651,050.00 USD 360,011,197.07

16 16 88.15% USD 412,915,664.29 USD 363,992,847.81

17 17 88.41% USD 414,109,128.58 USD 366,100,010.62

18 18 88.59% USD 14,972,087.50 USD 367,627,426.60

19 19 88.66% USD 415,310,403.57 USD 368,227,105.32

20 20 93.53% USD 438,116,525.45 USD 409,778,721.12

21 21 99.39% USD 465,555,218.75 USD 462,713,884.95

22 22 100.00% USD 468,414,000.00 USD 468,414,000.00

3.1.3. BCWS (Budgeted Cost of Work Scheduled)

This figure shows the budget for the work package, but compiled and linked with the

implementation schedule. Here, there was a mix between cost, schedule and scope of work, where

every element of the work has been given the allocation of costs and schedules can be a benchmark in

the implementation of the work.

Table 3. BCWS (Budgeted Cost of Work Scheduled)

No. Week- BCWS Cumulative BCWS

1 1 USD 8,850,366.25 USD 8,850,366.25

2 2 USD 1,974,271.25 USD 10,824,637.50

3 3 USD 12,956,045.83 USD 23,780,683.33

4 4 USD 55,954,405.64 USD 79,735,088.97

5 5 USD 48,646,317.65 USD 128,381,406.62

6 6 USD 31,022,830.15 USD 159,404,236.77

7 7 USD 59,175,971.81 USD 218,580,208.58

8 8 USD 23,266,067.41 USD 241,846,275.99

9 9 USD 27,862,599.97 USD 269,708,875.96

10 10 USD 42,988,051.54 USD 312,696,927.50

11 11 USD 17,984,197.50 USD 330,681,125.00

12 12 USD 28,660,337.50 USD 359,341,462.50

13 13 USD 31,343,987.50 USD 390,685,450.00

14 14 USD 9,982,800.00 USD 400,668,250.00

15 15 USD 9,982,800.00 USD 410,651,050.00

16 16 USD 2,264,614.29 USD 412,915,664.29

17 17 USD 1,193,464.29 USD 414,109,128.58

18 18 Rp 862,958.92 USD 414,972,087.50

19 19 Rp 338,316.07 USD 415,310,403.57

20 20 USD 22,806,121.88 USD 438,116,525.45

21 21 USD 27,438,693.30 USD 465,555,218.75

22 22 USD 2,858,781.25 USD 468,414,000.00

After getting the value of the indicators mentioned above, then proceed to make the S-curve

combination.

International Journal of Engineering & Industry ISSN: 2191-3315, Volume 3, Issue 1, page 19 - 31

Zambrut

Zambrut.com. Publication date: June 5, 2019.

Komarudin, T., Bahrowi, N., Mayangsari, Y. & Setyowati, A. 2019. Evaluation of Project Control Method

of Variance Analysis and Concept Development ................

24

Rp-

Rp100,000,000.00

Rp200,000,000.00

Rp300,000,000.00

Rp400,000,000.00

1 2 3 4 5 6 7 8 9 10111213141516171819202122

Minggu Ke-

Bia

ya

BCWS ACWP BCWP

Figure 2 ACWP composite curve, BCWS, and BCWP

3.2. Calculation of Cost Performance Index Calculation of cost performance using Concept Values Results and indicators that are used are

also the same as the indicators to look for cost variance value is ACWP (Actual Cost of Work

Performed) and BCWP (Budgeted Cost of Work Performed). But that is sought is the comparison by

using the formula:

Table 4. Cost Performance Index

No. Sunday

to -

Cumulative (Rp.)

CPI Performance

ACWP BCWP

1 1 USD

8,850,366.25 Rp 167,221.69 0.0189 Cost Budget <Actual Costs

2 2 USD

11,104,637.50 Rp 250,147.90 0.0225 Cost Budget <Actual Costs

3 3 USD

23,773,817.71

USD

1,207,309.99 0.0508 Cost Budget <Actual Costs

4 4 USD

77,421,458.97

USD

13,572,789.06 0.1753 Cost Budget <Actual Costs

5 5 USD

130,441,406.62

USD

35,186,364.13 0.2697 Cost Budget <Actual Costs

6 6 USD

161,464,236.77

USD

54,246,266.55 0.3360 Cost Budget <Actual Costs

7 7 USD

221,040,208.58

USD

101,998,035.03 0.4614 Cost Budget <Actual Costs

8 8 USD

244,306,275.99

USD

124,867,363.51 0.5111 Cost Budget <Actual Costs

9 9 USD

271,398,108.46

USD

155,296,122.17 0.5722 Cost Budget <Actual Costs

10 10 USD

315,357,927.50

USD

208,745,614.92 0.6619 Cost Budget <Actual Costs

11 11 USD

333,342,125.00

USD

233,447,348.78 0.7003 Cost Budget <Actual Costs

12 12 USD

362,002,462.50

USD

275,667,009.68 0.7615 Cost Budget <Actual Costs

13 13 USD

393,346,450.00

USD

325,855,164.11 0.8284 Cost Budget <Actual Costs

14 14 USD

403,329,250.00

USD

342,720,427.99 0.8497 Cost Budget <Actual Costs

International Journal of Engineering & Industry ISSN: 2191-3315, Volume 3, Issue 1, page 19 - 31

Zambrut

Zambrut.com. Publication date: June 5, 2019.

Komarudin, T., Bahrowi, N., Mayangsari, Y. & Setyowati, A. 2019. Evaluation of Project Control Method

of Variance Analysis and Concept Development ................

25

15 15 USD

413,312,050.00

USD

360,011,197.07 0.8710 Cost Budget <Actual Costs

16 16 USD

415,576,664.29

USD

363,992,847.81 0.8759 Cost Budget <Actual Costs

17 17 USD

416,770,128.58

USD

366,100,010.62 0.8784 Cost Budget <Actual Costs

18 18 USD

417,633,087.50

USD

367,627,426.60 0.8803 Cost Budget <Actual Costs

19 19 USD

417,971,403.57

USD

368,227,105.32 0.8810 Cost Budget <Actual Costs

20 20 USD

437,286,581.25

USD

409,778,721.12 0.9371 Cost Budget <Actual Costs

21 21 USD

462,766,656.25

USD

462,713,884.95 0.9999 Cost Budget <Actual Costs

22 22 USD

471,343,000.00

USD

468,414,000.00 0.9938 Cost Budget <Actual Costs

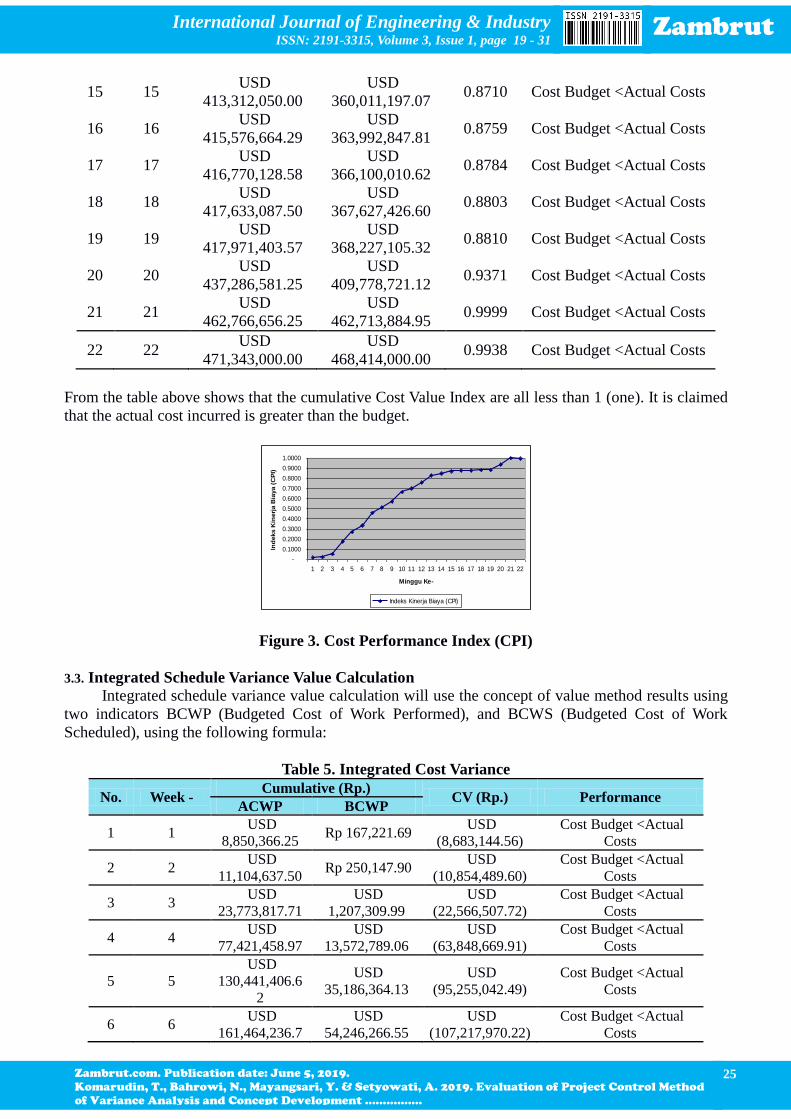

From the table above shows that the cumulative Cost Value Index are all less than 1 (one). It is claimed

that the actual cost incurred is greater than the budget.

-

0.1000

0.2000

0.3000

0.4000

0.5000

0.6000

0.7000

0.8000

0.9000

1.0000

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22

Minggu Ke-

Ind

eks K

inerj

a B

iaya (

CP

I)

Indeks Kinerja Biaya (CPI)

Figure 3. Cost Performance Index (CPI)

3.3. Integrated Schedule Variance Value Calculation

Integrated schedule variance value calculation will use the concept of value method results using

two indicators BCWP (Budgeted Cost of Work Performed), and BCWS (Budgeted Cost of Work

Scheduled), using the following formula:

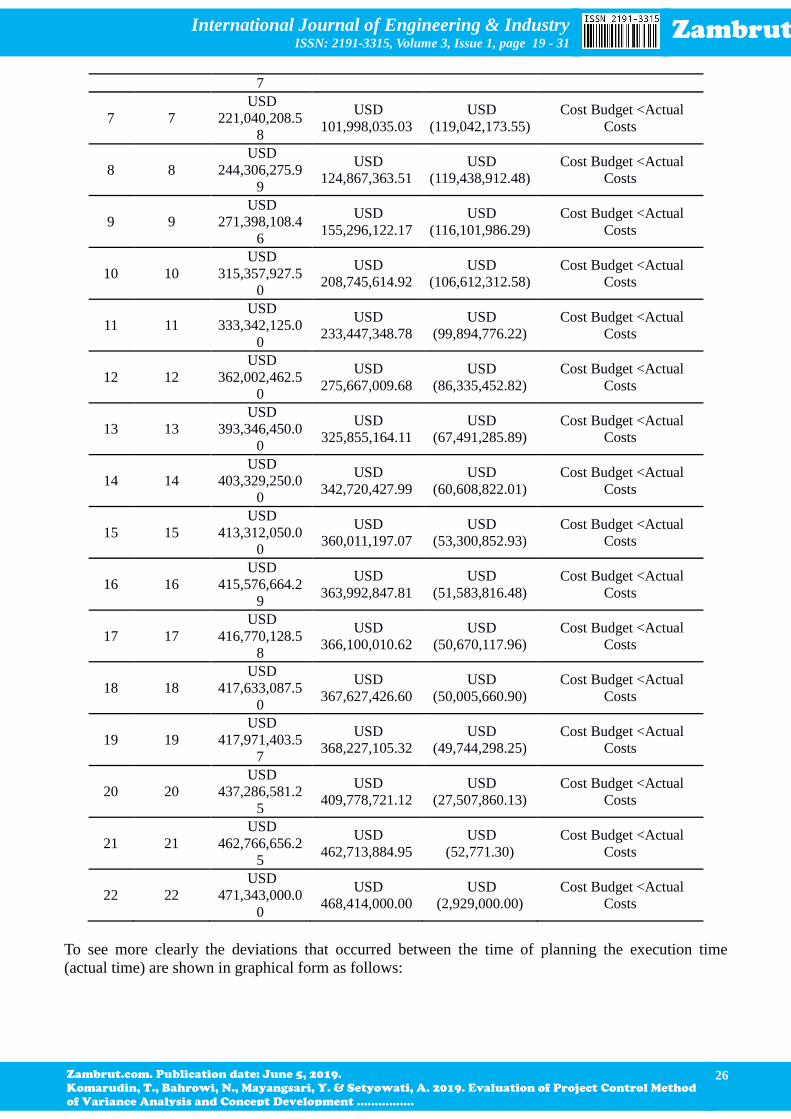

Table 5. Integrated Cost Variance

No. Week - Cumulative (Rp.)

CV (Rp.) Performance ACWP BCWP

1 1 USD

8,850,366.25 Rp 167,221.69

USD

(8,683,144.56)

Cost Budget <Actual

Costs

2 2 USD

11,104,637.50 Rp 250,147.90

USD

(10,854,489.60)

Cost Budget <Actual

Costs

3 3 USD

23,773,817.71

USD

1,207,309.99

USD

(22,566,507.72)

Cost Budget <Actual

Costs

4 4 USD

77,421,458.97

USD

13,572,789.06

USD

(63,848,669.91)

Cost Budget <Actual

Costs

5 5

USD

130,441,406.6

2

USD

35,186,364.13

USD

(95,255,042.49)

Cost Budget <Actual

Costs

6 6 USD

161,464,236.7

USD

54,246,266.55

USD

(107,217,970.22)

Cost Budget <Actual

Costs

International Journal of Engineering & Industry ISSN: 2191-3315, Volume 3, Issue 1, page 19 - 31

Zambrut

Zambrut.com. Publication date: June 5, 2019.

Komarudin, T., Bahrowi, N., Mayangsari, Y. & Setyowati, A. 2019. Evaluation of Project Control Method

of Variance Analysis and Concept Development ................

26

7

7 7

USD

221,040,208.5

8

USD

101,998,035.03

USD

(119,042,173.55)

Cost Budget <Actual

Costs

8 8

USD

244,306,275.9

9

USD

124,867,363.51

USD

(119,438,912.48)

Cost Budget <Actual

Costs

9 9

USD

271,398,108.4

6

USD

155,296,122.17

USD

(116,101,986.29)

Cost Budget <Actual

Costs

10 10

USD

315,357,927.5

0

USD

208,745,614.92

USD

(106,612,312.58)

Cost Budget <Actual

Costs

11 11

USD

333,342,125.0

0

USD

233,447,348.78

USD

(99,894,776.22)

Cost Budget <Actual

Costs

12 12

USD

362,002,462.5

0

USD

275,667,009.68

USD

(86,335,452.82)

Cost Budget <Actual

Costs

13 13

USD

393,346,450.0

0

USD

325,855,164.11

USD

(67,491,285.89)

Cost Budget <Actual

Costs

14 14

USD

403,329,250.0

0

USD

342,720,427.99

USD

(60,608,822.01)

Cost Budget <Actual

Costs

15 15

USD

413,312,050.0

0

USD

360,011,197.07

USD

(53,300,852.93)

Cost Budget <Actual

Costs

16 16

USD

415,576,664.2

9

USD

363,992,847.81

USD

(51,583,816.48)

Cost Budget <Actual

Costs

17 17

USD

416,770,128.5

8

USD

366,100,010.62

USD

(50,670,117.96)

Cost Budget <Actual

Costs

18 18

USD

417,633,087.5

0

USD

367,627,426.60

USD

(50,005,660.90)

Cost Budget <Actual

Costs

19 19

USD

417,971,403.5

7

USD

368,227,105.32

USD

(49,744,298.25)

Cost Budget <Actual

Costs

20 20

USD

437,286,581.2

5

USD

409,778,721.12

USD

(27,507,860.13)

Cost Budget <Actual

Costs

21 21

USD

462,766,656.2

5

USD

462,713,884.95

USD

(52,771.30)

Cost Budget <Actual

Costs

22 22

USD

471,343,000.0

0

USD

468,414,000.00

USD

(2,929,000.00)

Cost Budget <Actual

Costs

To see more clearly the deviations that occurred between the time of planning the execution time

(actual time) are shown in graphical form as follows:

International Journal of Engineering & Industry ISSN: 2191-3315, Volume 3, Issue 1, page 19 - 31

Zambrut

Zambrut.com. Publication date: June 5, 2019.

Komarudin, T., Bahrowi, N., Mayangsari, Y. & Setyowati, A. 2019. Evaluation of Project Control Method

of Variance Analysis and Concept Development ................

27

Rp(120,000,000.00)

Rp(100,000,000.00)

Rp(80,000,000.00)

Rp(60,000,000.00)

Rp(40,000,000.00)

Rp(20,000,000.00)

Rp-

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22

Minggu Ke-

Bia

ya

Varians Jadw al (SV)

Figure 4. Value of Integrated Schedule Variance (SV)

3.4. Calculation Schedule Performance Index The schedule performance index calculation also menggunakanMetode concept of value results,

which sought here is the same, namely ACWP ((Actual Cost of Work Performed) and BCWS

(Budgeted Cost of Work Scheduled).

Table 6. Schedule Performance Index

No. Week- BCWP BCWS SPI performance

1 1 Rp 167,221.69

USD

8,850,366.25 0:02 Late

2 2 Rp 250,147.90

USD

10,824,637.50 0:02 Late

3 3

USD

1,207,309.99

USD

23,780,683.33 0:05 Late

4 4

USD

13,572,789.06

USD

79,735,088.97 0:17 Late

5 5

USD

35,186,364.13

USD

128,381,406.62 0:27 Late

6 6

USD

54,246,266.55

USD

159,404,236.77 0:34 Late

7 7

USD

101,998,035.03

USD

218,580,208.58 0:47 Late

8 8

USD

124,867,363.51

USD

241,846,275.99 0:52 Late

9 9

USD

155,296,122.17

USD

269,708,875.96 0:58 Late

10 10

USD

208,745,614.92

USD

312,696,927.50 0.67 Late

11 11

USD

233,447,348.78

USD

330,681,125.00 0.71 Late

12 12

USD

275,667,009.68

USD

359,341,462.50 0.77 Late

13 13

USD

325,855,164.11

USD

390,685,450.00 0.83 Late

14 14

USD

342,720,427.99

USD

400,668,250.00 0.86 Late

15 15

USD

360,011,197.07

USD

410,651,050.00 0.88 Late

International Journal of Engineering & Industry ISSN: 2191-3315, Volume 3, Issue 1, page 19 - 31

Zambrut

Zambrut.com. Publication date: June 5, 2019.

Komarudin, T., Bahrowi, N., Mayangsari, Y. & Setyowati, A. 2019. Evaluation of Project Control Method

of Variance Analysis and Concept Development ................

28

16 16

USD

363,992,847.81

USD

412,915,664.29 0.88 Late

17 17

USD

366,100,010.62

USD

414,109,128.58 0.88 Late

18 18

USD

367,627,426.60

USD

414,972,087.50 0.89 Late

19 19

USD

368,227,105.32

USD

415,310,403.57 0.89 Late

20 20

USD

409,778,721.12

USD

438,116,525.45 0.94 Late

21 21

USD

462,713,884.95

USD

465,555,218.75 0.99 Late

22 22

USD

468,414,000.00

USD

468,414,000.00 1:00 Right

To see more clearly the deviations that occurred between the time of planning the execution time

(actual time) are shown in graphical form as follows:

0.0000

0.2000

0.4000

0.6000

0.8000

1.0000

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

Minggu ke-

In

dek

s K

inerja

Ja

dw

al

Indeks Kinerja Jadwal (SPI)

Figure 5. Schedule Performance Index

3.5. Project Performance Analysis per Sunday

Performance analysis of the project include cost and schedule performance. Because the unit of

time used in the Schedule Variance Variance Analysis Method is a day, whereas in this analysis units

used are the week, the schedule variance analysis will be done separately. On the Method of Analysis of

Variance, Cost Variance value obtained from a direct comparison between the costs used in the

implementation of the project with the budgeted costs. For example, Project Performance analysis

presented Sunday All 3 are presented in Table 7.

International Journal of Engineering & Industry ISSN: 2191-3315, Volume 3, Issue 1, page 19 - 31

Zambrut

Zambrut.com. Publication date: June 5, 2019.

Komarudin, T., Bahrowi, N., Mayangsari, Y. & Setyowati, A. 2019. Evaluation of Project Control Method

of Variance Analysis and Concept Development ................

29

Table 7. Project Performance Analysis 3rd Sunday

The third week

No. The method used Cost Schedule

1

Methods of Analysis of

Variance

Cost Variance Value Rp. 286,865.62

2

The concept of value

method Result

Integrated Cost Variance

(CV)

Rp.

(22,566,507.72)

Cost Performance Index

(CPI) 0.0508

Integrated Schedule

Variance (SV)

USD

(22,573,373.34)

Schedule Performance

Index (SPI) 0:05

Information :

a. Methods of Analysis of Variance.

For Cost Variance Value = Rp. 286,865.62, this means that the costs incurred in the third week is

less than the planned costs. in the third week it costs Rp. 23,773,817.71, while the cost is budgeted

at Rp. 23,780,683.33.

b. The concept of value method Result.

For Integrated Cost Variance = Rp. (22,566,507.72) or-Rp. 22,566,507.72, and Cost Performance

Index = 0.0508 this means that the actual cost of the expenditure is greater than the budget. For

Integrated Schedule Variance = Rp. (22,573,373.34) or-Rp. 22,573,373.34, and the Schedule

Performance Index = 0:05 this means that the implementation schedule behind schedule planning. In

the third week of this, the cost is less than the budget, this was due to the advance workmanship

excavation activities. This is due to the workload of the second week has accelerated during the day.

The big difference in the value of the varaians for Variant Analysis Method with Method Concept

of Value Analysis Method Results Varaians due to the variance obtained from the direct comparison

between the cost of implementation (actual cost) to the planned cost (budget). While the concept of

Value Method Results, integrated cost variance value obtained from the comparison between the results

of the completed work against budgeted costs (BCWP) and the actual cost of the work completed

(ACWP). For example, in the third week Methods of Analysis of Variance, Cost Variance value

obtained is positive (Rp. 286,865.62) is different when compared to the value of Integrated Cost

Variance on Concept of Value method results were negative Rp. (22,566,507.72) or-Rp. 22,566,507.72.

3.6. Performance Trend Analysis Project To see the trend of the performance of the overall project, the illustrated chart that reflects the

trend of the performance of the project during the period of analysis, in this case the unit of time used is

the week, so the trend images directly presented in units of weeks. Project performance trend analysis,

both costs and project schedule will be served directly by using two methods simultaneously, namely

Method of Analysis of Variance (Cost Variance value) and the Method Concept of Value Results

(Variance Value of Integrated Cost and Cost Performance Index) for more details can be seen on the

own image the following picture:

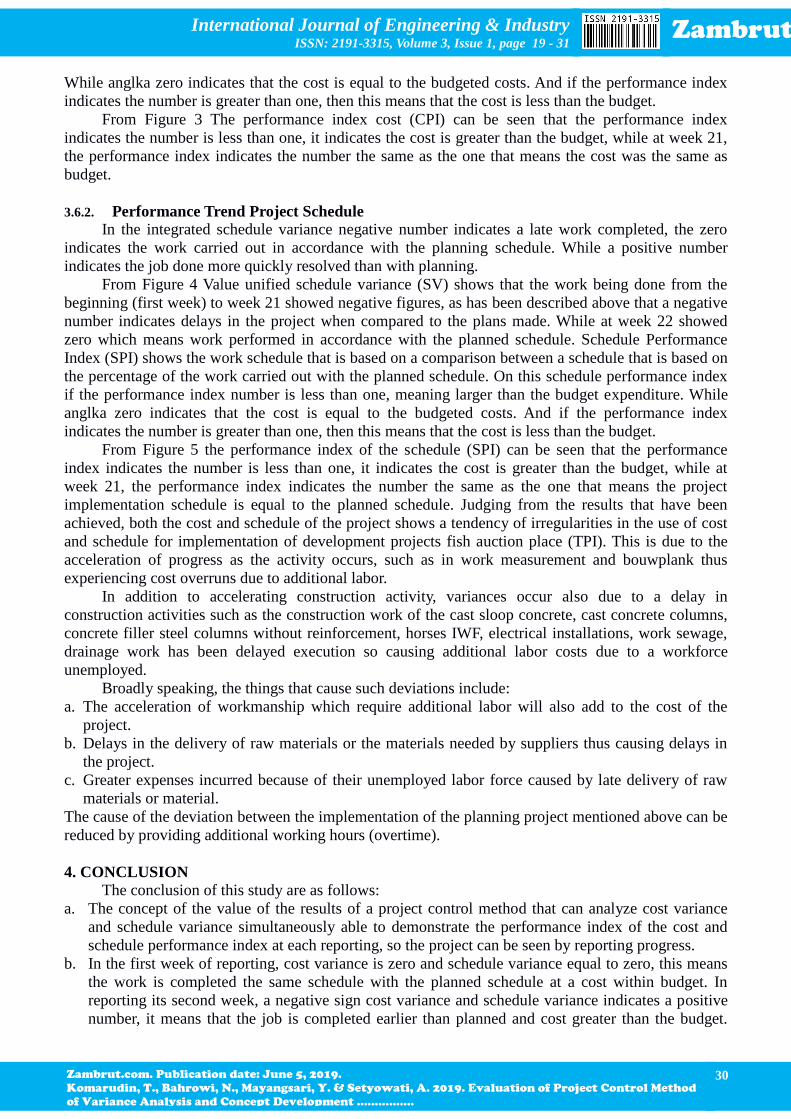

3.6.1. Performance Trend Project Cost Performance Index shows expenses incurred costs based on a comparison between the costs

incurred by the percentage of work performed by the actual costs incurred. At this cost performance

index if the performance index number is less than one, meaning larger than the budget expenditure.

International Journal of Engineering & Industry ISSN: 2191-3315, Volume 3, Issue 1, page 19 - 31

Zambrut

Zambrut.com. Publication date: June 5, 2019.

Komarudin, T., Bahrowi, N., Mayangsari, Y. & Setyowati, A. 2019. Evaluation of Project Control Method

of Variance Analysis and Concept Development ................

30

While anglka zero indicates that the cost is equal to the budgeted costs. And if the performance index

indicates the number is greater than one, then this means that the cost is less than the budget.

From Figure 3 The performance index cost (CPI) can be seen that the performance index

indicates the number is less than one, it indicates the cost is greater than the budget, while at week 21,

the performance index indicates the number the same as the one that means the cost was the same as

budget.

3.6.2. Performance Trend Project Schedule In the integrated schedule variance negative number indicates a late work completed, the zero

indicates the work carried out in accordance with the planning schedule. While a positive number

indicates the job done more quickly resolved than with planning.

From Figure 4 Value unified schedule variance (SV) shows that the work being done from the

beginning (first week) to week 21 showed negative figures, as has been described above that a negative

number indicates delays in the project when compared to the plans made. While at week 22 showed

zero which means work performed in accordance with the planned schedule. Schedule Performance

Index (SPI) shows the work schedule that is based on a comparison between a schedule that is based on

the percentage of the work carried out with the planned schedule. On this schedule performance index

if the performance index number is less than one, meaning larger than the budget expenditure. While

anglka zero indicates that the cost is equal to the budgeted costs. And if the performance index

indicates the number is greater than one, then this means that the cost is less than the budget.

From Figure 5 the performance index of the schedule (SPI) can be seen that the performance

index indicates the number is less than one, it indicates the cost is greater than the budget, while at

week 21, the performance index indicates the number the same as the one that means the project

implementation schedule is equal to the planned schedule. Judging from the results that have been

achieved, both the cost and schedule of the project shows a tendency of irregularities in the use of cost

and schedule for implementation of development projects fish auction place (TPI). This is due to the

acceleration of progress as the activity occurs, such as in work measurement and bouwplank thus

experiencing cost overruns due to additional labor.

In addition to accelerating construction activity, variances occur also due to a delay in

construction activities such as the construction work of the cast sloop concrete, cast concrete columns,

concrete filler steel columns without reinforcement, horses IWF, electrical installations, work sewage,

drainage work has been delayed execution so causing additional labor costs due to a workforce

unemployed.

Broadly speaking, the things that cause such deviations include:

a. The acceleration of workmanship which require additional labor will also add to the cost of the

project.

b. Delays in the delivery of raw materials or the materials needed by suppliers thus causing delays in

the project.

c. Greater expenses incurred because of their unemployed labor force caused by late delivery of raw

materials or material.

The cause of the deviation between the implementation of the planning project mentioned above can be

reduced by providing additional working hours (overtime).

4. CONCLUSION The conclusion of this study are as follows:

a. The concept of the value of the results of a project control method that can analyze cost variance

and schedule variance simultaneously able to demonstrate the performance index of the cost and

schedule performance index at each reporting, so the project can be seen by reporting progress.

b. In the first week of reporting, cost variance is zero and schedule variance equal to zero, this means

the work is completed the same schedule with the planned schedule at a cost within budget. In

reporting its second week, a negative sign cost variance and schedule variance indicates a positive

number, it means that the job is completed earlier than planned and cost greater than the budget.

International Journal of Engineering & Industry ISSN: 2191-3315, Volume 3, Issue 1, page 19 - 31

Zambrut

Zambrut.com. Publication date: June 5, 2019.

Komarudin, T., Bahrowi, N., Mayangsari, Y. & Setyowati, A. 2019. Evaluation of Project Control Method

of Variance Analysis and Concept Development ................

31

While in the third week of reporting, cost variance value of positive and schedule variance value of

zero, it indicates that the work accomplished in accordance with the schedule and cost less than the

budget. The amount that exceeds the cost of the project budget is 0.01% of the available budget.

5. REFERENCES [1] Lock, Dennis, (1987), Project management, Third Edition, Erland, Jakarta.

[2] Reksohadiprodjo, Sukanto, (1987), Project Management, Second Edition, BPFE, Yogyakarta.

[3] Suharto, Faith, (1998), Project Management (From Conceptual Up Operations), Volume 1, Second

Edition, PT. Erland, Jakarta.

[4] Ali, Tubagus Haedar, (1995), Principles of Network Planning, PT. Gramedia, Jakarta.

[5] Department of Livestock and Fisheries Cianjur (2008). Fisheries Production Development.

Zambrut Journal, Link Access;

https://zambrut.com

https://zambrut.com/development-value/

© Copyright International Journal of Zambrut | Zambrut, Inc.