integration of renewables in a traded power market...integration of renewables in a traded power...

TRANSCRIPT

Norton Rose Fulbright LLP

Athens, 12 June 2019

Integration of renewables in a traded power market5th Energy Commodities ConferenceGerd Stuhlmacher

Integration of renewables in a traded power market

1. Introduction

2. Corporate renewable PPAs in the European power sector

3. Generators’ and buyers’ perspective: Price stability, financing and bankability

as major drivers

4. Managing the merchant tail and the use of derivatives

5. Tailwind or obstacles to expect from the regulatory environment: Lessons

learned from various jurisdictions

Agenda

2

Integration of renewables in a traded power market

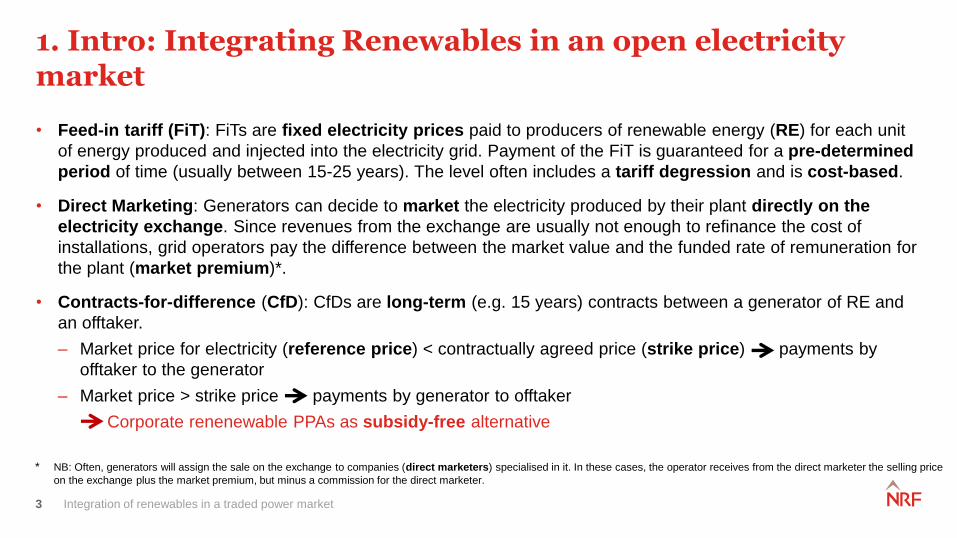

• Feed-in tariff (FiT): FiTs are fixed electricity prices paid to producers of renewable energy (RE) for each unit

of energy produced and injected into the electricity grid. Payment of the FiT is guaranteed for a pre-determined

period of time (usually between 15-25 years). The level often includes a tariff degression and is cost-based.

• Direct Marketing: Generators can decide to market the electricity produced by their plant directly on the

electricity exchange. Since revenues from the exchange are usually not enough to refinance the cost of

installations, grid operators pay the difference between the market value and the funded rate of remuneration for

the plant (market premium)*.

• Contracts-for-difference (CfD): CfDs are long-term (e.g. 15 years) contracts between a generator of RE and

an offtaker.

– Market price for electricity (reference price) < contractually agreed price (strike price) payments by

offtaker to the generator

– Market price > strike price payments by generator to offtaker

Corporate renenewable PPAs as subsidy-free alternative

1. Intro: Integrating Renewables in an open electricity market

* NB: Often, generators will assign the sale on the exchange to companies (direct marketers) specialised in it. In these cases, the operator receives from the direct marketer the selling price

on the exchange plus the market premium, but minus a commission for the direct marketer.

3

Integration of renewables in a traded power market

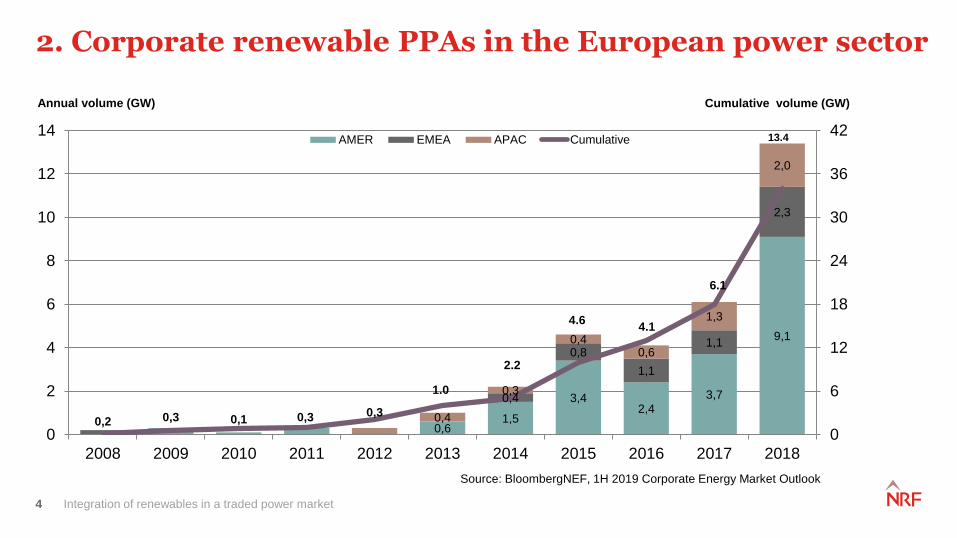

0,3 0,1 0,30,6

1,5

3,42,4

3,7

9,1

0,2

0,4

0,8

1,1

1,1

2,3

0,3 0,4

0,3

0,40,6

1,3

2,0

0

6

12

18

24

30

36

42

0

2

4

6

8

10

12

14

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

AMER EMEA APAC Cumulative

2.2

1.0

4.64.1

6.1

13.4

Source: BloombergNEF, 1H 2019 Corporate Energy Market Outlook

2. Corporate renewable PPAs in the European power sector

4

Annual volume (GW) Cumulative volume (GW)

Integration of renewables in a traded power market5

Mexico

• Arcelormittal & Walmart – EDF – Wind (160

MW)

• Coca Cola FEMSA & Heineken & OXXO –

Marena Renovoables (396 MW)

• GM & John Deere & Alsea – Enel Green

Power (129 MW)

• Industrias Penoles – EDP – Wind (200 MW)

Chile

Guanaco Compania Minera – Enel Green Power –PV & Wind (4 MW)

Brazil

• Nestlé – Engie & EDP & NC Energia – Hydro

(29 MW)

• Nestlé – Engie & EDP – Hydro & Biomass

(18 MW)

USA

• Amazon Web Services – EDP – Wind

(100 MW)

• Apple – First Solar – Solar (130 MW)

• Dow Chemical – NRG – Wind (150 MW)

• Google – EDF – Wind (225 MW)

• Google – Enel Green Power – Wind

(200 MW)

• Microsoft – EDF – Wind (225 MW)

• Unilever – NRG – Wind (150 MW)

• Walmart – Pattern Energy – Wind (116

MW)

UK

• BT – EDF – Wind

(72 MW)

• BT – Pennant Walters

–Wind (23 MW)

• Nationwide – BayWa –

Solar (45 MW)

• McDonalds – BayWa –

Solar (15 MW)

• HSBC – BSR – Solar

(61 MW)

Sweden

• Google – OX2 – Wind (72 MW)

• Norsk Hydro – Vestas/PKA/Vattenfall – Wind (211.8 MW)

Netherlands

• Google – Eneco –

Wind (62 MW)

• AkzoNobel – Eneco – Biomass

(50 MW)

Norway

• Alcoa – Eolus – Wind (330 MW)

• Alcoa – BlackRock – Wind (197

MW)

• Hydro Energi – Engie/Susi

Partners – Wind (208 MW)

Denmark

• Novo Nordisk/Novozymes –Vattenfall – Wind (120 MW)

Spain

Nike – Iberdrola –Wind (40 MW)

Data shows: Buyer – Developer – Energy Source (Power)

2. Corporate renewable PPAs in the European power sector

Integration of renewables in a traded power market

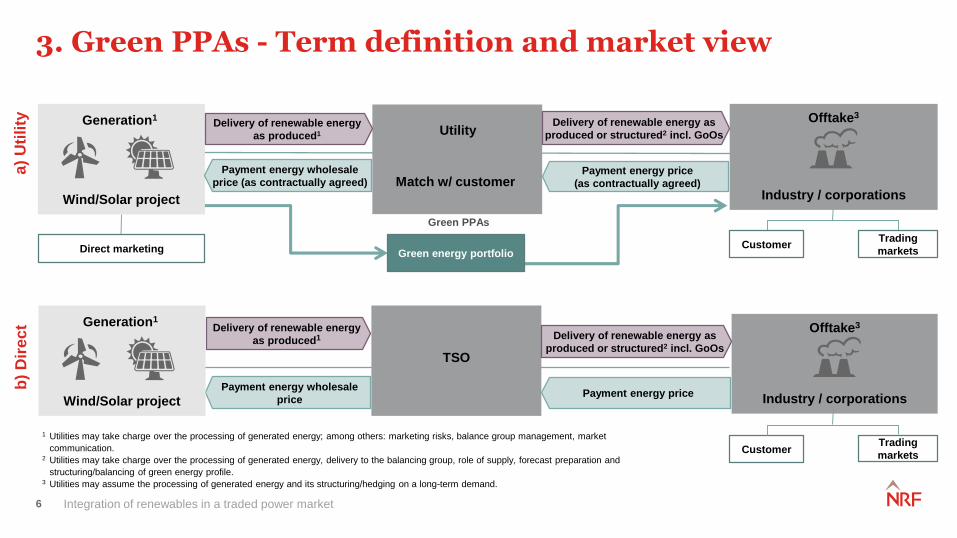

TSO

3. Green PPAs - Term definition and market view

Industry / corporations

Offtake3

Direct marketingTrading

marketsGreen energy portfolioCustomer

Match w/ customer

UtilityDelivery of renewable energy as

produced or structured2 incl. GoOs

Payment energy price

(as contractually agreed)

Green PPAs

Wind/Solar project

Generation1Delivery of renewable energy

as produced1

Payment energy wholesale

price (as contractually agreed)

a)

Uti

lity

b)

Dir

ec

t

6

Industry / corporations

Offtake3

Payment energy price

Delivery of renewable energy

as produced1

Payment energy wholesale

price

1 Utilities may take charge over the processing of generated energy; among others: marketing risks, balance group management, market

communication.2 Utilities may take charge over the processing of generated energy, delivery to the balancing group, role of supply, forecast preparation and

structuring/balancing of green energy profile. 3 Utilities may assume the processing of generated energy and its structuring/hedging on a long-term demand.

Delivery of renewable energy as

produced or structured2 incl. GoOs

Trading

marketsCustomer

Wind/Solar project

Generation1

Integration of renewables in a traded power market7

3. Rationales for entering into a corporate PPA

Developers’ view Buyers’ view

Risk Mitigation

• Can unlock a lower cost of capital through guaranteed offtake(s)

• Diversification of revenue stream away from traditional utility offtakers

• Development of an investment pipeline becomes less risky through

nurturing offtake relationships

• Diversifies the risk of payment default (multiple PPAs)

Bankability

• A stable and long-term income stream allows for easier bankability

with financial institutions

• Allows contracting with a high credit counterparty

Brand

• Effect on stocks

• Development of sustainable energy system

Business development

• Increases pool of potential offtakers and creates additional demand

• Can ease expansion into geographically new markets

• Reduces development cost by allowing standard terms and conditions

(partnerships)

Economics

• Allows corporate buyers to lock in a fixed electricity price or fixed cap,

with no upfront capital requirement

• Provides visibility over future electricity costs

• Hedges against fuel and electricity price volatility

• Reduces risks and related to potential future changes to carbon pricing

• Removes requirement for operational and management costs and

operational risks sit with the developer

Sustainability

Improve renewable footprint

Brand and Leadership

Increases recognition for renewable electricity achievements

Leverage

• Allows for the development of partnerships with a small number of

reliable and experienced counterparties

• In comparison to owning generation assets, PPAs allow a business to

remove focus from non-core areas

Integration of renewables in a traded power market

3. PPA risk allocation and pricing options

8

➔ Strategic question: How to avoid hardship or price revision?

• Electricity market price (time period, iliquidity)

• Profile risk

• Volume risk

• Credit risk

• Balancing risk

• Technical-based downtime

Allocated stakeholder (Generator, Offtaker, Bank)

➔ Offtaker

➔ Offtaker

➔ Generator/Offtaker

➔ Bank

➔ Offtaker

➔ Generator

Client/OfftakerGenerator

• Fix ➔ Fixed remuneration over agreed period

• Base ➔ Index on base price

• Spot ➔ Hourly spot price / month (variable)

• Floor ➔ Cap and Floor combined

• Index ➔ EPEX Spot, market value Wind/Solar

• Cap ➔ Index on (upper) cap

Bank

Integration of renewables in a traded power market

• Sculpted repayment profile with

burden of repayments reduced

during merchant period

• Mandatory prepayment of debt

from surplus cash flow to

restore cover ratios

• Cash sweep into secured

account if projected DSCR for

merchant period drops below

significantly higher threshold

(e.g. 1.4x) to bring DSCR back to

agreed threshold. Distributions

can be made periodically from

account provided projected

DSCR for merchant period is met

9

• Parent company guarantees /

LCs issued in favour of banks

to cover shortfall in debt

service or called on in

borrower insolvency

• Conditions for release

4. Financing approaches to merchant risk

Repayments and

prepaymentsLiquidity support

• Timing for updates of power

price projections

• Updates to reflect new

PPA/extension of PPA term

• Bank consent on case-by-case

basis for new PPAs vs. trading

strategy (as part of hedging

strategy)

• Trading strategy sets out

basis on which borrower can

enter into contracts for sale of

power (e.g. aim to sell

minimum capacity under

contract, credit criteria of

buyers, security over

contracts, form of direct

agreement etc.)

Market price forecasts / FM Trading strategy

Integration of renewables in a traded power market

5. RE investments in Greece

10

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

9.000

10.000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

RES

Inve

stm

ents

(m

illio

n €

)

Source: Hellenic Wind Energy Association (ELETAEN) – November 2018

Integration of renewables in a traded power market

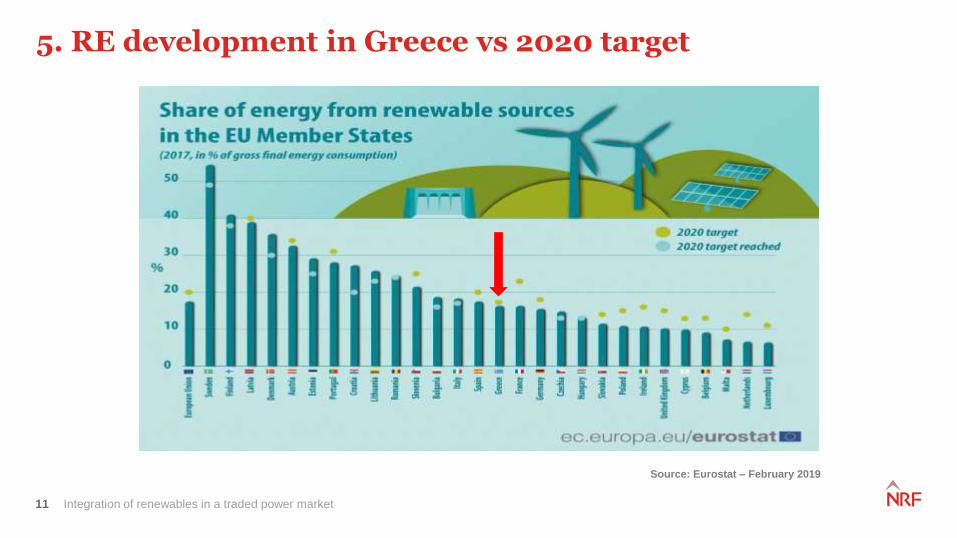

5. RE development in Greece vs 2020 target

Source: Eurostat – February 2019

11

Integration of renewables in a traded power market12

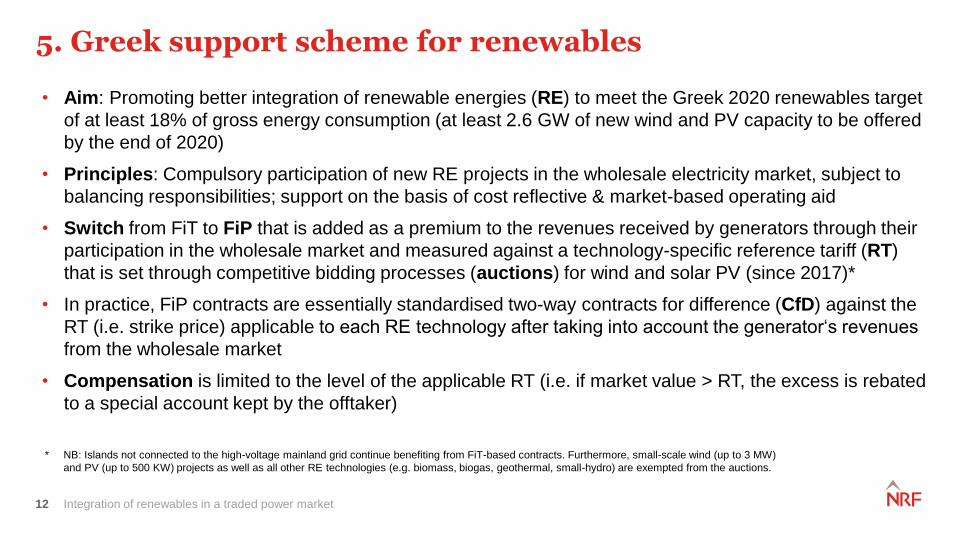

• Aim: Promoting better integration of renewable energies (RE) to meet the Greek 2020 renewables target

of at least 18% of gross energy consumption (at least 2.6 GW of new wind and PV capacity to be offered

by the end of 2020)

• Principles: Compulsory participation of new RE projects in the wholesale electricity market, subject to

balancing responsibilities; support on the basis of cost reflective & market-based operating aid

• Switch from FiT to FiP that is added as a premium to the revenues received by generators through their

participation in the wholesale market and measured against a technology-specific reference tariff (RT)

that is set through competitive bidding processes (auctions) for wind and solar PV (since 2017)*

• In practice, FiP contracts are essentially standardised two-way contracts for difference (CfD) against the

RT (i.e. strike price) applicable to each RE technology after taking into account the generator‘s revenues

from the wholesale market

• Compensation is limited to the level of the applicable RT (i.e. if market value > RT, the excess is rebated

to a special account kept by the offtaker)

5. Greek support scheme for renewables

* NB: Islands not connected to the high-voltage mainland grid continue benefiting from FiT-based contracts. Furthermore, small-scale wind (up to 3 MW)

and PV (up to 500 KW) projects as well as all other RE technologies (e.g. biomass, biogas, geothermal, small-hydro) are exempted from the auctions.

Integration of renewables in a traded power market13

• Advises on all aspects of Greek and European

energy law;

• Acts for clients in the power and gas sectors on

regulatory matters, M&A deals, project financing

and capital markets and privatisation transactions;

• Consistently listed as one of the leading energy

lawyers in Greece.

Partner | Head of Energy, Greece+30 210 94 75 415

Dimitris Assimakis

• Advises on all aspects of German and European

energy law;

• Specialized in compliance with regulatory

requirements and first-hand experience in price

adjustment disputes, restructurings and M&A

transactions in the energy sector;

• Since 2017 Partner at Norton Rose Fulbright,

before that (since 2008) Director of Legal and

Compliance at Uniper Global Commodities SE.

Partner | Head of Energy, Germany+49 89 212148 354

Gerd Stuhlmacher

Contact

Backup

Integration of renewables in a traded power market

1. Intro: What exactly are PPAs and are they a new thing?

15

What has changed to increase their attraction forcorporate consumers in Europe?

These PPAs allow corporates to reduce their carbonfootprint and manage volatile energy costs by maintaining afixed power price of energy over a period of years. Thislatter benefit is more eminent in times of volatile and risingprices.

For developers, it is a way to mitigate price risk in theabsence of a guaranteed feed in tariff or market premium.

The volume of these PPAs almost tripled in Europe in 2016compared to the year before. In the US, they accounted foralmost half of the installed renewable energy capacity in2016.

Clean

energy

buyer

Clean

energy

supplier

PPA

kWh

Integration of renewables in a traded power market16

Integration of renewables in a traded power market

Production Tax Credits and Investment Tax Credits

• Primary incentive available in the US

• PTC applies to wind, biomass and

geothermal

• ITC applies to solar, fuel cells and

cogeneration projects

• Strong incentive for corporate PPAs

Feed-in Tariffs

• Direct payments from the government to

supply RE

• Support technological development

• Fixed or variable FiTs

• Mean a lack of incentive for developers to

sign corporate PPAs

17

2. Which regulatory frameworks support corporate PPAs?

Renewable Portfolio Standards

• Quotas placed on utilities to source a

certain amount of electricity from RE

• Not enough certificates lead to purchase

from regulator or pay for RE generation

assets

• Lead to a higher uptake of corporate

PPAs

• E.g. Mexico and India

Contracts for Difference

• Grid-supplied RE

• Strike prices set by government,

regulators or auctions

• One-way or two-way

• No strong incentive to sign corporate

PPAs

Integration of renewables in a traded power market

Share of electricity generation from VRE – Top 10 countries

18

0

10

20

30

40

50

60

Denmark Uruguay Germany Ireland Portugal Spain United Kingdom Greece Honduras Nicaragua

Share of Electricity Generation from Variable Renewable Energy, Top 10 Countries, 2017

Solar PV

Wind power

Sh

are

of to

tal g

en

era

tion

(%

)

Law around the world

nortonrosefulbright.com

Norton Rose Fulbright US LLP, Norton Rose Fulbright LLP, Norton Rose Fulbright Australia, Norton Rose Fulbright Canada LLP and Norton Rose Fulbright South Africa Incare separate legal entities and all of them are members of Norton Rose Fulbright Verein, a Swiss verein. Norton Rose Fulbright Verein helps coordinate the activities of the

members but does not itself provide legal services to clients.

References to ‘Norton Rose Fulbright’, ‘the law firm’ and ‘legal practice’ are to one or more of the Norton Rose Fulbright members or to one of their respective affiliates (together ‘Norton Rose Fulbright entity/entities’). No individual who is a member, partner, shareholder, director, employee or consultant of, in or to any Norton Rose Fulbright entity (whether or not such individual is described as a ‘partner’) accepts or assumes responsibility, or has any liability, to any person in respect of this communication. Any

reference to a partner or director is to a member, employee or consultant with equivalent standing and qualifications of the relevant Norton Rose Fulbright entity.

The purpose of this communication is to provide general information of a legal nature. It does not contain a full analysis of the law nor does it constitute an opinion of any Norton Rose Fulbright entity on the points of law discussed. You must take specific legal advice on any particular matter which concerns you. If you require any advice or

further information, please speak to your usual contact at Norton Rose Fulbright.