global competitiveness report 2004/2005 - · pdf fileexcerpt from / fragmento del global...

TRANSCRIPT

Excerpt from / Fragmento del

GLOBAL COMPETITIVENESS REPORT 2004/2005

By / Por World Economic Forum

in collaboration with / con la colaboración de

IESE Business School

and the support of / y el apoyo de Nissan Chair of Corporate Strategy and International Business

Anselmo Rubiralta Center for Globalization and Business Strategy

Including/Incluye:

- Executive Summary - Chapter 1.2: Building the Microeconomic Foundations of Prosperity

- Competitiveness Spain

You can search for the full text at / Puede buscar el texto completo en:

http://www.weforum.org/site/homepublic.nsf/Content/Global+Competitiveness+Programme%5CGlobal+Competitiveness+Report

xi

Exec

utiv

e Su

mm

ary

Executive SummaryAUGUSTO LOPEZ-CLAROS, World Economic Forum

For well over two decades the World Economic Forumhas been trying to shed light on the question of why somecountries are able to grow on a sustained basis for pro-longed periods of time, in the process pulling large seg-ments of the population out of poverty, while othersremain stagnant or, worse, actually see an erosion of livingstandards.Through its flagship publication, The GlobalCompetitiveness Report, the World Economic Forum has led the way in assessing the competitiveness of nations.

The Forum may be in a singularly advantageous posi-tion, for at least two reasons, to contribute meaningfully to the debate on the key building blocks of successful economic development and improved competitiveness.First, it brings key representatives from the private sectorand the corporate world together with a broad spectrumof senior policymakers in government, creating opportuni-ties for the thoughtful exchange of ideas and experienceson best practices.This exchange may be an important catalyst in identifying the most critical factors in thedevelopment process.The role of corruption in delayingthe development process, the central importance ofwomen’s education for boosting per capita incomes, theinterplay between political and civil rights and the will-ingness of the public to engage in economic activity, therole of a free press, and the type of safety net arrangementsthat governments put in place to enhance the ability ofeconomic agents to participate in the life of the nation,are but some of the topics that have been at the centre ofthe agenda in many of the summits and other interactionsorganized by the World Economic Forum.

Second, the Forum has developed a vehicle, theExecutive Opinion Survey (EOS), which annually conveysa wealth of information about the obstacles to growth inmore than 100 countries, accounting for the lion’s share ofglobal GNP.Through the Survey, business executives inthese countries assess the importance of a broad range offactors central to creating a healthy business environmentin support of successful and productive economic activity.The tax and regulatory environment, labor market legisla-tion, the overall macroeconomic environment, the preva-lence of corruption and other irregular practices in theeconomy at large, the quality of the country’s infrastruc-ture and education are but a few of the areas covered bythe EOS. Over the years, the Survey has continued todeliver a treasure trove of information about both coun-try-specific strengths and weaknesses, and the challengesfaced by the business community. On the basis of theinformation provided by the EOS, the Country Profilesprepared by the Forum offer extremely valuable informa-tion for policymakers, aid agencies and others, working to improve economic performance and the quality of people’s lives.

The methodology used by the Forum to assessnational competitiveness has evolved over time, taking intoaccount the latest thinking on the factors driving compet-itiveness and growth.The Forum first introduced theGrowth Competitiveness Index (GCI) three years ago, in col-laboration with Professors Jeffrey Sachs and JohnMcArthur, in the Global Competitiveness Report2001–2002.The GCI aims specifically to gauge the abilityof the world’s economies to achieve sustained economicgrowth over the medium to long term. It primarily assess-es the impact of those factors that economic theory andthe accumulated experience of policymakers in a broadrange of countries have shown to be critical for growth,whether narrowly focused on elements of the macroeco-nomic environment or, reflecting the latest insights in theeconomics literature, institutional and other factors.

Professor Michael Porter’s Business CompetitivenessIndex, presented in Chapter 1.2 in this volume, is an espe-cially useful complement to the GCI, with its specialemphasis on a range of company-specific factors con-ducive to improved efficiency and productivity at themicro level.

The Growth Competitiveness IndexThe GCI is composed of three “pillars,” all of which arewidely accepted as being critical to economic growth: thequality of the macroeconomic environment, the state of acountry’s public institutions, and, given the increasingimportance of technology in the development process, acountry’s technological readiness. Using a combination ofpublicly available hard data, and information provided inthe Forum’s Executive Opinion Survey—which providesmore textured qualitative information on difficult-to-measure concepts—these three pillars are brought togetherin the three indexes of the GCI: the macroeconomic envi-ronment index, the public institutions index, and the tech-nology index.

Sachs and McArthur strongly emphasized that therole of technology in the growth process differs for coun-tries, depending on their particular stage of development.It is widely understood that technological innovation isrelatively more important for growth in countries close tothe technological frontier. Innovation will be key inSweden, but the adoption of foreign technologies, or thekind of technology transfer frequently associated with for-eign direct investment will be relatively more important ina country such as the Czech Republic. For this reason, inestimating the GCI, economies are separated into twogroups: the core economies, i.e. those for which technolog-ical innovation is critical for growth, and non-coreeconomies, i.e. those which can still grow by adoptingtechnologies developed abroad.

The critical importance of technological innovationfor core economies is taken into account in the technolo-gy index. Specifically, more weight is given to innovation,by means of the innovation subindex, for the coreeconomies, than for the non-core.To make a further dis-tinction, an additional measure is used of the ability ofnon-core economies to adopt technology from abroad:the technology transfer subindex. Finally, since the deter-minants of economic competitiveness vary for core andnon-core economies, the weighting of the three indexes inthe overall GCI differs between the two groups. For thenon-core economies, more weight is given to the qualityof institutions and the macroeconomic environment, sincethese countries can still make progress in achieving highergrowth by getting their fundamentals in order.

On the other hand, for the core economies that arecloser to the technological frontier, more weight is placedon technology. It is, of course, important for these coun-tries to have a sound macroeconomic environment andstrong institutions, but these economies will typically havelong ago entered a period characterized by “institutionalstability.” For these countries to continue to grow theymust innovate.This is why more weight is placed, for thecore innovators, on technology, than on the other two pil-lars. Chapter 1.1, by Jennifer Blanke and Augusto Lopez-Claros provides specific details on the composition andconstruction of the GCI, which this year covers a total of104 countries.

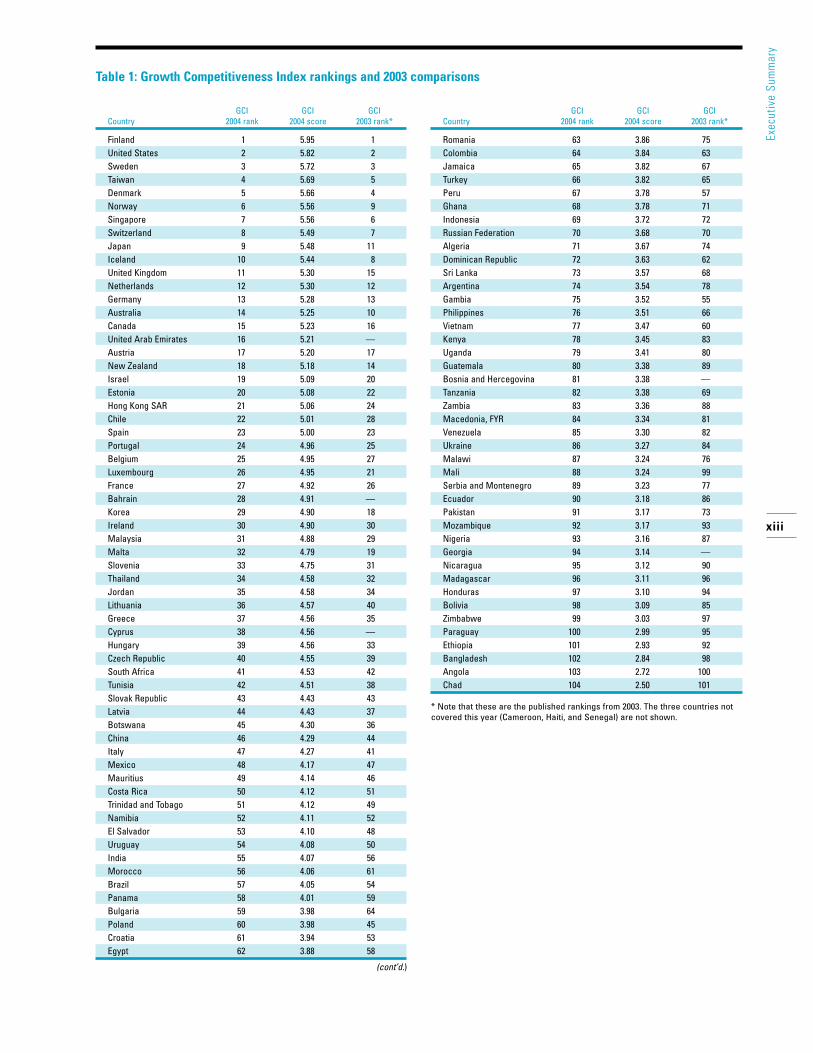

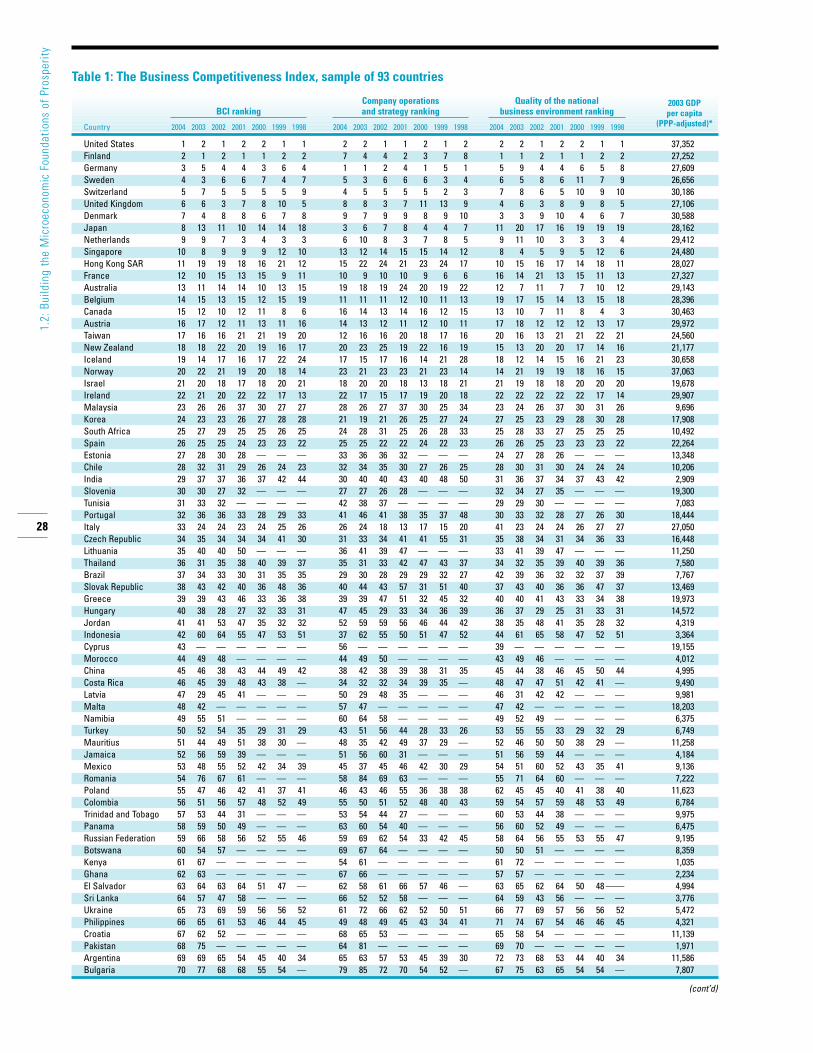

The Competitiveness Rankings for 2004Table 1 presents the rankings from this year’s GCI. For the third time during the last four years Finland tops therankings.The country is extremely well managed at themacroeconomic level, and scores very high in those measures which assess the quality of its public institutions.Moreover, Finland has very low levels of corruption andits firms operate in a legal environment in which there iswidespread respect for contracts and the rule of law.Finland’s private sector shows a proclivity for adoptingnew technologies, and nurtures a culture of innovation.Especially noteworthy is the fact that, for several years,Finland has been running budget surpluses, in anticipationof future claims on the budget associated with the agingof its population.The United States is ranked second, withoverall technological supremacy, and especially high scoresfor such indicators as companies’ spending on R&D, thecreativity of its scientific community, personal computerand internet penetration rates. However, these are partlyoffset by a weaker performance in those areas which cap-ture the quality of the macroeconomic environment andits public institutions.

As compared to the results of 2003, nine out of ten ofthe top performers remain in this category.Among these

xii

Exec

utiv

e Su

mm

ary

xiii

Exec

utiv

e Su

mm

ary

GCI GCI GCI Country 2004 rank 2004 score 2003 rank*

Finland 1 5.95 1United States 2 5.82 2Sweden 3 5.72 3Taiwan 4 5.69 5Denmark 5 5.66 4Norway 6 5.56 9Singapore 7 5.56 6Switzerland 8 5.49 7Japan 9 5.48 11Iceland 10 5.44 8United Kingdom 11 5.30 15Netherlands 12 5.30 12Germany 13 5.28 13Australia 14 5.25 10Canada 15 5.23 16United Arab Emirates 16 5.21 —Austria 17 5.20 17New Zealand 18 5.18 14Israel 19 5.09 20Estonia 20 5.08 22Hong Kong SAR 21 5.06 24Chile 22 5.01 28Spain 23 5.00 23Portugal 24 4.96 25Belgium 25 4.95 27Luxembourg 26 4.95 21France 27 4.92 26Bahrain 28 4.91 —Korea 29 4.90 18Ireland 30 4.90 30Malaysia 31 4.88 29Malta 32 4.79 19Slovenia 33 4.75 31Thailand 34 4.58 32Jordan 35 4.58 34Lithuania 36 4.57 40Greece 37 4.56 35Cyprus 38 4.56 —Hungary 39 4.56 33Czech Republic 40 4.55 39South Africa 41 4.53 42Tunisia 42 4.51 38Slovak Republic 43 4.43 43Latvia 44 4.43 37Botswana 45 4.30 36China 46 4.29 44Italy 47 4.27 41Mexico 48 4.17 47Mauritius 49 4.14 46Costa Rica 50 4.12 51Trinidad and Tobago 51 4.12 49Namibia 52 4.11 52El Salvador 53 4.10 48Uruguay 54 4.08 50India 55 4.07 56Morocco 56 4.06 61Brazil 57 4.05 54Panama 58 4.01 59Bulgaria 59 3.98 64Poland 60 3.98 45Croatia 61 3.94 53Egypt 62 3.88 58

(cont’d.)

GCI GCI GCI Country 2004 rank 2004 score 2003 rank*

Romania 63 3.86 75Colombia 64 3.84 63Jamaica 65 3.82 67Turkey 66 3.82 65Peru 67 3.78 57Ghana 68 3.78 71Indonesia 69 3.72 72Russian Federation 70 3.68 70Algeria 71 3.67 74Dominican Republic 72 3.63 62Sri Lanka 73 3.57 68Argentina 74 3.54 78Gambia 75 3.52 55Philippines 76 3.51 66Vietnam 77 3.47 60Kenya 78 3.45 83Uganda 79 3.41 80Guatemala 80 3.38 89Bosnia and Hercegovina 81 3.38 —Tanzania 82 3.38 69Zambia 83 3.36 88Macedonia, FYR 84 3.34 81Venezuela 85 3.30 82Ukraine 86 3.27 84Malawi 87 3.24 76Mali 88 3.24 99Serbia and Montenegro 89 3.23 77Ecuador 90 3.18 86Pakistan 91 3.17 73Mozambique 92 3.17 93Nigeria 93 3.16 87Georgia 94 3.14 —Nicaragua 95 3.12 90Madagascar 96 3.11 96Honduras 97 3.10 94Bolivia 98 3.09 85Zimbabwe 99 3.03 97Paraguay 100 2.99 95Ethiopia 101 2.93 92Bangladesh 102 2.84 98Angola 103 2.72 100Chad 104 2.50 101

* Note that these are the published rankings from 2003. The three countries notcovered this year (Cameroon, Haiti, and Senegal) are not shown.

Table 1: Growth Competitiveness Index rankings and 2003 comparisons

leaders, the largest improvement has been registered byNorway, which has moved up from ninth to sixth placesince 2003. Norway improved in all three areas of theIndex, most particularly with regard to its public institu-tions, driven by a much better score in the area of con-tracts and law. Indeed, the Nordic countries all occupyprivileged positions in the GCI ranking.

The GCI does a reasonably good job not only ofranking countries vis-à-vis each other, but also of trackingshifts in rank over time.This is perhaps not surprising inthe case of the macroeconomic environment index, whichis made up overwhelmingly of hard data variables—Norway, Estonia, and New Zealand get credit for runningbudget surpluses, while Turkey, India, and Japan are penal-ized for running large deficits—but applies to other com-ponents of the GCI as well.

Those countries showing the largest drops in rankingsin 2004—Bolivia, the Dominican Republic, Pakistan,Peru, Philippines, Poland,Vietnam, to name some—are allcountries that have witnessed significant deteriorations inone or more areas tracked by the Index. Others, such asVenezuela and Zimbabwe, already low last year, havedropped even further. Indeed, all of these countries havebeen prominent in the pages of the international press.Highly visible instances of official corruption, a crack-down on press freedoms and other civil liberties whichcontribute to capital outflows and harden the mood of thebusiness community, political instability linked to domesticinfighting in some cases leading to civil unrest, a weaken-ing in the rule of law have, to a greater or lesser degree,been prominent in some of the above cases.

The reverse is also true: countries may move up inthe rankings, when they show not only improvements inthe macroeconomic environment—e.g.Argentina in 2003,following the country’s harrowing experiences the previ-ous year—but some other factors, directly or indirectlyreflected in those variables tracked by the index.We arenot puzzled by the significant improvement in the rank-ings of Bulgaria and Romania, for instance.These coun-tries have an appointment to keep with the EU in 2007,and are gradually gearing up to meet EU accession crite-ria. In Latin America, we note that Chile improved itsperformance significantly, moving up from 28th to 22ndplace in the overall rankings. Chile not only has the high-est ranking in Latin America, but the gap with respect toits nearest rival (Mexico) is a full 26 places; there is noother continent in the world where we can observe thissymbolic “migration” from the region, in terms of per-formance. Chile’s case is featured separately in Chapter 2.3of this Report.

In Asia, the rankings are quite stable, with some smallimprovements—notably Indonesia and, more significantly,Japan, the latter by two places—and some small drops inthe rankings, as with Malaysia and Thailand.There are

two countries in the region, which stand out for their significant drop in the rankings: Korea and Vietnam, thelatter noted above. Korea’s drop is linked to a significantdecline in the macroeconomic environment subindex,falling from 23rd last year to 35th this year; moreover,Korea also experienced declines in the other two areasmeasured by the GCI.Vietnam’s decline is linked to significant drops in all three areas, particularly with regardto public institutions and technology.

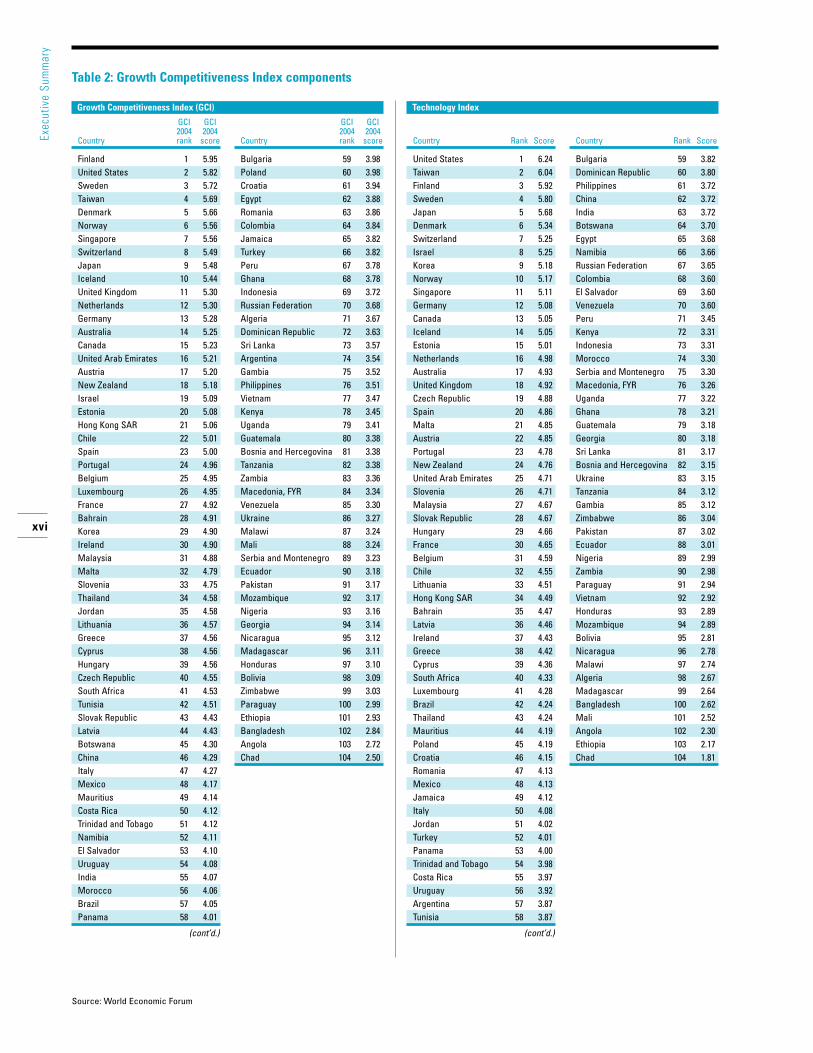

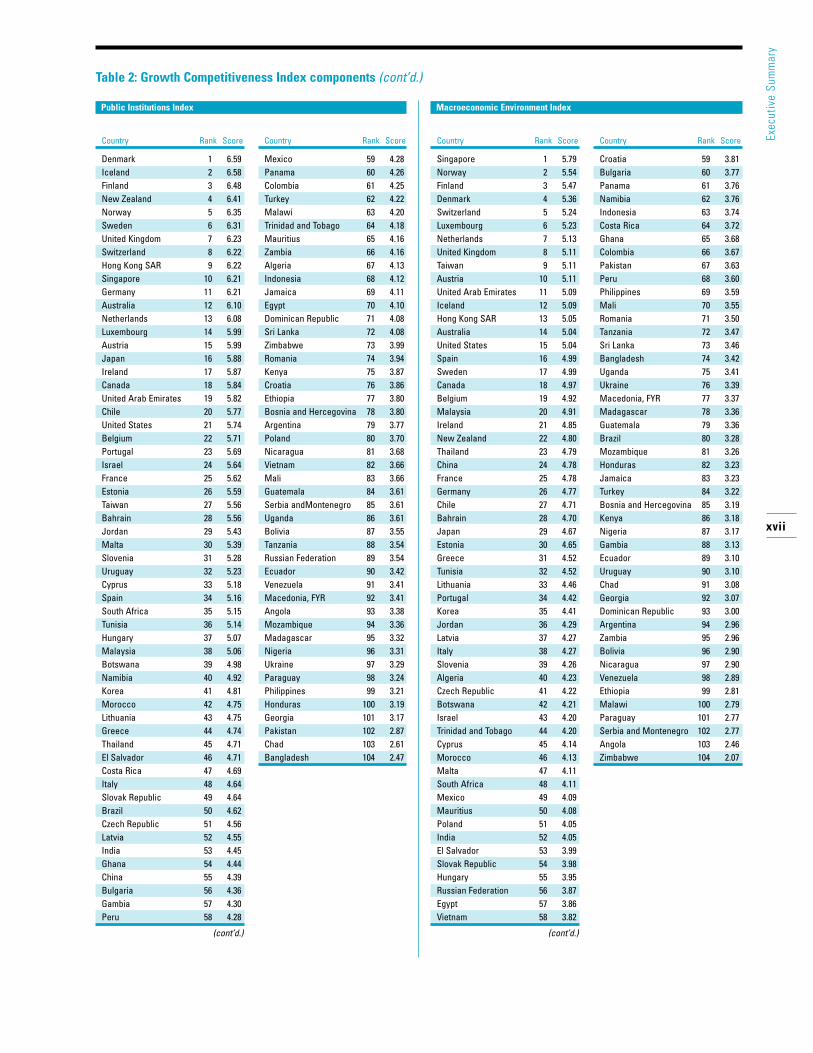

Countries in sub-Saharan Africa continue to holdplaces primarily at the bottom of the rankings, with a fewbright exceptions. South Africa improved its performancesomewhat, continuing to lead the region in competitive-ness, with an overall rank of 41, incidentally, well ahead of all countries in Latin America, except Chile. Likewise,while it did slip somewhat in the rankings, Botswana continues to outperform most of the other sub-SaharanAfrican countries, with a relatively strong performance,particularly in its public institutions, and a relativelyhealthy macroeconomic environment. Still, three of the five bottom-ranked countries are from this region,including Angola and Chad, which take the last two places in the ranking. It is clear that much work remainsto be done to improve competitiveness in Africa.Table 2provides more detailed information on the components of each of the three subindexes of the GCI for all 104countries in 2004.

The Business Competitiveness IndexThe Business Competitiveness Index (BCI) is a comple-ment to the medium-term, macroeconomic approach ofthe Growth Competitiveness Index. It evaluates theunderlying microeconomic conditions defining the currentsustainable level of productivity in each of the countriescovered, the underlying concept being that, while macro-economic and institutional factors are critical for nationalcompetitiveness, these are necessary but not sufficient fac-tors for creating wealth.Wealth is actually created at themicroeconomic level by the companies operating in eacheconomy.The BCI evaluates two specific areas, critical tothe business environment in each country: the sophistica-tion of the operating practices and strategies of companies,and the quality of the microeconomic business environ-ment in which a nation’s companies compete.The idea isthat, without these microeconomic capabilities, macroeco-nomic and institutional reforms will not bear full fruit.

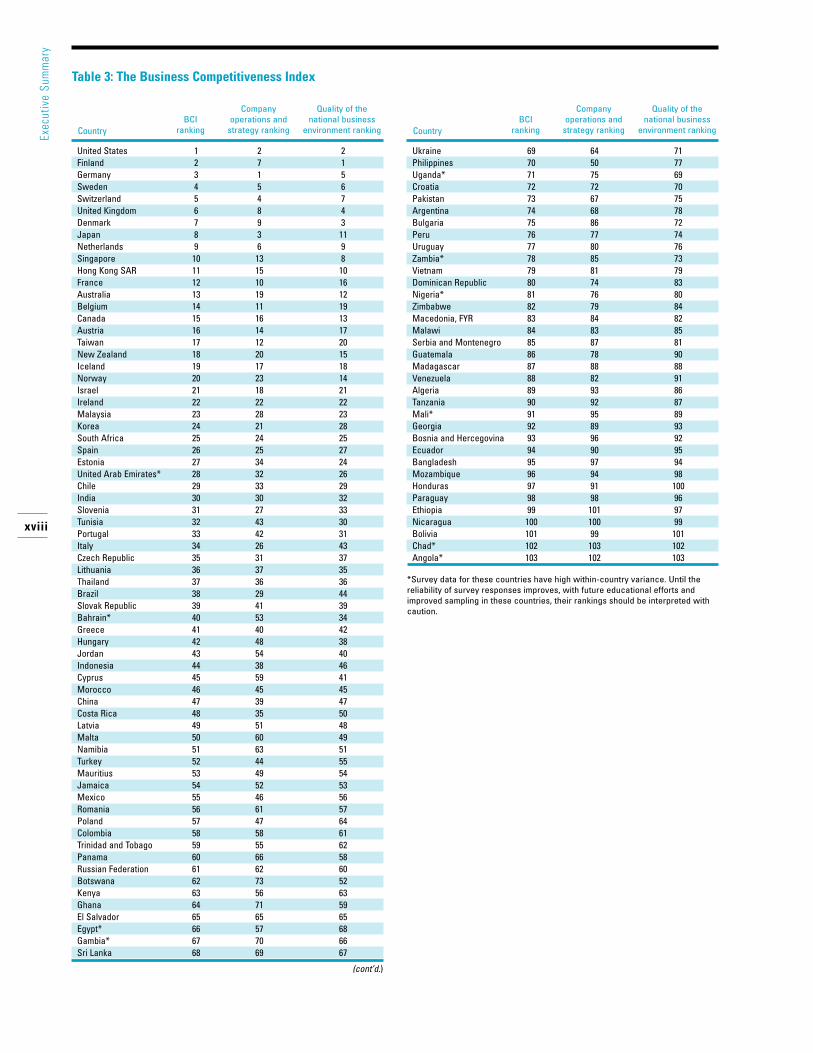

This year’s BCI rankings are shown in Table 3.Thefirst column shows the overall rankings, while the secondand third columns show the two interrelated subindexes:company operations and strategy, and the quality of thenational business environment.

The table shows that the United States has taken over the leading position from Finland, after dropping to

xiv

Exec

utiv

e Su

mm

ary

xv

Exec

utiv

e Su

mm

ary

second place last year.The United States benefited fromimprovements in the sophistication of marketing, the avail-ability of venture capital, the intensity of local competi-tion, local supplier quality, and local supplier quantity.Other advanced economies improving their rankingsinclude Hong Kong, by reflecting more sophisticatedfinancial markets and improvements in management prac-tices, Japan, by improving financial market sophisticationand improving quality of administrative services, andPortugal, by improving cluster strength. Japan registeredthe highest absolute improvement of its BCI score, fol-lowed by Hong Kong and Norway.

Advanced countries, which dropped in the rankingsinclude Italy, Malta, and Iceland. Italy dropped by a disap-pointing nine ranks, almost entirely driven by a deteriorat-ing business environment, now evaluated on a par withthat of Portugal and the Czech Republic. Italy deteriorat-ed especially in areas related to innovative capacity, such asuniversity-industry research collaboration, foreign technol-ogy licensing, government procurement of advanced tech-nology, company R&D spending, and venture capitalavailability.

Middle-income nations improving their business com-petitiveness rankings this year include Romania, Lithuania,the Slovak Republic, Russia, Namibia, and the Ukraine.Romania jumped by a remarkable 22 ranks, driven bystrong across-the-board improvements, especially in thearea of company sophistication. Romania’s improvementcomes after repeated slippage in the ranking since thecountry became part of The Global Competitiveness Reportin 2001.

Middle-income countries which have experienced afall in ranking include Latvia, the Dominican Republic,Poland, and Mauritius. Other countries with significantabsolute drops in BCI scores include Thailand andMexico. Latvia has moved back to a level consistent withits longer-term trajectory; last year’s strong improvementproved to be unsustainable optimism.The DominicanRepublic, down 13 places, continues the trend set by alarge drop last year, driven particularly by a decline inopenness to imports, and in the sophistication of its finan-cial market.

Among low-income countries, Indonesia made thegreatest improvement, jumping a remarkable 18 ranks.After years of turmoil, the country is now back to its 2000business competitiveness level.While improvements wereregistered in areas across the board, they were strongest inmeasures of company sophistication.Another low-incomecountry with large improvements is India, up 8 ranks,showing the benefits of increased company sophisticationand strengthened clusters.Vietnam slipped significantly,down 23 places, after a number of years of steadyimprovement. Conditions worsened most in areas relatedto technology and government administration.

As explained above, the GCI and the BCI measurecomplementary dimensions of competitiveness. Figure 1compares the two rankings for 2004, revealing their highcorrelation.

A look ahead—the new Global Competitiveness IndexOver the last several years the Growth Competitiveness Indexhas been a useful tool in thinking about key macroeco-nomic and institutional elements, critical to the growthprocess.The present rankings continue to provide policy-makers, businesses and organizations of civil society withvaluable insights into areas where further progress is calledfor, in order to improve the environment for private sectoreconomic activity, and generate sustainable growth.

The considerable utility of the GCI notwithstanding,the vertiginous pace of change of the global economy hasbrought into sharper focus the increasing role played by anumber of other factors in enhancing the ability of coun-tries to grow.The swift pace of innovation in informationand communications technology, and the concomitant fallin the costs of communication is leading to an accelera-tion in the pace of integration of the world economy.Theincreasingly global perspective of businesses in formulatingtheir strategies and decision making—already manifestinga global reach in the search for new markets and sourcesof supply—has now extended to the location of produc-tion, and resulted in the increasing internationalization ofthe labor force of the typical multinational corporation.Innovations in transportation, which have reduced the costof freight, mean that location is less of a factor than in thepast, and businesses are now looking for the right combi-nation of labor costs—coupled, ideally, with flexible labormarkets—skills, infrastructure, and the support provided bya good macroeconomic and institutional environment toreduce production costs.

Against the backdrop of these changes, countries arebeing forced to be increasingly creative, in order to main-tain their competitive edge.The role of multi-countryalliances in bringing together better combinations of capi-tal, labor, skills and regulatory frameworks for particularprojects is becoming more important. Countries with thenimbleness demanded for such cross-border arrangementsare reaping the benefits of higher economic growth ratesand improvements in living standards. Countries which arenot allocating sufficient resources to improve the qualityof their educational systems or to address major publichealth concerns, or which are otherwise engulfed in inter-nal conflicts and instability, are rapidly falling behind.Thenet effect of these trends is the growing complexity in the economic, social and political underpinnings of theenvironment faced by policymakers and business leaderseverywhere.This is not only putting enormous stress onthe institutions that sustain and support the global economy,

xvi

Exec

utiv

e Su

mm

ary

Table 2: Growth Competitiveness Index components

GCI GCI2004 2004

Country rank score

Finland 1 5.95United States 2 5.82Sweden 3 5.72Taiwan 4 5.69Denmark 5 5.66Norway 6 5.56Singapore 7 5.56Switzerland 8 5.49Japan 9 5.48Iceland 10 5.44United Kingdom 11 5.30Netherlands 12 5.30Germany 13 5.28Australia 14 5.25Canada 15 5.23United Arab Emirates 16 5.21Austria 17 5.20New Zealand 18 5.18Israel 19 5.09Estonia 20 5.08Hong Kong SAR 21 5.06Chile 22 5.01Spain 23 5.00Portugal 24 4.96Belgium 25 4.95Luxembourg 26 4.95France 27 4.92Bahrain 28 4.91Korea 29 4.90Ireland 30 4.90Malaysia 31 4.88Malta 32 4.79Slovenia 33 4.75Thailand 34 4.58Jordan 35 4.58Lithuania 36 4.57Greece 37 4.56Cyprus 38 4.56Hungary 39 4.56Czech Republic 40 4.55South Africa 41 4.53Tunisia 42 4.51Slovak Republic 43 4.43Latvia 44 4.43Botswana 45 4.30China 46 4.29Italy 47 4.27Mexico 48 4.17Mauritius 49 4.14Costa Rica 50 4.12Trinidad and Tobago 51 4.12Namibia 52 4.11El Salvador 53 4.10Uruguay 54 4.08India 55 4.07Morocco 56 4.06Brazil 57 4.05Panama 58 4.01

(cont’d.)

GCI GCI2004 2004

Country rank score

Bulgaria 59 3.98Poland 60 3.98Croatia 61 3.94Egypt 62 3.88Romania 63 3.86Colombia 64 3.84Jamaica 65 3.82Turkey 66 3.82Peru 67 3.78Ghana 68 3.78Indonesia 69 3.72Russian Federation 70 3.68Algeria 71 3.67Dominican Republic 72 3.63Sri Lanka 73 3.57Argentina 74 3.54Gambia 75 3.52Philippines 76 3.51Vietnam 77 3.47Kenya 78 3.45Uganda 79 3.41Guatemala 80 3.38Bosnia and Hercegovina 81 3.38Tanzania 82 3.38Zambia 83 3.36Macedonia, FYR 84 3.34Venezuela 85 3.30Ukraine 86 3.27Malawi 87 3.24Mali 88 3.24Serbia and Montenegro 89 3.23Ecuador 90 3.18Pakistan 91 3.17Mozambique 92 3.17Nigeria 93 3.16Georgia 94 3.14Nicaragua 95 3.12Madagascar 96 3.11Honduras 97 3.10Bolivia 98 3.09Zimbabwe 99 3.03Paraguay 100 2.99Ethiopia 101 2.93Bangladesh 102 2.84Angola 103 2.72Chad 104 2.50

Country Rank Score

United States 1 6.24Taiwan 2 6.04Finland 3 5.92Sweden 4 5.80Japan 5 5.68Denmark 6 5.34Switzerland 7 5.25Israel 8 5.25Korea 9 5.18Norway 10 5.17Singapore 11 5.11Germany 12 5.08Canada 13 5.05Iceland 14 5.05Estonia 15 5.01Netherlands 16 4.98Australia 17 4.93United Kingdom 18 4.92Czech Republic 19 4.88Spain 20 4.86Malta 21 4.85Austria 22 4.85Portugal 23 4.78New Zealand 24 4.76United Arab Emirates 25 4.71Slovenia 26 4.71Malaysia 27 4.67Slovak Republic 28 4.67Hungary 29 4.66France 30 4.65Belgium 31 4.59Chile 32 4.55Lithuania 33 4.51Hong Kong SAR 34 4.49Bahrain 35 4.47Latvia 36 4.46Ireland 37 4.43Greece 38 4.42Cyprus 39 4.36South Africa 40 4.33Luxembourg 41 4.28Brazil 42 4.24Thailand 43 4.24Mauritius 44 4.19Poland 45 4.19Croatia 46 4.15Romania 47 4.13Mexico 48 4.13Jamaica 49 4.12Italy 50 4.08Jordan 51 4.02Turkey 52 4.01Panama 53 4.00Trinidad and Tobago 54 3.98Costa Rica 55 3.97Uruguay 56 3.92Argentina 57 3.87Tunisia 58 3.87

(cont’d.)

Country Rank Score

Bulgaria 59 3.82Dominican Republic 60 3.80Philippines 61 3.72China 62 3.72India 63 3.72Botswana 64 3.70Egypt 65 3.68Namibia 66 3.66Russian Federation 67 3.65Colombia 68 3.60El Salvador 69 3.60Venezuela 70 3.60Peru 71 3.45Kenya 72 3.31Indonesia 73 3.31Morocco 74 3.30Serbia and Montenegro 75 3.30Macedonia, FYR 76 3.26Uganda 77 3.22Ghana 78 3.21Guatemala 79 3.18Georgia 80 3.18Sri Lanka 81 3.17Bosnia and Hercegovina 82 3.15Ukraine 83 3.15Tanzania 84 3.12Gambia 85 3.12Zimbabwe 86 3.04Pakistan 87 3.02Ecuador 88 3.01Nigeria 89 2.99Zambia 90 2.98Paraguay 91 2.94Vietnam 92 2.92Honduras 93 2.89Mozambique 94 2.89Bolivia 95 2.81Nicaragua 96 2.78Malawi 97 2.74Algeria 98 2.67Madagascar 99 2.64Bangladesh 100 2.62Mali 101 2.52Angola 102 2.30Ethiopia 103 2.17Chad 104 1.81

Growth Competitiveness Index (GCI) Technology Index

Source: World Economic Forum

xvii

Exec

utiv

e Su

mm

ary

Country Rank Score

Denmark 1 6.59Iceland 2 6.58Finland 3 6.48New Zealand 4 6.41Norway 5 6.35Sweden 6 6.31United Kingdom 7 6.23Switzerland 8 6.22Hong Kong SAR 9 6.22Singapore 10 6.21Germany 11 6.21Australia 12 6.10Netherlands 13 6.08Luxembourg 14 5.99Austria 15 5.99Japan 16 5.88Ireland 17 5.87Canada 18 5.84United Arab Emirates 19 5.82Chile 20 5.77United States 21 5.74Belgium 22 5.71Portugal 23 5.69Israel 24 5.64France 25 5.62Estonia 26 5.59Taiwan 27 5.56Bahrain 28 5.56Jordan 29 5.43Malta 30 5.39Slovenia 31 5.28Uruguay 32 5.23Cyprus 33 5.18Spain 34 5.16South Africa 35 5.15Tunisia 36 5.14Hungary 37 5.07Malaysia 38 5.06Botswana 39 4.98Namibia 40 4.92Korea 41 4.81Morocco 42 4.75Lithuania 43 4.75Greece 44 4.74Thailand 45 4.71El Salvador 46 4.71Costa Rica 47 4.69Italy 48 4.64Slovak Republic 49 4.64Brazil 50 4.62Czech Republic 51 4.56Latvia 52 4.55India 53 4.45Ghana 54 4.44China 55 4.39Bulgaria 56 4.36Gambia 57 4.30Peru 58 4.28

(cont’d.)

Country Rank Score

Mexico 59 4.28Panama 60 4.26Colombia 61 4.25Turkey 62 4.22Malawi 63 4.20Trinidad and Tobago 64 4.18Mauritius 65 4.16Zambia 66 4.16Algeria 67 4.13Indonesia 68 4.12Jamaica 69 4.11Egypt 70 4.10Dominican Republic 71 4.08Sri Lanka 72 4.08Zimbabwe 73 3.99Romania 74 3.94Kenya 75 3.87Croatia 76 3.86Ethiopia 77 3.80Bosnia and Hercegovina 78 3.80Argentina 79 3.77Poland 80 3.70Nicaragua 81 3.68Vietnam 82 3.66Mali 83 3.66Guatemala 84 3.61Serbia andMontenegro 85 3.61Uganda 86 3.61Bolivia 87 3.55Tanzania 88 3.54Russian Federation 89 3.54Ecuador 90 3.42Venezuela 91 3.41Macedonia, FYR 92 3.41Angola 93 3.38Mozambique 94 3.36Madagascar 95 3.32Nigeria 96 3.31Ukraine 97 3.29Paraguay 98 3.24Philippines 99 3.21Honduras 100 3.19Georgia 101 3.17Pakistan 102 2.87Chad 103 2.61Bangladesh 104 2.47

Country Rank Score

Singapore 1 5.79Norway 2 5.54Finland 3 5.47Denmark 4 5.36Switzerland 5 5.24Luxembourg 6 5.23Netherlands 7 5.13United Kingdom 8 5.11Taiwan 9 5.11Austria 10 5.11United Arab Emirates 11 5.09Iceland 12 5.09Hong Kong SAR 13 5.05Australia 14 5.04United States 15 5.04Spain 16 4.99Sweden 17 4.99Canada 18 4.97Belgium 19 4.92Malaysia 20 4.91Ireland 21 4.85New Zealand 22 4.80Thailand 23 4.79China 24 4.78France 25 4.78Germany 26 4.77Chile 27 4.71Bahrain 28 4.70Japan 29 4.67Estonia 30 4.65Greece 31 4.52Tunisia 32 4.52Lithuania 33 4.46Portugal 34 4.42Korea 35 4.41Jordan 36 4.29Latvia 37 4.27Italy 38 4.27Slovenia 39 4.26Algeria 40 4.23Czech Republic 41 4.22Botswana 42 4.21Israel 43 4.20Trinidad and Tobago 44 4.20Cyprus 45 4.14Morocco 46 4.13Malta 47 4.11South Africa 48 4.11Mexico 49 4.09Mauritius 50 4.08Poland 51 4.05India 52 4.05El Salvador 53 3.99Slovak Republic 54 3.98Hungary 55 3.95Russian Federation 56 3.87Egypt 57 3.86Vietnam 58 3.82

(cont’d.)

Country Rank Score

Croatia 59 3.81Bulgaria 60 3.77Panama 61 3.76Namibia 62 3.76Indonesia 63 3.74Costa Rica 64 3.72Ghana 65 3.68Colombia 66 3.67Pakistan 67 3.63Peru 68 3.60Philippines 69 3.59Mali 70 3.55Romania 71 3.50Tanzania 72 3.47Sri Lanka 73 3.46Bangladesh 74 3.42Uganda 75 3.41Ukraine 76 3.39Macedonia, FYR 77 3.37Madagascar 78 3.36Guatemala 79 3.36Brazil 80 3.28Mozambique 81 3.26Honduras 82 3.23Jamaica 83 3.23Turkey 84 3.22Bosnia and Hercegovina 85 3.19Kenya 86 3.18Nigeria 87 3.17Gambia 88 3.13Ecuador 89 3.10Uruguay 90 3.10Chad 91 3.08Georgia 92 3.07Dominican Republic 93 3.00Argentina 94 2.96Zambia 95 2.96Bolivia 96 2.90Nicaragua 97 2.90Venezuela 98 2.89Ethiopia 99 2.81Malawi 100 2.79Paraguay 101 2.77Serbia and Montenegro 102 2.77Angola 103 2.46Zimbabwe 104 2.07

Table 2: Growth Competitiveness Index components (cont’d.)

Public Institutions Index Macroeconomic Environment Index

xviii

Exec

utiv

e Su

mm

ary

Country

United States 1 2 2Finland 2 7 1Germany 3 1 5Sweden 4 5 6Switzerland 5 4 7United Kingdom 6 8 4Denmark 7 9 3Japan 8 3 11Netherlands 9 6 9Singapore 10 13 8Hong Kong SAR 11 15 10France 12 10 16Australia 13 19 12Belgium 14 11 19Canada 15 16 13Austria 16 14 17Taiwan 17 12 20New Zealand 18 20 15Iceland 19 17 18Norway 20 23 14Israel 21 18 21Ireland 22 22 22Malaysia 23 28 23Korea 24 21 28South Africa 25 24 25Spain 26 25 27Estonia 27 34 24United Arab Emirates* 28 32 26Chile 29 33 29India 30 30 32Slovenia 31 27 33Tunisia 32 43 30Portugal 33 42 31Italy 34 26 43Czech Republic 35 31 37Lithuania 36 37 35Thailand 37 36 36Brazil 38 29 44Slovak Republic 39 41 39Bahrain* 40 53 34Greece 41 40 42Hungary 42 48 38Jordan 43 54 40Indonesia 44 38 46Cyprus 45 59 41Morocco 46 45 45China 47 39 47Costa Rica 48 35 50Latvia 49 51 48Malta 50 60 49Namibia 51 63 51Turkey 52 44 55Mauritius 53 49 54Jamaica 54 52 53Mexico 55 46 56Romania 56 61 57Poland 57 47 64Colombia 58 58 61Trinidad and Tobago 59 55 62Panama 60 66 58Russian Federation 61 62 60Botswana 62 73 52Kenya 63 56 63Ghana 64 71 59El Salvador 65 65 65Egypt* 66 57 68Gambia* 67 70 66Sri Lanka 68 69 67

(cont’d.)

Country

Ukraine 69 64 71Philippines 70 50 77Uganda* 71 75 69Croatia 72 72 70Pakistan 73 67 75Argentina 74 68 78Bulgaria 75 86 72Peru 76 77 74Uruguay 77 80 76Zambia* 78 85 73Vietnam 79 81 79Dominican Republic 80 74 83Nigeria* 81 76 80Zimbabwe 82 79 84Macedonia, FYR 83 84 82Malawi 84 83 85Serbia and Montenegro 85 87 81Guatemala 86 78 90Madagascar 87 88 88Venezuela 88 82 91Algeria 89 93 86Tanzania 90 92 87Mali* 91 95 89Georgia 92 89 93Bosnia and Hercegovina 93 96 92Ecuador 94 90 95Bangladesh 95 97 94Mozambique 96 94 98Honduras 97 91 100Paraguay 98 98 96Ethiopia 99 101 97Nicaragua 100 100 99Bolivia 101 99 101Chad* 102 103 102Angola* 103 102 103

*Survey data for these countries have high within-country variance. Until thereliability of survey responses improves, with future educational efforts andimproved sampling in these countries, their rankings should be interpreted withcaution.

Table 3: The Business Competitiveness Index

BCI ranking

Company operations and

strategy ranking

Quality of the national business

environment rankingBCI

ranking

Company operations and

strategy ranking

Quality of the national business

environment ranking

xix

Exec

utiv

e Su

mm

ary

but is also changing our understanding of what areemerging as the key factors determining a country’sgrowth performance.

To address some of these challenges, we have beenworking with Xavier Sala-i-Martin and Elsa Artadi todevelop a more comprehensive competitiveness index.Reflecting the need to broaden our scope and look at alarger set of factors, the new index will bring into focus amuch richer set of pillars: human capital, labor and finan-cial markets efficiency, openness and market size, quality ofinfrastructure, to name a few of the new ones being incor-porated; in this spirit, it will be called the GlobalCompetitiveness Index. Chapter 1.3 of this Report is anexcellent presentation of the work that has been done todate. 2004 therefore constitutes a transition year betweenthe presentation of two indexes, the GCI and the BCI,and the subsequent consolidation of the World EconomicForum’s competitiveness work into a single index—theGlobal Competitiveness Index.

Selected issues of competitiveness and special topicsThis year’s Report contains a number of studies whichaddress different aspects of competitiveness and, more gen-erally, themes which emanate from the World EconomicForum’s deep concern with growth and development andthe state of the world. Some of these studies draw directlyfrom the Executive Opinion Survey for their analysis and

insight. Others are concerned with a broader set of issuesat the heart of the development agenda.All are businessrelevant, and highlight a range of issues which are various-ly shaping the global economic and business environment.

Selected issues of competitivenessDaniel Kaufmann’s “Corruption, Governance andSecurity: Challenges for the Rich Countries and theWorld” is an important addition to the literature in anincreasingly important field.Traditionally, governance andcorruption challenges have been seen as especially daunt-ing in poorer countries, with the richer ones viewed asgood examples, with their relative law and order, and welldeveloped institutions. Others might view them as publicsector problems, divorced from global governance or secu-rity issues. Using an empirical approach, based on thisyear’s EOS, Kaufmann challenges these notions, and showsus a more complex reality, revealing more subtle, yet costlymanifestations of misgovernance, afflicting not only poor,but rich countries as well.The traditional definition ofcorruption as the commission of an illegal act, such asoutright bribery, is here broadened to include new meas-ures of “legal corruption,” seen as the collusion of at leasttwo parties, typically from the public and private sectors,and where the rules of the game, laws and institutions areused, via influence peddling and even capture, to benefitvested interests.

0

10

20

30

40

50

60

70

80

90

100

0 20 40 60 80 100

Uruguay

India

Malta

Germany

Taiwan

Norway

Algeria

Indonesia

Botswana

Pakistan

France

Iceland

United States

Finland

SwedenSwitzerland

Hong Kong SAR

Belgium

United Arab Emirates

South Africa

Bosnia and Herzegovina

UkraineKenya

Zimbabwe

Portugal Brazil

Bulgaria

Figure 1: Growth and Business Competitiveness rankings

Bus

ines

s Co

mpe

titiv

enes

s ra

nkin

g

Growth Competitiveness ranking

By analyzing the interaction between rich countrytransnationals and the public sectors in emerging coun-tries, Kaufmann finds that ethics and corruption pose aserious challenge for many rich countries, and that theyrepresent key determinants of a country’s competitiveness,shaping its investment climate. Kaufmann ends his chapterwith an insightful analysis of the governance data from theEOS, separating the issues of national governance andglobal and domestic security, and challenging the notionthat security issues—common crime, organized crime,money laundering, and the threat of terrorism—are notsubject to measurement.The evidence suggests that somerich countries are faced not only with domestic challengesof undue influence, as regards many key public policies,laws and regulations, but with a new set of security threatsas well; even with their well-developed institutions, the G-7 and other rich countries must face the challenge ofguaranteeing level playing fields and mitigating the cost ofterrorist threats.

In his paper “The Competitive Edge in Environ-mental Responsibility,”Arthur Dahl argues that the envi-ronment has for too long been seen as an impediment tobusiness, since environmental regulations have increasedcosts.A review of global environmental problems revealsnot only challenges and risks for the private sector thatcannot be ignored, but also opportunities for businessesthat can work to their competitive advantage. Dahl high-lights the significant potential for business leadership inthe field of environment and sustainable development ateach stage of the development process. By taking a posi-tive, proactive view, the private sector can ensure suppliesof raw materials, increase efficiency, and generate newtechnologies to respond to these problems, thus openingup new markets, reducing costs, and allowing more timefor adaptation, with phased investments and reducedwrite-offs or special charges.

The 2004 Executive Opinion Survey evaluates theviews of business leaders on environmental and socialresponsibility issues, and demonstrates both the impor-tance of governmental leadership in providing an effectiveregulatory climate, and the key role of business leadershipin addressing environmental and social issues proactively.In Dahl’s analysis, countries are rated not on their presentenvironmental status, but on the efforts of both businessand government to improve that status, and to anticipateand address emerging problems. Nine countries receivedhigh ratings, another 34 were positive on balance, while24 showed progress in some areas, and 38 were making lit-tle or no effort to be environmentally responsible. Someemerging economies and developing countries scoredwell, driven perhaps by dynamic business sectors andenlightened governments, while some industrialized coun-tries were ranked far below their peers, suggesting a needfor greater efforts to remain competitive.The results

strongly suggest that combined efforts by business andgovernment to facilitate corporate social and environmen-tal responsibility do, indeed, generate a competitive edge.

In “Chile:The Next Stage of Development,”AugustoLopez-Claros notes that Chile has managed to grow fasterthan many other countries in the developing world,boosting per capita incomes, and making further progressto reduce poverty levels. It has done so against a backdropof fiscal discipline and rapidly declining public debt levels,while maintaining an admirably open trade and foreigninvestment regime, and improving to a remarkable degreethe quality of its public institutions, which have played astabilizing and pivotal role in the country’s recent evolu-tion. By a wide margin, Chile is the most competitiveeconomy in Latin America.

The author identifies a number of areas where chal-lenges remain, however, if Chile is to make a successfultransition to the next stage of its development.This phasewill require a combination of comparative advantages andthe adoption of new technologies to facilitate the emer-gence of clusters, centered mainly on the natural resourcesectors and the upstream development of supportingindustries with higher value added. Critical to this processof development will also be a substantial upgrading in thequality of Chile’s educational system, which remains sur-prisingly inefficient, given the country’s income levels.Lopez-Claros also raises the question of whether thecountry—and in particular its political leadership—havereached the right balance, as regards the role of the state inthe economy.Without doubt, the country has benefitedfrom a system that has built in a number of safeguards toprotect the public interest from the short-term interests ofpassing politicians, and from various forms of abuse. Butthis approach may need to make room for a more activerole for the state, as has been done in Finland, with regardto the support for new ventures, aimed at enhancing thecountry’s potential for innovation.

Chile aside, in “The Future of Competitiveness-Enhancing Reforms in Latin America,” Mario Blejerargues that despite a recent pickup in growth, the regioncontinues to confront important challenges and faces seri-ous struggles ahead.The difficulties concern the uncer-tainty regarding the sustainability of macroeconomicrecovery and, more importantly, the capacity of the regionto address long-term structural weaknesses.A significantproblem in Latin America is the incomplete nature of thereforms, evidenced by deficiencies in institutional develop-ment, and reflected in the loss of competitiveness. Indeed,Latin America is falling behind, not only with respect tothe economies of East Asia but, more significantly, withrespect to the transition economies of central and easternEurope.

In answer to the question what explains this worri-some trend, Blejer suggests that in most cases, reforms

xx

Exec

utiv

e Su

mm

ary

have remained incomplete and their economic benefitshave not been fully realized. Some of the successes in creating a more stable macroeconomic environment havenot been complemented by more broad-based “secondgeneration” reforms. He points out that any assessment of the current political and social realities in the regionsuggests that the short term prospects for further imple-mentation of market-oriented reforms would seem bleak.Reforms have not had the anticipated effects on growthand employment and, against a groundswell of the anti-globalization movement, the entire concept of structuralreform—with the exception of Chile—has been systemat-ically maligned and discredited across Latin America. Insuch an environment, it is clear that there is a widespreadlack of enthusiasm for further reforms. In practice, thedesign and introduction of a realistic reform agenda wouldrequire two key elements: compensation for those who arebound to be negatively affected from the process, and abetter set of international incentives for governments andcountries willing to swim against the current of publicopinion, and take the necessary steps to improve theireconomy.

In “International Productivity Comparisons: theImportance of Hours of Work,”Andrew Warner challengesthe traditional measures of productivity, by highlightingthe importance of hours worked. He demonstrates thatwhile growth of GDP or GDP per capita puts the UnitedStates clearly ahead of most industrial countries during theboom years of the new economy (1995–2000), thissupremacy is not quite so obvious when data on growthof GDP per hour is used to quantify productivity growth.Warner also questions the common notion that productiv-ity has suffered a serious decline in Europe over the lastdecade. Using GDP per hour calculations, he shows theclear lead of some European countries over the UnitedStates, and implies that the European “productivity slow-down” may be more myth than reality, when we focus onper hour data.

Given uncertainties about the reliability and compara-bility of existing data on hours worked, as well as lack ofcoverage of poorer countries, questions were introducedinto the 2004 Executive Opinion Survey on the extent ofhours worked.Warner uses this unique dataset to revealinteresting differences between the trends observed inindustrial countries and those in developing nations.Wagelabor in low-income countries work particularly longhours, whereas in rich countries as a whole, there is atrend for executive workers to put in more hours thanhourly labor.

Warner also uses the Survey data to highlight differ-ences in productivity barriers and to show how these vary across countries and income levels. Four barriers to productivity are examined: labor practices, business regulations, labor skills, and poor infrastructure.While the

perception of labor practices and business regulations asbarriers to productivity does not appear to be directlyrelated to income level, lack of skilled labor appears to bea hindrance in high-income countries, while the lack ofinfrastructure is typically, but not surprisingly, perceived asa productivity barrier in most low-income countries.

Special topicsBy analyzing trends in population growth, per capitaincome, and the effects of the IT revolution, RichardCooper, in “A Glimpse of 2020,” offers an insightful perspective on what the world will look like two decadesfrom now. Cooper paints contrasting demographic scenar-ios for 2020: low-income countries will see rapid popula-tion increase, placing heavy pressures on energy demandand urban infrastructure; rich countries will experiencepopulation decline, and a much higher ratio of elderly toworking age, severely taxing governments’ abilities tomaintain the high social benefits to which their citizenshave grown accustomed.

Dramatically decreased costs of communication willincrease mobility, reduce economic and cultural differ-ences between the regions of the world, but increaseinternational cooperation, not only in areas such as finan-cial regulation, tax and law enforcement and technologyexchange, but also in the willingness of nations to inter-vene where national governments have failed. Despite thenatural attraction of familiar languages and social environ-ments, businesses are becoming “footloose,” increasinglydriven by competition to outsource offshore, with head-quarters and production centers often situated at great dis-tances from each other. NGOs as well as criminal businessand terrorism will become increasingly international inscope, and repressive governments will find it more diffi-cult to insulate their populations from access to informa-tion. Cooper points out that by 2020, while there isbound to be uncertainty following the inevitable demiseof current dictators, more “South Koreas” will arise, i.e.developing countries which grow rapidly, democratize andjoin the ranks of the rich, forming new market opportuni-ties. Particular attention is paid to China, whose GDP by2020 could make it the world’s third largest economy, andwhere, although still poor, the high ratio of wage earnersto dependents will enable the country to become a majorworld player. Forecasting the future is hazardous business,but Cooper presents a cogent, business-relevant, vision of 2020.

A number of challenges to the well-being of oursocieties—demographic, technological, climatological, andgeopolitical—are visible on the long-term horizon. In“Confronting Long-Term Fiscal Challenges:Why itMatters for the Global Economy,” Peter Heller takes up anissue raised by Cooper in his own article, and perceptivelyexplains why some of these challenges are predictable,

xxi

Exec

utiv

e Su

mm

ary

while others are vague and uncertain. Even when clearlyanticipated, uncertainty still surrounds developmentswhose horizon may be measured in decades. Some, suchas aging populations, pose a threat to the financial solven-cy of national governments, raising the prospect of vastlyincreased future public outlays, whether for pensions,health care, long-term chronic care, infrastructure, or security.Accentuating these fiscal risks is the fact that thefuture resources of governments are already precommittedto an unprecedented extent. Not surprisingly, politicaleconomy factors work against efforts to address these challenges.

Heller contends that governments must do muchmore, now, to prepare for the fiscal consequences of thedevelopments that their countries face over the next sev-eral decades.The agenda for action will depend on thecountry, on the preferences and capacities of its peopleand institutions, on the extent of its existing policy com-mitments, and on the specific challenges it faces.Uncertainty does not absolve fiscal policymakers from theburden of addressing long-term issues.What they do, orfail to do, will critically influence both the welfare of cur-rent and future generations, and the role and capacity ofthe state itself. Delay in addressing these changes will onlyincrease their costs, some of which will be borne by thoseliving today.What to do? Heller suggests that no singlepolicy reform will suffice to meet long-term challenges.Reform must proceed on many fronts, utilizing additionalanalytic techniques, strengthening institutions to clarifyand monitor evolving budget trends, introducing detailedpolicy reforms, the sustained strengthening of the aggre-gate fiscal position, and working with other countries onareas where collective action is required.

In a compelling contribution to this year’s Report,entitled “Agricultural Policies in OECD Countries: anAgenda for Reform,” Stefan Tangermann makes a numberof fundamental points, which cast refreshing light on acomplex and politically charged subject.To begin with,there is an apparent inconsistency between the rapidlydeclining importance of agriculture among the 30Member countries of the OECD—whether measured interms of the sector’s contribution to total GDP or totalemployment—and the considerable attention devoted to itin the public debate.The resources transferred to farm-ers—an impressive US$257 billion in 2003, a full threequarters of which taking the form of production-linkedtransfers—seriously distort markets and competition ininternational trade.Tangermann shows that, despite long-standing discussions about the need for reforms, the levelof support during 2001–2003 is only marginally lowerthan during the period 1986–1988. However, within theOECD as a whole, there is considerable diversity acrosscountries, with New Zealand and Australia having essen-tially eliminated farm support as a result of comprehensive

reforms, and others, such as Norway and Switzerland, stillproviding levels of producer support more than twice theaverage in the EU, and hardly changed during the past 15 years.

Tangermann examines the reasons for these massivetransfers to farmers.Their motivation stems from a desireto address equity concerns in societies at large, and dealwith market failures associated with the interactionbetween agriculture and the environment. However, heprovides compelling data to show that, in fact, incomes offarm households in OECD countries are in line with, ifnot higher than, household incomes in the overall econo-my.Thus, broad-based support measures such as price andoutput support are unnecessary.Worse still, only 25 centsout of every dollar of support provided to farmers actuallyends up in farmers’ pockets, with a large share of the restgoing to large landowners.As regards the environment, theharsh effects of overproduction on the quality of farmlandand wildlife are well known. Finally, the extra output gen-erated by farm policies in OECD countries depressesprices for farm products in international trade, and hasbeen a contributing factor in the difficulties encounteredin promoting further multilateral trade liberalization.Theauthor concludes this important paper with some specificsuggestions for reform.

In his paper “Can Foreign Aid Make Poor CountriesCompetitive?”William Easterly offers insightful answers tothe question why foreign aid has not been more successfulat promoting competitiveness. In his review of the evi-dence on foreign aid and economic growth, the effective-ness of aid conditionality, and the bureaucratic nature ofaid agencies, Easterly questions and then examines theresults of the regression analysis published in 2000 byCraig Burnside and David Dollar, which investigated therelationship between foreign aid, economic policy and thegrowth of per capita GDP. Because of its conclusion, viz.that aid only works in a good policy environment, thisstudy was widely cited by media, governments and aidagencies, as a basis for increasing foreign aid. By expandingthe dataset, extending the time line and using alternativedefinitions of “aid,”“policy,” and “growth,” Easterly comesto some different and thought-provoking conclusions, tothe effect that the interaction term of aid and good policyis no longer statistically significant. Easterly also criticallyexamines the “financing gap” approach to aid, by which itis assumed that aid increases investment and investmentincreases economic growth, finding it both theoreticallyquestionable and empirically deficient, leading him toquestion why the international community has not heldagencies responsible for the failure of large flows of aid togenerate growth.

After discussing the detailed findings, Easterly analyzeshow aid agencies actually function, citing the excessive,dysfunctional bureaucracy of agencies, the fact that they

xxii

Exec

utiv

e Su

mm

ary

are answerable to the rich donors, rather than their voiceless recipients, the assumption of capital projectswithout maintaining them, and the pernicious tendency toovermeet, overextend and overstate. He saves particularlytrenchant criticism for the failure of aid agencies, despitethe presence of obviously well-intentioned and capableminds, to understand the deeper implications of and trulypractice “grassroots” development.The result of this fail-ure, he concludes, has been not only the continued pres-ence of unalleviated misery, but the loss of support for aidon the part of the rich countries most able to provide it.He ends in a positive tone, pointing to a successful projectin Ethiopia, by making a number of serious and realisticproposals for aid agencies, governments and developmentpractitioners, to assist them in revising expectations, meth-ods, and, hopefully, outcomes.

The Report ends with a section containing detailedcountry profiles for each of the 104 economies covered inour competitiveness indexes, as well as data tables for thevariables that are used as inputs in their construction.Abrief Annex, explaining how best to interpret the infor-mation contained in the country profiles and the datatables, is an essential companion to this section, as aretechnical notes clarifying the meaning of many variables,and listing relevant data sources.

xxiii

Exec

utiv

e Su

mm

ary

CHAPTER 1.2

Building the MicroeconomicFoundations of Prosperity:Findings from the BusinessCompetitiveness Index1

MICHAEL E. PORTER, Harvard University

Competitiveness has become a central preoccupation ofboth advanced and developing countries in an increasinglyopen and integrated world economy. Despite its acknowl-edged importance, the concept of competitiveness is oftenmisunderstood. Here, we define competitiveness concretely,show its relationship to a nation’s standard of living, andoutline a conceptual framework for understanding itscauses.

The Business Competitiveness Index (BCI), based onthis conceptual framework, provides a data-rich approachto measuring and analyzing the fundamental competitive-ness of a large number of countries in a comparative con-text.This year’s BCI includes 103 countries, up one fromlast year. Our aim is to rank country competitivenessacross countries, identify individual countries’ competitivestrengths and weaknesses, reveal the trends in competitive-ness in the global economy, and extend our basic knowl-edge about the sources of competitiveness and the processof economic development.

Most discussion of competitiveness and economicdevelopment is still focused on the macroeconomic, politi-cal, legal, and social circumstances that underpin a success-ful economy. It is well understood that sound fiscal andmonetary policies, a trusted and efficient legal system, astable set of democratic institutions, and progress on socialconditions contribute greatly to a healthy economy.However, these broader conditions are necessary but notsufficient.They provide the opportunity to create wealthbut do not themselves create wealth.Wealth is actuallycreated in the microeconomic level of the economy, root-ed in the sophistication of the operating practices andstrategies of companies as well as in the quality of themicroeconomic business environment in which a nation’scompanies compete. Unless these microeconomic capabili-ties improve, macroeconomic, political, legal, and socialreforms will not bear full fruit.

Beginning in 1998, we began an effort to examinestatistically the microeconomic foundations of competi-tiveness and prosperity across a wide array of countries.This is a daunting task, given the need to measure andcompare the complex array of national circumstances thatsupport a high and sustainable level of productivity.Theeffort aims to move beyond the examination of broad,aggregate variables typical of most economic growthanalyses to provide a framework for countries and compa-nies to understand their detailed competitive strengths andweaknesses. It also aims to be as rigorous as possible, veri-fying the importance of each measure statistically andusing statistical techniques to weight the contribution ofindividual variables. Finally, we know that improvement incompetitiveness is not a simple linear process but onewhere nations at different levels of development face dif-ferent challenges and priorities.This effort aims to high-light these differences.

19

1.2:

Bui

ldin

g th

e M

icro

econ

omic

Fou

ndat

ions

of

Pros

perit

y

The Business Competitiveness Index seeks to explorethe underpinnings of a nation’s prosperity, measured by itslevel of GDP per capita.The focus is on whether currentprosperity is sustainable, and on the specific areas that mustbe addressed if GDP per capita is to achieve higher levelsin the future.A separate Growth Competitiveness Index(GCI), discussed in the previous chapter of this Report,examines the sources of GDP per capita growth, which ismore dependent on investment rates and other macroeco-nomic policies.The sustainable level of current GDP percapita and its rate of growth will be related in the longterm, but each area requires its own distinctive policyagenda.The conceptual framework and statistical approachfollow that of the previous reports and the findings arefully comparable with previous MicroeconomicCompetitiveness Index results.

The analysis here is pragmatic, making use of the bestavailable data and econometric methods even though bothare far from perfect.We also confront the challenge ofestablishing the direction of causality given limited time-series data. However, even if definitive tests of causality arenot possible, understanding the microeconomic correlatesof prosperity remains crucial.There may be a natural ten-dency for some microeconomic conditions to improve asGDP per capita increases.Yet the large observed differ-ences across countries, even those at similar income levels,reveal that this improvement is far from automatic.

Despite the statistical challenges, the statistical findingsoverall are remarkably stable and robust compared withthe Global Competitiveness Report 2003–2004 (GCR) andearlier Reports.We expand this year’s analysis to include ananalysis of natural resource endowments and their role incompetitiveness, a crucial issue especially for developingcountries.The results again provide strong support for theimportance of microeconomic competitiveness for eco-nomic development and prosperity. Our findings also veri-fy the striking and regular pattern of microeconomicchanges that accompany economic development.

The Business Competitiveness Index (BCI) accountsfor 81 percent of the variation across countries in the levelGDP per capita.2 This level is remarkably high given thepresence of so many low- income countries and theinherent imperfections of national income data.Thesefindings highlight the pressing need to better incorporatemicroeconomic competitiveness agenda into efforts tostimulate economic growth. In advanced countries, whichhave largely gotten their macro policies right, it is microreform that holds the key to reversing unemploymentproblems, to growing exports, and to translating economicgrowth into a rising standard of living.

In developing countries, microeconomic failures nul-lify macroeconomic and social programs again and again.By accessing global capital markets, countries can engineerspurts of growth through macroeconomic stabilization and

financial reforms that bring in floods of capital and createthe illusion of progress as construction cranes dot the sky-line.Without microeconomic reforms, however, growthwill be snuffed out as exports and jobs fail to materialize,wages stagnate, and the return on investments proves dis-appointing.This disappointment, and the austerity thatresults from such cycles, is at the heart of the backlashagainst globalization.

Successful economic development requires progresson multiple fronts simultaneously. Reform efforts need tobe tightly connected to the country’s current stage ofdevelopment.As an economy progresses, the constraints toits continued advancement shift.At strategic points in thedevelopment process, the whole basis of national competi-tiveness must be transformed. Many aspects of companystrategy must be shifted and new requirements in thenational business environment must be met. Our analysisprovides the conceptual framework and comparative datato define such national agendas, and to measure progress.

Competitiveness and its causesMeasuring and ranking competitiveness requires a clearconceptual framework, drawing on the accumulatedknowledge about competitiveness and its sources.We sum-marize the framework here, drawing on previous years’chapters while extending it to incorporate recent learning.

What is competitiveness?Competitiveness remains a concept that is not well under-stood, despite widespread acceptance of its importance.The most intuitive definition of competitiveness is a coun-try’s share of world markets for its products.This makescompetitiveness a zero-sum game, because one country’sgain comes at the expense of others.This view of compet-itiveness is used to justify intervention to skew marketoutcomes in a nation’s favor (so-called industrial policy). Italso underpins policies intended to provide subsidies, holddown local wages, and devalue the nation’s currency, allaimed at expanding exports. In fact, it is still often saidthat lower wages or devaluation “make a nation morecompetitive.” Business leaders are drawn to the market-share view because these policies seem to address theirimmediate competitive concerns.

Unfortunately, the most intuitive view of competi-tiveness is deeply flawed, and acting on it works againstnational economic progress.The need for low wagesreveals a lack of competitiveness and holds down prosperi-ty. Subsidies drain national income and bias choices awayfrom the most productive use of the nation’s resources.Devaluation results in a collective national pay cut by dis-counting the products and services sold in world marketswhile raising the cost of the goods and services purchased

20

1.2:

Bui

ldin

g th

e M

icro

econ

omic

Fou

ndat

ions

of

Pros

perit

y

abroad. Exports based on low wages or a cheap currency,then, do not support an attractive standard of living.

To understand competitiveness, the starting pointmust be the underlying sources of prosperity.A nation’sstandard of living is determined by the productivity of itseconomy, which is measured by the value of goods andservices produced per unit of the nation’s human, capital,and natural resources. Productivity depends both on thevalue of a nation’s products and services, measured by theprices they can command in open markets and the effi-ciency with which they can be produced. Productivityalso depends on the ability of an economy to mobilize theavailable human resources. Some European economiesreport high levels of productivity per hour worked, buthigh unemployment, sick leave, and limited working hoursdepress national income per capita.3 Much of this is notvoluntary but reflects a lack of employment alternatives.4

True competitiveness, then, is measured by productiv-ity. Productivity allows a nation to support high wages, astrong currency, and attractive returns to capital—and withthem a high standard of living. Productivity is the goal,not exports per se. Only if a nation increases exports ofproducts or services that it can produce more productivelythan the average industry will national productivity rise.Also, productivity is the goal, not whether firms operatingin the country are domestic or foreign owned.What mat-ters most is not ownership, but the nature and productivityof the business activities taking place in a particular country.Finally, purely local industries also matter for competitive-ness because their productivity not only sets the wages inthese industries but also has a major influence on the costof living and the cost of doing business in the country.The productivity of the entire economy matters for thestandard of living, not just the traded sector.

The world economy is not a zero-sum game. Manynations can improve their prosperity if they can improveproductivity.The central challenge in economic develop-ment, then, is how to create the conditions for rapid andsustained productivity growth.

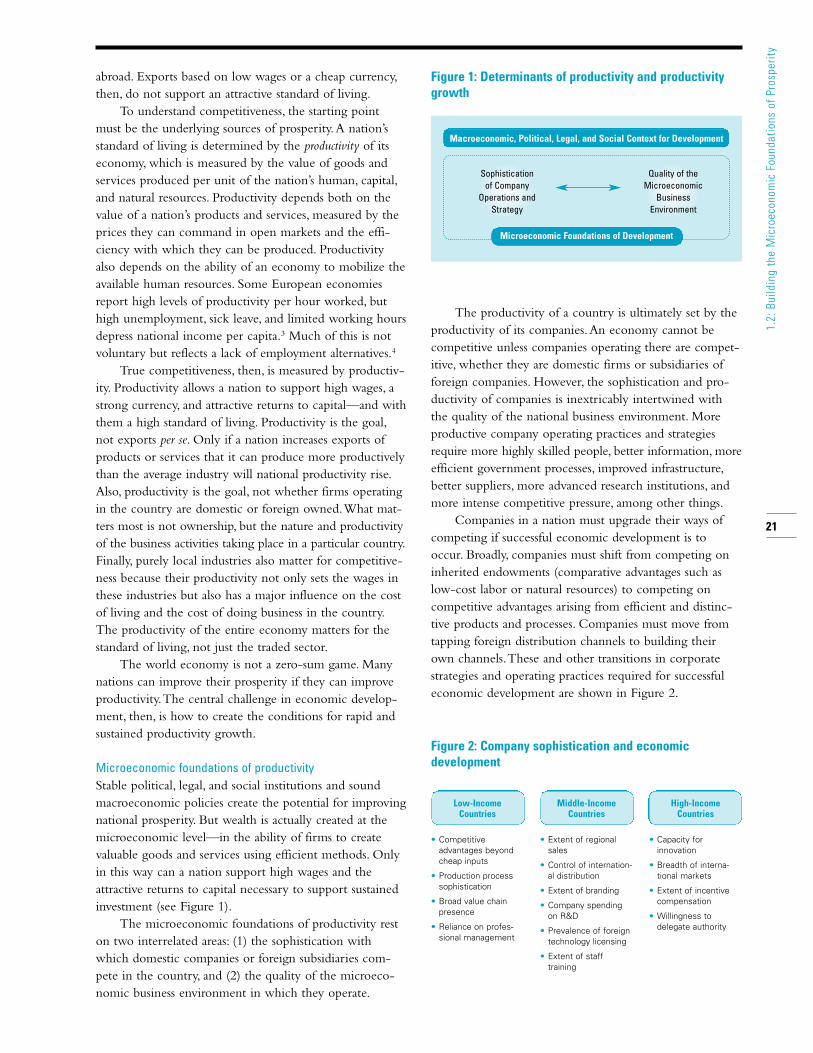

Microeconomic foundations of productivityStable political, legal, and social institutions and soundmacroeconomic policies create the potential for improvingnational prosperity. But wealth is actually created at themicroeconomic level—in the ability of firms to createvaluable goods and services using efficient methods. Onlyin this way can a nation support high wages and theattractive returns to capital necessary to support sustainedinvestment (see Figure 1).

The microeconomic foundations of productivity reston two interrelated areas: (1) the sophistication withwhich domestic companies or foreign subsidiaries com-pete in the country, and (2) the quality of the microeco-nomic business environment in which they operate.

The productivity of a country is ultimately set by theproductivity of its companies.An economy cannot becompetitive unless companies operating there are compet-itive, whether they are domestic firms or subsidiaries offoreign companies. However, the sophistication and pro-ductivity of companies is inextricably intertwined withthe quality of the national business environment. Moreproductive company operating practices and strategiesrequire more highly skilled people, better information, moreefficient government processes, improved infrastructure,better suppliers, more advanced research institutions, andmore intense competitive pressure, among other things.

Companies in a nation must upgrade their ways ofcompeting if successful economic development is tooccur. Broadly, companies must shift from competing oninherited endowments (comparative advantages such aslow-cost labor or natural resources) to competing oncompetitive advantages arising from efficient and distinc-tive products and processes. Companies must move fromtapping foreign distribution channels to building theirown channels.These and other transitions in corporatestrategies and operating practices required for successfuleconomic development are shown in Figure 2.

21

1.2:

Bui

ldin

g th

e M

icro

econ

omic

Fou

ndat

ions

of

Pros

perit

y

Macroeconomic, Political, Legal, and Social Context for Development

Sophistication of Company

Operations andStrategy

Quality of theMicroeconomic

Business Environment

Microeconomic Foundations of Development

Figure 1: Determinants of productivity and productivitygrowth

Low-Income Countries

• Competitive advantages beyondcheap inputs

• Production processsophistication

• Broad value chainpresence

• Reliance on profes-sional management

Middle-IncomeCountries

• Extent of regionalsales

• Control of internation-al distribution

• Extent of branding

• Company spendingon R&D

• Prevalence of foreigntechnology licensing

• Extent of staff training

High-Income Countries

• Capacity for innovation

• Breadth of interna-tional markets

• Extent of incentivecompensation

• Willingness to delegate authority

Figure 2: Company sophistication and economic development

What were strengths in competing at earlier stages ofdevelopment become weaknesses at more advanced levelsof development. Extensive technology licensing works forlower- and middle-income countries, but must give wayto indigenous technology development. Necessary changesare often resisted by the corporate sector because pastapproaches were profitable and because old habits aredeeply ingrained.

Moving to more sophisticated ways of competingdepends on parallel changes in the microeconomic busi-ness environment.The business environment can beunderstood in terms of four interrelated areas: the qualityof factor (input) conditions, the context for firm strategyand rivalry, the quality of local demand conditions, and thepresence of the related and supporting industries. Becauseof their graphical representation (see Figure 3), the fourareas have collectively become referred to as the diamond.

As the diamond framework reveals, almost everythingmatters for competitiveness.The schools matter, the roadsmatter, the financial markets matter, and customer sophis-tication matters, among many other aspects of a nation’scircumstances, many of which are deeply rooted in anation’s institutions, people, and culture.This makesimproving competitiveness a special challenge, becausethere is no single policy or grand step that can createcompetitiveness, only many improvements in individualareas that inevitably take time to accomplish. Improving

competitiveness is a marathon, not a sprint. How to sus-tain momentum in competitiveness improvements overtime is among the greatest challenges facing countries.

There are distinct influences on competitiveness atmultiple geographic levels: national, state, and local.5 In manycountries, we observe striking differences in economicperformance among subnational regions. In countries suchas China, India, and the United States, the benefits ofdecentralization of economic policy and strong initiativein individual regions is evident.The crucial need for eco-nomic strategies for sub-national units such as states orregions is among the most important new directions incompetitiveness thinking and practice.

National productivity can also be enhanced throughcoordinating policies among neighboring countries.Aconcerted effort to improve the business environment isneeded both within countries and across countries.

Government plays an inevitable role in economicdevelopment because it affects many aspects of the busi-ness environment. Government shapes factor conditions,for example, through its training and infrastructure poli-cies.The sophistication of home demand derives in partfrom regulatory standards, consumer protection laws, gov-ernment purchasing practices, and openness to imports.Similar policy influences are present in all four parts of thediamond. Many government departments and agenciesimpinge on competitiveness, as do government entities at

22

1.2:

Bui

ldin

g th

e M

icro

econ

omic

Fou

ndat

ions

of

Pros

perit

y

Factor (Input) ConditionsPresence of high quality, specialized inputs available to firms

• Human resources• Capital resources• Physical infrastructure• Administrative infrastructure• Information infrastructure• Scientific and technological

infrastructure• Natural resources

Related and Supporting Industries• Access to capable, locally

based suppliers and firms in related fields

• Presence of clusters instead of isolated industries

Demand Conditions• Sophisticated and demanding

local customer(s)

• Local customer needs that anticipate those elsewhere

• Unusual local demand in special-ized segments that can be servednationally and globally

Figure 3: The microeconomic business environment

Context for Firm Strategy and Rivalry• A local context and rules that

encourage investment and sustained upgrading (e.g.,Intellectual property protection)

• Meritocratic incentive systemsacross institutions

• Open and vigorous competitionamong locally based rivals

the provincial, state, and city levels.The question is notwhether government has a role, but what that role shouldbe and how to coordinate policies across parts of govern-ment. Many countries have sought to limit the inappro-priate roles of government while ignoring its positiveroles. Government must set the right rules and incentivesand make the public investments needed for a productiveeconomy.

National endowments such as natural resources play adeclining role in competitiveness as the resource intensityof the economy falls and as technology substitutes forresources or opens up new resource locations.The realprices of most resources or resource-intensive goods havebeen falling over the decades. It is the productivity withwhich natural resources can be utilized, not the resourcesthemselves, that normally have the strongest influence onprosperity.Abundant natural resources also carry a risk. Incountries where natural resources are abundant or domi-nate economic activity, forces are set in motion that limitthe development of policies, skills, and attitudes thatenhance competitiveness. Exploiting and redistributingresource spoils can become the dominant orientation notenhancing productivities.We explore the relationshipbetween natural resource endowments and competitive-ness in a later section.

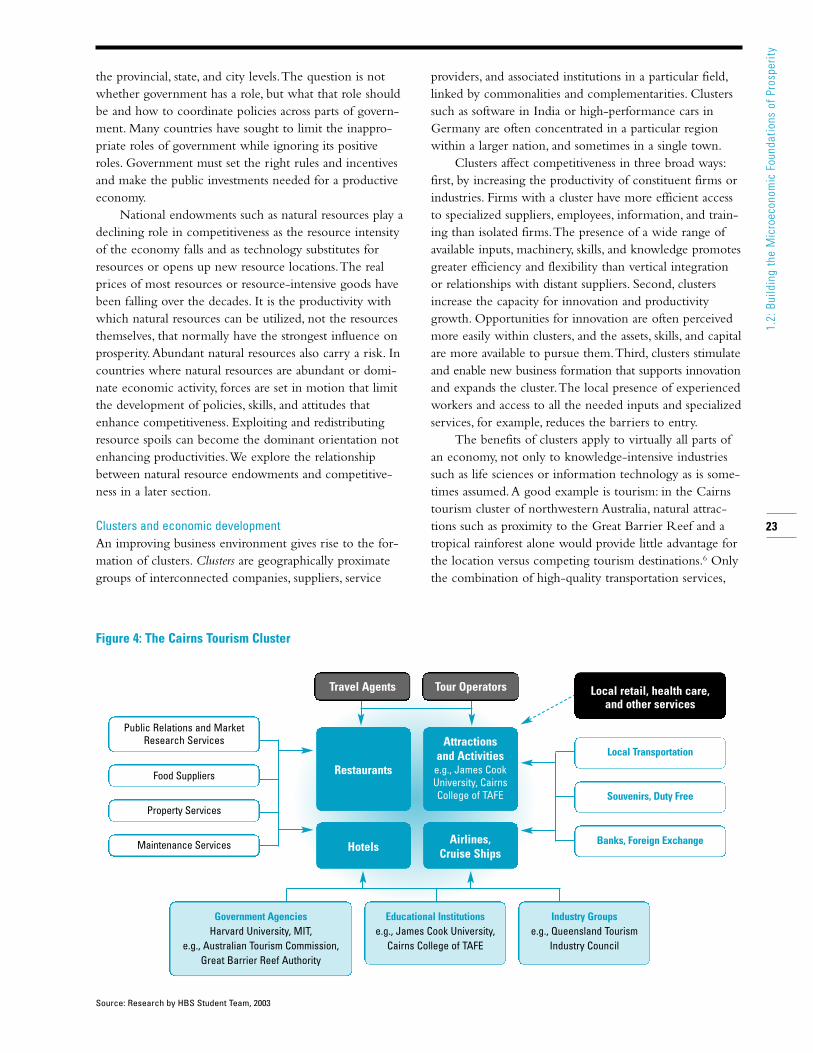

Clusters and economic developmentAn improving business environment gives rise to the for-mation of clusters. Clusters are geographically proximategroups of interconnected companies, suppliers, service

providers, and associated institutions in a particular field,linked by commonalities and complementarities. Clusterssuch as software in India or high-performance cars inGermany are often concentrated in a particular regionwithin a larger nation, and sometimes in a single town.

Clusters affect competitiveness in three broad ways:first, by increasing the productivity of constituent firms orindustries. Firms with a cluster have more efficient accessto specialized suppliers, employees, information, and train-ing than isolated firms.The presence of a wide range ofavailable inputs, machinery, skills, and knowledge promotesgreater efficiency and flexibility than vertical integrationor relationships with distant suppliers. Second, clustersincrease the capacity for innovation and productivitygrowth. Opportunities for innovation are often perceivedmore easily within clusters, and the assets, skills, and capitalare more available to pursue them.Third, clusters stimulateand enable new business formation that supports innovationand expands the cluster.The local presence of experiencedworkers and access to all the needed inputs and specializedservices, for example, reduces the barriers to entry.

The benefits of clusters apply to virtually all parts ofan economy, not only to knowledge-intensive industriessuch as life sciences or information technology as is some-times assumed.A good example is tourism: in the Cairnstourism cluster of northwestern Australia, natural attrac-tions such as proximity to the Great Barrier Reef and atropical rainforest alone would provide little advantage forthe location versus competing tourism destinations.6 Onlythe combination of high-quality transportation services,

23

1.2:

Bui

ldin

g th

e M

icro

econ

omic

Fou

ndat

ions

of

Pros

perit

y

Figure 4: The Cairns Tourism Cluster

Source: Research by HBS Student Team, 2003

Public Relations and MarketResearch Services

Restaurants

Attractions and Activities

e.g., James CookUniversity, CairnsCollege of TAFE

Airlines, Cruise ShipsHotels

Food Suppliers

Property Services

Maintenance Services

Government AgenciesHarvard University, MIT,

e.g., Australian Tourism Commission, Great Barrier Reef Authority

Educational Institutionse.g., James Cook University,

Cairns College of TAFE

Industry Groupse.g., Queensland Tourism

Industry Council

Local Transportation

Souvenirs, Duty Free

Banks, Foreign Exchange

Local retail, health care, and other services

Travel Agents Tour Operators

accommodation, restaurants, travel guides, and the manysupporting activities required to operate them creates thehigh level of value which tourists are looking for. Eventhe best hotel and the most unique tourist attractionwould loose greatly in value if local transportation serviceswere weak.

National economies tend to specialize in particularclusters, which account for a disproportionate share oftheir output and exports.This specialization is even moreevident in sub-national regions.The nature and depth ofclusters varies with the state of development of the econo-my. In developing countries, clusters are normally shallowor underdeveloped. Firms compete based on cheap laboror local natural resources, and they depend heavily onimported components, machinery, and technology.Specialized local infrastructure and institutions are absentor inefficient, which limits local processing of productsand limits quality.As economies advance, clusters developand deepen to include suppliers of specialized inputs,components, machinery, and services; specialized infra-structure; and institutions providing specialized training,education, information, research, and technical support.