gm events & presentations canadian dealer conference

DESCRIPTION

TRANSCRIPT

Forward Looking StatementsIn this presentation and in related comments by our management, our use of the words “expect,” “anticipate,” “estimate,” “goal,” “target,” “believe,” “improve,” “intend,” “potential,” “continue,” “designed,” “opportunity,” “risk,” “may,” “would,” “could,” “should,” “project,” “projected,” “positioned” or similar expressions is intended to identify forward-looking statements that represent our current judgment about possible future events. We believe these judgments are reasonable, but these statements are not guarantees of any events or financial results, and our actual results may differ materially due to a variety of important factors. The most recent reports on SEC Forms 10-K, 10-Q and 8-K filed by us or GMAC provide information about these and other factors, which may be revised or supplemented in future reports to the SEC on those forms.

Industry and market data contained in this presentation is based on internal GM market and industry analysis. Although management believes this data is reliable as of its respective dates, this data has not been independently verified and we cannot assure you as to accuracy or completeness of this data.

Unless specifically required by law, we assume no obligation to update or revise these forward-looking statements to reflect new events or circumstances.

Ray G. YoungExecutive Vice President & CFO

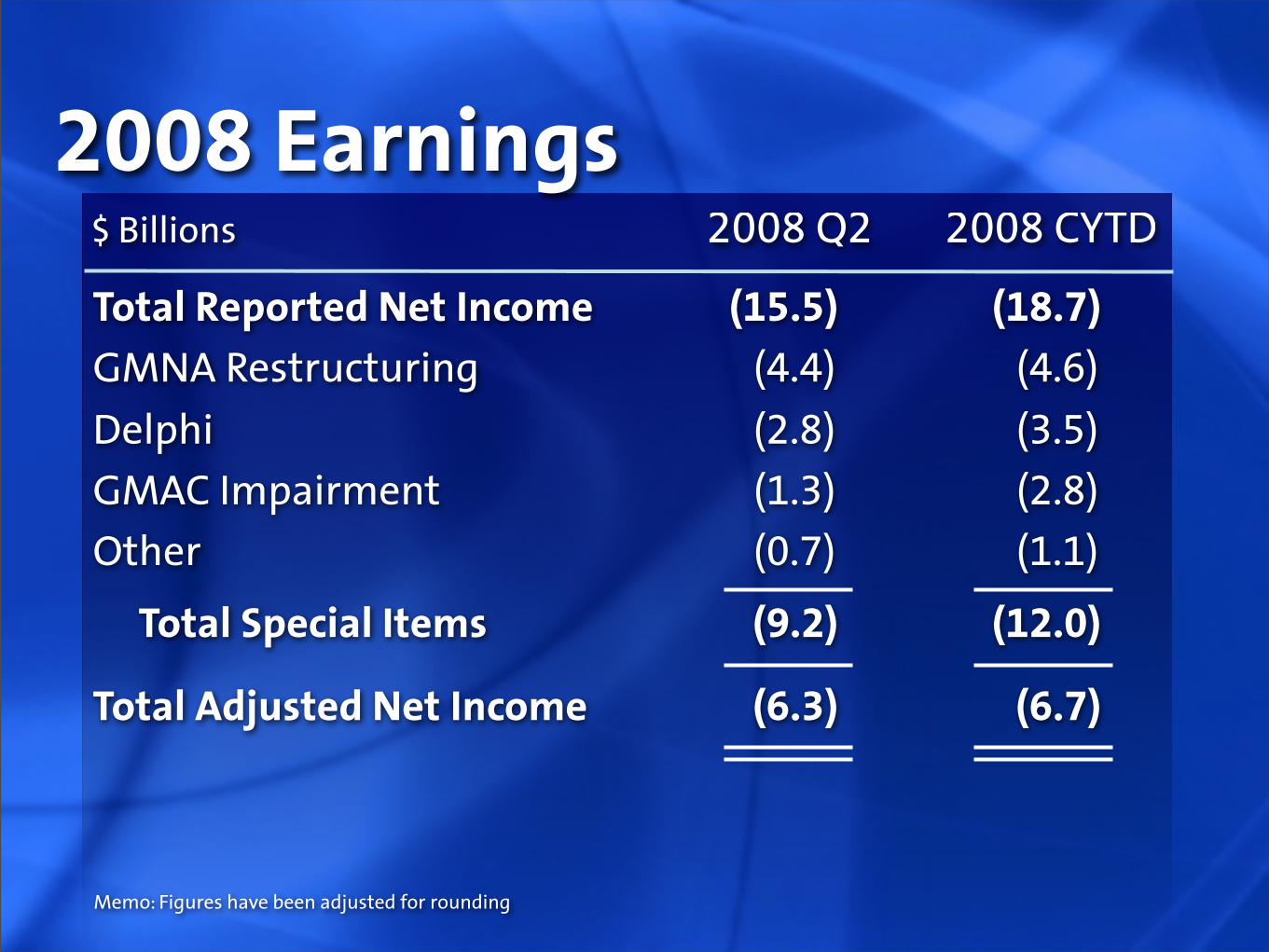

2008 Earnings$ Billions 2008 Q2 2008 CYTD

Total Reported Net Income (15.5) (18.7)GMNA Restructuring (4.4) (4.6)

Delphi (2.8) (3.5)GMAC Impairment (1.3) (2.8)Other (0.7) (1.1)

Total Special Items (9.2) (12.0)

Total Adjusted Net Income (6.3) (6.7)

Memo: Figures have been adjusted for rounding

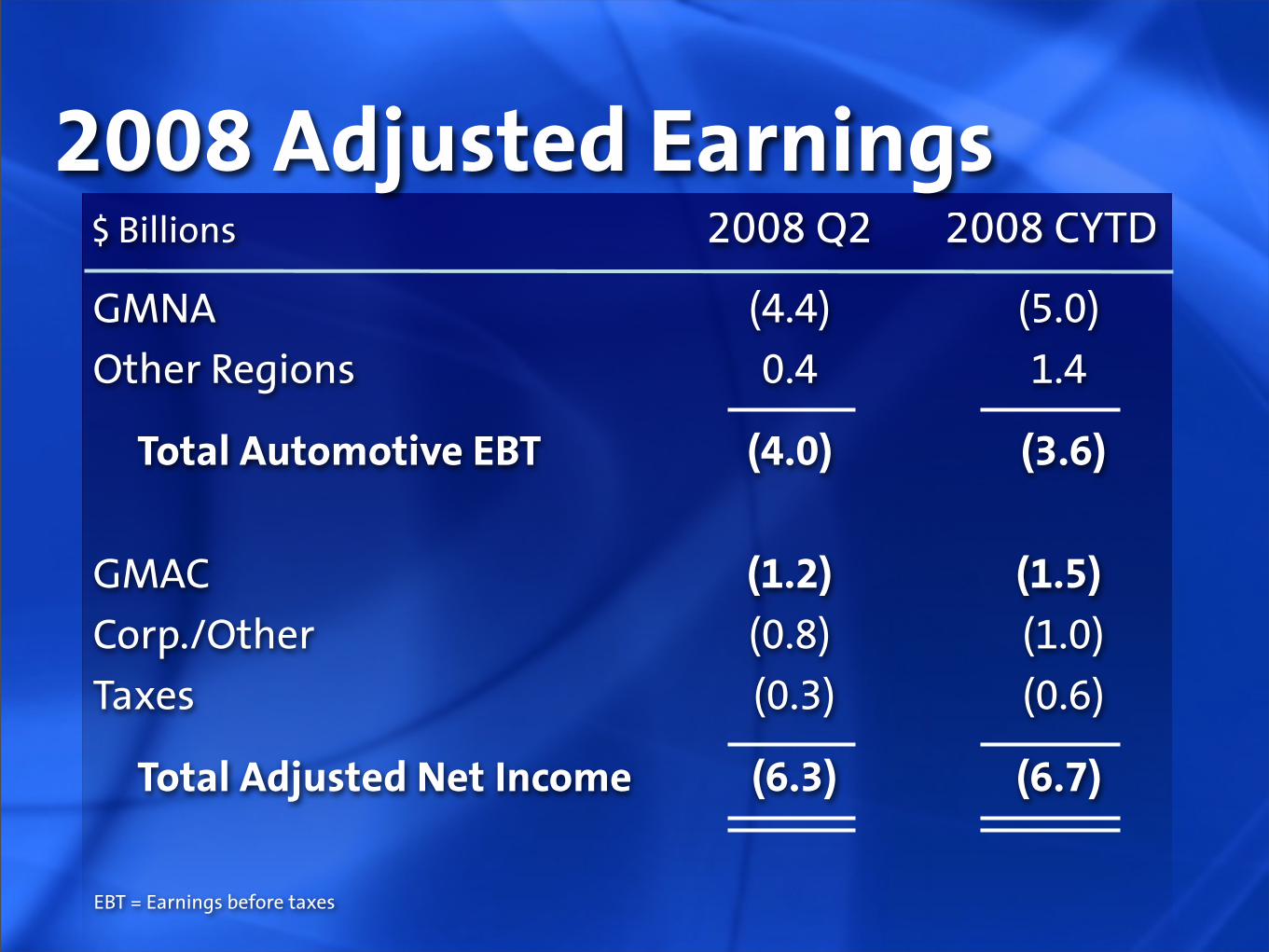

GMNA (4.4) (5.0)Other Regions 0.4 1.4

Total Automotive EBT (4.0) (3.6)

GMAC (1.2) (1.5)Corp./Other (0.8) (1.0)Taxes (0.3) (0.6)

Total Adjusted Net Income (6.3) (6.7)

2008 Adjusted Earnings

EBT = Earnings before taxes

$ Billions 2008 Q2 2008 CYTD

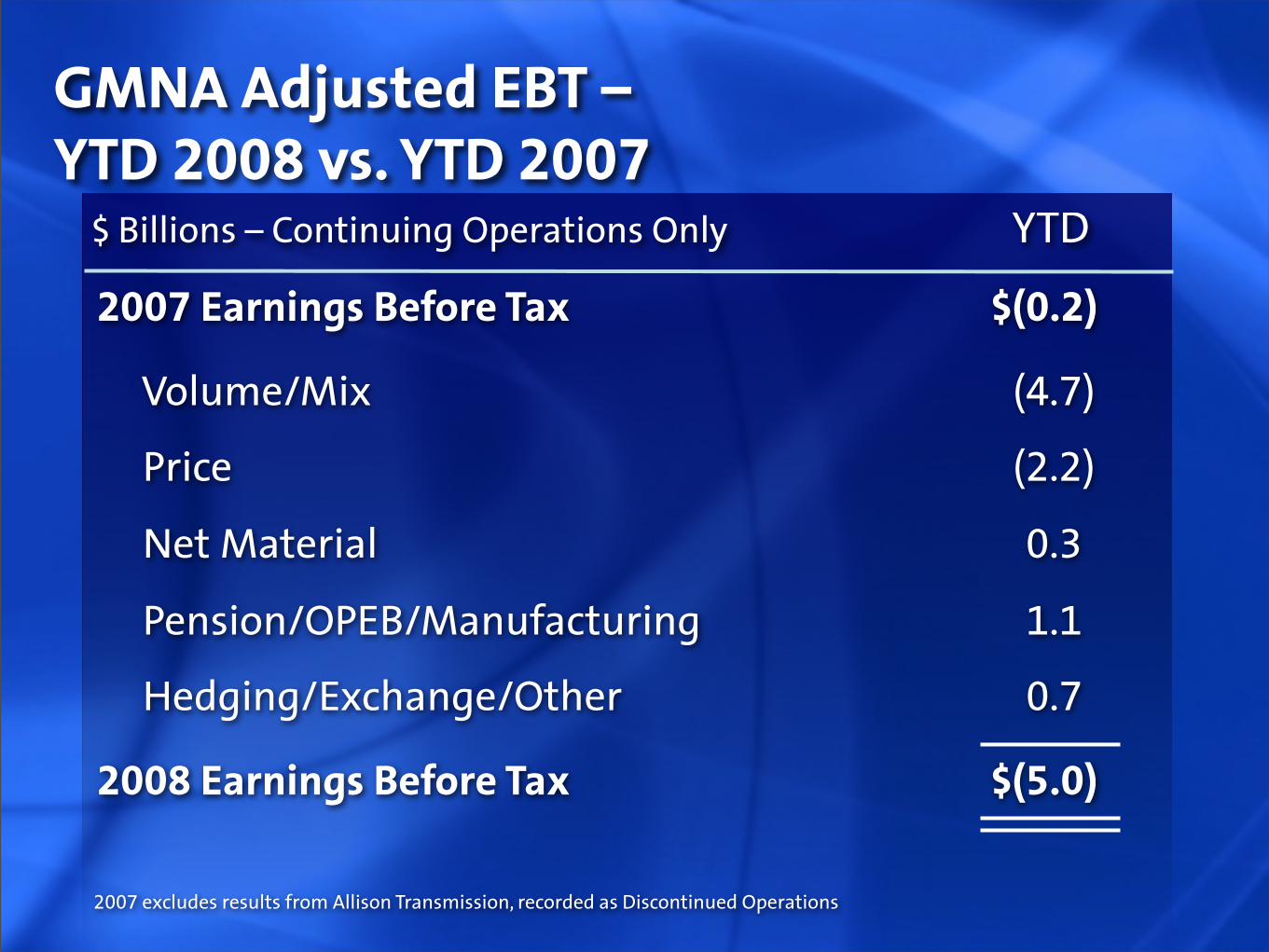

2007 Earnings Before Tax $(0.2)

Volume/Mix (4.7)

Price (2.2)

Net Material 0.3

Pension/OPEB/Manufacturing 1.1

Hedging/Exchange/Other 0.7

2008 Earnings Before Tax $(5.0)

GMNA Adjusted EBT –YTD 2008 vs. YTD 2007

2007 excludes results from Allison Transmission, recorded as Discontinued Operations

$ Billions – Continuing Operations Only YTD

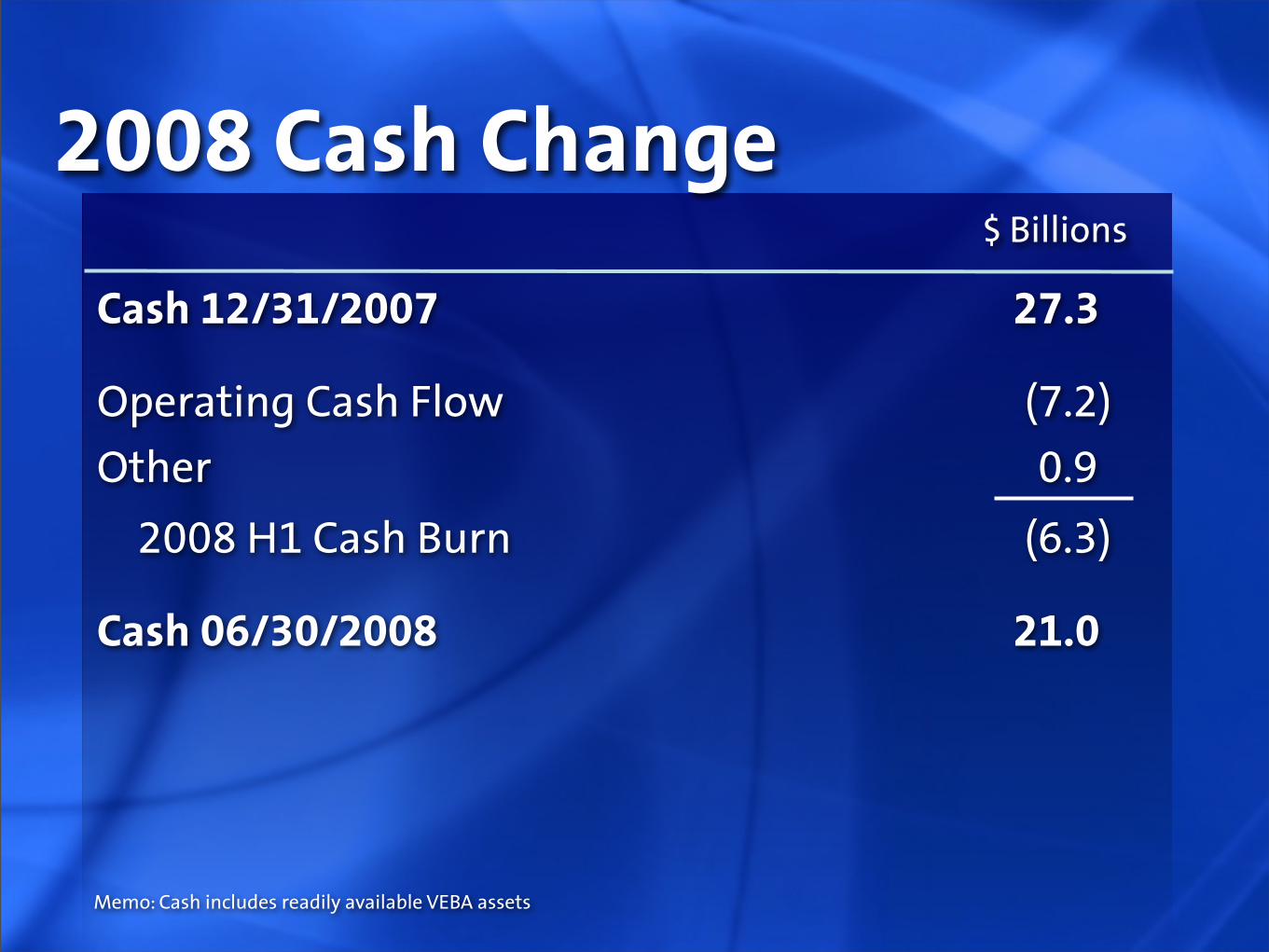

2008 Cash Change

Cash 12/31/2007 27.3

Operating Cash Flow (7.2)

Other 0.9

2008 H1 Cash Burn (6.3)

Cash 06/30/2008 21.0

$ Billions

Memo: Cash includes readily available VEBA assets

What Happened?

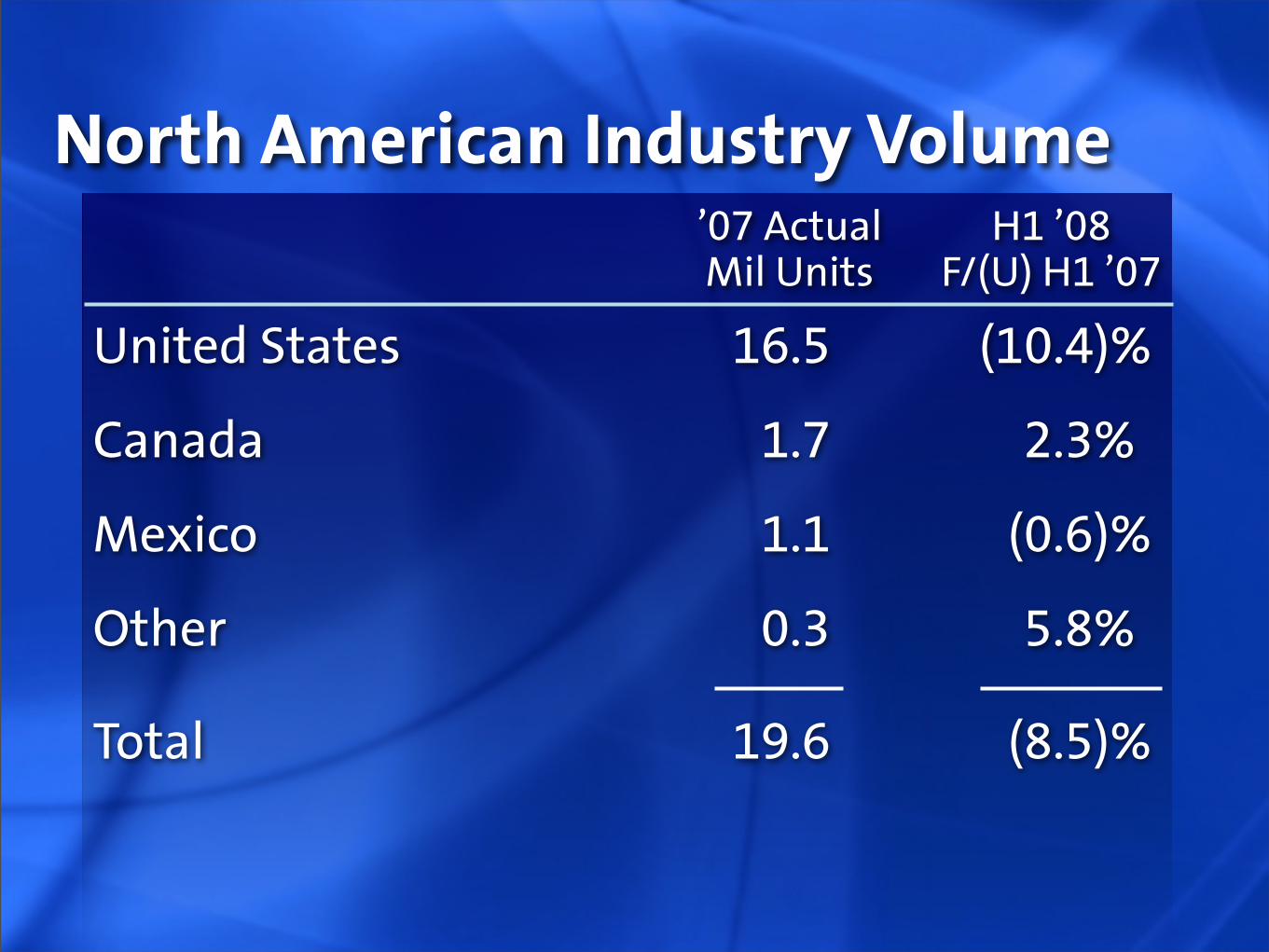

North American Industry Volume ’07 Actual H1 ’08 Mil Units F/(U) H1 ’07

United States 16.5 (10.4)%

Canada 1.7 2.3%

Mexico 1.1 (0.6)%

Other 0.3 5.8%

Total 19.6 (8.5)%

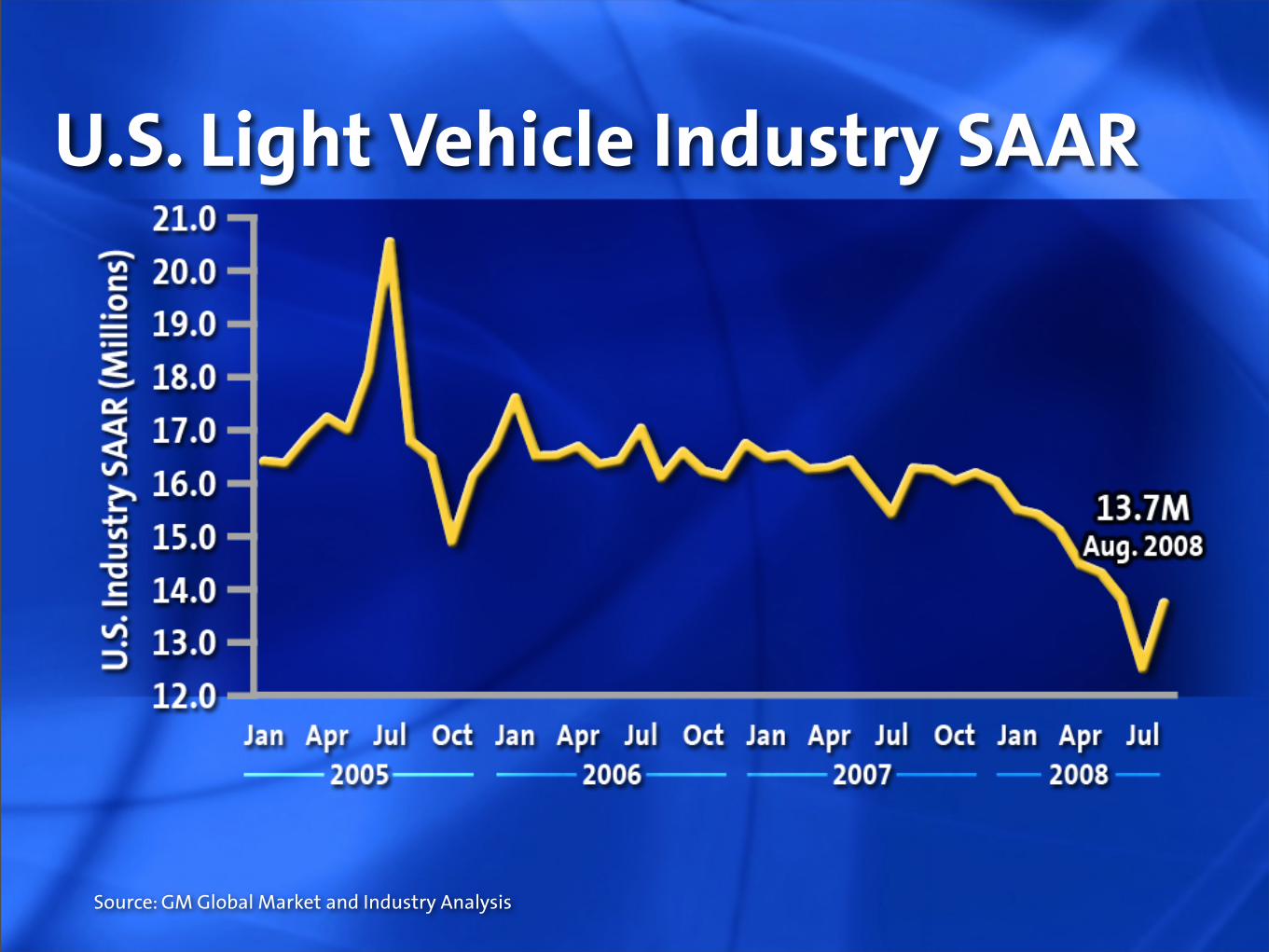

U.S. Light Vehicle Industry SAAR

Source: GM Global Market and Industry Analysis

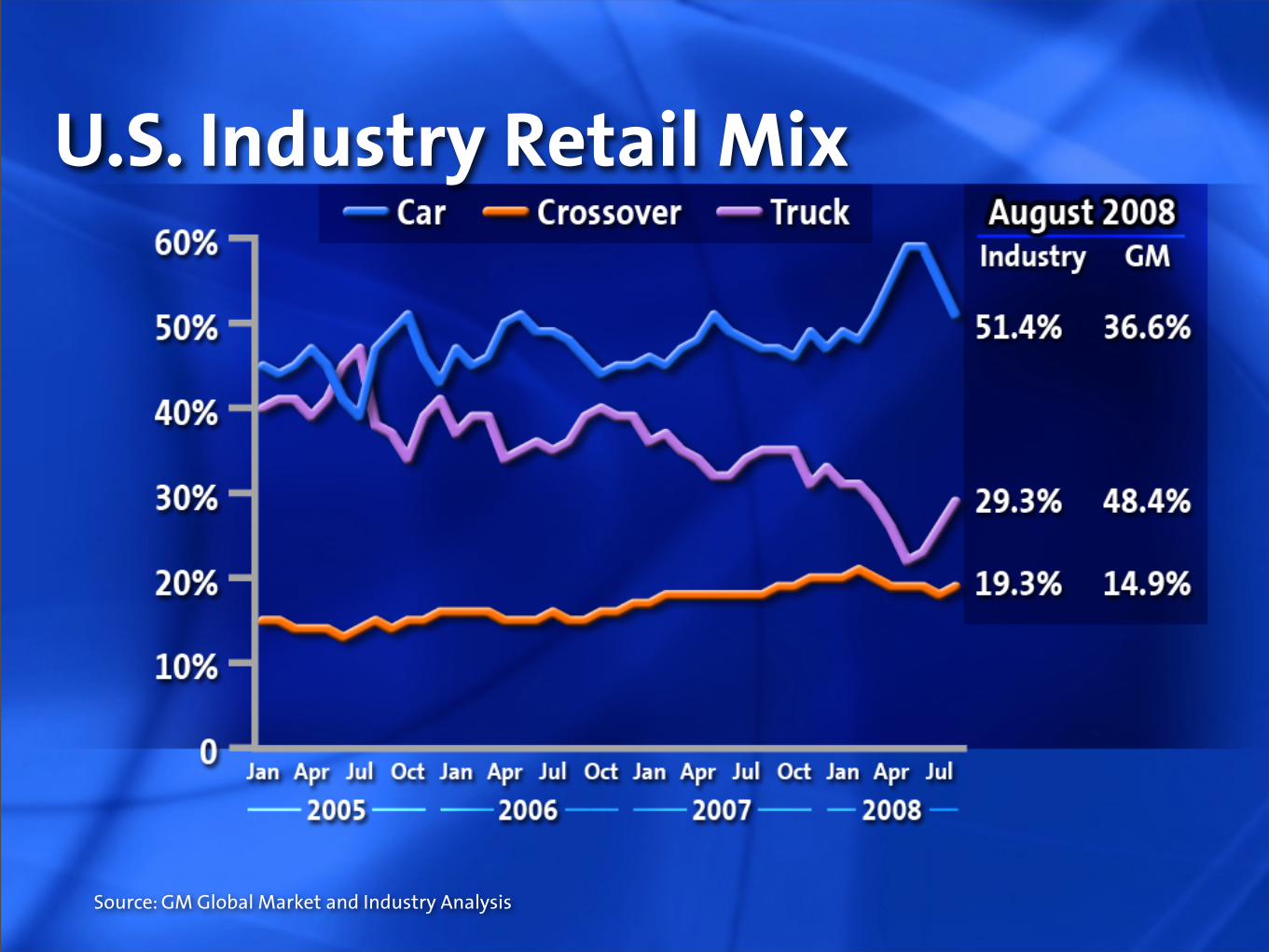

U.S. Industry Retail Mix

Source: GM Global Market and Industry Analysis

What Are We Doing?

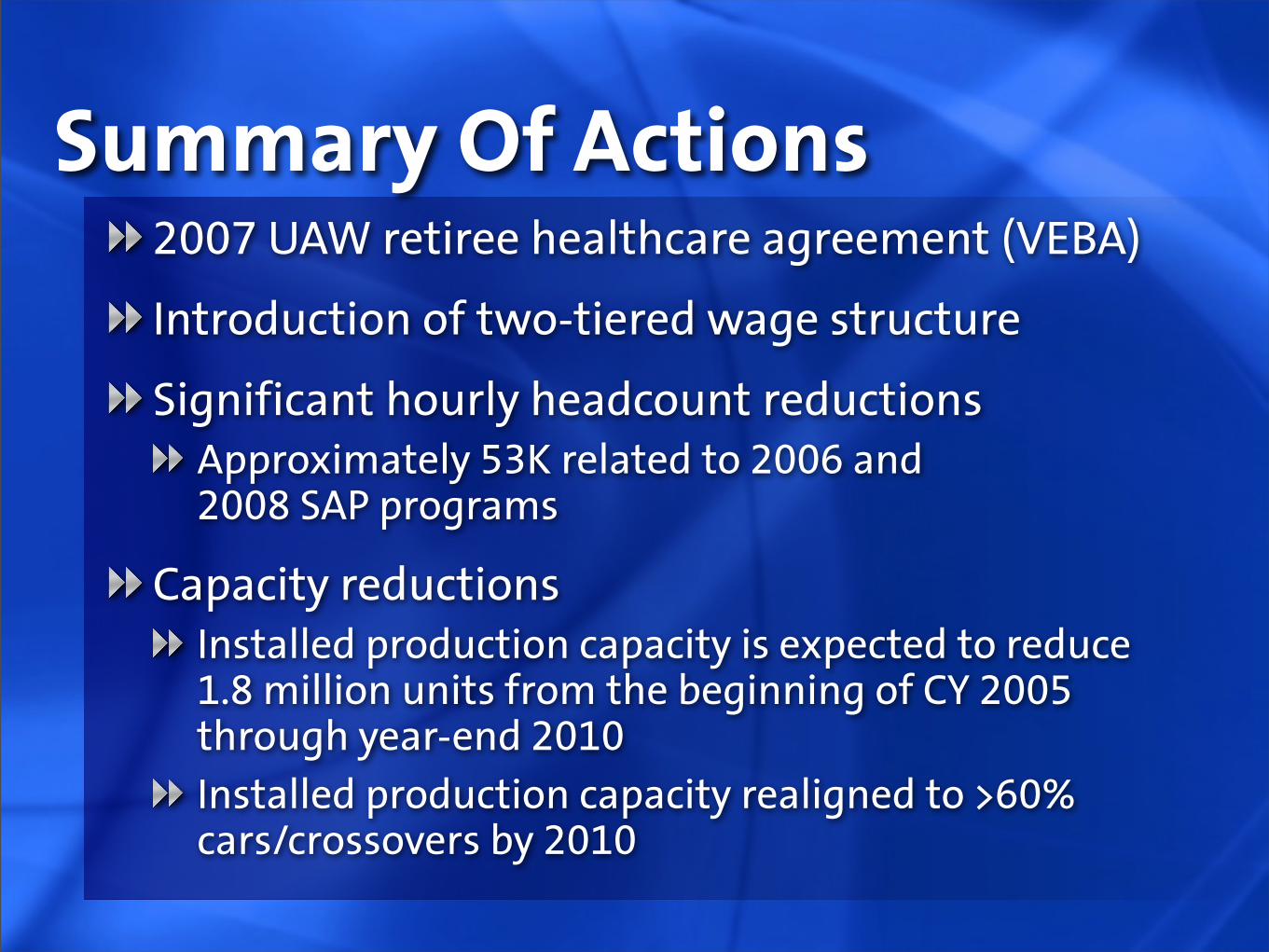

Summary Of Actions2007 UAW retiree healthcare agreement (VEBA)

Introduction of two-tiered wage structure

Significant hourly headcount reductionsApproximately 53K related to 2006 and2008 SAP programs

Capacity reductionsInstalled production capacity is expected to reduce1.8 million units from the beginning of CY 2005 through year-end 2010Installed production capacity realigned to >60% cars/crossovers by 2010

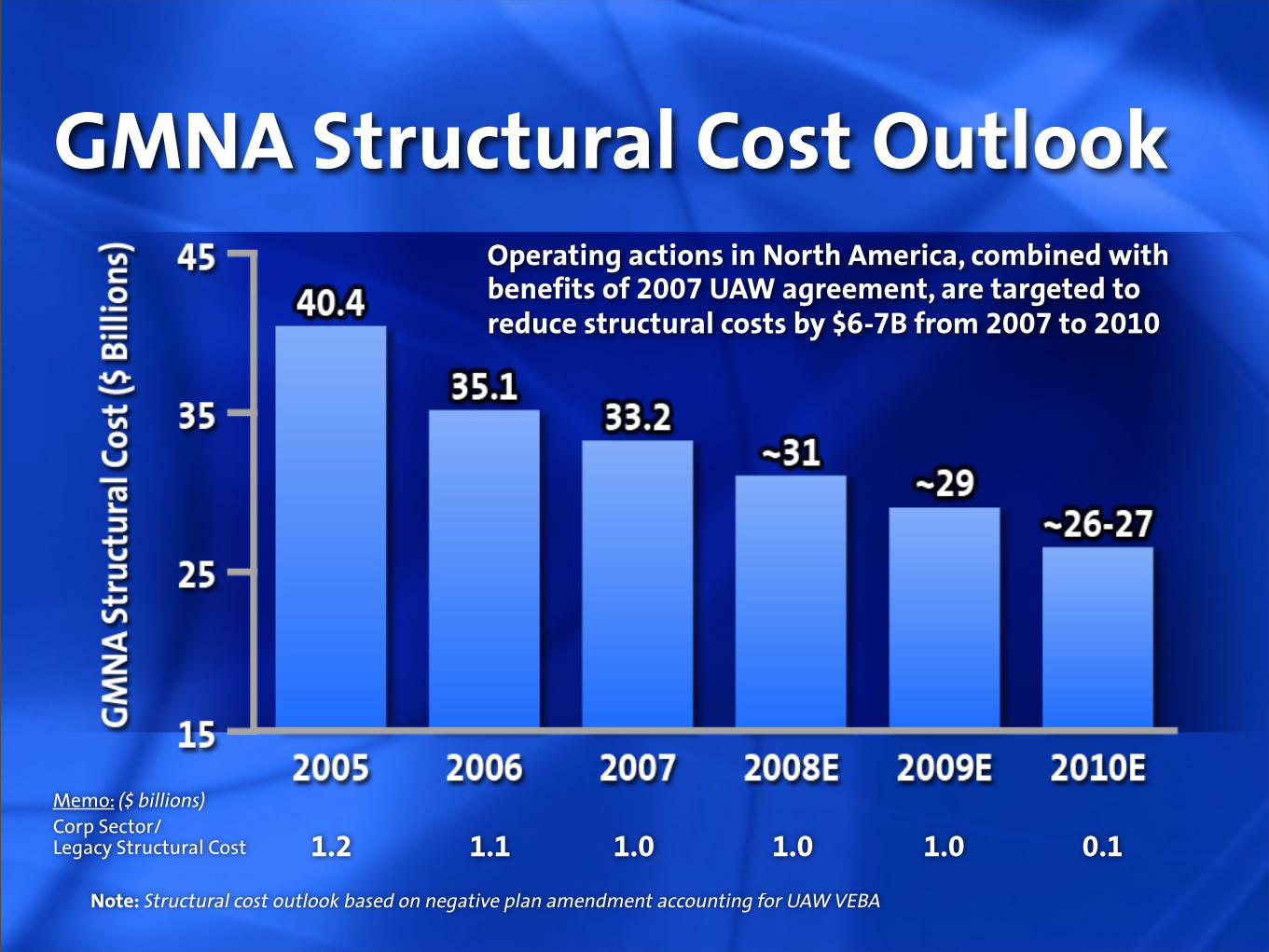

1.2 1.1 1.0 1.0 1.0 0.1

GMNA Structural Cost Outlook

Memo: ($ billions)Corp Sector/ Legacy Structural Cost

Note: Structural cost outlook based on negative plan amendment accounting for UAW VEBA

Operating actions in North America, combined with benefits of 2007 UAW agreement, are targeted to reduce structural costs by $6-7B from 2007 to 2010

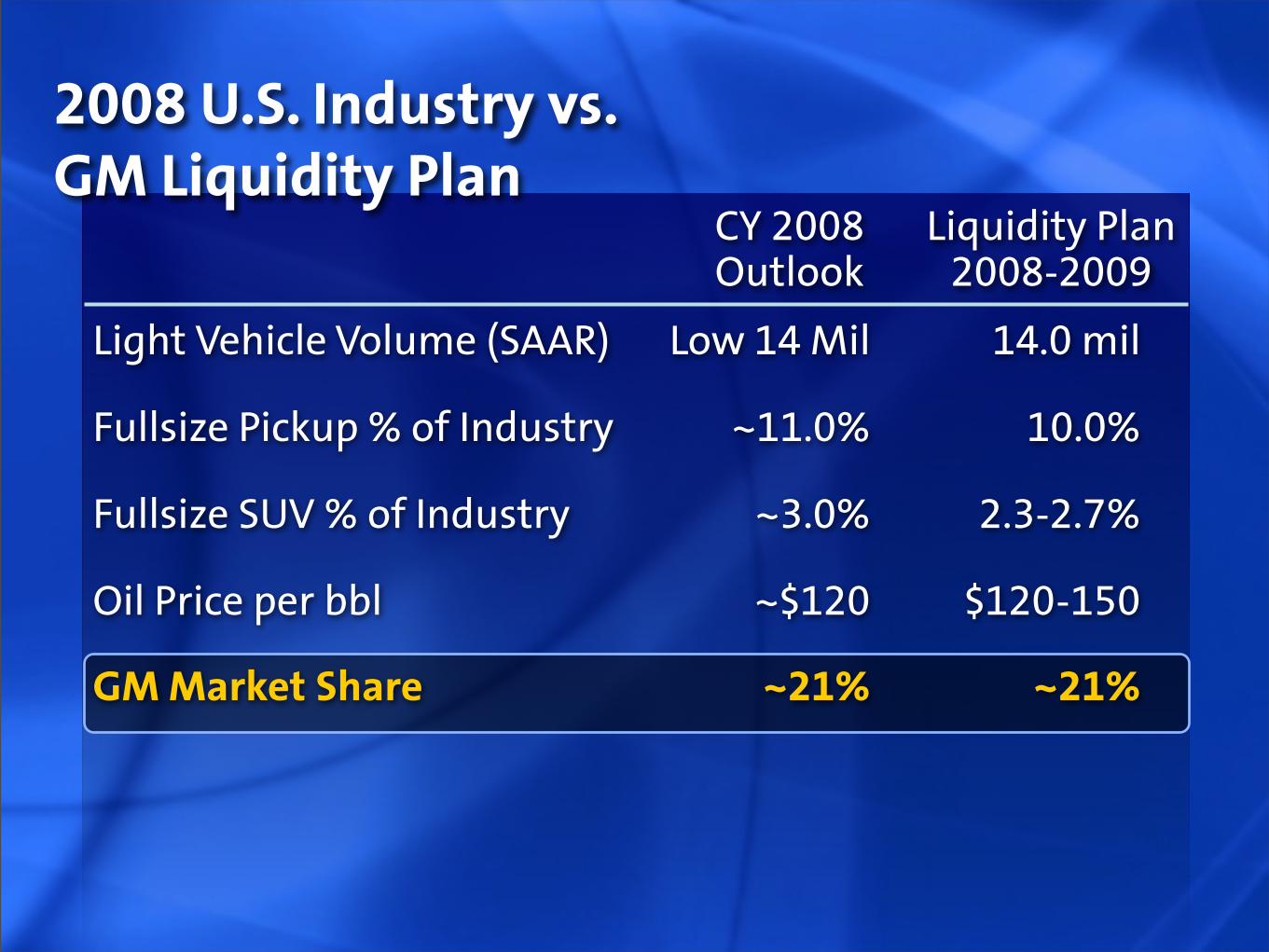

2008 U.S. Industry vs. GM Liquidity Plan

CY 2008 Liquidity Plan Outlook 2008-2009

Light Vehicle Volume (SAAR) Low 14 Mil 14.0 mil

Fullsize Pickup % of Industry ~11.0% 10.0%

Fullsize SUV % of Industry ~3.0% 2.3-2.7%

Oil Price per bbl ~$120 $120-150

GM Market Share ~21% ~21%

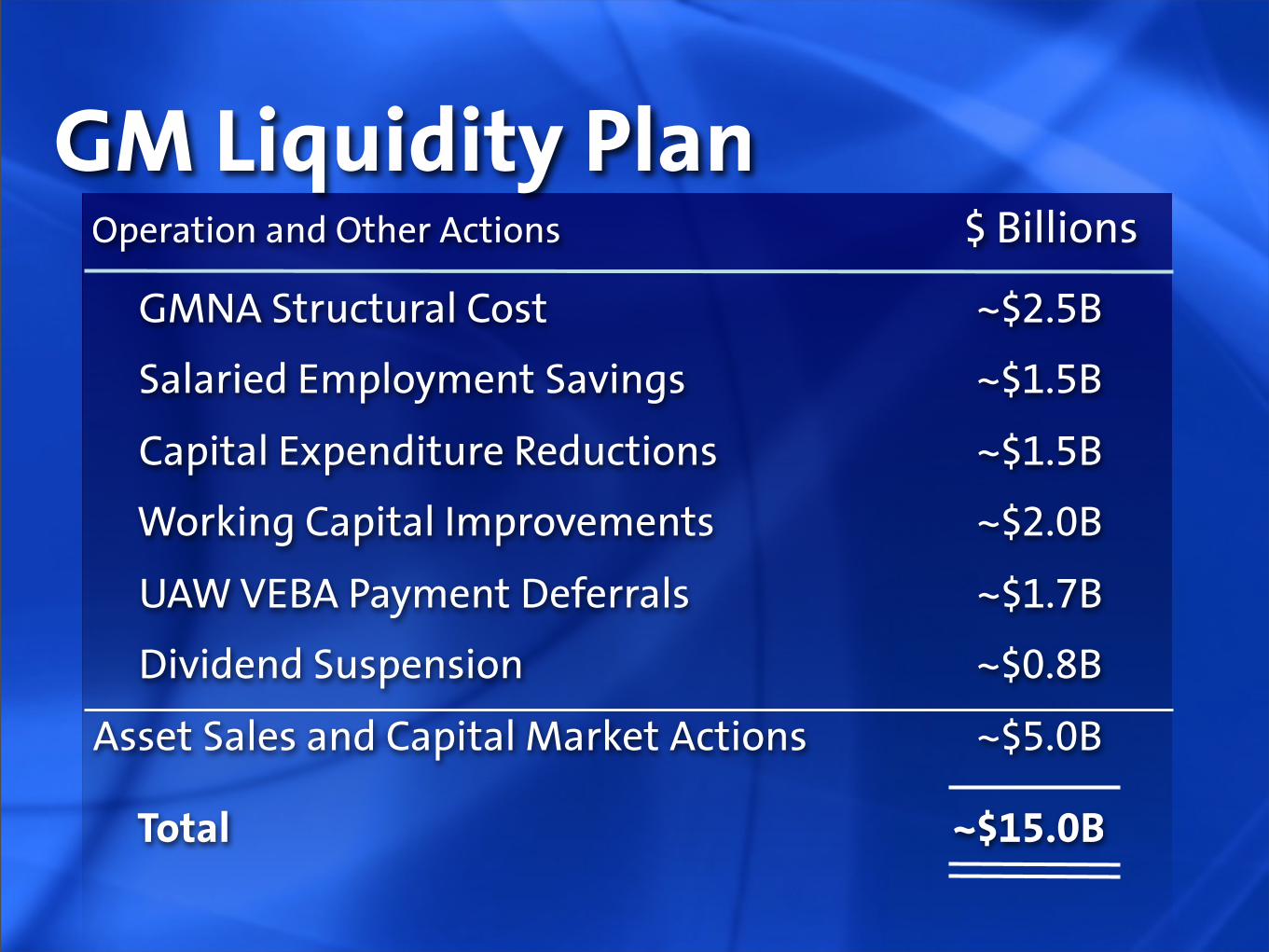

GM Liquidity Plan

GMNA Structural Cost ~$2.5B

Salaried Employment Savings ~$1.5B

Capital Expenditure Reductions ~$1.5B

Working Capital Improvements ~$2.0B

UAW VEBA Payment Deferrals ~$1.7B

Dividend Suspension ~$0.8B

Asset Sales and Capital Market Actions ~$5.0B

Total ~$15.0B

Operation and Other Actions $ Billions

What Is Happening Outside GMNA?

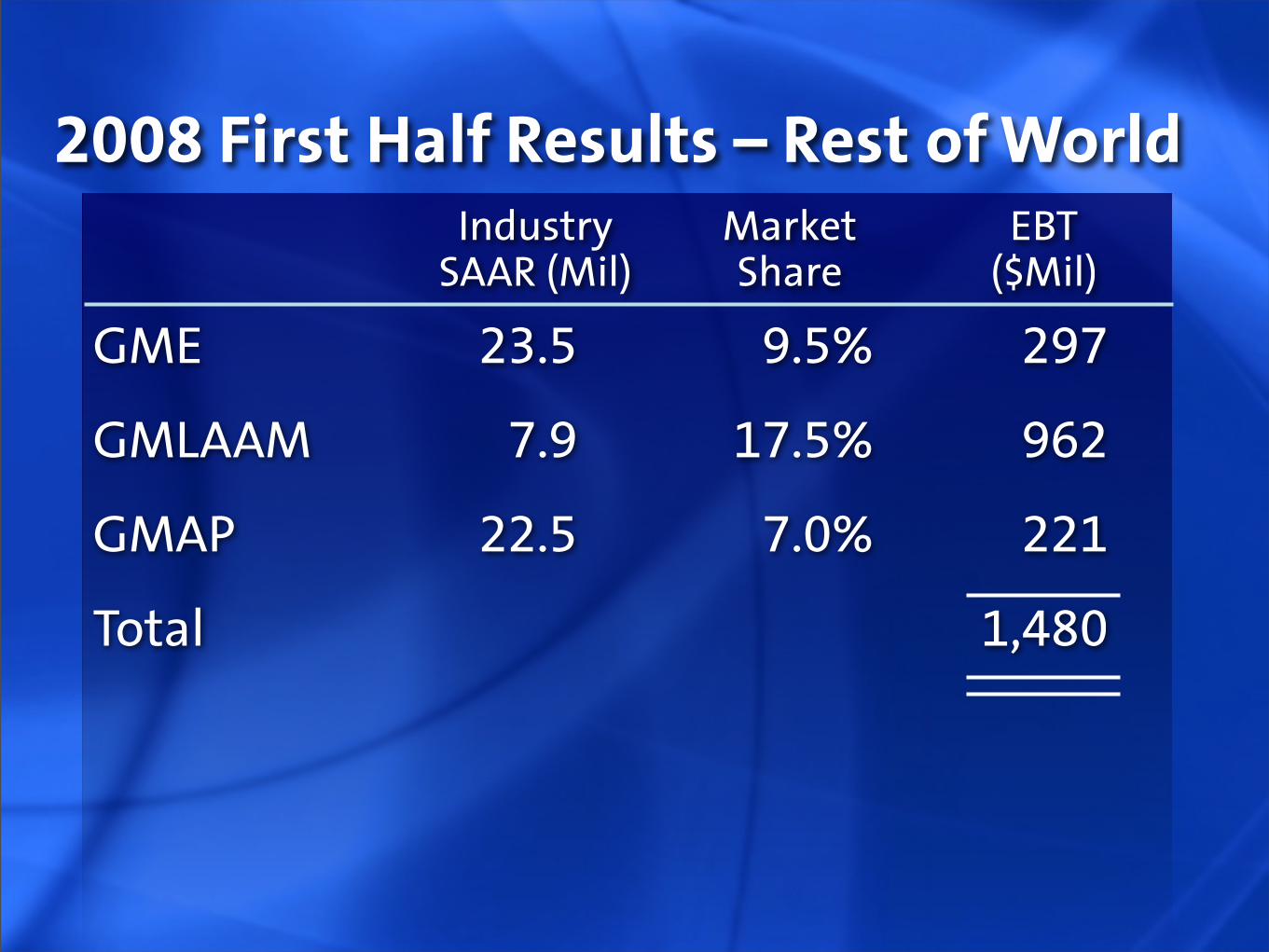

2008 First Half Results – Rest of World Industry Market EBT SAAR (Mil) Share ($Mil)

GME 23.5 9.5% 297

GMLAAM 7.9 17.5% 962

GMAP 22.5 7.0% 221

Total 1,480

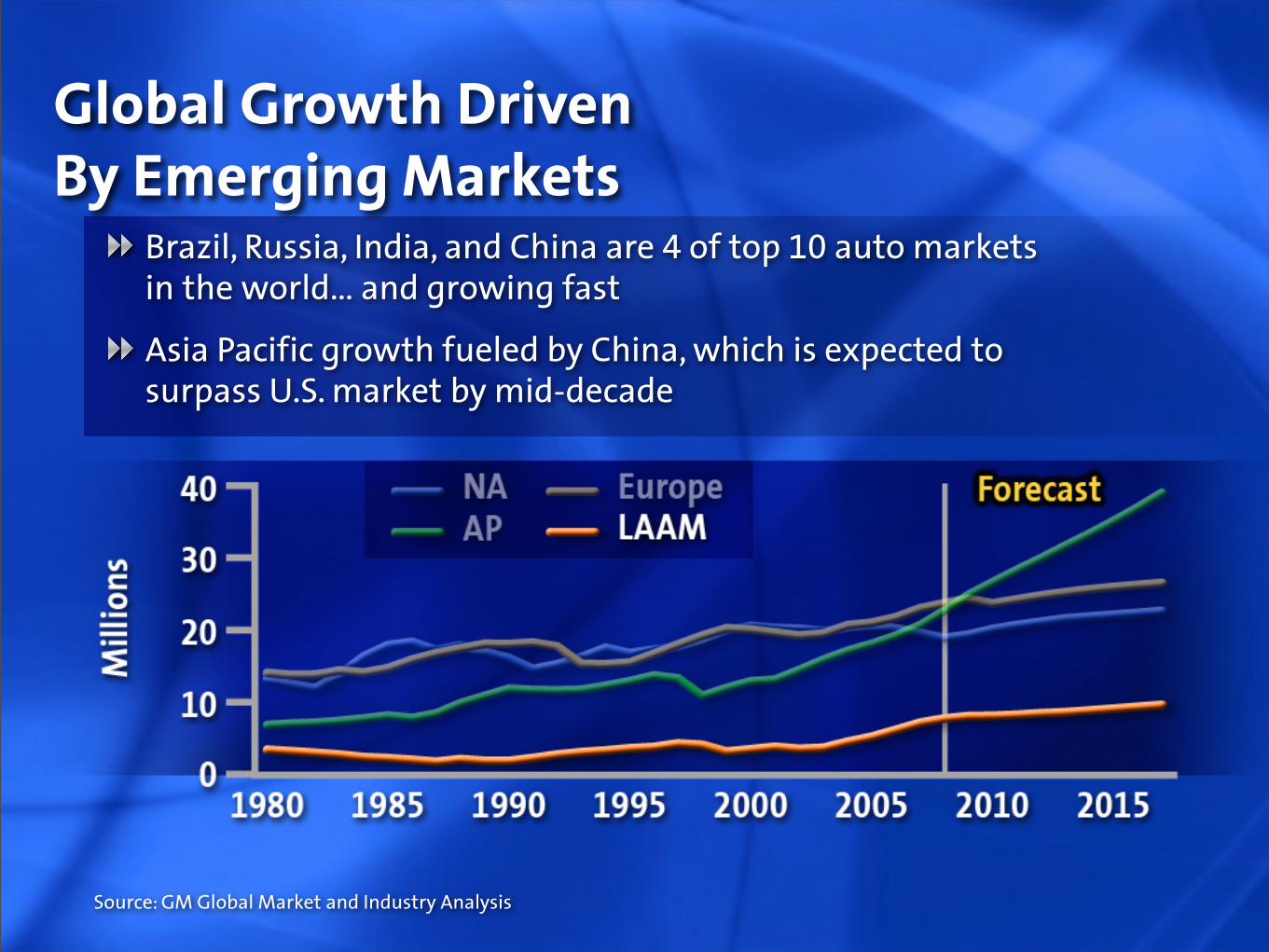

Global Growth Driven By Emerging Markets

Brazil, Russia, India, and China are 4 of top 10 auto markets in the world… and growing fast

Asia Pacific growth fueled by China, which is expected to surpass U.S. market by mid-decade

Source: GM Global Market and Industry Analysis

Running GM Globally

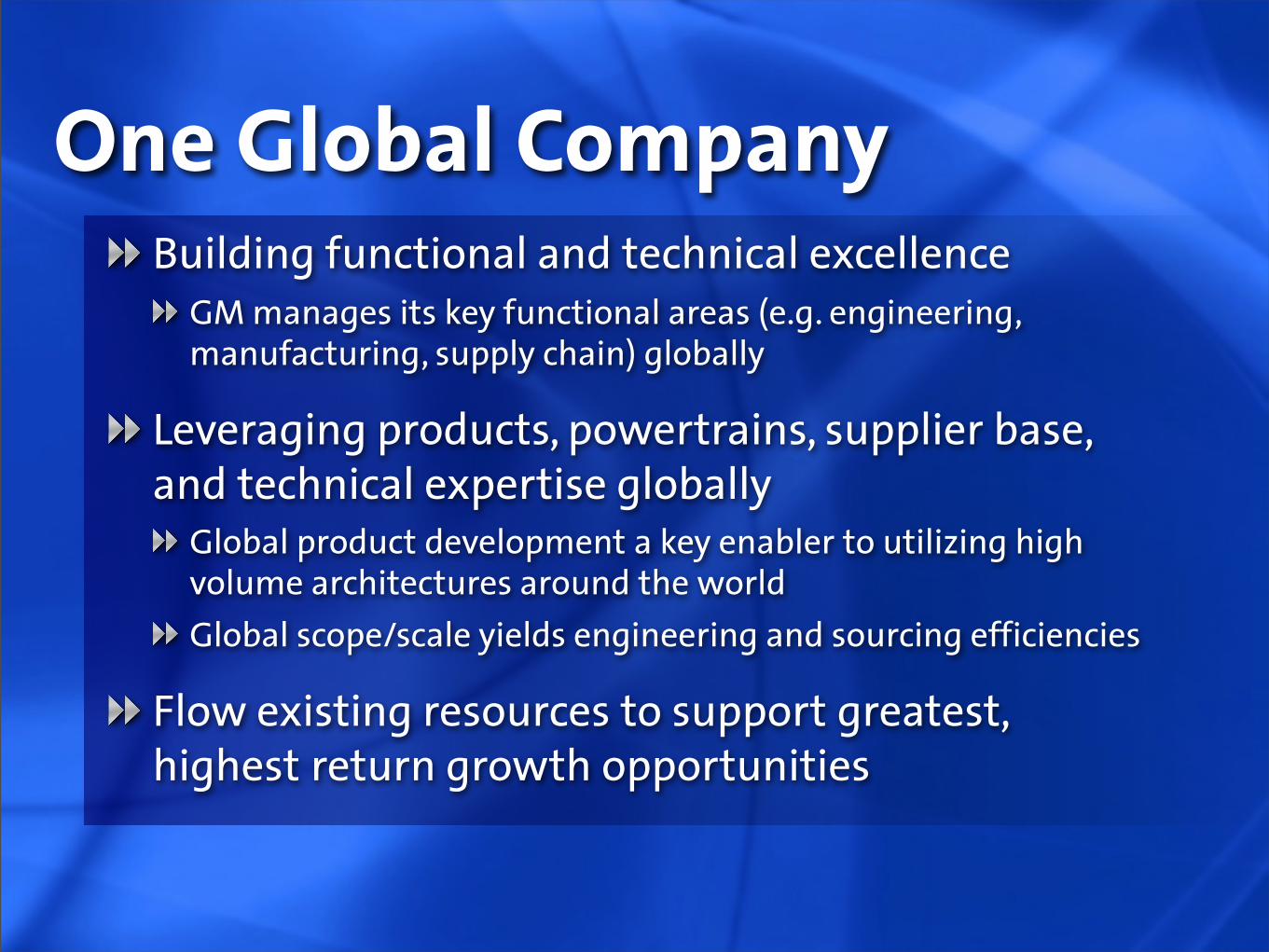

One Global CompanyBuilding functional and technical excellence

GM manages its key functional areas (e.g. engineering, manufacturing, supply chain) globally

Leveraging products, powertrains, supplier base, and technical expertise globally

Global product development a key enabler to utilizing high volume architectures around the world

Global scope/scale yields engineering and sourcing efficiencies

Flow existing resources to support greatest, highest return growth opportunities

Implications for Canada

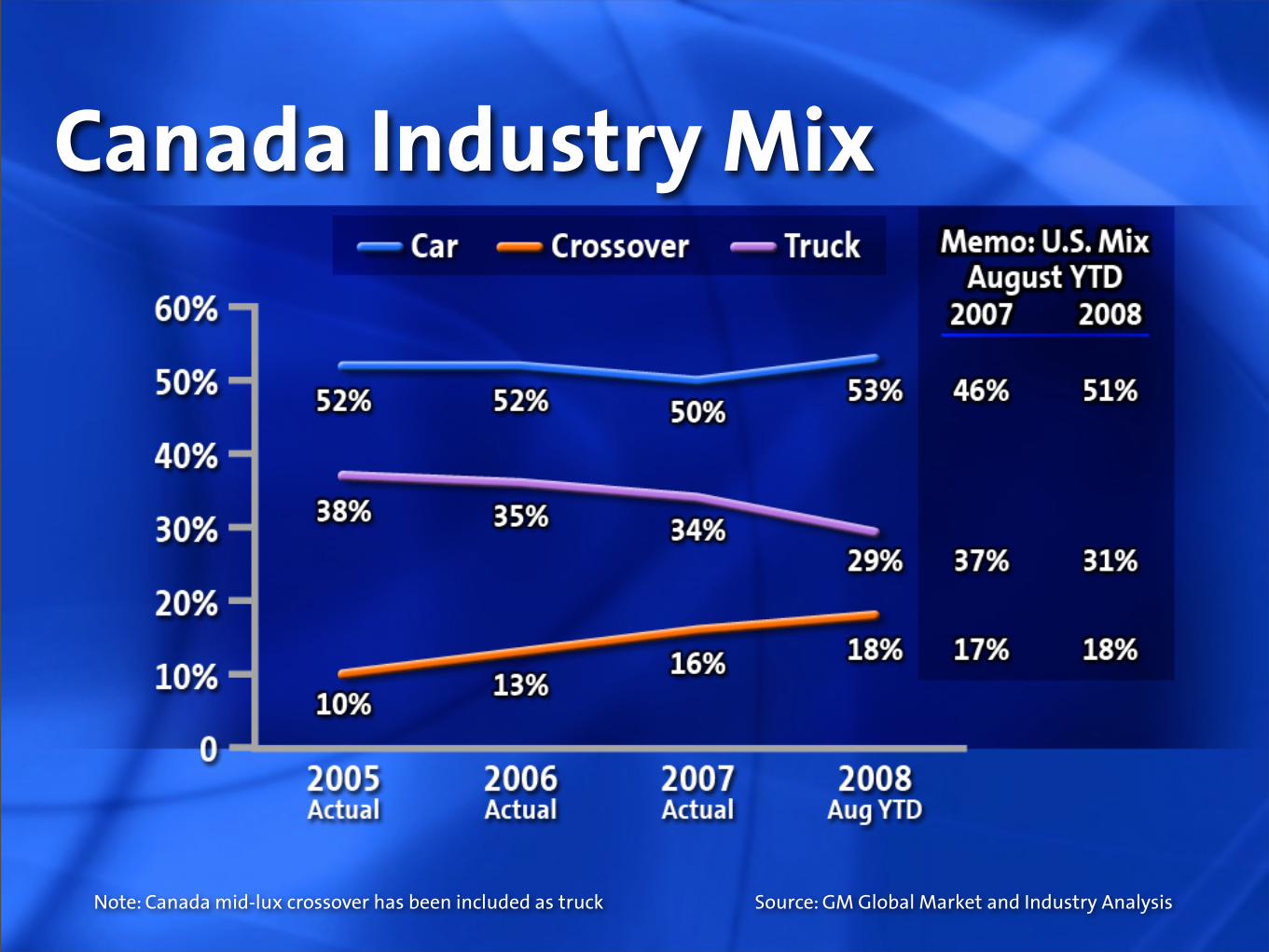

Canada Industry Mix

Note: Canada mid-lux crossover has been included as truck Source: GM Global Market and Industry Analysis

Shifting U.S. MixThe escalation of fuel prices has lead to a shift in U.S. market preferences to smaller more fuel efficient vehicles that have traditionally been more important in Canadian markets

As the U.S. portfolio transitions to a mix more comparable to Canada, increased volume and investment in key Canadian segments will result

To date, GM has responded by positioning 18 of the next 19 U.S. launches in car or crossover segments of which 18 will be available in Canada

ClosingRemarks

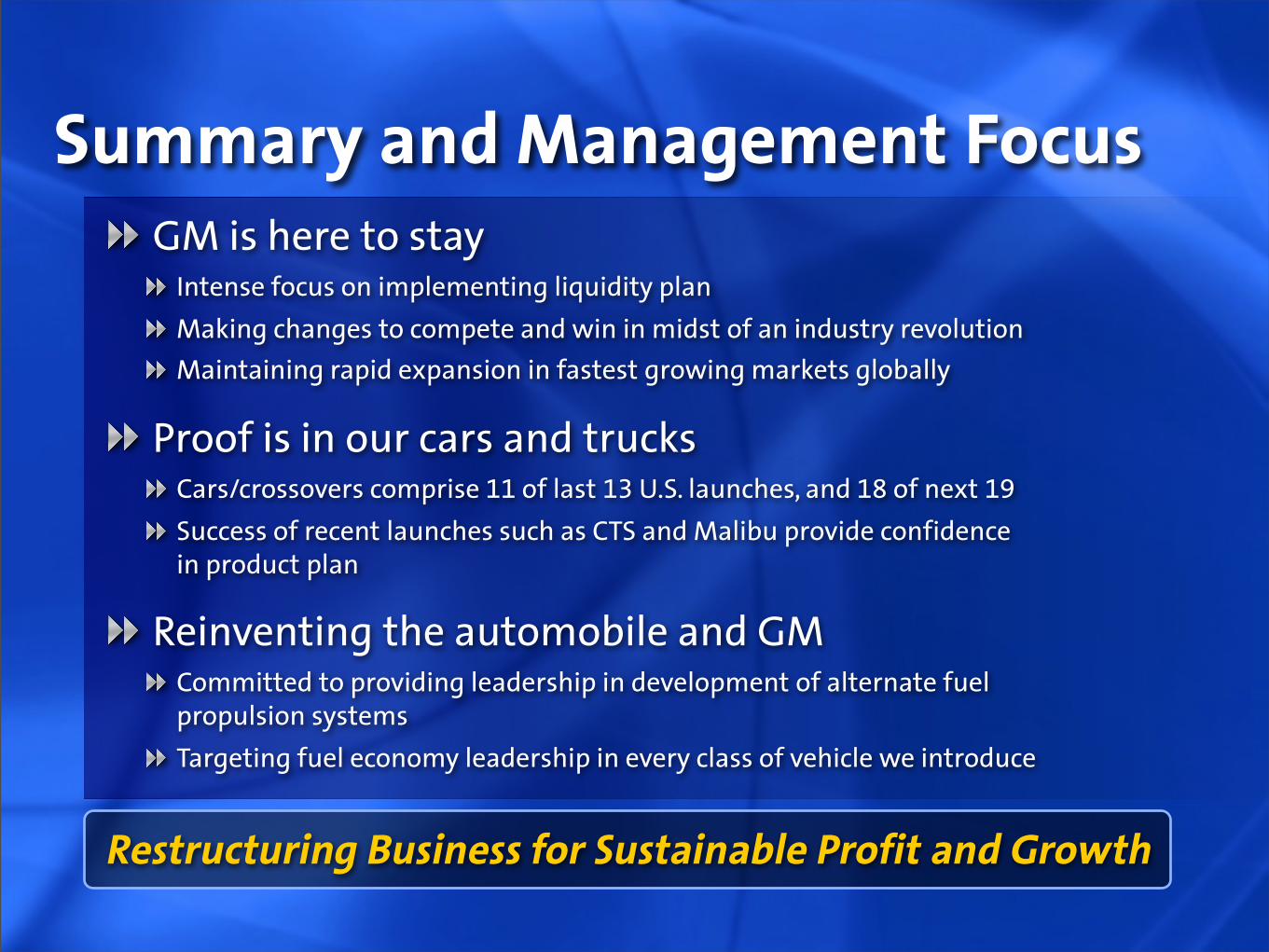

Summary and Management FocusGM is here to stay

Intense focus on implementing liquidity plan

Making changes to compete and win in midst of an industry revolution

Maintaining rapid expansion in fastest growing markets globally

Proof is in our cars and trucksCars/crossovers comprise 11 of last 13 U.S. launches, and 18 of next 19

Success of recent launches such as CTS and Malibu provide confidence in product plan

Reinventing the automobile and GMCommitted to providing leadership in development of alternate fuel propulsion systems

Targeting fuel economy leadership in every class of vehicle we introduce

Restructuring Business for Sustainable Profit and Growth