in cooperation with the netherlands institute of … · in cooperation with the netherlands...

TRANSCRIPT

Transparency Benchmark 2015The Crystal 2015

In cooperation with the Netherlands Institute of Chartered Accountants (NBA)

Transparency Benchmark 2015 The Crystal 2015 1

Transparency Benchmark 2015The Crystal 2015

In cooperation with the Netherlands Institute of Chartered Accountants (NBA)

Transparency Benchmark 2015 The Crystal 20152

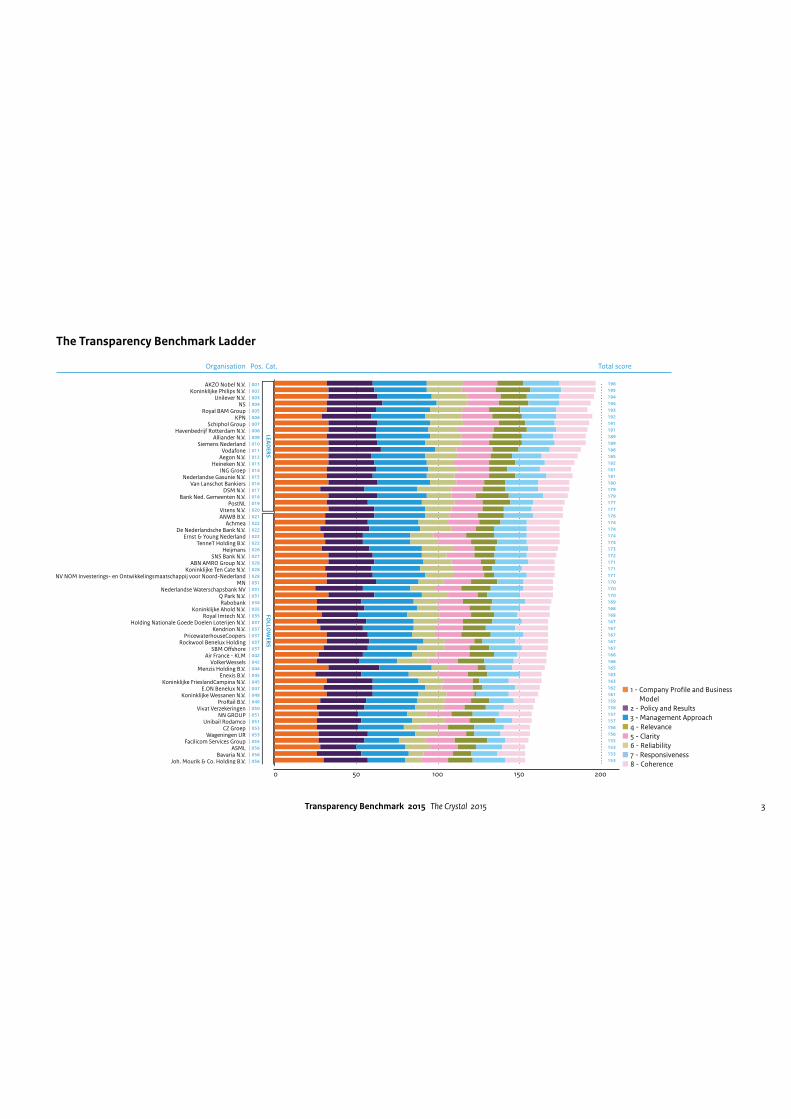

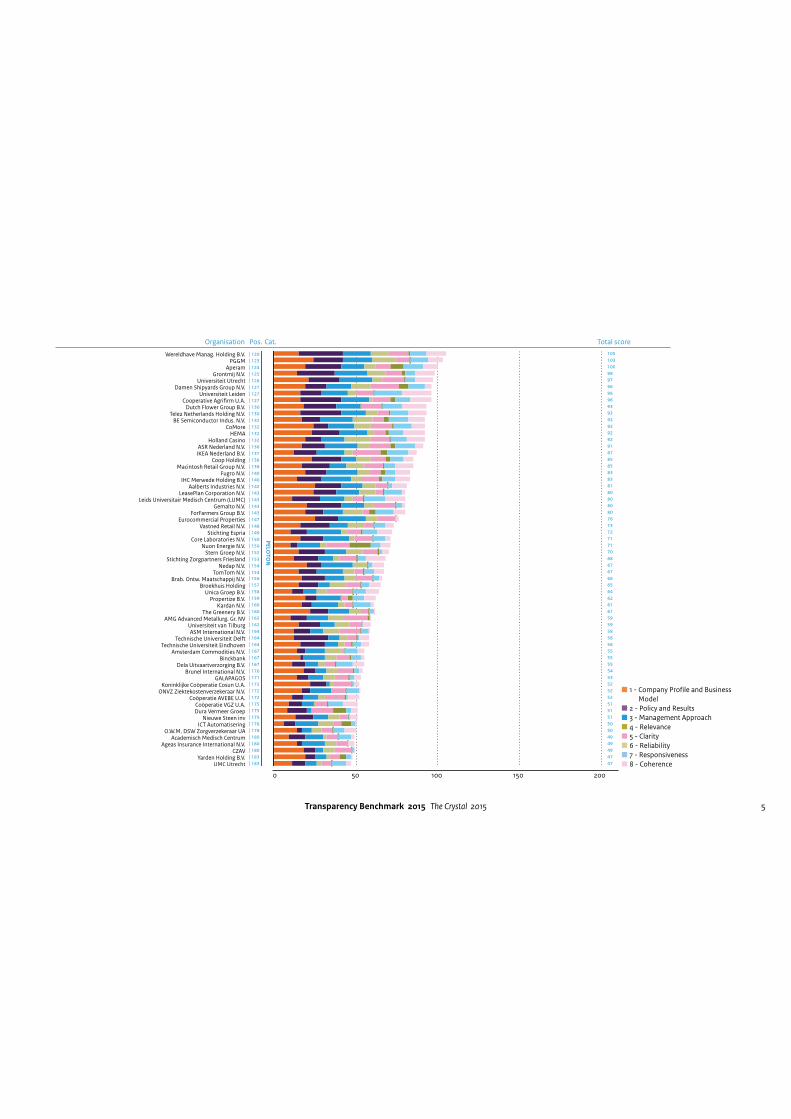

1 The Transparency Benchmark Ladder

The Transparency Benchmark Ladder provides an overview of the total scores of the participating organizations, including the sub scores

concerning 8 different criteria categories. The organizations that are included in the Transparency Benchmark are ranked in different groups:

Frontrunners, Followers, Peloton, Laggards and organizations with zero scores

Category transparancy ladder 2015 Ranking Positions

Leaders 1 - 20

Followers 21 - 70

Peloton 71 - 213

Laggards 214 - 245

Organisations with zero scores 246 - 461

Transparency Benchmark 2015 The Crystal 2015 3

1 - Company Profile and Business

Model

2 - Policy and Results

3 - Management Approach

4 - Relevance

5 - Clarity

6 - Reliability

7 - Responsiveness

8 - Coherence

The Transparency Benchmark Ladder

TMG - Telegraaf Media GroepJoh. Mourik & Co. Holding B.V.

Bavaria N.V.ASML

Facilicom Services GroupWageningen UR

CZ GroepUnibail Rodamco

NN GROUPVivat Verzekeringen

ProRail B.V.Koninklijke Wessanen N.V.

E.ON Benelux N.V.Koninklijke FrieslandCampina N.V.

Enexis B.V.Menzis Holding B.V.

VolkerWesselsAir France - KLM

SBM OdshoreRockwool Benelux Holding

PricewaterhouseCoopersKendrion N.V.

Holding Nationale Goede Doelen Loterijen N.V.Royal Imtech N.V.

Koninklijke Ahold N.V.Rabobank

Q Park N.V.Nederlandse Waterschapsbank NV

MNNV NOM Investerings- en Ontwikkelingsmaatschappij voor Noord-Nederland

Koninklijke Ten Cate N.V.ABN AMRO Group N.V.

SNS Bank N.V.Heijmans

TenneT Holding B.V.Ernst & Young Nederland

De Nederlandsche Bank N.V.Achmea

ANWB B.V.Vitens N.V.

PostNLBank Ned. Gemeenten N.V.

DSM N.V.Van Lanschot Bankiers

Nederlandse Gasunie N.V.ING Groep

Heineken N.V.Aegon N.V.Vodafone

Siemens NederlandAlliander N.V.

Havenbedrijf Ro_erdam N.V.Schiphol Group

KPNRoyal BAM Group

NSUnilever N.V.

Koninklijke Philips N.V.AKZO Nobel N.V. | 001

| 002| 003| 004| 005| 006| 007| 008| 009| 010| 011| 012| 013| 014| 015| 016| 017| 018| 019| 020| 021| 022| 022| 022| 022| 026| 027| 028| 028| 028| 031| 031| 031| 034| 035| 035| 037| 037| 037| 037| 037| 042| 042| 044| 045| 045| 047| 048| 049| 050| 051| 051| 053| 053| 055| 056| 056| 056| 056

196195194194193192191191189189186185182181181180179179177177176174174174174173172171171171170170170169168168167167167167167166166165163163162161159158157157156156155153153153153

LE

AD

ER

SF

OL

LO

WE

RS

0 50 100 150 200

Organisation Pos. Cat. Total score

Transparency Benchmark 2015 The Crystal 20154

1 - Company Profile and Business

Model

2 - Policy and Results

3 - Management Approach

4 - Relevance

5 - Clarity

6 - Reliability

7 - Responsiveness

8 - CoherenceWereldhave Manag. Holding B.V.

Roto Smeets Group N.V.PLUS Retail B.V.

Vos Logistics Beheer B.V.GVB Holding NV

Van OordStichting Exploitatie Nederlandse Staatsloterij

Waterweg WonenVreugdenhil Groep B.V.

Arcadis N.V.Vebego International N.V.

Sligro Food Group N.V.TNO

Universiteit TwenteBallast Nedam N.V.

Universiteit MaastrichtBeter Bed Holding N.V.

COVRA NVBidvest Deli XL

Corbion N.V.Wolters Kluwer N.V.

DOW Benelux B.V.Atradius N.V.

Universiteit van AmsterdamRijksuniversiteit Groningen

Delta Lloyd GroepRadboudumc

USG People N.V.Wavin N.V.

VimpelCom Ltd.TKH Group N.V.

Ontwikkelingsmaatschappij Oost Nederland NVVanDrie Group

TNT ExpressKoninklijke Vopak N.V.Albron Nederland B.V.

Beelen Groep B.V.Perfe_i v. Melle

N.V. HVCNidera B.V.

Zeeman Groep B.V.TBI Holdings

Industriebank LIOF N.V.EBN

Royal HaskoningDHVRELX Group N.V.

Jumbo Groep Holding B.V.Arla Foods B.V.

Accell GroupTUI Nederland

Randstad Holding N.V.Koninklijke Boskalis Westminster N.V.

Airbus Group N.V.Royal Dutch Shell

Nederlandse Financierings-Maatschappij voor Ontwikkelingslanden NVNutreco

Deloi_e Holding B.V.KPMG N.V.

Eneco Holding N.V.Ordina N.V.

GasTerra B.V.NIBC Bank N.V.Westland Infra

TMG - Telegraaf Media GroepJoh. Mourik & Co. Holding B.V. | 056

| 056| 056| 061| 062| 063| 064| 064| 066| 066| 068| 068| 070| 071| 072| 072| 074| 074| 074| 074| 074| 079| 079| 079| 079| 083| 084| 085| 086| 087| 087| 087| 090| 091| 092| 092| 092| 095| 095| 097| 098| 098| 100| 100| 100| 103| 104| 105| 106| 106| 108| 108| 110| 111| 111| 113| 113| 113| 116| 117| 118| 118| 120| 120| 120

153153153152151150148148147147146146144143140140139139139139139138138138138137136133132131131131130129128128128126126124122122121121121119118117116116115115114112112111111111110109108108105105105

FO

LL

OW

ER

SP

EL

OT

ON

0 50 100 150 200

Organisation Pos. Cat. Total score

Transparency Benchmark 2015 The Crystal 2015 5

1 - Company Profile and Business

Model

2 - Policy and Results

3 - Management Approach

4 - Relevance

5 - Clarity

6 - Reliability

7 - Responsiveness

8 - CoherenceUMC UtrechtYarden Holding B.V.

CZAVAgeas Insurance International N.V.

Academisch Medisch CentrumO.W.M. DSW Zorgverzekeraar UA

ICT AutomatiseringNieuwe Steen inv

Dura Vermeer GroepCoöperatie VGZ U.A.

Coöperatie AVEBE U.A.ONVZ Ziektekostenverzekeraar N.V.

Koninklijke Coöperatie Cosun U.A.GALAPAGOS

Brunel International N.V.Dela Uitvaartverzorging B.V.

BinckbankAmsterdam Commodities N.V.

Technische Universiteit EindhovenTechnische Universiteit Delb

ASM International N.V.Universiteit van Tilburg

AMG Advanced Metallurg. Gr. NVThe Greenery B.V.

Kardan N.V.Propertize B.V.

Unica Groep B.V.Broekhuis Holding

Brab. Ontw. Maatschappij N.V.TomTom N.V.

Nedap N.V.Stichting Zorgpartners Friesland

Stern Groep N.V.Nuon Energie N.V.

Core Laboratories N.V.Stichting Espria

Vastned Retail N.V.Eurocommercial Properties

ForFarmers Group B.V.Gemalto N.V.

Leids Universitair Medisch Centrum (LUMC)LeasePlan Corporation N.V.

Aalberts Industries N.V.IHC Merwede Holding B.V.

Fugro N.V.Macintosh Retail Group N.V.

Coop HoldingIKEA Nederland B.V.ASR Nederland N.V.

Holland CasinoHEMA

CoMoreBE Semiconductor Indus. N.V.

Tele2 Netherlands Holding N.V.Dutch Flower Group B.V.

Cooperative Agricrm U.A.Universiteit Leiden

Damen Shipyards Group N.V.Universiteit Utrecht

Grontmij N.V.Aperam

PGGMWereldhave Manag. Holding B.V.

Roto Smeets Group N.V.| 120| 123| 124| 125| 126| 127| 127| 127| 130| 130| 132| 132| 132| 132| 136| 137| 138| 138| 140| 140| 142| 143| 143| 143| 143| 147| 148| 149| 150| 150| 152| 153| 154| 154| 156| 157| 158| 159| 160| 160| 162| 162| 164| 164| 164| 167| 167| 167| 170| 171| 172| 172| 172| 175| 175| 175| 178| 178| 180| 180| 180| 183| 183| 185

10510310098979696969393929292929187858583838180808080767372717170686767666564626161595958585855555554535252525151515050494949474746

PE

LO

TO

N

0 50 100 150 200

Organisation Pos. Cat. Total score

Transparency Benchmark 2015 The Crystal 20156

Kramp Groep B.V.Audax B.V.

IMC TradingForbo Flooring B.V.

de Persgroep Nederland B.V.Maxeda Nederland B.V.

SHV Holdings N.V.Global City Holdings N.V.

The Royal Bank of ScotlandCimpress

Farm Frites Beheer B.V.Hertel Holding B.V.

ESPERITEVan Wijnen Groep N.V.Coöperatie Univé U.A.

VDL GroepBlokker Holding B.V.

Ultra-Centrifuge Ned. N.V.Brocacef Holding

Janssen De Jong Groep B.V.TMF Group Holding B.V.

NXP Semiconductors Netherlands B.V.Louis Dreyfus

De Goudse N.V.Exact Holding N.V.

APGDOCDATA N.V.

VION Holding N.V.DPA GROUP

Credit Europe Bank N.V.Value8

MonutaRobeco Groep N.V.

Koninklijke Brill N.V.GROOTHANDELSGEBOUW

FagronAerCap Holdings N.V.

NyenrodeB & S International B.V.

Radboud Universiteit NijmegenKAS BANK N.V.

Neways Electronics International N.V.Erasmus MCHurks groep

Oranjewoud N.V.Van Leeuwen Buizen Groep B.V

VUmcUniversitair Medisch Centrum Groningen (UMCG)

OCICentric Holding B.V.

StorkZorg en Zekerheid Groep

Euretco B.V.Erasmus Universiteit Ro_erdam

Legal & GeneralDelta N.V.

Allianz Nederland Groep N.V.Refresco Holding B.V.

Maastricht UMC+Open Universiteit

DOC KaasUMC Utrecht

| 185| 186| 187| 187| 189| 189| 189| 192| 193| 193| 195| 195| 197| 197| 197| 200| 200| 202| 203| 203| 205| 205| 207| 207| 209| 209| 209| 209| 209| 214| 215| 215| 217| 218| 219| 219| 219| 222| 222| 222| 222| 226| 227| 227| 229| 229| 231| 232| 233| 234| 234| 236| 237| 238| 239| 240| 241| 241| 243| 244| 245

46454444434343403939373736363635353433333232313130303030302928282726252525242424242322222121201918171716151413121010985

PE

LO

TO

NL

AG

GA

RD

S

Organisation Pos. Cat. Total score

Companies in the top 20 with the same rounded oU scores, were ranked based on a diUerence in decimal points, which were ultimately determined and awarded by the Panel of Experts.

1 - Company Profile and Business

Model

2 - Policy and Results

3 - Management Approach

4 - Relevance

5 - Clarity

6 - Reliability

7 - Responsiveness

8 - Coherence

0 50 100 150 200

Transparency Benchmark 2015 The Crystal 2015 7

Content

1 The Transparency Benchmark Ladder 2

2 Introduction 8

2.1 Preface 8

2.2 About this report 9

3 This year’s winners 10

4 What stands out? 11

4.1 Category comparison 11

4.2 Criteria comparison 12

4.2.1 Materiality 15

4.3 Sector comparison 18

4.3.1 Banking and insurance 19

4.3.2 Construction and maritime 20

4.3.3 Consumer products 21

4.3.4 Services 22

4.3.5 Energy, oil and gas 23

4.3.6 Trading 24

4.3.7 Industrial products 25

4.3.8 Media and communications 26

4.3.9 Pharmaceuticals 27

4.3.10 Retail 28

4.3.11 Technology 29

4.3.12 Transport 30

4.3.13 Universities and Medical Centres 31

4.3.14 Real estate 32

4.3.15 Food and beverage 33

4.3.16 Other 34

4.4 Corporate responsibility reporting in practice 35

5 In-depth theme:

The impact of Transparency 40

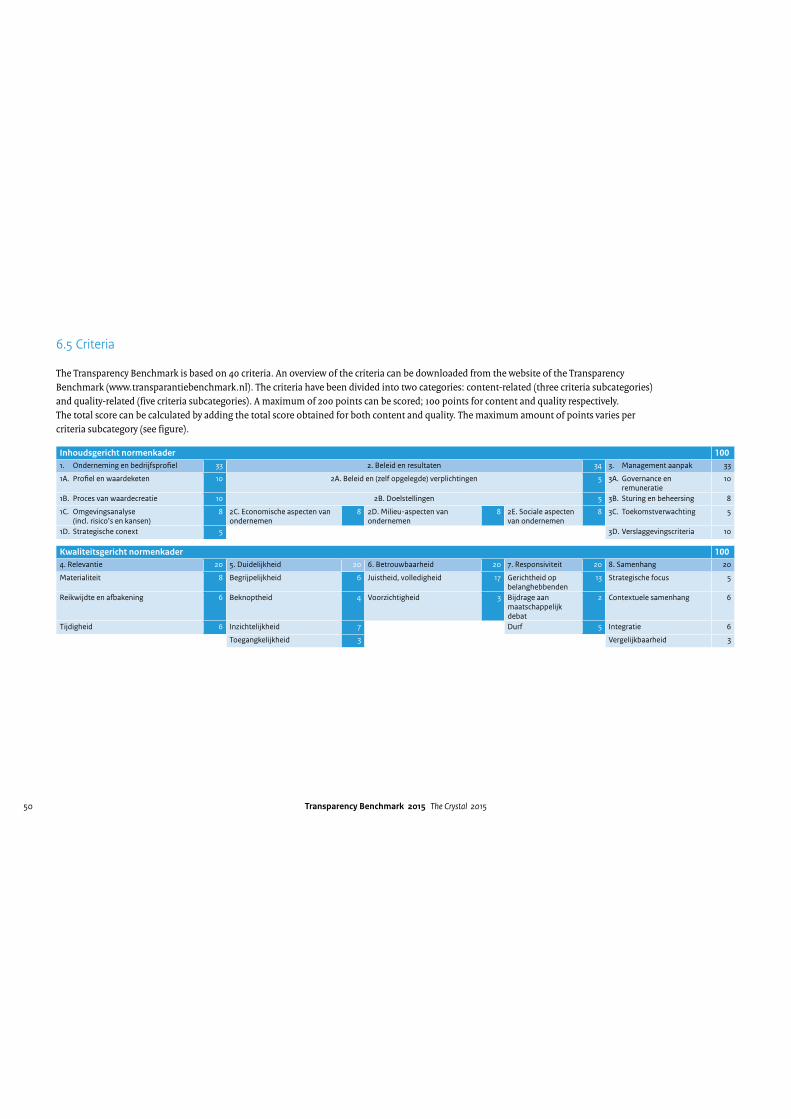

6 Explanation of the Transparency Benchmark 47

6.1 Goal 47

6.2 Differences to previous year 47

6.3 Boundary of publicly available accounting

information 48

6.4 Methodology 49

6.5 Criteria 50

6.6 Jury report 51

7 Appendices 56

7.1 New Participating organizations 56

7.2 Dutch organizations with an international

group report 59

7.3 Organizations with zero points awarded 60

7.4 Panel of Experts Transparency Benchmark 65

7.5 Jury of The Crystal 65

7.6 Literature 66

Transparency Benchmark 2015 The Crystal 20158

2 Introduction

2.1 Preface

This booklet contains the results of the Transparency Benchmark 2015, assessing organizations’ disclosures for the reporting year 2014.

The Transparency Benchmark provides insight into the degree of transparency from a corporate responsibility perspective of the 485 largest

organizations in the Netherlands.

The structure of the Transparency Benchmark 2015 is similar to the Transparency Benchmark 2014. The criteria were radically changed in 2014

to align them with the new GRI Guidelines and account for the trend in Integrated Reporting. This year, the criteria have not been changed with

regards to their content. However, some of the criteria have been redefined or provided with a supplement to enhance comprehensibility and

reduce room for interpretation. As a result of this fine-tuning, some elements of companies’ reports, which were eligible for points in 2014,

might have been rejected this year. The self-assessment methodology remained the same as last year:all organizations were invited to measure

the quality of their reports through an online self-assessment. By completing the online self-assessment, organizations obtained direct insights

into the strong elements of their report and those elements on which points were missed. The submitted answers of the self-assessment were

critically checked for accuracy by a team of researchers.

Additionally, the group of participating organizations was changed compared to last year. The executor of the Transparency Benchmark, EY,

has carefully checked the group,removing organizations that no longer belonged to the target group and adding new ones. Newly added

organizations were informed of their inclusion in the benchmark in March 2015. The participation protocol (available at www.transparantie-

benchmark.nl) describes the standards followed in defining the final participants group as well as the accounting information eligible for

obtaining points on the Transparency Benchmark Ladder.

An independent panel of experts has additionally assessed the top 20 based on their own criteria, which are also available on the website.

In addition, the website provides insights into all participating organizations and their respective scores.

The Crystal, developed in 2010 by the Ministry of Economic Affairs and the Netherlands Institute of Chartered Accountants (NBA), aims to be

the most prestigious award for the best corporate responsibility reporting . As such, it is presented to the organization with the highest score

on the Transparency Benchmark. The jury, consisting of Ms. Monika Milz, MBA (chairman), HRH Prince Carlos de Bourbon de Parme and

Transparency Benchmark 2015 The Crystal 2015 9

Professor. Leen Paape RA RO CIA, has chosen the winner from the top three. Next to the Crystal, additional awards are presented to the organiza-

tion that climbed the most places on the Transparency Benchmark ladder and the organization that addresses transparency in corporate

responsibility reporting in the most creative and innovative manner.

Stakeholders, like consumers, shareholders and governments expect an organization to be transparent about its tradeoffs and performance on

an environmental, social and governance level. By openly communicating on these matters, an organization assumes a vulnerable position as its

activities can be evaluated by its stakeholders. Transparency triggers the stakeholder dialogue, which can lead to adjustments in the company’s

policy. This has been the purpose of the Transparency Benchmark for the past11 years and it seems to work.

This year, the TB report includes an in-depth chapter in which transparency on social, environmental and governance elements is discussed.

What is it, how does it work and what is the impact of transparency on the way organizations conduct business today?

In order to gain a proper understanding of the Transparency Benchmark, it is important to emphasize that the benchmark is purely aimed at

measuring transparency in reporting. The Ministry gives no substantive judgment about the performance of organizations in the field of

corporate responsibility. However, the Transparency Benchmark goes beyond merely establishing scores for companies. The observed trends in

scores and patterns within sectors are also interesting to delve into. In this booklet, you will find more information in this respect, besides the

results of companies’ transparency over the reporting year 2014.

Transparency Benchmark 2015 The Crystal 201510

3 This year’s winners

The Jury has the task to determine the winners. The winners of 2015 are:

Fastest climber on the ladder of the Transparency Benchmark

Westland Infra has climbed this year from position 162 to position 56. An increase of a staggering 106 positions.

Most innovative report

The award for the most innovative report this year goes to Schiphol Group.

The Crystal Prize, First prize of the Transparency Benchmark

The third position is for Unilever, right behind number two, Philips. The winner of the Crystal Prize 2015 with 196 points is AkzoNobel.

The complete report with the considerations of the Jury can be found in paragraph 6.6.

Transparency Benchmark 2015 The Crystal 2015 11

4 What stands out?

This chapter will focus on the results of the Transparency Benchmark. The results concerning the criteria were based on the analyses of the

organizations that obtained a score on the Transparency Benchmark (245 organizations). Organizations with zero scores have thus not been

included in the analysis.

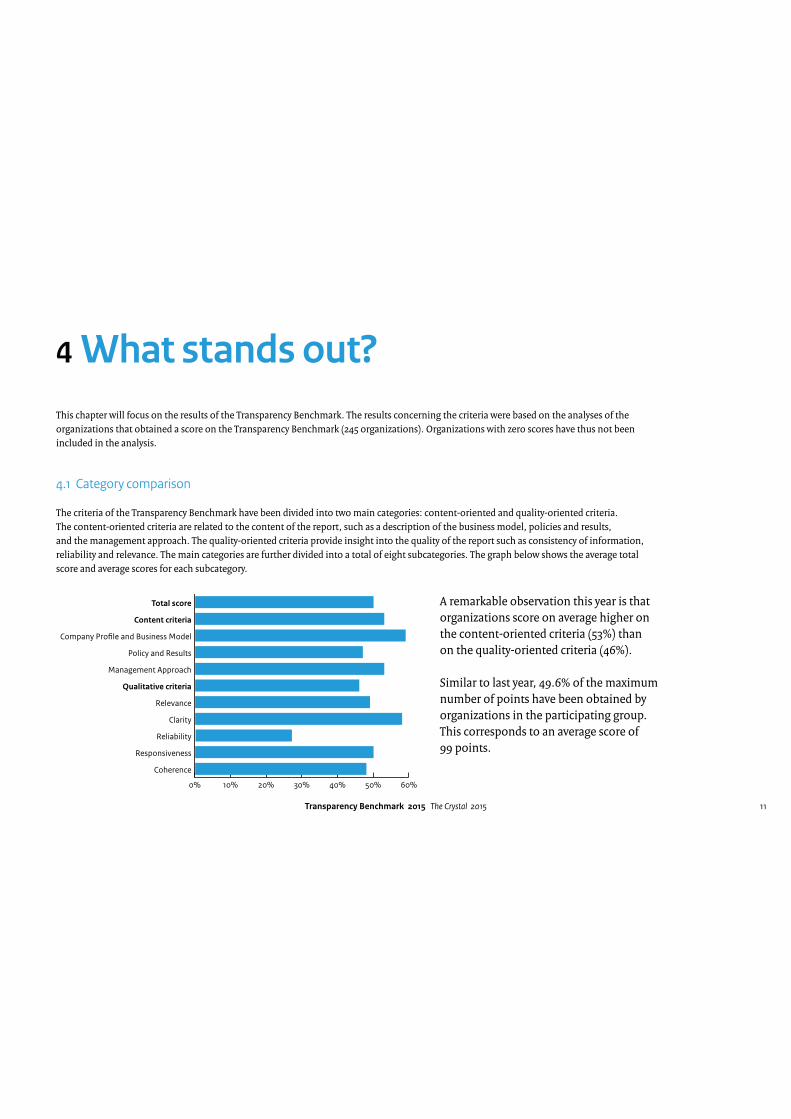

4.1 Category comparison

The criteria of the Transparency Benchmark have been divided into two main categories: content-oriented and quality-oriented criteria.

The content-oriented criteria are related to the content of the report, such as a description of the business model, policies and results,

and the management approach. The quality-oriented criteria provide insight into the quality of the report such as consistency of information,

reliability and relevance. The main categories are further divided into a total of eight subcategories. The graph below shows the average total

score and average scores for each subcategory.

0% 10% 20% 30% 40% 50% 60%

Coherence

Responsiveness

Reliability

Clarity

Relevance

Qualitative criteria

Management Approach

Policy and Results

Company ProBle and Business Model

Content criteria

Total score A remarkable observation this year is that

organizations score on average higher on

the content-oriented criteria (53%) than

on the quality-oriented criteria (46%).

Similar to last year, 49.6% of the maximum

number of points have been obtained by

organizations in the participating group.

This corresponds to an average score of

99 points.

Transparency Benchmark 2015 The Crystal 201512

4.2 Criteria comparison

The next pages will provide more information on the criteria of the Transparency Benchmark 2015. The table below indicates the criteria with the

best and worst scores obtained by the participating organizations. The highest and lowest scoring criteria are the same criteria as in 2014.

This table is then followed by, an overview of the most relevant and remarkable results of the Transparency Benchmark 2015. The graphs included

in this overview present the average scores along the organizational classification of the TB Ladder (as defined in chapter 1). Comparison with last

year’s scores is made possible by including the 2014 results. Moreover, based on a complementary in-depth analysis, the texts accompanying each

graph highlight further observations of this year’s TB results, which are not directly derived from the graphs themselves.

TOP 3 HIGHEST SCORINING CRITERIA TOP 3 LOWEST SCORING CRITERIA

Score & Criteria Explanation criteria Score & Criteria Explanation criteria

82% of the organizations achieved

the maximum score concerning

criterion 13

Complete understanding of

the organizational structure

67% of the organizations

obtained the minimum score

concerning criterion 30

No inclusion of a signed statement from

an independent third party, who has

verified the corporate responsibility

information

79% of the organizations achieved

the maximum score on criterion 1

General information about the

organization, a quantitative summary

of the organization’s profile (amount

of employees, amount of supplied

goods/ services, etc.)

65% of the organizations has

obtained the minimum score

concerning criterion 31

Subject matter experts or stakeholders

have not been invited to express their

opinion in the report itself (e.g. quotes

have not been included)

61% of the organizations

achieved the maximum score

on criterion 35

Sharing a vision on relevant corporate

responsibility themes and creating

awareness / understanding with

stakeholders on these specific themes

61% of the organizations has

obtained the minimum score

concerning criterion 40

The achieved corporate responsibility

results are not compared with relevant

publications from external parties (e.g.

listings, benchmark information, trend

analyses and best practices)

Top 3 best scoring categories: Top 3 lowest scoring categories:

1. Company Profile and Business Model (59% of maximum attainable score) 1. Reliability (27% of maximum attainable score)

2. Clarity (58% of maximum attainable score) 2. Policy and Results (47% of maximum attainable score)

3. Management Approach (53% of maximum attainable score) 3. Coherence (48% of maximum attainable score)

Transparency Benchmark 2015 The Crystal 2015 13

69% of organizations report on the value chain in which it operates. (compared to 73% in 2014).

The percentage of organizations receiving the maximum score on this

criteria increased from 16% to 22%. The full score can be obtained by

providing an explanation about the main corporate social responsi-

bilities that are of importance within the value chain and including a

graphical representation.

Category: Organization and Business Model

Value Chain

0 20 40 60 80 100

Laggards

Peloton

Followers

Leaders

Total 2014

Total 2015 69%

73%

100%

98%

9%

67%

91%

33%

2%

0%

27%

31%

Yes No

Business Strategy

0 20 40 60 80 100

Laggards

Peloton

Followers

Leaders

Total 2014

Total 2015 86%

88%

100%

100%

38%

90%

63%

10%

0%

0%

12%

14%

Yes No This year, 86% of the organizations provide an explana-tion on the business strategy. The percentage of organizations that obtained the maximum score

increased from 50% in 2014 to 55%. These organizations provide

specific information on the strategy and present a coherent set of

strategic themes, priorities and objectives. Additionally, they explicitly

link the strategy with other components of the report.

Category: Organization and Business Model

74% of the organizations have formulated specific targets concerning corporate responsibility in 2015.

This is comparable with previous year.In total, 29% of the organizations obtained the maximum score on

this criteria (4% more than previous year). These organizations provide

quantitative targets and link them with the material aspects.

Categorie: Policy and results

Objectives

0 20 40 60 80 100

Laggards

Peloton

Followers

Leaders

Total 2014

Total 2015 74%

73%

100%

100%

16%

74%

84%

26%

0%

0%

27%

26%

Yes No

Transparency Benchmark 2015 The Crystal 201514

33% of organizations have a statement of an independent third party included in the corporate

responsibility report. In comparison with previous year, it is remarkable that the followers-

group scores on average significantly better: 76% of the followers

obtained an independent statement, compared to 63% in 2014.

In total, 11 organizations gained the maximum score on this criteria.

Category: Reliability

0 20 40 60 80 100

Laggards

Peloton

Followers

Leaders

Total 2014

Total 2015 33%

30%

100%

76%

3%

15%

97%

85%

24%

0%

70%

67%

Yes No

Third-party Assurance

0 20 40 60 80 100

Laggards

Peloton

Followers

Leaders

Total 2014

Total 2015 74%

76%

100%

13%

76%

88%

24%

0%

100% 0%

24%

26%

Yes No

Stakeholder Engagement 74% of the organizations indicate how they engage their stakeholders in the strategy, policy and activities of the organization. This is a slight decrease from last year. There is room for improvement since only 17% of the organizations

achieve the maximum score. These organizations report on the

outcomes of the stakeholder dialogue, the involvement of the highest

governance body during the dialogue and indicate how the

stakeholder dialogue is related to the organization’s strategy and

established targets.

Category: Reliability

67% of the organizations report on the challenges, issues or dilemma’s faced with regards to their business,

a slight increase from last year.Moreover, there is a clear increase in the percentage of organizations

that achieved the maximum score on this criteria. These organizations

include the description on challenges, issues or dilemmas as a

stand-alone recognizable part within the report.

Category: Responsiveness

0 20 40 60 80 100

Laggards

Peloton

Followers

Leaders

Total 2014

Total 2015 67%

66%

100%

13%

65%

88%

35%

0%

94% 6%

34%

33%

Yes No

Challenges and Dilemmas

Transparency Benchmark 2015 The Crystal 2015 15

64% of organizations clearly report how their strategy, activities and results with regards to corporate

responsibility align to the organization’s strategy. 50% of the organizations achived the maximum score on this criteria.

These organizations use their set of strategic priorities as a guidance

for an explanation of the developments, results and future expecta-

tions regarding corporate social responsibility.

Category: Coherence

0 20 40 60 80 100

Laggards

Peloton

Followers

Leaders

Total 2014

Total 2015 64%

65%

100%

0%

60%

100%

40%

0%

100% 0%

35%

36%

Yes No

Link between CR

and Strategic Aspects

4.2.1 Materiality

Internationally, the subject of materiality within reporting has been receiving more and more emphasis. This includes a sharpened focus on

materiality of CSR themes in sustainability reporting in particular, evident from the latest GRI G4 guidelines. To keep the ever-increasing amount of

non-financial information clearly structured and relevant for users, companies need to focus on those subjects, which are of most material impor-

tance to their own business and/or the users of the report. Therefore, this year special attention was dedicated to materiality in the formulation of

criteria for the Transparency Benchmark 2015, leading to a redefinition of some criteria. The next pages provide insight in the conclusions related to

the criteria about materiality.

The precentages of organizations that report about material themes is 72% in 2015 (which is a decrease of 7%

from last year). Despite this total decrease, the percentage of organizations that

provide additional insights into their material themes (insights into

the relative importance of the identified material themes and

graphical representation of this) increased from 27% to 38%.

Category: Organization and business model

0 20 40 60 80 100

Laggards

Peloton

Followers

Leaders

Total 2014

Total 2015 72%

79%

100%

9%

73%

91%

27%

0%

100% 0%

21%

28%

Yes No

Materiality I: General

Transparency Benchmark 2015 The Crystal 201516

0 20 40 60 80 100

Laggards

Peloton

Followers

Leaders

Total 2014

Total 2015 61%

82%

100%

3%

56%

97%

44%

0%

100% 0%

18%

39%

Yes No

Materiality II: RelevanceCriteria 22 was changed in comparison to last year. Whereas last year

the organizations could obtain the maximum score if they reported

on at least five of the total pool of identified material issues, this

year, organizations could only obtain the maximum score if they

report on all (and exclusively on) the material themes, which they

have identified themselves. Due to these changes, there is a

noticeable decrease in the percentage of organizations that obtained

points on this criteria (82% in 2014 to only 61% in 2015).

Despite the changes and the stricter interpretation of the criteria,

37% of the organizations obtained the maximum score.

Category: Relevance

Monetary value

A large number of organizations describe the impact of their products/services on society. Quantifying and monetizing the generated impact

is becoming more popular. The monetary value of environmental or social impact is the value (in Euros or other monetary value) of the effect

on the environment or society. It should be noted that there is a significant difference between the monetary value of a cost saving for the

organization (or the supply chain) and the monetary value of an effect (impact) for society. An investment in charity or an energy-saving

program expressed in Euros of costs saved is not similar to the monetary value of a social of environmental effect. Monetizing the impact of

training and education on employees, (future) employers and society is an example of such monetary value.

Transparency Benchmark 2015 The Crystal 2015 17

Criteria 11 and 12 were also changed in comparison to last year. In 2014, the organizations were awarded full points for explanations in their

reports about a number of standard environmental and social aspects, specifically included in the criteria (assuming relevant aspects are similar

for all organizations). This year, these criteria were reformulated such that a list of possible environmental and social aspects was no longer

provided. Rather, organizations could only get points if all the material environmental and social aspects (as identified in their own reports) are

explained, i.e. the criteria took into account the fact that companies have material aspects specific to their own organization).

0 20 40 60 80 100

Laggards

Peloton

Followers

Leaders

Total 2014

Total 2015 74%

100%

19%

74%

81%

26%

0%

100% 0%

26%

74% 26%

Yes No

Materiality III: Environmental Aspects 74% of the organizations report about their material environmental aspects of business practice. Although last year, the same percentage reported about material environmental aspects, in 2014 this criteria looked at a standardized list of aspects.This year, 65% of the organizations included a quantitative explanation

of at least one material environmental aspect. In total 6 organizations

obtained the maximum amount of points on this criteria: in order to

receive the maximum amount of points it is required to express the

environmental results in a monetary value (see box about monetary

value).

Category: Policy and results

76% of the organizations report about their material social aspects of business practice.

Next to this, it is worth noting that 7 organizations have gained the

maximum amount of points on this criteria and have expressed their

social results in a monetary value ( see box about monetary value) .

Category: Policy and results

0 20 40 60 80 100

Laggards

Peloton

Followers

Leaders

Total 2014

Total 2015 76%

100%

13%

78%

88%

22%

0%

100% 0%

24%

84% 16%

Yes No

Materiality IV: Social Aspects

Transparency Benchmark 2015 The Crystal 201518

4.3 Sector comparison

The participating organizations of the Transparency Benchmark have been divided into 16 different sectors (similar to last year). The organiza-

tions that could not be included in a specific sector form the sector ‘other’, a total of 19 organizations.

The dynamics in the operating environment and challenges vary per sector making a sector-based analysis essential and valuable. The various

sectors demonstrate differences in average points received. A lower average score provides insights into the transparency within a particular

sector and not necessarily about the performance regarding corporate responsibility of the sector.

Sector Average score

2015

Percentage

zero scores

2015

As in last year, the transport sector has the highest average

score in 2015 with 156 points.

The average score of all organizations is exactly the same as

last year (99 points).

There are substantial differences between the scores of

sectors. An illustrative example of this is the difference of in

total 122 points between the transport sector and the pharma-

ceuticals industry.

In addition, it is noticeable that some sectors consist majorly

of organizations with a zero score. For example, although in

the consumer products sector the average is 133 points, 86% of

the organizations in this sector received a 0-score. On the

contrary, the real estate sector only achieves an average score

of 95 points, however all organizations have achieved a

positive in this sector.

Banking and insurance 108 5%

Construction and maritime 110 23%

Consumer products 133 86%

Services 94 32%

Energy, oil and gas 129 42%

Trading 75 76%

Industrial products 97 67%

Media and communications 66 44%

Other 91 74%

Pharmaceuticals 34 50%

Retail 85 60%

Technology 101 60%

Transport 156 63%

Universities and Medical

Centres

73 4%

Real estate 96 0%

Food and beverage 104 52%

For this year’s sector comparison a general reclassification has been made. This entails that some organizations have been assigned

to another sector compared to last year. In addition, 80 new organizations have been added to the Transparency Benchmark. Only

these 80 organizations are considered as new participants within the sectors.

Transparency Benchmark 2015 The Crystal 2015 19

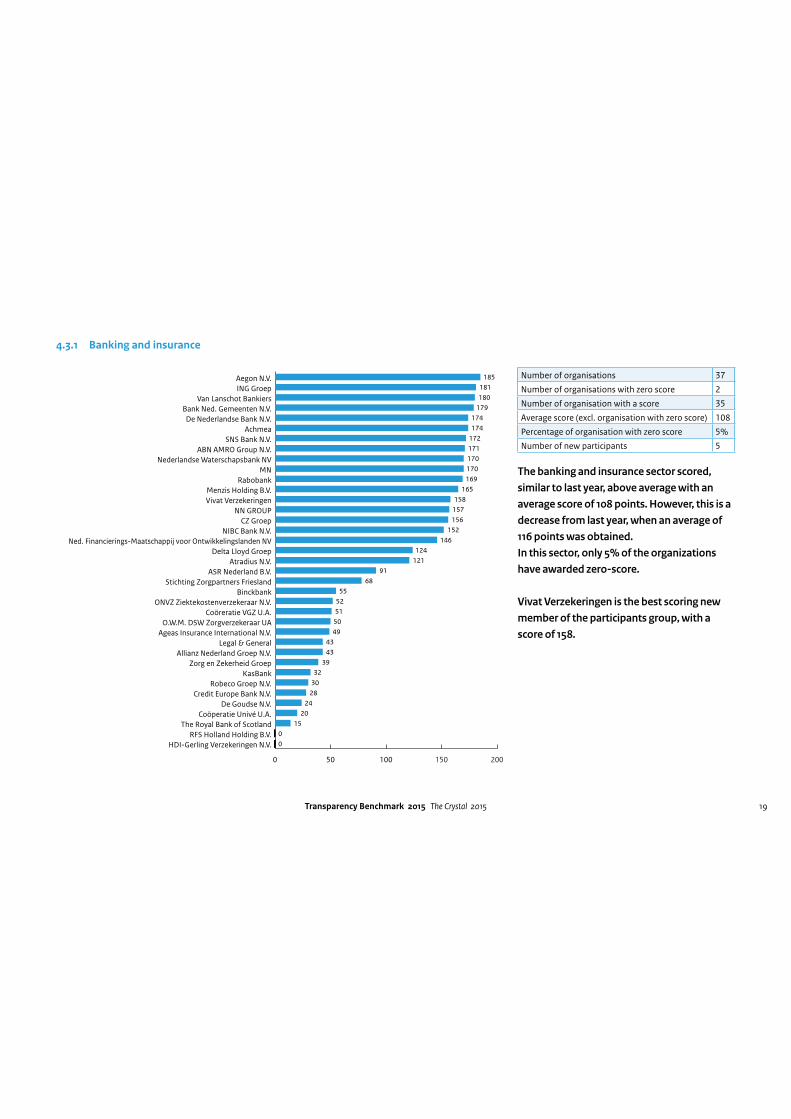

4.3.1 Banking and insurance

0 50 100 150 200

HDI-Gerling Verzekeringen N.V.

RFS Holland Holding B.V.

The Royal Bank of Scotland

Coöperatie Univé U.A.

De Goudse N.V.

Credit Europe Bank N.V.

Robeco Groep N.V.

KasBank

Zorg en Zekerheid Groep

Allianz Nederland Groep N.V.

Legal & General

Ageas Insurance International N.V.

O.W.M. DSW Zorgverzekeraar UA

Coöreratie VGZ U.A.

ONVZ Ziektekostenverzekeraar N.V.

Binckbank

Stichting Zorgpartners Friesland

ASR Nederland B.V.

Atradius N.V.

Delta Lloyd Groep

Ned. Financierings-Maatschappij voor Ontwikkelingslanden NV

NIBC Bank N.V.

CZ Groep

NN GROUP

Vivat Verzekeringen

Menzis Holding B.V.

Rabobank

MN

Nederlandse Waterschapsbank NV

ABN AMRO Group N.V.

SNS Bank N.V.

Achmea

De Nederlandse Bank N.V.

Bank Ned. Gemeenten N.V.

Van Lanschot Bankiers

ING Groep

Aegon N.V. 185

181

180

179

174

174

172

171

170

170

169

165

158

157

156

152

146

124

121

91

68

55

52

51

50

49

43

43

39

32

30

28

24

20

15

0

0

Number of organisations 37

Number of organisations with zero score 2

Number of organisation with a score 35

Average score (excl. organisation with zero score) 108

Percentage of organisation with zero score 5%

Number of new participants 5

The banking and insurance sector scored,

similar to last year, above average with an

average score of 108 points. However, this is a

decrease from last year, when an average of

116 points was obtained.

In this sector, only 5% of the organizations

have awarded zero-score.

Vivat Verzekeringen is the best scoring new

member of the participants group, with a

score of 158.

Transparency Benchmark 2015 The Crystal 201520

4.3.2 Construction and maritime

0 50 100 150 200

SPIE Nederland B.V.

Koninklijke Wagenborg

CRH Nederland B.V.

Bluewater Holding B.V.

A. Hakpark B.V.

Aan de Stegge Holding B.V.

Van Wijnen Groep N.V.

Janssen De Jong Groep B.V.

Hurks groep

Oranjewoud N.V.

Dura Vermeer Groep

Unica Groep B.V.

IHC Merwede Holding B.V.

Damen Shipyards Group N.V.

Van Oord

Ballast Nedam N.V.

Wavin N.V.

Beelen Groep B.V.

TBI Holdings

Koninklijke Boskalis Westminster N.V.

Joh. Mourik & Co. Holding B.V.

VolkerWessels

SBM ORshore

Royal Imtech N.V.

Heijmans

Royal BAM Group 193173

168167166

153143

138132

128115

10996

8364

513534

2319

000000

Number of organisations 26

Number of organisations with zero score 6

Number of organisation with a score 20

Average score (excl. organisation with zero score) 110

Percentage of organisation with zero score 23%

Number of new participants 2

This year, the construction and maritime

sector obtained an above-average score of

110 points. This is a decrease from an average

score of 120 points in 2014.

Oranjewoud N.V. is within this sector the

best new participant in the group with a

score of 35.

Transparency Benchmark 2015 The Crystal 2015 21

4.3.3 Consumer products

0 50 100 150 200

WE Europe B.V.

Van den Ban Autobanden B.V.

Tommy Hil<ger Europe

Swarovski (Europe) Holding B.V.

Smartwares B.V.

Remeha Group B.V.

Philip Morris Holland B.V.

Lekkerland Beheer

Hunter Douglas N.V.

Honeywell Netherl. Hold. B.V.

FUJIFILM Europe B.V.

De MandemakersGroep Holding B.V.

Canon Europa N.V.

Cabot Norit Activated Carbon

Bose Products

Apollo Vredestein B.V.

Action Service & Distributie

A.S. Watson B.V.

TomTom N.V.

Accell Group

Unilever N.V. 194139

67000000000000000000

Number of organisations 21

Number of organisations with zero score 18

Number of organisation with a score 3

Average score (excl. organisation with zero score) 133

Percentage of organisation with zero score 86%

Number of new participants 2

Despite the fact that only three

organizations in this sector received a score,

the average score (excluding zero scores) is

133 points.

The consumer products sector is the sector

with the highest percentage of organizations

with a 0-score: 86%.

Transparency Benchmark 2015 The Crystal 201522

4.3.4 Services

0 50 100 150 200

Xylem Water Solutions Nederland B.V.Van Gansewinkel Groep

United Parcel Service Nederland B.V.Unit 4 N.V.

Twynstra GuddeTP Vision Europe B.V.Oracle Nederland B.V.

Omron Europe B.V.Manpower Nederland B.V.

Loyens & LoeI N.V.ISS Holding Nederland B.V.

Holiday Holding RoNerdam B.V.Equens SE

EcurionCGI Nederland B.V.

Booking.com B.V.BCD Travel Holding

Amlin Corporate InsuranceADG dienstengroep B.V.

Adecco Nederland Holding B.V.Accenture B.V.

IMC TradingTMF Group Holding B.V.

Exact Holding N.V.DOCDATA N.V.

APGDPA GROUP

Value8Monuta

Centric Holding B.V.Yarden Holding B.V.ICT Automatisering

Nieuwe Steen invBrunel International N.V.

Dela Uitvaartverzorging B.V.Propertize B.V.

Broekhuis HoldingBrab. Ontw. Maatschappij N.V.

Stichting EspriaLeasePlan Corporation N.V.

Fugro N.V.Holland Casino

CoMoreGrontmij N.V.

PGGMStichting Exploitatie Nederlandse Staatsloterij

Arcadis N.V.Vebego International N.V.

TNOCOVRA NV

USG People N.V.Ontwikkelingsmaatschappij Oost Nederland NV

N.V. HVCIndustriebank LIOF N.V.

Royal HaskoningDHVRandstad Holding N.V.

DeloiNe Holding B.V.KPMG N.V.Ordina N.V.

Facilicom Services GroupPricewaterhouseCoopers

Holding Nationale Goede Doelen Loterijen N.V.NV NOM Investerings- en Ontwikkelingsmaatschappij voor Noord-Nederland

Ernst & Young NederlandANWB B.V. 176

174

171

167

167

155

150

148

147

140

139

138

136

129

126

117

114

112

111

110

103

98

92

92

83

80

72

66

65

62

55

54

51

50

47

37

29

28

27

25

25

25

24

9

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

Number of organisations 65

Number of organisations with zero score 21

Number of organisation with a score 44

Average score (excl. organisation with zero score) 94

Percentage of organisation with zero score 32%

Number of new participants 8

The service sector has the highest number of

participating organizations, in total there are

65 organizations included in this sector. The

average score is, just like last year, 94 points.

About one third of the organizations have a

0-score in this sector.

Propertize B.V. is within this sector the best

new participant in the group with a score of

62.

Transparency Benchmark 2015 The Crystal 2015 23

4.3.5 Energy, oil and gas

0 50 100 150 200

Yara Sluiskil B.V.

TOTAL Nederland N.V.

New World Resources

Neste Oil Netherlands B.V.

Kuwait Petroleum B.V.

Heerema Marine Contractors Holding Nederland B.V.

Essent

Delek Nederland B.V.

De Nederlandse Energie Maatschappij B.V.

Argos Group Holding B.V.

Ultra-Centrifuge Ned. N.V.

Delta N.V.

Nuon Energie N.V.

Core Laboratories N.V.

EBN

Royal Dutch Shell

Eneco Holding N.V.

GasTerra B.V.

Westland Infra

E.ON Benelux N.V.

Enexis B.V.

TenneT Holding B.V.

Nederlandse Gasunie N.V.

Alliander N.V. 189181

174163162

153151

148146

1387171

4322

0000000000

Number of organisations 24

Number of organisations with zero score 10

Number of organisation with a score 14

Average score (excl. organisation with zero score) 129

Percentage of organisation with zero score 42%

Number of new participants 3

The energy, oil and gas sector has achieved a

higher average score than last year. Last year,

the sector has achieved an average score of

124 points, while this year the average score

is 129.

Transparency Benchmark 2015 The Crystal 201524

4.3.6 Trading

0 50 100 150 200Transm. and Engineer. Services Netherl.

Toshiba Medical Systems Europe B.V.Scania Europe

RobaOxbow Coal B.V.

Momentive Specialty Chemicals BVMCB International B.V.

Interfood HoldingHager-Minnema-HuJen Beheer B.V.

Getinge Arjo Holding Netherlands B.V.Copaco Nederland B.V.

Auctus Holding B.V.N.V. Deli Maatschappij

SHV Holdings N.V.Amsterdam Commodities N.V.

Dutch Flower Group B.V.Nidera B.V. 137

9355

130000000000000

Number of organisations 17

Number of organisations with zero score 13

Number of organisation with a score 4

Average score (excl. organisation with zero score) 75

Percentage of organisation with zero score 76%

Number of new participants 3

The trading sector has an average score of 75

points, which is higher than the average of

last year: 73 points.

Transparency Benchmark 2015 The Crystal 2015 25

4.3.7 Industrial products

0 50 100 150 200

Yanmar EuropeVoestalpine Automotive Netherlands Holding B.V.

Tetra Laval Holdings B.V.Terberg Group B.V.

Tata SteelSynbra Holding B.V.

SIHI Group B.V.Scheuten Glass Holding B.V.

SABIC International Holdings B.V.Rockwell Automation B.V.P.L. v. Merksteijn Hold. B.V.

Otra N.V.Nedschroef Nederland B.V.

MHI Equipment Europe B.V.LyondellBasell Industries N.V.

Kuehne + Nagel N.V.INVISTA B.V.

International Flavors & Fragrances I.F.F. (Nederland) B.V.Inalfa Roof Systems Group B.V.

Huntsman Investments (Netherlands) B.V.Hitachi Machinery N.V.

FlowserveEnviem Holding B.V.

Denkavit Internationaal B.V.De Stiho Groep B.V.

De Hoop Terneuzen B.V.Citadel Enterprises B.V.

Caldic B.V.C. den Braven Beheer B.V.

Bosal Nederland B.V.Avery Dennison Materials Nederland B.V.

Ardagh Group Netherlands B.V.ArcelorMittal Netherlands B.V.

Ace Innovation Holding B.V.ABB B.V.

Sulzer Netherlands HoldingKramp Groep B.V.

Forbo Flooring B.V.Hertel Holding B.V.

Brocacef HoldingVan Leeuwen Buizen Groep B.V

StorkAMG Advanced Metallurg. Gr. NV

Nedap N.V.Aalberts Industries N.V.

AperamCorbion N.V.

DOW Benelux B.V.Rockwool Benelux Holding

Kendrion N.V.Koninklijke Ten Cate N.V.

DSM N.V.Koninklijke Philips N.V.

AKZO Nobel N.V. 196

195

179

171

167

167

121

119

100

81

67

59

37

35

22

17

10

5

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

Number of organisations 54

Number of organisations with zero score 36

Number of organisation with a score 18

Average score (excl. organisation with zero score) 97

Percentage of organisation with zero score 67%

Number of new participants 9

Last year, the sector had an average score of

89 points,while this year, the sector scores an

average of 97 points.

The industrial products sector is, a_er the

technology sector, the sector with the most

new participants.

Transparency Benchmark 2015 The Crystal 201526

4.3.8 Media and communications

0 50 100 150 200Stichting Nederlandse Publieke Omroep

Stage Entertainment B.V.Sanoma Magazines B.V.

RTL Nederland B.V.Nielsen N.V.

Koninklijke Wegener N.V.Endemol B.V.

Audax B.V.de Persgroep Nederland B.V.

Global City Holdings N.V.Cimpress

Koninklijke Brill N.V.Roto Smeets Group N.V.

Wolters Kluwer N.V.RELX Group N.V.

TMG - Telegraaf Media Groep 153139

121105

301614

108

0000000

Number of organisations 16

Number of organisations with zero score 7

Number of organisation with a score 9

Average score (excl. organisation with zero score) 66

Percentage of organisation with zero score 44%

Number of new participants 3

The average score of the media sector is 66

points. This is a sharp decline from the

average of 96 points last year. Remarkably,

all the organizations in this sector score

lower than last year.

Global City Holdings NV is within this sector

the best new participant in the group with a

score of 14.

Transparency Benchmark 2015 The Crystal 2015 27

4.3.9 Pharmaceuticals

0 50 100 150 200

Astellas B.V.

Alliance Boots B.V.

A&D Pharma Holdings N.V.

ESPERITE

Fagron

GALAPAGOS 5330

180

00

Number of organisations 6

Number of organisations with zero score 3

Number of organisation with a score 3

Average score (excl. organisation with zero score) 34

Percentage of organisation with zero score 50%

Number of new participants 4

Same as last year, the pharmaceuticals

sector has the smallest number of

participants and the lowest average score.

Four of the six organizations within this

sector are new compared to last year.

GALAPAGOS is within this sector the best

new participant in the group with a score

of 53.

Transparency Benchmark 2015 The Crystal 201528

4.3.10 Retail

0 50 100 150 200

Yamaha Motor Europe N.V.

V&D Group

St. Clair/ De Bijenkorf

SPAR Holding B.V.

Retailcom Beheer B.V.

Pon Holdings B.V.

Poiesz Beheer B.V.

PGA Nederland N.V.

Peugeot Nederland N.V.

Mitsubishi Motors Europe B.V.

Miss Etam B.V.

Mercedes-Benz Nederland B.V.

Markeur

Lohomij B.V.

Inter-Sprint Banden

Intergamma B.V.

Hoogvliet B.V.

Foot Locker Europe B.V.

Dirk van den Broek/Dekamarkt

Da Holding B.V.

BMW Nederland B.V.

Maxeda Nederland B.V.

Blokker Holding B.V.

B & S International B.V.

Euretco B.V.

Stern Groep N.V.

Macintosh Retail Group N.V.

Coop Holding

IKEA Nederland B.V.

HEMA

PLUS Retail B.V.

Beter Bed Holding N.V.

Zeeman Groep B.V.

Jumbo Groep Holding B.V.

Koninklijke Ahold N.V. 168

139

138

116

105

92

87

85

85

70

39

31

21

12

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

Number of organisations 35

Number of organisations with zero score 21

Number of organisation with a score 14

Average score (excl. organisation with zero score) 85

Percentage of organisation with zero score 60%

Number of new participants 6

The retail sector has achieved a higher

average score than last year. The sector

achieved an average score of 84 points in

2014, this year the average score is 85.

B & S International B.V. is within this sector

the best new participant in the group with a

score of 31.

Transparency Benchmark 2015 The Crystal 2015 29

4.3.11 Technology

0 50 100 150 200

Xerox Investments Europe

Verizon Business International Holdings B.V.

Tech Data Nederland B.V.

Specialist Computer Holdings Nederland B.V.

Sensata Technol. Holding N.V.

Saphin B.V.

Samsung Electronics Benelux B.V.

Plantronics B.V.

Nokia Solutions and Networks B.V.

Liberty Global Holding B.V.

KYOCERA Document Solutions Europe B.V.

Ingram Micro

IBM Nederland BV

Huawei Technologies Coöperatief U.A.

Fujitsu Technology Solutions (Holding) B.V.

Dell Global B.V.

Cisco Systems International B.V.

Chemours Netherlands B.V.

Boston ScientiYc Int. B.V.

ALTICE

Acer Europe B.V.

VDL Groep

NXP Semiconductors Netherlands B.V.

Neways Electronics International N.V.

OCI

ASM International N.V.

Gemalto N.V.

BE Semiconductor Indus. N.V.

Tele2 Netherlands Holding N.V.

VimpelCom Ltd.

TKH Group N.V.

ASML

Vodafone

Siemens Nederland

KPN 192

189

186

153

128

128

93

92

80

58

36

33

24

21

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

Number of organisations 35

Number of organisations with zero score 21

Number of organisation with a score 14

Average score (excl. organisation with zero score) 101

Percentage of organisation with zero score 60%

Number of new participants 14

The technology sector has the most new

participants in the group of the Transparency

Benchmark 2015, in total there are 14 new

organizations in this sector.

The average score of the sector increased

this year from 92 points to 101 points.

Vimpelcom Ltd. is within this sector the best

new participant with a score of 128.

Transparency Benchmark 2015 The Crystal 201530

4.3.12 Transport

0 50 100 150 200

Vroon Group B.V.

Thomas Cook Nederland B.V.

Sundio Group B.V.

Stolt Tankers

Samskip

Raben Group B.V.

Post-Kogeko Logistics B.V.

Handelsveem Beheer

Gaiwin B.V.

Ewals Holdings B.V.

Eur. Container Terminals B.V.

EEA Helicopter Operations B.V.

De Rijke Continental B.V.

DAF Trucks N.V.

Connexxion

Catom Enterprises B.V.

Universal Cargo Logistics

Vos Logistics Beheer B.V.

GVB Holding NV

TNT Express

Koninklijke Vopak N.V.

ProRail B.V.

Air France - KLM

PostNL

Schiphol Group

Havenbedrijf RoRerdam N.V.

NS 194191191

177166

159131131

108108

00000000000000000

Number of organisations 27

Number of organisations with zero score 17

Number of organisation with a score 10

Average score (excl. organisation with zero score) 156

Percentage of organisation with zero score 63%

Number of new participants 1

Similar to last year, the transport sector has

the highest average score. The sector

achieved an average score of 126 points in

2014. This year the average score is 156

points.

In addition, it is the only sector in which all

organizations with a score have achieved

more than 100 points.

Transparency Benchmark 2015 The Crystal 2015 31

4.3.13 Universities and Medical Centres

0 50 100 150 200

Vrije Universiteit

Nyenrode

Radboud Universiteit Nijmegen

Erasmus MC

VUmc

Universitair Medisch Centrum Groningen (UMCG)

Erasmus Universiteit RoBerdam

Maastricht UMC+

Open Universiteit

UMC Utrecht

Academisch Medisch Centrum

Technische Universiteit Eindhoven

Technische Universiteit DelJ

Universiteit van Tilburg

Leids Universitair Medisch Centrum (LUMC)

Universiteit Leiden

Universiteit Utrecht

Universiteit Twente

Universiteit Maastricht

Universiteit van Amsterdam

Rijksuniversiteit Groningen

Radboudumc

Wageningen UR 156

126

122

122

116

115

97

96

80

59

58

58

49

47

45

44

40

36

36

33

32

31

0

Number of organisations 23

Number of organisations with zero score 1

Number of organisation with a score 22

Average score (excl. organisation with zero score) 73

Percentage of organisation with zero score 4%

Number of new participants 6

The universities and medical centers (UMC)

sector has 6 new participants compared to

last year. This is caused by the fact that the

vast majority of UMC’s received

dispensation from the government last year.

The UMC’s did not publish their reports

before the 1st of June 2014, and therefore

they could not be included in last year’s

Transparency Benchmark.

This year, the average score of the sector is

73 in comparison to 85 points in 2014.

The Leids Universitair Medisch Centrum

(LUMC) is within this sector the best new

participant with a score of 80.

Transparency Benchmark 2015 The Crystal 201532

4.3.14 Real estate

0 50 100 150 200GROOTHANDELSGEBOUW

Refresco Holding B.V.

Vastned Retail N.V.

Eurocommercial Properties

Wereldhave Manag. Holding B.V.

Waterweg Wonen

Unibail Rodamco

Q Park N.V. 170157

111105

7673

4430

Number of organisations 8

Number of organisations with zero score 0

Number of organisation with a score 8

Average score (excl. organisation with zero score) 96

Percentage of organisation with zero score 0%

Number of new participants 1

This year, the real estate sector scores an

average of 96 points. This is a decrease from

last year when the average score was 107.

In the sector none of the participating

organizations ended with a zero score.

Transparency Benchmark 2015 The Crystal 2015 33

4.3.15 Food and beverage

0 50 100 150 200

Theobroma B.V.Storteboom Group B.V.

Plukon Food GroupNVDU Acquisition B.V.

Milkiland N.V.Mijwo Beheer B.V.

Meatpoint B.V.Mead Johnson B.V.

Mars Nederland B.V.Loders Croklaan Group B.V.

Koninklijke Zeelandia Groep B.V.Koninklijke De Heus B.V.

IMCD Holding B.V.Hoogwegt Groep B.V.

Hanos (Apeldoorn B.V.)H.L. Barentz B.V.

Glencore Grain RoSerdam B.V.DE Masterblenders 1753

Danone Baby and Medical Nutrition B.V.Cargill B.V.

Bakkersland Groep B.V.A-Ware Food Group B.V.

Addasta Holding B.V.Farm Frites Beheer B.V.

VION Holding N.V.DOC Kaas

CZAVKoninklijke Coöperatie Cosun U.A.

Coöperatie AVEBE U.A.The Greenery B.V.

ForFarmers Group B.V.Cooperative Agri]rm U.A.

Vreugdenhil Groep B.V.Sligro Food Group N.V.

Bidvest Deli XLVanDrie Group

Albron Nederland B.V.PerfeSi v. MelleArla Foods B.V.

Bavaria N.V.Koninklijke Wessanen N.V.

Koninklijke FrieslandCampina N.V.Vitens N.V.

Heineken N.V. 182

177

163

161

153

139

133

131

130

118

112

111

96

80

61

52

52

49

46

26

17

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

Number of organisations 44

Number of organisations with zero score 23

Number of organisation with a score 21

Average score (excl. organisation with zero score) 104

Percentage of organisation with zero score 52%

Number of new participants 6

With an average score of 104 points, the

food and beverage sector improved their

average in comparison to last year’s average

score of 97 points.

About half of the organizations in the food

and beverage sector has received a zero

score.

Transparency Benchmark 2015 The Crystal 201534

4.3.16 Other

0 50 100 150 200

Vroegop Ruhe & Co. B.V.

Optiver Holding B.V.

O;ce Depot International

NetApp & Manufacturing

Mosadex

Mediq

Koninklijke Distill. Dirkzwager B.V.

Hyva Group B.V.

Horedo/Rensa

Elopak B.V.

De Kon. Nederlandse Munt N.V.

Clondalkin Industries B.V.

Chicago Bridge & Iron Company N.V.

Center Parcs Europe N.V.

British American Tobacco International (Holdings) B.V.

Beleggingsmij. Braverassa B.V.

Advanced Travel Partners Nederland B.V.

Louis Dreyfus

AerCap Holdings N.V.

Kardan N.V.

TUI Nederland

Airbus Group N.V.

Nutreco 147

144

140

61

30

24

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

Number of organisations 23

Number of organisations with zero score 17

Number of organisation with a score 6

Average score (excl. organisation with zero score) 91

Percentage of organisation with zero score 74%

Number of new participants 1

Compared to last year, the industry sector

‘other’ has obtained a higher score. The

composition of the sector has signiicantly

changed compared to last year, a possible

explanation for the higher average score of

91 points this year. In 2014, the average score

was 53 points.

Transparency Benchmark 2015 The Crystal 2015 35

4.4 Corporate responsibility reporting in practice

The participating organizations that filled in the self-assessment were asked to (voluntarily) answer some additional questions about reporting

and the process of developing a report.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

20152014

Seperate CR Report

Other Relevant Information

None

Integrated Report - Other

Integrated Report - IIRC

Financial Report

Type of Report(Analysis based on 244 (2014) and 245 (2015) respondents)

24%

1%6%

33%

8%

29%

30%

14%

1%

22%

7%

26%

Compared to last year, the number of respondents who

indicated that they have some form of Integrated

Reporting in place increased from 37% to 41%. Of those

reports, 8% is based on the framework for Integrated

Reporting of the IIRC (International Integrated Reporting

Council).

This year, 24% publish a separate CSR report, a decrease

from last year. The percentage of organizations that only

publish a financial report has also risen (to 29%).

The biggest difference is in the percentage of organiza-

tions that state not to publish a report, decreasing from

14% to 6%.

Transparency Benchmark 2015 The Crystal 201536

0%

20%

40%

60%

80%

100%

20152014

No

Yes

Use of GRI Guidelines(Analysis based on 244 (2014) and245 (2015) respondents)

51%

49%

48%

52%

0%

10%20%30%40%50%60%70%80%90%

100%

20152014

G4 core

G4 comprehensive

G3.1

G3.0

48%

18%

26%

8%

20%

11%

17%

52%

GRI Version Used(Analysis based on 126 (2014) and 120 (2015) respondents)

Almost half of the organizations use the guidelines of the Global Reporting Initiative (GRI) in the preparation of the

(corporate social responsibility) report.

The use of the GRI 3.1 version has significantly decreased compared to last year from 52% to 26%partly explained by the

fact that GRI 3.1 can no longer be applied from 2015. As a logical consequence the use of the GRI G4 Core has increased

from 20% to 48% and GRI G4 Comprehensive from 11% to 18%. This shows that the majority of organizations follow

the development of the GRI guidelines and are committed to meet these new standards.

Transparency Benchmark 2015 The Crystal 2015 37

0%

5%

10%

15%

20%

25%

30%

35%

OtherNo useof frameworkfor reporting

ISO 26000SustainabilityAccounting

Standards Board

EMASCarbonDisclosure

Project

InternationalIntegratedReporting

Council (IIRC)framework

Use of Internationally Recognized Frameworks(Analysis based on 90 (2014) and 73 (2015) respondents)

31% 32%

23%25%

0%3% 4% 4%

20% 21%24% 25%

30%

18%

2014

2015

In addition to the use of the GRI guidelines (see above), 32% of organizations indicate that they make use of the

framework for integrated reporting by the IIRC, while 25% use the Carbon Disclosure Project. Compared to last year,

the number of organizations that indicate their use of another internationally recognized framework has fallen from

30% to 18%. Furthermore, it is remarkable that once again a quarter of organizations do not use any framework for its

reporting.

Transparency Benchmark 2015 The Crystal 201538

0%

10%

20%

30%

40%

50%

60%

OtherLack of appropriateknowledge/

expertisein the elaboration

of a CR report

The elaboration of the report is more time-consuming

than initially expected

The report is not

considered a key point

DiHculties with the interpretation

of external guidelines

Data collectionwithin the

organisationis complex

Most important challenges in the process of CR reporting(Analysis based on 137 (2014) and 99 (2015) respondents)

48% 50%

34%29%

18% 19%

45% 44%

9%6%

20% 18%

2014

2015

Most of the respondents indicate that the biggest challenges during the process of reporting can be found inside their

own organization, identifying in particular those related to data collection (50%), time investment (44%) and a lack of

priority (19%).

Compared to last year, the number of respondents who expressed difficulties in interpreting external guidelines

decreased from 34% to 29%.

Transparency Benchmark 2015 The Crystal 2015 39

0

10

20

30

40

50

60

70

80

90

100

20152014

Fully implemented

OECD guidelines

Not familiar with

OECD guidelines

Familiar with OECD

guidelines, but not

implemented

Used OECD guidelines as a starting point in the elaboration of the code of conduct and corporate governance

Use of OECD Guidelines(Analysis based on 108 (2014) and 71 (2015) respondents)

11%

14%

44%

31%

46%

12%

32%

10%

Of the organizations that answered this question, 42%

apply the OECD guidelines for International Enterprises

to some extent: while 31% use the guidelines only as the

basis for their Code of Conduct and Corporate

Governance Code, 11% have fully implemented the OECD

guidelines. On the other hand, 44% of the organizations

indicated that, although they are familiar with the OECD

guidelines, they don’t have them integrated in their

company policies. This is a slight decrease compared to

last year. Finally, 14% of the organizations indicated that

they are not familiar with the OECD guidelines.

Transparency Benchmark 2015 The Crystal 201540

5 In-depth theme: The impact of Transparency

IntroductionThe Transparency Benchmark focuses – as one can already imagine – on Transparency. Online dictionaries (www.financiële begrippen.com)

explain transparency as: the extent to which the management of a business is clear. In order to achieve transparency, companies will have to

communicate, i.e. provide useful information. However, the precise definition of ‘useful information’ differs per (group of ) stakeholders.

As a result, ‘transparency’ also carries a different meaning for different stakeholders. Furthermore, communication is not only about the

receiver, but it also concerns the sender of such information. The organization (i.e. the sender) has its own opinion of how often and in which

way useful information should be provided to the receiver.

Currently, people and organizations are in the position to know a lot more about one another due to the widespread usage of the internet,

which provides the opportunity to obtain a vast amount of relevant information. This makes transparency even more important,

allowing the right kind of information to reach the right receiver. Needless to say, information has an impact.

This section will focus on the existing relationship between the organization and its stakeholders by taking a so-called agency perspective

to clarify the choices that companies can make when communicating their information (through an annual report). Furthermore,

this section will include insights into the extent to which the organizations address the information needs of their stakeholders.

Agency TheoryAgency theory is a well-known and respected theory originating in both economics and business research. It explains the relationship between

principals (client) and agents (executor) in business. The traditional agency theory (Jensen & Meckling, 1976) reasons from the perspective that

ownership and management in (large) enterprises is separated. The shareholders (principals) transfer the management of the organization

(in which they have invested) to the board (the agents) of the organization. Agency theory argues that the principal and the agents could have

conflicting interests, due to the fact that principals have less knowledge about the activities and results of the organization. This situation is

referred to the presence of information-asymmetry.

Transparency Benchmark 2015 The Crystal 2015 41

However, next to the shareholders, other diverse parties including (social) organizations and persons may also have some stake in an organiza-

tion. The modernistic agency theory approach focuses on this larger basket of principals, i.e. the stakeholders. The concept of information

asymmetry is also applicable to these stakeholders (employees, clients, suppliers, banks, the government, interest groups and others).

CommunicationIn order to reduce the effect of information asymmetry (i.e. stakeholders having less knowledge about the organization), organizations should

provide adequate and useful information. This information should enable stakeholders to make justified choices in relation to the organization

(investing, procurement, employee relations, social level of acceptance and more), also referred to as ‘incremental information paradigm’.

Information asymmetry is only one element of agency theory. Another element important in the discussion of transparency is the conflicting

interests between the management of an organization and its stakeholders. This conflict of interests influences the way in which management

decides to provide information, leaving the stakeholders in a position of dependency within this process of information-sharing. The question

that arises is then: to what extent is the management of an organization able to reduce the asymmetry of information, given the conflicts of

interests? Providing information can thus be seen as an instrument of the management of an organization.

Annual reportingNowadays, organizations are primarily sharing information through their annual public reporting, the most common forms of which include

the financial statements, a management report, a sustainability report, and/oran integrated report. Additionally, organizations often communi-

cate other messages through their websites or additional publications. In the context of the Transparency Benchmark, this chapter will especially

focus on the communication of accounting information, which is periodically released through the annual reports.

The annual report of an organization includes the financial statement (a factual overview of the financial results of an organization) and the

management report (the board of an organization provides an explanation of the results of the organization and the related risks at year-end).

In addition to the management report, some organizations also report a so-called sustainability report, or integrate the results related to

sustainability in the management report. The financial statement primarily includes quantitative information, whereas the management report

mainly includes qualitative information. Basically, the management report can be viewed as an explanation of how the company is performing

through the perspective of the board of an organization.

Transparency Benchmark 2015 The Crystal 201542

The board of an organization asks itself the following question: whom do I want to reach through this annual report, what do message do I want

to convey and how am I going to realize this? In answering these questions, the board of an organization will make certain choices that will

influence the way in which the report will be presented. A reporting strategy will be formulated but not formally included in the report itself.

Communication StrategyAn important characteristic of the annual report is that it serves as a channel for the organization to communicate its corporate image.

As a result, the annual reports constitute a showcase of ‘company pride’ for the management of an organization. Though in essence a potentially

positive characteristic, this element of ‘company pride’ brings about a risk of presenting a biased picture for the readers of the report.

Deegan (2002) provides additional insights into the communication strategies that have been elaborated by Lindblom. In reporting information

an organization stands to: (1) provide full transparency about recent events related to the organization, (2) influence the perception of the

stakeholders, (3) manipulate the perception of the stakeholder by diverging attention, and (4) influence the expectations concerning the results

of the organization. In order to realize the communication strategy, the board of the organization has a wide set of reporting-instruments at its

disposal.

Communicating is making choices

The communication instruments available to management can be categorized into: design, presentation and phrasing.

Design Design can help accentuate important parts of information. The reader’s attention to certain elements in the report can be

influenced through different aspects in the design of the report itself. Some of these aspects refer to the positioning of

disclosures in the report, the layout/design of the different pages, the use of colors,pictures and graphics to convey a

particular message, and the use of different font types and text boxes throughout the report.

Presentation The presentation of information is related to the design of the report. As such, ‘presentation’ focuses on the selection of

topics to include, the right balance between positive and negative disclosures, the decision to provide insights into

dilemmas, the structure in which topics are introduced and elaborated on, the degree of detail in information, ,as well as a

balance between quantitative and qualitative information on the one hand, and prospective and retrospective information

on the other.

Phrasing Finally, information can also become biased as a result of the choices in phrasing. A message can be delivered in many ways,

positively or negatively formulated, in an easily comprehensible way, or with a series of very technical terms. Much research

Transparency Benchmark 2015 The Crystal 2015 43

has been done on the comprehensibility of reporting. Students of the University of Groningen have, for example, researched

this theme with great interest. The main findings across researchers highlight that annual reports are difficult to read.

This is based on word-phrase characteristics in the text (length and amount). This research, however, does not take into

account characteristics of the reader (e.g. level of expertise, experience, education and degree to which the person is

interested).

When managing the introduced instruments, many choices have to be made. The table below provides examples of relevant choices.

These choices are not meant as an either/or decision, but rather should be considered as two extremes of a continuum.

Choices made when drafting a sustainability report

• Separate or integrated report

• Annual report in pdf or printed versus and online report

• Graphical representations versus textual guidance

• Differences in lay-out

• Negative versus positive results

• Retrospective versus prospective information

• Verification or no verification of annual report

• Qualitative information versus quantitative information

• Detailed information versus general information

• Stakeholder relevance versus management relevance

• Absolute versus relative

• Comparable results (peer group related to time)

• All including annual reports (‘take a lot approach’) versus focused reports (materiality)

• Information grouped by theme or integrated in the subjects

• Measured information versus non-measureable information

• Information about targets or about results

• Information about actions or about the impact of the organization

• Vague versus specific formulations

• Simple usage of language or academic usage of language

• Neutrally comparing versus subjectively comparing

Transparency Benchmark 2015 The Crystal 201544

The stakeholder as starting point

It is of great importance – also within the Transparency Benchmark – that

organizations consult their stakeholders in order to discover which themes

and topics they consider to be important for the organization. Figure 1

provides an overview of an ideal situation regarding the development of an