gold derivatives the market impact

TRANSCRIPT

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 1/121

The market impact

Anthony Neuberger, London Business School

Report prepared for the World Gold Council, May 2001

GoldDerivatives:

W O R L D G O L D C O U N C I LO R L D G O L D C O U N CI L

GoldDerivatives:

LondonBusinessSchool

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 2/121

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 3/121

Gold Derivatives: The market impact

The views expressed in this study are those of the author and not necessarily theviews of the World Gold Council or the London Business School. While everycare has been taken, neither the World Gold Council nor the London BusinessSchool nor the author can guarantee the accuracy of any statement or representa-tions made.

Published by Centre for Public Policy Studies,World Gold Council, 45 Pall Mall, London SW1Y 5JG, UK.Tel +44(0)20 7930 5171 Fax + 44(0)20 7839 6561E-mail: [email protected] Website www.gold.org

Gold Derivati ves: The market impact by Anthony Neuberger, London BusinessSchool, advised by a Steering Group comprising Ian Cooper, Julian Franks andStephen Schaefer of London Business School.

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 4/121

Gold Derivatives: The market impact 3

CONTENTSForeword by Haruko Fukuda, Chief Executi ve, World Gold Council ..... ... ... ... ... ...7

About the author ........ ........ ......... ........ ......... ........ ......... ......... ........ ......... ......8

The steering group ......... ........ ......... ........ ......... ........ ......... ........ ......... ......... ...8

Executive summary .....................................................................................9

Chapter 1 The physical gold market ...........................................................151.1 Production...............................................................................15

1.2 Consumption...........................................................................211.3 Investment ...............................................................................231.4 Data Issues ..............................................................................28

Chapter 2 The paper market ......................................................................292.1 What makes gold special? .........................................................302.2 Gold derivative contracts ..........................................................322.3 The market ..............................................................................372.4 Downstream hedging ...............................................................402.5 Speculative traders....................................................................41

2.6 The banking sector...................................................................432.7 Producer hedging.....................................................................46

Chapter 3 The debate................................................................................533.1 The debate outlined .................................................................543.2 The impact of derivatives generally............................................563.3 What is special about gold ........................................................573.4 The simple consumption model ................................................583.5 Other effects of derivative markets.............................................60

Chapter 4 The empirical evidence..............................................................634.1 The impact of short-selling on the price of gold .........................634.2 The impact of hedging policy announcements...........................68

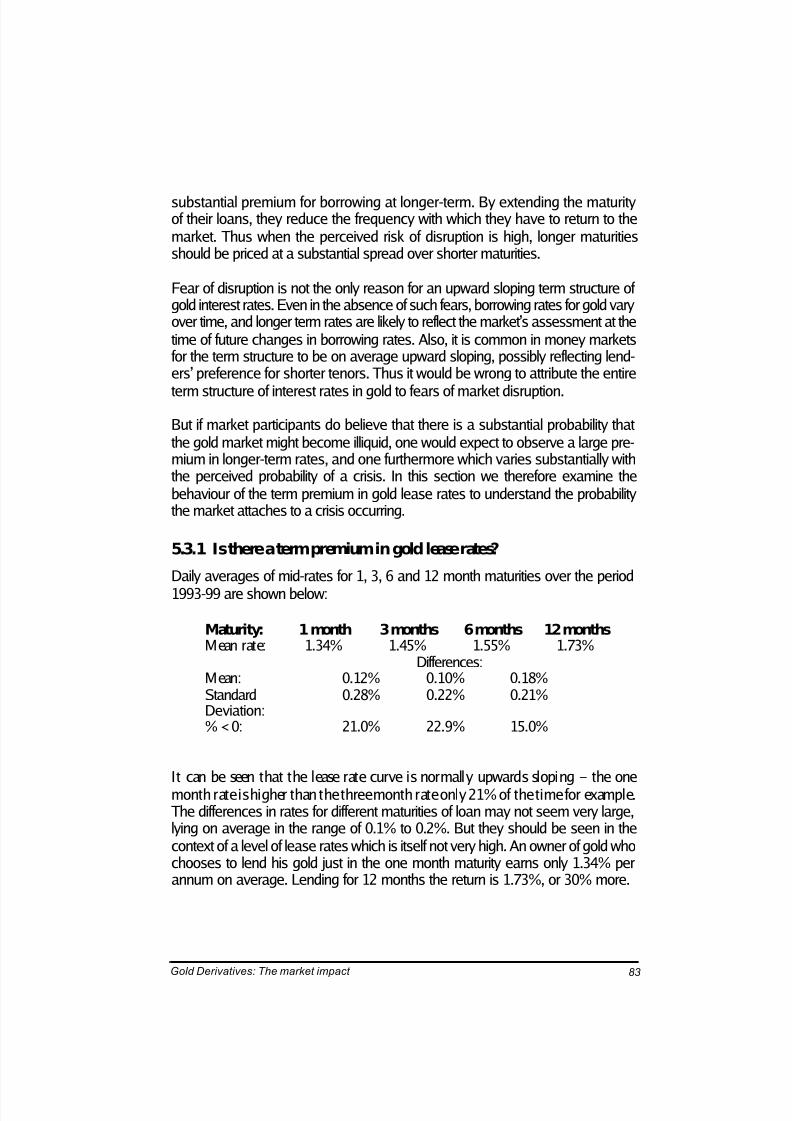

Chapter 5 The gold lending market and its stabil ity ...................................735.1 Scenario 1: A cutback in lending..............................................745.2 Scenario 2: A cutback in demand for borrowing........................805.3 The empirical evidenc from lease rates.......................................82

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 5/121

Gold Derivatives: The market impact 4

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 6/121

Gold Derivatives: The market impact 5

Appendices

Appendix 1

Overview ..............................................................................................87

1 The economic role of forward markets ..............................................88

2 Derivatives and market quali ty: theoretical considerations..................95

3 Derivatives and market quali ty: empirical evidence..........................102

4 Conclusions..................................................................................109

References ........................................................................................111

Appendix 2

A detailed analysis of producer hedge books....................................115

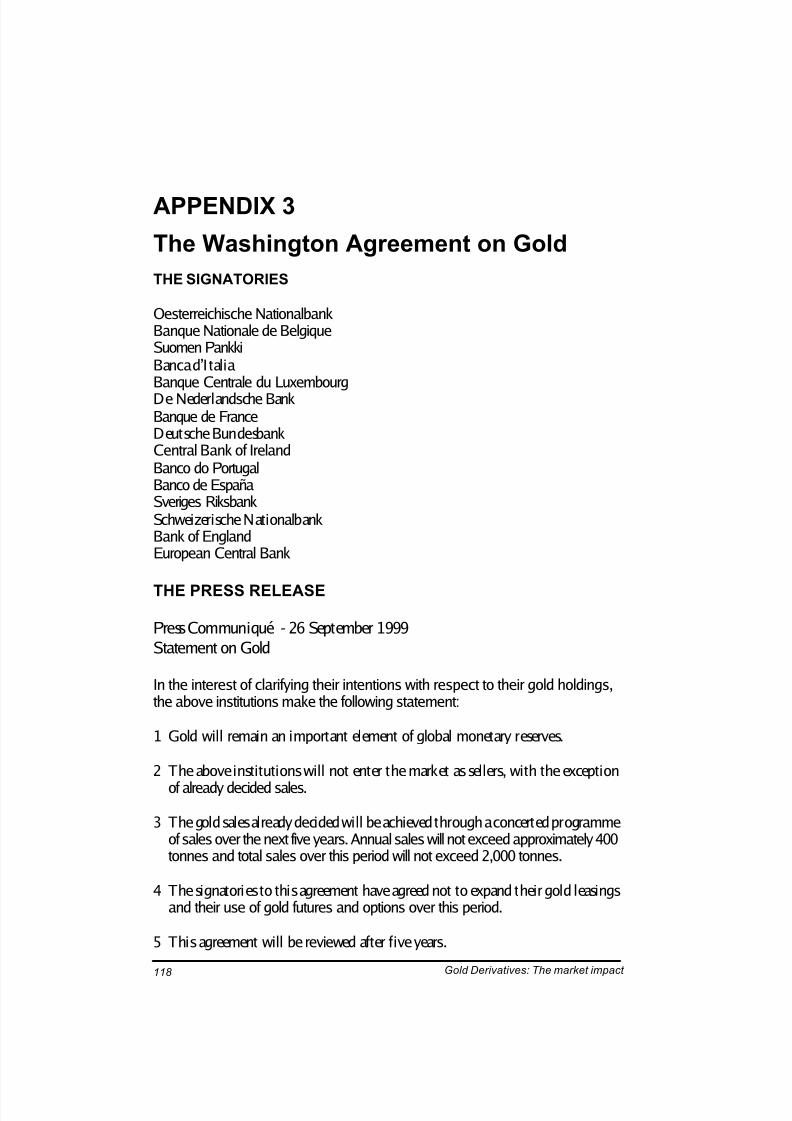

Appendix 3

The Washington Agreement on Gold .............................................118

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 7/121

Gold Derivatives: The market impact 6

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 8/121

Gold Derivatives: The market impact 7

FOREWORD

There has been much debate about the impact of the derivatives market on thespot market for gold. Some people attribute the decline in the dollar price of goldover the last decade to the rapid growth of the gold derivatives market. Othersclaim that the impact of derivatives has been largely beneficial for the gold mar-ket, improving liquidity and helping efficient risk management.

Despite the extent and often ferocity of this debate, there have been few system-atic studies of this important subject. To rectify this, the World Gold Council

asked Professor Anthony Neuberger, a leading expert on derivatives markets, andhis team from the London Business School, to analyse the arguments, present theevidence and reach conclusions on these issues.

This study forms the second part of a major research project on derivatives mar-kets sponsored by the World Gold Council. The first part, ‘Gold Derivatives: Themarket view’, by Jessica Cross was published in September 2000 and was widelyseen as the most comprehensive and detailed factual review of the market thus far.Professor Neuberger’s analysis draws heavily on Dr Cross’s empirical findings, inparticular her estimate of the size of the lending market.

The World Gold Council is grateful to the London Business School for the con-siderable care and effort that has gone into ‘Gold Derivatives: The market im-pact’. I do not believe it will answer all the questions or end all the disputes.Nevertheless I think that with this rigorously researched report Professor Neubergerand his colleagues have made an invaluable contribution to our understanding of how the market works, the impact derivatives have had so far and could have inthe future.

Haruko Fukuda

Chief Executive

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 9/121

Gold Derivatives: The market impact 8

About the author Anthony Neuberger is Associate Professor of Finance at London Business Schoolwhere he is also Associate Dean of the Masters in Finance programme (full-t ime).His published academic research includes work on hedging long-term commod-ity exposures using short-dated futures contracts, and the impact of trade disclo-sure requirements on market liquidity. Before joining the faculty at LBS in 1985he worked in the UK Civil Service, first in the Cabinet Office and latterly as aPrincipal in the Department of Energy.

The steering group

Ian Cooper is Professor of Finance at London Business School. He has publishedmany papers in the field of international finance, default risk in financial con-tracts, and corporate finance. He has held visiting appointments at the Universi-ties of Chicago and the Australian Graduate School of Management, and hasserved on the editorial boards of a number of academic and practitioner journals.

Julian Franks is Corporation of London Professor of Finance at London BusinessSchool where he has served as Director of the Institute of Finance and Account-ing, and Director of the MBA programme. He has held visiting appointments at

the Universities of North Carolina, Berkeley and UCLA. He has published widelyin the field of bankruptcy, corporate restructuring and corporate control, and hasserved on the editorial boards of many academic journals.

Stephen Schaefer is Tokai Bank Professor of Finance at London Business School,where he has served as Director of the Institute of Finance and Accounting andas Research Dean. He has held visiting appointments at the Universities of Bergamo,Chicago, Berkeley, British Columbia, Cape Town and Venezia, and has served onthe editorial board of numerous academic journals. He has published widely onthe term structure of interest rates, the pricing of derivatives, financial regulationand risk management.

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 10/121

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 11/121

Gold Derivatives: The market impact 10

When the derivative contract matures, the spot market hedge is removed, and thebank buys back the gold. Thus the effect of hedging by producers and fabricatorsis to bring forward or accelerate sales in the spot market. The volume of salesbrought forward is equal to the net short position of hedgers and speculators.

So long as the net short position is stable, with the initiation of new contractsbeing offset by the maturing of old contracts, the effect on the spot market isneutral. But over the decade of the 1990s the amount of hedging increased rap-idly, with much of the increase occurring in the second half of the period. The netshort position increased by a total of some 4,000 tonnes, or around 400 tonnes/

year on average. To put the point another way, to meet the demands of the deriva-tive markets, holders of gold increased their lending of gold to the market bysome 4,000 tonnes. The presence of this gold increased physical supply. Thevolume is significant, being equal to around 12% of non-investment demand forgold over the same period.

The impact of accelerated supply on price

The derivatives market does give rise to accelerated supply. The key issue is whatimpact this accelerated supply has on the spot price. Physical demand and supplymust match each period. New mined supply is inelastic in the short term. Theimpact of accelerated supply depends entirely on how demand respondsto price.

One view is that demand each period responds to the price level in the way it doeswith most consumable commodities. The incremental supply depresses the spotprice sufficiently so as to create the additional demand which will absorb it. Theprice impact can be computed using a price elasticity of demand in the conven-tional way.

Analysis on these lines suggests that the spot price of gold may have been de-pressed on average by something of the order of 10-15% below the level which itwould otherwise have attained over the decade. This model goes on to predictthat if and when the size of the aggregate short position stabilises, the price of gold will revert to the level it would have reached in the absence of short selling,

since the net addition to supply will disappear. This physical supply model of thegold market also suggests that central bank net selling, which added about 3,000tonnes to net supply over the decade, and the increased level of gold production,which was responsible for another 2,000 tonnes, must also have played a signifi-cant role alongside the 4,000 tonnes from the derivatives market.

However, there are reasons, both theoretical and empirical, for believing that thismodel greatly overstates the impact of the accelerated supply. I t ignores the factthat gold is held as a store of value and an investment as well as bought as a

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 12/121

Gold Derivatives: The market impact 11

consumption good. The net demand for gold is the result of the decisions of many individuals to increase or reduce their holdings of gold. From this perspec-tive, the accelerated supply of 4,000 tonnes should be compared with the stock of gold which exists (estimated at some 140,000 tonnes) rather than just with newlymined gold. Net investment demand for gold, like that for any other investmentgood, will be sensitive, not so much to the level of the gold price, but to smallvariations in the expected rate of return from holding it.

If accelerated supply does depress the spot price, and if the depression is tempo-rary because the size of paper short positions is not expected to increase indefi-nitely, then the market should expect the price to return in due course to the

levels it would have had in the absence of a derivatives market. Thus investorsshould see the temporary depression in the gold price as a buying opportunity.This increased investment demand would offset at least in part the acceleratedsupply from the paper market.

The theory suggests the impact of accelerated supply on the price should belimited. The empirical evidence broadly supports this position. We find nocorrelation between quarterly changes in the paper short position (as measuredby the aggregate short position of gold producers) and changes in the spotprice of gold. We looked to see whether the gold price rises when a goldproducer announces a reduction in hedging and falls when an increase is an-nounced. While such an effect is visible in the data, it is only marginallysignificant statistically.

While the evidence both theoretical and empirical is not conclusive, it does sug-gest that the accelerated supply due to increased forward selling in the lastdecade probably did depress the gold price, but the magnitude of the effect ismuch too small to explain all the real decline in the gold price seen over the lastdecade. The lack of transparency in the gold market may have led to an exagger-ated sense of the role played by derivatives in the decline. Market part icipantsmay have interpreted transactions generated by hedging demands as one com-ponent of a very much larger speculative order flow, and this may have had animpact on the gold price.

The wider impact of the derivatives market

There are a number of other ways in which the derivatives market has an impacton the spot market apart from through accelerated supply. The existence of thederivatives market is likely to affect the behaviour of those who use it, and there-fore indirectly affect the spot market. These indirect effects of derivative marketstend to increase both demand and supply for gold. Their impact on the spot priceis ambiguous.

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 13/121

Gold Derivatives: The market impact 12

Owners of gold can use the derivatives market to get extra income from theirholdings. Derivatives greatly widen the range of strategies available, particularlyto large holders, for managing their gold holdings. By increasing flexibility andreturn, they make gold a more attractive asset to hold.

The ability to borrow gold easily and at low rates is of benefit to all those involvedin downstream activities (refiners, fabricators and distributors). By reducing thecosts and risks associated with holding of large stocks, it allows the widespreaddistribution and availabil ity of gold and thus facilitates the marketing of gold tocustomers.

Derivatives also reduce the cost of capital for producers, and so tend to encourageproduction. Project finance for new mines is often conditional on output beingsold forward. There is evidence that producers who have sold their productionforward may be slower to cut production as spot prices fall.

The stability of the derivatives market and its impact on the spot market

The growth of the derivatives market has been made possible by the existence of large stocks of gold, largely in the official sector. For some official holders physicalpossession of their gold is important but for others the convenience yield onholding gold is small, and they are prepared to lend gold at very low lease rates,similarly to the way they might lend their bonds or other financial assets. This

ready supply of liquidity has led to lease rates for gold which are low and stablerelative to other commodities. Without that, there would be no long-term for-ward market. Forward prices and spot prices would decouple. Producers wouldbe unable to hedge the price risk on future production except in the short term.Fabricators would not be able to predict the cost of holding inventory more thana few months ahead. The amount of hedging would fall. The derivatives market ingold would resemble much more closely that in other commodities.

The future stability of the derivatives market depends on the continuing readi-ness of the official sector to lend its gold. Most lenders lend their gold for rela-tively short periods, typically three months at a time, though in general these

loans are then rolled over. It takes time for lending policies to be changed, and thesupply of lending at least in the short term is not very sensitive to lease rates.These factors make the lending market vulnerable to shocks, particularly if lend-ers are close to their current lending limits.

For example, if a number of central banks decided to withdraw their gold fromthe market, it would cause a serious squeeze. Lease rates and spot prices wouldrise sharply as borrowers tried to repay their loans. A large and sustained rise inlease rates would cause substantial losses to producers who have sold gold forwardand retained the lease rate risk, to fabricators and distributors, and to commercial

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 14/121

Gold Derivatives: The market impact 13

banks who are active in the market. The rise in lease rates and spot prices wouldattract holders of physical gold to lend or sell their gold into the market.

Some indication of the possible magnitudes can be gained from the behaviour of lease rates following the Washington Agreement in September 1999. This wascaused not by a cut in lending but only by a ceiling on future lending.

The shape of the term structure of gold lease rates historically suggests that themarket has perceived little risk of a crisis in the lending market. Had the per-ceived risk been substantial, this should have manifested itself through a spreador security premium between short- and long-term lending rates. The evidence

suggests that term premia in the gold lending market have been no higher thanthey are in the (US dollar) money market.

It is indeed hard to visualise circumstances under which several lenders decide towithdraw their gold from the market simultaneously. Credit risk is not a majorconcern since most of the borrowers are major commercial banks for whom gold isonly a small part of their portfolio. It is unlikely that many holders of gold willdecide to sell their gold at the same time, and seek to recover their lent gold forthat reason. They also have an interest in acting in a way which maintains anorderly market.

Concerns have also been expressed about the consequences for the derivativesmarket of a sudden reduction in the size of producer hedging books. However,there seems little reason for a concerted withdrawal from hedging, and indeed itwould be very costly for individual producers to cut back their hedge book at thesame time as others are doing it. So while it is possible that a sharp rise in the goldprice could lead to the sudden liquidation of short positions, it is unlikely to beon a larger scale than we have already seen.

The size of the derivatives market in future

There are reasons for believing that the rapid expansion in the size of the goldderivatives market is likely to slacken or indeed reverse. The Cross report esti-

mates that, given current policies, the scope for additional official sector lendingis no more than 1,000 tonnes. The private sector could become a major source of lending, but that is likely to require a substantial increase in the level of lease rates.

Underlying hedging demand by producers is likely to slacken given the decline innew mining developments. There is no reason why hedging demand downstreamshould grow other than broadly in line with any increase in demand. The maincontingent factors which will determine the size of hedging demand in futurewill therefore be the level and volatility of lease rates, and expectations aboutfuture returns on holding gold.

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 15/121

Gold Derivatives: The market impact 14

The level and volatility of lease rates is likely to have a significant impact in de-mand for hedging. Higher lease rates increase the cost of holding inventory, andtherefore tend to depress downstream demand for hedging. Greater volatility inlease rates reduces the effectiveness of long-term hedges by making them morerisky, and therefore reduces producers’ willingness to sell their production forward.

Conclusions

The main conclusions of this study are that:

1) the derivatives market has played an important role in reducing the cost of

capital for producers, in helping finance large downstream inventories, and ingiving holders of gold the possibility of earning income on their gold holdingsand managing them more flexibly;

2) the rapid growth of the derivatives market over the last decade has acceleratedthe physical supply of gold, and probably led to the gold price being some-what lower than it would otherwise have been, but the magnitude of the effectis much too small to explain all the real decline in the gold price seen over thelast decade;

3) the supply of liquidity from increased central bank lending has been indispen-sable to the growth of the derivatives market. The constraints on lending underthe Washington Agreement, together with weakness in demand for borrowinggold, provide reasons for believing that the period of rapid growth in the size of the derivatives market is now over. If this is indeed the case, then derivativeswill not provide accelerated supply to the spot market in the future, and what-ever impact this has had on the gold price in the past should be reversed.

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 16/121

Gold Derivatives: The market impact 15

CHAPTER 1 THE PHYSICAL GOLDMARKET

This chapter describes the various elements of the physical market and their characteris-

ti cs. T he main points made are:

· most of the gold which has ever been mined has been accumulated rather than con-

sumed; much of i t could return to the market again. The level of producti on, though

it has increased substantially over the last century, at 2,500 tonnes/year, i s small

compared wi th the stock of gold already produced (estimated at 140,000 tonnes).

Producti on does respond to the level of the gold price, but the full effects take several

years to work through (1.1).· demand for industrial and dental gold accounts for 400 tonnes/year, or around

17% of producti on. The great bulk of the demand for gold is for jewellery. Gold

jewellery is often an investment good, or a store of value, as well as a consumption

good. Demand is therefore likely to depend on expectati ons about future returns from

holding gold as well as on the current level of the price. I ncome, cultural and social

and other factors are also important determinants (1.2).

· pri vate investment holdings of gold are substantial (around 25,000 tonnes). Invest-

ment demand i s sensitive to economic conditions in the M iddle and Far East where it

is most widely held, and to confi dence in the fi nancial system. Net investment de-

mand i s likely to be much more sensitive to expectati ons about future returns than to

the price level. Official sector holdings (35,000 tonnes) have been fairly stable over

the last twenty years, though worries about the possibi li ty of future sales have been a

major influence on the market in the second half of the 1990s (1.3).

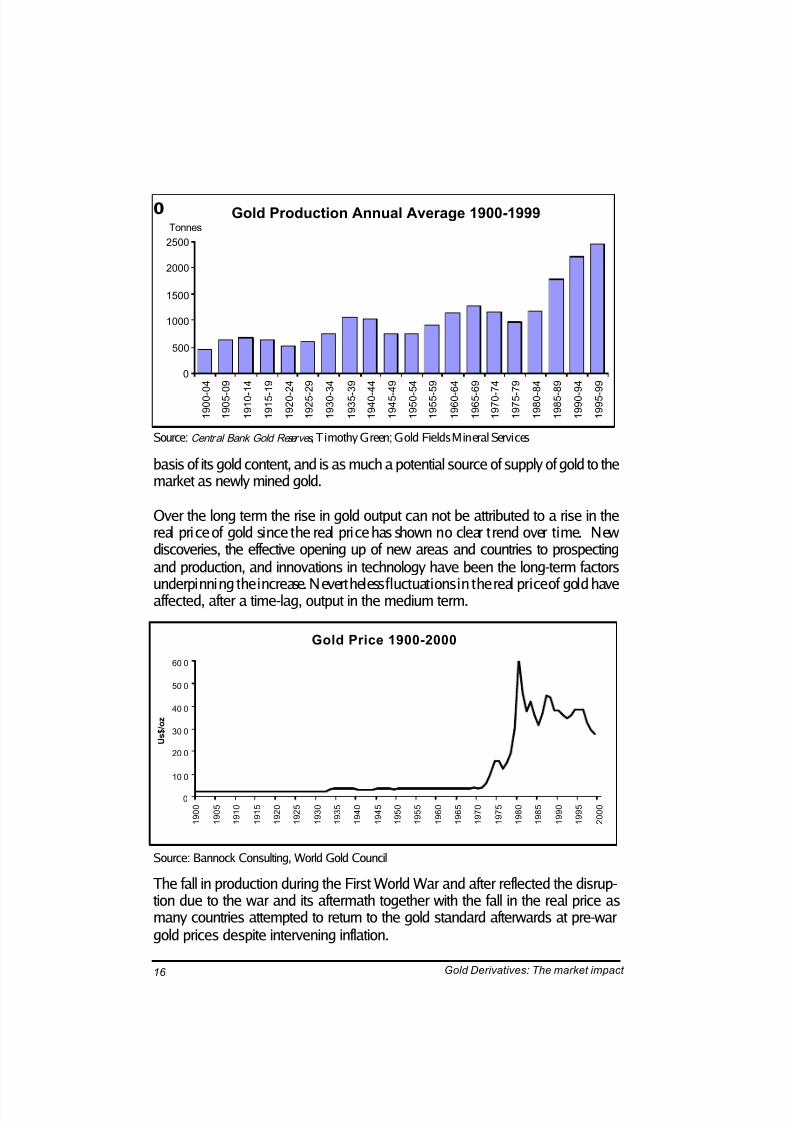

1.1 ProductionGold has been mined since time immemorial, but levels of production have in-creased rapidly since the mid-1800s. At the beginning of the twentieth century,total production amounted to 450 tonnes per year1 . By the end of it, productionexceeded 2,500 tonnes/year2 . With this growth in production, more than a thirdof all the gold that has ever been mined has been extracted in the last thirty

years3 .

The comparison of production levels with the total quantity ever produced is

relevant to gold in a way that is quite unlike other commodities. M ost of the gold

which has been produced has not been permanently consumed; much of it could

at some time come back to the market. Much of it will be traded largely on the

1 Central Bank Gold Reserves: An hi stori cal perspective since 1845 by Timothy Green, World Gold Council,Research Study No. 23, London 1999.2 Gold Survey 2000, Gold Fields Mineral Services Ltd (GFMS), London, 2000.3 Gold Survey 2000, GFMS, London, 2000.

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 17/121

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 18/121

Gold Derivatives: The market impact 17

The Real Price of Gold 1900-2000

in 1900 $

0.00

10.00

20.00

30.00

40.00

50.00

60.00

1 9 0 0

1 9 0 7

1 9 1 4

1 9 2 1

1 9 2 8

1 9 3 5

1 9 4 2

1 9 4 9

1 9 5 6

1 9 6 3

1 9 7 0

1 9 7 7

1 9 8 4

1 9 9 1

1 9 9 8

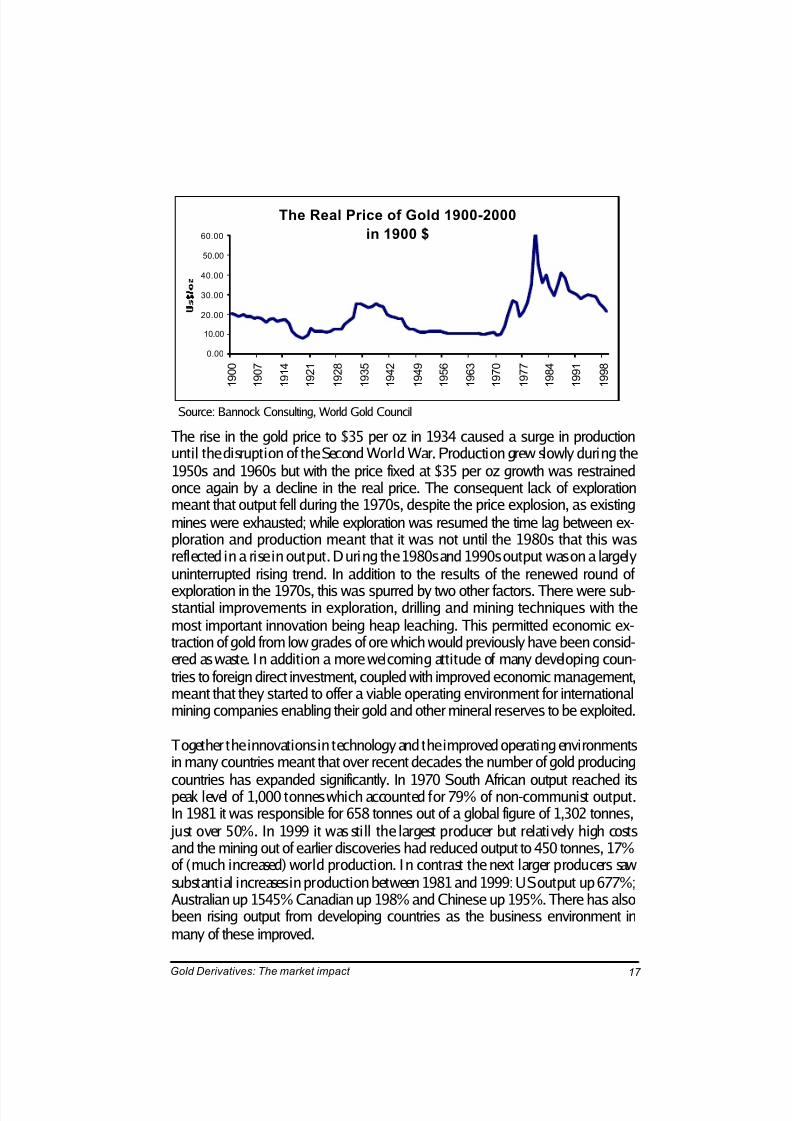

The rise in the gold price to $35 per oz in 1934 caused a surge in productionuntil the disruption of the Second World War. Production grew slowly during the1950s and 1960s but with the price fixed at $35 per oz growth was restrainedonce again by a decline in the real price. The consequent lack of explorationmeant that output fell during the 1970s, despite the price explosion, as existingmines were exhausted; while exploration was resumed the time lag between ex-ploration and production meant that it was not until the 1980s that this wasreflected in a rise in output. During the 1980s and 1990s output was on a largelyuninterrupted rising trend. In addition to the results of the renewed round of

exploration in the 1970s, this was spurred by two other factors. There were sub-stantial improvements in exploration, drilling and mining techniques with themost important innovation being heap leaching. This permitted economic ex-traction of gold from low grades of ore which would previously have been consid-ered as waste. In addition a more welcoming attitude of many developing coun-tries to foreign direct investment, coupled with improved economic management,meant that they started to offer a viable operating environment for internationalmining companies enabling their gold and other mineral reserves to be exploited.

Together the innovations in technology and the improved operating environmentsin many countries meant that over recent decades the number of gold producing

countries has expanded significantly. In 1970 South African output reached itspeak level of 1,000 tonnes which accounted for 79% of non-communist output.In 1981 it was responsible for 658 tonnes out of a global figure of 1,302 tonnes,

just over 50%. In 1999 it was sti ll the largest producer but relatively high costsand the mining out of earlier discoveries had reduced output to 450 tonnes, 17%of (much increased) world production. In contrast the next larger producers sawsubstantial increases in production between 1981 and 1999: US output up 677%;Australian up 1545% Canadian up 198% and Chinese up 195%. There has alsobeen rising output from developing countries as the business environment inmany of these improved.

Source: Bannock Consulting, World Gold Council

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 19/121

Gold Derivatives: The market impact 18

Breakdown of Production in 1999

17%

13%

12%

6%6%6%

5%

5%

10%

20%South Africa

USA

Australia

CanadaChinaIndonesia

Russia

Peru

Other Latin America

Rest of World

Total Production =2,571 Tonnes

Breakdown of Production in 1968

13%

6%

3%

3%

2% 6%

67%South Africa

USSR

Cananda

USA

Asia

Latin America Rest of World

Total Production =1,450 Tonnes

The rise in output in the 1980s and 1990s has, however, halted with output in2000 expected to be close to, or even slightly below, that in 1999. In part this isdue to the increase in output generated from the exploration of the 1970s and thetechnological improvements coming to a natural end. But the more serious factoris the effect of the fall in the real price of gold in the 1990s, a fall which wasaccelerated (at least in dollar terms) from the second half of 1996 when the nomi-nal price plunged as well. This has restricted output and resulted in a sharpdecline in exploration.

Source: Gold Fields Mineral Services

Source: Gold Fields Mineral Services

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 20/121

Gold Derivatives: The market impact 19

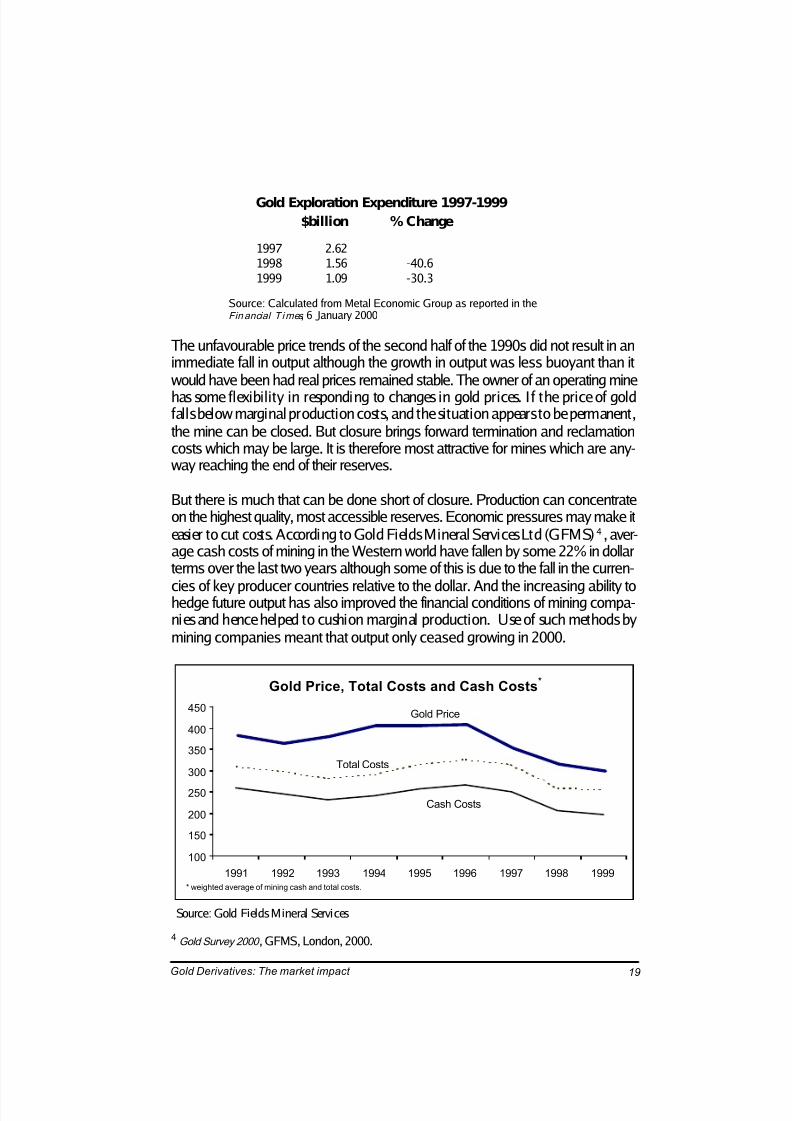

Gold Exploration Expenditure 1997-1999

$billion % Change

1997 2.621998 1.56 -40.61999 1.09 -30.3

Source: Calculated from Metal Economic Group as reported in theFinancial T imes , 6 January 2000

The unfavourable price trends of the second half of the 1990s did not result in animmediate fall in output although the growth in output was less buoyant than itwould have been had real prices remained stable. The owner of an operating mine

has some flexibility in responding to changes in gold prices. If the price of goldfalls below marginal production costs, and the situation appears to be permanent,the mine can be closed. But closure brings forward termination and reclamationcosts which may be large. It is therefore most attractive for mines which are any-way reaching the end of their reserves.

But there is much that can be done short of closure. Production can concentrateon the highest quality, most accessible reserves. Economic pressures may make iteasier to cut costs. According to Gold Fields Mineral Services Ltd (GFMS)4 , aver-age cash costs of mining in the Western world have fallen by some 22% in dollarterms over the last two years although some of this is due to the fall in the curren-

cies of key producer countries relative to the dollar. And the increasing ability tohedge future output has also improved the financial conditions of mining compa-nies and hence helped to cushion marginal production. Use of such methods bymining companies meant that output only ceased growing in 2000.

4 Gold Survey 2000 , GFMS, London, 2000.

Gold Price, Total Costs and Cash Costs*

100

150

200

250

300

350

400

450

1991 1992 1993 1994 1995 1996 1997 1998 1999

Gold Price

Total Costs

Cash Costs

* weighted average of mining cash and total costs.

Source: Gold Fields Mineral Services

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 21/121

Gold Derivatives: The market impact 20

Thus while output responds to price changes it does so only after a number of years. The unfavourable price trends of the 1990s, and in particular of the lastfour years of the decade, are only now starting to cause a fall in output. In theother direction, when exploration has been sharply cut it takes at least 7-8 yearsfor a rise in price to generate not just exploration but the subsequent exploitationof the results, let alone sufficient new output to compensate in addition for theexhaustion of existing mines.

Gold is found in a variety of geological formations and, to varying degrees, in allcontinents. It is at times found in conjunction with other exploitable metals,notably copper. Substantial quantities of gold can even be found in the oceans

although not, at the moment, economically exploitable. Mining companies’gold reserves below ground – which are defined as gold deposits economicallyexploitable at current prices and with current technology – are to a large de-gree, therefore, a function of price. While comprehensive data are not available,such reserves are known to have fallen in recent years due to the fall in price andthe cutback in exploration.

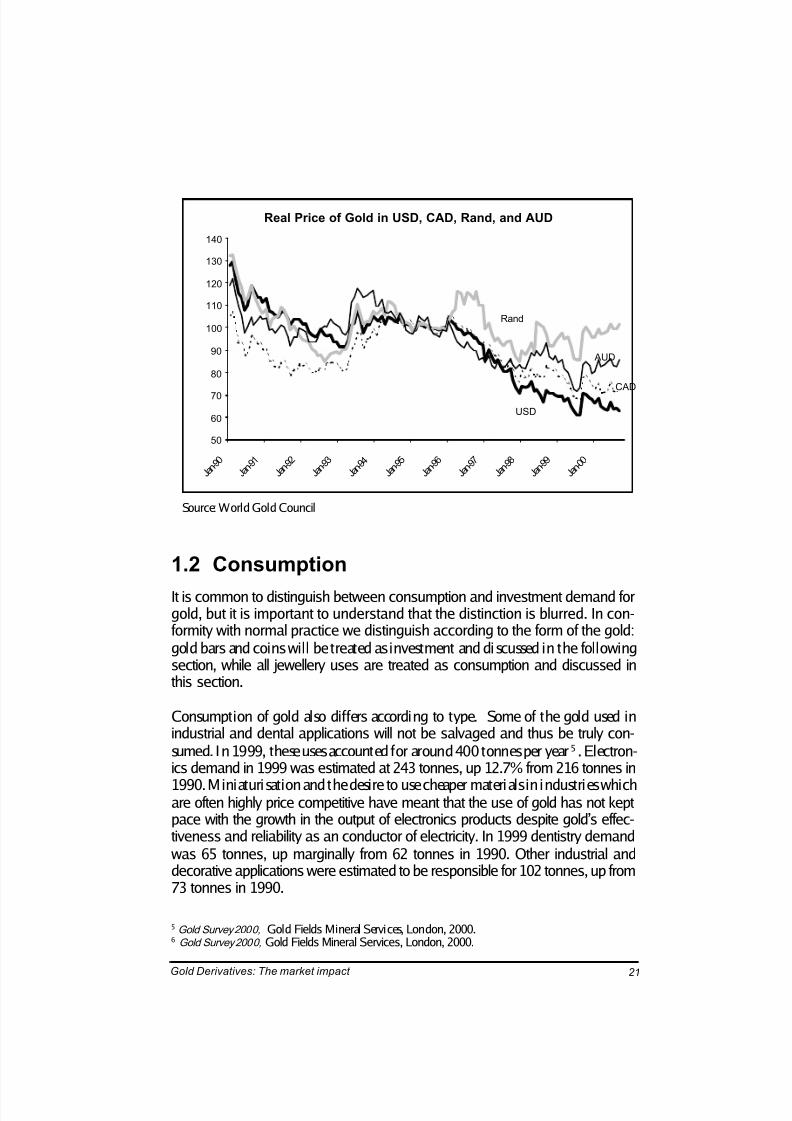

Throughout this section – and necessarily through most of this report – theanalysis has concentrated on the dollar price. While it is convenient to describethe price of gold in nominal or real US dollars, this is not necessarily the appro-priate measure for producers and consumers outside the US. With the very sub-stantial changes in real exchange rates that have been experienced over the last fewyears, the real price of gold as seen by a South African miner, or an Indian buyerof jewellery, may look very different. Indeed the recent fall in the dollar price of gold has been mitigated in a number of producer countries by the depreciation of a national currency against the dollar halting or limiting the decline in the na-tional currency gold price. However the real price of gold has fallen since 1990 inall the four main producer countries although the fall occurred at different times.In South Africa the real price fell in the early 1990s but has fluctuated around afairly stable level since. I n Australia the real price fell at the beginning of thedecade, recovered in 1993, then fell until September 1999 after which therehas been a very l imited recovery. In Canada, the real price fell at the start of the decade, recovered partly in 1994, then has been on a downward trend

since late 1996.

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 22/121

Gold Derivatives: The market impact 21

Source: World Gold Council

1.2 Consumption

It is common to distinguish between consumption and investment demand forgold, but it is important to understand that the distinction is blurred. In con-formity with normal practice we distinguish according to the form of the gold:gold bars and coins will be treated as investment and discussed in the followingsection, while all jewellery uses are treated as consumption and discussed inthis section.

Consumption of gold also differs according to type. Some of the gold used inindustrial and dental applications will not be salvaged and thus be truly con-sumed. In 1999, these uses accounted for around 400 tonnes per year5 . Electron-ics demand in 1999 was estimated at 243 tonnes, up 12.7% from 216 tonnes in

1990. Miniaturisation and the desire to use cheaper materials in industries whichare often highly price competitive have meant that the use of gold has not keptpace with the growth in the output of electronics products despite gold’s effec-tiveness and reliability as an conductor of electricity. In 1999 dentistry demandwas 65 tonnes, up marginally from 62 tonnes in 1990. Other industrial anddecorative applications were estimated to be responsible for 102 tonnes, up from73 tonnes in 1990.

5 Gold Survey 2000, Gold Fields Mineral Services, London, 2000.6 Gold Survey 2000, Gold Fields Mineral Services, London, 2000.

Real Price of Gold in USD, CAD, Rand, and AUD

50

60

70

80

90

100

110

120

130

140

J a n - 9 0

J a n - 9 1

J a n - 9 2

J a n - 9 3

J a n - 9 4

J a n - 9 5

J a n - 9 6

J a n - 9 7

J a n - 9 8

J a n - 9 9

J a n - 0 0

Rand

AUD

CAD

USD

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 23/121

Gold Derivatives: The market impact 22

Of the approximately 140,000 tonnes of gold which has been produced it isestimated that around 67,000 tonnes is in the form of jewellery6 . However, theterm jewellery covers a wide range of products with different characteristics vary-ing from market to market. In Asia and the Middle East much gold jewellery ishigh carat with a low mark-up. Such jewellery can readily be converted back intogold. In western developed markets gold jewellery is normally lower carat with amuch higher mark-up to cover the cost of design and distribution. Such items areless readily convertible back into pure gold.

Distribution of Global Above-Ground Gold (Tonnes)

Jewellery

(67,300)

Official Holdings*

(30,500)

Private

Investment

(25,200)

Other Fabrication

(15,700)

Unaccounted

(1,300)

Above-ground Stocks,

end-1999 = 140,000

* Excluding lent gold

Source: Gold Fields Mineral Services

While jewellery in western developed countries is primari ly bought purely asadornment, the high carat jewellery of Asia and the Middle East frequently has adual purpose and is considered also as a means of saving and a store of wealth.While gold is bought by all sections of society, this function of gold is particularlyimportant for the poorer and rural populations, who often do not have access to,or trust in, bank accounts and more sophisticated financial instruments; or whomay wish to save in a medium other than their national currency. It is also par-ticularly important to women in a number of cultures. Gold jewellery is consid-ered the woman’s personal property and therefore is her safeguard against divorceor other misfortunes. Gold giving is often therefore associated with weddings.

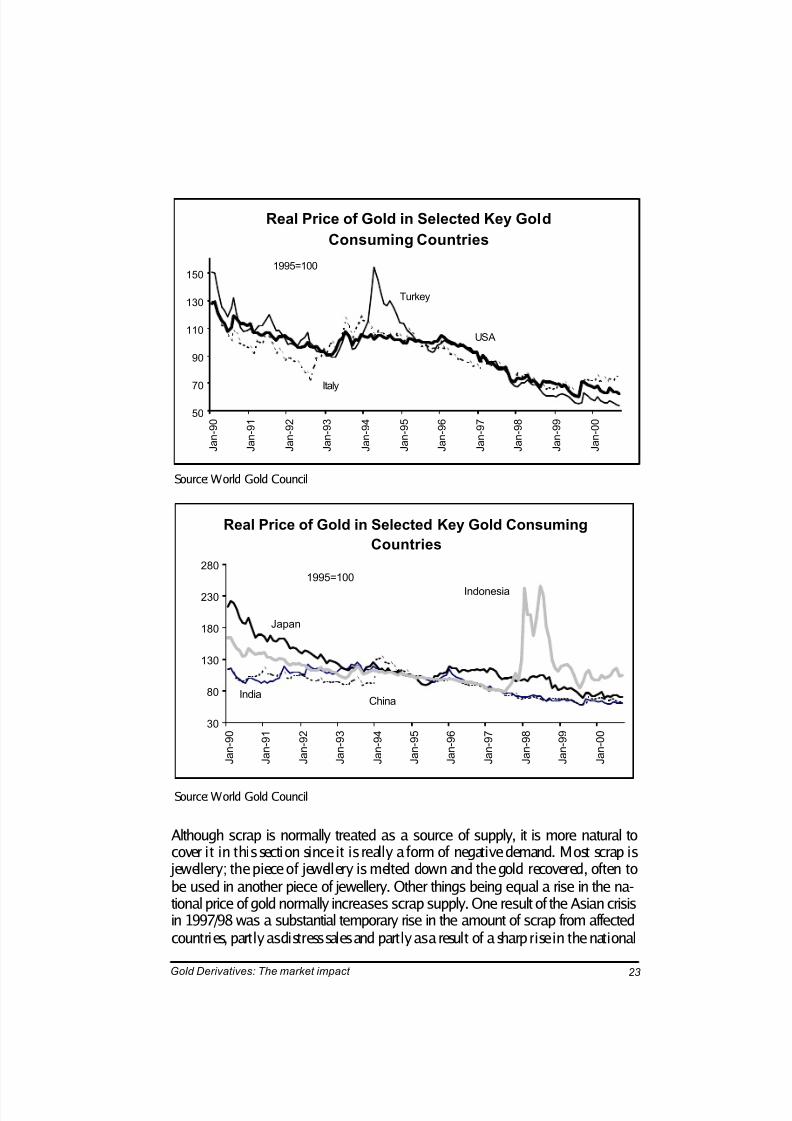

Demand for such gold is affected in the short term by price movements but lessin the long term; indeed the savings characteristic of gold means that a long-termrising trend in the price against the national currency wil l not deter purchase. Aswell as price and social and cultural factors gold demand is normally elastic withrespect to incomes, rising as incomes increase (indeed studies suggest gold ismore income than price elastic). As in the case of production, movements in thereal price of gold have varied substantially between consuming countries. Chinaand a number of key consuming countries in the Middle East have exchange ratesfixed in effect to the dollar, with occasional devaluations.

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 24/121

Gold Derivatives: The market impact 23

Source: World Gold Council

Real Price of Gold in Selected Key Gold Consuming

Countries

30

80

130

180

230

280

J a n - 9 0

J a n - 9 1

J a n - 9 2

J a n - 9 3

J a n - 9 4

J a n - 9 5

J a n - 9 6

J a n - 9 7

J a n - 9 8

J a n - 9 9

J a n - 0 0

Indonesia

Japan

ChinaIndia

1995=100

Source: World Gold Council

Real Price of Gold in Selected Key Gold

Consuming Countries

50

70

90

110

130

150

J a n - 9 0

J a n - 9 1

J a n - 9 2

J a n - 9 3

J a n - 9 4

J a n - 9 5

J a n - 9 6

J a n - 9 7

J a n - 9 8

J a n - 9 9

J a n - 0 0

Turkey

USA

Italy

1995=100

Although scrap is normally treated as a source of supply, it is more natural tocover it in this section since it is really a form of negative demand. Most scrap is

jewellery; the piece of jewellery is melted down and the gold recovered, often tobe used in another piece of jewellery. Other things being equal a rise in the na-tional price of gold normally increases scrap supply. One result of the Asian crisisin 1997/98 was a substantial temporary rise in the amount of scrap from affectedcountries, partly as distress sales and partly as a result of a sharp rise in the national

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 25/121

Gold Derivatives: The market impact 24

price of gold following substantial currency depreciation. The most spectacu-lar increase was due to the national gold collection campaign in South Koreawhere citizens were encouraged to turn in their gold in exchange for nationalcurrency bonds.

1.3 Investment

Investment demand can be split broadly into two, private and public-sectorholdings.

Private sector holdings come in the form of bars and coins. Unlike jewellery, whichis held at least in part for decorative purposes, these holdings are purely a store of value, although in the Middle East coins and small bars are often incorporatedinto jewellery. According to GFMS, private investment holdings amount to justunder 25,000 tonnes, a figure that has been growing slowly over t ime. Moreinterestingly the location of the bulk of these holdings is believed to have shifted.Whereas thirty years ago, a substantial portion of this was held by Westerninvestors, the overwhelming majority is now thought to be held in other partsof the world.

Reasons for holding physical gold vary widely. In markets with poorly developedfinancial systems, inaccessible or insecure banks, or where trust in the govern-ment is low, gold is attractive as a store of value which is portable, anonymous andreadily marketable anywhere. In countries with a stable political and financialsystem, the prime attraction of gold is as an investment which has very low, ornegative, correlation with other assets, and which may hold or increase its value if for some reason investors flee from purely financial assets like bonds and equities.

If gold is held primari ly as an investment asset, it does not need to be held inphysical form. The investor could hold gold-linked paper assets or could lend outthe physical gold on the market. While proper discussion of the gold lendingmarket is reserved to the second chapter of the report, suffice to observe here that

an investor who wants exposure to gold, particularly if his position is more than,say, 10,000 ounces, will normally be able to achieve an increase in return of perhaps 1% by lending out his gold over the return he would gain by holdingphysical gold. In addition he wil l save on the storage costs.

Investors who hold their gold with a bank in unallocated form (where they have aclaim on the bank for a fixed quantity of gold, but they have no claim to specificbars) allow the bank to lend out ‘their’ gold. The bank normally retains anyinterest on lending the gold, but passes on some of the benefit to its customers byremitting storage charges.

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 26/121

Gold Derivatives: The market impact 25

Total Official Sector Gold Holdings, 1970-1999

(Tonnes)

Institutions

Western Europe

North America

Developing

countries

Other developed

countries

0

5000

10000

15000

20000

25000

30000

35000

40000

1 9 7 0

1 9 7 2

1 9 7 4

1 9 7 6

1 9 7 8

1 9 8 0

1 9 8 2

1 9 8 4

1 9 8 6

1 9 8 8

1 9 9 0

1 9 9 2

1 9 9 4

1 9 9 6

1 9 9 8

2 0 0 0

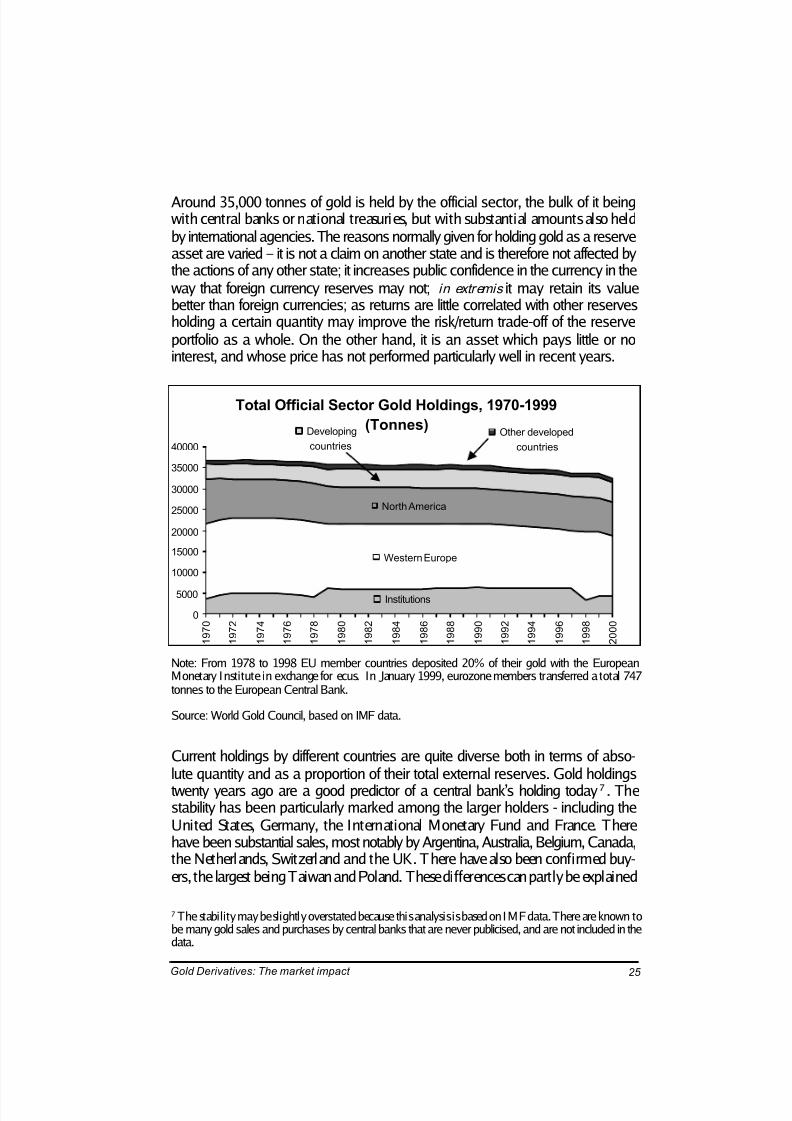

Around 35,000 tonnes of gold is held by the official sector, the bulk of it beingwith central banks or national treasuries, but with substantial amounts also heldby international agencies. The reasons normally given for holding gold as a reserveasset are varied – it is not a claim on another state and is therefore not affected bythe actions of any other state; it increases public confidence in the currency in theway that foreign currency reserves may not; in extremis it may retain its valuebetter than foreign currencies; as returns are little correlated with other reservesholding a certain quantity may improve the risk/return trade-off of the reserveportfolio as a whole. On the other hand, it is an asset which pays little or nointerest, and whose price has not performed particularly well in recent years.

Note: From 1978 to 1998 EU member countries deposited 20% of their gold with the EuropeanMonetary Institute in exchange for ecus. In January 1999, eurozone members transferred a total 747tonnes to the European Central Bank.

Source: World Gold Council, based on IMF data.

Current holdings by different countries are quite diverse both in terms of abso-lute quantity and as a proportion of their total external reserves. Gold holdingstwenty years ago are a good predictor of a central bank’s holding today7 . Thestability has been particularly marked among the larger holders - including theUnited States, Germany, the International Monetary Fund and France. Therehave been substantial sales, most notably by Argentina, Australia, Belgium, Canada,the Netherlands, Switzerland and the UK. There have also been confirmed buy-ers, the largest being Taiwan and Poland. These differences can partly be explained

7 The stability may be slightly overstated because this analysis is based on IMF data. There are known tobe many gold sales and purchases by central banks that are never publicised, and are not included in thedata.

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 27/121

Gold Derivatives: The market impact 26

by the way in which reserves are viewed nationally, and the way in which deci-sions on reserve policy are taken, and also by the very large size of reserves relativeto the underlying flow of production and consumption.

Central Bank Gold Holdings, 1978 and 1998

1

10

100

1,000

10,000

1 10 100 1,000 10,000

1978 tonnes

1998 tonnes

Dots below he linerepresent countries whosereserves fell between 1978

and 1998

Dots above the line

represent countries whose

reserves rose between 1978

and 1998

(Logarithmic Scale)

Source: IMF; World Gold Council calculations

Given the size of official reserves relative to consumption levels, the possibility of changes in policy have had a substantial impact on the gold price. Fears of sub-stantial official sector sales are thought to be one of the main factors behind thefall in the gold price since late 1996 – fears given credence by a small numberof substantial sales. In 1999 the UK gold sales together with the possibility of further gold sales by other parts of the official sector were thought to be majorfactors behind the extreme weakness of the gold price, which fell to $252/oz inAugust 1999.

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 28/121

Gold Derivatives: The market impact 27

The price subsequently recovered in September 1999 after the announce-ment of a pact between fifteen central banks8 to limit sales and lending, widelyknown as the ‘Washington Agreement on Gold’ (See Appendix 2). The signa-tories held between them about half of all official gold, and other large hold-

ers, such as the Uni ted States, IMF and Japan, unofficially associated them-selves with the agreement.

8 The European Central Bank, and the central banks of Austria, Belgium, France, Finland, Germany,Irish Republic, Italy, Luxembourg, the Netherlands, Portugal, Spain, Sweden, Switzerland and the UK.

Source: IMF, World Gold Council

Largest Official Gold Holdings (end 2000)

Tonnes Gold as a % of foreign exchangeholdings

1 United States 8,137 57%2 Germany 3,469 35%3 IMF 3,217 n/a4 France 3,025 42%5 Italy 2,452 40%6 Switzerland 2,420 40%7 Netherlands 912 46%8 Japan 764 2%9 ECB 747 14%10 Portugal 607 39%11 Spain 523 13%12 United Kingdom 480 9%13 Taiwan 421 3%14 China 395 2%15 Russia 382 12%16 Austria 377 19%17 India 358 9%18 Venezuela 319 16%19 Lebanon 287 30%20 Belgium 258 19%

All countries 28,871 12%

WAG 15,603 29%Euro-System 12,427 30%

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 29/121

Gold Derivatives: The market impact 28

1.4 Data issues

Published statistics on certain areas of physical supply and demand are well de-veloped but there remain gaps such as inventories, the extent of private institu-tional gold holdings, and the extent of below-ground reserves. Analytical prob-lems arise from informal or illegal activity. Some mining is still carried out byindividuals, notably in Latin America and Africa, and their activity is difficult totrack. Gold is easy to smuggle since small quantities have high value. Smugglingis generally declining as the gradual liberalisation and reduction in taxes underwayin many countries make it less worthwhile but where taxes are high or the marketheavily regulated it remains an important element of supply and one which is

inherently difficult to analyse.

One important form of demand for gold which is less easy to analyse is gold asinventory. Gold which is produced at the minehead does not immediately turninto jewellery around the neck of a customer. Quite substantial amounts of goldare held as inventory at various stages of the process and data on quantities do notexist. The existence of this stockpile is important because of its sensitivity to goldlease rates. So long as lease rates are very low, it is neither expensive nor risky tohold substantial quantities of gold in inventory because the gold can be borrowedcheaply. I f lease rates were to rise sharply (and we consider this possibility in moredetail later in the report), the immediate sources of additional supply of physical

gold would be from these inventories.

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 30/121

Gold Derivatives: The market impact 29

CHAPTER 2 THE PAPER MARKET

The chapter describes the nature and operati on of the derivati ves market in gold. The

main conclusions from the chapter are set out below, while the subsequent sections set out

the reasoning in more detail:

· gold supports a large and active derivatives market. I n part this is because of the very

qualities whi ch made it so widely used as money – its high value per unit weight, i ts

indestructibili ty, the ease wi th which i ts quali ty can be standardised and veri fied. But

more important than this has been the existence of large stocks of gold, and the

readiness of its owners – largely in the offi cial sector – to lend i t. The availabi lity of

abundant stocks for borrowing at low and generally stable rates, has made it possible

to design derivative products which meet the requi rements of producers, fabricators,

speculators and other market participants (2.1).

· the most important deri vative product is the forward contract. A forward sale is

equivalent to borrowing gold, selling it on the spot market, and depositi ng the sale

proceeds in a bank account. The forward dollar pr ice of gold i s determined by the

spot price of gold, the cost of borrowing dollars and the cost of borrowing gold (II .2.1).

· there is a wide variety of more complex derivati ves traded. Modern option pri cing

theory shows how such contracts can be replicated or hedged by dynamic trading of

forward contracts – that is strategies where the number of forward contracts held

depends on the level of the gold pr ice (2.2.2).

· the exchange traded market COMEX provides a good indi cati on of sentiment. But most derivatives trading takes place over-the-counter (OTC). The notional value of

banks’ derivati ve positi on in gold, though large relati ve to their other commodity

exposures, does not look large relati ve to derivative positions in other fi nancial mar-

kets. The evidence is consistent wi th the estimates in the Cross Report of the size of the

gold lending market (2.3).

· for downstream users and processors of gold (e.g. fabricators, refi ners and wholesal-

ers) the benefi ts of being able to borrow gold are straightforward. Their profi t mar-

gins are low relati ve to the value of gold inventory they hold, and can easi ly be wiped

out by adverse pri ce movements. Borrowing gold, or fi nancing their inventory through

gold l inked borrowing, can largely remove exposure to gold price risk. The fact that

lease rates are low and stable means that the cost and risks associated with carrying

high levels of inventory can be kept small (2.4).

· for speculators, the derivative market has made it cheap and easy to sell gold short.

One of the ri sks facing a short seller of commodi ties is a squeeze in the cash market

which raises borrowing rates for the commodi ty steeply, and thus forces premature

and costly liquidati on of a potentially profitable positi on. In the case of gold, the

existence of substantial stocks available for lending makes borrowing costs fai rly pre-

dictable and a squeeze unl ikely (2.5).

· commercial banks perform the standard economic functi ons of a fi nancial interme-

diary in any market. They manage the mismatch between lenders and borrowers –

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 31/121

Gold Derivatives: The market impact 30

mismatch of maturi ty, of lendi ng rates and of credi t. They also design and create

complex structures whi ch they hedge into the market. While they do take risk, they are

not well set up to take market r isk (e.g. on the level of the gold price) and are likely

to hedge much market risk back i nto the market (2.6).

· the derivative markets provide producers wi th a rich array of ri sk management in-

struments. Risk management has a number of di fferent objectives – hedging value,

hedging earni ngs and hedging cash flow – and the balance between them is a matter

of judgement. The size of a producer’s hedge book is likely to be influenced heavi ly by

management’s view of the likely profi tabi lity of the transacti on (2.7.1).

· accounting rules affect the size and composition of hedge books. Whi le the newly

introduced US Accounti ng Standard (FAS133) wi ll probably not affect the amount

of hedging, it may well influence the instruments used. Cash flow and fi nancing considerati ons wi ll limi t the size of hedge books for more highly leveraged producers

(2.7.2-3).

· the complexity of indi vidual producer hedge books and their long maturities may give

a misleading idea of the economic impact of producer hedging as a whole. M uch of

the optionali ty nets out; over-simplifying somewhat, the options bought by one pro-

ducer are effecti vely written by another producer, albeit wi th slightly different terms.

The long maturi ties of producer hedge books are more of a reflection of an accounting

decision to defer recogni tion of the profi ts or losses from particular transactions years

into the future rather than of the transfer of long-term forward price risk. From an

economic perspective, the main impact of the hedge book is fai rly well reflected by the

effecti ve short positi on or delta of the book (2.7.3).

2.1 What makes gold special?

Gold supports a very active derivatives market. In no other commodity do pro-ducers routinely sell their output five years ahead or more. According to the Bankfor International Settlements, gold derivatives account for 45% of the com-modity derivatives exposure of banks in the G10 countries. What features makegold so special?

Gold has certain qualities which have made it synonymous with money for manygenerations, and these go some way to explaining the flourishing derivatives mar-ket. Gold is valuable – 50,000 t imes as valuable tonne for tonne as oil for example– and does not deteriorate over time. Quality is easy to verify, and it is cheap totransform one traded form into another. Costs of storage and transport are smallwhen expressed as a percentage of value. This means that the gold market is asingle integrated market, with price differentials for location or quality being farless significant and less variable than they are for most other commodities.A change in the price of London good delivery gold bars has a direct and

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 32/121

Gold Derivatives: The market impact 31

propor tionate effect on the value of the inventory of a Far Eastern jeweller. Shocksin one part of the market are transmitted and absorbed throughout the world.Users and producers can all hedge or manage the same risk using the same con-tract; liquidity is pooled.

But at least as important has been a second distinguishing feature of gold: theextent of above ground stocks, and the reasons for which they are held. In othercommodities stocks are held either because they are necessary work in progress, oras a safeguard against a future shortage. The holders of these stocks place substan-tial value on having physical possession of the commodity. As the likelihood of ashortage looms and recedes, so does the value of the stock as a safeguard. When

there is a glut, stocks become a nuisance. This means that the lease rate for mostcommodities is extremely volatile.

Gold is different. For many holders of gold, physical possession of the metal is notimportant. The difference between possession of the gold and a warrant givingentitlement to delivery of the gold in a month or two is mainly a question of credit risk. The actual convenience yield – the benefit they ascribe to holdingphysical gold – is low or even slightly negative once storage costs are taken intoaccount.

For other holders of gold, both in the official sector and the private sector, physi-cal possession is central to the reason for holding gold. They want to hold goldprecisely because it is an asset which is no one else’s liability, and this advantagewould be lost by lending the gold.

The behaviour of the gold lending market over the course of the 1990s suggeststhat once a central bank has put in place a policy of lending gold, the amount of gold it is prepared to lend within its predetermined policy limits is largely insen-sitive to the level of lease rates. But it does take time for a new policy to be put inplace, or for an existing policy to be revised. Whether it is reasonable to expectgold interest rates to remain as low and stable in the future as they have been inthe past is a matter we turn to later (in Chapter 5). But, as we will argue in thenext section, it is the stability and predictability of gold interest rates that has

underpinned the development of the paper market and the growth in particularof very long-dated contracts.

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 33/121

Gold Derivatives: The market impact 32

2.2 Gold derivative contracts

The variety and complexity of derivative products and hedge books is consider-able. They are designed to achieve a variety of objectives – economic, financial,accounting, regulatory. In this section we focus particularly on the economic analysisof these products. We look at the types of risk which are transferred from thebuyers of derivatives to the sellers. We show that, however complex the structure,the main gold specific risks which are transferred can be decomposed into spotgold price risk, gold interest rate risk and gold price volatility risk. In additiongold derivatives often transfer currency interest rate and exchange rate risks, butthese risks are of less relevance to this study.

The simplest derivative contract is the fixed price forward contract. After showinghow it can be decomposed into a spot transaction and gold and cash borrowingand lending, we consider the nature and magnitude of the risks transferred be-tween the buyer and the seller. Then we extend the analysis to more complexproducts such as options, and examine the link between complex derivatives andtrading strategies involving simple forward contracts.

2.2.1 Forward contracts

The relation between forward markets and lending markets

In a forward contract one party contracts with another to deliver a fixed quantityof the commodity at some fixed price and date to a second party. The party whois delivering is short the contract and the one who is buying is long the contract.A forward sale is equivalent to borrowing the commodity, selling it on the spotmarket and investing the cash proceeds.

So for example a producer who wants to sell 1 million ounces of gold forward oneyear, when the spot price is currently $300/oz, could instead search for an inves-tor who has gold and is prepared to lend 1 million ounces for one year at a cashinterest rate of 2%. The producer borrows the gold and sells it on the spot mar-ket. He invests the proceeds of $300m in a 1 year US Treasury bond, yielding say

7%. In one year the bond matures giving $321m. The producer then gives theinvestor 1 million ounces of gold and $6m interest to repay the loan. The neteffect is that the gold producer hands over 1 million ounces of gold in one year’stime, and receives cash of $321 - 6 = $315 million. The producer has created asynthetic forward contract at $315/oz. The forward price is the spot price plusthe dollar interest rate, less the gold interest rate.

The equivalence of the two transactions is important because it ties the forwardmarket to the gold lending market. With a deep and liquid gold lending market

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 34/121

Gold Derivatives: The market impact 33

there is a deep and liquid forward market, going out at least as far as the goldlending market. Much of the lending of gold by central banks is short-term –typically out to three months, though the average tenor has been increasing. Theexistence of a long-term gold forward market in the absence of a long-term goldlending market depends on the expectation that gold interest rates will remainlow and stable.

To see this, suppose the producer wants to sell gold five years forward, andthe gold lending market only extends one year. H e decides to create a syn-thetic forward contract by borrowing the gold for one year at a time, usingthe new gold loan to pay back the old. The final price he gets for the gold will

equal the ini tial spot price plus the five year dollar interest rate less the cost of borrowing the gold for the five years. If the cost of borrowing is unpredict-able, the price is very uncertain. But the uncertainty about the average levelof the one year gold interest rate over the next five years is probably of theorder of ½%, so the uncertainty in the realised forward price is around 2-3%.The gold producer can create a synthetic long-term forward contract usingthe short term lending market, and thereby get rid of the great bulk of theprice risk he otherwise faces.

The idea of a producer using a synthetic forward contract may seem unrealistic.In practice, the producer is more likely to seek to sell the gold forward to a bank.But the hedging issue does not disappear. In the absence of a counterparty whowants to buy the gold forward five years, the bank will hedge its risk by shortterm gold borrowing. The bank then takes on the risk that gold interest rates willrise. A producer who wants to sell production forward therefore faces a choice: hecan pass the gold lease rate risk on to the bank and get a fixed price forwardcontract, or he can accept a forward contract where the price is adjusted in linewith lease rates, and he bears the lease rate risk. The fixed price deal will probablyprove more expensive since long-term lease rates are on average higher than short-term lease rates.

Whether the bank wri tes a contract with a fixed lease rate, taking on the lease raterisk, or whether the producer agrees to keep the risk by accepting a floating lease

rate, the point is the same. It is only because the risk is small, because goldinterest rates are so stable, that it makes sense to do the transaction at all in theabsence of a long-term forward buyer of gold. Were gold interest rates as volatileas oil interest rates, the final price on a long-term floating lease rate forward salecontract would be so uncertain that it would be quite ineffective in hedging fu-ture revenues. The premium a bank would charge to offer a fixed rate deal wouldtend to be so large as to make hedging unattractive. It follows that if the goldlending market were expected to become much more volatile, the long maturityderivatives market would shrink.

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 35/121

Gold Derivatives: The market impact 34

The value of a forward contract

A forward contract written at market prices has zero financial value initially. Some-one who has sold production forward can negate the contract either by cancella-tion or by buying gold forward on the same terms. But as time passes, and thegold spot price and gold and dollar interest rates move, the forward price of goldchanges and the contract becomes an asset to one side and a liability to the other.From the perspective of a producer who has sold known production forward thischange in value may not seem significant. Any change in value of the forwardcontract is exactly offset by a change in the value of his future output.

But there are at least three reasons why the change in the value of the forwardcontract is important. First, it represents the effect of hedging as opposed to nothedging. Second, it may create financing problems. Suppose the forward pricehas risen since the inception of the contract, so the hedge is loss-making from theproducer’s perspective. From the bank’s perspective, the contract with the pro-ducer is now an asset, while the hedging transaction it has entered into to offsetthe risk is an equal and opposite liability. If the producer were to get into financialdifficulties and be unable to honour the forward sale, the value of the contract isthe amount which the bank stands to lose. To protect itself, the bank may de-mand margin (a financial payment on account), or collateral (the posting of someasset as security) or even the right to terminate the contract prematurely.

The third reason that the value is important is that it can actually be realised. Itis far easier and cheaper to buy gold forward and then sell it than it is to buy agold mine and then sell it. It is the low level of transactions costs which allowsproducers to modify their hedges rapidly. The value of a forward sale contract canbe realised by terminating it or by entering into an offsetting purchase contract.To get some idea of the sensitivity of a forward contract to changes in marketconditions, consider the case of a producer who has sold gold forward five years ata fixed price when the spot price is $300/oz, and gold and dollar interest rates are2% and 7% respectively. The fair forward price is $381/oz. If the spot gold pricerises by $30/oz (a typical annual move) then the fair forward price in five yearsrises to 330x(1.07/1.02)5 = $419/oz. The producer is committed to selling his

gold in five years at $381/oz when the fair forward price today is $419/oz. Tocancel the hedge, the producer would have to agree today to buy the gold back at$419/oz, locking in a loss of $38/oz in five years’ time. Discounting the $38/ oz, the hedge has a negative value of $27/oz today. Of course, if the gold pricehad fallen $30/oz, the hedge contract would have a positive value of $27/oz tothe producer.

But it is not only the gold price that can affect the value of the contract. If dollarinterest rates go up 1% (again, a typical annual move) while spot gold stays at$300/oz, the fair forward price rises to $399/oz, and the hedge contract’s value

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 36/121

Gold Derivatives: The market impact 35

goes to +$12/oz. The mark-to-market value of a long-dated fixed dollar rate for-ward has a sensitivity to interest rates which is not much less than its sensitivity tothe gold price. If the dollar rate is floating, the sensitivity of value to interest ratesbecomes virtually zero, in exactly the same way as the sensitivity of value of abond to interest rates is large for long-dated fixed rate bonds, but small for float-ing rate bonds.

An increase in the long-term gold interest rate would have an effect similar inmagnitude but opposite in sign to an increase in interest rates. The mark-to-market value of a forward contract with a floating gold interest rate would havevirtually no sensitivity to gold lease rates. Thus looking from the perspective of

the value of the hedge book as opposed to the realised price at maturity, thefloating rate forwards may be less risky than the fixed rate forwards.

2.2.2 Options

In addition to simple forward contracts, there are many more complex productswhich are used by participants in the market. We have argued that long-datedforward contracts would not exist if they could not be hedged or synthesisedreasonably accurately using the spot and short-term gold lending market. Thesame holds true of more complex products.

Hedging options

Consider the case of a producer who wants to buy a put option, giving the rightto sell gold in five years’ time at $300/oz. The bank writing the option will onlybe able to offer a good price if it can either find some other party who is preparedto sell the bank a similar option, or if the bank can hedge itself. Writing theoption and taking the risk on its own books makes no economic sense; the bankhas no advantages and some disadvantages relative to a gold producer in takingthis risk on itself.

To hedge the risk, the bank will follow what is called a delta hedging strategy. Thevalue of the put option depends on the level of the gold price. If the gold price is

very low, the option is deep in the money, and very likely to be exercised, so a $1change in the gold price causes a $1 change in the value of the put. As the goldprice rises, the chance of the option being exercised falls, so the sensitivity to thegold price (or delta) is smaller. When the gold price is very high, the put optionis nearly worthless and its price barely changes with the gold price; its delta goesto zero.

If the bank sells gold forward, and varies the amount with the delta, then it canensure that profits or losses on i ts option position occasioned by movements inthe underlying gold price are offset by profits or losses on its gold forward

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 37/121

Gold Derivatives: The market impact 36

position. In an ideal world, if the hedge is executed properly, the bank should beperfectly hedged. All the risk that the producer is transferring to the bank is trans-ferred into the forward market, and thence into the spot and lending market.

Another way of looking at the transaction is to observe that a producer who wantsto create a floor on sale proceeds while remaining exposed to the upside could buya put option from a bank. Alternatively he could follow a suitable trading strategyin the forward market. He should sell some of his production forward; as the goldprice rises, he should buy forward, and as it falls he should sell forward. If thegold price falls sufficiently, he should sell all his production forward, thus lockingin a floor price for his production. If the gold price rises sufficiently he should buy

back all the forward contracts he had sold at the outset, and thus be fully exposedto the gold price. In this way the producer could create a synthetic put option.

The producer then has the choice between this synthetic put option and buyinga real put option from a bank which will then create a synthetic put to hedgeitself. I t is possible to see the producer, through the put option contract, in effectdelegating the operation of the dynamic trading strategy to the bank. Whether itbuys the put options or synthesises it, the net effect on the forward market is thesame. When the position is put on, the producer is directly or indirectly selling aquantity of gold forward equal to the product of the amount optioned and thedelta. As the gold price rises or falls, the forward sale position declines or increaseswith the delta.

Hedge error

In theory, given certain assumptions1 , the delta hedging strategy works perfectly.But in practice the assumptions do not hold perfectly, and there can be substan-tial hedge error. In particular, the efficacy of the strategy depends on the volatilityin the gold price. If the price turns out to be very volatile, the synthetic strategy,which involves buying whenever the price rises, and selling whenever it falls, willbe very expensive. A bank which writes a put option and hedges itself prices in acertain assumption about volatility. It makes a profi t or loss on the hedge depend-ing on whether the actual volatility is lower or higher than that factored into the

original price (the ‘implied volatility’).

For this reason, the writer of a put option is said to be selling volatility, and thebuyer of the option is buying volatility. A similar analysis holds for call options,except that the buyer of a call option is long gold, whereas a buyer of a put is shortgold. But both put and call option buyers are buying volatility, for in both casesthe replicating strategy involves buying as prices rise and selling as they fall.

1 The standard assumptions include the absence of transaction costs, constant interest rates on both thecurrency and the commodity, markets always open, no constraints on borrowing either cash or thecommodity, and the spot price of the commodity following a diffusion process with constant volati li ty.

7/28/2019 Gold Derivatives the Market Impact

http://slidepdf.com/reader/full/gold-derivatives-the-market-impact 38/121

Gold Derivatives: The market impact 37

Volatility is not the only factor which gives rise to hedge error. The error is alsoaffected by the detailed way the forward gold price behaves. Large jumps in theprice for example can throw out the hedge. But volatility is the main determinantof how well the hedge works.

Although we have looked at the particular example of a simple put strategy, thesame is true of any option, whether a vanilla option like a put or call, or a moreexotic structure such as one where the pay-out is conditioned by the price of goldhitting some critical level. To every option there corresponds a delta hedgingstrategy which replicates the option. The existence of the strategy makes it possi-

ble for the bank to offer the complex option, and also determines the price it mustcharge to cover i ts costs. I f the bank is fully hedged into the spot gold market atall times then the existence of the option gives rise to a corresponding position onthe spot market equal in size to the option’s delta.

2.3 The markets

2.3.1 Exchanges

Trading in gold derivatives takes place both over the counter and on organisedexchanges. The majority of exchange traded volume is on the New York Mercan-

ti le Exchange (NYMEX) in i ts COM EX division. Both futures and options aretraded with maturities going out as far as five years for the futures and two yearsfor the options. Actual delivery consists of the transfer of a COMEX warehousereceipt. The next largest exchange for gold derivatives is the Tokyo CommodityExchange which has about one third the volume of COMEX.

As is typical of futures markets the great majority of contracts are closed outbefore delivery. Virtually all trading takes place in the near-dated contracts –those with up to six months to maturi ty. Average daily futures volume on COMEXis some 35,000 contracts, corresponding to 100 tonnes per day or 25,000 tonnesper year. Average volume in the options market is around 20% of that in the

futures in terms of numbers of contracts or quantity of underlying metal.