hf july 2015 single pages

DESCRIPTION

Shared Ownership, Help to Buy, Affordable Housing, Low Cost Home Ownership, LCHO, Part Rent Part BuyTRANSCRIPT

WIN

homefocus

AT T R A C T I V E , A C C E S S I B L E , A F F O R D A B L E H O M E S

Shared Ownership

and Help to Buy

LOOKING TO BUY

YOUROWN

HOME?

REASONS TO BUY

NOT RENT

ANDREA McLEANgives her views on design, buying a first home and affordable housing

‘Now I’m paying less for a brand new home with an extra bedroom’ says Carla

TV Presenter

MADE MORE AFFORDABLE

JULY/AUGUST 2015

A LEATHER SOFA FROM FURNITURE CHOICE

WIN

2 homefocus • JULY/AUGUST 2015

With energy bills on the rise, call us free on 0800 0014 706 or visit www.myhomeenergyswitch.org.uk today to find the best price for your gas and electricity.

It’s free, fast and simple to switch and we’ll take care of all the paperwork.

DO YOU WANT TO PAY LESS FOR YOUR ENERGY

Don’t miss out...Get the next 6 issues of homefocus delivered through your doorPublished every other month to keep you up to date with the latest opportunities in shared and affordable home ownership

Just £12.95 for the next 6 issues

n The latest affordable developments in your region n Who to ask and where to find an affordable home n Advice on legal and mortgage matters from specialistsn Information about shared ownership, New Build HomeBuy, FirstBuy, and all low cost home ownership schemes

PLUS MUCH, MUCH MORE; celebrity interviews, competitions and reader offers, jargon busters and homestyle articles

To be sure of receiving the next 6 issues of homefocus, fill in the form and send your cheque* for £12.95 to:

Graid Publications Ltd, 1 Kings Hall12b Kings Rd, Westcliff SS0 8LR

*Please ensure that your cheque is made payable to Graid Publications

Call us on 0203 096 7141 for our bank details and you can pay online

Name ______________________________

Address ____________________________

____________________________________

____________________________________

____________________________________

Postcode ___________________________

Phone number ______________________

Email address ______________________

____________________________________

Signature ___________________________

Date _______________________________

Payment options:

n I’d like to receive the next 6 copies of homefocus and my cheque is enclosed

n I’d like to receive the next 6 issues of homefocus and would like to pay electronically. Please call me or email as above for me to make an electronic payment. Remember you can call us on 0203 096 7141 or email [email protected] for the info you need.

HOME OWNERSHIP FOR ALL?This issue of homefocus has quite a number of references to

‘the circus’…why? Well, just like the circus, home ownership is

intended for everyone. First time buyers, couples and families

from all walks of life.

But new data from the Generation Rent Report has found home

ownership is becoming elitist! The proportion of potential first time

buyers saving for a deposit has dropped 6% compared to three

years ago with many now given up on their dreams of becoming a

home owner..

That’s where shared ownership and Help to Buy come in! They

are Government sponsored schemes helping bring opportunities

within the reach of those buyers on more modest incomes.

At the risk of belabouring the comparison, the circus big top has

a safety net. With shared ownership, there’s a safety net too; a

financial interview to make sure that buyers buy as much as they

can afford but no more!

In fact there are rules, regulations and good practises to cover

many aspects of buying through shared ownership and Help to

Buy. Some people find them a bit off-putting. But just like the circus

safety net, they are there to prevent damaging accidents. Right

throughout this issue of the magazine, you’ll find examples of

those who successfully ‘walked the tightrope’ to home ownership.

I hope you’ll take inspiration from them and find your way to a

home of your own.

Happy home hunting

Jeffrey Gritzman • Publisher

ISSN No 1470-0360

ADVISORY PANELMaddie Cross LONDON BOROUGH OF BEXLEY

Dave Evans BE CREATIVE LONDON Tony Harker GENESIS HOMES

Dave Lakin GRAND UNION HOUSING GROUP Trevor Morley DIRECTION LAW

Yvette Ruggins SOUTH PARK ASSOCIATES

Isabel Saville CONCORDIA HOUSING CONSULTANCY

Simon Scott ORIGIN HOUSING

Sharon Shaw MARTIN SHAW CONSULTING

Richard Stone CENSEO LTD

Helen Towner HOMES AND COMMUNITIES AGENCY

Greg Warner-Harris SPECTRUM HOUSING GROUP

Chris Winfield LONDON BOROUGH OF BRENT

EDITORAlex Randell

e-mail: [email protected]

SUBSCRIPTIONS & GENERAL ENQUIRIESJulie Baugh Tel: 0203 096 7141

e-mail: [email protected]

PUBLISHER Jeffrey Gritzman Tel: 0203 096 7141

e-mail: [email protected]

PUBLISHED BYGraid Publications Ltd, 1 Kings Hall12b Kings Road, Westcliff SS0 8LR

Tel 0203 096 7141

DESIGN & PRODUCTIONJohn Eldridge Design Associates

Website: www.homefocus.co.uk

www.facebook.com/homefocus

www.twitter.com/homefocus

homefocus

Supports the aims of homefocus

Publisher’sComment

homefocus • JULY/AUGUST 2015 3

34

26

13

Hot properties 12 London A selection of affordable homes in the Capital

16 East & south-east And some in the east & south east region - as defined by the Homes & Communities Agency

20 South Affordable properties in the south

24 Midlands And some in the midlands

28 South west Finally, find affordable homes in the south west corner of the country

Just for you 3 Publisher’s comment Home ownership for all?

ContentsJULY/AUGUST 2015

Buying Guide 6 Destination home ownership Say goodbye to the rental circus

8 Home ownershipNot just for high flyers

10 Stop clowning around Compare the cost of renting and buying

42 Finding your place on the ladderShared ownership and Help to Buy bring buying opportunities to different all kinds of people

46 Time to buy When the developers and local authority invest in an area, it may well mean…time to buy!

Celebrity Status 34 In Conversationwith TV presenter Andrea McLean who says ‘home ownership ‘is a choice that everyone should be able to take part in’

Where next? Homefinder DirectoriesOr search affordable homes at www.homefocus.co.uk/Low-cost-homes-near-you

54 Introduction

55 Shows and Events

56 Property Listings

60 East and South East

61 South West

62 London 64 Midlands 65 South 66 Legal Directory

THE SMARTER WAY TO HOME OWNERSHIP IN LONDON OUTSIDE LONDONShared ownership is a cost effective way of getting your own property. You buy a 25%-75% share, with a mortgage and deposit, and then pay rent on the remainder. It’s often cheaper than renting the same property, with the bonus of owning part of it.

Genesis offers a wide range of homes available for shared ownership across London and Eastern England. Not only are those properties affordable, they’re designed to a high standard. Call us today to find out just how easy and affordable your next move could be.

*Starting prices are for a 25% share of the property. Eligibility requirements apply, please call us for more information. Details correct at time of going to press. Images representative only

Jessops At New Providence Wharf, Docklands 1 & 2 Bedroom Apartments From £96,188*

Zenith House, Colindale 2 Bedroom Apartments From £90,000*

Factory Quarter, Hammersmith & Fulham 1, 2 & 3 Bedroom Apartments, Prices To Be Confirmed

City Park West, Chelmsford 1 & 2 Bedroom Apartments From £46,250* Stoke Quay, Ipswich 1 & 2 Bedroom Apartments From £23,125*

For more details or to view a property call

0800 954 5633 genesishahomes.org.uk

Contact us... E-MAIL: [email protected] PHONE: 0845 474 4734

MAIL: homefocus magazine 1 Kings Hall, 12B Kings Rd Westcliff SS0 8LR

Lifestyle 38 Naturally neutralNeutral colours can add a sense of calm to any room

44 Super StripesBring bold colours into your home, …with stripes

Competition 52 CompetitionWin a Leather Sofa from Furniture Choice

homefocus

14

52

25

WIN38

44

THE SMARTER WAY TO HOME OWNERSHIP IN LONDON OUTSIDE LONDONShared ownership is a cost effective way of getting your own property. You buy a 25%-75% share, with a mortgage and deposit, and then pay rent on the remainder. It’s often cheaper than renting the same property, with the bonus of owning part of it.

Genesis offers a wide range of homes available for shared ownership across London and Eastern England. Not only are those properties affordable, they’re designed to a high standard. Call us today to find out just how easy and affordable your next move could be.

*Starting prices are for a 25% share of the property. Eligibility requirements apply, please call us for more information. Details correct at time of going to press. Images representative only

Jessops At New Providence Wharf, Docklands 1 & 2 Bedroom Apartments From £96,188*

Zenith House, Colindale 2 Bedroom Apartments From £90,000*

Factory Quarter, Hammersmith & Fulham 1, 2 & 3 Bedroom Apartments, Prices To Be Confirmed

City Park West, Chelmsford 1 & 2 Bedroom Apartments From £46,250* Stoke Quay, Ipswich 1 & 2 Bedroom Apartments From £23,125*

For more details or to view a property call

0800 954 5633 genesishahomes.org.uk

THE SMARTER WAY TO HOME OWNERSHIP IN LONDON OUTSIDE LONDONShared ownership is a cost effective way of getting your own property. You buy a 25%-75% share, with a mortgage and deposit, and then pay rent on the remainder. It’s often cheaper than renting the same property, with the bonus of owning part of it.

Genesis offers a wide range of homes available for shared ownership across London and Eastern England. Not only are those properties affordable, they’re designed to a high standard. Call us today to find out just how easy and affordable your next move could be.

*Starting prices are for a 25% share of the property. Eligibility requirements apply, please call us for more information. Details correct at time of going to press. Images representative only

Jessops At New Providence Wharf, Docklands 1 & 2 Bedroom Apartments From £96,188*

Zenith House, Colindale 2 Bedroom Apartments From £90,000*

Factory Quarter, Hammersmith & Fulham 1, 2 & 3 Bedroom Apartments, Prices To Be Confirmed

City Park West, Chelmsford 1 & 2 Bedroom Apartments From £46,250* Stoke Quay, Ipswich 1 & 2 Bedroom Apartments From £23,125*

For more details or to view a property call

0800 954 5633 genesishahomes.org.uk

THE SMARTER WAY TO HOME OWNERSHIP IN LONDON OUTSIDE LONDONShared ownership is a cost effective way of getting your own property. You buy a 25%-75% share, with a mortgage and deposit, and then pay rent on the remainder. It’s often cheaper than renting the same property, with the bonus of owning part of it.

Genesis offers a wide range of homes available for shared ownership across London and Eastern England. Not only are those properties affordable, they’re designed to a high standard. Call us today to find out just how easy and affordable your next move could be.

*Starting prices are for a 25% share of the property. Eligibility requirements apply, please call us for more information. Details correct at time of going to press. Images representative only

Jessops At New Providence Wharf, Docklands 1 & 2 Bedroom Apartments From £96,188*

Zenith House, Colindale 2 Bedroom Apartments From £90,000*

Factory Quarter, Hammersmith & Fulham 1, 2 & 3 Bedroom Apartments, Prices To Be Confirmed

City Park West, Chelmsford 1 & 2 Bedroom Apartments From £46,250* Stoke Quay, Ipswich 1 & 2 Bedroom Apartments From £23,125*

For more details or to view a property call

0800 954 5633 genesishahomes.org.uk

Great Advice 32 Never mind the b****cksShattering a few shared ownership myths and misconceptions

36 Juggling financesSome examples of what sort of property your income will get you under shared ownership and the Help to Buy schemes

40 Money, Money, Money Get yourself ready to get the best possible mortgage

48 Moving ChecklistWho to tell you’re on your way

50 Ask the Experts How to sell your share when you’re ready to move on

6 homefocus • JULY/AUGUST 2015

F ed up watching the high flyers in their mansions. Or paying rent to

clowns so that you finish up paying their mortgage instead of your own? Wondering why you have to do financial acrobatics each month when you have nothing to show for it?

You might still be living at home, or perhaps you’re already renting, maybe recently left a relationship without enough equity to buy another place. Wouldn’t it be great if you owned a home of your own?

Well, it could be possible and here is something that will help you pack your trunk but avoid the rental circus.

There are schemes that allow you to buy just a percentage of your home, and still move in. Collectively, these schemes are called low cost home ownership (LCHO) and they’re designed to be affordable, which means you not only do you get to live in ‘The Big Top’, but you’ll have something left over, to buy candy floss and ice cream at the interval!

No need to move aroundIf you’re ready to stop moving around and be part of the community by buying your own home, LCHO is a great idea. You’ll need a smaller mortgage and a smaller deposit than you probably expect. In many cases, it works out cheaper than renting a similar property privately.

Once you’ve found your own place through LCHO, it’s flexible enough to change with you when your circumstances alter. You can buy more of your home – in shared ownership this is called staircasing, and in most cases you can staircase until you own 100%. For equity loan schemes, you can pay off some or all of the equity loan. And when you come to sell, there should be a ready-made list of people who are hoping to buy through LCHO in your area. People who are in the same position you’re in now - keen to become home owners for the first time.

The Ringmaster The majority of LCHO schemes are backed by the government so the help you receive will be there for the long-run. It’s unlike renting privately, where your landlord could end your tenancy even if you’ve paid your bills on the dot.

The Ringmaster for the LCHO process is a Help to Buy Agent. These are organisations appointed by the government

to promote and co-ordinate LCHO in a particular area, and there’s a list of them of page 54. Outside

of London your Help to Buy Agent will process your application so you don’t

need to apply to every housing association, and they have a list of every government-funded LCHO home in their area. In London, things are slightly different, but there’s still a LCHO online portal

to get you started. Wherever you are, Help to Buy Agents will help run the show.

Three ringed circus There are three LCHO ways to

get onto the homeownership ladder and the scheme to go for depends on your personal circumstances. There’s no

guarantee that all options will be available to you,but where there

is a choice, your financial situation will dictate what’s offered. There are

more details of the specific schemes on the next two pages, but essentially they are:

Shared ownershipAlso known as part buy/part rent. This works by allowing you to buy a share of your home and pay a subsidised, capped rent on the remainder, which is owned by a housing association. You’ll be expected to buy the largest share you

Say goodbye to the rental circus!

TIME TO PACK YOUR TRUNK?

Buyer’sGuide

can afford –but don’t worry, the key word there is ‘afford’, so you’ll be able to discuss what share is right for you.

Equity loansYou own 100% of your home, but only have to cover a percentage of the cost initially with your mortgage and deposit. You can defer the rest for a while as it’s covered by an equity loan. There’s nothing to pay on the equity loan for a few years, and the scheme you choose will determine whether you pay any interest after this and when you have to pay the loan back.

Save to buyThere are two options offered by housing associations that will help and encourage you to save towards a deposit for a home. Rent to buy will allow you to pay a reduced rent on the understanding that you will buy that specific home in due course and intermediate market rent will provide you with a reduced rent to save for a deposit to buy elsewhere.

The oohs and aahs You may have already heard of LCHO but thought ‘it’s just for people with specific jobs or it’s social housing by a different name.’ Well, you couldn’t be more wrong! It’s home ownership, and you’ll take on all the responsibilities, and have all the benefits, that go with it. LCHO is designed for a whole range of people who’ve been otherwise priced out of the market.

The first time buyer schemes such as shared ownership and resales are appropriate for anyone with a household income LESS than £60,000 (£71,000 if you’re looking for one or two bedrooms in London and £85,000 for three bedrooms or more). And for Help to Buy, the criteria is even wider.

You COULD be eligible for the schemes if…• You’re a first time buyer• You’ve owned a home in the past but don’t own one now • You need to buy a home of your own for the first time, for example after a relationship breakdown

• You own your own home but it’s far too small for your needs. For example, you might have two children in a one-bedroom flat and can’t afford to buy somewhere bigger • You can’t otherwise afford to buy a suitable home in the area you need to live in• You’re working even though it’s not full time (you’ll have to show that you earn enough to cover your housing and living costs though. And you might be able to count long-term benefits towards your income)• You’ve got a large chunk of money to put down (for example if you have equity from a previous home after a relationship split and use that towards buying your share outright. Again, you’ll have to show you have enough coming in to cover your housing and living costs).

You’re NOT eligible for shared ownership if...• You already own a home that you’re living in and it’s adequate for your needs• You can already afford to buy a suitable home of your own in your area

You’re NOT eligible for any affordable home ownership scheme if...• You want to buy a property to rent out. LCHO funding is there to help people to buy a home, not to become a landlord• You already own a home and now want to help your adult child or children to get on the ladder. You can help them with their deposit BUT it’s your children who would have to apply and be eligible. • CCJ’s or a bad credit rating make it unlikely that you can pass financial assessments

homefocus • JULY/AUGUST 2015 7

8 homefocus • JULY/AUGUST 2015

Scheme type Shared ownership Help to Buy Save to Buy

Scheme name New Build Resales Help to Buy Equity Loan Help to Buy Mortgage Guarantee

Rent to Buy Intermediate Market Rent

YOU CAN FLY HIGH TOO

You buy the share of your home you can afford (between 25% and 75%) and pay a subsidised rent on the remainder. You can buy more shares over time until in most cases you own 100% of your home. You may see shared ownership referred to as part buy/part rent.

These are properties that have already been bought through shared ownership in the past, and where the owners are now looking to sell their share and move on. You buy the share they are selling and pay a subsidised rent on the remainder. You might see resales referred to as ‘existing shared ownership’.

Available on newly built properties up to a value of £600,000. You buy 100% of your home but only have to pay for 80% initially. The rest is covered by an equity loan from the government. There’s nothing to pay on the equity loan for the first five years, after which there’s a small interest charge.

Designed to make 95% mortgages available to a wide range of people. More importantly it means that you only need to raise a 5% deposit. These mortgages will be available on new and older properties costing up to £600,000.

This is available on selected new developments and gives you the opportunity to rent the home you wish to buy at a reduced rate, on the understanding that you’ll buy it through shared ownership within a specific time. In London there’s a similar scheme called Rent to Save, ideal if you want to buy a home in the city.

Offers you the chance to rent a brand-new or refurbished home or a home that is being re-let for a reduced rent. The rent charged is usually around 80% of the rent that you would expect to pay if you were renting from a private landlord

SURE-FOOTED Ideal if you live in an area where prices are high as you only need to buy the percentage you can afford (just as long as it’s over 25%). This means you need a smaller mortgage. It’s also perfect if you don’t have much in the way of savings as you only need to find the deposit for the share you’re buying.

Not limited to recently-built homes so properties are likely to be in established communities and you may have a wider choice of styles. The rent element is almost always lower than on new build because of controls on the amount the rent has been allowed to increase each year.

Great if you can almost afford your home but don’t have a thumping great deposit to start you off. You only have to find a 5% deposit. Not restricted to first time buyers, and doesn’t have the same income restrictions as shared ownership, so you can use the scheme to move to a larger home or one in a more expensive area.

It’s perfect if you can afford a mortgage for 95% of your home, but don’t have a large deposit. And as it’s available on existing properties as well as new ones, you can still benefit even if you want to live in an older home or somewhere that’s seen no new homes for a while.

Perfect if you can demonstrate that you could afford to buy 25% of your home, but are not in a position to do so straight away – for example you earn enough for a mortgage but don’t have a deposit saved. It gives you a chance to put down roots and move into your new home sooner.

Great if you’re looking to rent for the short term whilst building a deposit to buy your first home.

SAFETY NET As with the most of the schemes on these pages, the properties are all new-builds, which might not be to your taste. If you’re looking for period features, though, you might find a shared ownership home that’s a conversion of an older building.

You’re unlikely to be able to buy a smaller share than the previous owners are selling, though it may be possible to buy more. And you’re buying someone else’s taste in décor – though it’s fun to change it!

You still have to be able to afford 80% of your home with your mortgage and deposit, so if you live in a very expensive area house prices could still be out of reach.

You still have to be able to get a mortgage for 95% of your home, so might not be right for you if you want to live in an expensive area.

There are very few Rent to Buy properties available, and no more are planned outside London. You have to be disciplined to use the discount on your rent to save for your deposit.

This is a shorthold tenancy agreement only, initially covering just 6 months, after which the agreement can be extended.

BUY FROM JUST 25% WITH A SMALL DEPOSIT

WIDE CHOICE NOT JUST FOR FIRST TIME BUYERS

FOR HIGHER WAGE EARNERS

SAVE TO BUY THE NEW HOME YOU’RE LIVING IN

TYPICALLY 20% LESS THAN MARKET RENT

WANT MORE INFORMATION? Email: [email protected]

HOME OWNERSHIP:NOT JUST FOR HIGH FLYERS There are a number of ways to become a homeowner! This page gives you an at-a-glance reference to all the low cost home ownership (LCHO) schemes on offer, so if you find a home you like, you can check out the key points of the scheme.

What percentage of the home you need do you think you could buy with your deposit and mortgage?

Finding the right LCHO scheme can be a bit daunting, so focus on this question...

Scheme type Shared ownership Help to Buy Save to Buy

Scheme name New Build Resales Help to Buy Equity Loan Help to Buy Mortgage Guarantee

Rent to Buy Intermediate Market Rent

YOU CAN FLY HIGH TOO

You buy the share of your home you can afford (between 25% and 75%) and pay a subsidised rent on the remainder. You can buy more shares over time until in most cases you own 100% of your home. You may see shared ownership referred to as part buy/part rent.

These are properties that have already been bought through shared ownership in the past, and where the owners are now looking to sell their share and move on. You buy the share they are selling and pay a subsidised rent on the remainder. You might see resales referred to as ‘existing shared ownership’.

Available on newly built properties up to a value of £600,000. You buy 100% of your home but only have to pay for 80% initially. The rest is covered by an equity loan from the government. There’s nothing to pay on the equity loan for the first five years, after which there’s a small interest charge.

Designed to make 95% mortgages available to a wide range of people. More importantly it means that you only need to raise a 5% deposit. These mortgages will be available on new and older properties costing up to £600,000.

This is available on selected new developments and gives you the opportunity to rent the home you wish to buy at a reduced rate, on the understanding that you’ll buy it through shared ownership within a specific time. In London there’s a similar scheme called Rent to Save, ideal if you want to buy a home in the city.

Offers you the chance to rent a brand-new or refurbished home or a home that is being re-let for a reduced rent. The rent charged is usually around 80% of the rent that you would expect to pay if you were renting from a private landlord

SURE-FOOTED Ideal if you live in an area where prices are high as you only need to buy the percentage you can afford (just as long as it’s over 25%). This means you need a smaller mortgage. It’s also perfect if you don’t have much in the way of savings as you only need to find the deposit for the share you’re buying.

Not limited to recently-built homes so properties are likely to be in established communities and you may have a wider choice of styles. The rent element is almost always lower than on new build because of controls on the amount the rent has been allowed to increase each year.

Great if you can almost afford your home but don’t have a thumping great deposit to start you off. You only have to find a 5% deposit. Not restricted to first time buyers, and doesn’t have the same income restrictions as shared ownership, so you can use the scheme to move to a larger home or one in a more expensive area.

It’s perfect if you can afford a mortgage for 95% of your home, but don’t have a large deposit. And as it’s available on existing properties as well as new ones, you can still benefit even if you want to live in an older home or somewhere that’s seen no new homes for a while.

Perfect if you can demonstrate that you could afford to buy 25% of your home, but are not in a position to do so straight away – for example you earn enough for a mortgage but don’t have a deposit saved. It gives you a chance to put down roots and move into your new home sooner.

Great if you’re looking to rent for the short term whilst building a deposit to buy your first home.

SAFETY NET As with the most of the schemes on these pages, the properties are all new-builds, which might not be to your taste. If you’re looking for period features, though, you might find a shared ownership home that’s a conversion of an older building.

You’re unlikely to be able to buy a smaller share than the previous owners are selling, though it may be possible to buy more. And you’re buying someone else’s taste in décor – though it’s fun to change it!

You still have to be able to afford 80% of your home with your mortgage and deposit, so if you live in a very expensive area house prices could still be out of reach.

You still have to be able to get a mortgage for 95% of your home, so might not be right for you if you want to live in an expensive area.

There are very few Rent to Buy properties available, and no more are planned outside London. You have to be disciplined to use the discount on your rent to save for your deposit.

This is a shorthold tenancy agreement only, initially covering just 6 months, after which the agreement can be extended.

BUY FROM JUST 25% WITH A SMALL DEPOSIT

WIDE CHOICE NOT JUST FOR FIRST TIME BUYERS

FOR HIGHER WAGE EARNERS

SAVE TO BUY THE NEW HOME YOU’RE LIVING IN

TYPICALLY 20% LESS THAN MARKET RENT

WANT MORE INFORMATION? Email: [email protected]

Between 25% and 75%

Shared ownership could be right for you

Around 70% or more

Consider Help to Buy or an equity loan

100%, but I can only afford a 5% deposit Check out the mortgage guarantee schemes

I haven’t got enough for a deposit yet Time to start saving! Or take a look around for a try before you buy option

Buyer’sGuide

HOME OWNERSHIP:NOT JUST FOR HIGH FLYERS

homefocus • JULY/AUGUST 2015 9

10 homefocus • JULY/AUGUST 2015

F or some of us, renting is absolutely the right thing to do. It gives freedom and flexibility.

But if you’re serious about putting down roots and being part of the community, there’s nothing like owning your own home. It’s not just that you can decorate it as you want and have the security of knowing that you’re in control. You might find that buying through low cost home ownership (LCHO) could mean paying out less each month than if you rent. And who’ll be laughing then?

The figures on the next page show some typical comparisons from around the country. And in some of them, buying a minimum share works out less than renting a comparable property. It all depends on you being able to come up with that all important deposit. But before you tell yourself how much of an obstacle putting together a deposit can be, take a look at the deposits required for LCHO. Just 5% of the full amount for Help to Buy deals and only 5% of the share you’re buying under shared ownership. So buying may be more viable than you think.

With LCHO, you’ll also be able to afford a reasonable lifestyle too. The affordability checks that housing associations insist on before offering you LCHO mean that rather than paying every penny you earn just to keep a roof over your head, you’ll be able to get by comfortably.

So, if being a homeowner is what you really want, but you think that renting is a sensible stop-gap, just check and work through all of the figures first.

TIME TO STOP

CLOWNING AROUND?Getting your first place can be a hoot. Bed-sit, flat share, singles flat, private rent. All great fun. But if you want to avoid a ‘financial pie in your face’, take a serious look at the cost of renting compared to buying!

‘It’s nice to be on the property ladder having been forced to rent for so many years’

homefocus • JULY/AUGUST 2015 11

Architect Clementine Griggs, 30, was desperate to get on the property ladder in her home city of Chichester but didn’t think it was possible, until she discovered Affinity Sutton’s shared ownership apartments at Graylingwell Park; a development that combines new-build and renovated properties set in parkland.

Clementine had originally looked at two-bedroom apartments with the intention of buying with someone else, but it didn’t happen. A while later she worked out that on her own, she could afford to buy a share of a refurbished, one-bedroom apartment in a renovated section of the development’s original building.

‘I loved the apartment from the moment I saw it,’ says Clementine, ‘It’s a period property so it looks very pretty, but inside it is equipped with high quality modern fittings and has a great open plan living place.’

Through shared ownership, Clementine purchased a 35 per cent share of her new home for £60,375 (full market value £172,500). She currently pays £700 a month to cover her mortgage repayments and rent on Affinity Sutton’s share of the apartment. It’s far less than she was paying while renting. ‘It’s so nice to finally be on the property ladder having been forced to rent for so many years,’ said Clementine.

RentvBuy

Check the figures in your area…We’ve done a bit of checking around, and compared the price to rent a typical two-bedroom property with the cost of buying outright with a 95% mortgage, buying different shares through shared ownership, and buying through the 80% Help to Buy equity loan scheme. So do the sums and see if it’s time to stop clowning around.

Deposit Mortgage Mortgage pcm

Rent pcm Total monthly costs

Shared Ownership 25% share £3,600 £68,400 £400 £495 £895

Shared Ownership 50% share £7,200 £136,800 £800 £330 £1,130

Help to Buy 80% equity loan) £14,400 £216,000 £1,263 £0 £1,263*

Help to Buy Mortgage Guarantee £14,400 £273,600 £1,599 £0 £1,599

Renting Privately - - - £844 £844

Deposit Mortgage Mortgage pcm

Rent pcm Total monthly costs

25% share £6,325 £120,175 £703 £870 £1,573

50% share £1,2650 £240,350 £1,405 £580 £1,985

80% Help to Buy equity loan £25,300 £379,500 £2,219 £0 £2,219*

100% buy £25,300 £480,700 £2,810 £0 £2,810

Private rent - - - £1,736 £1,736

Deposit Mortgage Mortgage pcm

Rent pcm Total monthly costs

25% share £1,650 £31,350 £183 £227 £410

50% share £3,300 £62,700 £367 £151 £518

80% Help to Buy equity loan £6,600 £99,000 £579 £0 £579*

100% buy £6,600 £125,400 £733 £0 £733

Private rent - - - £569 £569

Deposit Mortgage Mortgage pcm

Rent pcm Total monthly costs

25% share £2,600 £49,400 £289 £358 £647

50% share £5,200 £98,800 £578 £238 £816

80% Help to Buy equity loan £10,400 £156,000 £912 £0 £912*

100% buy £10,400 £197,600 £1,155 £0 £1,155

Private rent - - - £977 £977

Deposit Mortgage Mortgage pcm

Rent pcm Total monthly costs

25% share £5,537 £105,213 £615 £761 £1,376

50% share £11,075 £210,425 £1,230 £507 £1,737

80% equity loan (Help to Buy) £22,150 £332,250 £1,942 £0 £1,942*

100% buy £22,150 £420,850 £2,460 £0 £2,460

Private rent - - - £1,302 £1,302

Chichester £288,000

Tooting £506,000

Plymouth £132,000

Birmingham City Centre £208,000

Bushey £443,000

The small print We’ve used an average repayment mortgage over 25 years at 5% to get our figures. Deposit amounts are 5% which reflects what is available in the market at the moment. Please note that Help to Buy Guarantee Mortgages are NOT available in conjunction with LCHO schemes. But we have used 5% deposits for 100% purchases assuming that the mortgage will be attained using a Help to Buy Mortgage Guarantee. Rent for shared ownership is based on 2.75% of the share you don’t own, per year (we then divide this by 12 to get a monthly rate). Private rents and property prices are based on averages in the area, taken from popular property websites not specific properties.* Please note that with a Help to Buy equity loan, you will be paying back some interest from year 6 onwards.

A major new development, Watermill Lane, is being launched adjacent to the North Middlesex Hospital. And Newlon Home Ownership is offering 28 one and two-bedroom apartments and 2 three-bedroom houses for shared ownership.

Each home has high quality finishes, smart layouts with open-plan living areas and large windows and all have been carefully designed to produce modern, energy efficient homes. All the apartments benefit from a balcony or winter garden

Incorporated into every home are wood laminate flooring to living areas,

Valley Park and Pymmes Park. First option will go to applicants

who live within the London Borough of Enfield.

Starting to think that you can buy your own home? Could buying in the Capital be more cost effective than renting or commuting? Then take a look at this selection of low cost home ownership (LCHO) homes. There are more listed on pages 57 & 58 and helpful contacts on our London homefinder, pages 62 & 63. Or visit www.homefocus.co.uk/Low-cost-homes-near-you.

London

WATERMILL LANE Edmonton, prices and shares tbc

Want to know more? Then email [email protected] with the name of the development that interests you in the subject line and don’t

forget to include your contact details. Or you can visit www.homefocus.co.uk.

* Approximate figures only, assuming a 25 year mortgage at 5.0%. **Assumes rent is charged at 2.75% of the share you don’t own, per year.; *** Help to Buy property, interest on the equity loan starts in year 6. Please note: monthly outgoings do not include service charges

www.homefocus.co.uk/Watermill-Lane

hallways and kitchens; with carpets to all bedrooms. Kitchens are by Moores from the Maida range and feature Bosch integrated appliances including fridge freezer, washing machine, dishwasher and a Zanussi hob and oven.

Satellite/terrestrial TV points and a secure door entry system are installed and Watermill Lane has some on-site parking.

The area is well served by bus routes, with Silver Street Overground Station a short distance away. Nearby are new and refurbished shopping centres, local amenities and attractive green space at Lee

12 homefocus • JULY/AUGUST 2015

London Properties

L&Q@GREENWICH PENINSULA Greenwich, prices and shares tbc

JESSOPS BUILDING New Providence Wharf from £93,688 for 25%

If jumps in house prices are anything to go by, then Greenwich is one of London’s most happening areas at the moment. And making it more affordable for those who would like to own their own home there, is L&Q’s mix of one and two-bedroom shared ownership apartments on the Greenwich Peninsula.

This is the first phase of L&Q’s development, a second phase is due later in the year with 34 apartments available across the two phases.

Dubbed ‘London’s ultimate village’, Greenwich Peninsula will transform 190 acres of marshland to deliver 10,000 new homes, 150 retail units and 48 acres of open green space, all set along 1.6 miles of prime Thames waterfront.

Interested? Email [email protected] with “Greenwich Peninsula” in the

subject. Remember to include your contact details. Or visit www.homefocus.co.uk/

Greenwich-Peninsula

Currently available on a shared ownership basis from Genesis, is Jessops Building in New Providence Wharf where a selection of one and two-bedroom apartments has been designed to a contemporary specification.

The homes are spacious, accompanied by balconies to most apartments, perfect for al fresco dining through the summer. Kitchens feature fitted units offering integrated Bosch

ELIZABETH WHARFRepton St E14 from £92,500 for 25%

Elizabeth Wharf is a car free development available via shared ownership from Currells.

This is a new residential development in up-and-coming area, right by the amenities of Mile End Park and the Regent’s Canal. An elegant footbridge carries you over from Salmon Lane to bustling Limehouse and leafy Mile End Park. And Riverside promenades along the Thames are a short walk away.

On offer are sixteen one, two and three-bedroom apartments set in a contemporary six storey building with

appliances including dishwasher and washing machine, granite worktops and chrome finishes. Bedrooms are spacious, and all rooms enjoy full height windows for plenty of natural light, balconies.

A hub of activity, New Providence Wharf is becoming a destination in its own right.

One-bedroom apartment: Full value: £374,750Minimum share: 25% • Cost of share: £93,6885% deposit: £4,685 • Mortgage on share*: £520Rent on remaining share**: £644 • Total costs: £1,164

Interested? Email [email protected] with

“Jessops Building” in the subject. Remember to include

your contact details.

Or visit www.homefocus.co.uk/Jessops-Building

* Approximate figures only, assuming a 25 year mortgage at 5%. **Assumes rent is charged at 2.75% of the share you don’t own, per year.; *** Help to Buy property, interest on the equity loan starts in year 6. Please note: monthly outgoings do not include service charges

a secure two-stage, dedicated entrance.The development is on the edge of

traditional residential streets and green open spaces, including Whitehorse Road Park –next to 10th century St. Dunstans – and Stepney Green Park, with its ever-popular City Farm.

First option will be given to those currently living or working in Tower Hamlets.

One-bedroom apartment: Full value: £370,000Minimum share: 25% • Cost of share: £92,5005% deposit: £4,625 • Mortgage on share*: £514Rent on remaining share**: £636Total costs: £1,150

Interested? Email [email protected] with

“Elizabeth Wharf” in the subject. Remember to include

your contact details.

Or visit www.homefocus.co.uk/Elizabeth-Wharf

homefocus • JULY/AUGUST 2015 13

Carla Rosser, 31, faced a common dilemma. She was desperate to escape

spiralling rent, but wanted to live close to her work and couldn’t afford the high property prices

Carla’s answer was to buy through shared ownership and she purchased a two-bedroom at XV11, Thames Valley Housing’s development in Tooting. Carla says ‘I’d been renting a one-bedroom apartment in Streatham Hill but rising rent was pricing me out of the area. I’m often on call with my work for the NHS

Blood and Transplant service at St George’s Hospital, so moving further out would have made life difficult’

The full price of Carla’s two-bedroom apartment, with off-street parking, was £380,000. She put down a £55,000 deposit and her 45% share cost £171,000. Her monthly outgoings are £1,101, made up of a £492 mortgage, £478 rent on the share she doesn’t own and service charges of £130.

‘The rent for my one-bedroom flat was £1,183 each month, says Carla, ‘now I’m

paying less for a brand new home with an extra bedroom, and I own a large share of it too’.

Carla also benefits from a new Thames Valley initiative – Shared Ownership PLUS which allows Carla to buy an extra 1% of her property each year over the next 15 years, potentially increasing her ownership to 60%. The cost of the extra share payments are predetermined so can be included in Carla’s budget and she can buy her home gradually at a pace she can afford.

Will this story inspire you to become a homeowner? See the list of low cost home ownership (LCHO) properties on pages 56-59. Or go to www.homefocus.co.uk/Low-cost-homes-near-you. Or you could call 0845 474 4734

‘I’m paying less for a brand new home with an extra bedroom, and I own a large share of it’

Carla Rosser

Previous situation: Renting

Scheme: Shared ownership

Location: Tooting

Provider: Thames Valley Housing

14 homefocus • JULY/AUGUST 2015

London Properties

THE VILLAGE E17 Walthamstow, from £96,250 for 35% (provisional price & share only)

VISIONGrahame Park, Collindale from £188,000 for 80%

Metropolitan Home Ownership is offering shared ownership at its new development in Shernhall Street, set between highly fashionable Walthamstow Village and the tube station.

Designed as two low level blocks to fit in comfortably with their surroundings, the shared ownership block will cover three floors and provide 6 one-bedroom apartments, 10 two-bedroom and 5 three-bedroom apartments.

A new phase of one, two and three-bedroom Help to Buy homes has been released by Genesis at Vision, part of the ongoing Grahame Park development in Collindale.

The homes are finished to an exacting standard with sleek, modern kitchens featuring granite worktops. Stainless steel appliances, including oven and microwave, and integrated white goods, combine style with practicality.

SAFFRON COURTE1 from £118,531 for 25%

Saffron Court is a new residential development in the heart of Spitalfields, close to the vibrant hub of Shoreditch. And Currell is offering a range of one and two bedroom apartments in this modern, six storey building with dedicated entrance, private amenity space, landscaped area, cycle parking and two children’s play areas.

All the apartments include a stylish interior specification, with some offering private balconies and patio areas. The development also provides a car club scheme for residents.

White bathrooms with chrome fittings are complemented by floor tiling and a heated towel rail.

One-bedroom apartment: Full value: £235,000 Minimum equity: 80% • Cost of equity: £188,0005% deposit: £11,750 Mortgage on 80% equity*: £1,030 Total costs: £1,030

Interested? Email enquiries@homefocus.

co.uk with “Vision” in the subject. Remember to

include your contact details.

Or visit www.homefocus.co.uk/Vision

* Approximate figures only, assuming a 25 year mortgage at 5%. **Assumes rent is charged at 2.75% of the share you don’t own, per year.; *** Help to Buy property, interest on the equity loan starts in year 6. Please note: monthly outgoings do not include service charges

Saffron Court is located on Pedley Street, close to Shoreditch station. A footbridge carries you over to bustling Cheshire Street and Brick Lane. The green spaces of Allen Gardens and Weavers Fields are a short walk away.

One-bedroom apartment: Full value: £474,124Minimum share: 25% • Cost of share: £118,5315% deposit: £5,927 • Mortgage on share*: £658Rent on remaining share**: £815 • Total costs: £1,473

Interested? Email [email protected]

with “Saffron Court” in the subject. Remember to

include your contact details.

Or visit www.homefocus.co.uk/Saffron-Court

A good bus service runs to Walthamstow Central and the tube and the overground station takes just over 15 minutes to Liverpool Street.

The Village is close to nurseries, primary and secondary schools and colleges. There’s a health care centre just across the road from the development and whilst we hope you never need to use it, Whipps Cross Hospital in close by.

First opportunities will be offered first, to those people already living or working in Waltham Forest.

One-bedroom apartment: Full value: £275,000Minimum share: 35% • Cost of share: £96,2505% deposit: £4,813 • Mortgage on share*: £535Rent on remaining share**: £556 • Total costs: £1,091

Interested? Email [email protected] with

“The Village” in the subject. Remember to include your

contact details.

Or visit www.homefocus.co.uk/The-Village

homefocus • JULY/AUGUST 2015 15

Want to know more? Then email [email protected] with the name of the development that interests you in the subject line and don’t

forget to include your contact details. Or you can visit www.homefocus.co.uk.

East & South East

Homes for singletons, couples and families are on offer through shared ownership at Heart of Medway’s St Andrews Park development in Halling.

A total of 38 homes is available and range from two, three and four-bedroom houses, and one and two bedroom apartments. All of the homes feature stylish fitted kitchens with integrated appliances, along with allocated parking.

Set in the picturesque North Downs,

Starting to think that you can buy your own home? Could buying in the east and south east be more cost effective than renting or commuting? Then take a look at this selection of low cost home ownership (LCHO) homes. There are more listed on pages 56 & 57 and East & South East homefinder on pages 60 & 61. Or visit www.homefocus.co.uk/Low-cost-homes-near-you.

ST ANDREWS PARK Halling from £73,750 for 25%

* Approximate figures only, assuming a 25 year mortgage at 5%. **Assumes rent is charged at 2.75% of the share you don’t own, per year. *** Help to Buy property, interest on the equity loan starts in year 6. Please note: monthly outgoings do not include service charges

St Andrews Park is close to the historic Medway towns and is surrounded by countryside and a beautiful blue chalk lake. Halling has its own train station, post office and convenience store as well as a local farm shop and two pubs.

Despite its delightful rural setting, Halling is far from remote. Its railway station provides high speed rail links to

London, while the nearby A228 gives swift access to the M2 and M20.

There is an infant and primary school within the village and the local secondary schools are Sir Joseph Williamson’s, Rochester Grammar School and the Robert Napier School.

Three-bedroom house: Full value: £295,000 • Minimum share: 25% • Cost of share: £73,750 • 5% deposit: £3,688Mortgage on share*: £410 • Rent on remaining share**: £507 • Total costs: £917

www.homefocus.co.uk/St-Andrews-Park

16 homefocus • JULY/AUGUST 2015

East & South East Properties

HIGHWOOD GREEN Marden from £320,000 for 80%

Golding Homes is offering shared ownership on a range of two and three-bedroom houses and two-bedroom apartments in a Redrow built development in Marden.

Named after the local World War One pilot Sidney William Highwood, Highwood Green is a classic, rural setting and offers a wonderful mix of traditional Kentish village life and modern living.

Commuters can reach London in 55 minutes from Marden station and travellers to further afield will find fast connections

BRIDGEWATER GARDENS Hoddesdon - prices and shares tbc

Overlooking New River and just a short walk to Rye House Marsh Nature Reserve, B3 Living is offering shared ownership (via its agent Red Loft), on 23 one and two-bedroom apartments at Bridgewater Gardens in Hoddesdon.

Each apartment has a contemporary design, with emphasis on light and good use of space.

The development is close to Rye House Station which has a direct service into Liverpool Street, taking commuters to the heart of the city in less than three quarters of an hour. Broxbourne is a 10 minute drive away where, where the fast service into Liverpool Street is even quicker.

The local area is all part of the Lee Valley Regional Park.

Interested? Email [email protected] with “Bridgewater” in the subject.

Remember to include your contact details. Or visit www.homefocus.co.uk/Bridgewater

* Approximate figures only, assuming a 25 year mortgage at 5%. **Assumes rent is charged at 2.75% of the share you don’t own, per year. *** Help to Buy property, interest on the equity loan starts in year 6. Please note: monthly outgoings do not include service charges

to the Channel ports and Paris via nearby Ashford International.

A pre-school and primary school is within walking distance of Highwood Green, together with access to Cornwallis Academy, Highweald Academy and the Maidstone Grammar Schools for older children.

First options will be given to those applicants with a local connection to Marden.

Interested? Email [email protected]

with “Highwood Green” in the subject. Remember to

include your contact details.

Or visit www.homefocus.co.uk/Highwood-Green

WATERLOO HOUSE Walton-on-Thames from £150,000 for 60%

Waterloo House is a development of one and two-bedroom apartments just over a mile from the centre of Walton-on-Thames, and Thames Valley Housing is offering them on a shared ownership basis.

An attractive four-story building, Waterloo House is characterised by soft red brick and cream render and set in landscaped grounds on Mayfield Road, a short stroll from Walton-on-Thames train station and easy commuting to London.

Each of the apartments is highly individual, with a choice of different layouts and all the homes feature an

open-plan living/dining/kitchen area that maximises the space.

Thames Valley is also making available their Shared Ownership PLUS scheme, a controlled and low cost way for buyers to increase their share each year.

One-bedroom apartment: Full value: £250,000Minimum share: 60% • Cost of share: £150,0005% deposit: £7,500 • Mortgage on share*: £833Rent on remaining share**: £229 • Total costs: £1,062

Interested? Email [email protected]

with “Waterloo House” in the subject. Remember to

include your contact details.

Or visit www.homefocus.co.uk/Waterloo-House

homefocus • JULY/AUGUST 2015 17

Retired graphic designer Grahame Dudley, 67, previously lived in a

three-bedroom, two-bathroom home in Iping and says, ‘As I owned that property with my ex-wife I was unsure whether I would be eligible for shared ownership but I was advised that this was not the case’.

Graham was able to purchase 33% of

his one-bedroom refurbished apartment at Affinity Sutton’s Grayingwell Park for £53,000 and just pays £378 per month in rent to Affinity Sutton on the remaining share. His total monthly outgoings are considerably less than the average rental cost in Chichester or West Sussex

Grahame is pursuing a BA degree in fine arts and found the ascetic side

of Grayingwell Park very appealing; ‘It’s a very beautiful development. The architecture and materials used in the building work have clearly been carefully considered and it shows,’ says Grahame. ‘The high windows and ceilings throughout the apartment flood the rooms with natural light and give every room an astounding sense of space.’

Will this story inspire you to become a homeowner? See the list of low cost home ownership (LCHO) properties on pages 56-59. Or go to www.homefocus.co.uk/Low-cost-homes-near-you.

Graham Dudley

Previous situation: Homeowner before relationship split

Scheme: Shared ownership

Location: Chichester

Provider: Affinity Sutton

Help to Buy Agent: Helptobuyese.org.uk

Grahame Dudley wanted to get back on the property ladder and rebuild his life

18 homefocus • JULY/AUGUST 2015

homefocus • JULY/AUGUST 2015 19

East & South East Properties

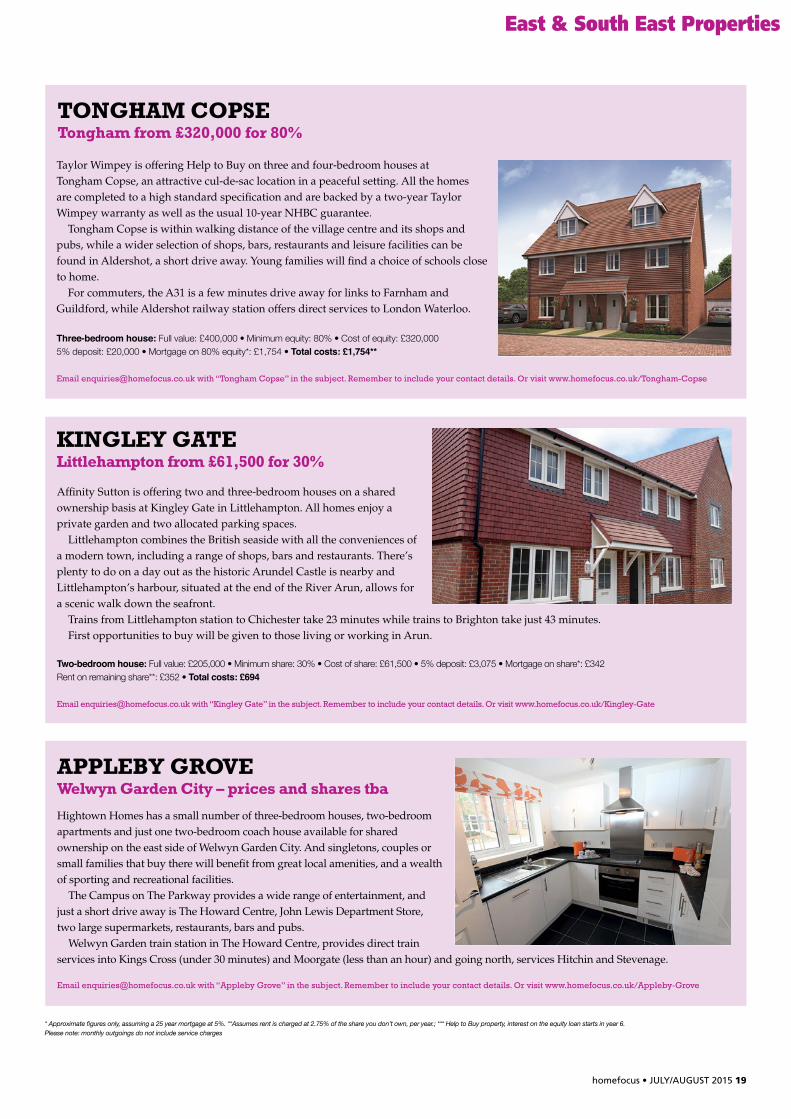

TONGHAM COPSE Tongham from £320,000 for 80%

* Approximate figures only, assuming a 25 year mortgage at 5%. **Assumes rent is charged at 2.75% of the share you don’t own, per year.; *** Help to Buy property, interest on the equity loan starts in year 6. Please note: monthly outgoings do not include service charges

KINGLEY GATELittlehampton from £61,500 for 30%

Taylor Wimpey is offering Help to Buy on three and four-bedroom houses at Tongham Copse, an attractive cul-de-sac location in a peaceful setting. All the homes are completed to a high standard specification and are backed by a two-year Taylor Wimpey warranty as well as the usual 10-year NHBC guarantee.

Tongham Copse is within walking distance of the village centre and its shops and pubs, while a wider selection of shops, bars, restaurants and leisure facilities can be found in Aldershot, a short drive away. Young families will find a choice of schools close to home.

For commuters, the A31 is a few minutes drive away for links to Farnham and Guildford, while Aldershot railway station offers direct services to London Waterloo.

Three-bedroom house: Full value: £400,000 • Minimum equity: 80% • Cost of equity: £320,000 5% deposit: £20,000 • Mortgage on 80% equity*: £1,754 • Total costs: £1,754**

Email [email protected] with “Tongham Copse” in the subject. Remember to include your contact details. Or visit www.homefocus.co.uk/Tongham-Copse

Affinity Sutton is offering two and three-bedroom houses on a shared ownership basis at Kingley Gate in Littlehampton. All homes enjoy a private garden and two allocated parking spaces.

Littlehampton combines the British seaside with all the conveniences of a modern town, including a range of shops, bars and restaurants. There’s plenty to do on a day out as the historic Arundel Castle is nearby and Littlehampton’s harbour, situated at the end of the River Arun, allows for a scenic walk down the seafront.

Trains from Littlehampton station to Chichester take 23 minutes while trains to Brighton take just 43 minutes. First opportunities to buy will be given to those living or working in Arun.

Two-bedroom house: Full value: £205,000 • Minimum share: 30% • Cost of share: £61,500 • 5% deposit: £3,075 • Mortgage on share*: £342Rent on remaining share**: £352 • Total costs: £694

Email [email protected] with “Kingley Gate” in the subject. Remember to include your contact details. Or visit www.homefocus.co.uk/Kingley-Gate

APPLEBY GROVEWelwyn Garden City – prices and shares tba

Hightown Homes has a small number of three-bedroom houses, two-bedroom apartments and just one two-bedroom coach house available for shared ownership on the east side of Welwyn Garden City. And singletons, couples or small families that buy there will benefit from great local amenities, and a wealth of sporting and recreational facilities.

The Campus on The Parkway provides a wide range of entertainment, and just a short drive away is The Howard Centre, John Lewis Department Store, two large supermarkets, restaurants, bars and pubs.

Welwyn Garden train station in The Howard Centre, provides direct train services into Kings Cross (under 30 minutes) and Moorgate (less than an hour) and going north, services Hitchin and Stevenage.

Email [email protected] with “Appleby Grove” in the subject. Remember to include your contact details. Or visit www.homefocus.co.uk/Appleby-Grove

20 homefocus • JULY/AUGUST 2015

South

Lovell is making Help to Buy available at Repton Grange in Brentry, north Bristol, in a range of homes suitable for singletons, couples, families and downsizers. Right now, just three-bedroom houses are on offer but before too long there will also be two and four-bedroom houses and a coach house.

The three-bedroom town houses provide a car port and parking. On the ground floor is a sleek kitchen/breakfast

area with French doors to the garden, dining room, hall and cloakroom. Moving to the first floor, you’ll find the spacious living room, family bathroom and bedroom three, while on the top floor is the master bedroom with en-suite and fitted wardrobe and the second bedroom.

Repton Grange is within easy reach of

central Bristol, as well as being close to the M5 –right by the Cribbs Causeway retail park. The area has plenty of green space and outdoor attractions and is just two miles from the historic village of Westbury-on-Trym.

Starting to think that you can buy your own home? Could buying in the South be more cost effective than renting or commuting? Then take a look at this selection of low cost home ownership (LCHO) homes. There are more listed on pages 59 and helpful contacts on our South homefinder, page 65. Or visit www.homefocus.co.uk/Low-cost-homes-near-you.

REPTON GRANGEBrentry from £258,400 for 80%

Want to know more? Then email [email protected] with the name of the development that interests you in the subject line and don’t

forget to include your contact details. Or you can visit www.homefocus.co.uk.

Three-bedroom house: Full value: £323,000 • Minimum equity: 80% • Cost of equity: £258,400 5% deposit: £16,150 • Mortgage on 80% equity*: £1,416 • Total costs: £1,416***

* Approximate figures only, assuming a 25 year mortgage at 5%. **Assumes rent is charged at 2.75% of the share you don’t own, per year.; *** Help to Buy property, interest on the equity loan starts in year 6. Please note: monthly outgoings do not include service charges

www.homefocus.co.uk/Repton-Grange

homefocus • JULY/AUGUST 2015 21homefocus • JULY/AUGUST 2015 11

South Properties

OAK COURT Bristol from £415,996 for 80%

LIMES PARK Basingstoke from £126,000 for 80%

The last family, five-bedroom ‘Stratford’ style remains at Barratt’s Oak Court development in Bishop Sutton near Bristol. Suited to those moving up the ladder, Oak Court is available with Help to Buy.

The ground floor includes a spacious lounge and a light and airy kitchen - with family area. Upstairs is a master bedroom with dressing area and en suite, two further bedrooms and an attractive bathroom.

On the second floor are two additional bedrooms and a shower room. The home also features a double garage and two parking spaces.

Bishop Sutton is, a small village within the Chew Valley. The development offers easy access to local amenities.

Five-bedroom house: Full value: 519,995 • Minimum equity: 80% • Cost of equity: £415,996 • 5% deposit: £26,000 • Mortgage on 80% equity*: £2,888 Total costs: £2,888***

Interested? Call 0845 4744734 or email [email protected] with “Oak Court” in the subject. Remember to include your contact details.

Or visit www.homefocus.co.uk/Oak-Court

Taylor Wimpey has one and two-bedroom apartments on offer at The Sycamores at Limes Park in Basingstoke.

A two-bedroom apartment, for example, features an open-plan kitchen/living/dining room, an en-suite master bedroom, a second double bedroom, a main bathroom and handy storage cupboards located off the entrance hallway. The property also benefits from allocated parking and access to a communal garden outside.

Limes Park is located off Park Prewett Road and the development forms part of the wider Park Village on the north-western fringes of Basingstoke, with the town centre just two miles away.

Open countryside is just a stone’s throw away, offering nature trails and opportunities for woodland walks and cycling.

One-bedroom apartment: Full value: £157,500 • Minimum equity: 80% • Cost of equity: £126,000 • 5% deposit: £7,875 • Mortgage on 80% equity*: £875 • Total costs: £875***

Interested? Call 0845 4744734 or email [email protected] with “Limes Park” in the subject. Remember to include your contact details.

Or visit www.homefocus.co.uk/Limes-Park

* Approximate figures only, assuming a 25 year mortgage at 5%. **Assumes rent is charged at 2.75% of the share you don’t own, per year.; *** Help to Buy property, interest on the equity loan starts in year 6. Please note: monthly outgoings do not include service charges

THE CEDARS Reading prices to be confirmed from 35%Southern Home Ownership is offering shared ownership at their new development, The Cedars, in Reading. The 14 one and two-bedroom apartments, and the 3 three-bedroom houses all have a bright, modern, high spec finishes.

The Cedars is sited in a leafy, green suburb of Reading, off Tilehurst Road, with easy access to Reading town centre, and the good news for commuters is that Reading’s main railway station will get you to London Paddington in less than half an hour. Being just off of the M4, there’s also great road links to London and the South West. And a half hourly coach service will get you to Heathrow Airport in around 40 minutes.

All Saints Junior School is just three minutes from The Cedars and Prospect Park is close by.

Interested? Email [email protected] with “The Cedars” in the subject. Remember to include your contact details.

Or visit www.homefocus.co.uk/The-Cedars

For 25 year old nurse Katie Glover, Affinity Sutton’s shared ownership

scheme at Graylingwell Park has done more than help her get on the property ladder, it’s also relieved her of a long commute to work and given her independence.

She says, ‘I was living with my parents in Southampton to save up for a deposit and the commute took up so much time and wasted lots of money. From Graylingwell Park it only takes me about 10 minutes to

walk to work, so I have more time to myself.’Katie, who works at St Richard’s Hospital

in Chichester is now able to be with her friends and work colleagues, rather than spend time on the train. ‘Most of my friends are local so it’s a lot easier now for me to meet up with them after work,’ she says

Katie purchased a 30% share in her one-bedroom apartment at Graylingwell Park for £46,650 (full market value £155,500), putting down a £7,000 deposit. She pays

£200 a month in mortgage payments and a further £360 to Affinity in rent. It’s less than the average for renting a one-bedroom apartment in the area.

‘I saw the apartment and thought it was perfect,’ says Katie. ‘I knew I wouldn’t be able to afford anything else like it. Thanks to shared ownership I was able to move out of my parents’ home a lot quicker than I had planned and I’ve got my independence at last!’

Will this story inspire you to become a homeowner? See the list of low cost home ownership (LCHO) properties on pages 56-59. Or go to www.homefocus.co.uk/Low-cost-homes-near-you. Or email [email protected]

‘I’ve got my independence at last!’

Katie Glover

Previous situation: Living with parents

Scheme: Shared Ownership

Location: Graylingwell Park

Provider: Affinity Sutton

Help to Buy Agent: Helptobuysouth.co.uk

22 homefocus • JULY/AUGUST 2015

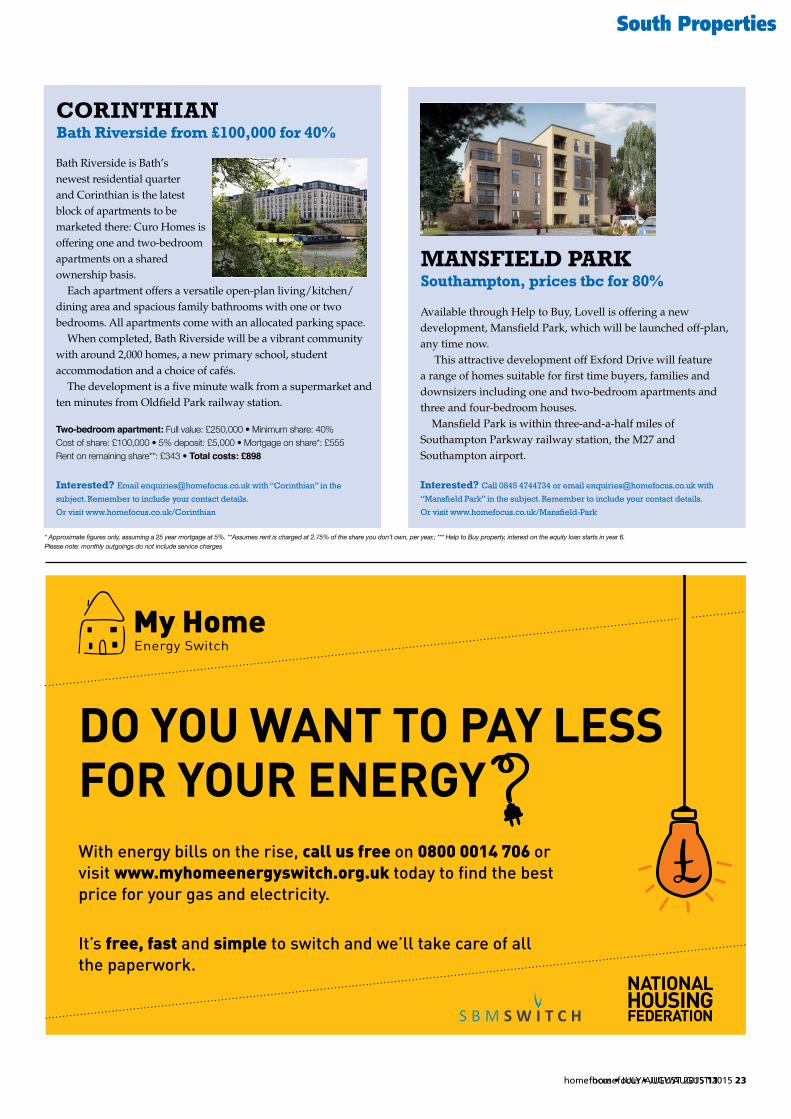

MANSFIELD PARKSouthampton, prices tbc for 80%

CORINTHIANBath Riverside from £100,000 for 40%

Available through Help to Buy, Lovell is offering a new development, Mansfield Park, which will be launched off-plan, any time now.

This attractive development off Exford Drive will feature a range of homes suitable for first time buyers, families and downsizers including one and two-bedroom apartments and three and four-bedroom houses.

Mansfield Park is within three-and-a-half miles of Southampton Parkway railway station, the M27 and Southampton airport.

Interested? Call 0845 4744734 or email [email protected] with

“Mansfield Park” in the subject. Remember to include your contact details.

Or visit www.homefocus.co.uk/Mansfield-Park

Bath Riverside is Bath’s newest residential quarter and Corinthian is the latest block of apartments to be marketed there: Curo Homes is offering one and two-bedroom apartments on a shared ownership basis.

Each apartment offers a versatile open-plan living/kitchen/dining area and spacious family bathrooms with one or two bedrooms. All apartments come with an allocated parking space.

When completed, Bath Riverside will be a vibrant community with around 2,000 homes, a new primary school, student accommodation and a choice of cafés.

The development is a five minute walk from a supermarket and ten minutes from Oldfield Park railway station.

Two-bedroom apartment: Full value: £250,000 • Minimum share: 40%Cost of share: £100,000 • 5% deposit: £5,000 • Mortgage on share*: £555Rent on remaining share**: £343 • Total costs: £898

Interested? Email [email protected] with “Corinthian” in the

subject. Remember to include your contact details.

Or visit www.homefocus.co.uk/Corinthian

* Approximate figures only, assuming a 25 year mortgage at 5%. **Assumes rent is charged at 2.75% of the share you don’t own, per year.; *** Help to Buy property, interest on the equity loan starts in year 6. Please note: monthly outgoings do not include service charges

South Properties

With energy bills on the rise, call us free on 0800 0014 706 or visit www.myhomeenergyswitch.org.uk today to find the best price for your gas and electricity.

It’s free, fast and simple to switch and we’ll take care of all the paperwork.

DO YOU WANT TO PAY LESS FOR YOUR ENERGY

homefocus • JULY/AUGUST 2015 23homefocus • JULY/AUGUST 2015 11

Midlands

Lovell is offering Help to Buy in the second and final phase of their Caldon Quay development, a waterside setting with high-quality homes.

A number of two-bedroom apartments are available in Beech House in the very heart of the development, plus just one ground floor canalside apartment, overlooking the water and with its own private entrance on offer.

All apartments have their own dedicated

parking space and master bedroom with en-suite facilities and a contemporary kitchen including an integrated fridge-freezer, brushed steel chimney hood and Bosch hob and double oven.

Located off Ridgeway Road, Caldon Quay is perfectly placed for the entertainment and excitement of the city

centre, while the soothing waterfront setting is ideal for unwinding when you need a rest from the bright lights

For train travellers, Stoke-on-Trent railway station is only a mile from the development.

Starting to think that you can buy your own home? Could buying in the Midlands be more cost effective than renting or commuting? Then take a look at this selection of low cost home ownership (LCHO) homes. There are more listed on pages 58 and Midlands homefinder on pages 64. Or visit www.homefocus.co.uk/Low-cost-homes-near-you.

CALDON QUAYStoke-on Trent from £83,960 for 80%

Want to know more? Then email [email protected] with the name of the development that interests you in the subject line and don’t

forget to include your contact details. Or you can visit www.homefocus.co.uk.

One-bedroom apartment: Full value: £104,950 • Minimum equity: 80% • Cost of equity £83,960 5% deposit: £5,248Mortgage on 80% equity*: £460 • Total costs: £460***

* Approximate figures only, assuming a 25 year mortgage at 5%. **Assumes rent is charged at 2.75% of the share you don’t own, per year.; *** Help to Buy property, interest on the equity loan starts in year 6. Please note: monthly outgoings do not include service charges

www.homefocus.co.uk/Caldon Quay

24 homefocus • JULY/AUGUST 2015

Midlands Properties

EDEN VALLEY Walsall from £99,960 for 80%

BELGRAVE RIVERSIDELeicester from 80% prices tbc

Situated just over a mile from Walsall’s centre is the Eden Valley development where Lovell is offering Help to Buy on two-bedroom homes.

The two-bedroom Keinton mid-terraced style house has two parking spaces, and features a kitchen with Bosch oven and hob, cloakroom and a spacious living/dining room with French doors to the garden.

Featured (and a little more expensive) is the ‘Gayton’ end terrace home with a surprising amount of space and driveway parking for two vehicles. This home offers

Westleigh is offering Help to Buy on the third phase of their new homes at Belgrave Riverside at Ross Walk in Leicester.

The development has transformed the former British Union Shoe Machinery head office into a desirable residential development, close to the city centre and Wesleigh is providing a mix of two, three and four-bedroom properties in two and three storey styles forming terraced town house street scenes.

THE LEYSWellingborough from £39,750 for 30%

Metropolitan is offering attractive two and three-bedroom family houses in Wellingborough, available through shared ownership.

All of the light and airy homes feature fitted kitchens, incorporating integrated Bosch and Smeg appliances and oak worktops. The fully fitted bathroom has a heated towel rail and each home comes with a downstairs w.c, carpet and tiles throughout. The living/diner leads into a rear garden and outside, is allocated parking (two spaces for the three-bedroom homes).

* Approximate figures only, assuming a 25 year mortgage at 5%. **Assumes rent is charged at 2.75% of the share you don’t own, per year.; *** Help to Buy property, interest on the equity loan starts in year 6. Please note: monthly outgoings do not include service charges

Rail links from Wellingborough will get you to into London St. Pancras (47 minutes), Nottingham (65 minutes), Corby (20 minutes) and Leicester (30 minutes).

Two-bedroom house: Full value: £132,500Minimum share: 30% • Cost of share: £39,7505% deposit: £1,898 • Mortgage on share*: £221Rent on remaining share**: £213 • Total costs: £434

Interested? Email [email protected]

with “The Leys” in the subject. Remember to include

your contact details.

Or visit www.homefocus.co.uk/The-Leys

a generous living room with French doors to the garden and attractive kitchen/dining room with kitchen appliances including a Bosch hob and oven.

Eden Valley has an established community with plenty to offer locally and excellent transport links connecting you to the motorway network and the rest of the West Midlands.

Two-bedroom house: Full value: £124,950Minimum equity: 80% • Cost of equity: £99,9605% deposit: £6,248 Mortgage on 80% equity*: £548 Total costs: £548***

Interested? Email [email protected] with

“Eden Valley” in the subject. Remember to include your

contact details.

Or visit www.homefocus.co.uk/Eden Valley

Parking courts have been created at the rear of homes to minimise their influence on the street scene and also to maximise privacy and security for vehicle owners.

The development is located off the A607 Belgrave Road, within a short walk of the Golden Mile and within easy reach of local amenities, Abbey Park and Leicester city centre.

Interested? Email [email protected]

with “Belgrave Riverside” in the subject. Remember

to include your contact details. Or visit www.

homefocus.co.uk/Belgrave-Riverside

homefocus • JULY/AUGUST 2015 25

With the cost of house prices in the capital rising so quickly, thousands

of young professionals have left London in search of a more affordable life. Ayo Bakare, 24, bought a brand new three-bedroom Barratt home at the Kings Rise development in Kings Norton.

Ayo, an Investment Consultant, moved from London Capital to the Midlands

due to work and says that without using the Help to Buy scheme, he wouldn’t have been able to afford a brand new home, ‘I have saved a lot of money by buying a home in Birmingham rather than in London. The Help to Buy scheme has proved to be a blessing as without it, I don’t think I would have my own house.’

Ayo continued; ‘Having lived with my

parents, it’s great to have all this space and independence. I am used to the hustle and bustle of city life and you still get that in Birmingham, but the great thing is that the countryside is never too far away which is very different from what I am used to.’

Kings Rise offers a range of three and four bedroom houses priced from £199,950 (that’s £159,960 with Help to Buy).

Will this story inspire you to become a homeowner? See the list of low cost home ownership (LCHO) properties on page 56-59. Or go to www.homefocus.co.uk/Low-cost-homes-near-you. Or email [email protected]

Ayo Bakare

Previous situation: Living with Parents

Scheme: Help to Buy

Location: Birmingham

Provider: Barratt Homes

Help to Buy Agent: www.helptobuymidlands.co.uk‘Without Help to Buy, I don’t think I would have my own house’

26 homefocus • JULY/AUGUST 2015

Midlands Properties

Help to Buy isn’t just for first time-buyers and Rippon Homes are offering this more affordable option on a range of three and four-bedroom homes at their development at Deerlands Road in Wingerworth.

Featured is the ‘Westminster style four-bedroom family home comprising a sitting room with feature bay window, a separate dining/family room and a large breakfast kitchen with French doors opening onto the south facing, private garden.

Upstairs, two of the bedrooms include fitted wardrobes, the master bedroom has an en-suite and there is also a separate family bathroom. Outside is a garage with driveway and parking space for three cars.

Three-bedroom house: Full value: £259,950 • Minimum equity: 80%Cost of equity 207,960 • 5% deposit: £12,998Mortgage on 80% equity*: £731 • Total costs: £731***

Interested? Email [email protected] with “Kings Meadow” in the subject. Remember to include your contact details. Or visit www.homefocus.co.uk/Kings-Meadow

KINGS MEADOW Wingerworth from £207,960 for 80%

GOODWIN PARK Kidderminster from £119,960 for 80%

Barratt Homes’ new development on Stoney Lane, Kidderminster features a range of three bedroom homes available with Help to Buy.

Ilustrated is the The Barwick style semi-detached family home. The ground floor comprises a lounge and dining area, with French doors leading to the rear garden, a fully fitted kitchen with family breakfast area, plenty of storage space and a useful cloakroom. Upstairs is a master bedroom with en suite, two further bedrooms and a family bathroom.

Three-bedroom house: Full value: £149,950 • Minimum equity: 80%Cost of equity 119,960 • 5% deposit: £7,498 • Mortgage on 80% equity*: £657Total costs: £657***

Interested? Email [email protected] with “Goodwin Park” in the subject. Remember to include your contact details. Or visit www.homefocus.co.uk/Goodwin-Park

To find out more call:

0845 600 3674 or email: [email protected] www.orbithomes.org.uk

Terms and conditions. Percentage shares offered vary by development and are subject to personal financial circumstances. Following a full financial review applicants will be offered the maximum share they can afford.

Full details are available from Orbit Homes.

With Help to Buy Shared Ownership you purchase a share in a brand new home and pay a subsidised rent on the part you don’t own.

Orbit Homes has developments of new homes right across the South East, Midlands, and East of England.

So whether you’re looking for a one bedroom apartment, a two bedroom house or a three bedroom family home we’re here to help you get your feet on the property ladder.

Do you need help to buy a new home?

* Approximate figures only, assuming a 25 year mortgage at 5%. *** Help to Buy property, interest on the equity loan starts in year 6. Please note: monthly outgoings do not include service charges

* Approximate figures only, assuming a 25 year mortgage at 5%. **Assumes rent is charged at 2.75% of the share you don’t own, per year.; *** Help to Buy property, interest on the equity loan starts in year 6

Taylor Wimpey is offering Help to Buy on a selection of houses, in Newton Abbott.

Illustrated is the three-bedroom semi-detached ‘Flatford’ style home with living/dining room opening through French doors to the private rear garden, plus a spacious kitchen/breakfast room and a guest cloakroom located off the entrance hallway.

Upstairs, the landing leads to an en-suite master bedroom, plus two further

bedrooms and a family bathroom, while outside, the property benefits from driveway parking for two cars.