industry conference 2014 - bvrla conference 2014 ... driverless cars, consumer rights, ... •...

TRANSCRIPT

Promoting responsible transport www.bvrla.co.uk

Toby Poston 4 December

Industry Conference 2014 Sponsored by Supported by

Promoting responsible transport www.bvrla.co.uk

Industry Conference 2014 Breakout Session C Fleet Technology Update Facilitator: Toby Poston, Director of Communications and External Affairs, BVRLA Panellists: John Parkinson, Director Motoring, Freight and London, DfT Sarwant Singh, Senior Partner, Frost & Sullivan Andrew Miller, Chief Technical Officer, Thatcham Research

Promoting responsible transport www.bvrla.co.uk

Introduction – Toby Poston Intelligent Mobility

What is it? Key Benefits Policy priorities and next steps

Promoting responsible transport www.bvrla.co.uk

Toby Poston 4 December

Fleet Technology Update

Promoting responsible transport www.bvrla.co.uk

Intelligent Mobility

Congestion

Population Environment Economy

Promoting responsible transport www.bvrla.co.uk

What is Intelligent Mobility?

Promoting responsible transport www.bvrla.co.uk

Key Intelligent Mobility Benefits

Fleet Management – more real-time information on mileage, fuel consumption, vehicle & driver performance Safety – autonomous safety technology Mobility services – wider variety of more efficient mobility services and integration with other modes Big Data – sharing and analysing data to be improve safety, efficiency and develop new business models Productivity – Enhanced through improved connectivity

Promoting responsible transport www.bvrla.co.uk

Supporting fleet technology Regulatory environment – driverless cars, consumer rights, emissions standards Monitoring the motoring agencies – online services, data feeds Promoting fair competition – fighting monopolies, ensuring access to data Positioning the industry – mobility services, intelligent mobility Advice and guidance – research, training and events

Promoting responsible transport www.bvrla.co.uk

Policy priorities Access and use of data

Support for car clubs/car sharing and mobility services Obtaining joined up government support Regulatory environment for connected and driverless vehicles

Promoting responsible transport www.bvrla.co.uk

Access to data Interoperable Real-time Open access Secure

Promoting responsible transport www.bvrla.co.uk

Use of data

UK - Data Protection Act UK - Information Commissioner US - Privacy Principles for vehicles (www.automotiveprivacy.com)

Promoting responsible transport www.bvrla.co.uk

Car clubs and mobility services London – Car Club Coalition Urban Mobility event – Q1 2015 BIS – Sharing Economy Review BVRLA research

Promoting responsible transport www.bvrla.co.uk

Government and regulation OLEV for the Intelligent Mobility sector Support autonomous vehicles Support Information Commissioner

Promoting responsible transport www.bvrla.co.uk

Where next?

Promoting responsible transport www.bvrla.co.uk

Connected Corridors • High-speed, high-bandwidth ‘wireless corridor’

for connected vehicles.

• To test systems for real-time traffic and road information, lane management, platooning, etc.

• Looking to demonstrate on a trial basis using an inter-urban stretch of motorway – probably the M6.

• Government funded.

Promoting responsible transport www.bvrla.co.uk

Pantograph Trucks

Promoting responsible transport www.bvrla.co.uk

Do you have any questions?

Toby Poston Director of Communications and External Relations 01494 545700 [email protected]

Thank you for listening.

Promoting responsible transport www.bvrla.co.uk

Andrew Miller Thatcham Research

Industry Conference 2014 Break-out Session C

Fleet Technology Update

BVRLA Industry Conference, Thursday 4 December 2014 Heritage Motor Centre, Gaydon Andrew Miller Chief Technical Officer, Thatcham Research

Fleet Technology Update - Big Data, Autonomous Vehicles, Connected cars

Thatcham: the UK motor insurers automotive research centre

• Not-for-profit research company established 1969

• Owned and funded by the majority of UK Motor Insurers

• Backed by the Association of British Insurers and Lloyds Market Association

• Experts in vehicle safety, security and repair,

Complexity 1. Body materials and construction

techniques. 2. Powertrain complexity. 3. Vehicle electronic system

complexity, including ‘drive by wire’ and autonomous capabilities.

4. ‘Cosmetic’ componentry which may become more feature rich.

Impact Potentially increased restrictions on access to repair data, complex components, repair process equipment and diagnostic systems

Autonomy Vehicle design is on a path to complete autonomy. • Stage 1: Collision avoidance inc AEB • Stage 2: Partially autonomous: ACC

and ‘traffic jam assist’ • Stage 3: High and then Fully

autonomous, Best guess for first cars of these type is 2020-30.

Impact 1. Reduction in repair and PI claims

frequency. 2. Potential for increased risk due to

cybercrime or incorrect repair 3. Potential increase in repair costs for

these systems 4. Potential long term change to

insurance business model

Connectivity Connection between vehicles, their owners, other vehicles, the road infrastructure, and personal and corporate third parties. For accident monitoring and communication: • Emergency call system (eCall), • European Commission considering

accident Event Data Recorder based on the US model.

Impact New claims management opportunities through higher quality claims data, increasing operational efficiency, reducing leakage and increasing customer satisfaction. It is also expected that it will reduce accident frequency, although this is yet to be proven.

Future Vehicle Trends

Data –Thatcham Research ‘Guideline Technical Requirements’

Device Type

Aftermarket

Mobile Phone OEM

Data transfer

Telematics

Physical download

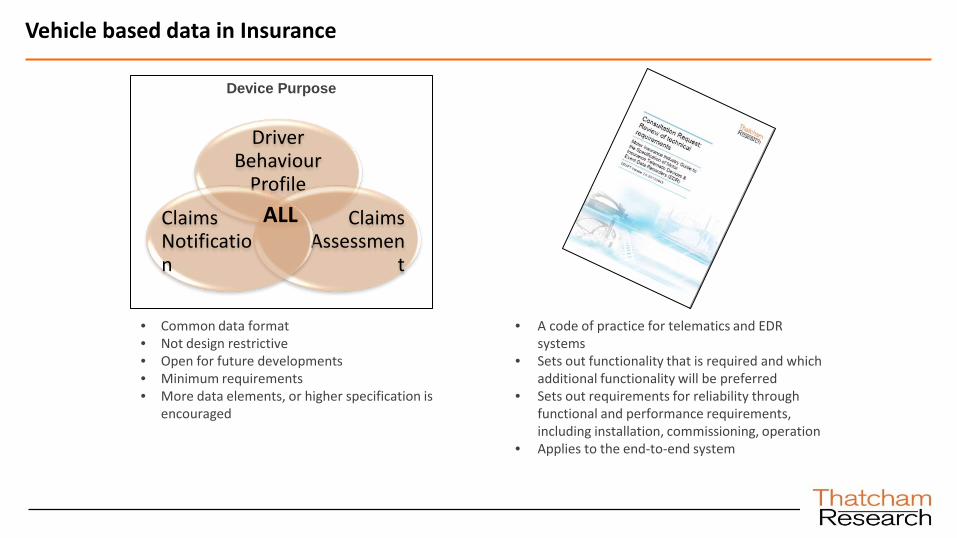

Vehicle based data in Insurance

Device Purpose

Driver Behaviour

Profile

Claims Assessmen

t

Claims Notification

ALL

• Common data format • Not design restrictive • Open for future developments • Minimum requirements • More data elements, or higher specification is

encouraged

• A code of practice for telematics and EDR systems

• Sets out functionality that is required and which additional functionality will be preferred

• Sets out requirements for reliability through functional and performance requirements, including installation, commissioning, operation

• Applies to the end-to-end system

Connected car and electronic system compromise

"Jailbreaking“ (Hacking)

Cracking software codes

UK Theft trends

Autonomous cars - Science Fiction?

Autonomous cars - Science Fact?

• Google are a new powerful player • A mapping and data company with aspirations to develop their data footprint into

mobility • Announced manufacturing in May 2014

The technical transition and where we are now

AEB Adaptive Cruise control

Parking and Lane Keep Assistance

xx

Level of Autonomy

Partial Autonomy

Full Autonomy

High Autonomy

The driver is completely in control but there are some

automated systems

Cruise control ABS ESC

Assisted Driving

Driver control

The steering and/or braking and acceleration are

automated but the driver controls other functions

Cruise control ABS ESC

The steering, braking and acceleration are automated and require no intervention

from the driver.

The vehicle can complete sections of a journey

autonomously, the driver is given and takes control

The vehicle completes the journey with no human

intervention

AEB Adaptive Cruise control

Parking and Lane Keep Assistance

Cruise control ABS ESC

AEB Adaptive Cruise control

Parking and Lane Keep Assistance

Adaptive Cruise Control with lane keeping

Traffic Jam Assistance

Cruise control ABS ESC

AEB Adaptive Cruise control

Parking and Lane Keep Assistance

Adaptive Cruise control with lane keeping

Traffic Jam Assistance

Road following Junction decisioning

Hazard detection and evasive decisioning

Mapping of other road users, intention prediction monitoring and decisioning

Ethical decisioning Etc.

Cruise control ABS ESC

Adaptive Cruise control with lane keeping

Traffic Jam Assistance

Road following Junction decisioning

Hazard detection and evasive decisioning

Mapping of other road users, intention prediction monitoring and decisioning

Ethical decisioning Etc.

Step Change

Where we are now

Autonomous Emergency Braking (AEB)

• Thatcham promotional campaign • Insurance premium discounts of 10% • In Euro NCAP ‘5 star ratings’ from 2014

AEB for pedestrians

• In Euro NCAP ‘5 star ratings’ from 2016

Junction crash detection

• Additional functionality for Low Speed AEB • A high priority for future Euro NCAP Strategy • High severity and high cost crashes

• Will also work with motorcycles – this scenario is a major cause of fatal and serious injuries for riders and car occupants

• KPMG LLP and the Center for Automotive Research (CAR) forecast improvements in productivity and energy efficiency.

• PricewaterhouseCoopers forecasts a reduction of traffic accidents by a factor of 10 and estimates that the US vehicle fleet could reduce from 245M to 2.4M.

• Increased road capacity and reduced traffic congestion due to reduced need for safety gaps and the ability to

better manage traffic flow.

• Potentially higher speed limit.

• Removal of all constraints on the driver’s ability or state – a fully autonomous/driverless car could have passengers which are blind, distracted, intoxicated, under age, over age, or otherwise impaired.

• Elimination of redundant passengers.

• Reduction in the need for traffic police.

• Possible eventual reduction of physical road signage.

• Relief of vehicle occupants from driving and navigation tasks. • Improved parking capacity - cars could drop off passengers, park far away where space is not scarce, and return

as needed to pick up passengers.

• It likely that intrinsically safe vehicles will have less collisions, and thus the type and scope of vehicle insurance could change.

Benefits?

Blind drivers?

Disadvantages?

Ethical machines?

• Moral/ethical choices: where an autonomous car's intelligence software is forced to choose between multiple courses of action, all of which cause harm.

• Overall intelligence software or vehicle sensor/system reliability.

• Cyber Security: a car's computer could potentially be

compromised, as could a communication system between cars.

• Drivers being inexperienced if situations arose requiring manual driving.

• Terrorism/Criminality: Driverless cars could potentially used by terrorists or other criminals i.e. they could be loaded

Predictions

Volvo XC90 ‘Adaptive Cruise

Control with Steer Assist

• Major automobile manufacturers and technology companies have made numerous predictions for the development of autonomous car technology in the near future.

• The new Volvo’s XC90 will feature ‘Adaptive Cruise Control with steer assist’ which will automatically follow the vehicle ahead in queues.

• By Mid-2010's, Toyota plans to sell vehicles with ‘Automated Highway Driving Assist with Lane Trace Control and Cooperative-adaptive Cruise Control’.

• ‘Mobileye’ expects to release fully autonomous car technology by 2016. Tesla has just launched its "autopilot" feature (Tesla has partnered with Mobileye).

When

• AEB • Adaptive

Cruise control • Parking and

Lane Keep Assistance

• Cruise control • ABS • ESC

• Adaptive Cruise Control with lane keeping

• Traffic Jam Assistance

• Road following • Junction

decisioning • Hazard detection

and evasive decisioning

• V2V, V2I

1. Driver Control

2. Assisted Driving

3. Partial Autonomy

4. High Autonomy 5. Full Autonomy

• Combination of all functions + Artificial intelligence and multiple redundancies – No driver monitoring

0%

20%

40%

60%

80%

100%

2005 2010 2015 2020 2025 2030 2035 2040 2045

New Car Sales %: Assisted

Driving

Fleet %: Assisted Driving

0%

20%

40%

60%

80%

100%

2005 2010 2015 2020 2025 2030 2035 2040 2045

New Car Sales %: Partial

Autonomy

Fleet %: Partial Autonomy

0%

20%

40%

60%

80%

100%

2005 2010 2015 2020 2025 2030 2035 2040 2045

Fleet %: High Autonomy

New Car Sales %: High

Autonomy

0%

20%

40%

60%

80%

100%

2005 2010 2015 2020 2025 2030 2035 2040 2045

Fleet %: High Autonomy

New Car Sales %: High

Autonomy

0%

20%

40%

60%

80%

100%

2005 2010 2015 2020 2025 2030 2035 2040 2045

2018: Volvo and Mercedes road

following autonomy

Google autonomous car

Adapted from Autonomous Road Vehicles – POSTnote 443, September 2013, Dr. Chandrika Nath, Parliamentary Office of Science and Technology, Parliamentary Copyright 2013

A fully autonomous

‘driverless’ fleet By 2040?

BVRLA Industry Conference, Thursday 4 December 2014 Heritage Motor Centre, Gaydon Andrew Miller Chief Technical Officer, Thatcham Research

Fleet Technology Update - Big Data, Autonomous Vehicles, Connected cars

Promoting responsible transport www.bvrla.co.uk

Open to the floor… • What do you feel is the most pressing issue for the

DfT in this area?

Promoting responsible transport www.bvrla.co.uk

Sarwant Singh Frost & Sullivan

Industry Conference 2014 Break-out Session C

Fleet Technology Update

Impact of Big Data on Automotive Industry Explicit Annual Savings of About $800 per vehicle

Sarwant Singh Senior Partner & Global Practice Director

Automotive & Transportation

© 2014 Frost & Sullivan. All rights reserved. This document contains highly confidential information and is the sole property of Frost & Sullivan. No part of it may be circulated, quoted, copied or otherwise reproduced without the written approval of Frost & Sullivan.

40

Agenda

No. Topic

1 Introduction to Connected Living and Big Data

2 Why Big Data in the Car Industry – The Business Case

3 Key Societal, Technology and other Challenges for Big Data Implementation

4 Big Data Impact on the Automotive Environment

5 Case studies of Big Data Implementation

41

ConnectedWorkConnectedHomeConnectedCity

Internet Economy* $14.7 Trillion

Global GDP $107.2 Trillion

Connected Living Market $731.70 billion

Connected Work $228 billion

Connected Home $111 billion

Connected City $392 billion

2012 2020 2012 2020 2012 2020

$111 $30

$392

$122 $75 $228

*Average based on data reported by OECD economies and BRIC nations as a percentage of GDP.

31%

54% 15%

Connected Living A Key Generator of Big Data Connected Living market expected to reach $731.70 billion by 2020 as the importance of internet and digital solutions grows in the overall economy, and our personal lives

Connected Living Market: Market Size, Global, 2020

Internet Economy as % Global GDP, 2020 % Breakdown of Connected Living Segments, 2020

Source: OECD and Frost & Sullivan analysis.

42 M94C-MT

Source: Frost & Sullivan analysis.

Connected Living: Value Chain of Smart Solutions Will Bring New Players Into the Market Who Will Integrate, Assimilate or Aggregate Bundled Services And Data Analytics Will be a Key Service Offering

Modules and component providers

Device Vendors

Network Providers

Platform providers

Systems Integrators

Three Types of Connected Living Service Providers (Bundled Solutions)

1 2 3 4 5

SIM cards, sensors, Transponders

E.g. Sendum,

Gemalto

Mobile device, appliance, utility, cars

E.g. Samsung, Apple

Applications, software, enabling technologies

E.g. SAP, Oracle

Interfaces, back-end, value-added services

E.g. IBM, Accenture

Integrators:

Platform Providers and Systems Integrators

Assimilators:

Device Vendors and Utilities

Aggregators:

Network Providers

Network, M2M, Wireless, Analytics

E.g. Telefonica,

AT&T, Cisco

End User

Connected Living, Value Chain Participants and Process, Global, 2013

43

Source: Frost & Sullivan analysis

Global Data Traffic in Zettabytes, 2010-2025 Global Big Data Market in $ Billion, 2010-2025

2010 2020

2025

2015

$3.56

$87.85

$122.6

$47.37

2010 2020 2015

1.2

34.1

100.2

7.6

Global Data Traffic and Big Data Market Revenue Potential, Global, 2010 - 2025

2025 2025

Global Data Traffic and Big Data Market Revenue Potential Digital content is doubling every 18 months

44

Note: All figures are rounded. The base year is 2013. Source: Frost & Sullivan analysis.

Connected and Non-Connected Cars, North America and Europe, 2013 and 2020

As of 2013 Frost & Sullivan expects less than 2 percent of vehicle data to be useful for monetization Meaningful data sets is expected to grow from 10MB to 5GB in an average connected car by 2017/2018

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

2014 2015 2016 2017 2018 2019

Uni

ts (M

illio

n)

Connected Car Non Connected Cars2020

~34.0–34.5 million

2013

~8.5–9.0 million

Connected Cars Accelerating Big Data Opportunities ~35 Million vehicles in 2020 will make available relevant data sets for OEM’s to assimilate and convert them into actionable insights

45

Digital Leads

Warranty Costs Reduction, Predictive Maintenance

User & Dealer Satisfaction

Internet Aggregators

Advanced Mobility services, Dynamic Navigation and Parking

Product Performance Analysis, Production and Supply Chain

Images and logos are only for representation Source: Frost & Sullivan analysis.

Why Big Data in the Car Industry – The Business Case Car makers recognize the revenue potential from big data - customer centric approach is important to convince the customer to invest and share data with the OEMs.

46

Big Data Case Study - TRUECar Comes to Europe Negotiation free car buying process based on real time information and complete pricing transparency (influenced 3.4% of all new car sales in US last year) Step 1: Visit

www.truecar.com or mobile app = access to aggregated transaction information & market data.

Step 2: Registration to see upfront pricing = actionable and guaranteed price for the selected vehicle.

Step 3: Receipt of guaranteed savings certificate = visit to certified dealer, purchase of desired vehicle at set price.

47

Key Societal, Technology and other Challenges for Big Data Implementation Harnessing relevant and prioritized vehicle and user data are key answers to industry challenges

Understanding the customer from the web (car vs. lifestyle preferences) – Customer Analytics and CRM The need for better data quality – High data transfer cost per vehicle for downloading information

Whose benefitting from the ecosystem – Monetizing data and sharing value amongst ecosystem partners

Big Data: Relevant & prioritized information – What data you process and what data you don’t

Shortage of skill set for data analytics and data governance – Data Scientists

Data privacy issues on the type of data being shared – Government limitations and driver concerns

Images and logos are only for representation Source: Frost & Sullivan analysis.

48

• Savings achieved from

• Reduction in insurance premiums after UBI

• Savings achieved from

• High quality of LBS services

• Savings achieved from

• Reduction in infrastructure development cost

• smart parking and other public use cases

• Reduction in congestion using big data

• Savings achieved from

• Reduction in warranty costs

• Reduction in product development costs

• Reduction in recall related expenses

• Increased aftersales revenues

OEM Infrastructu-re / Society

Vehicle Users

Service Provide

rs

Big Data Explicit Savings from a Vehicle Frost & Sullivan expects an annual savings of ~$700—800 per from leveraging Big Data

49

OEM

Product Planning

OEM Warranty &

Aftersales/Dealers

Connected Services Providers

Fleet Related Services

OEM

Marketing Component Failure

Prediction Optimizing Vehicle

Performance Apps & HMI Usage

Analytics Feature Demand by

Regions Demand Sensing –

Production Scheduling

Dynamic Parts Pricing

Predicting Recall Scenarios Proactive

Diagnostics

Feature Packaging (Option/Std)

Tailored Auto Financing

Used Car Valuation

Parts Inventory Management

Service Contracts Upselling

Targeted Digital Marketing

Social Media Usage Analytics

Brand Loyalty Analytics

Cross Brand Ownership Analytics

Deals & Rebates

Product Feature Campaigning

EV Related Services Crowdsourced

Traffic + Parking + Weather

Traffic Management

Road Infrastructure + Public Transport

Multimodal Journey Planning Disaster

Management

Eco-Driving + Driver Training Usage-Based

Insurance

Fleet Optimization

Dynamic Route Planning

Freight Pricing

Driver Behavior Analysis

Asset Tracking

Prognostics

Forward Looking Innovative Services Current Services which will benefit from Big Data

Where it can Help - Big-Data Features and Services Aftersales and Diagnostics are the first entry point for OEMs looking to invest in Big Data Business models

Source: Frost & Sullivan analysis.

50

C o n t a c t D e t a i l s a n d F u r t h e r R e a d i n g

Sarwant Singh Partner– Visionary Innovation

(44) 207 915 7843

Follow Sarwant’s series on Mega Trends And Future of Mobility on Forbes.com http://www.forbes.com/sites/sarwantsingh/

51

Discussions

Promoting responsible transport www.bvrla.co.uk

Open to the floor… • Are there any lessons that the automotive sector

can learn form other sectors when rolling out connectivity services?

Promoting responsible transport www.bvrla.co.uk

John Parkinson Department for Transport

Industry Conference 2014 Break-out Session C

Fleet Technology Update

Promoting responsible transport www.bvrla.co.uk

Open to the floor… • How long until the average company car driver,

rental customer or van courier is able to sit back and get on with something else while driving along a major motorway or trunk road?

• Do you have any view on what impact all this safety technology is going to have on motor insurance premiums?

Promoting responsible transport www.bvrla.co.uk

Thank you to our speakers.

Lunch now being served in Gallery 2. Back in Kestrel Suite by 14:10 please.

Industry Conference 2014 Break-out Session C

Fleet Technology Update