interest rate risk management for the banking book: macro …old.efrag.org/files/macro hedge...

TRANSCRIPT

Interest Rate Risk Management for the Banking Book:

Macro Hedging

Giuseppe Loforese

Head of ALM - Intesa Sanpaolo

Chair of ALM – Hedge Accounting WG – EBF

Co-Chairman IRRBB WG - EBF

Overview

Models

Representing Hedging Activity

AGENDA IRRBB: Macro Hedging

As pointed out in Basel Committee July 2004 Chapter X, Principle 14:

All material interest rate risk associated with the banking book must be assessed. To do this, internal systems must accurately incorporate all of a bank’s interest rate sensitive on- and off-balance sheet holdings;

internal systems must be capable of measuring risk using both an earnings and economic/sensitivity approach.

In this respect, best practice should at least comprise:

A. A methodology to identify the different risk components, with particular focus on those affecting the IRR (slide 11)

B. A set of instruments to deal with the management of IRR:

1. Standard measures for IRR sensitivity (PV01, bucketing, etc.) & limits. Slide 6-8

2. Models for optionalities (prepayment option & sight depos) & for Equity. Slides 13 -21

3. Standard measures for refixing and basis risk.

Slide 12 3

OVERVIEW IRR for the banking book: regulatory framework

Trading book vs Banking book: as for the management of interest rate risk, the trading book exposure is usually treated separately from the one arising from the banking book.

IRR management activity relates to the “pure” interest rate component of the larger Net Interest Margin (NIM), which includes both credit & liquidity spreads.

The main objective of IRR management of a bank with an “originate and hold” business model is to reduce the volatility of the “pure” interest margin and to produce a stable stream of “pure” interest income.

4

OVERVIEW trading vs banking book, objective of IRR management

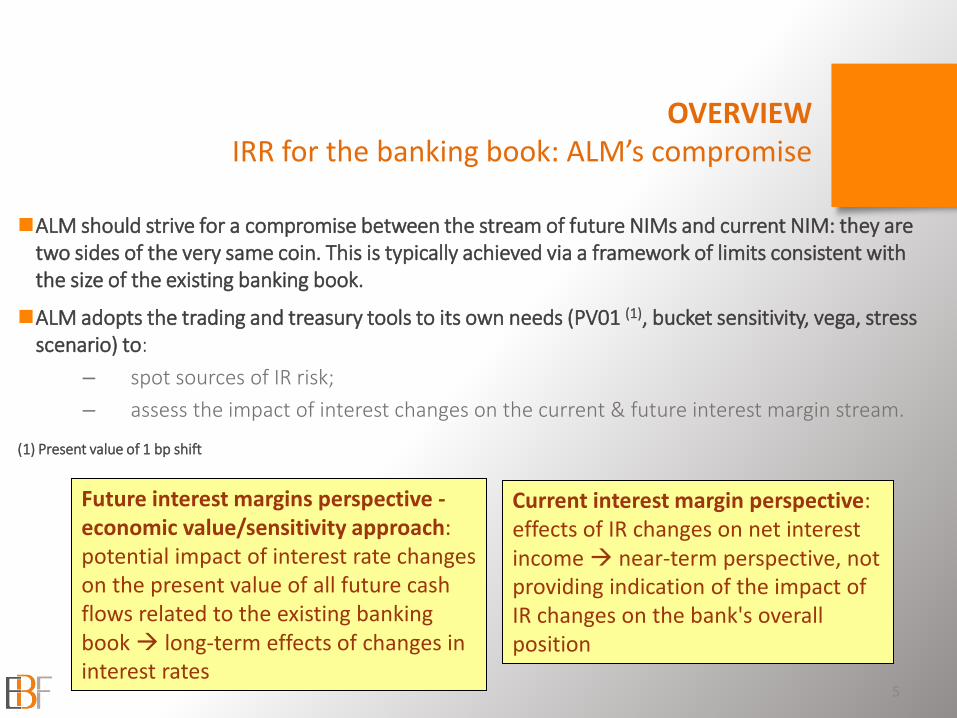

ALM should strive for a compromise between the stream of future NIMs and current NIM: they are two sides of the very same coin. This is typically achieved via a framework of limits consistent with the size of the existing banking book.

ALM adopts the trading and treasury tools to its own needs (PV01 (1), bucket sensitivity, vega, stress scenario) to:

– spot sources of IR risk;

– assess the impact of interest changes on the current & future interest margin stream. (1) Present value of 1 bp shift

5

Future interest margins perspective - economic value/sensitivity approach: potential impact of interest rate changes on the present value of all future cash flows related to the existing banking book long-term effects of changes in interest rates

Current interest margin perspective: effects of IR changes on net interest income near-term perspective, not providing indication of the impact of IR changes on the bank's overall position

OVERVIEW IRR for the banking book: ALM’s compromise

6

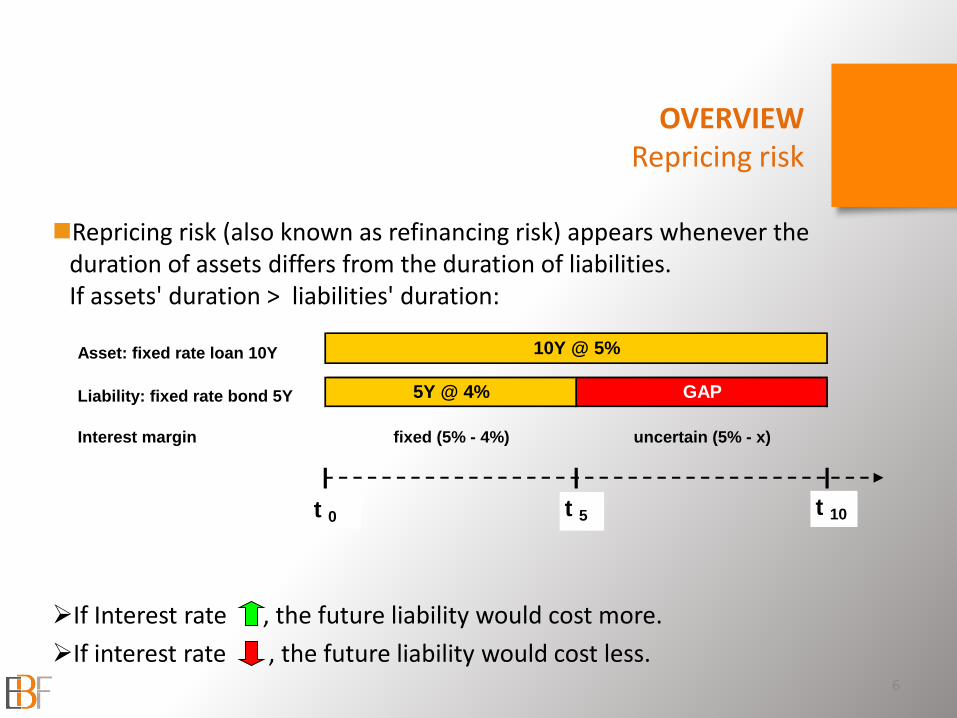

Repricing risk (also known as refinancing risk) appears whenever the duration of assets differs from the duration of liabilities. If assets' duration > liabilities' duration:

If Interest rate , the future liability would cost more.

If interest rate , the future liability would cost less.

OVERVIEW Repricing risk

Asset: fixed rate loan 10Y

Liability: fixed rate bond 5Y

Interest margin

10Y @ 5%

5Y @ 4% GAP

uncertain (5% - x)fixed (5% - 4%)

t 5 t 10t 0

7

A better understanding of IRR exposure could be assessed by bucketing cash flows and theirs sensitivities. Let’s assume the following banking book:

ASSETS

Fixed rate mortgages 15 €/bn 20y amort. 4.00%

LIABILITIES

Fixed rate liabilities 15 €/bn 10y bullet 3.50%

Interest rate swap 10 €/bn 10y bullet Rec 3.50% Pay EUR1M

Notional Maturity Rate

Notional Maturity Rate

Not prepayable

OVERVIEW Repricing risk

-15.00

-10.00

-5.00

-

5.00

10.00

15.00

0-1.5y 1.5-3y 3-5y 5-7y 7-10y 10-15y 15-20y

Fixed rate liabilities

Interest rate swap

Fixed rate mortgages

Net position

8

-15.0

-10.0

-5.0

-

5.0

10.0

15.0

1y 2y 3y 4y 5y 6y 7y 8y 9y 10y 11y 12y 13y 14y 15y 16y 17y 18y 19y 20y

Fixed rate liabilities

Interest rate swap (fixed leg)

Fixed rate mortgages

Net Cash Flows

Shift sensitivity (PV01 €/mln)

-15.00

-10.00

-5.00

-

5.00

10.00

15.00

0-1.5y 1.5-3y 3-5y 5-7y 7-10y 10-15y

Fixed rate mortgages

Fixed rate liabilities

Interest rate swap

Net position

Cash flows (€/bn)

-15.0

-10.0

-5.0

-

5.0

10.0

15.0

1y 2y 3y 4y 5y 6y 7y 8y 9y 10y 11y 12y 13y 14y 15y

Fixed rate mortgages

Fixed rate liabilities

Interest rate swap (fixed leg)

Net Cash Flows

Upper limit

Lower limit

OVERVIEW Repricing risk: bucket sensitivity & limits

-15.0

-10.0

-5.0

-

5.0

10.0

15.0

1y 2y 3y 4y 5y 6y 7y 8y 9y 10y 11y 12y 13y 14y 15y 16y 17y 18y 19y 20y

Fixed rate liabilities

Interest rate swap (fixed leg)

Fixed rate mortgages

Net Cash Flows

As mentioned, the Banking Book is what is not managed in the Trading Book

All single items belonging to a specific category (mortgages, bonds, sight depos, equity, etc.) flow undiscretionally into the banking book under management. With the exception of net equity, non-interest bearing items are excluded.

The resulting portfolio is tautologically an open portfolio/a sum of open portfolios managed as a single unit by the Treasury/ALM via an open portfolio of hedging instruments

9

OVERVIEW managing open portfolios

Mortgages

Loans

Bonds

CPs and CDs

Sight depos

Equity

USD

Mortgages

Loans

Bonds

CPs and CDs

Sight depos

Net Equity

Trading securities

Treasury ALM

banking book

under management &

hedging instruments

IRS

OIS

Swaption

Cap/Floor

Basis swap

Trading book

EUR

10

Bank’s treasury department gathers “pure” interest rate risk exposure stemming from the business units at the relevant benchmark rate (i.e. IRS or Euribor) via Transfer Price Process;

The treasury manages its net risk position by dealing with:

– the group’s investment bank and/or

– the internal trading desk and/or

– market counterparties

Investment

Bank/

Trading desk

Market

Business Unit

Business Unit

Business Unit Business

Unit Business Unit

Treasury ALM

OVERVIEW transfer pricing and internal deals

Floating rate loan

with cap @ 4%

Fixed Rate

Prepayable

Mortgage

Fixed Rate

Bond

(sub-libor:

bond's rate < IRS)

Subordinated

Bond

Basic example of IRR components’ segmentation

0.50%

3.00%3.00%

Euribor 3M

0.60%

Euribor 3M

1.00%

1.00%

3.00%

2.50%3.00%

Euribor 3M

0.60%

Euribor 3M

0.50%

Liquidity + Credit spread

Prep. Premium

Euribor 3M

Cap Premium

Euribor 1M

Base rate

1.00% 1.00%

-0.50%

3.00%

11

Euribor 3m

Liquidity + Credit Spread

Base rate: Fixed rate equivalent to

Euribor/Libor

Prepayment Premium: margin component

related to the cost of hedging the

prepayment risk

Cap Premium: margin component related

to the cost of hedging the IR cap

Assets Overall risk exposure Liabilities

All residual components: commercial margins, liquidity spread, etc.

Interest rate risk management

Optionality risk

Interest rate risk

OVERVIEW Segregation of risk components

12

Before the 2008 liquidity crisis, basis risk on the same currency was not an issue (i.e. Euribor 6m was quasi equivalent to Euribor 3m refinanced on forward rate for 3 months) and banks managed the refixing risk via OIS(2): It was sufficient to wait for the fixing day and enter into an OIS to hedge this risk perfectly.

As a consequence of the crisis, Euribor/Libor vs OIS rates started to diverge significantly

(2) Overnight Index Swap

OVERVIEW Refixing & basis risk

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

2006 2007 2008 2009 2010 2011

Euribor 6m OIS 6M

Both repricing and basis mismatch requires now different hedging mechanics.

The cost of the basis is also a component to be included in the “interest risk management” and transfer price process. See slide 11.

Overview

Models

Representing Hedging Activity

13

AGENDA IRRBB: Macro Hedging

Any IRR measure is based on the various assets' and liabilities' cash flows.

In some cases, these cash flows are not fully determined. In these cases, one has to use expected cash flows, i.e. a model.

The three most important areas where this is true are loans with prepayment options, sight deposits, and non-financial assets and liabilities.

MODELS

14

In many countries, debtors have a contractual or legal right to prepay all or a portion of their fixed-rate mortgage.

If the prepaid loan has carried a relatively high interest rate, the bank incurs an economic loss. In many cases, the customer does not have to pay a prepayment penalty that (fully) compensates the bank for this loss.

In risk management, this prepayment right is considered an option. It has to be taken into account as, on average, it will shorten the loans' cash flow profile – and therefore, by implication, change the bank's IRR.

Prepayment risk is necessarily modelled at an aggregate, i.e. portfolio, level. A "law of large numbers" effect usually reduces the uncertainty sorrounding the question, To what extent will any one customer actually exercise his option?

15

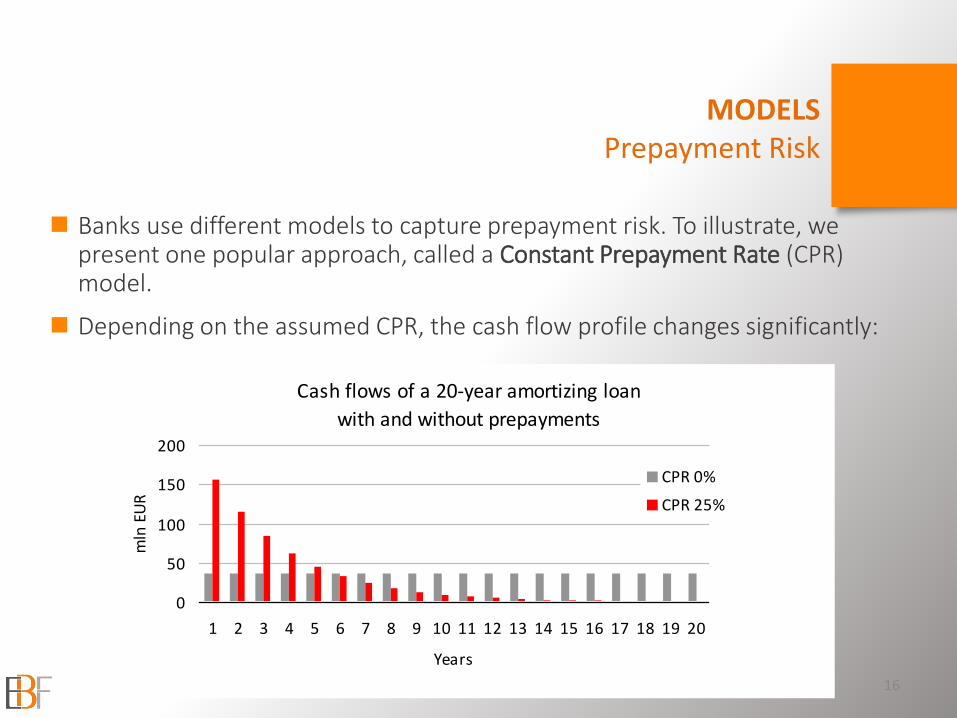

MODELS Prepayment Risk

16

Cash flows of a 20-year amortizing loan

with and without prepayments

0

50

100

150

200

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Years

mln

EU

R

CPR 0%

CPR 25%

Banks use different models to capture prepayment risk. To illustrate, we present one popular approach, called a Constant Prepayment Rate (CPR) model.

Depending on the assumed CPR, the cash flow profile changes significantly:

MODELS Prepayment Risk

17

Core CPR

Max CPR

MODELS Prepayment Risk

One important input when calibrating such a CPR model are historical data of actual prepayment rates:

EXPECTED

AMORTIZATION

0

10

20

30

40

50

60

70

80

90

100

apr-

11

apr-

13

apr-

15

apr-

17

apr-

19

apr-

21

apr-

23

apr-

25

apr-

27

apr-

29

apr-

31

Mln

CONTRACTUAL DEBT DEBT CPR 3% DEBT CPR 15%

18

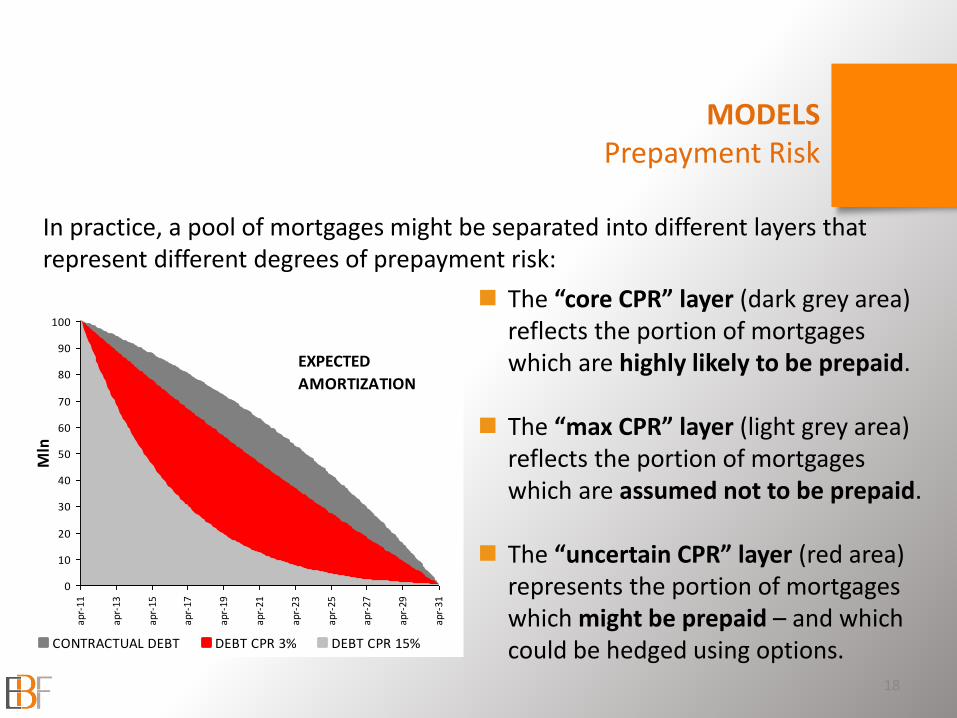

The “core CPR” layer (dark grey area) reflects the portion of mortgages which are highly likely to be prepaid.

The “max CPR” layer (light grey area) reflects the portion of mortgages which are assumed not to be prepaid.

The “uncertain CPR” layer (red area) represents the portion of mortgages which might be prepaid – and which could be hedged using options.

In practice, a pool of mortgages might be separated into different layers that represent different degrees of prepayment risk:

MODELS Prepayment Risk

19

From a contractual view point, sight deposits have an overnight maturity.

However, historical data show that, in aggregate, sight deposits are a relatively stable source of funding. Moreover, the average customer rate is rather sticky:

MODELS Sight Deposits

0

5

10

15

20

2005 2006 2007 2008 2009 2010

EUR

bn

0%

2%

4%

6%

8%

2005 2006 2007 2008 2009 2010

average customer rate1m Euribor10y average of 10y swap

20

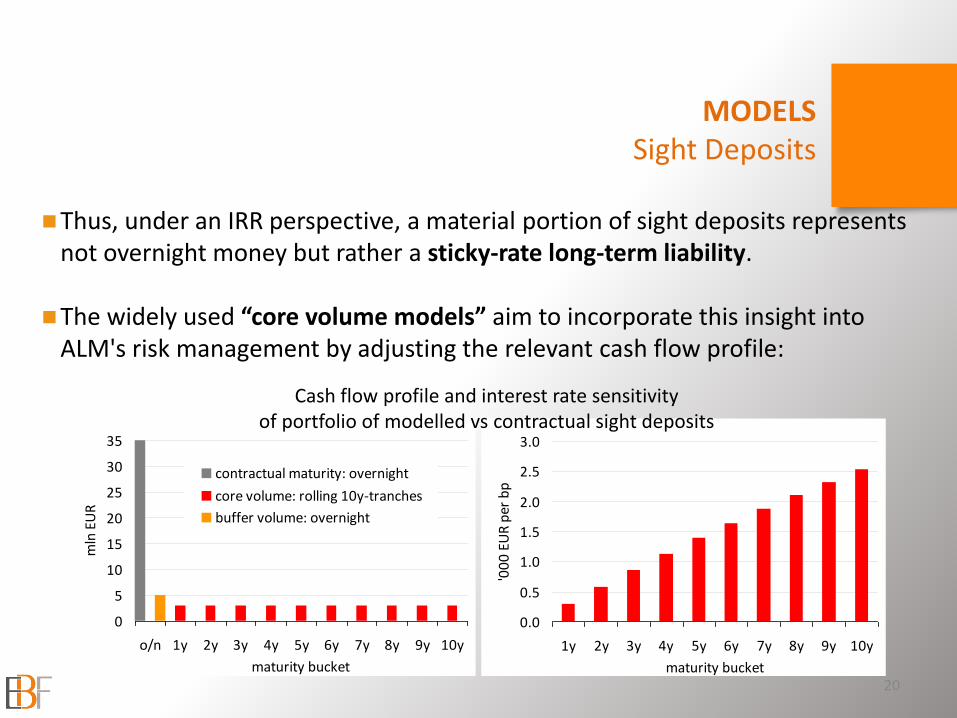

Thus, under an IRR perspective, a material portion of sight deposits represents not overnight money but rather a sticky-rate long-term liability.

The widely used “core volume models” aim to incorporate this insight into ALM's risk management by adjusting the relevant cash flow profile:

MODELS Sight Deposits

0

5

10

15

20

25

30

35

o/n 1y 2y 3y 4y 5y 6y 7y 8y 9y 10y

maturity bucket

mln

EU

R

contractual maturity: overnight

core volume: rolling 10y-tranches

buffer volume: overnight

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1y 2y 3y 4y 5y 6y 7y 8y 9y 10y

maturity bucket

'00

0 E

UR

per

bp

Cash flow profile and interest rate sensitivity of portfolio of modelled vs contractual sight deposits

21

The third area where modelling is used in IRR are non-financial assets and liabilities. They are often modelled as "net equity" (i.e. equity less assets such as property or equipment plus liabilities such as pension reserves).

MODELS Non-Financial Assets and Liabilities

In a recent survey by PwC, 58% of the banks said they incorporated a target duration for their net equity/assets into the IRR management. The majority of them used a duration of between 1 and 5 years.

Many banks use a so-called replication model for this purpose (i.e. they model a bottom layer of their equity as a number of staggered fixed-rate tranches which are rolled over at regular intervals).

financial

assets

financial

liabilities

non-financial

assets

non-financial

liabilities

equity

net equity/

net assets

Overview

Models

Representing Hedging Activity

22

AGENDA IRRBB: Macro Hedging

Let’s consider the following simplified Balance Sheet:

The Bank has an interest risk exposure of EUR 100 at 10 year.

The Treasurer/ALM reduces the risk by hedging EUR 80 via derivatives

23

Hedging IRR

Loan EUR 100mln Funding EUR 100mln

Fixed rate 5% Floating rate Eur1M

Maturity: 10Y (bullet) Maturity: 10Y (bullet)

Balance SheetAssets Liabilities

The Bank hedges EUR 80mln of the Loan through IRS A (Pay 5% Rec Eur1M) accounted as a FVH derivative. Let’s assume interest rates falling, B/S and P/L will be as follows:

Loan EUR 100mln Funding EUR 100mln

Fixed rate 5% Floating rate Eur1M

Maturity: 10Y (bullet) Maturity: 10Y (bullet)

IRS A (Not. EUR 80mln)

Pay 5% Rec Eur1M

Maturity: 10Y (bullet)

Balance SheetAssets Liabilities

24

1. Hedging IRR through FVH derivatives

Negative FV = -10

as interest rates

have decreased

ΔFV (Hedged portion) =

+10

as interest rates have

decreased

Income Statement

Loan EUR 100mln 5

Funding EUR 100mln -100 x Eur1M

IRS A fixed leg -4

IRS A floating leg 80 x Eur1M

Interst income/expense 1 - 20 x Eur1M

Hedged Loan EUR 80mln 10

IRS A -10

FV adjustments 0

Loan EUR 100mln Funding EUR 100mln

Fixed rate 5% Floating rate Eur1M

Maturity: 10Y (bullet) Maturity: 10Y (bullet)

IRS B (Not. EUR 80mln)

Pay 5% Rec Eur1M

Maturity: 10Y (bullet)

CFH Valutation Reserve

EUR -10mln

AssetsBalance Sheet

Liabilities

The Bank hedges EUR 80mln of the Funding through IRS B (Pay 5% Rec Eur1M) accounted as a CFH derivative. Let’s assume interest rates falling, B/S and P/L will be as follows:

25

2. Hedging IRR through CFH derivatives

Negative FV = -10

as interest rates

have decreased

Income Statement

Loan EUR 100mln 5

Funding EUR 100mln -100 x Eur1M

IRS B fixed leg -4

IRS B floating leg 80 x Eur1M

Interst income/expense 1 - 20 x Eur1M

The Bank hedges EUR 40mln of the Loan through IRS A (Pay 5% Rec Eur1M) accounted as a CFH derivative and EUR 40mln of the Funding through IRS B (Pay 5% Rec Eur1M). Let’s assume interest rates falling, B/S and P/L will be as follows:

Loan EUR 100mln Funding EUR 100mln

Fixed rate 5% Floating rate Eur1M

Maturity: 10Y (bullet) Maturity: 10Y (bullet)

IRS A (Not. EUR 40mln)

Pay 5% Rec Eur1M

Maturity: 10Y (bullet)

IRS B (Not. EUR 40mln)

Pay 5% Rec Eur1M

Maturity: 10Y (bullet)

CFH Valutation Reserve

EUR -5mln

AssetsBalance Sheet

Liabilities

26

3. Hedging IRR a mix of FVH and CFH derivatives

Negative FV = -5

as interest rates

have decreased

ΔFV (Hedged

portion) = +5

as interest rates

have decreased

Income Statement

Loan EUR 100mln 5

Funding EUR 100mln -100 x Eur1M

IRS A fixed leg -2

IRS A floating leg 40 x Eur1M

IRS B fixed leg -2

IRS B floating leg 40 x Eur1M

Interst income/expense 1 - 20 x Eur1M

Hedged Loan EUR 40mln 5

IRS A -5

FV adjustments 0

Loan EUR 100mln Funding EUR 100mln

Fixed rate 5% Floating rate Eur1M

Maturity: 10Y (bullet) Maturity: 10Y (bullet)

IRS A (Not. EUR 80mln)

Pay 5% Rec Eur1M

Maturity: 10Y (bullet)

AssetsBalance Sheet

Liabilities

The Bank hedges EUR 80mln of the Loan through IRS A (Pay 5% Rec Eur1M) under Portfolio Revaluation Approach. Let’s assume interest rates falling, B/S and P/L will be as follows:

27

4. Hedging risk through derivatives under PRA

Negative FV = -10

as interest rates

have decreased

ΔFV (whole revaluation) =

+12,5

as interest rates

have decreased

Income Statement

Loan EUR 100mln 5

Funding EUR 100mln -100 x Eur1M

IRS A fixed leg -4

IRS A floating leg 80 x Eur1M

Interst income/expense 1 - 20 x Eur1M

Loan EUR 100mln 12.5

Funding EUR 100mln 0

IRS A -10

FV adjustments 2.5

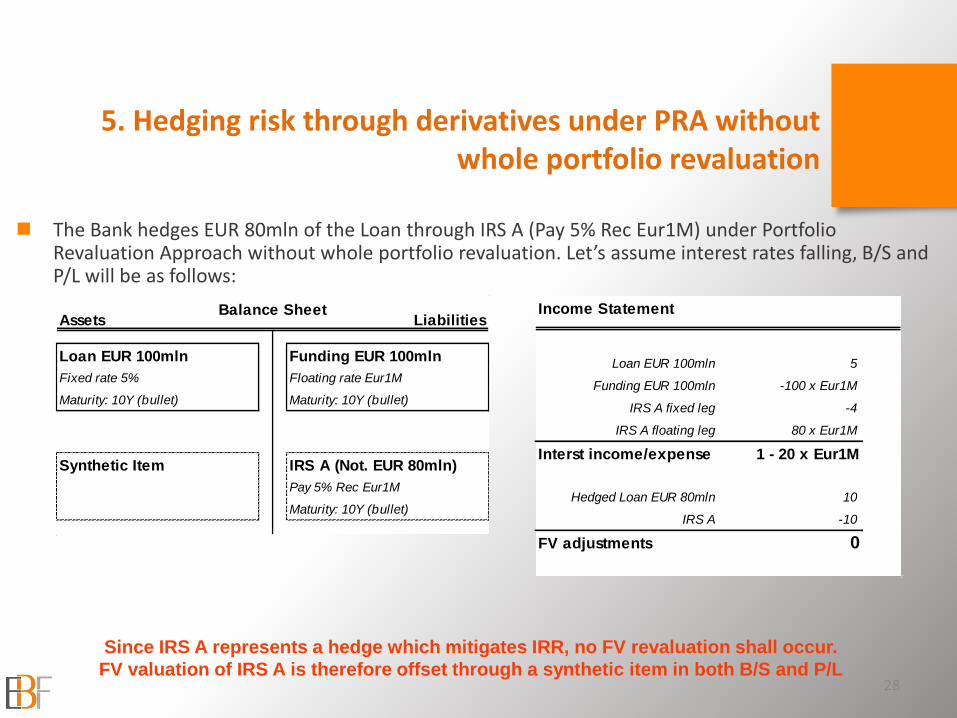

The Bank hedges EUR 80mln of the Loan through IRS A (Pay 5% Rec Eur1M) under Portfolio Revaluation Approach without whole portfolio revaluation. Let’s assume interest rates falling, B/S and P/L will be as follows:

Loan EUR 100mln Funding EUR 100mln

Fixed rate 5% Floating rate Eur1M

Maturity: 10Y (bullet) Maturity: 10Y (bullet)

Synthetic Item IRS A (Not. EUR 80mln)

Pay 5% Rec Eur1M

Maturity: 10Y (bullet)

AssetsBalance Sheet

Liabilities

28

5. Hedging risk through derivatives under PRA without whole portfolio revaluation

Since IRS A represents a hedge which mitigates IRR, no FV revaluation shall occur.

FV valuation of IRS A is therefore offset through a synthetic item in both B/S and P/L

Income Statement

Loan EUR 100mln 5

Funding EUR 100mln -100 x Eur1M

IRS A fixed leg -4

IRS A floating leg 80 x Eur1M

Interst income/expense 1 - 20 x Eur1M

Hedged Loan EUR 80mln 10

IRS A -10

FV adjustments 0