how does regulation affect the risk taking of banks? a u.s. and

TRANSCRIPT

Journal of Comparative Policy Analysis: Research and Practice 3: 59–83 (2001)c© 2001 Kluwer Academic Publishers. Printed in The Netherlands.

How Does Regulation Affect the Risk Takingof Banks? A U.S. and Canadian Perspective

JILL M. HENDRICKSON [email protected] of the South, 735 University Avenue, Sewanee, TN 37383-1000

MARK W. NICHOLSUniversity of Nevada, Reno, NV 89557

Key words: commercial banking, U.S. banking, Canadian banking, regulation, risk

Abstract

This historical study utilizes annual insured bank data from 1936 through 1989 to empirically eval-uate the impact of bank regulation on bank risk taking in a cross-country comparison of the UnitedStates and Canada. Risk is hypothesized to be determined, in part, by the regulatory environment inwhich a bank operates. The findings of this analysis contributes to the contemporary deregulationpolicy debate, since both branch banking restrictions and deposit insurance variables are foundto be detrimental to bank stability. More specifically, these results support the 1994 Riegle–NealInterstate Banking and Branching Efficiency Act, which removed legislative barriers to interstatebranching. These results also confirm expectations that deposit insurance increases risk taking andsupports the 1991 mandate by regulators that risk-based deposit insurance be created. Further,these findings support the 1988 Basel Accord to standardize bank capital requirements interna-tionally and to link these standards to bank risk taking.

Introduction

The structure of the U.S. commercial banking system has been undergoingprodigious change in the last two decades, and with the recent wave of merg-ers and proposed bills for deregulation, further change is inevitable. Withinthe last two decades, the banking system has been transformed by severalimportant developments: failure rates not seen since the Great Depression;deregulation of a regulatory structure constructed largely as a response tothe Great Depression; a rise in the number, and size, of bank mergers; anda large influx of competition from nonbank institutions. In response to thesedevelopments, scholars and policymakers are reevaluating the bank regulatoryenvironment in attempts to reestablish a stable and profitable banking sys-tem. Though many of the policy proposals that have been advanced call forcontinued deregulation, others caution that deregulation may further disruptand destabilize the system at a time when greater uncertainty and increasedcompetition characterize the banking environment. By examining the historical

60 HENDRICKSON AND NICHOLS

performance of banking relative to the regulatory structure, the present articleoffers insight into the contemporary debate surrounding the deregulation ofcommercial banking in the U.S. Specifically, this study considers what impactthe postwar regulatory structure had on the propensity towards risk taking ofcommercial bankers. This result is accomplished by comparing the U.S. postwarregulatory structure with that in Canada and using this comparison to explainrisk.1 In addition to bank risk, this study also examines the relationship betweenregulation and the incidence of bank failures, which, obviously, is related to bankrisk.2

While there are limits to making cross-country comparisons, the historicallycomparable levels of economic development and similar social and politicalenvironments in these two countries make Canada and the U.S. natural choicesfor comparison.3 Moreover, the stark contrast between the two countries interms of their regulatory environment and the number of bank failures deservesattention. This is especially true given the growing body of literature postulatingthat regulation has exacerbated the problem of bank instability.

The next section reviews the literature on the relationship between U.S. bankregulation and instability. The purpose of financial regulation and a discussion ofthe historically different regulatory environments between the U.S. and Canadafollow. Our models of bank risk and failures, as well as the empirical results, arethen presented followed by our conclusions.

Competing theories of bank regulation

Two general theories of regulation, namely, the public interest approach andthe self-interest theory, attempt to explain why regulation is relied upon in mar-ket systems. The public interest approach to regulation suggests that regula-tory measures are designed to protect against market failure, notably naturalmonopoly, imperfect information, and externalities (Litan and Nordhaus, 1983).Under the public interest approach, bank regulation, such as deposit insuranceand limitations on investment activity, exist for the benefit of the consumer. Bankregulation, for example, protects the consumer’s assets and reduces depositorexposure to the risk of bank failure and insolvency.

In contrast, the “capture’’ or self-interest theory of regulation, introduced byStigler (1971) and later expanded by Peltzman (1976) and others, suggests thatinterest groups seek regulation primarily for the benefits it produces for them.For banks, such regulation might be in the form of restricting entry into bankingservices and limiting access to potential substitutes.

Commercial banking has long been one of the most regulated industries inthe U.S. Legal restrictions and requirements (e.g., strict reserve requirements,prohibition on branching, and collateral requirements against currency) wereplaced on the first state and nationally chartered banks. The current regulatorystructure stems largely from the Banking Acts of 1933 and 1935, both of whichwere introduced as a consequence of the Great Depression and associated

HOW DOES REGULATION AFFECT THE RISK TAKING OF BANKS? 61

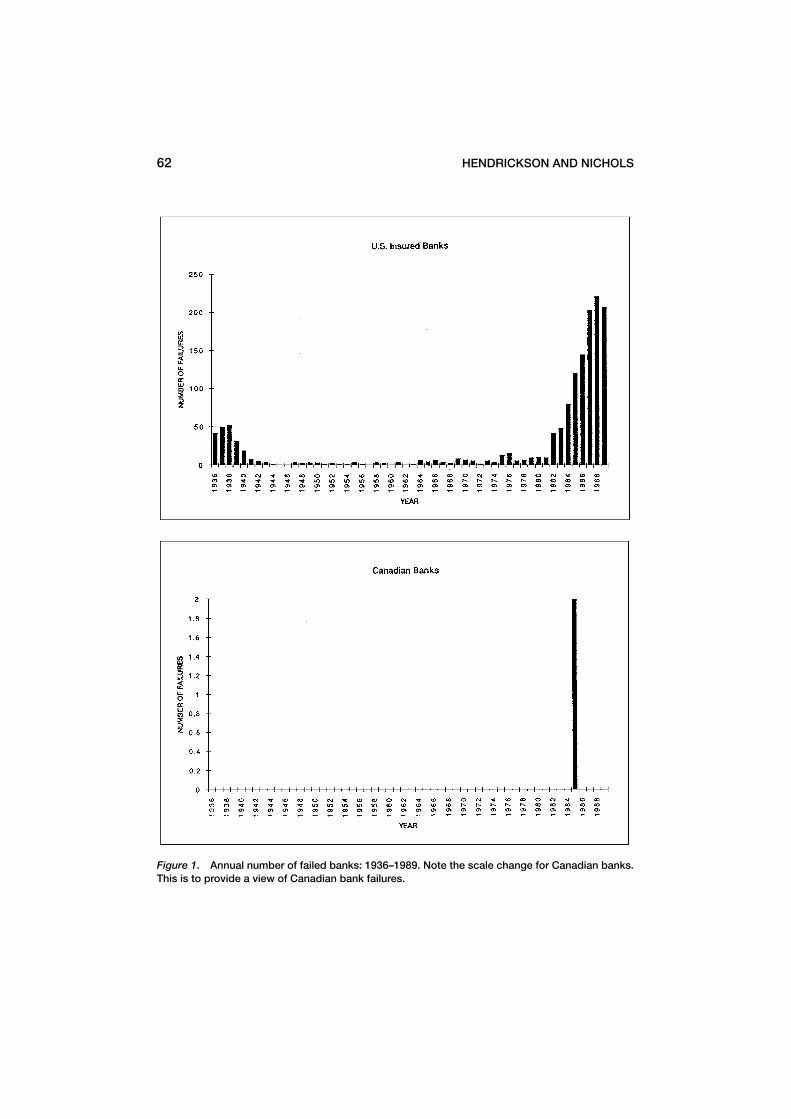

bank crisis. This regulatory structure appears to have increased stability duringthe first few decades (see Figure 1), but more recently there has been an increasein the number and size of bank failures. This pattern has led to a debate overregulation’s impact on bank stability.

In his book, What Should Banks Do?, Litan (1987) notes that “most bankswere primarily limited to accepting deposits and making loans; to conductingbusiness in their home states or even home countries; and to paying interest ondeposits at rates no higher than federally authorized ceilings.” He further notesthat “the various limitations were designed to ensure the safety and soundnessof depository institutions, to prevent conflicts of interest that could distort creditallocation, and to minimize aggregations of wealth and political power.”

Based on the above work of Litan (1987), it appears as though bankingregulation was, at least initially, consistent with the public interest theory ofregulation. If this is so, why the recent call for deregulation? Won’t deregula-tion harm consumer’s and destabilize the industry? Indeed, many other schol-ars espouse the public interest theory of regulation. Spong (1990), for exam-ple, advances three overriding objectives of bank regulation: protection of de-positors, stability of the payments system, and promotion of an efficient andcompetitive bank sector. Regulation to protect depositors under a fractionalreserve system came primarily in the form of federal deposit insurance fol-lowing the losses to depositors during the Great Depression. Regulating de-posit activity, e.g., deposit interest rates, deposit use, and deposit insurance,enhances monetary stability because of the crucial role commercial banksplay in controlling the amount of money in the economy. Finally, bank reg-ulation ensures that competitive prices exist on services such as loans anddeposits.

Edwards and Scott (1979), on the other hand, argue that the fundamental ob-jective of financial regulation is to preserve the solvency of banking institutions(1979, p. 66).4 In the process, depositor assets may be protected and the mon-etary system stabilized, but these consequences are secondary to the goal ofminimizing insolvencies.

More specifically, Edwards and Scott argue that the Federal Reserve’s roleof lender of last resort, federal deposit insurance, and a host of detailed regu-lation (e.g., price controls, activity restrictions, entry restrictions, and balancesheet requirements) are all meant to protect the solvency of commercial banksin the U.S. While deposit insurance may appear to be directed at protecting theindividual depositor, its primary purpose is to reduce or eliminate bank runs.Similarly, price controls (e.g., deposit rate ceilings), entry restrictions (e.g., lim-its on intrastate and interstate branching and charter requirements), and activ-ity restrictions (e.g., partial separation of commercial and investment banking)all limit competition and protect banks from failure. Finally, regulated balancesheet requirements, such as capital requirements, are defended on groundsthat holding capital reduces banks’ susceptibility to deposit withdrawals andfailure.

62 HENDRICKSON AND NICHOLS

Figure 1. Annual number of failed banks: 1936–1989. Note the scale change for Canadian banks.This is to provide a view of Canadian bank failures.

HOW DOES REGULATION AFFECT THE RISK TAKING OF BANKS? 63

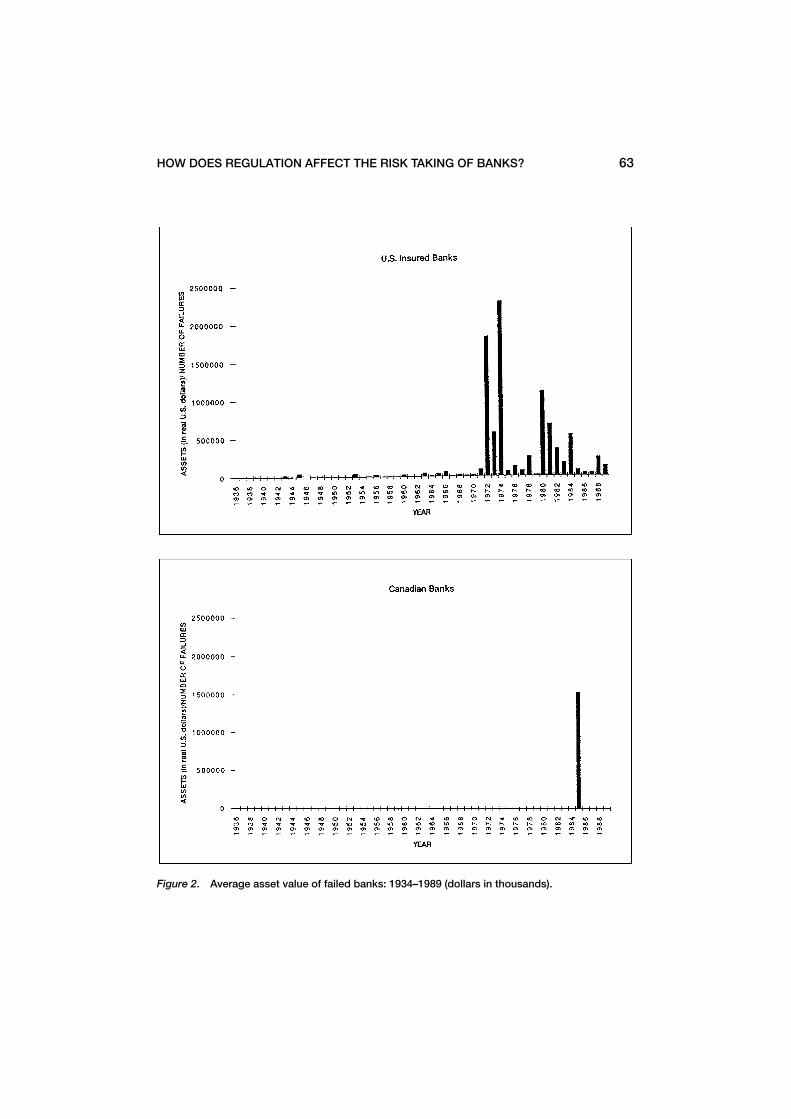

Figure 2. Average asset value of failed banks: 1934–1989 (dollars in thousands).

64 HENDRICKSON AND NICHOLS

Edwards and Scott conclude, however, that such a regulatory environment isexcessive. Many of the existing regulations are ineffective or counterproductive.Further, the lack of competition in banking imposes a high cost on society.Therefore, selective deregulation would improve social welfare.

In contrast to the work of Spong or Edwards and Scott, other scholars suggestthat the recent instability in the U.S. commercial banking sector is a conse-quence of excessive government regulation and changing economic condi-tions.5 Litan (1987) notes that the environment in which banks operate haschanged dramatically in recent years. In particular, high inflation, which droveup interest rates and spawned the explosion of money market mutual fundsand other substitutes for traditional bank deposits, and rapid advances ininformation technology have made obsolute the depression era controls placedon banking. Indeed, faced with this changing economic and competitive en-vironment and the inability to diversify into other lines of business, the veryregulation that was intended to ensure bank solvency now threatens thatstability.

In later work, Litan (1997) classifies bank regulation into two paradigms: theprevention–safety net paradigm and the competition–containment paradigm.The prevention–safety net paradigm describes the post-Depression era of bankregulation in the United States in which the regulators sought to prevent fur-ther individual bank failures and, at the same time, expanded a safety net toprotect individual depositors and creditors from loss. Regulations under thisparadigm include limits on bank activity, capital standards, and deposit insur-ance. Litan argues that the intent of this regulation has been to minimize therisk of bank failure and depositor loss. However, he would also argue that thesevery regulations, which aimed at minimizing risk and enhancing stability, ulti-mately were responsible for creating incentives for increased risk taking by theU.S. commercial banker and for destabilizing the commercial bank sector. Thisoutcome stems from the dynamic nature of the financial sector (i.e., advancesin information technology, innovation and increased competition by nonbanks,and globalization) and the inability of prevention–safety net regulation to ac-commodate change.

Because of the prevention–safety net paradigm’s inability to contain risk andpromote stability in a dynamic financial sector, Litan calls for a new paradigmthat is aimed at maintaining stability in a more competitive and evolving mar-ket. The new paradigm, known as the competition–containment paradigm, callsfor changing regulations to allow banks to compete with nonbanks and callsfor isolating and containing problems, preferably before crises occurs. Litanbelieves that we must move away from the post-Depression paradigm be-cause it, in part, now encourages excessive risk taking. The new paradigmwill, in part, minimize excessive risk taking by the commercial banker, eventhough there will be more competition. Thus, according to Litan, bank regu-lation has contributed to bank instability and risk taking in the past 30 or soyears.

HOW DOES REGULATION AFFECT THE RISK TAKING OF BANKS? 65

Many other scholars paint a picture of U.S. bank regulation that is similar tothat of Litan. For example, Pierce (1991) and White (1993) argue that the set ofpost-Depression era regulation is defined by two primary objectives, namely, tominimize competition and to create a federal safety net to protect consumers.The federal safety net, largely composed of deposit insurance, is said to encour-age risk taking because of the moral hazard associated with it. However, Pierceargues that the instability of deposit insurance does not reveal itself until banksare subject to increased competition and falling profitability. Both these devel-opments occurred in the United States in the early 1970s. Since then, bankinghas been an increasingly dynamic enterprise subject to increased competitionand changing balance sheet and off-balance sheet activity. Constrained andencouraged by regulation, banks have taken on increasingly risky projects inthis new era of dynamic banking.

Boot et al. (1999) also argue that the increasingly dynamic nature of commer-cial banking has increased risk taking by banks constrained by regulation. Thesescholars characterizes bank regulation into one of two types: direct and indi-rect. Direct regulation defines certain behavior or permissible activity for banksand other financial institutions. The separation of commercial and investmentbanking and prohibitions on interstate banking are examples of direct regula-tion in the United States. Indirect regulation, in contrast, does not prescribebehavior but, rather, uses both price and nonprice means to elicit certain be-havior from the banker. Risk-based capital standards and deposit insurancepremiums are examples of such regulation. Both are meant to discourage risktaking by making the loss to the bank greater (more costly) should the actionfail. Boot et al. (1999) argue that in a dynamic market, direct regulation tendsto be more problematic for bank performance, since the regulation remainsstatic while the market moves in unpredictable directions. From this perspec-tive, whether or not bank regulation is stabilizing may depend, to a large degree,on whether the regulation is direct or indirect and also on whether the finan-cial sector is experiencing rapid growth and change or if it is maintaining thestatus quo.

Perhaps the most obvious form of regulation is federal deposit insurance.Moral hazard problems arise because of flat-rate insurance premiums inde-pendent of bank risk (see, for example, White, 1993; Benston, 1991; McKenzie,1990; O’Driscoll, 1988; Benston and Kaufman, 1986; Shiers, 1994; Bhattacharyaet al., 1998). Instability increases because bankers have an incentive to in-crease risk. Moreover, depositors often perceive all insured banks as homoge-nous and consequently fail to monitor and discipline the banks using theirfunds.

Finally, it is also argued that bank regulation has promoted a fragmentedbanking system by prohibiting interstate branching.6 Salsman (1993), Benstonand Kaufman (1986), and Benston (1991) suggest that a prohibition againstbranching leads to less diversified banks that are more susceptible to local eco-nomic downturns and shocks. Wheelock (1992) provides supporting empirical

66 HENDRICKSON AND NICHOLS

evidence by examining the performance of Kansas banks in the 1920s, find-ing that limits on branching caused banks to be more vulnerable to economicshocks.

In many ways, Salsman’s (1993) historical analysis captures the essence of thebody of literature advancing a positive relationship between bank regulation andinstability by demonstrating that private bankers have continuously innovatedto restore stability to a system made unstable by government intervention andregulation:

When restrictions imposed on note issue under the National Banking Sys-tem caused money panics, they [bankers] developed “clearinghouse certifi-cates’’ and other forms of private currency that consumers demanded. Whenrestrictions imposed by the Glass–Steagall Act in the 1930s prevented banksfrom underwriting securities and doing business with the best U.S. compa-nies, they invented term loans. When branching and new product opportuni-ties were blocked by law and narrowly constrained banks in the 1950s, theycreated holding companies to permit growth and diversification. When inter-est rate ceilings and restrictions on deposit gathering, together with inflation-driven high interest rates, led to an outflow of deposits in the 1960s and 1970s,they created certificates of deposits and “Eurodollar’’ accounts. When cen-tral banking brought volatility to foreign exchange markets and interest ratesin the 1970s and 1980s, they created hedging products to enhance stability.More recently, in response to central banking’s double-digit growth rates inmoney and credit that ballooned bank balance sheets and dwarfed capital,they invented “securitization,’’ the process of preserving liquidity and capitaladequacy by packaging loans and selling them in the secondary markets. Tothe extent that there has been any stability in the banking sector under cen-tral banking, it has been achieved by the creative efforts and skilled privatebankers—in spite of central banking, not because of it (110–111).

In summary, the role of regulation in promoting stability is ambiguous. Regu-lation designed to protect depositors, reduce risk taking, and prevent failures issaid, by critics, to have had the exact opposite effect. Therefore, the impact reg-ulation has on risk taking and bank stability is ultimately an empirical question.

A brief comparison of bank regulation between the U.S. and Canada

Policymakers in Canada and the U.S. have used bank regulation in varyingamounts and degrees to achieve the objectives outlined above. Specifically,six provisions of banking regulation historically differentiate the operating envi-ronment of Canadian and U.S. banks: capital-asset requirements, permissibleinvestment activity, permissible loan activity, restrictions on deposit interestrates, branch banking rights, and deposit insurance. Table 1 provides a concise

HOW DOES REGULATION AFFECT THE RISK TAKING OF BANKS? 67

Table 1. Relevant chronology and description of banking regulation

Regulation United States Canada

Capital–assetrequirements

• Prior to 1981: capital require-ments were determined byregulatory agencies’ subject-ive examination of individualbanks, whereby capital levelswere compared to levels ofsimilar banks (see Keeley,1992, p. 147).

• Prior to 1980: bank managerswere responsible for determiningcapital levels.

• December, 1981: risk-basedcapital requirements wereestablished.

• Bank Act of 1980: empoweredthe Inspector General to set mini-mum capital requirements (seeKryzanowski and Roberts, 1992).

Investment activity • Prior to 1933: commercialbanks established securitiesaffiliates or used their bonddepartments for securitiesunderwriting and distribution.

• Prior to 1980: commercial bankswere able to directly underwriteand distribute government secu-rities and to underwrite and dis-tribute corporate securities.

• Banking Act of 1933: partiallyseparated commercial andinvestment banking, thoughcommercial banks were stillallowed to underwrite federalgovernment securities andstate and municipality bonds.a

• Bank Act of 1980: required thatthe distribution and underwritingof corporate securities utilize sub-sidiaries (see Kryzanowski andRoberts, 1992).

Lending activity • National Banking Act of 1864:limited permissible productline to commercial loans.b

• Prior to 1967: limited permissibleproduct line to commercial loans.

• DIDMCA 1980: lifted remaininglending restrictions for alldepository institutions.

• 1944–1967: loan interest ceiling of6%.

• Bank Act of 1967: liberalized per-missible lending activity and liftedinterest ceiling.

Deposit interest • Banking Act of 1933: placed a3% ceiling on time and savingsdeposits and prohibited inte-rest payments on demanddeposits.

• Prior to 1967: 6% interest ceilingon deposits.

• Late 1960s–1970s: interestceiling adjusted upwards tominimize disintermediation.

• Bank Act of 1967: allowed banksto pay market interest rate ondeposits.

• DIDMCA 1980: phased-out in-terest ceiling.

(Continued on next page.)

68 HENDRICKSON AND NICHOLS

Table 1. (Continued).

Regulation United States Canada

Branch banking • National Bank Act of 1864: inter-preted to limit nationally charteredbanks to a single location.

• Banks have always been allowedto establish branch units through-out Canada.

• State Chartered Banks: branchingrights and restrictions determinedon state-by-state basis.

• 1927 McFadden Act: afforded na-tionally charted banks the oppor-tunity to branch within the cityof the parent bank, provided thatstate law afforded similar opportu-nities to state banks.

• Banking Act of 1933: nationalbanks were given authority to es-tablish intrastate branches pro-vided that state law allowed it.

• Bank Holding Company Act of1956c: prohibited interstate acqui-sition of banks by bank holdingcompanies.

Deposit Insurance • Bank Act of 1993: created federaldeposit insurance available to allcommercial banks.

• Prior to 1967: implicit deposit in-surance for all commercial banks.

• 1967 Bank Act: created federal de-posit insurance for all commercialbanks.

aSee Kelly (1985) for a detailed history of securities activity by U.S. commercial banks, and Kauf-man (1988) for more recent changes.bLending restrictions were liberalized slowly over time, e.g., the Federal Reserve Act of 1913granted nationally chartered banks the right to extend farm mortgages. Huertas (1987, p. 140)discusses the segmentation of U.S. lending activity.cIncluding amendments in 1970 and 1979.

summary of the regulatory differences between the two countries and indicatesthe relevant chronology of change to the regulatory structures.

Generally, Canadian banks have been less regulated than U.S. banks. On theasset side, lower capital requirements and more liberal securities and lendingactivity characterize the Canadian banking system. On the liability side, usuryceilings on deposits were higher in Canada. Moreover, the ceilings were liftedsooner in response to rising interest rates in the late 1960s. Branch bankingopportunities clearly favor the Canadian system. Canadian banks have alwaysbeen allowed to establish a nationwide network of branches. In contrast, myriadlegislation has attempted to clarify U.S. branching rights and limit interstatebanking.7 While federal deposit insurance was made available to U.S. commer-cial banks in 1933, explicit deposit insurance was not introduced in Canadauntil the 1967 Bank Act created the Canada Deposit Insurance Corporation.

HOW DOES REGULATION AFFECT THE RISK TAKING OF BANKS? 69

Nonetheless, Canadian banks had enjoyed an implicit deposit guarantee sincethe early 1920s (Kryzanowski and Roberts, 1992). Prior to 1967, regulators andgovernment officials worked together to ensure the solvency of Canadian banksby standing ready to lend to, or find healthy banks to acquire, troubled banks.Essentially, implicit deposit insurance was created through the Canadian gov-ernment’s policy of guaranteeing all deposits at par. While Canadian bankersdid not pay insurance premiums, they benefited from a government policy thatwas equivalent to deposit insurance. This implicit insurance created depositorand borrower confidence in the banking system and allowed Canadian banksto hold relatively fewer noninterest-bearing assets.

Collectively, the individual regulations reviewed above create distinct environ-ments for the Canadian and U.S. banking sectors, with the Canadian systemcharacterized as less regulated than the U.S. system.8 By comparing these twocountries with different regulatory environments and failure rates, the role ofregulation as a stabilizing or destabilizing factor can better be inferred. Thenext section describes the data and model specification used for quantifyingthe impact of these regulatory differences on risk taking and the number of bankfailures.

Data and bank risk model

In creating a model of bank risk, this study utilizes annual balance sheet andincome/expense data for U.S. and Canadian commercial banks for the years1936–1989.9 The use of annual aggregate data implies that our study con-siders the “average’’ bank for both countries. Data on Canadian banks comefrom Canada Year Book, Bank of Canada Review, and Historical Statistics ofCanada. Data for insured commercial banks in the U.S. come from the FDIC His-torical Statistics on Banking and the 1991 Annual Report of the FDIC. All dataare adjusted for inflation using each country’s GNP deflator and are expressedin 1989 U.S. dollars.

Before presenting our risk model, we test for stationarity in each individualtime series. If series are nonstationary, it can lead to spurious results whenthe levels of variables are used for estimation. However, Granger (1981) showsthat nonstationary variables may have linear combinations that are stationarywithout differencing. If so, the series are said to be cointegrated.

Using the augmented Dickey–Fuller test, each series, with the exception ofthe unemployment rate, is found to be nonstationary. However, first differenc-ing results in all series being stationary. Using Johansen’s (1988) multivariatecointegration test, we find the regulatory variables to have at least two coin-tegrating equations, indicating that the series given in models (1) and (2) be-low possess a long-run equilibrium relationship. Consequently, the estimationof these bank risk and failure models uses levels rather than first differences.However, because of serial correlation revealed through ordinary least squares(OLS) estimation of the risk model, the technique of first-order autoregressive

70 HENDRICKSON AND NICHOLS

(AR(1)) correction is employed. Thus the OLS results of the risk model are allAR(1) correction estimates.

Model construction utilizes a set of explanatory variables meant to cap-ture the regulatory differences between the two nations. Further, the modelincludes a set of general control variables, Xt , to account for such factors aschanging macroeconomic conditions that might affect bank risk. The result is alinear model meant to capture how different regulatory regimes impact bank risktaking:

RISKt = β0 + β1(KAGAPt−1) + β2(DEPGAPt−1) + β3(LOANGAPt−1)

+ β4(SECGAPt−1) + β5(BANKSIZEt−1) + β6(PCTINSt−1)

+ βx Xt + εt . (1)

Each variable is defined next, along with a discussion of the expectedresults.

Dependent variable

The dependent variable, RISKt , is defined as the difference in the five-yearmoving average of the standard deviation of the return on capital for eachcountry.10 As such, it captures differences in bank risk taking between the twocountries.

Regulatory variables

The set of regulatory variables is defined as the U.S. value less the Canadianvalue. Further, the variables are all lagged one period to minimize potential si-multaneity bias. KAGAPt−1 is the difference in capital-asset ratios and capturesdifferences in capital requirements. LOANGAPt−1 represents the difference inloan returns for the two nations. SECGAPt−1 reflects return on security differ-ences created by the two regulatory regimes and captures, in part, investmentrestrictions that allow U.S. banks to only hold investment grade securities com-pared to Canada’s more liberal investment activities. The impact of RegulationQ is proxied by DEPGAPt−1, the difference in total deposits per capita betweenthe U.S. and Canada.11 Further, differences in branch banking laws are proxiedthrough BANKSIZEt−1, defined as total assets over the number of banks. Branchbanking may lead to scale economies that result when establishing branch unitslead to lower overhead, labor, and other costs (see Bordo, Rockoff, and Redish,1994; Kryzanowski and Roberts, 1992; Nathan and Neave, 1992). Finally, Shiers(1994) accounts for the moral hazard problem elicited by deposit insurance byincluding the percent of all insured deposits. Therefore, PCTINSt−1, the percent-age of total deposits insured, is included in model (1) to capture the impact ofdeposit insurance.

HOW DOES REGULATION AFFECT THE RISK TAKING OF BANKS? 71

As outlined above, most banking regulation is intended, either directly or in-directly, to enhance the stability and solvency of banks by protecting them frominterbank competition or reducing their exposure to risk. Branching restrictionsand charter requirements protect existing banks from competition and entry.Interest rate ceilings prevent price competition for deposits. Loan restrictionssegment the market, thereby reducing competition between banks and otherfinancial intermediaries. Further, the partial separation of commercial and in-vestment banking laws also limits competition. These barriers to competitionmay protect banks that may not remain solvent in an otherwise competitivemarket.12 In terms of risk-taking incentives, Regulation Q controls the cost of ob-taining deposits and may therefore limit the incentives for high-risk/high-returnlending and investing practices. Similarly, capital requirements may constrainexcessive risk taking, particularly in the face of underpriced deposit insurance.

On the other hand, the very existence of regulation may provide incentivesfor those participating in the intermediation process to increase their risk-taking behavior. Regulation may reduce the opportunities for diversification(e.g., restrictions on permissible investment activity, loanable funds, and branchbanking) and hence increase portfolio risk.13 Capital requirements limit theamount of funds available for lending or investment and may also increaserisk taking. Further, interest rate ceilings, while reducing interbank competition,may also lead to disintermediation problems when market interest rates riseabove regulated rates. Consequently, if disintermediation outweighs the stabi-lizing nature of regulation, we would expect regulation to increase risk taking bybankers. Deposit insurance is also thought to encourage risk taking because ofthe moral hazard problems associated with it. Perhaps this tendency was evenmore true in Canada when its insurance was explicit rather than implicit, sincethe banker bore none of the insurance costs yet benefited from the protectionand depositor confidence.

Other control variables

Several control variables were also created to account for real sector perfor-mance and regulatory developments throughout the sample period. A trendvariable, TRENDt , controls for macroeconomic or other exogenous shocks thatmay have affected bank failure rates. UNEMt−1 controls for fluctuations in un-employment rates in the U.S. and Canada, and BUSFAILt−1 accounts for theaverage liabilities of failed business enterprises. Higher values of both vari-ables may increase bank risk. Finally, as is well known, regulatory structureswere not constant during the sample period. In 1980, significant legislativechanges were made in both the U.S. and Canada. The Depository InstitutionsDeregulation and Monetary Control Act (DIDMCA) of 1980 drastically changedthe regulatory landscape by phasing out Regulation Q, increasing deposit in-surance from 40,000 to 100,000, and liberalizing lending activity.14 In Canada,the revisions to the Bank Act of 1980 extended bank powers to the activities

72 HENDRICKSON AND NICHOLS

of leasing and factoring, further reduced required reserves, removed securi-ties underwriting, and eased entry requirements. These regulatory changesare controlled for with YEAR80t , a dummy variable equal to 1 for the years1980–1989.

Failure model

In addition to the risk model, we also offer a failure model meant to illus-trate the robustness of model (1). The model for testing the effectiveness ofU.S. bank regulation in stabilizing the commercial bank sector utilizes Tobitregression analysis, since many of the observations are clustered at zero. Fail-ure model construction includes the same set of regulatory and control vari-ables from model (1) and adds a set of risk variables found in the bank failureliterature:

FAILt = β0 + β1(KAGAPt−1) + β2(DEPGAPt−1) + β3(LOANGAPt−1)

+ β4(SECGAPt−1) + β5(BANKSIZEt−1) + β6(PCTINSt−1)

+ β7(LARISKt−1) + β8(MGMTt−1) + β9(RERATIOt−1)

+ βx Xt + εt . (2)

The dependent variable, FAILt , is the annual percent of insured U.S. com-mercial banks that failed over the period 1936–1989. Thus, the data reflecta regulatory bank failure and not necessarily the precise date of bank insol-vency. Certainly, there are often discrepancies between the time when a bankbecomes insolvent and the time when regulators declare the bank to havefailed. This gap may arise, for example, because of different incentives fac-ing regulators charged with closing insolvent institutions (Kane, 1989). While itis important to consider the incentive structure facing regulators when exam-ining the period of time until failure (Demirguc-Kunt, 1989), the current studyfocuses on differences in regulation between the U.S. and Canada and the rolethese play in explaining differences in aggregate bank failures between the twocountries.15

While the independent regulatory and control variables are defined as inmodel (1), this failure model also includes two specific risk variables. As sug-gested in Avery and Hanweck (1984), bank loans are the most illiquid of bankassets and subject to the greatest threat of default. Consequently, the ratio oftotal loans to total assets, LARISKt−1, reflects U.S. banks’ exposure to defaultrisk. Asset quality may also be proxied as ratios of specific types of loans tototal loans. Since many local bank failure studies attribute real estate loans ascontributing to the large number of U.S. bank failures in the 1980s, this studyutilizes the ratio of real estate loans to total loans, RERATIOt−1, as a secondmeasure of asset quality.16 Finally, mismanagement or fraud may also lead tobank failures. Following Pantalone and Platt (1987), the ratio of total interest

HOW DOES REGULATION AFFECT THE RISK TAKING OF BANKS? 73

expense to total liabilities, MGMTt−1, measures management efficiency. Natu-rally, it is expected that lower risk will result in fewer bank failures.17

Empirical results

Risk model

Table 2 contains descriptive statistics for the variables used in models (1) and (2).Table 3 contains the results for the risk model and indicates that all the regulatoryvariables are of the expected sign and, except for the capital requirement proxyand the security returns variable, statistically significant.

The coefficient for differences in capital requirements, KAGAPt−1, is negative,indicating that higher capital holdings in the U.S. decreases bank risk. Greatercapital holdings may provide a source of funds that protect banks from fail-ure in the face of unexpected deposit withdrawals or loan defaults and mayconstrain risk taking. The positive coefficient for differences in security returns,SECGAPt−1, suggests that limits placed on U.S. banks’ security activity reducesbank risk, possibly by limiting the volatility and uncertainty often associated withsecurities dealings. Thus, both the capital requirements and securities regula-tion seem to enhance bank stability, supporting Garrison, Short, and O’Driscoll(1988), who argue that asset restrictions and capital requirements limit the moralhazard of deposit insurance by preventing banks from taking full advantage ofunderpriced deposit insurance.

Similarly, the positive coefficients on DEPGAPt−1 and LOANGAPt−1 suggestthat regulation that limits interest paid on deposits and the type of permissi-ble loan activity is effective in reducing bank risk. This outcome suggests thatthe effect of limited costs and competition introduced with Regulation Q out-weighed any destabilizing effect brought about by disintermediation. Moreover,the positive sign of DEPGAPt−1 supports Rolnick (1987), who finds a positivecorrelation between deposit rates and bank risk. Over the sample period, lowerloan returns appear to have been associated with decreased risk and limitedcompetition.

In contrast, the negative and statistically significant coefficient on BANK-SIZEt−1 indicates that the freedom to operate branch units reduces bank risk.This finding suggests that smaller banks may be less diversified, operatingwith riskier portfolios and therefore more prone to failure.18 Similarly, largerbanks may have a greater ability to raise new capital and reduce insolvencyin volatile or uncertain times. Finally, the positive and significant coefficienton the percent of deposits insured, PCTINSt−1, suggests not only that depositinsurance increase risk but also that it ultimately promotes instability in thebanking system. Therefore, if insurance is to be provided, it should be a functionof risk, as mandated by the 1991 Federal Deposit Insurance Improvement Act,rather than a simple flat fee. This approach would diminish the agency problemand promote stability.

74 HENDRICKSON AND NICHOLS

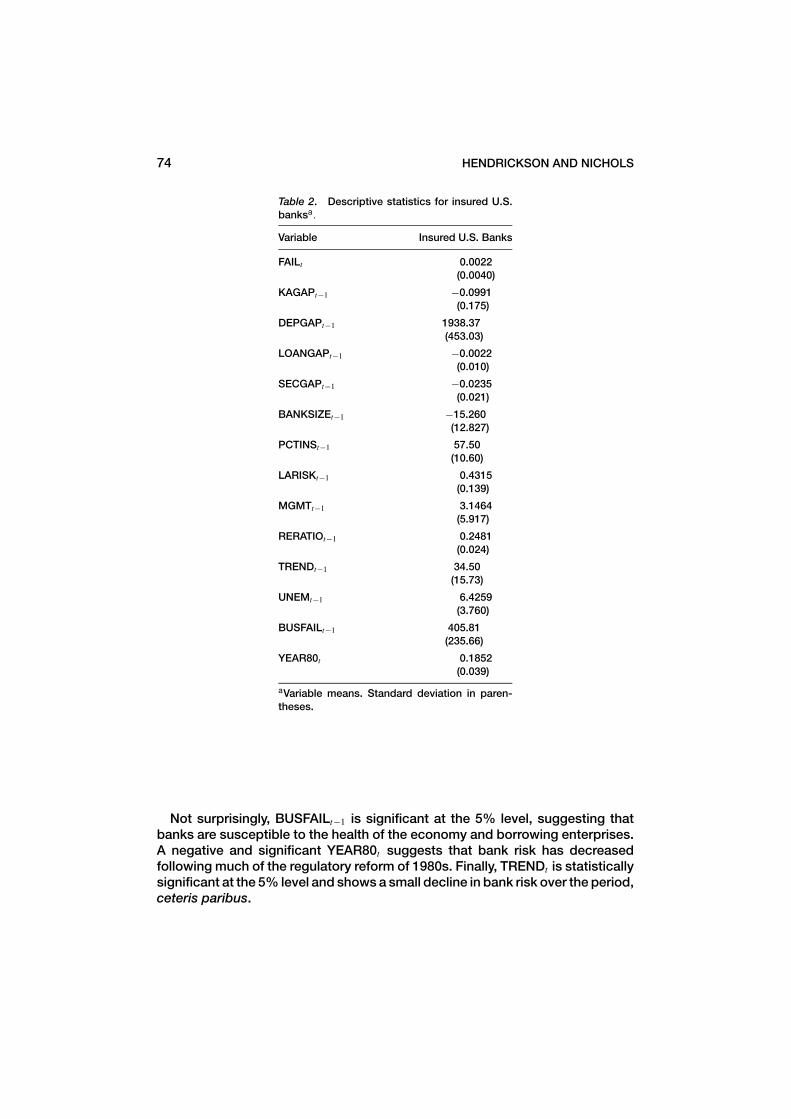

Table 2. Descriptive statistics for insured U.S.banksa.

Variable Insured U.S. Banks

FAILt 0.0022(0.0040)

KAGAPt−1 −0.0991(0.175)

DEPGAPt−1 1938.37(453.03)

LOANGAPt−1 −0.0022(0.010)

SECGAPt−1 −0.0235(0.021)

BANKSIZEt−1 −15.260(12.827)

PCTINSt−1 57.50(10.60)

LARISKt−1 0.4315(0.139)

MGMTt−1 3.1464(5.917)

RERATIOt−1 0.2481(0.024)

TRENDt−1 34.50(15.73)

UNEMt−1 6.4259(3.760)

BUSFAILt−1 405.81(235.66)

YEAR80t 0.1852(0.039)

aVariable means. Standard deviation in paren-theses.

Not surprisingly, BUSFAILt−1 is significant at the 5% level, suggesting thatbanks are susceptible to the health of the economy and borrowing enterprises.A negative and significant YEAR80t suggests that bank risk has decreasedfollowing much of the regulatory reform of 1980s. Finally, TRENDt is statisticallysignificant at the 5% level and shows a small decline in bank risk over the period,ceteris paribus.

HOW DOES REGULATION AFFECT THE RISK TAKING OF BANKS? 75

Table 3. OLS coefficients for insuredbanks: risk model.

Variable Estimated coefficient

KAGAPt−1 −0.00033(1.04)

SECGAPt−1 0.049(1.41)

LOANGAPt−1 0.493a

(1.83)

DEPGAPt−1 0.004a

(1.79)

BANKSIZEt−1 −0.0086a

(2.01)

PCTINSt−1 0.039b

(2.52)

YEAR80 −0.026b

(3.32)

UNEMt−1 0.011b

(2.79)

BUSFAILt−1 0.088a

(1.85)

TRENDt 0.009b

(3.24)

CONSTANT −9.382b

(3.27)

AR(1) 0.099a

(5.27)

R2 84.38

DW 1.94

aSignificance at the 10% level.bSignificance at the 5% level.Note: Absolute values of the t statisticappear in parentheses.

Failure model

Much like the risk model results, the failure model results found in Table 4provide conflicting evidence for the hypothesis that regulation increases insta-bility. While all the regulatory variables are statistically significant, some typesof regulation are found to reduce failures, while others are found to increase thenumber of bank failures.

More specifically, two of the regulatory variables are found to reduce bankfailures. The negative coefficient to KAGAPt−1 indicates that the higher cap-ital requirements in the U.S. reduce failures, an outcome that is consistent

76 HENDRICKSON AND NICHOLS

Table 4. Tobit and adjusted tobit coefficients for insuredbanks: failure model.

Variable Tobit Adjusted Tobit

KAGAPt−1 −0.0392b −0.00016(3.44)

DEPGAPt−1 0.0839b 0.0638(2.48)

LOANGAPt−1 0.193b 0.0938(2.32)

SECGAPt−1 0.0837a 0.0411(1.92)

BANKSIZEt−1 −0.0015b −0.00392(4.39)

PCTINSt−1 0.00183b 0.00099(3.29)

LARISKt−1 0.0617 0.0182(1.09)

MGMTt−1 0.00283b 0.00055(3.41)

RERATIOt−1 0.0288 0.0083(0.83)

TRENDt −0.034b −0.00129(3.57)

UNEMt−1 0.0038 0.00011(1.07)

BUSFAILt−1 0.000114b 0.000005(4.03)

YEAR80t 0.0382a 0.058(2.08)

CONSTANT −0.098b −0.0038(2.65)

LR Testc 95.49b

aSignificance at the 10% level.bSignificance at the 5% level.cLikelihood ratio test ∼χ2(13), where null is that all coeffi-cients except the constant are zero.Notes: Absolute values of the t statistic appear in parenthe-ses.The adjusted Tobit coefficient reflects the change in thedependent variable (for those observations above the limitof zero) caused by a change in the independent variable.Specifically, it equals β∗

i {1 − ( f (z)/F(z)) ∗ (z + f (z)/F(z))},where βi is the Tobit coefficient, z = Xβ/s, f (z) is the normaldensity, and F(z) is the normal distribution. See McDonaldand Moffit (1980).

HOW DOES REGULATION AFFECT THE RISK TAKING OF BANKS? 77

with the findings in the risk model. Similarly, the positive coefficient for dif-ferences in the return on securities suggests that the lower securities returnin the U.S. decreases failures—a finding that is, again, consistent with the riskmodel. The findings from the failure model differ in one other aspect from therisk model: increases in unemployment rates are found to increase risk slightly,whereas they are found to be statistically insignificant in the failure model. Thisoutcome suggests, perhaps, that macroeconomic conditions play an impor-tant role in risk taking but not to such a degree as to contribute to actualfailure.

All the risk variables are positive, suggesting that, ceteris paribus, higher riskincreases failure rates. However, only the management efficiency coefficientis statistically significant. This finding suggests that management control overinterest expenses reduces bank failures. Both LARISKt−1 and RERATIOt−1 areinsignificant, with the latter result likely reflecting that the widely publicizedproblems of real estate loans were concentrated in regional markets and in-significant from the perspective of the “average’’ U.S. bank.

Conclusions

The findings of this study suggest that certain regulations contribute to bankrisk taking and failures, while others tend to stabilize the industry. This find-ing further suggests that blanket reforms, where all aspects of the industry arederegulated, may not be an appropriate policy. While restrictions on branchbanking and deposit insurance are found to be destabilizing, regulations onallowable investments and loan types, and on the price of deposits, have theopposite effect. This outcome corroborates the conclusions of Edwards andScott (1979), who find that selective deregulation in areas such as branchbanking and price controls will increase stability and welfare but that bal-ance sheet controls, especially liquidity and equity requirements, should bemaintained.

The finding that asset restrictions and capital requirements work to constrainbank risk in the presence of moral hazard problems supports the 1999 Gramm–Leach–Bliley Act, which repealed the Glass–Steagall provisions and the 1991mandate for repricing deposit insurance to reflect bank risk. This finding alsoreveals the interdependence among various regulations. Since policymakersexpanded banks’ security investment activity, it is necessary for deposit in-surance to be a function of risk in order to limit the incentives for excessiverisk taking. Further, the finding that branch banking restrictions destabilize U.S.banking supports the 1994 Riegle–Neal Interstate Banking and Branching Effi-ciency Act, which allows banks to branch across state lines if state law allows.Finally, these findings indicate that higher capital holdings reduce both bankrisk and the number of failures. In this way, the findings provide support forthe 1988 Basel Accord that sets risk-sensitive capital requirements for banksacross the globe.

78 HENDRICKSON AND NICHOLS

Although the present study suggests that differences in regulatory regimesmay explain differences in risk taking and bank failure rates, another possibleexplanation may be found in differences in regulator behavior. For example,political pressure, regulator prestige, postemployment opportunities, etc. mayall play into a bank closure decision. In the U.S., the practice of regulatory for-bearance during the thrift crisis of the 1980s serves as an important example inwhich regulators extended survival time. If the incentives facing regulators varybetween the U.S. and Canada, regulator behavior may also explain discrepan-cies in bank failure rates. Indeed, determining whether regulator incentives varybetween the U.S. and Canada and, if so, how to incorporate these differencesinto an empirical model of bank risk and failures is an excellent topic for futureresearch.

Clearly, the list of regulations that may contribute to bank risk has not beenexhausted in this study (e.g., the 1977 Community Reinvestment Act, the 1983International Lending Supervision Act).19 Nonetheless, this comparative studybetween the U.S. and Canadian banking systems provides insight into under-standing both the relationship between regulation and risk and the number ofbank failures. This, in turn, provides some insight into the relationship betweenbank stability and regulatory policy that may be helpful in the contemporaryderegulation debate. The fact that all the regulatory variables in this model aresignificant suggests that regulation plays an important role in influencing theperformance of commercial banking, so discussions of policy must be takenseriously.

Finally, the findings of this study may shed some light on the theoreticaldebate of whether or not regulation promotes stability in commercial bank-ing. No consensus exists as to why banks are heavily regulated: is it to pro-tect depositors or to promote and protect industry participants? Theseempirical findings, which are consistent with much of the theoretical literature,suggest that regulation aimed at promoting safety and soundness, such as de-posit insurance, probably fails to advance consumer welfare. Further, to theextent that regulation is destabilizing, consumer welfare is certainly not ad-vanced. Nonetheless, it is difficult to determine the true intent of banking, orany, regulation because at times the consumer may benefit and at other timesthe regulated participants benefit. Indeed, this division of benefits betweenthe consumer and industry is consistent with Peltzman’s (1976) discussion ofthe politics of price-entry regulation. In particular, pure producer protection(the capture theory) is only rational in the absence of any consumer opposi-tion, and pure consumer protection (the public interest theory) is only rationalin the absence of any producer opposition. Given opposition on both sides,the regulator will find it politically attractive to obtain a balance between thetwo.

At the same time, however, there is more theoretical consensus that regulationin banking has tended to be increasingly destabilizing as the macroeconomy hasbecome more dynamic (See Competing Theories of Bank Regulation above).

HOW DOES REGULATION AFFECT THE RISK TAKING OF BANKS? 79

The results of this study corroborate this consensus by demonstrating thatimportant regulation on commercial banking increases risk taking. Specifically,deposit insurance and restrictions on interstate banking are both found to exac-erbate risk, and therefore, during times of greater uncertainty and change in theindustry, it is easy to envision more pressure and opportunity for risky behavior.In the case of deposit insurance, moral hazard problems tend to increase in theface of greater uncertainty, which is the outcome we have witnessed during thepast 30 years. Further, deregulation in 1994 removed interestate banking bar-riers, and commercial banking has seen greater stability and prosperity since1992. Although one cannot attribute such prosperity directly to deregulation,these findings suggests that the deregulation does play a role in stabilizingcommercial banking.

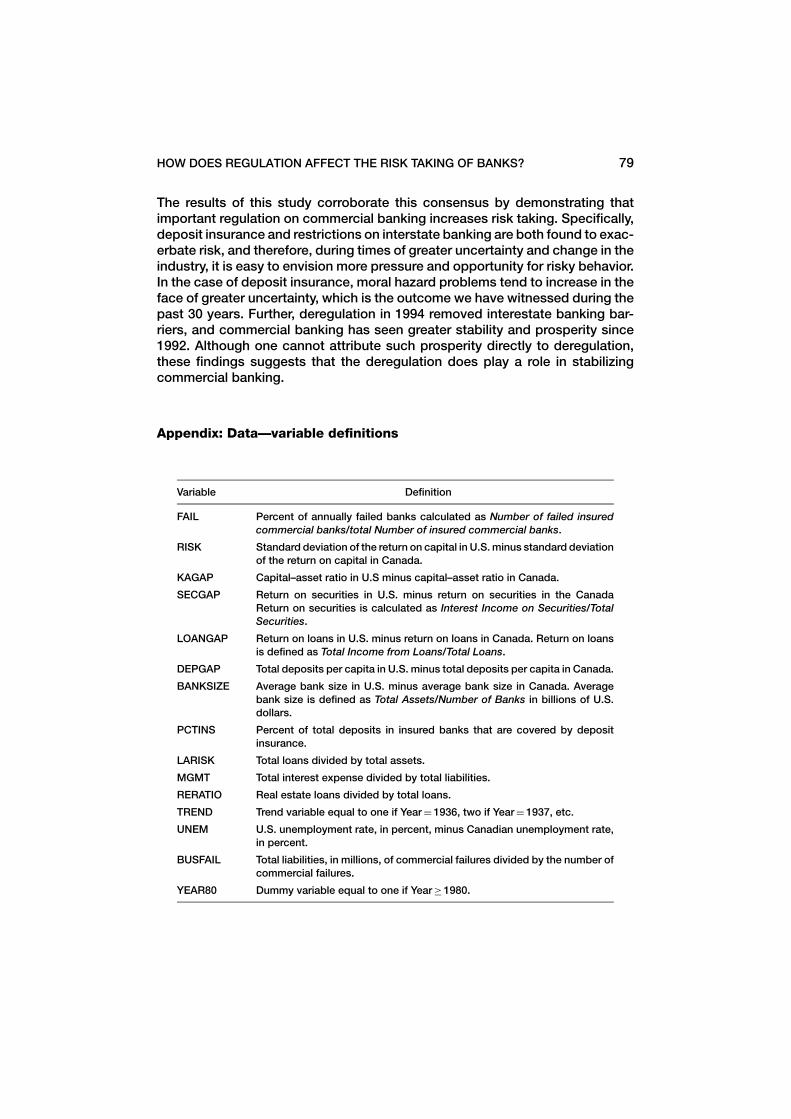

Appendix: Data—variable definitions

Variable Definition

FAIL Percent of annually failed banks calculated as Number of failed insuredcommercial banks/total Number of insured commercial banks.

RISK Standard deviation of the return on capital in U.S. minus standard deviationof the return on capital in Canada.

KAGAP Capital–asset ratio in U.S minus capital–asset ratio in Canada.

SECGAP Return on securities in U.S. minus return on securities in the CanadaReturn on securities is calculated as Interest Income on Securities/TotalSecurities.

LOANGAP Return on loans in U.S. minus return on loans in Canada. Return on loansis defined as Total Income from Loans/Total Loans.

DEPGAP Total deposits per capita in U.S. minus total deposits per capita in Canada.

BANKSIZE Average bank size in U.S. minus average bank size in Canada. Averagebank size is defined as Total Assets/Number of Banks in billions of U.S.dollars.

PCTINS Percent of total deposits in insured banks that are covered by depositinsurance.

LARISK Total loans divided by total assets.

MGMT Total interest expense divided by total liabilities.

RERATIO Real estate loans divided by total loans.

TREND Trend variable equal to one if Year = 1936, two if Year = 1937, etc.

UNEM U.S. unemployment rate, in percent, minus Canadian unemployment rate,in percent.

BUSFAIL Total liabilities, in millions, of commercial failures divided by the number ofcommercial failures.

YEAR80 Dummy variable equal to one if Year ≥ 1980.

80 HENDRICKSON AND NICHOLS

Acknowledgments

Our sincere thanks for their comments to the participants in a 1996 WesternEconomics Association session and to three anonymous referees. All remainingerrors are those of the authors.

Notes

1. In the context of our empirical analysis, the terms risk and risk taking refer to increased chancesfor failure. This is not to say that all forms of risk taking are undesirable or that all regulatorsview risk taking in this way. Indeed, risk taking in the form of innovation, entrepreneurship, etc.is necessary and vital for economic prosperity and may be stabilizing. However, our use of theterm risk taking throughout this article should be equated with increased likelihood of failure.

2. See Figure 1, which shows the number of bank failures in Canada and the U.S. for the period1936–1989, and Figure 2, which shows the asset value of failed banks for the sample period.

3. See, for example, Bordo, Rockoff, and Redish (1994) for a comparison of profit levels betweenthe two countries.

4. Gilbert (1975, p. 7) also argues that a primary objective of bank regulation is the prevention ofbank failures.

5. For an interesting historical interpretation of increasing bank regulation consistent with thisviewpoint, see Horwitz (1993).

6. Further, some states prohibited intrastate branching. For example, in 1933, 11 states prohibitedintrastate banking and 17 states limited intrastate branching. These numbers changed verylittle during our sample period because, in 1982, 10 states still prohibited the establishmentof branch units, and the number of states that placed restrictions on intrastate branching hadincreased to 26 (see Moore, 1995).

7. The passage of the 1994 Riegle–Neal Interstate Banking and Branching Efficiency Act changedbranch regulation in the U.S. by allowing banks to branch across state lines, provided that statelaw allows it. See Maggs and Pate (1995) or Kane (1996) for a discussion of the Act.

8. Swary and Topf (1992, p. 459) classify the Canadian banking regulation as “mild” and the U.S.banking regulation as “heavy.”

9. Although individual bank data would have been desirable, they are not available for this entiretime period. Further, it has been suggested that perhaps the instability of the 1980s may playa large role in the overall findings of this model. To test the robustness of the model for theentire time period, the model was also regressed for the period 1936–1979, and the resultswere statistically the same as those generated using the entire sample.

10. See the Appendix for a complete description of all variables in the model.11. Total deposits per capita, rather than the interest paid on deposits per capita, is used because

of multicollinearity problems with the loan interest rate.12. See O’Driscoll (1988, p. 5) who argues that the reduction in bank failures following the Great

Depression was due not to increased bank safety but rather to the result of reduced competitionvia regulation.

13. Benston (1991, pp. 226–227) finds that regulation limits diversification and hence reduces indi-vidual bank stability.

14. The 1982 Garn–St. Germain Act, also an important legislative development, focused primarilyon the troubled thrift industry. It is not controlled for within this study for this reason; moreimportantly, a dummy variable for the 1982 Act would be highly collinear with the 1980 dummyvariable. Nonetheless, several provisions related to commercial banks included a more rapidphaseout of Regulation Q, the introduction of money market deposit accounts to compete withmoney market mutual funds, and an increase in the national bank lending ceiling to individualborrowers. These provisions are consistent with the deregulation of U.S. banking in the 1980s.

HOW DOES REGULATION AFFECT THE RISK TAKING OF BANKS? 81

15. An important contribution to recent bank failure literature does consider the empirical questionof how long a bank will survive. Typically, such studies utilize cross-sectional data over a shortperiod of time to understand bank survival time and rely on regression techniques known assurvival models. For example, Cole and Gunther (1995) utilize a split-population survival timemodel to explain both bank failures and bank survival time. They find that, in general, differentsets of variables explain bank failures and survival time. Calomiris and Mason (1997) use a sur-vival duration model to forecast Chicago bank survival times during the Great Depression. Bothstudies compare a population of failed institutions against a population of surviving institutionsusing panel data.

16. Other asset quality ratios, such as commercial and industrial loans to total loans, and agriculturalloans to total loans, produced results similar to the real estate ratio.

17. Another commonly included risk variable is the capital-to-asset ratio (see, e.g., Avery andHanweek, 1984). This variable is included in the current specification and as discussed abovein the previous subsection.

18. These results are consistent with those of Benston (1991, p. 226).19. These and a host of other regulatory developments make it costlier for banks to operate. Com-

pliance and other cost data are not separately available for inclusion in this study.

References

Avery, Robert B. and Gerald A. Hanweck. (1984). “A Dynamic Analysis of Bank Failures.” In BankStructure and Competition, Proceedings of a Conference Sponsored by the Federal ReserveBank of Chicago, 380–401.

Benston, George J. (1991). “Does Bank Regulation Produce Stability? Lessons from the UnitedStates.” In Forrest Capie and Goeffrey E. Wood (eds.), Unregulated Banking: Chaos or Order?New York: St. Martins Press, 207–232.

Benston, George J. and George G. Kaufman. (1986). “Risks and Failures in Banking: Overview,History and Evaluation.” In George G. Kaufman and Roger C. Kormendi (eds.), DeregulatingFinancial Services: Public Policy in Flux. Ballinger Cambridge, MA: Ballinger, 49–77.

Bhattacharya, Sudipto, Arnoud W.A. Boot and Anjan V. Thakor. (1998). The Economics of BankRegulation.” Journal of Money, Credit, and Banking 30(4), 745–770.

Boot, Arnoud W.A., Silva Dezelan and Todd T. Milbourn. (1999). “Regulatory Distortions in aCompetitive Financial Services Industry.” Journal of Financial Services Research 16(2–3), 249–259.

Bordo, Michael, D., Hugh Rockoff and Angela Redish. (1994). “The U.S. Banking System from aNorthern Exposure: Stability Versus Efficiency.” The Journal of Economic History 54, 325–341.

Calomiris, Charles W. and Joseph R. Mason. (1997). “Contagion and Bank Failures During the GreatDepression: The 1932 Chicago Banking Panic.’’ American Economic Review 87(5), 863–883.

Cole, Rebel A. and Jeffrey W. Gunther. (1995). “Separating the Likelihood and Timing of BankFailure.” Journal of Banking & Finance 19, 1073–1089.

Demirguc-Kunt, Ash. (1989). “Deposit-Institution Failures: A Review of Empirical Literature.” FederalReserve Bank of Cleveland Economic Review, 2–18.

Edwards, Franklin R. and James Scott. (1979). “Regulating the Solvency of Depository Institutions:A Perspective for Deregulation.’’ In Franklin R. Edwards (ed.), Issues in Financial Regulation. NewYork: McGraw-Hill, 65–105.

Garrison, Roger W., Eugene D. Short and Gerald O. O’Driscoll, Jr. (1988). “Financial Stability andFDIC Insurance.’’ In Catherine England, and Thomas Huertas (eds.), The Financial Services Rev-olution: Policy Direction for the Future, Boston: Kluwer Academic Publishers, Chapter 8.

Gilbert, R. Alton. (1975). “Bank Failures and Public Policy.’’ Federal Reserve Bank of St. LouisReview, November, 7–15.

Granger, Clive W.J. (1981). “Some Properties of Time Series Data and Their Use in EconometricModel Specification.” Journal of Econometrics, May, 121–130.

82 HENDRICKSON AND NICHOLS

Horwitz, Steven. (1993). “Government Intervention: Source or Scourge of Monetary Order?” CriticalReview 7, 237–257.

Johansen, Sφren. (1988). “Statistical Analysis of Cointegration Vectors.’’ Journal of Economic Dy-namics and Control, Septmber, 231–254.

Kane, Edward J. (May 1996). “De Jure Interstate Banking: Why Only Now?’’ Journal of Money, Credit,and Banking 28, 141–161.

Kaufman, George G. (1985). “The Securities Activities of Commercial Banks.’’ In Handbook forBanking Strategy. New York: Wiley, 661–702.

Kaufman, George G. (1988). “Securities Activities of Commercial Banks: Recent Changes in Eco-nomic and Legal Environments.’’ Journal of Financial Services Research, January, 183–199.

Keeley, Michael. (1992). “Bank Capital Regulation in the 2980s: Effective or Ineffective?’’ In AnthonySaunders, Gregory F. Udell, and Lawrence J. White (eds.), Bank Management and Regulation.Mountain View, CA: Mayfield, 147–164.

Kelly, Edward J., III. (1985). “Legislative History of the Glass–Steagall Act.’’ In Ingo Walter (ed.),Deregulating Wall Street: Commercial Bank Penetration of the Corporate Securities Market. NewYork: John Wiley & Sons, 41–65.

Kryzanowski, Lawrence and Gordon S. Roberts. (1992). “Bank Structure in Canada.’’ In GeorgeG. Kaufman (ed.), Banking Structures in Major Countries. Bostom: Kluwer Academic Publishers,1–57.

Litan, Robert and William Nordhaus. (1983). Reforming Federal Regulation. New Haven: Yale Uni-versity Press.

Litan, Robert E. (1987). What Should Banks Do? Washington, DC: Brookings Institution.Litan, Robert E. (1997). “Institutions and Policies for Maintaining Financial Stability.’’ In Maintaining

Financial Stability in a Global Economy. The Federal Reserve Bank of Kansas City, August, 257–297.

McDonald, John and Robert Moffit. (1980). “The Uses of Tobit Analysis.” The Review of Economicsand Statistics, May, 318–321.

McKenzie, George. (1990). “Capital Adequacy Requirements, Deposit Insurance and Bank Be-haviour.’’ The Economic and Social Review 21, 363–375.

Nathan, Alli and Edwin Neave. (1992). “Operating Efficiency of Canadian Banks.’’ Journal of FinancialServices Research 6, 265–276.

Maggs, Gary and David Pate. (1995). “The New Federal Stance on Bank Expansion: The Riegle–NealInterstate Banking and Branching Efficiency Act of 1994.’’ Durell Journal of Money and Banking,Fall, 17–22.

Moore, Robert M. (1995). “Does Geographic Liberalization Really Hurt Small Banks?’’ FinancialIndustry Studies, Federal Reserve Bank of Dallas, December, 1–12.

O’Driscoll, Gerald P. Jr. (1988). “Bank Failures: The Deposit Insurance Connection.’’ ContemporaryPolicy Issues 6, 1–12.

Pantalone, Colleen C. and Marjorie B. Platt. (1987). “Predicting Commercial Bank Failure SinceDeregulation.’’ New England Economic Review, July/August, 37–47.

Peltzman, Sam. (1976). “Toward a More General Theory of Regulation.’’ Journal of Law and Eco-nomics 19, 211–240.

Pierce, James L. (1991). The Future of Banking. The Twentieth Century Fund, Inc.Rolnick, Arthur J. (1987). “The Benefits of Bank Deposit Rate Ceilings: New Evidence on Bank

Rates and Risk in the 1920s.’’ Quarterly Review, Federal Reserve Bank of Minneapolis, Summer,2–18.

Salsman, Richard M. (1993). “Bankers as Scapegoats for Government-Created Banking, Crises inU.S. History.’’ In Lawrence H. White (ed.), The Crisis in American Banking, New York: New YorkUniversity Press, 81–118.

Shiers, Alden F. (1994). “Deposit Insurance and Banking System Risk: Some Empirical Evidence.’’Quarterly Review of Economics and Finance 34, 347–361.

Spong, Kenneth. (1990). Banking Regulation: Its Purposes, Implementation and Effects. Kansascity: Federal Reserve Bank of Kansas City.

HOW DOES REGULATION AFFECT THE RISK TAKING OF BANKS? 83

Stilger, George. (1971). “The Theory of Economic Regulation.’’ The Bell Journal of Economics andManagement Science 2, 3–21.

Swary, Itzhak and Barry Topf. (1992). Global Financial Deregulation: Commercial Banking at theCrossroads. Blackwell, Chapters 7, 8, and 13.

Wheelock, David C. (1992). “Regulation and Bank Failures: New Evidence from the AgriculturalCollapse of the 1920s.’’ Journal of Economic History 52, 806–825.

White, Eugene Nelson. (1986). “Before the Glass–Steagall Act: An Analysis of the Investment Bank-ing Activities of National Banks.’’ Explorations in Economic History 23, 33–55.

White, Lawrence H. (1993). “Why is the U.S. Banking Industry in Trouble? Business Cycles, LoanLosses, and Deposit Insurance.’’ In Lawrence H. White (ed.), The Crisis in American Banking, NewYork: New York University Press, 7–28.

Jill M. Hendrickson is an Assistant Professor of Economics at the University of the South inSewanee, Tennessee. Her area of specialty is money and banking, with emphasis on the impact ofregulation on bank performance and behavior.

Mark W. Nichols joined the faculty of the Department of Economics at the University of Nevada,Reno in July 1996. Nichols’s area of specialty is industrial organization and public policy.