gold market

TRANSCRIPT

A REPORTON

GOLD MARKET

ByManish Madhogaria

Lohia Securities Pvt Ltd

A REPORTON

GOLD MARKET

ByManish Madhogaria

Lohia Securities Pvt Ltd

Date of submission-

AUTHORISATION

I have been authorized to undertake the project ldquoGold Market rsquorsquo as my SIP Project for Lohia Securities Pvt Ltd I have been assigned to do this project under Mr Jitesh Agarwal President HRD

ACKNOWLEDGEMENT

The present project is carried out in Lohia Securities Pvt Ltd located at Kolkata under the guidance of Icfai Business School Kolkata The project is not fully completed only half of the work has been done so far Now on the verge of writing this interim report I would like to thank a number of people from whom I have received generous support and who in different ways have contributed me in reaching so farFirst I would like to thank my company guide Mr Jitesh Agarwal of Lohia Securities Pvt Ltd and all the staff who have helped me Their support and comments have been of Inestimable value throughout whatever have been achieved in this projectI would also like to thank the staff at IBS kolkata and especially my faculty guide Dr Sutapa Banerjee for helping amp guiding me and at the same time solving all my queries Furthermore I would also like to thank my dean sir mr RK Mandan and all the faculty members present in IBS lucknow for supporting and helping me in this MBA program I would also like to thank Mr Rajib Kejriwal CEO Eureka Commodities Pvt Ltd Mr Sumit Choudhry Arbitrager Sreepati Balaji PvtLtd for extending their support and providing me all the necessary information needed to prepare the Interim Report

Manish Madhogaria

TABLE OF CONTENTS

Authorization I Acknowledgement II Abstract III 1 Introduction 2 MainText

21 Why Invest in Gold22 Gold Market Exchanges23 Special Features of Gold Market24 Terms and Terminologies in this Market25 Why prefer MCX26 Factors affecting Gold prices27 Inflation Exchange rate with Dollar Sensex and Gold prices28 Recent trend in Gold Market in India

3 Conclusion 31 Recommendation 5 References

ABSTRACT

My project ldquoGold Market rsquorsquo gives emphasis on the trading strategies which are followed by different trading firms and brokers and also it gives emphasis on how different factors like inflation affects the price of gold This will include learning of the gold market in detail from net how the market started what was the need behind creating such markets who regulates this market what is the minimum requirement etc The methodology that I have adopted to conduct the research work is to visit different trading firms Internet search engines like google yahoo is used and will be used to carry out the research work The main idea behind this market research is to gain basic idea what strategies different trading firms and brokers use to gain maximum profit

1 INTRODUCTION

Gold is a very solid asset Buying physical gold does have advantages compared with other investments Investments in gold-backed financial products and paper gold should be left up to the professionals says Mark Robinson a bullion analyst based in Dubai

Gold is the oldest precious metal known to man Therefore it is a timely subject for several reasons It is the opinion of the more objective market experts that the traditional investment vehicles of stocks and bonds are in the areas of their all-time highs and may be due for a severe correction

To fully appreciate why 8000 years of experience say gold is forever we should review why the world reveres what Englands most famous economist John Maynard Keynes cynically called the barbarous relic

Why gold is good as gold is an intriguing question However we think that the more pragmatic ancient Egyptians were perhaps more accurate in observing that golds value was a function of its pleasing physical characteristics and its scarcity

Gold is primarily a monetary asset and partly a commodity More than two thirds of golds total accumulated holdings account as value

for investment with central bank reserves private players and high-carat Jewellery

Less than one third of golds total accumulated holdings is as a commodity for Jewellery in Western markets and usage in industry

The Gold market is highly liquid and gold held by central banks other major institutions and retail Jewellery keep coming back to the market

Due to large stocks of Gold as against its demand it is argued that the core driver of the real price of gold is stock equilibrium rather than flow equilibrium

Economic forces that determine the price of gold are different from and in many cases opposed to the forces that influence most financial assets

South Africa is the worlds largest gold producer with 394 tons in 2001 followed by US and Australia

India is the worlds largest gold consumer with an annual demand of 800 tons

World Gold Markets London as the great clearing house New York as the home of futures trading Zurich as a physical turntable Istanbul Dubai Singapore and Hong Kong as doorways to important

consuming regions Tokyo where TOCOM sets the mood of Japan Mumbai under Indias liberalized gold regime

Indian Gold Market

Let us at first take a look at the evolution of the Indian Gold Market India was never in dearth of Gold Reserves History had been a witness of the fact that India was always self sufficient in all its natural resources and more so in case of gold It was this abundance in availability of such precious metals that lured foreign invaders from all parts of the globe as well as from time to time to come to India and plunder as much of it as was possible for them to do However there were a significant number of such intruders who after entering the country fell for the land and its cultural heritage which eventually led them to settle and establish their empire in India

As a inevitable consequence of the lavish livelihood exhibited by the Indian rulers the Gold reserves in India gradually diminished The arrival of the British in the hierarchy in the middle of the eighteenth century announced the decline of Indias Gold Reserves even further The colonial status given to India by the British crippled the economy which once boasted of its wealth in gold Huge quantities of the precious metal was carried to England right after their extraction As a result a major proportion of Indias Gold Reserves was vanishing without even entering into the economy

By the time India gained independence a huge vacuum had already been created as far as Gold Reserves in India was concerned Slowly after several decades have gone by India has finally started to fill up the vacuum in a big way After reaching a new height in the form of 8 growth in Gross

Domestic Product (GDP ) for the year 2005-06 India is being recognized as one of the fastest emerging economies of the world

Indias growing prospects can also be noticed in the gold market as well India is viewed as the largest consumer of gold in recent times According to the figures presented by the estimates of the World Gold Council (WGC) Indias total demand for gold in the year 2001 was 2432 tonnes which comprised 262 of the total world demand Gold is valued in India as a savings and investment vehicle and is the

second preferred investment after bank deposits India is the worlds largest consumer of gold in jewellery as

investment In July 1997 the RBI authorized the commercial banks to import gold for

sale or loan to jewellers and exporters At present 13 banks are active in the import of gold

This reduced the disparity between international and domestic prices of gold from 57 percent during 1986 to 1991 to 85 percent in 2001

The gold hoarding tendency is well ingrained in Indian society Domestic consumption is dictated by monsoon harvest and marriage

season Indian jewellery offtake is sensitive to price increases and even more so to volatility

In the cities gold is facing competition from the stock market and a wide range of consumer goods

Facilities for refining assaying making them into standard bars in India as compared to the rest of the world are insignificant both qualitatively and quantitatively

To sum up the Indian Gold Market has a very bright future ahead

Who is the regulator

The exchanges are regulated by the Forward Markets Commission Unlike the equity markets brokers dont need to register themselves with the regulatorThe FMC deals with exchange administration and will seek to inspect the books of brokers only if foul practices are suspected or if the exchanges themselves fail to take action In a sense therefore the commodity exchanges are more self-regulating than stock exchanges But this could change if retail participation in commodities grows substantially

Who are the players in commodity derivatives

The commodities market will have three broad categories of market participants apart from brokers and the exchange administration - hedgers speculators and arbitrageurs Brokers will intermediate facilitating hedgers and speculators

Hedgers are essentially players with an underlying risk in a commodity - they may be either producers or consumers who want to transfer the price-risk onto the market

Producer-hedgers are those who want to mitigate the risk of prices declining by the time they actually produce their commodity for sale in the market consumer hedgers would want to do the opposite

For example if you are a jewellery company with export orders at fixed prices you might want to buy gold futures to lock into current prices Investors and traders wanting to benefit or profit from price variations are essentially speculators They serve as counterparties to hedgers and accept the risk offered by the hedgers in a bid to gain from favourable price changes

21WHY INVEST IN GOLD

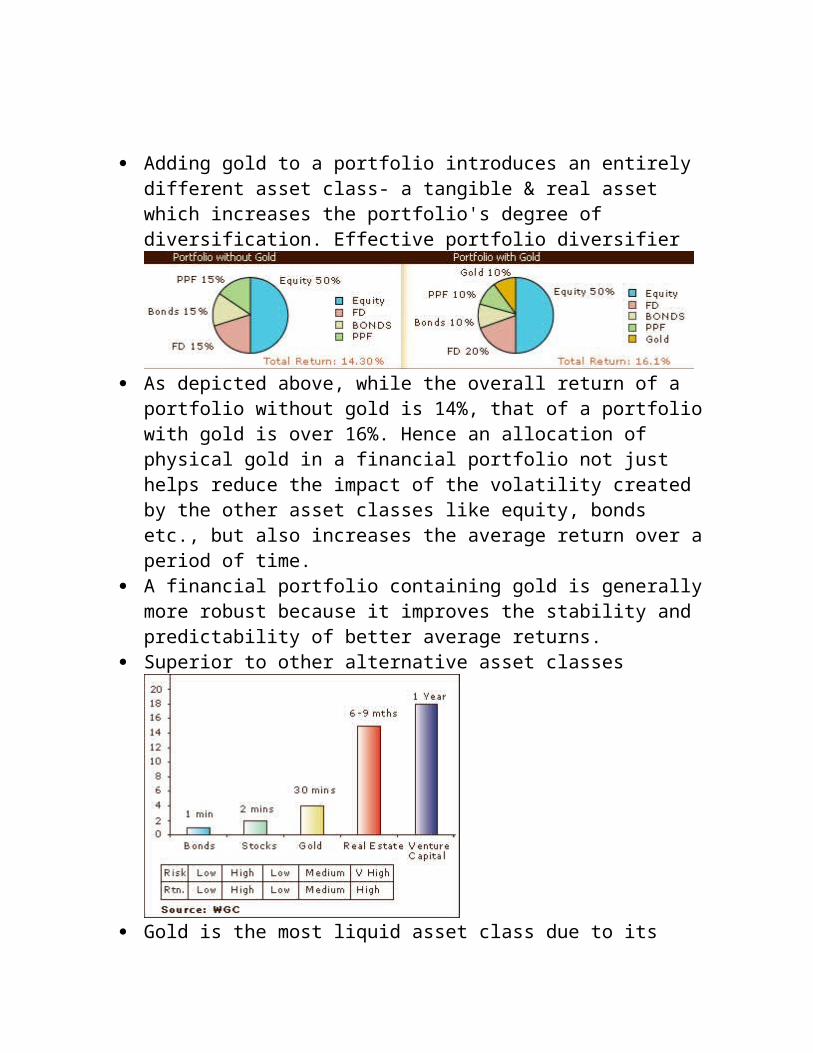

Adding gold to a portfolio introduces an entirely different asset class- a tangible amp real asset which increases the portfolios degree of diversification Effective portfolio diversifier

As depicted above while the overall return of a portfolio without gold is 14 that of a portfolio with gold is over 16 Hence an allocation of physical gold in a financial portfolio not just helps reduce the impact of the volatility created by the other asset classes like equity bonds etc but also increases the average return over a period of time

A financial portfolio containing gold is generally more robust because it improves the stability and predictability of better average returns

Superior to other alternative asset classes

Gold is the most liquid asset class due to its universal acceptance as an alternative to currency and also because globally the gold market is functional 24x7

Same cannot be said about any other asset class as they take much longer time to liquidate (from 1 day to upto 3-4 months)

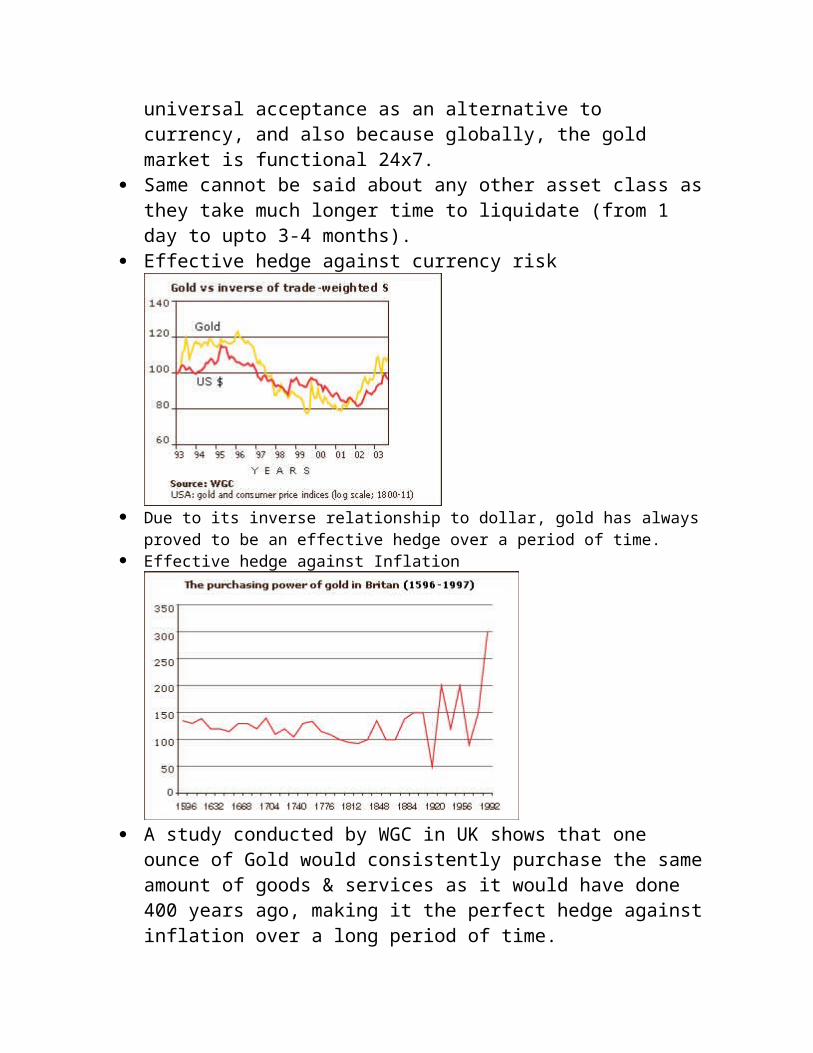

Effective hedge against currency risk

Due to its inverse relationship to dollar gold has always proved to be an effective hedge over a period of time

Effective hedge against Inflation

A study conducted by WGC in UK shows that one ounce of Gold would consistently purchase the same amount of goods amp services as it would have done 400 years ago making it the perfect hedge against inflation over a long period of time

Other Reasons More liquid as compared to the other asset classes Gold can be bought

sold or traded globally Performance of gold not linked to performance of any company industry

or government Gold needs no professional manager unlike mutual funds Gold is an asset which is not simultaneously a liability unlike stocks It doesnt require political amp social stability to survive in fact it thrives

under worst societal conditions Gold doesnt ever loose its intrinsic value Inspite of the growing demand for gold in India average retail household

has seldom considered ldquoinvesting in goldrdquo because of the absence of an efficient and effective platform

Gold vs Stock

bullPerformance of gold not linked to performance of any company industry or governmentbullGold needs no professional manager unlike mutual fundsbullGold is an asset which is not simultaneously a liability unlike stocksbullIt does not require political amp social stability to survive in fact it thrives in the worst conditionsbullGold will never loose its intrinsic value

22 GOLD MARKET EXCHANNGES

MCX (Multi Commodity Exchange)

Multi Commodity Exchange of India Ltd (MCX) an independent and de-mutualised multi commodity exchange has permanent recognition from the Government of India MCX a state-of-the-art nationwide digital exchange facilitates online trading clearing and settlement operations for a commodities futures trading Key shareholders of MCX are Financial Technologies (India) Ltd State Bank of India Union Bank of India Bank of India Corporation Bank amp Canara Bank Headquartered in Mumbai MCX is led by an expert management team with deep domain knowledge of the commodity futures markets and has successfully established a thriving digital market for trading in Gold Silver Steel Kapas Cotton Rubber Black Pepper Oil amp Oil Seeds Ferrous and Non-Ferrous Metals Agri Commodities Pulses and Soft commodities

MCX now stands amongst the top five bullion exchanges in the world and the largest gold futures exchange in India Between November 11 2003 and August 12 2004 MCX has clocked a total Gold turnover of more than 340 tons valued at around Rs 20000 crores which accounts for 90 per cent of the gold futures trading in the country MCX offers two types of contract in Gold ie Gold (1 Kg) and Gold Mini (100 Gms) facilitating a large spectrum of market participants to do trading MCX has also recorded Gold physical delivery in numerous contracts to the extent of 15 quintals

NCDEX (National Commodity amp Derivative Exchange Limited)

National Commodity amp Derivatives Exchange Limited (NCDEX) is a professionally managed on-line multi commodity exchange The shareholders are

Promoter shareholders Life Insurance Corporation of India (LIC) National Bank for Agriculture and Rural Development (NABARD) and National Stock Exchange of India Limited (NSE)

Other shareholders Canara Bank CRISIL Limited (formerly the Credit Rating Information Services of India Limited) Goldman Sachs Intercontinental Exchange (ICE) Indian Farmers Fertiliser Cooperative Limited (IFFCO) and Punjab National Bank (PNB)

NCDEX is the only commodity exchange in the country promoted by national level institutions This unique parentage enables it to offer a bouquet of benefits which are currently in short supply in the commodity markets The institutional promoters and shareholders of NCDEX are prominent players in their respective fields and bring with them institutional building experience trust nationwide reach technology and risk management skills

NCDEX is a public limited company incorporated on April 23 2003 under the Companies Act 1956 It obtained its Certificate for Commencement of Business on May 9 2003 It commenced its operations on December 15 2003

NCDEX is a nation-level technology driven de-mutualised on-line commodity exchange with an independent Board of Directors and professional management - both not having any vested interest in commodity markets It is committed to provide a world-class commodity exchange platform for market participants to trade in a wide spectrum of commodity derivatives driven by best global practices professionalism and transparency

NCDEX is regulated by Forward Markets Commission NCDEX is subjected to various laws of the land like the Forward Contracts (Regulation) Act Companies Act Stamp Act Contract Act and various other legislations

NCDEX is located in Mumbai and offers facilities to its members about 550 centres throughout India The reach will gradually be expanded to more centres

NCDEX currently facilitates trading of 57 commodities

23 WHY MCX

Multi Commodity Exchange of India Ltd (MCX) the largest player in the bullion futures trading is participating in the convention as lsquoExchange Partnerrsquo The convention is organized by Bangalore based Foretell Business Solutions Pvt Ltd and is supported by Bombay Bullion Association (BBA)

MCX now stands amongst the top five bullion exchanges in the world and the largest gold futures exchange in India Between November 11 2003 and August 12 2004 MCX has clocked a total Gold turnover of more than 340 tons valued at around Rs 20000 crores which accounts for 90 per cent of the gold futures trading in the country

MCX offers two types of contract in Gold ie Gold (1 Kg) and Gold Mini (100 Gms) facilitating a large spectrum of market participants to do trading MCX has also recorded Gold physical delivery in numerous contracts to the extent of 15 quintals

Gold is for big investors who can invest huge amount of money and is willing to take huge risk The price quote is per 10gmMaximum lot size is 10 kg While Gold Mini is for small investors in which we can trade in 100gm and the maximum lot size is 2MT

Now a days MCX is also providing contracts on Gold GuineaIn this the trading unit is 8gm It is like small gold coins

24 TERMS AND TERMINOLOGIES IN GOLD MARKET

This guide is intended to provide a basic understanding of commodity futures terminology Though the terminology of trading agricultural commodities goes far beyond the scope of this guide this information can be used to build a knowledge base from which a broader understanding of the futures market can be developed

Arbitrage The simultaneous purchase and sale of similar commodities in different markets to take advantage of a perceived price discrepancy

Basis The difference between the current cash price and the futures price of the same commodity for a given contract month

Bear market A period of declining market prices

Bull market A period of rising market prices

Broker A company or individual that executes futures and options orders on behalf of financial and commercial institutions or the general public

Call option An option that gives the buyer the right but not the obligation to purchase (go ldquolongrdquo) the underlying futures contract at the strike price on orbefore the expiration date of the option

Cash (spot) market A place where people buy and sell the actual (cash) commodities that is a grain elevator livestock market or the like

Commission (brokerage) fee A fee charged by a broker for executing a transaction

Convergence A term referring to cash and futures prices tending to come together as the futures contract nears expiration

Cross-hedging Hedging a commodity using a different but related futures contract when there is no futures contract for the cash commodity being hedged

and the cash and futures markets follow similar price trends For example hedging cull cows on the live cattle futures market

Daily trading limit The maximum price change set by the exchange each day for a contract

Day traders Speculators who take positions in futures or options contracts and liquidate them before the close of the same trading day

Delivery The transfer of the cash commodity from the seller of a futures contract to the buyer of a futures contract

Forward (cash) contract A cash contract in which a seller agrees to deliver a specific commodity to a buyer at a specific time in the future

Fundamental analysis A method of anticipating future price movement using supply and demand information

Futures contract A legally binding agreement made on the trading floor of a futures exchange to buy or sell a commodity or financial instrument sometime inthe future Futures contracts are standardized according to the quality quantity and delivery time and location for each commodity The only variableis price which is determined on an exchange trading floor

Hedger An individual or company owning or planning to own a cash commodity mdash corn soybeans wheat US Treasury bonds notes bills etc mdash andconcerned that the costs of the commodity may change before it can be either bought or sold in the cash market A hedger achieves protection againstchanging cash prices by purchasing (selling) futures contracts of the same or similar commodity and later offsetting that position by selling (purchasing)futures contracts of the same quantity and type as the initial transaction and at the same time as the cash transaction occurs

Hedging The practice of offsetting the price risk inherent in any cash market position by taking an equal but opposite position in the futures market Hedgers use the futures markets to protect their business from adverse price changes

Initial margin The amount a futures market participant must deposit into a margin account at the time an order is placed to buy or sell a futures contract

25 FACTORS AFFECTING GOLD PRICES

Historically gold prices have reacted sharply to geo-political and economic shocks inflationary fears dipping supply and rising demand a weak dollar and struggling equity markets Be it the oil shocks of the 1970s or the 1980 invasion of Afghanistan or the reaction to the collapse of investment banks last yearmdashin every case gold prices touched record highs In March 2008 for example gold touched all time highs of $1023 an ounce (31 grams) following news of the collapse of Bear Stearns Even in the current year recessionary conditions and the global equity sell-offs have ensured firm gold prices with the average going at $900 to an ounce

Gold also seems to be giving the best returns when the inflation rate is at high levels (gold has outperformed equities by a wide margin in the US during high inflationary periods) and thus is considered to be a good hedge against it While currently inflation is hardly a concern large amounts of liquidity injected by governments is likely to find its way into the market and push up inflation While this could lead to depreciation of currencies (as governments print more money and increase money supply) gold because of its limited supply (canrsquot increase it suddenly unlike currencies) continues to hold its own and is thus is considered as an effective inflation hedge

While a weak dollar has been positive for gold and the yellow metal has a negative correlation with the dollar currently both asset classes are in demand

Best among worstGold has moved up by 33 per cent since November 1 2008 and the dollar has been moving up against most currencies including the euro and the rupee Says Manasee S Gokhale economist NCDEX ldquoWith few other options available and as long as other currencies are falling dollar would continue to strengthenrdquo Despite the poor fundamentals of the US economy and a yawning fiscal deficit institutions have been buying dollars as it is considered the better bet among weak currencies

The movement of the gold and dollar in the upward direction is due to recessionary conditions and is therefore temporary believe experts Says Jayant Manglik president Religare Commodities ldquoThe gold-dollar relationship will get back to the trend line Unprecedented investments by governments should help economies recover by the end of the yearrdquo The frenzy of investment in gold going ahead he believes is likely to die down as recovering economies will bring equities into play once again

However till that happens the key reason for gold prices moving up will neither be dollars external shocks or the falling equity markets but as an investment option with investors seeking assets which have minimal risk offer stable returns and have low price volatility

The gold rushJewellery demand in India has always been the key demand driver making up over two-thirds of total global demand for gold This has however changed dramatically over the last one year due to increase in investment demand worldwide In 2007 jewellery in terms of volumes accounted for 68 per cent of demand while investments had a share of 19 per cent (rest used for industrial and dental purposes) A year on investment demand has shot up 64 per cent in volume terms especially in the last two quarters of 2008 (See chart Gold demand) with investors snapping up a 1000 tonnes of gold Share of investments now account for 30 per cent that of jewellery has fallen to 58 per cent

In addition to retail consumption of gold coins and bars shooting up investments in exchange traded funds (ETFs) have also seen a rise Unlike the situation in India where gold ETFs have a miniscule five tonnes of gold with them ETFs such as the NYSE-listed SPDR saw its gold holdings jump 14 per cent in one month to nearly 1000 tonnes (See graph ETFs in vogue) which is more than what India the largest consumer of gold imports in a year Will this trend continue Dharmesh Sodah of the trade body World Gold Council believes that while there will be profit-taking the assets under management of US-based ETFs have been increasing due to the lack of alternative investments making them sticky

In India the movement has not been as dramatic Says Gokhale ldquoETFs are a new concept in India and are likely to do well over the next two years once investors can see a record of stable returnsrdquo Demand in the short term however is likely to be hit due to the prevailing high prices Experts expect a rally in April (the Akshya Tritya festival pushes up gold sales) after which gold might stay down An upward

movement post September (start of the wedding season) could be seen with gold likely to touch about $1100 levels in a year

While global demand is expected to be steady supply constraints also favour firm prices

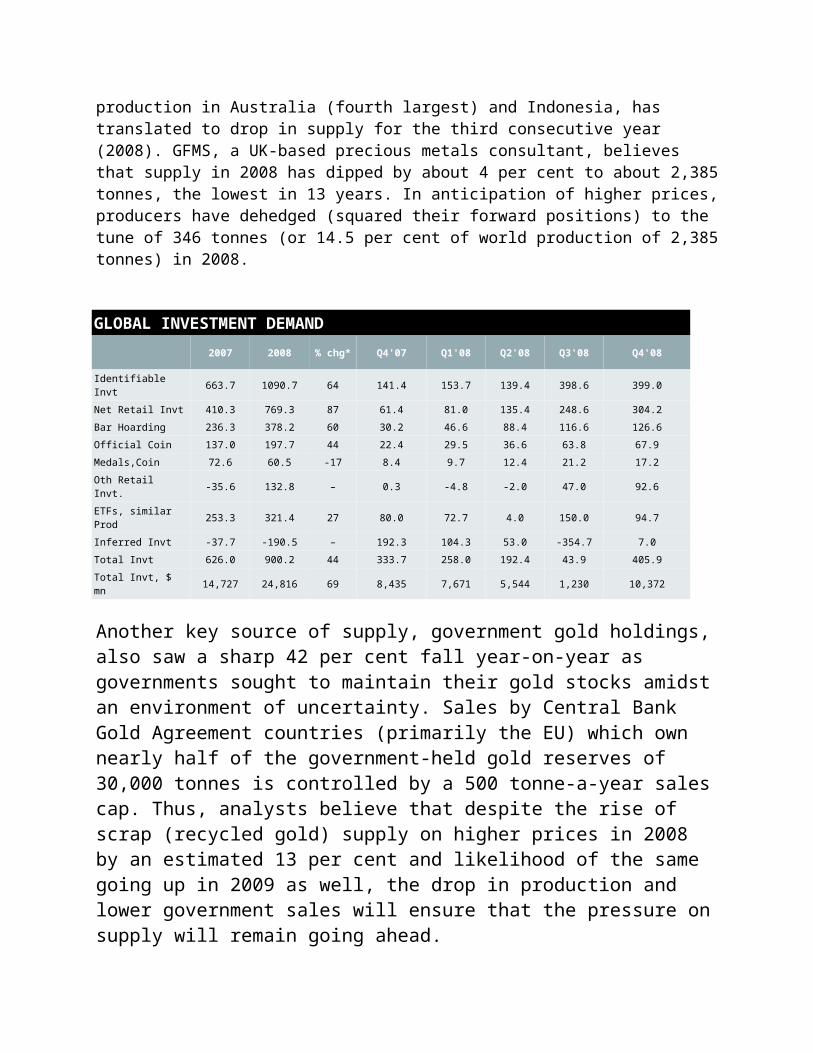

In short supplyGlobally with no fresh sources of mining available and a drop in gold prices in the 1990s has meant depressed production and mining activity since 2002 Acute power and labour shortages in South Africa (third largest producer) as well as sharp dips in production in Australia (fourth largest) and Indonesia has translated to drop in supply for the third consecutive year (2008) GFMS a UK-based precious metals consultant believes that supply in 2008 has dipped by about 4 per cent to about 2385 tonnes the lowest in 13 years In anticipation of higher prices producers have dehedged (squared their forward positions) to the tune of 346 tonnes (or 145 per cent of world production of 2385 tonnes) in 2008

GLOBAL INVESTMENT DEMAND

2007 2008 chg Q407 Q108 Q208 Q308 Q408

Identifiable Invt 6637 10907 64 1414 1537 1394 3986 3990

Net Retail Invt 4103 7693 87 614 810 1354 2486 3042

Bar Hoarding 2363 3782 60 302 466 884 1166 1266

Official Coin 1370 1977 44 224 295 366 638 679

MedalsCoin 726 605 -17 84 97 124 212 172

Oth Retail Invt -356 1328 ndash 03 -48 -20 470 926

ETFs similar Prod 2533 3214 27 800 727 40 1500 947

Inferred Invt -377 -1905 ndash 1923 1043 530 -3547 70

Total Invt 6260 9002 44 3337 2580 1924 439 4059

Total Invt $ mn 14727 24816 69 8435 7671 5544 1230 10372

Another key source of supply government gold holdings also saw a sharp 42 per cent fall year-on-year as governments sought to maintain their gold stocks amidst an environment of uncertainty Sales by Central Bank Gold Agreement countries (primarily the EU) which own nearly half of the government-held gold reserves of 30000 tonnes is controlled by a 500 tonne-a-year sales cap Thus analysts believe that despite the rise of scrap (recycled gold) supply on higher prices in 2008 by an estimated 13 per cent and likelihood of the same going up in 2009 as well the drop in production and lower government sales will ensure that the pressure on supply will remain going ahead

Price outlookIn light of the current scenario how will prices move Experts believe that since gold prices have moved up in the last three months the near-term could see some

softening Says Harish Galipalli head of research Karvy Comtrade ldquoThere is possibility of correction and gold might dip to $930 to an ounce from about $950 per ounce levels prevailing currentlyrdquo In the medium-term though the overall weak economic environment globally will keep upward pressure on gold prices as investors look for safety

Says Manglik ldquoWhile gold has given about 26 per cent returns in 2008 it will fetch a return of about 20 per cent from here on (rupee terms) over the next one year with the gains equally split between currency depreciation and investment demandrdquo While returns have been good over the last year future returns in the yellow metal will depend on the position of equity markets and the performance of other assets classes such as debt currencies and real estate

Gold is exhibiting all the classic signs of being in a structural bull market In the past year weve seen gold go up on fears of inflation then it rose on fears of deflation

The woes of the banking industry certainly appear to be aiding gold In a bizarre twist central bankers actually want the price of gold to rise because it would be an indication that attempts to stave off deflation are workingThe long-term story for gold however is as a re-monetization play as investors lose faith in fiat currencies

The Fed has flooded the market with newly-printed money Other countries are following suit Now that all of this money is printed it may be difficult to pull it back in This of course would lead to currency devaluations Some believe that the bottom in fiat currencies has begun and hard assets like gold and silver should benefitInvestors in Europe and north America went on an extraordinary shopping spree for gold coins and bars in the final quarter of 2008 snapping up 1485 tonnes a jump of 811 per cent compared with the same period in 2007 as the collapse of Lehman Brothers led to a massive increase in safe haven buying According to the World Gold Council this rush into physical gold by western investors pushed global retail investment up almost 400 per cent to 3042 tonnesGold is about 25 per cent above its peak from the last great bull market in the metal in 1980In yen terms gold is still barely half its 1980 level which might imply that there could be more gold demand to come from Japanese investors (referred to as Mrs Watanabe)

And in sterling terms gold is double its 1980 peak which implies either great worries about returning inflation in the UK or an overdone collapse of confidence in the pound sterling

The WGCs data confirmed earlier reports from traders about widespread shortages of coins and exceptional buying interest Investment inflows into gold exchange traded funds reached 947 tonnes in the fourth quarter up 18 per cent on the same period in 2007 but down from the record 150 tonnes of inflows seen in the third quarter of 2008

Rising prices for gold around the world mean that those currencies are depreciating Practically all currencies are depreciating relative to gold

The whole world of currencies is depreciating including the dollar But due to the liquidity provided by US debt during the financial crisis the dollar has appeared to rise in value within the overall currency bear market All currency ships are sinking the dollar ship is just not sinking as fast

For the better part of a century now the global gold trade has been dominated by the dollar

All over the world the prevailing gold price is a function of any currencys exchange rate with the dollar along with the dollar-price of gold

Back in July 2008 the dollar started rallying It wasnt for fundamental reasons but because the giant mortgage-backed bond industry was imploding and bond investors desperately sought the safety of US Treasuries

This kicked off the massive dollar panic rally in Q3 CY 2008 and the subsequent stock panic of Q4 CY 2008 accelerated it Until this anomalous rally erupted dollar gold remained strong in the high $800s and low $900s

At this dollar rallys apex on the very day the stock markets bottomed in late November the US Dollar Index had reached levels first seen in early 2004 when gold was near $400

Yet gold didnt even close under $700 in 2008s panic vastly stronger than the dollar alone would suggest it should be Once again this highlights the critical fact that the dollar is no longer golds primary driver even though it can still temporarily influence gold at times

In order to predict the future of gold prices one needs to keep an eye on gold lease rates a spike would be a good lead indicator that gold is about to punch higher as this would reflect a shortage of lendable bullion

Rising lease rates will cause gold to go into backwardation as holders of gold may not want to sell their gold forward under any circumstances a trend currently evidenced by the high physical premium being paid for gold coins

Rising lease rates prefigured the last big move in gold back in the spring of 2007 just as the two Bear Stearns hedge funds were blowing up Central banks feared counterparty risk for the first time in 20 years and substantially curtailed gold lending and sales

This led to a 40 per cent rally in gold from $700 to over $1000

Indians are collectively the worlds biggest gold investors so the rupee gold price is very important to the health of this global gold bull

Thanks to a rupee collapse during the stock panic to dismal levels underneath where its secular bull started in mid-2002 rupee gold has been very strong In fact it surged to new bull highs during the stock panic and ended 2008 near these levels During all this turmoil Indias deep cultural affinity for gold investment was strongly affirmed

The rupee gold price is an important one to watch thanks to Indias enormous influence in the global gold markets Even though tonnage of gold imports is suffering rupee expenditure levels are holding up well in India

Technical chartists say that gold could move into a parabolic fashion once the $1000 per ounce barrier is broken From there the speed of the move could accelerate sharply

For many structural reasons totally unrelated to the stock panic the fundamentals of gold remain awesomely bullish Its strong performance during the stock panic in most of the world is only icing on the cake that will drive additional investment demand

How high can gold ultimately go A Dow Jones Industrial Averagegold ratio of 21 would be a good sign the bull market in gold is getting well-advanced We saw this in 1932 and 1980

We are in a multi-year gold structural bull market that will eventually take the price to an integer multiple of where it is now

Within the broader and longer-term positive environment for gold we need to remember that short-term bursts of emotions might run to extremes This might be the case in the current situation Emotions have been running high Gold is seriously over-bought While investors need gold in their portfolio the current price situation might not be the best for buyers

Buy on price weakness not strength At the same time it is never advisable to sell in a structural bull market

28 INFLATION EXCHANGE RATE WITH DOLLAR SENSEX AND GOLD PRICES

Dollar is Negatively Co-related with Gold Correlation GoldDollar -70

For Inflation Hedge

The value of gold in terms of real goods and services that it canbuy has remained remarkably stable In contrast the purchasingpower of many currencies have varied over time

Gold has consistently reverted to its historic purchasing powerparity

Gold is an inflation hedge as proved by a 400-year study of thepurchasing power of gold in Britain between 1596 and 1997 Oneounce of gold would consistently purchase the same amount ofgoods and services as it would have done 400 years ago

GoldBeESGoldBeESTM

26 RECENT TREND IN GOLD MARKET IN INDIA

MUMBAI Gold is no longer glittering in India the biggest global market for the consumption and imports of the yellow metal Gold imports to the country has plunged to zero levels as no bank and trading houses imported any gold during the month of February

Gold analysts said that February 2009 is perhaps the only month in this decade where there has been no gold imports to India ldquoThis is a serious issue As gold market is all heated up and gold prices have skyrocketed imports of the yellow metal have practically stopped in Indiardquo said Akash Gupta a bullion trader in Mumbairsquos Zaveri Market

Buying of gold jewellery has fallen sharply in January leading to a slump in the yellow metalrsquos imports According to the Bombay Bullion Association there was more than 90 plunge in gold imports in January ldquoThe trend has worsened for February There was zero gold imports to India in Februaryrdquo the Association president Suresh Hundia In 2008 Indiarsquos gold imports dipped by 45 per cent to touch 450 tons

In the last eight years from 2000 gold imports to India every year have been between 400-800 tons But trade bodies have warned that gold imports this year could collapse to 100 tons if the current trend continues ldquoIt will not be a surprise if gold imports fall to an all-time low of 100 tons or below in 2009rdquo said bullion analyst Ashish Roy

High prices global economic meltdown and financial crunch among investors and bullion dealers led to low demand for gold in India where yellow metal is considered the best safe haven investment and people buy gold for weddings and other ceremonies

According to Hundia gold sales and demand are plunging to negligible levels because of high prices ldquoGold and jewellery sector is reeling under a crisis because of high prices and retrenchments across sectorsrdquo he said Gold prices which in December was from Rs 13505 for10 grams moved to an all-time high of Rs 16000 per ten grams last week

Analysts and India trade bodies have predicted that gold prices could zoom to Rs

17000 per ten grams by April this year They also say that if this lowest level of gold intake continues in India 2009 will be the worst year in this decade as far as gold imports are concerned But despite the gloom in gold imports and sales in India bullion traders hope that the gold market might pick up in April-May season

The World Gold Council has predicted there will be a modest gain in gold purchases in India during the summer wedding season and the Hindu religious festival of Akshaya Tritiya ldquoThere will be a modest growth of 10-15 per cent in the Indian domestic jewellery businessrdquo said K Shivram Vice-President World Gold Council Shivram says gold sales will pick in April-May-June after the dull season of December and January

3 CONCLUSION

Internationally trading in Gold has given the investors very safe and very fruitful option Today people who earlier feared from entering the market are investing in Gold as it is the most safest asset and also its price is less fluctuating Gold Market has developed vastly since it was started Recently gold prices touched the height of Rs16000- per 10gm which astonished everybody The reason may be any but today people willing to invest in Gold rather than Stock Below the graph relating to increase in investment in Gold is give

This graph is made by making an average of the whole months investment taking 16th as the base from the year October 2006 to the year February 2009 It clearly shows that how there is an increase of investment in gold Gold has significantly low correlation to other assets like equity indices fixed income and commodities Therefore adding gold to a portfolio may help improve risk adjusted returns or reduce volatility for the expected return

Indian ScenarioThere is need for an instrument which has1048708 Small denomination1048708 Cost efficiency1048708 Convenience for long term holding1048708 Greater uniform availability1048708 Transparency1048708 Liquidity1048708 Tax EfficiencyGold BeES Can fulfill this Need

Improving stability and predictability of returns1048708 Gold improves the stability and predictability of portfolio returns It is not correlated with other assets because the gold price is not necessarily driven by the same factors that drive the performance of other assets1048708 Adding gold to a portfolio introduces an entirely different class of asset Gold is unusual because it is both a commodity and a monetary asset1048708 Gold is one of the few financial assets that is not linked to a liability It can provide insurance against extreme movements on the value of traditional asset classes

31 Recommendation-

In my survey part first I visited Mr Sumit Choudhary an Arbitrager Sreepati Balaji Commodities Ltd and then I visited Mr Rajib Kejriwal CEO Eureka Commodities Ltd Both of them said that the recent increase in price of gold is due to the fact that stock market is down so people are investing less in the stock market and investing more in gold as it has become a less risk market Also the fact that dollar is going up has increased the price of gold as per them

A REPORTON

GOLD MARKET

ByManish Madhogaria

Lohia Securities Pvt Ltd

Date of submission-

AUTHORISATION

I have been authorized to undertake the project ldquoGold Market rsquorsquo as my SIP Project for Lohia Securities Pvt Ltd I have been assigned to do this project under Mr Jitesh Agarwal President HRD

ACKNOWLEDGEMENT

The present project is carried out in Lohia Securities Pvt Ltd located at Kolkata under the guidance of Icfai Business School Kolkata The project is not fully completed only half of the work has been done so far Now on the verge of writing this interim report I would like to thank a number of people from whom I have received generous support and who in different ways have contributed me in reaching so farFirst I would like to thank my company guide Mr Jitesh Agarwal of Lohia Securities Pvt Ltd and all the staff who have helped me Their support and comments have been of Inestimable value throughout whatever have been achieved in this projectI would also like to thank the staff at IBS kolkata and especially my faculty guide Dr Sutapa Banerjee for helping amp guiding me and at the same time solving all my queries Furthermore I would also like to thank my dean sir mr RK Mandan and all the faculty members present in IBS lucknow for supporting and helping me in this MBA program I would also like to thank Mr Rajib Kejriwal CEO Eureka Commodities Pvt Ltd Mr Sumit Choudhry Arbitrager Sreepati Balaji PvtLtd for extending their support and providing me all the necessary information needed to prepare the Interim Report

Manish Madhogaria

TABLE OF CONTENTS

Authorization I Acknowledgement II Abstract III 1 Introduction 2 MainText

21 Why Invest in Gold22 Gold Market Exchanges23 Special Features of Gold Market24 Terms and Terminologies in this Market25 Why prefer MCX26 Factors affecting Gold prices27 Inflation Exchange rate with Dollar Sensex and Gold prices28 Recent trend in Gold Market in India

3 Conclusion 31 Recommendation 5 References

ABSTRACT

My project ldquoGold Market rsquorsquo gives emphasis on the trading strategies which are followed by different trading firms and brokers and also it gives emphasis on how different factors like inflation affects the price of gold This will include learning of the gold market in detail from net how the market started what was the need behind creating such markets who regulates this market what is the minimum requirement etc The methodology that I have adopted to conduct the research work is to visit different trading firms Internet search engines like google yahoo is used and will be used to carry out the research work The main idea behind this market research is to gain basic idea what strategies different trading firms and brokers use to gain maximum profit

1 INTRODUCTION

Gold is a very solid asset Buying physical gold does have advantages compared with other investments Investments in gold-backed financial products and paper gold should be left up to the professionals says Mark Robinson a bullion analyst based in Dubai

Gold is the oldest precious metal known to man Therefore it is a timely subject for several reasons It is the opinion of the more objective market experts that the traditional investment vehicles of stocks and bonds are in the areas of their all-time highs and may be due for a severe correction

To fully appreciate why 8000 years of experience say gold is forever we should review why the world reveres what Englands most famous economist John Maynard Keynes cynically called the barbarous relic

Why gold is good as gold is an intriguing question However we think that the more pragmatic ancient Egyptians were perhaps more accurate in observing that golds value was a function of its pleasing physical characteristics and its scarcity

Gold is primarily a monetary asset and partly a commodity More than two thirds of golds total accumulated holdings account as value

for investment with central bank reserves private players and high-carat Jewellery

Less than one third of golds total accumulated holdings is as a commodity for Jewellery in Western markets and usage in industry

The Gold market is highly liquid and gold held by central banks other major institutions and retail Jewellery keep coming back to the market

Due to large stocks of Gold as against its demand it is argued that the core driver of the real price of gold is stock equilibrium rather than flow equilibrium

Economic forces that determine the price of gold are different from and in many cases opposed to the forces that influence most financial assets

South Africa is the worlds largest gold producer with 394 tons in 2001 followed by US and Australia

India is the worlds largest gold consumer with an annual demand of 800 tons

World Gold Markets London as the great clearing house New York as the home of futures trading Zurich as a physical turntable Istanbul Dubai Singapore and Hong Kong as doorways to important

consuming regions Tokyo where TOCOM sets the mood of Japan Mumbai under Indias liberalized gold regime

Indian Gold Market

Let us at first take a look at the evolution of the Indian Gold Market India was never in dearth of Gold Reserves History had been a witness of the fact that India was always self sufficient in all its natural resources and more so in case of gold It was this abundance in availability of such precious metals that lured foreign invaders from all parts of the globe as well as from time to time to come to India and plunder as much of it as was possible for them to do However there were a significant number of such intruders who after entering the country fell for the land and its cultural heritage which eventually led them to settle and establish their empire in India

As a inevitable consequence of the lavish livelihood exhibited by the Indian rulers the Gold reserves in India gradually diminished The arrival of the British in the hierarchy in the middle of the eighteenth century announced the decline of Indias Gold Reserves even further The colonial status given to India by the British crippled the economy which once boasted of its wealth in gold Huge quantities of the precious metal was carried to England right after their extraction As a result a major proportion of Indias Gold Reserves was vanishing without even entering into the economy

By the time India gained independence a huge vacuum had already been created as far as Gold Reserves in India was concerned Slowly after several decades have gone by India has finally started to fill up the vacuum in a big way After reaching a new height in the form of 8 growth in Gross

Domestic Product (GDP ) for the year 2005-06 India is being recognized as one of the fastest emerging economies of the world

Indias growing prospects can also be noticed in the gold market as well India is viewed as the largest consumer of gold in recent times According to the figures presented by the estimates of the World Gold Council (WGC) Indias total demand for gold in the year 2001 was 2432 tonnes which comprised 262 of the total world demand Gold is valued in India as a savings and investment vehicle and is the

second preferred investment after bank deposits India is the worlds largest consumer of gold in jewellery as

investment In July 1997 the RBI authorized the commercial banks to import gold for

sale or loan to jewellers and exporters At present 13 banks are active in the import of gold

This reduced the disparity between international and domestic prices of gold from 57 percent during 1986 to 1991 to 85 percent in 2001

The gold hoarding tendency is well ingrained in Indian society Domestic consumption is dictated by monsoon harvest and marriage

season Indian jewellery offtake is sensitive to price increases and even more so to volatility

In the cities gold is facing competition from the stock market and a wide range of consumer goods

Facilities for refining assaying making them into standard bars in India as compared to the rest of the world are insignificant both qualitatively and quantitatively

To sum up the Indian Gold Market has a very bright future ahead

Who is the regulator

The exchanges are regulated by the Forward Markets Commission Unlike the equity markets brokers dont need to register themselves with the regulatorThe FMC deals with exchange administration and will seek to inspect the books of brokers only if foul practices are suspected or if the exchanges themselves fail to take action In a sense therefore the commodity exchanges are more self-regulating than stock exchanges But this could change if retail participation in commodities grows substantially

Who are the players in commodity derivatives

The commodities market will have three broad categories of market participants apart from brokers and the exchange administration - hedgers speculators and arbitrageurs Brokers will intermediate facilitating hedgers and speculators

Hedgers are essentially players with an underlying risk in a commodity - they may be either producers or consumers who want to transfer the price-risk onto the market

Producer-hedgers are those who want to mitigate the risk of prices declining by the time they actually produce their commodity for sale in the market consumer hedgers would want to do the opposite

For example if you are a jewellery company with export orders at fixed prices you might want to buy gold futures to lock into current prices Investors and traders wanting to benefit or profit from price variations are essentially speculators They serve as counterparties to hedgers and accept the risk offered by the hedgers in a bid to gain from favourable price changes

21WHY INVEST IN GOLD

Adding gold to a portfolio introduces an entirely different asset class- a tangible amp real asset which increases the portfolios degree of diversification Effective portfolio diversifier

As depicted above while the overall return of a portfolio without gold is 14 that of a portfolio with gold is over 16 Hence an allocation of physical gold in a financial portfolio not just helps reduce the impact of the volatility created by the other asset classes like equity bonds etc but also increases the average return over a period of time

A financial portfolio containing gold is generally more robust because it improves the stability and predictability of better average returns

Superior to other alternative asset classes

Gold is the most liquid asset class due to its universal acceptance as an alternative to currency and also because globally the gold market is functional 24x7

Same cannot be said about any other asset class as they take much longer time to liquidate (from 1 day to upto 3-4 months)

Effective hedge against currency risk

Due to its inverse relationship to dollar gold has always proved to be an effective hedge over a period of time

Effective hedge against Inflation

A study conducted by WGC in UK shows that one ounce of Gold would consistently purchase the same amount of goods amp services as it would have done 400 years ago making it the perfect hedge against inflation over a long period of time

Other Reasons More liquid as compared to the other asset classes Gold can be bought

sold or traded globally Performance of gold not linked to performance of any company industry

or government Gold needs no professional manager unlike mutual funds Gold is an asset which is not simultaneously a liability unlike stocks It doesnt require political amp social stability to survive in fact it thrives

under worst societal conditions Gold doesnt ever loose its intrinsic value Inspite of the growing demand for gold in India average retail household

has seldom considered ldquoinvesting in goldrdquo because of the absence of an efficient and effective platform

Gold vs Stock

bullPerformance of gold not linked to performance of any company industry or governmentbullGold needs no professional manager unlike mutual fundsbullGold is an asset which is not simultaneously a liability unlike stocksbullIt does not require political amp social stability to survive in fact it thrives in the worst conditionsbullGold will never loose its intrinsic value

22 GOLD MARKET EXCHANNGES

MCX (Multi Commodity Exchange)

Multi Commodity Exchange of India Ltd (MCX) an independent and de-mutualised multi commodity exchange has permanent recognition from the Government of India MCX a state-of-the-art nationwide digital exchange facilitates online trading clearing and settlement operations for a commodities futures trading Key shareholders of MCX are Financial Technologies (India) Ltd State Bank of India Union Bank of India Bank of India Corporation Bank amp Canara Bank Headquartered in Mumbai MCX is led by an expert management team with deep domain knowledge of the commodity futures markets and has successfully established a thriving digital market for trading in Gold Silver Steel Kapas Cotton Rubber Black Pepper Oil amp Oil Seeds Ferrous and Non-Ferrous Metals Agri Commodities Pulses and Soft commodities

MCX now stands amongst the top five bullion exchanges in the world and the largest gold futures exchange in India Between November 11 2003 and August 12 2004 MCX has clocked a total Gold turnover of more than 340 tons valued at around Rs 20000 crores which accounts for 90 per cent of the gold futures trading in the country MCX offers two types of contract in Gold ie Gold (1 Kg) and Gold Mini (100 Gms) facilitating a large spectrum of market participants to do trading MCX has also recorded Gold physical delivery in numerous contracts to the extent of 15 quintals

NCDEX (National Commodity amp Derivative Exchange Limited)

National Commodity amp Derivatives Exchange Limited (NCDEX) is a professionally managed on-line multi commodity exchange The shareholders are

Promoter shareholders Life Insurance Corporation of India (LIC) National Bank for Agriculture and Rural Development (NABARD) and National Stock Exchange of India Limited (NSE)

Other shareholders Canara Bank CRISIL Limited (formerly the Credit Rating Information Services of India Limited) Goldman Sachs Intercontinental Exchange (ICE) Indian Farmers Fertiliser Cooperative Limited (IFFCO) and Punjab National Bank (PNB)

NCDEX is the only commodity exchange in the country promoted by national level institutions This unique parentage enables it to offer a bouquet of benefits which are currently in short supply in the commodity markets The institutional promoters and shareholders of NCDEX are prominent players in their respective fields and bring with them institutional building experience trust nationwide reach technology and risk management skills

NCDEX is a public limited company incorporated on April 23 2003 under the Companies Act 1956 It obtained its Certificate for Commencement of Business on May 9 2003 It commenced its operations on December 15 2003

NCDEX is a nation-level technology driven de-mutualised on-line commodity exchange with an independent Board of Directors and professional management - both not having any vested interest in commodity markets It is committed to provide a world-class commodity exchange platform for market participants to trade in a wide spectrum of commodity derivatives driven by best global practices professionalism and transparency

NCDEX is regulated by Forward Markets Commission NCDEX is subjected to various laws of the land like the Forward Contracts (Regulation) Act Companies Act Stamp Act Contract Act and various other legislations

NCDEX is located in Mumbai and offers facilities to its members about 550 centres throughout India The reach will gradually be expanded to more centres

NCDEX currently facilitates trading of 57 commodities

23 WHY MCX

Multi Commodity Exchange of India Ltd (MCX) the largest player in the bullion futures trading is participating in the convention as lsquoExchange Partnerrsquo The convention is organized by Bangalore based Foretell Business Solutions Pvt Ltd and is supported by Bombay Bullion Association (BBA)

MCX now stands amongst the top five bullion exchanges in the world and the largest gold futures exchange in India Between November 11 2003 and August 12 2004 MCX has clocked a total Gold turnover of more than 340 tons valued at around Rs 20000 crores which accounts for 90 per cent of the gold futures trading in the country

MCX offers two types of contract in Gold ie Gold (1 Kg) and Gold Mini (100 Gms) facilitating a large spectrum of market participants to do trading MCX has also recorded Gold physical delivery in numerous contracts to the extent of 15 quintals

Gold is for big investors who can invest huge amount of money and is willing to take huge risk The price quote is per 10gmMaximum lot size is 10 kg While Gold Mini is for small investors in which we can trade in 100gm and the maximum lot size is 2MT

Now a days MCX is also providing contracts on Gold GuineaIn this the trading unit is 8gm It is like small gold coins

24 TERMS AND TERMINOLOGIES IN GOLD MARKET

This guide is intended to provide a basic understanding of commodity futures terminology Though the terminology of trading agricultural commodities goes far beyond the scope of this guide this information can be used to build a knowledge base from which a broader understanding of the futures market can be developed

Arbitrage The simultaneous purchase and sale of similar commodities in different markets to take advantage of a perceived price discrepancy

Basis The difference between the current cash price and the futures price of the same commodity for a given contract month

Bear market A period of declining market prices

Bull market A period of rising market prices

Broker A company or individual that executes futures and options orders on behalf of financial and commercial institutions or the general public

Call option An option that gives the buyer the right but not the obligation to purchase (go ldquolongrdquo) the underlying futures contract at the strike price on orbefore the expiration date of the option

Cash (spot) market A place where people buy and sell the actual (cash) commodities that is a grain elevator livestock market or the like

Commission (brokerage) fee A fee charged by a broker for executing a transaction

Convergence A term referring to cash and futures prices tending to come together as the futures contract nears expiration

Cross-hedging Hedging a commodity using a different but related futures contract when there is no futures contract for the cash commodity being hedged

and the cash and futures markets follow similar price trends For example hedging cull cows on the live cattle futures market

Daily trading limit The maximum price change set by the exchange each day for a contract

Day traders Speculators who take positions in futures or options contracts and liquidate them before the close of the same trading day

Delivery The transfer of the cash commodity from the seller of a futures contract to the buyer of a futures contract

Forward (cash) contract A cash contract in which a seller agrees to deliver a specific commodity to a buyer at a specific time in the future

Fundamental analysis A method of anticipating future price movement using supply and demand information

Futures contract A legally binding agreement made on the trading floor of a futures exchange to buy or sell a commodity or financial instrument sometime inthe future Futures contracts are standardized according to the quality quantity and delivery time and location for each commodity The only variableis price which is determined on an exchange trading floor

Hedger An individual or company owning or planning to own a cash commodity mdash corn soybeans wheat US Treasury bonds notes bills etc mdash andconcerned that the costs of the commodity may change before it can be either bought or sold in the cash market A hedger achieves protection againstchanging cash prices by purchasing (selling) futures contracts of the same or similar commodity and later offsetting that position by selling (purchasing)futures contracts of the same quantity and type as the initial transaction and at the same time as the cash transaction occurs

Hedging The practice of offsetting the price risk inherent in any cash market position by taking an equal but opposite position in the futures market Hedgers use the futures markets to protect their business from adverse price changes

Initial margin The amount a futures market participant must deposit into a margin account at the time an order is placed to buy or sell a futures contract

25 FACTORS AFFECTING GOLD PRICES

Historically gold prices have reacted sharply to geo-political and economic shocks inflationary fears dipping supply and rising demand a weak dollar and struggling equity markets Be it the oil shocks of the 1970s or the 1980 invasion of Afghanistan or the reaction to the collapse of investment banks last yearmdashin every case gold prices touched record highs In March 2008 for example gold touched all time highs of $1023 an ounce (31 grams) following news of the collapse of Bear Stearns Even in the current year recessionary conditions and the global equity sell-offs have ensured firm gold prices with the average going at $900 to an ounce

Gold also seems to be giving the best returns when the inflation rate is at high levels (gold has outperformed equities by a wide margin in the US during high inflationary periods) and thus is considered to be a good hedge against it While currently inflation is hardly a concern large amounts of liquidity injected by governments is likely to find its way into the market and push up inflation While this could lead to depreciation of currencies (as governments print more money and increase money supply) gold because of its limited supply (canrsquot increase it suddenly unlike currencies) continues to hold its own and is thus is considered as an effective inflation hedge

While a weak dollar has been positive for gold and the yellow metal has a negative correlation with the dollar currently both asset classes are in demand

Best among worstGold has moved up by 33 per cent since November 1 2008 and the dollar has been moving up against most currencies including the euro and the rupee Says Manasee S Gokhale economist NCDEX ldquoWith few other options available and as long as other currencies are falling dollar would continue to strengthenrdquo Despite the poor fundamentals of the US economy and a yawning fiscal deficit institutions have been buying dollars as it is considered the better bet among weak currencies

The movement of the gold and dollar in the upward direction is due to recessionary conditions and is therefore temporary believe experts Says Jayant Manglik president Religare Commodities ldquoThe gold-dollar relationship will get back to the trend line Unprecedented investments by governments should help economies recover by the end of the yearrdquo The frenzy of investment in gold going ahead he believes is likely to die down as recovering economies will bring equities into play once again

However till that happens the key reason for gold prices moving up will neither be dollars external shocks or the falling equity markets but as an investment option with investors seeking assets which have minimal risk offer stable returns and have low price volatility

The gold rushJewellery demand in India has always been the key demand driver making up over two-thirds of total global demand for gold This has however changed dramatically over the last one year due to increase in investment demand worldwide In 2007 jewellery in terms of volumes accounted for 68 per cent of demand while investments had a share of 19 per cent (rest used for industrial and dental purposes) A year on investment demand has shot up 64 per cent in volume terms especially in the last two quarters of 2008 (See chart Gold demand) with investors snapping up a 1000 tonnes of gold Share of investments now account for 30 per cent that of jewellery has fallen to 58 per cent

In addition to retail consumption of gold coins and bars shooting up investments in exchange traded funds (ETFs) have also seen a rise Unlike the situation in India where gold ETFs have a miniscule five tonnes of gold with them ETFs such as the NYSE-listed SPDR saw its gold holdings jump 14 per cent in one month to nearly 1000 tonnes (See graph ETFs in vogue) which is more than what India the largest consumer of gold imports in a year Will this trend continue Dharmesh Sodah of the trade body World Gold Council believes that while there will be profit-taking the assets under management of US-based ETFs have been increasing due to the lack of alternative investments making them sticky

In India the movement has not been as dramatic Says Gokhale ldquoETFs are a new concept in India and are likely to do well over the next two years once investors can see a record of stable returnsrdquo Demand in the short term however is likely to be hit due to the prevailing high prices Experts expect a rally in April (the Akshya Tritya festival pushes up gold sales) after which gold might stay down An upward

movement post September (start of the wedding season) could be seen with gold likely to touch about $1100 levels in a year

While global demand is expected to be steady supply constraints also favour firm prices

In short supplyGlobally with no fresh sources of mining available and a drop in gold prices in the 1990s has meant depressed production and mining activity since 2002 Acute power and labour shortages in South Africa (third largest producer) as well as sharp dips in production in Australia (fourth largest) and Indonesia has translated to drop in supply for the third consecutive year (2008) GFMS a UK-based precious metals consultant believes that supply in 2008 has dipped by about 4 per cent to about 2385 tonnes the lowest in 13 years In anticipation of higher prices producers have dehedged (squared their forward positions) to the tune of 346 tonnes (or 145 per cent of world production of 2385 tonnes) in 2008

GLOBAL INVESTMENT DEMAND

2007 2008 chg Q407 Q108 Q208 Q308 Q408

Identifiable Invt 6637 10907 64 1414 1537 1394 3986 3990

Net Retail Invt 4103 7693 87 614 810 1354 2486 3042

Bar Hoarding 2363 3782 60 302 466 884 1166 1266

Official Coin 1370 1977 44 224 295 366 638 679

MedalsCoin 726 605 -17 84 97 124 212 172

Oth Retail Invt -356 1328 ndash 03 -48 -20 470 926

ETFs similar Prod 2533 3214 27 800 727 40 1500 947

Inferred Invt -377 -1905 ndash 1923 1043 530 -3547 70

Total Invt 6260 9002 44 3337 2580 1924 439 4059

Total Invt $ mn 14727 24816 69 8435 7671 5544 1230 10372

Another key source of supply government gold holdings also saw a sharp 42 per cent fall year-on-year as governments sought to maintain their gold stocks amidst an environment of uncertainty Sales by Central Bank Gold Agreement countries (primarily the EU) which own nearly half of the government-held gold reserves of 30000 tonnes is controlled by a 500 tonne-a-year sales cap Thus analysts believe that despite the rise of scrap (recycled gold) supply on higher prices in 2008 by an estimated 13 per cent and likelihood of the same going up in 2009 as well the drop in production and lower government sales will ensure that the pressure on supply will remain going ahead

Price outlookIn light of the current scenario how will prices move Experts believe that since gold prices have moved up in the last three months the near-term could see some

softening Says Harish Galipalli head of research Karvy Comtrade ldquoThere is possibility of correction and gold might dip to $930 to an ounce from about $950 per ounce levels prevailing currentlyrdquo In the medium-term though the overall weak economic environment globally will keep upward pressure on gold prices as investors look for safety

Says Manglik ldquoWhile gold has given about 26 per cent returns in 2008 it will fetch a return of about 20 per cent from here on (rupee terms) over the next one year with the gains equally split between currency depreciation and investment demandrdquo While returns have been good over the last year future returns in the yellow metal will depend on the position of equity markets and the performance of other assets classes such as debt currencies and real estate

Gold is exhibiting all the classic signs of being in a structural bull market In the past year weve seen gold go up on fears of inflation then it rose on fears of deflation

The woes of the banking industry certainly appear to be aiding gold In a bizarre twist central bankers actually want the price of gold to rise because it would be an indication that attempts to stave off deflation are workingThe long-term story for gold however is as a re-monetization play as investors lose faith in fiat currencies

The Fed has flooded the market with newly-printed money Other countries are following suit Now that all of this money is printed it may be difficult to pull it back in This of course would lead to currency devaluations Some believe that the bottom in fiat currencies has begun and hard assets like gold and silver should benefitInvestors in Europe and north America went on an extraordinary shopping spree for gold coins and bars in the final quarter of 2008 snapping up 1485 tonnes a jump of 811 per cent compared with the same period in 2007 as the collapse of Lehman Brothers led to a massive increase in safe haven buying According to the World Gold Council this rush into physical gold by western investors pushed global retail investment up almost 400 per cent to 3042 tonnesGold is about 25 per cent above its peak from the last great bull market in the metal in 1980In yen terms gold is still barely half its 1980 level which might imply that there could be more gold demand to come from Japanese investors (referred to as Mrs Watanabe)

And in sterling terms gold is double its 1980 peak which implies either great worries about returning inflation in the UK or an overdone collapse of confidence in the pound sterling

The WGCs data confirmed earlier reports from traders about widespread shortages of coins and exceptional buying interest Investment inflows into gold exchange traded funds reached 947 tonnes in the fourth quarter up 18 per cent on the same period in 2007 but down from the record 150 tonnes of inflows seen in the third quarter of 2008

Rising prices for gold around the world mean that those currencies are depreciating Practically all currencies are depreciating relative to gold

The whole world of currencies is depreciating including the dollar But due to the liquidity provided by US debt during the financial crisis the dollar has appeared to rise in value within the overall currency bear market All currency ships are sinking the dollar ship is just not sinking as fast

For the better part of a century now the global gold trade has been dominated by the dollar

All over the world the prevailing gold price is a function of any currencys exchange rate with the dollar along with the dollar-price of gold

Back in July 2008 the dollar started rallying It wasnt for fundamental reasons but because the giant mortgage-backed bond industry was imploding and bond investors desperately sought the safety of US Treasuries

This kicked off the massive dollar panic rally in Q3 CY 2008 and the subsequent stock panic of Q4 CY 2008 accelerated it Until this anomalous rally erupted dollar gold remained strong in the high $800s and low $900s

At this dollar rallys apex on the very day the stock markets bottomed in late November the US Dollar Index had reached levels first seen in early 2004 when gold was near $400

Yet gold didnt even close under $700 in 2008s panic vastly stronger than the dollar alone would suggest it should be Once again this highlights the critical fact that the dollar is no longer golds primary driver even though it can still temporarily influence gold at times

In order to predict the future of gold prices one needs to keep an eye on gold lease rates a spike would be a good lead indicator that gold is about to punch higher as this would reflect a shortage of lendable bullion

Rising lease rates will cause gold to go into backwardation as holders of gold may not want to sell their gold forward under any circumstances a trend currently evidenced by the high physical premium being paid for gold coins

Rising lease rates prefigured the last big move in gold back in the spring of 2007 just as the two Bear Stearns hedge funds were blowing up Central banks feared counterparty risk for the first time in 20 years and substantially curtailed gold lending and sales

This led to a 40 per cent rally in gold from $700 to over $1000

Indians are collectively the worlds biggest gold investors so the rupee gold price is very important to the health of this global gold bull

Thanks to a rupee collapse during the stock panic to dismal levels underneath where its secular bull started in mid-2002 rupee gold has been very strong In fact it surged to new bull highs during the stock panic and ended 2008 near these levels During all this turmoil Indias deep cultural affinity for gold investment was strongly affirmed

The rupee gold price is an important one to watch thanks to Indias enormous influence in the global gold markets Even though tonnage of gold imports is suffering rupee expenditure levels are holding up well in India

Technical chartists say that gold could move into a parabolic fashion once the $1000 per ounce barrier is broken From there the speed of the move could accelerate sharply

For many structural reasons totally unrelated to the stock panic the fundamentals of gold remain awesomely bullish Its strong performance during the stock panic in most of the world is only icing on the cake that will drive additional investment demand

How high can gold ultimately go A Dow Jones Industrial Averagegold ratio of 21 would be a good sign the bull market in gold is getting well-advanced We saw this in 1932 and 1980

We are in a multi-year gold structural bull market that will eventually take the price to an integer multiple of where it is now

Within the broader and longer-term positive environment for gold we need to remember that short-term bursts of emotions might run to extremes This might be the case in the current situation Emotions have been running high Gold is seriously over-bought While investors need gold in their portfolio the current price situation might not be the best for buyers

Buy on price weakness not strength At the same time it is never advisable to sell in a structural bull market

28 INFLATION EXCHANGE RATE WITH DOLLAR SENSEX AND GOLD PRICES

Dollar is Negatively Co-related with Gold Correlation GoldDollar -70

For Inflation Hedge

The value of gold in terms of real goods and services that it canbuy has remained remarkably stable In contrast the purchasingpower of many currencies have varied over time

Gold has consistently reverted to its historic purchasing powerparity

Gold is an inflation hedge as proved by a 400-year study of thepurchasing power of gold in Britain between 1596 and 1997 Oneounce of gold would consistently purchase the same amount ofgoods and services as it would have done 400 years ago

GoldBeESGoldBeESTM

26 RECENT TREND IN GOLD MARKET IN INDIA

MUMBAI Gold is no longer glittering in India the biggest global market for the consumption and imports of the yellow metal Gold imports to the country has plunged to zero levels as no bank and trading houses imported any gold during the month of February

Gold analysts said that February 2009 is perhaps the only month in this decade where there has been no gold imports to India ldquoThis is a serious issue As gold market is all heated up and gold prices have skyrocketed imports of the yellow metal have practically stopped in Indiardquo said Akash Gupta a bullion trader in Mumbairsquos Zaveri Market

Buying of gold jewellery has fallen sharply in January leading to a slump in the yellow metalrsquos imports According to the Bombay Bullion Association there was more than 90 plunge in gold imports in January ldquoThe trend has worsened for February There was zero gold imports to India in Februaryrdquo the Association president Suresh Hundia In 2008 Indiarsquos gold imports dipped by 45 per cent to touch 450 tons

In the last eight years from 2000 gold imports to India every year have been between 400-800 tons But trade bodies have warned that gold imports this year could collapse to 100 tons if the current trend continues ldquoIt will not be a surprise if gold imports fall to an all-time low of 100 tons or below in 2009rdquo said bullion analyst Ashish Roy

High prices global economic meltdown and financial crunch among investors and bullion dealers led to low demand for gold in India where yellow metal is considered the best safe haven investment and people buy gold for weddings and other ceremonies

According to Hundia gold sales and demand are plunging to negligible levels because of high prices ldquoGold and jewellery sector is reeling under a crisis because of high prices and retrenchments across sectorsrdquo he said Gold prices which in December was from Rs 13505 for10 grams moved to an all-time high of Rs 16000 per ten grams last week

Analysts and India trade bodies have predicted that gold prices could zoom to Rs