info system audit

TRANSCRIPT

The Information Systems Audit The Information Systems Audit November 25, 2009

qeErnst & Young Ford Rhodes Sidat Hyder

Chartered AccountantsA member firm of Ernst & Young Global Limited

1

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

Sajid H. KhanSajid H. KhanExecutive DirectorExecutive DirectorTechnology and Security Risk ServicesTechnology and Security Risk ServicesErnst & Young Ford Rhodes Sidat HyderErnst & Young Ford Rhodes Sidat Hyder

qeErnst & Young Ford Rhodes Sidat Hyder

Chartered AccountantsA member firm of Ernst & Young Global Limited

2

Institute of Chartered Accountants of PakistanICAP Auditorium, Karachi

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

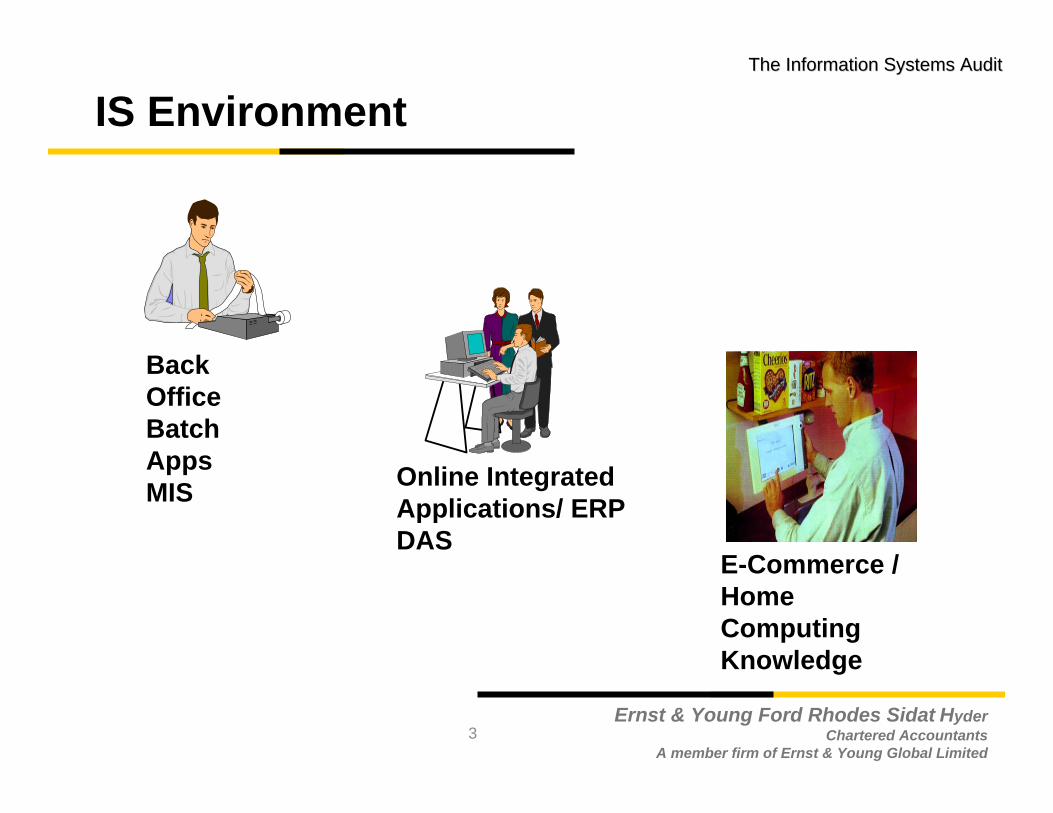

Back Office Batch AppsMIS Online Integrated

Applications/ ERPDAS

E-Commerce / Home ComputingKnowledge

3

IS Environment

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

The IT audit focuses on determining risks that are relevant

to information assets, and in assessing and evaluating

controls in order to reduce or mitigate these risks.

Any audit that encompasses review and evaluation (wholly or partly) of

automated information processing systems, related non-automated

processes and the interfaces between them.

Information Technology Audit

4

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

The IT audit's agenda may be summarized by the following questions:

• Integrity - Will the information provided by the system always be

accurate, reliable, and timely?

• Confidentiality - Will the information in the systems be disclosed only

to authorized users?

• Availability - Will the organization's computer systems be available for

the business at all times when required?

Purpose of IT Audit – Cont.

5

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

• Financial audits

• Operational audits• Integrated audits • IS audits• Specialized audits• Forensic audits

Classification of Audits

6

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

Specific goals of the audit

• Confidentiality

• Integrity

• Reliability

• Availability

• Compliance with legal / regulatory requirements

Audit Objectives

7

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

8

Types of IT Audits

• IT Policies & Procedures Review and Gap analysis

• Implementation Reviews (e.g. SAP / Oracle / JD Edwards)

• IT Security Reviews

• IT Forensic Investigations

• Application Integrity Reviews

• Business Continuity

• IT Disaster Recovery

These reviews may be performed in conjunction with a financial statement

audit, internal audit, or other form of attestation/special engagement.

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

9

Types of IT Audits

System Implementation Review - Example

• Business process/application controls

• Report Testing and documentation

• Testing (unit, volume, user)

• Data Cleansing and Conversion

• Segregation of Duties

• Roll out strategies

• IT General Controls

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

Various Standards and Frameworks

10

• COBIT

• COSO

• SOX

• ICFR

• BASEL II

• ITIL

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

• A framework with 34 high-level control objectives

– Planning and organization

– Acquisition and implementation

– Delivery and support

– Monitoring and evaluation

• Use of 36 major IT-related standards and regulations

CobIT

11

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

Framework for the ISACA IS Auditing Standards

• Standards

• Guidelines

• Procedures

ISACA - IS Auditing Standards Framework

12

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

Standards

• Must be followed by IS auditors

Guidelines

• Provide assistance on how to implement the standards

Procedures

• Provide examples for implementing the standards

ISACA - IS Auditing Standards Framework

13

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

Objectives of the ISACA IS Auditing Standards

• Inform management and other interested parties of the profession’s expectations concerning the work of audit practitioners

• Inform information system auditors of the minimum level of acceptable performance required to meet professional responsibilities set out in the ISACA Code of Professional Ethics

ISACA IS Auditing Standards Framework (cont.)

14

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

S1 Audit charter

S2 Independence

S3 Ethics and Standards

S4 Competence

S5 Planning

S6 Performance of audit work

ISACA IS Auditing Standards Framework (cont.)

15

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

ISACA IS Auditing Standards Framework (cont.)

16

S7 Reporting

S8 Follow-up activities

S9 Irregularities and illegal acts

S10 IT Governance

S11 Use of risk assessment in audit planning

S12 Audit Materiality

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

ISACA IS Auditing Standards Framework (cont.)

17

S13 Using the work of other Experts

S14 Audit Evidence

S15 IT Controls

S16 Electronic Commerce

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

Skills and Competence

An ideal background for an IS Auditor

»Business

»Auditing

»Information Technology

18

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

Skills and Competence (Contd.)

Specialized IS skills may be needed for an auditor to:

• Obtain understanding of the accounting and internal control systems affected by the IS environment.

• Determine the effect of IS environment on the assessment of risk at each level (e.g. process, account, transactions level)

• Design and perform appropriate tests of control and substantive procedures e.g. data analytics.

19

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

• Short and Long term planning

• Considerations

– New control issues– Changing technologies– Changing business processes– Enhanced evaluation techniques

IS Audit Resource Management & Planning

• Limited number of IS auditors• Maintenance of their technical competence• Assignment of audit staff

20

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

• An information technology audit, or information systems audit, is an examination of the controls within an Information technology (IT) infrastructure.

• It is a process of collecting and evaluating evidence of an organization's information systems, practices, and operations.

• The evaluation of obtained evidence determines if the information systems are safeguarding assets, maintaining data integrity, andoperating effectively to achieve the organization's goals or objectives.

Information Technology Audit - Process

21

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

A Typical IS Audit Cycle

• Planning

• Understand the Process(s)

• Walkthrough the Process/Controls.– Design of control

• Test the Controls– Operating Effectiveness

• Conclude and Report

22

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

Internal control objectives apply to all areas, whether manual or automated. Therefore, conceptually, control objectives in an IS environment remain unchanged from those of a manual environment.

IS Control Objectives

23

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

Key Controls

• A key control is a member of a set of controls that management identifies and relies upon in order to mitigate the risk of financial misstatement.

• In other words it is the main control that addresses the risk.

• Key Controls are usually identified by management.

24

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

Compensating Controls

• A compensating control is a control that would be in place to mitigate the risk of damage in the event a key control failed.

– Example: Key Control may be approval prior to access to systems but if it fails then compensating control might be the monthly monitoring of user access thus minimizing the risk to a period of one month.

25

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

Prevent / Detect Controls

Prevent Controls Detect Controls

Pre-Production Post Production

Production

Change Management Example

26

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

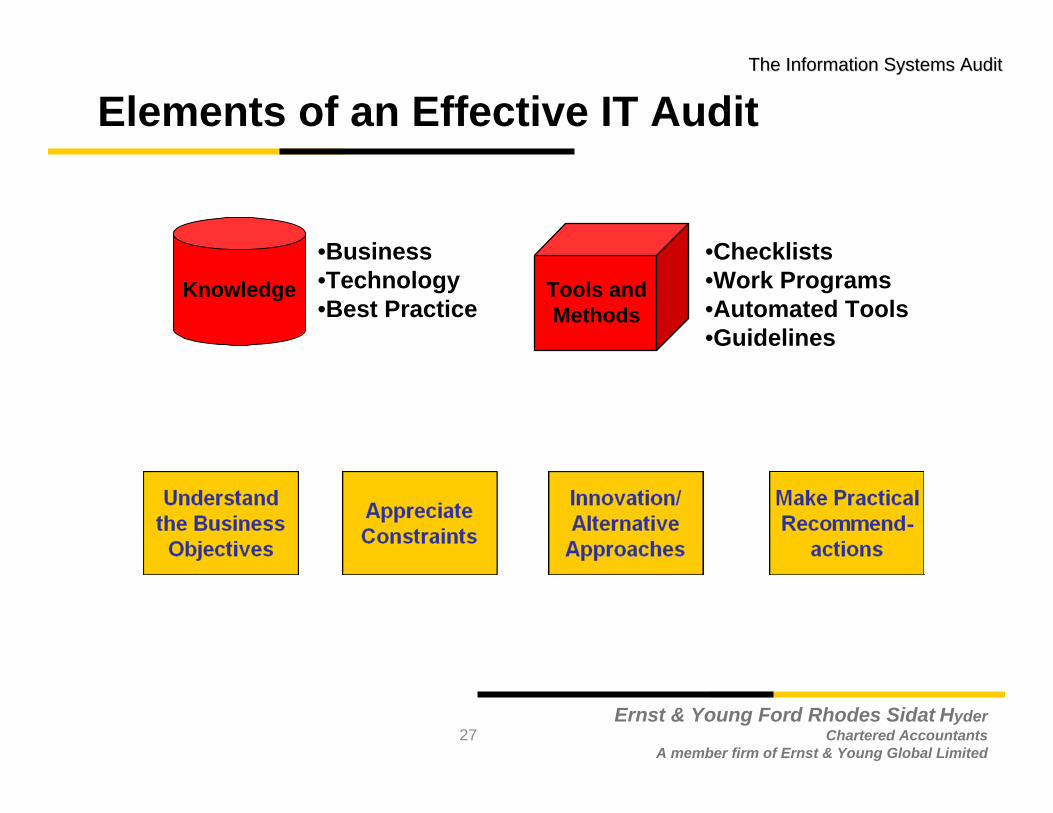

Elements of an Effective IT Audit

Knowledge

•Business•Technology•Best Practice

Tools andMethods

•Checklists•Work Programs•Automated Tools•Guidelines

27

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

Assessing Information Technology risks

• Risk assessments should identify, quantify and prioritize risks against criteria for risk acceptance and objectives relevant to the organization.

• Should be performed periodically to address changes in the environment, security requirements and when significant changes occur.

Risk Assessment

28

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

Treating security risks

• Each risk identified in a risk assessment needs to be treated.

• Controls should be selected to ensure that risks are reduced to an acceptable level

Risk Assessment Treatment

29

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

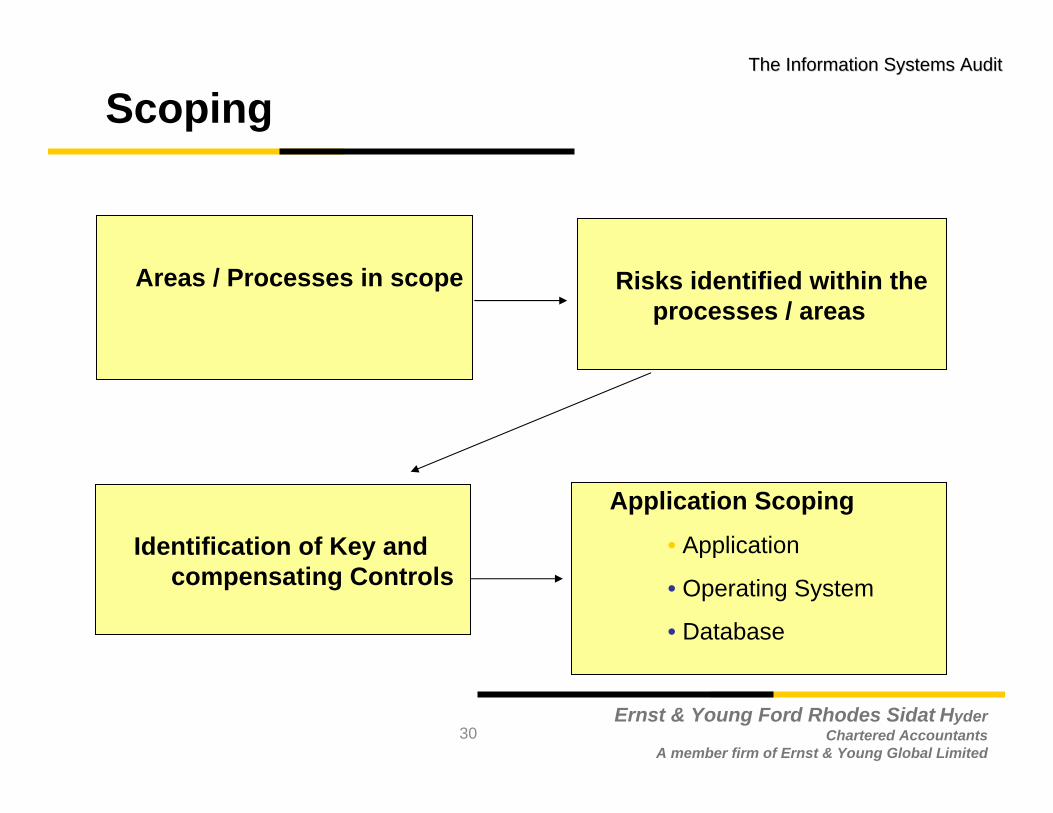

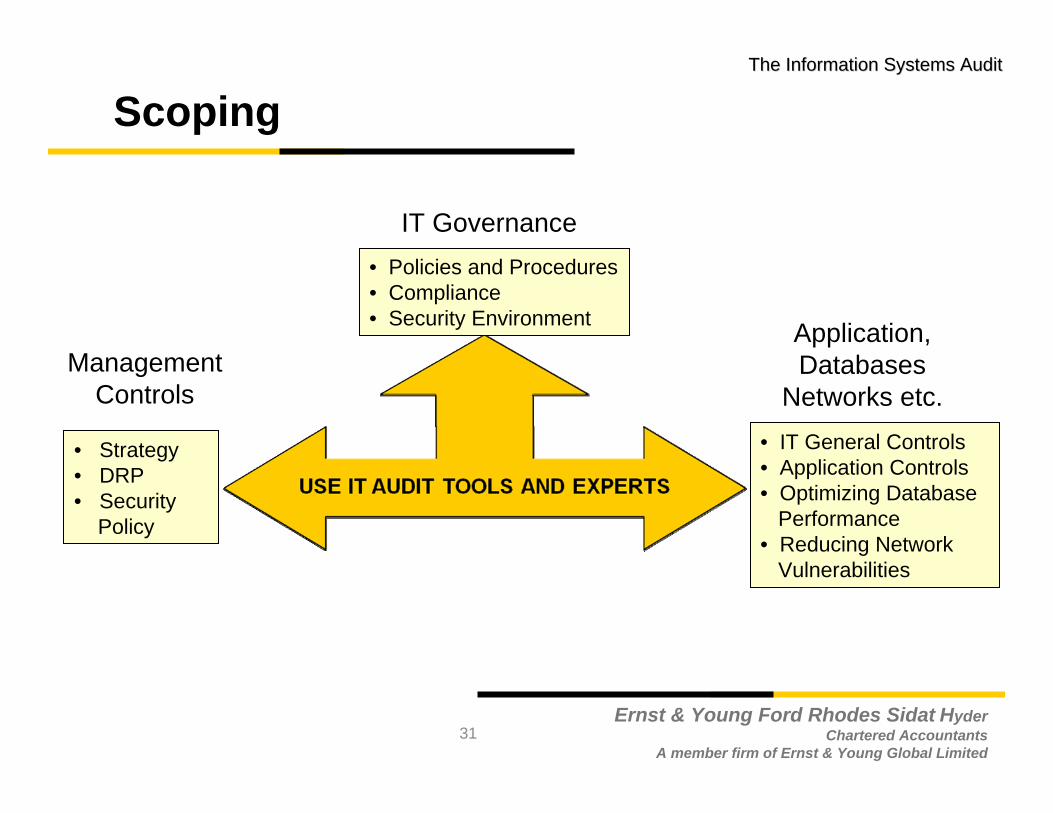

Scoping

Risks identified within the processes / areas

Identification of Key and compensating Controls

Application Scoping• Application

• Operating System

• Database

Areas / Processes in scope

30

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

Management Controls

• Strategy• DRP• Security

Policy

IT Governance• Policies and Procedures• Compliance• Security Environment Application,

DatabasesNetworks etc.

• IT General Controls • Application Controls• Optimizing Database

Performance• Reducing Network

Vulnerabilities

31

Scoping

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

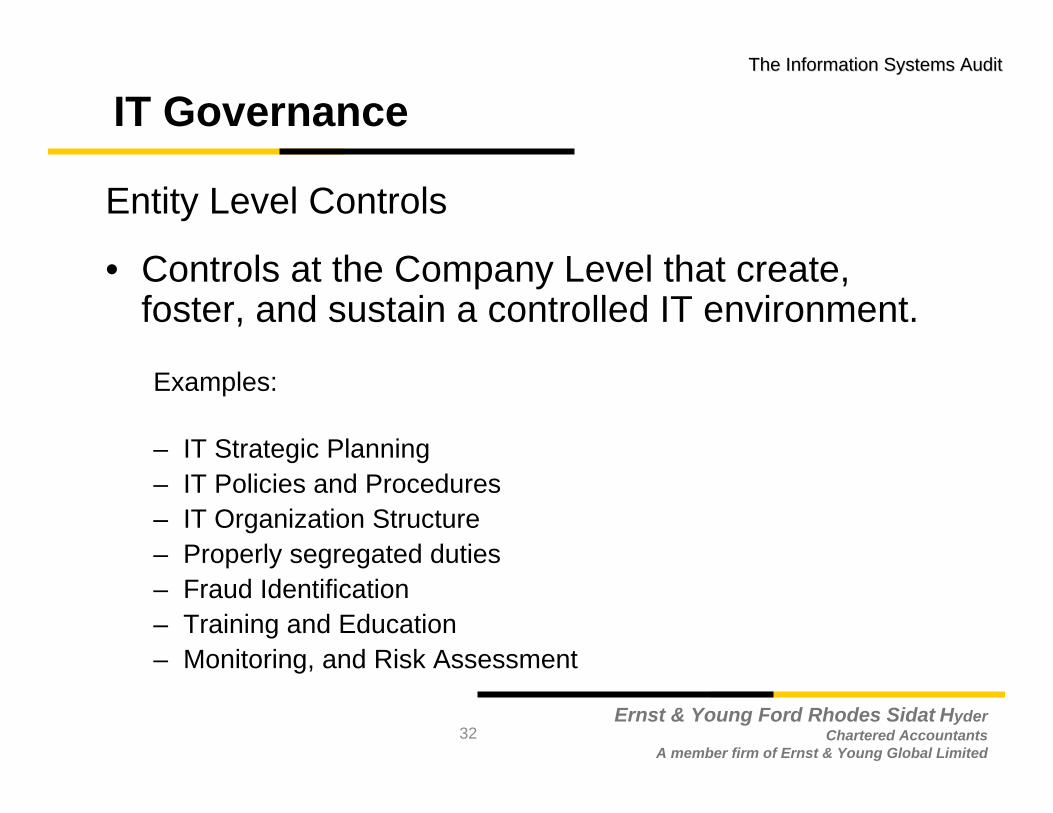

IT Governance

• Controls at the Company Level that create, foster, and sustain a controlled IT environment.

Examples:

– IT Strategic Planning – IT Policies and Procedures– IT Organization Structure– Properly segregated duties– Fraud Identification– Training and Education– Monitoring, and Risk Assessment

32

Entity Level Controls

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

IT General Controls: Layers of Controls

Business Processes

DataData

33

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

ITGC Domains

• ITGC Domains.

• Program Change Management

• Logical Access

• IT Operations (Backup & Recovery, Job scheduling, Problem and Incident Management)

34

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

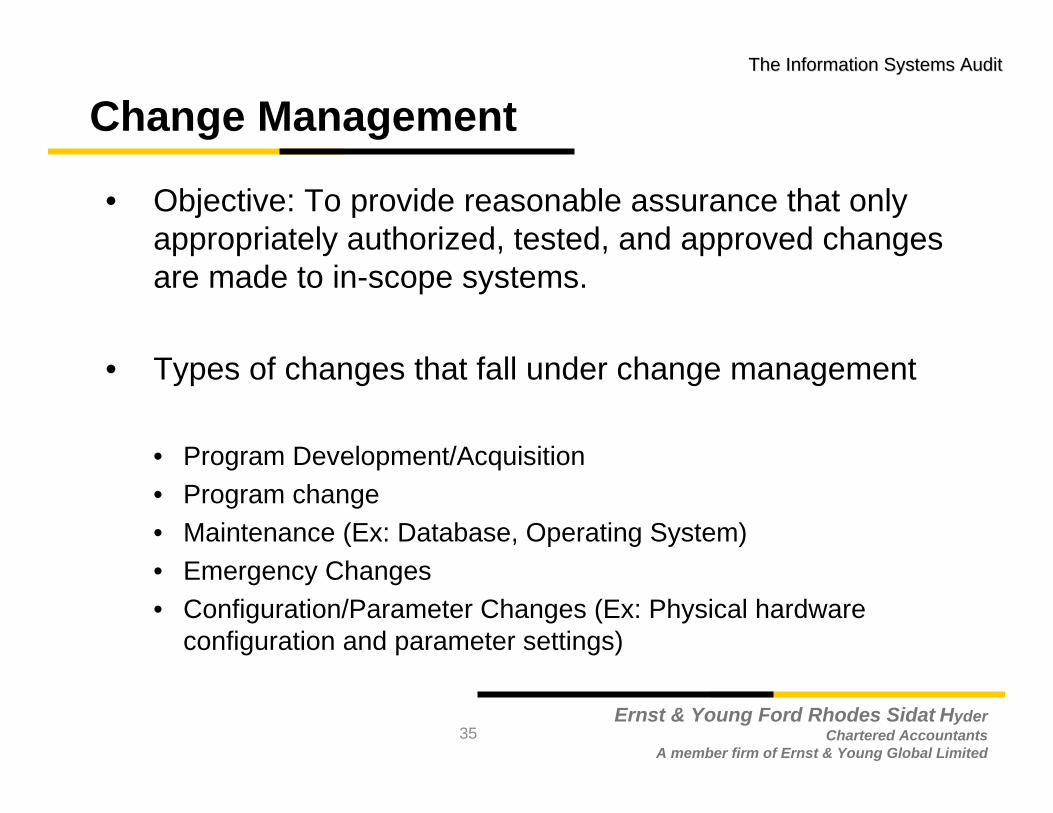

Change Management

• Objective: To provide reasonable assurance that only appropriately authorized, tested, and approved changes are made to in-scope systems.

• Types of changes that fall under change management

• Program Development/Acquisition • Program change • Maintenance (Ex: Database, Operating System)• Emergency Changes• Configuration/Parameter Changes (Ex: Physical hardware

configuration and parameter settings)

35

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

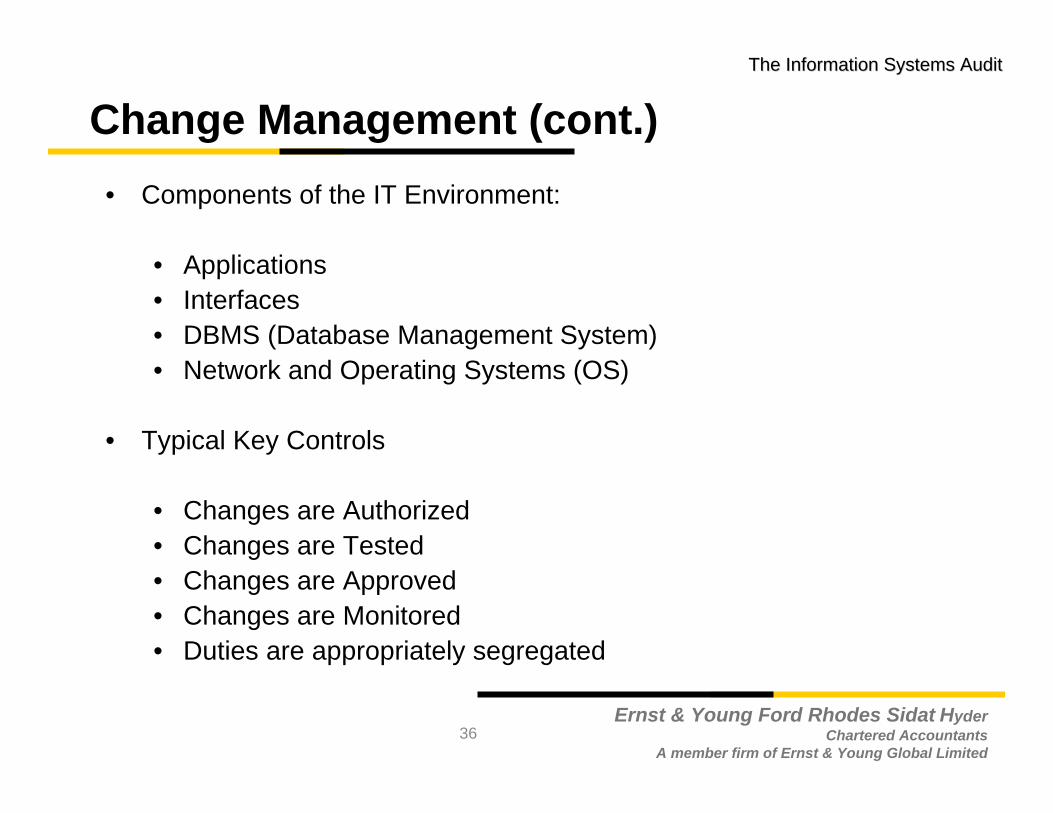

Change Management (cont.)• Components of the IT Environment:

• Applications • Interfaces• DBMS (Database Management System)• Network and Operating Systems (OS)

• Typical Key Controls

• Changes are Authorized• Changes are Tested• Changes are Approved • Changes are Monitored• Duties are appropriately segregated

36

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

Logical Access

• Objective: To determine that only authorized persons have access to data and applications (including programs, tables, and related resources) and that they can perform only specifically authorized functions.

• Levels of the logical access path

• Network / Operating System• Application• Database

37

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

Logical Access (cont.)

• General Systems Security Settings– Platform Specification

• Password Configuration

• Systems User Administration

– New User setup– Change/Transfer – Termination

38

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

Logical Access (cont.)

• Privileged Users

• User Access Reviews

• Segregation of Incompatible Duties (SOD)

• Request access• Approve access• Provision access

39

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

IT Operations

• To determine that the critical data is properly backed-up so that it can be accurately and completely recovered if there is a system outage or data integrity issue.

• To determine that only appropriate users have the ability to make changes to job scheduling.

• To determine that there is a problem and incident management process in place.

40

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

IT Operations (continued)

• Backup & Recovery

• Job Scheduling

• Problem & Incident Management

• Data Center Walkthrough

• Physical Access

41

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

Application Controls

• An application control is an automated control that is programmed within a system to perform the same function over and over again.

– Edit Checks– Validations– Calculations– Interfaces– Authorizations

42

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

Application Controls

Embedded Control – System is programmed to perform the control as a result of either custom coding or packaged delivery of that functionality.

Configurable Control – System has the capacity to perform the control depending on its setup, but may have been configured differently. Used especially in the context of ERP systems.

Example – A three way match within an application

43

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

Application Controls - Testing

• Embedded Control

– Re-performance via walkthrough– Inspection of authorization

• Configurable Control

– Inspect configuration– Re-performance via walkthrough– Inspection of authorization

Consider manual overrides and the underlying ITGCs.

44

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

IT Dependent Manual Controls

• An IT Dependent-Manual Control is any control activity where both an individual and an IT output are combined.

Example - System generated report review.

Consider the underlying ITGCs.

45

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

• Also called “Computer Assisted Audit Techniques” (CAATs).

• CAATs enable IS auditors to gather information independently.

• Multiple tools available to perform data analytics.

Data Analytics

46

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

• Functions supported by automated tools

– File access

– File reorganization

– Data selection

– Statistical functions

– Arithmetical functions

Data Analytics (cont.)

47

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

Considerations before utilizing CAATs

• Ease of use

• Training requirements

• Complexity of coding and maintenance

• Installation requirements

• Processing efficiencies

• Confidentiality of data being processed

Data Analytics (cont.)

48

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

• Completeness of the Population

• Time Period Coverage

• Key Control Tools – Scoping

• Additional Procedures – Controls Testing

• Impact on Application/ITDM testing if ITGC not effective

Challenges for IS Auditors

49

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

• Exit interview

– Correct facts

– Realistic recommendations

– Implementation dates for agreed recommendations

• Presentation techniques

– Executive summary and Visual presentation

Communicating Audit Results

50

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

Audit report structure and contents

• An introduction to the report (e.g. objectives, scope, procedures performed)

• High level Audit findings and recommendations

• The IS auditor’s overall conclusion and opinion

• The IS auditor’s reservations with respect to the audit

• Detailed audit findings and recommendations

Communicating Audit Results (cont.)

51

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

• Planning, audit scope and objectives

• Description on the scoped audit area

• Audit program(s)

• Audit steps performed and evidence gathered

• Other experts used

• Audit findings, conclusions and recommendations

Audit Documentation

52

Ernst & Young Ford Rhodes Sidat HyderChartered Accountants

A member firm of Ernst & Young Global Limited

The Information Systems AuditThe Information Systems Audit

Thank You

53