home entertainment & displays group

TRANSCRIPT

Home Entertainment& Displays Group

Philippe LambinetExecutive Vice President

HED Group

2

Audio• Analog Audio Amplification• Digital Audio Amplification• Digital Signal Processing

Home Video & Integrated Silicon Solutions

• Set-Top Box• High Definition DVD• Multimedia Player

TV & Monitor• Digital TV• Large-LCD Driver• TV Sound Processor• Internet TV• e-Paper• Display port

Leader in Multimedia Convergence Solutions

3

Computer Peripherals

Digital Consumer

AutomotiveCommunications

Industrial

2007 Rankings*:

#4 Digital Consumer

Source: iSuppli, March 2008

ST’s Targeted Segments: Focusing on Fast Growing Markets

4

Q106 Q206 Q306 Q406 Q107 Q207 Q307 Q407 Q108*

Digital Consumer Sales (ex Flash)

FY07: +10%

Q108: +9% excluding Genesis

Digital Consumer: Positive Momentum

*Q108 results include Genesis

5

• Set-top Box– >10Mpcs single-chip H.264 shipped since 2005: STi710x and STi520x

family of devices– Majority of products in leading-edge technologies, sampling 65nm– Leader in Operator markets: Cable, Satellite and IPTV– Solid position in retail markets (Free-to-Air): Satellite and Terrestrial

• Digital TV– Addressing market with STB “Plug-in” solutions

• >10Mpcs MPEG shipped in Digital TVs since 2006• Leading supplier of MPEG for European DTV market• Now shipping H.264 in Digital TVs: STi710x family

– Acquired Genesis: integrating image and video processors into ST’s product offering

2007: 78Mpcs MPEG decoders shipped worldwide +24% Y-o-Y

ST Leading MPEG SoC Supplier

6

• Enables ST to be at the forefront of the integration and convergence trends that are reshaping the marketplace

• Natural strategic fit / complementary technologies (image quality and image coding) – ST is a leader in digital consumer technologies, with a strong position in set-top box compression / decompression

technologies and “front-end” processing technologies in digital TV– Genesis is a leader in “back-end” image processing, video quality and digital interconnect technologies

• Ensure expanded market presence--both current and future generation DTV solutions– Exploit technology leadership: video processing chain 1080p120Hz– Fast execution capability at platform level– Genesis’s major customers include LG Electronics, Toshiba, Samsung and Dell

• Accelerate the penetration of DisplayPort into the consumer electronics market– An innovative technology for display interconnect– Improve positioning via ST’s leadership in the set-top box market

• Synergies from sales leverage, scale, cost savings and best-in-class R&D capabilities

ST to strengthen its leadership position in the fast growing DTV market

Genesis Acquisition: Strategic Rationale

7

• Effective control acquired on January 17th, 2008 – All-cash offer of $8.65 per share– Payment of about $170M, net of cash and equivalents, at closing, for the

acquired shares– Annual sales of approximately $200M

• Actions already implemented– Team fully integrated with ST’s TV and monitor team– Roadmap redefined and committed, leveraging both ST’s & Genesis’ IPs

• 2008 Action Plan / Priorities– Exploit cost synergies– Tape out next-generation single-chip TV: Freeman

Integration on track & clear roadmap defined

Genesis Acquisition: Integration Status

8

HD, H.264, DTV, DVR, Video over IP

IPTV

2007 2008 2009 2010 2011

New generation H.264 - 65nm / 55nm

ST’s Consumer Growth Opportunities

Home Connectivity

iDTV / Genesis

9

Set-Top Box• Capture market share in high-value applications

• Provide added-feature applications early to market

• Partner with OEMs, Operators, CA vendors, 3rd parties

• Accelerate move to smaller lithographies (90nm to 80nm, 65nm, 55nm)

Digital TV• Leverage set-top box expertise

• Target new high-volume applications

• Leverage Genesis products, sales and cost synergies

2008: Strategies for Growth

10

465

263

195

140100

75

35181062

324

387

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

ST introduces first MPEG-2

decoder

Satellite

Terrestrial

IPTV & iDTV

1-chip H.264

Cumulative MPEG-2 & MPEG-4 Shipments (Mu)

ST introduces OMEGA SoC

465

ST: # 1 in MPEGOver 465 Million MPEG Decoders Shipped

Highest shipment in one year

11

SAT

43%

CABLE

54%

DTT

42%

IPTV

37%

iDTV

21%

0

10

20

30

40

50

60

70

80

ST Others % Share

Mu

Source: ST, IMS Research (Dec. 2007)

#1 WW MPEG supplier#1 in Operators

#1 in H.264#1 in iDTV Europe

Solid position in FTA

“(in 2006) STMicroelectronics was the top supplier of MPEG-2 MP SD set top box decoder ICs and H.264 decoder ICs.”inStat, Jun’07

“STMicroelectronics led the Q307 IC market with stand-alone MPEG-2 processors shipping into DVB-T TVs.”DisplaySearch – Quarterly TV Report, Nov’07

2007: ST Leading the MPEG Market

12

1112Camcorders1112Personal & Portable Stereos1311Analog CRT TV1010Handheld Video Game Players79DVD Video Players78Digital Still Cameras77DVD Video Recorders55Video-Game Consoles65Digital Picture Frames34PMP / MP3 Players33Home Audio-System Components22Digital Set-Top Boxes11Digital TV

SemiEquipApplication

OverallMarket Opportunity Ranking (2007 2012)

Set-Top Box:Forthcoming Strong Market Growth

0

50

100

150

200

250

2007 2008 2009 2010 2011 2012$50

$100

STB (millions of units)

Manufacturing value ($) per box

Source: iSuppli, March 2008

Total STB manufacturing value CAGR 2008 2012 = +10%

13

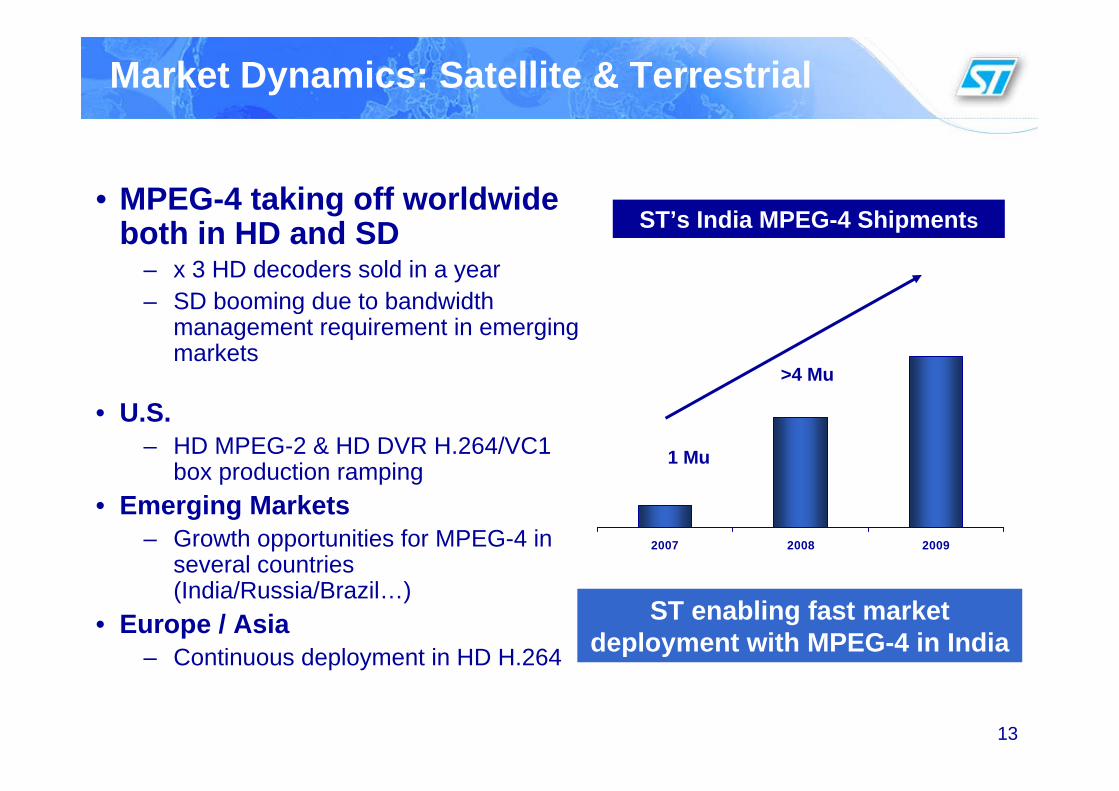

Market Dynamics: Satellite & Terrestrial

• MPEG-4 taking off worldwide both in HD and SD

– x 3 HD decoders sold in a year– SD booming due to bandwidth

management requirement in emerging markets

• U.S.– HD MPEG-2 & HD DVR H.264/VC1

box production ramping• Emerging Markets

– Growth opportunities for MPEG-4 in several countries (India/Russia/Brazil…)

• Europe / Asia– Continuous deployment in HD H.264

ST’s India MPEG-4 Shipments

2007 2008 2009

>4 Mu

1 Mu

ST enabling fast market deployment with MPEG-4 in India

14

Market Dynamics: IPTV STB

LYSESES AMERICOMSUREWESTTELEKOM AUSTRIATELEFONICATELIAetc…

ALICECHINA TELECOMCHINA NETCOMDARTY BOXFASTWEBFRANCE TELECOMKOREA TELECOM

Operators

ST positioned with market leaders

Success factors: Robust hardware + software system solutions, security, partnerships with software/security vendors

15

Market Dynamics: IPTV STB

• Market-proven ST solution:– Linux high-end feature set:

• PVR / DnP• Media Center• Video Conferencing• Enhanced Graphics

– Easy migration from SD to HD in H.264

– AVS solution qualified– 65nm in ‘08, 55nm in ‘09

• Market highlights– Europe: Strong ST position – China & Emerging Markets:

Very strong market growth in 2008 (H.264 and AVS)

– US: high-performance PVR solutions in production

2007 2008(e) 2009(e)

Europe Americas Asia/Pacific*

ST’s IPSTB Shipment by Region

2.2 Mu

>4 Mu

* Asia/Pacific includes China

16

Market Dynamics: Cable

• China – Continued market growth led by ST – Fast Analog to Digital transition– Shipping MPEG-4 and starting HD

MPEG-4• Europe

– ST enabling cable operators to offer Triple Play in HD MPEG-4

– Market growing at steady rate• Latin America & India

– Shipping volume, next opportunity for growth

• US – Partner of Cisco / Scientific Atlanta

0

50

100

150

200

2006 2007 2008 2009 2010

Analog Digital

China Cable Market

Source: Screendigest

Mu

17

• 80nm– Fast production ramp up in replacement of our

previous 90nm family – margin improvement

• 65nm 55nm– Deployment in ‘08 with major OEMs

– Extension of the HD MPEG-4 product family expands addressable market

• 7200 Dual TV – Media Center

• 7111 DVB-S2 & DVB-S Single-Chip Decoder

• 7141 DOCSIS Single-Chip Decoder PVR

– 55nm first engineering samples in fab

• 32nm – First product under definition

New Products Status

18

ST Designing Low-Power

• Transition to low-power advanced process– ST deployed MPEG-4 HD in 90nm, moving existing designs to 80nm– 65nm Low-Power technology 55nm

• 7111 HD MPEG-4 DVB-S2: lower than 2.5mW

• Active management of power savings– ST optimized solutions involving HW / SW know-how

• Other advantages for Energy-Saving initiatives:– Silence, slim design, resistance to heat, extended lifetime, cost

reduction

• Ahead of international ruling and supporting sustainable-development initiatives

Best-in-class performance

19

Market Dynamics: Digital TV

• Market expectations:– Bigger screens better image quality,

full HD & 120Hz

– Built-in DVR, time shift

– Watch Internet Video content

– Support H.264 HD broadcast (Europe first)

– Support for multiple front-ends(terrestrial, cable, satellite)

iDTV

Dig. Ready TV

Analog TV

0

50

100

150

200

250

300

2007 2008 2009 2010 2011 2012

CAGR ’08 ’12:Dig. Ready TV: +6%Integrated DTV: +25%Total TV: +5%

Source: iSuppli Q1’08

MU

20

Recognized Name in Home Theater

Faroudja - Established Brand Equity

• Winner of 3 Emmy awards• Manufactured exclusively by Meridian• Installed into high-end home theater installations

• 38 year history• Over 65 video patents• Focus on exceptional video quality

Faroudja Video Processors

Badge of Excellence

21

TV RoadmapM

id R

ange

Perf

orm

ance

20082008 20092009

Entr

y

High Quality 10-bit video procMulti-standard MPEG-2/H.264/AVSDVB-T DemodulatorWW Analog AudioFlash DVRFRCAdvanced MediaVUE

Global H.264 PlatformDVR + Network Connectivity

STi5163STi5163

Hudson IIHudson II

SequoiaMP: Now

SequoiaMP: Now

Hudson IIMP: Now

Hudson IIMP: Now

STi710xSTi710x

STi710xSTi710x

DouglasDouglas

SequoiaSequoia

Global H.264 PlatformMPEG2 H.264 Plug-inExtensible to DVR & Network Connectivity

Low cost SD MPEG-2

DouglasMP: Now

DouglasMP: Now

Analog TV SoC

Digital TV SoC

DTV Decoder

• Genesis & ST IP combined into unified architecture

• Building block for rapid deployment of next-generation devices

FreemanFreeman

22

Douglas: Key Value Add

• Latest Faroudja DCDi Cinema Processing

• Single-footprint worldwide DTV solution– WXGA/1080p at 50/60/100/120Hz, ATSC/DVB/China

• Built on proven, mature H/W & S/W technologies

• High-performance Audio / Video / Graphics

• Scalable / Customizable to OEM requirements

• Competitive BOM cost

• Turn-key solution for quick time to market

23

Douglas Design In/Wins

LG 50PG60XX, 42LG60XX (Europe)

In Production!!

JapaneseTier 1 OEM In Design

Europe, China Models

China OEM In PP China

Model

Large Taiwan ODM In Design Europe Models

China ODM In PP US, China

Models

24

The DisplayPort Ecosystem

Cables & Connectors

Test & Measurement

PCs & Monitors

Semiconductor Solutions

25

DisplayPort is digital, faster, secure, extends over higher range, has the smallest connectorDisplayPort can be used for external and internal displays, unlike legacy standardsDisplayPort specification is evolving, unlike some legacy standards

0 3m 6m 9m 12m 15m

DVI

DisplayPort

Range Difference = 10m!Range Difference = 10m!

DisplayPort

VGA

DVI

DisplayPort Compared to External Legacy Standards

26

Emerging DisplayPort Application in 2-Box TVs

Application: Wall-mounted, super-thin “2-unit” HDTV systems

DisplayPort’s Value Proposition for this Application– High-Bandwidth Digital Interconnect for 1920x1080, 120Hz HD Video and Audio– Optimum Range – supports FHD over 15m cables– HDCP “Hollywood-approved” content protection– 1Mbps, 2-way AUX Channel enables Remote Control functionality

Console

Set-Top boxes

Game Consoles

DVD players

DisplayPort

27

What’s Next for DisplayPort?

VESA is developing evolutionary enhancements to DisplayPort that address specific user needs while maintaining compatibility with DisplayPort 1.1

DisplayPort enhancements are planned for specification in 2008, and they are….

High Speed Auxiliary Channel Multi-Monitor Support Over Single Connector

Mini-Connector

Eliminate need forUSB cable to monitor

Single cable DisplayPort connectivity

Multiple remote displays Simple notebook dockingSimplified multi-monitorsupport for desktop &signage

Enable DisplayPort use on ultramobile PCsComplements standard DisplayPort connector Simple passive adapter supports use with standard DisplayPort cables