ifpri- food security and research gaps for agriculture development in south asia, p k joshi, ifpri

TRANSCRIPT

Food Security and Research Gaps for Agriculture

Development in South Asia

Challenges and Opportunities

P K Joshi

International Food Policy Research Institute

South Asia Regional Office

New Delhi 110012

Sri Lanka Agricultural Economics Society

Colombo, Sri Lanka

13 December 2014

International Food Policy Research Institute

Outline

Key challenges in South Asian agriculture

Opportunities in changing scenario

Research strategy and priorities

I

Key Challenges in South Asian Agriculture

International Food Policy Research Institute

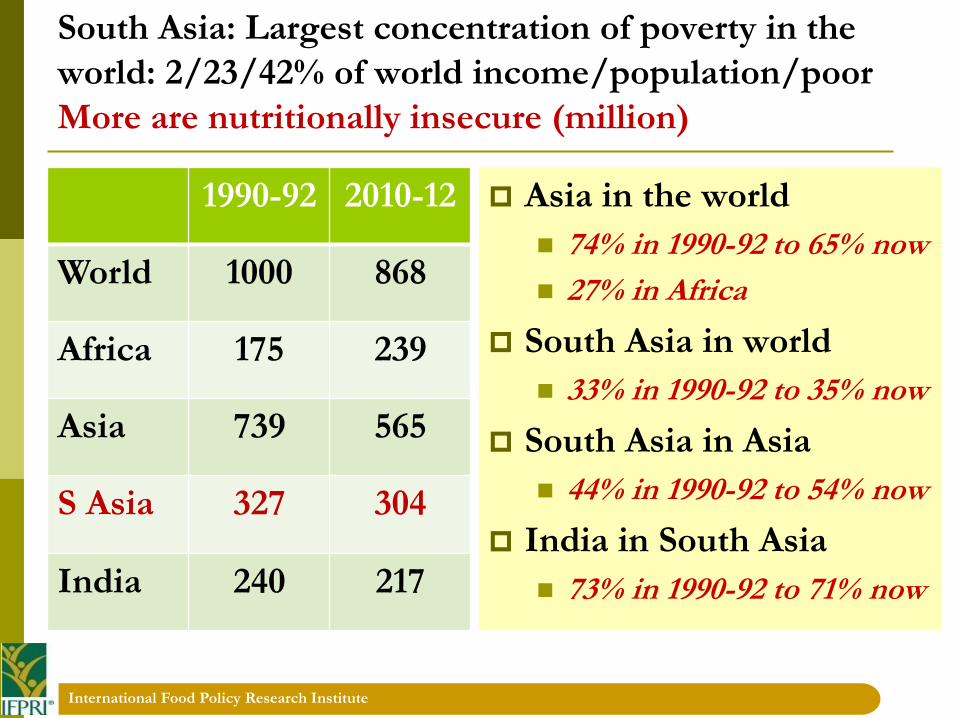

South Asia: Largest concentration of poverty in the

world: 2/23/42% of world income/population/poor

More are nutritionally insecure (million)

1990-92 2010-12

World 1000 868

Africa 175 239

Asia 739 565

S Asia 327 304

India 240 217

Asia in the world

74% in 1990-92 to 65% now

27% in Africa

South Asia in world

33% in 1990-92 to 35% now

South Asia in Asia

44% in 1990-92 to 54% now

India in South Asia

73% in 1990-92 to 71% now

International Food Policy Research Institute

Pop: 182 m.

<1.25$/day:

12.74%

NPL: 12.4%

Pop: 1.25 b.

<1.25$/day: 24.68%

NPL: 29.8%Pop: 20 m.

<1.25$/day: 4.11%

NPL: 8.9%

Pop: 156 m.

<1.25$/day: 43.25%

NPL: 31.51%

Pop: Pop: 27 m.

<1.25$/day: 23.74%

NPL: 25.2%

Extent of poverty in South Asian countries

International Food Policy Research Institute

Acute undernourishment

Country Under-nourished(%)

Children Underweight (%)

Under five mortality (%)

’90-’92 ’04-’06 ’11-’13 ’85-’92 ’03-’07 ’09-’13 ’90 ’05 ’12

Bangladesh 33.9 15.3 16.3 61.5 37.3 36.8 14.4 6.8 4.1

India 25.5 21.5 17.0 55.5 43.5 30.7 12.6 7.5 5.6

Nepal 25.4 21.8 16.0 45.6 38.8 29.1 14.2 6.1 4.2

Pakistan 27.2 22.2 17.2 39.0 30.8 31.6 13.8 10.1 8.6

Sri Lanka 33.4 28.0 22.8 31.0 21.1 21.6 2.1 1.3 1.0

South Asia 26.8 20.7 16.3 53.1 13.3 19.6 11.4 6.4 4.7

International Food Policy Research Institute

Global Hunger Index(2014): Country performance by severity

Alarming or extremely alarming levels of hunger in 16 countries

International Food Policy Research Institute

Global Hunger Index and South Asia

International Food Policy Research Institute

Environment Performance Index

International Food Policy Research Institute

Human Development Index

International Food Policy Research Institute

Other development related indices

Climate Change a big issue now

Country GEI EPI HDI

Bangladesh 112 115 129

Bhutan 98 - -

India 129 125 119

Nepal 113 38 138

Pakistan 115 120 125

Sri Lanka 74 55 91

GEI: Global Environment Index; EPI: Environment Performance Index; HDI: Human

Development Index

International Food Policy Research Institute

GDP per capita (constant 2005US$)

Country 1990 2001 2011

Bangladesh 270 362 569

Bhutan 643 1042 1917

India 403 596 1086

Nepal 233 305 385

Pakistan 525 596 756

Sri Lanka 710 1052 1725

E Asia & Pacific 554 3954 5222

International Food Policy Research Institute

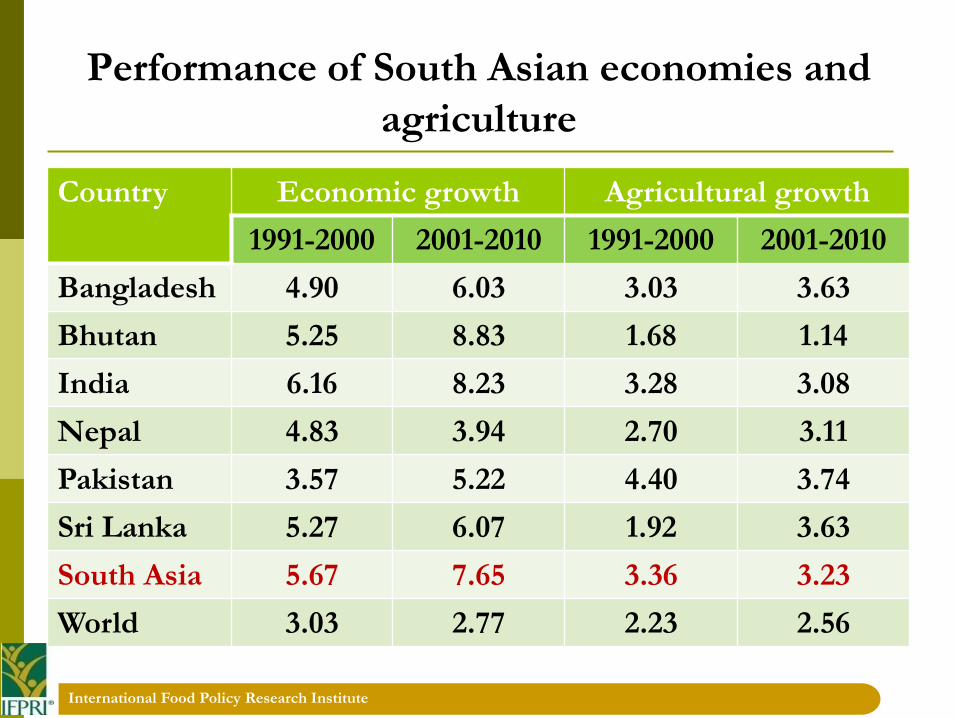

Performance of South Asian economies and

agriculture

Country Economic growth Agricultural growth

1991-2000 2001-2010 1991-2000 2001-2010

Bangladesh 4.90 6.03 3.03 3.63

Bhutan 5.25 8.83 1.68 1.14

India 6.16 8.23 3.28 3.08

Nepal 4.83 3.94 2.70 3.11

Pakistan 3.57 5.22 4.40 3.74

Sri Lanka 5.27 6.07 1.92 3.63

South Asia 5.67 7.65 3.36 3.23

World 3.03 2.77 2.23 2.56

International Food Policy Research Institute

Smallholder agriculture

0

0.5

1

1.5

2

2.5

3

3.5

0.8 0.80.9

1.23

3.11

Holding size, ha Tiny size of holdings

Majority are marginal,

having lands < 1 ha

Bangladesh 87%

India 80%

Nepal 90%

Pakistan 36%

Major objective

Food self-sufficiency

International Food Policy Research Institute

Dynamics of total factor productivity (% per year)

Country 1991-2000 2001-2005 2006-2011

Bangladesh 2.0 -0.2 3.6

India 0.8 1.5 3.7

Nepal -2.4 5.2 0.9

Pakistan 0.8 -0.9 0.6

Sri Lanka 1.6 0.5 1.9

International Food Policy Research Institute

Public spending on economic development in

agriculture

Country Public agricultural research

spending

(US$ millions)

Public

agricultural

spending as a

share of AgGDP

(%)2005 PPP 2005 US dollars

(million)

Bangladesh 125.9 44.3 0.31

India 2276.3 757.1 0.40

Nepal 22.3 7.1 0.23

Pakistan 172.3 55.3 0.21

Sri Lanka 37.5 13.1 0.34

Data available for year 2009

International Food Policy Research Institute

Weak institutions

Market risks

Long supply chains, high transactions costs and post-harvest losses

Higher transactions costs: 15% vegetables & 20% for milk

Post harvest losses: 25-30%

Low processing: 15% milk and 1 % meat processed

Access to credit

More informal sector

Food safety and quality

Rejection of consignments

International Food Policy Research Institute

Key challenge

Tackling the issue of poverty, hunger & malnutrition is

necessary without adversely affecting the natural

resources

International Food Policy Research Institute

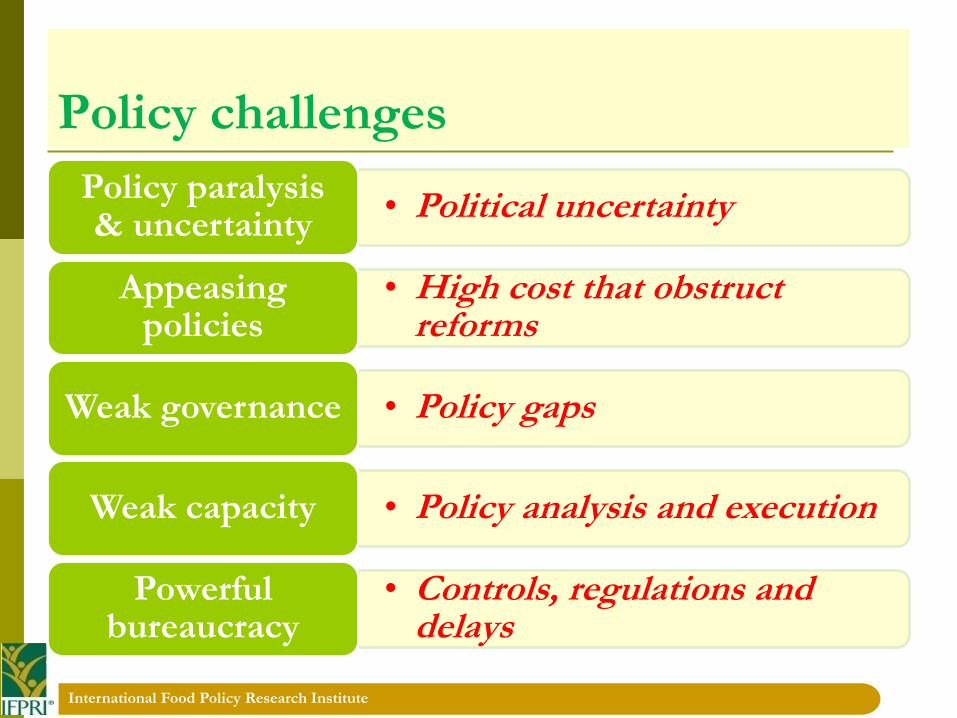

Policy challenges

• Political uncertainty Policy paralysis & uncertainty

• High cost that obstruct reforms

Appeasing policies

• Policy gaps Weak governance

• Policy analysis and execution Weak capacity

• Controls, regulations and delays

Powerful bureaucracy

II

Opportunities in Agriculture Sector in South Asia

International Food Policy Research Institute

Expenditure elasticities (based on FCDS)

Food Bangladesh India Nepal Pakistan Sri lanka

Rice -0.078 -0.016 0.016 0.025 -0.071

Wheat 0.004 -0.109 -0.111 -0.121 -0.027

Veg’bles 0.500 0.673 0.599 0.565 0.748

Fruits 0.666 0.702 0.698 0.710 0.556

Milk 0.581 0.589 0.634 0.575 0.689

Meat 0.822 0.892 0.860 0.670 0.866

International Food Policy Research Institute

Annual per capita consumption (kg)

Food item 2000 2025 Change, %

Rice 75.27 72.14 -4.16

Wheat 60.48 57.11 -5.58

Food grains 168.13 160.42 -4.59

Veg’bles 51.99 87.47 68.26

Fruits 35.17 61.87 75.76

Milk 70.42 117.45 66.80

Meat 5.35 10.90 103.62

Eggs 1.51 3.02 100.04

Fish 5.69 11.28 98.06

International Food Policy Research Institute

Annual growth in demand for food (%)

Food item 2000-15 2015-25 2000-25

Rice 1.27 0.92 1.13

Wheat 1.18 0.88 1.06

Food grains 1.24 0.91 1.11

Veg’bles 3.85 2.81 3.43

Fruits 4.04 2.98 3.61

Milk 3.79 2.82 3.41

Meat 4.70 3.51 4.22

Eggs 4.64 3.43 4.16

Fish 4.59 3.40 4.11

International Food Policy Research Institute

Production of food grain crops (m tons)

0

50

100

150

200

Pulses Maize Wheat Rice

15 12

76

152

16 16

110

182

19 22

126

189

1990 2000 2010

International Food Policy Research Institute

South Asian Countries: Production of

foodgrains (m tons)

Country Rice Wheat Maize

1990 2000 2010 1990 2000 2010 1990 2000 2010

Bangladesh 26.8 37.6 50.1 0.89 1.84 0.90 0.003 0.01 0.88

Bhutan 0.06 0.04 0.07 0.005 0.004 0.005 0.04 0.05 0.06

India 111.5 127.5 143.9 49.9 76.3 80.8 8.96 12.04 21.73

Nepal 3.5 4.2 4.0 0.85 1.18 1.56 1.23 1.41 1.86

Pakistan 4.9 7.2 7.2 14.3 21.1 23.3 1.18 1.64 3.71

Sri Lanka 2.5 2.9 4.3 - - - 0.03 0.03 0.16

International Food Policy Research Institute

Production of HVCs (m tons)

0

20

40

60

80

100

120

140

160

180

Meat Fruits Vegetables Milk

8

41

6676

11

64

94

116

18

110

132

167

1990 2000 2010

International Food Policy Research Institute

Emergence of innovative institutions: Self-help groups, contract farming, cooperatives, FPOs

Public sector initiatives

State level Agro-industries Corporation

Cooperative sector initiatives

Dairy sector; Safal

Mahagrapes; Mahabanana

Private sector initiatives

ITC

FieldFresh; Heritage

Mahindra Subhlabh

Nigger Agro; Goderej; Dabur

Venketeshwar/Saguna/ Pioneer

Multi-national firms

Nestle, Pepsi, Britannia, Perry

Opportunity for agri-input services

KHB (DCM Sriram group)

Mahindra & Mahindra

Financial institutions

Nationalized banks

Private Banks

Rise of Retail Chains

Reliance, Foodworld, MORE

Nilgiri, and many more…..

Cash & carry

Walmart, Metro

Producers’ Companies

Kaushalandera & ………

International Food Policy Research Institute

PPP initiative in Maharashtra

Crop Private sector Farmers covered

Maize Monsento, Pioneer, Vankys 6,000

Soya ADM 63,750

Pulses Rallies India 64,500

Cotton Nuziveedu Seeds 3,423

Onion Jain Irrigation system 3,423

Tomato Hindustan Lever 618

Potato PepsiCo 1,207

Grapes Mahendra 200

Sugarcane 12 sugar factories 1,200

International Food Policy Research Institute

Rise of organized food retail industry

Supermarkets and retail food chains are emerging

and linking producers and consumers

Indian alone has modern food retailing of more than

US$ 500 billion

Bring capital investments and also institutional

knowledge in procurement, distribution and sales

Reduces post-harvest losses and wastes

Improve market efficiencies (prices > 3-4 times farm gate)

Assure food quality and food safety

Provide more employment opportunities

International Food Policy Research Institute

Page 30

Private sector participation

Higher profit Access to better technology

Lower transaction costs

Involve smallholders participation

More gains to smallholders than the large farmers

Farmers receive higher prices 15-20% higher in vegetables (SAFAL case study)

25% higher in broiler (Venkateshwara Hatcheries case study)

4% higher in milk (Nestle case study)

Risk is shared As high as 88% risk is shifted by producers to the firm

III

Research Strategy and Priorities

International Food Policy Research Institute

Theory of change: 3-pronged strategy

Technologies

InstitutionsPolicies

International Food Policy Research Institute

Food security: GELWA (Gene, energy, land water)

Technologies, Policies and Institutions

Food Security

Land

Water

Gene

Energy

International Food Policy Research Institute

Indian illustration: Government strategy for

ensuring food security (national and household)

• Food Security Mission

• Subsidy in fertilizer and irrigation

• MSP and assured procurementProduction

• Food reserve and stocks (>80 million ton)

• 500 thousand fair price shopsAvailability

• Mahatma Gandhi National Rural Employment Guarantee Program

• Direct Cash TransferAccess

• Subsidized food to people BPL

• Food Security Bill (Right to Food)Affordability

International Food Policy Research Institute

Regional cooperation

SAARC Food Bank– Committed reserve: 486,000 metric tons

– India sharing 306,400 metric ton (about 63%)

SAARC Seed Bank (agreement signed in 2011)

Member country is will contribute 1 % of total seed requirement

SAFTA Trade increased (US$69K in 2006 to US$342 million in 2012; with a

peak of USD 663 million in 2010

Intra-SAARC trade is mere 2 per cent of total external trade; intra-ASEAN trade is 25% of all external trade

India (65%) and Bangladesh (27%) are major contributors (92%) inintra-regional trade

International Food Policy Research Institute

Promote climate smart agriculture (Source: Aggarwal 2010)

Climate Smart

Nitrogen smart

Water smart

Energy smart

Carbon smart

Weather smart

Knowledge

smart

Policy smart

Climate smart interventions (FAO)

Adapting/mitigating climate change

Ensure reducing the risk arising due to climate change

Augmenting farm income.

Triple wins (World Bank)

Higher yields, more carbon sequestration, and greater resilience to heat and drought

Feasible interventions

Resource endowments

Capacity indicators

International Food Policy Research Institute

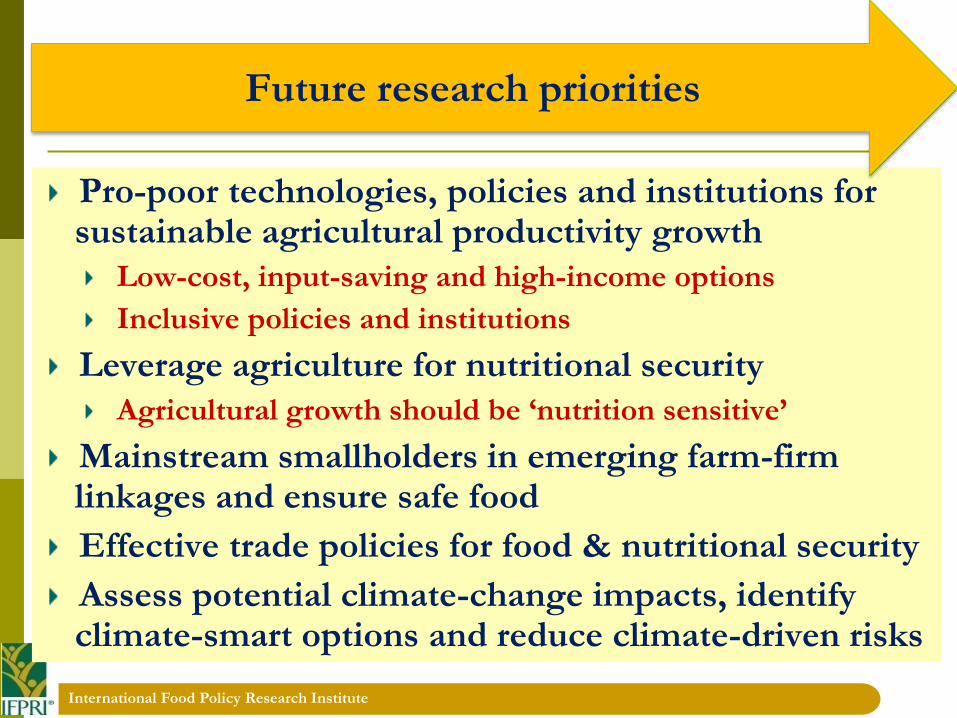

Pro-poor technologies, policies and institutions for sustainable agricultural productivity growth

Low-cost, input-saving and high-income options

Inclusive policies and institutions

Leverage agriculture for nutritional security

Agricultural growth should be ‘nutrition sensitive’

Mainstream smallholders in emerging farm-firm linkages and ensure safe food

Effective trade policies for food & nutritional security

Assess potential climate-change impacts, identify climate-smart options and reduce climate-driven risks

Future research priorities

International Food Policy Research Institute

Exchange knowledge and technologiesLeverage agriculture for food & nutrition security

Pro-poor technologies for sustainable agricultural productivity growthLow-cost, input-saving and high-income options

Promote regional tradeNiche commodities for within and outside the region

Best practices for ensuring food securitySocial safety net programs and institutional innovations

Climate changeClimate smart policies and institutions for building resilience

Capacity developmentBest practices

Policy analysis

Five issues for regional cooperation

Thank you