india morning roundup -...

TRANSCRIPT

Institutional EquitiesDa

ily M

ornin

g Upd

ate

India Morning Roundup

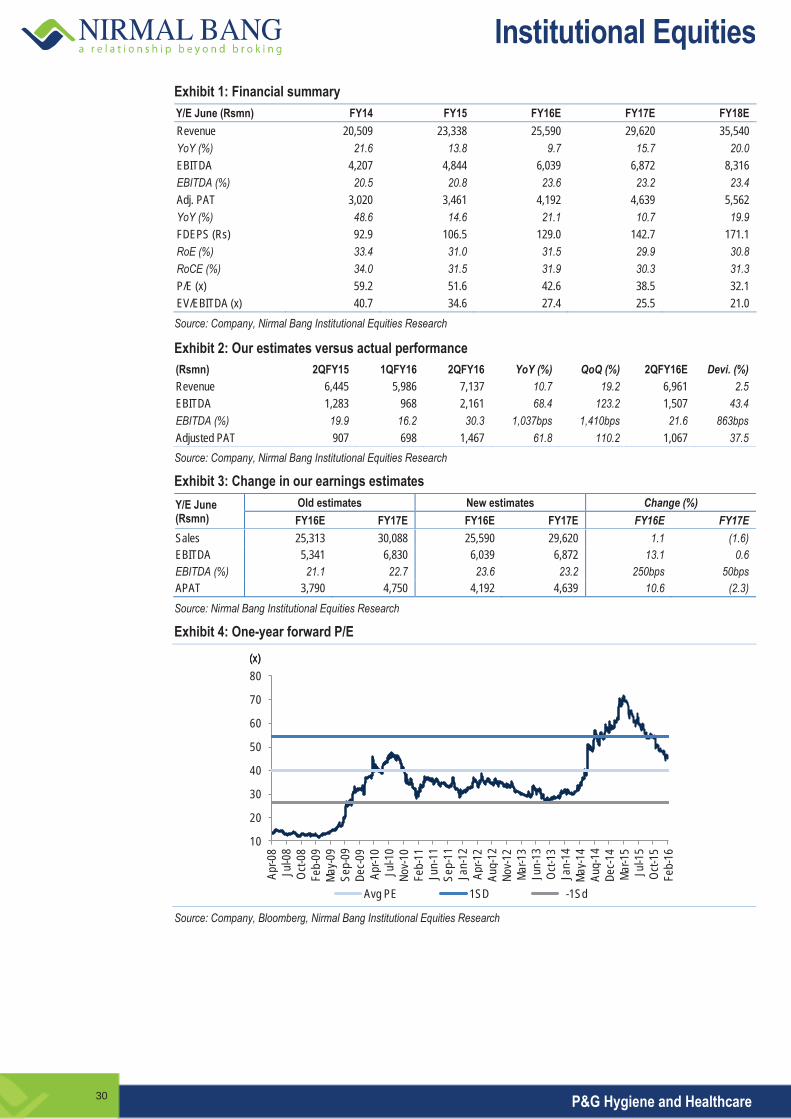

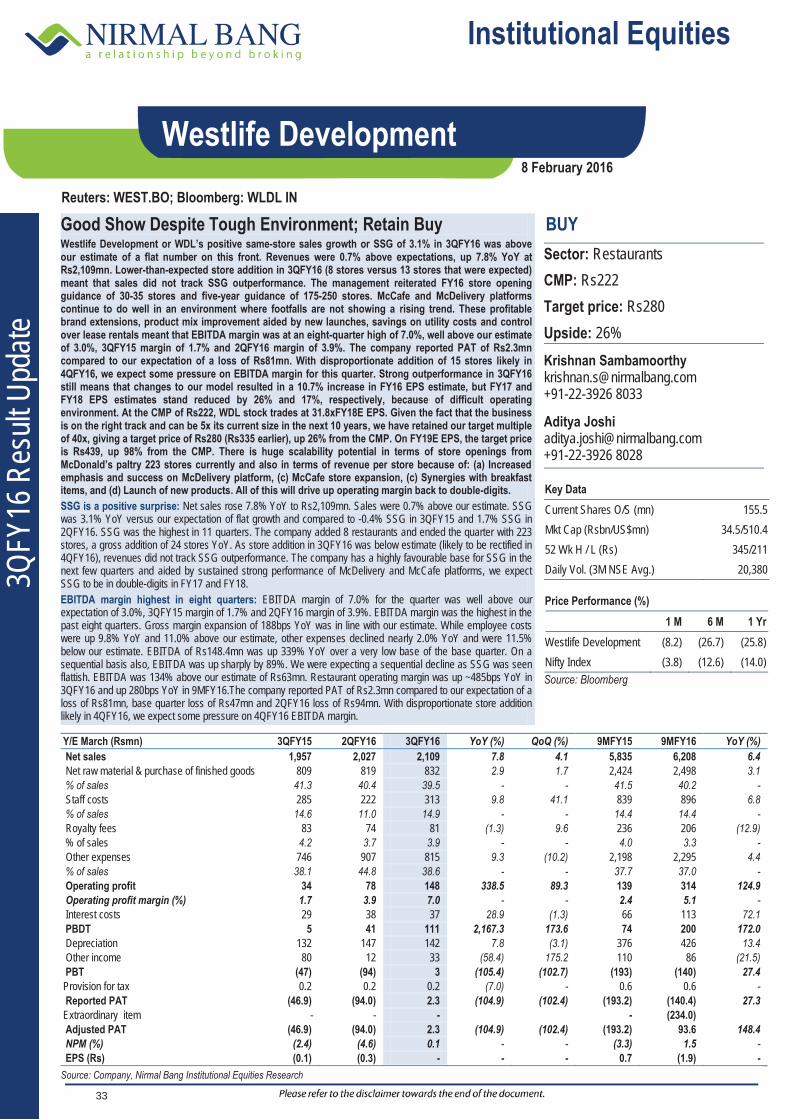

Contents Arvind- UNDER REVIEW - 3QFY16 Result Update - Subdued Performance: Following flattish revenue in textile division and 15.3%/11.8% growth in power brands/Brands & Retail or B&R division, respectively, consolidated revenue of Arvind in 3QFY16 grew 4.0% to Rs21,575mn, 9.9%/4.6% below our/Bloomberg consensus estimate, respectively, because of sluggish domestic environment, weak volume in denim which impacted the textile division and a 16% decline in Megamart’s revenue which dragged down the growth of B&R division. Cadila Healthcare- UNDER REVIEW - 3QFY16 Result Update - Stable Performance: Cadila Healthcare’s (CHL) reported 3QFY16 revenue of Rs24.3bn (up 11% YoY but down 1% QoQ) was 3%/1% below our/Bloomberg consensus estimate, respectively, on account of domestic business which declined 3.6% QoQ led by domestic formulations, down 5% QoQ. Export business grew 12%/3.8% YoY/QoQ, respectively, led by US formulations business, up 13.6%/4.6% YoY/QoQ, respectively, on account of growth witnessed in its existing portfolio. Divis Laboratories - UNDER REVIEW - 3QFY16 Result Update - Weak Performance Led By Lower Revenue Growth: Divis Laboratories (DLL) reported a weak set of numbers for 3QFY16, which were below expectations, with reported PAT of Rs2.5bn 10% below our/Bloomberg consensus estimate each, following lower revenue growth, which was 5%/9% below our/Bloomberg consensus estimate, respectively, at Rs8.5bn. Lakshmi Machine Works - BUY - 3QFY16 Result Update - Yet Another Quarter of Positive Surprise; Retain Buy: Lakshmi Machine Works (LMW) posted 3QFY16 performance that was better than our expectations. We are positively surprised by revenue traction in all segments coupled with margin expansion. Strong revenue and margin performance was led by higher exports in 3QFY16. Exports witnessed a YoY growth of 12.4% in 9MFY16 to Rs3.89bn. Lupin- UNDER REVIEW - 3QFY16 Result Update - Performance Beats Expectations Led By Growth In US Market: Lupin reported a better-than-expected performance for 3QFY16, with reported revenue of Rs35.6bn (up 12%/7% YoY/QoQ, respectively) being 8%/6% above our /Bloomberg consensus estimate, respectively, led by the US business which reported revenues of Rs14bn, up 22% QoQ, following improvement in base business portfolio, increased contribution from Suprax and Antara, price hikes and the flu season. P&G Hygiene and Healthcare - BUY - 3QFY16 Result Update - Strong Margins, Remarkable Balance Sheet Improvement: Net sales of P&G Hygiene and Healthcare or P&GHH grew 10.7% YoY to Rs7.1bn in 2QFY16, 2.5% above expectations, led by double-digit growth in feminine hygiene and healthcare segments. Strong gross margin improvement of 250bps YoY (2QFY16 witnessed highest gross margin in 2Q in five years), and decline in A&P spending and other expenses (at least part of the reason is likely to be one-offs, but not disclosed) along with better-than-expected sales led to a 24-quarter high EBITDA margin of 30.3%, resulting in 68.4% YoY growth in EBITDA to Rs2.2bn and PAT growth of 61.8% YoY to Rs1.5bn. Westlife Development - BUY - 3QFY16 Result Update - Good Show Despite Tough Environment; Retain Buy: Westlife Development or WDL’s positive same-store sales growth or SSG of 3.1% in 3QFY16 was above our estimate of a flat number on this front. Revenues were 0.7% above expectations, up 7.8% YoY at Rs2,109mn. Lower-than-expected store addition in 3QFY16 (8 stores versus 13 stores that were expected) meant that sales did not track SSG outperformance.

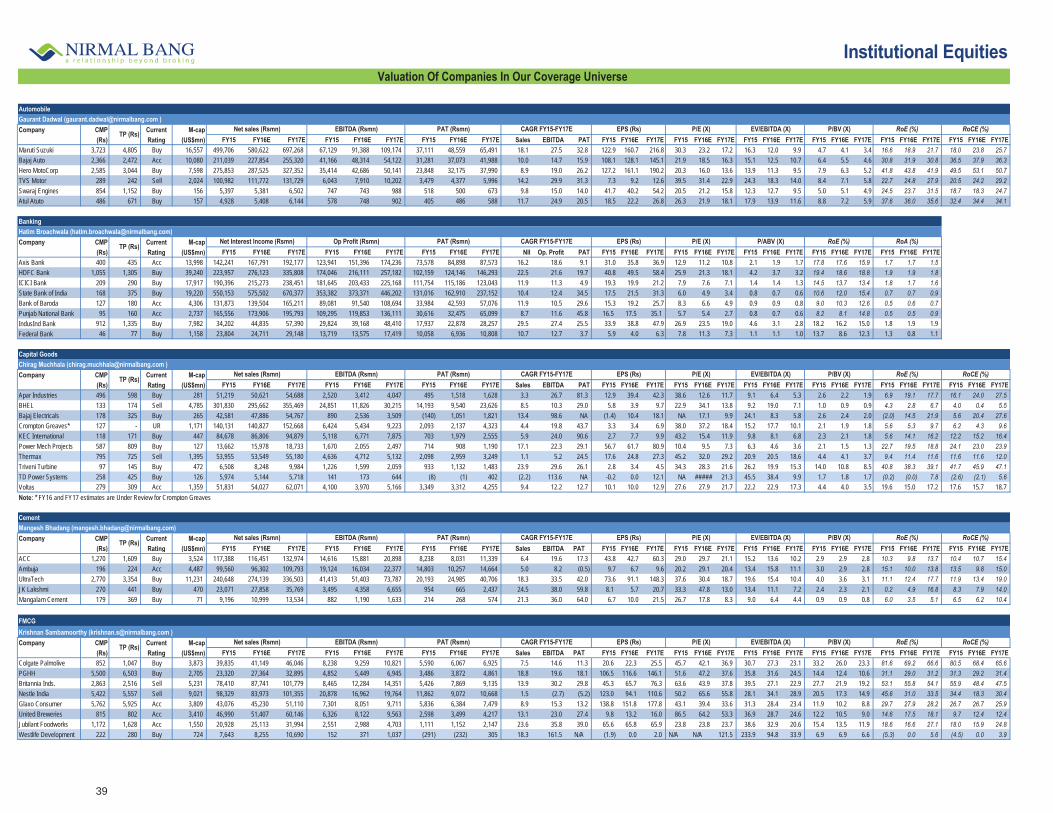

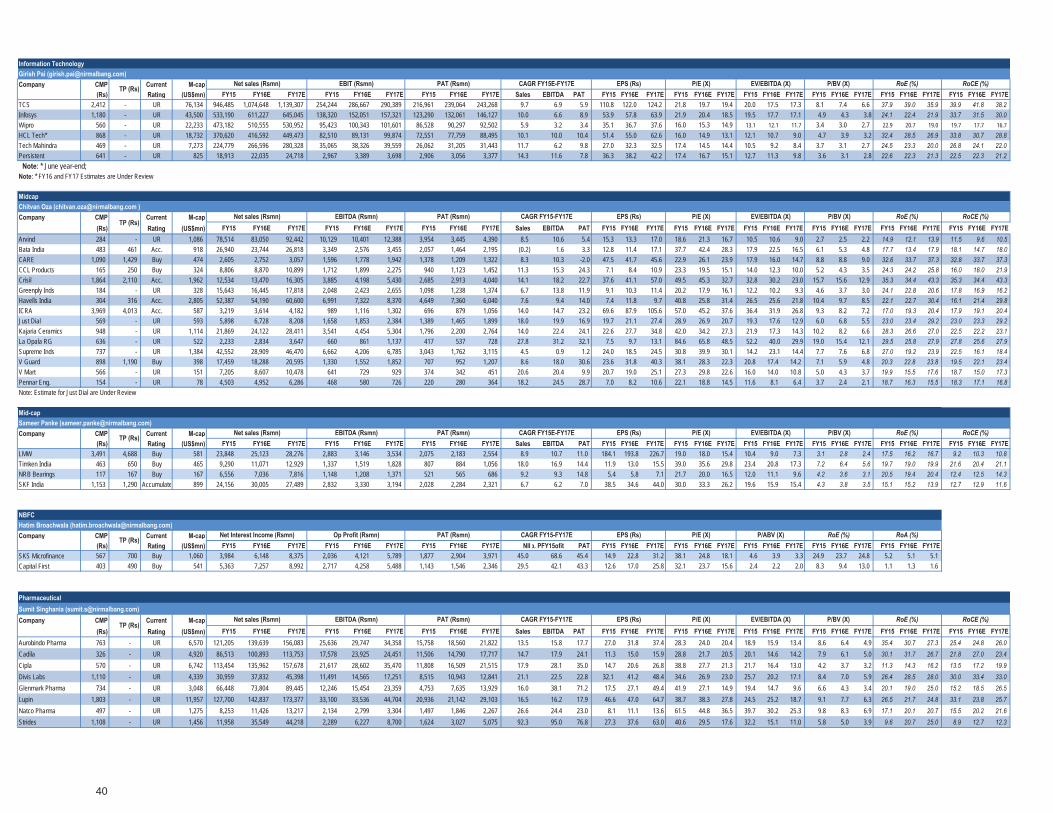

Corporate/Global/Local News Upcoming Events Valuation Of Companies In Our Coverage Universe Source: Bloomberg, NSE, Nirmal Bang Institutional

Equities Research

Local Indices(Chg %) Close Daily YTDBSE Sensex 24,617 1.1 (5.7) NSE Nifty 7,489 1.1 (5.8) Sectoral Indices(Chg %) Close Daily YTDCNX Mid-Cap 12,383 1.9 (7.6) CNX Bank Nifty Index 15,162 2.0 (10.4) CNX Metal Index 1,643 3.7 (10.1) CNX FMCG Index 19,465 1.0 (3.6) CNX Infrastructure Index 2,409 0.6 (13.0) CNX Auto Index 7,496 1.6 (9.2) CNX IT Index 11,228 0.1 0.1 World IndicesDow Jones 16,205 (1.3) (7.0) S & P 500 1,880 (1.8) (8.0) FTSE 100 5,848 (0.9) (6.3) Nasdaq 4,363 (3.2) (12.9) Hang Seng 19,288 0.5 (12.0) Shanghai Comp 2,763 (0.6) (21.9) Net Investment

8-Feb 1M 3MFIIs (US$mn) (46.5) (86.5) 10.3 MFs (US$mn) (379.4) 8.7 167.2 DII turnover (Rsmn) 476.4 13.2 636.2 Volume

8-Feb US$bn Chg%Cash (NSE + BSE) 1.1 1.1 (8.0) F&O (net) 4.0 0.4 1.7

8-Feb 1 D 1 M 3MRs/US$ 67.7 67.6 66.6 65.7Rs/EUR 75.8 75.6 71.7 71.4Rs/GBP 98.3 98.9 97.8 101.110 yr G-Sec 7.8 7.8 7.7 7.7Call Money 7.6 6.8 7.7 5.8

8-Feb 1 D 1 M 3 MGold (US$/ounce) 1,165 1,173 1,104 1,090 Brent Crude (US$/bbl) 34 34 35 50 Aluminimum (US$/mt) 1,499 1,535 1,463 1,507 Copper (US$/mt) 4,630 4,687 4,645 5,011

Commodities & others

Forex/Money Markets

7,350

7,400

7,450

7,500

7,550

9 AM 10 AM 11 AM 12 PM 1 PM 2 PM 3 PM

8 February 2016

1

Institutional Equities

Morning Note

Corporate News

Toshiba Transmission & Distribution Systems (India) announced completion of a 3bn Yen investment (around US$30mn) at its Hyderabad factory, an expansion which would enable it in meeting the growing domestic and global demand.

Adani Power Ltd to sign a deal to set up a US$2.2bn coal-based power plant in Jharkhand, two people with knowledge of the matter said, as its controlling shareholder aims to nearly double capacity this decade.

Biocon management clarifies that the US government’s decision to not allow overseas pharmaceutical companies to import active pharmaceutical ingredient (API) applies to only one particular anti – retroviral drug and is not a blanket ban.

Software provider Quick Heal Technologies Limited to enter market with initial public offering on Feb 8, IPO consists of a fresh issue of Rs2,500mn by the company and an offer for sale of up to 6.3mn equity-shares by promoters part from investments from Sequoia Capital.

Mudra Bank management said that Bank of Baroda, Bank of India and Punjab National Bank are in discussion for refinance and are seeking capital worth Rs5 –10bn.

Balaji Telefilms on Friday said that it will raise Rs1,500mn through the allotment of equity shares on a preferential basis.

SunEdison has commissioned 146 MW of solar power projects in Tamil Nadu, Andhra Pradesh and Telangana, the energy from the solar power plants would be sold to local distribution channels and private companies.

Global/Local News

The Income-Tax Department has issued detailed guidelines for using electronic communication, or emails, for paperless assessment proceedings, the government has allowed tax payers to reply to notices using their registered email address. Central government to sign MoU with Karnataka for railway JV, railways ministry to come to an agreement with the state government to ensure that a new entity in JV is created.

Foreign Portfolio Investors over Rs25bn in the Indian capital markets in the first week of the month after pulling out hefty funds in the preceding month.

Delhi government said it has made a collection of more than Rs20bn VAT within one month, the Department of Trade and Taxes collected the amount in the month of January.

China’s central bank to fine tune monetary policy and keep the Yuan basically stable while guarding against systemic financial risks. U.S. employment gains estimated to have slowed in January, non-farm payrolls probably increased by 190,000 jobs last month, according to Reuters.

2

Institutional Equities

Morning Note

Event Calendar

8 February 9 February 10 February 11 February GSK Consumer 3QFY16e Revenue: Rs 9.7bn EBITDA: Rs 842mn PAT: Rs 816mn Strides Shasun Ltd 3QFY16e Revenue: Rs 8.4bn EBITDA: Rs 1.5bn PAT: Rs 572mn Atul Auto 3QFY16e Revenue: Rs 1,505mn EBITDA: Rs 224n PAT: Rs 145mn

Britannia 3QFY16e Revenue: Rs 22.4bn EBITDA: Rs 3.1bn PAT: Rs 2.0bn Aurobindo Pharma 3QFY16e Revenue: Rs 36.1bn EBITDA: Rs 8.7bn PAT: Rs 5.6bn Timken India 3QFY16e Revenue: Rs 2.7bn EBITDA: Rs 293mn PAT: Rs 165mn

Bajaj Electricals 3QFY16e Revenue: Rs 11.9bn EBITDA: Rs 569mn PAT: Rs 187mn Bata India 3QFY16e Revenue: Rs 6,221mn EBITDA: Rs 647mn PAT: Rs 351mn

Jubilant FoodWorks 3QFY16eRevenue: Rs 6.6bn EBITDA: Rs 825mn PAT: Rs 313mn Voltas 3QFY16e Revenue: Rs 10.9bn EBITDA: Rs 701mn PAT: Rs 589mn SKF India 4QFY16e Revenue: Rs 6.0bn EBITDA: Rs 539mn PAT: Rs 410mn BHEL 3QFY16e Revenue: Rs 65bn EBITDA: Rs 2.3bn PAT: Rs 1.9bn Natco Ltd 3QFY16e Revenue: Rs 2.6bn EBITDA: Rs 641mn PAT: Rs 339mn Hero MotoCorp 3QFY16e Revenue: Rs 73.8bn EBITDA: Rs 10.7bn PAT: Rs 7.6bn

12 February 13 February 14 February 15 February Nestle India 4QCY15e Revenue: Rs 21.8bn EBITDA: Rs 4.0bn PAT: Rs 2.3bn

16 February 17 February 18 February 19 February

20 February 21 February 22 February 23 February

3

Institutional Equities3Q

FY16

Res

ult U

pdate

Reuters: ARVN.BO; Bloomberg: ARVND IN

Arvind

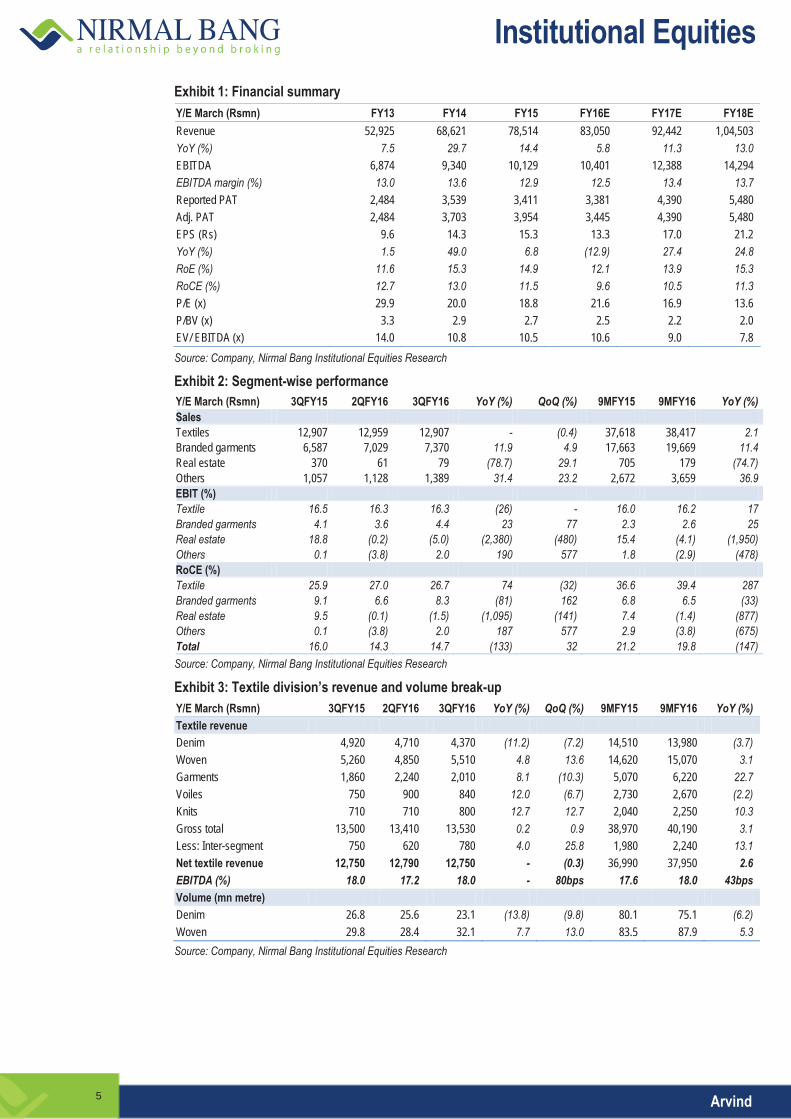

Subdued Performance Following flattish revenue in textile division and 15.3%/11.8% growth in power brands/Brands & Retail or B&R division, respectively, consolidated revenue of Arvind in 3QFY16 grew 4.0% to Rs21,575mn, 9.9%/4.6% below our/Bloomberg consensus estimate, respectively, because of sluggish domestic environment, weak volume in denim which impacted the textile division and a 16% decline in Megamart’s revenue which dragged down the growth of B&R division. In the wake of a challenging environment, brands segment achieved same-store sales growth or SSG of 1.7%. Core operating margin of B&R division improved 60bps, while the margins of power brands and textile division were flattish as a result of which consolidated operating margin declined 90bps to 13%, 100bps/64bps below our/Bloomberg estimate respectively. EBIT margin of textile/branded garment division declined/improved by 26bps/23bps to 16.3%/4.4% respectively. Following weak revenue growth and decline in margins, adjusted net profit fell to Rs1,042mn, 14.7%/11.3% below our/Bloomberg estimate, respectively. Working capital cycle of B&R division reduced from 154 days a year ago to 135 days in 3QFY16. Arvind reduced its inventory days in brands division by 32 days and in Megamart by 27 days. Departmental stores (contributing 30% to Arvind’s sales) operates on Sale or Return model now as a result of which the receivables increased for Arvind. The company is confident of bringing down the receivables level in FY17. The management expects brands division to grow 15%-16% and the company to grow 12%-14% for next five years. The management expects 4QFY16 to be very healthy as several large format stores have been set up during the quarter and expects a 9%-10% growth at company level. We have cut our FY16/FY17/FY18 revenue estimates by 4.1%/7.2%/9.1%, and PAT estimates by 6.6%/10.9%/13.3%, respectively. With a strong portfolio, Arvind has now turned selective in choosing new brands. It plans to partner with only those brands that have potential to deliver Rs5bn revenue, unlike its earlier benchmark of Rs1bn, leading to lower cash burn in future. Currently, the stock trades attractively at 13.6x/7.8x FY18E P/E and EV/EBITDA, respectively. Healthy margins in B&R division: Core operating margin of B&R division rose 60bps to 7.6%. Power brands’ revenue increased 15.3% to Rs4,150mn. Like-to-like growth (LTL) in power brands stood at 6%. Full-price sales in power brands has been very healthy and as a result it reduced the percentage of clothes sold on discount which affected LTL growth, although it has been profitable at EBITDA level. Improvement in working capital cycle in B&R division: Working capital cycle of B&R division reduced from 154 days a year ago to 135 days in 3QFY16. Arvind reduced its inventory days in brands division by 32 days and in Megamart by 27 days. Departmental stores (contributes 30% to Arvind’s sales) operate on Sale or Return model now as a result of which the receivables increased in FY16. The company is confident of bringing down its receivables level in FY17 by taking various initiatives. Denim impacts textile division: Textile division’s revenue was flat at Rs4,370mn. Denim volume declined 13.8% because of: a) Change in product mix, and b) Less off-take by some customers. There is no selling pressure in this division. Woven segment witnessed a rise in capacity to 130mn metres this year. It is growing steadily, although the pace is slower than what the management expected. The management expects ~116mn metres of woven fabric sales in FY16. Total capacity (India and Ethiopia) in shirt division increased from 6mn metres to 12mn metres and both countries are expected to have a significant improvement in shirt business in FY17.

UNDER REVIEW Sector: Retail CMP: Rs288

Chitvan Oza [email protected] +91-22-3926 8175

Key Data Current Shares O/S (mn) 258.2 Mkt Cap (Rsbn/US$bn) 74.3/1.1 52 Wk H / L (Rs) 366/216 Daily Vol. (3M NSE Avg.) 1,822,418 Price Performance (%)

1 M 6 M 1 Yr Arvind (17.2) (9.0) (1.5) Nifty Index (5.0) (13.1) (15.1)

Y/E March (Rsmn) 3QFY15 2QFY16 3QFY16 YoY (%) QoQ (%) 9MFY15 9MFY16 YoY (%) Net sales 20,737 20,964 21,575 4.0 2.9 58,109 61,309 5.5 Net RM costs & purchases of finished goods 9,066 9,080 9,492 4.7 4.5 25,773 26,637 3.4 % of sales 43.7 43.3 44.0 - - 44.4 43.4 - Employee costs 2,081 2,307 2,244 7.8 (2.7) 5,996 6,781 13.1 % of sales 10.0 11.0 10.4 - - 10.3 11.1 - Other expenses 6,708 6,964 7,034 4.9 1.0 18,807 20,206 7.4 % of sales 32.3 33.2 32.6 - - 32.4 33.0 - Operating profit 2,882 2,614 2,805 (2.7) 7.3 7,533 7,684 2.0 OPM (%) 13.9 12.5 13.0 - - 13.0 12.5 - Interest costs 1,018 947 895 (12.1) (5.4) 2,990 2,867 (4.1) Depreciation 558 614 654 17.1 6.5 1,563 1,895 21.2 Other income 150 320 188 25.4 (41.1) 702 756 7.6 Extra-ordinary income (25) (38) (13) (47.8) (66.0) (59) (79) 34.5 PBT 1,432 1,335 1,432 (0.0) 7.2 3,623 3,599 (0.6) Provision for tax 350 406 386 10.3 (4.9) 716 1,059 47.9 Effective tax rate (%) 24.4 30.4 26.9 - - 19.8 29.4 - Adjusted PAT 1,110 937 1,042 (6.1) 11.3 2,975 2,588 (13.0) NPM (%) 5.4 4.5 4.8 - - 5.1 4.2 - EPS (Rs) 4.3 3.6 4.0 (6.1) 11.3 11.5 10.0 (13.0) Source: Company, Nirmal Bang Institutional Equities Research

5 February 2016

4

Institutional Equities

Arvind

Exhibit 1: Financial summary Y/E March (Rsmn) FY13 FY14 FY15 FY16E FY17E FY18E Revenue 52,925 68,621 78,514 83,050 92,442 1,04,503 YoY (%) 7.5 29.7 14.4 5.8 11.3 13.0 EBITDA 6,874 9,340 10,129 10,401 12,388 14,294 EBITDA margin (%) 13.0 13.6 12.9 12.5 13.4 13.7 Reported PAT 2,484 3,539 3,411 3,381 4,390 5,480 Adj. PAT 2,484 3,703 3,954 3,445 4,390 5,480 EPS (Rs) 9.6 14.3 15.3 13.3 17.0 21.2 YoY (%) 1.5 49.0 6.8 (12.9) 27.4 24.8 RoE (%) 11.6 15.3 14.9 12.1 13.9 15.3 RoCE (%) 12.7 13.0 11.5 9.6 10.5 11.3 P/E (x) 29.9 20.0 18.8 21.6 16.9 13.6 P/BV (x) 3.3 2.9 2.7 2.5 2.2 2.0 EV/ EBITDA (x) 14.0 10.8 10.5 10.6 9.0 7.8 Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 2: Segment-wise performance Y/E March (Rsmn) 3QFY15 2QFY16 3QFY16 YoY (%) QoQ (%) 9MFY15 9MFY16 YoY (%) Sales Textiles 12,907 12,959 12,907 - (0.4) 37,618 38,417 2.1 Branded garments 6,587 7,029 7,370 11.9 4.9 17,663 19,669 11.4 Real estate 370 61 79 (78.7) 29.1 705 179 (74.7) Others 1,057 1,128 1,389 31.4 23.2 2,672 3,659 36.9 EBIT (%) Textile 16.5 16.3 16.3 (26) - 16.0 16.2 17 Branded garments 4.1 3.6 4.4 23 77 2.3 2.6 25 Real estate 18.8 (0.2) (5.0) (2,380) (480) 15.4 (4.1) (1,950) Others 0.1 (3.8) 2.0 190 577 1.8 (2.9) (478) RoCE (%) Textile 25.9 27.0 26.7 74 (32) 36.6 39.4 287 Branded garments 9.1 6.6 8.3 (81) 162 6.8 6.5 (33) Real estate 9.5 (0.1) (1.5) (1,095) (141) 7.4 (1.4) (877) Others 0.1 (3.8) 2.0 187 577 2.9 (3.8) (675) Total 16.0 14.3 14.7 (133) 32 21.2 19.8 (147) Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 3: Textile division’s revenue and volume break-up Y/E March (Rsmn) 3QFY15 2QFY16 3QFY16 YoY (%) QoQ (%) 9MFY15 9MFY16 YoY (%) Textile revenue Denim 4,920 4,710 4,370 (11.2) (7.2) 14,510 13,980 (3.7) Woven 5,260 4,850 5,510 4.8 13.6 14,620 15,070 3.1 Garments 1,860 2,240 2,010 8.1 (10.3) 5,070 6,220 22.7 Voiles 750 900 840 12.0 (6.7) 2,730 2,670 (2.2) Knits 710 710 800 12.7 12.7 2,040 2,250 10.3 Gross total 13,500 13,410 13,530 0.2 0.9 38,970 40,190 3.1 Less: Inter-segment 750 620 780 4.0 25.8 1,980 2,240 13.1 Net textile revenue 12,750 12,790 12,750 - (0.3) 36,990 37,950 2.6 EBITDA (%) 18.0 17.2 18.0 - 80bps 17.6 18.0 43bps Volume (mn metre) Denim 26.8 25.6 23.1 (13.8) (9.8) 80.1 75.1 (6.2) Woven 29.8 28.4 32.1 7.7 13.0 83.5 87.9 5.3 Source: Company, Nirmal Bang Institutional Equities Research

5

Institutional Equities

Arvind

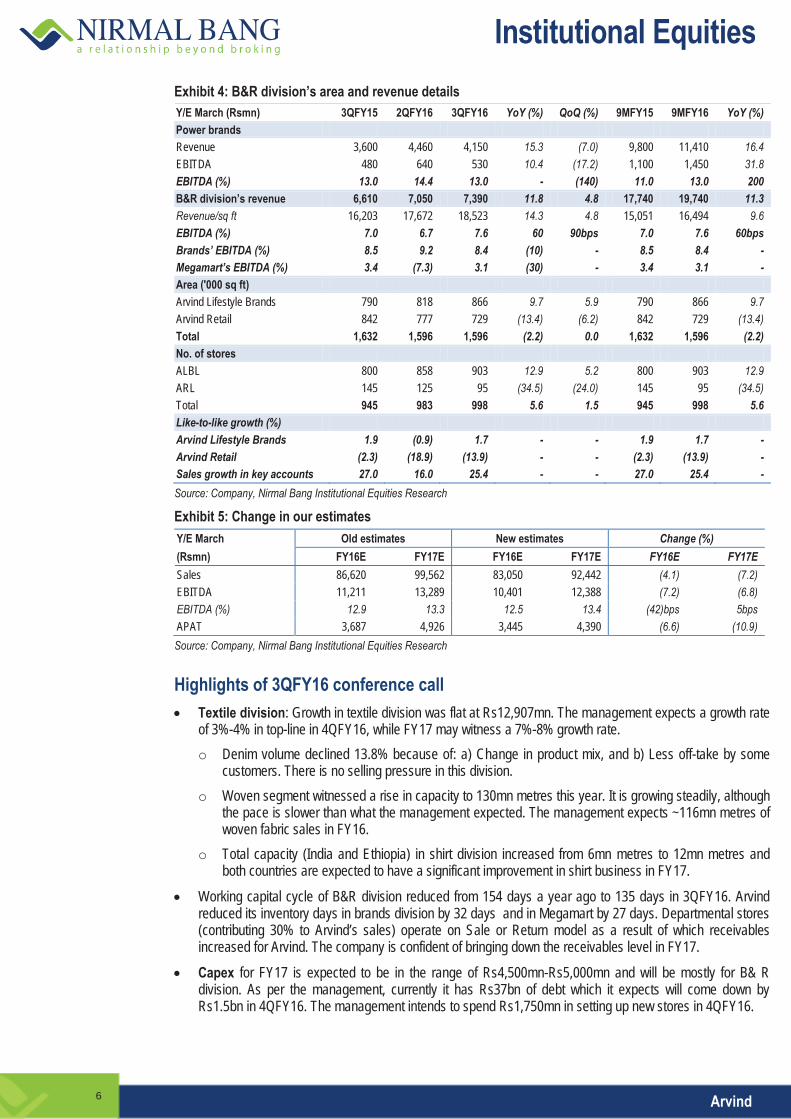

Exhibit 4: B&R division’s area and revenue details Y/E March (Rsmn) 3QFY15 2QFY16 3QFY16 YoY (%) QoQ (%) 9MFY15 9MFY16 YoY (%) Power brands Revenue 3,600 4,460 4,150 15.3 (7.0) 9,800 11,410 16.4 EBITDA 480 640 530 10.4 (17.2) 1,100 1,450 31.8 EBITDA (%) 13.0 14.4 13.0 - (140) 11.0 13.0 200 B&R division’s revenue 6,610 7,050 7,390 11.8 4.8 17,740 19,740 11.3 Revenue/sq ft 16,203 17,672 18,523 14.3 4.8 15,051 16,494 9.6 EBITDA (%) 7.0 6.7 7.6 60 90bps 7.0 7.6 60bps Brands’ EBITDA (%) 8.5 9.2 8.4 (10) - 8.5 8.4 - Megamart’s EBITDA (%) 3.4 (7.3) 3.1 (30) - 3.4 3.1 - Area ('000 sq ft) Arvind Lifestyle Brands 790 818 866 9.7 5.9 790 866 9.7 Arvind Retail 842 777 729 (13.4) (6.2) 842 729 (13.4) Total 1,632 1,596 1,596 (2.2) 0.0 1,632 1,596 (2.2) No. of stores ALBL 800 858 903 12.9 5.2 800 903 12.9 ARL 145 125 95 (34.5) (24.0) 145 95 (34.5) Total 945 983 998 5.6 1.5 945 998 5.6 Like-to-like growth (%) Arvind Lifestyle Brands 1.9 (0.9) 1.7 - - 1.9 1.7 - Arvind Retail (2.3) (18.9) (13.9) - - (2.3) (13.9) - Sales growth in key accounts 27.0 16.0 25.4 - - 27.0 25.4 - Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 5: Change in our estimates Y/E March Old estimates New estimates Change (%) (Rsmn) FY16E FY17E FY16E FY17E FY16E FY17E Sales 86,620 99,562 83,050 92,442 (4.1) (7.2) EBITDA 11,211 13,289 10,401 12,388 (7.2) (6.8) EBITDA (%) 12.9 13.3 12.5 13.4 (42)bps 5bps APAT 3,687 4,926 3,445 4,390 (6.6) (10.9) Source: Company, Nirmal Bang Institutional Equities Research Highlights of 3QFY16 conference call

Textile division: Growth in textile division was flat at Rs12,907mn. The management expects a growth rate of 3%-4% in top-line in 4QFY16, while FY17 may witness a 7%-8% growth rate. o Denim volume declined 13.8% because of: a) Change in product mix, and b) Less off-take by some

customers. There is no selling pressure in this division. o Woven segment witnessed a rise in capacity to 130mn metres this year. It is growing steadily, although

the pace is slower than what the management expected. The management expects ~116mn metres of woven fabric sales in FY16.

o Total capacity (India and Ethiopia) in shirt division increased from 6mn metres to 12mn metres and both countries are expected to have a significant improvement in shirt business in FY17.

Working capital cycle of B&R division reduced from 154 days a year ago to 135 days in 3QFY16. Arvind reduced its inventory days in brands division by 32 days and in Megamart by 27 days. Departmental stores (contributing 30% to Arvind’s sales) operate on Sale or Return model as a result of which receivables increased for Arvind. The company is confident of bringing down the receivables level in FY17.

Capex for FY17 is expected to be in the range of Rs4,500mn-Rs5,000mn and will be mostly for B& R division. As per the management, currently it has Rs37bn of debt which it expects will come down by Rs1.5bn in 4QFY16. The management intends to spend Rs1,750mn in setting up new stores in 4QFY16.

6

Institutional Equities

Arvind

Megamart: Arvind has almost completed its exercise of store closure as in 3QFY16 their number reduced to 95 stores from 145 earlier. It closed 35 stores (mainly small stores) in 3QFY16 as a result of which revenues of Megamart declined 16%. Revenues of Megamart declined from Rs4,620mn in 3QFY15 toRs4,030mn in 3QFY16. The management intends to set up a few large format stores next year. Megmart is expected to achieve a turnover in FY17 similar to FY16.

Online channel contributes to 6% of sales for brands division. The management expects its contribution to increase to 8% in FY17. Margins are better in online channel and the company intends to launch a beta version of its online portal in March 2016.

The management expects 4QFY16 to be very healthy as several large format stores have been set up during the quarter. The company expects a 28%-29% growth in B&R division with Megamart acting as a drag. Overall, company is expecting 9%-10% growth in 4QFY16.

Brands & Retail division: o Power brands’ revenue increased 15.3% to Rs4,150mn. Like-to-like growth (LTL) in power brands

stood at 6%. Full-price sales in power brands division has been very healthy, thereby reducing the percentage of clothes sold on discount which affected LTL growth, although it has been profitable at EBITDA margin level. The growth in power brands declined by 15% from 23%-24% earlier as many of its brands have already matured. The management expects growth in power brands to be 17%-18% for FY16.

o Growth brands (excluding new and power brands) are expected to grow 28% in FY16 and 40%-60% in FY17.

o Speciality Retail: Currently, it has four GAP stores, has inherited four stores of Sephora and set up one store in Mumbai last week, TCY had only one store, but it opened two more stores, Aeropostole has one store. Overall launches have been successful and they were done with minimal investment. From low turnover and marginal loss earlier, it intends to become profitable now. Arvind will get full-year benefits of these stores in FY17, unlike in FY16.

The management expects brands division to grow 15%-16% for the next five years and expects a 10%-12% growth for the next five years in retail segment. Overall, it expects the company to grow 12%-14%.

Exhibit 6: Our estimates versus actual performance (Rsmn) 3QFY15 2QFY16 3QFY16 YoY (%) QoQ (%) 3QFY16E Devi. (%) 3QFY16 BBE Devi.(%) Revenue 20,737 20,964 21,575 4.0 2.9 23,949 (9.9) 22,615 (4.6) EBITDA 2,882 2,614 2,805 (2.7) 7.3 3,353 (16.3) 3,084 (9.0) EBITDA (%) 13.9 12.5 13.0 (90) 53 14.0 (100) 13.6 (64) Adjusted PAT 1,110 937 1,042 (6.1) 11.3 1,222 (14.7) 1,175 (11.3) Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 7: One-year forward P/E Exhibit 8: P/E median band

Source: Nirmal Bang Institutional Equities Research

0

50

100

150

200

250

300

350

400

Aug-

11

Nov-1

1

Feb-

12

May-1

2

Aug-

12

Nov-1

2

Feb-

13

May-1

3

Aug-

13

Nov-1

3

Feb-

14Ma

y-14

Aug-

14

Nov-1

4

Feb-

15

May-1

5

Aug-

15

Nov-1

5

Feb-

16

(Rs)

9x

21x

6x

12x15x18x

0

5

10

15

20

25

30

Aug-

11

Nov-1

1

Feb-

12

May-1

2

Aug-

12

Nov-1

2

Feb-

13

May-1

3

Aug-

13

Nov-1

3

Feb-

14

May-1

4

Aug-

14

Nov-1

4

Feb-

15

May-1

5

Aug-

15

Nov-1

5

Feb-

16

(x)

Median 9.1x

7

Institutional Equities

Arvind

Exhibit 9: One-year forward EV/EBITDA Exhibit 10: EV/EBITDA median band

Source: Nirmal Bang Institutional Equities Research

30 40 50 60 70 80 90

100 110 120 130

Aug-

11

Nov-1

1

Feb-

12Ma

y-12

Aug-

12

Nov-1

2

Feb-

13Ma

y-13

Aug-

13

Nov-1

3

Feb-

14Ma

y-14

Aug-

14

Nov-1

4

Feb-

15Ma

y-15

Aug-

15

Nov-1

5

Feb-

16

(Rsbn)

7x

10x

9x

6x

8x

4

5

6

7

8

9

10

11

Aug-

11

Nov-

11

Feb-

12

May

-12

Aug-

12

Nov-

12

Feb-

13

May

-13

Aug-

13

Nov-

13

Feb-

14

May

-14

Aug-

14

Nov-

14

Feb-

15

(x)

Median 6.7x

8

Institutional Equities

Arvind

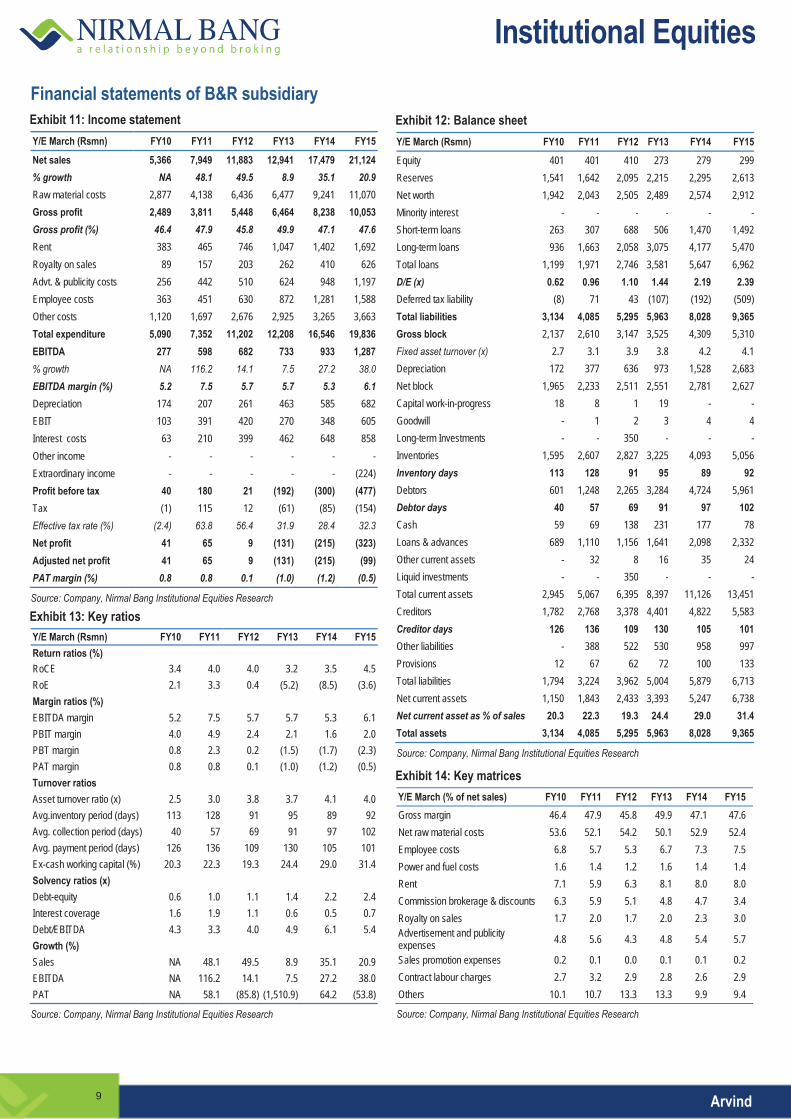

Financial statements of B&R subsidiary Exhibit 11: Income statement Y/E March (Rsmn) FY10 FY11 FY12 FY13 FY14 FY15 Net sales 5,366 7,949 11,883 12,941 17,479 21,124 % growth NA 48.1 49.5 8.9 35.1 20.9 Raw material costs 2,877 4,138 6,436 6,477 9,241 11,070 Gross profit 2,489 3,811 5,448 6,464 8,238 10,053 Gross profit (%) 46.4 47.9 45.8 49.9 47.1 47.6 Rent 383 465 746 1,047 1,402 1,692 Royalty on sales 89 157 203 262 410 626 Advt. & publicity costs 256 442 510 624 948 1,197 Employee costs 363 451 630 872 1,281 1,588 Other costs 1,120 1,697 2,676 2,925 3,265 3,663 Total expenditure 5,090 7,352 11,202 12,208 16,546 19,836 EBITDA 277 598 682 733 933 1,287 % growth NA 116.2 14.1 7.5 27.2 38.0 EBITDA margin (%) 5.2 7.5 5.7 5.7 5.3 6.1 Depreciation 174 207 261 463 585 682 EBIT 103 391 420 270 348 605 Interest costs 63 210 399 462 648 858 Other income - - - - - - Extraordinary income - - - - - (224) Profit before tax 40 180 21 (192) (300) (477) Tax (1) 115 12 (61) (85) (154) Effective tax rate (%) (2.4) 63.8 56.4 31.9 28.4 32.3 Net profit 41 65 9 (131) (215) (323) Adjusted net profit 41 65 9 (131) (215) (99) PAT margin (%) 0.8 0.8 0.1 (1.0) (1.2) (0.5)

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 13: Key ratiosY/E March (Rsmn) FY10 FY11 FY12 FY13 FY14 FY15 Return ratios (%) RoCE 3.4 4.0 4.0 3.2 3.5 4.5 RoE 2.1 3.3 0.4 (5.2) (8.5) (3.6) Margin ratios (%) EBITDA margin 5.2 7.5 5.7 5.7 5.3 6.1 PBIT margin 4.0 4.9 2.4 2.1 1.6 2.0 PBT margin 0.8 2.3 0.2 (1.5) (1.7) (2.3) PAT margin 0.8 0.8 0.1 (1.0) (1.2) (0.5) Turnover ratios Asset turnover ratio (x) 2.5 3.0 3.8 3.7 4.1 4.0 Avg.inventory period (days) 113 128 91 95 89 92 Avg. collection period (days) 40 57 69 91 97 102 Avg. payment period (days) 126 136 109 130 105 101 Ex-cash working capital (%) 20.3 22.3 19.3 24.4 29.0 31.4 Solvency ratios (x) Debt-equity 0.6 1.0 1.1 1.4 2.2 2.4 Interest coverage 1.6 1.9 1.1 0.6 0.5 0.7 Debt/EBITDA 4.3 3.3 4.0 4.9 6.1 5.4 Growth (%) Sales NA 48.1 49.5 8.9 35.1 20.9 EBITDA NA 116.2 14.1 7.5 27.2 38.0 PAT NA 58.1 (85.8) (1,510.9) 64.2 (53.8)

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 12: Balance sheet Y/E March (Rsmn) FY10 FY11 FY12 FY13 FY14 FY15 Equity 401 401 410 273 279 299 Reserves 1,541 1,642 2,095 2,215 2,295 2,613 Net worth 1,942 2,043 2,505 2,489 2,574 2,912 Minority interest - - - - - - Short-term loans 263 307 688 506 1,470 1,492 Long-term loans 936 1,663 2,058 3,075 4,177 5,470 Total loans 1,199 1,971 2,746 3,581 5,647 6,962 D/E (x) 0.62 0.96 1.10 1.44 2.19 2.39 Deferred tax liability (8) 71 43 (107) (192) (509) Total liabilities 3,134 4,085 5,295 5,963 8,028 9,365 Gross block 2,137 2,610 3,147 3,525 4,309 5,310 Fixed asset turnover (x) 2.7 3.1 3.9 3.8 4.2 4.1 Depreciation 172 377 636 973 1,528 2,683 Net block 1,965 2,233 2,511 2,551 2,781 2,627 Capital work-in-progress 18 8 1 19 - - Goodwill - 1 2 3 4 4 Long-term Investments - - 350 - - - Inventories 1,595 2,607 2,827 3,225 4,093 5,056 Inventory days 113 128 91 95 89 92 Debtors 601 1,248 2,265 3,284 4,724 5,961 Debtor days 40 57 69 91 97 102 Cash 59 69 138 231 177 78 Loans & advances 689 1,110 1,156 1,641 2,098 2,332 Other current assets - 32 8 16 35 24 Liquid investments - - 350 - - - Total current assets 2,945 5,067 6,395 8,397 11,126 13,451 Creditors 1,782 2,768 3,378 4,401 4,822 5,583 Creditor days 126 136 109 130 105 101 Other liabilities - 388 522 530 958 997 Provisions 12 67 62 72 100 133 Total liabilities 1,794 3,224 3,962 5,004 5,879 6,713 Net current assets 1,150 1,843 2,433 3,393 5,247 6,738 Net current asset as % of sales 20.3 22.3 19.3 24.4 29.0 31.4 Total assets 3,134 4,085 5,295 5,963 8,028 9,365

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 14: Key matricesY/E March (% of net sales) FY10 FY11 FY12 FY13 FY14 FY15 Gross margin 46.4 47.9 45.8 49.9 47.1 47.6 Net raw material costs 53.6 52.1 54.2 50.1 52.9 52.4 Employee costs 6.8 5.7 5.3 6.7 7.3 7.5 Power and fuel costs 1.6 1.4 1.2 1.6 1.4 1.4 Rent 7.1 5.9 6.3 8.1 8.0 8.0 Commission brokerage & discounts 6.3 5.9 5.1 4.8 4.7 3.4 Royalty on sales 1.7 2.0 1.7 2.0 2.3 3.0 Advertisement and publicity expenses 4.8 5.6 4.3 4.8 5.4 5.7

Sales promotion expenses 0.2 0.1 0.0 0.1 0.1 0.2 Contract labour charges 2.7 3.2 2.9 2.8 2.6 2.9 Others 10.1 10.7 13.3 13.3 9.9 9.4

Source: Company, Nirmal Bang Institutional Equities Research

9

Institutional Equities

Arvind

Financials (consolidated) Exhibit 15: Income statement Y/E March (Rsmn) FY13 FY14 FY15 FY16E FY17E FY18E Net sales 52,925 68,621 78,514 83,050 92,442 1,04,503 % growth 7.5 29.7 14.4 5.8 11.3 13.0 Raw material costs 22,272 31,241 34,939 36,922 40,467 45,561 Power & fuel 4,298 4,343 4,882 5,501 6,123 6,922 Staff costs 5,656 6,793 8,023 8,471 9,429 10,659 Other mfg. 13,825 16,904 20,542 21,755 24,035 27,066 Total expenditure 46,051 59,281 68,386 72,650 80,054 90,209 EBITDA 6,874 9,340 10,129 10,401 12,388 14,294 % growth 14.1 35.9 8.4 2.7 19.1 15.4 EBITDA margin (%) 13.0 13.6 12.9 12.5 13.4 13.7 Depreciation 2,043 2,252 2,124 2,553 2,808 3,040 EBIT 4,831 7,088 8,005 7,848 9,580 11,254 % growth 9.6 46.7 12.9 (2.0) 22.1 17.5 Interest 3,153 3,545 3,946 3,872 4,126 4,247 Other income 806 694 932 998 832 836 Extraordinary items - (164) (543) (79) - - Profit before tax 2,483 4,073 4,448 4,895 6,286 7,843 % growth (49.9) 64.0 9.2 10.1 28.4 24.8 Tax 3 548 1,072 1,488 1,886 2,353 Effective tax rate (%) 0.1 13.4 24.1 30.4 30.0 30.0 Net profit 2,481 3,526 3,376 3,407 4,400 5,490 % growth (43.1) 42.1 (4.2) 0.9 29.1 24.8 Extraordinary items - (164) (543) (64) - - Adjusted PAT 2,484 3,703 3,954 3,445 4,390 5,480 % growth 1.5 49.1 6.8 (12.9)

(12 9)27.4 24.8

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 17: Balance sheet Y/E March (Rsmn) FY13 FY14 FY15 FY16E FY17E FY18E Equity 2,580 2,582 2,582 2,582 2,582 2,582 Reserves 19,959 23,248 24,656 27,254 30,830 35,467 Net worth 22,540 25,830 27,239 29,836 33,413 38,049 Minority Int 108 242 348 374 384 394 Short-term loans 14,557 16,465 20,020 22,120 22,820 23,520 Long-term loans 10,051 13,455 13,941 14,641 15,441 15,441 Total loans 24,608 29,920 33,961 36,761 38,261 38,961 Deferred tax liability 58 435 471 1,058 1,812 2,754 Liabilities 47,313 56,427 62,018 68,029 73,870 80,157 Gross block 41,591 44,775 49,870 55,870 61,046 66,077 Depreciation 15,988 17,063 19,861 22,414 25,222 28,262 Net block 25,604 27,712 30,009 33,455 35,823 37,815 Capital work-in-progress 2,076 1,347 1,000 1,676 1,831 1,982 Goodwill 1,341 1,215 2,074 2,074 2,074 2,074 Long-term Investments 678 1,293 586 586 586 586 Inventories 14,129 16,281 18,450 18,768 20,681 23,304 Debtors 8,735 10,093 11,658 14,010 15,334 17,041 Cash 1,856 1,663 833 328 572 725 Other current assets 7,915 14,028 15,147 16,029 17,841 20,169 Total current assets 32,635 42,066 46,089 49,134 54,428 61,240 Creditors 10,978 12,495 13,494 14,328 15,788 17,791 Other current liabilities 4,043 4,711 4,245 4,568 5,084 5,748 Total current liabilities 15,021 17,205 17,739 18,896 20,873 23,539 Net current assets 17,614 24,860 28,350 30,238 33,556 37,701 Total assets 47,313 56,427 62,018 68,029 73,870 80,157

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 16: Cash flow Y/E March (Rsmn) FY13 FY14 FY15 FY16E FY17E FY18E EBIT 4,831 7,088 8,005 7,848 9,580 11,254 (Inc.)/dec. in working capital (2,895) (7,439) (4,320) (2,394) (3,073) (3,992) Cash flow from operations 1,937 (351) 3,685 5,454 6,507 7,262 Other income 806 694 932 998 832 836 Depreciation 2,043 2,252 2,124 2,553 2,808 3,040 Deferred liabilities (131) 377 36 587 754 941 Interest paid (-) (3,153) (3,545) (3,946) (3,872) (4,126) (4,247) Tax paid (-) (3) (548) (1,072) (1,488) (1,886) (2,353) Dividends paid (-) (498) (708) (768) (783) (813) (844) Share in profit/(loss) of

i ( P&L)3 13 35 (26) (10) (10)

Net cash from operations 1,003 (1,814) 1,026 3,424 4,066 4,625 Capital expenditure (-) (3,157) (3,630) (4,074) (6,676) (5,331) (5,182) Net cash after capex (2,154) (5,444) (3,048) (3,252) (1,265) (557) Inc./(dec.) in short-term b i

1,044 1,909 3,554 2,100 700 700 Inc./(dec.) in long-term b i

2,281 3,403 486 700 800 - Inc./(dec.) in borrowings 3,325 5,312 4,041 2,800 1,500 700 (Inc.)/dec. in investments (318) (490) (151) - - - Minority interest 17 134 105 26 10 10 Equity issue/(buyback) - - - - - - Cash from fin.activities 3,023 4,957 3,995 2,826 1,510 710 Others 278 295 (1,233) - - - Opening cash balance 709 1,856 1,663 833 328 572 Closing cash balance 1,856 1,663 833 328 572 725 Change in cash balance 1,147 (193) (830) (506) 245 153

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 18: Key ratios

Y/E March FY13 FY14 FY15 FY16E FY17E FY18E Per share (Rs) EPS 9.6 14.3 15.3 13.3 17.0 21.2 Book value 87.4 100.1 105.5 115.5 129.4 147.3 Valuation (x) P/E 29.9 20.0 18.8 21.6 16.9 13.6 P/sales 1.4 1.1 0.9 0.9 0.8 0.7 P/BV 3.3 2.9 2.7 2.5 2.2 2.0 EV/EBITDA 14.0 10.8 10.5 10.6 9.0 7.8 Return ratio (%) RoCE (Post tax) 12.7 13.0 11.5 9.6 10.5 11.3 RoCE (Pre tax) 12.7 15.1 15.2 13.8 15.0 16.2 RoE 11.6 15.3 14.9 12.1 13.9 15.3 Margin ratio (%) Gross margin 57.9 54.5 55.5 55.5 56.2 56.4 EBITDA margin 13.0 13.6 12.9 12.5 13.4 13.7 PBIT margin 9.1 10.3 10.2 9.4 10.4 10.8 PBT margin 4.7 5.9 5.7 5.9 6.8 7.5 PAT margin 4.7 5.4 5.0 4.1 4.7 5.2 Turnover ratio Asset turnover ratio (x) 1.1 1.2 1.3 1.2 1.3 1.3 Avg inventory period (days) 110 99 97 93 93 93 Avg collection period (days) 59 53 53 61 60 59 Avg payment period (days) 86 76 71 71 71 71 Ex-cash WC (% of sales) 29.8 33.8 35.0 36.0 35.7 35.4 Solvency ratios (x) Debt-equity 1.1 1.2 1.2 1.2 1.1 1.0 Interest coverage 1.5 2.0 2.0 2.0 2.3 2.6 Debt/EBITDA 3.6 3.2 3.4 3.5 3.1 2.7 Growth(%) Sales 7.5 29.7 14.4 5.8 11.3 13.0 EBITDA 14.1 35.9 8.4 2.7 19.1 15.4 PAT 1.5 49.1 6.8 (12.9) 27.4 24.8 Source: Company, Nirmal Bang Institutional Equities Research

10

Institutional Equities

Arvind

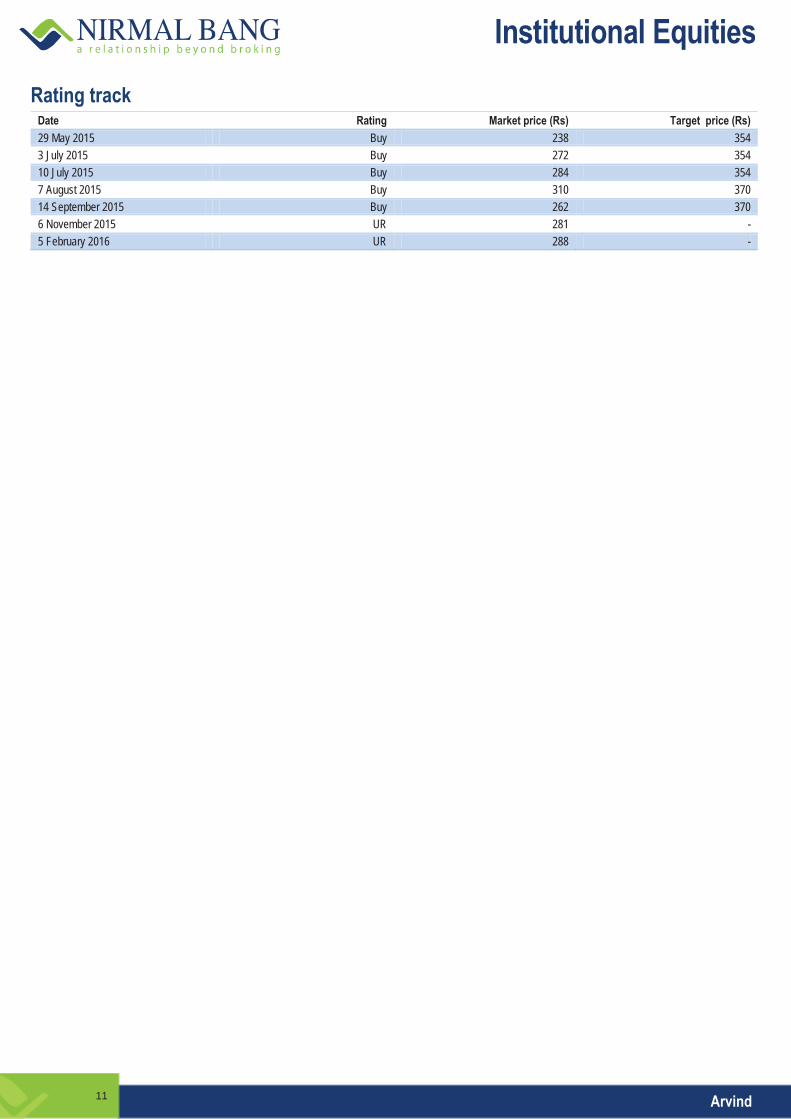

Rating track Date Rating Market price (Rs) Target price (Rs) 29 May 2015 Buy 238 354 3 July 2015 Buy 272 354 10 July 2015 Buy 284 354 7 August 2015 Buy 310 370 14 September 2015 Buy 262 370 6 November 2015 UR 281 - 5 February 2016 UR 288 -

11

Institutional Equities3Q

FY16

Res

ult U

pdate

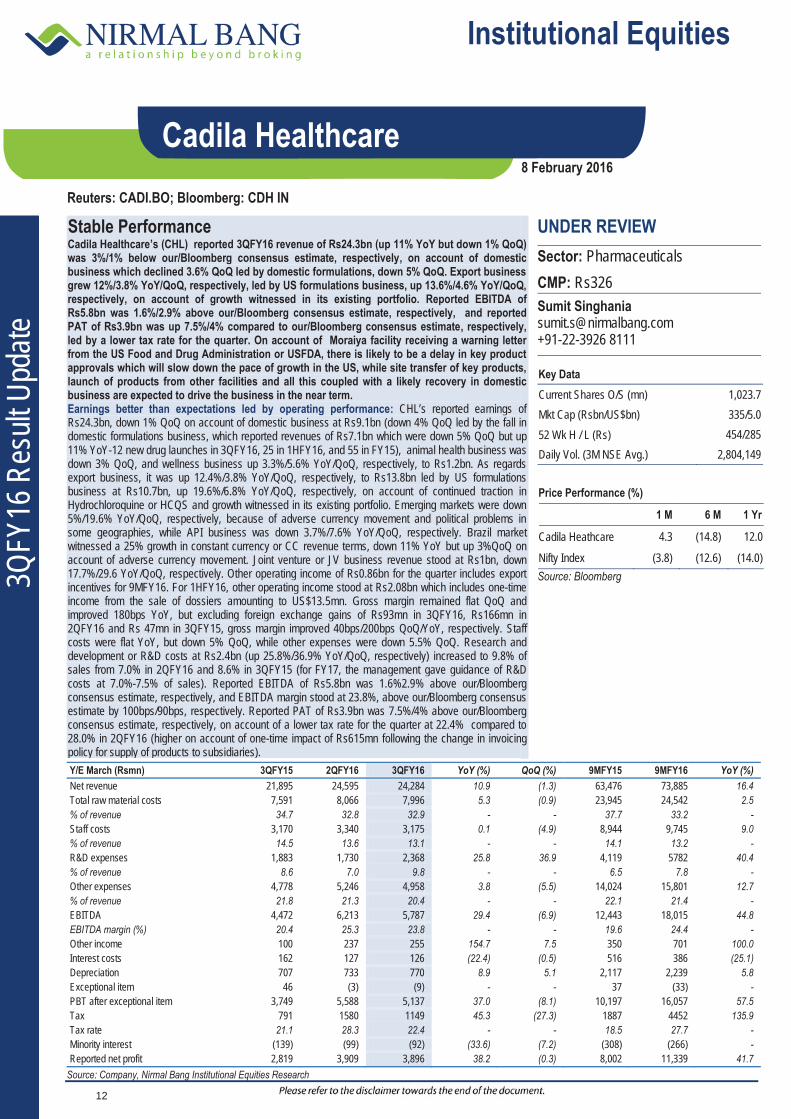

Reuters: CADI.BO; Bloomberg: CDH IN

Cadila Healthcare 8 February 2016

Stable Performance Cadila Healthcare’s (CHL) reported 3QFY16 revenue of Rs24.3bn (up 11% YoY but down 1% QoQ) was 3%/1% below our/Bloomberg consensus estimate, respectively, on account of domestic business which declined 3.6% QoQ led by domestic formulations, down 5% QoQ. Export business grew 12%/3.8% YoY/QoQ, respectively, led by US formulations business, up 13.6%/4.6% YoY/QoQ, respectively, on account of growth witnessed in its existing portfolio. Reported EBITDA of Rs5.8bn was 1.6%/2.9% above our/Bloomberg consensus estimate, respectively, and reported PAT of Rs3.9bn was up 7.5%/4% compared to our/Bloomberg consensus estimate, respectively, led by a lower tax rate for the quarter. On account of Moraiya facility receiving a warning letter from the US Food and Drug Administration or USFDA, there is likely to be a delay in key product approvals which will slow down the pace of growth in the US, while site transfer of key products, launch of products from other facilities and all this coupled with a likely recovery in domestic business are expected to drive the business in the near term. Earnings better than expectations led by operating performance: CHL’s reported earnings of Rs24.3bn, down 1% QoQ on account of domestic business at Rs9.1bn (down 4% QoQ led by the fall in domestic formulations business, which reported revenues of Rs7.1bn which were down 5% QoQ but up 11% YoY-12 new drug launches in 3QFY16, 25 in 1HFY16, and 55 in FY15), animal health business was down 3% QoQ, and wellness business up 3.3%/5.6% YoY/QoQ, respectively, to Rs1.2bn. As regards export business, it was up 12.4%/3.8% YoY/QoQ, respectively, to Rs13.8bn led by US formulations business at Rs10.7bn, up 19.6%/6.8% YoY/QoQ, respectively, on account of continued traction in Hydrochloroquine or HCQS and growth witnessed in its existing portfolio. Emerging markets were down 5%/19.6% YoY/QoQ, respectively, because of adverse currency movement and political problems in some geographies, while API business was down 3.7%/7.6% YoY/QoQ, respectively. Brazil market witnessed a 25% growth in constant currency or CC revenue terms, down 11% YoY but up 3%QoQ on account of adverse currency movement. Joint venture or JV business revenue stood at Rs1bn, down 17.7%/29.6 YoY/QoQ, respectively. Other operating income of Rs0.86bn for the quarter includes export incentives for 9MFY16. For 1HFY16, other operating income stood at Rs2.08bn which includes one-time income from the sale of dossiers amounting to US$13.5mn. Gross margin remained flat QoQ and improved 180bps YoY, but excluding foreign exchange gains of Rs93mn in 3QFY16, Rs166mn in 2QFY16 and Rs 47mn in 3QFY15, gross margin improved 40bps/200bps QoQ/YoY, respectively. Staff costs were flat YoY, but down 5% QoQ, while other expenses were down 5.5% QoQ. Research and development or R&D costs at Rs2.4bn (up 25.8%/36.9% YoY/QoQ, respectively) increased to 9.8% of sales from 7.0% in 2QFY16 and 8.6% in 3QFY15 (for FY17, the management gave guidance of R&D costs at 7.0%-7.5% of sales). Reported EBITDA of Rs5.8bn was 1.6%2.9% above our/Bloomberg consensus estimate, respectively, and EBITDA margin stood at 23.8%, above our/Bloomberg consensus estimate by 100bps/90bps, respectively. Reported PAT of Rs3.9bn was 7.5%/4% above our/Bloomberg consensus estimate, respectively, on account of a lower tax rate for the quarter at 22.4% compared to 28.0% in 2QFY16 (higher on account of one-time impact of Rs615mn following the change in invoicing policy for supply of products to subsidiaries).

UNDER REVIEW Sector: Pharmaceuticals CMP: Rs326 Sumit Singhania [email protected] +91-22-3926 8111

Key Data Current Shares O/S (mn) 1,023.7 Mkt Cap (Rsbn/US$bn) 335/5.0 52 Wk H / L (Rs) 454/285 Daily Vol. (3M NSE Avg.) 2,804,149 Price Performance (%)

1 M 6 M 1 Yr

Cadila Heathcare 4.3 (14.8) 12.0

Nifty Index (3.8) (12.6) (14.0) Source: Bloomberg

Y/E March (Rsmn) 3QFY15 2QFY16 3QFY16 YoY (%) QoQ (%) 9MFY15 9MFY16 YoY (%) Net revenue 21,895 24,595 24,284 10.9 (1.3) 63,476 73,885 16.4 Total raw material costs 7,591 8,066 7,996 5.3 (0.9) 23,945 24,542 2.5 % of revenue 34.7 32.8 32.9 - - 37.7 33.2 - Staff costs 3,170 3,340 3,175 0.1 (4.9) 8,944 9,745 9.0 % of revenue 14.5 13.6 13.1 - - 14.1 13.2 - R&D expenses 1,883 1,730 2,368 25.8 36.9 4,119 5782 40.4 % of revenue 8.6 7.0 9.8 - - 6.5 7.8 - Other expenses 4,778 5,246 4,958 3.8 (5.5) 14,024 15,801 12.7 % of revenue 21.8 21.3 20.4 - - 22.1 21.4 - EBITDA 4,472 6,213 5,787 29.4 (6.9) 12,443 18,015 44.8 EBITDA margin (%) 20.4 25.3 23.8 - - 19.6 24.4 - Other income 100 237 255 154.7 7.5 350 701 100.0 Interest costs 162 127 126 (22.4) (0.5) 516 386 (25.1) Depreciation 707 733 770 8.9 5.1 2,117 2,239 5.8 Exceptional item 46 (3) (9) - - 37 (33) - PBT after exceptional item 3,749 5,588 5,137 37.0 (8.1) 10,197 16,057 57.5 Tax 791 1580 1149 45.3 (27.3) 1887 4452 135.9 Tax rate 21.1 28.3 22.4 - - 18.5 27.7 - Minority interest (139) (99) (92) (33.6) (7.2) (308) (266) - Reported net profit 2,819 3,909 3,896 38.2 (0.3) 8,002 11,339 41.7

Source: Company, Nirmal Bang Institutional Equities Research 12

Institutional Equities

Cadila Healthcare

Other highlights 1) CHL has given tax rate guidance of 24% FY16 and around 20% for FY17. 2) As regards Moraiya unit, which received a warning letter from the US Food and Drug Administration or

USFDA in December 2015, the management highlighted that post implementation of remedial measures there could be a re-inspection by the USFDA to get the site cleared. This unit has around 74 abbreviated new drug applications or ANDAs awaiting approval.

3) CHL has secured approval for transfer of 11 of its existing products from Moraiya plant (received warning letter) to its other plant in Baddi. Of these11, the company has started commercial production in case of 9 products. Approvals for new products involving site transfer from Moraiya plant to other plants are expected to take around three to six months.

4) As far as the site transfers for key products like Asacol HD and Prevacid ODT are concerned, the company has initiated the process of site transfer.

5) The company has the option to launch Asacol HD AG in the market by July 2016. If it chooses to launch this product, then it will not be able to launch generic Asacol under 180-day marketing exclusivity.

6) Apart from Moraiya unit, the company also got a warning letter from the USFDA for its Ahmedabad-based API facility in December 2015.

7) The management expects to get around 15 ANDAs from the USFDA in FY17, primarily for its Baddi and SEZ facilities.

8) The company currently has 60 products in the US market. It has 90 product approvals. 9) In 3QFY16, the company filed for 20 products, in 2QFY16 it filed for 4 products while 6 filings were done in

1QFY16.The company expects to file for around 40 products in FY17. These filings will be for products from Baddi and SEZ facilities.

10) Other than Moraiya unit, the plant at Baddi does not have any sterile and injectable facilities and therefore the company is coming up with a new plant having the said facilities in Baroda. The construction of the new plant is complete and it is expected to go on stream in June/July of 2017. The filings from this plant will commence in FY17.

11) Gross debt stood at Rs24bn, net debt at 13.8bn and cash at Rs10.6bn.

Exhibit 1: Financial summary Y/E March (Rsmn) FY14 FY15 FY16E FY17E FY18E Revenue 72,240 86,513 100,893 113,753 130,397 YoY (%) 13.6 19.8 16.6 12.7 14.6 EBITDA 12,001 17,578 23,925 24,451 28,664 EBITDA (%) 16.6 20.3 23.7 21.5 22.0 Reported PAT 8,036 11,506 15,373 16,280 19,382 Adj. PAT 8,189 11,591 15,373 16,280 19,382 YoY (%) 25.3 41.5 32.6 5.9 19.1 Fully DEPS 8.0 11.3 15.0 15.9 18.9 RoE (%) 25.7 30.1 31.7 26.7 25.9 RoCE (%) 16.0 21.8 27.0 23.4 24.1 P/E (x) 41.6 29.0 21.7 20.5 17.2 EV/EBITDA (x) 29.6 20.1 14.6 14.2 11.9

Source: Company, Nirmal Bang Institutional Equities Research

13

Institutional Equities

Cadila Healthcare

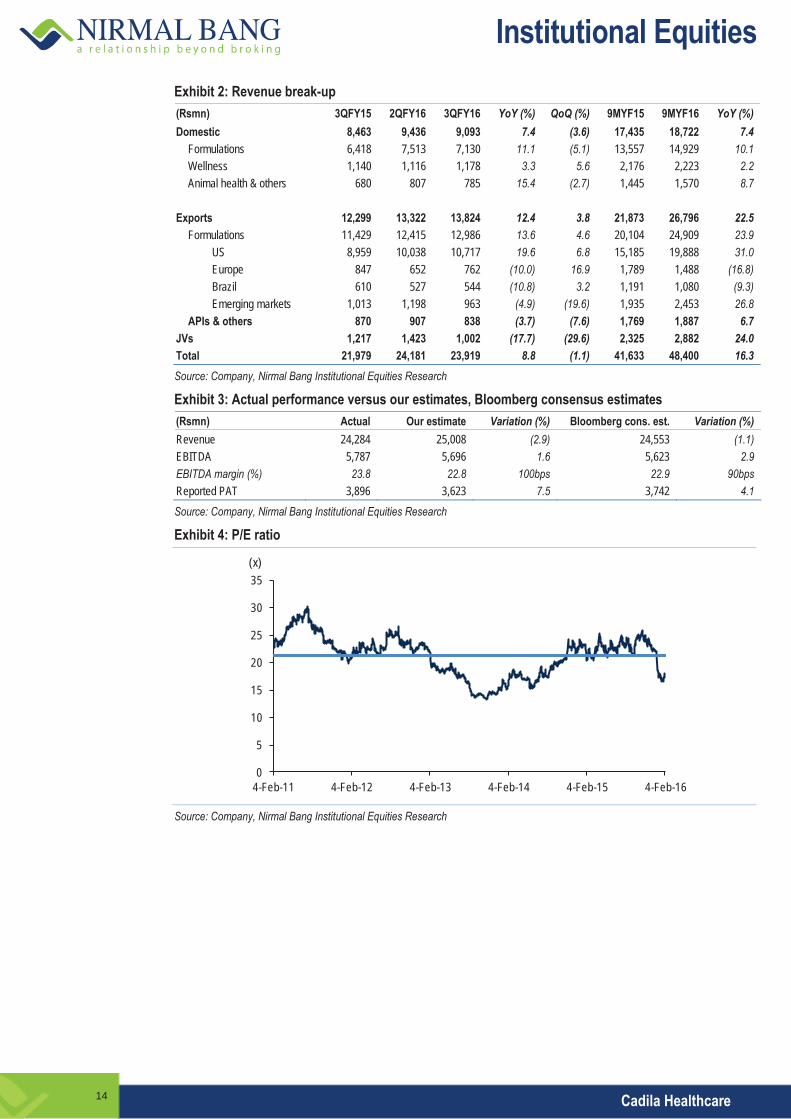

Exhibit 2: Revenue break-up (Rsmn) 3QFY15 2QFY16 3QFY16 YoY (%) QoQ (%) 9MYF15 9MYF16 YoY (%) Domestic 8,463 9,436 9,093 7.4 (3.6) 17,435 18,722 7.4

Formulations 6,418 7,513 7,130 11.1 (5.1) 13,557 14,929 10.1 Wellness 1,140 1,116 1,178 3.3 5.6 2,176 2,223 2.2 Animal health & others 680 807 785 15.4 (2.7) 1,445 1,570 8.7

Exports 12,299 13,322 13,824 12.4 3.8 21,873 26,796 22.5

Formulations 11,429 12,415 12,986 13.6 4.6 20,104 24,909 23.9 US 8,959 10,038 10,717 19.6 6.8 15,185 19,888 31.0 Europe 847 652 762 (10.0) 16.9 1,789 1,488 (16.8) Brazil 610 527 544 (10.8) 3.2 1,191 1,080 (9.3) Emerging markets 1,013 1,198 963 (4.9) (19.6) 1,935 2,453 26.8

APIs & others 870 907 838 (3.7) (7.6) 1,769 1,887 6.7 JVs 1,217 1,423 1,002 (17.7) (29.6) 2,325 2,882 24.0 Total 21,979 24,181 23,919 8.8 (1.1) 41,633 48,400 16.3 Source: Company, Nirmal Bang Institutional Equities Research Exhibit 3: Actual performance versus our estimates, Bloomberg consensus estimates (Rsmn) Actual Our estimate Variation (%) Bloomberg cons. est. Variation (%) Revenue 24,284 25,008 (2.9) 24,553 (1.1) EBITDA 5,787 5,696 1.6 5,623 2.9 EBITDA margin (%) 23.8 22.8 100bps 22.9 90bps Reported PAT 3,896 3,623 7.5 3,742 4.1

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 4: P/E ratio

Source: Company, Nirmal Bang Institutional Equities Research

0

5

10

15

20

25

30

35

4-Feb-11 4-Feb-12 4-Feb-13 4-Feb-14 4-Feb-15 4-Feb-16

(x)

14

Institutional Equities

Cadila Healthcare

Financials Exhibit 5: Income statement Y/E March (Rsmn) FY14 FY15 FY16E FY17E FY18E Net sales (incl. other oper. income) 72,240 86,513 100,893 113,753 130,397 % growth 13.6 19.8 16.6 12.7 14.6 Raw material costs (27,136) (31,966) (29,715) (35,499) (40,057) Staff costs (10,711) (12,085) (14,127) (16,085) (18,439) Research & development exp. (4,608) (5,607) (7,307) (8,320) (9,537) Other expenses (17,784) (19,277) (25,818) (29,397) (33,699) Total expenditure (60,239) (68,935) (76,967) (89,302) (101,732) EBITDA 12,001 17,578 23,925 24,451 28,664 % growth 6.7 46.5 36.1 2.2 17.2 EBITDA margin (%) 16.6 20.3 23.7 21.5 22.0 Other income 507 554 792 902 1,034 Interest costs (902) (679) (765) (735) (705) Gross profit 11,606 17,453 23,952 24,618 28,993 % growth 16.8 50.4 37.2 2.8 17.8 Depreciation (2,012) (2,873) (3,099) (3,639) (4,017) Profit before tax 9,594 14,580 20,853 20,979 24,976 % growth 18.6 52.0 43.0 0.6 19.1 Tax (1,060) (2,594) (5,005) (4,196) (4,995) Effective tax rate (%) 11.0 17.8 24.0 20.0 20.0 Minority interest (326) (376) (475) (504) (599) Net profit 8,036 11,506 15,373 16,280 19,382 % growth 23.0 43.2 33.6 5.9 19.1 Adj. profit 8,189 11,591 15,373 16,280 19,382 % growth 25.3 41.5 32.6 5.9 19.1

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 7: Balance sheet Y/E March (Rsmn) FY14 FY15 FY16E FY17E FY18E Equity 1,024 1,024 1,024 1,024 1,024 Reserves 33,366 41,493 53,523 66,263 81,431 Net worth 34,390 42,517 54,547 67,287 82,454 Total loans 27,004 26,513 25,513 24,513 23,513 Deferred tax liability 961 586 586 586 586 Minority interest 1,444 1,690 2,163 2,664 3,260 Total liabilities 63,799 71,305 82,808 95,048 109,811 Gross block 46,640 51,385 57,385 67,385 74,385 Depreciation 15,402 17,863 20,962 24,601 28,617 Net block 31,238 33,522 36,423 42,784 45,768 Capital work-in-progress 8,915 7,979 7,979 7,979 7,979 Long-term Investments 866 1,544 1,544 1,544 1,544 Inventories 13,675 15,357 18,685 21,275 24,736 Debtors 11,337 15,884 18,685 21,275 24,388 Cash 5,488 6,699 9,495 10,994 17,210 Other current assets 8,347 9,487 10,774 12,169 13,846 Total current assets 38,847 47,427 57,638 65,714 80,181 Creditors 9,108 10,909 12,180 14,132 16,099 Other current liabilities 6,959 8,258 8,596 8,841 9,562 Total current liabilities 16,067 19,167 20,776 22,973 25,662 Net current assets 22,780 28,260 36,862 42,741 54,519 Total assets 63,799 71,305 82,808 95,048 109,811

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 6: Cash flow Y/E March (Rsmn) FY14 FY15 FY16E FY17E FY18E EBIT 9,989 14,705 20,827 20,812 24,648 (Inc.)/dec. in working capital (1,703) (4,900) (6,113) (4,577) (6,237) Cash flow from operations 8,286 9,805 14,713 16,235 18,411 Other income 507 554 792 902 1,034 Depreciation 2,012 2,873 3,099 3,639 4,017 Interest paid (-) (902) (679) (765) (735) (705) Tax paid (-) (1,060) (2,594) (5,005) (4,196) (4,995) Dividends paid (-) (1,875) (2,268) (3,038) (3,345) (3,542) Net cash from operations 6,968 7,691 9,796 12,500 14,219 Capital expenditure (-) (4,437) (3,809) (6,000) (10,000) (7,000) Net cash after capex 2,531 3,882 3,796 2,500 7,219 Inc./(dec.) in long-term borrowing (2,174) (491) (1,000) (1,000) (1,000) Inc./(dec.) in borrowings (2,174) (491) (1,000) (1,000) (1,000) (Inc.)/dec. in investments 279 (678) - - - Cash from financial activities (1,895) (1,169) (1,000) (1,000) (1,000) Others (986) (1,502) - - - Opening cash balance 5,838 5,488 6,699 9,495 10,994 Closing cash balance 5,488 6,699 9,495 10,994 17,210 Change in cash balance (350) 1,211 2,796 1,499 6,216

Source: Company, Nirmal Bang Institutional Equities Research Exhibit 8: Key ratios Y/E March FY14 FY15 FY16E FY17E FY18E Per share (Rs) Reported EPS 7.8 11.2 15.0 15.9 18.9 Adjusted EPS 8.0 11.3 15.0 15.9 18.9 DPS 2.0 2.6 2.7 2.9 3.4 BV/share 33.6 41.5 53.3 65.7 80.5 Dividend payout (%) 30.7 29.6 21.7 21.7 21.7 Performance ratios (%) RoE 25.7 30.1 31.7 26.7 25.9 RoCE 16.0 21.8 27.0 23.4 24.1 Valuation ratios (x) P/E 41.6 29.0 21.7 20.5 17.2 P/BV 9.7 7.9 6.1 5.0 4.1 EV/net sales 4.9 4.1 3.5 3.1 2.6 EV/EBITDA 29.6 20.1 14.6 14.2 11.9 Efficiency ratios Asset turnover (x) 1.1 1.3 1.3 1.2 1.2 Working capital/sales (x) 0.4 0.4 0.4 0.4 0.5 Receivable days 58.6 68.2 70.0 70.0 70.0 Inventory days 70.7 66.0 70.0 70.0 71.0 Payable days 59.8 62.9 63.8 63.7 63.7

Source: Company, Nirmal Bang Institutional Equities Research

15

Institutional Equities3Q

FY16

Res

ult U

pdate

Reuters: DIVI.BO; Bloomberg: DIVI IN

Divis Laboratories 8 February 2016

Weak Performance Led By Lower Revenue Growth Divis Laboratories (DLL) reported a weak set of numbers for 3QFY16, which were below expectations, with reported PAT of Rs2.5bn 10% below our/Bloomberg consensus estimate each, following lower revenue growth, which was 5%/9% below our/Bloomberg consensus estimate, respectively, at Rs8.5bn. Revenue growth was weak because of shipments deferred to the next quarter. EBITDA of Rs3.2bn was 7%/11% below our/Bloomberg consensus estimate, respectively. Reported EBITDA margin of 37.8% was down 40bps/60bps versus our/Bloomberg consensus estimate, respectively. We continue to remain sanguine on DLL led by ramp-up at its DSN unit continuing coupled with future revenue growth set to kick in on account of newly announced capacity addition and expansion, reaffirming our stance that a 20% growth over next few years is likely. Earnings below expectation led by subdued revenue growth: DLL reported earnings of Rs2.5bn, 10% below our/Bloomberg consensus estimate each, led by lower revenue growth which was 5%/9% below our/Bloomberg consensus estimate, respectively, at Rs8.5bn. Revenue growth was weak because of shipments deferred to the next quarter. Generics business revenue of Rs4.1bn was down 14% QoQ, and custom synthesis (CS) business revenue of Rs3.8bn was down 11% QoQ. Revenue from carotenoids segment stood at Rs550mn compared to Rs460mn in 2QFY16 and Rs370mn in 3QFY15, up 49%/20% YoY/QoQ, respectively. The broad-based split between generics and (CS) businesses was 55% and 45%, respectively, in 3QFY16, which was the same for the previous quarter as well, while it was 54% and 46% in 3QFY15, respectively. For 9 months of FY16, the split was 55% and 45%, respectively. Reported EBITDA of Rs3.2bn was 7%/11% below our/Bloomberg consensus estimate, respectively. EBITDA margin for the quarter was 37.8%, 120bps down QoQ and 40bps/60bps down compared to our/Bloomberg consensus estimate, respectively. EBITDA for the quarter was down on account of lower revenue growth during the quarter, higher staff costs (up 22%/6% YoY/QoQ, respectively) and other expenses (up 10%/4% YoY/QoQ, respectively) although gross margin for the quarter improved 310bps/280bps YoY/QoQ, respectively, implying better margins from CS business. Other income was down 24%/49% YoY/QoQ, respectively, on account of lower forex gains amounting to Rs29.4mn compared to a gain of Rs116.6mn in 2QFY16 and Rs110mn in 3QFY15. Tax rate for the quarter was down at 19.8% compared to 21.2% in 2QFY16 and 20.6% in 3QFY15. The management has given guidance that the tax rate for FY16 will be 21%-22% and 22%-23% for FY17. Other highlights: a) For 9MFY16, DLL capitalised fixed assets to the tune of Rs1.8bn. b) For the new plant to be set up at Kakinada, DLL earmarked Rs5bn, but the capex is delayed and will now be incurred equally over the next two years. c) DLL will also expand its Vizag unit for which an additional capex of Rs2.5bn is earmarked to be spent in FY17E. d) DLL has retained its guidance of a 15%-20% revenue growth for FY16.

UNDER REVIEW Sector: Pharmaceuticals CMP: Rs1,110

Sumit Singhania [email protected] +91-22-3926 8111

Key Data Current Shares O/S (mn) 265.5 Mkt Cap (Rsbn/US$bn) 291.1/4.3 52 Wk H / L (Rs) 1,242/786 Daily Vol. (3M NSE Avg.) 304,522

Price Performance (%) 1 M 6 M 1 Yr

Divis Labs (4.4) 9.8 35.2 Nifty Index (3.8) (12.6) (14.0) Source: Bloomberg

Y/E March (Rsmn) 3QFY15 2QFY16 3QFY16 YoY (%) QoQ (%) 9MFY15 9MFY16 YoY (%) Net revenue 7,911 9,643 8,529 7.8 (11.6) 22,669 26,260 15.8 Raw material costs 3,186 3,854 3,175 (0.4) (17.6) 9,182 10,234 11.5 % of net revenue 40.3 40.0 37.2 - - 40.5 39.0 - Staff costs 746 860 912 22.2 6.1 2,043 2,575 26.1 % of net revenue 9.4 8.9 10.7 - - 9.0 9.8 - Other expenses 1,108 1,170 1,219 10.1 4.2 3,155 3,470 10.0 % of net revenue 14.0 12.1 14.3 - - 13.9 13.2 - EBITDA 2,871 3,760 3,223 12.3 (14.3) 8,291 9,981 20.4 EBITDA margin (%) 36.3 39.0 37.8 150bps (120bps) 36.6 38.0 (140bps) Other income 199 296 152 (23.8) (48.7) 482 788 63.6 Interest costs 5 3 2 (52.1) (32.4) 13 8 (37.8) Depreciation 288 301 299 3.8 (0.6) 913 889 (2.7) PBT 2,778 3,752 3,074 10.7 (18.1) 7,847 9,873 25.8 Tax 572 795 608 6.4 (23.5) 1,665 2,018 21.2 Tax rate (%) 20.6 21.2 19.8 - - 21.2 20.4 - Reported PAT 2,206 2,957 2,466 11.8 (16.6) 6,182 7,855 27.1

*Standalone numbers; Source: Company, Nirmal Bang Institutional Equities Research

16

Institutional Equities

Divis Laboratories

Exhibit 1: Financial summary (consolidated) Y/E March (Rsmn) FY14 FY15 FY16E FY17E FY18E Revenue 25,187 30,959 37,832 45,398 54,478 YoY (%) 18.9 22.9 22.2 20.0 20.0 EBITDA 10,391 11,491 14,565 17,251 20,702 EBITDA (%) 41.3 37.1 38.5 38.0 38.0 Reported PAT 7,733 8,515 10,943 12,841 15,615 YoY (%) 28.5 10.1 28.5 17.4 21.6 Fully DEPS 29.1 32.1 41.2 48.4 58.8 RoE (%) 28.3 26.4 28.5 28.0 28.5 RoCE (%) 33.2 30.0 33.4 33.0 33.6 P/E (x) 38.1 34.6 26.9 23.0 18.9 EV/EBITDA (x) 14.2 12.8 10.1 8.5 7.1 Source: Company, Nirmal Bang Institutional Equities Research Exhibit 2: Actual performance versus our estimates, Bloomberg consensus estimates Particulars (Rsmn) Actual Our estimate Variation (%) Bloomberg cons.est. Variation (%) Revenue 8,529 9,018 (5.4) 9,372 (9.0) EBITDA 3,223 3,447 (6.5) 3,603 (10.6) EBITDA margin (%) 37.8 38.2 (40 bps) 38.4 (60 bps) Reported PAT 2,466 2,737 (9.9) 2,737 (9.9)

Source: Bloomberg, Company, Nirmal Bang Institutional Equities Research

Exhibit 3: P/E ratio

Source: Bloomberg, Nirmal Bang Institutional Equities Research

0

5

10

15

20

25

30

4-Feb-11 4-Feb-12 4-Feb-13 4-Feb-14 4-Feb-15 4-Feb-16

(x)

17

Institutional Equities

Divis Laboratories

Financials Exhibit 4: Income statement Y/E March (Rsmn) FY14 FY15 FY16E FY17E FY18E Net sales (incl. other operating income) 25,187 30,959 37,832 45,398 54,478 % growth 18.9 22.9 22.2 20.0 20.0 Raw material costs (9,142) (12,132) (13,809) (16,797) (20,157) Staff costs (2,325) (2,904) (3,405) (4,086) (4,903) R&D expenses (254) (277) (378) (454) (545) Other expenses (3,076) (4,155) (5,675) (6,810) (8,172) Total expenditure (14,796) (19,468) (23,267) (28,147) (33,776) EBITDA 10,391 11,491 14,565 17,251 20,702 % growth 29.7 10.6 26.8 18.4 20.0 EBITDA margin (%) 41.3 37.1 38.5 38.0 38.0 Other income 469 619 709 827 1125 Interest costs (30) (29) (19) (19) (19) Gross profit 10,830 12,081 15,255 18,060 21,808 % growth 26.2 11.5 26.3 18.4 20.8 Depreciation (921) (1,360) (1,227) (1,597) (1,789) Profit before tax 9,909 10,721 14,029 16,463 20,019 % growth 26.8 8.2 30.9 17.4 21.6 Tax (2,176) (2,206) (3,086) (3,622) (4,404) Effective tax rate (%) 22.0 20.6 22.0 22.0 22.0 Net profit 7,733 8,515 10,943 12,841 15,615 % growth 28.5 10.1 28.5 17.4 21.6

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 6: Balance sheet Y/E March (Rsmn) FY14 FY15 FY16E FY17E FY18E Equity 265 265 265 265 265 Reserves 29,368 34,688 41,569 49,643 59,462 Net worth 29,634 34,954 41,834 49,909 59,728 Short-term loans 163 251 251 251 251 Long-term loans 21 16 16 16 16 Total loans 184 266 266 266 266 Deferred tax liability 1,150 1,262 1,262 1,262 1,262 Liabilities 30,968 36,482 43,363 51,437 61,256 Gross block 17,403 19,530 24,530 29,030 32,530 Depreciation 5,185 6,441 7,668 9,264 11,054 Net block 12,218 13,089 16,862 19,766 21,477 Capital work-in-progress 1,560 2,396 996 996 996 Long-term investments 5,019 7,330 8,830 10,330 14,830 Inventories 9,324 11,626 14,207 17,049 20,459 Debtors 7,237 7,416 9,063 10,875 13,051 Cash 405 652 620 697 175 Other current assets 1,342 1,541 1,863 2,217 2,642 Total current assets 18,308 21,236 25,754 30,838 36,327 Creditors 2,857 2,492 3,046 3,655 4,386 Other current liabilities 3,280 5,077 6,034 6,838 7,987 Total current liabilities 6,137 7,569 9,080 10,493 12,373 Net current assets 12,171 13,667 16,674 20,345 23,954 Total assets 30,968 36,482 43,363 51,437 61,256

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 5: Cash flow Y/E March (Rsmn) FY14 FY15 FY16E FY17E FY18E EBIT 9,470 10,131 13,339 15,655 18,913 (Inc.)/dec. in working capital (3,220) (1,338) (3,906) (4,300) (5,160) Cash flow from operations 6,249 8,793 9,433 11,355 13,753 Other income 469 619 709 827 1,125 Depreciation 921 1,360 1,227 1,597 1,789 Interest paid (-) (30) (29) (19) (19) (19) Tax paid (-) (2,176) (2,206) (3,086) (3,622) (4,404) Dividend (-) (2,329) (3,106) (3,195) (4,062) (4,767) Net cash from operations 3,105 5,431 5,068 6,076 7,479 Capital expenditure (-) (2,347) (2,963) (3,600) (4,500) (3,500) Net cash after capex 758 2,468 1,468 1,576 3,979 Inc./(dec.) in short-term borrowing (142) 87 - - - Inc./(dec.) in long-term borrowing (5) (5) - - - Inc./(dec.) in borrowings (146) 82 - - - (Inc.)/dec. in investments (941) (2,311) (1,500) (1,500) (4,500) Cash from financial activities (1,087) (2,229) (1,500) (1,500) (4,500) Others 325 8 Opening cash balance 409 405 652 620 697 Closing cash balance 405 652 620 697 175 Change in cash balance (4) 247 (32) 76 (521)

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 7: Key ratios Y/E March FY14 FY15 FY16E FY17E FY18E Per share (Rs) Reported EPS 29.1 32.1 41.2 48.4 58.8 Adjusted EPS 29.1 32.1 41.2 48.4 58.8 DPS 20.0 20.0 26.4 31.0 37.6 BV/share 111.6 131.7 157.6 188.0 225.0 Dividend payout (%) 40.2 37.5 37.1 37.1 37.1 Performance ratios RoE (%) 28.3 26.4 28.5 28.0 28.5 RoCE (%) 33.2 30.0 33.4 33.0 33.6 Valuation ratios P/E (x) 38.1 34.6 26.9 23.0 18.9 P/BV (x) 5.0 4.2 3.5 3.0 2.5 EV/net sales (x) 5.8 4.7 3.9 3.2 2.7 EV/EBITDA (x) 14.2 12.8 10.1 8.5 7.1 Efficiency ratios Fixed asset turnover (x) 1.3 1.4 1.5 1.5 1.6 Working capital/sales (x) 0.6 0.5 0.5 0.5 0.5 Receivable days 105 87 87 87 87 Inventory days 135 137 137 137 137 Payable days 41 29 29 29 29

Source: Company, Nirmal Bang Institutional Equities Research

18

Institutional Equities3Q

FY16

Res

ult U

pdate

Reuters: LKMC.BO; Bloomberg: LMW IN

Lakshmi Machine Works

Yet Another Quarter of Positive Surprise; Retain Buy Lakshmi Machine Works (LMW) posted 3QFY16 performance that was better than our expectations. We are positively surprised by revenue traction in all segments coupled with margin expansion. Strong revenue and margin performance was led by higher exports in 3QFY16. Exports witnessed a YoY growth of 12.4% in 9MFY16 to Rs3.89bn. However, exports in 1HFY16 were down 19% YoY to Rs1.88bn. 3QFY16 witnessed a bounce-back in exports with a 77% YoY growth to Rs2.01bn (31% of total net revenue) which resulted in YoY export growth turning positive in 9MFY16. Textile machinery division (TMD) registered an export growth of 17% YoY in 9MFY16 at Rs3.65bn and occupied a major share of 94% in total exports. In 3QFY16, total net revenue witnessed an increase of 14.7% YoY to Rs6,516mn, mainly on account of a 12.3% growth in TMD revenue which constituted 88% of revenue at Rs5,787mn. EBITDA registered a 27.8% surge with a 143bps YoY expansion in EBITDA margin to 14.1% (our estimate 12.7%). The YoY expansion in gross margin by 66bps to 40.4% (our estimate 39.4%) coupled with ~70bps YoY fall in other expenses as a percentage of revenue led to EBITDA margin expansion. The YoY decline of 31% in depreciation to Rs176.7mn (our estimate was an amount similar to a year ago – Rs256.1mn), a 427bps reduction in tax rate to 32.9% (our estimate – reduction of 418bps) resulted in a strong YoY growth of 41.8% in PAT to Rs634.9mn (our estimate – Rs445.5mn) along with a 186bps YoY expansion in PAT margin to 9.7% (our estimate- 7.6%). We have increased our revenue and PAT estimates for FY16 by 6% and 15%, respectively, to factor in the latest developments. However, by and large we have retained our FY17 revenue and PAT estimates. Market share, order book, exports and spare part sales: LMW maintained its domestic revenue market share at 60%-61% as of end-December 2015. LMW’s domestic order book (OB) stood at Rs25.8bn with a strong flow of export enquiries worth Rs2.7bn as of end-December2015. Project orders accounted for 65% of domestic order book and slow-moving orders have been reduced to 30% of order book. The company witnessed order inflow of Rs11bn in 9MFY16. Our estimate on order inflow stands revised upwards to Rs14.5bn for FY16. Total exports in 9MFY16 stood at Rs3.89bn against Rs3.46bn in the corresponding period a year ago and the current enquiry pipeline is to the extent of Rs2.67bn. LMW reported spare part sales amounting to Rs2.20bn in 9MFY16, which was in line with our annual estimate of Rs2.85bn. Retain Buy rating on LMW: We are positive on LMW on account of its strong financial health (debt-free status, positive free cash flow and huge cash on its books), strong management pedigree, market leadership status and export focus. LMW will continue to provide a high margin of safety and economic moat to investors. We expect LMW to cumulatively generate net operating cash flow of Rs10bn over FY16E-FY18E. We have rolled forward our valuation to FY18E EPS. We have retained Buy rating on LMW with a target price of Rs4,688, valuing the stock at 19x FY18E EPS of Rs247.

BUY Sector: Capital Goods CMP: Rs3,490 Target Price: Rs4,688 Upside: 34% Sameer Panke [email protected] +91-22-3926 8114

Key Data Current Shares O/S (mn) 11.3Mkt Cap (Rsbn/US$mn) 39.3/581.352 Wk H / L (Rs) 4,199/3,275Daily Vol. (3M NSE Avg.) 4,383 Price Performance (%)

1 M 6 M 1 Yr LMW (3.3) (11.7) (7.0) Nifty Index (3.8) (12.6) (14.0) Source: Bloomberg

Y/E March (Rsmn) 3QFY15 2QFY16 3QFY16 Chg. (YoY)% Chg. QoQ)% 9MFY15 9MFY16 Chg. (YoY)% Net sales 5,680 6,198 6,516 14.7 5.1 17,288 18,356 6.2 Raw materials consumed 3,420 3,890 3,884 13.6 (0.2) 10,574 11,116 5.1 % of sales 60.2 62.8 59.6 - - 61.2 60.6 - Employee costs 533 586 602 12.9 2.7 1,694 1,752 3.5 % of sales 9.4 9.5 9.2 - - 9.8 9.5 - Other expenditure 1,008 1,001 1,113 10.3 11.2 2,869 3,192 11.3 % of sales 17.8 16.1 17.1 - - 16.6 17.4 - EBITDA 719 721 918 27.8 27.3 2,151 2,296 6.7 EBITDA (%) 12.7 11.6 14.1 - - 12.4 12.5 - Other income 255 286 208 (18.2) (27.2) 786 735 (6.6) Exceptional items 2 2 1 (32.6) (26.2) 76 7 (90.9) Interest costs 2 1 2 (3.2) 94.2 6 4 (40.8) Depreciation 257 193 177 (31.1) (8.6) 731 602 (17.7) PBT 713 811 946 32.8 16.6 2,124 2,418 13.9 Total tax 265 247 311 17.5 26.3 722 780 8.0 Effective tax rate (%) 37.2 30.4 32.9 - - 34.0 32.3 - Net profit (+) / loss (-) 448 565 635 41.8 12.4 1,402 1,638 16.9 NPM (%) 7.9 9.1 9.7 - - 8.1 8.9 - Source: Company, Nirmal Bang Institutional Equities Research

8 February 2016

19

Institutional Equities

Lakshmi Machine Works

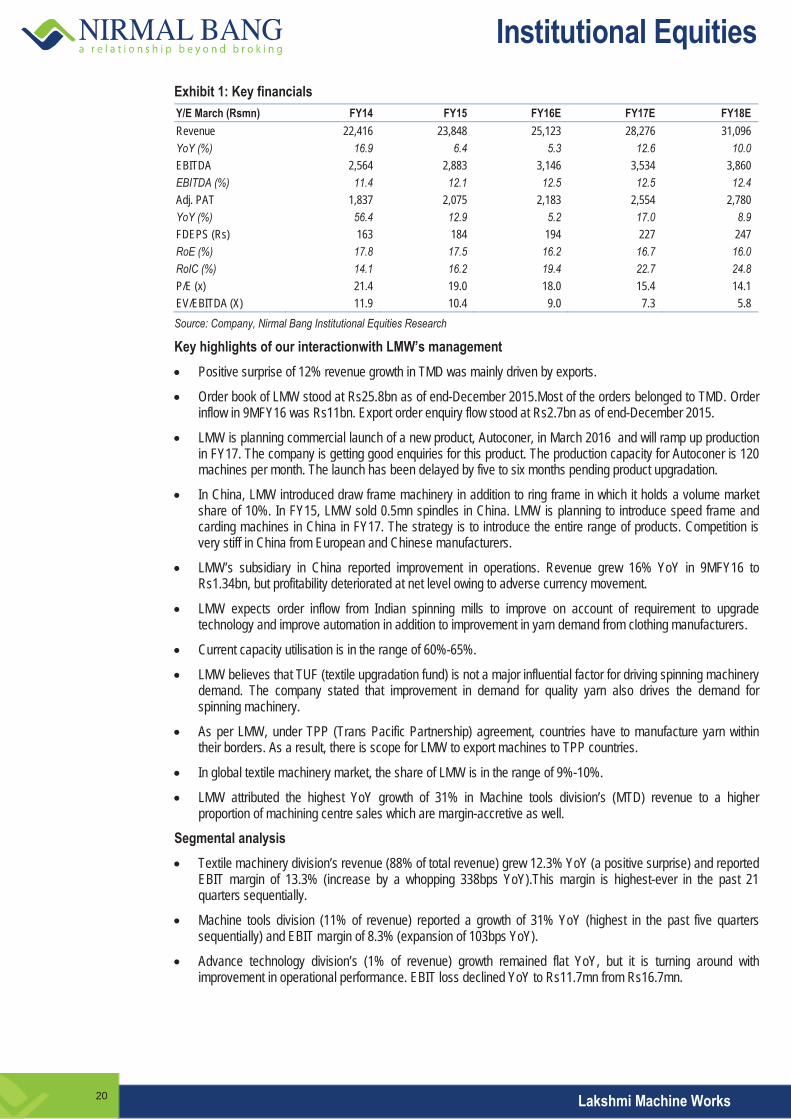

Exhibit 1: Key financials Y/E March (Rsmn) FY14 FY15 FY16E FY17E FY18E Revenue 22,416 23,848 25,123 28,276 31,096 YoY (%) 16.9 6.4 5.3 12.6 10.0 EBITDA 2,564 2,883 3,146 3,534 3,860 EBITDA (%) 11.4 12.1 12.5 12.5 12.4 Adj. PAT 1,837 2,075 2,183 2,554 2,780 YoY (%) 56.4 12.9 5.2 17.0 8.9 FDEPS (Rs) 163 184 194 227 247 RoE (%) 17.8 17.5 16.2 16.7 16.0 RoIC (%) 14.1 16.2 19.4 22.7 24.8 P/E (x) 21.4 19.0 18.0 15.4 14.1 EV/EBITDA (X) 11.9 10.4 9.0 7.3 5.8 Source: Company, Nirmal Bang Institutional Equities Research

Key highlights of our interactionwith LMW’s management Positive surprise of 12% revenue growth in TMD was mainly driven by exports.

Order book of LMW stood at Rs25.8bn as of end-December 2015.Most of the orders belonged to TMD. Order inflow in 9MFY16 was Rs11bn. Export order enquiry flow stood at Rs2.7bn as of end-December 2015.

LMW is planning commercial launch of a new product, Autoconer, in March 2016 and will ramp up production in FY17. The company is getting good enquiries for this product. The production capacity for Autoconer is 120 machines per month. The launch has been delayed by five to six months pending product upgradation.

In China, LMW introduced draw frame machinery in addition to ring frame in which it holds a volume market share of 10%. In FY15, LMW sold 0.5mn spindles in China. LMW is planning to introduce speed frame and carding machines in China in FY17. The strategy is to introduce the entire range of products. Competition is very stiff in China from European and Chinese manufacturers.

LMW’s subsidiary in China reported improvement in operations. Revenue grew 16% YoY in 9MFY16 to Rs1.34bn, but profitability deteriorated at net level owing to adverse currency movement.

LMW expects order inflow from Indian spinning mills to improve on account of requirement to upgrade technology and improve automation in addition to improvement in yarn demand from clothing manufacturers.

Current capacity utilisation is in the range of 60%-65%.

LMW believes that TUF (textile upgradation fund) is not a major influential factor for driving spinning machinery demand. The company stated that improvement in demand for quality yarn also drives the demand for spinning machinery.

As per LMW, under TPP (Trans Pacific Partnership) agreement, countries have to manufacture yarn within their borders. As a result, there is scope for LMW to export machines to TPP countries.

In global textile machinery market, the share of LMW is in the range of 9%-10%.

LMW attributed the highest YoY growth of 31% in Machine tools division’s (MTD) revenue to a higher proportion of machining centre sales which are margin-accretive as well.

Segmental analysis Textile machinery division’s revenue (88% of total revenue) grew 12.3% YoY (a positive surprise) and reported EBIT margin of 13.3% (increase by a whopping 338bps YoY).This margin is highest-ever in the past 21 quarters sequentially.

Machine tools division (11% of revenue) reported a growth of 31% YoY (highest in the past five quarters sequentially) and EBIT margin of 8.3% (expansion of 103bps YoY).

Advance technology division’s (1% of revenue) growth remained flat YoY, but it is turning around with improvement in operational performance. EBIT loss declined YoY to Rs11.7mn from Rs16.7mn.

20

Institutional Equities

Lakshmi Machine Works

Exhibit 2: Segment-wise snapshot Y/E March (Rsmn) 3QFY15 2QFY16 3QFY16 Chg.

(YoY)% Chg.

(QoQ)% 9MFY15 9MFY16 Chg. (YoY)%

Segment Revenue Textile machinery division (TMD) 5,154 5,590 5,787 12.3 3.5 15,603 16,446 5.4 Machine tools and foundry division (MTD) 562 680 739 31.4 8.6 1,837 1,977 7.6 Advance technology division (ATD) 59 47 58 (0.8) 25.0 134 177 31.5 Sub-total 5,775 6,316 6,584 14.0 4.2 17,574 18,600 5.8 Less : Inter-segmental revenue 39 52 46 19.9 (11.6) 103 132 28.7 Net sales/income from operations 5,736 6,264 6,538 14.0 4.4 17,472 18,468 5.7 Segment-wise profit from operations Textile machinery division (TMD) 512 591 770 50.5 30.2 1,532 1,796 17.2 Machine tools and foundry division (MTD) 41 67 61 50.2 (8.7) 154 171 11.4 Advance technology division (ATD) (17) (26) (12) - - (97) (50) - Total segmental profit 536 633 819 53.0 29.5 1,589 1,917 20.6 Add: Other non-allocable income net of non-allocable expenditure 177 179 127 (28.5) (29.1) 534 501 (6.2) Profit before tax 713 811 946 32.8 16.6 2,124 2,418 13.9 Capital employed Textile machinery division (TMD) 8,769 9,977 10,611 21.0 6.4 8,769 10,611 21.0 Machine tools and foundry division (MTD) 2,301 2,215 2,255 (2.0) 1.8 2,301 2,255 (2.0) Advance technology division (ATD) 41 66 73 77.5 10.7 41 73 77.5 Unallocated 1,336 1,350 1,303 (2.4) (3.5) 1,336 1,303 (2.4) Total capital employed 12,446 13,608 14,243 14.4 4.7 12,446 14,243 14.4 Segment-wise revenue share Textile machinery division (TMD) 89.2 88.5 87.9 - - 88.8 88.4 - Machine tools and foundry division (MTD) 9.7 10.8 11.2 - - 10.5 10.6 - Advance technology division (ATD) 1.1 0.7 0.9 - - 0.8 1.0 - Margin (%) EBIT margin - textile machinery division (TMD) 9.9 10.6 13.3 - - 9.8 10.9 - EBIT margin - machine tools and foundry division (MTD) 7.2 9.8 8.3 - - 8.4 8.7 - EBIT margin - advance technology division (ATD) (28.5) (54.9) (20.1) - - (71.9) (28.5) -

Source: Company, Nirmal Bang Institutional Equities Research Exhibit 3: Actual performance versus our estimates Y/E March (Rsmn) 3QFY15 2QFY16 3QFY16 Chg. (YoY)% Chg. QoQ)% 3QFY16E Devi (%) Revenue 5,680 6,198 6,516 14.7 5.1 5,855 11.3 EBITDA 719 721 918 27.8 27.3 744 23.5 EBITDA (%) 12.7 11.6 14.1 143bps 245bps 12.7 139bps Reported PAT 448 565 635 41.8 12.4 446 42.5

Source: Company, Bloomberg, Nirmal Bang Institutional Equities Research

Exhibit 4: Change in our earnings estimates Y/E March Old New Variation (%) (Rsmn) FY16E FY17E FY16E FY17E FY16E FY17E Revenue 23,672 28,245 25,123 28,276 6.1 0.1 EBITDA 2,792 3,539 3,146 3,534 12.7 (0.1) EBITDA (%) 11.8 12.5 12.5 12.5 73bps (3bps) Reported PAT 1,895 2,541 2,183 2,554 15.2 0.5

Source: Company, Bloomberg, Nirmal Bang Institutional Equities Research

21

Institutional Equities

Lakshmi Machine Works

Exhibit 5: P/E trend

Source: NSE, Nirmal Bang Institutional Equities Research

0

5

10

15

20

25

30

35

Feb-

05Au

g-05

Feb-

06Au

g-06

Feb-

07Au

g-07

Feb-

08Au

g-08

Feb-

09Au

g-09

Feb-

10Au

g-10

Feb-

11Au

g-11

Feb-

12Au

g-12

Feb-

13Au

g-13

Feb-

14Au

g-14

Feb-

15Au

g-15

Feb-

16

(x)

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Feb-

05Au

g-05

Feb-

06Au

g-06

Feb-

07Au

g-07

Feb-

08Au

g-08

Feb-

09Au

g-09

Feb-

10Au

g-10

Feb-

11Au

g-11

Feb-

12Au

g-12

Feb-

13Au

g-13

Feb-

14Au

g-14

Feb-

15Au

g-15

Feb-

16

Stock price 10x 15x 20x 25x 30x

(Rs)

22

Institutional Equities

Lakshmi Machine Works

Financials Exhibit 6: Income statement Y/E March (Rsmn) FY14 FY15 FY16E FY17E FY18E Net revenue from segments 21,652 23,126 24,580 27,667 30,415 Other operating income 764 722 543 610 681 Revenue from operations 22,416 23,848 25,123 28,276 31,096 Other income 1,155 1,063 929 1,158 1,218 Total revenue 23,571 24,912 26,052 29,435 32,314 Cost of raw material consumed 14,216 14,761 15,365 17,260 19,054 Change in inventories (270) (93) (119) (67) (176) Employee benefits expenses 2,269 2,277 2,441 2,901 3,109 Other expenses 3,637 4,020 4,290 4,649 5,249 Total expenses 19,853 20,965 21,977 24,742 27,236 EBITDA (incl. OI) 3,719 3,946 4,075 4,692 5,078 EBITDA (excl. OI) 2,564 2,883 3,146 3,534 3,860 Depreciation 1,025 965 901 1,006 1,090 EBIT (excl.OI) 1,539 1,918 2,246 2,528 2,770 Financial charges and interest

t6 6 10 13 19

PBT (before exceptional items) 2,688 2,975 3,164 3,673 3,969 Exceptional item - VRS 82 95 10 10 10 PBT 2,606 2,880 3,154 3,663 3,959 Total tax 769 805 971 1,110 1,179 Current tax 879 991 1,049 1,218 1,316 Deferred tax (net) (103) (121) (75) (103) (132) Prior-year tax (8) (65) (3) (6) (5) Profit after tax 1,837 2,075 2,183 2,554 2,780

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 8: Balance sheet Y/E March (Rsmn) FY14 FY15 FY16E FY17E FY18E Share capital 113 113 113 113 113 Reserves and surplus 10,932 12,492 14,166 16,177 18,414 Networth 11,044 12,605 14,279 16,290 18,527 Non-current liabilities 2,258 1,345 1,201 1,323 1,337 Deferred tax liabilities (net) 26 - - - - Other long-term liabilities 2,232 1,345 1,201 1,323 1,337 Current liabilities 6,924 7,769 6,625 7,379 8,276 Trade payables 2,921 3,092 3,157 3,594 3,967 Other current liabilities 3,539 4,074 2,898 3,179 3,702 Short-term provisions 463 603 570 605 607 Total liabilities 20,226 21,719 22,105 24,992 28,141 Total gross block 16,775 17,486 17,836 18,166 18,496 Accumulated depreciation 12,946 13,745 14,645 15,651 16,741 Net fixed assets 3,829 3,741 3,190 2,514 1,755 Capital work in progress 27 31 15 15 15 Non-current investments 1,288 1,288 1,288 1,288 1,288 Deferred tax assets - 97 97 97 97 Long-term loans and advances 224 236 257 251 194 Current assets 14,857 16,324 17,257 20,826 24,792 Inventories 2,806 2,887 3,008 3,228 3,537 Trade receivables 1,828 2,206 2,271 2,479 2,726 Cash and carry equivalents 8,794 9,416 11,028 13,559 17,001 Short-term loans and advances 928 1,386 588 1,068 1,023 Other current assets 502 430 361 491 504 Total assets 20,226 21,719 22,105 24,992 28,141

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 7: Cash flow Y/E March (Rsmn) FY14 FY15 FY16E FY17E FY18E EBIT (excl. OI) 1,539 1,917.9 2,246 2,528 2,770 Exceptional item (-) (82) (94.9) (10) (10) (10) (Inc.)/dec. in working capital (464) (284) 374 Cash flow from operations 1,107 1,823.6 1,771 2,234 3,134 Other income 1,155 1,063.3 929 1,158 1,218 Depreciation 1,025 965.0 901 1,006 1,090 Tax paid (-) (769) (805.5) (971) (1,110) (1,179) Inc/(dec.) other long-term liabilities - (886.9) (144) 123 14 Long-term assets (-) - (12.6) (20) 6 57 Net cash from operations 2,517 2,146.9 2,465 3,417 4,333 Capital expenditure (-) (60) (714.3) (334) (330) (330) Net cash after capex 2,457 1,432.6 2,131 3,087 4,003 Interest paid (-) (6) (6.3) (10) (13) (19) Dividends paid (-) (395) (508.5) (509) (543) (543) (Inc.)/dec. in investments (250) 0.0 - - - Cash from financial activities (651) (514.9) (519) (556) (562) Others (509) (295.5) - - - Opening cash balance 7,497 8,793.9 9,416 11,028 13,559 Closing cash balance 8,794 9,416.2 11,028 13,559 17,001 Change in cash balance 1,297 622.3 1,612 2,531 3,442

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 9: Key ratios Y/E March FY14 FY15 FY16E FY17E FY18E Per share (Rs) EPS 163.0 184.1 193.8 226.7 246.8 CEPS (Rs.) 254.0 269.8 273.7 316.0 343.5 BV 980.3 1118.8 1267.4 1445.9 1644.4 DPS 30.0 37.5 37.5 40.0 40.0 Dividend payout (%) 18.4 20.4 19.4 17.6 16.2 Valuation (x) P/E (x) 21.4 19.0 18.0 15.4 14.1 P/BV (x) 3.6 3.1 2.8 2.4 2.1 EV/EBDITA (x) 11.9 10.4 9.0 7.3 5.8 M.cap/ sales (x) 1.8 1.6 1.6 1.4 1.3 EV/sales (x) 1.4 1.3 1.1 0.9 0.7 Return ratios (%) RoANW 17.8 17.5 16.2 16.7 16.0 RoACE 8.1 9.1 10.3 10.8 10.5 RoAIC 14.1 16.2 19.4 22.7 24.8 Margins (%) EBITDA margin (excl. O.I.) 11.4 12.1 12.5 12.5 12.4 EBITDA margin (incl. O.I.) 16.6 16.5 16.2 16.6 16.3 EBIT margin 6.9 8.0 8.9 8.9 8.9 Tax/PBT 29.5 28.0 30.8 30.3 29.8 Net profit margin 8.2 8.7 8.7 9.0 8.9 Expense ratios (% of revenue) Cost of raw materials consumed 62 62 61 61 61 Employee benefit expenses 10 10 10 10 10 Total expenses 89 88 87 88 88 Turnover and working capital ratios Debtors period (days) 30 34 33 32 32 Inventory period (days) 57 56 56 53 53 Creditor period (days) 75 76 75 76 76 Cash conversion cycle (days) 12 13 14 9 9 Fixed asset turnover (x) 1.3 1.4 1.4 1.6 1.7 Working capital turnover (x) 3.2 2.9 2.6 2.3 2.1 Non-cash working capital (Rsmn) (860.2) (860.8) (396.3) (112.0) (485.8)

Source: Company, Nirmal Bang Institutional Equities Research

23

Institutional Equities

Lakshmi Machine Works

Rating track Date Rating Market price (Rs) Target price (Rs) 6 February 2015 Buy 3,793 4,725 22 May 2015 Buy 3,676 4,725 11 August 2015 Buy 3,657 4,725 6 October 2015 Buy 3,644 4,725 4 November 2015 Buy 3,701 4,725 5 February 2016 Buy 3,490 4,688

24

Institutional Equities3Q

FY16

Res

ult U

pdate

Reuters: LUPN.BO; Bloomberg: LPC IN

Lupin 8 February 2016