glass half full (65) 6320 1374 - kim eng holdings

TRANSCRIPT

4 June 2020

Macro

| F

X R

ese

arc

h &

Str

ate

gy

Glo

bal

SEE PAGE 15 FOR IMPORTANT DISCLOSURES

Global Markets Daily

Glass Half Full

Sentiment Still Buoyed by Data Improvement

Sentiment was buoyant for much of overnight session, keeping the

USDJPY close to the 109-figure. The US data released was better than

expected with ADP employment declines a fraction of consensus at -

2.76mn (vs. expected -9mn). US services PMI for May was a tad stronger

at 37.5 (vs. prev. 36.9). ISM Non-mfg was up at 45.4 vs. previous 41.8.

Market players largely ignored the Apr factory orders that declined

steeply by -13.0%m/m and the durable goods orders that fell -17.7%. The

DXY touched a low of 97.18 but shows signs of turning higher as bears run

into fatigue.

Oil falters; BoC Stands Pat; US’ Tit For Tat

Crude oil prices fell a tad overnight upon whispers that the Saudi-Russia

agreement on production cut extension for 1 month is conditional on

non-compliant members making deeper cuts in order to make up for past

non-compliance. USDCAD was whippy, drifting higher before the BoC’s

revision of its growth forecast (higher) brought it back towards day low.

The central bank kept its target overnight rate unchanged at 0.25% and

reduced frequency of its term repo operations to once a week and its

program to buy bankers’ acceptances to bi-weekly. In the meantime, the

US has suspended Chinese carrier flights from flying to the US according

to the US Transportation Department as China has not given permission

for US airline flights.

ECB decides on monetary settings; TH CPI, MY Trade

ECB decides on monetary settings today but we anticipate policy to be at

status quo. Other data due from the region includes Thailand’s CPI and

Malaysia’s trade data.

Implied USD/SGD Estimates at 4 June 2020, 9.00am

Upper Band Limit Mid-Point Lower Band Limit

1.3760 1.4040 1.4321

Analysts

G7: Events & Market Closure

Date Ctry Event

1 Jun AU, NZ Market Closure

2 Jun AU RBA Policy Decision

3 Jun CA BOC Policy Decision

4 Jun EU ECB Policy Decision

AXJ: Events & Market Closure

Date Ctry Event

1 Jun ID Market Closure

3 Jun TH Market Closure

Saktiandi Supaat

(65) 6320 1379

Fiona Lim

(65) 6320 1374

Christopher Wong

(65) 6320 1347

Tan Yanxi

(65) 6320 1378

MajorsPrev

Close% Chg Asian FX

Prev

Close% Chg

EUR/USD 1.1233 0.56 USD/SGD 1.3979 -0.18

GBP/USD 1.2575 0.19 EUR/SGD 1.5703 0.40

AUD/USD 0.6921 0.35 JPY/SGD 1.2836 -0.35

NZD/USD 0.6422 0.80 GBP/SGD 1.7577 0.00

USD/JPY 108.9 0.20 AUD/SGD 0.9676 0.21

EUR/JPY 122.34 0.79 NZD/SGD 0.8981 0.71

USD/CHF 0.9612 -0.12 CHF/SGD 1.4545 -0.01

USD/CAD 1.3495 -0.18 CAD/SGD 1.0358 0.00

USD/MYR 4.262 -0.34 SGD/MYR 3.051 -0.08

USD/THB 31.552 0.00 SGD/IDR 10111.68 -1.51

USD/IDR 14095 -2.22 SGD/PHP 35.8839 0.16

USD/PHP 50.109 -0.48 SGD/CNY 5.098 0.55

FX: Overnight Closing Prices

4 June 2020 2

FX Research & Strategy

G7 Currencies

DXY Index – Bears to Pause for Breath. USD found some support

after falling for 5 consecutive sessions to Mar levels. Last seen at

97.50 Bearish momentum on daily chart remains intact but RSI

shows sign of turning higher from near oversold conditions. Expect

USD bears to pause for now (in terms of momentum), potentially

consolidating in 97.20 – 97.80 range as we look to add to shorts on

rally. Resistance at 97.8 (61.8% fibo retracement of 2020 low to

high), 98.50 (200 DMA). Support at 97.20 (yest low), 96.60 levels

(76.4% fibo). This week brings Trade, Jobless claims (Apr) on Thu;

NFP, Unemployment rate, wage growth (May) on Fri. While USD

could still find support in times of risk aversion, US-China

geopolitical tensions (overnight saw response from US to ban

passenger flights from China as China refuse to let US airlines

resume flights to China as its pandemic subsides), we reiterate our

bias for weaker USD on - US is facing domestic problems at home

including violent street protests over police brutality, still a covid-

19 epicentre, potential political risks in the lead up to US

Presidential elections in Nov 2020, massive and increasing Fed’s

balance sheet amid QE, deteriorating twin deficits as well as

chatters of reserve diversification/reallocation away from USD as

well as countercyclical factor kicking in - as the world economy

picks up, cyclical proxy FX such as AUD, AXJs will strengthen while

USD weakens.

EURUSD – ECB in Focus. EUR rose overnight in response to Merkel’s

coalition agreement on another EUR130bn stimulus targeted to

spur short term consumer spending, get business to restart

investments, built 5G networks, improve railways and incentives

for Electric Vehicles – with a view to commit to the future. Some

key highlights include VAT cuts to 16%, from 19% through the end-

2020 (estimated to cost EUR20bn), bridge financing for SMEs of as

much as EUR25bn, accelerating EUR10bn in investment in digital,

security and defense projects. This round of package exceeded the

top end of expectations by 30% and the 2 packages (one was agreed

earlier in Mar) represent about EUR1.3tn of stimulus. Day ahead

brings ECB meeting decision - we expect the ECB to keep key policy

rates on hold at the upcoming GC: MRO at 0%, average deposit

facility at -0.5%. We expect rates to stay low at current levels to

support growth and inflation. We reiterate that there is no

incentive for ECB to reduce rate further given that rates are

already near lower bound and there is diminishing marginal returns

to lower them further (cost outweighs benefits). ECB is likely to

fall back on policy mix of unconventional monetary pools and push

for fiscal measures to support growth while keeping rates low (but

short of cutting rates further). The intent of policy at this point is

to reduce fragmentation in the Euro-area, narrow credit spreads

and keep the flow of funds going and to support businesses’ needs.

We expect some tweaks to the size of the EUR750bn Pandemic

Emergency Purchase Program (PEPP), likely to be enlarged to

EUR1tn region especially after Lagarde’s announcement that ECB

will purchase junk-rated bonds. Market expectations are

somewhere between EUR1-1.25tn – representing a EUR250-500bn

4 June 2020 3

FX Research & Strategy

expansion. EUR was last seen at 1.1220 levels. Bullish momentum

on daily chart intact while RSI is rising into overbought conditions.

We do not rule out short term retracement but likely to be shallow

towards support at 1.1170 (61.8% fibo retracement of 2020 high to

low), 1.1120, 1.1075 levels (50% fibo). Next resistance at 1.1260,

1.13 (76.4% fibo retracement of 2020 high to low). This week brings

Retail sales (Apr); ECB Policy meeting decision on Thu; German

factory orders (Apr) on Fri.

GBPUSD – Correction Risks. GBP eased from its highs after BoE

reiterated that lenders should prepare for the possibility of no-deal

post Brexit transition. GBP was last seen at 1.2540 levels. Mild

bullish momentum on daily chart intact while RSI is turning from

overbought conditions. Support at 1.2360/80 (23.6% fibo

retracement of Mar low to Apr-May double top, 50 DMA).

Resistance at 1.2570 (100 DMA), 1.2660/70 (200 DMA, Mar-Apr

high). This week brings Services PMI (May) on Wed; Construction

PMI (May) on Thu; GfK consumer confidence (May) on Fri.

USDJPY – Caution on Retracement. Pair remained largely where it

was yesterday morning. Last seen at 108.82. The US is barring

Chinese airlines as Beijing had rejected the requests of US carriers

to resume flights to China. The news was positive for US airline

shares, but likely negative for broader global sentiment. In the

meantime, 109.20 (23.6% fibo retracement from Mar low to high)

might be the next key resistance to watch. If that breaks, next

strong resistance is some way off at 111.70. Nonetheless, with

stochastics entering near-overbought conditions, there is a fair

chance that up-moves could slow, or we could see some modest

retracement lower. In that case, support is at 108.40 (200-DMA)

before 107.70 (38.2% fibo), 106.40 (50% fibo). Apr leading index

due Fri.

NZDUSD – RSI Overbought. NZD was last seen at 0.6415 levels.

Bullish momentum intact but RSI shows signs of turning lower from

overbought conditions. Tactically we look for a pullback lower.

Support at 0.6360, 0.6320 (200 DMA). Resistance at 0.6450 (76.4%

fibo retracement of 2020 high to low) before 0.66 levels. This week

brings Commodity Price (May) on Fri.

AUDUSD – Doji. AUD was propelled higher yesterday but bulls seem

to be overcome by fatigue into the latter part of the session, in

contrast to the US stock indices that closed near record high.

AUDUSD was last seen around the 0.69-figure and we see a bearish

divergence that could be played out this time. Three peaks of the

AUDUSD (Apr, May and Jun) were matched by lower peaks in MACD

forest. We look for a corrective play lower towards 0.6450. Interim

support around 0.6670 (200-dma before the next at 0.6450 (61.8%

Fibonacci retracement of the Jan-Mar fall). At home, the Australian

Council of Social Service criticized the government’s plan to

provide large grants to home builders and renovators as there is

still “the backlog of urgent social housing repairs and a shortfall in

social housing stock”. Week remaining has Trade (Apr) on Thu; FX

reserves (May) on Fri.

4 June 2020 4

FX Research & Strategy

USDCAD – Faltering in the Face of 200-dma. Strong risk appetite

continues to keep the USDCAD a tad pressured to the downside but

bears failed to break through the 200-dma, last seen around

1.3510. Oil prices have been firming with WTI seen above the

$38/bbl momentarily until news cited sources saying that the

Saudi-Russia agreement on production cut extension for 1 month is

conditional on non-compliant members making deeper cuts in order

to make up for past non-compliance. The Saudi Arabia has

proposed to move the OPEC meeting to mid-June to allow time to

review May production and compliance data. News flow swung the

USDCAD but resilient risk sentiment as well as BoC’s decision to

keep overnight target rate unchanged at 0.25% and scale back

some of its OMO supported the CAD. The central bank statement

(guided by Poloz for the last time) also saw a revision in the growth

outlook as “the Canadian economy appears to have avoided the

most severe scenario” in the Apr MPR. The contraction in 2Q is

expected to be 10-20% instead of the previous forecasted decline

of 15-30%. The central bank reduced frequency of its term repo

operations to once a week and its program to buy bankers’

acceptances to bi-weekly. Back on the USDCAD chart, the recent

breakout of the descending triangle could bring this pair through

the 200-dma at 1.3450 and the textbook target is 1.3070. However,

we do not rule out some retracement in the interim as 200-dma has

proved to be a strong support at 1.3460. Stochastics show signs of

turning higher from oversold conditions as well although MACD

suggests bearish momentum still. Retracement towards 1.3610

(61.8% Fibonacci retracement of the Jan- Mar rally) cannot be

ruled out before the next resistance is seen around 1.3738 (100-

dma). Week remaining has Apr trade data today and May labour

report tomorrow.

4 June 2020 5

FX Research & Strategy

Asia ex Japan Currencies

SGD trades around +0.40% from the implied mid-point of 1.4040 with the

top estimated at 1.3760 and the floor at 1.4321.

USDSGD – Bearish Still. Pair traded largely ranged yesterday. Last

seen at 1.3990. Bearish trend channel remains intact. Upside risks

for the pair are if global risk sentiments turn negative (starting

with US-China spat on airlines), and dollar stages a recovery. On

net though, we remain bearish on the pair. On daily chart,

momentum is bearish and stochastics are on the dip towards near-

oversold conditions. Resistance nearby at 1.4000, before 1.4100

(61.8% fibo retracement of Mar low to high), 1.4200 (50-DMA).

Support 1.3850 (200-DMA), 1.3760 (Mar low).

SGDMYR – Watching if Trend Breaks. SGDMYR was last seen at

3.05 levels. Daily momentum remains mild bearish while RSI is

falling. We said to respect the bullish trend channel till it breaks (or

closes below) – and this deserves monitoring. Trend ain’t your

friend if it breaks. Immediate support at 3.04 (200 DMA), 3.03 (50%

fibo retracement of 2020 low to high). Resistance at 3.0530/560 (50

DMA, lower bound of trend channel), 3.0610 (21 DMA).

USDMYR – Consolidate. Decline in USDMYR slowed. Pair was last

seen at 4.2675 levels. Bearish momentum intact but RSI shows signs

of turning from near oversold conditions. Consolidation likely.

Immediate support at 4.25 levels (50% fibo retracement of 2020 low

to high, 100 DMA). Resistance at 4.2950 levels (38.2% fibo), 4.3320

(21 DMA). We look for 4.25 – 4.28 range intra-day. Trade data due

for release on Thu and FX reserves on Fri.

1m USDKRW NDF – Range. 1m USDKRW NDF was last seen at 1217

levels. Mild bearish momentum on daily chart intact but RSI shows

signs of turning higher. Expect some consolidation intra-day in the

range of 1214 – 1220. We still cautioned for sino-US tension risks

(and its potential negative repercussion on KRW, typically more

sensitive to news flow) but acknowledged that broad USD weakness

and risk-on sentiment appear to offset any KRW downside risks for

now.

AUDSGD – AUDSGD – Bearish Divergence. Last seen at 0.9660, the

cross has also formed a doji yesterday and could be poised to come

off soon. Bearish divergence could play out. Only a clearance of the

21-dma at 0.9234 can nullify the recent uptrend. Price action has

added some confirmation to the bearish divergence that could play

out. Resistance at 0.9810 (61.8% Fibonacci retracement of the 2017-

2020 fall). Support at 0.9460 (50% fibo), 0.9350.

USDCNH – Eye 7.1050 Still, But Consolidative Action Likely. This

pair dropped under 7.10-figure at one point yesterday before rising

again back within the 7.10-7.20 band. 7.1050, marked by the 50-

dma, has proven to be a key support level and we continue to watch

that. The US has suspended Chinese carrier flights from flying to the

US according to the US Transportation Department as China has not

4 June 2020 6

FX Research & Strategy

given permission for US airline flights. Consolidation under the

7.1650 could nullify the ascending triangle and form a rising wedge

instead with lower bound guided by the 50-dma. We stand by the

view that USDCNH has to break the 7.1050 for the double top to

play out. At this point, more consolidative action is likely and risks

are tilted to the upside. Momentum indicators are lacking

directional cues.

1M USDIDR NDF – Signs of Upward Correction. NDF last seen at

14,200, having continued its down-move yesterday. Global risk

sentiments (which typically influences flows into assets including

IDR bonds) was benign for most of the week. A bond sale on Tues

saw a record IDR103.62tn of bids for a IDR24tn sale, excluding bills.

Nonetheless, we note more “points” of conflict between US and

China. The latest spat is over US’ barring of China airlines after

Beijing rejected US carriers’ requests to resume flights to China.

Key risks at this point are escalations in domestic contagion or US-

Sino tensions. Barring these risks, BI Governor Warjiyo commented

earlier that the IDR has the potential to strengthen to pre-pandemic

levels of around 13600-800, once investors’ risk appetite returns to

normal. Nonetheless, path could be rocky; NDF sees signs of jerking

upwards this morning. On daily chart, momentum indicator is mildly

bearish while stochastics are in oversold conditions. Support at

14,000, 13800, 13,600. Resistance at 14,500 (200-DMA), 15,000

(61.8% fibo retracement from Jan low to Mar high), 15,420 (50.0%

fibo).

USDTHB – Bearish Momentum Waning. Pair last seen at 31.58,

having largely traded ranged yesterday. BoT has summoned FX

dealers to meet today to discuss the THB’s recent gains, which it

considers to be out of line with economic fundamentals. Gold

dealers’ transactions will also be examined for compliance—gold

trading has been partly associated with recent THB strength.

Concerns over political uncertainty may weigh on sentiments a tad,

as more than half of Palang Pracharath party’s (party leading

Thailand’s ruling coalition) executive committee resigned on Mon,

which may induce changes in cabinet roles. Pair may hover near key

pivot at 31.60 (50.0% fibo retracement from 2020 low to high) for

now, or potentially recover higher. Next support at 31.20 (61.8%

fibo). Resistance at 32.00 (21-DMA), 32.40 (23.6% fibo). Momentum

on daily chart is mildly bearish, while stochastics remain in oversold

conditions.

1M USDPHP NDF – Risks Skewed to Upside. NDF last seen at 50.0,

having declined by about 1% thus far this week on broad dollar

weakness and positive global sentiments. BSP Governor Diokno says

the central bank is “happy where the current policy rate is” (i.e.,

2.75% after 125bps cuts this year). Developments in lockdown

loosening are largely akin to that of regional peers. We expect the

NDF to be more influenced by broad dollar moves in the interim,

and technical indicators suggest risks may be skewed to the upside

for now—tentative signs of bullish divergence on MACD and

stochastics are near oversold conditions. Next support at 49.7 (2018

low), before 49.0. Resistance at 50.60 (21-DMA), 50.95 (100-DMA).

4 June 2020 7

FX Research & Strategy

Malaysia Fixed Income

Rates Indicators

MGS Previous Bus. Day Yesterday’s Close Change (bps)

3YR MH 3/23 2.28 2.27 -1

5YR MO 9/25 2.47 2.48 +1

7YR MK 5/27 2.65 2.65 Unchanged

10YR MO 8/29 2.84 2.85 +1

15YR MS 7/34 3.19 3.19 Unchanged

20YR MY 5/40 3.45 3.44 -1

30YR MZ 7/48 3.80 3.85 +5

IRS

6-months 2.18 2.18 -

9-months 2.14 2.14 -

1-year 2.12 2.13 +1

3-year 2.14 2.14 -

5-year 2.27 2.30 +3

7-year 2.43 2.43 -

10-year 2.65 2.65 -

Source: Maybank KE

*Indicative levels

Global: Export Growth (% YoY,

Ringgit government bond yields moved rangebound mostly in the

+2bps to -3bps range, except for 30y MGS which ended 5bps higher

from its last traded level two days ago. Lifers continued to buy off-

the-run bonds selectively, though there was also some foreign

selling. It did not affect the 3y GII 5/23 reopening which garnered a

strong 2.50x bid/cover, supported by local trading accounts, and an

average yield of 2.306%. Post auction, 3y GII traded in a tight range

of 2.32-31% with some investor likely taking profit.

The MYR IRS market was in a lull for the first half of the day until a

foreign name consecutively took offers on the 5y IRS at 2.29-30%.

This sent rates at the belly of curve up 1-3bps. 3M KLIBOR came off

1bp to 2.28%.

PDS market activity picked up and were marginally firmer, with GG

yields flat to -1bp along the belly and long end of the curve. The

short end, however, was better offered and yields rose about 2-3bps

higher. Market appears to be less averse to duration risk as better

external risk sentiment continues to hold. AAA levels unchanged

with trades at the belly area, though Danga 2027 traded about 2bps

lower in yield. AA and lower credit spaces were quiet again and

mainly saw retail interests.

Analysts

Winson Phoon

(65) 6812 8807

Se Tho Mun Yi

(603) 2074 7606

4 June 2020 8

FX Research & Strategy

Singapore Fixed Income

Rates Indicators

SGS Previous Bus. Day Yesterday’s Close Change (bps)

2YR 0.29 0.31 +2

5YR 0.47 0.51 +4

10YR 0.85 0.92 +7

15YR 1.16 1.22 +6

20YR 1.24 1.29 +5

30YR 1.24 1.31 +7

Source: MAS

Another day of strong risk sentiment drove SGD rates and SGS yields

higher, spiking as much as 10-12bps before normalizing in the

afternoon. SGD IRS curve bear-steepened again and rose further by

2-8bps. SGS yield curve shifted higher by roughly the same

magnitude and in a mild steepening bias.

Asian credits strengthened further with strong demand for China, HK

and India IGs. India credits rebounded to rally 5-10bps tighter, while

China and HK credits tightened 3-8bps and saw new issuances such

as Tencent outperform. Sovereigns bonds such as INDONs and

PHILIPs saw better bids for their off-the-runs and the curves

tightened 3-7bps. Malaysian corporate USD paper TNBMK 2026

continued to see selling interests while its 2028 saw better buying

again, and PETMK tightened 5bps as crude oil prices edged higher.

4 June 2020 9

FX Research & Strategy

Indonesia Fixed Income

Rates Indicators

IDR Gov’t Bonds Previous Bus. Day Yesterday’s Close Change

(bp) Analysts

1YR 5.41 5.26 (0.15) Myrdal Gunarto

3YR 6.35 6.24 (0.11) (62) 21 2922 8888 ext 29695

5YR 6.65 6.49 (0.16) [email protected]

10YR 7.15 7.00 (0.15)

15YR 7.70 7.52 (0.19)

20YR 7.70 7.55 (0.15)

30YR 7.89 7.82 (0.08)

* Source: Bloomberg, Maybank Indonesia

Global: Export Growth (% YoY,signif

Indonesian government bonds were still on the rally trends yesterday.

Investors took positive momentum for coming back to Indonesian

financial markets after seeing recent positive progress on the global

“new normal” in both global and domestic side. President Joko Widodo

stated that the government is seeking ways to immediately implement

recovery programs in an attempt to anticipate growth contraction in 2Q

to 4Q. Quick implementation of the economic recovery programs is the

country’s biggest challenge, Widodo, known as Jokowi said in cabinet

meeting on Wednesday. Jokowi orders ministers to start drafting burden

sharing concept between the government, Bank Indonesia, Financial

Services Authority, banking sector and businesses for economic recovery

and minimizing massive unemployment triggered by the pandemic. The

2020 state budget must be credible, prudent, transparent and

accountable to avoid moral hazard, while ministers have been asked to

carefully calculate fiscal risks that emerges from rising spending.

Indonesia’s fiscal deficit ratio is now projected to widen to 6.34% of

gross domestic product, Ministry of Sri Mulyani Indrawati recently stated.

That’s the latest of several revisions since the government announced

just over two months ago that it was suspending its 3% ceiling. It will

consequently add more supply of government bonds in the domestic

market. Therefore, we foresee that it will restrain aggressive rally on

Indonesian government bond market during this year. Indrawati said this

year’s fiscal deficit is expected to reach Rp1,039.2 trillion, compared to

the previous estimate of Rp1,033 trillion. She said the government has

earmarked Rp677.2 trillion for virus relief. Furthermore, Bank Indonesia

has bought Rp26 trillion (US$1.8 trillion) in bonds from the primary

market since 21 Apr-20, Governor Perry Warjiyo said Wednesday. The

central bank’s policy arsenal would continue to be aimed at supporting

the recovery, including maintaining confidence among investors, Warjiyo

said.

Going forward, we believe that Indonesia’s government bond is a good

option amidst other investment assets in the emerging countries during

current pandemic Coronavirus condition. Nevertheless, we also warn

investors to keep underlining current high volatility conditions due

recent intensifying geopolitical tensions, such as conflict between the

United States against China, and instability security condition in Hong

Kong due to massive demonstration.

4 June 2020 10

FX Research & Strategy

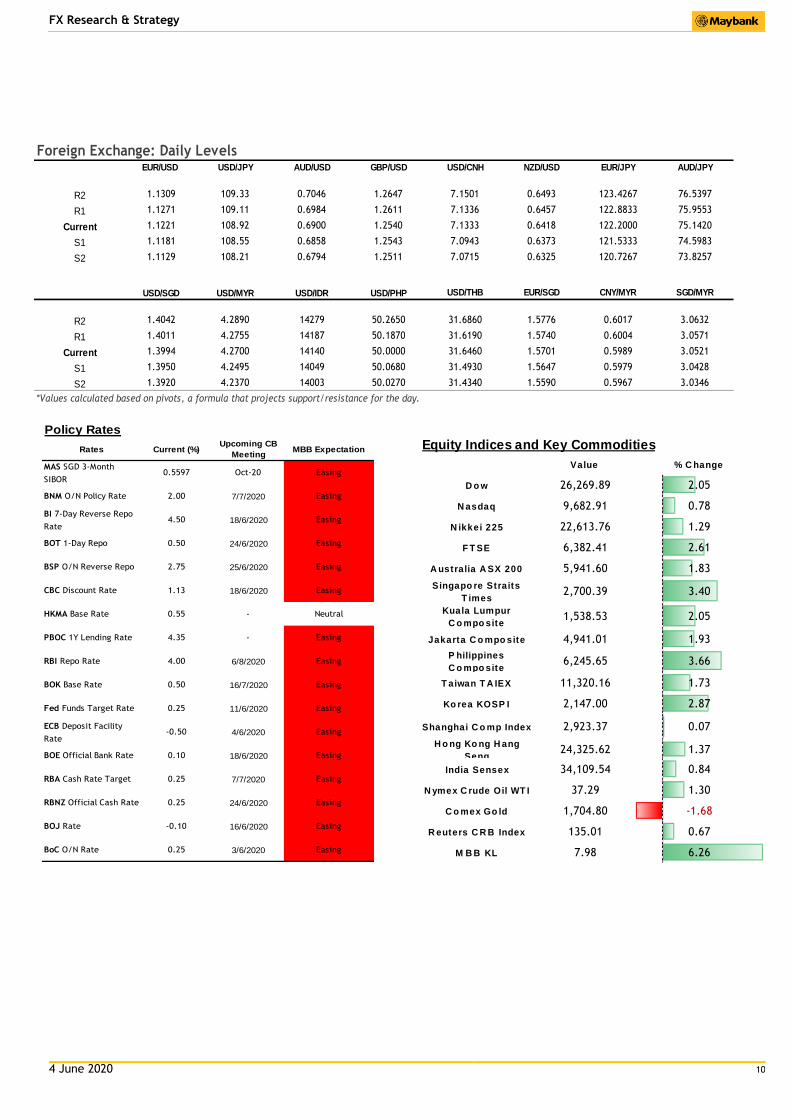

Equity Indices and Key Commodities

Value % C hange

D o w 26,269.89 2.05

N asdaq 9,682.91 0.78

N ikkei 225 22,613.76 1.29

F T SE 6,382.41 2.61

A ustralia A SX 200 5,941.60 1.83

Singapo re Straits

T imes2,700.39 3.40

Kuala Lumpur

C o mpo site1,538.53 2.05

Jakarta C o mpo site 4,941.01 1.93

P hilippines

C o mpo site6,245.65 3.66

T aiwan T A IEX 11,320.16 1.73

Ko rea KOSP I 2,147.00 2.87

Shanghai C o mp Index 2,923.37 0.07

H o ng Ko ng H ang

Seng24,325.62 1.37

India Sensex 34,109.54 0.84

N ymex C rude Oil WT I 37.29 1.30

C o mex Go ld 1,704.80 -1.68

R euters C R B Index 135.01 0.67

M B B KL 7.98 6.26

Foreign Exchange: Daily LevelsEUR/USD USD/JPY AUD/USD GBP/USD USD/CNH NZD/USD EUR/JPY AUD/JPY

R2 1.1309 109.33 0.7046 1.2647 7.1501 0.6493 123.4267 76.5397

R1 1.1271 109.11 0.6984 1.2611 7.1336 0.6457 122.8833 75.9553

Current 1.1221 108.92 0.6900 1.2540 7.1333 0.6418 122.2000 75.1420

S1 1.1181 108.55 0.6858 1.2543 7.0943 0.6373 121.5333 74.5983

S2 1.1129 108.21 0.6794 1.2511 7.0715 0.6325 120.7267 73.8257

USD/SGD USD/MYR USD/IDR USD/PHP USD/THB EUR/SGD CNY/MYR SGD/MYR

R2 1.4042 4.2890 14279 50.2650 31.6860 1.5776 0.6017 3.0632

R1 1.4011 4.2755 14187 50.1870 31.6190 1.5740 0.6004 3.0571

Current 1.3994 4.2700 14140 50.0000 31.6460 1.5701 0.5989 3.0521

S1 1.3950 4.2495 14049 50.0680 31.4930 1.5647 0.5979 3.0428

S2 1.3920 4.2370 14003 50.0270 31.4340 1.5590 0.5967 3.0346

*Values calculated based on pivots, a formula that projects support/resistance for the day.

Rates Current (%)Upcoming CB

MeetingMBB Expectation

MAS SGD 3-Month

SIBOR0.5597 Oct-20 Easing

BNM O/N Policy Rate 2.00 7/7/2020 Easing

BI 7-Day Reverse Repo

Rate4.50 18/6/2020 Easing

BOT 1-Day Repo 0.50 24/6/2020 Easing

BSP O/N Reverse Repo 2.75 25/6/2020 Easing

CBC Discount Rate 1.13 18/6/2020 Easing

HKMA Base Rate 0.55 - Neutral

PBOC 1Y Lending Rate 4.35 - Easing

RBI Repo Rate 4.00 6/8/2020 Easing

BOK Base Rate 0.50 16/7/2020 Easing

Fed Funds Target Rate 0.25 11/6/2020 Easing

ECB Deposit Facility

Rate-0.50 4/6/2020 Easing

BOE Official Bank Rate 0.10 18/6/2020 Easing

RBA Cash Rate Target 0.25 7/7/2020 Easing

RBNZ Official Cash Rate 0.25 24/6/2020 Easing

BOJ Rate -0.10 16/6/2020 Easing

BoC O/N Rate 0.25 3/6/2020 Easing

Policy Rates

4 June 2020 11

FX Research & Strategy

MYR Bonds Trades Details

MGS & GII Coupon Maturity

Date Volume (RM ‘m)

Last Done Day High Day Low

MGS 6/2013 3.889% 31.07.2020 3.889% 31-Jul-20 355 1.997 2.049 1.953

MGS 3/2015 3.659% 15.10.2020 3.659% 15-Oct-20 280 2.015 2.041 2.001

MGS 5/2017 3.441% 15.02.2021 3.441% 15-Feb-21 680 2.02 2.02 2.015

MGS 1/2011 4.16% 15.07.2021 4.160% 15-Jul-21 15 2.097 2.097 2.08

MGS 3/2014 4.048% 30.09.2021 4.048% 30-Sep-21 14 2.075 2.075 2.071

MGS 4/2016 3.620% 30.11.2021 3.620% 30-Nov-21 7 2.099 2.099 2.086

MGS 1/2017 3.882% 10.03.2022 3.882% 10-Mar-22 424 2.178 2.189 2.13

MGS 1/2012 3.418% 15.08.2022 3.418% 15-Aug-22 13 2.199 2.199 2.188

MGS 2/2015 3.795% 30.09.2022 3.795% 30-Sep-22 11 2.207 2.207 2.196

MGS 3/2013 3.480% 15.03.2023 3.480% 15-Mar-23 202 2.272 2.272 2.225

MGS 2/2018 3.757% 20.04.2023 3.757% 20-Apr-23 21 2.296 2.296 2.262

MGS 1/2016 3.800% 17.08.2023 3.800% 17-Aug-23 3 2.335 2.335 2.335

MGS 3/2019 3.478% 14.06.2024 3.478% 14-Jun-24 17 2.396 2.396 2.396

MGS 1/2014 4.181% 15.07.2024 4.181% 15-Jul-24 20 2.478 2.478 2.415

MGS 2/2017 4.059% 30.09.2024 4.059% 30-Sep-24 12 2.451 2.451 2.426

MGS 1/2015 3.955% 15.09.2025 3.955% 15-Sep-25 139 2.482 2.482 2.467

MGS 1/2019 3.906% 15.07.2026 3.906% 15-Jul-26 19 2.665 2.665 2.651

MGS 3/2016 3.900% 30.11.2026 3.900% 30-Nov-26 1 2.649 2.649 2.649

MGS 3/2007 3.502% 31.05.2027 3.502% 31-May-27 2 2.658 2.658 2.653

MGS 4/2017 3.899% 16.11.2027 3.899% 16-Nov-27 82 2.777 2.79 2.737

MGS 5/2013 3.733% 15.06.2028 3.733% 15-Jun-28 81 2.843 2.885 2.843

MGS 2/2019 3.885% 15.08.2029 3.885% 15-Aug-29 369 2.85 3.082 2.808

MGS 3/2010 4.498% 15.04.2030 4.498% 15-Apr-30 40 3.001 3.001 3

MGS 4/2012 4.127% 15.04.2032 4.127% 15-Apr-32 10 3.208 3.208 3.208

MGS 4/2013 3.844% 15.04.2033 3.844% 15-Apr-33 1 3.25 3.25 3.25

MGS 3/2018 4.642% 07.11.2033 4.642% 07-Nov-33 50 3.296 3.296 3.288

MGS 4/2019 3.828% 05.07.2034 3.828% 05-Jul-34 6 3.189 3.189 3.189

MGS 4/2015 4.254% 31.05.2035 4.254% 31-May-35 3 3.377 3.377 3.377

MGS 3/2017 4.762% 07.04.2037 4.762% 07-Apr-37 15 3.461 3.461 3.39

MGS 4/2018 4.893% 08.06.2038 4.893% 08-Jun-38 10 3.502 3.502 3.502

MGS 5/2019 3.757% 22.05.2040 3.757% 22-May-40 1 3.437 3.437 3.437

MGS 2/2016 4.736% 15.03.2046 4.736% 15-Mar-46 10 3.872 3.872 3.843

MGS 5/2018 4.921% 06.07.2048 4.921% 06-Jul-48 48 3.864 3.864 3.825

GII MURABAHAH 6/2013 23.03.2021 3.716% 23-Mar-21 45 2.089 2.089 2.039

PROFIT-BASED GII 3/2011 30.04.2021 4.170% 30-Apr-21 100 2.062 2.062 2.062 GII MURABAHAH 4/2018 3.729% 31.03.2022 3.729% 31-Mar-22 10 2.206 2.206 2.206 GII MURABAHAH 3/2017 3.948% 14.04.2022 3.948% 14-Apr-22 1 2.188 2.188 2.188 GII MURABAHAH 7/2019 3.151% 15.05.2023 3.151% 15-May-23 1,075 2.307 2.342 2.303 GII MURABAHAH 1/2016 4.390% 07.07.2023 4.390% 07-Jul-23 20 2.35 2.35 2.35

PROFIT-BASED GII 2/2013 31.10.2023 3.493% 31-Oct-23 20 2.361 2.361 2.361 GII MURABAHAH 3/2018 4.094% 30.11.2023 4.094% 30-Nov-23 180 2.387 2.394 2.382

GII MURABAHAH 8/2013 22.05.2024 4.444% 22-May-24 100 2.446 2.446 2.446 GII MURABAHAH 2/2017 4.045% 15.08.2024 4.045% 15-Aug-24 50 2.484 2.484 2.484 GII MURABAHAH 4/2019 3.655% 15.10.2024 3.655% 15-Oct-24 119 2.483 2.51 2.483 GII MURABAHAH 1/2018 4.128% 15.08.2025 4.128% 15-Aug-25 3 2.56 2.56 2.56 GII MURABAHAH 2/2018 4.369% 31.10.2028 4.369% 31-Oct-28 36 2.926 2.93 2.917

GII MURABAHAH 1/2019 4.130% 4.130% 09-Jul-29 69 2.92 2.926 2.92

4 June 2020 12

FX Research & Strategy

09.07.2029

GII MURABAHAH 2/2020 3.465% 15.10.2030 3.465% 15-Oct-30 3 2.703 2.703 2.703 GII MURABAHAH 6/2019 4.119% 30.11.2034 4.119% 30-Nov-34 30 3.273 3.273 3.26

Total 4,820

Sources: BPAM

4 June 2020 13

FX Research & Strategy

MYR Bonds Trades Details

PDS Rating Coupon Maturity

Date Volume (RM ‘m)

Last Done

Day High

Day Low

KHAZANAH 0% 08.03.2021 GG 0.000% 08-Mar-21 40 2.185 2.199 2.185

DANAINFRA IMTN 4.230% 23.07.2021 - Tranche No 20 GG 4.230% 23-Jul-21 5 2.237 2.237 2.237

PRASARANA IMTN 0% 04.08.2021 - MTN 3 GG 4.150% 04-Aug-21 110 2.198 2.198 2.198

PASB IMTN (GG) 4.23% 16.06.2023 - Issue No. 25 GG 4.230% 16-Jun-23 55 2.549 2.549 2.549

LPPSA IMTN 3.830% 21.09.2023 - Tranche No 3 GG 3.830% 21-Sep-23 70 2.551 2.551 2.551

DANAINFRA IMTN 4.210% 31.10.2023 - Tranche No 10 GG 4.210% 31-Oct-23 30 2.554 2.554 2.554

LPPSA IMTN 4.320% 04.04.2025 - Tranche No 19 GG 4.320% 04-Apr-25 20 2.729 2.729 2.729

PTPTN IMTN 12.03.2027 GG 4.450% 12-Mar-27 15 3 3 3

LPPSA IMTN 4.580% 16.04.2027 - Tranche No 9 GG 4.580% 16-Apr-27 85 2.997 3 2.997

PRASARANA SUKUK MURABAHAH 4.00% 06.09.2027 - T2 GG 4.000% 06-Sep-27 30 3 3 3

DANAINFRA IMTN 3.470% 26.09.2029 - Tranche 12 GG 3.470% 26-Sep-29 15 3.15 3.15 3.15

PRASARANA IMTN 4.97% 11.12.2030 - Series 4 GG 4.970% 11-Dec-30 70 3.19 3.19 3.187

PLUS BERHAD IMTN 4.860% 12.01.2038 - Series 1 GG 4.860% 12-Jan-38 60 3.59 3.61 3.59

PRASARANA IMTN 3.800% 25.02.2050- Series 5 GG 3.800% 25-Feb-50 20 3.967 3.973 3.967

CAGAMAS MTN 4.100% 08.10.2021 AAA 4.100% 08-Oct-21 40 2.503 2.503 2.503

CAGAMAS IMTN 4.080% 08.10.2021 AAA 4.080% 08-Oct-21 20 2.503 2.503 2.503

CAGAMAS IMTN 3.500% 12.08.2022 AAA 3.500% 12-Aug-22 60 2.616 2.616 2.616

DANUM IMTN 2.970% 13.05.2025 - Tranche 7 AAA (S) 2.970% 13-May-25 5 2.969 2.971 2.969

PLUS BERHAD IMTN 4.800% 12.01.2027 - Series 1 (11) AAA IS 4.800% 12-Jan-27 4 3.189 3.191 3.189

DANUM IMTN 3.140% 13.05.2027 - Tranche 8 AAA (S) 3.140% 13-May-27 5 3.149 3.15 3.149

DANGA IMTN 4.520% 06.09.2027 - Tranche 7 AAA (S) 4.520% 06-Sep-27 20 3.188 3.192 3.188

PLUS BERHAD IMTN 4.880% 12.01.2028 - Series 1 (12) AAA IS 4.880% 12-Jan-28 1 3.269 3.271 3.269

TELEKOM IMTN 31.10.2028 AAA 4.680% 31-Oct-28 20 3.265 3.281 3.265

SEB IMTN 4.700% 24.11.2028 AAA 4.700% 24-Nov-28 6 3.209 3.21 3.209

SEB IMTN 5.500% 04.07.2029 AAA 5.500% 04-Jul-29 34 3.229 3.25 3.229

SARAWAKHIDRO IMTN 4.56% 10.08.2029 AAA 4.560% 10-Aug-29 70 3.249 3.261 3.249

DANUM IMTN 3.290% 13.05.2030 - Tranche 9 AAA (S) 3.290% 13-May-30 5 3.31 3.311 3.31

RANTAU IMTN 0% 12.05.2031 - MTN 5 AAA (S) 5.050% 12-May-31 30 3.357 3.371 3.357

RANTAU IMTN 0% 16.01.2032 - Tranche No 10 AAA (S) 5.000% 16-Jan-32 20 3.401 3.401 3.387

TENAGA IMTN 27.08.2038 AAA 4.980% 27-Aug-38 20 3.69 3.695 3.69

CIMBBANK 4.700% 07.08.2026 - Issue No 4 AA+ 4.700% 07-Aug-26 1 3.379 4.247 3.379

KLK IMTN 3.95% 27.09.2034 - Tranche 2 AA1 3.950% 27-Sep-34 10 3.789 3.789 3.789

BENIH RESTU IMTN 4.620% 05.06.2025 AA2 (S) 4.620% 05-Jun-25 10 3.497 3.504 3.497

HLFG Tier 2 Subordinated Notes (Tranche 2) AA2 4.300% 14-Jun-29 5 3.36 3.36 3.36

EDRA ENERGY IMTN 5.820% 04.07.2025 - Tranche No 8 AA3 5.820% 04-Jul-25 1 4.481 4.485 4.481

MMC CORP IMTN 5.700% 24.03.2028 AA- IS 5.700% 24-Mar-28 1 4.397 4.474 4.397

IJM IMTN 5.050% 18.08.2028 AA3 5.050% 18-Aug-28 10 3.879 3.881 3.879

EDRA ENERGY IMTN 6.310% 05.01.2033 - Tranche No 23 AA3 6.310% 05-Jan-33 5 4.159 4.16 4.159

MAYBANK IMTN 4.080% PERPETUAL AA3 4.080% 22-Feb-17 10 3.569 3.572 3.569

CIMB 5.400% Perpetual Capital Securities - T3 A1 5.400% 25-May-16 2 4.185 4.563 4.185

MBSBBANK IMTN 5.250% 19.12.2031 A3 5.250% 19-Dec-31 10 4.592 4.592 4.569

AFFIN ISLAMIC PERPETUAL AT1 SUKUK WAKALAH (T1) A3 5.650% 18-Oct-17 20 4.349 4.349 4.349

AFFINBANK RM500M PERPETUAL AT1CS (T1) A3 5.800% 29-Jul-18 70 4.358 4.365 4.358

EWIB IMTN 6.400% 24.05.2023 NR(LT) 6.400% 24-May-23 1 5.467 5.475 5.467

MAH SING 6.900% PERPETUAL SECURITIES - SERIES NO 1 NR(LT) 6.900% 02-Apr-17 1 5.537 6.399 5.537

YNHP 6.850% PERPETUAL SECURITIES - TRANCHE NO 1 NR(LT) 6.850% 07-Aug-19 1 7.286 7.286 7.286

Total 1,141

4 June 2020 14

FX Research & Strategy

Sources: BPAM

4 June 2020 15

FX Research & Strategy

DISCLAIMER

This report is for information purposes only and under no circumstances is it to be considered or intended as an offer to sell or a solicitation of an offer to buy the securities or financial instruments referred to herein, or an offer or solicitation to any person to enter into any transaction or adopt any investment strategy. Investors should note that income from such securities or financial instruments, if any, may fluctuate and that each security’s or financial instrument’s price or value may rise or fall. Accordingly, investors may receive back less than originally invested. Past performance is not necessarily a guide to future performance. This report is not intended to provide personal investment advice and does not take into account the specific investment objectives, the financial situation and the particular needs of persons who may receive or read this report. Investors should therefore seek financial, legal and other advice regarding the appropriateness of investing in any securities and/or financial instruments or the investment strategies discussed or recommended in this report.

The information contained herein has been obtained from sources believed to be reliable but such sources have not been independently verified by Malayan Banking Berhad and/or its affiliates and related corporations (collectively, “Maybank”) and consequently no representation is made as to the accuracy or completeness of this report by Maybank and it should not be relied upon as such. Accordingly, no liability can be accepted for any direct, indirect or consequential losses or damages that may arise from the use or reliance of this report. Maybank and its officers, directors, associates, connected parties and/or employees may from time to time have positions or be materially interested in the securities and/or financial instruments referred to herein and may further act as market maker or have assumed an underwriting commitment or deal with such securities and/or financial instruments and may also perform or seek to perform investment banking, advisory and other services for or relating to those companies whose securities are mentioned in this report. Any information or opinions or recommendations contained herein are subject to change at any time, without prior notice.

This report may contain forward looking statements which are often but not always identified by the use of words such as “anticipate”, “believe”, “estimate”, “intend”, “plan”, “expect”, “forecast”, “predict” and “project” and statements that an event or result “may”, “will”, “can”, “should”, “could” or “might” occur or be achieved and other similar expressions. Such forward looking statements are based on assumptions made and information currently available to us and are subject to certain risks and uncertainties that could cause the actual results to differ materially from those expressed in any forward looking statements. Readers are cautioned not to place undue relevance on these forward looking statements. Maybank expressly disclaims any obligation to update or revise any such forward looking statements to reflect new information, events or circumstances after the date of this publication or to reflect the occurrence of unanticipated events.

This report is prepared for the use of Maybank’s clients and may not be reproduced, altered in any way, transmitted to, copied or distributed to any other party in whole or in part in any form or manner without the prior express written consent of Maybank. Maybank accepts no liability whatsoever for the actions of third parties in this respect. This report is not directed to or intended for distribution to or use by any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

4 June 2020 16

FX Research & Strategy

Published by:

Malayan Banking Berhad (Incorporated In Malaysia)

Foreign Exchange

Sales

Singapore Indonesia Malaysia

Saktiandi Supaat Juniman Azman Amiruddin Shah bin Mohamad Shah

Head, FX Research Chief Economist, Indonesia Head, Sales-Malaysia, GB-Global Markets

[email protected] [email protected] [email protected]

(+65) 6320 1379 (+62) 21 2922 8888 ext 29682 (+60) 03-2173 4188

Christopher Wong Myrdal Gunarto Singapore

Senior FX Strategist Industry Analyst Janice Loh Ai Lin

[email protected] [email protected] Co-Head of Sales, Singapore

(+65) 6320 1347 (+62) 21 2922 8888 ext 29695 [email protected]

(+65) 6536 1336

Fiona Lim

Senior FX Strategist Joanna Leong Wan Yi

[email protected] Co-Head of Sales, Singapore

(+65) 6320 1374 [email protected]

Yanxi Tan

(+65) 6320 1511

FX Strategist Indonesia

[email protected] Endang Yulianti Rahayu

(+65) 6320 1378 Head of Sales, Indonesia

(+62) 21 29936318 or

Fixed Income (+62) 2922 8888 ext 29611

Malaysia

Winson Phoon Wai Kien

Shanghai

Fixed Income Analyst

Joyce Ha

Treasury Sales Manager

(+65) 6231 5831

(+86) 21 28932588

Se Tho Mun Yi

Fixed Income Analyst Hong Kong

[email protected] Joanne Lam Sum Sum

(+60) 3 2074 7606

Head of Corporate Sales Hong Kong

(852) 3518 8790