growth trends in global agricultural output changing...

TRANSCRIPT

1

Changing Global Food Markets: The Role of Value Chains & Supply Chains

World Bank ESSD Workshop on Standards and Trade – April 6, 2005“Part 1: Small Scale Producers in Changing Food Markets”

Except otherwise noted, copyrighted April, 2005

by Abt Associates, Inc.

All Rights Reserved

Developed by John Lamb; presented by John

Holtzman, Abt Associates Inc.

April 6, 2004

Growth trends in global agricultural output

• Annual rate of growth in global ag sector GDP slowed in last decade (up just 1.8% between 1990 and 2002 vs. 2.6% in Eighties)

• Output slowed for all country-income groups in the latter Nineties, only to pick up the year after 9/11 as the 2002 globalrecession passed

• In most LDCs, agriculture still contributes at least 15% of GDP,sometimes much more (e.g. Benin 36%, Nicaragua 29%, Vietnam 22%), yet …

• Historical growth rates are much lower than the 4-6% needed to cover population growth & serve as the main driver of rural prosperity

April 6, 2004

Trends in value of agricultural exports

• After contraction in the late Nineties, global food and agricultural trade has been expanding faster than population since 2001 (up 6% in 2002, then 15% in 2003), reaching $674 billion in 2003

• All regions did well in 2003 ag exports (latest year reported): Western Europe up 19%; Asia up 12%; North America up 9%; Latin America up 15%; CEE/Baltic/CIS States up 26%; Africa up 16%

• Some countries are highly dependent on ag exports (e.g. in 2003, Paraguay 82%, Nicaragua 77%, Belize 74%, Ethiopia 72%), but the share of agriculture in exports tends to fall as development proceeds

April 6, 2004

Population growth in developing countries remains a key driver of food and agricultural trade

Source: Neil Conklin, Economic Research Service, 2004

2

April 6, 2004

Urbanization will also drive greater diversification in food consumption & expanded trade

Source: FAO, State of Agricultural Commodity Markets, 2004

April 6, 2004

Other characteristics of future developing country markets to keep in mind

Emerging middle class: higher value added to staple products; ↑ consumption of animal protein and vegetables (dietary diversification)

High-end segment will have same preferences as consumers in developed markets, e.g. convenience, variety, quality

Changing role of women in labor force & food preparation: ↑ demand for ready-to-cook food & meals away from home

Supermarkets’ share will increase

April 6, 2004

Diets diversify as incomes rise…

Source: Neil Conklin, Economic Research Service, 2004

April 6, 2004

The change has already begun: witness LDC agricultural trade balance since 1980

Source: FAO, State of Agricultural Commodity Markets, 2004

3

April 6, 2004

Trends in value of agricultural imports

• Some countries highly dependent on food and ag imports: e.g., Egypt at 29% of all merchandise imports; Madagascar and Syria at 20%

• Northern countries are tending to import a greater share of their needs in terms of value (in 2003: EU15

18%, USA 8%, Japan 6%, China 40%)

• At $308 B (billion) in 2003, EU is largest importer, US second at $77B, Japan third at $58 B, China moving up fast (probably to 2nd place by 2015)

April 6, 2004

Trends in composition of agricultural trade

• Composition of trade is changing, with greater share to:

– higher value products (80% food products vs. 20% agric. raw materials)

– consumer-oriented items with good value-added (within food)

• Changes due to better post-harvest & transport technology, improved equipment, and practices that enable shipment much greater distances & more quickly

• Seasonal windows are closing in most major markets, especially in Northern countries, but opportunities still remain in South and for regional trade

April 6, 2004

Seasonal windows on which the NTAE boom was built are closing

• Fresh produce whose windows have closed in the U.S.

– Apples

– Melons

– Lettuce

– Greens

– Asparagus

– Onions

– Oranges

– Carrots

– Potatoes

– Cucumbers

• Fresh produce with seasonal gaps or shortages in the U.S.

– Blueberries

– Cherries

– Stonefruit

– Red raspberries

– Tangerines

– Lychees

– Rambutan

– Mangosteen

– Apricots

April 6, 2004

Note that real prices for agricultural commodities continue to fall over time…

Source: FAO, State of Agricultural Commodity Markets, 2004

4

April 6, 2004

Differentiated products are progressively displacing commodities

• Advantages:

– Suppliers obtain higher prices & bigger margins

– Reduced price volatility

– Increased leverage of suppliers in the value chain

– Often displace commodity supplies when they appear on the market

• Disadvantages

– Costly to establish & maintain differentiation

– Sometimes encounter value chain resistance (from buyer/distributor side)

– High failure rates

April 6, 2004

Examples: Differentiation by product attributes or brand

April 6, 2004

Examples: Differentiation by type or appellation

April 6, 2004

Examples: Differentiation by process and certification

Certified Biodynamic

5

April 6, 2004

This partly explains why U.S. 2-way trade in high value products is increasing dramatically

Source: Neil Conklin, Economic Research Service, 2004

April 6, 2004

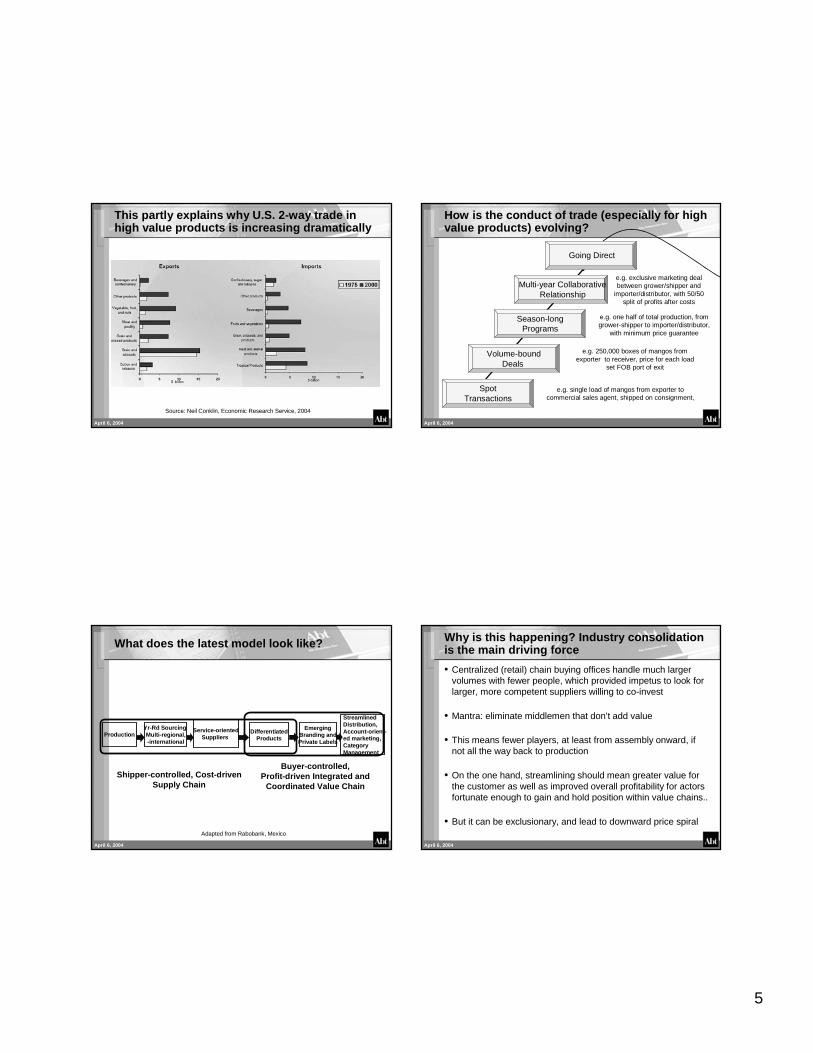

How is the conduct of trade (especially for high value products) evolving?

Spot Transactions

Volume-bound Deals

Season-long Programs

Multi-year Collaborative Relationship

e.g. single load of mangos from exporter to commercial sales agent, shipped on consignment,

e.g. 250,000 boxes of mangos from exporter to receiver, price for each load

set FOB port of exit

e.g. one half of total production, from grower-shipper to importer/distributor,

with minimum price guarantee

e.g. exclusive marketing deal between grower/shipper and

importer/distributor, with 50/50 split of profits after costs

Going Direct

April 6, 2004

ProductionYr-Rd Sourcing Multi-regional,-international

Service-orientedSuppliers

DifferentiatedProducts

Streamlined Distribution,Account-orient-ed marketing, Category Management

ShipperShipper--controlled, Costcontrolled, Cost--driven driven Supply ChainSupply Chain

BuyerBuyer--controlled,controlled,ProfitProfit--driven Integrated and driven Integrated and

Coordinated Value ChainCoordinated Value Chain

EmergingBranding andPrivate Labels

Adapted from Rabobank, Mexico

What does the latest model look like?

April 6, 2004

Why is this happening? Industry consolidation is the main driving force

• Centralized (retail) chain buying offices handle much larger volumes with fewer people, which provided impetus to look for larger, more competent suppliers willing to co-invest

• Mantra: eliminate middlemen that don’t add value

• This means fewer players, at least from assembly onward, if not all the way back to production

• On the one hand, streamlining should mean greater value for the customer as well as improved overall profitability for actors fortunate enough to gain and hold position within value chains..

• But it can be exclusionary, and lead to downward price spiral

6

April 6, 2004

How is this new and different?

1. Longer-term vision

2. More stable relationship between two companies, not based so much on personal relationships

3. Joint responsibility and accountability

4. Bottom line is profitability and growth of the category as a whole—year-end for category, not weekend results for a particular brand

5. Fewer players control more of the volume

6. Heavy emphasis on enterprise-wide IT

7. Shared staff, dedicated facilitiesApril 6, 2004

“Value chain” is not the same as “supply chain”

• Value chains:

– medium-to-long term: what will the market pay for a good offered for sale? (maximize profit)

– short-to-medium term: expand market share

• The main objectives of value chain management: maximize gross revenue & sustain it over time

• However, you can’t have a successful value chain without an efficient and reliable supply chain

April 6, 2004

What are some of the emerging “value chains”?

Consumer packs of specialty vegetables from Guatemala and Peru for the Southeast US chain stores

Freshcut fruit from Ghana and Costa Rica

Chilled Nile perch fillets from Uganda and Kenya for UK multiples

April 6, 2004

What is an agricultural supply chain?

Entire set of processes and activities required to produce a product then deliver it to a target market, i.e. to go from “farm to fork”

• “to produce” encompasses growing, transforming, or manufacturing

• Focus of supply chains: what does product cost and how long does it take to present product for sale

• The main objectives of supply chain management:

a) minimize costs by reducing the number of links & friction in the chain (bottlenecks, red tape, transaction costs, time to market)

b) improve reliability, speed & quality of goods delivered

7

April 6, 2004

What are some typical “supply chains”?

Cut flowers from Quito by air through Miami to the Eastern U.S. importer/distributors for retail sale in flower shops

CFA Franc Zone cotton lint overland to ports in Ghana, Senegal and Ivory Coast, then by sea to traders in Marseilles and Far East, for final delivery to spinners

Egyptian strawberries by sea from Alexandria to Trieste, then overland to receiver/distributors in Germany

April 6, 2004

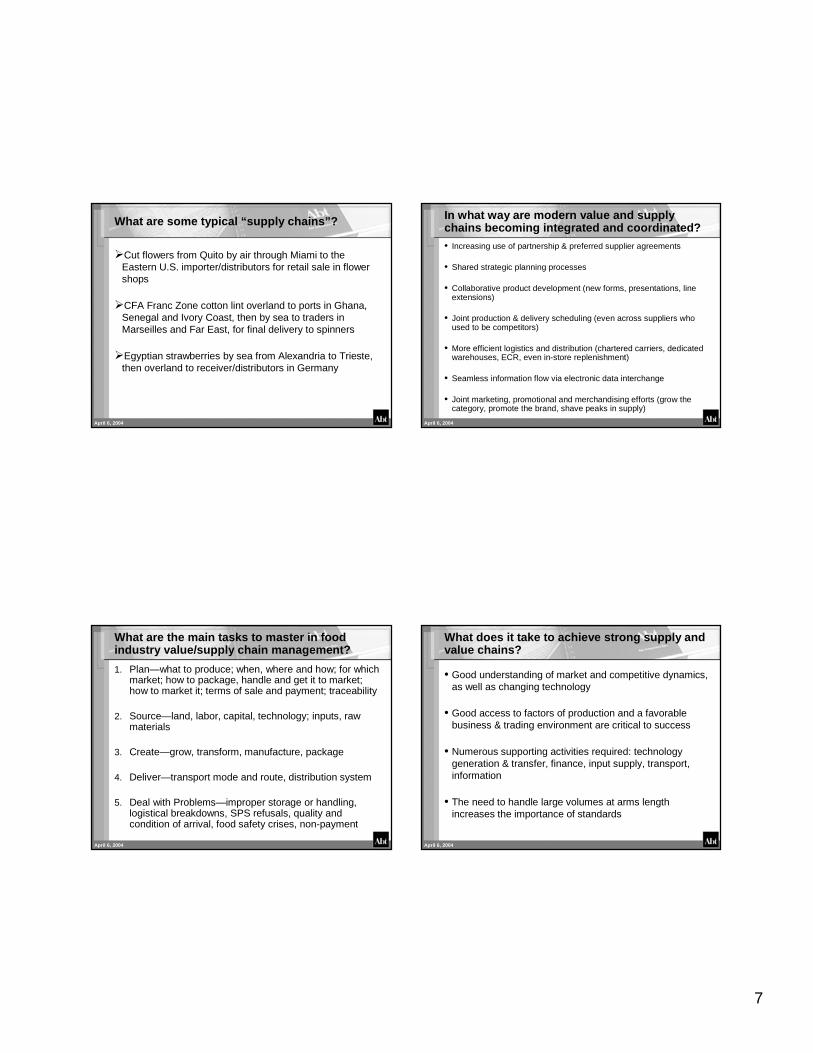

In what way are modern value and supply chains becoming integrated and coordinated?• Increasing use of partnership & preferred supplier agreements

• Shared strategic planning processes

• Collaborative product development (new forms, presentations, line extensions)

• Joint production & delivery scheduling (even across suppliers who used to be competitors)

• More efficient logistics and distribution (chartered carriers, dedicated warehouses, ECR, even in-store replenishment)

• Seamless information flow via electronic data interchange

• Joint marketing, promotional and merchandising efforts (grow thecategory, promote the brand, shave peaks in supply)

April 6, 2004

What are the main tasks to master in food industry value/supply chain management?

1. Plan—what to produce; when, where and how; for which market; how to package, handle and get it to market; how to market it; terms of sale and payment; traceability

2. Source—land, labor, capital, technology; inputs, raw materials

3. Create—grow, transform, manufacture, package

4. Deliver—transport mode and route, distribution system

5. Deal with Problems—improper storage or handling, logistical breakdowns, SPS refusals, quality and condition of arrival, food safety crises, non-payment

April 6, 2004

What does it take to achieve strong supply and value chains?

• Good understanding of market and competitive dynamics, as well as changing technology

• Good access to factors of production and a favorable business & trading environment are critical to success

• Numerous supporting activities required: technology generation & transfer, finance, input supply, transport, information

• The need to handle large volumes at arms length increases the importance of standards

8

April 6, 2004

There are three main kinds of standard

• Product standards: e.g. type, variety, size count, PLU stickers, color, maturity, sugar level, cosmetic appearance, organoleptic attributes, type of box, markings, etc

• Process standards: e.g. pesticide use, GAP, GMP, HACCP, labor conditions, certifications, traceability, etc

• Logistical standards: e.g. palletization, markings, barcoding, RFID, loading patterns, delivery time/place, crossdocking, recovery of pallets, rhythm of deliveries, etc

April 6, 2004

Sanitary and Phytosanitary Standards

Quality and Condition Standards

Environmental

Standards

Social

Standards

Service

Standards

There is also en evolving hierarchy of topical areas to which standards are applied

Let’s briefly examine each layer…

April 6, 2004

Official grades and standards for quality & condition still exist but private specs are increasingly dominant

April 6, 2004

Getting the right quality remains crucial

To achieve this kind of quality, small farmers will need to change how they grade, select, pack, handle, and ship

9

April 6, 2004

There is increasing concern for food safety

10 Least Wanted FoodbornePathogens

Campylobacter

Clostridium botulinum

E. coli 0157:H7

Listeria monocytogenes

Norovirus

Salmonella

Staphyloccus aureus

Shigella

Toxoplasma gondii

Vibrio vulnificus

April 6, 2004

So firm, industry, and even country management of food safety is a competitive necessity

April 6, 2004

Major buyers are requiring food safety and hygiene plans, audits, and certification

April 6, 2004

This has stimulated emergence of third-party suppliers of consulting and auditing services…

10

April 6, 2004

…as well as more reliance on privately managed, independent certification

April 6, 2004

Traceability is becoming especially important for food safety (and for possible bioterrorism)

April 6, 2004

Environmental standards and green certification are gaining momentum as well

Conservation Beef

April 6, 2004

Caution: small may be beautiful but it is not necessarily “green,” as this story reports…

“Poor use of pesticides leaves more than 200 dead each year”El Salvador has, within Centroamérica, the highest level of acute pesticide intoxication each year, caused by exposure to chemical compounds. Just in the first half of 2003, 132 deaths for this reason were recorded

published 22 January 2004, El Diario de Hoy

11

April 6, 2004

Social codes of conduct have been emerging, both from within chains and from outside

April 6, 2004

At the top of the hierarchy, service standards are the new battleground in global food trade

Slotting Allowances

Special Packs

Private Label Products

Promotional Support

Merchandising Support

Volume/Non-Volume Rebates

Capital Improvements

Timely, Consistent Delivery

Setting up Electronic Data Interchange or Merging Systems

Stock Replenishment by Supplier (Warehouse, Store)

Use of Returnable Containers

Prompt Problem Resolution

Trace-back Systems

April 6, 2004

Unfortunately, the market rarely pays for the higher standards, so less of the food dollar is going to the farmer

April 6, 2004

Implications: Need for quality, safety and volume means more contract farming

•Driven by desire for specific attributes: method of production; nutritional composition; variety; seasonality; size/count; maturity; presentation

•Buyers—processors, elevators & retailers—use production contracts to control input choices & production methods

•Farmers benefit: contracts can reduce income risks, ease credit requirements & guarantee higher prices for specific product attributes

•Among U.S. farms with at least $500,000 in annual sales, 61 percent used contracts for at least some of their production in 2001, compared with only 8 percent of farms with sales under $250,000.

•The use of contracts can spread rapidly through an industry. By 2001, contracts covered 54 % of cotton and 39 % of rice production, compared with 30 % and 20 %, respectively, in 1991.

12

April 6, 2004

Implications: Direct sourcing and direct selling are both increasing, to eliminate middlemen

Supermarkets DrivingKenya Flower Industry

April 6, 2004

Implications: Once you’ve found a winning product, work it through line extensions

April 6, 2004Index

Honeydew Watermelon Cantaloupe Galia Melon

CharentaisSeedless Watermelon

IQF Melon Balls

Implications: Once you’ve found a winning category, work it as well, by diversifying

Gift melons

April 6, 2004

Implications: Use technology to add value by extending transit and shelf life

Modified atmosphere packaging

13

April 6, 2004

Implications: Improve packaging to add value for both buyers and customers

April 6, 2004

Implications: Keep looking for the next cape gooseberry but…

…since that process is expensive, risky and time-

consuming…

Vietnam: “Dragonfruit”

Nicaragua: “Pitahaya”

April 6, 2004

Implications: …Meanwhile work on new value-adding product forms and presentations

April 6, 2004

Implications: Small farmers in developing countries need to get organized and connected

• They often lack risk capital, facilities, presence, marketing know-how and know-who, language

• They can often supply a limited number of products or varieties, over a limited timeframe

• They may not be able to police themselves to control quality, ensure food safety, deal with other standards

14

April 6, 2004

…because they have some significant weaknesses with respect to these changes.– Shortage of capital and lack of

collateral with which to borrow

– Lack of access to technology

– Difficult access to good land

– Environmental degradation, especially soils and water

– High pest/disease pressure in tropical and subtropical areas

– Inputs often not available, or late

– Power usually expensive

– Time, distance and cost to market

– Transport infrastructure and services often inadequate

– Small scale of farm units, difficulty delivering volumes needed

– Inability to speak English

– Lack of know-how and know-who for export markets

– Policy and enabling environment

– HIV/AIDS scourge

April 6, 2004

On the other hand, they do have some strengthsas well…

Vocation for agriculture

Low wage rates, and after training, low cost of labor

Good growing conditions for some crops

Extended growing season in tropical and subtropical areas

In some cases, low cost of production

Lack of options often means strong motivation

In many places, a tradition of working together (e.g. “minga” in Ecuador and Peru)

Nearness to growth market of the future for food products, which is developing countries in general, and urban markets in developing countries in particular

April 6, 2004

So small farmers can participate in supply chains, as long as they get help in:

Better understanding of markets and marketing

Identifying value chains worth developing

Streamlining the corresponding supply chains

Selecting and dealing with export catalysts & channel captains

Complying with official & commercial standards of all kinds

Generating the required volumes

Assimilating enabling technologies

Retaining & adding value once they have penetrated a market