hungarian energy and climate strategy - rekk

TRANSCRIPT

Hungarian Energy and Climate

Strategy

Quick summary of 2030 and 2050 energy and climate objectives

2

-

0,500

1,000

1,500

2,000

2,500

3,000

3,500

-

0,100

0,200

0,300

0,400

0,500

0,600

0,700

0,800

200

0

200

2

200

4

200

6

200

8

201

0

201

2

201

4

201

6

201

8

202

0

202

2

202

4

202

6

202

8

203

0

t C

O2eq

/mil

lió F

t

toe/

mil

lió F

t

Energiaintenzitás ÜHG-intenzitás

Energy and GHG intensity of Hungarian GDP

2000 - 2030

Energy intensity GHG intensity

Major energy and climate objectives for Hungary

2018: + 5,1% GDP, - 0,7% GHG

Table of Contents

The new National Energy Strategy and National Energy and Climate Plan (2030, with an outlook up to 2040)

Achievements of the Hungarian Energy and Climate policy

2

Achievements of the Hungarian Energy and Climate

policy

3

Integrated State Secretariat for Energy and Climate Policy within the

Ministry for Innovation and Technology (ITM)

Authority, Predictability, Accountability

• Governance of Energy and Climate Policy under the same

Secretariat since mid-2018

• Climate Policy is not (only) a green issue, but a new

economic development model (green growth)

• In line with integrated EU policies on climate and energy (2030 climate & energy framework, Clean Energy Package, National

Energy and Climate Plan)

• Other MIT competences provide for valuable synergies:

• Transport sector is the second largest GHG emitter

• Innovation and R&D is crucial to achieve long-term goals

• Economic development towards green growth

• Education is playing a key role in raising awareness

Strategy-making and planning (new National Energy Strategy, integrated Energy and Climate

Plans

Planning the use of

development funds

National Climate Authority

Legislation

Carbon allowance

allocation & trade

Measures to implement strategic objectives

Establishing strategic objectives

4

Hungary ranks the 9th best (with Denmark) in reducing GHG emissions

Reduction of GHG emissions in Hungary, 1990 - 2017

• 32% GHG emission reduction compared to 1990

• Several – ambitious – Member States have not

produced any reduction since 1990

• The Hungarian GHG emission per capita is only

75% of the EU average (the 6th lowest value)

energy agriculture waste IPPU

(kiloton)

5 Source: Hungarian NECP

Hungary is committed to achieve climate neutrality by 2050

International requirements

European goals

Carpathian Basin

Hungary

United Nations Framework

Convention on Climate Change

Clean Energy Package,

European Green Deal

Scientific evidence on climate change

impacts on the Carpathian Basin

Public survey and consultations on

preferences for climate protection

7

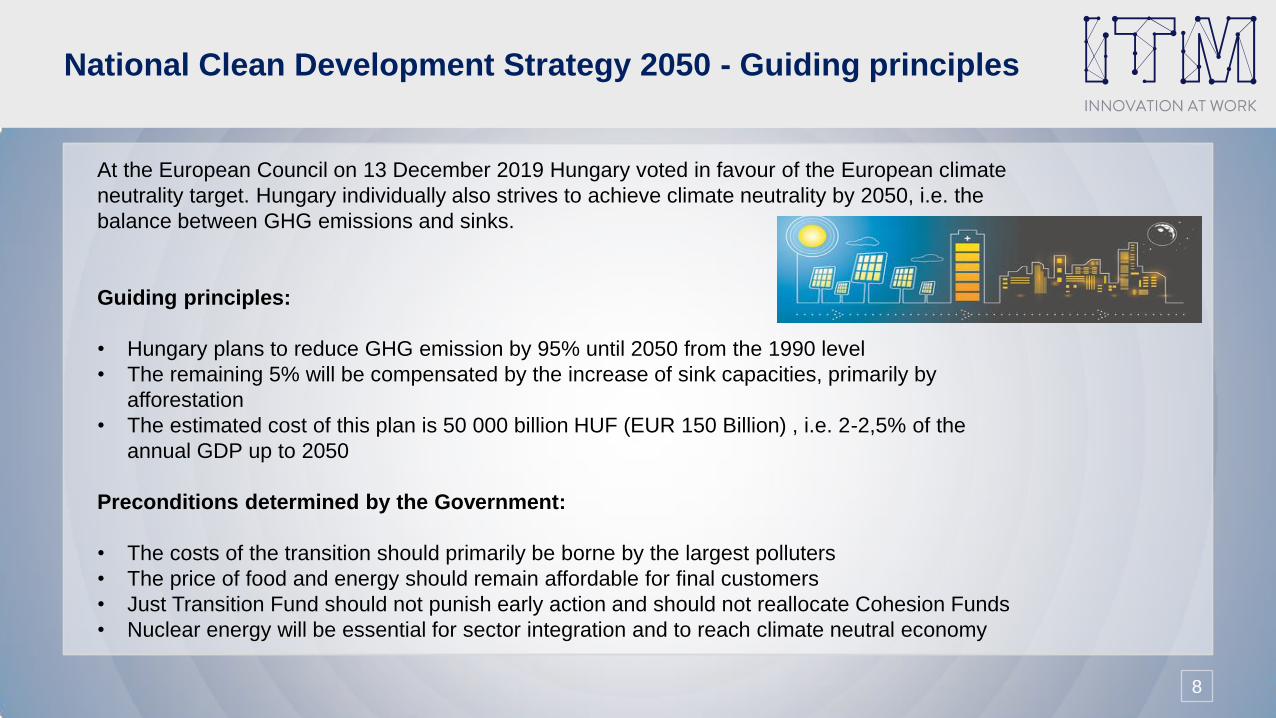

National Clean Development Strategy 2050 - Guiding principles

8

At the European Council on 13 December 2019 Hungary voted in favour of the European climate

neutrality target. Hungary individually also strives to achieve climate neutrality by 2050, i.e. the

balance between GHG emissions and sinks.

Guiding principles:

• Hungary plans to reduce GHG emission by 95% until 2050 from the 1990 level

• The remaining 5% will be compensated by the increase of sink capacities, primarily by

afforestation

• The estimated cost of this plan is 50 000 billion HUF (EUR 150 Billion) , i.e. 2-2,5% of the

annual GDP up to 2050

Preconditions determined by the Government:

• The costs of the transition should primarily be borne by the largest polluters

• The price of food and energy should remain affordable for final customers

• Just Transition Fund should not punish early action and should not reallocate Cohesion Funds

• Nuclear energy will be essential for sector integration and to reach climate neutral economy

The new National Energy Strategy and National Energy and Climate

Plan (2030, with an outlook up to 2040)

0

10

20

30

40

50

60

70

80

90

1001990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Sh

are

of

imp

ort

(%

)

Primer belföldi energia Szén- és lignit Földgáz

Kőolajtermékek Nyersolaj Villamos energia

Coal and lignite

Crude oil Electricity

10

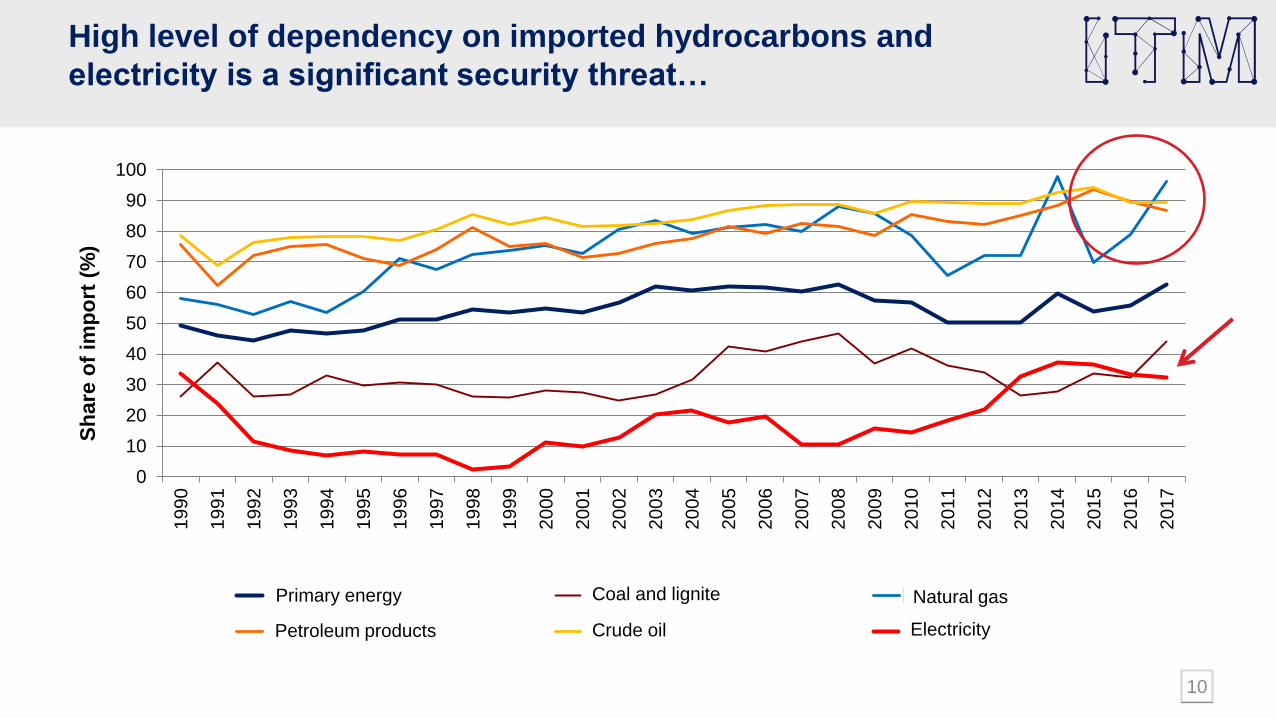

High level of dependency on imported hydrocarbons and

electricity is a significant security threat…

Primary energy

Petroleum products

Natural gas

1. Consumers are in the focus

3. Climate-friendly transformation of the energy

sector

2. Further strengthening security of supply

4. Promoting innovation and economic development

CLEAN, SMART, AFFORDABLE ENERGY

Implementation of flagship programmes and ~40 measures

…therefore, the primary objective of Hungary’s energy and climate

strategy is to strengthen energy independency

11

12

Balance

• Combating climate change

• Competitiveness

• Security of supply

Cost effectiveness

• GDP convergence

• Underdeveloped regions

Importance of additional benefits • Combating climate change +

decreasing import dependency + affordable prices + innovative economic development

Technology neutrality

• Energy efficiency measures

• RES utilization

• Maintenance of nuclear capacities

Fair transition

No one is left behind

Basic principles The Commission’s recommendations and the results of administrative,

regional and stakeholder consultations were built into our final NECP and NES.

The methodology of the two strategic documents have also been further

developed. (HU-TIMES model)

The two strategic documents complement each other.

Simultaneous finalization of NECP

and new National Energy Strategy

(NES)

All of our relevant strategies (NECP, NES) and action plans

(I. Climate Change Action Plan) should serve economic

development

Economic development and combating climate change are

mutually reinforcing objectives

Dimensions

of Energy

Union

Indicators

EU targets for

2030

Hungarian targets for

2030

Recent Hungarian

situation (2017)

Most important measures

De

ca

rbo

niz

ati

on

Reduction of GHG emission (%)

compared to 1990 min. -40% min. -40% -31.9 % Climate-friendly

transformation of the

electricity sector

Energy efficiency obligation

scheme

Greening transport

GHG intensity of GDP continuous decrease 1,98 t

CO2eq/million HUF

Reduction of GHG emission in

the non-ETS sector (%)

compared to 2005

min. -10% min. -7% -9.3%

Share of RES in gross final

energy consumption

min. 32% min. 21% 13.33%

Photovoltaics (PV)

E-mobility

Green District Heating

Program

En

erg

y

eff

icie

nc

y

Final energy consumption Indicative 32.5%

reduction

max. 785 PJ

The source of any

extra consumption can

be only RES between

2030 and 2040

775 PJ

Reduction of final

consumption by 0.8% per

year

Promotion of energy

efficiency investments in

industry

Comparison of EU and Hungarian targets for 2030

Nuclear, RES, energy efficiency and innovation = enhancement of

energy independency, affordable prices, economic development

13

14

-

500 000

1 000 000

1 500 000

2 000 000

2 500 000

3 000 000

3 500 000

4 000 000

4 500 000

5 000 000

-

10 000

20 000

30 000

40 000

50 000

60 000

70 000

80 000

90 000

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

2026

2028

2030

HU

F p

er c

ap

ita

kto

e; k

t C

O2eq

Végsőenergia-fogyasztás (ktoe) ÜHG kibocsátás (kt CO2e) GDP Ft/fő

-

0,500

1,000

1,500

2,000

2,500

3,000

3,500

-

0,100

0,200

0,300

0,400

0,500

0,600

0,700

0,800

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

2026

2028

2030

t C

O2eq

/mil

lion

HU

F

toe/

mil

lion

HU

F

Energiaintenzitás ÜHG-intenzitás

Calculated and estimated values of Hungarian GHG emission,

GDP per capita and final energy consumption, 2000-2030

Estimated values of energy- and GHG-intensity in Hungary,

2000-2030

Improved intensity indicators 2018: 4.9% increase of GDP, -0.7% decrease of GHG emission

Source(historic data): Eurostat

GHG emission is expected to decrease by at least 40%

until 2030 compared to 1990

Achieving our targets means that the energy- and GHG-intensity of

our GDP will be further decreased - we must continue this trend

Final energy consumption

(ktoe) GHG emission

(ktCO2e)

GDP per

capita Energy intensity GHG intensity

1. We place the Hungarian consumers in the focus of the new

national energy strategy (orange: priority proposals green: on-going projects with positive

results)

15

Strategic goals Projects

1 Keep energy price affordable for consumers

Enhancing competition in wholesale electricity and natural gas product markets

Introduction of energy efficiency obligation scheme to stimulate consumers’

energy-savings

Upgrading price regulation in the electricity, gas and district heating sectors

while preserving the results of the existing policy to keep energy price

affordable

2 Support local, decentralized RES production and

self- consumption

Promotion of renewable energy utilization in households

Encouraging the establishment of energy communities

Supporting local, renewable energy-based investments

3 Empower consumers to choose and control their

consumption

Smart metering program in the electricity and gas sector

Equip households connected to district heating with heat cost allocators making

their consumption measurable and controllable

Digitalization of supply service

Encouraging demand response (DSR); new regulations to help independent

aggregators to enter into the market

Creating differentiated Universal Service Packages in the electricity and gas

sectors

2. We will strengthen our energy supply security (orange: priority proposals ; green: on-going projects with positive results )

1 Decrease import dependence by increasing

local renewable energy production and by

exploring domestic hydrocarbon reserves

We will establish a Geothermal Exploration Risk Fund

Fine tuning of the successful hydrocarbon and geothermal concession

system

Supporting the exploration and exploitation of domestic non-conventional

hydrocarbon reserves

Supporting the production and consumption of biogas, biomethane, and

clean hydrogen in order to mitigate natural gas consumption

2 Strengthen the integration of the regional

electricity and gas markets

Building of a Hungarian-Slovakian, a Hungarian-Slovenian and a new

Hungarian-Romanian cross-border electricity transmission line

Gas market coupling between Hungary and Croatia

Promoting projects that can strengthen the regional role and liquidity of our

organized electricity and gas markets

3 Continue gas diversification to reach Black Sea

reserves and LNG sources, and improve the

competitiveness of strategic storage facility

Developing Romania-Hungary gas interconnector to enable an increased

flow and reverse flow; Hungarian-Slovakian-Austrian gas corridor,

Hungarian-Slovenian-Italian gas corridor

Access to LNG

Improvement of the regional competitiveness of our strategic gas storage

facilities

4 Guarantee the security of supply and stable

functioning of the electricity network to back up

increasing RES

Introduction of a strategic reserve system or network/breakdown backup

Strategic goals Projects

16

3. We will implement the climate-friendly transition of our energy sector (orange: priority proposals ; green: on-going projects with positive results )

1 Further decarbonize the electricity sector

Significant increase in PV capacities, introduction of RES-E

tendering

Replacement of the capacity of Paks Nuclear Power Plant

Integration of renewable electricity production by new regulations

that increase the flexibility of the power system

Transition plan and related regional development program for the

restructuring of lignite-fired Mátra Power Plant and for Heves

county

2 Support the reduction of energy consumption by

innovative solutions

(Price) regulation that encourages cost-effectiveness and

climate-friendly transformation in the energy sector (electricity,

gas, district heating)

3 Make district heating greener and more competitive

Program for energy efficient and RES-based district heating

Increased use of non-recyclable waste for heat generation on the

basis of waste hierarchy

Strategic goals Projects

17

4. We will take advantage of the opportunities in economic development

provided by energy innovation and combating climate change (orange: priority proposals ; green: on-going projects with positive results )

Strategic goals Projects

1 Support innovations in the energy sector Creation of a regulatory environment that promotes innovative solutions

Elaboration and implementation of innovative pilot projects

2 Implement the Second National Climate Change

Strategy Preparation of the Hungarian Climate Change Assessment Report

3 We will implement the Green Transport Program

Promote the domestic production of second-generation biofuels

Development of electro-mobility and alternative fuel infrastructure

Implementation of the Green Bus Program

Encouraging combined rail-and-road transport

4 Enable SMEs, companies to go green

Promotion of renewable self consumption and energy efficiency

investments in the private sector

Modernization of SME’s production technologies in terms of energy

efficiency

Fine tuning of energy efficiency investment related Corporate Tax

Advantage

5 Create opportunities for economic development

provided by the adaptation to climate change

Water management projects at Lake Balaton and other places;

Western Balkan Green Fund 18

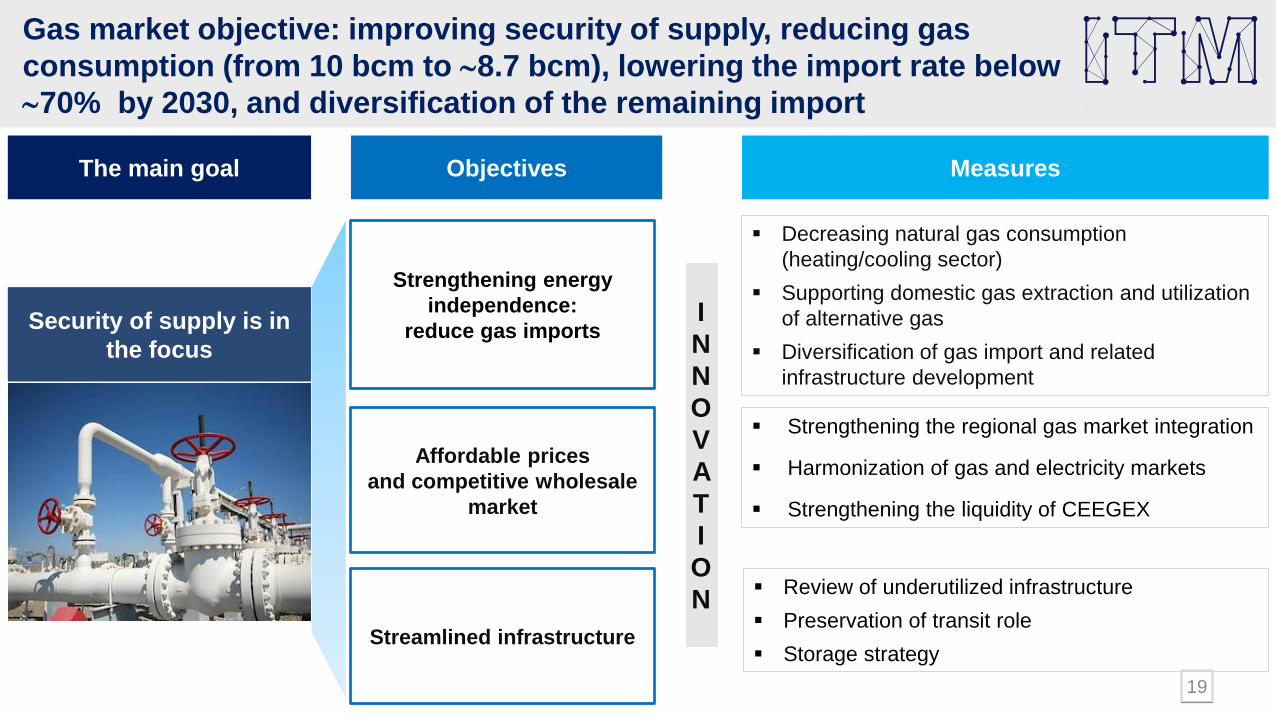

Security of supply is in

the focus

Decreasing natural gas consumption

(heating/cooling sector)

Supporting domestic gas extraction and utilization

of alternative gas

Diversification of gas import and related

infrastructure development

Strengthening the regional gas market integration

Harmonization of gas and electricity markets

Strengthening the liquidity of CEEGEX

The main goal

I

N

N

O

V

A

T

I

O

N

Objectives

Review of underutilized infrastructure

Preservation of transit role

Storage strategy

19

Gas market objective: improving security of supply, reducing gas

consumption (from 10 bcm to 8.7 bcm), lowering the import rate below

70% by 2030, and diversification of the remaining import

Measures

Strengthening energy

independence:

reduce gas imports

Affordable prices

and competitive wholesale

market

Streamlined infrastructure

Implementation of gas market diversification:

access to 4 sources (Russia, Croatia, Austria, Romania) and LNG

Pipeline gas

import Biogas,

biomethane

Domestic gas

reserves

Diversification

„Clean”

hydrogen

20

LNG

1 2 3 4 5

Infrastructure

development

Improving the

calculability of the

concession system

Promotion of biogas-

production via

obligatory feed-in

system

Launch of a pilot-

project to examine the

potential of blending

clean hydrogen and

natural gas

Electricity market transition 2040: No1 flagship

Decarbonising the power

sector

• 90% in 2030 vs 60% in 2020

Maintain nuclear capacity

Phase out lignite

Solar-heavy RES-E

portfolio: 6.6 GW by 2030;

12 GW by 2040

Gas based generation as

primary backup

Network development

Flexibility market

1 million smart meters

Import ratio: 20% in 2040

21

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

2017 fact Existing policies Natural gascapacity

replacement

Rapiddecarbonisation

Natural gas andrenewables

Balanced PV-centered

Inst

alle

d c

apac

ity,

MW

Nuclear Coal Natural gas Oil PV Wind Biomass Other renewable

Current and potential future fuel mix

scenarios, 2040

Hungarian renewable electricity portfolio fits well into the regional one

22

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Au

sztr

ia-2

01

7

Au

sztr

ia-2

03

0

Cse

hors

zág-2

01

7

Cse

hors

zág-2

03

0

Ho

rvát

ors

zág

-20

17

Ho

rvát

ors

zág

-20

30

Len

gy

elo

rszá

g-2

017

Len

gy

elo

rszá

g-2

030

Mag

yar

ors

zág

-20

17

Mag

yar

ors

zág

-20

30

Rom

ánia

-20

17

Rom

ánia

-20

30

Sze

rbia

-20

17

Sze

rbia

-20

30

Szl

ov

ákia

-20

17

Szl

ov

ákia

-20

30

Szl

ov

énia

-20

17

Szl

ov

énia

-20

30

Öss

zesí

tett

-201

7

Öss

zesí

tett

-203

0

Víz Szél Nap Egyéb

Cro

atia

201

7

Cro

atia

203

0

Pol

and

2017

Pol

and

2030

Hun

gary

201

7

Hun

gary

203

0

Rom

ania

201

7

Rom

ania

201

7

Ser

bia

2017

Ser

bia

2030

Slo

veni

a 20

17

Slo

vaki

a 20

17

Slo

vaki

a 20

30

Slo

veni

a 20

30

Allt

oget

her

2017

Allt

oget

her

2030

hydro

wind

PV

other

• RES-E sources: PV

and biomass • the most cost

efficient and most

favorable

conditions

• Fits well into the

balanced regional

renewable portfolio: • Poland: wind

• Romania, Austria:

hydro, wind

• Balkan: hydro

Estimated share of different renewable electricity production technologies within the CE region

Aus

tria

201

7

Aus

tria

203

0

Cze

ch R

epub

lic 2

017

Cze

ch R

epub

lic 2

030

Source: Eurostat, NECP of Hungary, NECP drafts

Innovative system stability (flexibility storage and demand management)

Encouraging the introduction of innovative energy service modes

Innovation program for improving energy efficiency

Innovation in the utilization of our domestic natural gas reserves

„Smart regulation” to create an interest in innovation for distributors and suppliers

Greening transport

Innovation in the promotion of renewable energy sources

Innovation in nuclear energy

Innovative seasonal storage solutions for electricity and heat

Main areas of intervention in the field of energy-related innovations:

Energy Innovation is an important tool to transforme our energy sector into a climate-friendly system, while creating opportunities for industrial development and contributing to economic growth.

23

Regional development program:

▪ Establishment of a V4 Innovation Platform

24

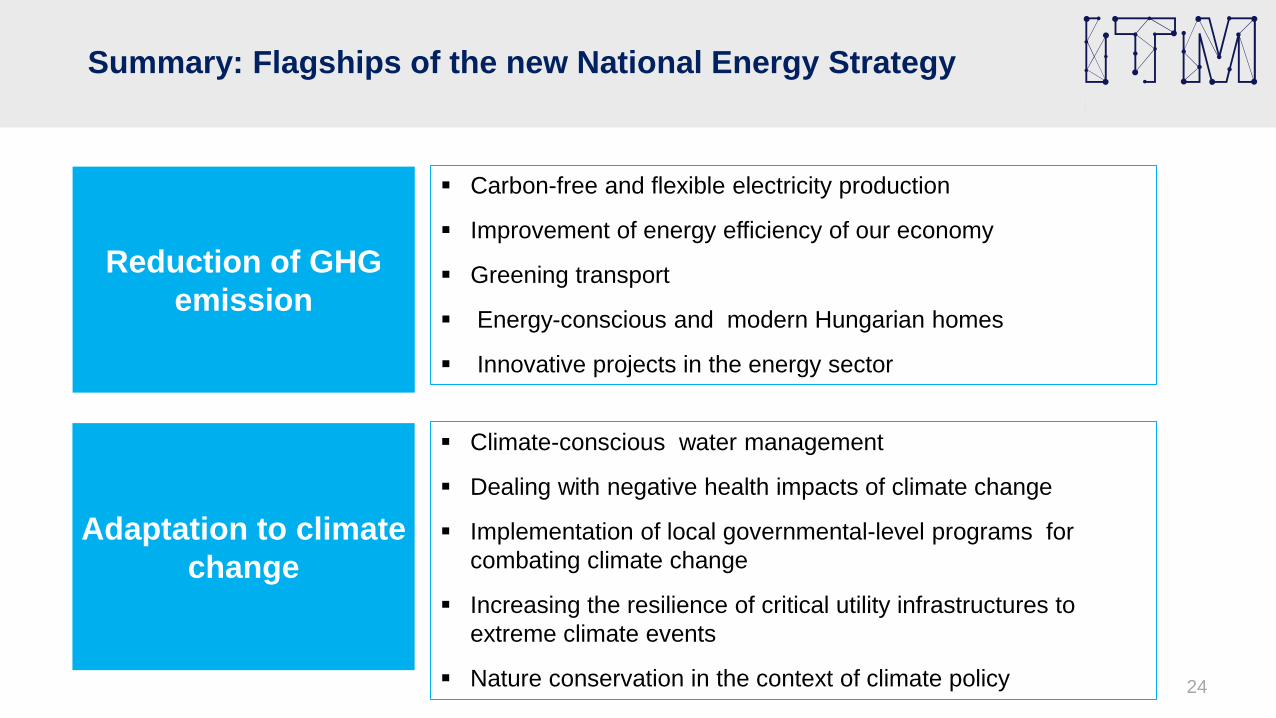

Summary: Flagships of the new National Energy Strategy

Carbon-free and flexible electricity production

Improvement of energy efficiency of our economy

Greening transport

Energy-conscious and modern Hungarian homes

Innovative projects in the energy sector

Reduction of GHG

emission

Climate-conscious water management

Dealing with negative health impacts of climate change

Implementation of local governmental-level programs for

combating climate change

Increasing the resilience of critical utility infrastructures to

extreme climate events

Nature conservation in the context of climate policy

Adaptation to climate

change 24

-2000

0

2000

4000

6000

8000

10000

2020 2025 2030 2035 2040

Kö

ltsé

ge

k vá

lto

zása

(W

AM

-WE

M)

/Mrd

Ft/

Beruházási költségek változása Fix OM költségek változása

Változó OM költségek változása Nettó teljes költség változás

Expected costs:

The total discounted system cost is

an additional 20.400 bn HUF (62 bn

EUR) compared to the WEM

scenario by 2040

It excludes the costs of grid

development: min. 500 bn HUF (1.5

bn EUR)

The investment need is expected to

be the highest between 2025 and

2030: worth waiting for the

introduction of new technologies

until their costs decline

Further cost reduction can be

achieved through lower operation

costs of the new technologies!

Costs of the implementation of additional measures (WAM scenario):

Achieving Hungary’s 2030 targets will cost 14.000 bn HUF (42 bn EUR) + Paks 2 =

18.000 bn HUF (55 bn EUR), and for 2040 it is estimated at 20.400 bn HUF (62 bn

EUR)

25

Investment costs

Net total costs

Fixed O & M costs

Variable O & M costs

Cha

nges

of c

osts

in W

AM

com

pare

d to

WE

M (

bn H

UF

)

Thank you

for your attention.